Abstract

The aim of this paper is to investigate the association and impact between online banking service practices on e-customer satisfaction, and e-customer loyalty. In addition, it aims to analyze mediating role of e-satisfaction to online banking service practices and e-loyalty. The research followed the E-S-QUAL model to measure the online banking service quality (OBSQL) by five dimensions: e-customer service, site of the organization, website efficiency, user-friendliness, security, and privacy. It is based on quantitative research approach with a structured questionnaire through primary data collection by stratified random sampling. Out of 475 questionnaires distributed, 384 usable questionnaires were used, and SPSS and AMOS were used to analyze. An exploratory factor analysis was used to confirm the online banking service quality dimensions and structural equation modeling was employed to estimate the parameters and structure. The result explained that the efficiency of the website and e-customer service were highly influential dimensions of online banking service practices, followed by user-friendliness, security and privacy, and the organization’s site. E-customer satisfaction significantly influences e-customer loyalty, and e-satisfaction mediates the association between online banking services and e-customer loyalty, which is a prime concern to bankers, users, and policymakers for continuous development. This research presents a model to recognize the quality of online banking services that affects electronic customer loyalty and satisfaction in developing countries of South Asia.

Keywords

Background

The fast-growing trend of information technologies in banking and other businesses has led to computerizing banking transactions and other companies (Omotayo, 2020). This information technology-based development has given rise to new ways for business organizations to communicate with their customers, which supports improving banking and financial services (Raza et al., 2020). Bank and financial institutions began the “home banking” business via a touch-tone telephone in the 1970s (Shannak, 2013), and cable television was considered an ideal tool for home banking in the 1980s (Kalakota & Whinston, 1997). In 1995, Security First National Bank (SFNB) was commenced in the USA as the first full-service of internet banking globally (Chou & Chou, 2000).

The online banking service quality increases customer satisfaction because a banking customer can access various financial operations through online banking (Firdous, 2017). Online banking is an innovative practice for banks and financial institutions. It provides several services to its customers, such as accessing their account balances, transferring funds from one account to another, paying different bills, purchasing goods and services without hard cash, and mailing a check (Chou & Chou, 2000). Banks and financial institutions allow users to perform financial transactions digitally rather than physically (Amin, 2016). It can increase electronic customer satisfaction and loyalty to boost business profitability (Kotler, 2011; Kotler & Keller, 2006). E-Banking is changing the financial services sector by promoting innovation, fostering growth, and boosting internal and external competitiveness (Ayinaddis et al., 2023; Yang et al., 2023). However, current banking services, particularly in developing countries, lack the distinguishing characteristics of online banking services (Amin, 2016; Banstola, 2008; Firdous, 2017; Rod et al., 2009).

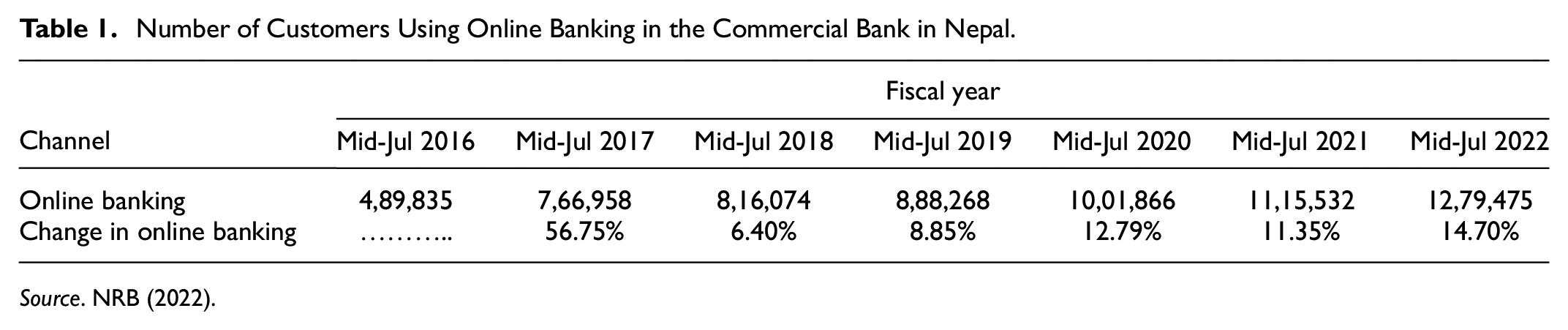

In Nepal, Kumari Bank was the first to provide online banking services to its customers in 2002 and introduced Short Messaging Service (SMS) banking in 2004. In 2006, Nepal Rastra Bank, Nepal’s central bank, formulated Nepal’s electronic transaction and digital signature act to formalize online banking practices (Banstola, 2008) which fueled to increase in technological innovation and aggressive infusion of information technology into the activities of banks and financial institutions. All commercial banks in Nepal offer online banking services and focus on proactive marketing to promote electronic banking. The number of customers using online banking in Nepal from 2016 to 2022 is presented in Table 1.

Number of Customers Using Online Banking in the Commercial Bank in Nepal.

Source. NRB (2022).

Nepalese banks and financial institutions face several difficulties in reforming their operations due to customers’ reluctance to embrace online banking despite its benefits. The banking industry faces intense rivalry to attract and retain consumers. Table 1 also explains online banking users are increasing, although fluctuating due to its services. Additionally, Khatri and Upadhyaya-Dhungel (2013) reported customers find it challenging to alter their physical banking activities into online services. To compete with competitors, they need to provide high-quality online banking services, which could contribute to a competitive and strategic advantage (Raza et al., 2020). Customers also find it hard to change their perceptions, actions, and attitudes toward online banking services (Amin, 2016; Khatoon et al., 2020; Khatri & Upadhyaya-Dhungel, 2013). Despite the increased use of online banking, customer interests have not been reached due to its reduced service quality (Banstola, 2008; Gaire, 2018; Khatri & Upadhyaya-Dhungel, 2013).

Therefore, the research raised a few questions: Do online banking service quality dimensions associated with e-customer satisfaction and e-customer loyalty? Is there an impact between online service quality dimensions on e-customer loyalty? Does e-customer satisfaction mediate between online banking service quality and e-customer loyalty? To address these questions, the objectives of the research were to explore the relationship between online banking service practices, e-customer satisfaction, and e-customer loyalty and examine the impact of both on e-customer loyalty. Further, this study aimed to identify the mediating impact of e-customer satisfaction on e-customer loyalty.

Literature Review

Online Banking Service Quality, E-Customer Satisfaction, and E-Customer Loyalty

Service quality contributes to customer satisfaction and loyalty. So, customer satisfaction is regarded as a predictor of service quality to create loyal consumers (Dahal, 2019; Firdous, 2017; Gaire, 2018; Sharma et al., 2020). Banks and financial institutions must constantly monitor customer satisfaction and loyalty to secure a continued presence in the financial industry. Parasuraman et al. (2005) and Zeithaml et al. (2002) researched online service quality and produced the e-SQ scale, in line with previous studies on service quality in traditional distribution channels. Efficiency, fulfillment, system availability, and privacy were identified as the core components of the E-S-QUAL, which consists of 22-item scales (Parasuraman et al., 2005). The second scale, E-RecS-QUAL, is only relevant to customers who had monotonous interactions with sites and consists of 11 items divided into three constructs: responsiveness, compensation, and contact (Zeithaml et al., 2002).

Alkhouli (2017) studied the link between bank website service quality and e-Satisfaction and their effects on e-Loyalty. The e-SQ for the Internet banking service offered by Malaysia’s commercial bank was ascertained using a modified version of the E-SERVQUAL instrument (Ariff et al., 2013). They discovered technical and functional aspects of a bank’s website in ensuring the quality of e-SQ that leads to e-Satisfaction and e-Loyalty. Cristobal et al. (2007) researched how perceived quality affected customer satisfaction and website loyalty. They discovered that perceived quality was a multidimensional construct influenced by design, customer-service, assurance, and administration. The perceived quality affected customer satisfaction, which was influenced by customer loyalty.

Yilmaz et al. (2018) studied link between the service quality, satisfaction, and loyalty of banks in Turkish by the SERVQUAL model. Data were explored using structural equation modeling (SEM) based on students’ real perceptions of banking services. Raza et al. (2015) considered the site of organization, responsibility, reliability, user-friendliness, and personal need as modified e-SERVQUAL model to examine the impact of Internet banking service quality on e-customer satisfaction and loyalty in Pakistan. They identified that businesses offer quicker transactions through easily accessible web portals to attract more customers. Therefore, banks should tactically increase customer awareness of online banking acceptance (Raza et al., 2020). The findings explained that all dimensions positively and impact customer satisfaction and loyalty.

Banking service quality levels have become a vital driving force in raising customer satisfaction and, as a result, expanding their loyal customer bases (Long & Vy, 2016). Anderson and Srinivasan (2003) defined e-customer loyalty in Internet banking as customers’ tendency to use a single website, visit it frequently, and demonstrate high site stickiness with high detention time. According to Amin (2016), all four dimensions of the website, such as personal need, organization site, user-friendliness, and website efficiency, demonstrated a significant favorable link between online banking, e-customer satisfaction, and e-customer loyalty. Matar & Alkhawaldeh (2022) also found Wi-Fi is one of the most advanced technologies to join the banking sector and offers considerable advantages to banks and customers. Yang et al. (2023) researched to rate the impact of Internet banking on the profit efficiency from outside and inner aspects in China. The researchers constructed a panel data set of 235 commercial banks in China from 2005 to 2016. The results revealed that commercial banks’ online banking business affects profitability and efficiency.

E-Customer Satisfaction and E-Customer Loyalty

Several studies on customer satisfaction and loyalty have been undertaken over the years (Amin, 2016; Anderson & Srinivasan, 2003; Arif et al., 2015; Cristobal et al., 2007; Ganguli & Roy, 2011; Long & Vy, 2016; Oliver, 1980; Raza et al., 2020; Siddiqi, 2011). Customer satisfaction is the key to a bank’s success and can directly impact customer loyalty. It is crucial from a theoretical approach to investigate which factors influence customer satisfaction. It has a noticeable and considerable impact on e-customer loyalty. So, it is the base for e-customer commitment (Al-Msallam, 2015; Ganguli & Roy, 2011).

The study of Anderson and Srinivasan (2003), explained that e-customer satisfaction directly and significantly impacts e-customer loyalty, and reciprocate to employee job satisfaction (Gautam, 2016). Amin (2016) reported that customers satisfied with their Internet banking experience would be more loyal to their bank. The result clearly explained that e-customer satisfaction is critical in determining e-customer loyalty. Raza et al. (2020) also examined the structural relationship between online banking service quality dimensions, electronic customer satisfaction, and loyalty. They revealed that as more people utilize the Internet as their primary means of communication with their bank, the Internet relevance in banking grows. Customer loyalty primarily focuses on keeping customers online by responding to their inquiries, problems with online banking, and overall pleasure.

Customer satisfaction and perceived value are two essential drivers of customer loyalty (Javed, 2017). The result showed customer satisfaction, perceived value, and organizational performance had a strong positive association. Customer satisfaction predicts consumer loyalty in business to consumers (B2C) e-commerce (Eid, 2011). The relevance of design features direct effect website satisfaction, trust, and e-customer loyalty in the Saudi online shopping culture.

A loyal customer is likelier than a non-loyal customer to find the service encounter and overall experience with a service provider more satisfactory. Therefore, satisfied customers can better demonstrate their devotion online than offline, maybe through bookmarks, search tools, and hot links associated with the website’s content (Shankar et al., 2003). Bloemer et al. (1998) and Fida et al. (2020) explored the effects of service quality on e-customer satisfaction and loyalty. They discovered that service quality, e-customer satisfaction, and e-customer loyalty all were significantly associated. Gaire (2018) also found service quality and customer satisfaction are associated considerably. Higher e-satisfaction and e-loyalty will result improved e-service quality. E-SQ factors were discovered to exhibit significant effects on e-satisfaction, indicating that enhancing e-SQ will lead to increased e-satisfaction, e-satisfaction had a strong positive impact on e-customer loyalty (Ariff et al., 2013), and higher customer satisfaction increases loyalty toward banks (Yilmaz et al., 2018).

Customer satisfaction and loyalty may open new avenues for improving services and gaining a competitive advantage (Siddiqi, 2011). Technology has been found to affect customer loyalty significantly and favorably. Customers build favorable value judgments about service providers based on the quality of their service experience (Banu et al., 2019; Ganguli & Roy, 2011).

The literature discussed above shows that an empirical investigation on e-customer satisfaction and e-customer loyalty which has a strong theoretical foundation. Customer satisfaction with the service quality experience leads to increased customer loyalty. The positive significant coefficient for the customer satisfaction and loyalty relationship indicates that consumers were satisfied with banking services and loyal to banks. A satisfied customer is critical to the development of a loyal customer. Businesses should endeavor to keep their customers satisfied. Customer loyalty and retention may be among the most effective weapons available to banks and financial institutions in their battle to obtain a strategic edge and survive in today’s increasingly competitive climate (Shanka, 2012). The quality of the E-banking offerings is the key determinant of customer satisfaction that encourages the client to stick with the banks and maintain long-term and fruitful relationships (Khatoon et al., 2020). So, customer satisfaction and loyalty are positively correlated with service quality parameters (Ayinaddis et al., 2023; Yang et al., 2023).

Research Framework

This research framework focuses on how online banking service practices impact e-customer satisfaction and e-customer loyalty. Based on the literature, we developed a framework of research (Figure 1) in which independent variable online banking service quality factors as e-customer service, organization site, website efficiency, user-friendliness, security, and privacy, the mediating role played by e-customer satisfaction, and e-customer loyalty is dependent variable.

Conceptual framework of OBSQL on ECSA and ECLO.

Figure 1 is designed to examine the relationship between five dimensions of online banking service quality practices, e-customer satisfaction, and e-customer loyalty. The research framework was based on E-S-QUAL (Parasuraman et al., 2005) and E-RecS-QUAL (Zeithaml et al., 2002). The model was used to discover that businesses offer quicker transactions through easily accessible web portals to attract more online customers and increase customer awareness of online banking acceptance (Raza et al., 2020). Based on the theories and research framework, the following research hypotheses were proposed:

H1: Online banking service quality has a positive relationship with e-customer satisfaction.

H2: Online banking service quality has a positive relationship with e-customer loyalty.

H3: E-customer satisfaction mediates the relationship between online banking service quality and e-customer loyalty.

Methodology

The deductive approach was adopted for the research. This study explained the causal-comparative relationship between online banking service quality, e-customer satisfaction, and e-customer loyalty. Deductive research is usually concerned with collecting quantitative data to interpret later and conclude the results (Saunders et al., 2003).

The target population of this study was all online banking customers of commercial banks in Nepal. Samples were taken from all commercial banks by stratified sampling techniques. The quantitative data were collected through a standardized questionnaire that had 42 questions and was split into three sections. The first segment included four questions about the respondent’s demographic information. The second segment, which asked about online banking services, consisted of six queries. The third segment asked for 32 statements about service quality, customer satisfaction, and loyalty. All survey items for the study variables were graded on seven-point Likert scale, with 1 representing strongly disagree and 7 indicating strongly agree. There were 475 questionnaires collected, but 50 were incomplete, and 41 surveys were eliminated as outliers. Thus, 384 questionnaires (76.8% response rate) were legitimate for further analysis (Bhattacherjee, 2012; Cooper & Schindler, 2014; Sekaran & Bougie, 2016). Transporting the data into a statistical package for social science (SPSS) and analysis of a moment structures (AMOS) were carried out for further investigation to identify results and presented in table, pie-chart, and model.

Analysis and Findings

Based on demographic composition nearly 60% are mail and the remaining female and 44% of respondents have age between 15 and 24 followed by 34% of those aged 25 to 35. The study included employed people at 47%, the student group at 42.4%, businesspeople at 6%, and the remaining others. Out of the total respondents, a large number 37% are having a bachelor’s degree, followed by 29% holding secondary level school education and a master’s degree each, and very least 1.5% of respondents were not formally educated.

The study considered other criteria such as the period of online banking service used, frequency of monthly use, purpose, reasons to use services, the effectiveness of online banking, and satisfaction rate. Based on the duration of online banking service, an equal number of respondents 21.6% used online banking for less than 6 months, and for 6 to 12 months each, a large number of respondents 34.6% of respondents utilized online banking for more than 1 to 3 years, while 22.1% had done so for more than 3 years. In terms of the monthly usage frequency of online banking services, 40.1% of respondents used Internet banking up to five times per month, whereas 32% used it more frequently than 5 to 10 times per month. It also found that 12.5% of all respondents have used Internet banking more than 10 to 20 times, and 15.4% used it more than 20 times. In terms of the purpose, it is explained that 50.5% of respondents used online banking to look up information about their accounts, and 5% utilized online banking for cash transfers and home banking. They utilized it for online stock trading at 41.9%, online money remittance at 29.5%, and electronic bill payment at 29.5%. They felt online banking was essential in the 21st century in every financial activity.

The main research tool was structural equation modeling. The two-step approach proposed by Bollen (1986), in which construct reliability is first ensured to develop a measurement model, and then the structural model is fitted. Model adequacy for measurement is determined by the fit between sample covariance and replicated covariance from causal model. The two-step approach will comprehensively evaluate the reliability of observable indicators before fitting the structural model (Hair et al., 1998).

Exploratory factor analysis was used before appropriating the measurement and structural model to achieve the theoretically expected factor solutions. The Kaiser–Meyer–Olkin (KMO) and Bartlett’s tests ensured that gathered sample was sufficient. The Kaiser–Meyer–Olkin (KMO) and Bartlett’s tests are shown in Table 2.

KMO and Bartlett’s Test to Sufficient of Gathered Sample.

Exploratory Factor Analysis (EFA), Bartlett’s Test of Sphericity (Chi-square 6,396.797) is significant (p-value = .000 < .05) as shown in Table 2. KMO value 0.835 (greater than 0.5) indicates that the relationship between variables was statistically significant and appropriate for EFA to provide a parsimonious collection of factors. Similarly, the significant value of Bartlett’s test of sphericity shows that correlation between measurement items was greater than 0.5, indicating that EFA was acceptable.

The KMO value was greater than 0.70, indicating that there were adequate and sufficient items for grouping, significance value was 0.000, which was less than 0.05, and the variables were adequately correlated, indicating that there was a sufficient basis for factor analysis (Dahal, 2019; Mattila et al., 2003; Raza et al., 2015). Kaiser Criterion suggested extracting seven factors. The seven factors F1, F2, F3, F4, F5, F6, and F7 correspondingly explained or extracted 15.226%, 9.847%, 9.348%, 9.311%, 9.093, 8.661, and 7.465% of the total variance, and altogether they extracted 68.951% of the total variance. Table 3 demonstrates that factor loading values greater than 0.50 were selected for further investigation.

Rotated Component Matrix a for Individual Scale Items.

Rotation converged in six iterations.

The factor loading matrix for each variable to each of the linked constructs is shown in Table 3 above as a rotated component matrix. The items were separated into seven essential components, and the factor loading for each item within each component was evaluated. Reliability is improved by removing two items ECUS 4 and SEPR 1 that fail to correlate at the 0.3 level with at least 50% of all other individual e-banking service quality items (Hair et al., 1998).

A measurement model is used to analyze the reliability and validity of the relationships between the constructs. The main objectives of the model are to assess composite reliability, convergent validity, and discriminant validity (Amin, 2016; Hammoud et al., 2018) shown in Table 4. Composite reliability is used to examine the reliability of constructs and convergent validity assess for standardized factor loadings (Bagozzi, 1981; Fornell & Larcker, 1981; Hu & Bentler, 1999) and discriminant validity evaluate constructs or measures that should not be linked or correlated (Anderson & Srinivasan, 2003; Bagozzi, 1981).

Model Fit Summary.

The measurement model, consisting of seven components measured by 30 scale items, was subjected to confirmatory factor analysis (CFA). The measurement model was evaluated for acceptable fit using standard model fit indices (Hair et al., 2010). Table 4 shows the CFA results for the overall measurement model.

Table 4 explains the sufficient on the following measures: χ2(389, N = 484) = 928.718, where CMIN/df (minimum discrepancy divided by degrees of freedom) = 2.387 (<3), Goodness of Fit Index (GFI) = 0.863 (<0.80), adjusted goodness of fit index (AGFI) = 0.836 (<0.80), comparative fit index (CFI) = 0.912 (<0.90), Tucker–Lewis index (TLI) = 0.902 (<0.90), normed fit index (NFI) = 0.859, and root mean square error approximation (RMSEA) = 0.060 (<1) (Hu & Bentler, 1999; Kim & Jindabot, 2022; Kline, 2011). So, it indicates research model fit indices. The findings of the measurement model are shown in Table 5, which shows that the model’s convergent validity has been reached.

Standardized Factor Loadings, Average Variance Extracted, Maximum Shared Variance, and Composite Reliability.

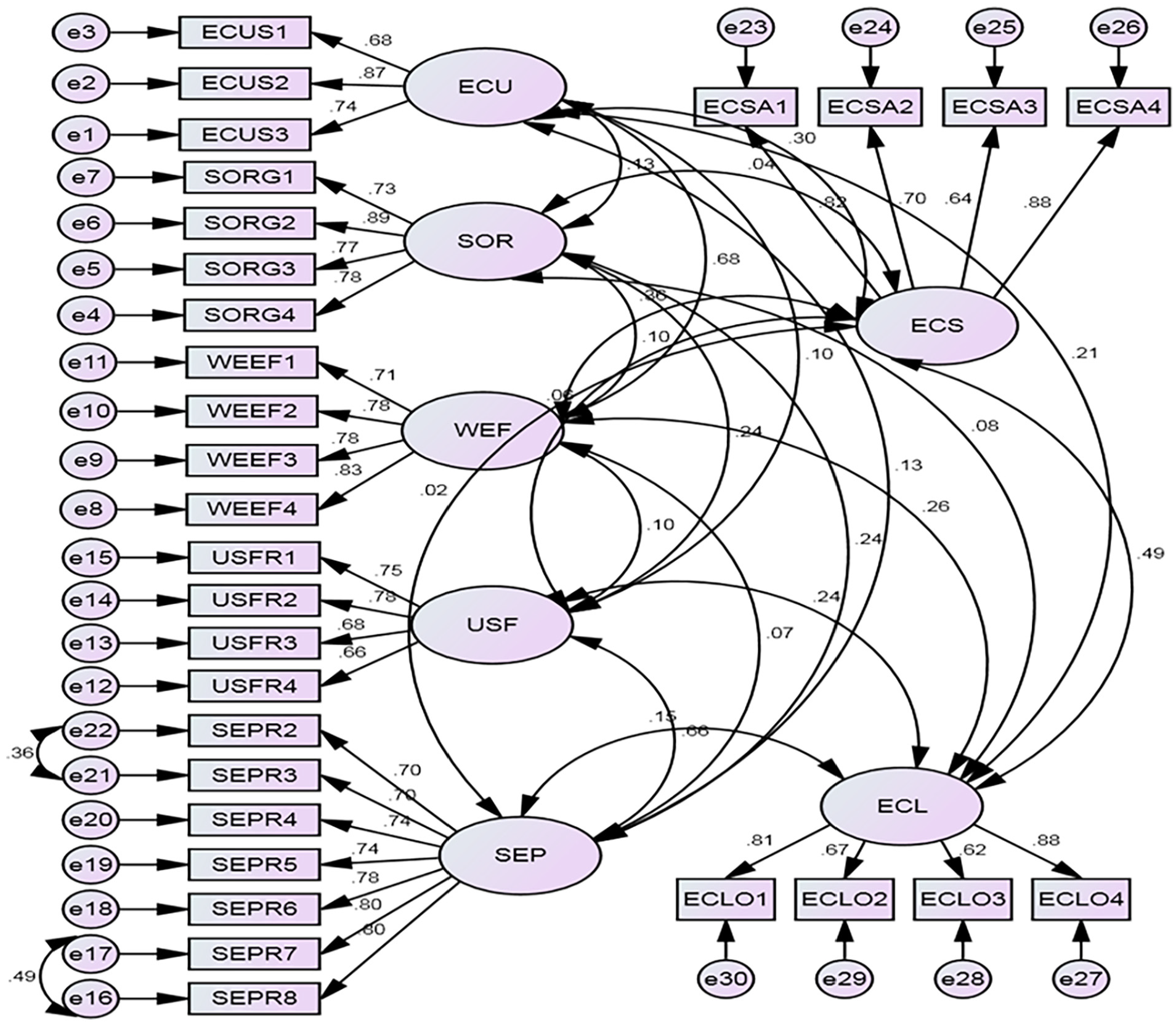

The coefficient alpha (α) was higher than the minimum obligation of .70 (Nunnally, 1978), indicating an excellent internal consistency estimate. The result shows that the convergent validity was established for each construct because each standardized factor loading of the reflective indicators ranged from 0.634 to 0.938 and exceeded the suggested level of 0.50 (Anderson & Srinivasan, 2003; Fornell & Larcker, 1981), composite reliability values ranged from 0.819 to 0.900, and exceeded the recommended level of 0.70 (Hair et al., 2010). AVE was also used to measure discriminant validity for the constructs (Black, 2010; Hair et al., 2010), and it ranged from 0.531 to 0.749 was greater than 0.5 and MSV is less than ASV (Anderson & Srinivasan, 2003; Bagozzi, 1981; Fornell & Larcker, 1981) suggesting that there were no discriminant validity issues with constructs. Matar and Alkhawaldeh (2022) also reported the fitted value removes validity issues and suggested no discriminant issues. A graphical presentation of measurement model shown in Figure 2.

The measurement model.

The path diagram of the final revised measurement model presented in Figure 2 shows that each indicator’s standardized factor loading ranged from 0.634 to 0.938, exceeding 0.50 (Anderson & Srinivasan, 2003; Fornell & Larcker, 1981).

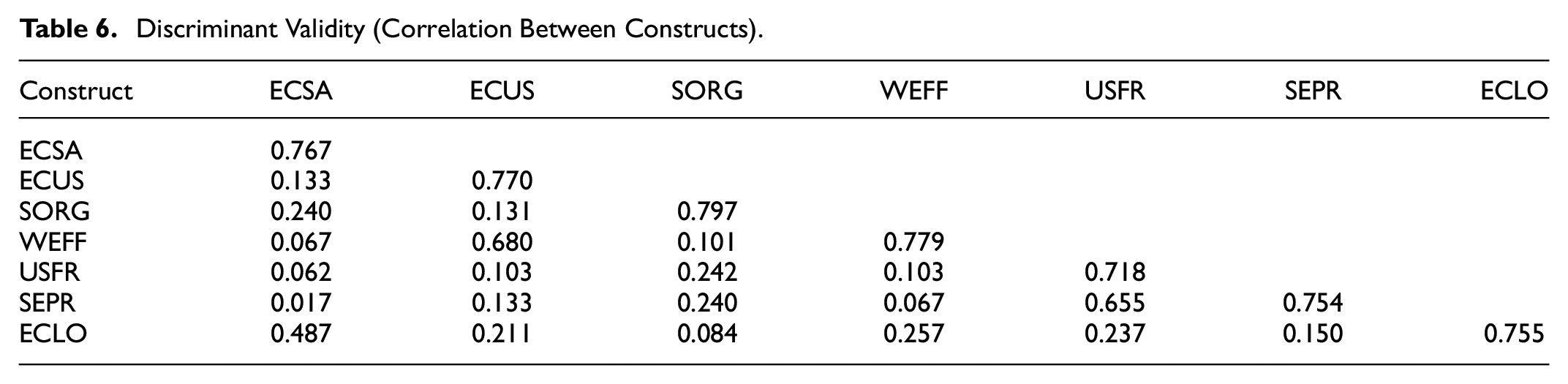

Discriminant validity was further verified by ensuring that the square root of each factor’s AVE was greater than the correlation between that factor and the rest of the model’s variables, indicating that there were no discriminant validity issues (Anderson & Gerbing, 1998; Fornell & Larcker, 1981). The square root of each factor’s AVE shows on the diagonal Table 6.

Discriminant Validity (Correlation Between Constructs).

It reveals the constructs’ discriminant validity; the square root of the AVE was greater than correlation calculated between factors. Thus the constructs' discriminant validity was confirmed (Bagozzi, 1981; Fornell & Larcker, 1981). Rahi and Abd. Ghani (2019) also reported the square root of the AVE was greater than corresponding row and column, indicating that the constructs were discriminant valid. According to Khan et al. (2019), the correlational relationships between the constructs provide a greater square root value than the correlations among the numerous constructs, indicating that discriminant validity was good. Quach et al. (2016) showed that all the constructs’ item loadings were higher than their respective cross-loadings of other latent variables, indicating good discriminant validity.

A structural equation modeling of online banking service quality on e-customer satisfaction and e-customer loyalty was used to estimate the parameters and structure of a study. A standardized beta coefficient was used to compare the strength of each independent variable’s effect on the dependent variable.

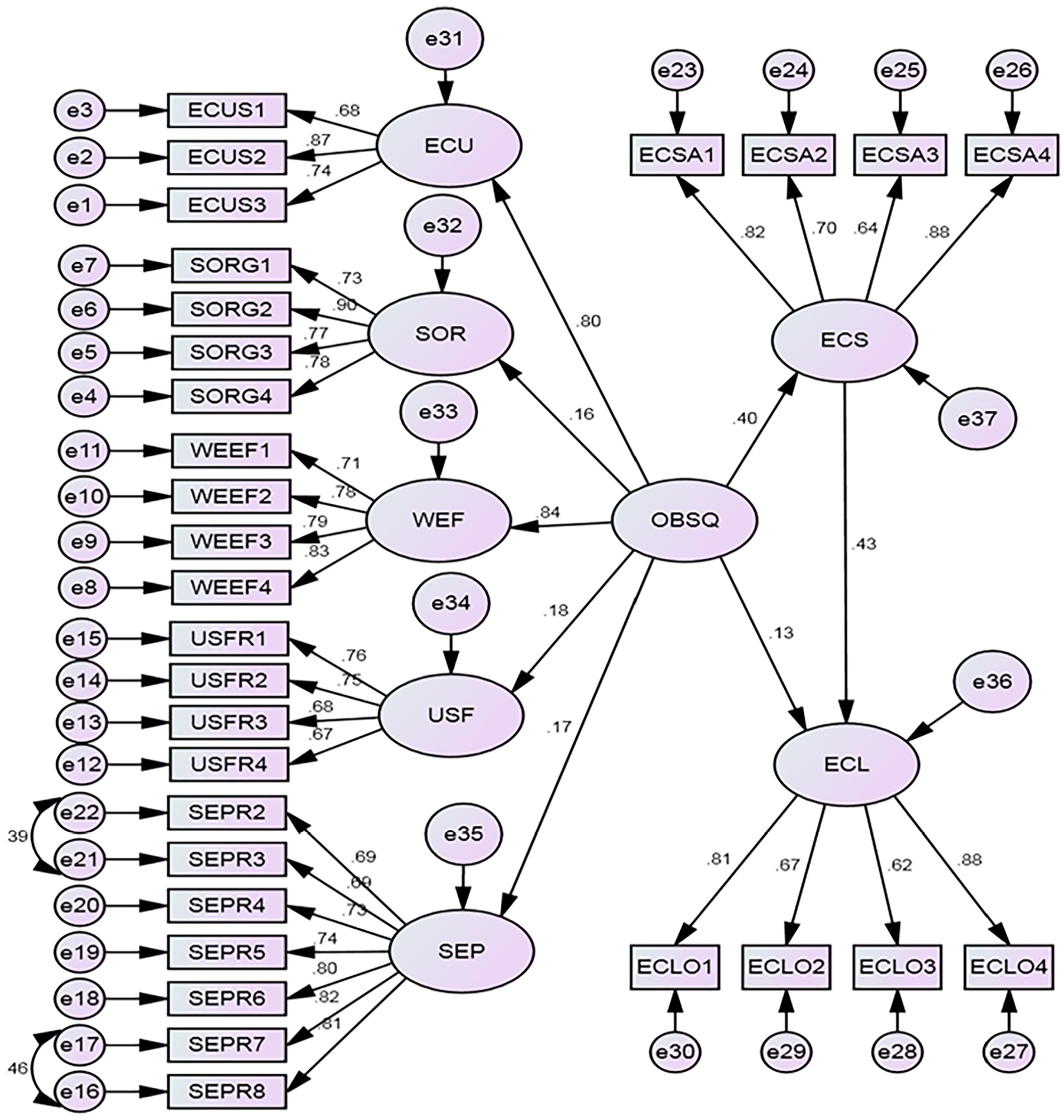

The structural effect of online banking service quality on e-customer satisfaction and e-loyalty explains its measurement scale, consisting of five-dimensions presented in Figure 3. The dimension of e-customer was measured by trio indicators by removing one, four indicators for site organization, and four for user-friendliness, three indicators for efficiency of the website, and seven for security and privacy. Similarly, e-customer satisfaction and e-loyalty are measured by four indicators for each. The results show the structure model of online banking service quality factors is good predictor of e-customer satisfaction and e-customer loyalty (Table 7).

The structural model.

Standardized Regression for Research Model.

Source. Author's calculation.

p < .001.

The standardized path was 0.840 for the efficiency of the website, 0.798 for e-customer service, 0.182 for user-friendliness, 0.165 for security & privacy, and 0.162 for site organization, respectively. Ayinaddis et al. (2023) reported trustworthiness, security and secrecy, pace, and suitability significantly influence customer satisfaction. Matar and Alkhawaldeh (2022) also found that perceived value, ease of use, and bank credibility have a positive and significant relationship using technology services.

The findings show online banking service quality has positive and significant relationship with e-customer satisfaction (β = .469; ρ < .001) and e-customer loyalty (β = .133; ρ < .05); thus, H1 and H2 were supported at 1% and 5% level of significance. This revealed a significant positive relationship between e-customer satisfaction and e-customer loyalty (β = 0.434; ρ < .001). Thus, H3 was also supported. The study discovered a substantial link between online banking service quality, e-customer satisfaction, and e-customer loyalty. Sasono et al. (2021) also found that e-service quality significantly positively influenced e-customer satisfaction and e-customer loyalty. E-customer satisfaction significantly influences e-customer loyalty, and e-satisfaction significantly mediates the impact of e-service quality on e-loyalty. Ayinaddis et al. (2023) reported the quality of electronic banking services significantly impacts customer loyalty. Conversely, they also found no statistically significant relationship between system accessibility, usability, service fee, and customer satisfaction.

However, Amin (2016) reported the quality of Internet banking services has no positive link with e-customer loyalty. According to Aldas-Manzano et al. (2011), banks must continuously and systematically examine the factors contributing to consumer satisfaction when using online financial websites. Customer loyalty is significantly impacted by how satisfied they are with the quality of electronic banking services. Conversely, there is no statistically significant relationship between system accessibility, usability, service fee, and customer satisfaction.

Conclusion

Nepalese Commercial Bank provides its loyal customers with simple online banking services to satisfy their needs and assist them in saving money while maintaining security. In the context of Nepalese Commercial Bank, this study expands on the association between the standard of online banking services, e-customer pleasure, and e-customer loyalty. Aspects of the quality of the online banking service have a significant impact on e-customer satisfaction and loyalty. It implies that improving the caliber of online banking services will boost e-customer loyalty by enhancing e-customer satisfaction.

In this study, e-customer satisfaction significantly impacted e-customer loyalty, as in most earlier studies. The relationship between the caliber of the online banking service and e-customer loyalty was mediated by e-customer satisfaction. Gaire (2018) discovered that ease of access, convenience, protection, secrecy, processing speed, and prices impacted customers’ satisfaction with online banking. According to Khatoon et al. (2020) finding, various factors, including dependability, efficiency, responsiveness, communication, security, and privacy, significantly and favorably influence customers’ intents.

The outcome indicated that website design and user-friendliness were the two aspects of Internet banking that had the most significant impact, followed by security and privacy considerations. Customer satisfaction is thus significantly positively correlated with website usability and design. This demonstrates that banks with efficient websites and quick transactions through easily accessible online portals attract customers more. Amin and Isa (2008) discovered that providing greater levels of services will result in more satisfied customers. Ayinaddis et al. (2023) found that customer satisfaction and system availability were both favorable and significant. However, Matar and Alkhawaldeh (2022) found no connection between perceived security issues and Wi-Fi service consumption.

It also shows the connection between security, privacy, and customer satisfaction. When interacting with banks and other financial institutions, customers are more concerned about the protection and confidentiality of the website. Omotayo (2020) states that banks should increase customers’ trust and confidence in Internet banking by offering dependable and secure platforms. Therefore, banks should strategically raise customer awareness of the acceptability of the Internet banking system. Banks should focus on all four factors, such as website design, usability, security, and privacy, to maintain a high level of bank service quality. Oliver (1980) also asserted that consumers are content when the perceived performance matches or exceeds their expectations for the level of service.

Therefore, banks and other financial institutions can benefit from this research while using online banking. However, Nepal’s main obstacles to e-banking are risk management, infrastructure, rules, regulation, and policy. Many technology-related issues, such as poor cell service and connectivity issues, occur when withdrawing cash from ATMs, impeding the growth of e-banking in Nepal. So, the study’s online banking service quality elements enable bank executives, managers, and policymakers to concentrate their efforts and resources profitably, efficiently, and economically. It helps the bank’s business grow by enticing new consumers to use Internet banking and retaining current clients.

Contributions

This study contributes significantly to the literature on bank and financial marketing. It also benefits academicians since it reveals how online banking service practices predict consumer e-satisfaction, eventually increasing e-loyalty. In this study, the five components of banking service quality influencing e-customer satisfaction and e-customer loyalty are e-customer service, organization site, website efficiency, user-friendliness, security, and privacy.

There are many challenges to maintaining all services and service quality in the banking sector. So, these findings definitely assist banking sector in developing efficient marketing strategies, establishing long-term relations with its customers, and gaining a strategic advantage in the marketplace. This study will also help to grow digital banking activities nationally and internationally. It will be helpful for individuals’ economic fitness strengthening communities and financial ties.

Limitations and Future Research

Only commercial banks were employed for online banking service quality for this study. Future research should be conducted on the overall bank and financial institutions’ online and mobile banking (Jahan & Shahria, 2022). Researchers can widen the study’s scope using different online banking service quality parameters to acquire more precise results.

Footnotes

Acknowledgements

We acknowledge respondents for survey participation, anonymous reviewers, and editors for their valuable comments and suggestions to improve the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We would like to acknowledge the University Grants Commission of Nepal, and Tribhuvan University for the research supports to carry out this research, and Patan Multiple Campus, Lalitpur for their kind cooperation.

Ethical Statement

We followed all ethical norms of research, and there are no requirements to get permission from elsewhere.