Abstract

Environmental management and sustainable financial growth are currently hot topics in academic research. This article examines the relationships among environmental management, debt financing, and sustainable financial growth in the Chinese tourism industry. The results show that environmental management and debt financing have promoted sustainable financial growth, and the overall effect of debt financing on sustainable financial growth has been affected by environmental management. After employing different methods of controlling the endogeneity, these conclusions are still robust. We also examine the mediating effect and threshold effect on environmental management, debt financing, and sustainable financial growth, and the results reveal that debt financing can mediate the effect of environmental management on sustainable financial growth and that there is nonlinear impact of debt financing on sustainable financial growth in different thresholds of environmental management. The analysis results show that the presented policy proposals promote the development of tourism companies from the aspects of debt financing and environmental management.

Introduction

This article explores how debt financing mediates the relationship between environmental management and sustainable financial growth. Debt financing can precisely reflect the real financing cost of the financing entity, and performs a significant role in the financial planning and investment decision-making of tourism enterprises. To explore the mediating role of debt financing, this article examines whether debt financing is positively affected by effective environmental management and whether debt financing, in turn, contributes to sustainable financial growth. Environmental management includes all actions taken systematically to supervise the ecological effect of the enterprise’s movements and to handle environment-related issues. This article employs the method proposed by Gil et al. (2001) and adopts environmental management variables. A sustainable growth model based on cash flow is also proposed in the literature concerning sustainable financial growth. Our article follows the method of Colley et al. (2002) to measure the sustainable financial growth to reduce the environmental impact of tourism enterprises.

Our article has contributions to the literature in the following aspects. First, a mediation model is adopted to investigate the intrinsic mechanism of environmental management and debt financing on sustainable financial growth. We also choose the panel data threshold model to check the nonlinear effect of environmental management and debt financing on sustainable financial growth, which extends the research scope of sustainable corporate growth. Second, to solve the endogeneity, different methods are employed that include two-stage least squares (2SLS), instrumental variables (IVs), and the system generalized moment method (System GMM) to confirm the results are robust. Finally, our article discusses the implications of environmental management and debt financing on sustainable financial growth by providing managerial contributions to tourism companies. The rest of our article is construed as follows. The second section shows the contents of literature review and proposed hypotheses, the third section explains the methodology, the fourth section reports the research results, and the final section provides the conclusions and implications.

Since the 21st century, the tourism industry has developed rapidly, and the positive effects, including economic, social, and cultural effects, caused by the tourism industry are obvious (Dai et al., 2017). However, the negative effects such as environmental deterioration and air pollution have become a critical bottleneck in the process of sustainable tourism development (L. Zhang & Gao, 2016). With the increasing pressure of resources and environmental protection, the importance of environmental management becomes more and more important (X. L. Xu et al., 2017, 2019). In 2009, the State Council of China issued the opinions on speeding up the development of the tourism industry, which proposed “promoting energy conservation and environmental protection,” “reducing water and electricity consumption in star-rated hotels and a-rated scenic spots by 20 percent within five years,” “rationally determining the tourist capacity of scenic spots,” “advocating a low-carbon tourism mode,” and other specific standards and requirements for the construction of a tourism environment (H. G. Xu & Sofield, 2016). These standards and requirements reflect the new governing philosophy and policy guidance in addressing the relationship between environmental protection and economic development and the relationship between man and nature (Tang, 2017).

With the improvement of residents’ income level and the change of consumption attitudes, the previous tourism industry development model and tourism products cannot meet the requirements of current consumers (Font & McCabe, 2017). In the meantime, the importance of finance to the development of the tourism industry has become increasingly prominent (Seetanah & Sannassee, 2015). Finance, as the core of modern economic development, plays a significant role in economic development. Debt financing, as an important financial tool, can promote the development of other related industries through the direct support of pillar industries to achieve the coordinated development of finance and industry (Kim et al., 2017; J. Li et al., 2018; X. Zhu et al., 2019). As for the tourism industry, the financial system can influence the optimization and adjustment of the tourism industry structure through financial instruments (Lado-Sestayo et al., 2016), while the manner in which the tourism industry structure develops further advances higher requirements for financial instruments. More diversified financial instruments, such as debt financing, are needed to meet the requirements of tourism enterprises (Falk & Steiger, 2018). Therefore, the formation of a reasonable matching relationship between financial instruments and the growth of the tourism enterprise is conducive to the sustainable development of the tourism industry.

The relationships between environmental protection and sustainable economic are discussed in the debate on “whether it pays to be green” to explore the relationship between sustainable financial growth and environmental management (Boons & Wagner, 2009; Molina-Azorin et al., 2009). This debate continues to evolve as the research findings on the relationships between sustainable financial growth and environmental management are inconsistent. The existence of contradictory results could be clarified by the research gaps on the theoretical basis. First, lots of studies have shown the relationship between sustainable financial growth and environmental management is not direct (Boons & Wagner, 2009; Zaid et al., 2018). Previous studies have called for investigations of the mediating variables to reduce environmental impacts to benefits for sustainable financial growth. Second, the various results in the literature on “whether it pays to be green” are supposed to be an assessment issue (Molina-Azorin et al., 2009). Especially, various measures and concepts have been adopted for environmental management and sustainable financial growth.

Literature Review and Proposed Hypotheses

Environmental Management, Debt Financing, and Sustainable Financial Growth

Environmental management

Huang (2003) believes that environmental management is the effort made by tourism enterprises to minimize the negative effect of their management activities on the tourism environment. In addition, Huybers and Bennett (2003) pointed out that environmental management consists of two components, namely, enterprises and governments. Enterprise environmental management refers to the environmental protection activities spontaneously conducted by tourism enterprises, and these activities are motivated by the reliance of tourism products on the quality of the natural environment. Government environmental management refers to the environmental protection regulations formulated by the government for tourism enterprises. As shown in Figure 1, environmental management in China has undergone the three stages of risk management, pollution prevention, and whole process management and the ecological industry (N. M. Wang et al., 2006).

The stage of environmental management in China.

The previous research on environmental management mainly focuses on the relationship between environmental management and financial performance; however, its conclusions are inconsistent. These conclusions could be divided into the following three types: environmental management has a positive impact on financial performance (Epstein et al., 2015; X. L. Xu & Liu, 2019); environmental management has a negative impact on financial performance; and environmental management is not correlated with financial performance (Hirunyawipada & Xiong, 2018; Muhammad et al., 2015).

In addition, other conclusions are also drawn in some literature. For example, some facets of social responsibility have impact on financial performance, whereas other facets have no significant relationship with financial performance (Flammer, 2015; Lins et al., 2017). Neville et al. (2005) employed a mediator variable such as corporate social reputation to explore the impact of corporate social responsibility on financial performance, and they conclude that corporate social responsibility is a benefit to gaining a corporate competitive advantage.

Environmental management, as a primary corporate social responsibility, could usefully enhance the reputation of enterprises and further improve their debt financing ability. B. Li and Wu (2017) believed that increasing environmental investment could reduce the profits and costs of enterprises, but the expenditures reduction was more pronounced; therefore, the profits of enterprises increased. However, whether the environmental management of tourism companies will improve their debt financing capacity and sustainable development needs to be further checked in specific scenarios.

Debt financing

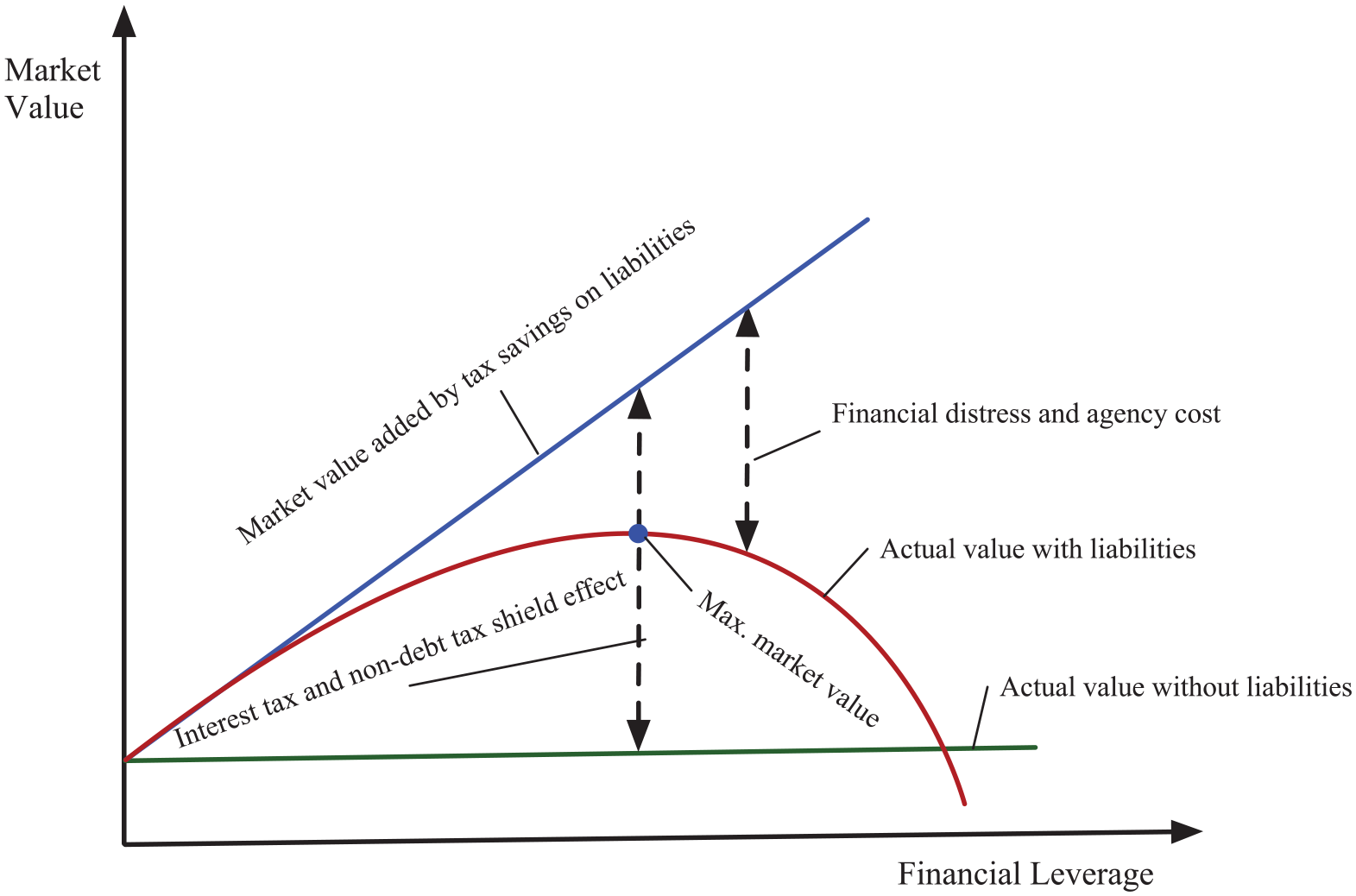

Modigliani and Miller (1958) put forward the M-M theorem. They believe that in a perfect market, if there is no corporate and personal income tax and no risk of corporate bankruptcy and the capital market operates fully and effectively, then the capital structure is not correlated with the market value of the company. Thereafter, Modigliani and Miller revised the M-M theorem and pointed out that in the presence of enterprise income tax, debt financing will take a tax savings impact on the company, the market value of the enterprise will increase with the increase of debt financing, and the change of capital structure will affect the total market value of the company (Modigliani & Miller, 1963). In the 1970s, Trade-off Theory further modified the M-M theorem, which states that enterprises with high risk and low profitability should have a low debt ratio, whereas enterprises with adequate tangible assets and high tax rates should have a high debt ratio (Kraus & Litzenberger, 1973; Rubinstein, 1973). As shown in Figure 2, the optimal capital structure of the company should be the best balance between maximizing the value of debt financing and the cost of financial distress and agency.

The relationship between financial leverage and market value of enterprises.

Most of existing literature has studied on the impact of debt financing on financial performance, in particular, on profitableness. El-Sayed and Ebaid (2009) believed that debt is negatively correlated with the return on assets (ROA). Nevertheless, the results have not revealed any significant impact of different types of debt on return on equity (ROE) or gross profit margins (GPMs). Salim and Yadav (2012) verified a negative relationship between long- and short-term debts and financial performance in terms of ROA, ROE, and earnings per share (EPS). Yazdanfar and Ohman (2015) demonstrated a negative relationship between debt ratios and corporate profitability. Onchong’a et al. (2016) explored the relationship between debt financing and financial performance of enterprises, and the results showed that the debt financing was negatively correlated with ROA. Cole and Sokolyk (2018) examined the various impacts of debt financing patterns of enterprises; the results showed that compared with all-equity enterprises, the enterprises that used debt at the start-up stage had better revenue.

All of this literature suggests that no consistent conclusion has been drawn in terms of the relationship between debt financing and financial performance. Considering the various methods and models employed and the various backgrounds of this literature, the institutional structure may affect the relationship between debt financing and financial performance, which could demonstrate the inconsistent results of the literature. Therefore, it is necessary to reexamine this relationship in terms of Chinese tourism industry.

Sustainable financial growth

Sustainable growth derives from development economics, which refers to the ability that ensures the long-term coordinated development of resources and the environment in the process of social and economic development to meet the needs of contemporary people without compromising future generations (Basiago, 1998). As shown in Figure 3, sustainable growth is generally measured through economic, environmental, and social longevity, which is called the triple bottom line (X. L. Xu & Chen, 2018; K. Q. Zhang & Chen, 2017). When this concept is introduced in the study of enterprise development, it not only retains its original meaning but also refers to the maximum growth level of enterprise sales without exhausting financial resources (Davidsson et al., 2009). To quantitatively analyze the sustainable development of enterprises, Higgins (1981) proposed a model of the sustainable growth rate; he believes that enterprises have their own path for suitable development and uses this model to solve the problem of enterprise growth management.

The essence of sustainable growth.

Academic views on the business objectives of enterprises tend to maximize the interests of shareholders; to achieve this goal, enterprises must be sustainably developed and grown (Feng et al., 2018; Post et al., 2002). From the perspective of financial management, the development of enterprises must be based on the continuous growth of enterprises. If the growth of enterprises is too slow, financial resources cannot be fully utilized, which results in a waste of resources and funds. However, if the growth of enterprises is too fast, it will cause a shortage of corporate resources, and the gap in corporate capital can only be filled by increasing financial leverage. If something goes wrong, enterprises could be faced with huge financial risks or even bankruptcy. Therefore, there is a dynamic relationship between enterprise growth and financial resources. If an enterprise wants to achieve sustainable development, it needs to balance the relationship between the two.

Due to the voluntary and mandatory nature of environmental standards, the subject of environmental management activities in the literature tends to be more popular. Vachon and Hajmohammad (2016) explored the effects of environmental management on financial business in the service sector. Valero-Gil et al. (2017) investigated the relationships between operations proactivity and execution of environmental management network.

This article focused on the environmental facets, which constitutes an important part of operational and production strategies (Feng et al., 2018). We study this topic from the perspective of industrial ecology, in which environmentally sustainable enterprises could reduce the negative impact on the environment by establishing production systems.

Proposed Hypotheses

At present, China’s tourism industry consumes large amounts of environmental resources, and society’s appeal to the environmental management of the tourism industry is becoming stronger. A company’s expenditures on environmental protection are conducive to reducing the information asymmetry between its internal environment and the outside world, especially the financing parties, to thereby enhance the company’s governance capacity. Furthermore, environmental expenditures may result in the decline of corporate profits because of excessive investments or the increase in corporate value because of appropriate investments. Therefore, measuring the profits derived from environmental expenditures is difficult. Whether environmental investments can help companies achieve sustainable financial growth is not conclusive in the academic field. This article analyzes the relationship between environmental management and corporate sustainable financial growth through the mediator variable of debt financing.

The existing literature believed that corporate social reputation could affect corporate market value and its sustainable financial growth. Y. J. Wang and Berens (2015) revealed that the indirect effect of enterprise social reputation on organizational performance is more stronger than the direct effect of enterprise social responsibility on financial performance. Q. H. Zhu and Zhang (2015) concluded that the corporate social responsibility has a significant positive impact on financial performance in China and these two variables have an interaction effect. Accordingly, this article puts forward the first hypothesis as follows:

H. Wang (2003) explored the relationship among the debt financing, market value, and corporate governance of listed companies in China. The results showed that debt financing has an impact on strengthening enterprise governance and increasing its market value, and debt financing could also reflect financial performance. Environmental management could enhance the social reputation and improve the financial performance of tourism enterprises. Therefore, to achieve the long-term sustainable development, tourism enterprise should increase its investments in the environment. Thus, this article puts forward the second and the third hypotheses as follows:

Research Methodology

Data Collection

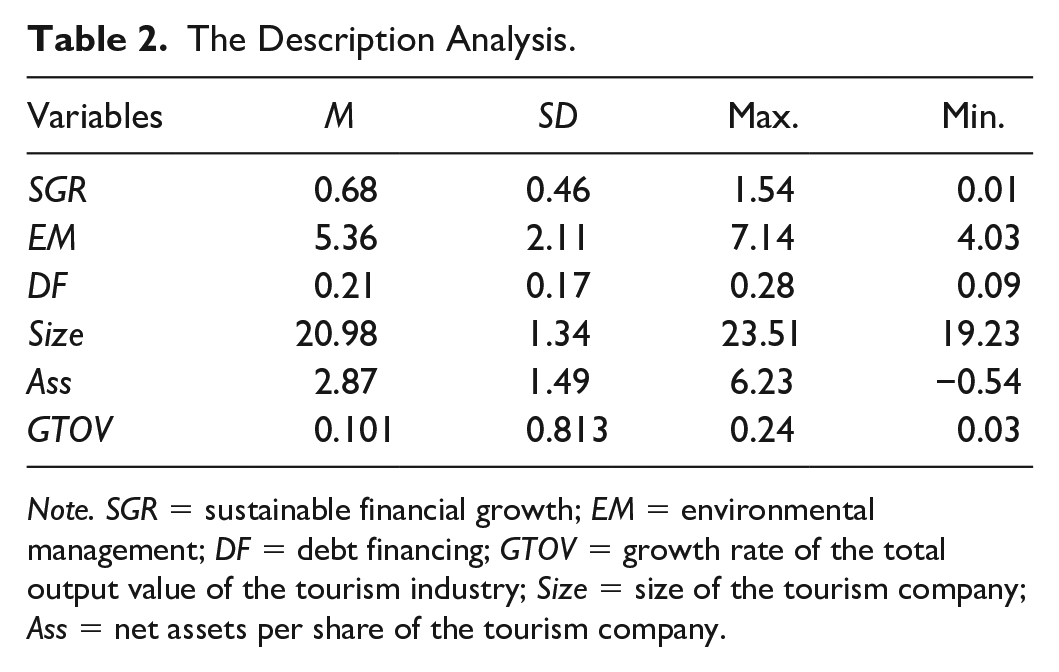

Our article employed the environmental reports and annual reports of tourism enterprises from 2008 to 2017. These data were downloaded from the CSMAR database and RESSET database. We collected the data for environmental management from 35 tourism companies through questionnaire surveys.

Variables

Sustainable financial growth

The truly meaning of sustainable growth is to create market value constantly. Only the market value with a continuous growth could represent the real sustainable growth. Accordingly, sustainable growth needs to avoid the financial risks from the view of operating capital management (J. Li et al., 2020) and set up a linkage between market value and continuous growth (K. Q. Zhang & Chen, 2017).

Currently, there are two types of sustainable financial growth models, including cash flow–based and accounting-based sustainable growth model. Our article examines the sustainable growth of tourism enterprises from the view of debt financing. Thus, the cash flow–based model is employed. Also, this type of model includes the Rappaport model and Colley model. Both models are based on certain hypotheses. Rappaport’s sustainable growth model requires the net cash flows produced by investment activities. However, in practice, this net cash flow in the financial statement of most tourism companies is negative. Thus, the sustainable growth rate based on Rappaport’s sustainable growth model is mostly negative, the annual variation is quite significant, and the gap between research and reality is overly large. However, the sustainable growth rate calculated by Colley’s sustainable growth model is relatively stable and more consistent with the actual operating conditions of China’s tourism companies. Therefore, this article uses Colley’s sustainable growth model.

There are some hypotheses in the Colley’s sustainable growth model: First, the dividend payout ratio and asset–liability ratio are unchanged; Second, the current assets, pretax profits, fixed assets, current liabilities, and other assets increase in proportion to sales growth; Third, depreciation could be utilized for fixed asset reinvestments. The equation is as follows:

where SGR, EBIT, I, t, DER, DPO, and NA0 denote the sustainable financial growth rate of tourism companies, the earnings before interest and taxes, the interest expenses on debt, the income tax rate, the debt-to-equity ratio, the dividend payout ratio, and the net assets at the beginning of the period, respectively.

Environmental management

Our article follows the methodology scales for the environmental management practices of tourism companies proposed by Gil et al. (2001). This article employed seven items to investigate the environmental management of tourism companies. We attempted to use these items to gain a comprehensive indicator of the balanced integration of different aspects of environmental management. Both technological and enterprise activities were considered. The environmental legislation concerning the tourism industry has demonstrated that most movements should be under the heading of “pollution prevention,” although some indicators focused on “pollution control.” Tourism company management was requested to evaluate these indicator items using a score of 0 to 10. The evaluation results reveal the function of their enterprises’ degree of involvement in activities.

In Table 1, the seven items were categorized in one group as a variable. The Cronbach’s alpha value (.84) is larger than the critical value (.70) proposed by Nunnally (1978) to ensure the internal consistency. In addition, the convergent validity of variable has been guaranteed by using complementary measurements. This article is based on studies that employed the formulation of environmental planning as a proxy for environmental management.

Factor Analysis Results for Environmental Management Scales.

Note. This scale is referenced from Alvarez Gil et al. (2001).

Debt financing

This article uses the proxy variable (leverage) to represent debt financing. The leverage is equal to the ratio of the long-term debt to the total assets and is calculated with the book values (Cole & Sokolyk, 2018). The adoption of “long-term book leverage” helps to diminish the likelihood of reverse causality between financial performance and the cash flow structure in two aspects. On one hand, long-term book values are different from market values and are insensitive to the evaluation of the capital market concerning the recent financial performance. On the other hand, although changes in leverage (e.g., leveraged buyouts) could indicate the fluctuations in expectations of subsequent product outcomes, the levels of leverage can have accumulative impacts on earlier financing decisions. Our article sets the debt-to-assets distribution of the sample in the scope of [0, 1], which indicates that the company-years with negative market equity (almost bankrupt companies) were excluded from the data sample.

Control variables (CVs)

According to the related existing literature, this article employs three CVs (S. Chen et al., 2018; Gil et al., 2001). We adopt the size of the tourism company (Size), the net assets per share of the tourism company (Ass), and the growth rate of the total output value of the tourism industry (GTOV). For the substitute variables, Ass is calculated as the ratio of the stockholder equity to the total stock, and Size is calculated as the natural logarithm of total assets.

Modeling

The model of environment management, debt financing, and sustainable financial growth is proposed as follows:

where i and t denote the enterprise and the year, respectively,

The Description Analysis.

Note. SGR = sustainable financial growth; EM = environmental management; DF = debt financing; GTOV = growth rate of the total output value of the tourism industry; Size = size of the tourism company; Ass = net assets per share of the tourism company.

Results and Discussion

Baseline Regression Analysis

Islam (2001) found that the least square dummy variable (LSDV) estimation method is even better than the IV estimation and GMM estimation for samples with large numbers of individuals but limited time periods. Since the data used are short term and the number of companies is relatively large, we first conduct the LSDV method to investigate the effects of environmental management and debt financing on sustainable financial growth. The results are presented in Table 3. It can conclude that the values of F statistic are large and significant at the 1% level, which indicates that all coefficients are significant and the result is reliable. Model I is the estimate results of Equation (2) deprived of the interaction terms and CVs, and Model II is the estimate results of Equation (2) deprived of the interaction terms. The regression coefficients of environmental management are positive significant at the 5% level, which indicates that the environmental management of tourism enterprises has notably enhanced their sustainable financial growth. Thus, H1 was verified. From the regression results of debt financing, its coefficient is positive at the 1% significance level in all models, which indicates that debt financing has a significant positive influence on sustainable financial growth. Thus, H2 was verified.

The Results of LSDV Regression.

Note. EM = environmental management; DF = debt financing; LSDV = least square dummy variable; GTOV = growth rate of the total output value of the tourism industry; Size = size of the tourism company; Ass = net assets per share of the tourism company; Cons. = constant.

**,*Significant at 1%, 5%, and 10% levels, respectively; values within parentheses represent the Z value.

Model III is the estimate results of Equation (2) using the interaction terms, which is employed to examine whether environmental management will worsen the influence of debt financing on sustainable financial growth. From the estimation result of Model III, the debt financing has a significant positive influence on sustainable financial growth, which again verifies the hypothesis of H2. The coefficient of the interaction term indicates that environmental management has a positive effect of debt financing on sustainable financial growth. Thus, the hypothesis of H3 is verified.

From the regression coefficients of the CVs, the significance of the Size coefficient reveals that larger tourism companies show an acceleration ability to fulfill the sustainable development target. The significance of the GTOV coefficient indicates that the growth rate of the total output value of the tourism enterprise has a positive impact on sustainable financial growth. The significance of the Ass coefficient indicates that when the tourism company’s profitability is stronger, its sustainable financial growth is higher.

Endogeneity Test

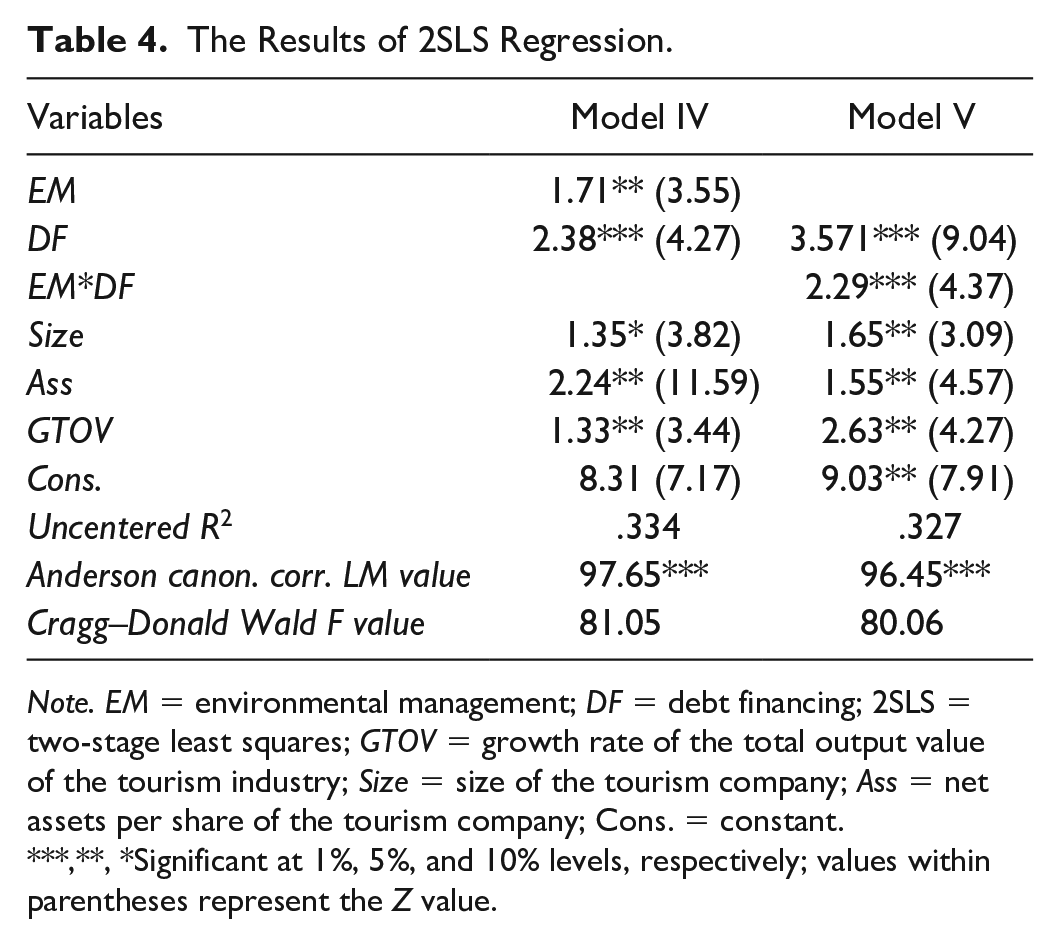

This article considers that the independent variables (environmental management and debt financing) could have endogeneity issue. To solve this issue, we first adopted the fixed-effect model with dispersion transformation and then evaluated the transformed model through the method of 2SLS. C.-M. Chen et al. (2011) applied the 2SLS method to evaluate the demand structure of Taiwan’s tourist hotel industry, and they found that the market’s uncertain demand significantly motivates hotels to increase their product variety. The 2SLS method involves that the endogenous independent variables should be specified first and then be defined by suitable IVs. In our article, environmental management and debt financing were considered as endogenous independent variables, and their lagged variables were employed as IVs. The results of the 2SLS method are presented in Table 4.

The Results of 2SLS Regression.

Note. EM = environmental management; DF = debt financing; 2SLS = two-stage least squares; GTOV = growth rate of the total output value of the tourism industry; Size = size of the tourism company; Ass = net assets per share of the tourism company; Cons. = constant.

**, *Significant at 1%, 5%, and 10% levels, respectively; values within parentheses represent the Z value.

Model IV of Table 4 is the results of 2SLS method estimates Equation (2) deprived of the interaction term, and Model V is the results of 2SLS method estimates Equation (2) with the interaction term. From the results of Table 4, the significance of the Anderson canon corr. LM statistic suggests that the employed IVs are reasonable. Meanwhile, the result of the Cragg–Donald Wald F statistic rejects the null hypothesis. Therefore, it concluded that the employed IVs are effective in the model. Besides, due to the amount of IVs employed is precisely equal to the amount of endogenous independent variables, there is no overidentification issue in the model. The coefficient significance of independent variables estimated is consistent with the regression results of Table 3, which indicates that there is no endogeneity issue in the model and the estimation using the LSDV method is suitable.

Robustness Test

Sustainable financial growth should be a continuous dynamic development, in which the early stage of financial status has a dynamic effect on the future financial developments. However, the model employed in our article ignores these dynamic impacts. Therefore, the results concluded above could not be robust. Lim and Zhu (2018) used the Difference and System GMM (generalized methods of moments) estimation to verify the impacts of meetings, incentives, exhibitions, and conventions (MICE) on tourism demand, and the results indicate that MICE have a significant positive influence on tourism demand.

Our article adopts the method of substituted variables, employing the lag term of sustainable financial growth to the model, and conducting the System GMM estimation to ensure the results of H1, H2, and H3 are robust. From the results of the robustness test, the residuals of all model differences have no second-order correlation. The Sargan test also suggests that the overrecognition constraints are effective (the p values are almost 1), which means that the employed IVs are suitable. The significance level of variable coefficient is consistent with that of LSDV analysis. Therefore, the results of robustness test verify H1, H2, and H3 again.

Mediating Effect in the Model

In the LSDV analysis above, the interaction term coefficient of debt financing and environmental management is significantly positive, which could be induced by the interaction between the environmental manners of the Chinese tourism companies and the capital allocation manners of the stock market. Thus, the “interaction item test” could not effectively identify the positive impact of environmental management on sustainable financial growth through debt financing as described in H3. Therefore, we employ the mediating effect model proposed by Baron and Kenny (1986) to precisely identify the intrinsic mechanism of environmental management → debt financing → sustainable financial growth.

Table 5 reports the mediating effect results, in which Model VI demonstrates that environmental management coefficient

The Results of the Mediating Effect Model.

Note. EM = environmental management; DF = debt financing; SGR = sustainable financial growth.

**Significant at 1% and 5% levels, respectively; values within parentheses represent the Z value.

Threshold Effect in the Model

The mediating effect results of the “interaction term test” above suggest that environmental management enhances sustainable financial growth through debt financing. However, the limitation of the mediating effect model is to suppose that “the impact of environmental management is a linear relationship of monotonous decreasing or increasing,” whereas the previous literature shows that the effect of environmental management on sustainable financial growth is nonlinear (W. X. Wang et al., 2017). This may cause the following issue: whether a nonlinear relationship exists among environmental management, debt financing, and sustainable financial growth? This issue means that environmental management could play a threshold role, means that, there are critical differences in the effect of debt financing on sustainable financial growth in different threshold values of environmental management. Therefore, to explore the nonlinear relationship in the mediating model, we adopt the panel threshold model proposed by Hansen (1999) to investigate the nonlinear impact of environmental management and debt financing on sustainable financial growth. On the basis of Equation (2), this article constructs the following model.

where

Table 6 presents the threshold model results. When the threshold value of environmental management is smaller than 5.03, the coefficient of debt financing on sustainable financial growth is 3.27; when the threshold value of environmental management is larger than this value, the coefficient is 2.84. When the threshold value of environmental management is larger than the value of 6.24, the coefficient is 3.04. These results mean that when the degree of environmental management implemented by tourism companies is higher, the promotion degree of sustainable financial growth by debt financing is greater.

The Results of the Threshold Effect Model.

Note. EM = environmental management.

**Significant at 1% and 5% levels, respectively.

Conclusion and Policy Implications

This study found that when the company’s profitability is stronger, its debt financing capabilities are better. A company’s investments in environmental management will help to reduce debt financing costs. Furthermore, environmental expenditures will offset the impacts of environmental management investments on the reduction of debt financing costs to some extent. However, company owners are not only concerned with reducing debt financing costs but are also focused on the long-term sustainable development of the company. Therefore, our article further studies the effects of environmental management on the sustainable financial growth of tourism companies. The results show that a weak debt financing capability will worsen a company’s capability of sustainable growth, whereas investments in environmental management can effectively help companies achieve sustainable growth by reducing the debt financing costs. The conclusions of our article could facilitate tourism enterprise management to understand that investments in environmental management will raise the operating costs, reduce the financing costs, and improve the corporate market value. In the future, investments in environmental management are beneficial to the sustainable financial growth of tourism companies.

The results show that environmental management investments can effectively help companies achieve sustainable financial growth by reducing debt financing costs. Therefore, tourism enterprises should carry out debt financing through various channels to reduce its average costs when expanding its core businesses. With the considerable advantages of debt financing, the scale of the enterprise could be enlarged, and large-scale tourism groups could be found through capital movements to reanimate stock assets and realize the target of low-cost development. Nowadays, the prime channels for the debt financing of Chinese tourism enterprises are commercial credit and bank borrowing. The top managers of banks must be made aware of the gains of suitable liabilities for the financial sustainable development of companies, and they should loosen up the conditions on the refinancing of tourism companies and support the debt financing of these companies. Besides, the profitableness of tourism companies also exhibits the intentions of investment foundations for its refinancing. For those tourism enterprises with durable profitableness, banks would relax the financing requirements. However, for tourism enterprises with weak profitableness and poor financial performance, banks would strengthen the management and tracking of its debt financing.

The promotion of investments in environmental management for tourism companies can be performed in several aspects. First, regulations referred to environmental protection can be improved, appropriate subsidies and rewards can be provided as incentives for the tourism companies that contribute to energy saving and environmental protection, and these companies can be encouraged to implement environmental management. Second, the government must create a green environment atmosphere and implement restrictions on tourism companies’ stakeholders to promote environmental management behaviors. For instance, the requirements for environmental protection must be strengthened among the government, community supervisors, consumers, investors, and employees. Partners and even competitors’ environmental protection activities may pressure tourism companies. Green benchmarking enterprises of tourism industry should be enhanced to support the environmental protection movements of tourism companies. Third, companies should emphasize the application of energy-saving and environmental protection technologies, promote the transformation and upgrading of tourism companies, and reduce their debt financing costs. The government and industrial associations can promote the utilization of energy-saving and environmental protection technologies in tourism companies by providing policy support or building platforms. For example, industry associations can provide unified training or technical support for tourism companies by using new technologies. Energy-saving technical companies should be encouraged to cooperate with tourism companies and provide customized environmental management technical services for them to thus improve the effectiveness of technical products.

This article adopts the sustainable growth model proposed by Colley et al. (2002) to assess the sustainable financial growth in the tourism industry. To extend the research method of sustainable financial growth, future studies could employ another method such as the financial sustainability model proposed by Sher and Yang (2005) to measure sustainable financial growth in the tourism industry.

Footnotes

Acknowledgements

We sincerely thank the editor and reviewers for their very valuable and professional comments.

Authors’ Contribution

The research is designed and performed by X.L.Xu. The data were collected by C.Shun and Y.L. Analysis of data was performed by X.L.X and N.Zhou. All authors wrote the paper and read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the National Social Science Foundation of China (19CGL030); China Postdoctoral Science Foundation (2020M670473); Youth Project of Humanities and Social Sciences of Ministry of Education in China (18YJC630213); Natural Science Foundation of Hunan Province (2019JJ50382); and Key Project of Hunan Education Department (19A292). The funding sponsors had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; and in the decision to publish the results.