Abstract

This research aims at identifying explanatory factors of the environmental disclosure of potentially polluting Brazilian companies listed on the São Paulo Security, Commodities, and Futures Exchange (BM&FBOVESPA), from 2005 to 2015. Financial and environmental disclosure information of 182 Brazilian companies of the high-, medium-, and low-polluting potential sectors were collected. Data were analyzed through content analysis of documents and Regression with Panel Data. Results indicate that the company’s size, profitability, internationalization, and sustainability report are explanatory factors of the disclosure of environmental information, while indebtedness presents an inverse relationship. This study concludes that the explanatory factors of environmental disclosure of potentially polluting Brazilian companies are, with a higher weight, the publication of the sustainability report and stock market internationalization and, with lower weight, size, indebtedness, and profitability. This study discusses the relevance of environmental disclosure to companies that perform potentially polluting activities to provide support for different agents linked to these companies they may have access. It presents as theoretical contribution the explanatory variables for environmental disclosure of potentially polluting companies, an analysis not yet carried out in the literature. The practical contribution is to present information to interested users that potentially polluting companies, larger in size, internationalized, and with more profitability, disclose their environmental information.

Introduction

In Brazil, discussions on the social commitment of companies involving entrepreneurs, community, politicians, and media took place in 1996. The pressures of society on social and environmental issues were relevant for companies to adopt socially and environmentally sustainable initiatives to reduce the impacts caused by their activities on the environment (Marcon, Medeiros, & Ribeiro, 2017).

Because of this, disclosure or environmental disclosure has been a medium used by organizations to legitimize their activities (Branco, Eugénio, & Ribeiro, 2008; Kathuria, 2009; Orsato, Garcia, Mendes-da-Silva, Somonetti, & Monzoni, 2015). The disclosure of environmental information has become routine in companies, not only to comply with regulations, but also, mainly, to demonstrate their environmental concern and social responsibility (Antonio, Manuel, Da Veiga, & Marchetti, 2016; Lu & Abeysekera, 2017). When a company conducts environmental disclosure, it increases communication and reduces the asymmetry of information, so that customers, suppliers, investors, civil society, Government, scientific community, and others may have access to the information (Husted & Sousa-Filho, 2018; Rosa, Ensslin, Ensslin, & Lunkes, 2011; M. A. Souza, Rásia, & Jacques, 2010). In Brazil, one of the ways to disclose the information on open capital companies is making the sustainability report (RSUST) available (Calixto, 2013).

Although environmental demand comes from society, in Brazil there is no standard governing the environmental accountability of the companies to disclose information of this nature, being thus granted voluntarily (Fabricio, Veiga, & Marchetti, 2017; Orsato et al., 2015; Pires & Silveira, 2008). There are some guidelines of regulatory agencies linked to open capital companies, such as Securities and Exchange Commission (SEC), the Institute of Independent Auditors of Brazil (IBRACON), and the Federal Accounting Council (CFC), which regulate the accounting activities of companies when disclosing information on financial statements (Kronbauer & Silva, 2012).

The National Policy on Environment, by means of Law No. 10,165/2000, presents potentially polluting activities and users of environmental resources. These business activities are classified according to their polluting potential as high, medium, or small (Lei nº 10.165, de 27 de dezembro de 2000; Monteiro & Guzmán, 2010). Due to this, companies linked to polluting activities are regulated by public policies that guide environmental management. This becomes a relevant factor for companies with potentially polluting activities to be more likely to disclose more environmental information than companies from other activities (Pereira, Bruni, & Dias Filho, 2010).

Several studies on the theoretical development of environmental evidence, as well as empirical analyzes, have been developed in countries with developed economies; on the contrary, such studies are incipient in developing countries, and a gap emerges, on the subject, to be explored in countries such as Brazil (Clarkson, Li, Richardson, & Vasvari, 2008; Liu & Anbumozhi, 2009; Pletsch, Brighenti, Silva, & Rosa, 2014).

Although research on environmental disclosure in the Brazilian context, thematically similar to this research, has been developed in recent years (Kronbauer & Silva, 2012; Lu & Abeysekera, 2014; Oliveira, Machado, & Beuren, 2012; Orsato et al., 2015; Rosa, Guesser, Hein, Pfitscher, & Lunkes, 2015; Rover, Tomazzia, Murcia, & Borba, 2012; Suttipun & Stanton, 2012; Vogt, Hein, Rosa, & Degenhart, 2017), we did not identify, on the journal databases consulted (Scielo and Spell—http://www.spell.org.br), studies that focused on the explanatory factors of environmental disclosure of potentially polluting Brazilian companies, in all segments of the potential polluters (high, medium, and small potential) from 2005 to 2015. This article adds to the existing literature in three ways. First, it presents information on the relevance of environmental disclosure to companies that perform potentially polluting activities to provide support for different agents linked to these companies they may have access. Second, it presents as theoretical contribution the explanatory variables for environmental disclosure of potentially polluting companies, an analysis not yet carried out in the literature. Third, a practical contribution is to present information to interested users that potentially polluting companies, larger in size, internationalized, and with more profitability (PROF), disclose their environmental information.

Literature Review

Theory of Legitimacy

The perspectives provided by the legitimacy theory indicate that organizations are not considered to be the owners of any rights inherent in the resources that they capture from the environment in which they are inserted or even exist. In fact, such organizations exist to the extent that society in particular regards them as legitimate, and if this is the case, society gives organizations the “state” of legitimacy (Deegan, Rankin, & Tobin, 2002). Therefore, organizations will seek to develop their activities in accordance with the expectations of society, adopting, for this purpose, practices and procedures that are appreciated by the same.

Legitimacy theory followers argue that one of the strategies companies use to gain, maintain, or regain legitimacy is corporate disclosure policies. We work with the hypothesis that some organizations are prone to expand their disclosure mechanisms, regardless of legal requirements, thus explaining the idea that legitimacy theory can contribute to explain and predict disclosure practices in the corporate environment (Dias Filho, 2012).

One of these techniques is the disclosure of social and environmental information, whose objective is to legitimize the activity of the company to make known what the company performs in terms of environmental protection and support to society, thus allowing all parties’ stakeholders to assess the value of the company, future prospects, and opportunities and risks, thereby legitimizing its activity (Eugénio, 2010; Iatridis, 2013), with financial statements and RSUSTs being the main means of communication for companies to disclose environmental information.

Lindblom (1994) states that if a company realizes that its legitimacy is threatened, it usually tries to recover or maintain it through a variety of strategies. In this article, Dias Filho (2012) mentions that organizations use accounting not only as an instrument to support economic decision making, but also as a way of conquering, preserving, and recovering the legitimacy of organizations in the environment in which they operate.

Stakeholder Theory

The stakeholders theory, according to Freeman (1984), presents the idea that long-term sustainability of organizations depends on the manager’s ability to recognize and balance the interests of the various stakeholders by responding to all of them. Because stakeholders have influence over a company, managers must take into account all their needs and, if necessary, modify their activities to minimize conflicts of interest (Huang & Kung, 2010).

According to Cardoso, De Luca, and Gallon (2014), corporate reputation represents the perception of stakeholders about the behavior of organizations, evidenced to the market with transparency and credibility, through communication and disclosure of information. Thus, Ullmann (1985), Huang and Kung (2010), and Lu and Abeysekera (2014) are unanimous in claiming that companies are motivated to evidence sufficient and adequate environmental information to stakeholders as an effective management strategy for development and maintenance of satisfactory relationships with stakeholders, thus ensuring the satisfaction of their needs and allowing their behavior to be perceived as legitimate. However, Rover (2009) emphasizes that the strategy of organizations, in front of their stakeholders, is that it will determine the level of their environmental disclosure: the greater, the more active the policy is.

Both the legitimacy theory and stakeholder theory are better viewed as two overlapping perspectives, which provide useful and different views; because, while it affects the expectations of society in general, it affects the expectations of certain interest groups. In general, it is important to consider them together to provide more insightful explanations of companies’ environmental disclosure practices (Lu & Abeysekera, 2014; Zeng, Xu, Yin, & Tam, 2012).

Environmental Disclosure

The adaptation of companies concerning environmental practices required by different social groups has provoked reflections on management and, also, the way practices related to the environment are reported (Morioka, Bolis, & Carvalho, 2018, Rover et al., 2012). When companies carry out environmental and social disclosure, they seek transparency to legitimize their activities, contributing to interested users to assess the value of the company, future prospects, opportunities, and risks, among others (Amarante et al., 2018; Trierweiller, Peixe, Tezza, & Bornia, 2013; Vogt et al., 2017). Through disclosure, companies can show investors, for example, that the activities and environmental practices carried out by them do not harm the environment (Lu & Abeysekera, 2017).

In companies, it is an environmental accounting duty to make environmental disclosure through their reports (Eckert, Leites, Cechinato, Mecca, & Biasio, 2014). As environmental information is of interest to all groups of users and have an impact, directly or indirectly, on the organization’s heritage, it is its accounting duty to disclose such information, thus serving as a useful tool to control and provide better decisions regarding its activities (R. S. Costa & Marion, 2007; Kasim, 2017; P. R. A. Monteiro & Ferreira, 2007). In China, for example, there are government subsidies that influence the voluntary disclosure of corporate social responsibility, reflected mainly in tax subsidies, thus indicating that the political cost may affect the presentation of information (Lee, Walker, & Zeng, 2017).

Although environmental disclose is a social demand, in Brazil there is no standard governing the environmental accounting of the companies to disclose information of that nature, therefore, they are voluntarily made (Brooks & Oikonomou, 2017; Catapan et al., 2013; Pires & Silveira, 2008). There are some guidelines of regulatory agencies linked to open capital companies, such as SEC, the IBRACON, and the CFC, which regulate the accounting activities of companies when disclosing information on financial statements (C. T. C. Costa, Silva, Almeida, & Veiga, 2017; Kronbauer & Silva, 2012; Marques, Ribeiro, & Barboza, 2018).

Although environmental disclosure is not mandatory in Brazil, the CFC issued Resolution No. 1,003/04, which approved the Brazilian Technical Accounting Standard 15 (NBC T 15), disposing of social and environmental information (CFC, 2004). This standard establishes procedures for disclosure of social and environmental information, aiming to demonstrate to society the participation and social responsibility of the entity. Another regulatory agency, the IBRACON, created the Audit Standard and Procedure 11 (NPA 11—Balance and Ecology) in 1996, to raise awareness of practices against pollution, assaults on human life, and the environment. The Brazilian SEC suggests that open capital traded companies disclosed, in their Management Report, information related to the protection of the environment.

Several research on environmental disclosure were developed. In Brazil, Miranda and Malaquias (2013) observed that the size of the company exerts influence on the level of disclosure, and that companies from regulated sectors (SREGs) disclosed more environmental information when compared with those from non-SREGs. Fernandes (2013) verified that the size of the company positively influences the level of environmental disclosing, and that the participation of Brazilian companies at the New Market governance level, as well as the degree of indebtedness (INDEBT), present negative relationship with environmental disclosure. Silva, Lima, Freitas, Filho, and Lagioia (2015) verified that the size or high PROF of open capital companies does not influence environmental disclosure, while private companies audited by the Big Four tend to make more environmental disclosures in their annual reports than private companies not audited by the Big Four.

By analyzing the 54 largest oil companies in the world, Lenciu, Popa, and Lenciu (2012) found that the presence of an environmental commission on corporate governance explains the increased disclosure of environmental information, as the structure of the board of directors, from a sufficient number of independent members of the Council. In China, Cheung, Jiang, and Tan (2010) found that companies in which the chief executive is not part of the board of directors had a higher rate of voluntary disclosure.

In Thailand, Suttipun and Stanton (2012) found that variables such as the type of industry, status of the property, and type of audit are explanatory of the environmental disclosure in corporate sites. Lu and Abeysekera (2014) verified that the size of the company, PROF, and industry classification are significant for greater social and environmental disclosure in Chinese companies. When analyzing 31 countries, Dhaliwal, Li, Tsang, and Yang (2014) identified a negative relationship between environmental disclosure and the cost of the share capital, especially in countries that target stakeholders more. In the United States, a positive relationship was found between the quality of voluntary environmental disclosure and the value of the company in terms of cash flow and cost of capital components (Plumlee, Brown, Hayes, & Marshall, 2015).

Conceptual Development of the Hypotheses

Based on evidence from the literature, we formulated 12 hypotheses related to possible explanatory factors to the disclosure of potentially polluting companies. It is argued by Liu and Anbumozhi (2009) and Fernandes (2013) that the size of the company is linked to a greater propensity of disclosing environmental information because such companies are subject to observation of society for being in evidence. Added to this, larger companies are likely to present quality information systems (Lopes & Rodrigues, 2007). These authors are the base for the first research hypothesis.

Another explanatory factor of environmental disclosure is INDEBT. Macagnan (2009) clarifies that the higher the level of INDEBT of an entity, the greater the need to reduce information asymmetry among stakeholders, considering that agency costs are higher for companies with more debt in their capital structure, as mentioned by Jensen and Meckling (1976). Thus, company managers are encouraged to disclose information on corporate activities, so as to satisfy creditors as they may adopt more critical postures regarding the companies (Huang & Kung, 2010). These considerations support the second hypothesis.

One way for companies to differentiate themselves is through the dissemination of environmental information, aimed at revealing their “good news” to the financial markets, that is, to provide a signal of their decisions and actions. Thus, entities with greater PROF are inclined to disclose more information, with the intention of differentiating themselves from those with lower PROF, thus demonstrating an advantage over their competitors (Lang & Lundholm, 1993; Lu & Abeysekera, 2014). Based on this, the third hypothesis is presented.

Audit is presented as an explanatory factor for environmental disclosure, when linked to consulting firms such as the Big Four, because they have more independence than other companies due to their size and less influence on the possible loss of a customer (Sunder, 1997). Choi (1999) argues that such firms are fairer and more impartial in their audit opinions and therefore less likely to be influenced by their client firms. As a way of preserving their brand and reputation, the Big Four are prone to require their client companies to disclose additional information, according to Huang and Kung (2010), and as a consequence, to disseminate high-quality environmental information (Wang, Xu, & Wang, 2013). Thus, the fourth hypothesis can be presented.

In the governance structure, the board of directors presents relevance in environmental disclosure. When the board of directors comprises a larger number of members, there is more room for participation by more experienced members and greater efficiency in management. This suggests that greater attention to questions about environmental evidence disclosure can be given when there is a large number of members on the board (Lenciu et al., 2012). Although there is no classification on the number of members to determine the size of the board as large, medium, or small, in Brazil, the Brazilian Institute of Corporate Governance (IBGC, 2010) suggests that the board of directors should be composed of at least five members and at the most, 11. Such arguments support the fifth research hypothesis.

In addition to the previous hypothesis, the presence of a board of directors with independent members can contribute to environmental disclosure. The presence of independent members seeks to neutralize potential conflicts of interests, as well as ensure transparency of financial and environmental information (Lenciu et al., 2012). In addition, when the chief executive of the organization is not part of the board of directors, the transparency of information shall be greater (Cheung et al., 2010). This disclosure becomes more prominent when these independent members act as independent members in other companies (Rupley, Brown, & Marshall, 2012). The quantity of independent directors shall depend on the degree of maturity of the organization, its life cycle, and its characteristics (IBGC, 2010). The sixth research hypothesis is presented.

The international insertion of the company is exposed to be an explanatory factor for environmental disclosure. When companies trade their shares in more than one financial market, the greater is their tendency to disclose environmental information due to regulations of other stock markets (Masullo, 2005). In this argument, emphasis is given to companies that trade shares on the New York Stock Exchange (NYSE), considered the most important stock exchange in the financial market worldwide (Morris & Tronnes, 2008). In this context, the seventh hypothesis is presented.

Companies classified in sectors subject to regulation present more environmental disclosure. The pressures exerted by the regulations make companies classified in SREGs adopt conformity conducts; there is the reason why they comply with requirements, which also aids them to become environmentally sustainable (Jose & Lee, 2007). This argument provides the basis for the eighth research hypothesis.

To complement the eighth hypothesis, a caveat might be added. In Brazil, some companies of São Paulo Security, Commodities, and Futures Exchange (BM&FBOVESPA) are not classified in SREGs; however, they are classified in subsectors subject to regulation. Thus, for companies that belong to a SREG, but which are not subject to regulation, and therefore are not considered a regulated company (CREG), we proposed an extension to the eighth hypothesis.

Agency theory points out that, in a dispersed ownership environment, corporations will provide more information to reduce agency costs and informational asymmetry. The less concentrated ownership motivates managers to disclose more relevant information in view of the pressure they have had to disclose information about socioenvironmental responsibility to meet the demands of the various shareholders (Gondrige, 2010; Lu & Abeysekera, 2014). Thus, the ninth hypothesis can be presented.

The publishing of the RSUST contributes to environmental disclosure. That report is specific to environmental information disclosure (Mota, Mazza, & Oliveira, 2013; Mussoi & Van Bellen, 2010). Thus, the 10th research hypothesis can be described.

In Brazil, in 2005, the corporate sustainability index (ISE) was created, which assesses the performance of companies in business management practices for sustainability (Macedo, Barbosa, Callegari, Monzoni, & Simonetti, 2012). It is argued that companies classified in the ISE present quality, transparency, and commitment to the dissemination of environmental information (Orsato et al., 2015; Reale, Magro, & Ribas, 2018). Based on the information, the 11th hypothesis is presented, considering the ISE as a control variable.

Regarding the 10th (H10) and 11th research hypotheses (H11), an exception must be made. Such variables (RSUST, presence at the ISE), can be correlated with other explanatory variables, and will be used as control variables in the statistical test (Rover, 2009). This occurs because some companies do not develop RSUSTs and/or are not classified at the ISE, but can present a high level of disclosure on environmental disclosure of Explanatory Notes and/or Administrative Reports.

Methodological Procedures

Data were collected from all open capital companies classified as potentially polluting, with shares traded on the Brazilian Stock Exchange BM&FBOVESPA, totaling 182 companies. These companies have published information on standardized financial statements, reference forms, or RSUSTs and/or annual reports in the period between 2005 and 2015.

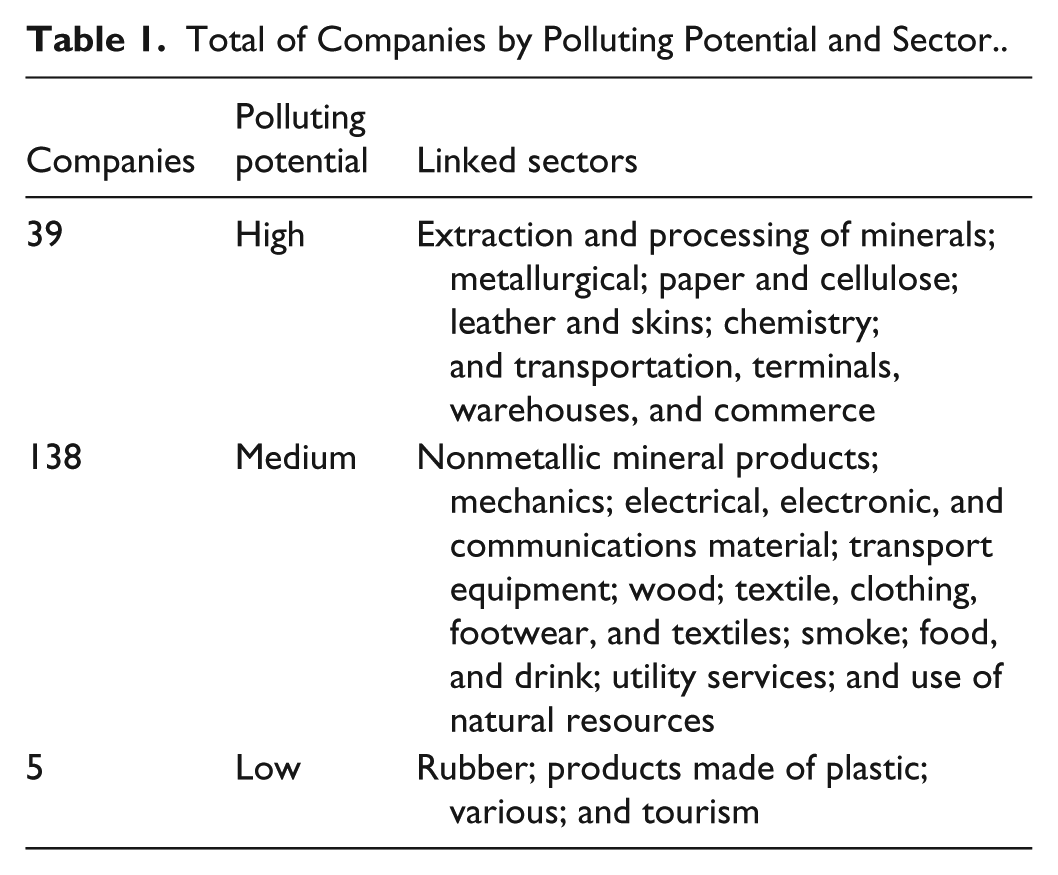

Companies classified as potentially polluting presented a tendency of polluting the environment as a result of their activities and therefore are subject to stricter regulation. For the definition of potentially polluting classification, we used Annex VIII of law No. 10,165/2000, from the Brazilian National Environmental Policy, which ranks the economic activities of companies as high, medium, and low environmental risk. Table 1 presents the total of companies by polluting potential and sector.

Total of Companies by Polluting Potential and Sector.

Two companies were excluded from the final sample (Centro de Tecnologia Canavieira—CTC and Terra Santa) for not presenting the information available, linked to a medium rating of polluting potential. The temporal perspective of the analysis (2005 to 2015) was used for considering the 4-year cycle of institution of Law No. 10,165, which established the potentially polluting classification.

Among the sectors that are regulated are those of exploration, refining, and distribution, inserted in the transportation, terminals, warehousing, and commerce sector, regulated by the National Petroleum Agency (ANP); air transport, inserted in the transportation material sector by the National Civil Aviation Agency (ANAC); electricity and water and sanitation, inserted in public utility services by the National Electric Energy Agency (ANEEL) and the National Water Agency (ANA), respectively; and food and beverage industry by the National Health Surveillance Agency (ANVISA).

To identify the environmental information disclosed by the companies in the sample, we performed content analysis of documents, such as standardized financial statements and the reference forms available on the websites of the BM&FBOVESPA and annual and RSUSTs published on the websites of the companies.

The disclosure variable was defined from a framework of categories and information for analysis of environmental disclosure, adapted from the studies of Rover (2009), C. B. Sousa, da Silva, Ribeiro, and Weffort (2014), and the Sustainability Reporting guidelines of the Global Reporting Initiative (Global Reporting Initiative, 2016). In this framework, we evaluated the presence or absence of information covering nine categories, arranged in 39 items, as presented in Table 2.

Categories and Items of Analysis of Environmental Information Disclosure.

Source. Adapted from Rover (2009), C. B. Sousa, da Silva, Ribeiro, and Weffort (2014) and Global Reporting Initiative (2013).

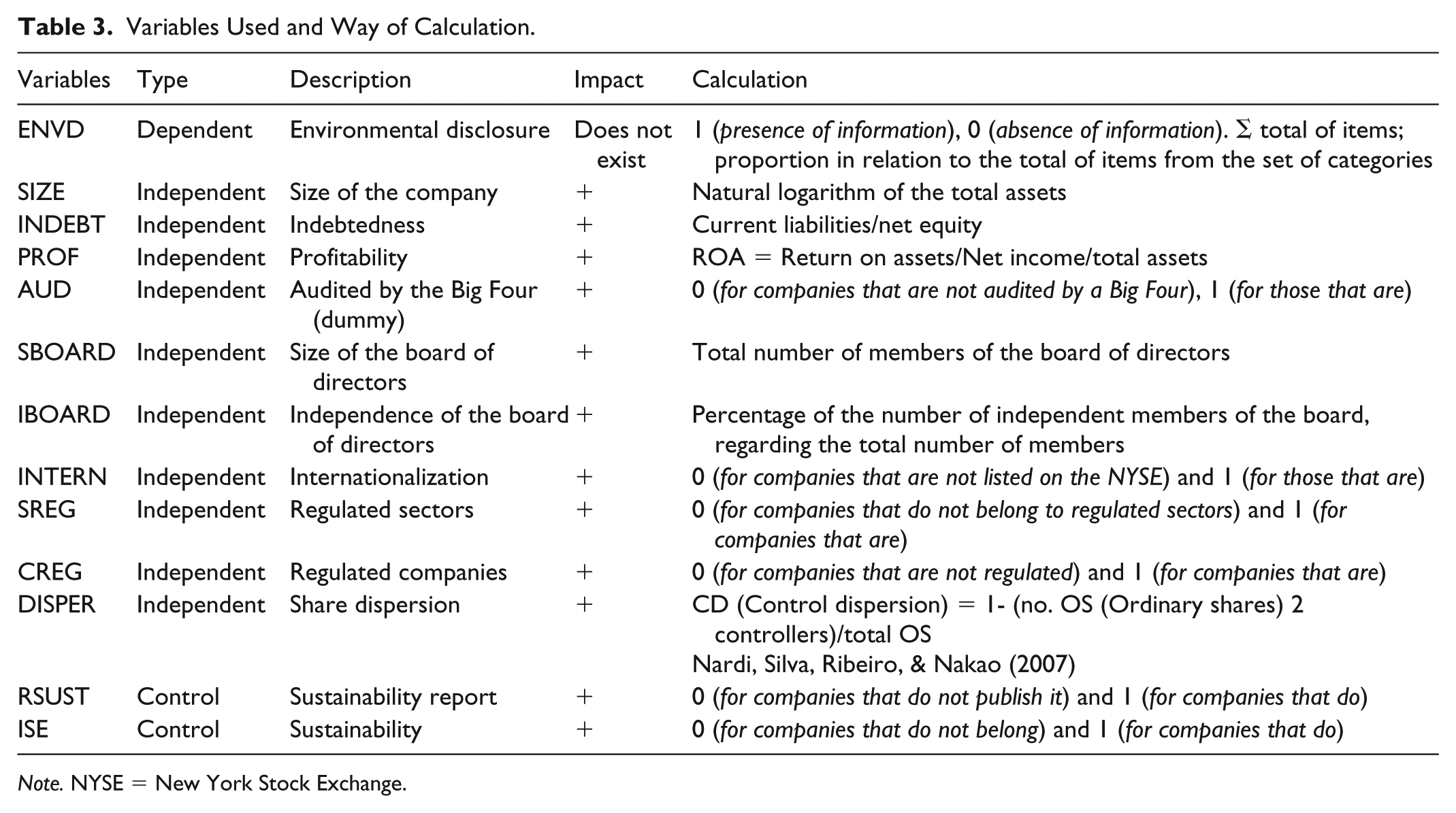

For each highlighted item in the reviewed documents, we assigned the value 1 for the presence of information (disclosure), and the value 0 for the absence of information (nondisclosure). We performed the sum and its equivalence in proportion to the total of items from the set of information for each company. Table 3 presents the variables used and their way of calculation.

Variables Used and Way of Calculation.

Note. NYSE = New York Stock Exchange.

In the databases Comdinheiro (https://www.comdinheiro.com.br/home2/) and Thompson Reuters, we collected information on the variables: company size (SIZE), INDEBT, and PROF. information on the variables audit (AUD), internationalization (INTERN), SREGs, and ISE were collected on the websites of the NYSE, Portal Brasil, and BM&FBOVESPA. For the variables CREGs, RSUSTs, size of the board of directors (SBOARD), independence of the board of directors (IBOARD), and share dispersion (DISPER), data were collected on the websites of the studied companies.

The unbalanced panel was developed, covering the data from the time series and cross section data for 13 variables, in the 10-year period, 2005 to 2015. The option for the use of this type of panel occurred due to the existence of companies with missing data in the period. Data were analyzed by means of econometric regression estimation method with panel data. Equation 1 presents the calculation proposed in this study.

where the dependent variable of the model is the environmental information evidence (environmental disclosure [ENVD]); the independent variables are SIZE, INDEBT, PROF, AUD, SBOARD, IBOARD, INTERN, SREGs, CREGs, stock Dispersion (DISPER); and the control variables are the RSUSTs and the ISE.

The estimation of the regression with panel data was based on three models, ordinary least squares (OLS), fixed effects, and random effects. To identify the most appropriate model, the tests of Chow and Hausman were performed. We also met the assumptions of estimation of regression with panel data as observation of the measures of variance inflation factor (VIF), the heteroscedasticity, and autocorrelation.

Results of Descriptive Statistics and of the Econometric Model

Analyzing Table 4, it can be observed that some variables, such as SIZE (2.1487), INDEBT (55.2194), and PROF (816.0753), present a greater dispersion of the data around the mean, unlike variables INDEBT (0.2171), SREG (0.4993), and CREG (0.5001), which show less data dispersion. It can be seen that SIZE (21.2504) and SBOARD (7.0040) are the variables with the highest mean, and PROF (–32.6868) and INTERN (0.0984), with the lowest mean. A certain difference between the mean and the median of the variables is also observed, indicating that the distribution of the data is asymmetric.

Descriptive Statistics of Variables.

Table 5 shows the Pearson correlation between the search variables, as well as their level of significance.

Pearson Correlation Matrix.

Source. Data research. *Significant at 5%.

From this, we can verify that the ENVD dependent variable has a positive correlation with all variables, at a significance level of 1%, except for INDEBT and DISPER, whose correlations were negative. It is also observed that the explanatory variables most correlated with ENDV are RSUST (0.6940) and SIZE (0.6101); those with weak correlation are PROF (0.0483) and IBOARD (0.2068).

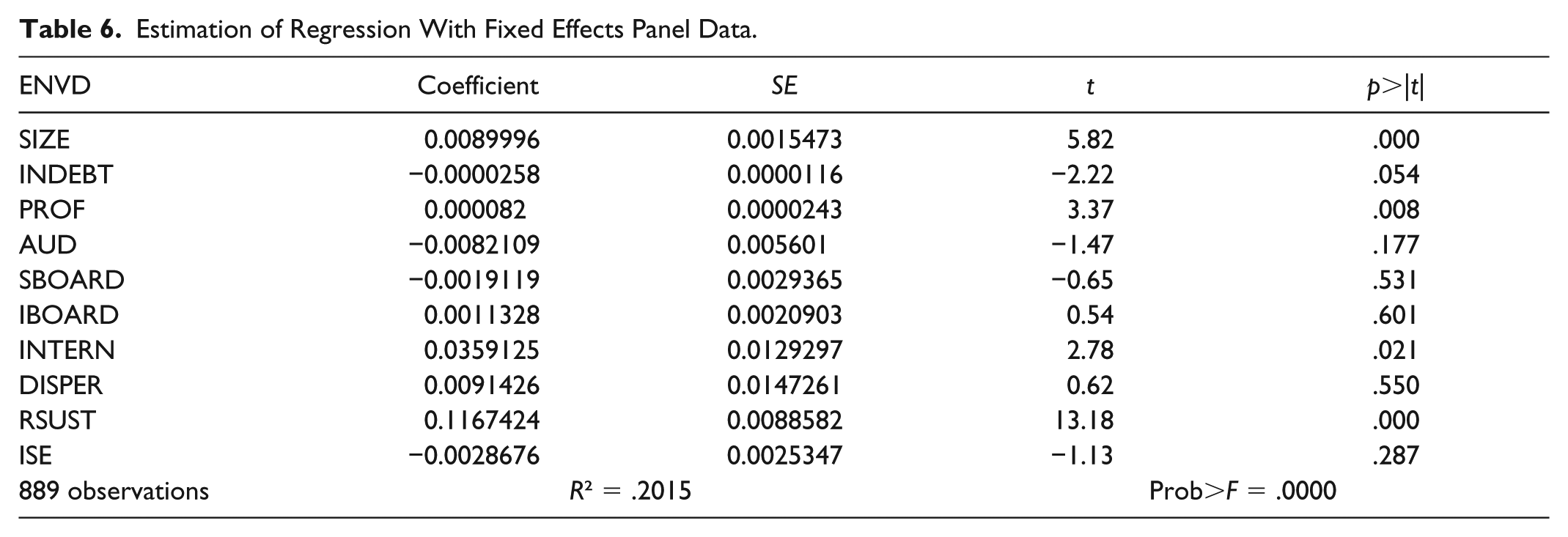

Regression with panel data was estimated using the OLS model. Results indicated the presence of multicollinearity with VIF values above 10 to two variables CREG (VIF = 38.82) and SREG (VIF = 38.40). Such value for the test characterizes the nature of the two variables of being very close, one covering CREGs and the other, SREGs. We excluded from the analysis the variable CREG, being the multicollinearity corrected after the new estimation. The estimation of the tests of Chow and Hausman confirmed that the fixed effects model is the most appropriate. Therefore, there was no need to perform the Breusch–Pagan test for pooling and random estimators.

The Wald test indicated that the fixed effects model is heteroscedastic. The Wooldridge test confirmed the presence of autocorrelation among residuals of the regression with panel data. As a corrective measure for heteroscedasticity and autocorrelation, the Driscoll and Kraay (1998) correction was performed, which includes the two estimators. Table 6 presents the results of the estimation of the regression with fixed effects panel data.

Estimation of Regression With Fixed Effects Panel Data.

The probability value indicated that the regression is significant, indicating, by the value of R2, that 20.15% of the variation in ENVD of potentially polluting companies are explained by the independent variables. The results indicate that ENVD is explained by the variables SIZE, PROF, and RSUST (99% of significance); INTERN (95% of significance); and INDEBT (10% of significance). We did not find significant evidence that ENVD is explained by the variables AUD, SBOARD, IBOARD, DISPER, and ISE. The SREGs variable was omitted from the model for being a dummy variable fixed along the panel. Significant results for the variable SIZE (p value = .000) confirm the first hypothesis (H1: Larger companies disclose more environmental information than smaller companies). This suggests that the larger the company, the more it will be prone to disclose environmental information. A possible explanation is that such companies are subject to observation of society because they are in evidence (Fernandes, 2013; Liu & Anbumozhi, 2009).

The significance for the INDEBT variable (p value = .054) offers support to reject the second research hypothesis as its impact is negative (H2: Companies with bigger INDEBT disclose more environmental information than those that present less INDEBT). The implications of this result suggest that indebted companies tend to disclose less environmental information. A possible explanation is that the disclosure of information implies costs for the companies, whose benefit might not be optimized, if investors do not realize that this information adds value (Silva, Slewinski, Sanches, & Moraes, 2015). Cormier and Magnan (2003) further argue that reporting strategy depends on the financial condition of firms, so that only those that are financially sound may be able to generate costs to disclose information related to their performance. The result is consistent with Cormier and Magnan (2003), Brammer and Pavelin (2006), and Fernandes (2013) and contrary to Huang and Kung (2010).

The variable PROF is presented with an explanatory factor to the disclosure of information (p value = .008), confirming the third research hypothesis (H3: More profitable companies disclose more environmental information than less profitable companies). As companies present positive results, it is expected that they disclose more information as managers can attract a larger number of investors through it, as mentioned by Zhang, Guo, Li, & Wang (2009).

The variable AUD showed no statistical significance (p value = .177), rejecting the fourth research hypothesis (H4: Companies audited by one of the Big Four disclose more environmental information than companies audited by other audit firms). The company being audited by the Big Four does not influence the disclosure of environmental information, suggesting that companies may be audited by a Big Four firm, despite not having environmental practices and, consequently, not disclosing information of this nature. These results corroborate with Lu and Abeysekera (2014) and Cheng, Wang, Keung, and Bai (2017).

The presence of a larger board of directors (SBOARD) does not explain greater ENVD (p value = .531), thus rejecting the fifth research hypothesis (H5: Companies with a larger board of directors disclose more environmental information than companies with a smaller board of directors). The size and composition of the council varies between countries; in Brazil, however, the number of members should vary between 5 and 11 advisors (Halme & Huse, 1997; IBGC, 2010). Although Lenciu et al. (2012) claim that a larger board of directors is composed of experienced members, the results showed in Table 5 indicate that it does not explain the greater disclosure of environmental information in potentially polluting companies. This result is consistent with Halme and Huse (1997).

The presence of a board of directors composed of a large number of IBOARDs showed no statistical significance (p value = .601) with ENVD, thus rejecting the sixth research hypothesis (H6: Companies that possess a board of directors composed of more independent members disclose more environmental information than those with less independent members). The presence of independent members seeks to neutralize potential conflicts of interests, as well as ensure transparency of financial and environmental information (Lenciu et al., 2012).

The presence of INTERN (p value = .021) is an explanatory factor for ENVD, confirming the seventh hypothesis (H7: Companies with shares traded on the NYSE disclose more environmental information than those listed just in their country of origin). This result is consistent with Murcia, Rover, Lima, Fávero, and Lima (2008) as the requirements concerning the disclosure of information are larger in the American market, considering that Form 20-F has a lot of information not required on the national scenario.

The presence of DISPER showed no significance (p value = .550) for a greater ENVD, thus rejecting the ninth research hypothesis (H9: Companies that present greater dispersion of their shares disclose more environmental information than those that are more concentrated). Although Lu and Abeysekera (2014) argue that a dispersed ownership and control structure motivates managers to disclose more information, in this study with potentially polluting companies this was not confirmed. Zolini (2008) argues that the concentration of property, on the part of large shareholders, will motivate them to take an active position, with an interest in the company’s performance. Therefore, such shareholders can find themselves obliged to adopt environmentally sustainable attitudes due to pressure from various stakeholders and, to achieve satisfactory results, the organizations begin to incorporate a good environmental performance in their strategy.

Publishing RSUSTs (p value = .000) is an explanatory factor for greater ENVD, confirming the 10th hypothesis (H10: Companies that publish RSUSTs disclose more environmental information than those who do not publish it). This result is consistent with Moraes, Zevericoski, Ferrarezi, Gehlen, and Resis (2017) who stated that in the publication of RSUSTs, companies communicate actions taken and results achieved both by the economic-financial approach, as in their attitudes concerning social and environmental issues.

The ISE showed no statistical significance (p value = 0.287), thus rejecting the 11th research hypothesis (H11: Companies belonging to the ISE disclose more environmental information than companies that do not belong in it). Although we expected that the fact the companies belonged to the ISE exercised positive influence on the practice of disclosure of environmental information, due to their commitment to sustainability, this relationship was not confirmed in potentially polluting companies. Table 7 presents the synthesis of the obtained results.

Synthesis of the Obtained Results.

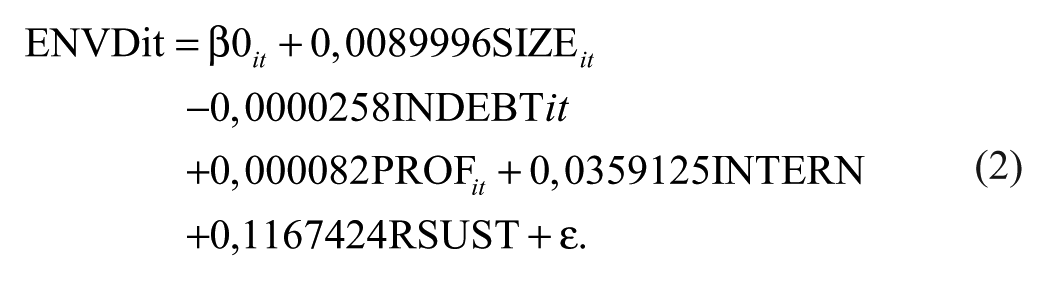

The information presented in Table 7 indicates that the hypotheses H1, H3, H7, and H10 were confirmed and their positive explanatory effect was consistent with the expected, from evidence from the literature. Although the variable INDEBT (H2) has presented statistical significance, the negative sign obtained was contrary to the expected, thus rejecting the hypothesis H2. The other hypotheses (H4, H5, H6, H9, and H11) did not present statistical significance, thus being rejected. It should be stressed that the variable-CREGs were excluded from the model for causing multicollinearity problems, and the variable-SREG was omitted from the model as it is a dummy variable, which remained constant throughout the period. Equation 2 represents the explanatory factors of environmental disclosure in potentially polluting companies.

Explanatory factors of environmental disclosure that present the greatest weight are the publication of the RSUST (β = .11674) and INTERN (β = .0359125). For each variation of one unit of the variable size (SIZE), the environmental disclosure increases 0.0089996. Although the weights of INDEBT and PROF are too small, the variation of one unit of these variables decreased environmental disclosure to 0.0000258 and increased to 0.000082, respectively. For variations of one unit on INTERN, disclosure increased 0.035125, while for the publication of the RSUST environmental disclosure increases to 0.1167424.

Final Considerations

This research aimed at identifying explanatory factors of the environmental disclosure of potentially polluting Brazilian companies listed on the BM&FBOVESPA, from 2005 to 2015. The regression with fixed effects panel data was estimated for a sample of 182 companies. Results indicate that companies with larger size, more PROF, and whose shares have traded on the NYSE and which publish RSUSTs, disclose more environmental information. These results converge with the existing literature on the subject, demonstrating that these factors explain the practice of environmental disclosure. INDEBT presents a negative relationship with the environmental disclosure. This result is controversial with the literature and can be justified by the environmental information disclosure costs being high.

On the contrary, organizations audited by an auditing firm belonging to the group of the Big Four, those with a larger board of directors, those with a large number of independent members on the board of directors, and those that presented DISPER did not disclose more environmental information. Companies linked to the ISE also do not disclose more information than those that do not belong to the index. In other words, these factors are not explanatory of the disclosure of environmental information of potentially polluting companies listed on the BM&FBOVESPA, as we expected. This study concludes that the explanatory factors of environmental disclosure of potentially polluting Brazilian companies listed on the BM&FBOVESPA, in the period from 2005 to 2015 are, with a higher weight, the publication of the RSUST and INTERN through stock trading on the NYSE. Other explanatory factors for environmental disclosure, but with less weight, are SIZE, INDEBT, and PROF.

This study is relevant in three aspects. First, it presents information on the relevance of environmental disclosure to companies that perform potentially polluting activities to provide support for different agents linked to these companies they may have access. Second, it presents as theoretical contribution the explanatory variables for environmental disclosure of potentially polluting companies, an analysis not yet carried out in the literature. Third, a practical contribution is to present information to interested users that potentially polluting companies, larger in size, internationalized, and with more PROF disclose their environmental information.

Future studies could compare the environmental disclosure of Brazilian companies with that of other countries, both those that have an environmental regulatory framework, as well as those which do not, with the addition of other proxies and other theoretical approaches. Future studies could also compare the environmental disclosure of potentially polluting companies with companies that are not potentially polluting. The limitation of this research is linked to the employment of companies linked to the Stock Exchange BM&FBOVESPA, thus not being possible to perform generalizations to other Brazilian companies that are not linked to the financial market.

Footnotes

Acknowledgements

We are also grateful to our anonymous reviewers for the tips, contributions, and recommendations.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.