Abstract

Prior evidence that firm’s investment behavior is positively affected by its corporate social responsibility (CSR) disclosure, as one of the key CSR areas of the company, leaves unaddressed whether all kinds of disclosure have the same effect. Drawing on stakeholder theory, this study analyzes the issue in a more exhaustive way. A cross-sectional logistic regression model is used to test the hypothesized association, and the results imply that firms’ high (low)-quality disclosure regarding their engagement in CSR activities increases their chances of being from the investment-efficient (inefficient) group. The obtained results conclude that CSR reporting activity is not beneficial for companies unless a meaningful disclosure of sustainability information is made. Our results are robust to using alternative proxies for CSR disclosure quality. This study contributes to the scarce evidence on CSR reporting in Pakistan and provides a useful method for assessing quality of CSR reports.

Introduction

he rise of corporate scandals in Pakistan in the shape of exploitation of workers (Ashraf, 2018) and child labor (Delaney et al., 2017) is the reason behind corporate social responsibility (CSR) coming to the limelight in Pakistan. In addition, such kind of corporate scandals has compelled corporations to satisfy the needs of all stakeholders (Elias et al., 2004). From product and service quality to social behavior of companies, everything is under a tight scrutiny from the stakeholders. Moreover, there is an increased demand for firms to report publicly on different aspects of their CSR performance by the influencing stakeholders like international clients, international regulatory authorities, foreign investors, (Azizul Islam, 2008; Momin & Parker, 2013; Rahaman et al., 2004), and so on to catch any unethical practice employed by the firms. The recently evolved CSR forums in Pakistan like CSR Pakistan, NGOs like WWF, and CSR standards like OHSAS, ISO 14000, and so on are also encouraging companies to include CSR disclosure in their business policies (Ali & Frynas, 2018). CSR disclosure is the information provided by corporations in association to their policies, aspirations, and activities toward community, customers, environment, and employees (Gray et al., 1995). These disclosures come with a cost and need a considerable amount of time; however, management is usually not confident if the disclosures accomplish the anticipated goals of being informational. If the disclosure caters stakeholders’ informational need and helps them in making investment decision, then it should significantly increase the information symmetry in the market and consequently company’s financial performance (Chowdhury et al., 2016).

The literature shows that sustainability reporting possess potential to positively affect the investment behavior of firms (Hope & Thomas, 2008; McNichols & Stubben, 2008) by reducing the chances of adverse selection (Lambert et al., 2007) and improving corporate control mechanisms, which prevents managers from expropriating investors’ wealth (Fama & Jensen, 1983). In connection to this line of inquiry, Beretta and Bozzolan (2008) examined the quantity and quality of disclosures. It is demonstrated in research that disclosure quantity does not reflect disclosure quality adequately (Rezaee & Tuo, 2019). Recent researchers like Michelon et al. (2015) recommend to further study the area of CSR disclosures because of incomplete and non-credible information provided by firms in the name of CSR reporting. In connection to their recommendation, this article studies the relationship betweeen CSR disclosure quality and corporate investment decisions, which are highly affected by information asymetry and agency costs. The research to date has tended to neglect the difference between quantity and quality of disclosure. According to disclosure theory, the quality aspects of corporate disclosure have incremental information value over and beyond the quantity of disclosure (Li, 2010; Miller & Skinner, 2015). In fact, Hasseldine et al. (2005) found that the quality of corporate environmental disclosures has stronger impact on firm’s performance in comparison with quantity. The indication is that the quality aspect of corporate disclosures is a main source of information for stakeholders about the company. Good quality CSR disclosures attract the attention of investors and media, which raises the odds of management getting caught and punished in case of any misconduct. Thus, a high-quality CSR reporting has a tendency to increase information symmetry and restrain the management from unethical activities. Although existing research examines the link of investment efficiency with CSR performance (Benlemlih & Bitar, 2018) and CSR disclosures (Zhong, 2017), the CSR disclosure quality as a driver of efficient investment behavior has not been explored in contemporary academic research.

Pakistan is selected as a case for this research because CSR disclosure literature has mostly focused on developed markets; however, a market setting where it is innately difficult to mitigate investment inefficiency is more interesting for this study. In Pakistan, the Securities and Exchange Commission of Pakistan (SECP) requires publicly listed firms to report on their CSR activities but firms enjoy a greater leeway to choose between the amount and details of such disclosures. There are two viewpoints, namely, information and opportunistic perspectives available in the literature from Anglo-Saxon markets, concerning the rationale and results of CSR disclosures (Healy & Palepu, 2001). The first one contends that companies present high-quality disclosures in a bid to reduce information asymmetry and financing constraints, which subsequently reduces the cost of capital (Bozzolan et al., 2009), whereas the second one claims that management discloses misleading CSR information to sway stakeholders’ perceptions (Li, 2010). While research demonstrates that the prospects of CSR information to delude the stakeholders are suppressed by the sound mechanism of investor protection in the Anglo-Saxon markets (de Villiers & Marques, 2016; Fasan et al., 2016), the emerging markets do not have such counterforces because of weak institutional settings. Thus, the findings of this study will help companies enhance their understanding and implementation of CSR communication strategies to improve their overall business performance.

Using 1,980 firm-year sample observations in the multiple logistic regression model, our findings suggest that only good quality disclosures improve investment efficiency. The data used for analysis are collected from Pakistan Stock Exchange (PSX), companies’ annual reports, and State Bank of Pakistan (SBP).

Prior Research and Hypotheses Development

he neo-classical theory states that companies need to take-up all positive net present value (NPV) projects and decline the negative NPV projects (Modigliani & Miller, 1958). However, this theory is still debated in the literature (R. Chen et al., 2017; Hubbard, 1998), as financing constraints and market frictions sometimes restrain managers from commissioning all profitable investment projects. Therefore, companies opt to diverge from their optimal investment levels and end-up in investment inefficiency (Liu et al., 2016).

The past literature has primarily focused on information asymmetry as a source of market friction and noise (Stein, 2003). Information asymmetry hypothesis argues that communication gap between managers and shareholders increases the financing cost for companies. As a result, the management of companies becomes unable to raise sufficient capital to finance even the positive NPV projects. In this regard, agency theory poses that sustainability disclosure has a virtue to improve information symmetry and capital market efficiency (Brown & Hillegeist, 2007; Clarkson et al., 2008; Martínez-Ferrero et al., 2015). As different issues are covered in CSR reports, for instance, relationship with creditors, shareholders, society, and employees, such detailed disclosures can reveal information regarding management’s honesty and credibility, which is used by outside investors to judge firm’s efficiency (Kim et al., 2012). This confidence of investors on firm’s management further increases the information symmetry between managers and investors. Moreover, the transparency of company with its stakeholders acts as a controlling tool for management to stay away from sub-optimal investment choices (Francis et al., 2009). This implies that when stakeholders share the same information as management, then it will not be possible for management to hide their inefficient investment choices from the stakeholders. Hence, information asymmetry reduces the chances of hiding information, which results for managers less likely to engage in investment inefficiency. In the same vein, stakeholder theory contends that along with meeting the needs of shareholders, companies should also consider the concerns of other stakeholders regarding providing high-quality financial and non-financial information. According to stakeholder theory, the mechanism connecting investment efficiency and CSR disclosure quality is a reduction of information asymmetry between firms and external suppliers of capital (Botosan & Plumlee, 2002; Cheng et al., 2014) that hampers efficient investment.

Regarding CSR reporting, Guidry Ronald (2010) posits that quantity of social disclosure is not as effective as quality with regard to predicting the positive market reaction. According to communication perspective, not only the content of firm’s communication matters but the style of communication also plays a significant role. But despite its importance, contrarily, quantity aspects of disclosures have been emphasized in the current CSR literature and the qualitative features have been ignored (García-Sánchez et al., 2019). These qualitative features can effectively determine how the disclosures are viewed by the receivers. L. Chen et al. (2016) have classified credibility as a pre-requisite for using any financial or non-financial disclosure for decision making because of opportunistic behavior and information credibility problems in firms’ disclosures. Analyzing the current literature, we expect that considering quality as an important factor for disclosures might enhance the understanding of CSR research.

We argue that the higher the firm’s CSR disclosure quality, the more credible and reliable the information disclosed (Leitoniene & Sapkauskiene, 2015). Issuing high-quality CSR disclosure benefits firms in multiple ways, for example, (a) companies gain more trust of investors—making it easier for them to obtain capital, alleviate financing constraints, and improve reputation (Dhaliwal et al., 2011); (b) it improves information symmetry (Cho et al., 2013) and vanishes the impression of any irregularity in disseminated information; and (c) it effectively attenuates the economic frictions caused by information asymmetry, such as adverse selection and moral hazard, through providing easy access to capital (Biddle et al., 2009). The CSR literature generally assumes that the disseminated information is based on real facts and compliances to high quality, whereas some studies show that firms perform adjustments in information disclosure strategies to attain their expected market reaction. For instance, firms tend to keep high disclosure frequency before their equity offers (Jo & Kim, 2007), mislead the investors by reducing report readability (Lo et al., 2017), and give false information to mislead investors especially in weak institutional environment like Pakistan.

As there are chances that CSR disclosure quality will have a less significant role in emerging markets setup but some arguments suggest otherwise, the economic theories claiming a significant role of CSR reporting quality are not confined to only developed markets, except that the impact maybe grand in such settings. The benefits of CSR disclosure quality like improvement in control mechanism and mitigation of adverse selection can be less visible in developing markets due to weak institutional setting but not muted. Moreover, because of weak institutional setting and less analyst and media coverage, companies in emerging markets go the extra mile in disclosing quality CSR information by adopting reporting guidelines, assurances, and so on. Consequently, this disclosure becomes a comparatively important aspect of information that is considered by different stakeholders while making decisions. In comparison with firms of developed markets, our sample does not have to follow any obligatory requirements with regard to CSR disclosures. This gives our sample firms more leeway in choosing CSR reporting quality, and this decision can be potentially important for their investment behavior.

In summary, the high-quality CSR reporting gives more information about the firm, reducing information asymmetry and consequently increasing investment efficiency in the weak institutional setting. Similarly, low-quality disclosure extends limited information, which does not decrease information asymmetry, resulting in negative impact on investment efficiency.

Based on the above given argument, the following hypotheses are formulated:

Research Design

Sample

he sample consists of all non-financial listed firms on PSX which report their CSR performance either in their annual reports or issue a standalone report. There were a total of 220 firms reporting their CSR activities in 2017, so they all are taken as a sample of this study. Our study period starts from 2009 on the basis of a General Order issued by SECP in 2009, asking companies to voluntarily disclose their CSR activities in descriptive and monetary terms. Therefore, considering post-reform data as a starting point of our research will increase the validity and accuracy of our results (Ma et al., 2017).

Variables

Investment efficiency

Investment efficiency of a company is its ability to take-on all positive NPV projects. The following model (Equation 1) has been used to predict the optimal level of investment by regressing lagged sales growth over the total investment:

where

CSR disclosure quality

he readers of CSR reports do give consideration to the quantity and themes of information disclosed but neither of these attributes reflects the quality of the disclosures made. The extant literature of CSR has estimated CSR disclosure by either the length of space apportioned for it or the theme of the disclosures made but qualitative features have been ignored (Michelon et al., 2015). To overcome the limitations with the prior studies, we employed a different approach to incorporate the quality of CSR disclosure. Our approach focuses more broadly on qualitative characteristics for decision-useful information and is rooted in the conceptual frameworks of sustainability reporting standard-setting bodies like global reporting initiative (GRI). GRI in its discussion of desirable qualitative dimensions of reported information mentions several principles and one of them is reliability, which means that the information in a report should be readily subjected to examination and verification. The categories included in our CSR disclosure quality index are proven to enhance the credibility and quality of the reported information (Rahman & Post, 2012). Therefore, to measure CSR reporting quality, this study develops a modified model from the hard disclosure themes of environmental disclosure index by Clarkson et al. (2008) and social disclosure index by Widiarto Sutantoputra (2009) and informational quality attributes as recommended by the GRI. The index is further adjusted according to the voluntary disclosure environment like Pakistan. As CSR reporting is voluntary and self-regulated in Pakistan, therefore the firms either choose the quantity and quality of their CSR reporting by themselves or take guidance by reporting standards like GRI (Ali & Frynas, 2018). Therefore, the CSR disclosure quality index of our study uses GRI framework as its base. Moreover, the utilization of well-established indices to collect data increases the reliability of the content analysis process. Nine criteria used to assess a firm’s CSR disclosure quality are listed in Table 1.

CSR Disclosure Quality Index.

Note. CSR = corporate social responsibility; CSRCP = Corporate Social Responsibility Center Pakistan; ISO = International Organization for Standardization; CoP = communication on progress; GRI = global reporting initiative; UNGC = United Nations Global Compact; PwC = Price waterhouse Coopers; HSE = health safety and environment.

The quality of a report is ranked by allocating a score in the presence of the above-mentioned quality criterions. If all the qualities are present in a report, it is allocated 9 score in total (100%). To transform this score into continuous data, the total score obtained is divided by the maximum score attainable, that is, 9. Following Cureton (1957), we ranked and grouped the samples by CSR disclosure quality; the high disclosure quality (HDQ) group comprised those in the top 27%, whereas the low disclosure quality (LDQ) group contained those in the bottom 27% in the respective year. The aim behind segregating disclosure quality (DQ) variable in high and low groups is to check the separate effect of high- and low-quality CSR disclosure on investment behavior of firms. Several alternative proxies for CSR disclosure quality is used in the robustness test section to generalize our results and reduce measurement error. In particular, CSR reporting awards and CSR reporting quality index developed from sustainability data published in annual/standalone reports of Pakistani firms are used as additional proxies. The coefficients of these CSR disclosure quality proxies are expected to be positive.

Research Model

he proposed binary logistic regression model employed to check the association between investment efficiency and DQ has been estimated as,

here IED is the dichotomous variable created based on the residuals from the investment model (Equation 1), where 1 represents the efficient investment and vice versa. DQ represents the CSR disclosure quality score. CSR disclosure quality score is measured by the average score of firms on CSR disclosure quality index. Disclosure quality variable is being lagged by 1 year since sustainability reports are issued toward the end of the year, so quality of sustainability report influences the investment efficiency of the subsequent year. The rest are control variables that are found to effect investment efficiency: The positively significant coefficient of DQ variable shows that high CSR disclosure quality by the firms increases their investment efficiency.

As a proxy for slack (SLK), current ratio is used, which is measured as current asset by current liabilities. Log of age is used as a proxy for firm size (FS). Leverage (LEV) is measured by dividing total liabilities on total assets. Sales volatility (SV) measures the standard deviation of sales over the previous 5 years. Financial distress (FD) is measured by Z-score. The effect of firms financial performance (FP) is controlled by including Tobin Q in the equation. To control for industry effects (IND), a dummy variable is used as it is possible for investment efficiency to fluctuate between industries. If the company is active in one of the industries, the dummy variable is assigned a value of 1 and zero otherwise. Year fixed effect (YEAR) is also controlled for any time trend present in the data.

Binary Logistic Regression Analysis

Considering the specific characteristics of the data, parametric testing is not found appropriate for the following reasons. First, the sample is not normally distributed as Shapiro–Wilk test for normality of errors is significant. Second, Breusch–Pagan/Cook–Weisberg test confirms the presence of heteroscedasticity. Accordingly, we expect that non-parametric tests, specifically logistic regression model, will contribute a sound estimation and explanation of investment efficiency–CSR disclosure relationship. The main assumptions of general linear models, such as normality, linearity, and homoscedasticity, are not required by logistic regression, although linearity and independence of errors are main assumptions in logistic regression (Field, 2013), which are fulfilled by our data.

In a bid to find the level of inflation in standard errors potentially caused by multicollinearity, the variance inflation factor (VIF) is calculated for all the variables. The obtained value of VIF for each variable is below the critical value of 5 as shown in Table 3, which shows that the data do not suffer from multicollinearity problems (Field, 2013). Moreover, following the premise given by Scott (1997), we have included at least 10 observations for each variable for performing logistic regression analysis.

Empirical Findings

Trends in CSR Disclosure

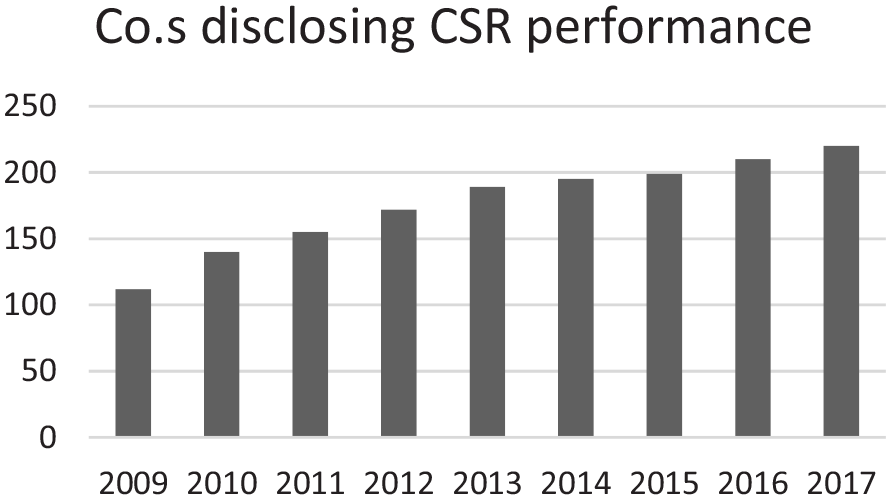

Figure 1 shows the progress of CSR disclosure quality index for the years 2009 to 2017. Comparing 2009 to 2017, it can be seen that the average disclosure quality saw a sluggish growth over the whole study period of 2009 to 2017. The plausible reason attributed toward this behavior of Pakistani firms maybe due to the fact that there has been no guideline from SECP on how to disclose sustainability information. Figure 2 shows that 112 firms reporting on CSR performance in 2009 increased to 220 firms in 2017. This shows 96% increase in the number of firms reporting on their sustainability activities. This notable increase can be attributed to the SECP’s General Order passed in 2009, asking companies to make disclosures regarding their CSR performance.

Average DQ (disclosure quality) score.

Companies disclosing CSR.

Descriptive Statistics and Correlation for Regression Variables

Table 2 presents the descriptive statistics for the regression variables. To control for the effect of outliers, all continuous variables are winsorized at 1% and 99% of the distribution. The mean of IED shows that, on average, 40% of the companies in the sample exhibit efficient investment behavior. The mean score for DQ is 0.15, which shows that DQ for companies averaged about 0.15 over the study period. This low mean of DQ variable suggests that, overall very few companies have issued good quality disclosures. Moreover, it is evident from the descriptive statistics that the companies do not show significant variation regarding CSR disclosure quality.

Means and Standard Deviations for Regression Variables.

Note. Sk = skewness; K = kurtosis; J-B = Jarque–Bera test for normality.

Significant at 1%.

Assuming a non-parametric distribution, this study employs Spearman’s rank correlation (rho) to determine the level of association existing among the variables. The correlation matrix indicates that investment efficiency positively correlates with DQ. As can be seen from Table 3, the HDQ has a significant positive correlation with IED, whereas LDQ is significantly and negatively correlated with IED. All of these findings are aligned with our hypotheses. In addition, SLK, SV, FD, and FP positively correlate with IED, whereas FS and LEV negatively correlate, which is consistent with the results of the previous studies. Finally, the correlation of less than .55 between explanatory variables suggests that multicollinearity is not a major concern and the model selection is reasonable.

VIF and Spearman’s Rank Order Correlations for Regression Variables.

Note. Bold values indicate statistical significance at least at the 5% level. VIF = variance inflation factor.

Test Result of Hypotheses

Table 4 reports the coefficient estimates and odds ratio of independent variables on the probability of efficient investment behavior by firms. Results of estimating Equation 2 support our first hypothesis for claiming a positive association between the probability of quality CSR disclosure and investment efficiency possibly because of easy access to finance and good reputation of socially responsible companies. In particular, the parameter estimate on DQ index is 1.47; this implies that the quality disclosure of firms regarding their engagement in CSR activities increases their chances of being from the investment-efficient group. The commonly used method to measure the effect of independent variables on the binary dependent variable is odds ratio. In our model, the CSR disclosure quality increases the likelihood of being in the investment-efficient group by 4.39 times, keeping all other factors constant. Hence, when CSR disclosure quality is raised by a unit, the odds ratio is 4.39 times as large, and therefore the firm is 4.39 more times likely to belong to the group of investment-efficient companies. In addition, the likelihood of being in the group of investment-efficient companies increases with higher slack, lower firm size, lower leverage, higher sales volatility, and higher financial distress.

Regression of CSR Disclosure Quality on Investment Efficiency.

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; FE: fixed effects.

Results show that all of the control variables are significantly related with firms’ investment efficiency. Specifically, the regression coefficient for size (FS) is significantly negative in all the models. This result suggests that larger firms are more likely to have fewer growth opportunities that can reduce their investment activities, which explains the negative relation between firm size and its investment efficiency. Firm size is notably one of the most significant control variables in this study, as it is significant in almost all the regression models. This is consistent with previous studies that claim firm size as the most significant variable in corporate finance research. The coefficient of slack (SLK) is positive because managers in firms with slack resources are able to devote resources to positive NPV projects, which explains why SLK is associated with high investment efficiency. Similar to the results of Jensen (1986), the regression coefficient for leverage (LEV) is negative in all of our models, as highly leveraged firms are bound to pay more interest and are less likely to obtain additional debt financing due to overhang of existing debt (Myers, 1977). These problems impede their spending even in positive NPV projects leading to the problem of underinvestment. Moreover, sales volatility (SV) is found to be loaded positively and is statistically significant, implying that sales volatility leads to high investment efficiency. Similar to the argument of Eisdorfer (2008), the estimated coefficient of FD is significantly positive. The coefficient indicates that financially stressed firms are less likely to deviate from efficient investment behavior. The obtained finding contradicts to intuitive narrative, which states that higher bankruptcy typically results in increased agency conflicts. However, this finding could be explained by less flexible behavior of management in financially stressed firms. In such cases, the management is left with fewer options to indulge in agency conflict because of higher level of monitoring and restrictions. Finally, the coefficient of firm’s financial performance (FP) is also found to be positively associated, this shows that good financial performance leads to efficient investment decisions. Taken together, these results from the set of our control variables are in line with the findings of earlier studies (Biddle et al., 2009; S. Chen et al., 2011; R. Chen et al., 2017; Gomariz & Ballesta, 2014). Moreover, the Wald chi-square statistics is used to check the statistical significance of individual regression coefficients (Peng et al., 2002). The Wald test shows that our disclosure quality variable and all the control variables contribute significantly in predicting investment behavior of the firms.

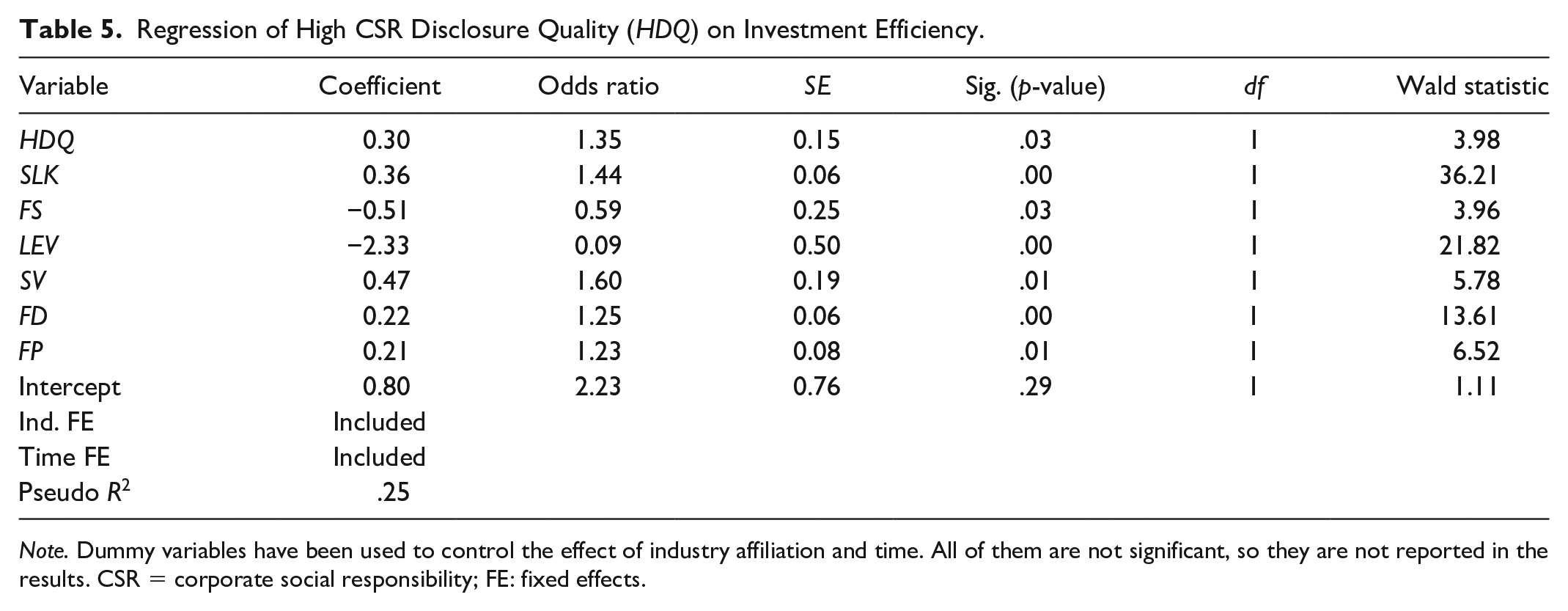

To test the second hypothesis, the DQ is replaced by HDQ in Table 5 and LDQ in Table 6. The effect of HDQ on investment efficiency is positive and significant at 1% level, implying them as meaningful and value relevant.

Regression of High CSR Disclosure Quality (HDQ) on Investment Efficiency.

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; FE: fixed effects.

Regression of Low CSR Disclosure Quality (LDQ) on Investment Efficiency.

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; FE: fixed effects.

However, the very symbolic statements (LDQ) claiming the involvement of companies in CSR activities exhibit negative impact on investment efficiency. This result suggests that firms engaged only in lip service, without disclosing meaningful CSR information, do not have the potential to reduce the information asymmetry and consequently create negative impact on investment efficiency.

The results of the current study with regard to CSR disclosure quality also support the findings of Schons and Steinmeier (2016). Taken together, these results suggest that merely engaging in CSR disclosure activity is not beneficial for companies unless it is a meaningful disclosure of sustainability information. Good quality disclosure has the potential to lessen information asymmetry between the firm and its stakeholders, leaving the firm better placed to take advantage of future investment opportunities. These results provide support for Hypotheses 2 and 3 with the positive impact being driven particularly by the HDQ. Overall, our findings propose that emerging markets can benefit from improved disclosure quality.

All the regression models presented above have high significance level of .00 when p-values are less than .05 and psuedo R-squares are also in a good range, that is, .24–.27.

Robustness Tests

he potential endogeneity and omitted variable bias are common concerns regarding analysis in the CSR literature. These problems may obscure findings or lead to biased inferences, concerning the relation between investment efficiency and CSR reporting quality. To mitigate these concerns, in this study, we take the following measures.

Addressing omitted variable bias

o ensure that our results do not suffer from omitted variable bias, which may arise despite controlling for a sufficiently rich set of independent variables, this study observes coefficient movements after including several additional control variables. Table 7 tests the sensitivity of main model by including further control variables, which are found in the literature to affect the investment efficiency of a firm.

Effect of CSR Disclosure Quality on Investment Efficiency: Robustness to Omitted Variable Bias.

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; FE: fixed effects.

***, **, and * indicates statistical significance at the 1%, 5%, and 10% level, respectively.

In Model 1, we control for the effect of family ownership (Fam-Own), as Shahzad et al. (2018) argue that investment behavior of a firm is positively affected when ownership is in the hands of family members. We find that the impact of CSR disclosure quality on investment efficiency remains positive and significant. Next, we control for the life cycle stage (LCS) the company is passing through in Model 2 as it is expected to significantly affect the investment behavior of firms (Koval et al., 2017). The results show that CSR disclosure quality continues to have a significant impact on firms’ investment behavior after controlling for LCS. As a third additional control, we include board effectiveness (B-Effctv), as it contains the non-financial information which could affect the relationship between CSR disclosure quality and investment efficiency. Model 3 of Table 7 shows that CSR disclosure quality coefficient remained significant and positive. Asset tangibility (ASTAN) is controlled for in Model 4, and the result remained unchanged. Finally, in Model 5, all additional control variables are included and after controlling for the potential impact of each of these variables, CSR disclosure quality continues to load positively and significantly on firms’ investment efficiency. This confirms that our findings do not suffer from omitted variable bias.

Alternative CSR disclosure quality proxies

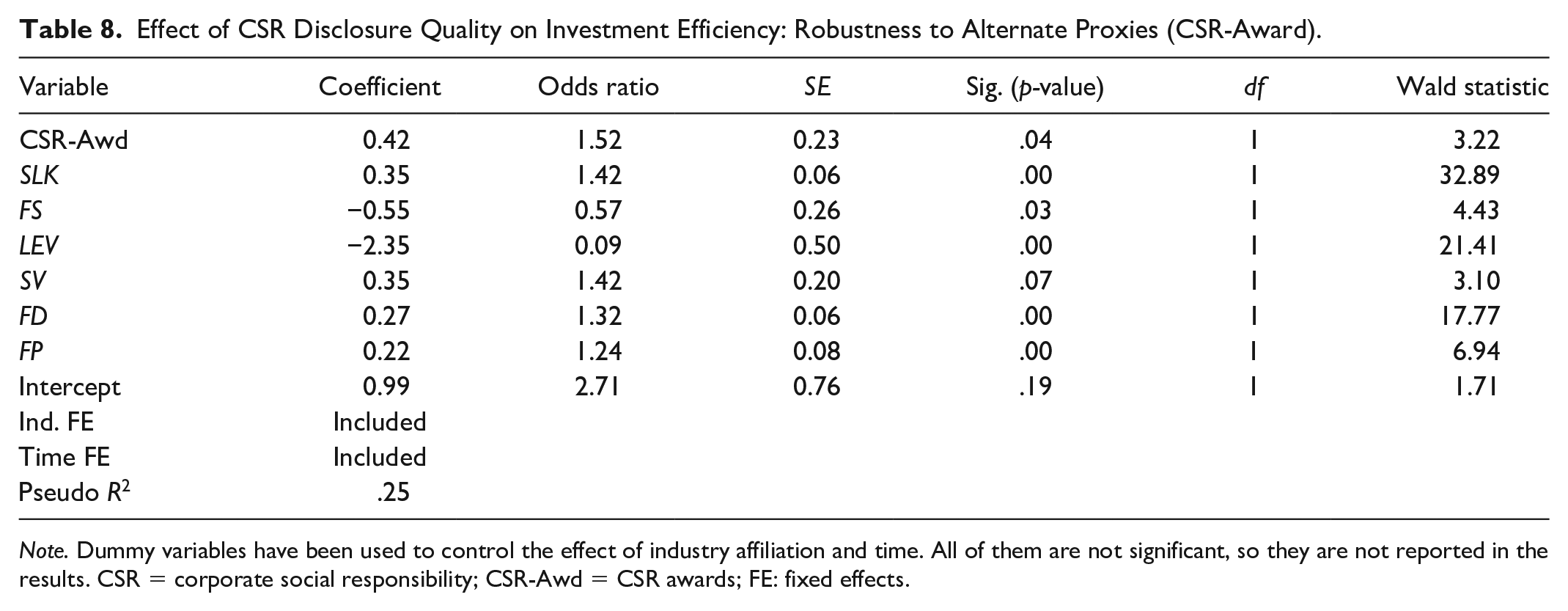

Following Hou (2019), this study uses sustainability reporting awards as a proxy for CSR disclosure quality. The Best Corporate and Sustainability Report Award by ICAP and ICMAP and ACCA—WWF Pakistan Environmental Reporting Award launched in 2011 and 2002, respectively, are used as the second proxy for CSR reporting quality. Awards are used as a direct measure of firms’ CSR disclosure quality because the awards are based on strict criteria provided by an independent organization. We regard companies that are awarded on their sustainability reporting as having better CSR disclosure quality than companies which are not awarded (Table 8).

Effect of CSR Disclosure Quality on Investment Efficiency: Robustness to Alternate Proxies (CSR-Award).

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; CSR-Awd = CSR awards; FE: fixed effects.

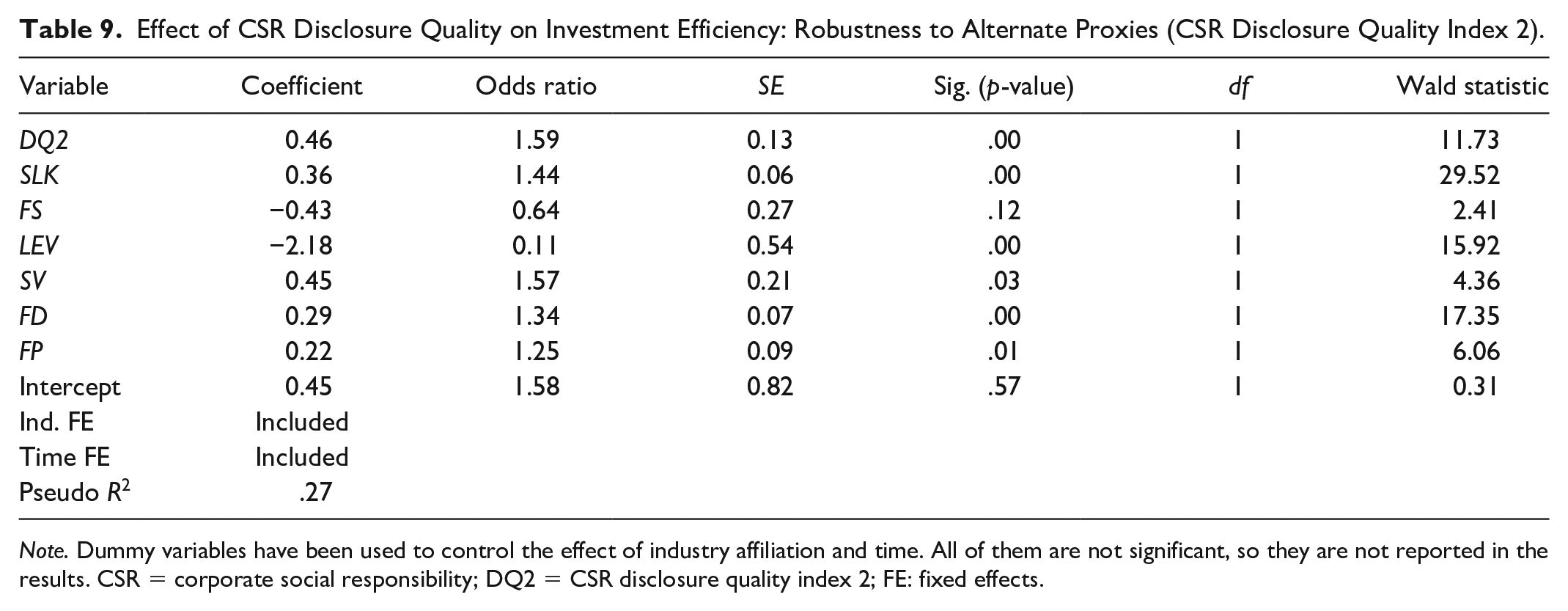

To be consistent with many previous studies that measure CSR disclosure quality in addition to quantity, the present study adopts a similar approach. Following Wiseman (1982), this study develops a weighted-CSR disclosure quality index (Appendix 1) which measures the quality of specific disclosures in addition to counting the presence of items (Table 9). Weighted-scoring procedure can measure disclosure quality of information because it can incorporate the understandability, completeness, and relevance of information. Similar to Wiseman (1982), a score of “0” is given to a company on respective item if no CSR information is disclosed at all, whereas “1” indicates a generic CSR disclosure, “2” indicates a non-quantitative specific disclosure, and “3” indicates disclosure of qualitative and quantitative information. Following the prior disclosure studies, this study adopts the formula given below to construct the CSR disclosure quality index:

where

Effect of CSR Disclosure Quality on Investment Efficiency: Robustness to Alternate Proxies (CSR Disclosure Quality Index 2).

Note. Dummy variables have been used to control the effect of industry affiliation and time. All of them are not significant, so they are not reported in the results. CSR = corporate social responsibility; DQ2 = CSR disclosure quality index 2; FE: fixed effects.

In both of the regression models presented above, the sign of the proxies used for disclosure quality remains unchanged, showing high robustness and consistency. The pseudo R-square values demonstrate that the predictive and explanatory powers of the models are good.

Conclusion

his article provides new evidence on the topic “When does CSR disclosure affect investment efficiency” by identifying the condition that makes CSR disclosure valuable enough to affect the financial performance of firms. Our findings contend CSR disclosure as a mean to improve firms’ investment behavior when it is substantial because it mitigates information asymmetry, which eventually increases investment behavior of firms. We find empirical support that high-quality CSR disclosure affects investment efficiency of firms positively, whereas symbolic disclosure has negative effects.

This article has examined the effects of CSR disclosure quality on investment efficiency as theory suggests an inverse relation between disclosure quality and information asymmetry (Brown & Hillegeist, 2007). Studies in agency theory state that more transparency increases firm value by improving manager’s investment decisions (Bushman & Smith, 2001; Lambert, 2001). Our findings of positive relation between CSR reporting quality and degree of efficient investment support this theory. Overall, our results show that increased disclosure quality has a significant real impact on internal investment decisions via the mechanism of increased information accessibility to the outsiders. Our study confirms previous findings and contributes additional evidence which suggests that investment efficiency is effected not only by the quantity of information disclosed as claimed by previous research (Benlemlih & Bitar, 2018; Biddle et al., 2009; Biddle & Gilles, 2006; Shahzad et al., 2018; Zhong, 2017), but the quality of disclosures also affect investment efficiency. This also suggests that investors can consider greater disclosure quality as a signal for efficient investment behavior by firms.

Despite the fact that CSR reporting is growing around the globe, the developed markets have remained the focus of much of the current literature. While Du et al. (2017) propose that CSR is country specific and recommend to specially study the emerging markets for this reason, the present study contributes to the literature on CSR disclosure and investment efficiency based on evidence from one of the developing markets, that is, Pakistan. This would improve the understanding with regard to the economic impact of CSR disclosure quality.

Overall, the provided robust and strong evidence is consistent with agency and stakeholder theory that quality of CSR disclosure is a tool to decrease information asymmetry between management and shareholders, which leads to efficient corporate investment behavior. Our results recommend that sustainability disclosures have broader implications, which were not previously discussed in the literature and suggest that quality of CSR disclosures should be considered as the process of value creation for the firms. The empirical results are consistent with our hypotheses and are robust to different methods to address endogeneity and omitted variable bias.

Implications

Our findings add to the extant literature on the link between CSR disclosure and investment efficiency by differentiating between high and low quality of CSR disclosures. This investigation has essential implications for managers. Our findings clearly show that CSR reporting improves investment efficiency subjected to conditions. As awareness and skepticism in general regarding corporate behavior including sustainability reporting have risen dramatically (Leonidou & Skarmeas, 2017), the camouflaging tactics like green-washing can no more be considered possible. Moreover, CSR reporting is found to be not merely an expense but also an investment and management strategy to enhance corporate performance. This shows that management should work toward improving the CSR disclosure quality of their firms to benefit from it. In addition, such findings increase the confidence of socially responsible managers and encourage them to further pursue and report on their CSR engagements. CSR performance and reporting contribute positively to the society while simultaneously benefiting the firms by improving their investment efficiency. On the contrary, the managers of less socially responsible firms should consider investing and reporting on such activities, as doing so increases investment efficiency of the firms.

With the consequence of this study, the Government of Pakistan, while pursuing its foreign direct investment (FDI) attraction policy, can make strategies for improving CSR disclosure quality to attract foreign capital in its stock market (Mohammadi et al., 2018). Thus, engagement and disclosure of CSR activities can be used as a strategy to attract investors and improve financial performance of companies. The results would also help the policy making and regulatory organizations like PSX to ensure a certain level of CSR disclosure quality by the firms through introducing new requirements to decrease the information asymmetries. Our results suggest that to curb the widespread inefficient investment behavior of listed firms in Pakistan, the regulatory authorities should help and guide firms to increase the CSR disclosure quality.

Footnotes

Appendix

Disclosure Themes and Indicators.

| Customer-related disclosure | Environment-related disclosure |

|---|---|

| • Info about types of product & services | • Environmental protection policy disclosure |

| • Research & development | • Waste management |

| • Product improvement | • Product impact on environment |

| • Product safety standards disclosed | • Air emission information |

| • Sanitary procedures followed in production | • Air emission processing |

| • Product quality & safety | • Water discharge information |

| • Improvement in customer services | • Effluent treatment |

| • Consumer protection measure | • Recycling of waste products Solid waste disposal |

| • Pollution-prevention technologies | |

| • Conservation of natural resources | |

| • Land reclamation & forestation programs | |

| • Energy saving & conservation | |

| • Energy production | |

| • Direct energy use | |

| • Compliance with environmental standards | |

| Community-related disclosure | Employees-related disclosure |

| • Sponsoring educational institution(s) | • Firm’s relationship with labor unions |

| • Scholarship program | • Equal employment opportunity |

| • Community support & uplift | • Sports/fun activities |

| • Public health related activities | • Reduction of pollutants in work place |

| • Establishment/funding of hospital | • Discussion of accidental statistics |

| • Recreation clubs, parks, & public libraries | • HSE certification |

| • Part-time employment of students | • Receiving a safety (HSE) award |

| • In-kind donations | • Medical surveillance |

| • Rehabilitation of disaster affectees | • HSE trainings |

| • Technical/vocational training programs | • Human resource development |

| • Rural development programs | • Educational facilities |

| • Charitable foundation/ trust | • Facility of day-care, maternity leaves |

| • Clean water provision for communities | • Hajj sponsorship |

| • Contribution to national exchequer |

HSE = health, safety and environment.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.