Abstract

Investment demand depends on the level of uncertainty in the economy, it could have not only direct, but also indirect impact – it could significantly reduce the effectiveness of monetary policy by making investments less responsive to market signals. This issue has not been sufficiently studied in the economic literature; there are no empirical estimates of direct and indirect impacts of uncertainty on investment demand for a large sample of countries, so the scarcity of such studies has created a theoretical gap. Considering this research gap, our study used GMM estimator to analyze data for 161 countries from 2002 to 2022 to confirm that the interest elasticity of investment tends to be a function of the national level of uncertainty. This implies that reducing the interest rate may not be an effective way to stimulate investment under conditions of high uncertainty. In addition, the study empirically validated the impact of global uncertainty on investment in different countries. The findings contribute to investment theory by providing a better understanding of how uncertainty directly and indirectly influences investment demand. Several practical implications are proposed. However, the study has a limitation in that it only considers the dependence of investment elasticity on uncertainty as a single factor. There may be other significant factors that influence investment demand that were not included in the analysis. This fact creates a research gap that needs to be addressed in future studies.

Keywords

Introduction

Classical investment analysis assumes that the amount of investments directly depends on the expected future cash flows and the expected rate of return. Expectations of economic agents play an important role in investment decisions (Bernanke, 1983; Plosser, 1989; Romer, 2011). Under conditions of negative expectations, investors tend to postpone implementation of their investment programs until they have additional information to forecast cash flows and returns more accurately. Negative expectations are closely related to the level of uncertainty in the economy (Ghosh & Olsen, 2009; Gulen & Ion, 2016; Tingli et al., 2022).

Correlation between the level of uncertainty and the investment dynamics has been the subject of analysis by various researchers. Negative impact of uncertainty on investment activity may be caused by fluctuations in the business cycle (Kydland & Prescott, 1982; Long & Plosser, 1983; Plosser, 1989; Romer, 2011), lack of transparency in government regulations of the financial and commodity markets (Gulen & Ion, 2016; Julio & Yook, 2012). Increased risk significantly raises expected returns, making projects less attractive for investment (Bradley et al., 2016; Pastor & Veronesi, 2013).

The main research question of this paper is to empirically assess the direct and indirect effects of uncertainty on the level of investment demand worldwide, as well as the impact of this indicator’s global value on investment activities within countries.

In this study, we suppose that the uncertainty factor not only has an immediate direct impact on the level of investments, but also an indirect one. Unlike previous researches in this field, we suggest that when uncertainty is high, the efficiency of market regulators is considerably reduced. Under high levels of uncertainty, interest elasticity of investment decreases and investors tend to adopt “wait and see” approach in their investment decisions (Chen et al., 2020). Thus, this paper clarifies the mechanism by which uncertainty affects the level of investment demand worldwide.

Our study also examines both the role of country-level uncertainty and the impact of global indicator values on investment dynamics. As globalization increases, the correlation between financial and commodity markets of nations in the world has significantly increased (Kimiagari & Keivanpour, 2018; Vahid et al., 2020). Companies must integrate additional risks associated with changes in global uncertainty into their investment analysis and use more sophisticated systematic approaches to assess and manage risk (Kimiagari & Keivanpour, 2018; Kimiagari & Montreuil, 2017). It turns out that uncertainty both in key world economies can also have a significant impact on the country’s economic situation (Lee et al., 2024). While most publications have examined the direct impact of uncertainty on investments at the micro and macro levels, there is a lack of research about the impact of global uncertainty on investment dynamics within a country.

So this research aims to analyze both the direct and indirect impacts of the national uncertainty on investment dynamics, to study a potential influence of the global value of the indicator on investment demand within a country. The research problem is presented in a novel way, which highlights the significance of this study.

The presented approach proceeds as follows. We examine 161 countries from 2002 to 2022 to analyze the direct and indirect effects of uncertainty on investment dynamics. For this purpose, we use GMM estimator with inclusion of instrumental variables to address the endogeneity issue and obtain robust results.

This study identifies three key findings. First, the national uncertainty has an immediate direct impact on investment demand for 161 countries in the sample. It turns out that when uncertainty grows, investment demand decreases – companies prefer to postpone investment projects. Second, the national uncertainty affects the elasticity of investment to interest rate. With a high level of uncertainty, economic agents may postpone or significantly reduce investment programs even if conditions for raising funds are favorable. Finally, it appears that the decrease in interest rates in the economy with a high level of uncertainty may not lead to the increase in investment demand. In such countries, it is extremely important for policy-makers to stimulate investment demand by creating a so-called investment impulse, which may include promoting public-private partnerships. Finally, global uncertainty has a significant impact on investment demand. Thus, the global uncertainty can significantly slow down investment growth even when economic conditions in the country are favorable.

All of the conclusions obtained have the research and practical interest, as they demonstrate the importance of finding alternative instruments to stimulate investment in conditions of increasing uncertainty. This is because empirical evidence shows that the effectiveness of traditional monetary measures is decreasing when the uncertainty level is high. In addition, the study assesses the impact of external shocks associated with increased global uncertainty, which should be taken into account when designing investment-stimulating policies.

Literature Review

Uncertainty has an impact on key economic indicators at both the macro and micro levels. Baker et al. (2016) showed that economic policy uncertainty could lead to a decrease in investment, employment and GDP. The study focuses on the relationship between the degree of uncertainty and the change in potential GDP, showing that when uncertainty increases potential output decreases in 1 to 2 months. Uncertainty can also affect the rate of economic growth (Alao et al., 2023), energy efficiency (Lee et al., 2024), business cycles of firms, leading to lower levels of output (Baker et al., 2016; Gulen & Ion, 2016), risk management process (Kimiagari & Keivanpour, 2018) and, the level of investment itself (Olasehinde-Williams & Özkan, 2022).

According to the classical investment theory, investments depend on the expected future cash flow and the level of expected return, discount rate. The discount rate reflects the existing risk, which includes the level of uncertainty faced by the investors in implementing the project (Caixe, 2021). Uncertainty also negatively affects investors’ expectations of future cash flows as it is difficult to predict future demand accurately (Kang et al., 2014).

The theoretical foundations of the impact of uncertainty on investment decisions are developed in the researches of various authors, including Bernanke’s (1983), Dixit and Pindyck (1994), McDonald and Siegel (1986), Pindyck (1988). McDonald and Siegel (1986) note that under uncertainty, the importance and value of additional information significantly grows, leading to higher transaction costs and consequently lower investment activity. Dixit and Pindyck (1994) present a theoretical model of investment behavior, considering a short period of time. The authors note that uncertainty could significantly increase the volatility of future cash flows and the level of expected returns, investors are likely to adopt a “just waiting” strategy, postponing investment decisions to a later date. Thus, if firms assume that economic agents are not willing to invest and do not expect high demand for their products, they are likely to delay investments in the current period (Kydland and Prescott (1982), Long and Plosser (1983), Romer (2011).

Recent studies have also found a negative relationship between investment and uncertainty, both for developed (e.g., for Australia [Moore, 2017]) and emerging market countries (Saxegaard et al., 2022; Wang et al., 2014). However there is the lack of research about such dependence for the large sample last years.

Based on the above analysis, hypothesis 1 is proposed.

The expected return depends on the cost of raising funds. According to the classical theory, the lower the cost of financing, the more profitable is the implementation of investment projects, other things being equal. Uncertainty drives up financial and operational risks, and investors require higher risk premiums to compensate for the higher probability of losses (Bradley et al., 2016; Pastor & Veronesi, 2013). It is also noted that higher uncertainty leads to a significant increase in the cost of capital (Liao et al., 2015; Wang et al., 2014). A possible indirect effect is also discussed in a study by Khan et al. (2020) who suggest that it can be observed through changes in the company’s cash flow.

In our study, we propose the hypothesis that uncertainty has an indirect effect on investments, it reduces the efficiency of the transmission mechanism. When uncertainty increases, the sensitivity of investments to changes in interest rates decreases. Even under favorable conditions for raising long-term funds, economic agents may refrain from implementing investment programs due to high uncertainty.

Despite the debate on possible indirect effects of the indicator on investments, previous researches have not considered the impact through decreased the interest elasticity of investment. Based on this, hypothesis 2 is proposed.

In the context of globalization, the commodity and financial markets of most countries of the world are becoming more interconnected. The active process of internationalization and globalization pushes companies to participate more actively in international markets. The current state and future development direction of the world’s commodity and financial markets, with their diverse cultural settings, have a significant impact on management, finance and business (Vahid et al., 2020). Effective positioning in the global market largely depends on the company’s ability to adopt a systematic approach to operations and risk management (Kimiagari & Montreuil, 2017). So this study assumes that not only the national level of uncertainty affects the investment behavior of economic agents, but also the global uncertainty has an impact on investments within the country. The analysis and assessment of the impact of global level of uncertainty on investment demand has not been sufficiently covered in previous studies.

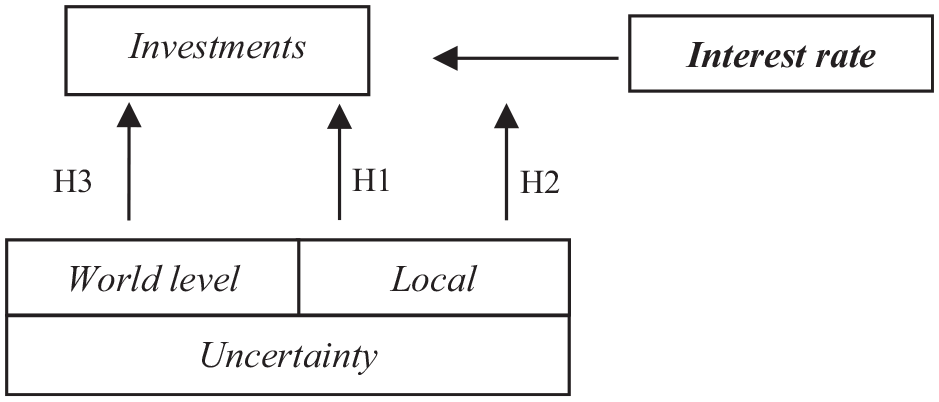

In summary, this research examines the indirect impact of local uncertainty on investments through its elasticity to changes in interest rates and the direct effect of the world level of uncertainty on domestic investment demand. These aspects represent the authors’ contribution to this area of research (Figure 1).

Theoretical framework.

All three hypotheses follow from the research objective: to confirm the existence of direct impact of uncertainty growth, as well as to show the existence of a significant indirect impact factor on the level of investment by reducing its sensitivity to changes in the interest rate.

Methodology and Data

Methodology

The study uses data for 161 countries in the period from 2002 to 2022. Each country has its own distinctive features and characteristics of socio-economic development. We use panel data analysis for this reason. It allows to take into account individual characteristics due to fixed individual effects in the error term. We assume that investments in a country is serially correlated over time.

i– number of objects in the sample, t– time variable and j– number of variables. In the equation presented above X is the vector scalar, which includes all explanatory variables except the lag of the dependent variable. The disturbance term consists of two orthogonal components: the fixed individual effects,

Under normal circumstances, when the lag of dependent variable is significant the estimation is complicated by the problem of endogeneity:

To solve this problem, we use the Arellano and Bond approach (Arellano & Bond, 1991). It means that we perform the first-order difference operation in both sides of the equation to obtain the following:

We assume that the difference of the dependent variable is not correlated with

On the one hand, it helps to solve the endogenous problem, but can also cause another one – such as error correlations and the problem of overidentification due to too many instruments (Kripfganz, 2019). The number of instruments increases rapidly with the number of regressors and the number of periods (Roodman, 2009). Therefore, after estimation, it is important to make the post estimation overidentification tests, such as – Sargan-Hansen of overidentifying restrictions (2-stage weighting matrix and 3-stage weighting matrix). In terms of correlation, when

Variable Selection

The Explained Variable

Gross fixed capital formation is used as the dependent variable. The indicator is calculated in fixed prices of 2015. The indicator represents the acquisition of produced assets (including purchases of second-hand assets), including the production of such assets for producers for their own use, minus disposal. This study uses the natural logarithm in the regression. The data comes from the World Band Dataset.

Uncertainty Level

This study examines the impact of uncertainty on investments. Uncertainty affects the level of expectations and, accordingly, investment decisions. In this case, we are talking about investors’ uncertainty about future cash flows and the excepted return. In order to choose a quantitative indicator of uncertainty, we consider the existing approaches to its assessment (Table 1).

Approaches to Measuring the Level of Uncertainty.

Source. Made by the authors.

There are two large groups of approaches to estimate the uncertainty. The first group contains estimation methods based on calculating the volatility of financial market indices or macroeconomic indicators. The second group is based on textual analysis (based on Twitter messages, national media sources or international reports).

The aim of this article, as mentioned earlier, is to investigate the direct and indirect effects of uncertainty on global investment demand. Therefore, we would like to quantify uncertainty to reflect the level of economic agents’ expectations and make it comparable for different economies of the world. In such a case, it is difficult to apply the volatility-based approach, as the economies and financial markets of the countries in the sample differ in key characteristics, such as trading volumes, liquidity level and volatility.

A textual analysis approach may be more reflective of public sentiment and comparable across countries. But, even in this case some difficulties may arise. When considering the textual analysis, the resulting uncertainty estimate may depend significantly on the list of publications used for calculation. For example, uncertainty for China calculated based on the South China Morning Post (SCMP), a newspaper published in Hong Kong (Baker et al., 2016), and one based on periodicals in mainland China (Huang & Luk, 2020) differ drastically during the external shocks (e.g., trade war with the United States).

This study uses the WUI (World Uncertainty Index) as a quantitative indicator of uncertainty. The calculation of the index is presented for a large set of countries in the world, and for the world economy as a whole (Ahir et al., 2022). The quantitative calculation of the index is based on textual analysis of the EIU country reports (Economist Intelligence Unit). The advantage of this method is that its quantitative assessment does not depend on editorial policy, as in the case of the EPU indicator (Baker et al., 2016). These reports have a single, unified structure for all countries, the requirements for presentation of information are uniform, it allows to obtain comparable estimates of the indicator for different countries. The assessment process appears to be standardized, as there is a single source for calculation covering all countries. In this study, the World Uncertainty Index was used as a factor of local uncertainty for each country and as a global uncertainty level. The growth rate of WUI is included into regression.

Control Variables

Interest rate (interest). According to classical macroeconomic theory, investment is a function of interest rate in the economy (Dixit & Pindyck, 1994). This study uses the lending rate. The lending rate is the bank interest rate that normally covers the short and medium-term financing needs of the private sector. This interest rate is usually differentiated according to the creditworthiness of the borrower and the objectives of its financing.

GDP per capita (GDP per capita). The existing level of welfare may have an impact on investment dynamics (Kydland & Prescott, 1982; Long & Plosser, 1983; Plosser, 1989; Romer, 2011). GDP per capita is the gross domestic product divided by the population at mid-year. GDP is the sum of the gross value added of all resident producers in the economy plus all product taxes and minus all subsidies that are not included in the value of the products. It is calculated without deductions for the depreciation of produced assets or for the depletion and extraction of natural resources. The data are in constant 2015 U.S. dollars. In order to eliminate heteroscedasticity, the natural logarithm of the indicator was used in the analysis. The data comes from the International Monetary Fund, International Financial Statistics and data files.

Price level (the inflation rate). Since we have included the nominal interest rate and also want to find out the impact of the inflation rate on investment demand, we have included the price level factor. Barrero et al. (2017) demonstrated the importance of price level and included it into the regression to analyze its potential impact on investment demand. Inflation, as measured by the consumer price index, reflects the annual percentage change in the cost to the average consumer of purchasing a basket of goods and services, which may be set or collected at specified intervals, for example, annually. In general, the Laspeyres formula is used. The data comes from World Bank Dataset.

Table 2 presents the descriptive statistics for all variables (the non-transformed Investment level, interest rate and GDP per capita).

Statistical Description of Variables.

During the period under review, the highest nominal interest rate was observed in Zimbabwe in 2022, while the lowest value was observed for the EU countries between 2016 and 2022, it was equal to 0.25% per annum. At the same time the average value of the nominal interest rate for all countries in the sample for the same time period is 11%. The level of uncertainty for the research period averaged 0.194 (or 19.4%) for all the countries in the sample.

Model Construction

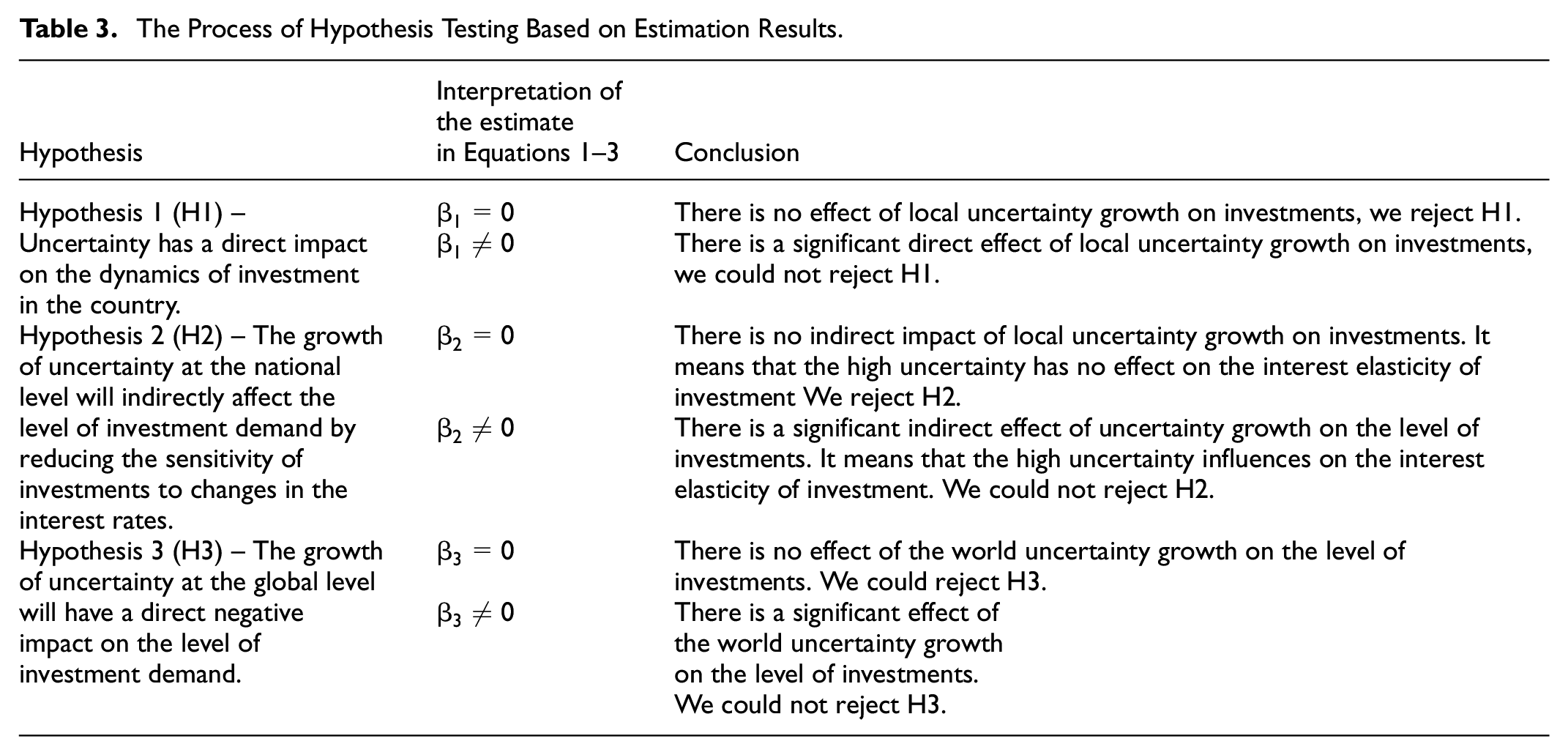

According to the research task formulated, the article analyzes the direct and indirect impacts of uncertainty on investment demand levels. To test these assumptions, three key hypotheses have been put forward.

To test the hypotheses 1 to 3 above, we estimate Equation 1 to 3.

We evaluate Equation 1 to analyze the direct impact of the national uncertainty on investment level. In the Equation 1, the dependent variable is gross fixed capital formation (its natural logarithm,

The equation contained data for 161 countries.

To test the hypothesis 2 we estimate the Equation 2. It includes the regressor for the indirect effect of the local uncertainty on investment demand, growth rate of local WUI and interest rate (WUI × interest). We assume that an increase in the uncertainty factor will significantly reduce the effectiveness of traditional monetary policy instruments and decrease the impact of interest rate changes on investment demand.

To test the hypothesis 3 the Equation 3 is estimated. It includes the growth rate of the global level of the uncertainty (

We use GMM estimator with instrumental variables, so multicollinearity is not a problem as the effect of independent variables is isolated from group effect. However, we estimate the Spearmen correlation to analyze the dependence between local and world uncertainties and find that it is equal to 0.7, 2 so variables are highly correlated. We decide to estimate three different equations with including local and world level of uncertainty separately.

The lags of both dependent and independent variables are used as instrumental variables. The depth of these lags varied depending on the results of the Arellano-Bond test for AR(1) and AR(2).

We estimate the Equations 1 to 3 and based on the results, we make the conclusions on the hypotheses made earlier (Table 3).

The Process of Hypothesis Testing Based on Estimation Results.

Results

Impact of Local and World Uncertainties

This paper uses Stata software for the analysis. The results are presented in Table 4 below. In some cases we reject AR(2) test with the lagging period of investments, so we use the usual strategy such as adding deeper lags of dependent variable and regressors to get the reliable results for AR(1) and AR(2) tests (Kripfganz, 2019). As the serially correlated residuals mean invalidity of instrumental variables (and as the result estimator inconsistency) we implement also the portmanteau test (Jochmans, 2020). Jochmans (2020) proposes this test for panel with small T (like in our case) and demonstrates that it was more powerful for the short panels.

System GMM Estimations for the basic specifications.

Note. This table shows the results for dynamic panel model. Column (1) contains the estimation results for Equation 1 with the national level of uncertainty. Column (2) contains the estimation results for Equation 2 with the indirect impact of local uncertainty. Column (3) contains the results for Equation 3 with the world level of uncertainty. The standard errors of robustness are in parentheses, ***, ** and * indicate statistical significance at 1%, 5% and 10%, respectively. The depth of the lag for the variables was determined by trying out different options and examine the results of Arellano-Bond test for AR(1) and AR(2).

When analyzing dynamic panel data, the problem of “too many instruments” can arise – the number of instruments grows rapidly with the number of regressors and the number of periods. (Roodman, 2009). This problem may cause biased coefficient and standard error estimates and weakened specification tests (Kripfganz, 2019), to reduce the number of them we implement a collapsing approach: instead of the GMM type instruments we use “standard” ones (Kripfganz, 2019). The price, nominal interest rate, GDP per capita and uncertainty level in the country are all assumed to be strictly endogenous with deeper lags included. The world level of uncertainty is assumed to be pre-determined (lags for two periods included). Time variables are included as instruments only for the level model.

Column (1) presents the estimations for Equation 1 with only national level of uncertainty.

The lagging first-order of investment pass the significance test at 1% and the lagging second-order of investment passed it at 5%. It means that the current investment and the previous adjustment of investment are closely related, here the dynamic adjustment process could be observed. The coefficient of the nominal interest rate is negative, indicating that the increase in it is negative correlated with the investment growth. The coefficient for GDP per capita is positive, passing the test at the significance of 1%. When the economic development level increases it stimulates investment demand in the country.

The country uncertainty level (WUI) is significant, demonstrates its significance at the 5% level. Its coefficient is equal to −0.0549. The lagging first-order of local WUI is not significant. It means that increase in uncertainty level within the country causes the decrease in investment growth at the same period. Similar findings are discussed in Kydland and Prescott (1982), Long and Plosser (1983), Romer (2011) and Saxegaard et al. (2022).

Column (2) presents the estimations for Equation 2 with the indirect effect of the local uncertainty. The factor of indirect effect, cross-multiplier of WUI and interest rate is significant with the 5% level. Its coefficient is positive. Despite favorable conditions for attracting funds, economic agents could prefer to postpone the implementation of investment plans. If the uncertainty is high, it is extremely difficult to forecast demand and future costs, to define the expected cash flows. In such a situation, monetary policy instruments may be ineffective. For a country facing a high level of uncertainty growth rate, a possible measure to stimulate investment demand may be the so-called investment push, for example, the implementation of projects with public-private partnership.

Column (3) contains the results for Equation 3 with the analysis of world uncertainty impact on investment demand. In this case the negative significance of interest rate and the positive significance of GDP per capita are also observed. The current level of the world uncertainty is insignificant, and the lagging first-order demonstrates its negative significance. This fact indicates that investment demand in the country is sensitive to changes in the level of uncertainty in the world with a one period lag. At the same time, as mentioned earlier, the impact of national uncertainty is observed during the same period.

All post-estimation tests confirmed the quality of the instruments used.

The Sargan-Hansen tests check the model for an overidentification problem, problem of too many instruments. In our case, we reject the null hypothesis for all modifications on the basis of both tests, find the evidence for the reliability of the estimates obtained.

Robustness Check

We check the robustness, replacing the WUI variable for each country with the dummy variable. It is equal to 1 in case there is the growth of uncertainty and 0 otherwise. We re-analyze the direct and indirect effects of local uncertainty adding the dummy in Equations 1 and 2. The regression results are presented in Table 5. The key explanatory variables didn’t change significance. The direction and extent of the direct and indirect impacts of uncertainty did not change much.

System GMM Estimations for robustness check.

Note. This table shows the results for dynamic panel model. Column (1) contains the estimation results for Equation 1 with the dummy variable. It is equal to 1 in case WUI increases and 0 – otherwise. Column (2) contains the estimation results for the indirect impact of uncertainty. It contains the cross-multiplier of dummy for WUI increase and the nominal interest rate. The standard errors of robustness are in parentheses, ***, ** and * indicate statistical significance at 1%, 5% and 10%, respectively.

Based on the empirical results (Table 4), the negative impact of the national level of uncertainty on the investment dynamics is empirically confirmed. Thus, when uncertainty increases, investment demand will slow down by an average of 3.6% for the sample during the research period. Similar conclusions are obtained for the indirect effect of uncertainty. With the increase of the national uncertainty, the interest elasticity of investment significantly declines, thereby reducing the effectiveness of monetary policy instruments.

Conclusion

Investments directly depend on the expected future cash flows and expected returns. Future cash flows depend on the future demand while the expected return take into account investment risks. Uncertainty significantly affects the future dynamics of demand and the value of the risk premium. Under conditions of uncertainty, economic agents prefer to adopt “a wait-and-see” approach, it impacts both the level of consumption (subsequently affecting forecast of the aggregate demand) and investment expenditures. Empirically, the direct effect of uncertainty on investments has been confirmed by Baker et al. (2016), Chen et al. (2020), Ghosh and Olsen (2009).

The idea of uncertainty affecting the level of investments is not new one and has been discussed in numerous studies. However, to date, there are no works in the economic literature that consider and assess the direct and indirect impact of uncertainty on investment demand around the world, as well as take into account the impact of the global value of this indicator.

Based on the application of GMM estimator, this study also shows that an increase in uncertainty leads to a decrease in investment activity. At the same time, the impact of the national level of uncertainty is observed immediately in the same period. Hypothesis 1 is confirmed.

We assume that effectiveness of stimulative monetary policy significantly diminishes under conditions of high uncertainty. For 161 countries over the period from 2002 to 2022, it is shown that the interest elasticity of investment is a function of the level of uncertainty. A positive significant coefficient indicates that when the WUI grows, a decrease in the interest rates may not lead to increase in the investment activities, but instead may reduce it. The second hypothesis is also confirmed. This result represents significant research and practical value. When local uncertainty is high, monetary policy may not be effective in stimulating investment demand.

In addition, this study emphasizes the importance of considering not only the level of uncertainty in the country, but also at the global level. However, the impact of the global level of uncertainty does not occur immediately, but with a 1-year lag. Hypothesis 3 is also confirmed.

Based on empirical results, we can formulate the following practical recommendations for policy-makers. First, when designing measures to support investment demand, it is important to assess the existing level and analyze the dynamics of uncertainty both at the national and global levels. Second, stimulative tools of monetary policy may be less effective when the level of uncertainty in a country is high. Despite favorable conditions for attracting long-term funds, economic agents may tend to reduce the investment programs or postpone their implementation for a longer period of time. Reduced sensitivity of investment to interest rate may be a result of high level of uncertainty. In such circumstances regulators should consider creating an investment stimulus, providing conditions for significant projects to be realized, including those with the public-private partnership.

The limitation of the presented study is the fact that the interest elasticity of investment can actually be influences not only by the uncertainty factor, but also by other indicators of socio-economic development. For example, it may depend on the state of the institutional environment (Wolfgang et al., 2018) or on developments in the financial market (Y. Lu et al., 2024). We plan to take these factors into account in the future research.

Footnotes

Acknowledgements

The authors gratefully acknowledges comments on earlier version of the paper by seminar participants in SAXO Fintech Business School at Sanya Unversity.

Author Contributions

Haifei Wang: Conceptualization, Formal analysis, Investigation, Resources, Data Curation, Writing – original draft. Ekaterina Isupova: Methodology, Software, Validation, Writing – review and editing, Supervision.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the Financial Innovation and Multi-Asset Intelligent Trading Laboratory, which is part of the Key Laboratory for Philosophy and Social Sciences at the University of Sanya in Hainan Province.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available in [World Bank Open Data] at [URL://data.worldbank.org]. These data were derived from the following resources available in the public domain: [https://data.worldbank.org].