Abstract

This research investigates the impact of working capital management (WCM) on the profitability and market performance of firms that constitute an Islamic market index (Karachi Meezan Index [KMI-30]) in Pakistan during 2002–2013. The data have been divided into three parts, that is, preglobal (2002–2007), during (2007–2008), and postglobal financial crisis period (2008–2013), to examine the proposed relationship in different macroeconomic settings. Net trade cycle (NTC) and its components are used to measure the WCM efficiency, while NTC square is used to proxy the impact of excessive holdings of working capital on corporate performance. The econometric models are calculated in a generalized method of moments (GMMs)-based regression environment to ensure the robustness of empirical outcome. The results reveal that, as opposed to conventional businesses, KMI-30 firms are more ethical in their short-term financial management. Besides, such firms adopted a conservative WCM policy during the global financial crisis of 2007–2008. Furthermore, we confirm the presence of a concave relationship between working capital levels and firm performance as NTC is positively, whereas NTC square is negatively, related to firm performance. This article makes a significant contribution to the extant literature as it evaluates the impact of WCM on the profitability and market performance of Islamic market indexed firms under varying macroeconomic conditions.

Keywords

Introduction

The aftermath of the U.S. financial crisis and the liquidity crunch that followed, invigorated the attention of financial managers to focus on the short-term financial health of firms. Efficient working capital management (WCM) reflects the policies, adjustments, and management of the level of short-lived assets and liabilities of the firm in such a way that maturing obligations are timely met, and the fixed assets are adequately serviced (Osisioma, 1997). In line with this description, the quantity of each component of working capital should be managed appropriately to optimize working capital, as excess working capital is simply unproductive and does not earn any cost of capital. Thus, it is perfectly reasonable for firm managers to strive for an optimal level of working capital, which in turn will maximize firm value (Aktas et al., 2015; Baños-Caballero et al., 2014).

WCM is a forthright idea to make sure that the company can bridge the gap of funds between short-term assets and short-term liabilities. There are four key components of working capital: cash, inventories, accounts receivables, and accounts payable. Efficient management and control of all these components are imperative for a firm’s financial health and conducive to curtail financial distress (Ramiah et al., 2014). Therefore, managers have to spend a considerable amount of time and effort to achieve an optimal level of working capital that creates a balance between risk and efficiency. Firms should strike an optimum level of working capital by keeping the liquidity and profitability trade-off in perspective as inadequate WCM can lead to financial vulnerabilities, which may escalate the possibility of insolvency. Dunn and Cheatham (1993) posit that poor WCM is the chief reason for small enterprise failures in the United States and United Kingdom. When enterprises face financial distress or approaching insolvency, WCM becomes a focus of attention for financial institutions and legal advisers. Besides, financial institutions assess the working capital level of an enterprise to decide whether or not to extend further business loans, while legal advisers evaluate working capital data to determine whether a firm is legally insolvent (Ramiah et al., 2014).

The past two decades have witnessed the emergence of a list of socially responsible investments (SRIs). The upsurge in ethical or SRIs has provided an impetus to the Islamic investments that expanded 40 times since 1982. This trend has also prompted the growth of Islamic market indices in recent years (see, for instance, Kuala Lumpur Shariah Index [KLSI], Dow Jones Islamic Market index [DJMI], Financial Times Stock Exchange [FTSE], NASDAQ-100 Shariah indexSM, OMXSBSHARIA, Jakarta Islamic indices, Morgan Stanley Capital Index [MSCI], KMI30, and American Islamic Index [Ameri]). Although Islamic indices and SRIs have many similarities, there are also a few differences between the two investments (Sadeghi, 2008). SRIs typically do not engage in any business relating to gambling, tobacco, alcohol, and armaments. In addition to these restrictions, firms that constitute Islamic indices do not deal in pork products and also follow the financial screening rules maintained by Shariah or Islamic law (Monzurul Hoque et al., 2015).

KMI-30 is an Islamic market index of the Pakistan Stock Exchange. The index is constructed using free-floating market capitalization rule and comprises 30 companies that are recomposed semi-annually based on criteria laid down by the Shariah supervisory board. A company has to fulfill the following minimum criteria to become a part of the KMI-30.

The main business of the investee company must comply with the principles of Shariah. Thus, it is not permitted to invest in the shares of the companies that are dealing with interest or companies involved in some kind of business that is not legitimate under the ambit of Islamic law.

Interest-bearing debt of the investee company must be less than 37% of its assets.

Non-Shariah-compliant investments to total assets ratio must be less than 33%.

Noncompliant income should be less than 5% of the total revenue of the investee company.

Illiquid assets must be at least 25% of the total assets. In terms of Shariah, all those assets are illiquid that are not cash or cash equivalents.

Market price per share must be equal to or greater than net liquid assets per share.

Keeping in view the screening criteria, it is understood that both financing and investment avenues are very limited for KMI-30 firms when compared with the other non-Shariah-compliant firms. Thus, regardless of the optimal capital structure, these firms have limited space (<37% of total assets) to obtain financing from conventional financial institutions. Likewise, KMI-30 indexed firms cannot invest in any interest-bearing financial instruments; therefore, such firms cannot invest in bonds of the public and private companies, government securities, interest-bearing investment schemes of conventional banks and leasing companies, investment banks, and insurance companies. Moreover, to invest in stocks, these firms are not free to buy the shares of any company; rather, they have to follow a strict screening filter to figure out the firms for investment.

The impact of WCM on firm performance has been extensively investigated across the globe. However, these studies did not explore how the association between WCM and firm profitability or market performance prevails in firms that constitute an Islamic market index such as KMI-30. Thus, the present study focuses on KMI-30 firms because, unlike conventional businesses, these firms have to follow a different set of rules to manage their short-term financial affairs.

Furthermore, in a survey on WCM, KPMG (2010, p. 6) maintained that “Enterprises around the world are now focusing more on cash holdings and WCM to cope up with the liquidity crunch during the 2008 financial crisis.” Emphasis on efficient WCM picked momentum during and after the global financial crisis (GFC) mainly as efficient WCM can release free cash flows by minimizing the funds that are tied up in various accounts of working capital (Mohamad & Saad, 2010). Hence, it would be interesting to investigate the firm’s WCM strategies pre-, during, and post-GFC. Nevertheless, it is evidenced that Islamic financial institutions were more stable and were less affected by the recent crisis compared with their conventional counterparts (see, for instance, Beck et al., 2013; Hasan & Dridi, 2011).

The extant literature has mainly concentrated on the WCM practices of conventional firms. Nevertheless, as Shariah-compliant businesses need to operate within the purview of Islamic Shariah, the WCM policies and practices of Shariah-compliant firms are entirely different from their conventional counterparts. Hence, the present study aims to fill this gap in the literature.

The contribution of this research is threefold; first, it is the pioneer study that examines the impact of WCM policies on the profitability and market performance of Islamic market indexed firms. Second, considering that the GFC had seriously hampered the corporate liquidity, we empirically investigate how GFC influenced the WCM practices of KMI-30 firms, as compared with their conventional counterparts, by observing the proposed relationship in different time windows, such as pre-GFC (2002–2007), during the crisis (2007–2008), and post-GFC time-period (2008–2013). Third, we examine the data in a GMM-based regression environment to ensure that our results are robust and are not affected by endogeneity, which could be present in the data and can seriously compromise our research outcomes.

The rest of the article is organized as follows: The section “Review of Literature” summarizes the previous literature. This is followed by the sections “Data, Sample, and Variables,” “Research Hypothesis and Method,” “Results and Discussion,” and “Robustness check.” The section “Conclusion and Policy Implications” concludes the study.

Review of Literature

As one of the key areas in corporate finance, WCM is a very important component of corporate financial decision-making. Smith (1980) was the first to highlight the trade-off between liquidity and profitability. He postulated that approaches that tend to maximize firms’ liquidity tend not to maximize firm profitability. Conversely, the entire focus on liquidity will adversely affect firm profitability. Efficient WCM can enable firms to adjust quickly to the changes in market fundamentals, such as interest rates and fluctuation in the prices of raw material, and move ahead of its competitors (Appuhami, 2008).

A list of empirical studies found a significant association between WCM practices and firm performance (e.g., Baños-Caballero et al., 2014; Juan García-Teruel & Martinez-Solano, 2007; Padachi, 2006; Raheman & Nasr, 2007; Tahir & Anuar, 2016; Tauringana & Adjapong Afrifa, 2013). The aforementioned studies indicate that the WCM–Performance relationship is highly dependent on the internal factors, particularly on the WCM policy pursued by an enterprise (Juan García-Teruel & Martinez-Solano, 2007; Tauringana & Adjapong Afrifa, 2013). Companies pursue either an aggressive or a conservative WCM strategy. Hence, a particular WCM strategy opted by the firm can considerably influence its risk and return dynamics (Baños-Caballero et al., 2012). Firms adopting a conservative WCM policy prefer to make a relatively higher investment in working capital accounts, expecting that increasing the stock of inventory and receivables will boost sales volume and consequently result in higher profitability (Tauringana & Adjapong Afrifa, 2013). An increase in inventory levels also reduces the probability of stock-outs (Deloof, 2003) as well as a reduction in supply costs and price variations (Blinder & Maccini, 1991). Moreover, an increase in receivables can boost sales volume as it allows customers more time to make payments for their purchases (Deloof & Jegers, 1996; Long et al., 1993). Contrarily, substantial investments in working capital accounts require heavy external financing that can also escalate firms’ bankruptcy risk.

On the contrary, firms adopting aggressive WCM policies prefer to tie fewer funds in working capital accounts. These firms tend to curtail investments in inventory and receivables, and therefore such firms make higher use of short-term liabilities. By decreasing the inventory holding period, firms can increase their profitability because this practice can considerably reduce warehouse, insurance, and theft costs (Kim & Chung, 1990). An aggressive WCM policy can also increase firm profitability by lowering the time taken to collect receivables. This policy will increase the net cash available with the firm, which can not only be used to meet day-to-day liquidity requirements but also finance long-term investment projects, consequently decreasing the necessity for expensive external financing. However, McInnes (2000) reveals that 94% of the firms did not integrate their components of working capital as proposed by the theory. These findings accentuate substantial differences between the WCM practices of firms.

The existing literature on WCM in Pakistani firms mainly focuses on the profitability side and ignores the market response to the WCM policy. Moreover, conflicting results have been reported by various empirical studies. For example, Raheman et al. (2010) described that WCM plays a significant role in the profitability of manufacturing firms; Ali (2011) and Tahir and Anuar (2016) observed that profitability increases with an increase in the length of cash conversion cycle (CCC) for the textile companies of Pakistan; Chhapra and Naqvi (2010) observed a positive relationship between working capital and profitability of the textile firms; and Zubairi (2011) reveals that increase in current ratio leads to higher profitability.

In contrast, the following studies report contradictory results from the aforementioned studies: Sial and Chaudhry (2012) reported a significant negative relationship between all the working capital measures and return on assets; Tufail and Khan (2013) stated that an aggressive working capital policy negatively affects the firm profitability; and Arshad and Gondal (2013) also found a negative relationship between working capital and accounting profitability. Moreover, Khan et al. (2016) and Akbar and Akbar (2016) found an inverted U-shaped relationship between WCM and firm performance for the textile sector and Islamic market indexed firms of Pakistan, respectively. Likewise, Akbar et al. (2020) observed that excess funds tied up in working capital accounts have an adverse consequence for long-term investments and financing portfolios of firms. In a recent study, Wang et al. (2020) found corporate life cycle as one of the possible reasons for contrasting results between the association of WCM and firm performance. They provide evidence that the WCM–performance association varies with a change in the stage of the corporate life cycle.

The overseas studies also showed mixed evidence about the relationship between WCM and firm performance. Lazaridis and Tryfonidis (2006) and Zariyawati et al. (2009) noted a negative relationship between CCC duration and firm profitability for Greek and Malaysian firms, respectively. Baños-Caballero et al. (2014) reported an inverted U-shaped relationship between the net trade cycle (NTC) and Tobin’s Q (TQ), referring that each firm has a particular optimal working capital level and investment in working capital; lower than that optimal level enhances firm performance. Abuzayed (2012) found a negative and insignificant relationship between the CCC, and TQ revealed that Jordanian stock investors did not account for the firm’s working capital efficiency in their investment decisions. Ukaegbu (2014) studied how WCM relates to a firm’s profitability in four African countries; empirical analysis showed a significant negative relationship between working capital and accounting profitability for all of the four countries. Akbar (2014a) also reported a negative relationship between the NTC and profitability of the Chinese textile firms.

Albdwy et al. (2014) investigated whether the profitability of Shariah-compliant and non-Shariah-compliant firms of Malaysia reacts differently to the WCM. The findings revealed that, comparatively, Shariah-compliant firms have adopted better accounts receivable management systems as well as a higher inventory turnover mechanism. Therefore, such firms enjoy a higher return on equity (ROE) ratio compared with their conventional counterparts. To observe the working capital and profitability relationship during different business cycles, Julius Enqvist et al. (2014) tested a sample of Finnish listed companies and found that working capital and profitability relationship becomes more evident during the period of an economic downturn as compared with the economic boom.

In the context of GFC of 2007–2008, Ramiah et al. (2014) studied the impact of GFC on the WCM practices of Australian corporations. They came up with the conclusion that during the crisis period, most of the firms focused on shortening the CCC, while capital expenditures and inventory levels were curtailed to preserve cash, and firms become more risk-averse with tight credit controls. Likewise, Gunay and Kesimli (2011) examined the influence of GFC on the working capital of Turkish real sector firms. Their results revealed that the receivable turnover ratio was badly affected by GFC as it was 15.18 times for the precrisis era and dropped to merely 5.04 times during the crisis period. They concluded that companies which manage their working capital optimally during times of recession come out stronger after the recession period. In a more recent study, Singh and Kumar (2017) found that WCM practices of Indian firms have become more efficient after the GFC of 2008. However, it still remains unclear as to whether Islamic market indexed firms adopt a different approach to WCM, especially under different macroeconomic settings. The present study aims to fill this gap.

Data, Sample, and Variables

Data and Sample Selection

This research only includes non-financial firms as the performance measurement of financial sector firms is markedly different from their non-financial counterparts (Ahmed et al., 2021; Akbar et al., 2019; Hussain et al., 2020).The data for this study has been collected from the OSIRIS database from 2002 to 2013. KMI-30 comprises 30 companies. Each company must have published data of at least five consecutive years to become a part of the sample; 26 companies meet this criterion and four were excluded from the final sample because of the nonavailability of data.

Variables Selection

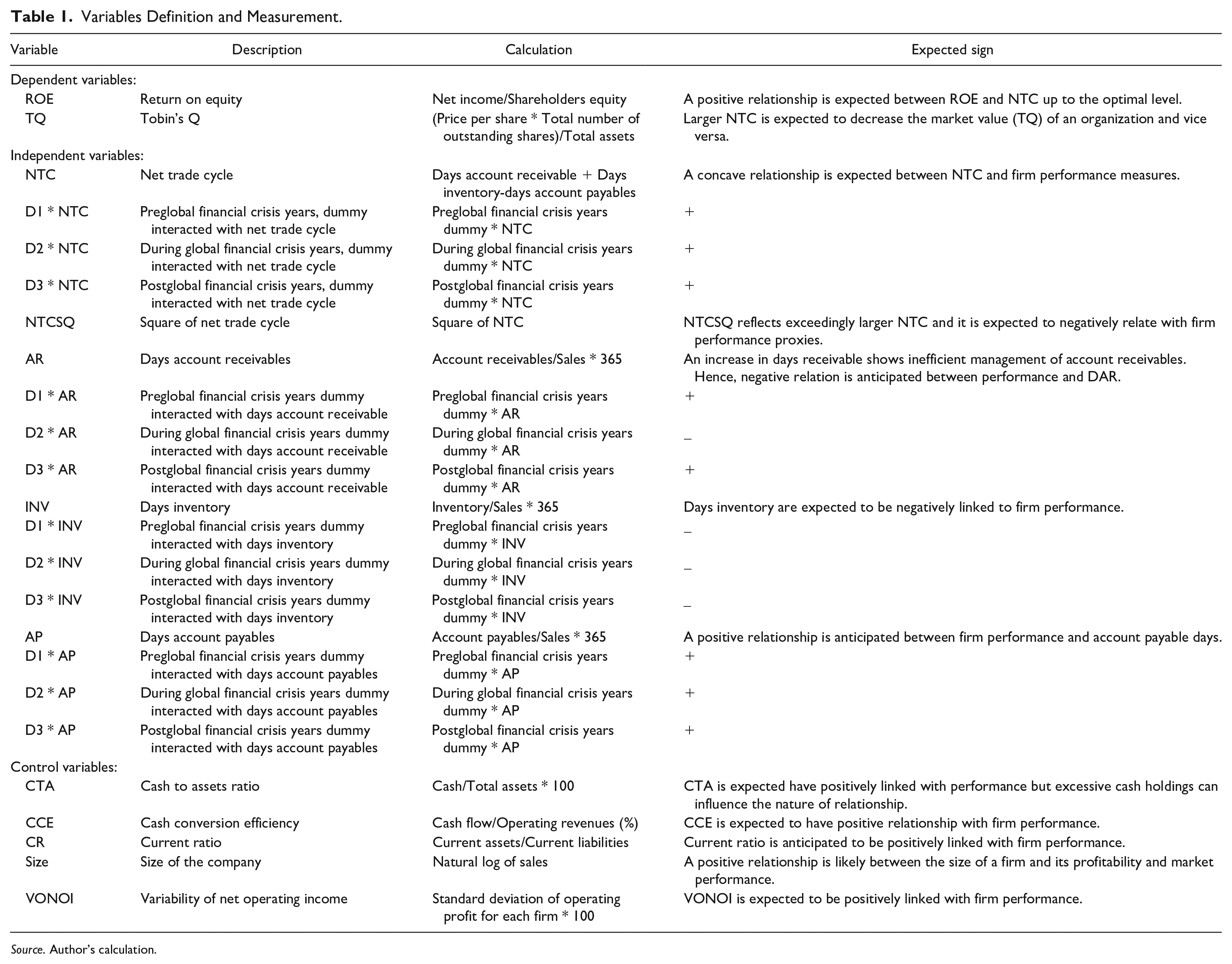

Table 1 provides a description of the variables used in this study. ROA and ROE are commonly used measures to proxy the corporate profitability (A. Akbar, 2014b; Yang et al., 2019; Akbar et al., 2020). Following Albdwy et al. (2014), M. Akbar and Akbar (2016), Baños-Caballero et al. (2014), Agrawal and Knoeber (1996), Florackis et al. (2009), and Wu (2011), among others, ROE and TQ are the measures of profitability and market performance, respectively. ROE indicates how wisely shareholder’s money is used to generate profits. Besides, it demonstrates the rate of return that shareholders received after the deduction of all financing costs, operating costs, and taxes. TQ ratio was introduced by Tobin in 1969 and is calculated by multiplying the total number of shares outstanding with market price per share, and then dividing it by total assets.

Variables Definition and Measurement.

Source. Author’s calculation.

NTC is used to proxy the WCM practices of sample firms. Bernstein (1993) introduced a modified version of CCC termed as the NTC. The new measure employs sales in the denominator for all the components of CCC. Bernstein (1993) argued that this measure improves the simplicity and uniformity in the calculation of a firm’s liquidity position. Moreover, NTC is the most practical alternative in most situations where the financial information required in the calculation of CCC is not available in its entirety. Empirical investigations revealed that both CCC and NTC generate similar information about the short financial management of a company (Shin & Soenen, 1998). Following these studies, NTC and its components are used to measure the WCM efficiency of firms. Square of NTC is also included in the quadratic equation to test whether excessive levels of working capital negatively affect a firm’s performance indicators. A similar approach is employed in Baños-Caballero et al. (2014). This variable also provides deeper insight into the existence of an optimal level of working capital in KMI-30 firms. Besides, as the firm performance can be influenced by several firm-specific characteristics, such as cash to asset ratio, cash conversion efficiency (Bates et al., 2009), current ratio (Tufail & Khan, 2013), size (Peel & Wilson, 1996), and variability of net operating income (Abuzayed, 2012), they are incorporated as control variables in our regression models.

Research Hypothesis and Method

Hypothesis and Model Development

A firm can implement an aggressive WCM policy by keeping a small amount of current assets in proportion to total assets or by maintaining higher current liabilities. On the contrary, by adopting a conservative WCM policy, a firm will keep a higher amount of current assets or a lower amount of current liabilities. Once an organization has adopted a WCM strategy, it encounters the dilemma of achieving an optimal level of working capital that creates a trade-off between liquidity and profitability (Hill et al., 2010). Deloof (2003) posits that firms need to optimize their working capital by considering each of the three components of WCM (receivables, inventories, and payables). This optimal level can maximize the value of a firm. Baños-Caballero et al. (2014) found an inverted U-shaped relationship between WCM and firm performance, implying that there exists an optimal level of investment in working capital that maximizes firm value. Thus, working capital below or above this level will negatively affect the firm’s performance. Subsequently, this evidence is confirmed by Afrifa (2016), Afrifa and Padachi (2016), M. Akbar and Akbar (2016), and Khan et al. (2016). Based on the aforementioned arguments, the following hypotheses are developed:

We develop two groups of models to examine the impact of WCM on firm performance by following Deloof (2003), Enqvist et al. (2014), and Ukaegbu (2014).

In the first group of models, profitability is measured by ROE, NTC is a measure of firm’s WCM efficiency, and NTCSQ is square of NTC. Following Erkens et al. (2012), dummy variables are introduced to segregate the study period into pre-, during, and postcrisis era. D1, D2, and D3 are dummy variables that represent a precrisis era, during the crisis, and postcrisis period, respectively. DAR is the average number of days a firm took to recover its receivables, DAP is the average number of days a firm spent to pay its short-term debt, DINV represents the average number of days that are required to sell the inventory, CTA is cash to asset ratio, CCE is cash conversion efficiency, CR is current ratio, SIZE is firm size, VONOI is variability in net operating income, and µ is an error term.

In the second group of models, TQ is used to measure firm market performance, while the rest of the variables are similar to those mentioned in the first group.

Empirical Strategy

Considering the panel nature of the data, we employ panel-based econometric models. A similar approach is used by Abuzayed (2012), Baños-Caballero et al. (2014), and Tahir and Anuar (2016). They employ GMM-based regression estimates due to the following advantages over the ordinary least squares (OLS)-based regression models. First, it allows us to control for unobserved heterogeneity and, therefore, eliminates the risk of obtaining biased results arising from this heterogeneity. Firms are heterogeneous and there are always characteristics that might influence their value that are difficult to measure or are hard to obtain, and which are not in our model.

Second, although the panel fixed-effects and random-effects models solve the heterogeneity problem, yet they do not address the endogeneity issue that may be present in our data. Studies on WCM–performance association highlight the possible existence of endogeneity problems (see, for instance, Baños-Caballero et al., 2014; Deloof, 2003; Juan García-Teruel & Martinez-Solano, 2007; Lyngstadaas & Berg, 2016; Pais & Gama, 2015). This problem arises when the observed relationship between firm profitability and firm-specific characteristics demonstrates not only the effect of independent variables on corporate profitability but also the influence of firm profitability on explanatory variables. As, in the present study, both exogenous and endogenous variables consist of financial ratios with many overlapping ingredients, there is a strong possibility of an endogeneity problem that could seriously compromise the empirical outcome. Therefore, the present study estimates the proposed models by employing two-step GMM regression models proposed by (Roodman, 2009). This methodology allows us to control for endogeneity problems by using instruments. Particularly, the study has employed all the independent variables as instruments, lagged up to 4 times. A similar approach was adopted in Baños-Caballero et al. (2014).

Results and Discussion

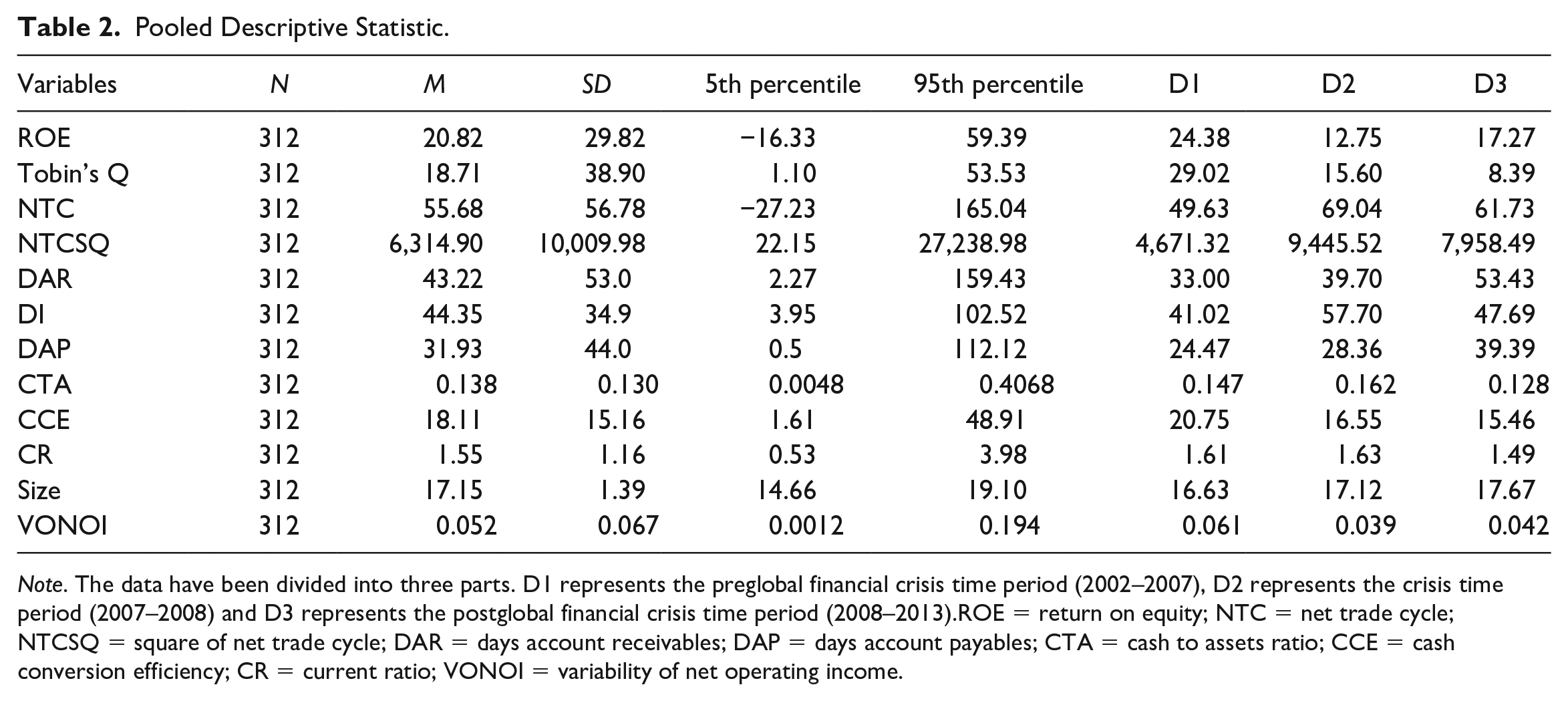

This section provides a brief account of empirical analysis conducted to observe the impact of WCM on the accounting and market performance of KMI-30 firms. Table 2 provides the descriptive statistics of all the variables employed in the study.

Pooled Descriptive Statistic.

Note. The data have been divided into three parts. D1 represents the preglobal financial crisis time period (2002–2007), D2 represents the crisis time period (2007–2008) and D3 represents the postglobal financial crisis time period (2008–2013).ROE = return on equity; NTC = net trade cycle; NTCSQ = square of net trade cycle; DAR = days account receivables; DAP = days account payables; CTA = cash to assets ratio; CCE = cash conversion efficiency; CR = current ratio; VONOI = variability of net operating income.

Descriptive Analysis

Table 2 provides the descriptive statistics of the variables. The average ROE of KMI-30 firms is 20.82, which is higher than Malaysian Shariah-compliant firms (18.67; see, for instance, Albdwy et al., 2014). If we look at the crisis dummies, ROE fairly presents a U-shaped behavior, that is, 24.8 for the precrisis era, 12.75 during the crisis period, and 17.27 in the postcrisis era. The average TQ ratio is 18.71, which depicts that sampled firms are fairly overpriced. The mean value of NTC for the precrisis era (49.63), crisis era (69.04), and postcrisis era (61.73) purports some interesting facts. In the literature, it is widely argued that during the GFC there was a rare availability of external credit; therefore, firms tightened their WCM policy to preserve their cash levels (Ramiah et al., 2014; Singh & Kumar, 2017). In contrast, our statistics reveal that during GFC, KMI-30 firms adopted a very conservative WCM approach as compared with the pre- and postcrisis era. One plausible reason for this contrasting evidence could be that KMI-30 has limited reliance on conventional financial institutions, mainly because of their financial screening criteria. Hence, depression in the conventional financial sector has minimal effects on such firms. Moreover, the larger collection period and smaller payment period contradict the conventional WCM strategy proposed by Gitman and Zutter (2011), but are in line with the Shariah principles because Islamic law emphasizes that the repayment terms should be convenient for the debtor. On the contrary, one should try to return the debt obligation as early as possible (Gilani, 2015). These statistics suggest that firms following the Shariah guidelines are more ethical in their management of account receivables and accounts payable. The average cash to assets ratio (CTA) ratio and current ratio are highest during the GFC era, which shows that, despite a lenient WCM strategy, sampled firms were in no danger of liquidity crisis.

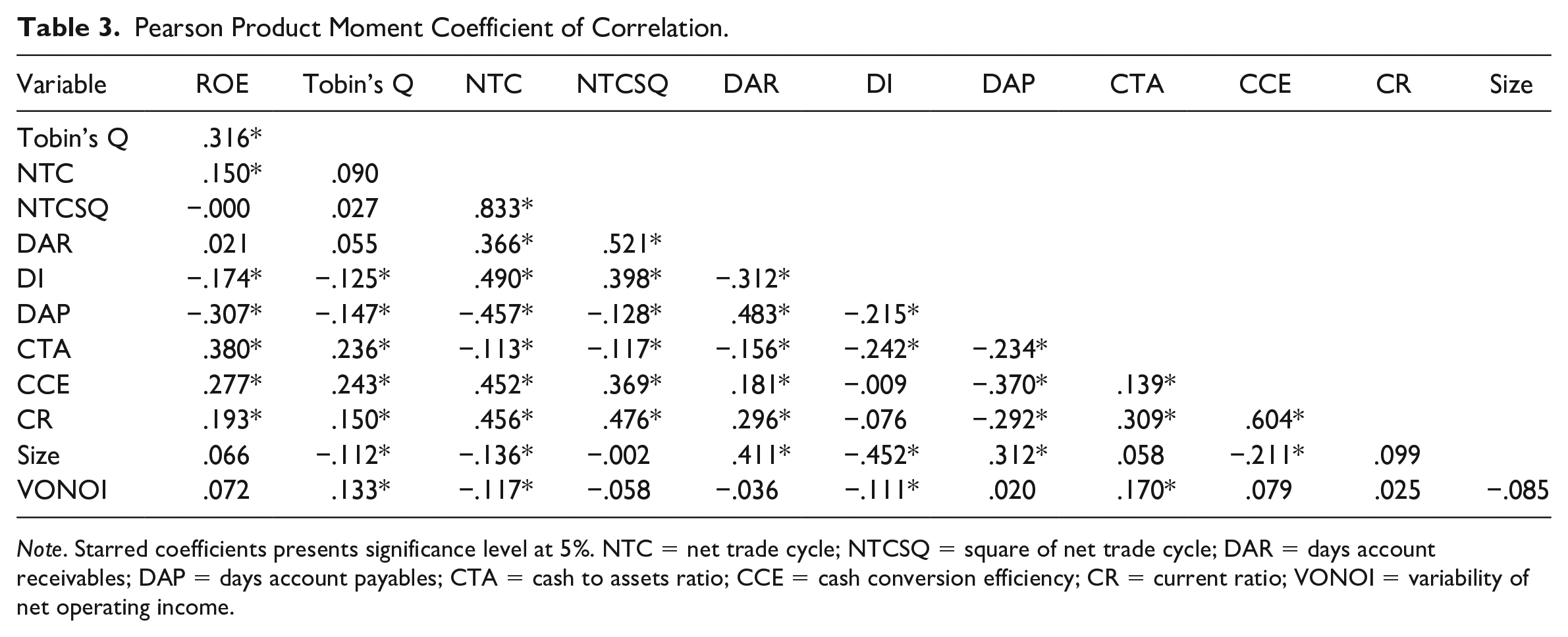

Table 3 presents the results of the Pearson product–moment coefficient of correlation. The correlation coefficient indicates the degree of a linear relationship between two or more variables. A significant positive correlation between ROE and TQ reveals that a firm’s accounting performance has a direct impact on its market performance. Moreover, NTC has a significant positive correlation with both ROE and TQ, which demonstrates that KMI-30 firms have further room for investment in working capital. One possible reason for this underinvestment could be that these firms can take lesser interest-bearing debt to comply with the guidelines of the Shariah supervisory board. A positive and statistically significant correlation coefficient is found between ROE and all the control variables (CTA, CCE, CR, Size, and VONOI). DINV is negatively correlated with both ROE and TQ, which indicates that KMI-30 firms can enhance their performance by increasing the inventory turnover. Similarly, all control variables have a positive association with TQ except firm size, which is in line with the previous studies (see, for instance, Peel & Wilson, 1996) that larger firms have less growth potential as compared with the small firms.

Pearson Product Moment Coefficient of Correlation.

Note. Starred coefficients presents significance level at 5%. NTC = net trade cycle; NTCSQ = square of net trade cycle; DAR = days account receivables; DAP = days account payables; CTA = cash to assets ratio; CCE = cash conversion efficiency; CR = current ratio; VONOI = variability of net operating income.

Regression Estimations

Association between WCM and firm profitability

Table 4 provides results of the regressions examining the relationship between WCM and the firm’s accounting performance. The NTC and its three components are separately regressed with ROE, a profitability measure of firm performance. The effect of GFC is taken into consideration by interacting NTC with D1 (precrisis era dummy), D2 (crisis-era dummy), and D3 (postcrisis-era dummy), respectively. Likewise, the components of NTC, that is, days accounts receivable, days accounts payable, and inventory turnover period are also interacted with the respective period dummy to explore the effects of individual components of WCM on firm performance in pre-, during, and postfinancial crisis era. The results indicate that the overall NTC has a significant positive (p < .01), whereas NTC square has a significant negative (p < .01), association with firm performance and hence supports our first hypothesis.

Regression Analysis (ROE as Dependent Variable).

Note. ***, **, and * represent 1%, 5%, and 10% significance level respectively. Whereas, ROE = return on equity; NTC = net trade cycle; NTCSQ = square of net trade cycle; AR = account receivable; SIZE = firm size; CR = current ratio; VONOI = variability of net operating income.

These results confirm an inverted U-shaped relationship between WCM and the performance of KMI-30 firms. These findings are consistent with the previous research (Afrifa, 2016; Afrifa & Padachi, 2016; Baños-Caballero et al., 2014). Moreover, a positive association between WCM and profitability indicates that KMI-30 firms have room for further investment in working capital to optimize their performance. One possible reason for this under-investment could be that firms have limited access to short-term finances in the developing countries (Abuzayed, 2012). Also, KMI-30 firms are even more constrained and have fewer external financing alternatives as these firms have to keep their interest-bearing debt below the limit defined by Shariah supervisory board.

The interaction dummy variables (D1 * NTC, D2 * NTC, and D3 * NTC) depict that the WCM–profitability relationship remains unchanged for the pre-, during, and postfinancial crisis era. However, the coefficient value for crisis era (0.213) is larger than pre- (0.162) and postcrisis period (0.162), which reveals that the WCM–profitability relationship was more pronounced during the GFC of 2007–2008.

Model 2 in Table 4 analyzes the influence of individual components of WCM (day’s receivables, days payable, and day’s inventory turnover) on profitability. The results for DAR highlight a positive and statistically significant (p < .05) relationship with profitability, implying that KMI-30 firms can increase their profitability by adopting a more generous credit policy as the optimal level of WCM has yet to reach. Similarly, Deloof and Jegers (1996) argue that firms with higher profitability should possess higher account receivables because these firms have more cash to lend to their customers. This result is in line with Abuzayed (2012), whereas it differs from Albdwy et al. (2014) and Raheman and Nasr (2007). Besides, we find a negative and statistically significant relationship between DAP and profitability, which suggests that a shorter account payable cycle can further enhance the profitability of sampled firms. Thus KMI-30 firms can increase their profitability by offering trade discounts on accounts payable instead of utilizing trade credits as a source of finance. Similar results were reported by Abuzayed (2012) and Enqvist et al. (2014). DINV also indicates a negatively significant (p < .01) coefficient with profitability. It suggests that firms can increase profitability by shortening inventory conversion periods. This result contradicts Abuzayed (2012) and Kenyan firms (Mathuva, 2010), whereas it is consistent with Malaysian Shariah-compliant firms (Albdwy et al., 2014), Finnish companies (Enqvist et al., 2014), and Pakistani firms (Raheman & Nasr, 2007). Overall, these findings suggest that KMI-30 firms can achieve optimal working capital level by increasing day’s accounts receivable while decreasing days’ accounts payable and inventory conversion period.

Models 4, 5, and 6 in Table 4 examine the influence of individual components of WCM (DAR, DAP, and DINV, respectively) on firm profitability for pre-, during, and postcrisis period. The reported results indicate that these components do not have a static relationship with profitability under different macroeconomic settings. The DAR–profitability relationship is significant only for postcrisis era. It suggests that the importance of DAR concerning the profitability has been increasing after the GFC of 2007–2008. The negative relationship between DAP and ROE during (p < .01) and after (p < .01) the crisis period implies that timely payments by KMI-30 firms help to improve performance. Moreover, the DINV-profitability relationship is significant (p < .1) only for the crisis period. It reveals that the role of efficient inventory management was more pronounced during GFC compared with the pre- and postcrisis era.

The results for control variables are in aggregate and represent the overall period of study, 2002–2013. CTA, CCE, SIZE, and VONOI have a positive and statistically significant association with the firm performance, which indicates that sampled firms can enhance profitability by improving liquidity, reducing bad debts, and expanding sales volume.

Moreover, the values of AR2 in all the above regression models are insignificant, confirming that there is no issue of autocorrelation. Besides a healthy value of the Hansen test shows that there is no endogeneity problem in our models.

Association between WCM and market performance

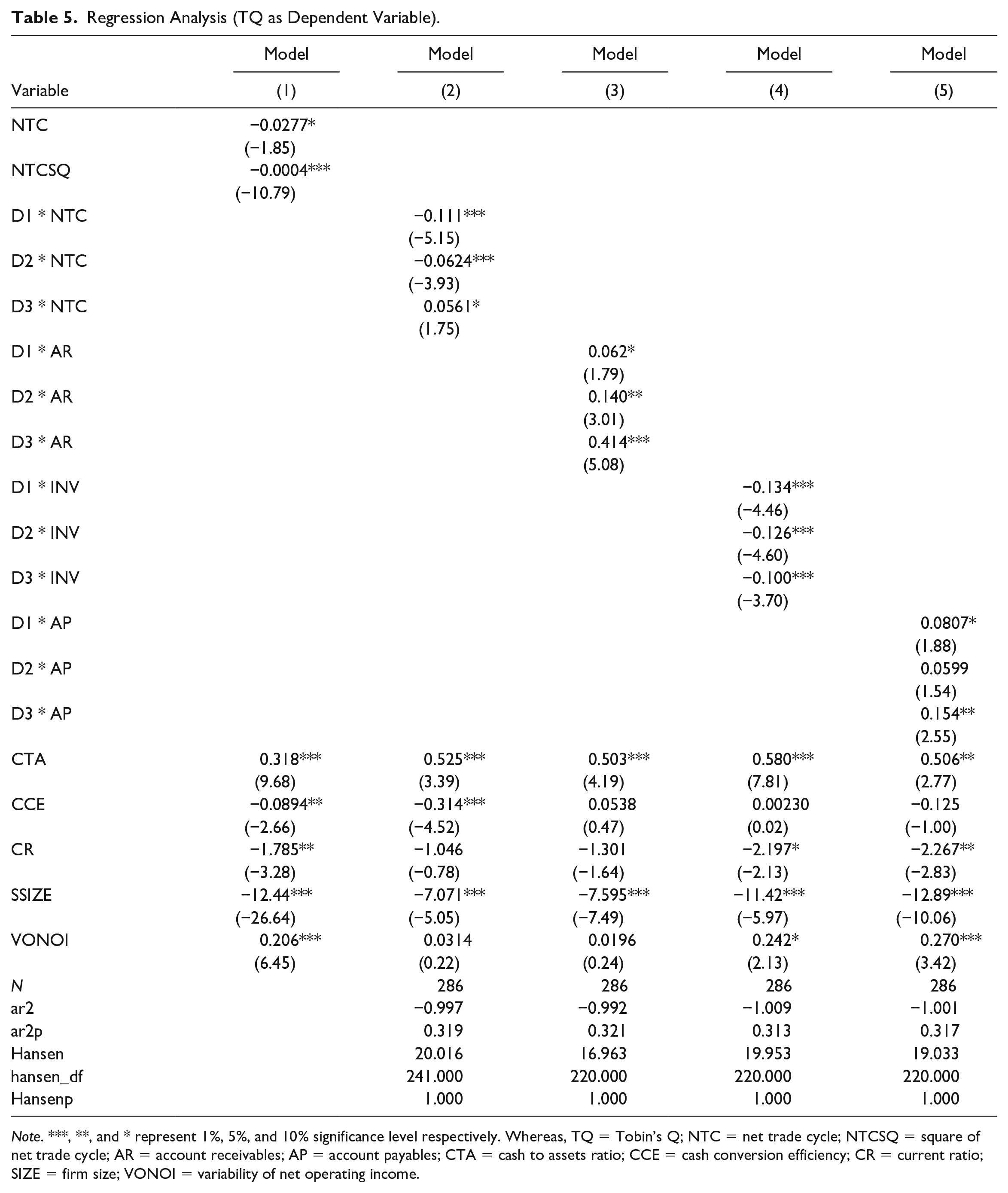

Table 5 provides the results of the regression models examining the association between WCM and a firm’s market performance. NTC and its three components are separately regressed with TQ. The effects of GFC are taken into consideration by interacting NTC and its components with D1, D2, and D3, respectively. Contrary to the findings of ROE, TQ has a negative coefficient with both NTC and NTCSQ, significant at 10% and 1% level, respectively. It implies that unlike firm profitability performance, investors have an aggressive approach toward firm WCM practices and thus any additional investment in WCM hurts its market performance.

Regression Analysis (TQ as Dependent Variable).

Note. ***, **, and * represent 1%, 5%, and 10% significance level respectively. Whereas, TQ = Tobin’s Q; NTC = net trade cycle; NTCSQ = square of net trade cycle; AR = account receivables; AP = account payables; CTA = cash to assets ratio; CCE = cash conversion efficiency; CR = current ratio; SIZE = firm size; VONOI = variability of net operating income.

If we look at the interactive dummy variables, it indicates that the precrisis and crisis-era WCM–market performance relationship was significantly negative, whereas after the crisis period it became positive. This suggests that keeping a higher working capital level for precrisis and crisis (postcrisis) time was perceived inefficient by the investors. Moreover, the descriptive statistics unveil that the working capital level for the precrisis period (49.63) is lower than the postcrisis era (61.73). This indicates that optimal working capital level does not remain static; rather, it varies with a change in the prevailing macroeconomic environment.

In Models 4, 5, and 6, each component of WCM separately interacts with the crisis dummies. The results reveal that TQ has a positive coefficient for DAR in all the observed periods, suggesting that further investment in receivables can enhance a firm’s market value. Moreover, in contrast to ROE, TQ is positively associated with DAP, which indicates that the account payable deferral period exerts a different impact on firm profitability and market performance. This is attributed to the fact that investors interested in wealth maximization have a different perspective to evaluate a firm’s operating fundamentals than financial managers. A negative and statistically significant coefficient between DINV and market performance makes economic sense as lesser inventory holdings will decrease operating costs related to product storage and expiration.

Supplementary findings reveal that size of the firm is negatively linked to market performance because of lesser potential for further growth. The CTA has a positive coefficient with TQ, while the current ratio is found to have a negative association with market performance. It suggests that, in contrast to other current assets, an increase in cash levels helps to enhance a firm’s market performance.

Robustness Check

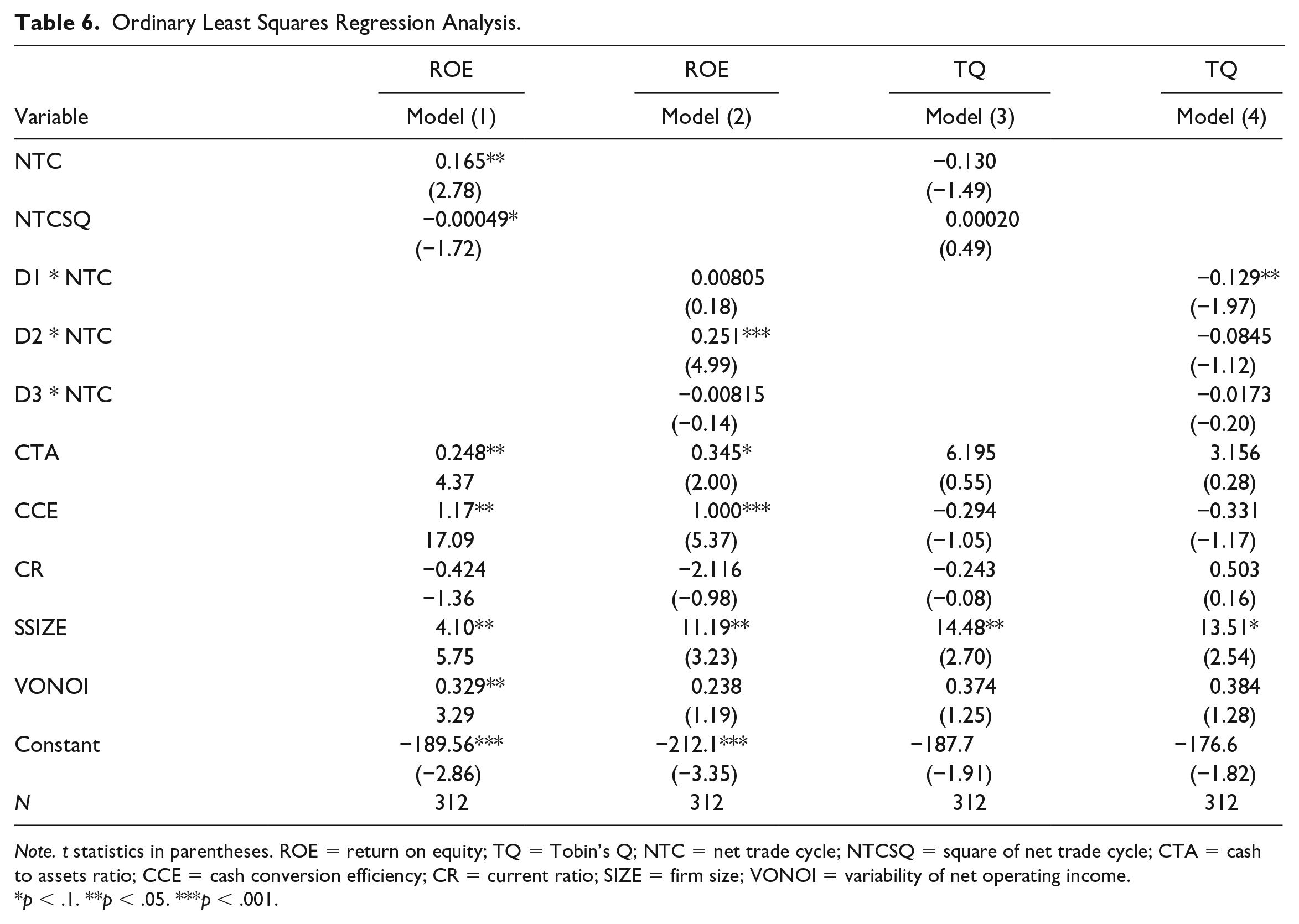

As a robustness check, we have reestimated our regression analysis using the OLS technique while controlling for firm and year fixed effects. The results are reported in Table 6. In line with the findings of Table 4, NTC is found to have significant positive effects on ROE. Once again, NTCSQ is negatively associated with firm performance, strengthening the proposition of inverted U-shaped relationship between WCM and accounting performance of KMI-30 indexed firms. In a nutshell, the results of OLS regression analysis are very much similar to those found in GMM settings, with few exceptions of the level of significance for some crisis dummies.

Ordinary Least Squares Regression Analysis.

Note. t statistics in parentheses. ROE = return on equity; TQ = Tobin’s Q; NTC = net trade cycle; NTCSQ = square of net trade cycle; CTA = cash to assets ratio; CCE = cash conversion efficiency; CR = current ratio; SIZE = firm size; VONOI = variability of net operating income.

p < .1. **p < .05. ***p < .001.

Conclusion and Policy Implications

As firms that constitute an Islamic market index have to follow a different set of guidelines to manage their operations, this study examined the impact of WCM efficiency on the profitability and market value of firms listed on KMI-30 for pre- (2002–2007), during (2007–2008), and post-GFC era (2008–2013). The results of descriptive statistics reflect that, by contrast to the conventional businesses, KMI-30 firms adopted a very conservative WCM policy during the GFC of 2007–2008. Besides, these firms are also more ethical in their short-term financial management practices. Furthermore, the study confirms the finding of Baños-Caballero et al. (2014) as a concave relationship is observed between WCM and firm performance in KMI-30 firms of Pakistan. The results of GMM regression estimation suggest that there exists an optimal working capital level; the relationship between investment in working capital and firm performance stays positive until that optimal level is reached. Beyond that inflection point, excessive investment in working capital negatively affects the firm performance. Moreover, it is also evident that optimal working capital level does not remain static, rather it changes with a change in the prevailing macroeconomic environment as varying empirical outcomes were observed in the pre-, during, and post-GFC scenarios.

The study has several policy implications for the stakeholders. First, the WCM is a dynamic concept, so the financial managers need to adjust the WCM practices in response to the prevailing macroeconomic environment. Second, a negative association between excess working capital and market performance proxy indicates that investors penalize the firms for their inefficient WCM. Therefore, management must also consider the adverse effects of poor short-term financial management on the stock market performance. Third, the firms following the guidelines of KMI were found to be more ethical as they make timely payments to the creditors without unnecessary delays, which is a positive sign for the creditors who are dealing with such firms. Fourth, a concave relationship between WCM and firm performance asserts that there exists an optimal working capital for firms up to which investments in working capital accounts have a positive impact on a firm’s financial performance. However, any further investment beyond that optimal point adversely affects corporate performance. Hence, firms must strive to achieve an optimal working capital level to boost financial performance. Finally, in the face of limited financial resources, corporate policy makers in developing countries shall encourage firms to optimize their WCM, so that these excess funds could be allocated to value-enhancing investment projects.

Nonetheless, the present research is not without limitations. First, the KMI-30 index only constitutes 30 firms that fulfill its partially Shariah compliance criteria. Therefore, our analysis is confined to only those firms that comply with the criteria laid down to be included in the KMI-30 index. Future studies in this domain shall explore the working capital practices of firms listed in indices that constitute a large sample size coming from diverse regions such as the Dow Jones Islamic market world index. Notwithstanding, the KMI-30 index only encompasses Pakistani firms, so our results could only be generalized to the firms operating in Pakistan or to firms working in countries that are at a similar stage of economic development as Pakistan. Hence, future research can investigate Shariah-compliant firms from various geographical settings to ascertain the validity of this phenomenon.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research and/or authorship of this article: The authors highly acknowledge the financial support of the Guangzhou College of South China University of Technology under the “Excellent PhD Research Project” vide Grant YB180001.