Abstract

Identifying financial strategies, which help a bank to survive a crisis, is the main purpose of the article. Low oil prices and the COVID-19 pandemic is the latest crisis being faced by the Gulf Cooperation Council (GCC) banks. This article examines the financial strategies of those banks that managed to retain good credit ratings both before and after the global financial crisis, so as to throw light on the characteristics of banks that managed to remain steady and stable. This article analyzes the Fitch credit ratings of 51 Islamic and conventional banks, operating in the GCC, divided into pre–global financial crisis (2002–2007) and post–global financial crisis (2008–2013) periods. Trend and behavior of average ratios of top-rated banks in both the periods is first attempted before moving to the “Ordered Choice Logit” regression method to further analyze the data. Regression results indicate that size and cost management are very important factors in ratings both before and after the financial crisis. As long as asset quality is under control, liquidity is the focal point in achieving good ratings. Top-rated Islamic banks seem to be following a strategy of allowing capital ratios to trend down during a crisis as long as capital is well above the regulatory requirements. The article is the first of its kind, which examines credit rating strategies of GCC Islamic banks and conventional banks. The findings of the article are useful for banks as they throw light on appropriate strategies to be adopted by banks during crises.

Keywords

Introduction

The net profits of banks in the Gulf Cooperation Council (GCC) countries (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates) are under pressure due to low oil prices and the COVID-19 pandemic. Furthermore, banks across the world are facing financial crises periodically, the most recent being the one due to the COVID-19 pandemic. Pressures facing the banks in the GCC region are both domestic and global. The rationale of the article is to examine the question, “What are the best financial management practices that are important for banks in the GCC to remain credit worthy, active, viable, and healthy both before and after a crisis?”

The article hopes to find answers by looking at the 2008 global financial crisis (GFC), and how it has affected the credit rating and ranking of GCC conventional and Islamic banks. The article throws light on the characteristics of the top-ranking banks both before and after the financial crises. It also recommends the internal financial strategies that bank managements should follow to ensure that the credit rating of a bank is not affected by a crisis that may be due to domestic factors, such as low oil prices, or global factors, such as the COVID-19 pandemic.

This article analyzes the Fitch credit ratings of 51 banks (Islamic and conventional) operating in the six GCC countries, divided into pre-GFC (2002–2007) and post-GFC (2008–2013) periods. The trend and behavior of average ratios of top-rated banks in both the periods is first attempted before moving to the “Ordered Choice Logit” regression method to further analyze the data.

Although there may be an argument that the article is based on old data, the justification for using the data is to arrive at lessons that help banks to not only survive but also improve their credit ratings even during a crisis. The article is the first of its kind, which examines credit rating strategies of conventional and Islamic banks operating in the Gulf region. The findings of the article are extremely important for banks as they throw light on appropriate strategies to be adopted by banks during crises.

One key distinction between the two types of systems is that conventional banks earn by charging interest and service fee, whereas Islamic banks earn by sharing profits (and losses), leasing, charging fees for offerings rendered, and the usage of different sharia contracts of exchange. The purpose of the article is not to find out whether Islamic banks perform better during a financial crisis. Rather, the purpose is to examine whether these two groups of banks use different strategies to stabilize and improve credit ratings during a crisis.

The main findings of the article are that size and cost management are very important factors in ratings both before and after the financial crisis. As long as asset quality is under control, liquidity is the focal point in achieving good ratings. Top-rated Islamic banks seem to be following a strategy of allowing capital ratios to trend down during a crisis as long as capital is well above the regulatory requirements.

Following the “Introduction” section, the article consists of six sections, namely, “Literature Review,” “Research Design,” “Sample and Data,” “Ratio Analysis Results,” “Ordered Choice Regressions Results,” and “Conclusion and Policy Implications.”

Literature Review

Horrigan’s (1966) article was one of the early articles that evaluated the power of financial ratios in predicting corporate bond ratings. Quantitative studies on determinants of bank credit ratings identify asset quality, capital adequacy, liquidity, profitability, earnings quality, and size as the key variables that can explain differences in ratings between banks (Bheenick and Sirimon, 2010; Caporale et al., 2009; Huang & Shen, 2011; Poon et al., 1999; Wolf, 2015). The impact of financial crises on the credit rating of banks has been the focus of a large number of studies, for example, Berger and Bouwman (2008, 2013), Cetorelli and Goldberg (2011), Chiaramonte and Casu (2017), and Meriläinen and Junttila (2020). These studies find that behavior of liquidity and adequacy of capital ratios are two key factors influencing the rating of banks during financial crises. There are no studies on the impact of GFC on the behavior of credit ratings of GCC banks.

Cetorelli and Goldberg (2011) find that profitability and precrisis capital levels can give an indication of the rating of the bank before the onset of a financial crisis (refer to Murthy, 2013 for a more elaborate review). They further find that liquidity plays a major role in the credit rating of the bank in the postcrisis period. Berger and Bouwman (2008), using U.S. bank data, examined the role of liquidity in precrisis and postcrisis periods. They find that there is either a sharp decrease or a sharp increase in liquidity before a financial crisis. Large banks that maintained good profitability and liquidity levels during a crisis were able to improve their rating in the postcrisis period and, similarly, small banks with strong capital ratios improved their position.

One strand of literature on financial crisis looks at the impact of foreign funding on the ability and stability of banks operating in a particular country. These studies conclude that banks that depend on external funds stopped or reduced lending during the financial crisis, whereas banks that depended on domestic deposits continued to operate normally (Haas & Lelyved, 2011). The more the dependence of banks on external funds, the higher the possibility of transmission of financial crisis from across the borders (Cheung et al., 2009). Another strand of literature examines the linkage between the financial sector and the real sector during crisis periods (Bernanke & Gertler, 1989; Dell’Ariccia et al., 2008; Sarno & Taylor, 1999). During financial crises, banks reduce lending, interest rates tend to move up, and corporate investment dries up, thus leading to a slowdown in economic activity and, perhaps, a recession. Asset prices move down and collateral values fall, leaving banks with a large amount of nonperforming assets (NPA), thus leading to down rating by rating agencies.

Another recent strand of literature looks at whether efficiency helps a bank to survive and thrive during financial crises. A particularly interesting study by Assaf et al. (2019) uses data from five U.S. financial crises situations and concludes that banks that are cost-efficient during the precrisis period have reduced probability of failure due to the upcoming crisis.

Studies related to the impact of financial crisis on Islamic finance can be broadly divided into two groups. One set of studies looks at the impact of global financial shocks on Islamic investment/financial products (Abdul Razak & Amin, 2013; Ali & Nisar, 2016; Arshad & Rizvi, 2013; Rahman & Kassim, 2017; Siddique & Sheik, 2016). Another set of studies looks at the impact of GFC on Islamic banks and how they performed relative to conventional banks (Abdelle & Kassim, 2012; Akhtar, 2013; Chapra, 2017; Hasan & Dridi, 2010; Miniaoui & Gohou, 2013; Yorulmaz, 2017; Yusuf & Kassim, 2012; Zehri & Al-Herch, 2013).

Ahmed et al. (2014) examined the resilience of Islamic banking during the GFC. They conclude that if all banks were Islamic, financial crises would be less likely because they have built-in stabilizers that lower the probability of crises, a view similar to that expressed by Ahmed (2010) and Chapra (2017). Hasan and Dridi (2010) find that Islamic banks’ business model helped limit the adverse impact on their profitability (in Year 2008) compared with conventional banks. Hidayat et al. (2014) found that the financial crisis significantly affected financial performance of Islamic banks in the GCC. A significant difference between the above study and the present study is that, whereas the Hidayat et al., study uses return on assets (ROA) to measure financial performance, the present study uses credit ratings, which is a more comprehensive measure of strength and stability.

Research Design

Data of 40 GCC conventional banks and 11 GCC Islamic banks are used in this study to identify the financial practices that contribute to the position (or rating and ranking) of a bank among its peers. Bank ratings, as reported by Fitch Ratings Inc., are used to rank a bank among its competitors. Bank financial practices are measured by eight dimensions (Prefontaine et al., 2002) and the related ratios are presented in Table 1:

Key Ratios Related to Bank Financial Management Practices.

At the second stage, the article uses the logit regression technique to analyze the data to identify which factors contribute most to rating and rating changes (this article further extends the work undertaken by Murthy, 2013). The behavior of banks, which managed to get good Fitch ratings both before and after the crisis, helps us to learn lessons about good financial management practices that are important for banks to remain healthy, viable, and active. Data for the article are drawn from BankScope database and covers the period from 2002 to 2013. Years 2002 to 2007 are identified as pre-GFC years and Years 2008 to 2013 are post-GFC years. The E-Views software was used for the purpose of estimation of ordered choice logit regressions.

Two alternate approaches to estimation, the Copula approach (Cherubini et al., 2004; Nguyen & Bhatti, 2012) and ordered choice regression approach (Greene, 2008) were considered. As the study is based on annual data from 2002 to 2013, and in view of limitations with respect to the number of observations of data available, it was decided to go with the regression approach rather than the Copula approach.

Ordered choice logit regression is a well-accepted technique used for estimation in the presence of the qualitative dependent variables. The GCC banks included in this study are ordered as per their Fitch ratings. The values assigned to the qualitative dependent variables and the associated Fitch ratings are shown in Table 2.

Fitch Ratings and Dependent Variable Values.

The independent variables used in the logit regression are the eight variables representing the eight dimensions of financial management practices, including log of total assets (TA) as a control variable for the size (the empirical model used in this article is adapted from Murthy, 2013).

The following Ordered choice model was estimated using the logit technique:

RAi = β0 + β1*CAPi + β 2*ROEi + β3*ROAi + β4*COSTi + β5*NIMi + β6*LIQi + β7*LLGLi + β8*TAi,

where RAi is the rating of the bank (dependent variable can take values from 1 to 14, where 14 is the highest rating and 1 is the lowest); CAP is total capital ratio; ROE is return on equity; ROA is return on assets; COST is cost to income ratio; NIM is net interest margin; LIQ is liquid assets to demand deposits; LLGL is loan loss reserves to gross loans; and TA is total assets.

Ordered choice regression technique allows us to focus on financial management practices that are most important for a bank to obtain a high rating. Assuming that the original Fitch rating does differentiate between good and bad performance, the regression technique allows us to identify variables that lead to better performance.

Sample and Data

All the GCC banks for which Fitch ratings are reported by the BankScope (now renamed as Orbis Bank Focus) database are included in the sample. The banks operating in the GCC region are divided into two groups: conventional banks and Islamic banks. The data of 40 conventional banks and 11 Islamic banks were used for estimation. The appendix gives the list of banks included in the study. Classification of banks into conventional banks and Islamic banks is as given by BankScope database. Issues related to changes in classification and misclassifications are also explained in the same appendix. One key distinction is that conventional banks earn by charging interest and service fee, whereas Islamic banks earn by sharing profit and loss, leasing, charging fees for offerings rendered, and the usage of different sharia contracts of exchange.

Regression results for conventional banks for pre- and post-GFC periods, and for Islamic banks for the post-GFC period are reported in the “Results and Discussion” section. Fitch ratings for very few GCC Islamic banks for the pre-GFC period are reported and the data have many missing values. Therefore, pre-GFC Islamic bank regression is not attempted.

Estimating the regressions equation using ordinary least squares (OLS) method is not valid when using a qualitative dependent variable. Limited dependent variable regressions techniques such as ordered logit and probit are good alternatives in such cases (Hill et al., 2001). Estimation is done by using the maximum-likelihood method. This method is an iterative estimation technique that is particularly useful for estimating nonlinear equations (Asteriou & Hall, 2011). Although there is difference between logit and probit methods, the differences are marginal (Gujarati, 2003; Woolridge, 2000). In this study, the limited dependent variable regression is estimated using Ordered Choice Logit—Brendt, Hall, Hall and Hausman (BHHH) algorithm. The BHHH algorithm has the advantage that, if certain conditions apply, convergence of the iterative procedure is guaranteed.

Pooled estimation method was not used because credit rating (the dependent variable) is not time dependent or unit dependent (Snijders, 2005). Credit rating given by reputed rating agencies is not likely to be biased by the name of the bank or the year in which rating is being done. Snijders (2005) says that, if the dependent variable is not unit dependent, it is superfluous to use this set of units as a level in the multilevel analysis. Instead, to handle possible problems due to heteroscedasticity, robust (Huber/White heteroscedasticity consistent) standard errors are reported. To the extent that the method is not panel estimation, typical questions that arise in panel estimation, such as short versus long panels, balanced versus unbalanced panels, and inadequate sample size are not relevant here. Furthermore, the sample size in both pre- and post-GFC periods is large enough (n = 175 and 223 for pre-GFC and post-GFC regressions, respectively), and therefore the results reported in this study do not suffer from problems related to lack of degrees of freedom.

Model Selection, Miss-Specification Tests, and Robustness Checks

Both forward and backward regressions methods were used to check for linkages. Jarque–Bera (JB) miss-specification test for normality of residuals was used at the model selection stage. Akaike information criterion (AIC) and Bayes information criterion (BIC) were used to decide whether to include or drop a variable. JB improved dramatically when the TA variable was transformed into a log form. Multicollinearity between net interest margin (NIM), ROA, and return on equity (ROE) was a problem affecting all regressions. In preparing bank income statements, NIM is one of the most important items used to calculate operating income and net income after taxes, implying that there is likelihood of strong correlation between these variables, which was indeed the case. ROA and ROE variables were dropped to overcome the problem of multicollinearity. To handle any possible problems due to heteroscedasticity, robust (Huber/White heteroscedasticity consistent) standard errors are reported.

Results and Discussion

The “Results and Discussion” section is divided into two parts: The first part shows the results of the ratio analysis, and the second part presents the regression results.

Ratio Analysis Results

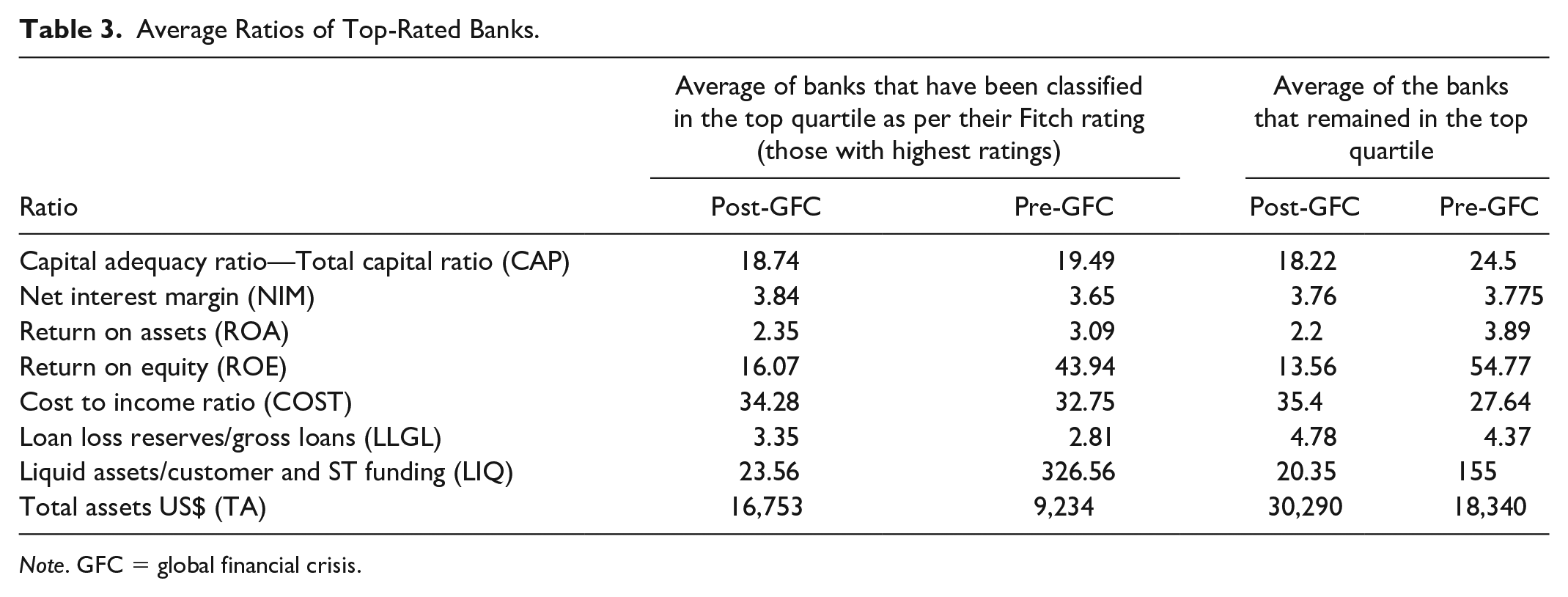

Fitch ratings are used to identify the best banks operating in the six GCC countries. Statistics related to the banks that were ranked in the top quartile as per post-GFC ratings and those which remained in the top quartile both before and after the financial crisis are reported in Table 3.

Average Ratios of Top-Rated Banks.

Note. GFC = global financial crisis.

For the purpose of ratio analysis, Year 2006 is taken as the representative pre-GFC year and 2009 as the representative post-GFC year. Average of 5 years before and 5 years after could have been done but was not attempted as it would mean too much of averaging because, as it is, the figures in Tables 3 and 4 are already average of all GCC banks. Quartile values—first (lowest) quartile, second quartile, and third quartile—for all GCC banks are reported in Table 4. In trying to find out which financial ratios did make a difference in ranking, we compare the ratios of the top quartile banks reported in Table 3 with the quartile values reported in Table 4. Such an analysis allows us to achieve a deeper understanding on what makes a top-rated bank different from the rest of the crowd.

Ratios of All Locally Incorporated Banks in GCC.

Note. GCC = Gulf Cooperation Council; GFC = global financial crisis.

The behavior of ROA and ROE of top-ranked banks compared with others before and after the financial crisis is especially worth noting while reading the figures in Tables 3 and 4. Banks that were top rated (as per Fitch ratings) reported better returns on equity both before and after the financial crisis. The case is similar with respect to the ROA figures. Banks in the lowest quartile suffered badly due to a sharp drop in ROA to a figure as low as 1% compared with 2.35% of the top-ranked banks. Before the financial crisis, bottom-rung banks managed to do reasonably well in terms of profitability (ROE at 18%). The crisis had a clear adverse impact on these banks as their ROE declined to 9%.

ROE and TA figures reported in Tables 3 and 4 show that top Fitch-rated banks not only delivered double digit profitability but also showed healthy growth in spite of a financial crisis. These banks were adopting financial management practices—higher levels of capital, liquidity, and margins—which allowed them to operate without hindrance during the financial crisis.

Ratios of the banks (Table 3), which remained in the top quartile, tell us that, to be top ranked, a bank should maintain a high total capital ratio (CAP; above 18.22% in 2009 and above 24.5% in 2006.). Compared with quartile values of all GCC banks (reported in Table 4), these figures are above the median. We conclude that, for a bank to be top credit rated, it should be well capitalized with a CAP of around 20%.

Interestingly, the top banks reduced the level of capitalization with the onset of crisis. Another way of looking at the figures would be to conclude that, to be successful, a bank should have higher than the required capital ratios before the onset of a financial crisis, so that it can allow the capital ratios to drop during a crisis while continuing to operate normally. The fact that capital is higher than the regulatory requirements before the crisis allows them to continue to operate effectively during the crisis period.

Nonperforming assets ratio (LLGL), as measured by loan loss reserves to total loans of the top banks, were higher than median values of all GCC banks both before and after the financial crisis. However, the NPA of the top banks did not change much during the crisis period. While interpreting the NPA figures, we first note that a higher NPA ratio is the result of higher amount of loan loss reserves (as ratio of gross loans), and that higher NPAs should result in lower performance and lower rating—that is to say that there is negative relationship between NPA and rating. We can take the argument one step further and say that if a bank is able to generate high profits, is well capitalized, has high interest margins, and has sufficient liquidity it can overcome the handicap due to higher NPAs (i.e., poor asset and credit quality). This statement is true for the top banks when we compare their profits (ROA and ROE), capitalization (CAP), margins (NIM), and liquidity (LIQ) with median values of all GCC banks.

Costs to income ratios of the top banks are lower than the median values of all GCC banks in the pre-GFC period but higher in the post-GFC period. Cost to income ratio (COST) is derived by taking overheads (administrative and staff expenditure) as a percentage of net interest income plus other income. A higher COST implies that, to generate US$1 of income, a bank is spending more on overheads compared with other banks. That is to say that the bank is spending more on staff and infrastructure. This may be due to higher salaries, larger size of manpower employed, costlier equipment, higher rents, and so on. High COST would result in low operating profits that lower ROA other things remaining unchanged. Results from Tables 3 and 4 indicate that better ranked banks are experiencing higher COSTs, as compared with all GCC banks, but that COSTs of top-ranked banks is only marginally higher. While it is difficult to conclude on the basis of quartile means, the regression results presented in the next section give a clearer picture, showing that higher COSTs have a negative impact on credit ratings.

Liquidity peaked in GCC countries in 2007, reflecting the inflow of speculative capital. The UAE received the bulk of these inflows as indicated by the significant rise in its liquidity ratios in 2007. Liquidity conditions started to tighten in early 2008 as speculative capital inflows reversed. Liquidity was squeezed further, following Lehman’s collapse in September 2008 (Al-Hassan et al., 2010).

Liquidity behavior (as measured by liquid assets to customer and short-term funding) of the top banks is very interesting when compared with the other banks. Before the onset of the crisis, the top banks maintained very high liquidity ratios, but they reduced liquidity sharply after the crisis. Table 3 shows that the highly ranked banks maintained a very high liquidity ratio (more than 4 times) before the crisis as compared with all GCC banks, but reduced liquidity to a level below the all GCC banks in the postcrisis period. As the crisis developed, these banks seem to have kept on reducing liquidity from a very high level to a very low level. What could be the reasons for this behavior is definitely worth asking. Liquid assets include cash in hand, money at call and short notice, deposits with central bank, deposits with other banks, government treasury bills, and government securities.

The difference in liquidity behavior between the top banks and other GCC banks is due to their loan book. The top banks experienced high growth in deposits (80% plus and double the growth of all GCC banks) and, at the same time, they increased their loan book compared with available deposits. The loan to deposit ratio of the top banks almost doubled during the period 2006 to 2009 from around 50% to above 100%. What happened is a change in the asset mix and asset allocation of the top banks. As the top banks passed through the period of crisis, they kept on increasing their loan and advances portfolio while reducing liquid assets (as a percentage of TA). This resulted in a sharp decrease in liquidity ratios of these banks. In comparison, the average liquidity ratio of all GCC banks did not change much during this period. Two possible reasons for the sharp increase in loan to deposit ratio of the top banks are as follows: (a) During a crisis period, low-ranked banks may be unable to lend (due to lower deposit inflows, capital constraints, and liquidity constraints) and therefore borrowers move to top banks that are able to accommodate requests for new loans and, in the process, top banks may be able to generate higher spreads (NIMs), and (b) the sharp decrease in interbank interest rates and money market interest rates during the crisis period made loans and advances more attractive compared with investing in government securities and lending to other banks.

NIMs of top-ranked banks are significantly higher than median values of GCC banks both before and after the financial crisis. Furthermore, top-ranked banks increased their NIMs during the crisis period, whereas all GCC banks experienced a substantial reduction in NIMs. One reason for higher NIMs is the riskiness of the loan portfolio. Lending is typically riskier during a financial crisis as the chances of non-repayment increase, especially if the financial crisis has a substantial impact on the real sectors. This is borne out by the experience of banks in Dubai during the financial crisis. During the crisis, many banks experienced problems such as lower deposit inflows, lack of liquidity, and inability to lend at their normal pace. In such a situation, borrowers naturally search for other banks that are willing to give loans even if the cost of borrowing is higher. Top banks that had lots of liquidity and were experiencing substantial deposit inflows were not only able to lend but also charged higher NIMs. To the extent that higher NIMs proxy for higher risk levels, rating agencies downgrade a bank although it still remains as a top-ranked bank among the banks in that region. A few examples of downgrade by Fitch are Emirates NBD, National Bank of Abu Dhabi, National Bank of Kuwait, and Conventional Bank of Dubai.

Ordered Choice Regressions Results

Regressions results for conventional banks for the pre-GFC (2002–2007) and post-GFC periods (2008–2013) and for Islamic banks for post-GFC period are reported in this section. As mentioned earlier, pre-GFC Islamic bank regressions were not attempted because very few Fitch ratings are available for GCC Islamic banks for period before the GFC.

Conventional Bank Regression Results

Table 5 shows the estimation results using Fitch pre-GFC ratings and Fitch post-GFC ratings. Both the ordered choice logit estimates reported below are good in terms of likelihood ratio (LR). The LR statistic is a chi-square goodness-of-fit statistic (Field, 2009).

Conventional Banks.

Note. Ordered choice logit regression results. Method: Maximum likelihood (Brendt, Hall, Hall and Hausman [BHHH] algorithm) with robust (Huber/White heteroscedasticity consistent) standard errors. GFC = global financial crisis; COST = cost to income ratio; TA = total assets; CAP = total capital ratio; LIQ = liquid assets to demand deposits; LLGL = loan loss reserves to gross loans; NIM = net interest margin; AIC = Akaike information criterion; LR = likelihood ratio.

p < .01 (significant at 1% level). **p < .05 (significant at 5% level).

Although statistical packages routinely report pseudo R2, many experts caution against using it. Pseudo R-squared does not have the same interpretation as the normal R-squared, and for this reason is not used very much by most researchers (Asteriou & Hall, 2011). Furthermore, they are a wide variety of pseudo R2 statistics that can give contradictory conclusions and should be interpreted with great caution (UCLA-IDRE, 2018). Therefore, in this study, LR statistic is used instead of pseudo R2 to measure goodness of fit. In ordered choice response models, what matters is statistical significance of the regression coefficients and their expected signs. Goodness of fit is of secondary importance (Gujarati, 2003).

The LRs at 190.17 (p value = .000) and 165.81 (p value = .000), for both the conventional banks regressions reported in Table 5, indicate that we have a good fit. As the p value is less than .01 (significant at less than 1%) the null hypothesis that all slope coefficients are simultaneously equal to zero gets strongly rejected, indicating that behavior of ratings is well explained by the selected variables.

Three variables are statistically significant in the pre-GFC regression that is based on 2002–2007 data: NIM, COST, and log of TA. Log of TA has a positive impact on ratings, whereas COST and NIM have a negative impact. All these three variables are significant at 1% level, indicating a strong linkage to Fitch ratings.

In the post-GFC regressions, which are based on 2008–2013 data, three variables are statistically significant: COST, log of TA, and liquidity as measured by liquid assets to customer and short-term deposits (LIQ). TA has a strong positive coefficient, whereas COST has a strong negative linkage to Fitch ratings (significant at 1% level). Liquidity is positively linked to ratings and is significant at 5% level. Previous studies based on banking systems in developed countries (Berger & Bouwman, 2008; Cetorelli & Goldberg, 2011) have also pointed to the importance of liquidity during a crisis for an individual bank to remain stable and strong.

The TA variable is a significant factor in determining ratings both in the pre- and post-GFC regressions. This implies that both before and after the financial crisis, size is an important variable in Fitch ratings. This fact is also borne out by raw data that clearly show that bigger banks have better Fitch ratings both before and after the financial crisis. Whereas Fitch ratings of some banks improved after the financial crisis, some banks were down rated by Fitch after the financial crisis. A good example is Emirates NBD, the biggest bank in our sample, which had a rating of A+ in 2006 before the GFC and was downgraded by Fitch to AA– by 2009, that is after the crisis. On the contrary, Samba Financial Group was upgraded by Fitch from A before the crisis to A+ after the crisis. The raw data clearly indicate that size is an important factor in ratings and rankings by credit rating agencies. This fact is also borne out by the quartile values reported in this article in Table 3. Banks in the top quartile exhibited a quartile average of US$23,574 million in postcrisis period and US$20,149 million in precrisis period as compared with the lowest quartile averages, which were US$3,238 million and US$2,027 million in post- and precrisis years, respectively. Both the regression results and the quartile data show that size is an important determinant of ratings. The logic could be that size indicates stability and also that size indicates the importance of the bank in the banking system of that country. There is a strong case for arguing that regulatory agencies and governments in any country will not allow the biggest banks in the country to fail because of a financial crisis. The increase in size of the banks from pre-GFC to post-GFC implies that the big GCC banks adopted well thought-out growth strategies despite the ongoing financial crisis.

A result that is unique to this study is the importance of cost management for a typical GCC bank to remain highly rated. The coefficient of the COST is negative and is statistically significant in both the pre- and postcrisis regressions. The major items of cost for a bank are staff expenses, administrative expenses, and technology costs. A high COST could lead to lower operating profit, and net profit, thus leading to a downgrade in the rating of a bank. The negative sign, along with the fact that the variable is statistically significant in both the regressions, implies that banks with higher COST have lower ratings. The international benchmark for bank COST is 50% according to Ernst and Young (2010). COSTs of banks operating in GCC countries are low compared with the benchmark both in the precrisis and postcrisis periods (see Table 4). Ordered choice regressions results reported in Table 5 indicate that a bank can improve its rating by controlling costs.

NIM is a proxy for risk management practices of banks. The higher the risk embedded in the loan (or asset) portfolio of a bank, the higher the NIM will be. Higher risk results in a lower rating of a bank. Whereas NIM is negative and statistically significant in the precrisis regression, in the postcrisis regression it is not a statistically significant variable in explaining differences between ratings of banks. A possible explanation could be compression of differences in interest margins among banks. After the GFC, GCC banks in general have become more risk averse, resulting in a situation where even those banks that used to give risky loans in the past have stopped doing so. Therefore, differences in interest margins no longer contribute to differences in ratings.

In the post-GFC regression, liquidity comes through as a significant variable. The immediate problem for banks in the GFC period was the lack of liquidity, which can have an immediate negative impact on a bank’s ability to function. Table 6 shows that mean liquidity levels (LIQ) fell from 35% in the pre-GFC period to 22% in the post-GFC period. Agencies such as Fitch seem to have focused more on the availability (or lack) of liquidity in giving rating for a bank. Our regressions clearly indicate a change in focus of rating agencies toward liquidity and its importance. A number of GCC banks, especially in the Dubai region, suffered from severe lack of liquidity during the crisis years and had to depend on central bank intervention for a bail out. It is also a fact that during the financial crisis, central banks in the region took extra care to ensure sufficient liquidity in the banks.

Descriptive Statistics.

Note. GFC = global financial crisis; CAP = total capital ratio; NIM = net interest margin; ROA = return on asset; ROE = return on equity; COST = cost to income ratio; LLGL = loan loss reserves to gross loans; LIQ = liquid assets to demand deposits; TA = total assets.

Islamic Bank Regressions

Table 7 shows the estimation results using Fitch post-GFC ratings. As mentioned earlier, Fitch ratings for very few Islamic banks are available for the pre-GFC period and therefore regressions was not attempted. LR at 61.79 (p < .01) indicates a good fit. In the Islamic bank regressions, NIM variable is not used as concept of interest itself is not applicable. Instead, the ROE variable is included. Log of TA and CAP are the two variables that are significant. As expected, there is a strong positive link between TA and Fitch ratings. The mean value of Fitch ratings of Islamic banks (8.77) is higher than that of conventional banks (8.65). However, the difference is marginal, and therefore does not really support the conclusions drawn by some studies that if all banks were Islamic, financial crises would be less likely because they have built-in stabilizers that lower the probability of crises (Ahmed et al., 2014).

Islamic Banks.

Note. Ordered choice logit regression results. Method: Maximum likelihood (Brendt, Hall, Hall, and Hausman [BHHH] algorithm) with robust (Huber/White heteroscedasticity consistent) standard errors. GFC = global financial crisis; COST = cost to income ratio; TA = total assets; CAP = total capital ratio; EQTA = equity to total assets; LIQ = liquid assets to demand deposits; LLGL = loan loss reserves to gross loans; ROE = return on equity; ROA = return on asset; AIC = Akaike information criterion; LR = likelihood ratio.

p < .01 (significant at 1% level). **p < .05 (significant at 5% level).

Reading the results of the conventional bank regressions and the Islamic bank regressions together, it is obvious that size is the key variable considered by rating agencies in arriving at ratings. The bigger the bank, the more stable it is expected to be. CAP has a strong negative linkage to rating. CAPs of Islamic banks are higher than those of conventional banks and are well above the regulatory requirements. As mentioned in the section on ratio analysis, top banks reduced the level of capitalization with the onset of crisis. The strategy of highly rated banks, conventional and Islamic, seems to be that, as long as capital is higher than the regulatory requirements, allow capital ratios to trend down while continuing to operate effectively during the crisis period.

Conclusion and Policy Implications

This article started by ranking 40 conventional banks and 11 Islamic banks in the GCC countries using Fitch ratings. The study uses data from 2002 to 2013, which are divided into pre-GFC (2002–2007) and post-GFC (2008–2013) periods. Eight dimensions were used to analyze the behavior of the bank before and after the GFC. Analysis using median and quartile values indicates that variables important for achieving good rating are higher TA, good capital ratios, higher ROA, and ROE.

Ordered choice logit regressions using Fitch ratings were done for both the periods before and after the GFC. Regression results indicate that size (as measured by TA) is a very important factor in ratings both before and after the financial crisis. Another conclusion drawn from the results is that good cost management by keeping tight control over COST is important for a bank to improve its rating. Furthermore, high NIMs lead to lower rating. To the extent that higher NIMs proxy for higher risk levels, this result is expected. A lower level of risk as indicated by lower NIMs is an important factor in achieving good ratings. Higher levels of liquidity are extremely important for a bank during a financial crisis and this fact is strongly brought out by the post-GFC regressions. As long as asset quality (as measured by NPA ratio) is under control, liquidity seems to be the focal point in achieving good ratings. Top-rated Islamic banks seem to be following a strategy of allowing capital ratios to trend down during a crisis, as long as capital is well above the regulatory requirements. A key conclusion of the article is that risk, liquidity, and cost management practices of banks are of critical importance during a period of financial crisis. While during normal times liquidity is given only passing importance, poor liquidity management invariably leads to problems, especially when the economies are passing through a crisis. A combination of circumstances such as poor liquidity and poor credit risk control, combined with a series of external economic shocks (such as the COVID-19 pandemic and low oil prices), could push a bank toward bankruptcy.

The study is unique to the extent that it focuses on banks in GCC countries. But the study can be expanded by including banks in the Middle East and North Africa (MENA) region and by taking credit ratings given by other rating agencies. This would strengthen the policy implications suggested above.

Footnotes

Appendix

Classification of banks into conventional (commercial) banks and Islamic banks is as given by BankScope database (now renamed as Orbis Bank Focus). Al Rajhi Bank and Tamweel PJSC are classified as commercial banks by BankScope in the Pre-GFC period and as Islamic banks in the Post-GFC period. In addition, Tamweel public joint-stock company (PJSC) is classified as a bank by BankScope.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.