Abstract

This study delves into the factors influencing consumer purchase intention of Thai insurance company policies, focusing on service quality, corporate image, perceived value, and insurance technology. Employing a quantitative approach and multi-stage random sampling, the study selected 440 consumers from 10 Thai insurance agencies in January 2022, using a Google Form link distributed via social media for data collection. The structural equation model path analysis was conducted using LInear Structural RELations (LISREL) 9.1, complemented by descriptive statistics analysis in Statistical Package for the Social Sciences (SPSS) for Windows Version 21. Expert input informed adjustments to questionnaire items, and a pilot test with 35 participants ensured item reliability. The results reveal that insurance technology (0.68), corporate image (0.54), perceived value (0.53), and service quality (0.34) were all influential factors affecting purchase intention, collectively explaining 76% of the variance (R2). Seven of the nine hypotheses tested found support, with the corporate image-perceived value relationship proving the strongest, followed by a moderately strong association between perceived value and insurance technology. Among the 25 observed variables, the quality of services and data standards provided by service quality stood out, with consumers valuing clear, concise, and convenient services as pivotal for agency satisfaction. This research contributes to the existing literature by offering post-COVID-19 insights into consumer insurance purchase intentions in Asia. It also provides valuable knowledge for policymakers and regulators seeking to enhance their sectors and strengthen national economic competitiveness.

Plain Language Summary

This study delves into the factors influencing 440 Thai consumers insurance policy purchase intention. The study focused on how service quality, corporate image, perceived value, and insurance technology affected their decisions. The results reveal that insurance technology, corporate image, perceived value, and service quality were all influential factors affecting purchase intention. The corporate image-perceived value relationship proved to be strongest, followed by a moderately strong association between perceived value and insurance technology. The research contributes to the existing literature by offering post-COVID-19 insights into consumer insurance purchase intentions in Asia.

Keywords

Introduction

The insurance industry in Thailand is playing an increasingly vital role in the country’s economic and social fabric (Limna & Kraiwanit, 2022). As a crucial institution, it contributes to the nation’s financial stability, efficiently managing risks for individuals and businesses, thereby fostering a stable and robust economy (W. Chen & Yuan, 2021). Furthermore, it generates long-term savings and capital for developmental projects and capital market growth, thus underpinning economic progress (Dwivedi et al., 2021; Terdpaopong & Rickards, 2021).

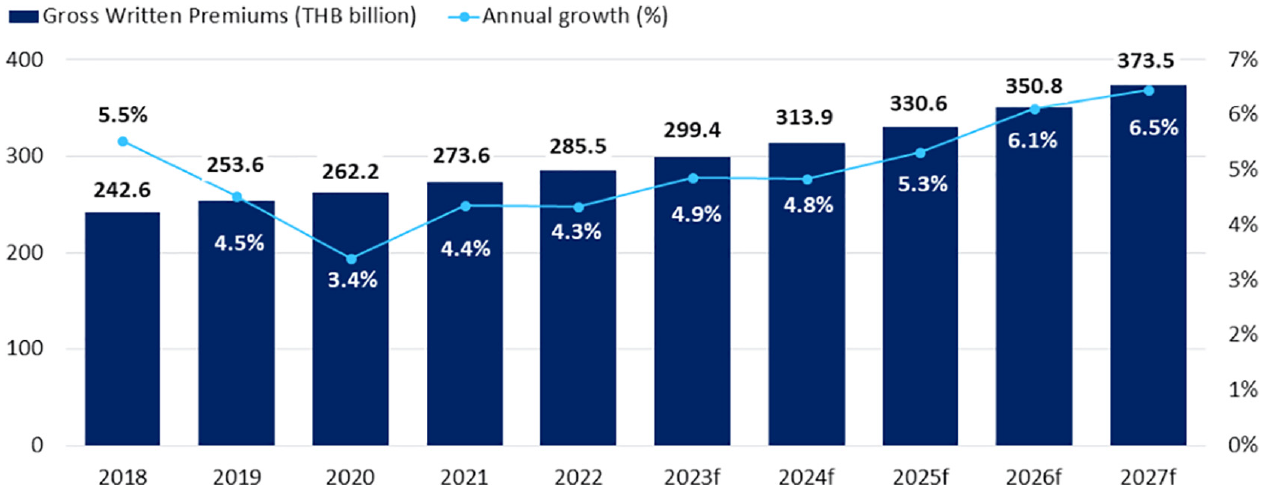

Notably, the majority of Thai citizens, approximately 74.5%, had acquired universal coverage cards (UCCs) as of 2021, with over 67.7 million individuals benefiting from multiple health insurance plans (Statista, 2021). Furthermore, as the Global Data Insurance Intelligence Center (2023) projected, Thailand’s general insurance sector is poised to reach $11 billion by 2027 (Figure 1).

Thailand’s Insurance Sector (2018–2027): Present and future.

Within the expansive realm of general insurance, diverse categories encompass fire, automobile, marine and transportation, and miscellaneous insurance. The regulation of this multifaceted industry falls under the purview of Thailand’s Office of the Insurance Commission (OIC) (Terdpaopong & Rickards, 2021), tasked not only with nurturing the growth of insurance operations but also acting as a vigilant guardian of sectoral order, representing government interests (Sangnuan, 2023; The Star, 2022).

Insurance is a fundamental safeguard against economic uncertainties, protecting businesses across various sectors (Maman & Rosenhek, 2020). By mitigating risks, insurance companies reduce the volatility experienced by enterprises, facilitating smoother economic activities. This risk-mitigation role underscores the pivotal role of insurance policies in ensuring business stability, thus contributing to the ongoing and rapid expansion of the insurance industry (Nikomborirak, 2001).

However, the insurance sector has challenges. For instance, Thailand’s lump-sum insurance segment suffered substantial losses of $1.1 billion due to the COVID-19 pandemic, accounting for 19% of the sector’s surplus and capital as of September 2021 (Sangnuan, 2023). These losses led to the revocation of licenses for two companies, Southeast Insurance, and Thai Insurance, which could not meet the $540 million in COVID-19 insurance claims (The Nation, 2022). This regulatory action was taken under the purview of the Non-Life Insurance Act, resulting in the transfer of 8 million consumer policies from the affected insurers to 31 insurance companies and the state-owned Dhipaya Insurance. As of February 2023, only 52 insurance companies remained in Thailand, with 47 belonging to the non-life category (Sangnuan, 2023; The Star, 2022).

To fortify the remaining agencies, Thailand’s primary insurance regulator, the OIC, actively encouraged sectoral mergers to enhance their financial health and competitiveness (Sangnuan, 2023). Initiatives were also undertaken to facilitate foreign investor entry into the market and increase knowledge exchange between the merged entities. Under new Ministry of Finance (MOF) directives, insurance companies, upon receiving approval, can grant foreigners the ability to hold up to 100% of the total voting shares, subject to MOF permission.

Simultaneously, the ever-evolving technological landscape has made insurance distribution channels more accessible. This technological transformation significantly impacts how insurance services are delivered and accessed (Archapitakvong, 2020). However, as Thailand prepares for liberalization and seeks to bolster the stability and competitiveness of its insurance industry, a robust understanding of capital management becomes paramount. Adequate capital reserves are essential to cushion insurance companies against various risks they encounter. To achieve this and foster customer loyalty, insurance companies in Thailand need to focus on service quality and the fulfillment of promised services. Attributes such as reliability, convenience, and swift customer service (Li et al., 2021) significantly influence customer perception and decision-making. Effective communication, attentiveness to customer needs, and other critical elements further shape Thailand’s insurance industry landscape.

The perception and image of insurance companies in Thailand play a pivotal role in shaping consumer intentions to use their services. A positive image is often synonymous with a good reputation achieved through active participation in corporate social responsibility (CSR) activities (Lee et al., 2017), maintaining open and constructive customer interactions, and demonstrating a solid commitment to ethical business practices. Innovation and uniqueness, including the use of diverse advertising channels such as newspapers, television, and various social media platforms, contribute to insurance companies’ overall image and reputation. A robust CSR strategy promotes a positive image (Lee et al., 2017) and underscores the ethical commitment of insurance companies in Thailand, building trust and confidence among consumers. Moreover, perceived value, encompassing benefits, product value, and reasonable pricing, significantly influences customer decisions, as insurance companies can offer flexible and cost-effective solutions. Meeting customer expectations regarding coverage is a crucial driver of customer willingness to engage with insurance services.

Insurance technology, or InsurTech, is a pioneering innovation in the insurance industry, poised to transform and enhance insurance operations (Bughin et al., 2017). This technology addresses critical challenges, improving efficiency and aligning insurance services more closely with customer needs. InsurTech promises to be a driving force in the future of Thailand’s insurance business, making it faster and more customer-centric (de Ferrieres, 2021; McKinsey, 2017).

By ensuring rapid communication with customers, especially concerning potential security issues, InsurTech bridges the gap in service quality, maintaining a consistent standard of excellence. It also offers a competitive edge over traditional insurance technology. InsurTech introduces various elements that influence customers’ intentions to use insurance services. It calls for modernization, long-term service planning, and fostering a sense of enduring commitment to the services.

While digital disruption often benefits consumers, it poses challenges for companies with significant market shares (McKinsey, 2017), as digital transformation necessitates fundamentally reconsidering corporate strategies. Organizations that adapt may avoid competitors who leverage InsurTech to reduce costs and enhance returns on investment.

The booming insurance industry in Thailand has drawn attention to the patterns of customer service intentions. Understanding the structural equation of variables that impact customer service intentions is crucial. By identifying the variables that exert direct and indirect influences, innovative strategies can be formulated to strengthen the industry further. The study addresses the evolving landscape of the insurance business in Thailand, providing insights into enhancing customer service intentions and driving continuous improvement in the sector.

Statement of the Problem

In the dynamic landscape of the insurance industry in Thailand, characterized by substantial growth and the ongoing impact of the COVID-19 pandemic, understanding consumer behaviors and preferences has become increasingly crucial. Despite challenges, insurance services have gained economic significance, prompting a closer examination of the factors influencing customers’ intentions to engage with insurance companies.

The industry faces challenges and opportunities shaped by economic shifts and technological advancements, particularly in the realm of InsurTech. The critical role of insurance companies’ image and perceived value emerges as pivotal in shaping customer intentions, presenting an intricate interplay of variables that require careful examination.

This study centers on the exploration and decoding of the underlying variables that significantly impact customers’ intentions to utilize insurance services in Thailand. As the industry experiences growth and consumers’ preferences evolve, understanding these variables becomes paramount for both individual insurance companies and the industry as a whole.

The outcomes of this study will serve as a foundation for developing innovative strategies within the insurance industry. Identifying which constructs wield direct influence on purchase intentions and unraveling the intricate web of indirect influences is essential for crafting strategies that resonate with the ever-evolving preferences of Thai consumers.

The ultimate goal is to facilitate the development of tailored strategies that address the unique needs and expectations of Thai consumers. As the insurance industry continues its expansion and adapts to emerging trends, the insights garnered from this research will play a pivotal role in guiding future research endeavors and contributing to the evolution of the industry.

Research Objectives

In this study, our research aims to comprehensively explore the critical determinants influencing Thai consumers’ purchase intention (PI) toward insurance company policies. To accomplish this, a comprehensive Structural Equation Model (SEM) analysis of the variables influencing consumer service intentions will be undertaken. By discerning the direct and indirect influences of constructs such as service quality, corporate image, perceived value, and InsurTech, the research aims to provide actionable insights.

The primary objectives are as follows:

Investigate Determinants: We will examine key factors, including service quality, corporate image, perceived value, and insurance technology, to understand their impact on Thai consumers’ purchase intentions.

Develop a Structural Equation Model (SEM): To quantitatively analyze and model the intricate relationships among these variables, we will construct a comprehensive Structural Equation Model (SEM). This model will provide insights into how service quality, corporate image, perceived value, and insurance technology collectively influence and interact with each other in shaping Thai consumers’ purchase intentions.

Examine Results and Recommendations: Following the SEM analysis, we will thoroughly examine the results and draw meaningful conclusions. Based on our findings, we will provide recommendations for insurance companies to enhance their strategies and improve consumer engagement.

By addressing these research objectives, our study aims to contribute valuable insights to the field and guide future research in understanding and improving consumer behaviors in the context of insurance policy purchases.

Literature Review

Service Quality (SQ)

The foundational framework of service quality in academic discourse revolves around three key concepts: customer satisfaction, service quality, and customer value (Parasuraman et al., 1991).

Expanding the marketing perspective, Rust et al. (1995) broadened the definition, viewing service quality as an extension of the service process and organizational capabilities. It is defined as the ability to meet or exceed individual expectations, aligning with the satisfaction framework. This perspective is supported by Kettinger and Lee (1994), who assert that service quality can be gauged through the satisfaction levels of service recipients.

Recognizing the pivotal role of service quality in business, maintaining a positive service quality position provides a competitive advantage, while subpar service quality places a business at a competitive disadvantage. The interplay between service quality and customer satisfaction is crucial, as dissatisfied customers may swiftly opt for services from alternative providers.

The significance mentioned above gives rise to a framework for considering the model of service quality studies based on three fundamental perspectives. These perspectives manifest in two dimensions. Firstly, service quality can be evaluated by considering all three components or at least two components combined. Secondly, service quality can be assessed using indicators developed from one of the two main perspectives: customer satisfaction or a model like SERVQUAL proposed by Parasuraman et al. (1991), among others.

A common subsequent question is whether to measure public or service recipient satisfaction or to measure from the perspective of service quality. A preliminary answer suggests flexibility, advocating for the adoption of any fundamental concept depending on the significance of the evaluation’s goals and objectives. The key is to measure based on what is important, particularly in the context of utilizing evaluation data for practical benefits. While theoretical concepts and general research conclusions seem to support and accept various methods of measuring service quality, they extend beyond the framework of merely assessing customer satisfaction.

In Thailand, Limna and Kraiwanit (2022) showed that Thailand’s insurance sector is highly competitive. However, the authors believe that service quality is critical in unlocking each organization’s competitiveness and creating customer satisfaction and loyalty (Savitri et al., 2023). Also, Meeboonsalang and Chaveesuk (2019) investigated consumer loyalty within the auto insurance sector in Thailand. Their findings showed that service quality positively and strongly influenced customer satisfaction. This is consistent with Nzyoka and Orwa (2016), who noted the sector’s competitiveness while stating that service quality is critical for obtaining a sustainable competitive advantage. However, Chimedtseren and Safari (2016) reported on the human resource challenges of delivering service quality and, thus, customer satisfaction, maintaining that staff needs problem-solving skills in improving service design and service delivery.

From the theory and literature about SQ, the study’s authors formulated three hypotheses, with the corresponding observed variables detailed in Table 1:

Study Constructs, Survey Items, and Supporting Literature and Theory.

Source. Authors’ research.

Corporate Image (CI)

The information provided on corporate image draws from various studies in different countries, emphasizing the significance of corporate social responsibility (CSR) and its positive impact on consumer loyalty, purchase intention, and corporate image within the insurance industry. Here is a summary:

Finding: CSR has a positive influence on both consumer loyalty and corporate image within the insurance industry in Taiwan.

Implication: The study suggests that investments in CSR can enhance a company’s competitive advantage and financial performance, contributing to a positive corporate image.

Finding: CSR is identified as a critical element in purchase intention within the insurance industry in Pakistan.

Implication: The authors highlight that CSR investments not only influence purchase intention positively but also contribute to a corporation’s competitive advantage and financial performance.

Finding: Service quality and customer satisfaction positively impact customer loyalty, but corporate image hurts loyalty in the context of an Indonesian Bank.

Implication: This study indicates that while service quality and customer satisfaction contribute to loyalty, the corporate image needs careful management as it can have a counterproductive effect on customer loyalty.

Observation: Service quality and corporate image affect customer perception, and company image, perceived value, and service quality are crucial in consumer retention strategies.

Implication: The overall industry perspective suggests that service quality and corporate image are essential factors that influence how consumers perceive and engage with insurance providers.

Importance: A positive corporate image is vital, conveying trustworthiness, reliability, and financial stability.

Consumer Perception: Trust in the insurer’s ability to honor claims and provide excellent customer service is linked to a strong and reputable corporate image.

Impact: A positive corporate image attracts and retains customers, while a negative image can deter potential customers, affecting trust and confidence.

Practice: Companies actively invest in building and maintaining a positive corporate image.

Objective: The goal is to attract new customers, retain existing ones, and foster long-term relationships based on trust and reliability.

From the theory and literature about CI, the study’s authors formulated three hypotheses, with the corresponding observed variables detailed in Table 1:

Perceived Value (PV)

Consumer PV has become a topic of higher interest over the past decade (Dhasan & Aryupong, 2019), and many now realize that PV is an essential factor in the decision-making process of insurance consumers and holds critical importance within the insurance sector (Uzir et al., 2021). Meeboonsalang and Chaveesuk (2019) have added that PV can lead to consumer satisfaction within Thailand’s auto insurance sector, with PV concerned with how individuals assess the benefits they expect to gain from an insurance policy concerning the price they are willing to pay.

These statements are consistent with a 2023 survey conducted in Thailand from which Thailand was reported to have taken the lead in a study of five Asia-Pacific markets in its willingness to share social media information. However, despite Thailand being called a “digital innovation incubator,” it is still old-fashioned value for money (52%), trust in the brand (37%), affordable premiums (38%), and sales policies (Capco, 2023). Some might feel that PV is the linchpin upon which insurance consumers make their decisions, as it is not solely about finding the lowest-priced policy but about finding a policy that offers the best coverage combinations. Therefore, this evaluation is subjective and value-driven (El-Adly, 2019). Furthermore, it profoundly affects whether a potential policyholder chooses one insurance provider over another.

Insurance consumers naturally seek to maximize the benefits they receive while minimizing the costs they incur. PV allows them to strike the right balance, ensuring they obtain adequate coverage for their needs without overpaying for it (Ulbinaitė et al., 2013).

Moreover, consumers often face many insurance options offering distinct features and pricing structures. Perceived value enables them to make informed decisions by comparing the relative advantages of various policies in light of their unique requirements.

From the theory and literature about PV, the study’s authors formulated two hypotheses, with the corresponding observed variables detailed in Table 1:

Insurance Technology (InsurTech)

In recent years, the insurance industry in East Asia, particularly in Thailand, has undergone a significant transformation propelled by the advent of InsurTech. As early as June 2017, Thailand’s Office of Insurance Commission created an InsurTech “sandbox” (Mueller, 2018). A year later, the sandbox welcomed Singapore-based InsurTech Vouch (FairDee in Thailand) as the first InsurTech to take part in the insurance regulatory sandbox (Schellhase & Warden, 2018).

InsurTech involves the innovative use of technology to enhance and streamline insurance operations, marking a departure from traditional practices (Bughin et al., 2017; McKinsey, 2017). The broader vision of Thailand to become a regional financial hub underscores the critical importance of InsurTech in achieving this goal.

The region is currently experiencing the convergence of traditional insurance practices with cutting-edge technology, resulting in the emergence of more accessible, cost-effective, and customer-centric insurance solutions. This integration is especially relevant as Thailand’s insurance industry positions itself for further evolution and growth, leveraging advancements in technology (Archapitakvong, 2020).

The digital revolution brought about by InsurTech is often described as “disruptive,” signaling a paradigm shift where only the robust and adaptable will thrive (McKinsey, 2017). The recent substantial losses incurred by insurance companies due to COVID-19 claims have intensified the need for strategic responses. Thailand’s insurance regulator views this as a call for mergers and acquisitions, fostering knowledge transfer within the industry. InsurTech emerges as a key enabler to accelerate these transformations, offering innovative solutions to navigate challenges and capitalize on opportunities (Sangnuan, 2023; The Star, 2022).

Specific variables within Insurtech:

With the rise of the Internet and the loss of face-to-face interaction, factors such as perceived risk and trust’s importance have grown in importance to researchers (Pavlou, 2003).

This comprehensive overview highlights the dynamic landscape of Insurtech in East Asia, emphasizing its pivotal role in reshaping the insurance industry, particularly in Thailand and driving innovation to meet evolving consumer demands and industry challenges.

From the theory and literature about InsurTech, the study’s authors formulated the final hypothesis, with the corresponding observed variables detailed in Table 1:

Purchase Intention (PI)

Purchase intention has been defined by Crosno et al. (2009) as the probability that a consumer will choose a product brand within a purchasing context. Ulbinaitė et al. (2013) have added that many factors influence insurance PI in Europe’s Lithuania, which states how much the consumer got for how much they paid. They were also concerned with the premium amounts and tried to reduce this if possible. Krajaechun and Praditbatuga (2019) used the Theory of Reasoned Action (TRA) model to discuss consumer insurance PI in Thailand. The authors noted that the consumer’s attitude toward the product was the most significant factor in PI for non-life insurance products. These findings were consistent with Yu (2022), whose study on word-of-mouth (WOM) insurance consumer communications determined that management should pay close attention to policyholder WOM as it helps strengthen CI and trust. Similarly, Guan et al. (2020) stated that the marketing mix influenced insurance PI, with the product being the most influential.

Finally, Table 1 presents the study’s constructs, observed variables supporting theory, and literature overview.

Research Methodology

Research Questions

The primary research questions addressed in this study are:

RQ1: Relationship Between Service Quality and Consumer Perceived Value:

Explore the strength and nature of the relationship between service quality and consumer perceived value.

RQ2: Relationship Between Service Quality and Insurance Technology:

Investigate the relationship between service quality and agency insurance technology, examining the impact of service quality on technological adoption.

RQ3: Relationship Between Service Quality and Purchase Intention:

Explore the relationship between service quality and consumer purchase intention, assessing the influence of service quality on the decision to purchase insurance.

RQ4: Corporate Image Influence on Consumer Perceived Value:

Examine the influence of corporate image on consumer perceived value, investigating the role of image in shaping consumer perceptions.

RQ5: Corporate Image Influence on Insurance Technology Adoption:

Investigate the impact of corporate image on agency insurance technology adoption, exploring the link between image and technological integration.

RQ6: Corporate Image Influence on Purchase Intention:

Explore the relationship between corporate image and consumer purchase intention, assessing the role of image in shaping the decision to purchase insurance.

RQ7: Perceived Value Influence on Insurance Technology Adoption:

Investigate the influence of perceived value on agency insurance technology adoption, examining how value perceptions drive technological adoption.

RQ8: Perceived Value Influence on Purchase Intention:

Explore the relationship between perceived value and consumer purchase intention, assessing the impact of value perceptions on the decision to purchase insurance.

RQ9: Insurance Technology Influence on Purchase Intention:

Examine the influence of insurance technology on consumer purchase intention, assessing the role of technological factors in shaping the decision-making process.

Figure 2 shows the nine hypotheses conceptualized from the related research questions, theory, and literature for Thai insurance company policies’ consumer purchase intention (PI).

Research Framework.

Research Design

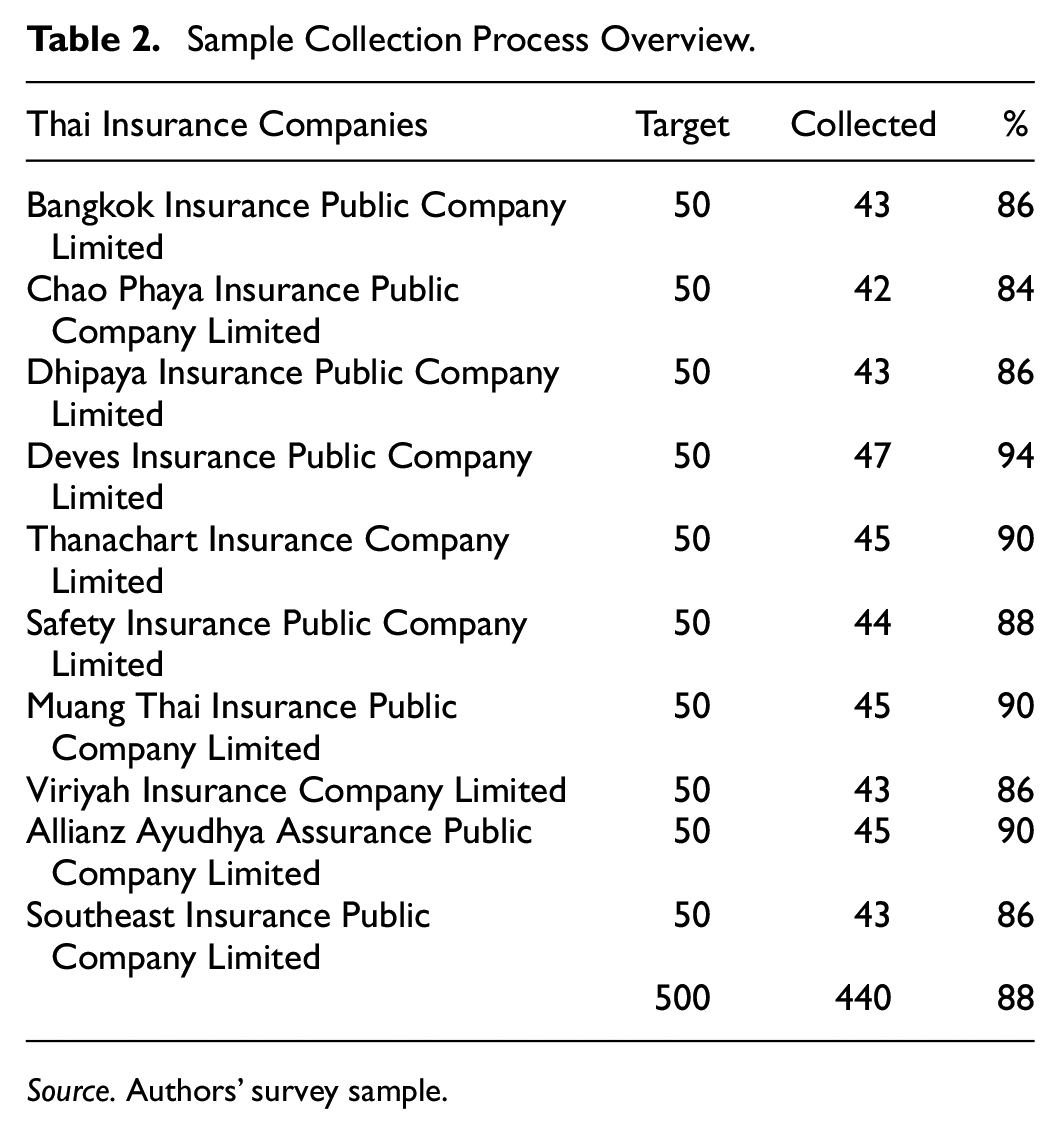

This study set out to investigate Thai working-age adults’ consumer insurance purchase behavior. For this study, the data were collected from individuals 21 years of age or older, as this group has finished their studies and usually moved out from the protection of their families and can support themselves and their close relationships financially. The population is Thai insurance agency consumers in 2022. According to data from Thailand’s Office of the Insurance Commission, there were 52 insurance agencies at the start of the study.

Study sample sizes are determined through various methods, with numerous studies adding their commentary and observations as to the statistically valid number. Therefore, the authors opted for the more straightforward determination method, a multiple of the observed variables. Even in using this method, studies can be found that state that as few as 10 questionnaires per observed variable are valid (Markus, 2012).

However, most studies today suggest multiples of 10 to 20 (Schumacker & Lomax, 2016), which depends on a model’s complexity. Therefore, the study’s initial target was 20 questionnaires for each of the study’s 25 observed variables (500). Upon completion, 88% of the target of 500 had been obtained (440 questionnaires), which represented a ratio of 17.6 (Table 2), which is at the higher end of suggested sample sizes for studies that use CFA/SEM methods (Kyriazos, 2018).

Sample Collection Process Overview.

Source. Authors’ survey sample.

The online survey data collection process was undertaken in January 2022. This study designed a Google form highlighting the purpose and reporting procedure of the study, which was used to collect informed consent from all respondents before survey participation. The online questionnaires were distributed to respondents after initial phone contact and by sharing the Google Form link of the questionnaire using social media (e.g., WhatsApp, Facebook, Line). A total of 440 valid responses were yielded for this study.

Finally, the authors used multi-stage random sampling as follows:

Simple random sampling was accomplished by drawing 10 companies out of 52 companies.

Then a systematic random draw was used to select five customer names from each of the remaining 10 insurance companies, for a total of 50 individuals each.

Survey Instrument

Data were gathered using self-administered questionnaires accessed from a Google Form link, with the questionnaire adopted from the literature. Part 1 contained items covering each consumer’s characteristics. These items were gender, age, education level, relationship status, occupation, and monthly income.

Questionnaire Parts 2 to 6 used a seven-level scale to assess each respondent’s opinions concerning five main topics, including Part 2’s service quality (SQ), Part 3’s corporate image (CI), Part 4’s perceived value (PV), and Part 5’s insurance technology (IT) on Part 6’s purchase intention (PI) of Thai consumer insurance policies. These five sections constituted the core of the questionnaire and employed a seven-level scale to gauge opinions. The scale was anchored with “participants’1” representing “strongly disagree” (ranging from 1.00 to 1.85) and “7” signifying “strongly agree” (6.11–7.00). The remaining five scale values were represented by “2” as “agree” (5.26–6.10), “3” as “somewhat agree” (4.41–5.25), “4” as “neutral or no opinion” (3.56–4.40), “5” as “somewhat disagree” (2.71–3.55), and “6” as “disagree” (1.86–2.70). However, to be more accurate, each questionnaire item was written with agreement language that allowed the respondent to better understand and interpret the response.

Latent Variable Modeling Using LISREL 9.1

In this study, the authors utilized LISREL 9.1 for latent variable modeling and SPSS 21 for descriptive statistics analysis. The choice of LISREL 9.1 was driven by its effectiveness in handling non-normal data distributions and small sample sizes, making it well-suited for modeling complex relationships (Jöreskog et al., 2016). Moreover, LISREL’s flexibility in accommodating models without strict assumptions about goodness of fit was particularly advantageous for our study. Concurrently, SPSS 21 was employed for descriptive statistics analysis due to its widespread use and familiarity in the field. While recognizing the availability of more recent versions, such as SPSS 27.0, we opted for SPSS 21 due to compatibility, consistency with existing practices, and university ownership of the software programs. Latent variable modeling is a robust statistical technique that assesses the relationships between latent constructs and their observed indicators (Deng & Yuan, 2023). Studies use the SEM method to investigate the causal model with the measurement model’s validity and reliability (Li et al., 2021).

The data analysis process using LISREL 9.1 involved a two-step approach. In the first step, we conducted a measurement model assessment to evaluate the reliability and validity of the latent constructs and their corresponding indicators (Gagne & Hancock, 2006). This step ensured that the measured variables accurately represented the underlying constructs in the model. Various fit indices, such as the CFI and the RMSEA, were used to evaluate the measurement model’s adequacy.

In the second step, we used the SEM to evaluate the latent variable construct relationships and test our research hypotheses. This analysis focused on determining the significance of the paths between latent variables and evaluating their causal effects. Model estimation was assessed using fit indices like the GFI and the SRMR to evaluate the overall model fit.

Furthermore, to assess the impact and relevance of each path within the model, we calculated coefficients of determination (R2), which Kline (1979) states is used to measure the variance proportion explained by exogenous variables on the endogenous variables. This analysis categorized the latent constructs based on their importance and performance, allowing us to identify which constructs were of relatively higher or lower importance and interpretation concerning the endogenous construct (Hair et al., 2021).

Ethics Clearance

Approval and ethics clearance for the study (Certificate No: EC-KMITL_66_023) were obtained from the Research Ethics Committee of King Mongkut’s Institute of Technology Ladkrabang (KMITL) before consultation with experts on the questionnaire’s design. Moreover, the study was performed following the Declaration of Helsinki. An informed consent form was given to each of the study’s experts, pilot-survey group, and primary study respondents, from which their signature was obtained. At every step, the anonymity of the participants was considered and ensured, with all interviewees informed that no information concerning their private information, such as name or passport number, would be used. These forms were collected, scanned, and secured on a password-protected thumb drive. The initial paper forms were then shredded.

Findings

Consumer Characteristics

In understanding consumer behavior within the insurance industry, demographic characteristics play a crucial role. Previous research has indicated that factors such as gender, age, education, marital status, occupation, and income can significantly impact individuals’ perceptions and decisions regarding insurance services (Boateng & Awunyor-Vitor, 2013; Mathur et al., 2015). Table 3 provides a snapshot of the demographic distribution in our study, laying the foundation for further exploration into how these characteristics might influence the variables under investigation.

Insurance Consumer Personal Characteristics.

Source. Authors’ analysis.

Table 3 details the consumer responses concerning their characteristics, indicating that 58.41% were men. The age groups of 31 to 40 and 41 to 50 were nearly equal, representing 30.91% and 29.77%, respectively. Education levels were also high, with 52.95% indicating they had obtained an undergraduate degree with another 23.86% indicating they had completed a post-graduate degree. Surprisingly, 42.50% were single, with only 16.59% still married. Concerning employment, 31.14% indicated they were working in private firms. Finally, 39.77% of those surveyed had monthly incomes over $1,240 (45,000 Thai baht).

CFA Exogenous & Endogenous Latent Variables

Before delving into the SEM analysis, we conducted a Confirmatory Factor Analysis (CFA) following the recommendations of Jöreskog et al. (2016). CFA, rooted in the works of Westen and Rosenthal (2003), serves as a foundational step to establish the reliability and validity of our latent constructs. The theoretical underpinnings of CFA lie in its ability to assess construct reliability (CR), discriminant validity (DV), and convergent validity (CV). Our results in Table 4 showcase strong AVEs and CR values, affirming the robustness of our measurement model.

Cronbach’s alphas, AVEs, Construct CRs, Factor Loadings, and R2s.

Source. Authors’ analysis.

CR reflects consumer responses, while CV measures the means. AVE values should be ≥0.5, and CR should be ≥ 0.6. Results in Table 4 show that AVEs were strong, ranging from 0.74 to 0.79, and CR values were from 0.93 to 0.96, signifying robust CV. Additionally, studies suggest standardized loadings should be statistically significant and appropriately high (acceptable ≥ .50 and good ≥ .707) (Pimdee, 2021). Finally, an R2 value ≥.75 is substantial, ≥.50 is moderate, and ≥.25 is weak (Mamun et al., 2021). These findings affirm strong CV and CR, validating the model’s suitability for SEM analysis.

Goodness-of-Fit (GoF) Analysis

The Goodness-of-Fit (GoF) analysis, depicted in Figure 3, serves as a critical evaluation of how well our SEM model aligns with established criteria and theoretical frameworks (Byrne, 2013; Hu & Bentler, 1999). The theoretical underpinnings of GoF analysis lie in its ability to validate the model against predefined criteria, ensuring that the proposed relationships are supported by the observed data. Our results affirm the harmony between our model and established criteria, reinforcing the theoretical soundness of our SEM approach (Byrne, 2013; Doğan, 2022; Hair et al., 2021; Hu & Bentler, 1999; Jöreskog et al., 2016; Schumacker & Lomax, 2016).

Consumer Insurance PI Model Goodness-of-Fit (GoF) Analysis.

Data Analysis Results

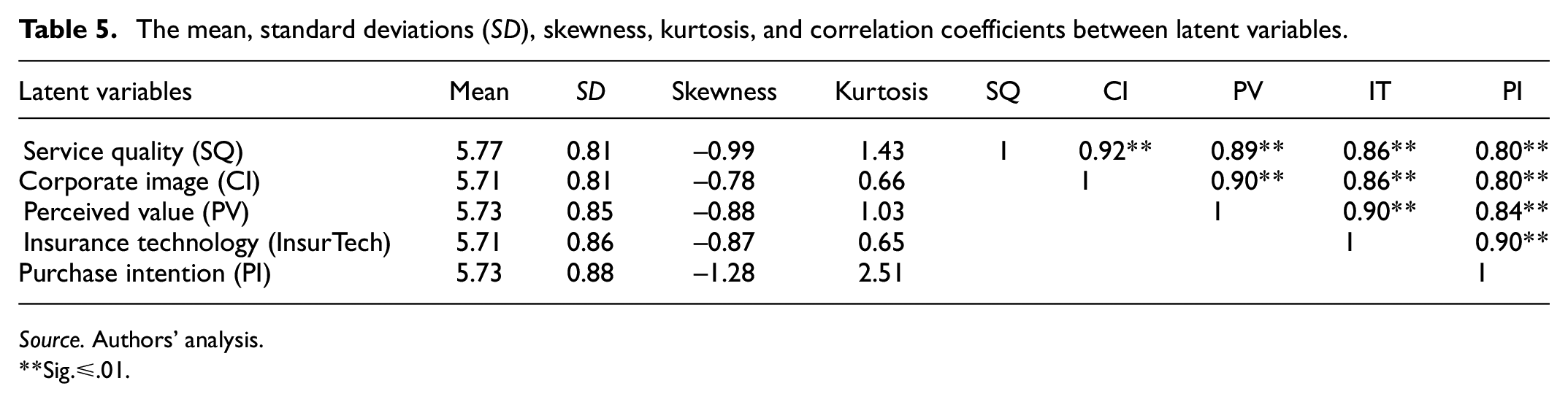

Moving beyond the technical details, the substantive findings of our analysis in Table 5 provide a comprehensive view of the correlation decomposition results, highlighting the relationships between latent variables. Notably, the robust correlation between service quality (SQ) and corporate image (CI) suggests a pivotal role of SQ in shaping CI. Building on this insight, Figure 4 visually represents the final Structural Equation Model (SEM), showcasing the significant direct and indirect effects among latent variables. These findings are in agreement with prior literature, underscoring the theoretical importance of our identified relationships.

The mean, standard deviations (SD), skewness, kurtosis, and correlation coefficients between latent variables.

Source. Authors’ analysis.

Sig.≤.01.

Final LISREL 9.1 SEM of variables influencing consumer insurance purchase intention.

Additionally, Table 5 shows the correlation decomposition results (Pimdee, 2020), with the interpretation of the analysis suggesting that the strongest interrelationship pair is SQ to CI with a coefficient of correlation = .92, **p ≤ .01. An interpretation of this data suggests that insurance agency service quality plays a very significant role in an insurance agency’ corporate image.

During the examination of the LISREL 9.10 skewness and kurtosis values, it is easier to interpret the results by knowing that the suggested values for skewness should be ≤ |2| and kurtosis ≤ |7| (Curran et al., 1996). Kim (2015) added that skewness and kurtosis p-values assess data normality. Therefore, Table 5 details the latent variables’ skewness values (−0.78 to −1.28) (≤ |2|) and kurtosis values (0.65 to 2.51) (≤ |7|), with all relationships determined to be significant at the p ≤ .01 level. Furthermore, internal consistency was achieved as all the variables were significantly higher than ≥0.70 (Hair et al., 2021).

Table 6 shows the direct effect (DE), indirect effect (IE), and total effects (TE) between the latent variables, confirming the positive effects of the SEM causal variables on the consumer insurance PI SEM, which, when combined, explain 76% of the variance in factors influencing purchase intention (R2). Finally, the constructs influencing purchase intention from highest to lowest were InsurTech (0.68), corporate image (0.54), perceived value (0.53), and service quality (0.34) were all determined to affect purchase intention.

Standardized SEM coefficients of influence of variables influencing PI.

Source. Authors’ analysis.

Sig. ≤ .05. **Sig. ≤ .01.

The TE represents the overall impact of a predictor variable on an outcome variable, considering both the DE and IEs. It quantifies the TE of a variable on another, considering both the immediate influence and the influence mediated through other variables. Researchers use TEs to understand the comprehensive impact of one variable on another, capturing both the direct and indirect pathways. DE, IE, and TE are essential in establishing a model’s causal relationships, which help researchers identify the presence of an association between variables and whether it is direct or mediated.

Table 7 and Figure 4 show the results from the SEM analysis. Seven of the nine conceptualized hypotheses were determined to be consistent with the data and supported.

Results of Research Hypothesis Testing.

Source. Authors’ analysis.

Note. coef. = coefficient of determination.

Sig. ≤ .05, **Sig. ≤ .01.

Discussion

In synthesizing our results, it is evident that the interplay between Service Quality (SQ), Corporate Image (CI), Perceived Value (PV), and Insurance Technology (InsurTech) significantly influences consumer Purchase Intention (PI). Notably, the direct and indirect effects identified in Table 7 highlight the dynamics within our model, shedding light on the comprehensive impact of each variable on consumer behavior. These insights contribute to the ongoing theoretical discussions (Table 1), reinforcing the theoretical foundations of our study.

From the research to develop a structural equation model of variables that influence Thai insurance consumer purchase intention, it was determined that all the causal variables in the model positively influenced guest purchase intention. These variables can explain 76% of the variance in factors influencing purchase intention (R2). When the order of latent variable importance was reviewed, insurance technology (InsurTech) (TE = 0.68) was judged most important. This was followed by corporate image (CI), perceived value (PV), and service quality (SQ), with total effect (TE) values of 0.54, 0.53, and 0.34, respectively.

Furthermore, the descriptive statistics analysis of the five latent variables showed that the questionnaire items for service quality (mean = 5.77, SD = 0.81) found significant agreement from the consumer insurance buyer respondents (Table 8).

Descriptive Statistics Analysis Results of the Latent Variables.

Source. Authors’ data analysis.

Note. 6 = “mostly agree” (5.26–6.10).

Service Quality (SQ) Hypotheses and Descriptive Statistics Testing Results

Service quality hypotheses testing found that two of the three conceptualized hypotheses were supported, with H1’s relationship between service quality and consumer perceived value being weak but positive (r = .25, t-test = 2.30, p ≤ .05). The same was true for H2’s relationship between service quality and insurance technology (r = .29, t-test = 3.12, p ≤ .01).

However, H3’s relationship between service quality and purchase intention was unsupported as the correlation coefficient (r) for the relationship between service quality (SQ) and consumer purchase intention (PI) was very low (r = .01), the t-test value is extremely low (t-test = .10), and the p-value was not significant (p > .05). The low correlation indicates that variations in service quality are not strongly associated with variations in consumer purchase intention. The findings imply that factors other than service quality may play a more influential role in shaping consumer purchase intentions in the context of the insurance industry under consideration.

This is consistent with Ramij (2021) who has alternatively reported that in Bangladesh, consumers who purchase insurance are motivated by an individual’s dependent number, type of work, and their monthly salary. However, age, education, and gender had no significant impact on life insurance policy buying decisions. Similarly, Chimedtseren and Safari (2016) noted that service design and service delivery were key components in insurance purchase intention.

Abdur Rehman et al. (2021) have also observed that positive perceptions of corporate service quality are achieved through reliability, tangibility, and personalization in Malaysia. Marcos and Coelho (2022) have added that service quality has a direct relationships with perceived value and satisfaction.

Moreover, from the descriptive statistics analysis of the five observed variables, it was shown that the questionnaire items for SQ4 were judged the strongest (provided services) (mean = 5.83, SD = 0.90). This was followed by SQ3’s data standards (mean = 5.81, SD = 0.89). Overall, all five aspects for SQ’s items were “mostly agreed” to by the consumer respondents (mean = 5.77, SD = 0.81).

Corporate Image (CI) Hypotheses and Descriptive Statistics Testing Results

Corporate image hypotheses testing found that two of the three conceptualized hypotheses were supported, with H1’s relationship between corporate image and perceived value being the strongest of the nine conceptualized hypotheses (r = .71, t-test = 6.33, p ≤ .01). However, H2’s relationship between CI and IT (r = .23, t-test = 1.98, p ≤ .05) was weak but positive. Unsupported was H6’s relationship between corporate image and PI (r = .01, t-test = 0.05).

These findings are also consistent with C. C. Chen et al. (2021), who investigated the role of CSR and corporate image during times of crisis (e.g., Covid-19). The authors found that economic, legal, and ethical CSR significantly impacted corporate image during difficult times. Additionally, the relationship between corporate image and purchase intention in the context of consumer insurance can vary based on several factors, and research findings may differ across different regions, including Thailand. In some cases, the corporate image may not strongly influence purchase intention in the consumer insurance sector due to the complexity of the decision-making process and the influence of other factors such as product features, pricing, and trust in the insurance provider.

While word of mouth, direct referrals, and friend feedback were widely used to evaluate different choices before the digital era, online recommendations, opinions from influencers, product ratings, anonymous reviews, or customer testimonials are now critical for consumers to make their final decisions (Miklošík, 2015), thus reducing the importance and need for corporate image (H6’s rejection).

Moreover, from the descriptive statistics analysis of the five observed variables, it was shown that the questionnaire items for CI2 were judged the strongest (social responsibility) (mean = 5.76, SD = 0.84). This was followed by CI1’s advertising (mean = 5.72, SD = 0.87). Overall, all five aspects for CI’s items were “mostly agreed” to by the consumer respondents (mean = 5.71, SD = 0.81).

Perceived Value (PV) Hypotheses and Descriptive Statistics Testing Results

Perceived value hypotheses testing found that both conceptualized hypotheses were supported, with H7’s relationship between perceived value and IT being moderately strong (r = .47, t-test = 5.75, p ≤ .01). However, H8’s relationship between perceived value and PI was weak but positive (r = .21, t-test = 2.06, p ≤ .05). These findings are consistent with a study from Malaysia in which Abdelfattah et al. (2015) wrote that healthcare insurance consumers are influenced by SQ, followed by perceived value in insurance service provider loyalty. Within Thailand’s automotive industry, Dhasan and Aryupong (2019) have observed that perceived value operates as a multidimensional construct consisting of the product’s quality (cognitive perceived value), service quality (affective PV), and price fairness (cognitive PV). These factors then predict customer engagement and loyalty.

Moreover, from the descriptive statistics analysis of the five observed variables, it was shown that the questionnaire items for PV5 were judged the strongest (perceived value) (mean = 5.78, SD = 0.91). This was followed by PV2’s expectations (mean = 5.76, SD = 0.93). Overall, all five aspects for PV’s items were “mostly agreed” to by the consumer respondents (mean = 5.73, SD = 0.85).

Insurance Technology (InsurTech) Hypothesis and Descriptive Statistics Testing Results

Implementing technological changes, particularly in the realm of InsurTech, emerges as a significant factor influencing the adoption of new technologies and enhancing competition within technological sectors such as healthcare and the related insurance sector (Bansal et al., 2023) The study’s hypothesis testing (InsurTech hypothesis, H9) reveals a moderately strong conceptual relationship between InsurTech and consumer purchase intention (r = .68, t-test = 4.32, p ≤ .01).

This finding aligns with existing research, such as the work conducted by Chang and Lee (2020) in Taiwan, who established a significant positive impact of life insurance service innovation on word-of-mouth (WOM) and behavioral intention. Similarly, Khatoon et al. (2020) demonstrated in Qatar that the quality of e-banking services significantly contributes to consumer satisfaction and serves as a motivator for retaining long-term and satisfied banking clients. At the regional level, Bansal and Singh (2021) have stated that within the six-member Gulf Cooperation Council (GCC), insurers are the next critical component of the financial sector as these companies play a crucial role in each country’s economic development by doing risk transfer. They minimize the risk exposure on corporates, allowing banks to provide capital at a lower cost and help in better allocation of capital and asset protection.

Reinforcing these observations, Archapitakvong’s (2020) study on health insurance purchase intention in Thailand underscores the trend of insurance consumers opting for online channels and exercising decision-making power. Notably, consumers actively search for health insurance policies in a specific price range ($138 to $275). The disruptive nature of InsurTech, crucial for sustaining or gaining a competitive advantage, has also been emphasized by Bughin et al. (2017), while Yao et al. (2007) reported that trust although a predominant factor for insurance agency clients, is usually associated with big firms as the small firms are more susceptible to insolvency.

Further supporting the significance of InsurTech, the descriptive statistics analysis of the five observed variables indicates that consumer responses to IT1 (technology innovation) were particularly strong (mean = 5.76, SD = 0.88). Additionally, IT4’s safety (mean = 5.75, SD = 1.03) and IT5’s system performance (mean = 5.74, SD = 1.00) received high ratings. Overall, consumers “mostly agreed” with all five aspects of InsurTech (mean = 5.71, SD = 0.86). This highlights the considerable impact and positive reception of technological innovations in the insurance sector.

Purchase Intention (PI) Descriptive Statistics Testing Results

The descriptive statistics analysis of the five observed variables showed that the questionnaire items for PI1 were judged the strongest (intention) (mean = 5.75, SD = 0.98). PI2’s planning followed this (mean = 5.75, SD = 1.03) and PI5’s loyalty (mean = 5.74, SD = 1.01). Overall, all five aspects of purchase intention items were “mostly agreed” to by the consumer respondents (mean = 5.73, SD = 0.88).

Conclusion

In conclusion, this study significantly advances our understanding of the nuanced factors shaping the purchase intentions of Thai consumers regarding insurance policies. By delving into the intricate interplay of service quality (SQ), corporate image (CI), perceived value (PV), and insurance technology (InsurTech), we contribute valuable insights to the field. The comprehensive quantitative approach, involving a diverse sample of 440 consumers across 10 Thai insurance agencies, allowed us to extract meaningful patterns and relationships.

Employing advanced statistical tools, including structural equation modeling (SEM) and descriptive statistics analysis, our findings underscore the pivotal roles played by InsurTech (0.68), corporate image (0.54), perceived value (0.53), and service quality (0.34) in jointly explaining a substantial 76% of the variance in purchase intention (R2). This not only affirms the relevance of these constructs but also emphasizes their interconnected influence on consumer decision-making in the insurance landscape.

Of particular note is the strong empirical support for seven out of nine hypotheses, with the corporate image-perceived value relationship emerging as a standout, closely followed by the connection between perceived value and insurance technology. However, the service quality and corporate image variables do not have a direct influence on purchase intention, but have an indirect influence through perceived value and Insurtech. Therefore, the insurance business should give more importance to promoting perceived value and Insurtech than service quality and corporate image. These empirical validations ground our conclusions in concrete evidence, offering a foundation for future research and practical applications within the insurance industry.

Moreover, our study extends beyond the immediate findings to provide post-COVID-19 insights into consumer behaviors in the Asian insurance market. In recognizing the enduring impacts of the global health crisis, our research goes beyond the traditional scope, offering practical implications for policymakers and regulators. The dynamism of consumer habits and expectations post-pandemic is paramount, and our study urges insurance agencies to adapt strategically.

Implications and Suggestions

Navigating the Post-COVID-19 Landscape in the Thai Insurance Industry

The findings of this study not only shed light on the current state of the Thai insurance industry but also offer nuanced insights that can significantly impact the strategies of government regulatory agencies and insurance providers, particularly in the aftermath of the COVID-19 pandemic. This global health crisis has not only disrupted daily life but has also left an indelible mark on the financial and insurance sectors, with several agencies in Thailand experiencing notable losses and, in unfortunate instances, closure.

The study underscores the pivotal role that consumer habits and perceptions play in shaping purchase intentions, especially in the altered landscape post-COVID-19. Insurance agencies need to recognize that consumers, now more conscious of their health and financial security, harbor different priorities and expectations. The significance of factors such as service quality, corporate image, perceived value, and insurance technology (InsurTech) in influencing purchase intentions cannot be overstated.

Recommendation: Insurers are strongly urged to amplify their focus on online channels, recognizing the shifting consumer behavior toward digital interactions. Additionally, there’s a call for innovative and creative policy customization options, allowing consumers to tailor insurance products according to their unique needs and preferences (Archapitakvong, 2020).

In light of the evolving consumer dynamics, insurance agencies must proactively adapt their strategies. Recognizing the newfound emphasis on health and financial security, agencies are encouraged to realign their services and products accordingly. This involves not only acknowledging the importance of SQ, CI, PV, and IT but also integrating these factors into a holistic approach that resonates with the changed consumer mindset.

Recommendation: Insurance agencies should consider adopting flexible and personalized policy options that reflect an understanding of the diverse needs of post-pandemic consumers. Embracing technological innovations to enhance service quality and streamline processes is imperative for staying competitive in this dynamic environment.

For regulatory bodies, the study signals the necessity of staying attuned to the changing dynamics within the insurance industry. The post-COVID-19 era demands a proactive approach to monitoring and adapting regulations to ensure their relevance and effectiveness. Regulatory bodies should prioritize staying informed about industry trends, soliciting consumer feedback, and keeping abreast of emerging technologies that are reshaping the insurance sector.

Recommendation: Regulatory bodies should consider establishing mechanisms for continuous feedback and collaboration with industry stakeholders. Regular assessments of regulatory frameworks should be conducted to ensure they align with the evolving needs of consumers and the rapidly advancing technological landscape.

The study’s insights serve as a roadmap for insurance agencies to not only weather the recent setbacks but to thrive in the post-pandemic era. By recognizing and adapting to changing consumer preferences, the industry can instigate a robust recovery and position itself for sustained growth.

Recommendations

Insurance agencies should view the post-COVID-19 period as an opportunity for innovation and resilience. Initiatives aimed at rebuilding consumer trust and confidence, coupled with strategic investments in technological advancements, can pave the way for a resilient and thriving industry.

In conclusion, the study’s implications and suggestions extend beyond immediate tactical adjustments; they offer a strategic blueprint for the Thai insurance industry to navigate the complexities of the post-COVID-19 landscape successfully. A collaborative effort between insurance agencies and regulatory bodies, informed by the study’s insights, is essential for fostering an environment of adaptability, innovation, and sustained growth.

Limitations

Some limitations of this study arise from its geographic scope. Data were collected solely from a single country, Thailand. Consequently, the use of the findings within an international context may be limited. It is essential to recognize that consumer behaviors, preferences, and insurance markets can vary significantly across countries and regions. Future research should replicate and extend these findings to a broader and more diverse set of nations to enhance the validity of the results.

Moreover, the data collection relied on social media platforms to share the online questionnaire link, which led to a self-selected group of respondents. This approach can introduce selection bias, as those who voluntarily participate may have unique characteristics that differ from the broader population. Inherent biases and preferences of social media users may affect the study’s results. Future research should consider more diverse data collection methods to reduce potential biases.

This study also focused on a specific set of constructs, including service quality (SQ), corporate image (CI), perceived value (PV), and insurance technology (IT) concerning purchase intention (PI). The limited number of constructs examined in this study may not capture the factors influencing consumer behavior in the insurance industry. For instance, Mamun et al. (2021) have suggested that education levels and rural versus urban consumers are essential to insurance PI. Future studies can consider additional variables.

Furthermore, Thai consumer behavior in the insurance industry can be affected by cultural and contextual factors unique to Thailand, which did not delve into certain psychological aspects, such as the role of social norms and consumer knowledge, which can significantly impact the intention to purchase insurance. Future research may benefit from employing different theoretical frameworks, such as the social exchange theory, to examine the psychological factors driving consumer behavior in the context of insurance purchases.

Despite these limitations, this study contributes valuable insights into the contributing factors influencing the purchase intentions of Thai consumer insurance policies. While it provides a foundation for understanding consumer behavior in the Thai insurance market, future research should address these limitations to provide a comprehensive understanding of the subject.

Footnotes

Acknowledgements

The authors would like to thank Ajarn Charlie for his invaluable contribution in editing and proofreading this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Approval and ethics clearance for the study (Certificate No: EC-KMITL_66_023) were obtained from the Research Ethics Committee of King Mongkut’s Institute of Technology Ladkrabang (KMITL) before consultation with experts on the questionnaire’s design. Moreover, the study was performed following the Declaration of Helsinki. An informed consent form was given to each of the study’s experts, pilot-survey group, and primary study’s respondents, from which their signature was obtained. At every step, the anonymity of the participants was considered and ensured, with all interviewees informed that no information concerning their private information, such as name or passport number, would be used. These forms were collected, scanned, and secured on a password-protected thumb drive. The initial paper forms were then shredded.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.