Abstract

This article examines the linear and non-linear relationships between environmental, social, and governance (ESG) performance and bank risk-taking in developed and emerging economies, with a focus on the moderating effects of environmental uncertainty. This paper employs a cross-country unbalanced sample of 315 listed banks in China and the USA over the 2011 to 2022 period. The authors employ a two-step generalized methods of moments (2sGMM) regression model to mitigate potential endogeneity issues. The two-stage least squares (2SLS) regression technique was also used for the robustness check. The findings disclose a significant negative relationship between ESG performance and bank risk-taking, highlighting that higher ESG performance generally mitigates risk exposure. Additionally, the analysis shows a non-linear, U-shaped relationship, suggesting that while ESG practices initially reduce risk, there is a threshold beyond which the benefits diminish. Moreover, environmental uncertainty significantly moderates the ESG performance-risk-taking nexus, especially in the Chinese banking sector. These findings highlight the trade-offs between enhancing sustainability practices and managing external volatility. These findings embrace the robust results after using alternative methods and individual components of ESG performance. This article also contributes to the growing body of literature by providing valuable policy insights into the importance of ESG consideration in enhancing bank stability while navigating global uncertainties.

Plain Language Summary

This study analyzes how banks’ ESG performance affects risk-taking using data from China and the US. We find that stronger ESG performance lowers risk, but only up to a point. Environmental uncertainty can weaken this effect, especially in China. Overall, ESG helps promote bank stability, but its impact depends on changing external conditions.

Introduction

The banking sector is a pivotal part of maintaining financial stability and contributing to the sustainable development of the economy on national and global levels (Perdana et al., 2023). Banks not only provide capital and credit but also play the role of key agents in the process of encouraging sustainable business performance by investing and granting credit (Cregan et al., 2024). In the last few years, Environmental, Social, and Governance (ESG) performance has attracted increasing interest because of climate change, sustainability, and social justice issues (C. Li et al., 2024; Vu, 2025). ESG initiatives have become a significant concern for investors, regulators, and academic researchers to influence sustainable business models, manage risks, and achieve better and sustainable financial performance (Atif & Ali, 2021; Shakil, 2021). Governmental and regulatory authorities are also accelerating pressure on the companies to implement policies that are socially and environmentally sustainable, arguing for stakeholder value, such as investors, consumers, employees, and the public, over and above the shareholder value (G. He et al., 2023; Houston & Shan, 2022). Therefore, firms that adopt ESG performance in their business models can achieve competitive advantages (Mohammad & Wasiuzzaman, 2021) and sustainable development prospects in both developed and emerging economies (Vodenska et al., 2022). Due to this influence, it is expected that banks should adopt ESG factors into their business since it will affect their risk profile and strengthen them in the face of economic shocks.

As the two largest economies in the world, China and the United States are integral to current financial markets and sustainable business finance. Each of the countries is experiencing different difficulties in integrating ESG factors into the existing economic and legal environment. These tendencies prove the significance of ESG practices that guarantee organizational sustainability and effectiveness. Therefore, firms have no option but to embrace ESG factors to gain investors’ confidence, manage corporate risks, and achieve sustainable financial performance, particularly in the banking industry. At present, sustainability and transparency are important factors; thus, banks must incorporate ESG performance to mitigate the reputational risk and guarantee a competitive advantage in the global business environment. Thus, by implementing highly developed ESG standards, banks not only protect themselves against losses due to environmental and social issues but also guarantee their future sustainable financial performance (Sain & Kashiramka, 2024). Furthermore, the emphasis on the world’s two largest economies is justified because these countries demonstrate contrasting ESG strategies, which reflect the differences in the legal frameworks, culture, and market demands. Although ESG activities are primarily market-led in the US banking sector and include social and governance factors in addition to the environmental issue, Chinese ESG activities are controlled by government regulations with an emphasis on the environmental issue (Bagh, Zhou, et al., 2024). ESG performance has thus become linked to bank risk in both countries, although the process and factors leading to this integration may vary (Bagh, Fuwei, & Khan, 2024). This research aims to establish the relationship between ESG performance and bank risk-taking in the largest economies, including China and the USA. Considering these two economies, this study offers valuable policy insights into how ESG performance affects bank risk-taking across different corporate environments. The study underscores that the regulatory authorities and institutional frameworks in China and the USA shape the ESG performance that significantly impacts bank risk-taking, which in turn ensures sustainable financial performance. While the ESG performance in the Chinese economy is evolving and needs to establish unique disclosure standards, the US economy has structured sustainable performance. Despite growing investor interest in ESG disclosure, there is still academic debate regarding the extent to which ESG engagement influences financial stability and firm performance.

Although the relationship between ESG performance and firm risk-taking has received considerable attention (Anwer et al., 2023; Khorilov & Kim, 2024; E. X. Liu & Song, 2025), few studies have been conducted on how ESG practices specifically affect bank risk in different geopolitical contexts (Gangwani & Kashiramka, 2024; Izcan & Bektas, 2022; Korzeb et al., 2025). However, sustainable investment has been gaining attraction in many developed and developing countries as a way to not only boost bank performance but also to improve overall financial stability (Bagh, Fuwei, & Khan, 2024; Singhania & Saini, 2023). Indeed, most of the studies have extensively investigated the consequences of ESG disclosure, such as the effect of ESG initiatives on firm performance (Agarwal et al., 2023; S. Chen et al., 2023; S.-P. Lee & Isa, 2023), financial stability (Chiaramonte et al., 2022; Lupu et al., 2022), corporate solvency (Yu & Su, 2024), firm value (Bagh, Fuwei, & Khan, 2024; Perdana et al., 2023; F. Zhang et al., 2020), cost of capital (Bhuiyan & Nguyen, 2020; Priem & Gabellone, 2024), cost efficiency (Chang et al., 2021), green innovation (H. Liu & Lyu, 2022; Zhai et al., 2022), and so on. Furthermore, in some of the studies conducted by Anwer et al. (2023), Baldi and Lambertides (2024), and Ding et al. (2025), the relationship between ESG performance and firm risk-taking has been extensively examined in non-financial sectors. Moreover, few studies have been conducted on the relationship between ESG performance and bank risk-taking (Di Tommaso & Thornton, 2020; Gao, 2024; Izcan & Bektas, 2022; Neitzert & Petras, 2022), there is limited empirical research that particularly examines the ESG performance-bank risk-taking nexus, which has not been extensively studied until now. The emphasis on banks is relevant because the financial sector plays a pivotal role in the shift toward a resource-efficient economy. They also play an important role in promoting economic growth by accelerating capital formation, which makes them essential for this process of transformation (Chiaramonte et al., 2022; Teng et al., 2021). In addition, this study includes the moderating effect of environmental uncertainty (ENVU), which remains largely unexplored in corporate finance and economics literature. To bridge these research gaps, this study used data from 2011 to 2022, covering both stable and crisis periods, and aims to empirically evaluate the effects of ESG performance on bank risk-taking in the US and Chinese banks, with a particular focus on the moderating role of ENVU.

Despite many studies addressing the relationship between ESG performance and firm risk (Giannopoulos et al., 2022; G. He et al., 2023; J. Lee & Koh, 2024), this is the first to consider the banks in emerging and developed economies like China and the USA. So, the first objective of the study is to investigate the effects of ESG performance on bank risk-taking in both China and the USA. In this study, the authors also evaluate the non-linear impact of ESG performance on bank risk-taking, which is the second objective of the study. However, the impact of ESG issues on bank risk-taking is influenced not only by regulatory structures and market dynamics but also by external factors such as environmental uncertainty. Although the influence of ENVU on firm performance is significant (W. Wang et al., 2023), the literature lacks clear evidence on the interaction effect of environmental uncertainty on the ESG performance-bank risk-taking nexus. Hence, this study also investigated the moderating effects of environmental uncertainty on the nexus. Considering the environmental uncertainty, the third objective of the study is to examine the moderating effect of environmental uncertainty on the relationship between ESG strategies and bank risk-taking between the two world-leading economies. The pandemic has only intensified stakeholder oversight of corporate accountability, and banks in particular have felt the pressure to maintain robust ESG factors to avoid adverse effects (Anwer et al., 2023; Bolibok, 2024). ESG performance in the COVID-19 period may help protect banks from reputational and operational risks, while low ESG scores increase their sensitivity to reputational risks (Broadstock et al., 2020; Galletta et al., 2023). Therefore, the fourth research question is to determine the extent to which COVID-19 moderates the relationship between ESG performance and bank risk-taking with particular reference to this relationship in the two largest economies globally.

To the authors’ knowledge, this study is the first attempt to examine the relationship between ESG performance and bank risk-taking for a sample of 315 banks between 2011 and 2022 across China and the USA. The data was composed from the Refinitiv Eikon DataStream from the year 2011 within the banking industry. This timeframe allows the study to capture essential changes in the global corporate governance and sustainability standards, such as the implementation of the Paris Agreement and the UN Sustainable Development Goals, that have influenced the ESG standards post-2015. Starting the analysis in 2011 also enables the author to look at changes and trends in ESG performance and bank risk-taking over 12 years. Additionally, data up to 2022 accounts for the impact of COVID-19, enabling the study to reflect both stable and crisis periods. The aim is to investigate the direct impact of ESG factors on bank risk-taking, as well as the moderating effect of environmental uncertainty and COVID-19 on the nexus. Second, previous studies have predominantly concentrated on manufacturing and related sectors in some developed (Erol et al., 2023; Sandberg et al., 2023) and developing (Maji & Lohia, 2023; Z. Wu & Chen, 2024) countries. However, no study shows a comparative analysis of the ESG-bank risk-taking nexus between developed and developing countries. Moreover, previous studies did not show the moderating effect of ENVU on the nexus. Thus, our research is pioneering in its focus on the world’s two largest economies, China and the USA, examining the ESG performance-bank risk-taking nexus. Finally, this study mainly used 2sGMM (Q. Chen & Shen, 2024; Khatib et al., 2022; Zheng, Khan, et al., 2023) and 2SLS-IV (Banna et al., 2021; Zheng, Rahman, et al., 2023) to overcome the endogeneity, heteroscedasticity, and autocorrelation issues and investigate the relationship between ESG factors and bank risk-taking. This research seeks to lay the foundation for governments, central banks, investors, practitioners, and academic researchers to reconfigure market policies, considering ESG performance for long-term sustainability.

The remainder of this paper is structured as follows: Literature review displays a comprehensive literature review on the nexus between ESG performance and bank risk-taking, with particular emphasis on the moderating effects of environmental uncertainty. Research methodology outlines the research methodology and data sources. Next Section presents empirical results and discussion, Next Section highlights the discussion and policy implications, and Final section concludes the study.

Literature Review

This part provides an extensive analysis of the literature on the association between ESG performance and bank risk-taking, highlighting the potential moderating effect of environmental uncertainty. First, we discuss the background of this research, and then, we review the literature on ESG practices and bank risk-taking. In light of agency theory, legitimacy theory, and risk management theory, this review develops a framework that captures the external factors that affect the ability of ESG practices to manage bank risk-taking. The proposed hypotheses are an important starting point for empirical analysis; the study’s goal is to determine how ESG performance and environmental uncertainty affect bank risk-taking in China and the United States.

As research has found, ESG performance affects operational efficiency and risk-taking because sustainable methods are efficient and minimize risks. ESG best performers are associated with higher investment and lower risk, while ESG worst performers are associated with financial and reputational risks. The nexus between ESG initiatives and bank risk-taking is still relatively understudied, especially concerning the current increased environmental uncertainty and the COVID-19 environment. Financial institutions, particularly in China and the United States, have become sensitive to the changes in the regulatory environment and social norms. ESG practices are a significant aspect of the risk management framework for banks because failure to consider social and environmental factors may lead to regulatory, reputational, and operational risks. This research aims to understand the relationship between ESG activities and bank risk-taking in China and the USA, with the moderating roles of ENVU. In business organizations, the management (agents) is assigned the responsibility of performing daily tasks and making strategic decisions (Zheng et al., 2024). However, agents may self-serve at the expense of shareholders, hence creating a conflict of interest between management and shareholders. There are two contrasting views in the literature about the relationship between sustainability and the stability of banks (Chiaramonte et al., 2022; M. S. Rahman et al., 2024; Sendi et al., 2024). The agency perspective implies that the implementation of ESG policies can decrease the risk of business because cooperation with stakeholders and the promotion of financial sustainability become the priorities for companies. However, the extant research still lacks evidence on how the institutional distance between the United States and China affects the extent to which ESG performance reduces agency costs, especially under circumstances with ESG controversies and environmental turbulence.

Conversely, legitimacy theory postulates that ESG activities are adopted to improve the organizational image and legitimacy of banks to key stakeholders, including the regulators, customers, and society, especially given the growing calls for sustainable and ethical corporate governance. However, there is a theoretical gap regarding how different societal norms and expectations in these two economies influence the legitimacy gains of ESG performance, more so when environmental uncertainty increases due to crises such as the pandemic. Moreover, risk management theory emphasizes that ESG performance is a strategic approach to managing environmental and social risks. Banks that practice good ESG risk and returns management are more likely to protect themselves against losses resulting from financial, reputational, and operational risks during environmental volatility. However, the impact of the two environmental dynamics on the moderating role of environmental uncertainty on the ESG performance-bank risk-taking relationship remains unexplored in both countries. Altogether, these theoretical viewpoints offer a rich theoretical background for explaining the effects of ESG practices on bank risk-taking in two of the largest economies of the world, with moderating roles of ENVU. Much research has examined the link between ESG performance and bank risk employing different theoretical perspectives. This paper aims to investigate the impact of ESG performance on bank risk-taking in China and the USA, and how ENVU affects these nexuses. Through examining these dynamics, this paper aims to provide policy implications for the shifting nature of ESG performance in international financial systems.

ESG Performance and Bank Risk

ESG factors are now more apparent in the international banking sector since stakeholders realize the importance of sustainable and responsible corporate actions. The banking sectors of China and the USA function under different legal, social, and economic environments, so the connection between ESG factors and bank risk-taking must be learned to manage risks and develop sustainable banking systems. This relationship, however, is not straightforward and may be influenced by several factors, including the country of operation, regulatory environment, and others. ESG factors can be contingent because they can affect the risk profiles of banks by subjecting them to ESG risks. For instance, climate change risks affecting the physical environment of borrowers may affect loan portfolios through physical loss, changes in regulatory requirements, and reputational issues (Neitzert & Petras, 2022). Other social risks, such as labor unrest or community issues, may negatively impact the customers’ perception and consequently brand image (Trinh et al., 2023). This means that internal and external governance factors, especially board independence and transparency, affect the quality of risk management and regulatory compliance (Abdul Razak et al., 2023).

Previous research has produced mixed results concerning the relationship between ESG performance and financial risk. A few works have reported a negative, positive, mixed, or insignificant relationship between ESG performance and firm risk-taking in various industries and countries (Shakil et al., 2019). In general, most of the literature provides ambiguous evidence regarding the association between ESG performance and firm risk-taking. For example, studies by Suttipun (2023), Naseer et al. (2024), Izcan and Bektas (2022), and Nirino et al. (2022) found a negative relationship between ESG performance and bank risk, indicating that banks with stronger ESG practices exhibit lower levels of credit risk and operational risk. Di Tommaso and Thornton (2020) reveal a negative relationship with quarterly data of 81 banks in 19 European economies from 2007Q3 to 2018Q4, utilizing CDS spread, Z-score, and Non-performing loans as risk proxies. In addition, F. He et al. (2023) offer evidence with Chinese listed firm-level data between 2010 and 2020 and find a negative correlation between ESG rating and corporate risk-taking. Similarly, Landi et al. (2022) demonstrated the positive impact of ESG integration on corporate financial risk using a 5-year longitudinal study from 2014 to 2018 on the Standard & Poor’s index. The studies showed a U-shaped by Korinth and Lueg (2022), and an inverted U-shaped by Anwer et al. (2023), De la Fuente et al. (2022), and Pistolesi and Teti (2024) between the nexus. However, Murata and Hamori (2021) found an insignificant association between ESG factors and stock price crash risk, suggesting that in certain circumstances, ESG performance may not significantly influence risk management practices. This inconsistency in results across different studies and markets underscores the relationship between ESG performance and risk-taking, particularly in large, dynamic economies like China and the USA, where regulatory frameworks and stakeholder expectations vary widely (Maiti, 2021; Shakil, 2021). Therefore, our first hypothesis is as follows:

Non-Linear Relationships in ESG and Finance

Although some studies have been conducted on ESG initiatives in the banking industry (Azmi et al., 2021; Menicucci & Paolucci, 2023; Sain & Kashiramka, 2024), there remains a gap in empirical studies that particularly examine ESG performance and risk-taking behavior within this sector. Most of the studies focus on single-country analyses and linear relationships using traditional accounting risk metrics. This study addresses these limitations by incorporating a non-linear regression to investigate the connection between ESG consideration and risk-taking across listed banks in two world-leading countries. Despite the growing body of finance literature on the relationship between ESG issues and bank risk, several gaps warrant further investigation, particularly in the context of China and the USA. Hence, it is imperative to do more empirical research that particularly investigates the link between ESG performance and the risk in the banking industry to address this gap in the existing body of knowledge. Based on the theoretical rationale and empirical evidence, the following hypothesis is recommended:

The Moderating Role of Environmental Uncertainty

The growing interest in ESG performance in the banking sector suggests its capability to help reduce financial risks in line with the stakeholders’ demands for sustainable practices. Over the past few years, Chinese and US banks have experienced increasing pressure to implement ESG practices due to growing regulatory concerns about environmental and social problems (Bagh, Fuwei, & Khan, 2024). Consequently, ESG performance is a key driver for banks that want to build trust and stability in an industry where reputational risk is very high (Izcan & Bektas, 2022). Nevertheless, the increasing incidence of climate change and new rules and regulations have made it necessary for banks to adopt new, effective risk management techniques. In China, where the government supports high climate goals, the threats arising from environmental factors are critical for banks to adhere to these policies to avoid sanctions and financial risks (Bagh, Zhou, et al., 2024). There is also a higher level of ENVU that surrounds firms’ risk-taking in both countries due to the unpredictability of regulatory changes or climate risks to long-term ESG investments. Therefore, the banks that manage this uncertainty by adopting ESG strategies to deliver efficient investment and mitigate risks concerning the uncertain environment (Di Tommaso & Thornton, 2020).

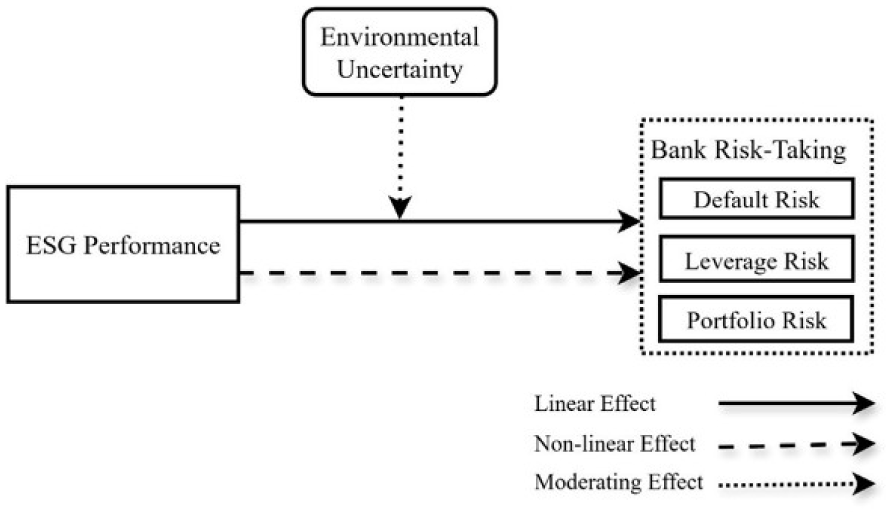

The previous studies recognize the ability of ESG performance to reduce financial risk by enhancing the level of disclosure, building credibility, and meeting the standards of stakeholders (Fu et al., 2024). Research shows that companies with sustainable ESG strategies are considered less risky, and their equity gains more investors’ confidence and customer patronage (Anwer et al., 2023). However, environmental uncertainty, such as natural disasters, unpredictable events, changes in the regulatory structure, and scarce resources, may weaken or strengthen the negative affiliation between ESG disclosure and financial risk. Furthermore, studies across different sectors have revealed a strong positive relationship between environmental uncertainty and various variables, including financial performance (Singh, 2020), ESG performance (Bin-Feng et al., 2024; W. Wang et al., 2023), corporate innovation (Deng et al., 2022), supply chain performance (Inman & Green, 2022), and corporate investment (K. Li et al., 2021). Furthermore, some studies employed environmental uncertainty as the moderating variable on the relationship between corporate environmental performance and corporate financial performance (Y. Zhang et al., 2020), innovation dimension and firm performance (Kafetzopoulos et al., 2020), external involvement and green product innovation (Zhao et al., 2018), corporate social responsibility and financial investment (Ul Huq et al., 2016; Zhuang & Duan, 2025). However, no study has been conducted on the moderating effect of environmental uncertainty on the nexus between ESG performance and firm risk-taking. However, limited research addresses the nexus between ESG performance and bank risk-taking in comparing the different economies. Despite extensive research on ESG and financial risk, the moderating impact of ENVU in the banking sector remains underexplored. By exploring this moderating effect, we aim to fill a critical gap in understanding how banks can leverage ESG performance to mitigate risk in volatile environments. Therefore, we hypothesize that environmental uncertainty moderates the relationship between ESG score and bank risk-taking, potentially diminishing the effectiveness of ESG efforts under volatile conditions (Figure 1). Based on the above, we propose the following hypothesis:

Conceptual model.

Research Methodology

Data Source and Sample Selection

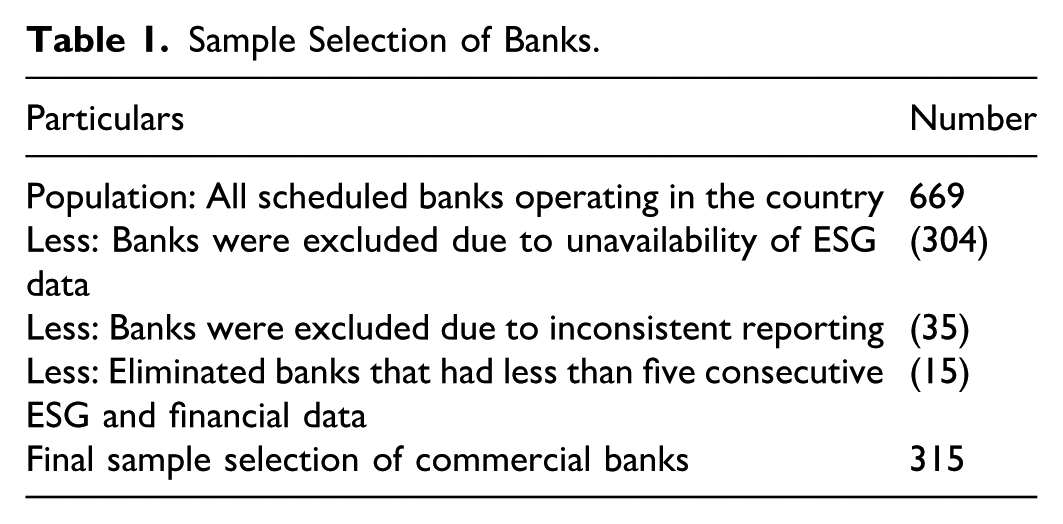

To analyze the moderating influence of environmental uncertainty (ENVU) on the relationship between ESG performance and bank risk-taking in China and the United States, we mainly used secondary data, especially the unbalanced dataset. The United States has the highest number of banks, representing 90.79%, and China has 9.21% respectively (Galletta & Mazzù, 2023). The sample dataset represents a broad cross-section of the banking industry in both countries, encompassing large national banks and regional/local banks, thus offering a comprehensive view of the ESG performance and risk-taking dynamics in these major global economies. We considered the panel dataset to include a sample consisting of 315 listed banks, including 3,708 bank-year observations spanning from 2011 to 2022. We considered this period the most recent five consecutive years when writing the paper. The year 2011 was selected as the starting point as it marks the period following the highest impact of the financial crisis. This period also allows for analysis of how the fluctuations in an environment (e.g., the COVID-19 pandemic) affected the ESG performance-bank risk-taking nexus. To test our hypotheses, we begin by retrieving data on ESG scores and bank-level control variables from the Refinitiv Eikon DataStream database, which has already been used extensively in previous research (Anwer et al., 2023; Bissoondoyal-Bheenick et al., 2023; Shakil, 2021). We also sourced our macroeconomic data from the “World Development Indicators.” Refinitiv Eikon, complemented by DataStream, is a highly regarded international database offering extensive financial and accounting data. At first, we considered all banks in two countries that follow the ESG disclosure. However, to mitigate potential sample selection bias, specific criteria were applied to create the final list of banks (Table 1). Winsorization is applied to all continuous variables at the 5th and 95th percentiles to minimize the impact of outliers. The final dataset reports all values in thousands of USD.

Sample Selection of Banks.

Variable Definitions and Measurement

Independent Variable (ESG Performance)

ESG performance serves as the independent variable, measured by the ESG combined score that evaluates a firm’s environmental, social, and governance practices based on data from the Refinitiv Eikon database, a source extensively used in previous research (Kolsi et al., 2023; Shakil, 2021; Yuen et al., 2022). This combined score encompasses 68 environmental, 62 social, and 56 corporate governance indicators, resulting in a total ESG score ranging from 0 to 100 (Refinitiv Eikon, 2023). The environmental dimension includes 20 metrics for resource use, 28 for carbon emissions, and 20 for green innovation. The social dimension covers 30 metrics for the workforce, 8 for human rights, 14 for community, and 10 for product responsibility. Governance metrics comprise 35 measures for management, 12 for shareholder rights, and 9 for CSR strategy. According to Refinitiv Eikon, an ESG score between 0 and 25 reflects poor comparative performance, while scores from 75 to 100 indicate outstanding performance. This study relies on the Refinitiv ESG score, which is recognized as one of the most trusted, reputable, reliable, and comprehensive databases for ESG metrics (Anwer et al., 2023; Bătae et al., 2021).

Dependent Variables (Bank Risk-Taking)

Consistent with the previous literature (Banna et al., 2021; Danlami et al., 2023; Hakimi et al., 2022), we measure risk-taking using (i) default risk (DRISK), (ii) leverage risk (LRISK), and (iii) portfolio risk (PRISK). To assess default risk, we utilize the Z-Score, a commonly applied measure in relevant research such as that by Danisman and Tarazi (2020) and Galletta and Mazzù (2023). Risk-taking is conceptualized as the inverse of bank stability, meaning that a higher (lower) level of risk-taking reflects a lower (higher) degree of bank stability. The formula for the Z-score is provided in Equation 1 as follows:

Where ROA represents a total return on total assets, EQTA is total equity to total assets, and (ROA) denotes the SD of ROA. We use a 3-year rolling period to capture variations in the Z-score. Specifically, DRISK directly reflects financial stability, with higher values signifying increased stability (Banna et al., 2021). Here, DRISK measures the likelihood of a borrower failing to meet debt obligations, used as a proxy for bank stability; multiplying DRISK by (−1) implies that lower DRISK values indicate reduced default risk and thus higher stability. Further, the Z-Score components include leverage risk (LRISK) and portfolio risk (PRISK). LRISK, measured by Ln[EQTA/σ(ROA)] × (−1), captures the risk associated with the bank’s leverage. PRISK, measured by Ln[ROA/σ(ROA] × (−1), pertains to risks arising from the composition and quality of the bank’s assets. Together, these metrics provide a comprehensive view of a bank’s risk profile.

Moderating Variables

Environmental uncertainty (ENVU): This research applies the method which was proposed by Ghosh and Olsen (2009) to define environmental uncertainty as the industry-adjusted standard deviation (SD) of the residual sales revenue over five consecutive years. To measure environmental dynamism, the stable growth component should be eliminated, and the fluctuation of the sales revenue of the firm over the last 5 years should be taken. This approach has been adopted in subsequent research (Bin-Feng et al., 2024; K. Li et al., 2021). The formula is as follows:

Revenue is the operating revenue in the banking sector in the given years, and Year is the annual variable, where the current year has been assigned 5 and the previous year 4, and so on in a backward manner. In this case, φ1 is the regression coefficient and ε is the regression standard error. In model (2), the bank’s operating income for the past 5 years is used to calculate the ENVU, sequentially calculating the abnormal operating revenue for these years. Next, the standard deviation of these abnormal service values over 5 years is calculated and divided by the average bank operating revenue over the same period, yielding an initial measure of environmental uncertainty (ENVU) without industry adjustments. To account for industry-specific factors, this unadjusted measure of environmental uncertainty is further normalized using the method developed by Ghosh and Olsen (2009). Specifically, each bank’s unadjusted ENVU is divided by the median unadjusted environmental volatility of all companies within the same year and industry, producing an adjusted measure of corporate ENVU. A higher adjusted ENVU value indicates greater environmental volatility, reflecting the impact of external fluctuations on a company’s operational environment and performance. This adjusted ENVU metric is used in this study to give a better measure of the external volatility that impacts business stability.

Control Variables

Based on previous significant studies (Abdelkader et al., 2024; M. M. Rahman et al., 2015; W. Wang et al., 2023; Zheng, Chowdhury, et al., 2023), this study controls for bank-level, governance, and macro-level variables, including bank size (SIZE), cost-to-income ratio (CIR), Tobin’s Q (TobinQ), Cash ratio (CASH), board size (BS), independent board member (IBM), CEO duality (CEOCD), GDP growth rate (GDP), and inflation rate (INF). Table 2 outlines the variables with their symbols, measurements, references, and sources.

Variable Definitions and Measurement.

Note. Refinitiv = Thomson Reuters’ Refinitiv Database; WDI = World Development Indicators.

Econometric Methodology

Following Bagh, Fuwei, and Khan (2024), Zheng, Rahman, et al. (2023), and Abdelkader et al. (2024), the 2sGMM method developed by Arellano and Bond (1991) is used in this paper to provide efficient and consistent estimates of parameters. This method addresses the potential endogeneity caused by omitted variables, reverse causality, and simultaneity. This method could consider unobserved factors, considering the lagged value of dependent variables as an instrument that highlights the problem of serial correlation and unobserved heterogeneity. This model is better, which allows different diagnostic tests, such as AR(1), AR(2), and the Hansen test, to ensure model validity and robustness. AR(1) and AR(2) are Arellano-Bond tests for first-order and second-order autocorrelation in the model’s residuals. The Hansen test examines the instruments’ validity and over-identification, assessing whether the instruments are exogenous. A high p-value suggests that the instruments are valid, indicating no correlation between the instruments and the residuals (Arellano & Bover, 1995; Bagh, Fuwei, & Khan, 2024; Yuen et al., 2022). STATA 17 software is employed to carry out the statistical analysis.

Equation 3 tests the association between ESG performance and bank risk-taking, considering other control variables based on prior literature (Baldi & Lambertides, 2024; Fu et al., 2024).

Where RISK is measured by the three proxies, such as DRISK, PRISKL, and RISK, as the dependent variables; ESG performance indicates the key explanatory variables; BS, IBM, and CEOCD are governance variables, and SIZE, TobinQ, CIR, and CASH are bank-level control variables; GDP and INF are macro-level control variables; i denotes the banks and t indicates the year; β represents the constant; and ε is the error term.

Based on the studies of Zheng, Chowdhury, et al. (2023) and Bagh, Fuwei, and Khan (2024), we have expanded our baseline equation by introducing the square of the dependent variable. Therefore, the non-linear equation is outlined below:

Next, to assess the joint effect of environmental uncertainty and ESG performance proxied by ESG × ENVU on the dependent variable, we have expanded our equation following the literature of Shakil (2021) and Abdelkader et al. (2024). Our extended model is outlined below:

Empirical Results and Discussion

Descriptive Statistics

In analyzing ESG performance on bank risk-taking in China and the USA with the moderating effect of environmental uncertainty, distinct variations emerge in the financial and governance dynamics of banks across these regions. Chinese banks exhibit a higher average ESG performance score (3.712) compared to US banks (3.446), indicating potentially greater formal adherence to ESG principles in China. However, this elevated ESG focus does not appear to mitigate higher levels of default risk (DRISK) and leverage risk (LRISK), which average −5.867 and −5.751 for Chinese banks, respectively, as opposed to −5.111 and −5.005 for US banks. The heightened default and leverage risks in Chinese banks may reflect increased vulnerability to regulatory and economic fluctuations, especially given the pandemic’s ongoing economic effects. Conversely, US banks display elevated portfolio risk (PRISK of −2.738) relative to Chinese banks (−3.637), suggesting different risk-bearing strategies and portfolio diversification approaches across the two regions. The influence of environmental uncertainty (ENVU) is pronounced in the US, where banks report a higher mean ENVU score (1.692) compared to Chinese banks (1.383; Table 3).

Descriptive Statistics.

Pearson Correlation Coefficients Matrix and VIF

Table 4 displays the Pearson correlation coefficient matrix to verify the correlations among the explanatory variables. For the full sample, the ESG variable exhibits a modest yet significant negative correlation with ENVU at 0.057, at a 1% significance level, indicating that higher ESG performance is associated with slightly lower levels of environmental uncertainty. A significant and positive correlation of ESG with SIZE (.487) suggests that larger banks tend to perform better in ESG. However, correlations between ESG performance and other key variables generally remain below the threshold of 0.7, indicating no major multicollinearity concerns in the present study (Atif & Ali, 2021; L. Wang & Yang, 2023). When the full sample is divided into US and Chinese banks, the conclusion is the same. Table 4 also reports the VIF values for the variables across the full sample, Chinese banks, and US banks, providing insight into potential multicollinearity. Generally, VIF values below 10 indicate that multicollinearity is not a significant concern (Abdelkader et al., 2024; Shakil, 2021). For the full sample, VIF values range from 1.03 to 2.56, with a mean VIF of 1.42, suggesting no multicollinearity issues.

Pearson Correlation Matrix and VIF.

, **, and *** indicate the level of significance at .01, .05, and .10 respectively.

Baseline Regression Results (Linear Relationship)

Table 5 highlights the findings of the direct effect of ESG performance on bank risk-taking for the full sample, Chinese banks, and US banks using the 2sGMM approach. We carefully consider bank-level and macroeconomic control variables, as recommended by Shakil (2021), J. Lee and Koh (2024), and S. Wu et al. (2025). In all the models, different risk measures are the dependent variables for the total sample, US banks, and Chinese banks. We utilized three proxies of bank risk-taking: (i) default risk, indicated as DRISK, (ii) leverage risk, represented as LRISK, and (iii) portfolio risk, denoted as PRISK. In the full sample, the lagged dependent variable (L.RISK) shows consistently high positive and statistically significant coefficients, suggesting strong persistence in risk-taking behaviors among banks. Specifically, in the full sample, L.RISK coefficients range from 0.606 to 0.648, indicating a significant positive effect on risk levels across different risk measures (DRISK, LRISK, PRISK). Similar trends are evident within both Chinese and US banks, reinforcing that past risk levels are a critical predictor of future risk.

The Direct Effect of ESG Performance on Bank Risk-Taking.

Note. The study uses 2sGMM to address the endogeneity issues. AR(1) and AR(2) tests are used for autocorrelation issues. The Hansen test is reported for the validity of instruments. DRISK = default risk; ESG = ESG combined score; BS = board size; IBM = independent board member; CEOCD = CEO duality; SIZE = bank size; TobinQ = Tobin’s Q; CIR = cost-income ratio; CASH = cash ratio; GDP = annual growth rate; INF = inflation rate.

, **, and *** indicate significance at 1%, 5%, and 10% respectively.

Notably, the results are shown in Table 5, derived from Equation 3. The findings indicate that ESG performance significantly affects default risk, leverage risk, and portfolio risk at a 1% level of significance in the full sample, Chinese and US banks, suggesting that banks with higher ESG performance tend to take lower risk levels. Specifically, a one SD increase in ESG in the full sample (0.394, as per Table 7) leads to a 37.23% (0.394 × 0.945) decrease in default risk, a 37.39% (0.394 × 0.949) decrease in leverage risk, and a 40.26% (0.394 × 1.022) decrease in portfolio risk. Moreover, the coefficients of Chinese and US banks confirm that ESG performance reduces DRISK, LRISK, and PRISK at 10%, 5%, and 1% significance levels. This effect is consistent across the three risk measures and particularly pronounced in the case of portfolio risk. The effect is stronger in Chinese banks, where coefficients are more negative and statistically significant at higher levels, especially for default and leverage risk, implying that Chinese banks may benefit more from ESG consideration in mitigating risk. Thus, these findings that ESG performance mitigates risk-taking in both Chinese and US banks which is consistent with the results from previous studies (Di Tommaso & Thornton, 2020; Fu et al., 2024; Shakil, 2021). Thus, the results confirm Hypothesis 1, suggesting that ESG performance mitigates the risk-taking of banks in both developing and developed economies.

Furthermore, the findings validate stakeholder theory (Freeman, 1984), information asymmetry theory (Suchman, 1995), and bank risk management theory (Pyle, 1997). According to Stakeholder Theory, banks prioritizing ESG factors can better meet the expectations of key stakeholders, including customers, investors, regulators, and communities (Freeman, 1984). By aligning with these stakeholders’ values, banks enhance their reputation and trust, which reduces the pressure to engage in high-risk, short-term profit-seeking behavior (Shakil, 2021). Information asymmetry theory further explains this relationship, suggesting that strong ESG performance reduces information gaps between banks and their stakeholders (Akerlof, 1970). Transparent ESG practices signal to investors and regulators that the bank is managing risks effectively, reducing uncertainty, and lowering perceived risks. With more reliable information, stakeholders are less likely to demand riskier strategies to “compensate” for perceived uncertainty. Finally, Risk Management Theory posits that banks with robust ESG practices are better equipped to identify and mitigate both financial and non-financial risks, including environmental and social risks. By addressing these risks, banks adopt more conservative, sustainable strategies that inherently reduce the likelihood of engaging in high-risk behaviors. Collectively, these theories highlight that high ESG performance not only aligns with stakeholder expectations but also serves as a tool for reducing information gaps and managing risks, leading to lower risk-taking behavior in banks.

Non-Linear Relationship Analysis

This study also highlights the non-linear association between ESG performance and bank risk-taking using DRISK, LRISK, and PRISK for both Chinese and US banks (Table 6). The initial negative coefficients for ESG on all risk types are particularly significant in DRISK and LRISK across the full sample and in Chinese banks, suggesting that as ESG scores increase, banks experience a considerable reduction in risk. This is particularly evident in Chinese banks, where higher ESG levels correlate with stronger reductions in default and liquidity risks. For US banks, the effect of ESG on PRISK is notably strong, suggesting that ESG practices significantly reduce portfolio risk. However, the positive quadratic term (ESG2) indicates that at higher levels of ESG investments, these risk-reduction benefits start to taper off, and beyond a certain threshold, the risk may even increase slightly. This results in a U-shaped relationship where ESG performance first reduces risk but eventually reaches a point where additional ESG focus may slightly elevate risk, particularly portfolio risk, due to factors like reduced diversification or limited investment options.

The Non-Linear Effect of ESG Performance on Bank Risk-Taking.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Furthermore, the country-specific results indicate that Chinese banks experience relatively stronger initial benefits from ESG in reducing DRISK and LRISK. This could reflect heightened regulatory pressures and the rapid adaptation of ESG practices in China, where banks may more aggressively leverage ESG investments as a competitive and compliance strategy. In contrast, US banks show a more pronounced non-linear effect, particularly with portfolio risk, potentially due to a stronger market orientation and established ESG practices that may already be at or near the optimal ESG threshold.

Moderating Effects of Environmental Uncertainty

The findings from Table 7 reveal a significant moderating role of environmental uncertainty (ENVU) on the relationship between ESG performance and bank risk-taking across both Chinese and US banks. The negative coefficients for ENVU across all risk types indicate that higher environmental uncertainty correlates with increased bank risk, reflecting the heightened vulnerability of banks to external shocks and unpredictable factors. However, the positive and significant interaction term (ESG × ENVU) across default risk, leverage risk, and portfolio risk suggests that environmental uncertainty enhances the risk-reducing impacts of ESG performance. This interaction indicates that during periods of heightened environmental uncertainty, the stabilizing benefits of ESG performance are amplified, establishing ESG practices as a vital buffer against risk. In the case of Chinese banks, this moderating effect is consistent across all risk types, indicating that ESG initiatives greatly improve vulnerability during volatility because of the regulatory and economic environments that promote risk management. For the US context, the interaction between ESG performance and ENVU is more significant for portfolio risk (PRISK); the negative relationship between ESG performance and risk-taking becomes stronger under conditions of high ENVU. This might be because US banks are market-oriented, and ESG strategies are important to manage a portfolio during downturns. The result for the interaction term of PRISK is positive, which means that US banks with a better ESG framework can better control portfolio risk through sustainable investment and reasonable governance, regardless of environmental uncertainty. Moreover, the similar significance of the interaction term for both default risk and leverage risk in both countries proves that ESG can be used as an effective instrument for risk management, not only at the portfolio level but also to address the problems of default and liquidity risks in conditions of uncertainty. The results presented in this paper stress the significance of ESG performance as the key strategic factor, particularly when the environment is characterized by high levels of uncertainty.

Moderating Effect of Environmental Uncertainty on the Nexus Between ESG and Risk.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Robustness Check Using 2SLS Regression

The stability of results across the full sample using the 2SLS approach (Table 8) and the individual components of ESG performance demonstrates the robustness of our findings and suggests that the observed relationships between ESG performance, environmental uncertainty, COVID-19, and bank risk are likely not influenced by potential endogeneity or other biases. Our findings show that our main results are consistent across different risk types and further confirm the moderating impacts of both environmental uncertainties on ESG performance in mitigating bank risk-taking.

ESG Performance and Bank Risk: Linear and Non-Linear Effects.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Robustness Tests Using Individual Components of ESG Performance

We conducted further analysis for the robustness checks using a two-step system GMM for individual components of environmental (ENV), social (SOC), and governance (GOV) performance on bank risk-taking (DRISK, LRISK, and PRISK), demonstrating that each element negatively influences bank risk-taking in both Chinese and US banks depicted in Tables 9 to 11. The nexus between ENV, SOC, and GOV performance and bank risk-taking also suggests a non-linear U-shaped relationship, indicating that ESG initiatives initially reduce bank risk-taking, but the benefits diminish after reaching a certain threshold. The results are almost similar to our primary regression analysis.

Environmental Performance and Bank Risk: Linear and Non-Linear Effects.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Social Performance and Bank Risk: Linear and Non-Linear Effects.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Governance Performance and Bank Risk: Linear and Non-Linear Effects.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Effect of Interaction Between ESG and COV19 (2020–2022) on Bank Risk

In Table 12, the interaction term between ESG performance and the COVID-19 pandemic (ESG × COV19) reveals a significant positive moderating effect across all models for both Chinese and US banks, indicating that the effect of ESG performance on risk-taking is enhanced during the COVID-19 pandemic. The significant interaction term (ESG × COV19) across all three risk types (DRISK, LRISK, PRISK) shows that the COVID-19 pandemic amplifies the influence of ESG performance on risk. Specifically, the positive and significant coefficients for ESG × COV19 for default risk, leverage risk, and portfolio risk are 1.816, 1.834, and 3.425 at a 10% significance level in the total sample, indicating that during the pandemic, the risk-reducing benefits of ESG become more pronounced, suggesting that ESG investments provided additional resilience for banks facing heightened uncertainties. This further supports the notion that the COVID-19 crisis amplifies the risk-mitigating benefits of high ESG performance, particularly in times of economic uncertainty.

Moderating Effect of COVID-19 on the Nexus Between ESG Performance and Bank Risk.

, **, and * denote the significance of correlation at .01, .05, and .10 levels, respectively.

Discussion and Policy Implications

Discussion of Key Findings

This study investigates the influence of ESG performance on bank risk-taking, including default risk, leverage risk, and portfolio risk, and bolstering resilience, particularly in times of uncertainty in the two world’s largest economies. Using an unbalanced sample of 315 listed banks across China and the USA from 2011 to 2022 and the 2sGMM and 2SLS approach, the study examined the linear and non-linear effects of ESG considerations on bank risk-taking with an emphasis on the moderating roles of environmental uncertainty. The empirical findings offer an adverse and significant impact on bank risk-taking and a significant and positive non-linear impact of ESG issues on bank risk-taking. Our results are also supported by the analysis of individual components of the ESG performance, highlighting the non-linear impacts. Our sub-sample analysis further supports the hypothesis that robust ESG performance influences bank risk-taking in both China and the USA, with the moderating effects of environmental uncertainty, revealing that ESG practices become even more essential under challenging conditions. The separate analysis of ESG components reveals that each component contributes uniquely, specifically environmental initiatives that significantly mitigate portfolio risk, while social and governance aspects reduce default and leverage risks. This comprehensive analysis demonstrates that ESG performance is a strategic asset for banks, bolstering stability and resilience, especially in the face of unpredictable external challenges. Overall, this study positions ESG as a proactive tool for enhancing bank stability, recommending that banking institutions prioritize a balanced ESG performance as part of a comprehensive risk management strategy.

Policy Implications

This article contributes to investors, bank managers, and policymakers. According to the investors’ perspective, incorporating ESG issues into the banking strategy mitigates bank risk-taking due to stakeholders’ reaction to the sustainable business performance. Moreover, this study’s empirical findings support the agency, legitimacy, and risk-management theory by highlighting a significant negative effect of ESG performance on bank risk-taking. Agency theory provides evidence that ESG performance aligns bank management’s interests with those of broader stakeholders by reducing risk. Higher ESG scores suggest a commitment to responsible management practices that limit excessive risk-taking, particularly relevant in agency-prone sectors like banking, where managers may otherwise engage in risky behaviors. ESG thus serves as a governance mechanism that mitigates agency conflicts and aligns management behavior with long-term stakeholder interests, especially under uncertain conditions. The results support legitimacy theory, showing that banks’ commitment to ESG practices enhances their legitimacy in society, especially during crises like the COVID-19 outbreak. The positive impact of ESG on risk reduction suggests that banks can enhance public trust and legitimacy by actively addressing environmental and social issues. By demonstrating the significant risk-reducing effects of ESG practices, this study reinforces the relevance of risk management theory in the banking sector. Our findings indicate that ESG functions as an effective risk management tool, reducing exposure to default, liquidity, and portfolio risks. These insights are particularly valuable during periods of heightened environmental uncertainty and global crises.

Limitations and Future Research

While this study highlights valuable insights, several limitations should be acknowledged. First, potential endogeneity may influence the observed relationships despite using 2sGMM and 2SLS methods. Second, inconsistencies in ESG rating methodologies across countries could affect comparability. Third, country-level heterogeneity may limit the generalizability of findings beyond China and the US Finally, measurement error and reliance on listed banks restrict the broader applicability of results to the global banking sector. Also, the analysis is limited to focusing on the banking industry in China and the USA from 2011 to 2022, ending in 2022, may not reflect recent reporting developments, and reliance on Refinitiv’s aggregate ESG score could obscure differences across alternative scoring methodologies. Future research should explore component-level effects using more recent and granular ESG datasets. Additionally, the ESG data used reflects historical practices and may not capture recent shifts in ESG reporting and management. The study also does not discuss the effect of individual components of ESG disclosure. Future research could extend the sample to include banks from diverse geographical areas, considering ESG controversies to explore the potential impact on firm performance, firm value, cost of equity, and green innovation across different regulatory frameworks and market structures. Another avenue for future research is to explore the impacts of each ESG component more granularly across different risk types in various banking models, including ownership type, which may face distinct ESG-related challenges. Another limitation of this study is that it treats Chinese and US banks as relatively homogeneous, despite differences in size, ownership, and business models. Such heterogeneity may affect ESG practices and their impact on risk. Future research could examine specific bank types, such as large commercial, regional, state-owned, or private banks, to capture these variations. A further limitation is that our analysis does not account for ESG controversies, such as governance violations or environmental scandals, which can increase bank risk even for institutions with high ESG scores. Future research could incorporate ESG controversy indicators to provide a more nuanced understanding of how negative ESG events affect the ESG–risk relationship, particularly under conditions of uncertainty. Finally, given the findings related to environmental uncertainty, future studies could examine other post-crisis contexts to see if ESG continues to provide similar stabilizing effects, thereby enriching our understanding of ESG as a resilience tool in a rapidly changing world. These insights are valuable for bank leaders, investors, and policymakers, illustrating that balanced ESG strategies can mitigate risks and enhance resilience in an increasingly uncertain environment. Therefore, the investors, customers, and stakeholders may place greater importance on banks that prioritize strong ESG commitments, which ultimately foster public trust and ensure long-term stability.

Conclusion

This study examines the linear and non-linear relationship between ESG performance and bank risk-taking, incorporating the moderating effects of environmental uncertainty across developed (USA) and emerging (China) economies. Using a sample of 315 listed banks from 2011 to 2022 and employing robust econometric techniques (2sGMM and 2SLS), our findings reveal several key insights. First, we establish a significant negative relationship between ESG performance and bank risk-taking, suggesting that banks with stronger ESG commitments tend to exhibit lower risk exposure. This aligns with stakeholder theory, as robust ESG practices enhance transparency, trust, and long-term resilience. However, we also uncover a non-linear (U-shaped) relationship, indicating that while initial ESG improvements reduce risk, excessive ESG investments beyond an optimal threshold may lead to diminishing returns or even heightened risk due to rising compliance costs or overextension. Second, our analysis highlights the moderating role of environmental uncertainty, particularly in the Chinese banking sector. During periods of heightened uncertainty, the risk-mitigating effect of ESG weakens, implying that external shocks can disrupt the stability benefits of sustainability practices. The pandemic further amplified this effect, underscoring the need for adaptive ESG strategies in volatile environments. By bridging the gap between ESG performance and bank risk-taking, this study contributes to the evolving discourse on sustainable finance, offering actionable insights for enhancing financial stability amid global uncertainties.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author on request.