Abstract

With the accelerated opening of China’s capital account, China’s banking sector is exposed to the impacts of cross-border capital flows. This article explores the impact of cross-border capital flows on banks’ risk-taking in China. Employing bank-level data of 50 Chinese commercial banks from 2005 to 2018 and a sys-GMM (system generalized method of moments) estimation method, we show that cross-border capital flows are positively associated with the risk-taking of Chinese commercial banks. Moreover, banks that are larger, more capital adequate, and more profitable are more sensitive to the degree of capital account openness toward risk-taking, and the capital account openness has the greatest influence on the profitability-driven bank risk-taking. Nevertheless, such positive effects of capital account openness on bank risk-taking may be weakened under bad macro-environment, indicated by low economic growth, poor legitimate law enforcement, and unstable political condition.

Keywords

Introduction

The outbreak of the subprime mortgage crisis in 2008 has drawn researchers’ attention to the potential risks underneath the decision-making of the banking sector, and academic studies of bank risk-taking have emerged ever since (Adrian & Boyarchenko, 2012; Adrian & Shin, 2014; Agur, 2014; Altunbas et al., 2010; Angeloni et al., 2015; Brissimis & Delis, 2010; Brunnermeier & Sannikov, 2014; Buch et al., 2014; Dell’Ariccia et al., 2014, 2017; He & Krishnamurthy, 2013; Hilscher & Raviv, 2014; Ioannidou et al., 2009; Laeven et al., 2010; Maddalonia & Peydro, 2013; Paligorova & Santos, 2017). Prior literature put forward traditional bank risk-taking channel theory that relates monetary policy to bank risk-taking, which proposes that the adjustment of monetary policy affects the risk attitude of commercial banks and further affects the risk of the banks’ portfolios, their market prices, and financing costs, eventually shaping the commercial banks’ decision-making in many aspects (Borio & Zhu, 2012; Dell’Ariccia et al., 2014; Jiménez et al., 2014). However, traditional bank risk-taking channel theory is confined under close economy assumptions, which does not take account of cross-border capital flows in an open economy (Borio et al., 2014). Therefore, many researchers further examine the novel bank risk-taking channels from the perspective of an open economy. The most prominent is the research of Bruno and Shin (2015), which is based on Miranda-Agrippino and Rey’s (2015) study of the “global financial cycle” and empirically reveals that currency appreciation pushes up the leverage of the banking sector and increases financial risks. They also put forward the theory of “international risk-taking channels.” In their view, the “international risk-taking channel” is an extension of the traditional closed risk-taking channel, indicating that the cross-border capital flows affect the risk attitude of a country’s financial intermediary and thereby change its risk-taking decisions and financing activities and form the risk-taking of the whole financial system. Furthermore, Plantin and Shin (2018) find that cross-border capital inflows have depressed the sovereign debt yields of emerging economies, which leads to currency appreciation and increased risk-loving in credit activities. Della Corte et al. (2018) find that rising credit default swap (CDS) spreads lead to more cross-border capital outflows. In this regard, the risk attitude in credit activities tends to be more conservative, and banks are more exposed to systemic risks. Baskaya et al. (2017) empirically show capital flows and the international credit channel in Turkey, whereas Dinger and te Kaat (2020) look at international sample to present empirical evidence that capital inflows induce more bank risk-taking and that agency issues reinforce the link, as is indicated in the theoretical model in Martinez-Miera and Repullo (2017). However, the existing studies do not examine the Chinese banks’ risk-taking on account of the cross-border capital flows; therefore, we wish to contribute to the literature and fill in this gap.

In recent years, the process of opening up China’s capital account has continued to accelerate. However, at the same time, the nonperforming loan balance of commercial banks has continued to rise, and the decline in the nonperforming loan rate also reversed. There is no doubt that the deterioration of the banks’ balance sheet is definitely related to factors such as the surge in channel business and off-balance-sheet business, which have caused banks to enter the leveraged cycle. However, as the opening of the capital account has increased, China has faced a growing cross-border capital flow impact; therefore, is the change in bank risk-taking behavior also an important factor? In other words, with the acceleration of the process of opening the capital account, is there an “international risk-taking channel effect” of cross-border capital flows into China’s banking system? What makes Chinese setting so special is that with the gradual opening of China’s capital account, we can examine the degree of capital account openness as a measure of cross-border capital flows, instead of the absolute capital inflows and outflows. The latter is more dominantly driven by macro-economic conditions, indicating more serious endogeneity issues.

This article intends to systematically analyze the transmission pathways of cross-border capital flows affecting bank risk exposure, by referring to existing research results at home and abroad, and aims to draw on the bank risk exposure model of Delis and Kouretas (2011) to illustrate the relationship between capital account openness and bank risk exposure. Based on this benchmark model, the system GMM (generalized method of moments) estimation method is used to empirically test the sample data of 50 commercial banks in China from 2005 to 2018, to verify whether there is an “international risk-taking channel effect” in our banking system.

Channels of Risk-Taking

Based on the way that cross-border capital enters a country’s financial system, and the impact on and mechanism of the banking system, this article summarizes the four transmission paths of cross-border capital flows affecting bank risk commitments, as follows: the balance sheet path, the asset price path, the spread path, and the foreign bank path.

Balance Sheet Path

The inflow of cross-border capital, whether as direct investment or indirect investment, will affect the foreign currency assets and liabilities of a country’s commercial bank, and then affect the bank’s balance sheet. Specifically, when cross-border capital flows into a country in the form of foreign direct investment (FDI), the increase in FDI not only directly increases the number of foreign currency deposits of banks in that country, but the local currency supporting funds it brings will also boost the country’s currency supply through indirect channels, causing volume expansion. When cross-border capital flows into a country in the form of bank loans, if the country implements a compulsory foreign exchange settlement and sales system, commercial banks must sell this portion of foreign exchange to the central bank. This will not only increase the central bank’s foreign exchange reserves; it will also increase the commercial bank’s domestic currency loanable funds. Thus, if the country implements a nonexchange currency system, although the central bank will not buy foreign currency from the commercial bank, the commercial bank’s domestic currency funds have not reduced. The increase in foreign currency funds will also lead to the expansion of foreign currency credit. When cross-border capital flows into a country in the form of securities investment, the conversion of foreign currency assets by securities investors into the domestic currency will cause the bank’s domestic currency to increase, or the foreign currency is directly invested in the country, if the seller of the securities deposits the foreign currency directly. Capital entering a commercial bank will increase the bank’s supply of foreign currency deposits. If the securities seller deposits the foreign currency received into the commercial bank, it will eventually cause the bank’s domestic currency to increase. Both methods will eventually lead to the expansion of bank balance sheets and increase of loanable funds, which will lead to the growth of bank credit.

Asset Price Path

Driven by the influence of profitability and the “animal spirit,” a large amount of short-term irrational speculative capital inflows will have an impact on a country’s asset prices. Specifically, after the frenetic short-term capital flows into the host country, where the effects on technology, labor, infrastructure, and other related supporting facilities are not affected in the long term, foreign capital that cannot be absorbed by the real sector will flow into high-risk real estate and stocks, and so on. In the high-yield industry, with the deepening trend of institutionalization of cross-border capital flows, speculative strategies can strengthen the role of “leader” in the “herd effect”; this triggers a follow-up situation, further increases asset prices, and easily creates asset price bubbles. On one hand, under the so-called “ratcheting effect,” the excessive optimism toward asset prices by households and the business sector will increase their risk appetite, which will increase demand for credit. On the other hand, rising asset prices will increase the net value of borrowers; as a result, the adverse selection effect is reduced, the external financing premium is reduced, and lenders’ loans to high-risk borrowers increase.

Spread Path

For open economies, after the capital account is opened, in the face of world interest rates, it is not possible to autonomously adjust the domestic interest rate level; this is because as long as there is a difference between the national interest rate and the world interest rate level, interest rate spreads will narrow until the country’s interest rate is the same as the world’s. Therefore, when a country is facing cross-border capital inflows, on one hand, the domestic currency appreciation expectation will eventually lead to a reduction in the country’s actual interest. Different sensitivities can cause changes in banks’ net assets. Generally, when the interest rate of a country decreases, the sensitivity of bank assets to the decline of interest rates is greater than the sensitivity of its liabilities. Therefore, the increase in the value of bank assets will be greater than the increase in the value of bank liabilities. Finally, the increase of the net asset value of the bank encourages the bank to increase its leverage ratio. On the other hand, due to the existence of financial friction, cross-border capital inflows caused by appreciation expectations have pushed up the final lending rate of the real sector, thereby increasing the interest rate spread of the banking sector, and increasing leverage.

Path of Foreign Banks

When a country relaxes control over foreign banks’ entry and business scope, the large number of foreign banks entering mainly affects the host country’s risk-taking in two aspects, as follows. On one hand, foreign banks rely on their advanced technology and mature business management models. As well as strong financial innovation ability, this has formed a competitive situation with domestic banks in terms of business, customers, and talents; this erodes the domestic banks’ relative competitive advantages and leads to the mass loss of high-quality customers for domestic banks, which are left with only high-risk customers. This produces a “defatting effect.” The loss of high-quality customers has caused domestic banks to lower the entry barriers and credit standards for credit customers; hence, the credit quality has declined, and the nonperforming loan ratio has increased, thereby increasing the risk exposure of domestic banks. On the other hand, as a country’s restrictions on foreign bank access are reduced, the value of domestic banks’ franchise rights will decrease, and it is expected that the reduction in the present value of excess profits will lead to greater risk exposure and lower risk control for banks. This incentivizes shifting to high-risk credit or investment businesses, and increases the moral hazard of banks.

Model, Variables, and Data

Benchmark Model

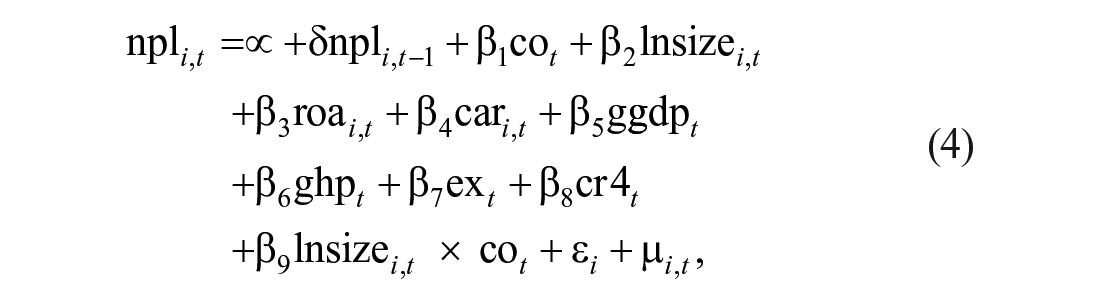

Considering that there is a “habit formation path” for bank risk-taking, this article draws on the research of Delis and Kouretas (2011) by introducing the lagging period values of bank risk-taking agent variables as explanatory variables. It then constructs a relationship that reflects the openness of the capital account and bank risk-taking benchmark model, as shown in Equation 1:

where

Variables

In the existing literature, the variables that measure a bank’s risk exposure mainly include nonperforming loan ratio, expected default rate, Z-score, and risk-weighted asset ratio. Theoretically, the expected default rate is the most effective variable to measure the bank’s risk because it is an ex-ante variable. Compared with other proxy variables, it can better reflect the bank’s willingness to take risks actively. However, because the calculation of the expected default rate is more complicated, only professional rating agencies will regularly publish these data; hence, the domestic rating system is not yet complete, and relevant data for domestic commercial banks cannot be obtained. Some scholars also use Z-score (

The measurement of capital account openness can be roughly divided into two methods: regulatory indicators and factual indicators. Regulatory indicators are a qualitative measurement method, mainly based on the restrictions that a country’s laws and regulations impose on capital account opening, which reflects the current national government’s willingness to open the capital account and policy guidelines. The factual indicator is a quantitative measurement method, which reflects the real capital flow of a country by examining the comprehensive impact of the behavior of participating entities on the market during the capital account opening process. However, both methods have certain drawbacks. For instance, the regulatory indicators are forward-looking and reflect the wishes of government leaders; on one hand, many statutory indicators cannot effectively measure the strength of capital controls, whereas on the other hand, they cannot measure the causality between system-level controls and actual cross-border capital flows. The relationship may not be so strong, so it is prone to producing errors and distortions in the judgment of effects. Factual indicators have better objectivity and real-time accuracy, but because they measure market phenomena, they will be affected by many potential factors and have great volatility, which may weaken the economic significance of capital account openness to a certain extent. In addition, factual indicators have measurement errors and endogenous problems. Therefore, to ensure objectivity and accuracy, many scholars use mixed indicators to measure the level of capital account openness. Lou and Qian (2011) find the benchmark level of a country’s capital account openness through the correlation of different indicators, and consider the accuracy of each indicator in practice and the importance of the field of application to give different weights, to construct an indicator covering a wide range of countries and applicable to multiple countries. Zhang and Shi (2015) borrowed the ideas of Lou and Qian (2011) and give equal weight to the regulations and factual indicators, as a weighted average to obtain a mixed indicator.

This article mainly draws on China’s capital account openness indicators constructed by Zhang and Shi (2015). Among them, the statutory measures are mainly based on the Annual Report of Exchange Arrangements and Exchange Restrictions issued by the International Monetary Fund (IMF) every year. A total of 52 subprojects in 13 major categories under the capital account were obtained by adding four grades of assignments; in fact, the method of measuring the size of capital flows in Driscoll and Kraay (1998) was used as a reference. To measure the specific gravity, the results of the calculation are shown in Figure 1.

China’s capital account openness from 2005 to 2018.

As can be seen in Figure 1, since 2005, China’s capital account openness has gradually increased, which is in line with China’s policies to promote capital account openness. In particular, it can be seen from the statutory level that China’s control of the capital account is being relaxed year by year, and the capital account openness has continued to rise from 43.92% in 2005 to 66.39% in 2018. The fact that the degree of the capital account openness index fluctuates to some extent is mainly due to the impact of the global financial crisis. Before 2007, the degree of capital account openness increased rapidly. During the financial crisis, due to the impact of the unstable global financial environment, the sudden decline in cross-border capital flows led to a more serious decline in the degree of capital account openness at the de facto level, but it has since quickly resumed its growth trend.

In terms of controlling variables, this article mainly selects the logarithm of bank size (

Based on the above analysis, the benchmark model can be embodied in the following form:

where i indexes banks, and t years;

Data

This article mainly selects the unbalanced panel data of 50 commercial banks in China from 2005 to 2018 as the research sample, including five state-owned commercial banks, 12 shareholding commercial banks, nine rural commercial banks, and 24 municipal commercial banks. The bank-level and macro-level data are mainly obtained from the Bankscope, CSMAR (China Stock Market & Accounting Research), the official website of State Administration of Foreign Exchange (SAFE) and the International Monetary Fund (IMF), and the annual reports of the commercial banks. The descriptive statistics of the main variables are shown in Table 1.

Descriptive Statistics of the Main Variables.

Note. This table presents number of observations means, standard deviations, minimums, and maximums for variables. The sample consists of 50 Chinese commercial banks from 2005 to 2018, including five state-owned commercial banks, 12 shareholding commercial banks, nine rural commercial banks and 24 municipal commercial banks. See the appendix for variable definitions.

From the descriptive statistical results of the variables shown in Table 1, it can be seen that the bank risk commitment value measured by the risk-weighted asset ratio (

We can obtain a more intuitive understanding of the relationship between capital account openness and bank risk exposure, according to the descriptive statistics of the sample, that is, the average of the risk-weighted asset ratio (

Relationship between capital account opening and bank risk commitment.

In the previous period, the change in the risk-weighted asset ratio lags slightly behind the change in the capital account openness, which is also in line with economic theory and realistic results. At the same time, at the 95% confidence interval, in most years the risk-weighted asset ratio increased with the increase in the degree of capital account openness, and the two showed a positive correlation. Therefore, we can put forward an empirical hypothesis: Bank risk exposure is positively related to the openness of the capital account; that is, the higher the openness of the capital account, the greater the bank’s risk exposure. In other words, the “international risk-taking channel effect” exists in China’s commercial banking system.

Results

To effectively solve the possible endogenous problems of the model and avoid effects of heteroscedasticity and the autocorrelation of random error terms, a system GMM estimation method is selected for the empirical analysis. According to the economic meaning of the variables set in this article, GDP growth rate (

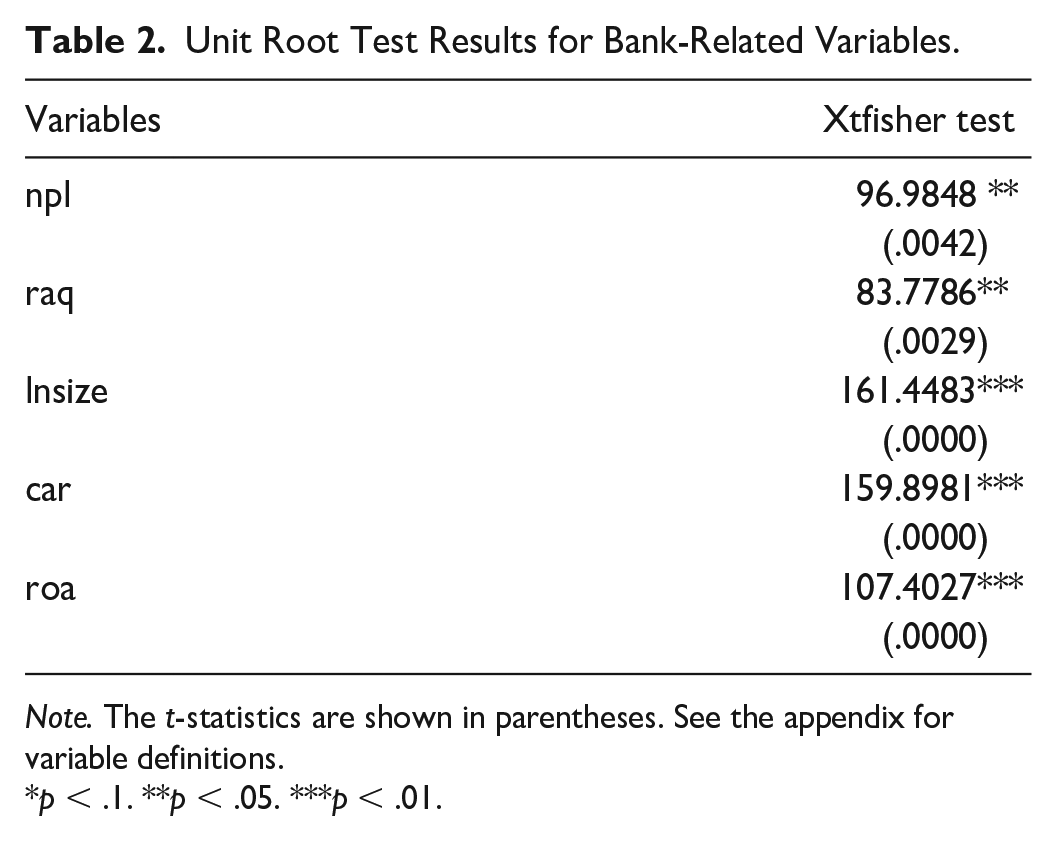

Unit Root Test of Panel Data

To ensure the validity of the estimation results and avoid “pseudo-regression,” before formal regression of the model, the panel Fisher unit root test method is used to test the unit root of each variable. The values are the same for GDP growth rate (

Unit Root Test Results for Bank-Related Variables.

Note. The t-statistics are shown in parentheses. See the appendix for variable definitions.

p < .1. **p < .05. ***p < .01.

Parameter Estimation Results and Analysis

Table 3 shows the results of estimating the benchmark model by using the risk-weighted assets ratio (

Sys-GMM Estimation Results of the Benchmark Model of Capital Account Opening Affecting Bank Risk Exposure.

Note. The t-statistics are shown in parentheses. See the appendix for variable definitions. Sys-GMM = system generalized method of moments.

p < .1. **p < .05. ***p < .01.

From the estimation results in Table 3, it can be seen that the estimated coefficients of most variables are significant at a significance level of 5%. Among them, the lag period risk-taking variable (

The significantly positive coefficient of

As for the capital account openness (co), with every 1 unit increase in the capital account openness (co), the bank’s weighted risk asset ratio (

In addition, it can be seen that when the nonperforming loan ratio (

A detailed analysis of the estimated results of the control variables follows.

First, the estimated coefficient of asset size (

Second, the estimated coefficient of profitability (

Third, the estimated coefficient of capital adequacy (

Fourth, the real estate price index growth rate (

Fifth, the estimated coefficient of the nominal exchange rate (

Heterogeneity of Bank Risk-Taking With the Opening of the Capital Account

Based on the above empirical models, the interaction terms of bank size (

where i indexes banks, and t years;

When the interactive terms of bank micro-variables and capital account openness are added to the model, because the interactive terms contain the current bank-level control variables, the original variables and their interactive terms are also present in the extended model; this makes it easy to produce multiple collinearity, which in turn affects the sign and significance of the estimated coefficients of capital account openness (

Variable Correlation Coefficient Matrix When Constructing Interaction Terms According to Original Variables.

Note. See the appendix for variable definitions.

Variable Correlation Coefficient Matrix When Constructing Interaction Terms According to Centralized Variables.

Because the interaction term contains the endogenous variable of bank size (

Heterogeneous sys-GMM Estimation Results of Banks’ Risk-Taking Behavior Under the Opening of the Capital Account.

Note. See the appendix for variable definitions. The t-statistics are shown in parentheses. Sys-GMM = system Gaussian Mixture Model.

p < .1. **p < .05. ***p < .01.

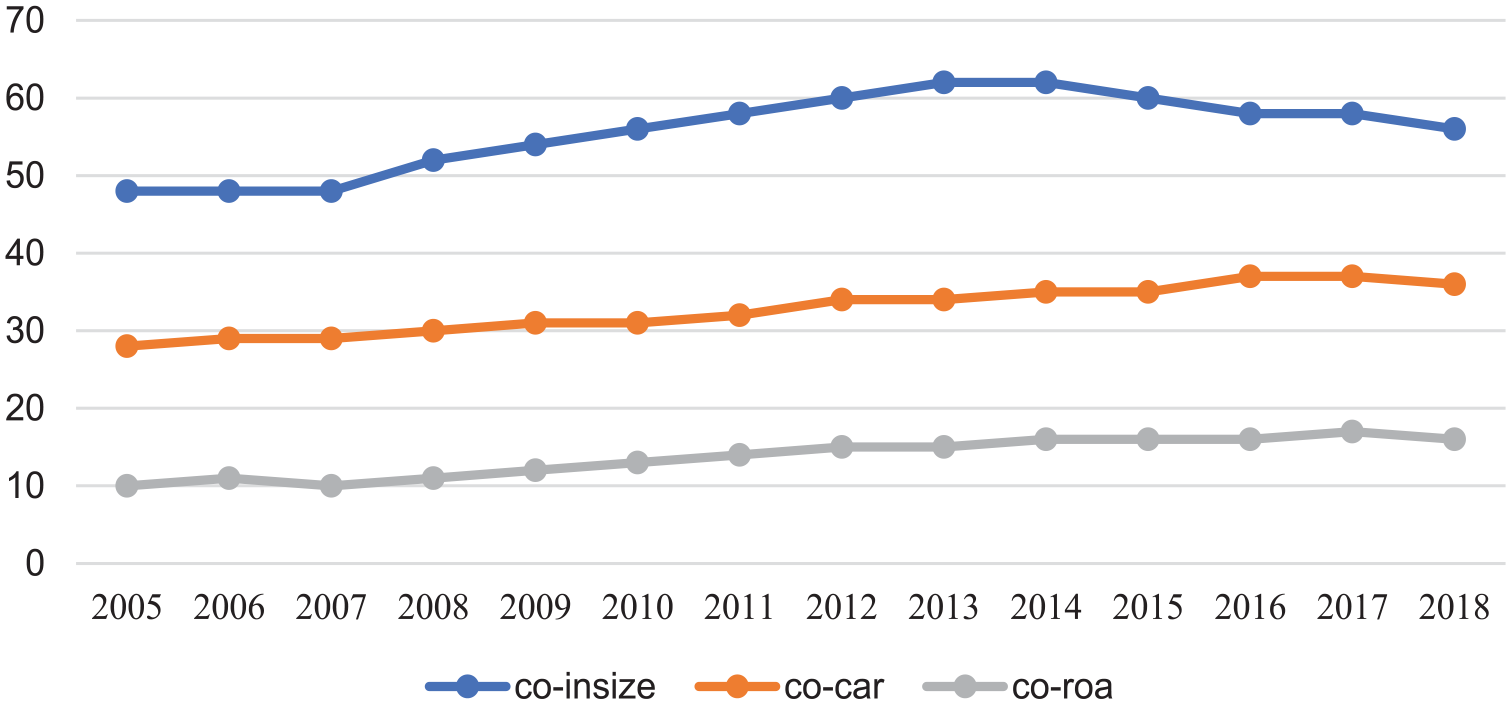

Wooldridge (2010) proposes that when the model contains interaction terms, the interpretation of the parameters of original variables alone is meaningless; they should be analyzed in combination with the parameters of the interaction terms. For example, the coefficient β2 of the bank size (lnsize) in equation (3) cannot fully reflect the extent of bank risk exposure. To examine how the characteristics of the bank’s size affect the degree of impact that the opening of the capital account has on the bank’s risk exposure, we can analyze the partial effect of the bank’s asset size on the bank’s international risk and bring the co-value in different quantiles into the equation. In the estimation result of equation 2.2, we study the partial effect of bank size on international risk under the condition of capital account opening. According to the estimated coefficients in Table 6, all banks are plotted under the quantiles of different capital account openness (Note: percentiles are selected from 1%, 5%, 10%, 25%, 50%, 75%, 90%, 95%, 99%); the partial effect of scale on banks’ international risk exposure and the analysis of partial effect on capital adequacy ratio and profitability are the same, as shown in Figure 3.

Partial effect of international risk-taking under the opening of the capital account.

It can be seen from Figure 3 that under the condition of capital account opening, the partial effects of bank asset size, profitability, and capital adequacy ratios on international risk exposure are all greater than 0. Furthermore, for the estimated coefficients of the main variables of the model after the interaction term is added, the sign and salience remain essentially the same; that is, the larger the bank, the stronger the profitability, the higher the capital adequacy ratio, and the greater the bank’s risk exposure; this is consistent with the conclusion drawn by the benchmark model. In addition, the coefficients of the interaction terms are also estimated to be greater than 0, indicating that with the increase in the degree of capital account openness, the impact of bank asset size, profitability, and capital adequacy ratio on its risk exposure is strengthened. It can also be seen from the size of the interaction term coefficient that different banks’ micro-characteristics respond differently to the opening of the capital account. From the partial effect curve in Figure 3, it can also be seen that the partial effect of profitability (

Conclusion

This article distinctively examines how the cross-border capital flows affecting bank risk-taking in China. We analyze the channels through which the cross-border capital flows affect bank risk-taking, which include the size, the capital adequacy, and the profitability. Based on a research sample of 50 Chinese representative commercial banks in 2005–2018 and the classic bank risk-taking model of Delis and Kouretas (2011), we construct a benchmark model to examine the relationship between capital account openness and bank risk-taking. The system GMM method is used for estimation to address the endogeneity issue. The empirical results show that the opening of the capital account is positively associated with the risk-taking of Chinese commercial banks. Therefore, the “international risk-taking channel effect” exists in China’s commercial banking system. and the more open the capital account, the greater the risk-taking of the banks.

In addition, this article also finds that the impacts from capital account opening to bank risk-taking are contingent on heterogeneous factors, such as bank size, capital adequacy, and profitability. More precisely, the higher the openness of the capital account, the stronger the role of the bank’s asset size, capital adequacy ratio, and profitability to promote bank risk-taking; the capital account openness has the greatest influence on the effect of profitability. Conversely, the partial effect on bank risk exposure most affected by the opening of the capital account is profitability. These findings may be explained by that, on one hand, cross-border capital inflows have increased the liquidity of China’s banking system, which renders Chinese banks more profitability and stronger risk-taking resilience to be more risk-loving and to invest more in high-risk assets; on the other hand, with foreign banks’ entry into China’s market, the market competition is more fierce. Chinese commercial banks are forced to pursue risker business model to attain profits, indicating moral hazard and agency problems in banks’ risk-taking, as is proposed by the theoretical model in Martinez-Miera and Repullo (2017) and empirically proved by Dinger and te Kaat (2020).

The main contribution of this article is that we distinctively look at the Chinese banks’ risk-taking on account of the cross-border capital flows. What makes Chinese setting so special is that with the gradual opening of China’s capital account, we can examine the degree of capital account openness as measure of cross-border capital flows, instead of the absolute capital inflows and outflows. The latter is more dominantly driven by macro-economic conditions, indicating more serious endogeneity issues.

Based on the above analysis, we believe that to reduce the adverse impact of the opening of the capital account on the risk exposure of banks, financial supervision should be strengthened, the financial supervision system should be improved, and the supervision methods, supervision mechanisms, supervision regulations, and market restriction rules of the banking system should be strengthened. Effectiveness and timeliness have fundamentally caused banks to attach importance to the loan review process; this limits banks’ overinvestment behavior after the capital account is opened, and guides loan investment in a directional manner, and direct lending in a direction that reduces the likelihood that cross-border capital inflows will cause banks to take excessive risks. At the same time, because banks with different micro-characteristics have different responses to the opening of the capital account, it is necessary to carry out dynamic and differentiated prudent management for banks with different micro-characteristics.

Therefore, the policy authorities should further strengthen the monitoring and forecasting of cross-border capital flows under other investment projects in the future supervision of bank risk-taking, focusing on the prevention of other investment projects under the cross-border capital movements on the stability of the bank caused serious impact. In addition, due to the limited sample data, this article only studies the effect of cross-border capital flows on the soundness of 50 Chinese banks, and the impact of extreme volatility of cross-border capital flows on the bank risk-taking and bank crises. This article further studies the impact of extreme volatility of cross-border capital flows on the bank risk-taking by using the overthreshold model or Probit model.

Footnotes

Appendix

Variable Definitions

| Category | Name | Symbol | Description | Source |

|---|---|---|---|---|

| Dependent variable | Risk-weighted asset ratio | raq | Commercial banks’ ratio of risk-weighted assets to total assets | Bankscope; Author’s calculation |

| NPL ratio | npl | Proportion of nonperforming loans in commercial banks in total loan balance | Bankscope; Author’s calculation |

|

| Independent variables | Capital account openness | co | (Status of capital account openness + facts of capital account openness) / 2 | SAFE; IMF; Author’s calculation |

| Bank-level control variables | Bank size | lnsize | Logarithm of total assets of commercial banks at the end of the year | Bankscope; Annual Reports; Author’s calculation |

| Profitability | roa | Measured by return on total assets | Bankscope; Annual Reports; Author’s calculation |

|

| Capital adequacy ratio | car | (Capital-Capital Deduction) / (Risk-Weighted Assets + 12.5 times Market Risk Capital) | Bankscope; Annual Reports; Author’s calculation |

|

| Macro-level control variables | Economic development | ggdp | Year-on-year GDP growth | CSMAR |

| Asset price | ghp | China’s 70 large and medium-sized cities | CSMAR | |

| Exchange rate | ex | The average exchange rate of RMB to USD | CSMAR | |

| Banking market structure | cr4 | The total assets of the top four banks in the total assets of the banking industry | CSMAR | |

| Figure 1–3 variables | De facto capital account openness | co-factor | Following the Zhang and Shi (2015) | SAFE; IMF; Author’s calculation |

| De jure capital account openness | co-jure | Following the Zhang and Shi (2015) | IMF; |

|

| Capital account openness average | avrco | The average of the capital account openness | IMF; |

|

| Risk-weighted asset ratio average | avrraq | The average value of the risk-weighted asset ratio | Bankscope; |

|

| Partial effect of size | co-lnsize | The partial effects of bank asset size on bank risk exposure from Model 4 | Author’s calculation | |

| Partial effect of roa | co-roa | The partial effects of profitability on bank risk exposure from Model 5 | Author’s calculation | |

| Partial effect of car | co-car | The partial effects of capital adequacy on bank risk exposure from Model 6 | Author’s calculation |

Note. The appendix details the names and acronyms for all the variables used in empirical analysis, the variable construction, and the data source. NPL = nonperforming loan; SAFE = State Administration of Foreign Exchange; IMF = International Monetary Fund; GDP = gross domestic product; CSMAR = China Stock Market & Accounting Research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Chongqing 2011 collaborative innovation center of the intelligent justice research project on “Internet court construction and trial research”(Grant No: ZNSF2020K05).