Abstract

Commercial insurance is an important risk management tool whose demand is affected by psychological factors. Music can promote consumption by evoking non-random emotional and behavioral responses in consumers . Using data from the China Comprehensive Social Survey, we examined the impact of music on commercial insurance purchase behavior using a probit model, an instrumental variable, propensity score matching, and other methods. The results indicate that music can significantly increase the probability of residents purchasing commercial medical insurance and endowment insurance by 2.569% and 1.869%, respectively. Regarding the mechanism, music encourages residents to purchase insurance by increasing their general cognition, risk cognition, insurance cognition, and ability to manage risk. Furthermore, an analysis of heterogeneity shows that music plays a greater role in promoting the aforementioned behavior of residents with lower levels of education, lower frequencies of social interaction, internet usage, an agricultural household registration, and of residents with jobs.

Keywords

Introduction

Do you purchase insurance to maximize your expected utility (as the expected utility theory holds)? Do you know that music in your daily life has a subtle effect on your mind and behavior? It is beneficial for residents to purchase insurance to manage risk. According to the expected utility theory in traditional economics, a rational economic man makes choices based on the maximum expected utility. Under the actuarial fairness assumption, consumers purchase insurance for full coverage against losses. However, the assumption of complete information cannot be satisfied in an actual insurance market. Philip Kotler, the father of modern marketing, suggests that consumers have a low cognition of insurance products. Moreover, customer behavior is affected by complex psychological mechanisms (Wanyan & Suo, 2016). Baicker et al. (2012) argue that the key to the success of health insurance coverage reform is to understand the behavioral barriers to purchasing insurance, which is likely governed by psychology as much as economics.

Music is more powerful than wisdom and philosophy, and is an effective means of expressing one’s thoughts. Music greatly influences psychology, and the study of music and psychology has developed into a relatively mature discipline. According to the psychological theory of music, psychological processes include emotion, cognition, and intention (Li, 2017). Intention is the initial stage of a person’s actions, and we believe that it is influenced by an individual’s underlying abilities, such as one’s intelligence quotient (IQ).

Music, Emotion, and Insurance

Several scholars have studied the influence of music worldwide. Music can reduce stress (de Witte et al., 2022), regulate emotions, and improve psychological health (Chanda & Levitin, 2013), quality of life (Daykin et al., 2018), and life satisfaction (Krause et al., 2020) by affecting the nervous, cortical, and subcortical systems (Hou et al., 2017), brain waves, brain biochemistry, immune system, heart rate, and blood pressure (Yehuda, 2011). Music therapy—a relatively mature discipline—is excellent for health treatment (Daykin et al., 2018). Hence, we suppose that these functions of music may have some influence on consumers’ behavior, as suggested by Pitthan and De Witte’s (2021) analysis of behavioral biases, concluding that mental accounting and narrow framing can lead to underinsurance, while “affection bias can be a double-edged sword toward insurance demand, which may cause over-insurance to events with big emotional connection, and underinsurance to events with none or low emotional connection.”

Music, Cognition, and Insurance

Studies have found a correlation between music and cognitive abilities. Music lessons can positively affect cognition, especially during childhood (Huttenlocher, 2002). Music can improve self-awareness (Chanda & Levitin, 2013) and the cognitive ability of patients with consciousness disorders (Grimm & Kreutz, 2021). For older adults with unimpaired cognitive abilities, music has a protective effect on cognition later in life (Fancourt et al., 2020). Families with higher cognitive abilities can effectively obtain information and make more reasonable asset allocation decisions (Christelis et al., 2010). Cognitive ability is a major factor in making an advantageous selection in the Medigap insurance market, as it affects individuals’ ability to evaluate the costs and benefits of purchasing insurance and the information about health risks (Fang et al., 2008). Scholars find that low demand for long-term care insurance arises from inadequate risk cognition (Zhou-Richter et al., 2010) and low cognition of insurance products (Boyer et al., 2017). The perception of health risk is not sufficiently objective and cannot be estimated properly because of errors and biases (Klein & Stefanek, 2007). Most people are overconfident about health risks, and this suppresses the demand for health insurance (H. L. Wei & Li, 2007). Myopic and overconfident individuals usually underestimate the risk probability when making insurance decisions (Pitthan & De Witte, 2021; H. L. Wei & Li, 2007).

Music, Intelligence Quotient, and Insurance

Many studies have investigated the relationship between music and IQ. Music training for children can improve their visual–spatial, language, and mathematical performance (Ho et al., 2003; Schellenberg, 2004; Schlaug et al., 2005) and IQ scores (Degé et al., 2011; Orsmond & Miller, 1999) in the long term. For example, the famous “Mozart effect,” first put forward by Francis Rauscher and Gordon Shaw, illustrates that college students who listened to Mozart’s sonata earned higher scores in Stanford university’s two-level intelligence tests compared with college students who did not listen to any music. Regarding the effect of IQ, previous literature suggests that people with a high IQ are more efficient and innovative in problem-solving tasks (Byington & Felps, 2010) and may be more perceptive about potential health risks (Fang et al., 2008). Burhan et al. (2015) found that financial numeracy, which is a sign of a high IQ, was an important factor in making an advantageous selection when purchasing insurance.

Music and Marketing

Many scholars have studied the influence of music on consumer behavior. These studies can help us better understand consumer emotions and their important role in consumer behavior (Bruner, 1990). Music is widely used in different markets, such as supermarkets and shopping malls, to elicit favorable customer responses (Bruner, 1990) by influencing their emotional state, cognition, and behavior (Jain & Bagdare, 2011; Sherman et al., 1997). Music marketing is a branch of sensory marketing that is more likely to trigger subconscious consumer awareness of a product than daily word of mouth (Krishna, 2012). It is such an important area of marketing research that a business magazine called “Marketing through Music” has been devoted to it (Bruner, 1990). Specifically, fast music is more effective than slow music in evoking positive purchase intentions (Pantoja & Borges, 2021).

Following previous studies, we deem that music may affect residents’ insurance demand through three paths: (1) emotions that trigger the subconscious consumption demand for insurance; (2) improvement of residents’ cognition level, which results in a better recognition of insurance products and one’s risk; and (3) improvement of residents’ IQ, which results in an enhanced risk management ability.

This study focuses on whether and how music can promote residents’ commercial insurance purchase behavior. According to existing research, music can affect factors such as residents’ emotion, cognition, and intelligence quotient. Consequently, these factors can affect residents’ risk cognition, insurance cognition, and risk management ability. Thus, music may encourage residents to manage risk through purchasing commercial insurance. The aforementioned effect of music on residents should be the result of its long-term impact on residents, which may be different from the existing music marketing theory.

Generally, listening to music is a habit. The frequency of listening to music at ordinary times can represent the “level” of music listening. In three waves of the Chinese General Social Survey (CGSS), the respondents were asked how often they listened to music at home in their spare time. Moreover, the CGSS also investigated residents’ purchase of commercial insurance, as well as the relevant information of residents’ cognitive ability and intelligence. Thus, the CGSS provides valuable data support for us to empirically study the impact of music on residents’ purchase of commercial insurance. Applying a probit model, an instrumental variable, propensity score matching, a placebo test, and other methods—based on data from the CGSS—we explore the relationship between music and residents’ commercial insurance purchase behavior. The results indicate that music significantly promotes this behavior.

This study contributes to the existing literature in three aspects: (1) to the best of our knowledge, it is the first study to empirically examine whether music promotes residents’ behavior of purchasing commercial insurance; (2) it explores how music affects this behavior through moderating and mediating effects; and (3) most of the previous related studies apply experimental methods to investigate the impact of music on residents’ consumption based on a small number of samples, while this study uses a large sample comprising 28 provinces (including municipalities and autonomous regions) of China. Hence, the representativeness of the sample is stronger, and the research results are more reliable.

The rest of the paper is structured as follows. Section 2 presents a background of the development of commercial insurance and music in China. Section 3 introduces the data and variables and provides the descriptive statistics. Section 4 explains the empirical strategy. Section 5 reports empirical results. Section 6 presents extended analyses, including analyses of endogenous problems, robustness of the results, the mechanism, and heterogeneity. Section 7 presents the discussion of the regression results. Section 8 presents the conclusion and policy implications. Lastly, Section 9 presents limitations and future research direction.

Background

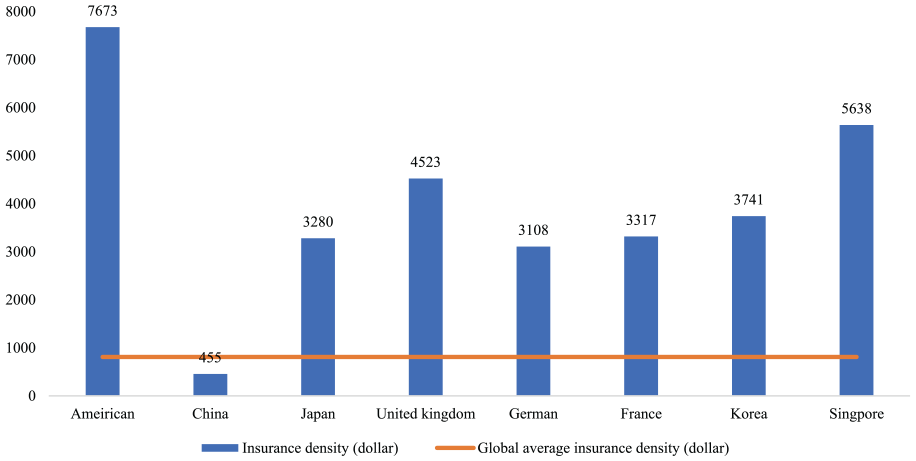

China’s economy has developed rapidly since its reform and opening up in 1978, during which commercial insurance started to develop gradually. This development played an important role in meeting individuals’ diversified security needs, and contributed to the improvement of China’s multi-level social security system. According to a report published by the Swiss Re Institute, China has become the second largest insurance market in the world since 2017. According to the latest data, premium income has risen to $655.9 billion in 2020, accounting for 10.43% of the global insurance market. However, the insurance depth and density in 2020 were $455 and 4.5%, respectively, much lower than the world average of $809 and 7.4%, respectively. These figures are much lower than of other countries with higher development levels of insurance (see Figures 1 and 2). What factors restrain the demand in China’s commercial insurance market?

Insurance density.

Insurance depth.

In China, psychological, cultural, and market factors have particularly significant impacts on the behavior of residents regarding commercial insurance purchase. Chinese people consider it a taboo to talk about death, disease, and disasters (H. L. Wei & You, 2012). Traditional Chinese culture holds that raising children to provide for the parents during their old age is the most reliable insurance (Chen, 2020). Moreover, the reputation of the insurance market is low because of non-compliant market behaviors, such as misleading sales and false publicity. The aforementioned psychological, cultural, and market factors lead to the prejudice or misrecognition of Chinese residents toward insurance and risk. Accordingly, residents usually avoid discussing insurance (Cui & Xie, 2014).

In China, the psychology of music can be traced back to the spring and autumn, and the Warring States period in the eighth century BC (Luo, 2000; Luo & Huang, 2008). Yue Ji is the earliest music theory work with a relatively complete system in China, in which the author thought that music had a great influence on people’s feelings, character, and will. Confucius, the founder of Confucianism, regarded music as the highest stage in life cultivation. He stated that music is a tool for consolidating the interests of the ruling class and advocated the combination of music and rites as a means of governing a country. Since the ancient times, music in China has experienced slow development and integration of Chinese and Western music. At present, China’s economic and social development is inseparable from music. According to the data published by China’s National Bureau of Statistics and Communication University of China, the total scale of China’s music industry in 2019 reached $56.5 billion, accounting for 0.4% of GDP or 0.74% of the added value of the tertiary industry, with more than 607 million digital music users in China. Moreover, the penetration rate of online music users reached 71.1%. Thus, music has become an indispensable part of residents’ daily lives, subtly affecting their emotions, cognition, intelligence, and consumption behavior. Can music improve residents’ cognition of risk and insurance and further increase their insurance consumption? To answer this question, it is necessary to empirically explore the intrinsic causality between music and residents’ purchases of commercial insurance.

Data and Variables

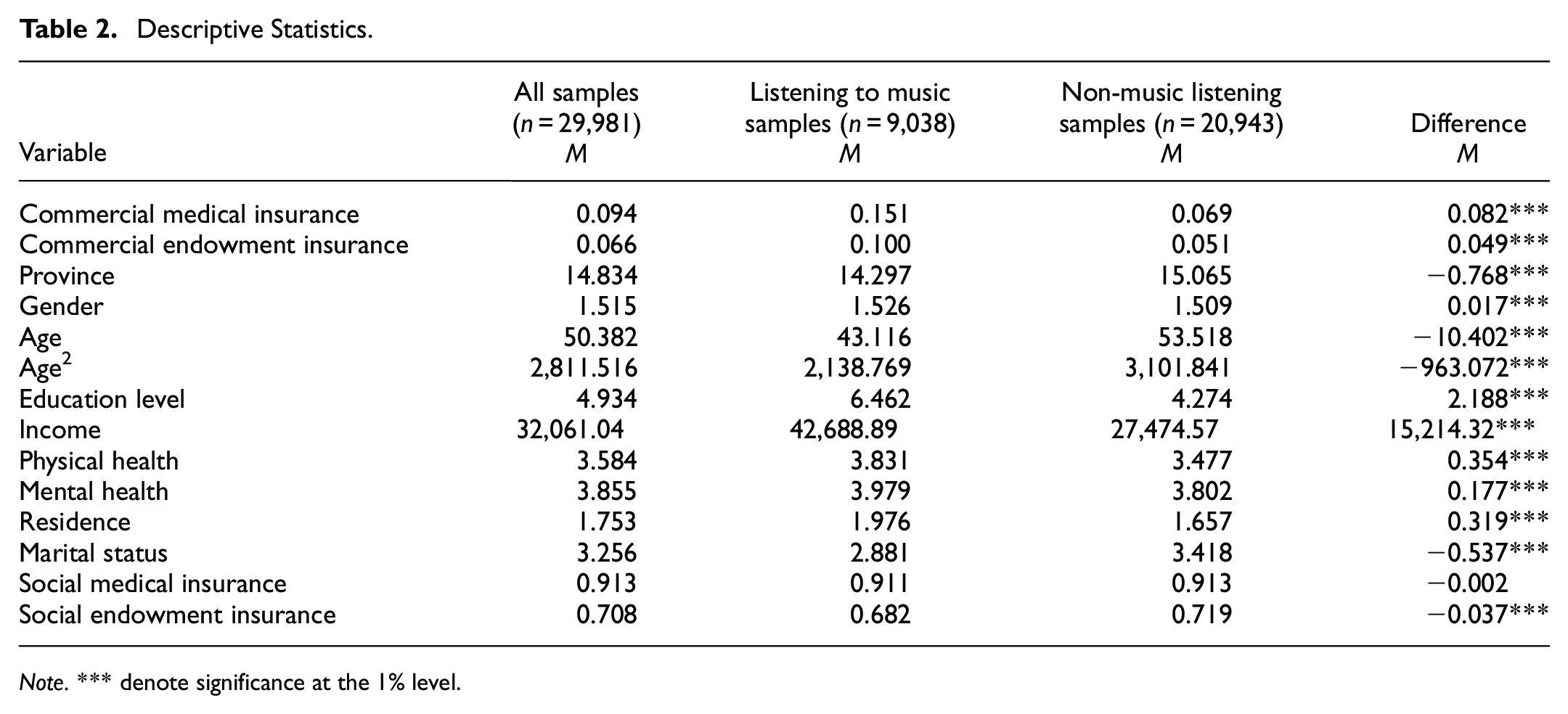

We use data from the CGSS, which is the first national, comprehensive, and continuous large-scale social survey project in China. The CGSS systematically and comprehensively collects data at multiple levels: society, community, family, and individual. The annual survey involves individuals in 125 counties (districts), 500 streets (townships and towns), 1,000 neighborhood (village) committees, and 10,000 families. This study uses the latest three-wave data (i.e., 2013, 2015, and 2017). After deleting the outliers and missing values, we obtain 29,981 valid samples.

Table 1 shows the dependent, independent, and control variables used in this study. To distinguish the effects of music on different types of commercial insurance, we consider two dependent variables: commercial medical insurance and commercial endowment insurance, both of which are binary variables. Respondents were asked whether they had purchased commercial medical insurance and commercial endowment insurance. A value of 1 is assigned if the individual has purchased commercial insurance and 0 otherwise. The independent variable is music, a binary variable. The respondents were asked whether they often listened to music at home during their spare time in the past year. A low (high) frequency is denoted by 0 (1).

Variable Definition.

Following the existing literature (Burhan et al., 2015; Fang et al., 2008; Gao & Wang, 2021), we control for other variables on demographics, health status, and social insurance participation, which may influence residents’ consumption of commercial insurance. Demographic variables include age and its square term, gender, education level, income, residence, and marital status. Health status variables include physical and mental health. When the independent variable is commercial medical insurance, we use social medical insurance as the control variable, whereas, when the independent variable is commercial endowment insurance, we use social endowment insurance as the control variable. We also control for the variables of province and year.

The mean value of commercial medical insurance from the Listening to music samples is 0.151, which is significantly larger than the value of 0.069 for the Non-music listening samples. The mean value of commercial endowment insurance for the samples Listening to music samples is 0.100, which is significantly larger than the value of 0.051 for the Non-music listening samples. From the descriptive statistics, we conclude to some extent that music can encourage residents to purchase commercial medical insurance and commercial endowment insurance. However, this conclusion needs to be verified by further empirical analyses (Table 2).

Descriptive Statistics.

Note. *** denote significance at the 1% level.

Empirical Strategy

Because the dependent variables in this study are binary variables, the probit model is established as the basic model:

The binary variable

Empirical Results

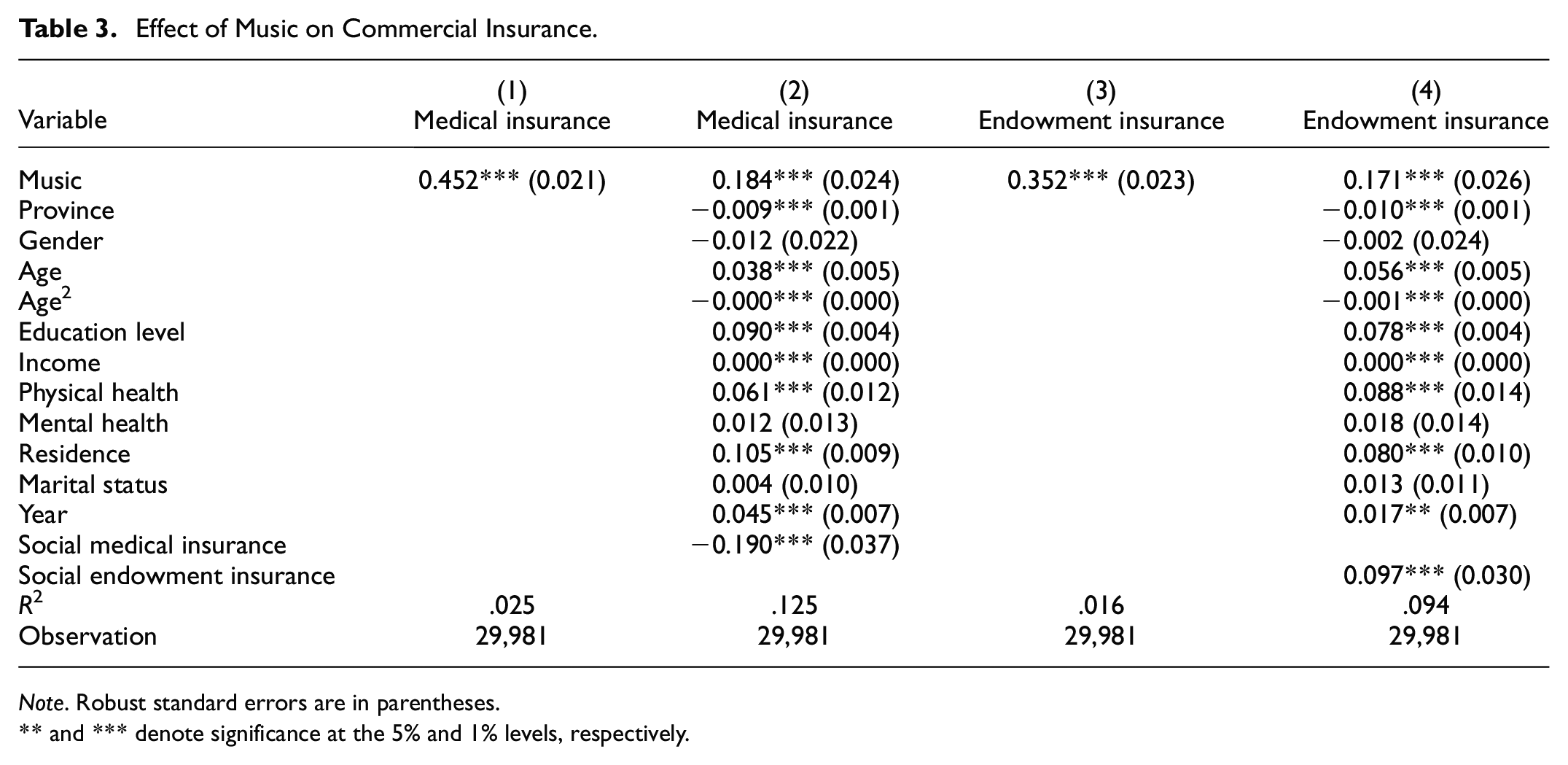

We examine the impact of music on residents’ purchases of commercial medical insurance and commercial endowment insurance. Table 3 shows the regression results. For commercial medical insurance, the regression result in Column (1) shows that the coefficient of the independent variable is significantly positive. When the control variables are added in Column (2), the coefficient of the independent variable is .184 and remains significant. After our calculation, the corresponding marginal effect is .02569, indicating that listening to music can significantly increase the probability that residents will purchase commercial medical insurance by 2.569%.

Effect of Music on Commercial Insurance.

Note. Robust standard errors are in parentheses.

and *** denote significance at the 5% and 1% levels, respectively.

For commercial endowment insurance, the regression result in Column (3) shows that the coefficient of the independent variable is significantly positive. When the control variables are added in Column (4), the coefficient of the independent variable is .171 and remains significant. After our calculation, the corresponding marginal effect is .01869, indicating that listening to music can increase the probability that residents will purchase commercial medical insurance by 1.869%.

Extended Analysis

Analysis of Endogenous Problem

To overcome potential endogeneity problems such as measurement error, omitted variables, and simultaneous causality in the basic regression, we apply instrumental variable regression and propensity score matching regression.

Instrumental Variable Regression

To solve the endogeneity problem, we take the average frequency level of listening to music in each province as an instrumental variable. Table 4 shows the regression results using this instrumental variable. The instrumental variable coefficient in the first-stage regression is significantly positive, and the F-statistic is 469.74 and 469.03 when the dependent variables are commercial medical insurance and commercial endowment insurance, respectively. The F-statistic is far greater than 10, indicating that the selection of the instrumental variable is effective. The results of the two-stage regression show that the coefficients of the independent variables are statistically, significantly positive, indicating that music can significantly promote residents’ purchase of commercial medical insurance and commercial endowment insurance.

Effect of Music on Commercial Insurance: Instrumental Variable Regression.

Note. Standard errors are in parentheses.

denote significance at the 1% level.

Propensity Score Matching Regression

We also apply propensity score matching regression to investigate the influence of residents’ purchase of commercial insurance. A single matching method may affect the regression results. Therefore, we use three matching methods—nearest neighbor matching, radius matching, and kernel matching. Moreover, the matching variables are all of the control variables in the basic regression. After sample matching, the standardized deviation of variables is significantly smaller, and the standardized deviation of all variables is less than 10%. This indicates that the matching results meet the balance requirement well. After matching, the fitting degree of the treatment group and the control group is better. Regression results in Table 5 show that music can promote residents to purchase commercial medical insurance endowment insurance.

Effect of Music on Commercial Insurance: Propensity Score Matching Regression.

Robustness Analysis

To test the robustness of the regression results, we conduct further analyses by applying three methods: adjusting the samples, changing the estimation method, and a placebo test.

Adjusting the Samples

Adjusting the samples is an important method for testing the robustness of the results. We use data from 2013, 2015, and 2017 to conduct a regression of the basic model. Table 6 shows the regression results. The coefficients of the independent variables are all significantly positive in the regression results, based on data from different years. Moreover, considering that insurance companies may reject the older population after reaching 65 years of age due to their health status, we conduct a regression based on the data excluding the samples of the older population (aged above 65 years), and the coefficients of independent variables all remain significantly positive.

Effect of Music on Commercial Insurance: Adjusting the Samples.

Note. Robust standard errors are in parentheses.

and *** denote significance at the 5% and 1% levels, respectively.

Changing the Estimation Method

Following Hu (2014), this study uses ordinary least squares (OLS) to estimate the basic model. The regression results in Columns (1) and (2) of Table 7 show that the coefficients of the independent variables are significantly positive. Because the independent variable in this study is a binary variable, the logistic model is used to test the robustness of the model. The regression results in Columns (3) and (4) show that the coefficients of the independent variable are significantly positive. Additionally, we use a Poisson model for a further analysis in Columns (5) and (6), and the coefficients of the independent variable in the regression results are significantly positive.

Effect of Music on Commercial Insurance: Changing the Estimation Method.

Note. Robust standard errors are in parentheses.

denotes significance at the 1% level.

Placebo Test

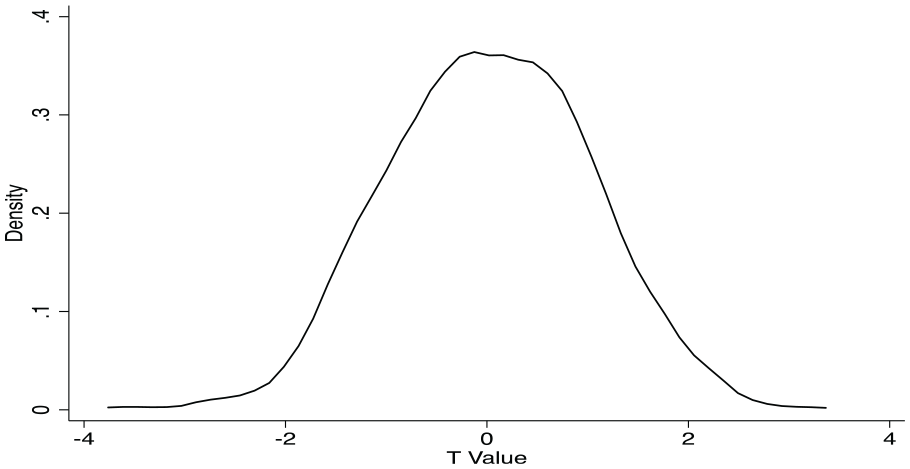

We apply a placebo test to analyze the robustness of the basic regression. When the independent variable is commercial medical insurance, the placebo test process is as follows: the number of valid samples is 29,981, including 9,038 samples with a high frequency of listening to music, and 20,943 samples with a low frequency of listening to music. We randomly select 9,038 samples from the whole sample and regard them as samples with a high frequency of listening to music and assign the corresponding independent variable, Music, a value of 1. We regard the remaining samples as samples with a low frequency of listening to music and assign the corresponding independent variable, Music, a value of 0. Then, probit regression is performed according to the basic regression model, and the T-values corresponding to the regression coefficients of the independent variable Music are saved. We repeat this operation 1,000 times, and then draw the saved probability density distribution of the T values. Figure 3 shows that in most regression results, the T-value of the music coefficient is smaller than that of the music coefficient in the basic regression results (7.756), and most of the music coefficients are at an insignificant level. This result indicates that listening to music frequently can significantly promote residents’ commercial medical insurance purchase behavior.

Placebo test (a).

When the independent variable is commercial endowment insurance, the placebo test is similar to the process discussed above. Figure 4 shows that the T-value of the music coefficient in most of the regression results is smaller than that of the music coefficient in the basic regression results (6.508), and most of the music coefficients are at an insignificant level. This result shows that, to a certain extent, listening to music frequently can significantly promote residents’ commercial endowment insurance purchase behavior.

Placebo test (b).

Mechanism Analysis

We investigate the potential channels through which music might influence commercial insurance consumption by applying a mediating effect model based on the bootstrap method of deviation correction. We conduct 500 repeated samplings with returns to obtain bootstrap samples similar to the original samples. By calculating the coefficient product of the sample and the estimated value of the total effect after each sampling, we obtain the nonparametric approximate sampling distribution of the intermediary effect. In this process, an intermediate effect confidence interval with 95% confidence is constructed between the 2.5th and 97.5th percentiles. Table 8 shows the results of the mediating effects for general cognition, risk cognition, and risk management ability. The definitions of the mediating variables used in this subsection are provided in the Appendix, Table A1.

Mediating Effect Analysis.

Note. ** and *** denote significance at the 5% and 1% levels, respectively.

As analyzed in the introduction, music helps increase residents’ cognition (Fancourt et al., 2020; Grimm & Kreutz, 2021; Huttenlocher, 2002), and a high level of cognition can promote residents’ commercial insurance purchase behavior. As such, music may encourage residents to purchase insurance by increasing their cognition. Language ability is an important aspect of cognition, and we use the ability to understand Mandarin and the ability to speak Mandarin to measure residents’General cognition (understand) and General cognition (speak), respectively. As shown in Table 8, the coefficients of the indirect effects are all significantly positive, and 0 is not included in the 95% confidence interval.

We further verify the above-mentioned hypothesis that music may increase residents’ consumption of insurance through risk cognition. Residents with a high level of risk cognition usually practice risk management more judiciously, for example, by improving the frequency of physical activity to manage health risk, and by applying investment strategies to manage their own financial risk. We use the frequency of physical exercise and risk investment status to measure residents’Risk cognition (exercise) and Risk cognition (investment), respectively. The coefficients of the indirect effects are all significantly positive, and 0 is not included in the 95% confidence interval. Therefore, we confirm the aforementioned assumption to a certain degree.

We assume that music may encourage residents to purchase commercial insurance through another channel, risk management. Music improves residents’ risk management ability, thereby encouraging their insurance purchase behavior. This study uses the ability to think of ways to deal with the challenges of life and work and the ability to think of ways to achieve goals to measure Risk management ability (challenge) and Risk management ability (goal), respectively. The coefficients of the indirect effects are all significantly positive, and 0 is not included in the 95% confidence interval.

Heterogeneity Analysis

This study further introduces the cross terms of education level, residence, social interaction frequency, internet usage frequency, job status, and music in the basic model to examine the heterogeneity of the impact of music on residents’ commercial insurance purchase behavior. The definitions of the moderating variables are provided in the Appendix, Table A1. According to the regression results in Table 9, music plays a greater role in promoting the insurance purchase behavior of residents with lower levels of education, an agricultural household registration, lower frequency of social interaction, lower frequency of internet usage, and those with jobs.

Heterogeneity Analysis.

Note. Robust standard errors are in parentheses.

, **, and *** denote significance at the 1%, 5%, and 10% levels, respectively.

Discussion

According to the regression results in Table 3, music significantly promotes residents’ purchases of commercial medical insurance and commercial endowment insurance, which is consistent with the conclusion obtained from the descriptive statistical analysis. Based on the instrumental variable regression results in Table 4, and the propensity score matching regression results in Table 5, we conclude that after overcoming potential endogeneity problems, music can continue to promote, to a certain extent, residents’ risk management through commercial insurance. A series of regression results in Tables 6 and 7, and the placebo test results in Figures 3 and 4, indicate that the research results are robust.

The regression results of the mediating effects in the mechanism analysis section, indicate that music can influence commercial insurance consumption by increasing residents’ general cognition, risk cognition, insurance cognition, and ability to manage risk. We therefore interpret that music has a significant role in promoting residents’ cognitive ability, such that residents with a higher cognitive ability may have a more objective risk cognition and a better understanding of insurance. Consequently, this may encourage residents to purchase commercial insurance.

Existing research has found that music can affect emotions (Chanda & Levitin, 2013), while different emotions—especially strong emotions—affect people’s risk cognition and have different effects on decision-making behavior (Johnson & Tversky, 1983; Lerner et al., 2003). In addition, music can improve people’s IQ scores (Degé et al., 2011; Orsmond & Miller, 1999) in the long term, and residents with a high IQ are likely to be more efficient and innovative in problem-solving tasks (Byington & Felps, 2010), facilitating their selection of insurance (Burhan et al., 2015). The ability to deal with risk is an important aspect of IQ, which can promote residents’ ability to manage risk, especially the ability to select insurance when reading insurance terms that are difficult to comprehend.

As we discussed in the heterogeneity analysis in Table 9, music plays a greater role in promoting the insurance purchase behavior of residents with lower levels of education, lower frequencies of social interaction, lower frequencies of internet usage, an agricultural household registration, and those with jobs. The main reasons for these results may be as follows.

First, residents with low cognition are more likely to be encouraged by music to purchase insurance. This is consistent with the findings of existing literature (Park & Young, 1986). Schneeweis et al. (2014), which finds that education has a positive causal effect on memory performance and could lead to long-term improvement of cognitive ability. Therefore, we conjecture that residents with lower levels of education and lower frequency of learning may have a low level of cognition. Similarly, the low rate of internet use (J. L. Wei et al., 2019) and low level of education in rural districts may affect the cognition of residents with an agricultural household registration. Residents with a low level of education may hold fewer insurance policies, and their insurance demands have not been encouraged. Therefore, music plays a greater role in promoting these residents’ consumption of commercial insurance.

Second, social interaction (D. Li et al., 2019) and internet usage (Brown & Goolsbee, 2002; Huang & Yang, 2020) can significantly encourage residents to purchase commercial insurance (D. Li et al., 2019). The factors that encourage residents to purchase commercial insurance usually play a greater role in promoting the insurance demand of residents with fewer insurance policies. We speculate that residents with less social interaction and less frequent internet usage may purchase fewer insurance policies, and their insurance demands have not yet been fully promoted. Thus, music can play a greater role in encouraging these residents to purchase commercial insurance.

Third, residents with jobs usually face more stress and risk, such as health risks, which may increase their risk cognition, as previously analyzed. In turn, this may promote residents to manage risk through various methods, such as the purchase of commercial insurance.

Conclusion and Policy Implications

Based on the data of the CGSS and our examination using the probit model, an instrumental variable, propensity score matching, placebo test, and other methods, this study analyzes whether music can encourage residents to purchase commercial insurance. The regression results show that music significantly encourages residents to purchase commercial medical insurance and commercial endowment insurance by 2.569% and 1.869%, respectively. After considering the endogenous problem, the research results do not change. A series of robustness analysis that include adjusting the samples, changing the estimation method, and a placebo test, shows that the regression results of the model are robust. Regarding the mechanism, music encourages residents to purchase commercial medical insurance and commercial endowment insurance by increasing their general cognition, risk cognition, insurance cognition, and ability to manage risk. Moreover, music plays a greater role in promoting residents with lower levels of education, an agricultural household registration, lower frequency of social interaction, lower frequency of internet usage, and those with jobs, to purchase commercial medical insurance and commercial endowment insurance.

This study provides theoretical support for improving residents’ risk protection levels by encouraging them to purchase commercial insurance. First, governments can take useful measures to boost the development of the music industry while effectively improving residents’ cognitive ability and risk management ability throughout their life by increasing their music listening frequency. Second, governments and other authorities can enhance the dissemination of insurance knowledge through various media to ensure that the public can better understand the function and value of insurance products. Third, insurance regulatory authorities need to strengthen the supervision of the insurance market to optimize its business environment. Insurance companies should continually strive to match the level of insurance supply with demand by providing innovative insurance products and improving the structure of the products.

Limitations and Future Research Direction

This study has some limitations. First, although the CGSS is a multi-period survey, it is not a tracing survey. Therefore, it does not allow us to apply better methods, such as the difference-in-differences estimation, to solve the potential endogeneity problems in this study. Second, the CGSS has relevant indicators only on whether the respondents have purchased commercial medical insurance or commercial endowment insurance. Therefore, we are unable to study the influence of music on residents’ purchase of other types of commercial insurance. Third, cognition includes mathematical skills, verbal fluency, and recall skills (Christelis et al., 2010), etc. However, limited by the available data, we only have indicators of verbal skills to measure the cognition level. Finally, we conjecture that music may affect the emotions that trigger the subconscious consumption demand for insurance. However, we have not obtained the necessary data to test it.

This study focuses on whether and how music can promote residents to manage risks by purchasing insurance. This should be the result of the long-term impact of music on people, which is different from the existing music marketing. This valuable and important issue deserves further study. In the future, we can further and more systematically, study the impact of music on residents’ risk perception and risk management behavior. This further exploration can promote the cross-study of musicology, psychology, and management theory, which are both interesting and meaningful. Furthermore, we can continue to study the impact of music on residents’ purchase of other types of insurance—property insurance, health insurance, casualty insurance—to explore the heterogeneity of music in promoting residents’ purchasing of different types of insurance. In addition, it is possible to study the macro level impact of the music industry development on the insurance industry. This is an important supplement to the micro-level study of relevant issues.

Footnotes

Appendix

Definitions of the Mediating and Moderating Variables.

| Variable | Variable definition |

|---|---|

| Mediating variables | |

| General cognition (understand) | The ability to understand Mandarin: good or very good = 1; cannot understand, poor, or general = 0 |

| General cognition (speak) | The ability to speak Mandarin: good or very good = 1; cannot understand, poor, or general = 0 |

| Risk cognition (exercise) | The frequency of physical activity: every day or several times per week = 1; several times per month, several times or less per year, or never = 0. |

| Risk cognition (investment) | The investment status (including stocks, funds, and real estate) of the respondent’s household: have investments = 1; otherwise = 0 |

| Risk management ability (challenge) | Based on the respondent’s response to: “If you find yourself in trouble, you can think of many ways to get out of it”—relatively consistent, quite consistent, or completely consistent = 1; completely inconsistent, quite inconsistent, relatively inconsistent, slightly inconsistent, or slightly consistent = 0 |

| Risk management ability (goal) | Based on the respondent’s response to: “I can think of many ways to achieve my recent goals”—relatively consistent, quite consistent, or completely consistent = 1; completely inconsistent, quite inconsistent, relatively inconsistent, slightly inconsistent, or slightly consistent = 0 |

| Moderating variables | |

| Education level | With no education = 1, private school = 2, primary school = 3, junior middle school = 4, vocational high school = 5, ordinary high school = 6, technical secondary school = 7, technical school = 8, college (adult higher education) = 9, college (formal higher education) = 10, undergraduate (adult higher education) = 11, undergraduate (formal higher education) = 12, and graduate or above = 13 |

| Residence | Agricultural household registration or resident household registration (formerly agricultural household registration) = 1; non-agricultural household registration or resident household registration (formerly non-agricultural household registration) = 0 |

| Social contact frequency | The frequency of getting together with relatives with whom the participant does not live: every day or several times per week = 1; several times per month, several times or less per year, or never = 0 |

| Internet usage frequency | The frequency of Internet use (including using the Internet via mobile phones): every day or several times per week = 1; several times per month, several times or less per year, or never = 0 |

| Job status | Whether the respondent has a job: has a job = 1; otherwise = 0 |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Research Foundation for Youth Scholars of the Beijing Technology and Business University, the Major Program Project of the National Social Science Foundation of China [grant number 13&ZD042], the Major Program Project of National Social Science Foundation of China [grant number 17ZDA090], and the National Social Science Foundation of China [grant number 22BRK037].