Abstract

This article aims to investigate the impact of financial support on output of township and village enterprises (TVEs) during 2007 to 2013. We use panel data of 28 provinces of China to study the heterogeneous effects of financial support on output of TVEs by introducing control variables and financial support variables of interaction terms and panel threshold model. This article uses the counterfactual measurement method to measure the actual contribution of financial support toward the output of TVEs. The results show that there is an inverted-U relationship between financial support and output of TVEs. Foreign capital participation and economic development enhance the driving effect of financial support, whereas, export intensity, fiscal support, and expansion of enterprise scale reduce the financial support effect. Regional analyses indicate that financial support in the central region of China has a significant positive effect; however, the effect of financial support is not significant in the western region. Furthermore, the contribution of financial support to the total output is 16% to 18% in the eastern region, and 14% to 16% in the central region.

Keywords

Introduction

China’s economy has maintained a momentum of rapid growth since the economic reforms of 1978 and opening up era. The progress of township and village enterprises (TVEs) has played a significant role in the rapid development of rural economy. The growth of TVEs can engage the rural labor force and drive rural economic development; it can also narrow the income gap between urban and rural areas and promote the rationalization of industrial structure and the sustainable development of the national economy. From the corporate structure viewpoint, TVEs are mostly small- and medium-sized enterprises. Most of the large-scale enterprises are concentrated in urban areas. For the western regions, where the urbanization rate is not high, accelerating the development of TVEs and their robust role in rural economic development can also narrow the regional development gap. However, the development of TVEs is attached with policy support. Under China’s current supply-side reforms, the investment efficiency of TVEs is linked with their growth to increase the profit from this sector. Therefore, more investment can continuously promote the sustainable development of both rural and national economies.

Financial institutions’ support is the key to promote the development of TVEs. For the fixed asset investment of TVEs, the loan amount of financial institutions was 158.9 billion Yuan in 2003. By 2013, these loan funds reached 1.443 trillion Yuan, with an average growth rate of almost 24% per annum. The proportion of loans from financial institutions is maintained at around 12% to 15%. From the perspective of regional differences, TVEs’ loan amount from financial institutions in the eastern region was the highest, standing at 925 billion Yuan.

It is generally believed that financial development can lower the degree of financial constraints for enterprises and encourage them to increase investment, thereby increasing the productivity of enterprises. However, because different types of enterprises are subject to different degrees of financing constraints, the large-scale enterprises are usually subject to a lower level of financial constraints. Thus, the financial support for large-scale enterprises may be relatively minor. In addition, unnecessary financial support provided to the enterprises will cause excessive investment due to the bias of financial institutions’ loans, which can reduce the business performance. Therefore, the questions of whether the loan support of financial institutions significantly promotes the growth of TVEs, whether there is heterogeneity of financial support in the effects of TVEs in different regions and how much has financial support contributed to the output of TVEs need to be further studied.

Literature Review

In view of the important role of financial support in the development of enterprises, plenty of literature is available on financial development affecting the growth of enterprises at home and abroad. Most of the available studies support the view that financial support can promote the growth of enterprises; there may be some differences in the perspective of research, but the findings are similar. Love (2003) asserted that financial development can reduce the degree of information asymmetry, ease corporate financing constraints, and then increase the efficiency of corporate investment. Beck, Demirgüç-Kunt, and Maksimovic (2006) found that the development of financial intermediaries, such as banks, helps the enterprises’ growth. Y. Lin and Sun (2005) verified that informal finance has advantages in collecting “soft information” of small and medium enterprises (SMEs) and can improve the efficiency of capital allocation in credit markets. Ju, Lu, and Huang (2015) carried out a research on nonfinancial listed companies in China and suggested that formal financial system reforms at different stages have different effects on the growth of enterprises. P. Zhang and Shi (2016) found that financial markets can help in easing the financing constraints on various types of enterprises. Wu and Jia (2016) indicated that development of small- and medium-sized banks can improve the productivity of industrial enterprises.

Using the provincial level data, Dacosta and Carroll (2001) argued that the rapid Chinese economic growth is associated with the international trade and investment. The role of TVEs is more significant than the state-owned enterprises (SOEs) in the development of China. Smyth, Wang, and Kiang (2001) argued that TVEs performed better than SOEs due to their internal mechanism. The lower efficiency and less productivity are associated with the close link between government and local firms. The increased level of debt deteriorated the performance of small firms resulted into alternative control measures from the local government. These measures included shareholding and outright privatization. Using the data of 80 TVEs, Chang, McCall, and Wang (2003) examined the impact of financial incentives and the form of ownership on the firms’ performance; the results indicated that most of the community-owned local-government-controlled firms first introduced managerial incentive contracts and then more clearly defined income and control rights. The incentives have positive impact on performance, and the better defined rights enhance the performance of these firms.

Analyzing the productive efficiency of TVEs in the manufacturing sector, Fu and Balasubramanyam (2003) found that TVEs are more efficient and productive than SOEs as well as more competitive in international market. The efficient management, which effectively uses the national endowments and resources, is essential for the success of manufacturing enterprises. Examining the efficiency of collective-owned township and village enterprises (COTVEs) in Wuxi City, China, Shiraishi and Yano (2004) concluded that the efficiency of COTVEs remained constant but the productivity level declined as compared to other firms. In addition, these firms faced serious shortage of capital and lower efficiency during financial crises. This indicates that privatization of COTVEs without other macroeconomic policy measures took place to deal with the declining productivity of firms.

Investigating the impact of economic and institutional reform packages on firms’ performance, Ito (2006) concluded that competition is a key factor promoting efficiency; moreover, the modernization of financial and fiscal institutions eliminated the soft-budget regime and promoted both privatization and the performance of TVEs. In addition, the reform packages collectively produced the financial benefits from privatization. Cheng, Nugent, and Qiu (2006) tested the effects of managerial autonomy on efficiency with and without alignment with incentives in a panel of Chinese TVEs. Their results confirmed that the positive impact of managerial autonomy is only linked with incentives. Since the economic reforms of 1978, the TVEs played an important role in the sustainable development of China. Examining the development and current status of TVEs in China, Liang (2006) suggested that the TVEs should develop advanced internal and external mechanism to perform efficiently in the modern era; this includes supporting private sector, elevation of industrial structure, improving quality and branding, boosting small business in towns and stimulating regional economic and technical cooperation for a sustainable contribution from TVEs.

At initial level, the economic reforms and the fiscal decentralization helped to improve the performance of domestic firms. This ability has declined with the rising competition and market expansion. However, the local government policy has also negatively affected the situation (Kung & Lin, 2007). Discussing the evolution of Chinese TVEs, Xu and Zhang (2009) elaborated that these firms were a significant contributor to the rapid Chinese economic growth in the past and played a major role in promoting entrepreneurship before legal protections of private property rights, and the SOEs were not performing well to meet the market demand. After the recognition of private ownership, the TVEs lost their market share. The mergers between private firms and government emerged rapidly and changed the industrial environment. This recent change has influenced the role of TVEs in China.

Using a moderated mediation model, Ding, Li, and Wu (2018) examined the effects of government affiliation on the performance and real earnings management of privately held firms in China; the aforementioned affiliation has shown positive impact on performance, whereas regional economic development regulates the relationships between political affiliation and real earnings management as well as firm performance. It is an admitted fact in developed economies that the managerial empowerment and incentives are directly linked with the productivity of a firm. The results of P. Li, Zhang, and Lu (2008) and Shen, Dang, and Wu (2013) showed that the total factor productivity (TFP) of Chinese TVEs continued to decline. However, Fan and Cai (2009), and Sun and Xu (2011) found that the production efficiency of Chinese TVEs was gradually improving. The study of Ju et al. (2015) showed that the formal financial system reforms at different stages have different effects on the growth of enterprises; therefore, the influence of financial support on TVEs may also be heterogeneous. The authors also found that the estimation results obtained using the threshold model are more accurate as compared to the results of linear regression model.

In addition to the aforementioned literature, there are some recent studies related to our topic. Cumming, Deloof, Manigart, and Wright (2019) described that entrepreneurial finance is a distinctive aspect of corporate finance that focuses on different points in the finance life cycle, including work on trade credit, debt finance, micro-cap IPOs, venture capital, and angel finance in various regions of the world. Considering the financial constraints, Vereshchagina (2019) argued that decreasing returns of scale and financial issues stimulate the unequal rules of partnership. The contribution of all partners varies and all stakeholders share the mutual benefit. Exploring the impact of government support on the sale and employment growth of 512 entrepreneurial ventures in Spain, Bertoni, Martí, and Reverte (2019) found a significant link between the variables studied; the impact was more significant for small and young ventures and the loan was more beneficial during financial crises period. Investigating the effects of financial openness on changes in entrepreneurship, Gregory (2019) established that capital controls have a negative and a positive effect on entrepreneurialism in emerging market countries and developed markets, respectively.

Although significant amount of research is available on the influence of financial support on business growth, the literature on TVEs is relatively small and mostly focused on changes in productivity. As compared to the existing studies on TVEs, the novelty of this article includes panel data model with interaction items, panel threshold model and study of the heterogeneous effects of financial support on the growth of TVEs. In the previous studies on the influence of financial development on TVEs, the research on nonlinear effects was relatively scarce. Second, several factors may affect the effectiveness of financial support; hence, the effectiveness of financial support among the three regions might also be different. Therefore, this article performs a more detailed analysis of the difference in financial support on the growth effects of TVEs among the three regions.

We measure the total output of TVEs with financial support variables as well as without financial support variables and discuss the actual output improvements that financial support brings to TVEs with the help of counterfactual measurement method. We also explore the impact of financial support on TVEs in a more objective manner, thereby providing relevant evidence for the formulation of policy recommendations to promote the development of domestic TVEs. Therefore, this study addresses the abovementioned aspects to fill the vacuum in the current literature.

Specification of Model

Basic Model

This article uses a basic fixed-effect panel data model to estimate, the model is expressed as,

wherein FD is the core explanatory variable, financial support, expressed by FD2, is a quadratic term, and the impact of financial support on output of TVEs is likely to be nonlinear; y is the interpreted variable, that is, output of TVEs; α i is the cross-section individual effect; X refers to other control variable that affects the output of TVEs, the subscripts i and t represent the region and year, respectively. However, there may be an interaction effect between control variables and financial support on the output of TVEs, that is, the impact of financial support on the output of TVEs is heterogeneous. In model (1), the intersections of the remaining explanatory variables and the core explanatory variable FD is added to compare the heterogeneous effects of financial support on different types of TVEs.

Variable Selection and Description

The dependent variable chosen in this article is the total output value (Y) of TVEs in each region. To eliminate the influence of price, the total output value of TVEs is converted to the actual total output value of the constant price according to the ex-factory price index of industrial products. Then the natural logarithm of the total output value is used as the dependent variable of this article, namely lnY.

The core explanatory variable of this article FD is measured by the proportion of financial institutions’ loan in the fixed asset investment of TVEs in the current year. At the same time, to explore the nonlinear influence of financial support on TVEs, this article also introduces the quadratic term FD2 of the financial support variable. The control variables selected in this article include the following: (i) Basic input variables: labor input L and capital input K. The labor input L is measured by the number of employees in the regional TVEs at the end of the year, and then is processed by natural logarithm, that is, the explanatory variable is lnL. Capital input K is calculated using the perpetual inventory method. The formula for the measurement of capital stock is (ii) The government’s financial support is expressed by Gov. Financial subsidies will also significantly affect a company’s output because it may reduce the company’s financing constraints (Boycko, Shleifer, & Vishny, 1996; Ren & Lu, 2014). The proportion of funds of countries and relevant parts of the fixed-assets investment in TVEs was measured in that year; (iii) Foreign investment participation (Fdi) is measured by the proportion of foreign investment in the local fixed-assets investment of TVEs.

1

(iv) Export intensity is shown by Export. The openness of TVEs may also affect their output, as enterprises can obtain new technologies through exports to increase productivity, that is, “export learning effects” (Keller, 2009; Loecker, 2013). This article uses the ratio of export delivery value to total output value of TVEs in the current year to measure export intensity; (v) Enterprise scale is expressed by Scale. The scale of an enterprise may also affect its production efficiency. This article uses the ratio of the actual total output value to the number of TVEs to measure scale, and the natural logarithm is processed on this ratio; (vi) Regional economic development level (lnrgdp). The local economic development level will also affect the output of TVEs because the regions with better economic development are driven by local cities to a great extent, and the local urban development will significantly promote the development of local TVEs. This article uses the GDP per capita (rgdp) to measure the local economic development and converts it into actual values according to the GDP implicit price deflator, and the natural logarithm is used.

Sources and Explanations of Data

The data used in this article are derived from Yearbooks of China’s TVEs and Agricultural Products Processing Industry from 2008 to 2012 and Yearbook of China’s Agricultural Products Processing Industry in 2013 to 2014. The gross domestic product (GDP) per capita of each province, and the GDP implicit price deflator, price index of fixed-asset investment, ex-factory price index of industrial product are used to eliminate the impact of price factors and are derived from the “China Statistical Yearbook” of the year. Due to the availability of data and other reasons, the data used in this article includes panel data of 28 provinces from 2007 to 2013; therefore, a total of 196 research samples are included.

Empirical Analysis

Estimated Results of the Basic Fixed-Effect Model

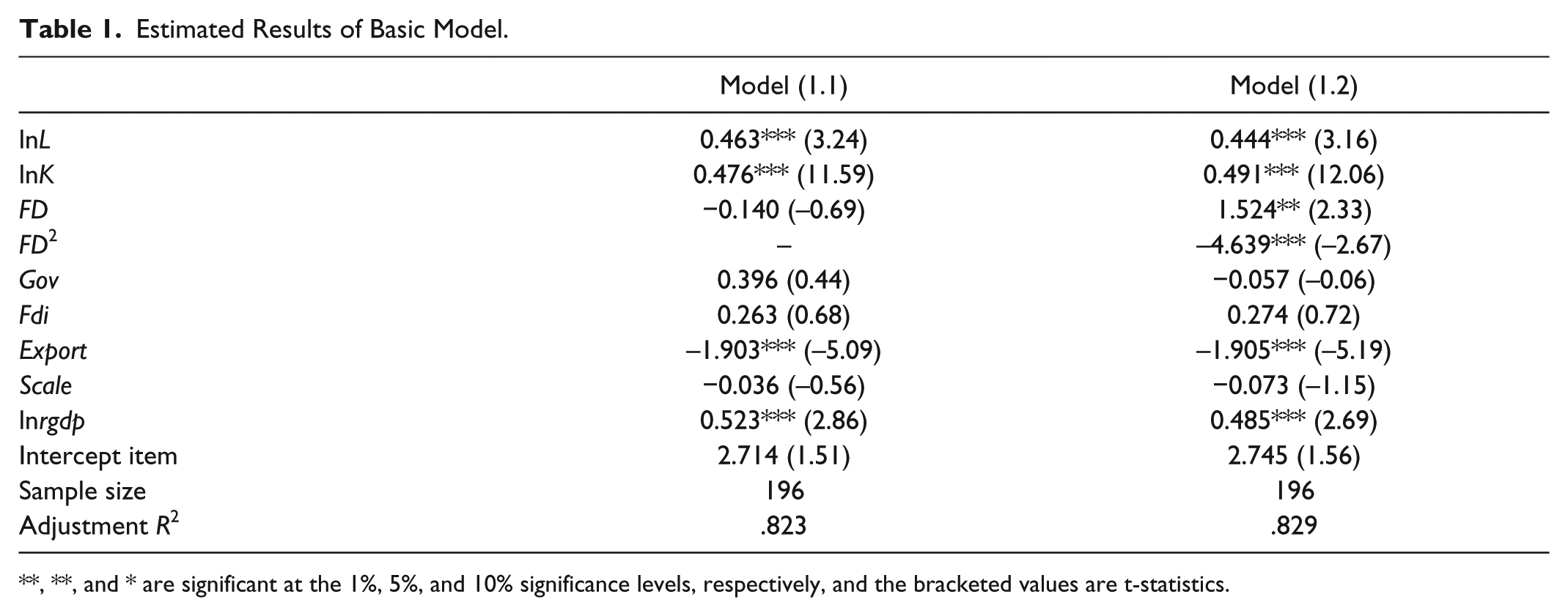

This study used the stochastic effect method to estimate the robustness of results. The results indicated that the conclusions are basically the same whether the fixed-effect estimates or the random effect estimates are used. In addition, the Hausman test also supported the fixed-effects model in most cases and the probability values are significant at given level of significance. Therefore, this article obtained all estimations from the fixed-effects model. To test whether the influence of financial support on enterprises’ output is nonlinear, we use a quadratic term and use the fixed-effect method; the results of the fixed-effect model are presented in Table 1. The second column model (1.1) indicates an estimation output without a quadratic term of the kernel variable, and the third column model (1.2) shows an estimation output with a quadratic term of the financial support.

Estimated Results of Basic Model.

, **, and * are significant at the 1%, 5%, and 10% significance levels, respectively, and the bracketed values are t-statistics.

From the second column of Table 1, it can be seen that when the quadratic term is not introduced, the coefficient of the variable FD is negative, but the coefficient of the variable FD does not pass the significance test. However, according to the third column, after the variable FD2 is introduced, the coefficient of the variable FD becomes large and significantly positive, while the coefficient of the variable FD2 is significantly negative, indicating that the effect of the financial support on the output of TVEs is nonlinear. The turning point of the variable FD is about 0.164. It can be seen that most of the provinces are on the left side of the inverted-U curve, indicating that financial support generally promotes the growth of output of TVEs, but the marginal effect has been decreasing. In addition, compared with the adjusted coefficient of determination of estimated results, it can be seen that the goodness of fit of the introduced variable FD2 is higher than that of the nonintroduced quadratic term, which indicates that the estimation effect after the introduction of the quadratic term is better.

According to the coefficient of the control variables, the coefficient of variable Gov is positive in the model (1.1) and negative in model (1.2), but it does not pass the significance test, indicating that the impact of government’s financial support on the output of TVEs is not significant. The coefficients of the variable Fdi in both model (1.1) and model (1.2) are positive but do not pass the significance test, which indicates that foreign participation has a positive influence on the growth of output of TVEs but is not significant. The estimated coefficient of input variable lnK is higher than that of lnL, which indicates that the output elasticity of capital is higher than that of labor, and the capital of TVEs is relatively scarce at this stage. The coefficient of the variable Export is negative and significant, which may be related to the current “export-productivity paradox” in China. To be precise, companies with higher export intensity in China are often not high-productivity companies. The coefficient of the variable Scale is negative but not significant, indicating that the scale of the business has no significant effect on the output of TVEs. The coefficient of the variable lnrgdp is positive and significant, indicating that the development of the local economy will help to increase the output of local TVEs.

Heterogeneous Effects

To examine the heterogeneous effects of financial support on output of TVEs, this article introduces the interaction terms of each control variable (excluding the basic input variables) and the financial support variable in the model. The estimated results after the introduction of interactive items are shown in Table 2. Model (2.1) to model (2.5) are the estimation results after introducing each control variable and the financial support variable, and model (2.6) is the estimation result after introducing five interaction terms.

Heterogeneous Effects of Financial Support on Output of TVEs.

Note. TVEs = township and village enterprises.

, **, and * are significant at the 1%, 5%, and 10% significance levels, respectively, and the bracketed values are t-statistics.

From the estimation result of model (2.1), we can see that the coefficient of variable FD·Gov is negative, but it does not pass the significance test. This shows that the increase in government financial support will reduce the effect of financial support on the output of TVEs, although it is not statistically significant, the absolute value of the coefficient is relatively large, so the economic significance is still obvious. In addition, after the introduction of this intersection item, the coefficient of the variable Gov becomes positive but does not pass the significance test.

From the estimation result of model (2.2), we can see that the coefficient of variable FD·Fdi is positive, but it does not pass the significance test. This shows that the increase in foreign participation will increase the effect of financial support on the output of TVEs, although it is not statistically significant, the estimated value of the coefficient is relatively large, so the economic significance is still obvious.

From the estimation result of the model (2.3), it can be seen that the coefficient of the variable FD·Export is significantly negative, which indicates that the increase of export intensity will reduce its effect on the use of financial loans, that is, loan support from financial institutions has a stronger effect on the promotion of TVEs with lower export intensity, and the promotion effect on the TVEs with higher export intensity is smaller.

From the estimation results of Model (2.4), we can see that the estimated coefficient of the variable FD·Scale is negative but does not pass the significance test, which indicates that the expansion of the enterprise scale will reduce the effect of financial support, that is, loan support from financial institutions has a more pronounced role in promoting small businesses, although the effect of this difference does not pass the significance test.

From the estimation results of model (2.5), we can see that the estimated coefficient of the variable FD·lnrgdp is positive, which indicates that financial support better promotes TVEs in economically developed areas, although such effect difference does not pass the significance test.

From the model (2.6), we can see that after introducing all five interaction terms, the estimated coefficient symbols of each interaction item variable are exactly the same as models (2.1) to (2.5), which show that each control variable has the same effect on financial support for promoting output of TVEs after introducing all interaction terms. However, the significance level of interaction terms is different from before.

In each model, it can be seen that, after the introduction of interactive items, adjusted R2 is generally improved to a certain extent as compared to no interactive items, indicating that the model’s fit is better after the introduction of interactive items. Adjusted R2 of model (2.6) is the largest after introducing all interactive items, which further shows that each control variable may affect the influence of financial support on output of TVEs.

Estimation of Threshold Model

According to the estimation results in Table 2, although it could determine that the influence of financial support on output of TVEs is heterogeneous, the impact of financial support on output of TVEs may not be repetitive with the change of each control variable. The model that introduces the interaction items determines that the control variable can only promote, suppress, or change the financial support effect. In addition, there is a strong correlation between independent variables and interaction terms, which results in strong multicollinearity of the model, thus making the estimation of model inaccurate. Therefore, the article uses the panel threshold model proposed by Hansen (1999) to study the nonlinear influence of financial support on output of TVEs. It can both enhance the accuracy of the model and further verify the results shown in Table 2. The panel threshold model used in this article can be expressed as:

wherein FD is the core explanatory variable, q is the threshold variable, X is the control variable of the remaining dependent variable y, and γi represents the ith threshold value. In this article, Gov, Fdi, Scale, Export, and Inrgdp are used as threshold variables, and the results of the threshold effect are shown in Table 3. 2

Test Results of Threshold Effect.

Note. The p value and the threshold value are obtained by repeated sampling 300 times using the “Bootstrap” method.

, **, and * are significant at the 1%, 5%, and 10% significance levels, respectively.

Each threshold variable passed the double threshold effect test, but the second threshold values of the threshold variables Gov and Export are smaller than those of the first threshold, so a single threshold model can effectively describe the effect of financial support and export intensity on output of TVEs. The ordinary least squares (OLS) estimation is performed on the model according to the above threshold, and the estimation results are shown in Table 4. The estimation coefficients of the variables FD1, FD2, and FD3, respectively, represent the estimated coefficients of the first, second, and third threshold estimation variables FD.

Estimation Results of Threshold Model.

, **, and * are significant at the 1%, 5%, and 10% significance levels, respectively, and the bracketed values are t-statistics.

According to adjusted R2 of each model, the goodness of fit of model (4.1) to model (4.5), estimated by the threshold model, is higher than model (2.1) to (2.5) that introduces the interaction items, which indicates that the estimation effect of the threshold model is better. From the estimation result of the model (4.1), it can be seen that in the first threshold range, the estimated coefficient of variable FD is positive and significant. In the second threshold range, the coefficient of variable FD is still positive and significant. However, the estimated coefficient decreased from 1.757 in the first threshold to 1.249 in the second threshold, indicating that when the government’s financial support reaches a certain level, the promotion effect of financial loans on output of TVEs will be significantly reduced.

From the estimation results of model (4.2), it can be seen that in the first threshold range, the estimated coefficient of the variable FD is 1.141 and it is significant at the significance level of 10%. In the second threshold, the estimated coefficient of the variable FD increased from 1.141 in the first interval to 1.533 and passed the test at the 5% significance level. When Fdi is located in the third threshold range, the estimated coefficient of the variable FD further increases to 2.548 and passes the significance test. This shows that the influence of financial support on output of TVEs will be affected by Fdi. With the increase of foreign participation, financial support will have a better effect on the output of TVEs.

From the estimation results of model (4.3), it can be seen that in the first threshold range, the estimated coefficient of variable FD is 1.054 and does not pass the significance test. In the second threshold range, the estimated coefficient of variable FD increases to 2.644 and passes the significance test. In the third threshold range, the estimated coefficient of the variable FD drops to −0.359 and does not pass the significance test. Therefore, the impact of financial support on output of TVEs increased first and then declined with the development of the local economy. However, there is a small number of provinces with FD > 4.277 in the third threshold, and only a few regions, such as Shanghai, have TVEs in the third threshold and most of the provinces are in the first and second thresholds. Therefore, with the expansion of enterprise scale, the supporting effect of financial loans as a whole shows a downward trend.

From the estimation results of model (4.4), it can be seen that in the first threshold range, the estimated coefficient of variable FD is 1.753 and passes the significance test. In the second threshold range, the estimated coefficient of variable FD drops to 0.555 and does not pass the significance test. This shows that the impact of financial support on output of TVEs is affected by Export. With an increase in export intensity of TVEs, the promotion effect of financial support on output of TVEs is declining.

From the estimation results of model (4.5), it can be seen that in the first threshold range, the estimated coefficient of variable FD is 1.981 and passed the significance test. In the second threshold range, the estimated coefficient of variable FD drops to 0.884 and does not pass the significance test. In the third threshold range, the estimated coefficient of variable FD increases to 1.502 and passes the significance test. As a result, the impact of financial support on output of TVEs declines first and then increases with the expansion of business scale. However, the number of provinces with lnrgdp > 1.236 is small in the third threshold range. Only a very few regions such as Shanghai are in the third threshold, most of the provinces are located between the first and second thresholds, so the overall supporting effect of financial loan still shows a significant upward trend.

Based on the estimation results in Table 2 and Table 4, it can be seen that using interaction terms or the threshold model, the heterogeneity in financial support for output TVEs is roughly the same. Specifically, the increase in foreign participation and the development of the local economy are all conducive to improving financial support’s effect on the output of TVEs, while export intensity, financial support, and the expansion of business scale will have an inhibitory effect on financial support.

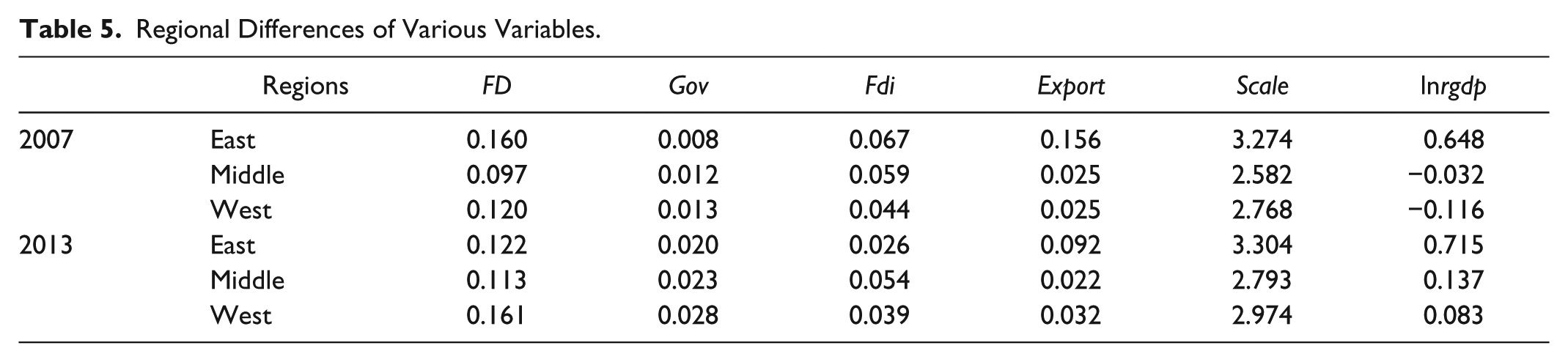

Differences Among the Eastern, Central, and Western Regions

The average values of the control variables and FD in the three major regions in the east, middle, and west of China in 2007 and 2013 are shown in Table 5. The results indicate that the financial support in the eastern region was the highest in 2007, but by the end of 2013, the financial support in the western region was the highest. There are significant differences among the control variables in the eastern, central, and western regions, of which the greatest difference is still the level of economic development.

Regional Differences of Various Variables.

From the estimation results in Table 2 and Table 4, it can be seen that each control variable has significant influence on the impact of financial support on output of TVEs. Therefore, the financial support of each region may have significant differences in the impact on output TVEs. To compare the differences of financial support effects on output of TVEs, this article introduces the dummy variables East, Middle, and West and interaction terms of financial support variables FD and FD2 to compare the differences among the three regions. Table 6 shows the model estimation results after the introduction of dummy variables of the three regions and the financial support variables. The coefficients of the variables Middle·FD2 and West·FD2 in the models (6.1) to (6.3) does not pass the significance test, which indicates that the influence of financial support on the output of TVEs in the central and western regions does not show an inverted U-shaped relationship. While the coefficient of East·FD2 was negative and passed the significance test, the coefficient of East·FD was positive and passed the significance test, indicating that the influence of financial support on output of TVEs in the eastern region demonstrate an inverted U-shaped relationship.

Differences of Impact of Financial Support on Output of TVEs Among the Three Regions.

Note. TVEs = township and village enterprises.

, **, and * are significant at the 1%, 5%, and 10% significance levels, respectively, and the bracketed values are t-statistics.

The results of model (6.4) further indicate that the impact of financial support on output of TVEs is significantly different among the three major regions. Among them, the impact of financial support on the output of TVEs in the eastern region shows an inverted U-shaped curvilinear relationship, and the axis of symmetry of inverted U-shaped curve in the eastern region is about 0.171, and most of the provinces are on the left side of the inverted U-shaped curve. This shows that the financial support in the eastern region mostly promotes the growth of TVEs. The financial support in the central region is the smallest compared to the eastern and western regions. As the financial support in the central region is smaller and the impact of financial support in the central region on the output of TVEs is positive, it has not showed an inverted U-shaped relationship.

The influence of financial support in the western region on output of TVEs is not significant, which is mainly because the impact of financial support on TVEs in the western region is affected by various control variables. The marginal impact of financial support on output of TVEs can be roughly estimated based on the estimated coefficient of model (2.6). The marginal impact can be calculated using the following formula:

The largest gap among the three regions is still the level of economic development. For example, in 2013, the average value of lnrgdp in the west was 0.083, while the average value in the eastern region reached 0.715. The economic development level has a significant effect on the impact of financial support on output TVEs, and the level of economic development in the western region is low, which will significantly suppress the effect of financial support. The estimation results of threshold model in Table 4 further verify this conclusion. When the variables except the level of economic development are used as threshold variables, the estimated values of the FD coefficient for each threshold range change, but the extent of variation is not significant. However, when using the economic development level as a threshold variable, the coefficients of the variable FD in the first and the second threshold range change greatly. This also indicates that the local economic development level has greater influence on the impact of financial support on output TVEs. The low level of economic development in the western regions has significantly inhibited financial support for TVEs, which has resulted in insignificant impact of financial support on output of TVEs in the western region is not significant.

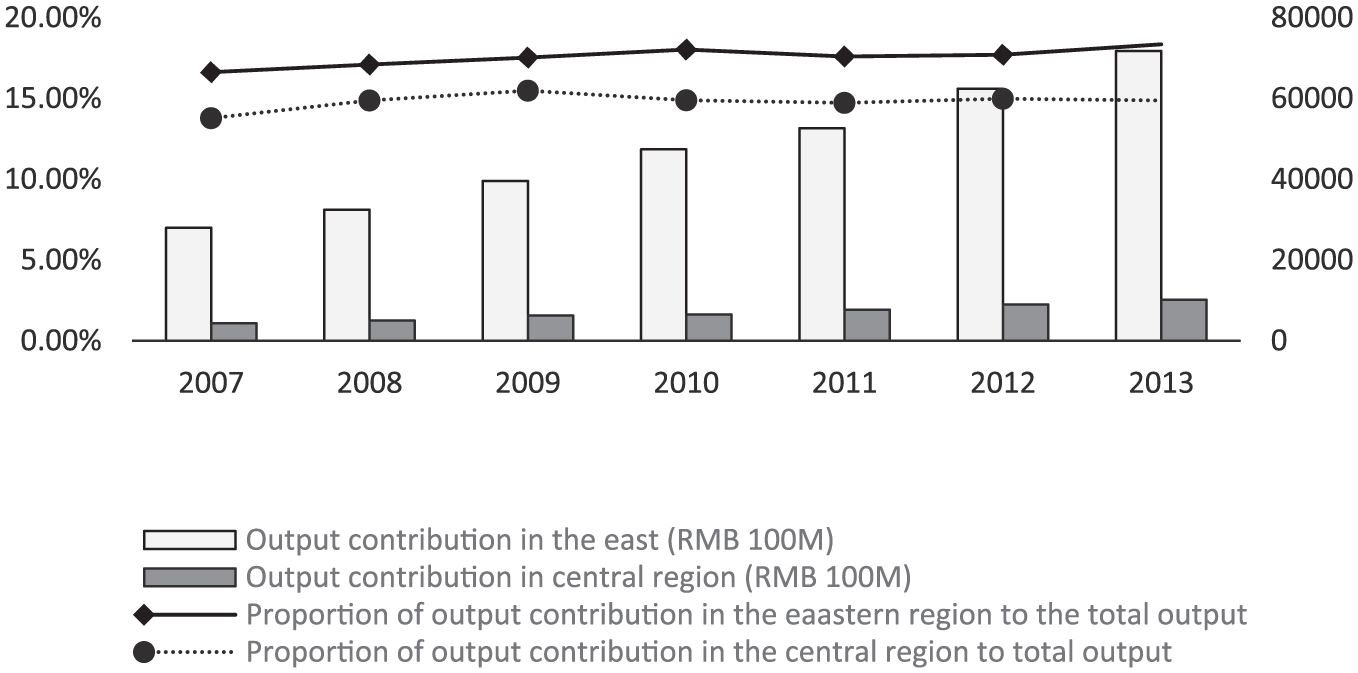

Output Contribution of Financial Support

The above research findings demonstrate that the impact of financial support on output of TVEs in the eastern region is an inverted U-shaped curve, and the financial support in the central region has a significant positive effect on TVEs, while the influence of financial support on output of TVEs in the western region is not significant. But how much does financial support contribute to the output of TVEs? As the impact of financial support in the western region is not significant, this article only measures the influence of financial support on output of TVEs in the eastern and central regions. The method of counterfactual measurement is used in this article. The counterfactual measurement method has a wide range of applications. For example, Fogel (1962) used the counterfactual measurement analysis method to study the impact of railways on the U.S. economy in the 19th century. B. Lin and Du (2013) used the counterfactual measurement method to analyze the energy loss brought by factor market distortions. Y. Li (2018) used the counterfactual measurement method to measure the contribution of tax incentives to the innovation efficiency of high-tech industries. Referring to the aforementioned studies, the specific measurement method is used to assume that the financial support variable FD = 0, and substitute it into the estimation result of the model (6.4) to calculate the output of the TVEs assuming there is no financial support, namely, the counterfactual output y*, then the financial support’s output contribution to TVEs is

Output contribution of financial support.

As it can be seen from Figure 1, the output contribution of financial support in the eastern region to TVEs has gradually increased from 2,798.3 billion Yuan in 2007 to 7,171.8 billion Yuan in 2013. The contribution of financial support in the central region to TVEs also shows an upward trend, but the upward trend is not obvious compared with the output contribution in the eastern region, rising from 432.7 billion Yuan in 2007 to 1.0142 trillion Yuan in 2013. This shows that the output contribution of financial support to the output of TVEs in the eastern region is significantly greater than that of the central region. This is mainly due to the fact that the total output of TVEs in the eastern region is significantly higher than that in the central region.

On the contrary, the proportion of output contribution of financial support to the output of TVEs remains generally stable whether in the eastern region or the central region, but in relative terms, the output contribution of financial support in the eastern region accounts for a higher proportion. From 2007 to 2013, the contribution of financial support to the total output in the eastern region was maintained at approximately 16% to 18%, while the output contribution of the financial support in the central region accounted for approximately 14% to 16% of the total output. This is mainly due to the greater financial support in the eastern region. For example, in 2007, the financial support for TVEs in the eastern region was 0.160, while the financial support in the central region was only 0.097. By 2013, the gap in financial support has decreased. However, this gap still exists.

Conclusions and Policy Implications

Based on the panel data of 28 provinces and cities in China from 2007 to 2013, this article first uses a fixed-effect panel data model to estimate the impact of financial support on output of TVEs. Then we study the heterogeneous effects of financial support on output of TVEs by introducing control variables and financial support variables of interaction terms and panel threshold model. Finally, this article uses the counterfactual measurement method to measure the actual contribution of financial support to the output of TVEs. The major findings obtained in this article are as follows:

From the overall estimation results across the country, the impact of financial support on output of TVEs is an inverted U-shaped relationship. That is, the impact of financial support on output of TVEs decreases with the increase in financial support. Furthermore, China’s most provinces are on the left side of the inverted U-shaped curve, which shows that currently the financial support still has a significant positive impact on the output of TVEs in most regions;

Based on the estimated results of interaction terms, foreign participation and economic development will increase the effect of financial support on the output of TVEs. However, the export intensity, financial support, and the expansion of business size have an inhibitory effect on the effectiveness of financial support. The threshold effect of the panel threshold model passes the significance test, and the estimation results of the threshold model further support the above conclusions.

By region, there is an inverted-U relationship between eastern region’s financial support and output of TVEs, while the central and western regions do not show an inverted U-shaped relationship. In the central region, financial support has a significant positive effect on output of TVEs. The effectiveness of financial support in the western region is not significant. This is mainly due to the fact that the relatively backward economic development significantly inhibits the financial support effect in the western region.

From the results of counterfactual measures, the output contribution of financial support to the output of TVEs in the eastern region is significantly greater than that of the central region. This is mainly due to the fact that the total output of TVEs in the eastern region is significantly greater than that in the central region. The proportion of the contribution of the financial support in the eastern region to the total output is 16% to 18%, and the proportion of the contribution of the financial support in the central region is 14% to 16%.

The policy implications of this study are as follows: (a) although the impact of financial support on the output of TVEs shows an inverted U-shaped relationship, most of the provinces in China are on the left side of the inverted U-shaped curve; therefore, financial support has significant positive effects on the output of TVEs in most regions. Especially, increasing financial support in areas with small financial support can effectively boost local output of TVEs. However, some provinces with excessive financial support may lead to over-investment. Therefore, the financial support for local TVEs should be appropriate but not too big; (b) because foreign participation and economic development increase the driving effect of financial support on the output of TVEs, providing financial loans to TVEs with relatively higher levels of foreign participation and higher levels of economic development can significantly promote the growth in output of TVEs; however, the export intensity, financial support, and the expansion of business size have an inhibitory effect on the effectiveness of financial support, providing financial support to TVEs with lower export intensity, smaller financial support and size can better exert the driving effect of finance on TVEs; (c) due to the low level of economic development in the west, it significantly inhibits the financial support effect. Thus promoting the development of urbanization in the western region and the driving effect of cities to rural areas can improve the effect of financial support on the output of TVEs in the western region, and thus narrow the gap between the eastern and central regions. (d) The actual contribution of financial support to the output of TVEs is the greatest in the eastern region, followed by the central region and western region. As a result, the current financial support for TVEs will only further widen the gap among the TVEs in the eastern, western, and central regions. Therefore, it is still very import to improve the economic environment in the central and western regions, enhance the financial support in the central region, and better play the driving effect of the financial support to local TVEs.

Considering the importance of this topic, research on technological innovation of township enterprises will be a valuable addition to the literature. On the same note, a study on the development path of township enterprises combined with the current market situation can also be conducted to enrich the available literature.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.