Abstract

This study investigates the relationship between the dimensions of electronic (E)-banking service quality and customer purchasing intentions with the mediating role of customer satisfaction. Data were collected from employees and customers, working in different banks of Qatar through a validated closed-ended questionnaire from a sample of 235. Correlation analysis and regression analysis were implied to the obtained data to test the study hypothesis, and the report provided accurate results as per our expectations. The results of the study indicate that reliability, efficiency, responsiveness, communication, security, and privacy have a significant and positive impact on customer purchasing intentions. Customer purchasing intentions are significantly increased when the customers are satisfied with E-banking service quality. The mediating role of customer satisfaction was established for E-banking service quality and customer purchase intentions. Customer satisfaction tested as a mediator has shown a partial impact on the relationship between information technology (IT), E-banking service quality, and customer purchasing intentions. This study has significantly contributed to the area of research primarily within the domain of behavioral finance. The study also provides significant implications for academicians and practitioners.

Keywords

Introduction

The current business conditions are exceptionally dynamic (Statista, 2018) with an ever-increasing technological advancement. The banking industry of the 21st century is working in complex and aggressive situations revealed by these changing circumstances and an extensive financial market (Ogare, 2013). Banks play a vital role in the economic development of any country. Banks are facing rapid changes because of the innovativeness and consistently changing electronic services in the marketplace. Access to the technological advancements made people aware of what is happening around the globe in a single touch (Tseng & Wei, 2020). The mobile phone plays an essential role in this scenario. It is a tool to stay connected, knowledge sharing, shop, entertain, and, more importantly, getting the online services (Tseng & Wei, 2020; Zheng et al., 2019). It is essential to work on the competence and effectiveness of the Bank as the leading players in the financial service providers of a nation; therefore, it cannot be ignored (Binuyo & Aregbeshola, 2014). Businesses with E-banking services (Sardana & Singhania, 2018) transact quickly as compared with traditional banking processes, and hence, their mode of transaction is becoming faster and reliable (Alalwan et al., 2017). Global digitalization, internet, and mobile phone facilities helped the financial institution to introduce new ways of banking services that are much easier for the customer to avail (Alkhowaiter, 2020) as well as the banker to provide flawless services to its customers. Ovia (2001) argued that E-banking is the consequence of the internet business in the field of banking and financial organizations. Robinson (2000) believed that providing online banking services facilitate banks to establish and expand relationships with customers.

Qatar is one of the stable economies in the Gulf with a variety of banking services (Hashim & Chaker, 2009). The country is well-versed in its Islamic values and principles in every span of life Anouze and Alamro (2019) Performance of the banking sector, and the customer satisfaction relies on the rich text of values and norms of people (Noman, 2002).On the other hand, the country has considerable investment opportunities and potential. Firms are investing and focusing on the different factors necessary for pumping in more revenue. In this scenario, E-banking has been noticed as an essential variable (Alkhowaiter, 2020) that manages customer purchasing intentions. With the emergence of technology and its rapid globalization, E-banking services are the demand of customers; however, the online services are not always available to every customer, which is a reality. It may be due to limited access to the technology, internet, or lack of awareness of technology, or some people may feel insecure or to avoid the excessive fees charged for E-banking services (Alkhowaiter, 2020). According to Al-Khalaf and Choe (2020), Qatar is one of the advanced states with access to E-banking facilities with robust e-commerce ecosystems. A total of 75% population of Qatar was using smartphones and positioned on the top in the Gulf region in access to (Metodieva, 2012) with an increasing shift toward online services (Al-Khalaf & Choe, 2020).

Businesses with E-banking services transact within seconds, and hence their mode of the transaction becomes faster and reliable. Such fast E-banking services fulfill business needs, and therefore the performance of the business is improved. Customer purchasing intention is an inclination toward a particular product when it comes to deciding on the purchase of a product. It has been noticed that in the digital era of banking, E-banking is setting new heights in the business world, and such banking trends are seemed to influence consumer buying behavior. Customer satisfaction is associated with high-tech E-banking, business performance, and customers’ purchase intentions. When the customer is satisfied, business performance is enhanced, and hence the business is flourished. One can find dozens of similar studies around the globe. Still, Hammoud et al. (2018) studied the E-banking service quality on customer satisfaction in the Lebanese banking sector, and Asiyanbi and Ishola (2018) study on availing E-banking services and customer satisfaction was the inspiration to conduct this study. The authors found that service quality dimensions such as efficiency, reliability, security, privacy, responsiveness, communication, availability, and access to E-banking services positively affect customer satisfaction, which in turn determine their purchase intentions and long-term relationship with the bank. In this study, we extended the level of research to the impact of E-banking service quality (efficiency; reliability; security and privacy; and responsiveness and communication) on customer purchase intentions with the mediating role of customer satisfaction in the banking sector in Qatar.

The objective of this study is to find the determinants of customer purchase intentions and the usage of E-banking services among Qatari citizens in the banking sector. For that, the research will focus on the effect of variables such as efficiency, reliability, security and privacy, and responsiveness and communication on customer satisfaction, which in turn determine the customer purchase intentions. This study will significantly contribute to existing literature and will provide evidence on factors determining customer purchase intentions and the level of satisfaction on E-banking services. The study will provide a rich source of information for decision-makers in the banking sector, which will reveal the secrets to boost customer satisfaction levels and identify the factors to harvest long-term and healthy relationships with the customer with an exceptional contribution to Qatar’s banking sector.

Literature Review

Banks have fundamentally shifted from traditional banking to E-banking in the past few decades (Hammoud et al., 2018; Joseph & Stone, 2003; Sardana & Singhania, 2018). The trends of innovation and technological advancements helped banks to expand their customer base and E-banking services (Alkhowaiter, 2020; Al-Zadjali et al., 2015), which paw the roadmap to expend the banking services toward advancements and ease of access. Customers can track the bank balances, transfers of credit, checking accounts, text messages, payment exchanges, and different organizations based on instructions sent to them on mobile phone s by banks are listed as the newest development in E-banking services (Saleem & Rashid, 2011). E-banking is often referred to as online banking and mobile banking. Online banking and mobile banking are two platforms through which banks can provide better-access services to customers. Specifically, the customer using online banking is through the computer associated with the internet, whereas the customer using mobile banking is through the wireless gadget (Al-Khalaf & Choe, 2020). Khraim et al. (2011) clarified that the use of mobile banking by wireless shows the difference between online banking and mobile banking settings, while customers consider portability to be the most critical feature of the mobile banking industry. Reliability is the most crucial part of mobile banking. More importantly, bank customers believe that valuable internet banks are being used, although web-based banking is considered the cheapest channel.

E-Banking Service Quality and Customer Purchase Intention

E-banking provides a twofold advantage: the banks adopt a better, faster, and cheaper way to market and deliver services and products online, whereas customers are enabled to conduct banking transactions over the internet anytime and anywhere (Lussier & Hendon, 2017; Polatoglu & Ekin, 2001). The bank began to communicate to customers, a quality online experience (Manju, 2020); as a result, web-based banking grants continue to evolve and have become an unstoppable underlying competitive agent for banks to attract and retain customers (Sadowski, 2017). Kassim and Abdullah (2010) emphasized that by leveraging the internet, business organizations can free up revenues through online websites, provide customers with higher value levels in new ways, and provide opportunities for companies and customers to interact more.

Today, consumers rely heavily on online information produced or shared by different consumers to address purchase choices (Hu et al., 2012). Therefore, internet banking has a substantial impact on consumer brand mindfulness, emotions, and mentality (Mangold & Faulds, 2009). Currently, everyone uses the internet in their daily lives, so they contribute to electronic word-of-mouth when they buy any product (Berger, 2014). Omar et al. (2010) investigated the data of 201 respondents to examine the relationship and showed that the service quality and purchase intention relationship is mediated by satisfaction. Laroche et al. (2005) used a sample of 266 customers in the shopping mall based on the service quality on consumers’ purchase intention or decision. They found that the quality of service in the shopping mall was mediated between the risk of buying and the purchase intentions of customers. Bloemer et al. (1999) studied the same phenomenon by using a sample of 708 respondents working in different firms and found that perceived quality of service has a positive impact on purchase intention:

E-Banking Service Quality and Customer Satisfaction

Quality of service is essential for a company’s survival in the marketplace (Anouze & Alamro, 2019; Anouze et al., 2019; Manju, 2020). The way customers perceive the quality of services now is different from the quality of services in the past. Therefore, it is vital to check the quality of services in the online banking industry (Choudhury, 2013; George & Kumar, 2014; Ranaweera & Sigala, 2015). In addition to understanding how customers evaluate automated online banking, it is crucial to determine essential components for assessing the quality of online banking services (Amin, 2016). Customer view and variety of service preferences have a significant impact on the success of banks (Gupta & Bansal, 2012). Parasuraman et al. (1985) reported a right affiliation with customers’ understanding of their service quality and their willingness to support the company. On the other hand, customer satisfaction with E-banking services depends upon the trust of internet services and the security of customer’s privacy. Many customers are seen resistant to the use of E-banking services; hence, the branch services are much necessary too. The threats posed to the customer include identity theft, the risk to private information and sensitive data, and the danger of loss of money due to internet scammers (Sardana & Singhania, 2018). According to Manju (2020), service quality is the prime indicator of customer satisfaction. On the one hand, they face increasing competition and increasing customer demand for better services, whereas on the other hand the profit margins are decreasing. Banks have to focus on customer satisfaction by focusing on their efficiency, reliability, and being on the service of the customer (Anouze et al., 2019).

Customer satisfaction (Anouze et al., 2019) and quality are parallel (Liljander & Strandvik, 1995). E-banking (Sardana & Singhania, 2018) plays a more critical role in the development of the banking industry by boosting customer satisfaction levels through reliability and tenability (Al-Zadjali et al., 2015). Customer satisfaction is a crucial factor in all sectors, especially in the service sector (Pooya et al., 2020; Tseng & Wei, 2020). Customer satisfaction is related to the people who pay for goods or services and the use of these goods and services (Ling et al., 2016). Client perceptions and service quality preferences have an enormous impact on the success of the bank (Gupta & Bansal, 2012). Customer satisfaction is associated with high-tech electronic banking, business performance, and customer intentions. When the customer is satisfied, business performance is enhanced, and hence the business can be flourished. Satisfaction has a strong connection to quality of service. Online banks must seem to be more concerned about the customer perception of online banking services because the advantages of competitive services can easily be measured (Santos, 2003). Customer pleasure is the support of the absolute achievements of the quality revolution, which is mainly reliant on customer’s cognizance of overall service quality (Husnain & Akhtar, 2016) as stated by Toor et al. (2016).

It evaluates the effectiveness and efficiency of websites to encourage shopping, buying, and shipping products or services. Santos (2003) described it as “Every consumer’s assessment and decision about the brilliance of electronic services.” Ariff et al. (2013) found that confirmation fulfillment, efficiency-framework accessibility, privacy, contact responsiveness, website style, and guide that constitute an E-website, efficiency-system accessibility, and contact-responsiveness of the internet banking electronic service quality were significantly affecting the electronic satisfaction. Most mobile banking users believe that it is advantageous to have access to numerous mobile banking services; they can access their account information such as mini-statement and the history of the transaction. Before online and mobile banking, customers needed to visit their bank branches to check account information (Saoji & Goel, 2013). Using banking services through mobile apps is very easy. Individuals do not have to worry about any other ability to use the app. They only need to introduce applications to their phones and enter PINs. Khan and Mahapatra (2009) reported that consumers were comfortable with the efficiency of the bank’s services but were not satisfied with the user-friendly elements. In this way, the studies show the need to estimate the effectiveness of trust, the availability of online banking, perceived value, and the impact of service quality on customer satisfaction and customer accountability. Website design, reliability, responsiveness, and trust can affect service quality and customer satisfaction, which can significantly affect customer’s willingness to buy.

Reliability, responsiveness, conformability, assurance, empathy, and tangibles have not changed significantly over the years. Still, there is a considerable discrepancy between customer demand and the apparent performance of traditional banking services (Harridge-March et al., 2008). Singhal and Padhmanabhan (2008) also found that customers moved from conventional banking to web-based banking due to the security and privacy given by their respective banks. In this way, the protection and confidentiality of the website, ease of use, and the bank’s notoriety make customers happy, and they make decisions to use web-based banking channels (Alsajjan et al., 2006; Hashim & Chaker, 2009; Sadowski, 2017). Lee and Lin (2005) concluded that website design, reliability, responsiveness, and trust often affect service quality and customer satisfaction, which significantly affects customers’ willingness to buy. Khurana (2009) argued that a variety of service measures, such as efficiency, responsiveness, implementation, the privacy of personnel information, and ease of use, are metrics for online banking that affect customer satisfaction. It has been observed that importance, responsiveness, and compassion measurement play an essential role in predicting customer behavioral expectations (Ravichandran et al., 2010). Nupur (2010) proposed that reliability, responsiveness, conformability, sympathy, and tangibility are core service quality metrics for customer satisfaction in E-banking:

Customer Satisfaction and Customer Purchase Intention

Oliver (1980) defined customer satisfaction as the higher levels of customer fulfillment of expectations on the product or service. A happy and satisfied customer is always the priority of any successful business, especially the banks. Higher the affiliation of the customer with the bank, higher its market shares and profitability (Asiyanbi & Ishola, 2018; Kondo, 2001). According to Fornell (1992), variability in a customer’s level of satisfaction differs from past choices; he further articulated that quality is measured by the customer, and the most critical quality assessment is the process by which it influences consumer loyalty. Customer satisfaction is associated with high-tech electronic banking, business performance, and customer intentions. When the customer is satisfied, business performance is enhanced, and hence the business is flourished (Al-Khalaf & Choe, 2020):

Customer Satisfaction as a Mediator

Customer satisfaction enables firms to increase their sales revenue and achieve a competitive edge over competitors (Lewin, 2009), as well as it leads to long-term profits by gaining customer loyalty (Wirtz, 2003). Therefore, customer satisfaction originates from the recognition that firms have to interact with changing environments consistent with customer behavior to sustain the longevity and stability of companies in the market competition (Smith et al., 1996). Parasuraman et al. (1985) pointed out that the high quality of service is positively associated with customer satisfaction. Palmer et al. (2005) stated that the difference between quality and consumer satisfaction to all managers and researchers is essential because banks should know whether their target is to satisfy consumers or provide the highest quality services. Possibly, service quality and customer satisfaction contribute to the success and continuity of the work (Daniel & Berinyuy, 2010; Sadowski, 2017). Hsu et al. (2012) studied the impact on customer satisfaction of website quality and purchase intentions with the perceived playfulness and perceived flow as a mediator. Results showed that website quality influences the perceived playfulness and the perceived flow of the customer. This study revealed that the quality of service is more critical to customer satisfaction than information and quality of the system:

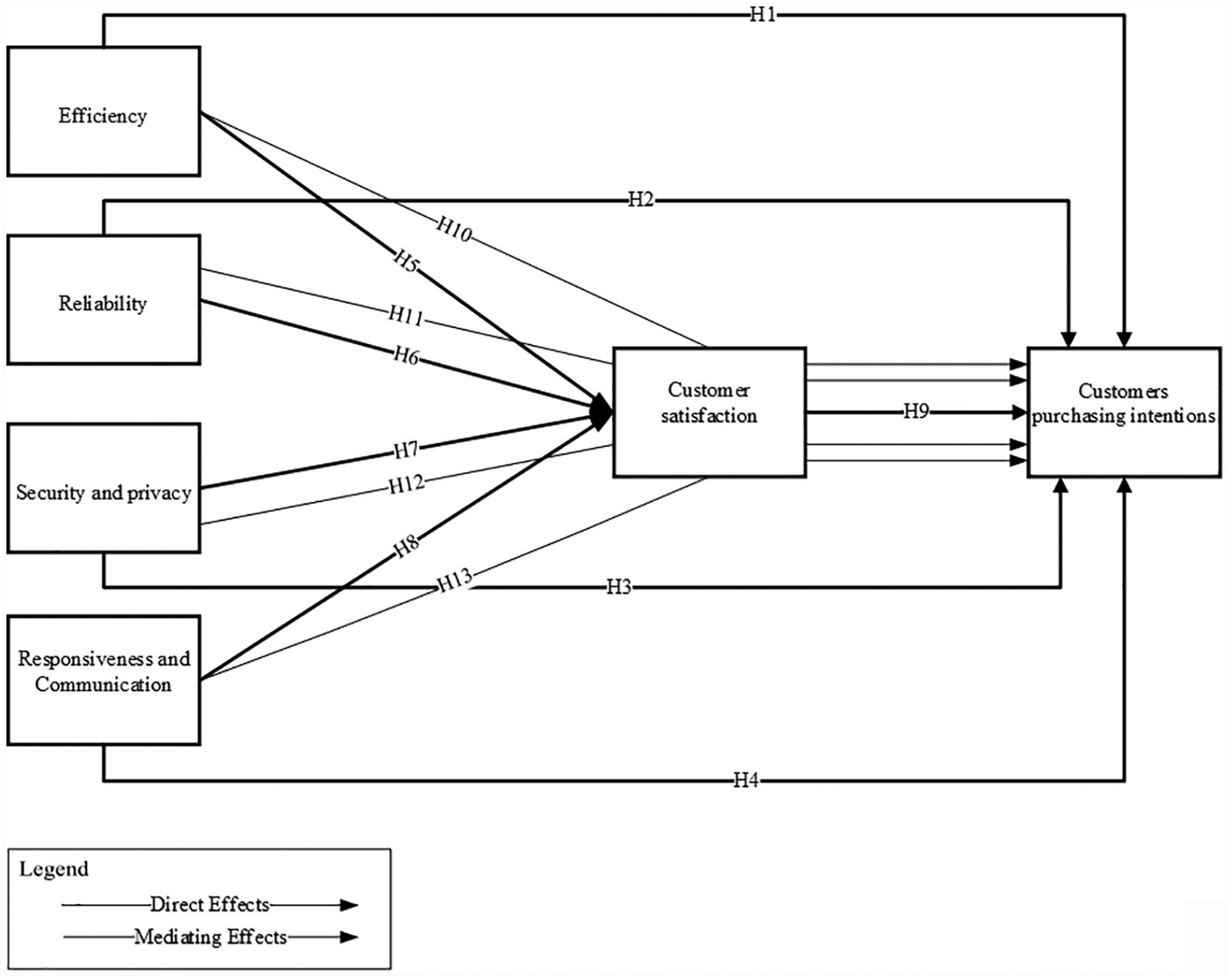

Figure 1 representing a graphical abstract of all the variables and relationships of this study.

Theoretical framework.

Method

The study is explanatory and follows a deductive approach to investigate the impact of E-banking services quality on customers’ purchase intention with the mediating role of customer satisfaction in the banking sector of Qatar. The sample comprised general bank employees and customers in Doha, Qatar. Continence sampling has been followed to collect primary data from a study sample of 235 through a cross-sectional approach. The bank employees and the walk-in customers were taken as the sampling frame, which significantly represents the population of study and, a close ended questionnaire was used to collect firsthand data from the convenient bank branches at the city of Doha. The obtained data are processed and tested for the study hypothesis in SPSS-26 using Baron and Kenny (1986) mediation regression method.

The research instrument used in this study comprised six main variables along with demographic variables (age, gender, education, and experience), which has been adopted from relevant past research studies. Customer purchase intention, the dependent variable, is measured with the scale, adopted from Hays and Hills (1999) with reliability (α = .70); E-banking service quality dimensions (efficiency [α = .83], reliability [α = .74], security/privacy [α = .80], and responsiveness/communication [α = .82]); and customer satisfaction (α = .75) from Hammoud et al. (2018).

Sample Description

The study sample’s descriptive statistics are shown in Table 1.

Frequency Tabulation.

Results

Data obtained from a sample of 235 were further codded in SPSS-25, and statistical tests were conducted to check the study hypothesis, including the test of reliability, frequencies distribution, descriptive statistics, correlation analysis, and regression analysis. The following are the detailed results of the test conducted on data. Table 1 demonstrates the demographic information of the sample of the study. A better blend of samples based on age was taken in which 22.1% falls in the category of 20 to 29 years, 29% were between 30 and 39 years, 14.5% were between 40 and 49 years, 20.4% were 50 and 59 years, and 14% were above 60 years. Female participation was observed less than expected, which was only 23.8%, whereas 76.2% were male. The sample was well educated, and 57% of the sample completed their 16 years of education at university levels. Demographic variable, experience, shows the involvement of example in economic activities with an approximately equal distribution ranging from less than 3 years to 10 years of experience.

Reliability Statistics

Table 2 shows the results of Cronbach’s alpha for study variables. The Cronbach’s alpha for variable customer purchase intention, the dependent variable, was recorded as (α = .67), efficiency (α = .83), reliability (α = .744), security and privacy (α = .807), and responsive and communication (α = .82) and for customer satisfaction, the mediating variable, was (α = .75). The test of reliability indicates how satisfactory our results are with the measuring instrument. The results obtained here are satisfactory and are in an acceptable range in social sciences.

Reliability Statistics.

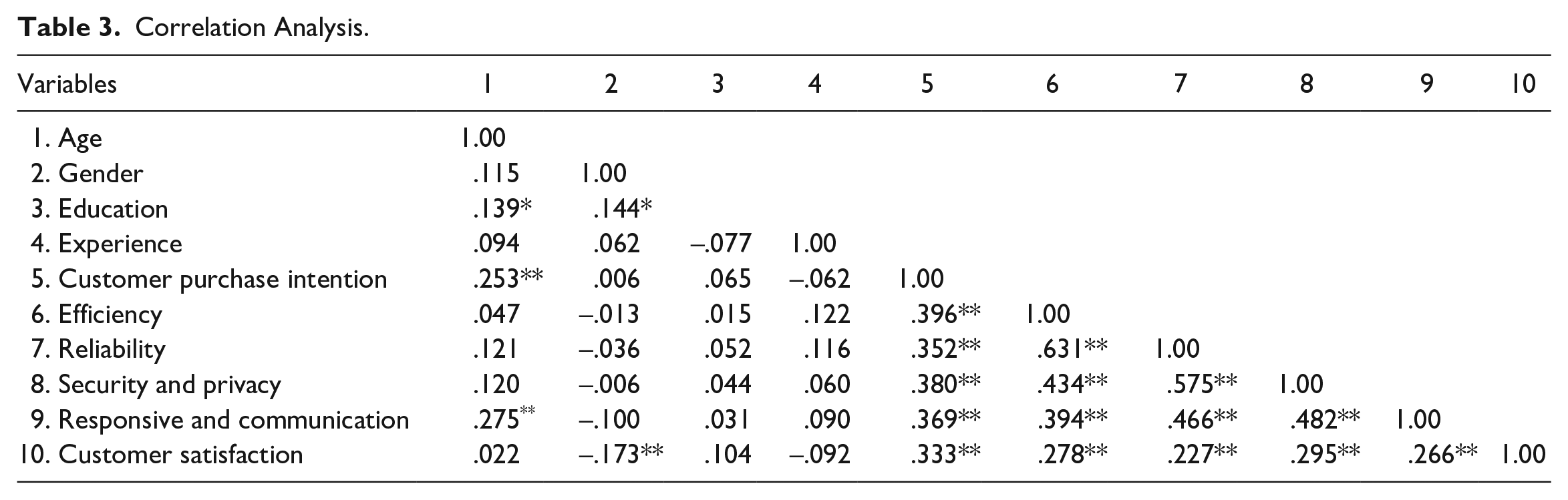

Correlation Analysis

Table 3 shows the results of correlation among study variables. Efficiency is positively and significantly associated with customer purchasing intentions (r = .396**, sign. ≤ .1) and was also positively correlated with customer satisfaction (r = .278**, sign. ≤ .1). Reliability has significant positive correlation with customer purchasing intentions (r = .352**, sign. ≤ .1) and customer satisfaction (r = .227**, sign. ≤ .1). Likewise, security and privacy have also significantly and positively correlated with customer purchase intention (r = .380**, sign. ≤ .1) and customer satisfaction (r = .295**, sign. ≤ .1). Responsiveness and satisfaction also has a strong positive correlation with customer purchase intention (r = .369**, sign. ≤ .1) and customer satisfaction (r = .266**, sign. ≤ .1). Similarly, customer satisfaction correlates with customer purchasing intention (r = .333**, sign. ≤ .1). On the contrary, the independent variables are also significantly correlated with each other; efficiency and reliability (r = .631**, sign. ≤ .1) is the highly significant value observed in this study; efficiency and security and privacy (r = .434**, sign. ≤ .1); efficiency and responsive and communication (r = .394**, sign. ≤ .1). Reliability shows significant positive correlation (r = .575**, sign. ≤ .1) with security and privacy and (r = .466**, sign. ≤ .1) with responsiveness and communication. Security and privacy positively and significantly associated with responsiveness and communication (r = .482**, sign. ≤ .1). The control variable does not show any significant correlation with study variables except age, which shows a strong positive correlation with responsive and communication (r = .275**, sign. ≤ .1) and customer purchase intention (r = .253**, sign. ≤ .1). Gender shows significant negative correlation with customer satisfaction (r = .173**, sign. ≤ .1). Age and education were positively correlated (r = .139*, sign. ≤ .05) and gender and education (r = .144*, sign. ≤ .05).

Correlation Analysis.

Regression Analysis and Testing of Hypothesis

Regression analysis results have been reported in Table 4. The results of the regression analysis showed that efficiency was a significant predictor of customer purchasing intentions (β = .340, p < .01). Thus, we found support for H1 that efficiency would lead to customer purchasing intention. Table 4 shows that value of R2 is 15.7%; it means that the efficiency is explaining the 15.7% variations in the customer purchase intention. According to H2, reliability has a positive impact on customer purchasing intentions. The proposed positive relationship of reliability and customer purchasing intentions is significantly supported by the results of the regression coefficient (β = .326, p < .001), thus confirms the projected H2. The results of the regression analysis showed that security and privacy were two significant predictors of customer purchasing intentions (β = .492, p < .01), and R2 is 14.5%. The beta value (β = .304**) illustrates a positive impact of responsiveness and communication on customer purchasing intentions. Here, the significance of R2 is 13.6%; it means that the responsiveness and communication explain the 13.6% variations in the customer purchase intention. The p value of .000 confirmed the proposed H4.

Regression Analysis (N = 235).

p < .05. **p < .01. ***p < .001.

H5 states that efficiency has a positive impact on customer satisfaction. The proposed positive relationship of efficiency and customer satisfaction is significantly supported by the results of the regression coefficient (β = .186, p < .001), thus confirmed proposed H5. H6 stated that reliability is positively related to satisfaction, which is supported by the results in Table 4 (β = .165**, p < .01). H7 establishes that security and privacy have a positive impact on customer satisfaction, and the results supported this relationship significance too (β = .298**, p < .01). H8 states that responsiveness and communication have a positive impact on customer satisfaction. H8 is supported by the results shown in Table 4 (β = .171**, p < .01), and this relationship is significant at 1% level. The results also confirm that there is a positive relationship between customer satisfaction and customer purchasing intentions (β = .427**, p < .01).

Table 5 shows the mediation test results of customer satisfaction between the relationship of efficiency and customer purchase intention. Results show that the relationship between efficiency and customer purchasing intention is partially mediated by satisfaction (β = .261**, p < .01) with efficiency and was still a significant interpreter of customer purchasing intention. Hence, H10 was partially supported.

Mediation Regression Analysis 1 (N = 235).

p < .05. **p < .01. ***p < .001.

Mediation Regression Analysis 2 (N = 235).

p < .05. **p < .01. ***p < .001.

H11 indicates that customer satisfaction mediates the relationship between reliability and consumer purchasing intentions. Results showed that the relationship between reliability and customer purchasing intentions partially mediated by satisfaction (β = .242**, p < .01; reliability was still a significant interpreter of customer purchasing intention). Hence, H11 was partially supported too.

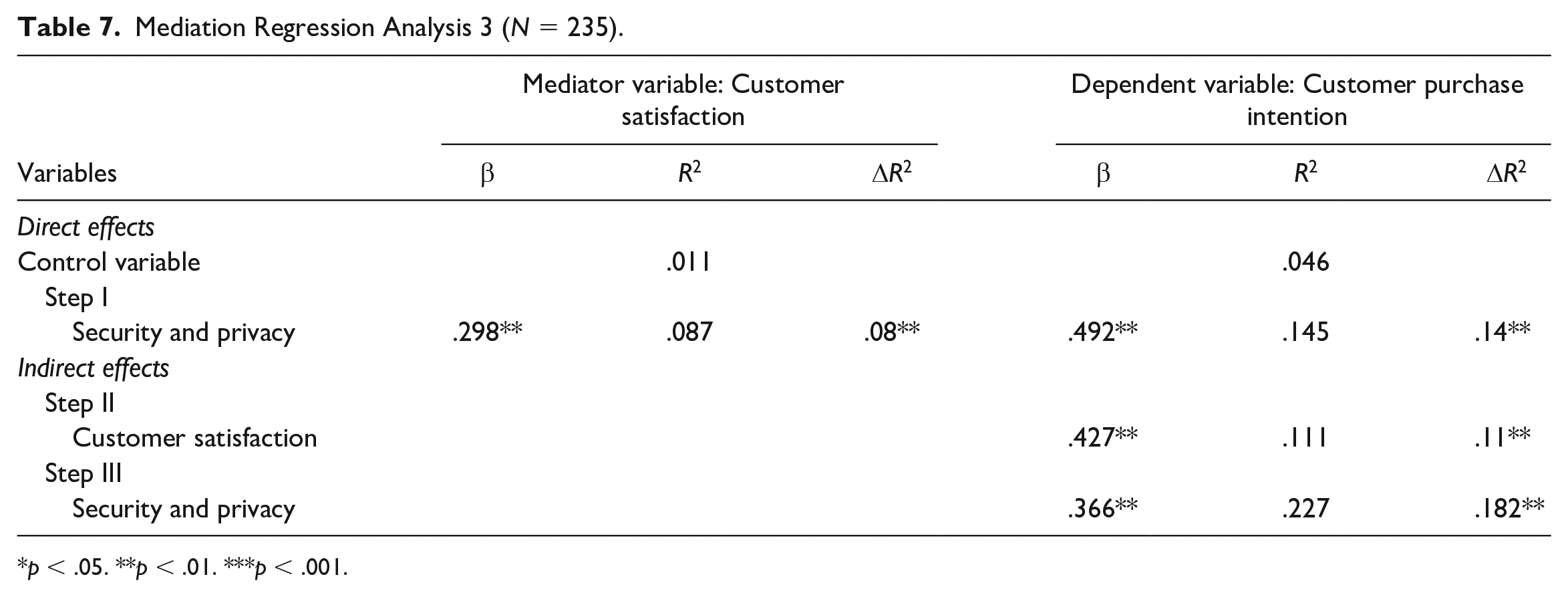

Mediation Regression Analysis 3 (N = 235).

p < .05. **p < .01. ***p < .001.

In H12, we proposed that customer satisfaction plays a mediating role between security and privacy and consumer purchasing intentions. Results showed that the relationship between security and privacy and customer purchasing intention partially mediated by consumer satisfaction with significant statistical values (β = .366**, p < .01). Therefore, H12 was partially supported.

Mediation Regression Analysis 4 (N = 235).

p < .05. **p < .01. ***p < .001.

Results revealed that controlling for the mediator, customer satisfaction, responsiveness, and communication was still a significant predictor of customer purchase intentions (β = .220**) with R2 = 22.1% change in the dependent variable. The finding indicates partial mediation of customer satisfaction between the relationship of responsiveness and communication and customer purchase intention.

Discussion

Customer is considered to be the center of concern in every business; that is why the researchers and the business personnel are highly interested in customer satisfaction. Higher customer satisfaction yields strong relationships and reliable relationship results in long-term relationship through motivation and intentions. Here, customer purchase intentions are of greater concern, and we studied the impact of E-service quality (efficiency, reliability, security and privacy, and responsiveness and communication) on customer purchase intention with the mediating role of customer satisfaction.

Results reported that E-service quality has a positive and significant impact on customer purchase intentions. This relationship can be defined as the increase in E-banking service quality increases purchase intentions and satisfaction acts partially as a mediator in this relationship. In this study, E-service quality has been studied under there independent variables as (a) efficiency, (b) reliability, (c) security and privacy, and (d) responsiveness and communication. Let us discuss the results obtained in brief. Efficiency was found the significant predictor of customer purchase intention (β = .340, p < .01) and customer satisfaction (β = .186, p < .001). Reliability yields significant results (β = .326, p < .001) with customer intention (β = .165**, p < .01) and with customer satisfaction. Likewise, security and privacy were also found in a significant positive association with customer purchase intention (β = .492, p < .01) and customer satisfaction (β = .298**, p < .01). The fourth variable, responsiveness and communication, yields a significant positive relationship with customer purchase intention (β = .304**, p < .01), and customer satisfaction (β = .171**, p < .01). The mediator, customer satisfaction, also shows a significant positive relationship with customer purchase intention (β = .427**, p < .01). It partially mediates the relationship of efficiency (β = .261**, p < .01), reliability (β = .242**, p < .01), security and privacy (β = .366**, p < .01), and responsiveness and communication (β = .220**, p < .01) with customer purchase intention.

While surfing for the past relevant studies, Hammoud et al. (2018) are the most pertinent. The authors applied structural equation modeling to study the impact of dimensions of e-service quality on customer satisfaction in banking sector of Lebanon and found significant results with high standardized beta values (β = .92; p =.000) and R2 values .66 for efficiency, .75 for reliability, .46 security and privacy, and .63 for responsiveness and communication, which shows the predictive ability of constructs in the model. Wandi et al. (2020) studied the impact of product and service quality on awareness and customer satisfaction in Islamic banks, and it showed a positive and significant effect of quality services on customer awareness that leads to a boost in customer satisfaction. The relationship of product quality with customer satisfaction was obtained with regression coefficients of .542 and a t value of 18.488. Raza et al. (2015) studied internet banking service quality and customer satisfaction in Pakistan, and it showed a significant impact of service quality factors on customer satisfaction with a regression analysis results of Adjusted R2 = .338, F-statistics = 20.280 and p = .000.

Asiyanbi and Ishola (2018) found that customers are highly satisfied with E-banking services and prefer conventional banking systems. Customers feel comfortable using ATMs to withdraw cash, e-money, and internet banking frequently, which minimizes the customer’s visit to the bank branch. Anouze et al. (2019) studied customer satisfaction in the Islamic banking sector in Jordan doing a confirmatory factor analysis on data obtained and found a significant impact of factors including the perception of employees in improving customer satisfaction. Alkhowaiter (2020) recently did a meta-analysis of 46 studies to observe the behavioral intentions and found seven factors with significant affecting power to motivate behavioral intentions. Many other studies (Sharif & Raza, 2017; Hossain & Leo, 2009; Anouze & Alamro, 2019; and Al-Khalaf & Choe, 2020) also found significant results. Hence, past studies and the statistical results of this research endeavor support the premise that e-service quality has a strong link to customer satisfaction and customer purchase intention.

Conclusion and Implications

This research endeavor intended to explore the impact of e-service quality on customer satisfaction in Qatar’s banking sector. This report starts with a brief introduction explaining the research intention followed by relevant literature review justified and arranged according to the proposed theoretical framework and hypothesis than methodology, results, and conclusion are reported.

Results show that the E-banking series quality is the prime indicator of customer satisfaction that motivates the customer to stay with the banks and hold long-term and healthy relationships. The moderating role of customer satisfaction is taken in this study to highlight the impact of satisfaction levels and future purchase intentions. It is found that customer satisfaction plays a vital role as a mediator and the predictor of customer purchase intention, especially in the banking sector. Customer is well aware of advancements in services and technology and expects flawless service quality form their respective banks. This research will help to develop an understanding of how banks probably leverage progress in information technologies adoption.

Furthermore, developing new services to fulfill the expectations of their consumers provides comprehensive feedback and an overview of the E-banking service quality within Qatar, and it can be successfully implemented in other countries too. Understanding service quality, customer satisfaction, and customer purchase intentions has practical implications for the banking industry. Banks can get to a competitive advantage with a specified focus on E-banking service quality and maintaining customer touchpoints by using the internet and adopting the latest technological advancements. It will yield a twofold objective. One, to attract and retain a good customer base for the organization, and the other is to compete in the marketplace with a better competitive edge. This research contributes to the existing knowledge in the field of behavioral finance.

On the other hand, it is quite useful for professionals in the banking sector, especially in Qatar, to strategically plan the future while adapting and tailoring e-service quality to their customers. The banking sector in Qatar has become much sophisticated in the last few years. And the timely decisions on improvement on customer satisfaction through e-business service quality may provide a better edge to cope with and lead the banking industry in the country toward new heights of success.

The current research study has few limitations, which can be taken as an opportunity for future research. First, the generalization of the study is limited as it is focused on the banking sector only. Study findings may not be replicated on the overall industry other than the banking sector. Second, we discussed only one mediator variable, that is, customer satisfaction, while other settings might exist to be considered. Any other suitable moderating variable may be introduced through which E-banking service may affect customer purchase intentions. Finally, researchers may study other E-banking service quality features, and their impact on customer purchase intentions may be checked. Future researches may also focus on a qualitative approach to study customer intention or use different methods and data types to conduct research studies on this topic.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.