Abstract

This study identifies and gauges the extrinsic national-level drivers of foreign direct investment (FDI) flows into and out of the Central African Economic & Monetary Community (CEMAC) region. Drawing on the literature that simultaneously explains the reinforcing loop between FDI inflow/outflow and the broader literature on FDI, this study identifies macro factors that motivate the investment decisions of multinational enterprises. Based on factor Analysis, five decision pillars were identified. Using a fixed effect panel model with a backward stepwise procedure, the findings confirm a reinforcing link between the initial level of FDI inflow/outflow and the current pace of FDI flows. In addition, we found that inbound FDI location decision in CEMAC and Sub-Saharan Africa is strongly influenced by good governance, improved welfare, and efficient communication infrastructure. Additionally, the prior levels of FDI inflow strongly influence the outflow of investment from domestic investors.

Keywords

Introduction

Foreign Direct Investment (FDI) is a cornerstone of global economic integration, widely recognized as a critical driver for transferring not just capital, but also technology, managerial skills, and knowledge across borders (Sindze et al., 2021). For nations worldwide, the pursuit of FDI is a central development strategy, with its inflows directly linked to enhanced welfare, job creation, and sustainable economic growth (Adegboye et al., 2021; Nam & Ryu, 2023). This topic is vital for non-specialists to understand because the ability of a country to attract and benefit from investment is not an abstract economic concept; it has tangible impacts on livelihoods, poverty reduction, and the availability of goods and services (Djokoto et al., 2023; Djokoto, Agyei Henaku, et al., 2022; Fagbemi & Osinubi, 2020). While the determinants of FDI in developed and major emerging economies are well-established (Blonigen, 2005; Paul & Singh, 2017), a significant knowledge gap persists regarding the forces that shape investment in the world’s most promising yet challenging contexts, particularly in Africa.

The drivers of FDI are broadly categorized as intrinsic or extrinsic.

Despite extensive debate on multinational decision-making, a significant gap remains in understanding how extrinsic factors sustain FDI flows in the African context, particularly for both inbound and outbound investment. While several studies have examined the determinants of FDI inflow to developing nations (Chakraborty & Basu, 2002; Delevic & Heim, 2017; Liu et al., 2002), scholarly attention has disproportionately focused on inflows, neglecting how a country’s macro-environment influences local firms’ decisions to engage in outbound FDI. This gap is critical, especially given Africa’s status as the smallest recipient of global FDI and its minimal representation in outbound flows (Bartels et al., 2009; Jaiblai & Shenai, 2019). This research gap is most acute in the Central African Economic and Monetary Community (CEMAC). Extant literature on African FDI often aggregates data from disparate countries, failing to account for the unique, shared economic paradigm of a regional bloc like CEMAC (Bartels et al., 2009; Jaiblai & Shenai, 2019). A regional analysis, however, allows for a more nuanced comparison among member states that operate under a common growth strategy (Brakman et al., 2011). Therefore, by focusing on the extrinsic drivers of both inbound and outbound FDI within CEMAC, this study addresses a critical and overlooked area, moving beyond generic cross-country comparisons to provide targeted insights for a strategically important yet under-researched economic community.

Within Africa, CEMAC represents a region of profound strategic importance that remains critically understudied. Comprising Cameroon, Congo, Gabon, Equatorial Guinea, the Central African Republic, and Chad, CEMAC is an economic bloc with immense potential, heavily reliant on its natural resources. However, it is also one of the continent’s least integrated and most volatile regions, characterized by unique institutional and macroeconomic challenges (Besong et al., 2022; Ibara, 2020). Despite a common currency and trade policy aimed at fostering integration, the region’s average FDI inflow as a percentage of GDP has stagnated, and its outbound FDI is virtually negligible (Moussavou, 2022). For example, data from the World Bank (Figure 1) indicates that the average contribution of FDI inflow to GDP between 1990 and 2023 is 2.7% which is slightly above the average of SSA (0.35%) and the World (2.5%) (https://databank.worldbank.org). This underperformance highlights an urgent need to investigate the extrinsic determinants, such as institutional quality, financial market development, and macroeconomic stability, that inhibit or could catalyze both inbound and outbound investment flows within this unique community.

Comparative trend of FDI inflow/outflow in the CEMAC region, Sub-Saharan Africa, and the world from 1990 to 2023 according to data from World Development Indicators of the World Bank.

Therefore, this study seeks to address this gap by answering a pivotal question: What are the key macro-level drivers influencing both the inflow and outflow of FDI in the CEMAC region? We do this by first identifying the main macro drivers of localization decisions and then testing their impact on FDI flows. This approach is vital because understanding the location decisions of investors provides direct, actionable insights for policymaking. Our investigation is guided by the concept of “spiral reinforcement,” where a favorable macro-environment attracts foreign investment, which in turn stimulates domestic competition and capability, eventually enabling local firms to internationalize (Stoian, 2013). This process is further conceptualized by the Investment Development Path (IDP), which links a nation’s net investment position to its stage of economic development (Dunning, 2020).

The contribution of this study to the literature is threefold. First, we extend the literature on FDI determinants by simultaneously analyzing the factors driving both inbound and outbound flows, a rare approach, especially in the African context. Second, we provide one of the first focused empirical analyses on the CEMAC region, offering insights tailored to its specific economic union and challenges. Third, by employing recent data and modern empirical techniques, we provide timely and actionable evidence for policymakers. Rather than asking if FDI is beneficial, a question already explored in prior regional studies (Pea-Assounga & Wu, 2022; Sindze et al., 2021), we address the more pressing question of how sustainable and mutually reinforcing investment flows can be responsibly encouraged. The findings aim to inform strategies that not only attract foreign capital but also cultivate competitive regional champions, ultimately contributing to the CEMAC region’s sustainable economic development and the welfare of its population.

Theoretical Underpinning for Extrinsic Factors Impacting the Flow of FDI

FDI, in its simplest form, is an investment of resources in production and business activities by a foreign investor outside their home country (Yavas & Malladi, 2020). In early times, international business scholars often evaluated how macroeconomic factors such as taxes, exchange rate movements, and tariffs affect a firm’s foreign investment decision. This has further been expanded in recent literature to include other exogenous determinants such as the quality of the regulatory institutions, human capital, and financial and infrastructural development (Alzaidy et al., 2017; Moussavou, 2022; Nguyen, 2022; Nketiah-Amponsah & Sarpong, 2019). FDI is deemed pivotal in stirring economic, social, and environmental development, particularly in countries where financial and technological resources are scarce. The benefits of FDI to a country are conditioned on good governance, human capital, financial capital, clarity in government regulation, international and domestic-oriented infrastructure, domestic business infrastructure, international outlook, and quality of life (United Nations Industrial Development Organization [UNIDO], 2003). Thus, the methodological steps for answering the research question ‘What are the main extrinsic-level factors influencing the flow of FDI into or out of the CEMAC region? are systematically developed through the review of extant literature on FDI and international business. The purpose of the analysis is to identify which determinants are important for sustaining FDI flows necessary for sustainable development and to evaluate the causal connection between these determinants and FDI flows (in/outbound).

Exchange Rate Effect

On the nexus between exchange rates and FDI, scholars have studied the subject from various angles, including the bilateral level of the exchange rate between countries and the volatility of exchange rates. Early studies on the exchange rate effects assumed that fluctuations in exchange rates do not influence the investment decisions of multinationals. However, the work of Froot and Stein contradicts this hypothesis and emphasizes that in an imperfect market, movements in the exchange rate affect investment decisions due to their effect on the expected return on investment (Froot & Stein, 1991). In this regard, a depreciation in a foreign currency will trigger an appreciation in the investor’s home currency, allowing them to invest extra wealth. Recent findings support Froot and Stein’s hypothesis that exchange rate depreciation increases FDI in Nigeria (Nwosa, 2021), Mauritius (Ang, 2008), and across develop and developing counties (Warren et al., 2023).

Tax Effect

An observable hypothesis is that countries with high corporate tax rates may deter foreign investors, as it reduces potential profits; however, lower tax rates can attract more FDI by providing a favorable business environment. Nevertheless, the effects of taxes vary markedly by type of taxes, estimation method of FDI activity, and tax treaty on double taxation between the host country and the investor’s country of origin (Blonigen, 2005). Early studies on taxation and FDI generally focused on corporate tax. The evidence presented suggests that tax harms FDI as well as the profit margin of the foreign subsidiary in the host country (De Mooij & Ederveen, 2021; Shirodkar & Konara, 2017). The academic scholarship has further considered the effect of other forms of tax, such as income tax and bilateral and multilateral tax. In a working paper, Desai et al. (2004) find that the effect of indirect business taxes on FDI is similar to the effects of corporate tax. Similarly, an increased tax rate was also found to be detrimental for FDI inflow into Africa (Abille & Mumuni, 2023). In a nutshell, irrespective of the type of tax, the outcome is negative on FDI once the tax rate increases.

Trade/Export Effect

The literature on the trade effect of FDI is timid, even though FDI has been portrayed as an alternative to export for the host country (Blonigen, 2005). The discussion of FDI being a substitute for export can be traced back to the 1980s (Buckley & Casson, 1981). The choice to export or acquire FDI was the focus of early economic theorists (Bhasin & Paul, 2016). These scholars found, on the one hand, a complementary effect (Lipsey & Weiss, 1981) and a substitution effect on the other hand (Grubert & Mutti, 1991) between export and FDI. Recent findings also reported complementary (Bashir et al., 2023) and substitution effects (Bricongne et al., 2023). Scholars have also considered a unified approach to analyzing the export/FDI decisions of multinationals. This unified approach is underpinned by the assumption that both export and FDI are key determinants of a multinational firm’s investment decision (Jin et al., 2021).

Institutional Effect

Several development studies have highlighted the role of quality institutions as pivotal if the gains of development are to be attained and sustained (Mariotti & Marzano, 2021; Polemis & Stengos, 2020; Susan & Natu, 2023). Similarly, the quality of institutions is perceived to be a key decision criterion for multinationals when deciding on an investment location (Abille & Mumuni, 2023). The conclusions on the effect of the quality of institutions on DFI flow are mixed. Using corruption as an approximation for governance, Wei observed that these indices have a strong negative correlation with FDI (Wei, 2000), which is contrary to earlier studies (Wheeler & Mody, 1992). Conversely, governance mechanism like control of corruption and government effectiveness was found to have a positive impact on the inward flow of FDI (Abille & Mumuni, 2023). It should be noted that the estimation of the quality of institutions is somewhat difficult. Prior studies have often relied on some composite index of a country’s political, legal, and economic institutions, based on survey responses from officials or businessmen familiar with the country. Therefore, studies that attempt to estimate the degree of the effect of institutions on FDI are scanty due to the lack of a proper proxy for good governance (Nam & Ryu, 2023). Nevertheless, with the introduction of the World Governance Indicators by the World Bank, comparative analysis on this variable can now be performed across countries over time.

Financial Development

Finance is an engine for economic growth. Studies have empirically analyzed the role of finance as a determinant of FDI (Alfaro et al., 2004; Nguyen, 2022). The literature on financial development has largely seen financial development from the perspective of banks. Nevertheless, it has been argued that the efficiency of the financial market is also important for investment decisions (Nguyen, 2022). However, not all regions across the world have well-functioning financial markets. Thus, it is believed that the banking sector is still pivotal in creating much-needed credit for the private sector, particularly in Africa. There is no doubt that financial development is important in attracting and retaining FDI. However, the empirical evidence is inconclusive, particularly in defining the threshold point at which the benefits from FDI will be optimized. Scholars have also explored the role of financial development as a moderator of FDI and economic growth (Nguyen, 2022). However, much is yet to be uncovered about the direct impact of financial development on the decision to acquire FDI by multinational enterprises.

In sum, the effect of the identified extrinsic country-level determinants on FDI varies between the scope of the analysis and the methodology used. Concurrently, there is a growing consensus that home country macroeconomic indicators (Jaiblai & Shenai, 2019; Kalotay, 2008) or host country development-related indicators (Gidiglo et al., 2023; Gohou & Soumaré, 2012) significantly impact FDI flows. Therefore, we believe that a more in-depth analysis of home country macro-factors that influence the investment decision of multinationals is needed, specifically in the CEMAC region, where the scholarship on FDI flows remains scarce and the region is yet to fully take advantage of this source of development finance.

Research Methodology

Data Collection and Variable Definition

The primary sources of data for this analysis are the World Bank database and the United Nations Development Program (UNDP). The sample consists of the six member states of the CEMAC region, and the analysis period is from 2010 to 2021. The sample size was motivated by the full availability of data for all variables and countries. Most notably, the data for one of the indicators of social welfare (inequality index) is only available from 2010 in the UNDP database (Human Development Index | Human Development Reports). In addition, a subsample for Sub-Saharan Africa (SSA) is included in the analysis for comparison (Angola, Benin, Botswana, Burkina Faso, Burundi, Cabo Verde, Cameroon, Central African Republic, Chad, Comoros, Congo Dem. Rep., Congo Rep., Cote d’Ivoire, Equatorial Guinea, Eritrea, Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea-Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Nigeria, Rwanda, Sao Tome and Principe, Senegal, Seychelles, Sierra Leone, South Africa, Tanzania, Togo, Uganda, Zambia, and Zimbabwe). To address the issue of missing data in some variables, cases were eliminated using pairwise exclusion (Tabachnick et al., 2007). All variables are defined in Table 1.

Definition of Variables.

WDI: World Development Indicators of the World Bank; WGI: World Governance Indicators of the World Bank; UNDP: United Nations Development Program.

Outcome Variables

In this study, two outcome variables are deployed and selected following the notion that countries want to attract FDI to boost development. Based on this drive, the first dependent variable is the net inflow of FDI as a proportion of GDP. This variable is the most widely used indicator for FDI by scholars, particularly for cross-country analysis (Bashir et al., 2023; Jaiblai and Shenai, 2019; Nwosa, 2021). Studies have also demonstrated that firms and governments of developing countries aspire to internationalize their operations in a bid to gain recognition and improve their competitive advantage back home (Stoian, 2013). In this light, we also evaluate what factors trigger private and state-owned enterprises to go international. To this end, the construct that has been frequently used in outward FDI analysis is deployed as a second variable for FDI. This is estimated as the net outflow of FDI as a percentage of GDP (Stoian, 2013; Zamani, 2023).

Localization Determinants (Explanatory Variables)

There is extensive literature on the determinants of FDI flow, and this has revealed that the relationship between them is complex. In this study, we do not go into the complexity of how many factors collectively affect the magnitude of FDI flows; rather, the focus is to simply identify factors that are correlated with some degree of significance with FDI flows. To this end, a list of localization determinants is identified and grouped into five broad categories: economic, socio-demographic, financial, physical infrastructure, and governance. For the causality test, each sub-category is assumed to be independent of the other due to variations in performance by countries in the different categories. This has been proven true for SSA countries (Jaiblai & Shenai, 2019). Therefore, a good performance in one dimension does not mean a similar performance in the other dimension.

Economic Factors

The economic factors considered in this analysis are based on those that have been found to have some association with FDI. In the first place, the income level of the country is introduced as an indicator. This variable is operationalized using the growth rate of GDP per capita, which is the most widely used proxy for economic growth (Moussavou, 2022; Nguyen, 2022). Economic factors like trade openness (Agbloyor, 2019; Djokoto, Agyei Henaku, et al., 2022; Djokoto, Gidiglo, et al., 2022; Evans & Kelikume, 2018; Hamdi & Hakimi, 2022), inflation (Aloui, 2019; Djokoto, Gidiglo, et al., 2022; Hamdi & Hakimi, 2022), gross domestic investment (Jaiblai & Shenai, 2019), official exchange rate (Desai et al., 2004; Nwosa, 2021; Warren et al., 2023), and tax on profit (De Mooij & Ederveen, 2021; Shirodkar & Konara, 2017) were also considered. All these variables have been documented to have an association with the flow of FDI. Additionally, the lag of dependent variables was introduced as economic indicators based on the argument that a retrospective and reinforcing loop exists between FDI inflow and outflow (Dunning, 2020; Stoian & Filippaios, 2008).

Socio-Demographic Factors

Social and demographic factors that motivate investment are considered. Specifically, human capital has been highlighted as a key determinant for localization (Agbloyor, 2019; Djokoto, Agyei Henaku, et al., 2022). To this end, policies that promote education, health, and equity will enable the manifestation of a positive spillover effect (Agbloyor, 2019). Similarly, it is suggested that labor cost, labor quality, and market size are the key determinants of FDI inflows (Djokoto, Agyei Henaku, et al., 2022; Gidiglo et al., 2023). Thus, the following factors are considered for this analysis: literacy rate (Djokoto, Agyei Henaku, et al., 2022), equity (Agbloyor, 2019), labor force participation rate (Groot, 2014), population growth (Alfaro et al., 2004; Ibhagui, 2020), and final government expenditure (Gidiglo et al., 2023).

Financial Development Factors

Finance is important for promoting investment, and access to finance has been found to propel business expansion (Desbordes & Wei, 2017). Also, financial development creates an enabling environment for firms to monitor investments and improve their investment efficiency (Abille & Mumuni, 2023). To operationalize financial development, the following variables are employed: domestic credit to the private sector as a percentage of GDP; bank capital to asset ratio; bank liquid reserve; and proportion of non-performing loans. These variables collectively demonstrate the stability of the financial sector and its ability to create credit and have been widely used (Alfaro et al., 2004; Nguyen, 2022).

Physical Infrastructure Factors

Infrastructural development has been highlighted as an important criterion for investment decisions (Castrén et al., 2014). Basic infrastructures such as paved roads and information and communication technology (ICT) are necessary to attract and retain FDI as they break investment and geographical barriers in trade (Wafure & Nurudeen, 2010). Specifically, the use of mobile phones and internet connectivity has been reported to enhance financial inclusion in the CEMAC region (Susan et al., 2022). In this light and consistent with prior studies, the physical infrastructural variables that are considered necessary tools for sustainable development include mobile phone penetration (MS), internet penetration (NeT), fixed telephone subscription (Tel), and fixed broadband subscription (FB) (Djokoto, Agyei Henaku, et al., 2022; Jaiblai & Shenai, 2019).

Governance Factors

For a vibrant economy, there must be firm governance principles in place to protect the rights of all. Specifically, empirical literature suggests that for any economy to sustain its attractiveness, administrative institutions must be efficient in the discharge of their responsibilities (Susan & Natu, 2023). Concurrently, the quality of institutions is an important determinant of FDI activity, particularly for developing and underdeveloped countries (Abille & Mumuni, 2023). To estimate governance, we utilized the World Governance Indicators of the World Bank, which have been widely used as a comparative proxy for quality institutions.

Governance (quality institution) is an indicator variable with six dimensions: voice and accountability (VA), control of corruption (CC), rule of law (RL), government effectiveness (GE), political stability and absence of violence (PSV), and regulatory quality (RQ). The variable scores range from −2.5 to 2.5 in standard normal units and 0 (lowest) to 100 (highest) in percentile rank terms. The absolute scores (−2.5 to 2.5) were used for the analysis.

Model Specification

The selection of variables influencing FDI flows, particularly in an understudied context like the CEMAC region, presents a challenge due to the multitude of potential macroeconomic, institutional, and financial factors. To empirically explore the most salient country-specific factors associated with FDI inflows and outflows, we employed a backward stepwise regression procedure. This method was selected over the more conventional “Enter” (or “All-in”) method for several reasons pertinent to our research objectives. While the Enter method includes all candidate variables simultaneously, it is highly susceptible to multicollinearity and overfitting, especially with a limited number of observations, potentially obscuring the most robust predictors (Hastie et al., 2021). In contrast, the backward stepwise approach provides a principled, data-driven method for variable selection. It begins by estimating a general model with all potential explanatory variables. The least statistically significant variable is then iteratively removed based on a pre-specified threshold (p-value < .10), and the model is refit until only variables that contribute meaningfully to explaining the variance in the dependent variable remain (Cohen, 2013).

We acknowledge the documented limitations of stepwise regression, including its tendency to capitalize on chance variations in the data and to produce inflated R2 values (Smith, 2018). Therefore, the results of this procedure are not interpreted as definitive causal inferences but rather to identify a parsimonious set of strong candidate variables for further investigation in the CEMAC context. This approach is particularly valuable for exploratory research in areas with limited prior empirical evidence, as it helps to reduce a large set of potential predictors to a core model that balances goodness-of-fit with simplicity and generalizability.

The general form from which the stepwise was built follows the econometrics basis given as:

where X1– Xn represents the individual macro-level FDI decision variable as defined above. Concurrently, given the limited number of countries (N=6) and the relatively short time series available, a direct application of a high-dimensional fixed-effects panel model with all potential covariates is statistically infeasible and would lead to a critical loss of degrees of freedom and possibly unreliable estimates. To address this challenge, our empirical strategy employed a two-stage approach, clearly distinguishing between the exploratory variable selection stage and the confirmatory inference stage. For the initial variable selection, we utilized a classical Pooled Ordinary Least Squares (OLS) regression with a backward stepwise procedure. The linear form of Eq. 1 is expressed in Eq. 2, following previous literature (Sarma & Pais, 2008).

where FDI_flowj,t denotes the dependent variables (FDI_Inflow and FDI_Outflow) for country j at time t, X1…..Xn are explanatory variables, β1, …, βn, are the parameters to be estimated from the data, and ε is the error term. Cognizant that a classical OLS does not control for unobserved heterogeneity, the final estimates from which inferences are made follow a rigorous panel data model. Specifically, we apply a fixed effect panel model to account for all unobserved, time-invariant country-specific characteristics that may influence FDI flows, thereby mitigating potential omitted variable bias. The final model is presented as Eq. 3.

where,

The conceptual framework of the study.

Results and Discussion

Summary Statistics

The statistical relevance of each investment decision indicator as presented in extant literature was evaluated using the Kaiser-Meyer-Olkin (KMO) Measure of Sample Adequacy (MSA) and Bartlett’s test of sphericity from Principal Component Analysis (PCA). PCA is a statistical dimension reduction tool used in converting an array of potentially correlated variables into fewer uncorrelated factors without altering the original values significantly. It is also used to determine how many components are needed for factor analysis based on the Initial Eigenvalues (Pituch & Stevens, 2015). In this study, PCA was employed first as a dimension reduction strategy to operationalize a composite index for the main decision pillars. Secondly, it further provides guidance on the number of possible factors that can be obtained from all the identified FDI decision criteria. Table 2 presents the results of the test of validity for all identified decision criteria. It was observed that MSA for the combined set of investment decision indicators included in the analysis is respectively 0.657 and 0.817 for the CEMAC region and SSA, which is above the threshold value of 0.5 (Kaiser & Rice, 1974). Also, the MSA of the individual indicators is largely within the threshold of 0.50. This indicates items within the constructs can be summed/averaged together to calculate a composite score for each decision category. In addition, the probability associated with Bartlett’s test of sphericity was adequately satisfied, with p < .000. Interestingly, the ‘Initial Eigenvalues’ categorization suggests that there are five components/factors, which is consistent with our initial random categorization of criteria into five groups based on extant literature. Overall, there is little variation between the countries in the analysis, as the values of the standard deviation are relatively smaller compared to the mean. Appendix A presents the descriptive statistics of all regression variables.

Component Scores and Measure of Sample Adequacy (MSA) of the Determinants of FDI Decision in CEMAC.

The Main Decision Pillars of FDI Flows

To determine the index of the five FDI decision pillars identified, PCA was employed to identify those variables within each decision pillar with factor loadings that give a combined Measure of Sampling Adequacy (MSA) of at least 0.5% with a p-value < .01 to formulate the index. After identifying these variables, the component score of each variable was assumed to represent the weight of that variable, which was then interacted with the original value for the variable. Then, the sum of all variables after the interaction was used to represent the value for each decision category, as shown in Eq. 4. The main categories/pillars included the economic, socio-demographic, financial, physical infrastructure, and governance. It is important to note that the lag-dependent variables were not included in the factor analysis but were added separately as predictors in the regression model. The MSA and component scores for each category are presented in Appendix B.

where Indexj is the index for each decision category; Wj is the component score weight of the parameter; X is the respective original value of the constituents, and p is the number of variables in the equation.

After formulating the index for each investment decision pillar, their empirical importance was evaluated using a backward stepwise procedure (Table 3). Based on the results in Columns 1 and 2, the inflow of FDI is principally driven by the prior rate of outbound FDI, followed by good governance, infrastructural development, and socio-demographic factors (Table 3). Taking each significant predictor in turns, initial outbound FDI increases the current inflow of FDI. That is, in a country with a median outbound FDI of 0.021% or 0.041% per year, the estimated coefficients of 0.832 and 0.829 will imply a relatively small increase in FDI inflow by approximately 0.017% (0.832*0.021) and 0.034% (0.829*0.041) in CEMAC and SSA, respectively. Similarly, an increase in the quality of governance has a positive impact on the inflow of FDI. Conversely, the estimated coefficient for infrastructure and wellbeing was negative, which indicates that as these factors decreased, so did the inflow of FDI both in the CEMAC region and SSA.

The Main Decision Pillars of FDI Flows.

Note. P-Value of *** < 1% is reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

Furthermore, economic growth and financial development did not have any noticeable effect on the inflow of FDI. This is unexpected given that prior studies have highlighted that economic growth and financial intermediation are prerequisites for attracting FDI into SSA (Bartels et al., 2009). However, these two factors seemed to be absent, and the current flow is largely due to the opportunities for the growing demand for natural resources from rapidly growing economies, and knowledge gathered from existing multinationals in this market. This is intuitively and theoretically reasonable, as studies revealed that the localization decision of Norwegian multinationals rests on information gained from enterprises that share a common origin and institutional quality of a host country (Ragnhild & Tøndel, 2013). Although there was no statistical evidence of economic and financial development as predictors of FDI inflow, the findings largely support the argument in the literature that, in the absence of quality governance and infrastructure for doing business, location-specific advantages are not sufficient to attract significant volumes of FDI (Bartels et al., 2009).

Regarding the outflow of FDI from CEMAC and SSA, only the prior level of inbound FDI was found to significantly influence this variable. In essence, companies in these countries, after competing with foreign multinationals, seek to internationalize their operations to access resources necessary to compete with foreign multinationals in their home country. In other words, based on the state of competitiveness in the domestic economy, local firms have developed ownership advantages that allow them to successfully internationalize their operations. This strand of the result is consistent with the IDP hypothesis that FDI inflow enhances FDI outflow (Dunning, 2020; Stoian & Filippaios, 2008).

The Analysis of Individual Decision Criteria in Each Decision Pillar

Our analysis so far has been on the main decision pillars of multinational enterprises. In this section, we replace the index of each decision pillar with the individual variables.

The Empirical Result of Economic Factors

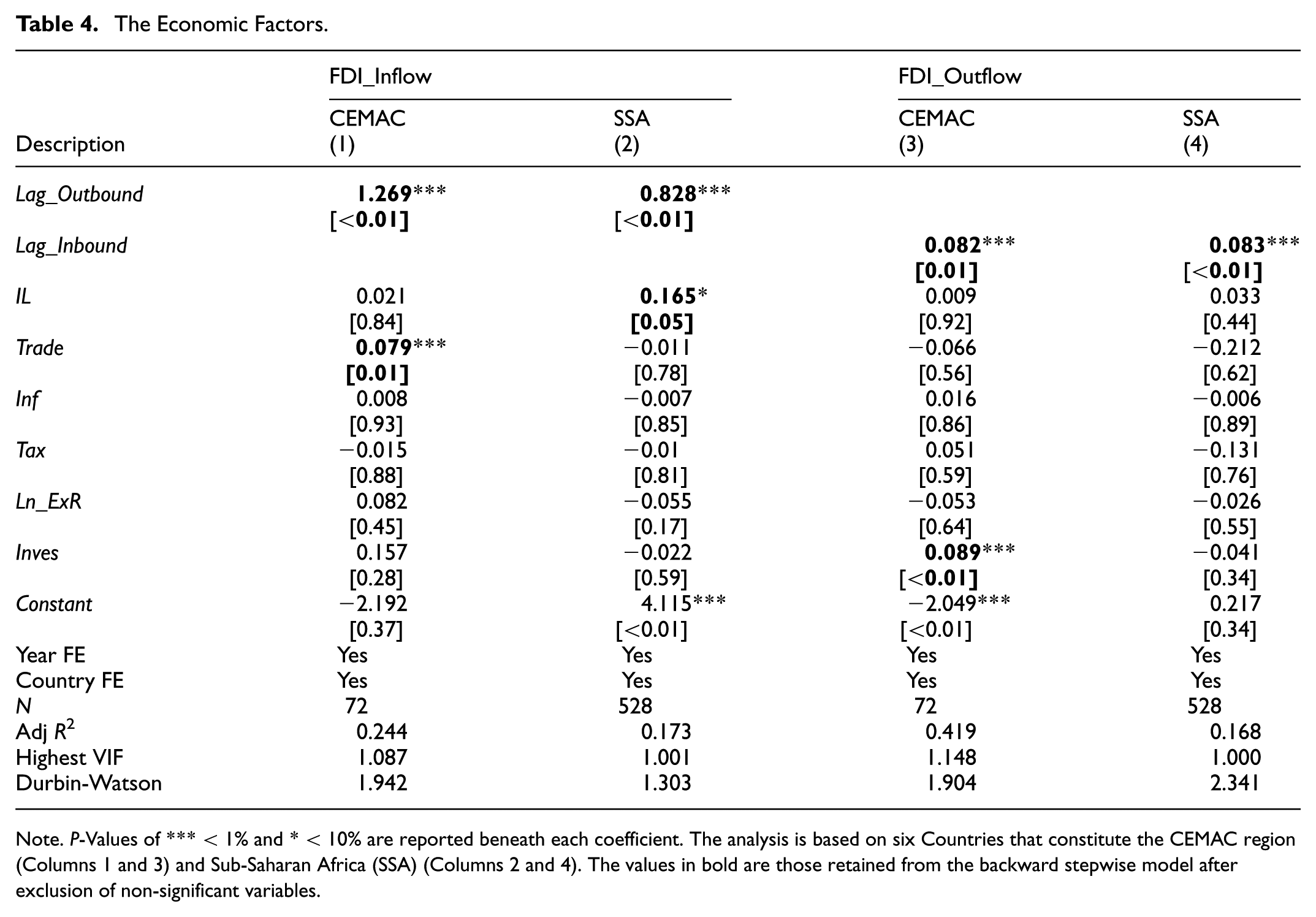

Building on the hypothesis that a retrospective effect exists between outbound and inbound FDI flows (Dunning, 2020; Stoian & Filippaios, 2008), we regressed FDI flows on seven economic indicators, including income level, trade openness, inflation, tax, exchange rate, domestic investment, and the lag1 values of FDI in/outflow. The lag indicators test how the initial inflow/outflow of FDI impacts the current period investment flows. Columns 1 and 2 of Table 4 show the result of FDI_inflow for, while Columns 3 and 4 show the result of FDI_outflow for CEMAC and SSA, respectively. The results obtained suggest that for the CEMAC region and SSA, not all these variables are critical determinants of FDI decisions. More interestingly, the variables with some level of significance based on the backward-stepwise procedure vary between CEMAC and SSA. Looking at the variable that drives the inflow of FDI, in Column 1, only Lag-outbound and Trade were found to be positive predictors of FDI_inflow for the CEMAC region, while in Column 2, Lag-outbound and income (IL) positively predicted the inflow of FDI into SSA. Similarly, Lag-inbound was found to be a positive predictor of FDI outflow for both the CEMAC region and SSA. Additionally, domestic investment (Inves) had a positive causality with FDI-outflow in the CEMAC region (Column 3).

The Economic Factors.

Note. P-Values of *** < 1% and * < 10% are reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

Considering the variables with significant association, the result suggests that when trade openness increases, it encourages more inflow of FDI by 8% in the CEMAC region. This finding aligns with the hypothesis that when countries relax trade restrictions, it motivates multinationals to shift from being export-centric to establishing subsidiaries to reduce their operational cost (Bhasin & Paul, 2016; Blonigen, 2005). In essence, as trade barriers reduce, multinationals can penetrate foreign markets and build market presence, and once there is evidence of rising demand for a commodity, FDI might be attracted to the host country to produce that product locally, leading to a rise in FDI inflow (Bashir et al., 2023; Kosekahyaoglu, 2006). This result collectively affirms the proposition that FDI contributes more to the growth of the host country when the trade regime is open (Bricongne et al., 2023). By the same token, as the income level of a host country increases, the approximate rise in FDI inflow is 17% in SSA. This finding supports the argument that foreign multinationals are attracted to countries with rising income levels since this reveals the ability of the locals to afford their products owing to greater purchasing power and could lead to higher returns on investment (Azam & Lukman, 2008). Also, the initial level of FDI outflow from a country was found to statistically predict the current inflow of FDI for both CEMAC and SSA. This is consistent with the Dunning investment development path (IDP) proposition, whereby as developing countries gain a localization advantage, they attract more FDI, which will spur some outbound FDI (Dunning, 2020). Then, when these firms internationalize and gain experience, they re-invest in the domestic economy, leading to a rise in FDI inflow. Based on identified drivers of FDI (Lag_Outbound FDI, trade openness, and income level), the policy implication for the host countries is to focus on reforms that advance the income level of locals and promote trade openness.

Concerning the determinants of FDI outflow, it was observed that the most relevant determinant on statistical grounds is the prior level of inbound FDI (Lag_Inbound). This confirms the theoretical underpinning of a retrospective link between inbound and outbound FDI. The estimated coefficient suggests that an increase in initial inbound FDI increases the proportion of FDI outflow by approximately 8% in CEMAC and SSA. This is an indication that domestic firms have developed ownership advantages that they can explore through internationalizing their operations abroad. For the CEMAC region, domestic investment was found to be a positive predictor of outbound FDI flow, which suggests that local experience provides a platform necessary for local firms to internationalize, leading to a rise in FDI outflows. Therefore, these advantages of ownership may be a result of experience gained from domestic investment that is associated with a higher level of a country’s economic growth or with spillovers from foreign investors operating in the domestic economy. This finding is consistent with prior literature (Rugraff, 2010; Stoian, 2013) and further provides support for the IDP theory.

The Empirical Result on Socio-Demographic Factors

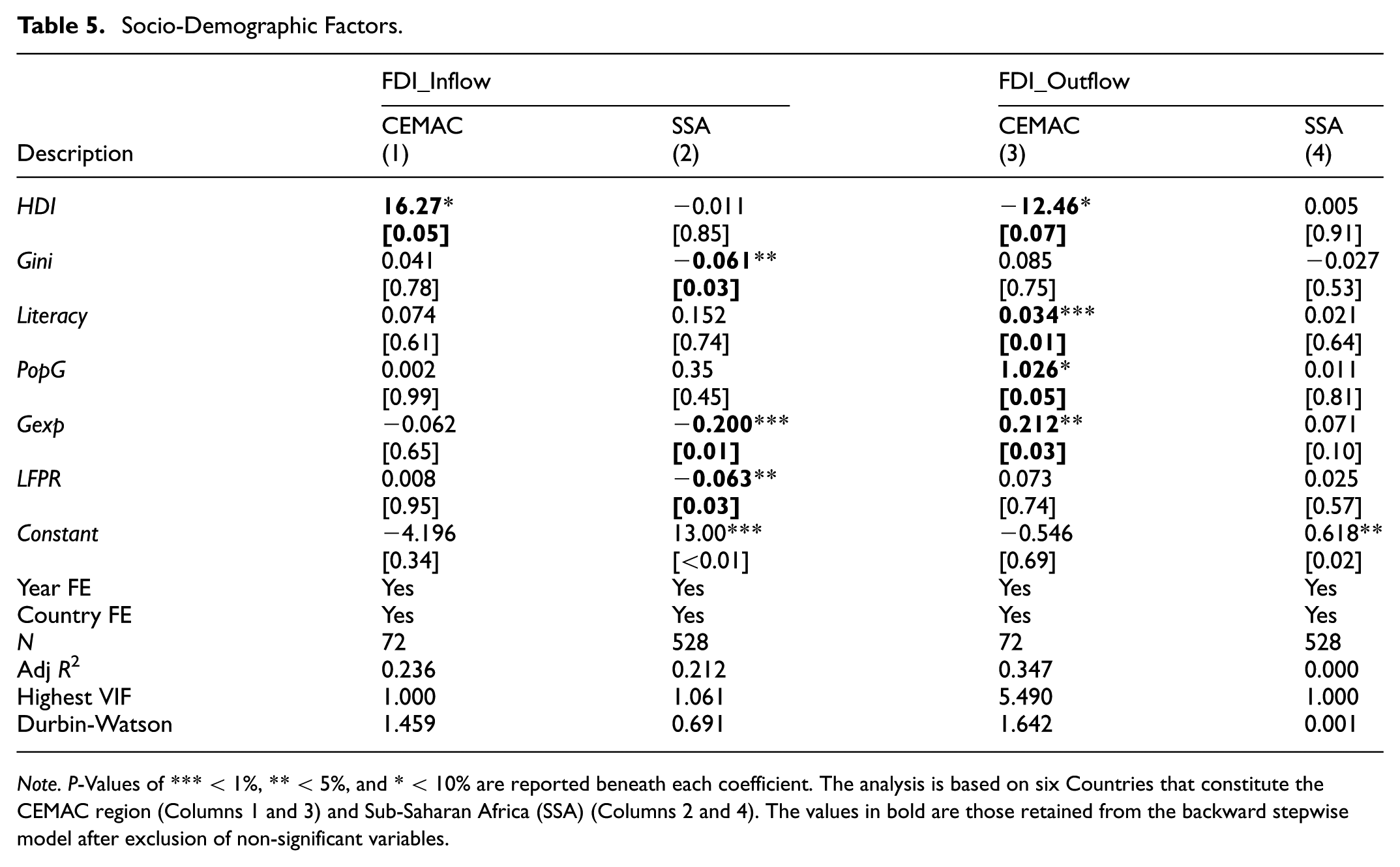

In Table 5, the extent to which some socio-demographic factors influence FDI flows is shown. From Column 1, human development (HDI) is the only significant predictor of FDI inflow in the CEMAC region. This suggests that as the human development index of a host country increases, investors are more attracted to that nation. This aligns with the arguments that multinational enterprises are efficiency-centric in their localization decisions (Luo, 2003), and this efficiency is affected by wellness and knowledge, which are all embedded in the HDI. For SSA, three variables were found to influence the inflow of FDI. Notably, a 1% decline in equity proxied by the Gini coefficient (Gini) leads to a reduction in the inflow of FDI by 6%. In other words, rising inequality in a host country will undermine the decision to invest in that country. Also, a decline in local government expenditure to support local consumption (Gexp) and labor force participation rate (LFPR) leads to a fall in FDI inflow by approximately 20% and 6%, respectively. This further reiterates the necessity for increasing the value of the high productivity-adjusted cost of skills (Bartels & Freeman, 2000) through government support and a quality labor force.

Socio-Demographic Factors.

Note. P-Values of *** < 1%, ** < 5%, and * < 10% are reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

The outflow of FDI is driven principally by HDI, Literacy, population growth (PopG), and government expenditure (Gexp) in the CEMAC region. Specifically, a reduction in HDI depletes the outflow of FDI since domestic investors lack the knowledge and skills necessary to explore ownership advantages that spur them to go abroad. On the other hand, a rise in Gexp, PopG, and Literacy allows domestic firms to utilize learning and ownership advantages to explore foreign markets. Unfortunately, no statistical evidence was found to conclude that any of the socio-demographic factors impact the outflow of FDI from SSA. The ‘no-effect’ hypothesis has been corroborated by studies in Sub-Saharan Africa (Evans & Kelikume, 2018), Central, Eastern, and Southern Sub-Saharan Africa (Aloui, 2019), and Nigeria (Adegboye et al., 2021; Fagbemi & Osinubi, 2020). This has largely been associated with an increased concentration of foreign investment in sectors that are deemed lucrative, such as oil and gas. Thus, leaving other sectors perceived as less profitable, such as health and education, less investible (Agbloyor, 2019). Indeed, this limits the learning and ownership advantage necessary for internationalization. Nevertheless, the significant result aligns with the hypothesis that the situation within a country determines the extent of the spillover effect of FDI (Moussavou, 2022; Sindze et al., 2021), and Literacy is instrumental in taking advantage of the spillover from FDI (Ibara, 2020).

The Empirical Result of Financial Development Factors

Table 6 presents regression results for the financial determinants. A total of four determinants were employed, and only two of these determinants demonstrated an association with the FDI decision with some degree of significance. In this light, it was observed that the sign on the coefficient for a non-performing loan (NPL) is negative and statistically significant at 1% in Column 2. A negative NPL is an indication that banks are not giving out credit to low-income groups, and hence, the level of financial exclusion in the SSA is high. The downside of this is reflected in the low inflow of FDI. This outcome is contrary to the expectation that NPL should increase financial inclusion and thus spur investment (Sarma & Pais, 2008). Conversely, the bank’s liquid ratio was found to be a positive predictor of FDI inflow in SSA. Accordingly, the higher a bank’s safety nets, the more its ability to satisfy short-term liquidity constraints, which investors can leverage to reduce costs when expanding their operations. This is consistent with prior studies, which reported that some conglomerates liaise with banks to penetrate new markets on the premise that banks offer a cheaper source of funding and lower the cost of monitoring (Desbordes & Wei, 2017; Hoshi et al., 1991). Thus, the financial development of a host country influences a multinational’s location decision.

Financial Factors.

Note. P-Values of *** < 1%, ** < 5%, and * < 10% are reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

Regarding the outward flow of FDI, we observe that NPL was the only financial predictor with statistical significance at 1% and 10% in the CEMAC region and SSA, respectively. The estimated coefficient is negative, which indicates that as banks attempt to reduce the risk of moral hazard by limiting credit, this hurts the ability of domestic firms to explore overseas markets. Studies have shown that domestic credit to the private sector (DCPS) plays a pivotal role in stirring new investment (FDI_In/flow) (Nguyen, 2022). However, this study did not find any statistical evidence to conclude that this holds for the CEMAC region and SSA in general. This is somewhat expected as extant studies in Africa suggest that the efficacy of financial development in stirring FDI-inflow must be within a defined threshold (Ibhagui, 2020). To this end, it will appear that such a threshold is yet to be attained. Similarly, no statistically significant observations were made regarding the bank’s adequacy ratio (CAR).

The Empirical Result on Physical Infrastructure Factors

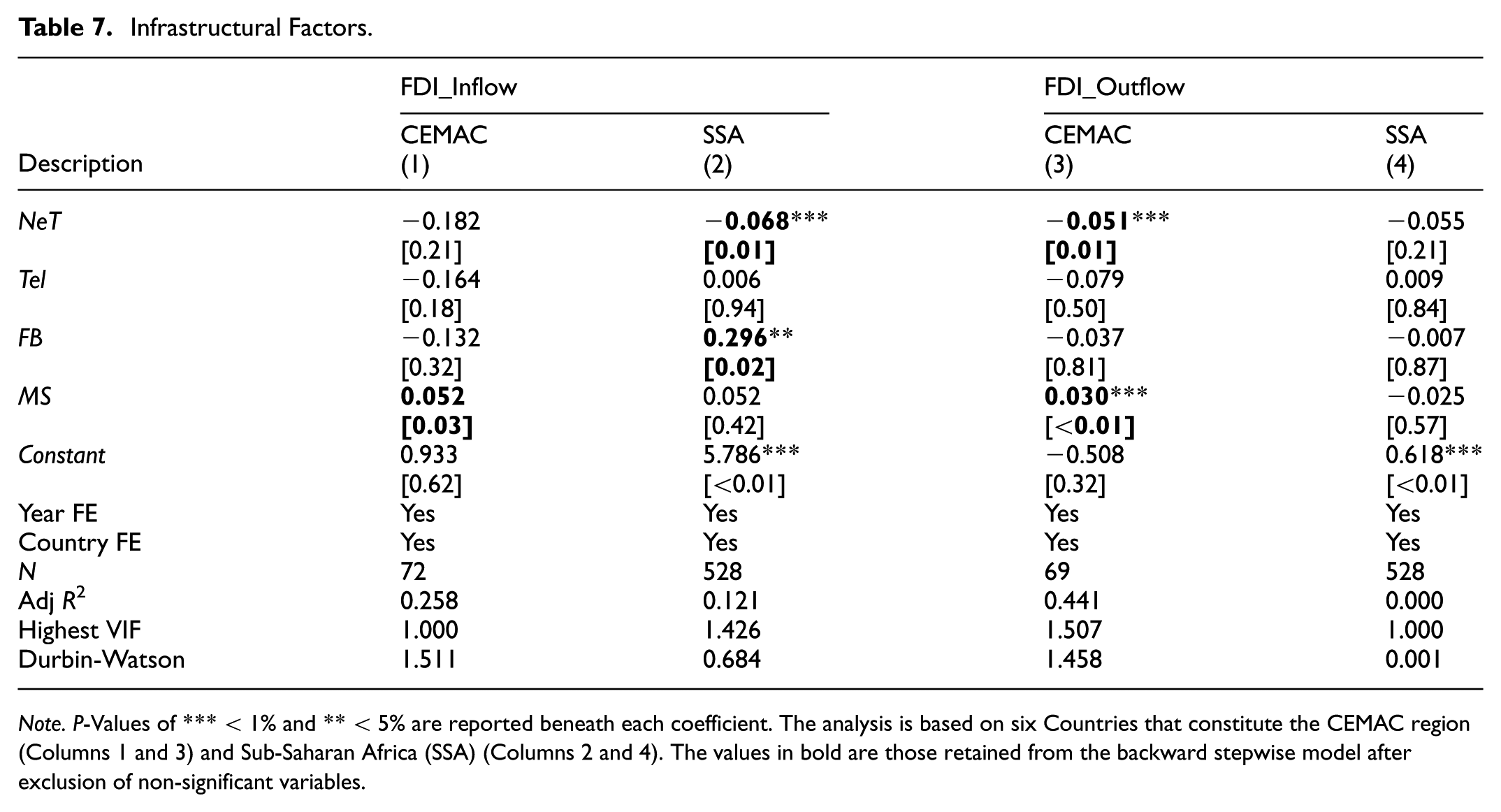

The decision to invest is partly driven by the availability of relevant and reliable information. In this light, infrastructures that facilitate the flow of information have been reported to alleviate information asymmetry in trading relationships (Ozaki & Shaw, 2022). Similarly, information and communication technology are being used to facilitate financial inclusion and trade (Besong et al., 2022; Nevado-Peña et al., 2019). Table 7 presents the regression results of some infrastructural variables that capture both connectivity and availability of information. The result reveals that a 1% rise in the number of mobile phone subscribers (MS) in the CEMAC region increases the inflow of FDI by 5%. Regarding SSA, internet connectivity and fixed broadband connection (FB) were found to be the only significant predictors of FDI inflow. On the one hand, low rates of internet penetration dwindle the inflow of FDI, whereas an increase in FB increases the FDI inflows.

Infrastructural Factors.

Note. P-Values of *** < 1% and ** < 5% are reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

Turning to the outflow of FDI, Table 7 (Column 3), we observed that internet connectivity has a negative coefficient at a 1% level of significance, while mobile subscription has a positive and significant causality with FDI outflow in the CEMAC region. This result is interpreted as a fall in the proportion of people with access to internet services will lead to a decline in FDI outflows by about 5%. Suggesting that a lack of access to the internet undermines the possibility of local enterprises to internationalize and become competitive. Besides, internet connectivity remains low in developing countries, particularly in rural settlements, which further dampens the flow of information (Osabohien et al., 2020). On the other hand, a rise in the number of mobile subscribers increases the proportion of FDI outflow by 3%. Collectively, MS was found to facilitate both inflow/outflow of FDI into and out of CEMAC. This is an indication that mobile subscription increases access to information necessary to make relevant investment decisions. Similarly, MS has been reported to facilitate access to finance in the CEMAC region (Susan et al., 2022). Thus, this finding corroborates extant evidence of MS being pivotal in facilitating information sharing and access to credit, especially for those underserved by the formal financial sector (Besong et al., 2022; Nevado-Peña et al., 2019). However, no statistical evidence was obtained to make an inference that mobile subscriptions influence investment flows to and from SSA. Also, fixed telephone networks had no noticeable influence on FDI flows. In summary, on the one hand, an increase in mobile subscriptions enhances FDI flow into and out of the CEMAC region, and a decline in internet access reduces FDI flow on the other hand.

The Empirical Result of Governance Factors

Rules and regulations are instituted to ensure that the rights and freedoms of all are respected. Similarly, the quality of institutions is perceived to be a key decision criterion for multinationals when deciding on an investment location (Abille & Mumuni, 2023). In this regression, we attempted to evaluate the extent to which the quality of institutions explains the flow of FDI. The variables considered here are the six dimensions of the world governance indicators, and the results are presented in Table 8. We found that not all the indicators are significant predictors of FDI flows. In Column 1, which looks at the inflow of FDI into CEMAC, it was observed that political stability (PSV) and voice & accountability (VA) are positive predictors of inward FDI flows at 1% and 5%, respectively. That is, as these variables rise, so too does the inflow of investment increase. Conversely, the estimated coefficient for regulatory quality was negative and significant, suggesting the need to propagate and implement policies that support private sector development. By the same token, Goldsmith (2003) advocated for the reduction of administrative bottlenecks linked to FDI, which concurrently will limit the rent-seeking behavior of public officials in host countries.

Governance Factors.

Note. P-Values of *** < 1%, ** < 5%, and * < 10% are reported beneath each coefficient. The analysis is based on six Countries that constitute the CEMAC region (Columns 1 and 3) and Sub-Saharan Africa (SSA) (Columns 2 and 4). The values in bold are those retained from the backward stepwise model after exclusion of non-significant variables.

From the perspective of SSA (Column 2), in addition to PSV and VA, control of corruption (CC) positively stimulates the inflow of FDI, while low confidence in the enforcement of contracts and the protection of property rights (RL) adversely impacts the inflow of FDI. This reiterates the need to embed good governance in FDI-attracting strategies. This is because good governance will attract efficiency-seeking investors whose investment has a positive spillover effect but deters exploitative investors (Abille & Mumuni, 2023; Bartels et al., 2009). In the Context of CEMAC and SSA at large, upholding good governance will reduce transaction costs faced by multinationals, thus reducing their propensity to exploit market and governance lapses (Goldsmith, 2003). This will create a level playing field for domestic and foreign investors to compete, leading to positive spillovers of FDI and improvement of the firm-specific advantages of domestic enterprises.

Concerning the outflow of FDI, the observed predictors for CEMAC (Column 3) and SSA (Column 4) are like those observed in Columns 1 and 2. It was observed that PSV and VA have a significant positive association with FDI_outflow at 1% in Column 3 (CEMAC) and 10% in Column 4 (SSA). Whereas RL and government efficiency (GE) have a negative association with FDI outflow in CEMAC and SSA, respectively. This finding is consistent with the theoretical underpinning that good governance will generate positive externalities of FDI inflows, which indigenous companies can leverage to build ownership advantages that allow them to compete in overseas markets. Since most of the governance predictors are significant for both the CEMAC region and SSA at large, this study lends support for the inclusion of governance factors into the IDP framework as suggested in the literature (Stoian, 2013). Thus, we complement studies that posit that governance quality matters for the outward flow of FDI from China (Kang & Jiang, 2012; Wang et al., 2012) and Central and Eastern European Countries (CEECs) (Stoian, 2013), as this intuition holds for countries in the CEMAC region and SSA. Collectively, the result suggests that quality institutions spur the inflow/outflow of FDI, and the reverse is the case when the quality of governance diminishes (Bartels et al., 2009; Stoian, 2013). In addition, this finding also supports arguments in the literature that effective laws allow individuals and corporations to fight for and receive equal opportunities (Mariotti & Marzano, 2021; Polemis & Stengos, 2020).

Conclusion, Policy Implications, and Future Research

Conclusion and Policy Implications

This study identified five macro-level pillars of localization investment decisions: economic, socio-demographic, financial, infrastructure, and governance dimensions. Using a fixed effect panel model with a backward stepwise procedure, we observed on statistical grounds that not all the pillars are critical in driving FDI into/out of the CEMAC region and SSA at large. Specifically, the economic and financial pillars had no significant link with both inbound and outbound FDI. We associate this outcome with the possibility that the region has not attained the threshold necessary for these two factors to motivate FDI in the region. On the other hand, good governance and the proportion of prior outbound FDI increase the inflow of FDI, whereas a decline in wellbeing and infrastructural development hurts the inflow of FDI. This finding supports the argument that no amount of localization-specific advantage can sustainably drive FDI inflow in the absence of proper functioning institutions and infrastructure.

Turning to factors motivating the outflow of FDI from this region, only the prior level of FDI inflow had a significant impact on the proportion of FDI outflow, specifically for the CEMAC region. This provides supportive evidence to the theoretical and intuitive proposition of a reinforcing loop between FDI inflow and outflow. From Appendix A, it was observed that the inbound FDI from both CEMAC and SSA is contributing more to GDP when compared to the contribution of FDI outflow. According to the IDP, this is an indication that this region is in stage 2 of its IDP. However, the rising quantity of FDI is not predominantly due to improved localization advantages but due to the rising demand for natural resources and knowledge gathered from existing multinationals in this market. In the context of this region, the reinforcing externalities of FDI could be sustained through a pro-development FDI strategy. In this light, the policy drive should directly address the initial externalities of FDI through improved well-being, governance, and communication infrastructure to make the region more investible. In doing so, the prerequisite for attracting and encouraging FDI flows could be attained, which will complement the pro-FDI development strategy where interventions directly target development with the hope of attracting and retaining more FDI. In this regard, the spillover effects of FDI can sustainably stimulate development.

Furthermore, the decision pillars were disaggregated, and the outcome variables regressed on the individual variables to ascertain which of these variables specifically could encourage efficient FDI flows. The result revealed that not all these variables are statistically relevant for enhancing FDI. From an economic standpoint, the initial rate of FDI inflow/outflow single-handedly explains FDI flows in CEMAC and SSA. In addition, factors that predict the flow of FDI into CEMAC include: trade openness, human development, mobile subscription, political stability, regulatory quality, and voice & accountability. In SSA, these factors include: income level, equality, government spending to encourage consumption, labor force, non-performing loans, bank lending ratio, internet connectivity, fixed broadband, control of corruption, political stability, rule of law, and voice & accountability.

Concerning outbound FDI, the identified drivers for the CEMAC region include domestic investment, human development, literacy rate, population growth rate, government expenditure to encourage consumption, non-performing loans, internet connectivity, mobile subscription, political stability, rule of law, and voice & accountability. However, in SSA, the factors include non-performing loans, government efficiency, political stability, and voice & accountability. These variables should simultaneously be promoted as part of progress towards responsible and efficient FDI. In essence, these variables should serve as policy priority areas for policymakers of the CEMAC region and SSA in attracting FDI and encouraging local multinationals to go overseas to become competitive.

From the perspective of multinationals as investors, they are attracted to locations with good communication infrastructure, as it alleviates information asymmetry, good governance that protects their investment, and improved welfare that supports productivity performance and lowers overall production cost. Domestic investors going abroad are motivated by the presence of foreign multinationals, who provide learning opportunities that increase the domestic firms’ competitive advantages necessary to invest overseas.

Limitations and Future Research

The primary limitations of this research are threefold: First, we used a backward stepwise regression model, which is effective for variable selection in exploratory research; it is inherently data-driven. This approach can capitalize on chance correlations within a specific dataset, potentially leading to model overfitting and inflated R2 values (Smith, 2018). Although the results identify robust associations, they should be interpreted as indicating strong candidate relationships rather than definitive causal proofs. Thus, to strengthen the inferences that could be drawn from our analysis, we further incorporated time and country fixed effects to minimize endogeneity biases. However, the fixed effect model only corrects the problem of endogeneity but does not eliminate it. Therefore, future studies could employ alternative methods that mitigate the limitations of stepwise regression. Techniques such as Bayesian Model Averaging (BMA) or LASSO (Least Absolute Shrinkage and Selection Operator) regression could provide more robust variable selection. Furthermore, the proposition of a “reinforcing loop” between FDI inflow and outflow presents an excellent opportunity for future research to apply Structural Equation Modelling (SEM) or system GMM estimators for dynamic panel data to formally test these causal pathways and feedback mechanisms.

Secondly, the study focuses on a specific region using national-level macro data across CEMAC and SSA. While the regional focus on CEMAC is a key contribution, the findings may not be fully generalizable to other developing contexts with different economic structures and historical trajectories. Furthermore, the reliance on country-level data may mask significant sub-national variations in economic activity, infrastructure, and governance. In this light, a fruitful avenue would be to conduct a comparative study between CEMAC and another regional economic community (e.g., ECOWAS in West Africa) to identify commonalities and differences in FDI drivers. This would help distinguish region-specific factors from pan-African trends.

Finally, macro-level analysis by design does not capture firm-specific or industry-specific factors that are critical to individual FDI decisions, such as managerial capabilities, firm size, or strategic motives (e.g., market-seeking vs. resource-seeking). A micro-analysis is, however, beyond the scope of the current studies. Nevertheless, the finding that economic and financial pillars were insignificant may reflect this aggregation, as specific variables within these categories (e.g., a particular sector’s growth rate) might be highly relevant for certain types of investment. To bridge the macro-micro gap, a critical next step is research utilizing firm-level data from surveys or administrative records. This would allow for a direct test of how the macro-level pillars identified here (e.g., governance, infrastructure) influence the investment calculus of individual firms. Investigating sectoral heterogeneity (e.g., comparing FDI in extractive industries vs. services) would also yield more nuanced and actionable policy insights. Additionally, qualitative case studies of specific multinational enterprises (MNEs) that have invested in or originated from the region would provide a deep contextual understanding of the strategic motivations and challenges behind the statistical relationships uncovered in this study.

Footnotes

Appendix

Variables for estimating the index of FDI decision pillars.

| Panel A: SSA | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Economic | Socio-demographic | Financial | Infrastructure | Governance | |||||

| Description | Component score | Description | Component score | Description | Component score | Description | Component score | Description | Component score |

| Inves | 0.838 | HDI | 0.711 | CAR | 0.713 | NeT | 0.692 | CC | 0.556 |

| Tax | 0.559 | LFPR | 0.509 | NPL | 0.758 | Tel | 0.727 | GE | 0.870 |

| Trade | 0.841 | PopG | 0.534 | BLR | 0.173 | FB | 0.742 | PSV | 0.568 |

| Inf | 0.536 | Gexp | 0.323 | MS | 0.635 | RL | 0.934 | ||

| RQ | 0.833 | ||||||||

| VA | 0.724 | ||||||||

| KMO and Bartllet’s Test | |||||||||

| KMO-MSA | 0.504 | 0.689 | 0.525 | 0.689 | 0.863 | ||||

| Bartllet’s Test of Sphericity | |||||||||

| Approx. Chi square | 352.4 | 376.3 | 225.0 | 1243.3 | 3213.7 | ||||

| df | 6 | 6 | 3 | 6 | 15 | ||||

| Sig. | <0.01 | <0.01 | <0.01 | <0.01 | <0.01 | ||||

| Panel B: CEMAC | |||||||||

| Economic | Socio-demographic | Financial | Infrastructure | Governance | |||||

| Description | Component score | Description | Component score | Description | Component score | Description | Component score | Description | Component score |

| Inves | 0.734 | HDI | 0.569 | CAR | 0.767 | NeT | 0.729 | CC | 0.803 |

| Trade | 0.752 | Gini | 0.835 | NPL | 0.657 | Tel | 0.353 | GE | 0.824 |

| Ln_ExR | 0.144 | LFPR | 0.668 | BLR | 0.599 | FB | 0.764 | PSV | 0.924 |

| PopG | 0.538 | DCPS | 0.570 | MS | 0.546 | RL | 0.944 | ||

| RQ | 0.847 | ||||||||

| VA | 0.872 | ||||||||

| KMO and Bartllet’s Test | |||||||||

| KMO-MSA | 0.525 | 0.696 | 0.565 | 0.653 | 0.0747 | ||||

| Bartllet’s Test of Sphericity | |||||||||

| Approx. Chi square | 28.88 | 118.8 | 16.32 | 89.75 | 373.1 | ||||

| df | 3 | 6 | 6 | 6 | 15 | ||||

| Sig. | <0.01 | <0.01 | 0.012 | <0.01 | <0.01 | ||||

Ethical Considerations

There are no human participants in this article and informed consent is not required.

Author Contributions

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Humanities and Social Science Fund of the Ministry of Education of the People’s Republic of China (23YJAZH225).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.