Abstract

This article aims to understand the impact of gender diversity on a firm’s equity volatility along with the moderating effect of chief executive officer (CEO) pay–performance sensitivity, institutional activism, and corporate social responsibility (CSR) activities. The sample consists of 200 South Asian health care firms over the period 2010 to 2018. After confirming the prevalence of endogeneity, we rely on the results of system generalized method of moments (GMM) rather than any static model. The results show that a higher representation of women on the board can mitigate the firm’s equity volatility. The findings of the study also purport that CEOs with higher pay–performance sensitivity exploit female directors to take the excessive risk, whereas institutional investors support the risk-averse behavior of these directors. However, we find no statistical evidence that CSR activities moderate the relationship between gender diversity and firm’s equity volatility. Our results theoretically support both stakeholder and agency perspectives that South Asian capital markets should enhance the representation of women on board to mitigate agency conflicts and to improve long-term firm’s sustainability.

Introduction

Increasing business complexity and constantly changing the corporate environment has shifted the attention of researchers and practitioners to appoint female directors on the corporate board as they effectively perform board functions (Chapple & Humphrey, 2014). A wide range of prior academic literature asserted that the participation of women on board is associated with higher equity capital, a higher level of liquid assets, better earnings quality, effective monitoring of managerial activities, and higher financial returns (Liao et al., 2015; Lückerath-Rovers, 2013; Sila et al., 2016; Srinidhi et al., 2011). It is also argued that female executives less likely lead a firm to financial distress due to their less volatile decisions (Faccio et al., 2016). Thus, a gender-diverse board strengthens the governance and decision-making quality of a firm by mitigating agency conflicts, managing business challenges, and efficiently understanding the concerns of different stakeholders (Abad et al., 2017; Gordini & Rancati, 2017; Herring, 2009; Liu et al., 2014). Indeed, “companies who fail to recruit and retain women—and ensure they have a pathway to leadership positions—undermine their long-term competitiveness” (Schwab, 2014, p. v).

Gender studies evaluate certain similarities and differences across nations and even within the country. Differences can be observed in terms of employment contracts, national legislative frameworks, and regional labor markets, whereas similarities include the low proportion of women in senior management positions, a gender–pay gap, and insecure employment compared with men (Strachan et al., 2015). Western developed countries have already recognized the essence of women representation on the board a long time ago. However, there are still deep-rooted discrimination and severe underrepresentation of women in decision-making administration in South Asia (Mehrotra & Kapoor, 2009). In Bangladesh, India, and Pakistan, women represent only 26% of the workforce and that too are low-status and low-paid jobs (F. Ali, 2010; Pio & Syed, 2013; Strachan et al., 2015). Owing to these gender prejudices and inequalities, studies in the Western context cannot be substantiated for South Asian markets. Therefore, it is important to assess how these South Asian women are influencing the key decisions of the firm.

A wide range of academic literature has focused on the association between women on the board and firm’s value or financial performance (Adusei et al., 2017; Campbell & Mínguez-Vera, 2008; Conyon & He, 2017; Kılıç & Kuzey, 2016; Low et al., 2015; Lückerath-Rovers, 2013; Wiley & Monllor-Tormos, 2018). However, there is inconclusive and lack of evidence on the relationship between gender diversity and a firm’s risk or equity volatility (Berger et al., 2014; L. H. Chen et al., 2019; Loukil & Yousfi, 2016). In addition, according to our best knowledge, prior studies have not given any attention to the South Asian region in this context despite its absolute exigency. In this study, we have purported that women on the board can effectively control and manage the firm’s equity volatility due to their capability of enhancing decision and governance quality.

Our study provides new statistical evidence on the relationship between gender diversity and the firm’s equity volatility of South Asian pharmaceutical firms. It is believed that this study will help in convincing policymakers to break through the glass ceiling to the upper level of management for South Asian women. We select the health care sector including pharmaceutical firms, biotechnology, medical equipment suppliers, biochemical firms, and other health care providers due to their direct influence on the country’s health system, quality of life, and well-being. These firms improve a patient’s well-being by creating value in services, vaccines, and medicines. Thus, the growth and sustainability of these firms are very essential for improving public health in a country. Another objective of this study is to examine certain moderators with the aforementioned relationship. Generally, shareholders have diversified portfolios and they want to maximize the returns from their limited liability. Accordingly, they enforce management and board members to choose risky investments (Easterbrook & Fischel, 1985). As discussed above, women on the board do not want to ruin their reputation by taking excessive risk, there are certain institutional mechanisms that influence their risk-taking decisions. For instance, some explicit executive compensation contracts compel chief executive officers (CEOs) to involve themselves in risky investments (Bolton et al., 2015; Coles et al., 2006). Thus, we believe that higher CEO pay–performance sensitivity influences women on the board to take more risky decisions, which may enhance the CEO’s compensation.

However, active institutional investors and corporate social responsibility (CSR) restrict managers to take excessive risks. Institutional investors manage equity volatility proficiently due to their effective monitoring role in restricting managers from degrading earnings quality (Koh, 2003). In addition, it is their fiduciary obligation to select less risky investments to protect their client’s wealth (Del Guercio, 1996). Thus, we believe that institutional activism acts as a strong supporting mechanism to fortify women’s optimal risk-taking decisions against external pressures. Similarly, Harjoto and Laksmana (2018) revealed that firms with a higher level of CSR could balance the interests of multiple shareholders due to which it reduces excessive risk avoidance and risk taking. Consequently, it is posited that CSR restricts female directors from taking excessive risk and supports their optimal risk-taking behavior. By instigating these moderating variables in our empirical model, our study can contribute a more detailed understanding of how the risk-taking behavior of women on board changes with the intervention of certain mechanisms.

The following section provides a concise literature review and development of hypotheses. Research methodology, data collection process, and empirical model are discussed in the “Research Design and Method” section. Results and robustness tests are interpreted in the “Empirical Results and Discussion” section. Finally, the conclusion and policy implications of our study are provided in the last section.

Literature Review and Hypotheses Development

Board gender diversity has become one of the important components of strong corporate governance. Regulatory bodies in many developed countries (such as Norway, Spain, France, Belgium, Italy, United Kingdom) have passed a law requiring large public listed corporations to appoint at least 30% to 40% women on the board. Most of these countries have also penalized firms for not complying with the gender diversity quota laws (Adams & Ferreira, 2009; Berger et al., 2014; Seierstad & Opsahl, 2011; Seierstad et al., 2017). However, the situation is different in South Asia due to lax gender quota laws. The underrepresentation of women on corporate boards in these countries can be observed from recent statistics. The proportion of female directors in Pakistani listed companies is only 6.4% (Securities and Exchange Commission of Pakistan [SECP], 2017), 15% in India (Pratap, 2017), and 22% in Sri Lanka (Devadas & Silva, 2017).

At large, traditional academic literature on gender diversity is descriptive (Sealy et al., 2017). Over the past decade, researchers examining the association between women on the board and firm performance empirically direct the attention of business leaders to appoint women in top-tier positions. However, Ferreira (2015) argued that women’s participation of the board should also be linked to other firm’s characteristics as financial performance is determined by many factors including creativity, innovation, and quality decision making. Gender-diverse boards are more efficient than male-dominant boards as females may bring more creative abstractions for some market or business segments, which eventually improve the quality of the board’s decisions (Singh & Vinnicombe, 2004). The higher representation of women on the board can also enhance the external prestige of an organization due to its compliance with a strong antidiscrimination policy. Female representation in top management can motivate the women in middle management and incorporates innovation in a firm’s strategy (Dezsö & Ross, 2012).

The advocates of prominent theories have considered gender diversity as an instrument to enhance problem-solving quality and efficient monitoring function. For instance, agency theorists argued that women on the board mitigate organizational inefficiencies by restricting managerial opportunism (Sabatier, 2015). Likewise foreign investors, ethnic minorities, and independent directors, women also have contemporary stances for complicated organizational aspects, which help in reducing informational partialities during strategy development (Westphal & Milton, 2000). From the agency-theoretic standpoint, diverse groups in a corporation create a more balanced board that restricts a specific group from dominating the key decisions (Hillman & Dalziel, 2003).

By further supporting the agency perspective, Adams and Ferreira (2009) argue that women on the board take neutral and independent decisions due to which they are more likely to fire CEOs for their poor performance. It is also believed that female directors restrict managers from distorting stock value by strengthening voluntary disclosure and transparency policy (Gul et al., 2011). Women on the board focus more on long-term performance due to which they reduce the variability and riskiness of a firm. Creditors and bondholders believe that their interests will be protected in the presence of female directors as they also mitigate agency conflicts and the probability of default through low cost of debt (Tanaka, 2014).

Stakeholder theory is also in favor of appointing board members from a diversified group. A broad set of stakeholders including large institutional investors and shareholder activists could pressurize firms to appoint women in senior management positions (Fields & Keys, 2003). Diversified boards assist in addressing shareholders’ needs and concerns in a complex societal environment (Chapple & Humphrey, 2014; Jizi, 2017). Female directors enhance board service roles and align their decisions with the interests of multiple stakeholders, which advance firms’ social welfare (Lückerath-Rovers, 2013; Mallin & Michelon, 2011). Women consider a wide range of environmental and societal issues while executing a strategy that improves their decision quality, and it is likely to be reflected in a firm’s risk (Colaco et al., 2011; Liao et al., 2015).

Most of the prior studies maintained normative analysis to study the influence of gender diversity of the firm’s risk or volatility, but empirical evidence on this linkage is lacking and inconclusive. For instance, Lenard et al. (2014) analyzed the firms from the RiskMetrics database over the period 2007 to 2011 to investigate the relationship between gender diversity and firm risk. They argued that women on the board influence firm risk by contributing to lower variability of the stock market return. Furthermore, Jizi and Nehme (2017) examined nonfinancial firms listed on the Financial Times Stock Exchange (FTSE) 350 index from the years 2008 to 2013. Using the generalized method of moments (GMM) and the one-step Arellano and Bond technique, the authors revealed that gender diversity reduces the firm’s equity volatility, especially in utilities, health care, consumer services, and consumer goods industry. In the same lines, Fauzi et al. (2017) also found women on the board a firm’s risk by using 30 Indonesian firms in their analysis. They also postulated that younger female CEOs with business degrees and overseas qualified are more likely to reduce the firm’s stock volatility.

However, while investigating the Standard & Poor (S&P) listed firms from 1997 to 2013, L. H. Chen et al. (2019) found a positive association of board gender diversity with the firm’s financial risk. However, they asserted that women on the board reduce the reputational risk of a firm by restricting aggressive tax strategies. Berger et al. (2014) also contended that female executives increase a bank’s portfolio risk. Sila et al. (2016) present slightly different evidence by examining U.S.-listed firms over the period 1996 to 2010. Their results suggest no significant association between gender diversity and the firm’s risk. They argued that the negative association can be explained by unobserved between-firm heterogeneous factors. Likewise, Loukil and Yousfi (2016) also did not find any statistically significant link between women on the board and propensity to take financial or strategic risk in Tunisian firms. Owing to the mixed evidence, further exploration of this relationship is needed especially in the South Asian context. As most of the aforementioned literature is more inclined toward the assertion that women on the board improve the quality of the decisions. Thus, we propose that board gender diversity is negatively associated with a firm’s equity volatility as a lower level of volatility is needed for organizational sustainability and long-term performance. Accordingly, we hypothesize the following:

Agency theory proposed that equity-based compensation should be encouraged to align the interests of executives (agents) with that of shareholders (principals) through which agency conflicts can be mitigated (Jensen & Meckling, 1976). Accordingly, equity-based compensation plans have adopted expeditiously from the 1990s to generate high returns for the shareholders (Coles et al., 2006; Murphy, 1999). However, it is a well-known phenomenon that aligning CEO’s incentives with performance to maximize shareholder wealth can lead to excessive risk-taking behavior (C. R. Chen et al., 2006; Cuñat & Guadalupe, 2009; Rajgopal & Shevlin, 2002). Consistent with risk shifting, DeFusco et al. (1990) argued that executive stock option plan announcements cause equity volatility to rise and bond prices to fall.

The financial instruments such as Vega (sensitivity of executive compensation to stock volatility) and delta (sensitivity of executive compensation to stock price) could encourage executives to maximize shareholders’ wealth through value creation investment decisions but the executives also get exposed to incentive risk. Under the alignment hypothesis, excessive incorporation of the restricted options and stocks in executive compensation plan may encourage to choose more risky investment projects, which enhance overall stock returns’ volatility. To gain excess remuneration, executives can manipulate stock prices through backdating or spring-loading (Aboody & Kasznik, 2000; Bebchuk & Fried, 2010). There is a stream of studies that demonstrate that high CEO pay–performance sensitivity may give rise to excessive firm’s volatility (Bebchuk & Fried, 2010; Bolton et al., 2015; Coles et al., 2006; Jensen & Murphy, 1990; Wiseman & Gomez-Mejia, 1998).

Generally, strong boards support only smart entrepreneurial risk with wise counsel and sensible oversight (Sonnenfeld et al., 2013). However, CEOs can influence the board’s monitoring ability and manipulate their decisions for their benefits (Adams et al., 2005). In light of this discussion, we propose that CEOs with high pay–performance sensitivity can also manipulate boards to approve the investment in risky ventures. Despite the risk-averse behavior of women on the board, CEOs may enforce them to favor risk-taking decisions with their compensation tightly linked with performance. Accordingly, we develop the hypotheses as below:

Corporate watchdogs and researchers have blamed certain shareholders for risk mismanagement in the wake of the financial crises. Consequently, financial deregulation allows institutional investors to become key players operating in capital markets (Diez-Esteban et al., 2014; Johnson et al., 2010). Institutional investors are believed to be stewards for the organizations due to their effective monitoring capability and active participation in the decision-making process to enhance their client’s returns (Abernethy et al., 2014; Croci et al., 2012; Ivanova, 2017). Consistent with the prudent-man law hypothesis, J. Cheng et al. (2011) argue that institutional investors do not elevate the riskiness of the investee firms. However, disaggregating institutional investors according to their active and passive roles can further specify their influence on important corporate decisions.

Strong corporate governance is one of the crucial goals of institutional investors due to which several institutions voluntarily engage themselves in shareholder activism (McCahery et al., 2016). Nielsen (2000) observed that institutional investors prefer to have voting rights with their long-term stakes as share prices significantly decline when they sell their share, resulting in significant losses to the institutions. Thus, studies posit that institutional activism is effective for underperforming corporations and improve the overall shareholder value (Caton et al., 2001; Lee & Park, 2009). Through board nomination, active financial institutions have long-term stakes in the firms and improve performance through efficient monitoring (Afza & Nazir, 2015). Ho (2016) also asserts that risk-related activism signifies a realignment of shareholder interests with core regulatory goals and long-term firm value. Based on the prior literature support, it can be suggested that active institutional investors sustain optimal risk-taking decisions in an organization and discourage women on the board to take value destructing risky investment decisions under any internal or external pressure. Consequently, we developed the hypotheses below:

CSR is also one of the effective control mechanisms to protect investor rights and balance the interests of multiple stakeholders (Mason & Simmons, 2014). High engagement of firms in CSR activities could improve shareholder’s well-being and value (Becchetti et al., 2015; Harjoto & Laksmana, 2018). While building the link between CSR and the firm’s risk taking, prior studies also rely on stakeholder theory. CSR activities can reduce a firm’s resource acquisition risk, build a strong relationship with the major stakeholders, and enhance the overall organizational prestige (Backhaus et al., 2002; Frooman, 1999). CSR activities are upmarket, which require executives to utilize the firm’s resources that could otherwise be used for risky investments. In tandem to this phenomenon, Harjoto and Laksmana (2018) argued that both risk avoidance and excessive risk-taking strategies can be restrained through CSR engagement. CSR engagement balances the interests of both noninvesting stakeholders (communities) and investing stakeholders (shareholders). Excessive risk avoidance makes the firms less attractive to potential investors and shareholders, whereas excessive risk taking neglects the needs of noninvesting these stakeholders due to which sustaining an optimal level of risk taking is mandatory.

Because women on the board also do not intend to elevate the firm’s equity volatility, firms with high CSR activities support them in their risk-averse decisions for the best interests of multiple shareholders. A wide range of literature has positively associated CSR with gender diversity (see Francoeur et al., 2008; Setó-Pamies, 2015; Yasser et al., 2017) as CSR creates unforeseen opportunities, attracts high-quality employees, and provides better access to value-creating resources. Thus, we hypothesized that firms with high CSR engagement give value to the decisions of minorities, and thereby act as a shield against the extraneous intervention of management in women’s decisions. We developed our hypothesis as below:

Research Design and Method

Data and Sample

The article seeks to explore the influence of gender diversity on a firm’s equity volatility along with the moderating role of CEO pay–performance sensitivity, institutional activism, and CSR in South Asian health care firms. After eliminating the incomplete and missing firm’s data, the sample consists of 12 health care firms from Bangladesh, 168 Indian firms, seven Pakistani firms, and 13 Sri Lankan firms over the period 2010 to 2018. This leaves us with an initial sample of 1,800 firm–year observations. Most of the South Asian countries have a weak legal environment and lack of transparency due to which the data of their respective listed firms are not available on DataStream. Therefore, we developed a hand-collected data set retrieved from annual reports and the company’s website. The observations with abnormal values were eliminated from the data set using Cook’s distance and leverage value. After excluding 87 outliers from the data set, the final unbalanced panel of 1,713 observations was retained.

Measures

The dependent variable of our study is the firm’s equity volatility. To estimate the volatility of time series, the generalized autoregressive conditional heteroskedasticity (GARCH) model developed by Bollerslev (1986) is considered to be the most efficient model. The GARCH(1, 1) model provides very accurate results and satisfactory explanations related to stock returns volatility as compared with any other complex model (Hansen & Lunde, 2005). The conditional variance is also a linear function of its lags and can be defined as follows:

Board gender diversity is the independent variable of this study. A wide range of studies has measured this variable by the percentage of women on the board (Adams & Ferreira, 2009; Campbell & Mínguez-Vera, 2008; Jizi & Nehme, 2017; Lenard et al., 2014). We have also adopted an alternative proxy to measure gender diversity, that is, 1 if there is a female board member in a given year, 0 otherwise. CEO pay–performance sensitivity is the first moderating variable, which is measured using Jensen and Murphy’s (1990) model. The model provides a sensitivity measure pertaining to the changes in the value of CEO remuneration to changes in the value of the shareholder’s wealth. With a little specification, Murphy (1999) proposed the following formula to estimate pay–performance sensitivity:

where β estimates the elasticity of the CEO pay–performance association by the percentage change in CEO remuneration with respect to the percentage change in shareholder value. To measure institutional activism, the study of Afza and Nazir (2015) is taken into consideration. The financial institution is considered active if it has a board nomination or representation. The third moderating variable of this study is CSR, which we measure using the index developed by M. H. Khan (2010). The scoring methodology is utilized to quantify the data measured by the theme. The index is the sum of information disclosed in each subcategory (donations, environmental issues, product and services, education sector, employee welfare, natural disaster). For each subcategory, 0 is assigned for nondisclosure and 1 is assigned for disclosing the information.

We also control for a set of the firm- and board-related factors to avoid model misspecification. A wide range of academic literature has controlled board size and board independence in corporate governance–related studies. Large board size reflects more discussion before making a decision, which leads to certain compromises. Therefore, it is associated with less variable stock returns and less risky outcomes (S. Cheng, 2008; Sah & Stiglitz, 1991). Prior studies also assert independent directors efficiently monitor the managerial opportunistic behavior, limit the chances of fraud, and improve the earnings quality; thus, their presence leads to a lower level of stock volatility (Jiraporn & Lee, 2017). For firm-specific control variables, we include firm size and profitability (return on assets [ROA]). Firms with a higher level of profitability have the ability to resist external shocks and certain financial problems, which encourage managers for further risk taking. However, large firms face less stock volatility because of the ability to access capital markets and diversify their investments (Baek et al., 2004).

Model Development

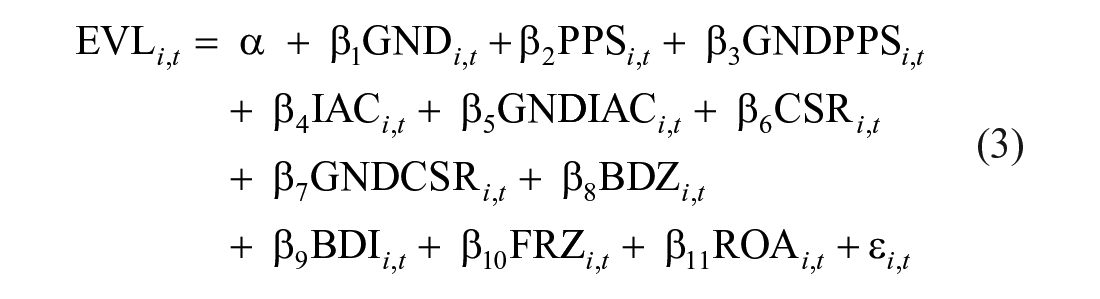

We use the following statistical model to test our proposed hypotheses:

where EVL = equity volatility, GND = board gender diversity, PPS = pay–performance sensitivity, GNDPPS = interaction of gender diversity with pay–performance sensitivity, IAC = institutional activism, GNDIAC = interaction of gender diversity with institutional activism, CSR = corporate social responsibility, GNDCSR = interaction of gender diversity with CSR, BDZ = board size, BDI = board independence, FRZ = firm size, ROA = return on assets, ε = error term, and i, t = for each firm and year. To mitigate the issue of correlated residuals, standard errors are clustered by firm (Petersen, 2009).

Building a causal link between equity volatility and gender diversity is intricated as firms choose board characteristics endogenously to suit their contracting and operating environment (Coles et al., 2006). Recent studies have revealed that the association between corporate governance mechanisms and firm’s risk or volatility is dynamic rather than static due to which endogeneity issues may emerge (L. H. Chen et al., 2019; Jizi & Nehme, 2017; Lenard et al., 2014; Sila et al., 2016). Traditional econometric models are not appropriate in the presence of endogeneity bias as fixed-effect estimation may suffer from downward bias, whereas the ordinary least squares (OLS) model provides upwardly biased estimates. How a firm’s equity volatility influences women on the board, CSR, and institutional activism is not the primary interest of this study but the issue of reverse causality cannot be ignored. There is a possibility that firms with a lower level of volatility may intentionally involve in CSR activities, choose more women on the board, align CEO’s compensation with performance, and promote institutional activism. To confirm the issue of endogeneity, we analyzed both static and dynamic OLS models. Equation 4 presents a static OLS model.

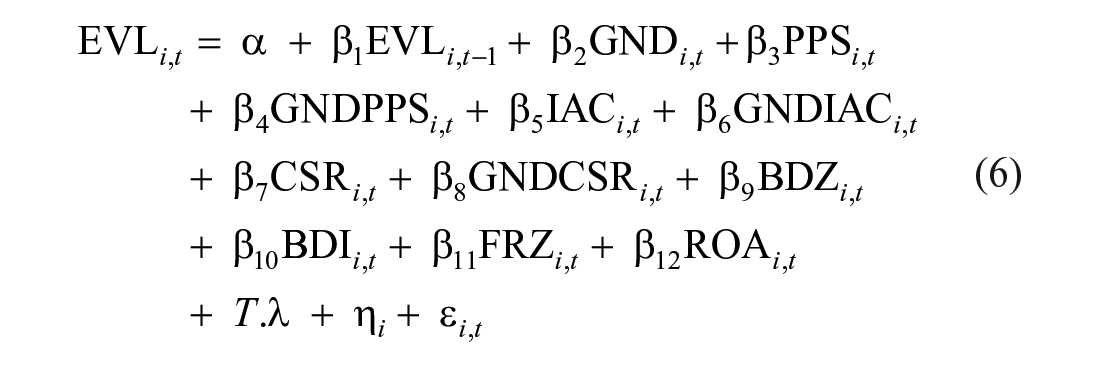

where X i,t denotes independent and moderating variables, Ω i,t is a vector of control variables, η i is unobserved time-invariant firm effects, and ε i,t signifies error term. For the dynamic OLS model, we include the lagged dependent variable in Equation 5 to confirm whether it is also one of the regressors.

The issue of reverse causality is detected as the adjusted R2 improves significantly in the dynamic OLS model (from 30%–50%). In addition, the influence of lagged EVL in the dynamic model also shows significant results, which further confirms the endogeneity bias (see Table 3). To further strengthen our assumptions, exogeneity among the variables was evaluated using the Wooldridge (2002) test by incorporating future values of the endogenous variables. Results were statistically significant for gender diversity (p = .034), pay–performance sensitivity (p = .002), and CSR (p = .004).

Thus, we explicitly treat gender diversity, CSR, and pay–performance sensitivity as endogenous variables and evaluate their possible determinants as instrumental variables. Following the previous literature review, we utilize foreign investors as an instrument for CSR (W. Ali et al., 2017), family ownership for board gender diversity (Saeed et al., 2016), and dividend policy for CEO pay–performance sensitivity (Yahya & Ghazali, 2017). Usually, including the lagged dependent variable as a regressor gives rise to the autocorrelation problem (Dezsö & Ross, 2012). Thus, we use the GMMs to account for autocorrelation and endogeneity issues simultaneously. Accordingly, we have rewritten our empirical model in Equation 6.

Empirical Results and Discussion

Descriptive statistics for dependent and explanatory variables are shown in Table 1. Equity volatility ranges from 0.04 to 0.36, with an average of 0.001. Overall, the volatility of the health care sector in South Asia is low as regulatory and monitoring bodies restrict managers from taking excessive risk after the financial crisis. Results also show that there is only a 9% representation of women on the board in South Asian capital markets. Board gender diversity is slightly higher in health care firms as compared with other firms. For instance, Saeed et al. (2017) found 5.9% of women on the board in India, whereas Wellalage and Locke (2013) report 7.4% of women representation on Sri Lankan boards.

Descriptive Statistics.

Note. CEO = chief executive officer; PPS = pay–performance sensitivity; CSR = corporate social responsibility; ROA = return on assets.

On average, CEO pay–performance sensitivity is 0.21, which shows positive but weak elasticity of CEO compensation with shareholder’s wealth in South Asian firms. These results can be supported with the meta-analysis by Yahya and Ghazali (2018) who also found a weak CEO pay–performance link in Asian capital markets. Furthermore, the board representation of financial institutions is 24%, which is lower than the average evaluated by Afza and Nazir (2015) in the context of the Pakistani capital market.

The disclosure of CSR activities ranges from 9.451 to 71.631, with an average of 21.32, which is higher than Bangladesh (22.3; A. Khan et al., 2013) but lower than Pakistan (60.79) (Lone et al., 2016) and India (47.43; Kansal et al., 2014). There are different methods to estimate the CSR disclosure index due to which extensive variation in results can be observed. In the case of control variables, there are eight board members on average and 39% independent nonexecutive directors on the boards of the South Asian health care industry.

The average firm size is 9.39, which is close to many prior studies in the South Asian context (see Lone et al., 2016). ROA in South Asia is also reported by Manrique and Martí-Ballester (2017; i.e., 10.23), which is very close to our results. Table 2 documents the Pearson correlation for the explanatory variable to identify whether there is any multicollinearity issue. Results show that there is no issue of multicollinearity as no correlation value is above .8 and no variance inflation factor (VIF) value is above 10.

Pearson Correlation Matrix.

Note. VIF = variance inflation factor; GND = board gender diversity; PPS = pay–performance sensitivity; IAC = institutional activism; CSR = corporate social responsibility; BDZ = board size; BDI = board independence; FRZ = firm size; ROA = return on assets.

p < .05.

Hypothesis Testing

To compare and select the most robust estimation model, we utilize OLS, fixed-effect, and system GMM econometric techniques. Table 3 reports that the results of fixed-effect estimation suffer from downward bias, whereas estimates of OLS are upwardly biased and inconsistent. In the presence of dynamic relationships, the static model cannot be utilized to provide robust estimates. However, the two-step system GMM deals with endogeneity efficiently and more appropriately for shorter panel data set (shorter T and larger N; Blundell & Bond, 1998; Bond, 2002). Stock et al. (2002) criticized the GMM estimator for weak instruments identification due to which we analyze certain instrumental validity tests suggested by Arellano and Bond (1991), that is, (a) the Hansen J test of overidentifying restriction and (b) the Arellano–Bond test for second-order serial correlation (AR(2)).

Regression Analysis.

Note. Values in parentheses are the estimated p values. Hansen J test refers to the overidentification test for the restrictions in GMM estimation. The AR(1) is the Wooldridge test for the first-order autocorrelation and the AR(2) test is the Arellano–Bond test for the existence of the second-order autocorrelation in the first differences of residuals. OLS = ordinary least squares; GMM = generalized method of moments; GND = board gender diversity; PPS = pay–performance sensitivity; IAC = institutional activism; CSR = corporate social responsibility; BDZ = board size; BDI = board independence; ROA = return on assets.

Indicates significance at the 10% levels. **Indicate significance at the 5% levels. ***Indicates significance at the 1% levels.

The Wooldridge first difference–based test for AR(1) suggests that there is a significant serial correlation in residuals; however, the Arellano–Bond test for second-order serial correlation accepts the null hypothesis that there is no autocorrelation, confirming the validity of instruments and system GMM model. In addition, the Hansen J test has yielded a p value of .533, suggesting that instruments used in the model are valid. As it is confirmed that the sys-GMM estimator is the most appropriate technique, we have interpreted our results for this model accordingly.

Results in Table 3 show that lagged equity volatility significantly explains the variation in current volatility (β = 0.007, p < .05) when the dynamic OLS technique is used; however, the potential endogeneity issue is mitigated through system GMM technique as 1-year lagged volatility coefficient is found to be insignificant (β = 0.002, p > .1). It is also evaluated that gender diversity 1 is significantly and negatively associated with equity volatility (β = −0.039, p < .05), which is supported by many prior studies (Fauzi et al., 2017; Jizi & Nehme, 2017; Lenard et al., 2014). We believe that despite a lower level of representation, South Asian women on the board can improve the quality of the board’s decisions (Singh & Vinnicombe, 2004), restrict managerial opportunism (Sabatier, 2015), take neutral and independent decisions to balance the interests of multiple shareholders (Liao et al., 2015; Lückerath-Rovers, 2013), and thereby, restrict excessive risk taking in a firm. In the light of system GMM estimates, we accept our first hypothesis.

However, we cannot accept our second hypothesis as there is no significant association of CEO pay–performance sensitivity with equity volatility (β = 0.103, p > .1). Our results are not consistent with prior studies that performance-based compensation contracts of CEOs lead to excessive risk-taking behavior (Bebchuk & Fried, 2010; Bolton et al., 2015; Coles et al., 2006). Nevertheless, they have the ability to influence the risk-taking decisions of a firm by manipulating board members. The evidence is statistically weak but significant that CEO PPS weakens the negative association between gender diversity and equity volatility (β = 0.001, p < .1), which leads to the acceptance of the third hypothesis. In line with the argument of Adams et al. (2005), we assert that self-interested CEOs can distort a board’s decision-making quality and manipulate them for their benefits. Specifically, in the South Asian health care firms, we proclaim that CEOs induced with risk-taking behavior may pressurize or exploit the women on the board to elevate the firm’s volatility to gain more compensation.

In reference to institutional activism, our results are also consistent with our proposition. A high proportion of active institutional investors also lead to lower variability in the firm’s equity. Statistical significance indicates that we can accept our fourth hypothesis (β = −2.557, p < .05). In tandem with assertions of prior studies, it can be argued that institutional activism can be utilized as an effective monitoring mechanism (Abernethy et al., 2014) and protect their long-term stakes by controlling the excessive risk taking in the investee firms (J. Cheng et al., 2011). Furthermore, we also reveal that active institutional investors support the risk aversion of women on the board. Results of the system GMM show that institutional activism strengthens the negative association between gender diversity and the firm’s volatility (β = −0.099, p < .05). Thus, the significance of the fifth hypothesis can also be confirmed. Nonetheless, results are not significant for our last two hypotheses.

Results are not supporting the tentative hypothesis that the relationship between CSR and firm’s equity volatility is significant (β = 0.026, p > .1) and it also does not moderate the relationship between gender diversity and equity volatility (β = 0.005, p > .1). Neither are our results consistent with previous literature, which found a statistically significant association CSR and firm risk (Albuquerque et al., 2018; Nguyen & Nguyen, 2015), nor do we anticipate that a higher level of CSR activities supports risk-averse behavior of women on the board. Last but not the last, it is evaluated that there is no significant association of board independence (β = −0.049, p > .1) and profitability (ROA; β = 0.194, p > .1) with firm’s volatility. However, larger boards elevate firm’s riskiness (β = 0.091, p < .1), whereas larger firms opt less risky strategies (β = −2.752, p < .1).

Conclusion and Policy Implications

This article investigated the potential influence of gender diversity on a firm’s equity volatility along with the moderating role of CEO pay–performance sensitivity, institutional activism, and CSR in South Asian health care firms. Our findings support the argument that a high representation of women on the board can mitigate the firm’s equity volatility. The estimates of system GMM also indicate that performance-adjusted compensation of CEOs does not directly influence the firm’s risk-taking decisions but they are able to manipulate and exploit female directors to elevate the firm’s riskiness to enhance their compensation. In line with the agency perspective, we find a significant and negative association of institutional activism and the firm’s volatility. Furthermore, it can act as a supporting mechanism in the favor of female directors’ risk-restraining decisions. Finally, we examine that CSR activities do not influence equity volatility and also do not moderate the link between gender diversity and firm’s equity volatility.

In light of this study’s results, it can be claimed that gender-diverse boards make decisions consistent with the interests of multiple shareholders and restrict managerial opportunism. Female directors are against the unnecessary elevation of a firm’s risk to improve organizational sustainability. Thereby, it is suggested that regulatory bodies in South Asian capital markets should promote and increase the women’s representation on the boards. It is also recommended that more efficient compensation structures for executives should be designed, which could retain the optimal level of risk taking in an organization. Institutional activism is also one of the effective monitoring tools to mitigate agency conflicts and excessive risk taking in a firm. South Asian firms should encourage the representation of a board member from financial institutions to protect the rights of minority shareholders. At this instance, CSR activities in South Asian economies have no direct or indirect influence over the firm’s key decisions such as risk taking. Therefore, it is also suggested that CSR activities should be enlarged up to a certain level where it could positively influence the firm’s value and its key decisions.

According to our best knowledge, this article has contributed to several research gaps in the field of corporate governance and finance. First, it is the first attempt to examine the association between gender diversity and the firm’s equity volatility (measured by GARCH) in the South Asian health care industry. Second, no prior study has introduced the moderating role of CEO pay–performance sensitivity, institutional activism, and CSR activities between the aforementioned relationship. Furthermore, most of the prior studies have relied on static models but we have unraveled the dynamic relationship between the concerning variables. Nonetheless, despite these theoretical and empirical contributions, our study is not free from certain limitations that can be covered by future studies.

This study is limited to the South Asian health care industry, so its results should be carefully generalized. Equity volatility and organizational structures vary from industry to industry; thus, future studies should compare and analyze other sectors in the South Asian capital markets. GARCH(1, 1) is a strong model to calculate volatility but does not identify the optimal level of a firm’s risk. Thus, future studies should test these variables with optimal risk taking as utilized by Harjoto and Laksmanan (2018) to draw a line between excessive risk-taking and risk-avoidance strategies. Finally, it is recommended that contemporary corporate governance mechanisms (such as CEO, audit committee, and board characteristics) should be incorporated as moderators to examine other restrictive or supporting mechanisms for female directors’ risk-averse behavior, which we were not able to investigate due to lack of financial reporting disclosure in South Asian capital markets.

Footnotes

Compliance With Ethical Standards

The authors received no specific funding for this work. This article does not contain any studies with human participants or animals performed by any of the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.