Abstract

This article, based on experimental evidence, reports insights into how chief financial officers—experts—and master’s students in accounting—novices—perceive economic rationality within the field of accounting. Based on the prospect theory and the fourfold pattern, four scenarios, covering everyday business situations, are used as a measurement instrument for capturing the experimental subjects’ perception of economic rationality. The findings of the article indicate that the experts and the novices seem to be more economically rational when it comes to dealing with risk and uncertainty related to gains than when dealing with risk and uncertainty associated with losses. Furthermore, the novices tend to deal with the sunk-cost fallacy in a more economically rational way than the experts. From an economically rational point of view, mental accounting should not be particularly important in accounting judgment and decision making, but sometimes the experimental subjects seem to frame the scenario/issue at hand in mental-accounting terms.

The quest for rational decisions is interesting, especially in today’s automated economy (Brynjolfsson & McAfee, 2011, 2014; Domingos, 2015; Ford, 2015), in which humans, including chief financial officers (CFOs), have to partner digitized machines. It is generally accepted that accounting at its core is about the judgment and decision making (JDM) of individual CFOs (cf. Ashton & Ashton, 1990, 1995; Bonner, 2008; Gibbins & Mason, 1988). A huge body of research exists covering various aspects of accounting and individual JDM (e.g., Ashton & Ashton, 1995; Bonner, 2008). Although the findings of the accounting literature are largely consistent with the findings of the psychological literature, they are somewhat fragmented and subject to interpretation. According to Bonner (2008), the findings of the accounting research indicate that producers, users, auditors, regulators, and evaluators of accounting information do not always make high-quality judgments and decisions. Many of these errors are systematic (cf. Barberis & Thaler, 2003; Kahneman, 2002; Kahneman & Tversky, 1972, 1979, 2000; Thaler, 2015), which can lead to several economic consequences for the individuals making the judgments and decisions as well as for the firms that employ them and especially for the users of this information (e.g., Berg, Dickhaut, & McCabe, 1995; Bloomfield, Libby, Nelson, & Hopkins, 2003; Thaler, 2015).

The normative expected utility theory (Savage, 1972; Von Neumann & Morgenstern, 1953) is considered to be the right way to make rational decisions, whereas the descriptive alternative, the prospect theory (Kahneman & Tversky, 1979; Tversky & Kahneman, 1986, 1992), aims to give a good prediction of the actual choices that humans make (Thaler, 2015). Thaler (2015) elegantly captures the essence of the value function of the prospect theory: “. . . we experience life terms of changes, we feel diminishing sensitivity to both gains and losses, and losses sting more than equivalently-sized gains feel good” (p. 34). Alternatively, in the words of Kahneman (2002), “the core idea of prospect theory . . . is that changes and differences are much more accessible than absolute levels of stimulation” (p. 456). From a 30-year perspective, Barberis (2013) concludes that the prospect theory is still commonly viewed as the best-available description of how humans evaluate risk in experimental settings. However, the prospect theory is not complete, because it does not elucidate from where the reference point comes and it does not provide a theory of mental accounting regarding how humans combine gains and losses in different domains (Thaler, 2013).

March and Shapira (1987) report that managers do not seem to follow the rules of the standard rational model of economics, but they also have a tendency to think about risk that is difficult to reconcile with classical theoretical conceptions of risk. Based on a database of 706 managers, Shapira (1995) draws the conclusion that managers’ attitudes toward risk taking are embedded in the context of life in organizations; thus, the implication of risk and uncertainty is context dependent. In addition, managers do not think in probability terms but more in terms of well-known examples.

Within the target domain of this study, the field of accounting, the preparer of financial reporting, the CFO, or someone with an equivalent position is the manager. One rationale for studying accountants, including CFOs, is that they, according to Bonner (2008), may have higher average levels of personal involvement in JDM than other professionals. Ashton and Ashton (1995, p. 18) maintain that judgment and decision research has not paid enough attention to preparers of external accounting information, which opens the possibility for making an important contribution in this “underresearched” area that could be substantial (p. 19).

The study intends to answer the questions of whether CFOs tend to make economically rational choices (high-quality JDM) within the field of accounting and from where their reference point comes. Furthermore, do CFOs tend to make more economically rational choices (higher quality JDM) than master’s students in accounting? How does mental accounting fit into this context? In addition, the aim is to increase our understanding of the studied phenomenon.

JDM—The Context

Judgments in accounting, in the view of Bonner (2008), tend to be judgments made under uncertainty and take particular forms—either probabilities or quantities. In addition, “the term judgment refers to forming an idea, opinion, or estimate about an object, an event, a state, or another type of phenomenon” (Bonner, 2008, p. 2). Judgments in accounting are likely to take the form of predictions about future conditions or events or the evolution of current but not completely knowable conditions or events (Bonner, 2008). In the normative JDM theories, decisions typically follow judgments, involving a choice between different options based on judgments about those options and preferences for factors such as risk and money (Bonner, 2008). This article adopts the JDM research terminology and makes a distinction between judgments and decisions. To become a “professional judgment,” or in this context an “accounting judgment,” the judgment has to be informed by a more extensive process requiring relevant expertise and knowledge and following the requirements and responsibilities of one’s job (Gibbins & Mason, 1988, p. 5). Consequently, following Gibbins and Mason (1988), “accounting judgment” (p. 5) is judgment exercised with due care, objectivity, and integrity within the framework provided by applicable accounting standards by experienced and knowledgeable people.

According to Libby and Luft (1993), four distinctive features tend to distinguish the domain of accounting and auditing from any other domain. These are “(1) the multiperiod/multiperson nature of the judgments and decisions, (2) enormous financial (and other) consequences involved, (3) the presence of markets, and (4) important institutional considerations” (Ashton & Ashton, 1995, p. 6). The “multiperiod/multiperson nature” accentuates an approach to JDM that is sequential and iterative and emphasizes the significance of accountability on the part of the decision maker (Ashton & Ashton, 1995, p. 6). Accounting and auditing decisions may have primary as well as secondary consequences in that the effect may extend to parties other than those who are immediately affected (Ashton & Ashton, 1995). The presence of markets may induce a form of competition among individual decision makers, which, in turn, may add complexity to the decision-making process (Ashton & Ashton, 1995). Finally, accounting and auditing judgment and decision tasks are embedded in a comprehensive institutional context, including professional societies, a regulatory and legal environment, independent auditing, and accounting firms (Ashton & Ashton, 1995).

Some significant aspects of accounting JDM (Gibbins & Mason, 1988) are (a) involving a meaningful choice; (b) involving a process from perceiving the problem to making the decision; (c) arising from one’s job responsibilities; (d) using personal integrity and related attitudes and beliefs; (e) involving expertise and due care, including knowledge of relevant professional standards and current practice; (f) based on experience in such problems and their circumstances; and (g) made in circumstances permitting professional objectivity.

JDM—The Prospect Theory

The expected utility theory is the most important theory in the social sciences (Kahneman, 2002, 2012). Whereas the expected utility theory is concerned with long-term outcomes, the prospect theory (Kahneman & Tversky, 1979, 2000; Tversky & Kahneman, 1981, 1992) emphasizes short-term consequences by portraying the emotions that are experienced at moments of change from one state to another (Kahneman, 2000; Mellers, 2000). This is an important contribution, because people tend systematically to fail to comply with the predictions of the expected utility theory (Barberis, 2013; Barberis & Thaler, 2003; Kahneman & Tversky, 2000). The prospect theory presents a new model of risk attitude, which captures the experimental evidence on decision making under risk. The expected utility theory suggests that risk attitudes affect the subjective assessment of choices (Bonner, 2008). Choices, in the view of prospect theory, are made by considering gains and losses rather than the final states (Kahneman & Tversky, 1979). That is, choices are framed as gains and losses. The overall focus is on changes, and emotion is triggered by changes (Kahneman, 2002). According to the prospect theory, the decision maker needs to know the reference point, which is the initial position relative to which gains and losses are assessed. In the expected utility theory, the decision maker needs to know only the state of wealth, not the reference point. Therefore, the prospect theory is more complex than the expected utility theory (Kahneman, 2012). Retrospectively, Barberis (2013) concludes that, more than 30 years after the publication of the seminal article, the “prospect theory is still widely viewed as the best available description of how people evaluate risk in experimental settings” (p. 173).

The three cognitive features that form the basis of the prospect theory are as follows: (a) evaluation is relative to a neutral reference point, (b) diminishing sensitivity is attributed to both sensory dimensions and the assessment of changes in wealth, and (c) loss aversion (Kahneman, 2012). According to Kahneman (2012), these cognitive features are common to many automatic processes of perception, judgment, and emotions, and they should be seen as operating characteristics of System 1 (Stanovich & West, 2000).

In the words of Scholten and Read (2014), the “prospect theory is a weighted-value model, in which outcome value is multiplied by a probability weight” (p. 79). The psychological value of gains and losses is represented by an S-shaped value function (a concave shape reflecting gains and a convex form mirroring losses), which runs through two separate domains, one to the right and the other to the left of the zero-reference point. The S-shaped value function represents diminishing sensitivity to gains as well as to losses. A distinctive feature of the S-shaped function is that the two curves are asymmetric, which represents that the response to losses is stronger than the response to parallel gains (Kahneman, 2012). The bending of the value function where gains pass to losses transforms into a much steeper slope, reflecting that a loss is weightier than the corresponding gain (Tversky & Kahneman, 1981).

One of the main achievements of the prospect theory is the fourfold pattern of risk attitudes (Kahneman, 2012), which illustrates that the decision weights assigned to outcomes are different from probabilities; that is, decision weights overweight low probabilities and underweight moderate-to-high probabilities. The asymmetry at the low end of the scale, where unlikely events are overweighted, reflects the possibility effect, whereas at the other end, the certainty effect can be found (Kahneman, 2012). The top row in the fourfold matrix illustrates the certainty effect in cases of high probability, whereas the bottom row exemplifies the possibility effect in cases of low probability. The two columns of the matrix reflect the dichotomy between gains and losses.

The top-left cell (certainty effect, high probability, gains) elucidates that individuals are risk averse in situations in which there is a significant chance of achieving a large gain [risk averse over high-probability gains] (Kahneman, 2012, p. 317).

The top-right cell (certainty effect, high probability, losses) demonstrates that individuals seek risks in the domain of losses, just as they are averse to risks in the domain of gains [risk seeking over high-probability losses] (Kahneman, 2012, p. 318).

The bottom-left cell (possibility effect, low probability, gains) displays risk-seeking behavior when there is hope of a large gain, notwithstanding that the probability of realization of this aspiration is low [risk seeking over low-probability gains] (Kahneman, 2012, pp. 317-318).

The bottom-right cell (possibility effect, low probability, losses) exhibits a situation in which there is fear of a large loss but a low probability that this will happen, which triggers risk-averse behavior [risk averse over low-probability losses] (Kahneman, 2012, p. 318).

Harbaugh, Krause, and Vesterlund (2009) examine the robustness of the fourfold pattern of risk attitudes. They find that individuals, on average, when provided with prices for gambles, seek risk over low-probability gains and high-probability losses and are risk averse over high-probability gains and low-probability losses. However, their results reveal that the price ordering of risky prospects can be very different from the choice ordering. The authors conclude that an increase in the cognitive load may aggravate behavioral biases (Harbaugh et al., 2009).

Scholten and Read (2014) examine the fourfold pattern of risk preference deducted from the prospect theory with a corresponding pattern identified by Markowitz (1952) and conclude that, at the qualitative level, the findings indicate less risk seeking for large gains than for small ones when the probabilities are low and more risk aversion for large gains than for small ones when the probabilities are high. Furthermore, the authors find risk aversion for losses when the probabilities are low and risk seeking when the probabilities are high, but they find no consistent pattern of stake dependence (Scholten & Read, 2014). Scholten and Read conclude by stating that stake dependence emerges as a major challenge to the theories of choice under risk, including the prospect theory.

Chang, Yen, and Duh (2002) set out to test the explanatory power of the prospect theory within a managerial accounting context using the framing effect. As the authors stress, most accounting tasks require accountants to make judgments in collecting and providing accounting information for managers to use when making decisions (Chang et al., 2002). The way in which the information is presented may evoke a particular emotion, and different ways of presenting the same information may evoke different emotions (Kahneman, 2012). This phenomenon is commonly referred to as the framing effect. The prospect theory is applied in many accounting studies using the framing effect (Chang et al., 2002).

Levin, Schneider, and Gaeth (1998) suggest that the prospect theory probably best explains the choices made by individuals committing the framing bias, but they question whether one theory can be used to interpret the empirical evidence of choices under risk in different contexts. This reasoning is consistent with Wang and Johnston (1995), who argue that the framing effect is a context-dependent phenomenon.

After reviewing the literature on decision making under risk, Harbaugh et al. (2009) conclude that (a) very few studies examine the robustness of the fourfold pattern of risk attitudes and (b) those studies that test the fourfold pattern tend do so by studying choices over a large set of relatively complex gambles (cf. Camerer & Hogarth, 1999; Gonzalez & Wu, 1999; Harless & Camerer, 1994; Hey & Orme, 1994; Holt & Laury, 2002; Scholten & Read, 2014). In accordance with other studies, Harbaugh et al. find that individuals are on average risk seeking over low-probability gains and high-probability losses and risk averse over high-probability gains and low-probability losses.

Mental accounting is, in the view of Thaler (1999), the set of cognitive operations used by individuals to organize, evaluate, and keep track of monetary activities. In so doing, individuals recognize their money in different accounts, of which some are physical and some only mental (Kahneman, 2012). The mental accounts, which are used to keep matters under control and manageable, are linked to the value function depicted by the prospect theory. Individuals strive to close the accounts with a positive balance, as losses hurt about twice as much as gains make us feel good (Kahneman, 2012; Thaler, 2015). Related to the fourfold pattern, throwing good money after bad rather than closing the account with a negative balance may result from choosing between a sure loss and an unfavorable gamble.

Managers’ Perspective on Risk and Risk Taking

March and Shapira (1987) elaborate how managers define and react to risk. They observe that (a) managers are much more inclined to use a few key values to describe risk than to use a single quantifiable probability measurement, (b) they think that risk is manageable and that skill or information can reduce the uncertainty, and (c) they see choice as a commitment to a performance target. Empirical observations of managers’ perspective on risk and risk taking indicate that risk is not understood primarily as a probability concept; rather, risk could better be comprehended in terms of the amount to lose (March & Shapira, 1987). Most managers see themselves as discerning risk takers and as less risk averse than their colleagues. In keeping with Kahneman and Tversky (1979), March and Shapira suggest that risk taking is affected by the relation between current performance (e.g., profit, liquidity, sales) and some critical reference points. Furthermore, the value that managers attach to different choices may depend not only on whether they are framed as gains or losses but also to which of two targets (the “success” target or the “survival” target) they refer (March & Shapira, 1987, p. 1410; see also Lopes, 1987).

If a manager is above a performance target, March and Shapira (1987) argue that the focal attention is on avoiding transactions that might place the manager below the performance target—which leads to relative risk aversion on the part of successful managers or managers who reach their target. On the contrary, for managers who are, or who are expected to be, below the performance target, the aspiration to meet the target tends to lead to risk taking—focusing on potential gains rather than on possible losses (March & Shapira, 1987). March and Shapira conclude that managers in general consider probability estimates to be unreliable and, instead of assessing or accepting risk, look for alternatives that can be managed to meet or surpass the targets.

Shapira (1995) emphasizes that for managers the meaning of risk and uncertainty is context dependent and that they tend to refer to well-known examples (heuristics). Managers do not think in terms of probabilities but rather about how to handle worst-case scenarios and how to reduce negative consequences or avoid taking responsibility for negative consequences.

Kahneman (2012) and Kahneman and Lovallo (1993) assert that decision makers (e.g., CFOs) are inclined to treat problems as unique, ignoring the statistics of the past (the inside view) as well as the multiple opportunities of the future (the outside or broader view). The former view may lead to excessively optimistic risk taking, whereas the latter may result in exceedingly cautious attitudes. The crunch, according to the authors, is to strike a balance between the two, which will affect the risk-taking propensities of decision makers. Kahneman and Lovallo’s cognitive analysis indicates that decision makers (e.g., CFOs) tend to have a strong intuitive preference for the inside view, and they tend to treat decision problems as unique, despite the presence of information that may support a broader view.

In his seminal work, Knight (1921) distinguishes between risk and uncertainty or, more precisely, in the business world between measurable risk and unmeasurable uncertainty. To deal with uncertainty, business leaders have to become entrepreneurs in that they have to exercise critical judgment to make a profit. Drawing on Knight, Mousavi and Gigerenzer (2014) assert that, in unique situations involving uninsurable risk and a lack of properties that satisfy the mathematics of probabilities, heuristics are indispensable tools. Related to a priori probability (risk), the decision process is deductive, whereas statistical probability (risk) presumes inductive or statistical inference (Mousavi & Gigerenzer, 2014). Under uncertainty, on the contrary, decision making refers to situations in which the probabilities cannot be estimated reliably (Mousavi & Gigerenzer, 2014).

As a consequence of increasingly deeper insights into cognitive biases, Kahneman, Lovallo, and Sibony (2011), among others, give advice regarding how executives can unearth defects in thinking in an organizational context by implementing proper review tools.

Research Design

The bulk of JDM research in accounting is experimental (Bonner, 2008; Mala & Chand, 2015). The experimental research design, in the view of Bonner (2008), allows researchers, inter alia, to manipulate variables systematically and to measure variables validly and reliably. However, this design sets out from an abstraction of the real world and thus may have shortcomings in terms of external validity. One major disadvantage of interviews (and survey studies) when measuring JDM quality is that the interviewees may not recall the specific decisions in question when interviewed (cf. hindsight bias; Plous, 1993). However, cautiously designed surveys and interview studies may result in intriguing insights (Nelson, Elliott, & Tarpley, 2002; Nielsen, Mitchell, & Nørreklit, 2015).

The present study is based on an experimental design complemented by brief interviews with the CFO respondents and written comments by the master’s student respondents. In experimental studies of JDM in accounting, convenience samples of students are common (Bonner, 2008; Bryman & Bell, 2007). The collected data can be compared with extensive empirical evidence; thus, the collected data from the CFO respondents’ sample can be compared with the data collected from the master’s student respondents’ sample (cf. Lukka & Kasanen, 1995).

JDM quality is defined from the perspective of a respondent’s selection of one choice from the option of two choices, together with the respondent’s stated rational for his or her choice. From a validity point of view, it is crucial that the respondents can relate to the presented scenarios. The scenarios were subjected to comprehensive pretesting. During the data collection phase, no respondents asked any questions concerning the content or form of the scenarios. Instead, several respondents spontaneously expressed that the scenarios were interesting and useful. Another aspect considered when choosing this sampling method is that the bulk of the literature gives evidence for the prospect theory. Thus, the collected data can be compared with extensive empirical evidence. Furthermore, putting CFO respondents to the test regarding the extent to which they are economically rational may be a very sensitive issue. This may indicate that a probability sampling method would produce a high nonresponse rate.

Another issue is whether the master’s students might have associated the task more closely with an exam, whereas the CFOs might have associated it with a casual request for information. The master’s students exhibited a high level of commitment to the task, but that also applies to the CFOs. The CFOs considered the survey questions to be sensitive, and as they did not want to lose face, they showed a high level of commitment to the task. Some CFOs even considered the survey questions to be so sensitive that they took far-reaching actions to avoid having to answer them.

Data Collection

A web survey titled “Survey of Economic Judgments—Four Cases of Economic Judgments” was drafted in an online survey tool. The survey consisted of three sections: an introduction, a background question, and scenarios. One background question was included, concerning work experience as a CFO (or equivalent) in terms of years. Then the scenario section followed. The respondents were encouraged to respond to the questionnaire choices (the scenarios) swiftly to capture their preferences.

Adjacent to the survey (within 2 to 3 days), the interview question (personal or by phone)—on what grounds did the CFO respondents make their choices?—was asked.

Fifteen CFOs from 11 listed companies (73%), three larger private companies (20%), and one consultancy firm (7%) constituted the CFO sample. The master’s student sample comprised 28 master’s students with majors in accounting. Both samples were nonprobability convenience samples including those respondents who were most readily available to take part in the study (cf. Bryman & Bell, 2007; Remenyi, Williams, Arthur, & Swartz, 1998; Ryan, Scapens, & Theobold, 2002).

The CFOs were contacted by phone, and an Internet-based survey was dispatched to those who were willing to participate in the study. The CFO respondents were selected on the basis that they had both courage and knowledge to choose the questionnaire options related to each scenario. Courage is a key dimension in that CFOs portray themselves as being economically rational (cf., for example, Thaler, 2015).

On the same occasion, a date and time for a short follow-up interview, either by phone or in an office at the company, were arranged. The interview took 10 to 15 min to conduct. The master’s students, with the exception of two students, completed the survey on an individual basis and gave explanations in writing for their choices of alternative after a lecture in an accounting class in a master’s program. Two of the students had filled out the surveys on an earlier occasion. The respondents took part in the study anonymously. The rate of nonresponse regarding the master’s students’ sample equals 0%. Of the 21 CFOs approached, 15 agreed to participate in the study, so the rate of nonresponse for the CFO sample amounted to 29%. However, the longer the data collection progressed, the more difficult it was to gain the approached CFOs’ agreement to participate in the study.

The years of time spent as a CFO or in an equivalent position are used as a proxy for experience-related knowledge or knowledge content (see Bonner, 2008, for a discussion on the use of experience proxies). The arithmetic mean equals 12.7 years: The median value corresponds to 10 years, whereas the mode value for this distribution is 15 years. The extreme values are 5 years and 28 years. The CFO respondents have extensive experience and thus may be considered experts. In comparison, the master’s student respondents may be designated as novices. The total sample of experts and novices is denoted “subjects.”

The Questionnaire

It took on average 11.2 min (the median value equals 10 min) for the experts to complete the questionnaire. It took somewhat more time for the novices to fill out the questionnaire, because they also had to give reasons for their choices of alternatives in writing. The arithmetic mean equals 16.4 min, whereas the median value corresponds to 16 min.

The fourfold pattern of risk attitudes is the theoretical model with which the subjects’ performance is compared to determine the rationality of their choice. The brief interviews with the experts and the written comments by the novices serve as the basis for analyzing the rationale for their choices.

The Fourfold Pattern—Four Scenarios

The use of the fourfold pattern of risk attitudes as the theoretical model against which the subjects’ choices are assessed requires the translation of each of the patterns into equivalent and distinct accounting events. This translation is critical for the validity and reliability of the study, because it represents the main measurement instrument. According to Gibbins and Mason (1988), judgments, including decision making, may be influenced by the wording of the text. The wording of the scenarios was kept neutral, direct, and frugal. Simultaneously, the complexity and amplitude of the different scenarios were kept on an equal level.

The content of the scenarios refers to the accounting domain; more specifically, the focus is on operational, day-to-day tasks as opposed to strategic accounting tasks (cf. Kahneman et al., 2011). The subjects, in this case experts, were immediately able to relate to the content. In a real interview/survey situation, the subject must be able to grasp the scenario instantly; otherwise, he or she may consider the scenario not to be reliable. There is no second chance. A characteristic of the scenarios in terms of knowledge content is that no irrelevant information is included, and the scenarios were designed to provide diagnostic information with respect to prior probability (base rate).

In relation to each scenario, the respondent can choose between two options: Choice 1 and Choice 2. The scenarios are arranged according to the fourfold pattern.

High probability

1. Top-left cell (certainty effect, gains):

Scenario 1. Offer to participate in a lucrative oil exploration project. By a former business associate, Events After the Reporting Period, Inc., is offered 5% confidence for participating in a lucrative oil exploration project (chance = 10,000,000 SEK) at a completely negligible cost. The offer is the first of its kind that Events After the Reporting Period, Inc. receives. The likelihood that the oil exploration project will find oil has been estimated at 95%. The company accepts the offer. (1) As the company’s CFO, you shortly thereafter are offered to sell the 5% confidence participation for 425,000 SEK. (2) Alternatively, the company retains its 5% confidence participation. (Ignore tax, interest rate, and liquidity effects.)

2. Top-right cell (certainty effect, losses):

Scenario 2. Bad debts expense, Annual Report as per 31 December 20X4. As the CFO of the financially solid company Events After the Reporting Period, Inc., you are facing a situation of choice when it comes to the valuation of a bad debt related to the company’s customer Bad Debts, Inc. The customer, which operates in a highly profitable growth industry, is an average major customer, and the margin of the current deal is also average. The company Bad Debts, Inc. has liquidity problems owing to too rapid an expansion. The risk of loss in trade receivables of 1,200,000 SEK is 95%. As the CFO you are offered 80,000 SEK as full payment for bad debt of nominal 1,200,000 SEK. (1) If the proposed settlement is accepted, 80,000 SEK will be transferred no later than 14:00 on 31 December 20X4 to a bank account belonging to Events After the Reporting Period, Inc. (2) Alternatively, Events After the Reporting Period, Inc. awaits the settlement of the full amount of 1,200,000 SEK or, at least, a much better bargain. (Ignore tax, interest rate, and liquidity effects.)

Low probability

3. Bottom-left cell (possibility effect, gains):

Scenario 3. Uncertain outcome of a pending damages trial. Events After the Reporting Period, Inc. has sued a competitor in an action for damages and requires the defendant to pay 7,500,000 SEK as compensation for financial loss. The competitor is an average major competitor. Events After the Reporting Period, Inc. does not intend to make any public mark with reference to the liability case. As the company’s CFO, you discuss with the company’s legal representative as well as with the country’s top legal experts. The overall assessment is that the company will, with 5% probability, win the case. (1) The defendants have clearly indicated that they are willing to enter into a settlement agreement under which Events After the Reporting Period, Inc. receives 450,000 SEK from the respondents. (2) The alternative is to take the process further. (Ignore tax and liquidity effects and the costs of judicial proceedings.)

4. Bottom-right cell (possibility effect, losses):

Scenario 4. Offer to take out insurance. Events After the Reporting Period Inc. operates a development project that has market potential of 18,000,000 SEK (net of the discounted cash flow from the project is positive and amounts to 4,000,000 SEK). The probability that the development project will be a market success is high and is expected to reach 95%. The development project is based on a newly developed material that has unique properties. One drawback is that the production process involves a physical element of uncertainty that can completely destroy the project. Experts estimate that the risk factor amounts to 5%. (1) As the company’s CFO, you are offered an insurance policy that fully covers the uncertainty factor. The insurance company determines the premium to be 300,000 SEK. (2) The alternative is not to take out any insurance. (Ignore tax, interest rate, and liquidity effects.)

Results

Given that people’s decision making is influenced by subjective utility and subjective probability (Kahneman & Tversky, 1984), initial questions were raised as to whether experts tend to make economically rational choices within the field of accounting and if whether experts tend to make more economically rational choices than novices in accounting.

The Fourfold Pattern

Table 1 presents the relative frequency per scenario, per standard rational model of economics, and per prospect theory for the subjects. As evidenced by Table 1, the subjects tend to rely on the standard rational model of economics for Scenario 1 (oil exploration—instead of being risk averse over high-probability gains, they are risk seeking) and Scenario 3 (damages trial—instead of being risk seeking over low-probability gains, they are risk averse); that is, the subjects tend to be economically rational in Scenario 1 (oil exploration) and Scenario 3 (damages trial).

The Relative Frequency per Scenario, Standard Model, and Fourfold Pattern for the Accountants.

Expected value: Option 2 = reject unfavorable settlement = gain 50,000 SEK.

Expected value: Option 1 = accept settlement = gain 20,000 SEK.

Expected value: Option 1 = accept settlement = gain 75,000 SEK.

Expected value: Option 2 = reject unfavorable settlement = gain 110,000 SEK.

On the contrary, and from the viewpoint of the standard rational model of economics, the subjects tend to be less economically rational regarding Scenario 2 (bad debts—they are risk seeking over high-probability losses) and Scenario 4 (insurance—they are risk averse over low-probability losses). According to the prospect theory, the difference between, on one hand, Scenario 1 (oil exploration) and Scenario 3 (damages trial) and, on the other hand, Scenario 2 (bad debts) and Scenario 4 (insurance) is that the former describes gain prospects, whereas the latter depicts loss prospects. Hence, it seems that subjects tend to be better at dealing with prospect-gain situations than with prospect-loss situations.

If we split the subjects into the experts and the novices, can we discern any differences between the two categories of subjects in terms of decision making?

Compared with all the subjects (Table 1), the experts tend to make an even more subjective decision regarding Scenario 2 (bad debts). All the other relative frequencies in Table 2 (experts) seem to be consistent with the corresponding relative frequencies in Table 1 (subjects).

The Relative Frequency per Scenario, Standard Model, and Fourfold Pattern for the Experts.

As for the novices (Table 3), there seems to be correspondence between the relative frequencies in Table 3 and those in Table 1 (subjects), with the ostensive exception of Scenario 2 (bad debts) in that there is an even distribution of relative frequencies over Option 1 and Option 2 in Table 3 (novices).

The Relative Frequency per Scenario, Standard Model, and Fourfold Pattern for the Novices.

Reference Point

Evaluations, according to the prospect theory, are made relative to a reference point (Kahneman, 2012). An outcome that is better than the reference point is considered to be a gain, whereas an outcome below the reference point is seen as a loss. The term category refers to the argument or the rationale given for choosing one option.

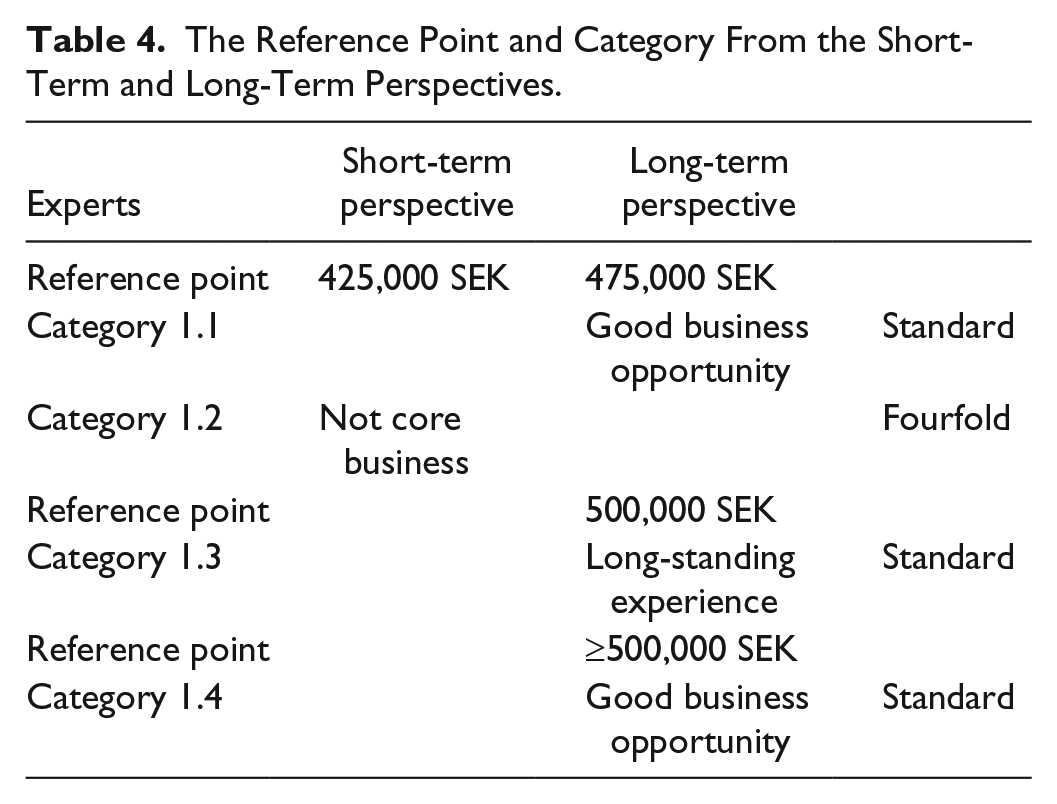

Reference Points Related to Scenario 1 (Oil Exploration)—Experts’ Perspective

Almost every expert chose Option 2 (reject unfavorable settlement) or the option according to the standard model. Just one expert opted for Option 1 (accept unfavorable settlement) or the fourfold pattern on the justification that the project “does not belong to the core business” (see Table 4). The rest of the experts took a long-term perspective on the stake in the oil exploration project. One expert referred to his or her long-standing experience as a CFO, whereas another expert calculated the expected value before he or she made a decision. The remaining experts recognized the stake in the oil exploration project as a good business opportunity, overlooking the expected value. A long-term perspective implies that the expert considers that the oil project holds a potential financial upside, whereas short-term perspective indicates that the expert is looking for quick closure.

The Reference Point and Category From the Short-Term and Long-Term Perspectives.

Reference Points Related to Scenario 1 (Oil Exploration)—Novices’ Perspective

None of the novices calculated the expected value; that is, they did not take full advantage of the information presented in the scenario. However, very few of the novices made the choice (quick profit) anticipated by the fourfold pattern (see Table 5); in this scenario, to accept an unfavorable settlement, 86% of the novices chose to reject the unfavorable settlement without first calculating the expected value. About half of the novices took a short-term perspective, whereas the other half assumed a long-term perspective, when dealing with the given task. In comparison with the experts, the novices adopted a shorter profit opportunity view of the business outlined in Scenario 2 (oil exploration).

The Reference Point and Category From the Short-Term and Long-Term Perspectives.

Reference Points Related to Scenario 2 (Bad Debts)—Experts’ Perspective

The situation outlined in Scenario 2 (bad debts) is an example of the sunk-cost fallacy, whereby the choice is between a sure loss and an unfavorable gamble (Kahneman, 2012). According to the standard or the rational-agent model, a rational decision maker considers only the future consequences of the present situation.

Most experts (87%) decided along the line depicted by the fourfold pattern and rejected the favorable settlement (see Table 6). Just two experts chose according to the standard model.

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

One expert realized that this is a sunk-cost situation but, despite this insight, argued that “at the same time, doing business is to find a solution, a payment plan. Maybe we have had a long business relationship.”

Those experts who chose to reject the favorable settlement seemed to think that, even if the settlement amount would be doubled or tripled, they would reject the settlement. The settlement amount was just too small. The experts gave different reasons for their rejection of the settlement amount. Some reasoned from how they deal formally with expected bad debt losses (accountancy-based view), whereas others referred to company rules and policies (rule-based view) or how large companies manage expected bad debt losses (large-company perspective). Yet other experts mentioned that the company has great potential in a growing market (growth company in a profitable industry) or referred to their own experience (long-standing experience). Finally, one expert just stated that the settlement amount was too small (waiting for a better deal). This may be considered as a residual category when it concerns the experts’ rational preferences.

Reference Points Related to Scenario 2 (Bad Debts)—Novices’ Perspective

Compared with the experts (Table 6), the novices (Table 7) made use of fewer categories when giving a reason for their choice of options related to Scenario 2 (bad debts). The most common categories were sunk cost and waiting for a better deal. 1 Category 2.1 (sunk cost) is split into two (reference point = 0 SEK and reference point = 60,000 SEK); whereas the former encompasses novices (80%) who reasoned and came to a rational decision without calculating the expected value, the latter includes students (20%) who reasoned and reached a rational decision based on the expected value.

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

In Table 7, the experience-related categories (business relationship, rule-based view, large-company perspective, and long-standing experience) are conspicuous by their absence and largely covered by the categories sunk cost and waiting for a better deal.

Relative to the experts, the novices tended to base their reasoning on what they have learned in their academic training. On the contrary, the experts tended to reason from their experience.

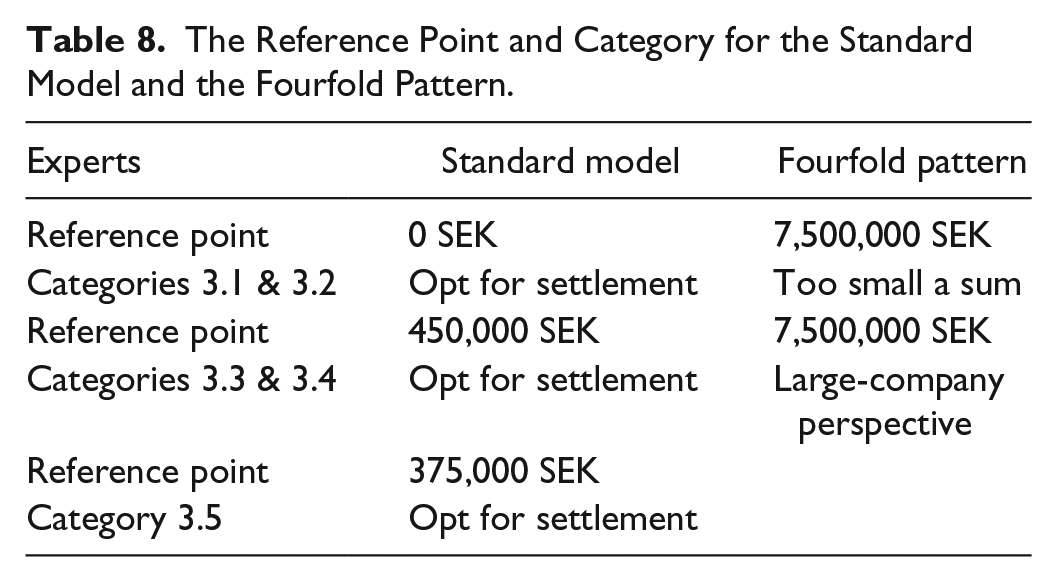

Reference Points Related to Scenario 3 (Damages Trial)—Experts’ Perspective

The information that the respondent should ignore, not just tax and liquidity effects but also the costs of judicial proceedings, is given in Scenario 3. Without this information, the reference point could actually assume substantial negative values. However, a few experts did not take notice of this information and involved costs of judicial proceedings in their reasoning. Most experts (73%) accepted the favorable settlement but from somewhat different perspectives. Just one expert computed the expected value (375,000 SEK), and, based on this value, he or she opted for settlement (see Table 8). The large majority of the experts opting for settlement (Category 3.3) referred to difficulties concerning judicial processes. These experts referred to their experience, while a few experts estimated the expected value intuitively, and, based on that estimation (Category 3.1), they opted for a settlement. With the exception of one expert, the small minority of experts who rejected the favorable settlement (Category 3.2) regarded the settlement amount as far too small to be considered. Finally, one expert took the large-company perspective (Category 3.4).

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

Reference Points Related to Scenario 3 (Damages Trial)—Novices’ Perspective

Contrary to the majority of the experts, who chose the experience-based Category 3.3, the majority of the novices chose Category 3.1 (see Table 9). These novices, realizing that the possibility of winning the case was slim, considered the settlement to be a favorable one (Category 3.1). Similar to the experts, just one novice calculated the expected value and opted for the settlement (Category 3.5). While most of the experts set out from an experience-based view, perceived the settlement institute as a mechanism for conflict solutions, and opted for settlement (Category 3.3), just one novice chose this category. The novices tended to accept the settlement after recognizing the low probability of winning the case but without computing the expected value (Category 3.1). The experts, on the contrary, tended to accept the settlement based on their experience and knowledge of judicial proceedings (Category 3.3). A small minority (14%) rejected the favorable settlement (Category 3.2 and Category 3.6). The difference between Category 3.2 and Category 3.6 is that the intention behind the former is to conclude the legal proceedings while the latter aims to pursue the process to gain a better settlement.

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

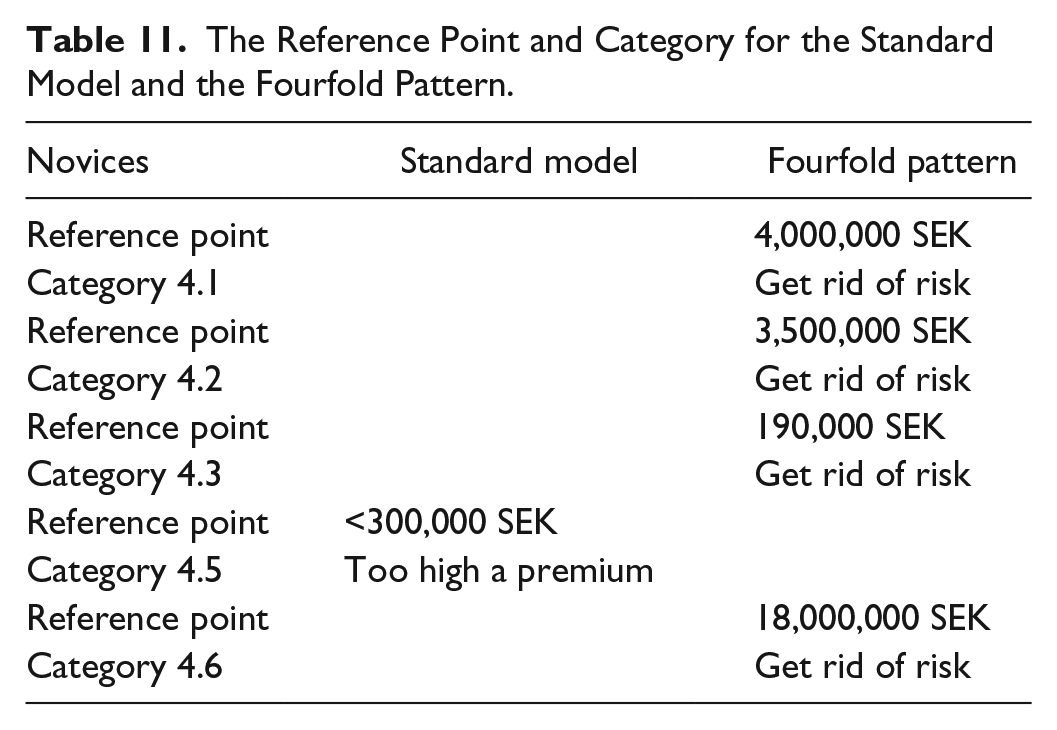

Reference Points Related to Scenario 4 (Insurance)—Experts’ Perspective

The most common category (see Table 10) related to the fourfold pattern (take out insurance) was “get rid of risk” (87%), and the most frequent subcategories within “get rid of risk” were Category 4.1 and Category 4.2; that is, the experts referred to 4,000,000 SEK (discounted cash flow from the project) or to 3,500,000 SEK (also considering the market potential of the project and the insurance premium). Remarkably, all of these experts made estimates, none made explicit calculations, and many did not take advantage of all the information provided. The focus was on safeguarding the net cash flow from the project. Just a few experts within “get rid of risk” took a different perspective (Category 4.3), because they were mostly focused on the cost of the premium from an expected-value perspective. Even though they considered the premium to be expensive, they opted for the insurance all the same.

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

On the contrary, a few experts estimated the return of the project and considered the insurance premium to be too expensive. They regarded the project as a business opportunity and, as such, subjected to uncertainty that has to be dealt with in business terms.

Reference Points Related to Scenario 4 (Insurance)—Novices’ Perspective

There is similarity regarding the category “get rid of risk” between the experts and the novices. Most of the novices referred to the discounted net cash flow of the project when considering safeguarding the project. In a similar vein to the experts, most of the novices based their opinions on estimates.

Categories 4.1 to 4.3 (see Table 11) produced a similar pattern across experts and novices. However, a few novices (Category 4.6) referred to the revenue (18,000,000 SEK) of the project instead of the net discounted cash flow (4,000,000 SEK).

The Reference Point and Category for the Standard Model and the Fourfold Pattern.

The experts’ “business opportunity” category is represented by the novices’ “too high a premium” category. The difference between the experts and the novices in this respect is that the former focused on the return of the project while the latter emphasized that the insurance premium was too high. Similar to the experts, the majority of the novices did not explicitly make use of all the available information, and their choices seem to have been based on estimations, not calculations.

Discussion and Analysis

Given that the expected utility is the right way to make economic decisions (cf. Thaler, 2015; Von Neumann & Morgenstern, 1953), the studied subjects tended to be semirational judgment and decision makers in that they had bounded rationality (cf. Simon, 1972, 1979).

As evidenced by Table 1, the subjects tended to be better at dealing with prospect-gain situations (Scenario 1 and Scenario 3) than with prospect-loss situations (Scenario 2 and Scenario 4). This finding parallels the findings of the prospect theory that losses and disadvantages have a greater impact on preferences than gains and advantages (Kahneman, 2002; Kahneman, Knetsch, & Thaler, 1991; Tversky & Kahneman, 1992). This indicates that, despite the subjects’ experience and training in logic, due care, and professional objectivity, they tended, at least to some extent, to be influenced by emotions.

Each scenario (Scenarios 1-4) is framed as a risk situation, in which the risks are weighed against two choices: on one hand, a certain outcome in that a settlement/agreement can be reached, and, on the other, an uncertain outcome due to a settlement/agreement that has not been reached. Mousavi and Gigerenzer (2014) extend uncertainty to situations in which some of the alternatives and outcomes, besides probabilities, can be unknown. This mirrors the uncertainty options in the presented scenarios. Furthermore, the nature of decisions made in the everyday world of business (like those in the scenarios) resembles decisions under uncertainty more than decisions under risk (cf. Knight, 1921; Mousavi & Gigerenzer, 2014).

According to Knight (1921), business profit is achieved through mastering decisions under uncertainty. In addition, to master decisions under uncertainty, managers have to become entrepreneurs. Scenario 2 (bad debts) is an instance of the sunk-cost fallacy. The subjects tended to opt for rejecting the suggested agreement. Hence, they chose the uncertainty option. From a standard model perspective, this decision is not economically rational. That is, in this instance, the subjects should adopt an entrepreneurial role. Regarding Scenario 4 (insurance), Kahneman (2012) emphasizes that, when individuals purchase insurance, they purchase more than coverage against improbable calamity; they also “. . . eliminate a worry and purchase peace of mind” (p. 318). The subjects tended to opt for the safe option instead of the uncertain option, which is the correct option from an economic rationality point of view. That is, in this case, the subjects should preferably assume the role of an entrepreneur. Hence, the implication of uncertainty is context dependent (cf. Shapira, 1995; Wang & Johnston, 1995). The subjects must also have excellent discernment ability in that they have to know in which specific situations they have to assume an entrepreneurial role.

Reference Points and Assessments

There can be many reference points and different aspiration levels due to, for example, exogenous effects (Shapira, 1995). Setting out from Knight (1921), Mousavi and Gigerenzer (2014) discuss decisions under risk versus uncertainty in terms of the nature of the unknown, Knightian probability, decision process, method, and generated knowledge. From the formulated scenarios, the Knightian probabilities a priori (designed) probability and estimated (based on opinion, not fully reasoned) probability are relevant to the discussion. The probabilities presented in the scenarios are a priori or designed probabilities, which are linked to risk, deductive reasoning, optimization, and the generation of deterministic knowledge (Mousavi & Gigerenzer, 2014). On the contrary, estimated or not fully reasoned probability is associated with uncertainty, heuristic, and satisficing solutions and intuition (Mousavi & Gigerenzer, 2014). The designed probability, that is, the expected value, serves as a reference point against which Option 1 (risk avoidance) and Option 2 (risk seeking) are weighted.

From a decision theory perspective (the standard model), the scenarios are straightforward and frugal. Notwithstanding this, in most cases, the subjects interpreted the scenarios as instances of daily business problems.

Regarding Scenario 1 (oil exploration), Choice 1 (accept the agreement, risk avoidance) refers to a short-term perspective, whereas Choice 2 (reject the agreement, risk seeking) is attributable to a long-term perspective. The scenario does not include information about whether the company is above or below the average (cf. Shapira, 1995). Some experts made the assumption that the company is well above the average; that is, the company has no liquidity shortage. The reference point is then linked to good business opportunities and long-standing experience (reject the agreement, risk seeking), which implies a reference starting point at 475,000 SEK. Another aspect is that not only the performance target is important but also the strategy (cf. March & Shapira, 1987; Shapira, 1995). An argument for accepting the agreement (risk avoidance) is that the transaction does not fit within the company’s core business, which, in this case, sets the reference point at 425,000 SEK.

Scenario 2 (bad debts) is an instance of sunk costs. The information is provided that the company is well above the average in financial terms. Some subjects used this information as a basis for adopting a long-term, risk-seeking perspective (Choice 2, reject the agreement). As regards the Knightian probability, the subjects applied deductive reasoning (calculating the expected value) as well as estimating in terms of heuristics, reason, and experience to identify the sunk-cost situation—Choice 1, risk avoidance (cf. Mousavi & Gigerenzer, 2014). Regarding rejecting the agreement, risk seeking (Choice 2), mental accounting may have an indirect, underlying implication for those subjects who set the reference point at 1,200,000 SEK (Categories 2.4-2.8) and a direct implication for Category 2.9 (waiting for a better deal; reference point equals 1,200,000 SEK). The subjects opting for Choice 2 do seem to have treated the issue at hand as unique, ignoring the statistics of the past (cf. Kahneman, 2012; Kahneman & Lovallo, 1993).

Notwithstanding the a priori designed probability structure of Scenario 3 (damages trial), just two subjects calculated the expected value (reference point equals 375,000 SEK; cf. Gigerenzer, 2014). Based on estimation, the vast majority concluded that the chance of winning was too slim (accept the agreement, risk avoidance). The experts tended to refer to their experience, whereas the novices tended to apply common-sense reasoning. This is in line with March and Shapira (1987), who conclude that risk can be understood better in terms of money to lose than a probability concept.

Of those who chose to reject the agreement (Choice 2, risk seeking), some focused their attention on what they considered to be too small a sum (reference point equals 7,500,000 SEK), whereas others tried to gain advantages by temporarily stalling the arbitration process (reference point >450,000 SEK). Among the former, a mental account seemed to come into play (cf. Kahneman, 2012; Thaler, 2015).

Two distinguishing features of Scenario 3 are that references were made neither to performance targets or strategy (cf. March & Shapira, 1987; Shapira, 1995) nor to whether the company is operating above or below average (Shapira, 1995). The focus was on the judicial process.

One result of the possibility effect is that individuals tend to overweigh small risks, and, as a consequence, they seem to pay excessive insurance premiums (Kahneman, 2012). Scenario 4 (insurance) is a case in point of the possibility effect. Just a few subjects calculated the expected value; the vast majority made a more or less advanced estimate (cf. Mousavi & Gigerenzer, 2014). The subjects seem to have made a mental accounting projection of the development project as one that is potentially profitable and in need of protection (cf. Thaler, 2015). An important aim is to eliminate risk. The estimate of the return may be seen as an indirect reference to a performance target or a performance requirement (cf. March & Shapira, 1987; Shapira, 1995). The choice of reference point depends on the measurement of the return is chosen. The development project tended to be considered profitable, and no reference was made to whether the company was running above or below the average (Shapira, 1995).

The standard model favors risk seeking in this case. The business opportunity argument may be perceived to be in line with the Knightian view of how to generate economic profit (cf. Knight, 1921).

Conclusion

This article presents the results of one experiment. To continue to improve our understanding of experts’ and novices’ perception of rationality, a great number of experiments as well as empirical studies need to be conducted. The subjects seemed to be more rational when dealing with risk and uncertainty related to gains than when dealing with risk and uncertainty associated with losses (cf., March & Shapira, 1987).

Furthermore, the novices tended to deal with the sunk-cost fallacy in a more economically rational way than the experts (cf. Bonner, 2008; Kahneman, 2012).

From a standard model point of view, mental accounting should not be that important in accounting JDM, but sometimes subjects seem to frame the scenario/issue at hand in mental-accounting terms (cf. Thaler, 2015). The reference point seems to be dependent on how the subjects frame the scenario/issue at hand (cf. March & Shapira, 1987; Shapira, 1995; Wang & Johnston, 1995).

As regards Knightian probability, just a few subjects calculated the expected value, that is, a priori or designed probability measurement. The vast majority of the subjects made some estimates based on reasoning, experience, examples, accounting rules and principles, company policy, heuristics, and so on (cf. Mousavi & Gigerenzer, 2014).

It appears that the judicial process takes the upper hand over business reasoning, such as the examples in Scenario 3 (damages trial). References were made neither to performance targets nor to whether the company is operating above or below the average (cf. Lopes, 1987; March & Shapira, 1987; Shapira, 1995).

To strike a balance between the perception of economic rationality and the complexity of real-world business affairs, it may seem that both experts and novices must continue to improve their economic understanding of rational choices in everyday business life. Brynjolfsson and McAfee (2014) assert that systems that execute human-like feats of reasoning will significantly reshape the way in which work is carried out (see also Domingos, 2015; Ford, 2015). Hence, subjects may have to improve constantly to be able to assert themselves against, for example, new forms of digitalized judgment and decision systems (cf. Kahneman et al., 2011).

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was financed by Handelsbanken’s Research Foundations (No. P2010-0039:1) and by Torsten Söderberg’s Foundation (2013, R6/13).