Abstract

This article analyzes the relationship between inflation, increase of investment in fixed assets, monetary policy, financial openness, national savings, macro-economic climate index, deposit rate, and the development of insurance industry in China. We set the incremental indicators as the variables and constructed an analysis integrating a multiple linear regression, stepwise regression, and robustness analysis, and used historical monthly data sample during the period of January 2004 to December 2017 for empirical analysis. The result indicates that (a) the national savings and macro-economic climate index are the major factors that influence the development of insurance industry in China by now; (b) to improve the development of insurance industry, both the economic growth and people’s income should continue to advance; and (c) financial openness should be paid more attention to, which is insufficient, and there is lack of competitive vitality in the whole insurance market.

Keywords

Introduction

Insurance constitutes an integral part of finance, thus the healthy development and safety of insurance industry are of great significance to the social and economic development in a country, which even involve the safety and stability of the whole community to a certain degree. In China, premium reached 3.66 trillion Yuan in 2017, making the premium size of China the second largest in the world. However, in terms of insurance depth, density of China is weak, which represents that the development depth and breadth of insurance industry of China is weak. In 2016, the insurance density of China was US$377 per person, while the average insurance density of the world was US$621 per person, which is almost twice as high as China. Meanwhile, the insurance depth of China was 4.1%, while the average insurance depth of the world was 6.1% (Hu, 2018). It is obvious that there is a big gap between China and the average level of the world. Therefore, it is necessary to study and analyze the factors that affect the development of the insurance industry to promote further development of the insurance industry in China.

In addition, in terms of financial openness of China, the insurance industry is the earliest and most open. By the end of 2017, the original premium income of foreign insurance companies was 214.06 billion Yuan, and the market share was 5.85%. In detail, (a) 22 foreign property insurance companies (85 property insurance companies in China) had original premium income of 20.639 billion Yuan, accounting for 1.96% of the market share; (b) 28 foreign life insurance companies (85 life insurance companies in China) had original premium income of 19.366 billion Yuan, accounting for 7.43% of the market share; and (c) in Beijing, Shanghai, Shenzhen, and Guangdong, where the foreign insurance companies are relatively concentrated, the market shares of foreign insurance companies were 14.65%,15.22%,8.91%, and 10.46%, respectively (Feng et al., 2018). By contrast, foreign insurance companies have higher market share in regions with more openness. Overall, foreign insurance companies currently account for small share and limited influence on the insurance industry of China. However, there are great differences in the regions with more openness, which indicates the problem of regional development imbalance. Therefore, we should set the financial openness as a factor which can influence the development of Chinese insurance industry. Moreover, at the Boao Forum in the spring of 2018, Chinese President Xi Jinping has expressly proposed to accelerate the opening up (openness) of insurance industry and cancel the restriction on the proportion of foreign shareholding. The expansion of opening up will bring new opportunities and challenges to insurance industry in China. To seize the new opportunities and cope with the challenges, it is necessary to analyze the major factors influencing the development of insurance industry in China, especially add the factor of financial openness.

A fair large of literatures have analyzed the factors influencing the development of insurance in China. The scholars analyzed from different perspectives, including the macro, medium, micro, and economic perspectives by applying various methods. Arena (2008), Lee et al. (2016), Rudra et al. (2016, 2017), and Anghelache et al. (2019) have conducted research on the relationship between insurance development and economic growth and used data from different countries of the world. Hong et al. (2014), Tang (2015), Gao (2018), and Wang (2019) have analyzed the relationship between insurance development and economic growth in China. They have found that the economic growth significantly promoted the development of insurance, since the economic growth reflects the insurance demand and the financial situation of people represents the purchasing power of insurance. Zhou (2014), Yuan (2015), and Yang and Zhu (2019) have researched the impact of monetary policy on the development of insurance industry in China. They have found that different types of monetary policy can affect the development of insurance industry differently. Hu and Chen (2012), Wang (2019), and Paunica et al. (2019) have studied how the inflation influence the development of insurance industry, resulting that the inflation would cause price rise expectations and make long-term insurance demand reduction. Tian (2017), Fu and Wang (2017), and Wang (2019) focused on the empirical analysis of the development of insurance industry in China. Their studies indicate that the national savings and increase of investment in fixed assets are important factors influencing the development of insurance industry in China. Meanwhile, Zhou and Guo (2012) and Tian (2017) have found that there is a significant negative correlation between the real interest rate and the per capita insurance expenditure in China. Moreover, different scholars have found different factors that can influence the development of insurance industry from different perspectives, such as the education (Dong, 2017; Wu & Zhao, 2011), rational industrial structure (Dong, 2017; Zheng & Zheng, 2017), market competition (Wu & Zhao, 2011), institutional environment (Lee & Chang, 2015; Lee et al., 2016), age structure (Dong, 2017) and urbanization level (Zheng & Zheng, 2017).

On the basis of the existing research, we should take into account the recent unique environment in China, especially with the acceleration of the liberalization of the Chinese insurance industry. Guo and Dong (2018) and Feng et al. (2018) have pointed out the importance of financial openness influencing the development of insurance industry in China. Therefore, we set the expansion of financial opening up in China as one of the factors influencing the insurance industry which was rarely considered before. We construct a special analysis integrating a multiple linear regression, stepwise regression, and robustness analysis to analyze the factors influencing the development of insurance industry in China.

Previous Studies and Hypotheses Development

Variables

Based on previous studies and data availability, we select premium income as the leading indicator to evaluate the development of insurance industry in China, and the major factors influencing the development of insurance industry consist of the inflation, increase of investment in fixed assets, monetary policy, financial openness, national savings, macro-economic climate index, and deposit rate.

Premium income

Gu and Wang (2008) indicate that the safety of Chinese insurance industry requires that the effective supply of insurance industry should match the level of social and economic development. The effective demand of Chinese insurance industry should at least not be lower than that of developed countries in the same period. The insufficient effective demand of insurance industry (also the actual insufficient effective supply) means the effective supply cannot meet the needs of current social and economic development. If the effective supply (demand) is not reached, it denotes that the insurance industry is in an unsafe situation; the greater the gap, the higher the degree of unsafe. The total premium can reflect the scale of the development of the insurance industry; the higher the amount, the higher the effective supply of the insurance industry, and the higher the safety degree of the insurance industry. Therefore, in this article, we set premium income (

Inflation

The Fisher effect has pointed out that the inflation expectation showed a positive correlation with the interest rate. It means that the interest rate will increase upon the rise of the inflation expectation. Generally, insurance uses a fixed predetermined interest rate to calculate the premium. When the nominal interest rate increases rapidly with inflation and far higher than the insurance predetermined interest rate, the premium appears more expensive. Thus, the demand for new insurance orders reduces, and the withdrawal of cash by existing policy holders increases. Moreover, inflation will cause people to form future price rise expectations, prompting them to expand spot consumption and reduce the demand for long-term insurance, which is not conducive to the development of the insurance industry (Wang, 2019). Therefore, we can consider the inflation as an important factor affecting the development of insurance industry. In this article, we use the year-on-year growth rate of consumer price index (CPI) of the current month (

Increase of investment in fixed assets

The total investment in fixed assets of a country reflects the main amount of fixed asset reproduction. The growth of fixed asset investment will stimulate the growth of property insurance, thus affecting the growth of the insurance industry (Tian, 2017). In 2006, the investment in fixed assets was 934.72 billion Yuan for the whole year in China. By 2017, this figure had increased to 631.68 billion Yuan (Wang, 2019). Actually, we can assume that two thirds of the assets are invested in the construction in progress and buy insurance products at a rate of 1%, which will generate a large premium income. It can be said that the growth of fixed asset investment plays an important role in the development of insurance industry. Therefore, the increase of investment in fixed assets (

Financial openness

Since the opening of Chinese insurance industry to the outside world, foreign-funded insurance institutions have played a positive role in promoting the standardized development of Chinese insurance industry. The impact on the insurance market has gradually increased, although there are relatively slow development of foreign insurance institutions and relatively small share. Guo and Dong (2018) have pointed out that the policy of further opening up can help foreign insurance institutions to open up the Chinese market and play a positive role in promoting the insurance industry. It can improve the product research and management, promote the competition in the insurance industry, and, thus, improve market efficiency and protect the interests of consumers. Although the influence of further financial opening policy on the competition pattern of Chinese insurance industry is limited in the short term, it is an important factor affecting the development of Chinese insurance industry in the long run.

Dong (2019) thinks that (a) the contents of financial openness can be basically reflected by the provisions and constraints of financial items through policies and regulations; (b) the regulations or constraints on capital account and financial services trade are the core contents of financial openness; and (c) the larger the total amount of capital and financial account inflow and outflow in the current year, the smaller the government’s restrictions on financial openness, and the greater the corresponding financial openness. In this article, we adopt the total inflow and outflow of the capital and financial account in balance of international payments of China as the indicator of financial openness (

National savings

National savings (

Macro-economic climate index

The development of macro-economy can influence or determine the insurance demand. Insurance demand refers to the real purchasing power demand for various insurance products. To prevent risk and avoid losses, the policyholders are willing to pay the premium to avoid the major losses that may arise in the future. Tang (2015) has found that the main reasons that can affect the insurance demand are risk tolerance, idle funds, and insurance awareness. However, the development of macro-economy can determine the abovementioned reasons, mainly reflected as follows: (a) in the case of rapid economic development, the amount of existing wealth of policy holders will increase. It will bring more financial security concerns and resulting in an increase in the total amount of risk, so that the demand for insurance; (b) it will actually increase the average income level of residents and improve the real purchasing power of people to insurance; and (c) the development of macro-economy will raise the people’s demand for various consumer goods, thus producing more demand for insurance.

Generally, the development of macro-economy is measured with gross domestic product (GDP) by scholars. However, the GDP is not publish by monthly in China, we employ the macro-economic climate index (

Deposit rate

The deposit rate will affect the savings of residents, thus affecting the development of the insurance industry. Zhou and Guo (2012) have concluded through an empirical research that there is a significant negative correlation between the real interest rate and the per capita insurance expenditure in China. When the rate is high, the people will choose the products of bank instead of the insurance. According to previous research, we choose the 1-year deposit rate (

Data Source

The historical data set consisting of 168 monthly data samples from the Wind database during the period of January 2004 to December 2017 is used for empirical analysis in this article. Before the test, we have carried on a stationarity test to the data to make sure it is stationary. For some data missing, we have done the following: (a)

To eliminate the heteroscedasticity and multi-collinearity of data, and prevent the violent fluctuation caused by data changes, we adopt the logarithm values of premium income (

Descriptive Statistics of Relevant Variables.

Method

We construct an analysis integrating a multiple linear regression, stepwise regression, and robustness analysis. The process can be expressed as three parts, as follows:

1. Construct an initial model and check the multi-collinearity: a multiple linear regression is applied to build the initial model as:

where

2. Find an optimal combination of variables without collinearity: a stepwise regression is used. A stepwise regression is actually a feature extraction method that can find an optimal combination of variables that can explain most dependent variable variation. In this step, Formula 1 can be improved as:

where

3. Perform a robustness analysis: the common DF method proposed by Dickey–Fuller is applied for the variable stationarity test first. If the variables are stationary, a vector auto-regressive (VAR) model will be built; if the variables are non-stationary, a vector error correction model (VECM) will be constructed, and then a cointegration test and other model tests (model residual autocorrelation test and VECM system stability test) will be generated.

Empirical Test and Results

Initial Model Construction and Regression Analysis

A multiple linear regression is applied to construct the initial model to analyze the relationship between the year-on-year growth rate of CPI of the current month (

Table 2 shows the results of the regression analysis for all the factors that influence

Regression Results of the Initial Model.

Note. Robust standard errors in parentheses.

***p < .01.

Correlation Coefficient Matrix of Independent Variables.

Stepwise Regression for Finding an Optimal Combination of Variables

A stepwise regression is used as a feature extraction method to find an optimal combination of variables that can explain most dependent variable variation. Forward selection, backward elimination, and bidirectional elimination are the three methods used usually. (a) Forward selection: only one independent variable is in the model that explains the largest dependent variable variation first, and then another independent variable is added to see whether the dependent variable variation explained by the whole model increases significantly after adding it (F-test, t-test, etc.). This process iterates over until no independent variable meets the conditions of adding the model. (b) Backward elimination: in contrast to forward selection, all variables are put into the model, and then try to remove one of the independent variables to see whether there is a significant change in the variation of the explanatory variables in the whole model, and the variables that minimize the amount of interpretation will be eliminated. This process continues to iterate until no independent variables meet the condition of elimination. (c) Bidirectional elimination: it is equivalent to combining the forward selection and backward elimination. It is not blindly increasing variables, but after adding one, all variables in the whole model are tested and the variables with no significant effect are eliminated. Finally, an optimal combination of variables is obtained.

In this article, we apply the bidirectional elimination. First, we construct six simple linear regression models of

Estimated Results of Simple Linear Regression of

Note. Robust standard errors in parentheses.

***p < .01.

With the model of

According to the result shown in Column 6 of Table 5, the main factors affecting the premium income (insurance safety) are financial openness, national savings, and deposit rate. In detail, the coefficient of

Results of Stepwise Regression.

Note. Robust standard errors in parentheses.

**p < .05. ***p < .01.

Endogenous Analysis

The endogeneity of the variables caused by bidirectional interactions is the most common endogeneity issue. In this article, there may be bidirectional interactions between the safety degree of the insurance industry and financial openness. On one hand, the higher the safety degree of insurance industry, the more and deeper the expansion of financial openness. On the other hand, the more and deeper expansion of financial openness can always make a higher safety degree of insurance industry. Therefore, we have made an endogenous analysis and introduced the import and export (Win.d database:IMEX, data from Win.d database) as an instrumental variable of financial openness.

In general, the use of instrumental variables should satisfy both the exogenous and the endogenous conditions. With regard to endogenity, a larger

Regression Results of Instrument Variable.

Note. Robust standard errors in parentheses.

p < .1. **p < .05. ***p < .01.

The results shown in Columns 3 and 4 of Table 6 are the regression results of the two-stage least squares for the instrumental variable. In Column 3, the first-stage regression result shows that the coefficient of

Robustness Analysis

To verity the reliability and non-randomness of the previous results, a cointegration test for

Variable stationarity test

The DF method proposed by Dickey and Fuller is applied to carry out the unit root stationarity test. If the variables are stationary, a VAR model will be built; if the variables are non-stationary, a VECM model will be constructed. Table 7 shows the results, where

Unit Root Stationarity Test Results.

Cointegration test

Before the cointegration test, we shall determine the cointegration rank of the system as well as the lag order of VAR representations corresponding to the system. The lag order is determined based on the lag length criteria in the lag structure. In this article, the Akaike information criterion (AIC) minimum standard is applied to find the optimum lag order, and it can be expressed as:

where

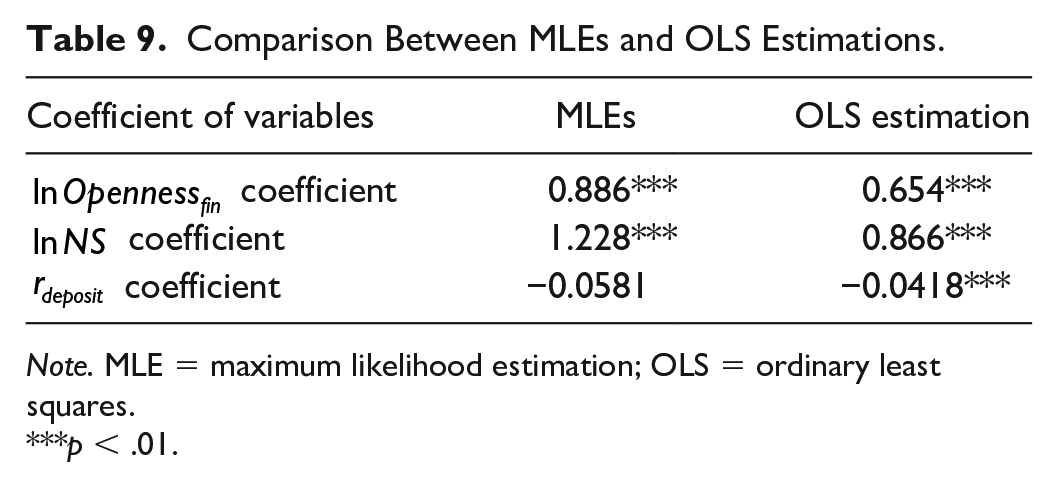

Table 9 shows the result of comparative analysis between the maximum likelihood estimations (MLEs) and the ordinary least squares (OLS) estimations. Since the OLS estimations are significant and similar to Johansen’s MLEs, the empirical results are reliable. It indicates that the financial openness and the national savings are the factors affecting the insurance industry in China. However, the long-term relation between the deposit rate and the development of insurance industry is not significant. Based on the results shown in Column 6 of Table 4, the coefficient of

Cointegration Test Results.

Comparison Between MLEs and OLS Estimations.

Note. MLE = maximum likelihood estimation; OLS = ordinary least squares.

p < .01.

Model tests

A series of tests consisting of model residual autocorrelation test and VECM system stability test should be performed to insure the VECM model is optimum.

The model residual autocorrelation test aims to determine whether there is any autocorrelation in the residuals of the model. If any autocorrelation is present, the lag order should be increased. Table 10 shows the results that the original assumption of “no autocorrelation” is accepted, which means the lag order of 13 is the optimum one.

Model Residual Autocorrelation Test Results.

In this article, we examine whether the VECM features a stationary process through characteristic values. A stationary process requires all characteristic values inside the unit circle. Table 11 and Figure 1 show the results of the stability test; all characteristic values of the matrix, except the hypothetical unit roots of the VECM model itself, are located inside the unit circle. Therefore, it can be confirmed that this VECM model is stable.

Model Stability Test Results.

Note. VECM = vector error correction model.

Model stability test results.

Conclusion

In this article, we conducted the research using the incremental indicators which can influence the development of insurance industry in China, and analyzed the relationship between inflation, increase of investment in fixed assets, financial openness which was rarely considered in the past, national savings, macro-economic climate index, deposit rate, and premium income which can evaluate the development of insurance industry. We constructed an initial model by applying multiple linear regression, then found an optimal combination of variables for feature extraction using a stepwise regression, performed a robustness analysis to test the variable stationarity, built a VECM model, and finally related tests. Moreover, we used the monthly data samples during the period of January 2004 to December 2017 for empirical analysis. The analysis result shows that (a) the major factors that influence the development of insurance industry in China include the financial openness, national savings, and deposit rate by now; (b) the financial openness should be further expanded to inject vitality into the development of the insurance industry; and (c) national savings should be improved to guarantee the development of insurance.

In the future work, we will focus on how to improve the lack of competitive vitality in the whole insurance market and expand financial openness for better development of insurance industry in China.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is supported by the R&D Program of Beijing Municipal Education commission (Grant No. KJZD20191000401). We also thank for the support of the Program of the Co-Construction with Beijing Municipal Commission of Education of China (Grant Nos. B20H100020, B19H100010), and thank for the funding from the Key Project of Beijing Social Science Foundation Research Base (Grant No. 19JDYJA001).