Abstract

How does the economy of China and Japan interact with each other? Through building vector autoregression (VAR) model, this study examines the transmission mechanism of economic synchronization among the two nations from three perspectives, namely foreign direct investment (FDI), bilateral trade, and political relation. Based on this, relevant stabilizing measures for China’s economy are proposed. The findings of this study are as follows: (a) There exists business cycle co-movement between China and Japan. (b) The transmission mechanism of this co-movement contains bilateral trade and FDI. Therein, import contributes the most to China’s economic fluctuation, which is followed by FDI and export. (c) Bilateral political relation exerts indirect influence on China-Japan economic synchronization. (d) The impact of Japan’s economic fluctuations on the economy of China would be mitigated by expanding international trade markets, reducing financial market access restrictions, strengthening the political mutual trust, and encouraging communications between China and Japan in science, technology, and education, etc.

Keywords

Introduction

Since the 2008 financial crisis and the 2010 European debt crisis, the global economic downturn had ensued until 2017. According to the International Monetary Fund (IMF), China contributed to 31.73% of the increase in the world economic growth between 2013 and 2016, and has become the main driving force for global economic development (Yu, 2018). Since the continuingly spectacular economic growth, China has become the world’s second-largest economy in 2009, only after the United States, and produced 8.6% of global gross domestic product (GDP; Lin, 2011). In 2017 and 2018, its GDP accounted for 15% and 15.5% of the global GDP, respectively. As one of the fast-growing emerging economies, China plays an important role in the global economic recovery and development. Therefore, maintaining its economic stability is of great significance.

With the deepening and broadening of global integration, the economic co-movement across nations is growing. China may experience an increasing number of economic shocks caused by other countries, which may result in domestic economic instability. Consequently, while obtaining the benefits brought about by globalization, China also needs to withstand and reduce the negative effects from foreign economic fluctuations to maintain national economic stability. International business cycle theory focuses on the economic fluctuation across countries, which may stem from various factors, such as internal demand shock of specific countries or globally common shocks (Bagliano & Morana, 2010), and its impact on each economy (Backus et al., 1993). This theory indicates that the main determinants of international economic co-movement are economic interdependence among countries, which mainly results from bilateral trade and foreign direct investment (FDI; Barrell & Pain, 1997; Surugiu & Surugiu, 2015).

Regarding bilateral trade, Frankel and Rose (1998) indicated close trade ties would transmit the demand shocks or spillover effect from one country to another. Hence, the closer trade integration is relative to the stronger business cycle co-movement. This standpoint was proved by Juvenal and Monteiro (2017). They stated that bilateral trade linkage was highly correlated with the economic synchronization among 21 Organisation for Economic Co-operation and Development (OECD) countries. In the aspect of FDI, Hsu et al (2011) have summarized its potential channels affecting business cycle synchronization. First, provided that the foreign firm introduces new technologies, the domestic firm will benefit from its spillover and diffusion. Second, the stagnant economic environment in the foreign enterprise’s nation will deteriorate its financial situation. Hence, the foreign firm may curtail the future investment, salary, and other inputs of the domestic companies, which result in the international rent sharing and the transmission of economic disturbance among multiple countries. Third, under the situation of capital mobility between countries, the saving and investing policy change in foreign country will have significant impacts on the availability and price of financial assets, which will strengthen the business cycle synchronization. Fourth, in an outward FDI position, undesirable economic condition in foreign country will decrease the benefit and value of the domestic investing enterprise via financial statement and capital market. Many studies have validated the link between FDI and multinational economic synchronization. Imbs (2004) affirmed that the stronger economic synchronization emerges within the regions with more solid financial link, which is also concluded by Hsu et al. (2011) and Jos Jansen and Stokman (2014).

In addition to the bilateral trade and FDI, bilateral political relation is newly considered factor of international business cycle synchronization. From the theoretical perspective, huge amount of FDI and bilateral trade will alleviate international political conflicts and improve bilateral political relation (Jie & Shunhong, 2009; Jinjarak, 2009; H. Lee & Mitchell, 2012). In turn, bilateral political relation will also have impact on the bilateral trade and mutual direct investment, which will indirectly affect the economy of both countries simultaneously according to the international business cycle theory (Azam et al., 2012; Pan & Jin, 2015; C. J. Zhao, 2018). In summary, bilateral trade and FDI are the direct determinants of the economic co-movement across countries, and the bilateral political relation is the indirect one.

Japan is one of the closest trading partner countries for China. In recent decades, these two countries have increasing trade intensity and financial ties. China-Japan economic interdependence has emerged and grew substantially (Alvstam et al., 2009). In 2018, China was the largest trade partner of Japan, and Japan was the third largest trade partner for China. In addition, as the largest investor for China, the FDI from Japan in 2018 stood at US$3.80 billion, which accounted for 2.8% of the total FDI in China. Similarly, China’s FDI outflows to Japan are significantly increasing since 2003 (H. Liu & Hou, 2017). In 2017, China’s investment to Japan arrived at US$1.0 billion, which is a new record high.

According to the international business cycle theory and the determining factors for the economic synchronization across countries, it is not difficult to infer that output synchronization may exist between Japan and China (Berdiev & Chang, 2015; T. Wu & Pan, 2014). Therefore, many scholars have paid huge attention on this issue. Generally, based on the relevant theories and empirical research results, prior studies attempted to detect the China-Japan business cycle co-movement mainly from two transmission channels, namely bilateral trade and FDI.

In the aspect of bilateral trade, some studies hold the viewpoint that trade is the major factor for business cycle correlation. For instance, by constructing linear regression model, Choe (2001) studied the effect of trade interdependence on the business cycle of 10 East Asia countries, including China and Japan. It presented that there existed synchronization of economic fluctuations within the countries while the trade interdependence among them is strengthened. Similar conclusions are also presented by Rana (2007) and Allegret and Essaadi (2011); they both studied the countries in East Asia, and argued that enhancing bilateral trade would accelerate the business cycle co-movement. Baxter and Kouparitsas (2005) utilized the extreme bounds analysis to research on the economic co-movement over 100 countries. They claimed that robust correlation existed between bilateral trade and output synchronization. Ning and Ye (2012) examined the impact of bilateral trade between China and Japan on the synchronization of their economic fluctuations with the generalized autoregressive conditional heteroskedasticity (GARCH) model and proved the trade association was the major channel of China-Japan economic co-movement.

In addition to above static analysis, the dynamic between trade and China-Japan business cycle correlation is also examined. He and Liao (2012) investigated the dynamic among the business cycle co-movement of Asian and G-7 economies, which contained China and Japan, by applying the factor model. The results indicated that trade fostered the business cycle co-movement among Asian economies. The similar result is also attained by G. H. Lee and Azali (2010) through the generalized method of moments (GMM) method.

It can be seen that all the above papers believed the positive association of bilateral trade to China-Japan economic synchronization. However, several studies held the opposite standpoint and they argued that the effects of trade might be overvalued. Kumakura (2006) indicated that trade did not serve as the key determinant of business cycle co-movement among 13 Asia-Pacific countries incorporating Japan and China, through using correlation analysis. Shin and Wang (2003) studied the relation of trade integration to business cycle synchronization among 12 Asian economies. The conclusions implied that trade volume increase would not result in fostering output co-movement. Rana et al. (2012) further stated that intraindustry trade growth was the main force of synchronizing business cycle rather than the interindustry trade. By establishing the regression model, Crosby (2003) even argued that there is no correlation between trade intensity and output synchronization in Asian-Pacific area. Hence, the impact of trade linkage on China-Japan economic co-movement still remains ambiguous.

It can be seen that huge attention has been paid on the relation of trade to China-Japan business cycle co-movement. However, to our best knowledge, only several studies focused on the impact of FDI on business cycle symmetry between China and Japan. Wang (2010) discovered the existence of economic interdependence between China and Japan from two perspectives, that is, bilateral trade and FDI, which are measured by the proportion of traded goods and FDI flow. Zhang and Akgmetova (2018) proved that international trade and FDI were the driving factors of synchronized economic fluctuations among China, Japan, South Korea, and Association of Southeast Asian Nations through building the linear regression model. Therein, the FDI flow was applied to represent the FDI indicator. Dynamic analysis in regard to FDI is also executed by existing studies. Lee and Azali (2010) applied the GMM with dynamic panel data to ascertain the positive dynamic association of bilateral trade and financial link to the symmetry business cycle among East Asian economies. In contrast, some scholars disagreed with the positive linkage between FDI and China-Japan business cycle synchronization. Based on interdependence theory, Gong and Kim (2013) examined the impacts of financial integration and trade intensity on the business cycle synchronization in Asia. The results implied that trade intensity was one of the major sources of tightening economic co-movement. Nevertheless, the financial integration had negative effect on the economic synchronization.

Generally, previous studies provide meaningful and valuable reference in this research area, whereas some shortcomings still exist. It can be seen from the aforementioned literature that although many of them have examined the effect of bilateral trade, the conclusions do not reach an agreement. Also, the impact of FDI is rarely investigated. What is more, the several existed related studies have drawn opposite conclusions. Third, few prior studies detected the dynamic between transmission paths and China-Japan business cycle linkage, therein the dynamic investigation about the role of FDI was even fewer. Fourth, all the papers that examined the effect of FDI applied the FDI flow as the independent variable. However, because FDI flow only represents the foreign investment inflow in 1-year period, it is incapable of reflecting the actual available investments which is directly associated with the economic development. This drawback can be solved by applying FDI stock because it is the indicator which reflects how foreign capital affects domestic economic growth, and represents the productive capacity of the host countries (Yang & Yuan, 2009). In addition, to our best knowledge, all the prior studies ignore the function of bilateral political relation, which may have indirect impacts on the economy of the two countries simultaneously through significantly affecting trade and investment among countries. Last but not least, previous studies rarely focused on the stabilizing measures for China’s economy to mitigate the negative impacts caused by Japan’s economic shock.

Given that, the main aims of the current work can be summarized as follows: This study considers FDI stock, bilateral trade, GDP of China and Japan as well as bilateral political relation as the variables to detect the economic synchronization between China and Japan, and investigate its underlying driving forces from the aspect of bilateral trade, direct investment, and bilateral political ties. To fulfill this research aims, the vector autoregression (VAR) model, generalized impulse response function (GIRF), and variance decomposition are employed to examine the dynamic economic correlation of the two countries and the dynamic effect of bilateral trade, FDI, and bilateral political relation on the economic co-movement. On this basis, to propose the stabilizing measures which benefit to reduce the economic fluctuation of China, relevant index and historical data analysis regarding trade and FDI are applied. The research framework is presented as below:

The rest of the article is organized as follows. Section “The China-Japan Bilateral Political Relation” contains the calculation of the China-Japan bilateral political relation index (BPRI) and related analysis. Section “Methodology and Data Source” presents the data source and relevant methodologies. Section “Results and Discussion” puts forward the results and discussion. Conclusions are given in section “Conclusion”.

The China-Japan Bilateral Political Relation

The impact of China-Japan bilateral political relation on their economy is significant. Xu and Chen (2014) reported that the potential loss of China’s export to Japan was about US$31.3–US$31.8 billion in 2012, for which root cause was the bilateral political relation between China and Japan worsened. Combined with the discussion regarding the effects of bilateral political association on economic synchronization (see section “Introduction”), in this study, the bilateral political relation is considered as the indirect factor which influences the economy of both countries.

There are some methods to quantify the bilateral political relation. Therein, United Nations voting data are a popular way (Bailey et al., 2017). However, this method is always applied to measure the political relation among huge number of countries. Moreover, the main shortcoming of this means is the hypothesis that voting is related to the similar preference of the countries. In detail, providing that a group of countries votes repeatedly on a disputed issue, the divergence between these countries is magnified with the voting times increasing. This will distort the accuracy of international political relation measurement. Another extensively used path is the event weighting based on the bilateral political events. This method allows to measure the bilateral diplomatic relation from diverse dimensions and avoid biased evaluation. Moreover, given the importance and severity of the events, different weights are assigned to the events and then a comprehensive political relation index is obtained. Also, it can be applied to small-scale measurement. Therefore, the event weighting method is employed in the study.

According to J. H. Zhang et al. (2011), J. H. Zhang and Jiang (2012), the BPRI is established based on four indicators: (a) the number of state visits between China and Japan, which contains the important state leader visits (such as the premier, vice president, and president) and other state leader visit. To embody different significance of these visits, the corresponding weights are set as 2 and 1, respectively; (b) bilateral conflicts, which is divided into two categories, namely intensified ones and general ones. The according weights are designated as −2 and −1, respectively; (c) official activities and amicable negotiation; and (d) the growth rate of sister cities. The weights of the last two proxies are both one. The relevant information is from the official website of Ministry of Foreign Affairs in China and People’s Daily online. Due to the data accessibility, the study period is from 1983 to 2018. Hence, based on the event weighting method, the China-Japan BPRI and the value of four components during 1983–2018 are reported in Figure 2.

The left section of Figure 2 depicts the value of four indicators, and the results of BPRI are shown in the right section. Regarding the China-Japan BPRI in the period of 1983–2018, it can be seen that some fluctuations emerge according to the relevant results, which indicates that the bilateral political relation between China and Japan varies frequently from relative intensity to amicability. The root cause of this frequent variation, according to the left section of Figure 2, is the important state leader visit and bilateral conflict due to the large proportions of these two elements. Also, the pattern of BPRI is basically in line with the reality. In particular, as shown in Figure 2, the BPRI positioned highly during 2006–2011 and soared in 2007–2008. According to the official media comments, during 2006–2011, China-Japan bilateral relation reached a new level. Especially in 2007 and 2008, these years are named as “spring-heralding year” and “warm-spring year” by the China’s social media. During this period, the mutual visit, official activities, and negotiation increased significantly. In contrast, the comparatively tense bilateral relation emerged in 1996, 2013, and 2016. This is mainly caused by the bilateral dispute upgrade, which is induced by the issues left over by history, and shrinkage in the number of important state leader visit. In detail, the primary conflicts of the specific years involve visiting the Yasukuni war shrine by the Japanese prime minister, the Diaoyu Islands, and South China Sea disputes. As can be seen from the left section of Figure 2, the mutual political visit declined of the two countries with the conflicts sharpening, and vice versa. Therefore, in essence, the two main factors, namely important state leader visit and bilateral conflict, are mutually influence, which will further deteriorate or develop the relationship between China and Japan.

The research framework.

China-Japan bilateral political relation index.

Methodology and Data Source

The main aim of this study is to discover the dynamic pattern in China-Japan economic synchronization, and then investigate and analyze the corresponding transmission mechanisms. On this basis, the related stabilizing measures are proposed to mitigate the effects of economic fluctuation from Japan on China’s economy, which may contribute to the steady economic development in China. To achieve these study goals, with respect to the exploration of the transmission mechanisms of China-Japan economic synchronization, referring to the previous studies, it will start from the investigation of effects of bilateral trade, FDI, and bilateral political relation through the VAR model and relevant methods. On this basis, taking the linking factors of economic linkage between China and Japan as the cutting points, the index analysis and historical data analysis are utilized to detect the stabilizing pathways for China’s economy to prevent from the negative impacts caused by Japanese economic shock.

Exploration of Transmission Mechanism of China-Japan Economic Co-Movement

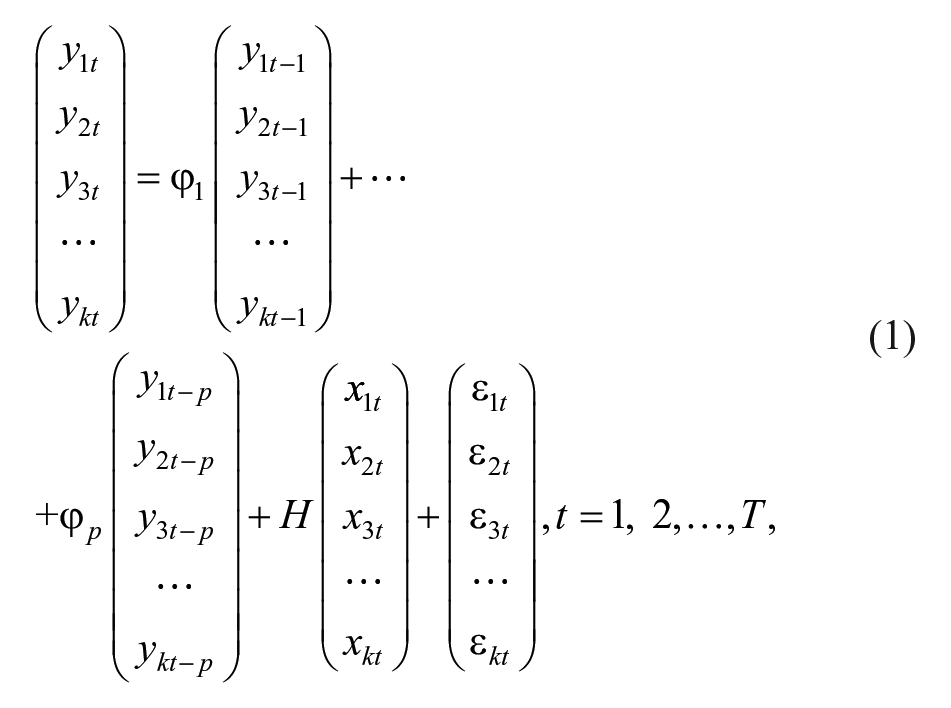

To probe the economic transmission pathways between China and Japan, the VAR model is employed because it is able to capture the linear interdependencies among multiple time series and allows for interaction between the variables under consideration (Hatemi-j, 2003). According to Sims (1980), the VAR model can be written as follows:

where ykt means the endogenous variables, which are k-dimensional column vectors; xkt indicates the exogenous variables which are k-dimensional column vectors; p represents the lag order; and t denotes time.

Moreover, to examine the dynamic economic relation between China and Japan and uncover the related transmission channels, the GIRF and variance decomposition based on the VAR model are employed. The former can be applied to investigate the response of one specific endogenous variable to other variables’ shocks. The latter is used to obtain the corresponding contributions of other variables to the response (B. Zhao & Yang, 2020).

One premise of building the VAR model is the stationary properties of the endogenous variables. Moreover, impulse response and variance decomposition requires all the variables are stationary and integrated of the same order (Pradhan, 2009), which can be tested by the unit root test. In this study, the popular Augmented Dickey–Fuller (ADF) test is employed. The results of the unit root tests also lay the sound foundation for the cointegration test, which is used to investigate the long-term relationship among variables in this work. Another necessary precondition of building the VAR model is to determine the lag length of endogenous variables. The related results are attained with the widely used criteria including Akaike information criterion (AIC), Schwarz Criterion (SC), and Hannan–Quinn Information Criterion (HQ). Hence, the testing process starts from the unit root test, which is followed by the cointegration test, lag order selection, VAR model determination, GIRF, and variance decomposition analysis.

On the basis of previous works, this study assumes that the main factors affecting the economic co-movement across countries are bilateral trade, FDI, and bilateral political relation. Therefore, to study on the business cycle synchronization between China and Japan and its transmission mechanism, the variables in the VAR model include the GDP of China (CGDP), GDP of Japan (JGDP), China’s export to Japan (CEX), Japan’s export to China (JEX), Japan’s FDI to China (FDI; simplified as “FDI” in the following contents), and political index (Pt).

It should be noted that instead of the FDI flow, the FDI stock is applied in this study based on the study aims. Hence, in the light of the prior studies, as a transmitting channel, the indicator represented FDI should be relative to the domestic economic situations. From a theoretical perspective, the FDI flow measures the capital that enters to a country in the current year, while FDI stock reports the information regarding the foreign capital accumulation or productive capacity that is available to contribute to the domestic economic development (Kornecki & Raghavan, 2011). Some studies have reached consensus in this standpoint, such as Kornecki and Raghavan (2011), Popescu (2014). Therefore, FDI stock serves as the foreign investment inflow proxy. According to Yang and Yuan (2009), the FDI stock is measured by the equation as follows:

where FDI represents the China’s FDI stock from Japan, I stands for new investments, that is, the FDI flow, PFDI indicates the price indices of investment in fixed assets, t means time, and δ represents depreciation rate which is set as 7.5% because it meets the requirement regarding the average service life of fixed assets in China (Yang & Yuan, 2009).

To eliminate the effect of heteroskedasticity, this study takes the logarithmic term of the variables except for Pt. The variable definitions are presented in Table 1.

Variable Definitions.

Note. FDI = foreign direct investment; GDP = gross domestic product.

Hence, the basic VAR model in this study can be described as follows:

where p will be determined by the lag length test, the results of which will be specified in section “Results and Discussion.”

Detection of Stabilizing Measures for China’s Economy

Referring to the previous works, the economic linkage between China and Japan is majorly derived from the bilateral trade, FDI, and bilateral political relation. Moreover, owing to the vital role of China in world economy, maintaining China’s economic stability is of great significance. Hence, probing stabilizing pathways for China’s economy to enable it to avoid the passive effects from Japan’s economic upheaval is crucial. This is examined from the three root causes of multinational economic linkage, that is, bilateral trade, FDI, and bilateral political relation. To fulfill this target, the index analysis and historical data analysis are utilized, which are widely utilized in prior studies (Calderon et al., 2007; Elmorsy, 2015; Fertö & Hubbard, 2003; Rasoulinezhad & Saboori, 2018; Y. Wu & Zhou, 2006). Therein, the former is used to reveal the bilateral trade pattern and features between China and Japan, which benefits to discover the competitive industries and the weak industries in China, thus building some solutions to improve the industrial performance and decreasing the product dependence on Japan. The latter is applied to analyze the characteristics of FDI, which is conductive to unveil the core industries in China that acquired more investment from Japan. Furthermore, through the industrial strength analysis, the complementary policies will be proposed to stimulate the industrial stable development in China.

Regarding the index analysis of bilateral trade, five indices have been introduced. They are the trade intensity index (TII), HM index (HM), the revealed comparative advantage (RCA) index, trade complementarity index, and comprehensive trade complementarity index, which will be detailed as follows.

Trade intensity index (TII). TII reflects the relative importance in trade between countries. TII can be further divided into two subtype indexes, that is, Export Intensity Index (EII) and Import Intensity Index (III). EIIij and IIIij denote the ratio of the proportion of country i’s trade with country j relative to the proportion of world trade destined for country j. EIIij > 1 or IIIij > 1 indicates that the trade flows between the two countries are larger than the expected, which represents the close trade relation between the two countries in export or import. EIIij and IIIij can be calculated as follows:

where

HM index (HM). It measures the interdependence between two countries in trade. For country i, higher HMij stands for greater trading dependence on country j. It can be described as follows:

The variable definitions of HMij are consistency with those of TII.

The revealed comparative advantage (RCA) index. This index is used to measure the competitiveness of industry k in country i. It can be presented by

where

To uncover the comparative advantage regarding various products of China and Japan, this study classifies all the trade commodities into 10 categories based on the SITC Rev.3, namely Standard International Trade Classification. It is the standard classification method for international trade goods. SITC Rev.3 refers to the third revised edition of SITC. The classification results of goods are shown in Table 2.

SITC Rev.3 Classification.

Note. SITC 9 contains the commodities and transactions not classified elsewhere, which are not analyzed in this study. SITC = Standard International Trade Classification.

On this basis, the RCA of each product category has been calculated. Hence, the industry-specific comparative strengths and weakness will be discovered, which lays the foundation of formulating relevant policies or paths to improve the product competitiveness and achieve the balanced development over China’s industries.

4. Trade complementarity index

where

where

With respect to the historical data analysis for FDI, to implement detailed analysis, the industries in China have been classified into two major categories, namely manufacturing and nonmanufacturing industries. Therein, the latter one contains eight types of sectors, which are the agriculture sector, architecture sector, transportation sector, telecommunication sector, wholesale and retail trade sector, finance and insurance sector, real estate sector, and service sector. On the basis, according to relevant FDI data, the sector-specific pattern and features of Japan’s FDI to China are analyzed.Furthermore, the policy suggestions for stabilizing and augmenting China’s industrial performance and development have been proposed. In the same spirit, the research in terms of bilateral political relation between China and Japan is executed via the historical trend analysis, which has been discussed in section “The China-Japan Bilateral Political Relation.” Thus, this section only details the analysis of FDI.

In addition, because the earliest bilateral trade data of China are from 1992, relevant data cover 1992–2018 and they are acquired from the UN Comtrade.

Results and Discussion

With regard to the research of driving forces of China-Japan economic synchronization, VAR model is employed. As stated in the preceding section, the unit root test results are the precondition of executing cointegration test and constructing VAR model. Moreover, based on the VAR model, GIRF and variance decomposition are applied to reveal the dynamic of economic fluctuation synchronization and related transmission channels between China and Japan. The related test results are presented in this section.

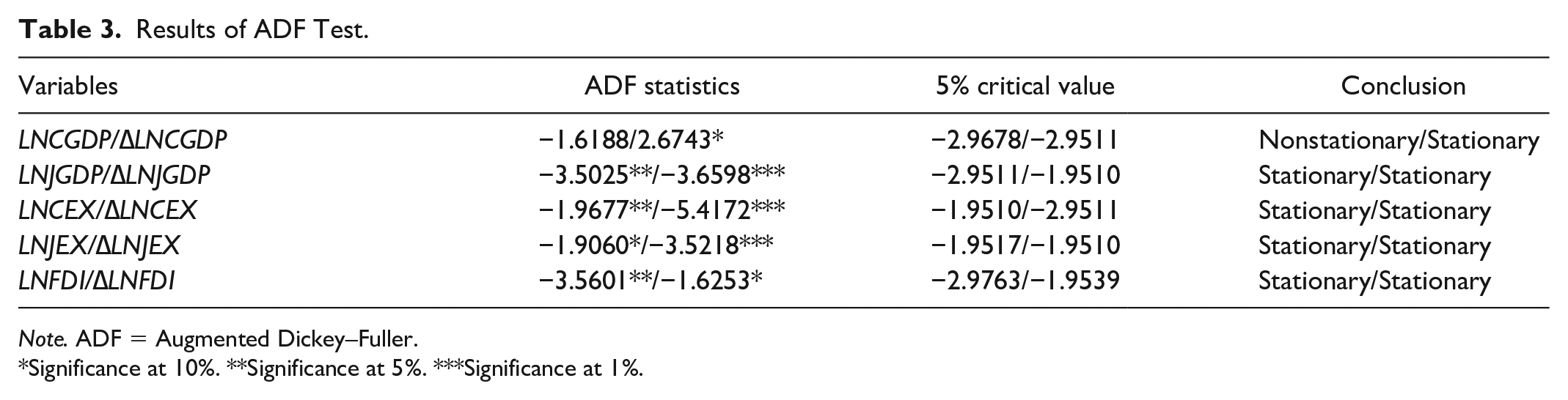

The first step is to determine the stationarity of the variables through ADF test, which is a popular unit root testing method. The related results are reported in Table 3. It can be seen from Table 3 that only LNCGDP is nonstationary at its level, whereas each variable is integrated of Order 1, that is, I(1).

Results of ADF Test.

Note. ADF = Augmented Dickey–Fuller.

Significance at 10%. **Significance at 5%. ***Significance at 1%.

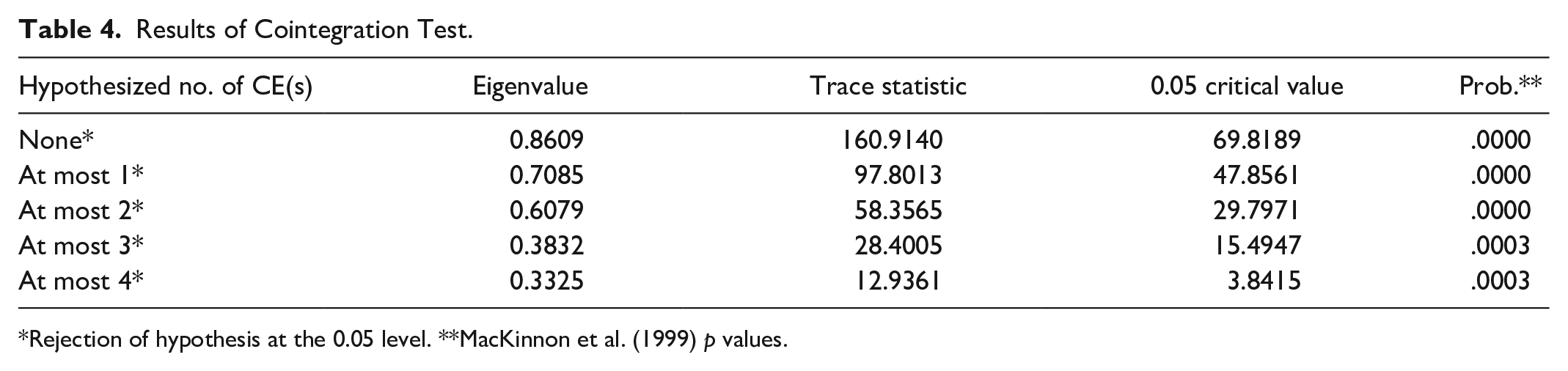

Because all the variables are I(1), the condition of implementing cointegration test is satisfied. The results of trace test and max-eigenvalue test are reported in Table 4, which confirm the existence of cointegration relationship among variables.

Results of Cointegration Test.

Rejection of hypothesis at the 0.05 level. **MacKinnon et al. (1999) p values.

As shown in Model (3), in VAR model, the endogenous variable can be represented by their lagged forms and the exogenous variables; thus, the lag order of endogenous variables should be determined. The results of six lag-order selection criteria are shown in the Table 5.

The Results of Lag-Order Selection Criteria.

Note. LR = sequential modified LR test statistic (each test at the 5% level); FPE = final prediction error; AIC = Akaike information criterion; SC = Schwarz Criterion; HQ = Hannan–Quinn Information Criterion.

The lagged order selected by the criterion.

It can be seen from Table 5 that the maximal lag length of VAR in this study is determined as 3. On the basis of the test results above, the VAR model is built, which applied LNCGDP, LNJGDP, LNCEX, LNJEX, and LNFDI as the endogenous variables, and Pt as the exogenous variable. Also, combined with the results of unit root test, the first different forms of the corresponding variables are utilized to ensure all the endogenous variables are stationary and meet the requirement of the VAR model. Therefore, the VAR model in this study is depicted as follows:

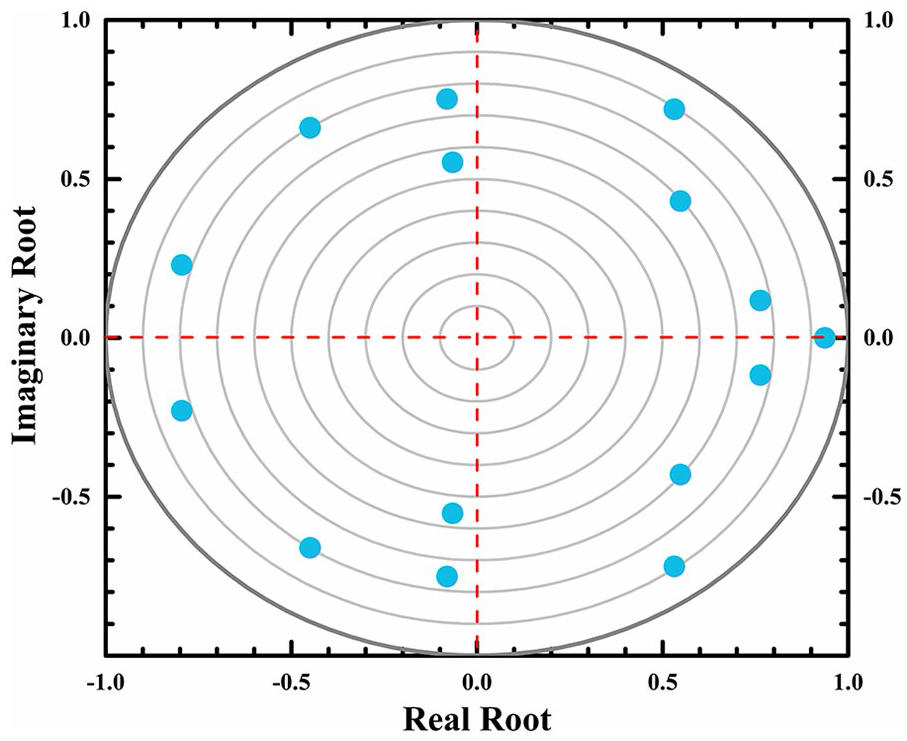

Before estimating Model (12), it is necessary to conduct stability test of VAR model to examine whether Model (12) is well-specified. Figure 3 shows that all the characteristic roots are less than 1 and lies inside the unit circle, which verifies the stability of Model (12).

VAR roots of characteristic polynomial.

Following determination of model stability and lag order, the GIRF and variance decomposition analysis are implemented to explore the dynamic in China-Japan economic synchronization, which is rarely investigated in previous works. Specifically, GIRF is applied to analyze the economic impacts of China and Japan when the endogenous variables have unexpected shocks. The main feature of GIRF is the responses are independent with the variable order; thus, the robustness and reliability of estimated results will be improved (Ewing et al., 2007). The related results of the GIRF results regarding the economic responses in China and Japan to the variables’ impulses are provided in Figures 4 and 5 accordingly. Moreover, the responses of endogenous variables to the one standard impulse of exogenous variable, namely Pt, are reported in Figure 6 to discover the potential influence of bilateral political relation on the economy of the two countries.

Responses of ∆LNCGDP to the variable shock.

Responses of ∆LNJGDP to the variable shock.

Responses of bilateral political relation shock.

As shown in Figure 4, in response of one positive shock of ∆LNJGDP, ∆LNCGDP increases initially and then declines. This fluctuation pattern repeats for several times and gradually tends to convergence. Similarly, as can be seen from Figure 5, when Japan’s economy undergoes one positive standard impulse, the response of economic situation in China is ascending followed by short-term decrease. This fluctuating type occurs for several times and then achieves stability. The resemblance in terms of economic response of one country to the economic impulse of the other implies the business cycle synchronization exists between China and Japan. This result is consistent with that of Wu and Pan (2014) and Berdiev and Chang (2015). They all claimed that business cycle synchronization emerged between China and Japan.

Moreover, integrating the contents in Figures 4 and 5, the shocks of ∆LNFDI, ∆LNCEX, and ∆LNJEX create similar influences on the two economies. Specifically, regarding the economic situations in China and Japan, the according changing patterns resulting from the ∆LNCEX, ∆LNJEX, and ∆LNFDI all start from negative initial impacts. Then, the impacts increase to the positive level, which is followed by the wave-like variation and gradual convergence. The similarity in the impacts of bilateral trade and FDI on the two countries’ economic situations further validates the China-Japan economic co-movement, and reveals that bilateral trade and foreign investment are the driving forces of this synchronization. The results are in line with some existing studies. Shin and Sohn (2006) examined the relation of bilateral trade to the business cycle synchronization in East Asia, through building linear regression models. They have found that trade benefits to create economic co-movement. The same results are also obtained by Abbott et al. (2008). Cheng and Cen (2010) demonstrated that FDI was closely relative to the economic co-movement between China and her trade partners including Japan, with ordinary least squares (OLS) estimator for panel data.

With respect to the effects of Pt impulse on the endogenous variables, namely ∆LNCGDP, ∆LNJGDP, ∆LNCEX, ∆LNJEX, and ∆LNFDI, the related results are depicted in Figure 6 accordingly. It can be seen from Figure 6 that the initial impacts of Pt on ∆LNCGDP, ∆LNCEX, ∆LNJEX, and ∆LNFDI are all positive, which indicates that the bilateral political improvement may promote the economic development in China, and stimulate bilateral trade and FDI. This is in agreement with the results of Wen and Jiang (2014) and Du (2015). They all argued that for China, political relation posed positive impacts on bilateral trade and FDI. Moreover, Kuang and Xiang (2017) indicated that China-Japan diplomatic relation deterioration would worsen the bilateral trade. It should be noted that in Figure 6, although the initial response of ∆LNJGDP presents negatively, it then soars immediately and reaches to the largest positive level. This implies that the significant lagged acceleration effect occurs between political relation augment and domestic economic growth in Japan. Overall, due to the positive impacts of political relation on the economy of the two countries, it is rational to improve the China-Japan diplomatic linkage not merely from the perspective of economic enhancement, but also from the perspective of coordinated development in multiple dimensions, such as trade and investment. This can be achieved through many ways, such as enhancing the communications in science, education, and other areas. In addition, except for the ∆LNJEX and ∆LNFDI, the positive influences of Pt increment on other variables are expected to last for several periods. However, the ∆LNJEX and ∆LNFDI are the most sensitive factors to the Pt variation because the correspondingly highest positive responses are achieved by them in period one. It implies that political relation transition may bring about lasting effects on China’s export to Japan and the two countries’ economy, but instantly strong short-run influence on the China’s import from Japan and FDI. Generally, the patterns in the impact of Pt on the ∆LNCGDP, ∆LNCEX, ∆LNJEX, and ∆LNFDI are alike; nevertheless, that on the ∆LNJGDP is different. The asymmetry regarding the effects on the economies indicates that political factor is not the direct determinant for China-Japan business cycle synchronization. However, combining with the GIRF results, China-Japan diplomatic relation exerts indirect impacts on the business cycle co-movement can be concluded, which is rarely investigated in prior studies.

Variance decomposition is applied to examine the impact magnitude to which the shocks of endogenous variables influence the China and Japan’s economy, namely ∆LNCGDP and ∆LNJGDP. The related results are shown in Figure 7.

The results of variance decomposition.

It can be seen from Figure 7 that 4.76%–8.60% of ∆LNCGDP fluctuation can be explained by ∆LNJGDP. Moreover, ∆LNCGDP contributes to 2.04%–14.25% variation in ∆LNJGDP. This result not only implies that Japan’s economy is more vulnerable to the economic fluctuation in China but also indicates the fact of mutually economic influence in the two countries, which supports the conclusion from the GIRF analysis, namely the existence of business cycle co-movement between China and Japan. In the aspect of ∆LNCEX, ∆LNJEX, and ∆LNFDI, they explain 0.65%–4.58%, 6.23%–38.70%, and 10.07%–14.48% of economic variation in China, respectively. For Japan, 1.07%–3.24%, 2.62%–32.44%, and 0.09%–3.61% of the economic fluctuation can be attributed to ∆LNCEX, ∆LNJEX, and ∆LNFDI shocks, respectively. This strengthens the results obtained in GIRF analysis that bilateral trade and FDI are the main factors for economic fluctuation synchronization in China and Japan. Also, the results imply that China’s economy is highly sensitive to the domestic import value from Japan. The sensitivity of FDI comes second and that of export value to Japan is in the last place. The strong impacts of import value may stem from the truth that import promotes the introduction of technologies, equipment, and raw material that is scarce in China; this benefits China’s economic growth (G. Y. Xu, 2007). Nevertheless, in regard to the contribution level of import and export to the economic variation in China, the opposite results are attained by some previous studies. Ma (2012), J. Chen and Dong (2012) claimed that the marginal impacts of export on economic growth in China were higher than those of import. This consequence may be valid but not be suitable for current stage of economic growth in China. In detail, as China has stepped into the “new normal” economic phase to pursue sustainable development, export restructuring has been implemented to achieve the relevant environmental goals such as energy intensity decrease and CO2 emissions reduction (Zhao & Yang, 2020). Hence, the export structure has varied from the food, textile, and minerals to advanced equipment and machinery. It has been proved that this restructuring is conductive to the economic growth in China but may lead to decline in export volume (Wu et al., 2019), which may be the reason of lower contribution of export to China’s economic fluctuation.

Undoubtedly, integrated with the transmission channels of China-Japan economic synchronization, it is crucial to further study on the features of the channels and then propose rational stabilizing measures for China’s economy to avoid the impacts of economic disturbance from Japan. The results above not only confirm the existence of China-Japan economic co-movement but also uncover the significant influences of bilateral trade and FDI from Japan, which can be concluded as the main factors of transmission mechanism in this economic co-movement. Moreover, China-Japan political linkage has been unveiled as the indirect driving force of the economic co-movement. Hence, the stabilizing measures for China’s economy should be explored through the three driving determinants, namely bilateral trade, FDI, and political relation. To attain this research target, index analysis and historical data analysis have been applied. Therein, the former is used to analyze the bilateral trade features, and the latter is applied to the rest of factors.

As stated in section “Methodology and Data Source,” five indices, that is, TII, HM, RCA,

The results of trade intensity index.

The results of HM index.

It can be seen from Figure 8 that the EII and III of the two countries during 1992–2018 are all greater than 1, which interprets that there exists more intense trade relation between China and Japan compared with their trading pattern with rest of the world. Through further comparison, EIIcj is less than EIIjc since 2005, which implies that after 2005, there exists stronger dependence in Japan on China’s exports than that in China on Japan’s exports. With respect to import intensity, IIIcj is larger than IIIjc since 2006. This indicates that the dependence of China on Japan’s imports is less than that of Japan on China’s imports, which further consolidates the conclusions in terms of EII. Simply put, it can be concluded that China has become one of the biggest importers for Japan. On the contrary, Japan is one of the biggest exporters for China. According to the natural trading partner theory that uncovers countries tend to trade more with neighbors and close proximate partners (Eicher et al., 2012), China and Japan are geographically close; hence, the trading linkage is stronger. Owing to the product superiorities in Japan, China has imported huge amounts of commodities or materials from Japan. However, by analyzing the changing pattern of IIIcj, it is found that an overall downturn trend emerges in this index value, which deduces that China’s importing intension from Japan is declining and this inference will also be verified with the HM index analysis presented below.

In terms of HM, it can be seen from Figure 9 that HMcj gradually declined while the HMjc increased. This denotes that the significance of China’s market to Japan is raising. However, the influence and importance of Japan’s market for China has gradually weakened. This phenomenon may be determined by the augment of product quality and product diversity, the advancement of producing technologies, and enormous market demand in China. Technological progress and commodity quality enhancement are conductive to improve the producing efficiency, meet the increasing demands timely, and enlarge the attraction of native goods; thus, the needs from Japan’s supply market will gradually shrink. In addition, the huge demand market in China contains inestimable business opportunities, which attaches great importance to China’s market and triggers its increasing significance for Japan. This will result in the decrease of China’s import demand from Japan, which is in line with the aforementioned inference regarding TII.

In addition, these conclusions regarding TII and HM also can be strengthened by the variance decomposition results. In Figure 7, it can be seen that ΔLNJEX is responsible for the largest driving force for economic fluctuation in China and Japan, which indicates the importance of Chinese market to Japan and huge effect of Chinese import from Japan. In contrast, the impact of ΔLNCEX on China’s economy is relatively low. It implies that Japan’s market attraction is weakening. Moreover, it also indicates that China has been out of the export reliance and the economic engine has achieved diversification.

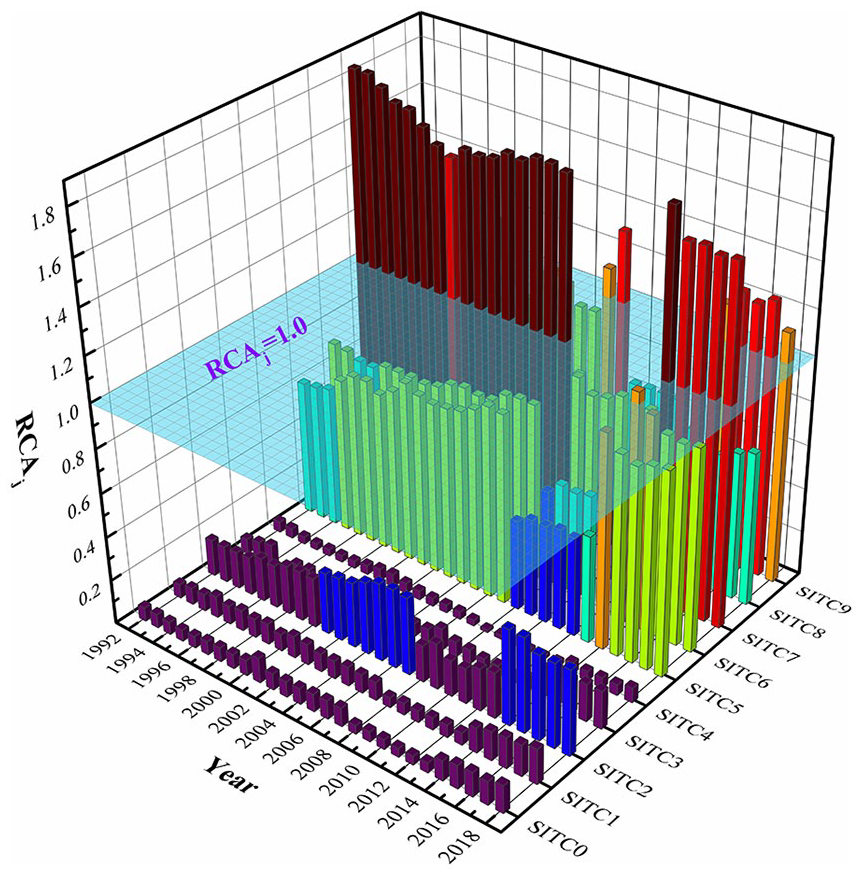

With regard to RCA, the relevant results of China and Japan in 1992–2018 of each commodity category (see Table 2), that is, RCAc and RCAj, respectively, are provided in Figures 10 and 11.

Revealed comparative advantage index of China.

Revealed comparative advantage index of Japan.

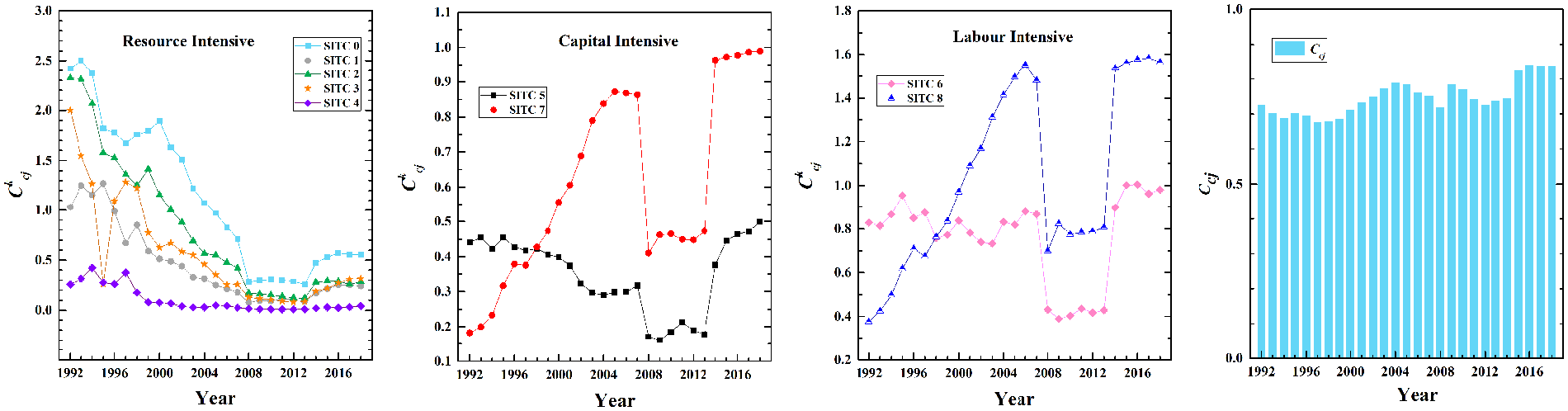

According to Figures 10 and 11, it is noted that both China and Japan are at a disadvantage in exporting resource-intensive products after 1994. RCAj of SITC5 and SITC7 is greater than the corresponding RCAc, which denotes there exists comparative advantage in Japan’s capital-intensive products. Moreover, the RCAc of SITC6 after 2013 are all within 1.25 and 2.5. Besides, RCAc of SITC8 before 2003 are all larger than 2.5. Even though some decline occurs, the index is exceeding 1.25 after 2013. This indicates the strong comparative advantage of labor-intensive industry in China. Through further comparing, the RCAc of SITC6 and SITC8 are all more than the corresponding RCAj, which implies that more strength exists in labor-intensive products in China than that in Japan. Therefore, to mitigate the dependence of capital-intensive goods in Japan, it is crucial for China to advance the relevant production technologies, and deepen industrial upgrade. Specifically, the resource and capital are supposed to be more inclined to manufacture of advanced equipment and chemical products.

Furthermore, combined with the TII and HM results, it can be found that importing demand from Japan in terms of capital-intensive products is enormous, which may be the main determinant that China has become Japan’s largest importer. Similarly, high dependence of China’s labor-intensive industry makes China become the biggest exporter for Japan because China has larger comparative advantage than Japan in this type of industry.

Regarding the trade complementarity,

Trade complementarity index of China.

Trade complementarity index of Japan.

It can be seen from Figures 12 and 13 that the trade complementarity of SITC6, SITC7, and SITC8 exported from China is high, and the trade complementarity of SITC2, SITC5, SITC6, and SITC7 exported from Japan reaches a high level. This is in line with the analysis regarding the RCA index, that is, China and Japan have advantages in labor- and capital-intensive goods, respectively. In terms of the comprehensive trade complementarity,

Apart from the index analysis for bilateral trade between China and Japan, the historical data analysis is used to reveal the pattern of another direct main force of China-Japan economic synchronization, that is, FDI, thereby providing some foundations of formulating some stabilizing measures for China’s economy. Japan is an important source of investment for China. All along, Japan’s direct investment in China has greatly promoted China’s economic growth and industrial restructuring (Li, 2014). Figure 14 illustrates the pattern of Japanese direct investment in China.

Pattern of Japan’s direct investment in China.

In general, Japan’s direct investment in China is manufacturing centered. Moreover, the largest share of nonmanufacturing investment is in wholesale and retail trade sector, which is followed by finance and insurance sector, real estate sector, and service sector successively. In comparison, the smallest proportion is acquired by the agriculture sector. The main reason for this phenomenon is that Japan valued China’s vast market space, which may bring substantial profits to Japan (Li, 2014). China focused on Japan’s core technology in machinery and equipment. To improve the technical level and promote the industrial structural upgrade in China, the supportive policies of introducing and purchasing Japan’s advanced technologies were formulated. Consequently, Japan invests heavily in China on machinery and equipment. This feature can also be consolidated in the GIRF and variance decomposition results. Specifically, integrated with the results of GIRF and variance decomposition, which denote that the impact of FDI on China’s economy is larger than that on Japan, it can be inferred that as the biggest beneficiary of FDI, manufacturing industries advance rapidly and their cooperation and linkage with Japan’s investors have deepened. In addition, manufacturing is the economic development pillar for China in the past decades. Thus, FDI may play a role in boosting economic growth in China. This may also be caused by the advanced producing technologies introduced to China alongside the investment.

Due to China’s market access restrictions, Japan’s investment in China is not high in the nonmanufacturing industries such as communications, finance, and service sectors. Hence, to mitigate the influence of Japan’s investment on China’s economy, it is imperative to attract the capital from other countries. Also, developing the production technologies of advanced machinery and equipment and implementing industrial upgrade is necessary.

Based on the above results of the trade index analysis, historical data analysis, and the conclusions regarding the impacts of China-Japan political relation on bilateral trade, FDI, and business cycle synchronization, this study proposes the following suggestions to alleviate the influences of Japan’s economic fluctuations on China’s economy from three perspectives, that is, bilateral trade, FDI from Japan, and bilateral political relation.

Bilateral trade. First, through increasing the R&D investment and deepening industrial upgrade, the development of China’s high-tech industries will be promoted, and then the technological gap with Japan will be narrowed, which will reduce dependence on Japanese capital-intensive products. Second, China’s economic openness should be further expanded to establish closer trade partnership with other countries and discover more potential international markets, which will reduce the negative impact on China’s economy due to excessive dependence on export to Japan.

FDI from Japan. First, the government should develop China’s economy, which will reduce China’s dependence on Japan’s capital. Second, the scope of financial cooperation between China and other countries should be broadened by relaxing financial market access restrictions and the foreign shareholding ratio restrictions (Yang et al., 2019).

Bilateral political relation. First, under the background of the “One Belt, One Road,” there is a broader space for the China-Japan cooperation development. Chinese and Japanese governments must strengthen political mutual trust, and further consolidate China-Japan relations. Second, the governments of China and Japan should actively promote the establishment of the China-Japan Free Trade Agreement, and the discussion about “One Belt, One Road” encourages exchange between the two countries in politics, economy, culture, science, and technology, which may benefit the long-term political stability for the two countries.

Conclusion

With the development of global integration, the correlation of economic fluctuations across countries has become increasingly prominent. As the world’s second-largest economy, China plays a crucial role in the development and stability of global economy. Therefore, stabilizing China’s economy is of great importance. China and Japan are geographically adjacent, they have increasingly close economic cooperation, and the economic interdependence between the two countries is gradually rising, which may result in the economic synchronization between China and Japan according to the international business cycle theory. In addition, due to historical issues, the bilateral political relations between China and Japan are complex and have some impacts on the economy of the two countries. To stabilize the China’s economy and mitigate the economic effects from economic fluctuations of Japan, this study researches the correlation of China-Japan economic fluctuations and its transmission mechanism. Specifically, based on the data from 1983 to 2018, the VAR model is established. Furthermore, the GIRF and variance decomposition are employed to examine the dynamic correlation of economic fluctuations between China and Japan and its transmission mechanism. The research conclusions are as follows: First, there exists business cycle co-movement between China and Japan. Second, the transmission mechanism of the co-movements of economic fluctuations between China and Japan are bilateral trade and Japan’s direct investment in China. China’s economy is highly sensitive to import from Japan. The FDI from Japan comes second and export to Japan is at the last place. Third, China-Japan political relation has indirect influence on China-Japan economic synchronization. Its improvement will stimulate the growth in FDI and bilateral trade instantly.

Based on the above conclusions, this study applies trade index analysis and historical data analysis to research the features of bilateral trade and Japan’s direct investment in China, namely the transmission mechanism of economic synchronization between China and Japan, and further proposes the methods of mitigating the effects of Japan’s economic fluctuations. In terms of the pattern of bilateral trade and Japan’s direct investment in China, it is concluded that the trade relation between China and Japan is close. China and Japan have strong comparative advantages and trade complementarity in labor- and capital-intensive products, respectively. The comprehensive trade complementarity between China and Japan is strong. Because Japan values the great potential market space of China, and China focuses on the advanced manufacturing technology of Japan, the Japan’s direct investment in China is manufacturing centered. In addition, the improvement of bilateral political relations between China and Japan would benefit to stabilize and promote China’s economic development. Therefore, to prevent Chinese economy from being affected by Japan’s economic fluctuations, this article proposes the following suggestions: increasing R&D investment and deepening industrial upgrade to promote the development of China’s high-tech industry; relaxing market access restrictions to attract high-quality foreign investment; establishing and expanding trade and financial cooperation with other countries; strengthening the political mutual trust; and encouraging communications between China and Japan in science, technology, education and so on.

In general, the main contributions of this study are as follows: applying the FDI stock rather than the FDI flow to represent the FDI variable, which is beneficial to acquire more precise estimation results; executing dynamic analysis for China-Japan economic co-movement and the according transmission channels, which are rarely considered in previous studies, with the VAR model, impulse response, and variance decomposition methods; detecting the effects of China-Japan political relation on economic co-movement between the two countries, which is rarely examined in the existing studies; and through relevant index and data analysis and historical data analysis, proposing the stabilizing measures for China to mitigate the economic shock in Japan. The findings of this study would provide reference in mitigating the external shocks to China’s economy and formulating relevant policies for economic stability, and may be of some practical significance.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440211001372 – Supplemental material for The Transmission Mechanism of China-Japan Economic Co-Movement and Stabilizing Measures for China’s Economy

Supplemental material, sj-docx-1-sgo-10.1177_21582440211001372 for The Transmission Mechanism of China-Japan Economic Co-Movement and Stabilizing Measures for China’s Economy by Wanping Yang and Bingyu Zhao in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is the periodical results of the Key Research Project of Shaanxi Provincial Federation of Social Sciences (20ZD195-65), and Key Projects of Philosophy and Social Sciences Research, Ministry of Education in China (20JZD012).

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.