Abstract

The paper investigates the implications of busy directors on bank performance and bank risks in Brazil. The study employs an event study based on a change in board status as an identification strategy, Heckman’s two-stage model, and the propensity score matching method to account for endogeneity. The study findings show that busy directors contribute to an increase in bank market value. Regarding bank risks, the study shows that multiple directorships contribute to an increase in asset risk and insolvency risk. The study contributes to the existing literature by showing that busy directors are associated with high bank risks in foreign-owned banks while they disproportionately reduce bank risks in state-owned banks. Considering the importance of bank stability in promoting economic growth in Brazil and the positive impact of busy directors on bank risks, there is need for the policymakers to craft clear corporate governance clauses which guide the selection of multiple directors and enforce feedback and accountability mechanisms that govern busy directors who serve in Brazilian banks. Reducing excessive participation for busy directors serving in bank boards ensures that the directors have adequate time and attention to discharge their governance responsibilities efficiently, thus resulting in robust risk monitoring strategies in bank operations.

Keywords

Introduction

There is a growing perception that weak corporate governance systems contribute to managerial opportunism, poor bank performance and excessive bank risk. It is argued that close monitoring of the management by effective boards on behalf of the shareholders can help minimize the agency conflicts (Faleye et al., 2018; Jensen & Meckling, 1976). However, literature is ambiguous on what constitutes an effective board. While the agency theory emphasizes the oversight role of directors, the resource dependency theory connotes that outside directors also bring a wealth of human capital resources in the business which disproportionately contributes to robust corporate governance and firm performance (Pfeffer, 1972; Pfeffer & Salancik, 1978). Thus, according to the resource dependency theory appointing busy directors is another channel that businesses can use to complement scarce internal human capital and financial resources.

Busy directors are directors who serve on multiple boards of several companies. According to the resource dependency theory, companies carefully select busy directors based on their reputation (Fama & Jensen, 1983) and expertise which are essential for robust monitoring and advising (Carpenter & Westphal, 2001; Pfeffer, 1972) in complex organizations like banks (Elyasiani & Zhang, 2015). Literature sheds some evidence which suggests that busy directors are associated with high corporate governance standards (Adams & Ferreira, 2012), high transparency, high management efficiency (Carpenter & Westphal, 2001), low cost of debt (Chakravarty & Rutherford, 2017), high firm performance (Di Pietra et al., 2008; Pombo & Gutiérrez, 2011; Sarkar & Sarkar, 2009), and low risk (Elyasiani & Zhang, 2015). However, there is another strand of literature from the agency perspective which argues that multiple directorships are detrimental to firm performance. For instance, it is argued that busy directors are associated with low performance (Hwang & Kim, 2009), a low book to market value (Hauser, 2018), shirking of performance (Fich & Shivdasani, 2006), excessive pay (Core et al., 1999), low monitoring capacity (Hwang & Kim, 2009) and low board meeting attendance (Jiraporn et al., 2009). Given the mixed evidence in the literature, this study seeks to extend the literature by examining the implications of busy directors on performance and risk in the banking sector.

This research aims to give clarity on the impact of busy directors on bank performance and bank risks using a sample of Brazilian banks. Even though there is a growing literature on how networked directors influence bank performance (Cooper & Uzun, 2012; Elyasiani & Zhang, 2015; Kutubi et al., 2018), the evidence is inconclusive. For example, in support of the agency theory, Cooper and Uzun (2012) show that busy directors contribute to high bank risk; in contrast, Elyasiani and Zhang (2015) in agreement with the resource dependence theory, report that busy directors contribute to high returns and low bank risk. Furthermore, recent evidence by Kutubi et al. (2018) shows that there is an inverse relationship between multiple directorships and bank performance. Thus, our understanding of busy directors’ implications on bank performance is incomplete, hence the need to further study the subject using robust novel estimation methodologies.

The banking sector is fundamental and a pillar of any economy even in countries with robust equity markets. Banks act as suppliers of external financing for investments that are critical for long-term sustainable economic growth. Given that the banking sector plays a critical role in financing firm investment and stimulating economic growth especially in bank-based economies like Brazil, any failure in the banking system poses far-reaching effects to depositors, domestic firms and the economy at large. The global financial crisis of 2008/2009 revealed that poor bank governance costs society and highlighted the need for robust monitoring mechanisms and effective risk management strategies that promote resilience and stability in the banking sector.

The 2008/2009 financial crisis renewed interests among researchers and policymakers to find mechanisms that enhance high corporate governance standards to avoid a future global financial crisis. For instance, literature shows that director independence, CEO independence, diversity, and board size influence firm performance, however, most corporate governance studies are concentrated in non-financial firms (Adams & Ferreira, 2012). However, there is little evidence in the literature on how multiple directorships affect bank performance and risks. Banks have their unique characteristics different from non-financial companies, and they fall under the multiple firms’ category (Coles et al., 2008). The banking industry is a sensitive and vital sector that needs a lot of skills and expertise to increase value for investors and protect depositors’ funds. Therefore, there is a need for careful attention and increased research on bank corporate governance mechanisms. Hence this study seeks to increase our apprehension of how busy directors influence bank operations using a sample of Brazilian banks.

Furthermore, the research findings have policy implications for emerging markets, considering that other countries have started setting some limits on multiple directorships. Studying the composition of directors is very imperative since the policy prescriptions for board structures in emerging markets may need to vary from developed markets due to different systems of governance (Levit & Malenko, 2016; Mbanyele, 2020). The study complements scanty literature on busy directors in emerging countries, China (Chen et al., 2014) India (Sarkar & Sarkar, 2009), Brazil (Goncalves et al., 2019) and some Asian countries (Kutubi et al., 2018). Increased studies on emerging markets enrich policy decision making in institutional environments with weak legal systems. For instance, Brazil is a civil law country where companies are mainly owned by a few large shareholders, and there is limited protection of minority shareholders (Djankov et al., 2008). Thus, the large ownership concentration weakens the governance system as it promotes managerial opportunism and agency conflicts (Jensen & Meckling, 1976), and promotes bank instability. The corporate governance system in Brazil is characterized by low transparency, small board sizes, and less director independency (Black et al., 2010). Besides, the poor corporate governance system in Brazil contributes to a large wedge of information asymmetry not only between the majority shareholders and minority shareholders but also contributes to information frictions between insiders and outsiders. Therefore, implementing incompatible policies in emerging markets informed by developed nations’ studies usually leads to high policy failures which worsen the existing governance systems. Hence, considering the unique features of the Brazil institutional environment and it being one of the largest economies in Latin America and among the emerging economies, this study focuses on Brazil. The study seeks to increase our understanding of how multiple directorships shape corporate governance and influence bank performance and risks in emerging markets.

The study findings contribute to the bank literature in several ways. First, the study documents that busy directors contribute to an increase in bank market value in agreement with the resource dependency theory and the reputational hypothesis. Also, the study reports that multiple directorships contribute to excessive bank risk-taking after accounting for endogeneity. This study further contributes to the growing research on bank boards by explaining two mechanisms through which busy directors influence bank performance. The study evidence indicates that the presence of busy directors in foreign-owned bank boards does not affect bank performance but contributes to high bank risk. Also, the study sheds evidence that suggests that the inclusion of busy directors in state-owned boards contributes to a decrease in bank risk-taking.

Furthermore, the study significantly contributes to the literature by providing evidence which suggests that busy boards contribute to a substitution effect between bank performance and risk. In contrary to Elyasiani and Zhang (2015), the study contributes to extant literature using endogeneity free evidence by showing that incorporating busy directors in banks contributes to a trade-off between high bank market value and high bank risks. The trade-off hypothesis between bank market value and bank risk is persistent throughout the study in most of the models. The study evidence seems to suggest that multiple directorships bring great advisory benefits and bank reputation but at the expense of low monitoring abilities which result in excessive bank risks.

Finally, the study contributes to the literature by using rigorous methodologies to deal with reversal causality and simultaneity bias, which affect most prior studies on busy directors. The research employs an event study approach as an identification strategy, and the paper treats the change of bank board status from zero busy directors to at least one busy as an exogenous event. Specifically, the event study approach allows the study to analyze the changes in bank performance and bank risks around the changes in board composition. The study makes use of the propensity score matching and the two-stage Heckman (1979) correction models for dealing with endogeneity concerns.

The remaining sections of the study are as follows: Section “Institutional Background of Brazil” contains the institutional background for Brazil. Section “Related Literature and Hypothesis Development” covers related literature and hypothesis development. Section “Data and Sample Description” sample design and methodology. Section “Empirical Findings” presents the empirical findings, and finally, Section “Discussion and Conclusion” contains the discussions and conclusion.

Institutional Background of Brazil

The Brazilian banking industry is one of the largest banking sectors in Latin America and among emerging markets, with a very long history of financial reforms (for a comprehensive history, see Cortes & Marcondes, 2018). The banking sector is fundamental and a pillar in Brazil considering that the equity market is still in developmental stage, thus banks in Brazil are the main suppliers of external finance for firm investments. Therefore, the banking sector in Brazil plays a critical role in financing firm investment and stimulating economic growth. Thus, any failure in the banking system has far-reaching effects on depositors, domestic firms and the economy at large. Given that the corporate governance system in Brazil is characterized by low transparency, small board sizes and less director independence (Black et al., 2010), there is a need for robust monitoring mechanisms that promote resilience and stability in the banking sector.

The Brazilian banking industry endured through turbulent times in the 1990s which led to financial distress (Beck et al., 2005) but shortly recovered after the Real Plan economic stabilization program in 1994 that reduced inflation. There was excessive risk-taking by banks in the aftermath of the Real Plan program which resulted in a rise in the proportion of non-performing loans (NPL) to 15% in 1997 from as low as 5% in 1994 (Cortes & Marcondes, 2018); this was exacerbated by hyperinflation and low-risk monitoring in the sector. Given that most state-owned banks displayed high-risk distress during this period due to limited risk management strategies, the Brazilian government started liberalizing the banking sector and privatizing most banks from 1997 going forward, which led to a decline of total deposits to 6.5% in 1998 from 19.3% in 1996 in state-owned banks (Baer & Nazmi, 2000). After 2002, the economy started to recover, boosting investor confidence in the banking sector and started attracting many players in the industry including foreign investors following the privatization of banks between 1997 and 2007 which promoted bank competition. This period marked an increase in participation of foreign investors in the banking sector through Merger and Acquisition (M&A) activities which was also promoted by the government through tax incentives. The government increased bank competition to promote bank efficiency and bank stability in the industry spearheaded by foreign-controlled banks and private-owned banks. The banking sector responded to the government initiatives as evidenced by rapid credit expansion, as the private sector banks supplied more money to the market.

The Brazilian banks remained resilient in the global financial crisis of 2008/2009, with substantial credit expansion dominated by state-owned banks. However, excessive lending by state-owned banks at high fiscal costs has been criticized as the leading cause of the Brazilian crisis which began in 2014. Even though the Brazilian sector demonstrated resilience during the global financial crisis, the post-financial crisis period posed some instability in the banking industry. The banking sector has not been spared in the 2015 to 2017 economic recession in Brazil which was characterized by low confidence, a drop in investments and a decline in national output. The ratio of NPL to total assets deteriorated in the period leading to the recession, for instance the NPL rose from 2.7% in 2014 to 3.8% in 2015. The profitability of the banking sector has been slowly increasing reaching 13.8% as of 2017 and 11.6 in 2016.

The banking sector in Brazil is composed of state-owned banks, domestic private banks, and foreign-owned banks, however, five banks dominate the industry as revealed by a large ownership concentration of at least 70% of the industry assets (Cortes & Marcondes, 2018). Even though the state implemented several reforms by opening up the banking industry, some issues are affecting the sector like large ownership concentration, lack of independent boards and small board sizes which poses a problem in promoting stability in the sector. Considering that most corporate in Brazil are controlled by few shareholders, families and other related parties, incorporating outsiders in bank boards may promote transparency, attract investors, and boost bank stability. Corporate governance is still evolving in Brazil and in 2018 the nation made a milestone achievement by adopting the first corporate governance code in the country. In summary, the banking sector in Brazil has thrived in a turbulent environment characterized by economic cycles and an evolving corporate governance system.

Related Literature and Hypothesis Development

A board of directors plays a critical role in upholding sound corporate governance standards in organizations like banking institutions. The board is responsible for monitoring and advising management on behalf of the shareholders to minimize agency costs and promote firm value (Jensen & Meckling, 1976). Thus, the quality and composition of a bank board play an essential role in formulating and promoting bank policies that enhance managerial decision making, bank performance, and mitigate risks. From the agency theory perspective, independent outside directors are better qualified to monitor the management as compared to insiders. Given the importance of the oversight role of the boards, most banks incorporate prestigious busy directors in their boards who also serve in other companies’ boards to promote strong governance, bank stability, and resilience. Busy directors have multiple directorships in several companies. There are two competing views regarding the implications of multiple directorships on corporate governance and firm performance.

The seminal works of Pfeffer (1972) and Pfeffer and Salancik (1978) explain the importance of multiple directorships in business operations from the resource dependency perspective. The resource dependency theory connotes that busy directors bring a wealth of human capital resources in the business which disproportionately contributes to robust firm performance (Pfeffer, 1972; Pfeffer & Salancik, 1978). Thus, businesses carefully select prestigious directors based on their expertise and industry experience to gain reputational benefits from appointed busy directors. Therefore, according to the reputational hypothesis, busy boards are critical in improving performance in complex organizations like banks especially in weak institutional environments like Brazil. However, according to agency theory, multiple directorships contribute to inefficiency, and low firm performance (Falato et al., 2014; Fich & Shivdasani, 2006). It is argued that director monitoring and advisory roles demand attention and need more time which is scarce for busy directors. Also, multiple directorships can lead to the cognitive workload which can limit the effectiveness of directors to exercise their advisory function efficiently (Kress, 2018). Thus, from this perspective, busy directors are likely to be ineffective monitors and most probably contribute to weak governance and low firm value.

Recent empirical research suggests that busy directors spur bank performance due to their extensive monitoring and advising capabilities (Elyasiani & Zhang, 2015). Even though busy directors have many duties on several boards, their connections with banks force them to be active monitors due to scrutiny from the regulators and shareholders (Adams & Ferreira, 2012). It is not unusual for bank directors to be dragged to court after bank failures, and sometimes heavy monitoring penalties are imposed on them by regulators for breaching their mandates (Macey & O’Hara, 2003). Hence, busy directors attached with banks have no motivation to shirk performance, but instead, they put more effort to protect their reputation. The banking sector is a protected industry which cannot be muddled with since its collapse does not only affect shareholders but also depositors and the government through bailout costs. Therefore, from this perspective, busy directors in bank boards are less likely to shirk performance when there are set standards by the regulators which monitor corporate boards. Multiple directorships enhance managerial competencies due to the extensive experience gained from multiple firms’ boards (Carpenter & Westphal, 2001). Elyasiani and Zhang (2015) argue that busy directors bring a wealth of resources in banks, which contribute to an increase in firm value and low risk in banking institutions. It is argued that busy directors possess a wealth of expertise, which makes them competent advisors (Adams et al., 2010). Also, networked directors can exchange valuable information about borrowers’ creditworthiness and financial risk profiles, which improve banks’ screening and lending systems (Abdelbadie & Salama, 2019). Besides, there is empirical evidence in some countries that support the positive implications of busy directors on firm performance as shown by Di Pietra et al. (2008) in their study on Italian businesses, Pombo and Gutiérrez (2011) in their research on firms in Colombia and Sarkar and Sarkar (2009) on Indian firms. Overall, the evidence suggests that busy directors possess a lot of professional, diversified knowledge and relevant experience, which enhances their capabilities to strengthen financial stability, reduce information asymmetry, and enhance monitoring of banks’ external environments. Thus, considering the Brazilian institutional environment with a less strict governance code, busy directors may contribute to high corporate governance standards and robust bank performance.

On the other hand, professional ties between directors of different firms bring great advisory benefits to the firms but at the expense of low monitoring abilities, which may weaken the firm’s performance (Hwang & Kim, 2009). Networked directors are usually time-constrained and may shirk performance by failing to attend board meetings (Kress, 2018). Banks do not only need advisory know-how usually possessed by networked directors but, also require extensive monitoring capabilities since bank operations are very complex and opaque (Elyasiani & Zhang, 2015). Hauser (2018) study findings show that a reduction in the total seats occupied by directors on other boards significantly contributes to an increase in the firm market to book value and profitability. From the agency theory perspective, multiple directorships contribute to the shirking of performance, which is costly to shareholders (Fich & Shivdasani, 2006). Fich and Shivdasani (2006) show that directors with more seats in other companies’ boards contribute to low firm market value and low profitability. Several studies support a negative implication of busy boards on firm performance (Cashman et al., 2012; Falato et al., 2014). Core et al. (1999) contend that multiple directorships are associated with excessive pay, which is detrimental to firm value. Also, Sarkar and Sarkar (2009) link busy internal directors with low firm performance. Besides, there is some bank literature evidence that suggests that busy directors are related to high bank risk levels. Busy directors compromise corporate governance in financial holdings (Kress, 2018) due to low monitoring capacity (Hwang & Kim, 2009), by attending fewer board meetings (Jiraporn et al., 2009) and serving in few board committees (Jiraporn et al., 2009). Nguyen et al. (2015) and Adams and Mehran (2011), in their study of U.S. banks, conclude that busy directors have negative implications on bank market performance. Also, Cooper and Uzun (2012) document that an increase in busy directors contributes to an increase in excessive bank risk-taking due to more distractions from other multiple directorships.

Given the competing arguments from both theoretical and empirical literature, the study formulates the hypotheses based on the balance of the weight of the evidence from bank literature taking into consideration the Brazilian institutional environment with weak governance mechanisms. Brazil, unlike other developed nations, has a weak corporate governance strategy which lacks stringent external monitoring on the functionality of corporate boards. Thus, busy directors may shirk performance without reprimand from the regulators. Considering that Brazil did not have a formalized corporate governance code until 2018, it is likely that busy directors were not effectively executing their duties in challenging management due to a lack of a clear and authoritative external regulatory monitoring instruments. In a study of Brazilian firms, Santos et al. (2012) document that the negative impact of board connectedness is more prominent in firms with busy directors. Second, most boards in Brazil are not independent, most directors have close connections with the focal companies which diminish the value of busy directors as monitors. Thus, these governance features promote managerial opportunism and expose banks to high risks. Hence, the inclusion of overloaded busy directors with low monitoring abilities is detrimental to bank performance considering that banks need extensive monitoring mechanisms in addition to advisory duties. Therefore, given the busyness of multiple directors, the complexity in bank systems and low regulatory governance in Brazil, the study makes the following hypotheses:

Data and Sample Description

The study uses a sample of listed banks on Brazil Stock Exchange from 2002 to 2015 to probe the impact of networked directors on bank stability. The relatively long study period is critical as it encapsulates the 2008/2009 global financial crisis-era, which helps to clearly understand the role of busy directors in promoting bank stability. The sample information is obtained from a publicly shared dataset constructed by Rossoni and Goncalves (2019). The study drops banks with less than three consecutive years of information to improve the study results’ reliability. The research sample includes all active and non-active banks with more than three consecutive years of information to reduce survival bias concerns. The final sample comprises 335 bank year observations.

Variables Construction

Measures of bank performance

Several studies investigate the performance of banks from different perspectives like bank profitability (Tan, 2016, 2017), bank efficiency (Konara et al., 2019; Tan & Anchor, 2017), and bank productivity (Tan & Floros, 2013a, 2013b) among others. This study following other studies on multiple directorships uses the Tobin Q and return on assets (ROA) to measure bank performance (Elyasiani & Zhang, 2015; Fich & Shivdasani, 2006; Kutubi et al., 2018).

Tobin’s Q is measured as the total firm market value of equity plus the total book value of assets minus the total book value of equity divided by the total book value of assets. The Tobin’s Q is a firm market value proxy measure that captures firm growth opportunities and intangible resources like corporate reputation (Elnahass et al., 2019), thus qualifying it to be an effective measure to examine the implications of busy directors on bank performance.

ROA is calculated as the total profit before interest and tax divided by total bank assets. The study employs the ROA as it measures the accounting performance of a bank, thus it helps to examine the implications of multiple directorships on bank profitability.

Measures of bank risk

The study uses three bank risk proxy measures; market risk, asset risk, and insolvency risk. Market risk is proxied by market beta calculated as (covariance between return on asset and market) divided by variance of return on the market. The study measures the bank asset risk following prior literature (Kutubi et al., 2018; Saghi-Zedek & Tarazi, 2015) as the return on assets divided by the standard deviation of return on assets. A low value represents a high-risk level, while a high value indicates low bank risk.

Following prior literature (Abdelbadie & Salama, 2019; Elyasiani & Zhang, 2015) the study uses the z-score as a measure of insolvency risk. Insolvency risk is a measure of the probability of a bank going into insolvency, thus it measures the distance to bankruptcy. The study calculates the insolvency risk as the sum of the return on assets and capital adequacy ratio divided by the standard deviation of return on assets. The study uses the natural logarithm of z-score to normalize the proxy measure for insolvency risk. A higher insolvency risk value shows that the firm is stable and has fewer chances of defaulting while a lower value is unfavorable as it is a signal that the company has insufficient resources to meet its liabilities, which may lead to insolvency or bankruptcy.

Measure for busy directors

The primary explanatory variable is busy_director, which is measured following prior literature as the number of directors in bank boards who sit in three or more boards of other companies (Abdelbadie & Salama, 2019; Elyasiani & Zhang, 2015).

Control variables

Several corporate governance variables are controlled to capture managerial and firm heterogeneities. To control for manager attributes, the study controls for CEO duality, a binary variable that equals one if the CEO is also the chairperson and zero otherwise. Other corporate governance controls included the size of the board, the percentage of outside directors, and the percentage of independent directors. Following Hauser (2018), the paper controls for firm characteristics that have been found in prior research to influence firm performance. The study controls for bank size, bank leverage, volatility, and bank ownership (Elyasiani & Zhang, 2015; Fich & Shivdasani, 2006; Kutubi et al., 2018). Bank leverage is calculated as the ratio of total bank liabilities to total bank assets. Bank size is calculated as the natural logarithm of total bank assets. Volatility is measured as the annual volatility based on the 12-month stock returns of the bank.

Model Specification

The study uses the following ordinary least squares (OLS) estimation baseline model to examine the implications of busy directors on bank performance, for preliminary findings:

where Bank performance represents return on assets (ROA) the ratio profit before interest and tax to total bank assets, Tobin’s Q the sum of the total firm market value of equity and debt divided by the total book value of assets, market risk, asset risk, and insolvency risk. Busy_director is the total of directors who sit in three or more boards of other companies. The controls are as defined in Table 1—the study controls for bank dummies and year dummies to capture bank heterogeneity characteristics and time variations.

Variable Definitions.

Note. ROA = return on assets.

Empirical Findings

Descriptive Statistics

Table 2 reports the summary statistics for the period 2002 to 2010. The mean value of total bank assets is 141 million Brazilian reals, while the median is 13.1 million Brazilian reals, which suggests that the banking industry in Brazil is a mix of huge banks and small banks. The study uses the natural logarithm of total bank assets to reduce the right skewness of assets size. The banks’ average leverage value of 0.827 shows that banks keep more liabilities as a proportion of total assets. The ROA average value is 1.787, while the average for Tobin’s Q is 0.329. On average, banks have seven members who sit on the board, and an average of independent directors is 10.5%. This shows that non-independent directors dominate bank boards in Brazil. An average of 12.7% of bank board members are busy directors.

Summary Statistics.

Note. ROA = return on assets.

Busy Directors, Bank Performance and Bank Risks

Table 3 reports the results on the implications of busy directors on bank performance and bank risk results based on the OLS estimation method. The results in Table 3 show that the percentage of the busy director (P_busy) is positively related to bank market value as measured by Tobin’s Q. However, the study reports in Table 3 Column 2 show that the percentage of busy directors has an insignificant negative effect on bank profitability as measured by ROA. The results in Table 3 Column 3 show that the percentage of busy directors (P_busy) is negatively related to market risk at 10% statistical level of significance. However, the study results show that an increase in the number of busy directors on the board has no significant implication on bank insolvency risk and asset risk.

Busy Directors, Bank Performance and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is the percentage of busy directors (P_busy). All the control variables are lagged by one year and defined as in Table 1. Year fixed effects, and bank fixed effects are included in the regressions with robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

To further investigate the implications of network directors on bank performance, the study regresses the changes in bank performance and bank risk indicators on changes in the percentage of busy directors. The time-series dimension results are presented in Table 4 and are comparatively the same as the previously reported results in Table 3. The coefficient in Table 4 Column 1 for Tobin’s Q is now significant at 1% level from 5% significance level shown in Table 3. The significance levels of coefficients for other bank performance variables are the same as those previously reported in Table 3.

Changes in Busy Directors, Changes in Bank Performance and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is the percentage of busy directors(P_busy). All the control variables are lagged by 1 year and defined as in Table 1. Year fixed effects, and bank fixed effects are included in the regressions with robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

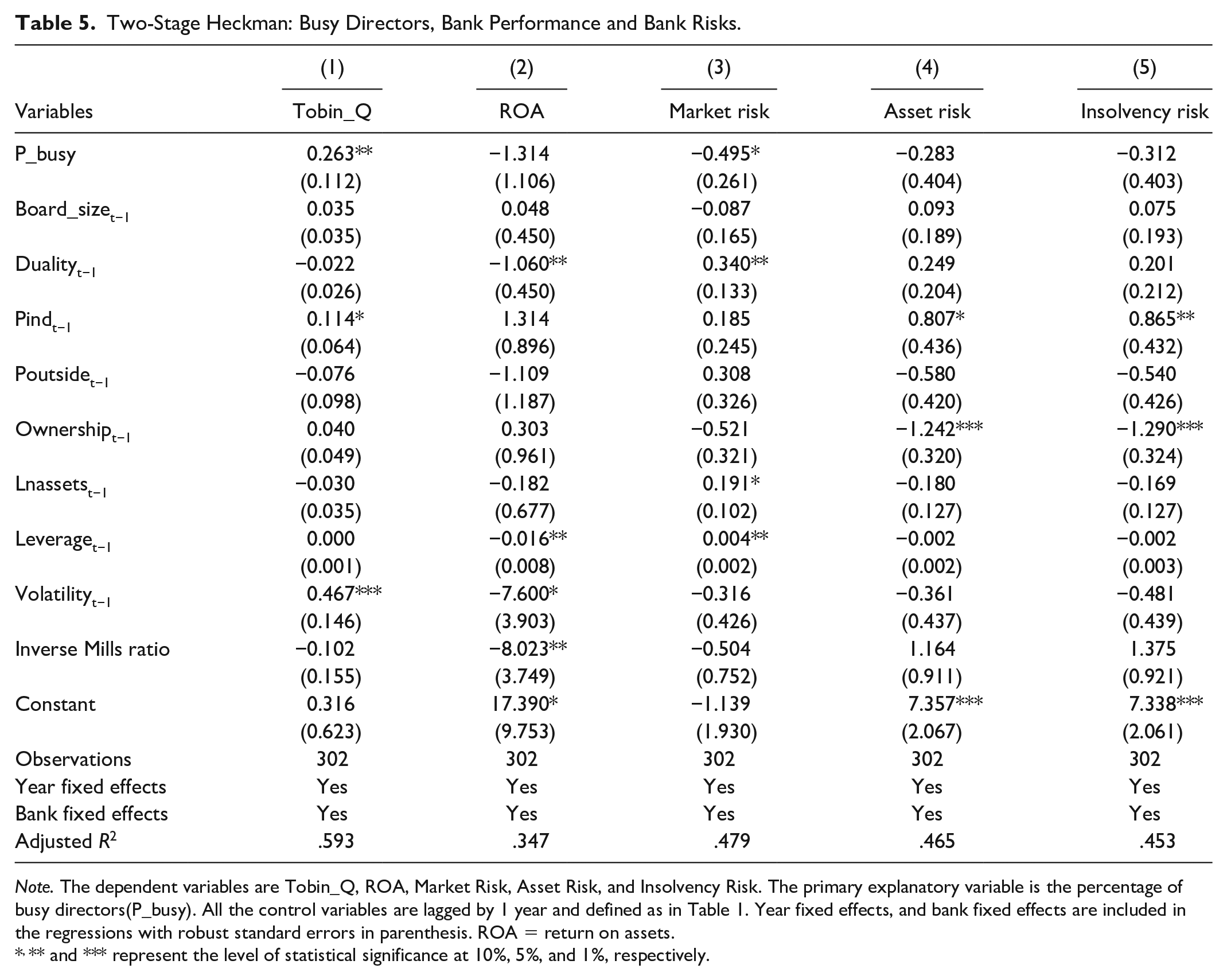

Self-Selection Bias

The study results reported so far may be spurious if there is self-selection bias. Selection bias arises when a non-randomly selected sample that does not represent the overall population is used for behavioral analysis (Heckman, 1979). For instance, the sample includes banks with different ownership types, different headquarters locations, and other different bank features, thus raising self-selection concerns. If these differences explain why some banks have busy directors in their boards, while other banks do not have busy directors then the study sample suffers from self-selection bias and can contribute to spurious results due to specification errors. Therefore, the study attempts to deal with the potential self-selection bias in the sample using the Heckman (1979) two-stage model. In the first stage, the study uses banks’ total assets, board size, headquarters location, year, and ownership type to find the probability of a bank choosing a busy director. In the second stage, the calculated inverse Mills ratio is used in the regressions to estimate the implications of busy directors on bank performance. The study reports the second stage results in Table 5. The second stage results after correcting for self-selection bias shown in Table 5 are comparatively the same with the previously reported results before correcting for selection bias. For example, the positive association of busy directors and Tobin Q has remained significant at 5% level, as shown in Column 1 of Table 5, but its magnitude has increased from 0.237 before correction, as shown in Table 3 to 0.263 after correction as displayed in Table 5 Column 1. The impact of busy directors on ROA reported in Table 5 Column 2 shows an insignificant negative sign as in Table 3 before correction, but the magnitude of the coefficient increased after correction. The coefficients of busy directors on bank risk measures, bank market risk, asset risk, and insolvency risk remain the comparatively the same after Heckman’s (1979) self-selection correction, as shown in Table 5. The association of busy directors and market risk is significant at 10%, while the impact of busy directors on asset risk and insolvency risk remain insignificant with the same signs. Overall, the study results after correcting for self-selection bias support the hypothesis that networked directors contribute to an increase in bank market value. However, the study does not report any association between return on assets and busy directors. Furthermore, the results suggest that busy directors are associated with low market risk, no effect on bank asset risk, and insolvency risk.

Two-Stage Heckman: Busy Directors, Bank Performance and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is the percentage of busy directors(P_busy). All the control variables are lagged by 1 year and defined as in Table 1. Year fixed effects, and bank fixed effects are included in the regressions with robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

Endogeneity

Studying the implications of busy directors on bank performance is challenging because of endogeneity issues in corporate governance studies (Demsetz & Lehn, 1985; Hauser, 2018; Wintoki et al., 2012). Endogeneity bias arises due to omitted variables, simultaneity problem and measurement error. Omitted bias exists when certain observable and unobservable variables that impact the dependent variable are omitted in the model, thus resulting in spurious results. The simultaneity problem or reversal causality bias arises when there is a two-way relationship between the dependent variable and the independent variable thus making it difficult to establish the direction of causality. Measurement error arises when proxy measures for unobservable variables or variables in the models fail to represent correctly what they intend to measure. The study first tries to deal with omitted variable bias by using bank fixed effects and lagged control variables to reduce reversal causality concerns. However, there is a likelihood that the results may still suffer from endogeneity because of the relationship that exists between bank performance and busy directors. For example, banks with poor performance and high-risk exposure may appoint more networked directors with more experience and high advisory reputation to increase firm performance (Adams et al., 2010; Abdelbadie & Salama, 2019; Elyasiani & Zhang, 2015).

The study follows Chakravarty and Rutherford (2017) and uses an event study as an identification strategy to deal with endogeneity and as an attempt to establish causality between busy directors and bank performance. There are two cohorts identified at the beginning of the study sample period; the first one is for banks that enter the sample period with at least one busy director, and the second one is for banks that enter the study period without a busy director. The study identifies the movement of a sub-sample of banks from zero busy directors to at least one busy director as an exogenous event. The banks which have no busy directors during the beginning of the study period but later include busy directors in their boards are selected as the treatment group. Those banks which do not have a busy director during the study period are used as the control group. Those banks which had busy directors in their boards before the study sample period are excluded to ensure that the results are robust. To make sure the results are reliable, the bank characteristics between the treatment banks and control banks do not have to be significantly diverse from each other. Hence, the study makes use of the Propensity Score Matching (PSM) to match the firms using total bank assets, year dummies, the board size, CEO duality, board independence, ownership, and leverage. After matching the treatment and control groups, the following regression model is used to estimate the performance implications from the switching of board status from zero busy directors to at least one busy director:

where the dependent variables are Tobin’s Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The main explanatory variable is Post × Treatment. Treatment encompasses all firms that switch from zero busy directors to at least one busy director. Post is the year of change from zero busy directors to at least one busy director. All the controls are as defined in Table 1. The study reports the event study results in Table 6.

Busy Directors, Bank Performance, and Bank Risks: Event Study.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is Post × Treatment. Post is the period after switching to at least one busy director. Treatment is a variable for firms that switch from zero busy directors to at least one busy director. Post is the year of change from zero busy directors to at least one busy director. All the control variables are defined as in Table 1. Robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

The results reported in Table 6 after the study’s attempt to address endogeneity concerns show qualitatively similar results with those previously reported for the primary explanatory variable (Post × Treatment). The coefficient for the primary variable (Post × Treatment), which measures the impact of the change in board status in Table 5, Column 1, is positive and significant at 10%. The study results suggest that switching of a bank board from zero busy directors to at least one busy director has a positive significant causal impact on bank market value. On the contrary, the results for return on assets are negatively insignificant.

Furthermore, the results in Table 6 Column 3 show that the market risk measure changes the sign from negative to positive, and it becomes insignificant when a board switches from zero busy directors to at least one director. Besides, the event study results in Table 6 in Columns 4 and 5 contrary to prior study findings reported using OLS estimation show that the coefficients of Post × Treatment for bank asset risk and insolvency risk are significant at 5% level which suggests that a change in board busy status from zero to at least one busy director contribute to an increase in bank asset risk and high probability of bankruptcy. The results suggest that the previously reported results using OLS estimation for risk measures are probably affected by simultaneity bias. This highlights the importance of giving attention to endogeneity issues in corporate finance research. Overall, the event study results show that busy directors contribute to an increase in bank market value and an increase in bank risks.

Bank Ownership

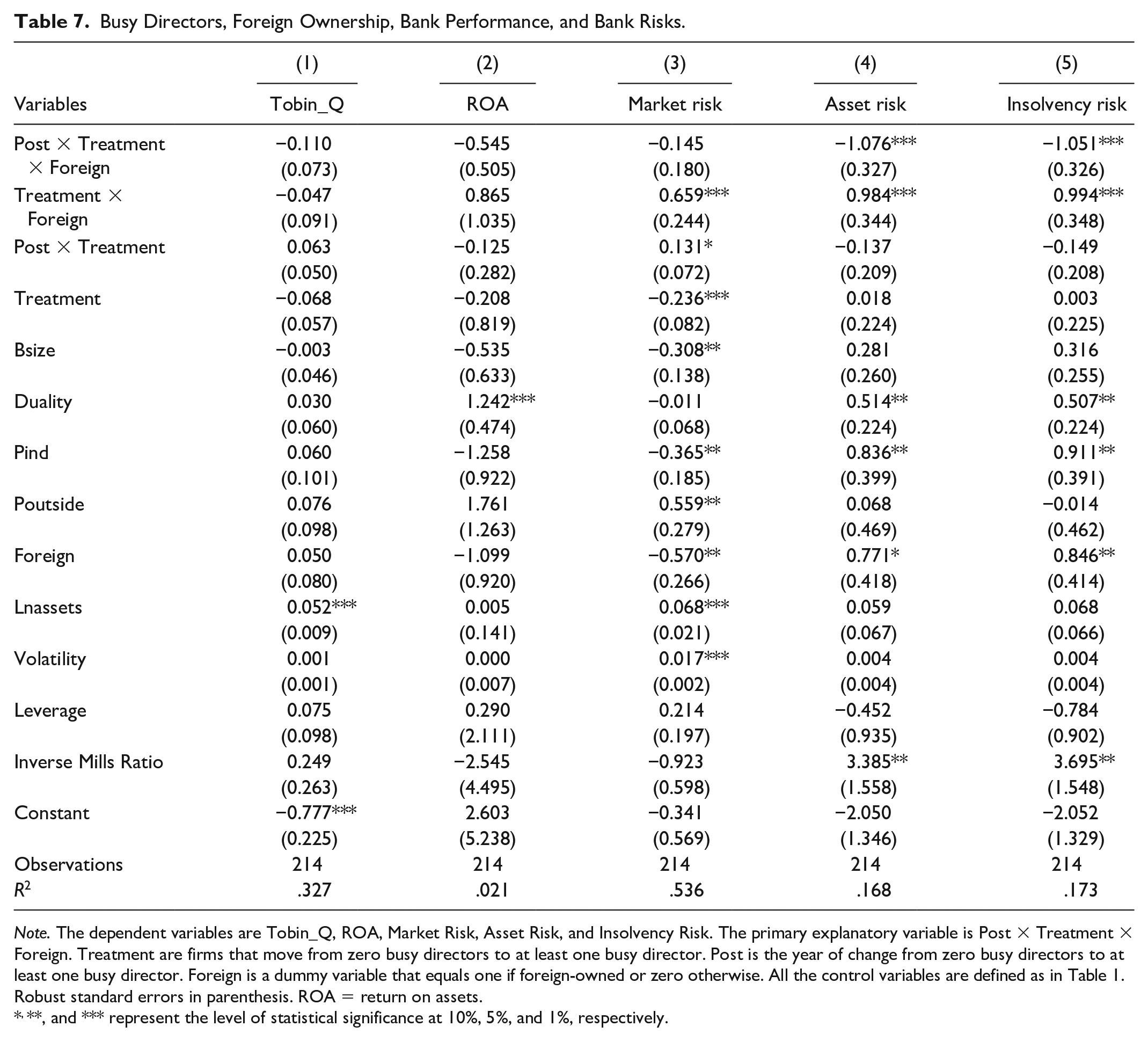

The study contributes to the extant literature by examining other channels through which busy directors influence bank performance. The study sample comprises foreign-owned firms, state-owned banks, and local private firms. Considering ownership type is essential when studying bank corporate governance systems, there is a likelihood that the firm ownership strongly influences governance and performance relationship. On the other hand, foreign-owned firms are associated with highly skilled and experienced personnel. Due to highly skilled and quality expertise, foreign-owned banks may have high advisory personnel and extensive monitoring mechanisms thus deeming the need for busy directors less important. However, state-owned firms are usually associated with low corporate governance systems, low profitability, and high risk (Cornett et al., 2010). Thus, the influence of busy directors in state-owned banks is likely to be different from privately owned banks. Experienced and highly reputable directors are likely to contribute to sound corporate governance systems in state-owned banks, which ultimately improve bank performance. State-owned companies usually suffer from inefficiencies and weak corporate governance systems, which usually trigger losses and insolvency in banks; hence, governments spend lots of money to bail out collapsing banks. Therefore, examining the implications of busy on bank stability in state-owned banks is very important for enhancing our understanding of board structure dynamics and for policy formulation. The study expects busy directors to reduce bank risk in state-owned companies.

Busy directors, foreign ownership, and bank performance

The results in Table 7 display negatively insignificant coefficients for all bank performance measures in Columns 1 to 2. This suggests that adding busy directors in foreign-owned bank boards does not affect the bank’s market value and profitability. The results also show that the presence of busy directors in foreign-owned bank boards does not affect market risk. In contrast, the results in Table 7 Column 4 suggest that busy directors contribute to high asset risk and high insolvency risk in foreign-owned banks. Besides, the coefficients of Treatment × Foreign are positive and significant in Table 7 for all risk measures at 1% significant levels, which suggest that foreign banks in the study sample had low risk before incorporating busy directors in their boards. Thus, there is some evidence that suggests that networked directors increase bank risk-taking in foreign-owned banks. Overall, the study results in Table 7 suggest that the presence of busy directors in foreign-owned banks increases bank asset risk and insolvency risk while posing no significant influence on bank performance and bank market risk.

Busy Directors, Foreign Ownership, Bank Performance, and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is Post × Treatment × Foreign. Treatment are firms that move from zero busy directors to at least one busy director. Post is the year of change from zero busy directors to at least one busy director. Foreign is a dummy variable that equals one if foreign-owned or zero otherwise. All the control variables are defined as in Table 1. Robust standard errors in parenthesis. ROA = return on assets.

, **, and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

Busy directors and state-owned banks

In a quest to deepen our understanding of multiple directorships, the study uses the effect of the triple interaction to examine how ownership type influences the associations between busy directors and bank performance. The study results in Table 8 show that the triple interaction coefficient (Post × Treatment × State) is positive and insignificant in Column 1 and Column 2. This signifies that busy directors do not significantly influence Tobin’s Q and return on assets in state-owned companies. The coefficient for market risk is negative but insignificant, which indicates that busy directors pose no influence on bank market risk. In contrast, the coefficients of the primary variable (Post × Treatment × State) in Column 4 and Column 5 of Table 8 are positive and significant at 5% levels. The evidence suggests that busy directors reduce bank asset risk and lowers the probability of insolvency in state-owned banks.

Busy Directors, State Ownership, Bank Performance and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is Post × Treatment × Foreign. Treatment represents firms that move from zero busy directors to at least one busy director. Post is the year of change from zero busy directors to at least one busy director. Foreign is a dummy variable equals to one if foreign-owned or zero otherwise. All the control variables are defined as in Table 1. Robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

Furthermore, the results in Table 8 in Columns 4 and 5 show that the coefficients for Treatment × State are negative and significant at 10% level suggesting that the state-owned had high bank risk before adding at least one busy director. Collectively, the study results show that adding networked directors on the board does not affect bank performance in state-owned banks but instead reduces bank asset risk and probability of bankruptcy.

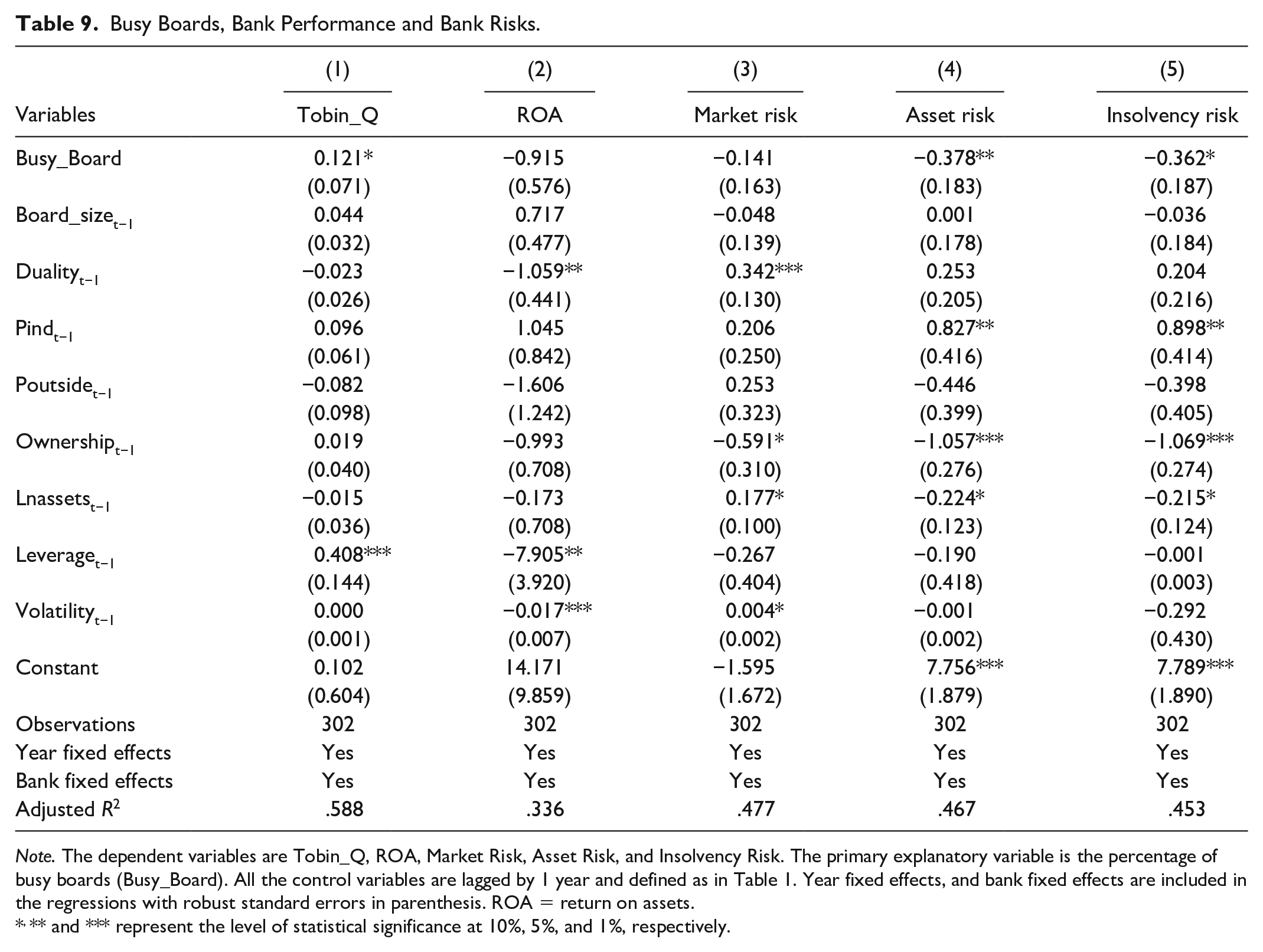

Robustness

In this section, the study tests the robustness of previously reported results using the busy board as an alternative measure for busy directors, and the results are reported in Table 9. Following prior literature, a busy board is defined as a board with at least 50% of the members who serve in three or more boards in any given period. The study results displayed in Table 9 using a busy board as the primary explanatory variable are comparatively similar to the previously reported results using the percentage of busy directors. For example, the coefficient for Tobin Q is positive in Table 9 Column 1 and significant at 10%, while in Table 9 Column 2, the results show that the return on asset is negatively insignificant. This suggests that busy boards promote an increase in a bank’s market value but exert no influence on bank profitability. The bank risk results in Table 9 Column 3 show that the bank’s market risk has no relationship with busy boards. In contrast, the coefficients for bank asset risk and insolvency risk in Table 9 Columns 4 and 5 are negative and significant at 5% level, thus indicating that busy boards are associated with high bank risk levels. Overall, the results support that busy boards contribute to an increase in bank market value measured by Tobin’s Q and an increase in bank risk.

Busy Boards, Bank Performance and Bank Risks.

Note. The dependent variables are Tobin_Q, ROA, Market Risk, Asset Risk, and Insolvency Risk. The primary explanatory variable is the percentage of busy boards (Busy_Board). All the control variables are lagged by 1 year and defined as in Table 1. Year fixed effects, and bank fixed effects are included in the regressions with robust standard errors in parenthesis. ROA = return on assets.

, ** and *** represent the level of statistical significance at 10%, 5%, and 1%, respectively.

Discussion and Conclusion

Since the financial crisis of 2008 to 2009 banks, there is an increased interest in corporate governance studies focusing on banks (Adams & Mehran, 2011; Elyasiani & Zhang, 2015). It is widely agreed that bank operations are very complex and opaque, which require high impact advisory personnel and extensive monitoring. However, recent researches are divided on whether busy directors impede or spur bank performance. Specifically, the research dependency theory supports the notion that networked directors improve firm performance while the agency theory identifies busy directors with weak firm performance. Thus, this study extends the flourishing bank literature on networked directors by examining the implications of busy directors on bank performance and bank risks in an emerging market. The study employs an event study as an identification strategy to obtain robust results; the paper treats the change of the bank board from zero busy directors to at least one busy as an exogenous event. Besides, the study makes use of the propensity score matching and the two-stage Heckman (1979) correction model for dealing with endogeneity concerns.

The overall study results show that the existence of busy members on the board positively and significantly affects bank market value. The study findings are in agreement with the resource dependency theory that posits that multiple directorships contribute to an increase in bank market value. The study findings on bank market value partially suggest that multiple directorships contribute to an increase in banks’ intangible resources in alignment with the reputational hypothesis. Besides, the study findings are consistent with several studies on networked directors that support a positive impact of busy directors on bank market value (Di Pietra et al., 2008; Elyasiani & Zhang, 2015; Pombo & Gutiérrez, 2011; Sarkar & Sarkar, 2009).

While the study shows that an increase in busy directors positively and significantly affects the bank’s market value (Tobin’s Q), the study evidence shows no effect on bank profitability (ROA). The plausible explanation of the results is that Tobin Q is a proxy measure for firm growth or investment opportunities, while ROA measures the internal bank profitability.

Moreover, on bank risks, the study shows that the increase in busy directors contributes to an increase in bank asset and insolvency risk after correcting for endogeneity. In contrast, the study evidence shows that busy directors contribute to low market risk in two models in agreement with Elyasiani and Zhang (2015); however, the coefficient loses significance after accounting for endogeneity using the event study as an identification strategy. The study findings seem to support the argument that busy directors in Brazil are overloaded and have little time to actively participate in corporate strategic decision making and to diligently monitor managers which results in high bank risks (Adams & Mehran, 2011; Cooper & Uzun, 2012; Kress, 2018; Nguyen et al., 2015). Another possible explanation given the familial ties and friendship ties in Brazil is that the busy directors may be closely related to the management which compromises their oversight duties in protecting shareholders from managerial opportunism.

Furthermore, the study identifies two mechanisms that influence the effect of busy directors on bank performance. The study documents that the presence of busy directors in foreign-owned bank boards contributes to an increase in bank asset risk, and the probability of bankruptcy, however, poses no effect on Tobin’s Q, ROA, and bank market risk. As expected, the study results suggest that the inclusion of busy directors in state-owned bank boards contributes to a decrease in bank asset risk and insolvency risk while posing no influence on bank performance. The plausible explanation of the results is that networked directors bring in the much-needed advisory quality and extensive monitoring in state-owned banks. State-owned banking institutions may benefit from busy directors due to external regulatory monitoring mechanisms that force directors to challenge management against self-dealing activities. State institutions have specific regulatory governance requirements that are applicable state owned banks only, thus maybe another plausible reasonable why multiple directorships benefit state-owned banks as compared to private-owned banks.

Collectively after a series of robust checks and accounting for endogeneity, the study, in contrast to Elyasiani and Zhang (2015), contributes to the extant literature by showing that busy directors contribute to a trade-off between bank market value and low bank risk. The substitution hypothesis between bank market value and bank risk is persistent throughout the study in most of the models. For example, networked directors contribute to high bank market value and high bank risk in the general sample after accounting for endogeneity. The plausible explanation for the study finding is that busy boards in Brazil may serve as reputational devices which boost investor perception and bank market value while bank risks increase due to low director monitoring abilities to assess bank strategies and risks due to work overload and inadequate time. The study findings resonate with the agency perspective of over boarded busy directors who have little time to perform their governance responsibilities, thus endangering bank holding institutions.

The study findings have some policy implications for regulators and investors. Given that the study findings show that the increase in busy directors in banks improve bank market value but at a trade-off with high bank risk, the study does not recommend multiple directorships in highly distressed banks and foreign-owned banks. Based on research evidence, this study recommends increasing busy directors in state-owned banks that mainly care about bank stability rather than profitability and have strict external regulatory monitoring standards for board of directors.

The negative impact of multiple directorships on bank risk may be an indication of overloaded directors with less time for effective monitoring. Thus, even though reputable busy directors may be beneficial for learning and networking opportunities, sitting in too many boards may diminish their monitoring capacity thus contributing to excessive bank risks. Given a weak institutional environment in Brazil, extensive monitoring of the management is critical rather than a board reputation. Therefore, regulators in Brazil need to implement some mechanisms to measure the participation of busy directors in banks they serve to promote efficiency and institute accountability apparatuses to deal with any negligence by the board of directors in accomplishing their duties.

Even though the study does not recommend a specific limit on the number of directorships, bank regulators in developing countries like Brazil with weak legal institutions should detect and curb excessive participation of directors in multiple boards in the banking industry. Reducing excessive participation for busy directors serving in bank boards ensures that the directors have adequate time and attention to discharge their governance responsibilities, thus resulting in robust risk monitoring strategies in bank operations. Therefore there is a need for regulatory authorities to set strict standards with supervisory expectations that guide the selection of multiple directors and enforce feedback mechanisms that govern busy directors in Brazil.

This study paper focuses on listed banks only in Brazil due to data restrictions; therefore, the results should be interpreted in this context. Considering the importance of governance in banks in both developed nations and in emerging markets, it will be beneficial for future researches to conduct cross country studies comparing the impact of busy directors on bank performance in emerging markets and in developed countries.

Footnotes

Acknowledgements

I thank the editor and three anonymous reviewers who helped to improve this paper. I would also like to extend my thanks to Professor Fengrong Wang. All the errors and mistakes that remain are mine.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.