Abstract

This article is an attempt to assess the business relations between the tourism sector and suppliers of various types of business services. It focuses on knowledge-intensive business services (KIBS). The reasons why tourism businesses purchase outsourced services are also discussed. An Internet survey was conducted and the results were used to calculate and discuss a number of indices. Cross-tabulation statistics are used to assess the interrelation between types of tourist firms, their localization and size, and the types and number of services they use. The largest numbers of KIBS used by the Polish tourism sector are from the accounting, IT, and advertising sectors, whereas the smallest relate to research and experimental development in the social sciences and humanities. This article fills a gap in the knowledge about usage of KIBS services by the tourism sector at the national level.

Introduction

In recent years, the tourist market has become extremely competitive (Gonzalez, Llopis, & Gasco, 2011; Su, Cheng, & Huang, 2011). Reaching and sustaining a strong market position requires that an enterprise possesses a wise and long-term strategy. An important part of this strategy is the decision as to which aspects of the enterprise should be self-sufficient, and for which aspects it can purchase goods or services from other firms (Gonzalez et al., 2011; Manzin & Kodrič, 2009). Insufficient research has been conducted on the subject of purchase by tourism companies of other, knowledge-based services. In every destination, the tourism industry works to improve its position by launching innovative products and applying innovation in marketing (Bieger, 2005; Kozak, 2014; Prats, Guia, & Molina, 2008). The in-house potential of individual companies (people, information, knowledge, procedures, and financial resources), especially micro and small tourism enterprises (MSTE), is often insufficient for them to do this independently. Cooperation with knowledge-intensive business services (KIBS) providers, which offer external specialization and expertise, can bring strong support in generating new concepts and solutions. There have been studies that focus on the activities of KIBS providers on the market (Aslesen & Isaksen, 2007; Simmie & Strambach, 2006; Strambach, 2008; Wong & He, 2005), but there are none showing how these services are used by tourism enterprises. What is new in the approach adopted in this study is the insight from the angle of the tourism industry into the types of KIBS that are bought and how often. Outsourcing activities in tourism have been studied, but only in respect of their relationship with the hospitality industry and outsourcing within this segment (Barrows & Giannakopoulos, 2006; Espino-Rodríguez & Gil-Padilla, 2005; Espino-Rodríguez &Padrón-Robaina, 2005; Lam & Han, 2005; Lamminmaki, 2005; Shang, Hung, & Wang, 2008). This approach narrows down the subject and does not give the full picture of the different types of services purchased by the tourism industry. This article is an attempt to assess the scope and directions of purchasing of professional services by the tourism sector. For that reason, the aim of the study was to focus on the kinds of services that are most frequently purchased by tourism firms, and on the ways in which the profiles of particular companies influence their purchasing decisions. The research presented in this article was conducted as a project financed by a National Science Centre grant. Attention was focused on KIBS as a significant factor in strengthening the market position of the purchasing enterprise.

Literature Review

Outsourcing as the Conceptual Basis for the Study

The term outsourcing is a combination of the words “outside” and “resource” and “using” (Wullenkord, 2005, p. 3). All tourism companies have to take decisions as to whether to make or buy particular resources. Outsourcing is strictly connected with these decisions (Mikkola, 2003, p. 443). An outsourcing-focused orientation is connected with a drive for greater efficiencies and maximization of cost reductions. These objectives lead enterprises to outsource processes that were traditionally performed in-house. In the case of tourism companies, which are mostly MSTE, the most important stimulus [for purchase of KIBS] could be the lack of employees qualified or competent to do certain kinds of tasks (or a volume of work so small as to make employee training in a given area financially unviable). Tourism companies need to compete with others on the market on new ideas and products (services), but at the same time on price. Solutions that meet these criteria can be offered by suppliers of KIBS.

Two theoretical frameworks—transaction cost economics (TCE) and resource-based view (RBV)—may be applied to understand the outsourcing decisions taken by the managers of tourism companies. Both of them have some limitations (McIvor, 2010, p. 73), but it is worth discussing them briefly in the context of the development of tourism companies. According to the TCE theory, there are certain conditions in which an enterprise should manage economic exchange both internally and externally (manage the barriers and create suitable conditions for both types of exchange). In this approach, the characteristics of the transaction determine what creates the most efficient governance structure for the organization—the market, hierarchy, or alliance (McIvor, 2009; Williamson, 1975). The key factors influencing transactional difficulties include elements such as bounded rationality, opportunism, small numbers bargaining, and information impactedness (McIvor, 2009). For tourism enterprises, the exchange is mostly restricted to the immediate environment—that is, micro and small firms usually cooperate with local or regional partners (Borodako, 2011). The decisions involved in the transaction are mostly related to sourcing and selecting cheap and high-quality services that can fill the gap in the area in which the tourism firm operates. For the outsourcing of KIBS services, this theoretical framework seems to be less applicable than the other, but it could of course form the conceptual basis for further analysis. In the alternative theory, the RBV, the organization is a unique bundle of assets and resources that can create competitive advantage if used in distinctive ways (Barney, 1991; Peteraf, 1993). According to this approach, resources and capabilities are treated as valuable if they allow an organization to exploit opportunities and counter threats in the competitive environment. They should also be considered as rarities (rarity criterion) relative to the number of competitors that possess such valuable resources. The key criterion for the creation of competitive advantage is imitability—the ease with which competitors on the tourism market can replicate the valuable and rare resources possessed by a given company. The last condition in this approach is proper organization—the enterprise must be organized in such a way as to enable it to exploit its resources and possibilities. The key aspect in both approaches is knowledge, which can be a key resource of the company and give it the competitive advantage. This knowledge can be bought from the market with the support of KIBS firms.

KIBS—Definition of the Category

There are many definitions of KIBS. One of the oldest, but still the most commonly used, says that they are services that involve economic activities which are intended to result in the creation, accumulation, and dissemination of knowledge (Miles et al., 1995). KIBS are also characterized as expert-based business-to-business services where knowledge plays an important role in both the delivery and the output of the service (Tuominen & Toivonen, 2011).

KIBS are confirmed by the existence of four “high” degrees: a high degree of knowledge, a high degree of technology, a high degree of interaction, and a high degree of innovation (Yang & Yan, 2010). Closer analysis of the above features permits the statement that KIBS are assumed—obviously—to represent a high degree of knowledge. This knowledge is not only related to codified knowledge but also to tacit knowledge, which is controlled by employees and agents, and whose generation, reproduction, and application are much more complex for enterprises to organize (Vence & Trigo, 2009). Of course, this is a subjective judgment, and it is very difficult to assess and prove that a service really is knowledge intensive. But, generally speaking, for a service to be both competitive and able to meet the needs of demanding contemporary clients, it has to be regularly updated, customized, and based on the newest accessible and affordable solutions, which usually requires deep knowledge. Deep knowledge is embodied in the team of employees of the service supplier, in respect of whom knowledge must be considered not only an important tool but also the core of their final product. KIBS are “responsible for the combination of knowledge from different sources and for the distribution of knowledge itself” (Hipp & Grupp, 2005, p.518). All of the above conditions impose the necessity for the implementation of the highest level of accessible technology.

A high degree of interaction means that at each stage of a service preparation, there is close contact and cooperation between the firm ordering the service and the service supplier. Client–producer interaction has lately been the focus of attention in literature (Sundbo, 2000). Although it has been noted that KIBS providers are expected to demonstrate the strong intellectual capital of their personnel, it must be stressed that the client firm, in this case a tourism market firm, has the largest experience in its own market and a very deep knowledge of its microenvironment. Thus, consultations facilitating the exchange of information and points of view are necessary at each stage of the process of service creation, giving the opportunity for a synergy effect to occur. KIBS, therefore, develop their activities in direct contact with their clients and as such have a more intense level of interaction than enterprises in other service subsectors do. The ad hoc mode of innovation and high level of interface with clients in KIBS lead to the development of customized products (Vence & Trigo, 2009), which is very important in the tourism market.

The Role and Types of KIBS

Some studies (Müller & Zenker, 2001; Pardos, Gomez-Loscos, & Rubiera-Morollon, 2007) have pointed to KIBS as the driving force in innovation in the services sector. It must be stated that numerous studies have addressed the role of KIBS in customers’ innovation activities (e.g., Bessant & Rush, 1995; Miles, 1999) and in local and national innovation systems (e.g., Den Hertog & Bilderbeek, 2000; Kautonen, 2001). Thus, the role of KIBS in innovation systems may be summarized in three ways, as follows (Den Hertog, 2000; Miles, 1995):

innovation promoter;

innovation disseminator; and

innovation source.

Personnel qualification is considered a key element in the service innovation process (Sundbo & Gallouj, 2000). Consumption of the service usually brings about the improvement of the client company’s intellectual capital. KIBS have key characteristics instrumental to the rise of the knowledge-based economy (a fact which has a direct impact on tourism companies) and constitute one of the most dynamic elements of the service sector in many developed countries (Strambach, 2001).

There have been some attempts in the literature to classify KIBS. Some key examples of these might be Miles et al. (1995); Wong and He (2005); Javalgi, Gross, Joseph, and Granot (2011); and National Science Board (1995). On the basis of these papers and analysis of the tourism industry environment, an extended and modified classification has been proposed which incorporates a clear division into services focused on enterprise (mostly operational activities), market-oriented services delivered to the client firm, and last but not least, technical services (focused more on technology and related issues).

This classification (Table 1) has been extended to include professional services to tourism companies hosting or organizing events as part of business meetings (business travel). The two most important of these are event management services and technological (A/V) event support. Both are tourism industry specific and largely related to business travel. Due to the lack of empirical data, both these services were excluded from the analysis. But, further studies in this area should cover both types of services.

Types of KIBS.

Source. Own elaboration.

Note. KIBS = knowledge-intensive business services.

Method

A number of research questions were posed, the main one given as follows:

To answer this question it was necessary to find answers to three detailed questions:

What kinds of KIBS are generally preferred by the tourism sector in Poland in the process of improving innovativeness and competitiveness through cooperation?

What is the level of intensity of business relations between KIBS providers and tourism companies in Poland in 2012?

What features of tourism firms were most significant in the taking of the decision to cooperate with KIBS suppliers?

A questionnaire-based survey was conducted by email in March 2013 with the help of a special survey program, Remark Web Survey. Invitations to participate were sent to all Polish firms operating on the tourism market whose email addresses the authors were able to collect (a total of 5,100). These entities represented a range of different segments of the tourism supplier market: various types of accommodation, restaurants, and tourist agents and offices. Of this sample, 417 emails were returned with the information that the company had wound up its operations or suspended them for the low season. A further 234 emails returned with reports of delivery problems (wrong address, problem with server, etc.). The total number of firms to which the invitation was delivered was 4,449. A total of 173 firms sent the completed questionnaire back. Such a low response level (3.89%) is a result of several factors. The first is the use of an email-based survey program, which has certain disadvantages in terms of communication with recipients, including the lack of personal contact, which likely renders it less binding (Jin, 2011). However, this solution allowed the research team to contact thousands of companies in the country at significantly lower cost, in a shorter time and with the possibility of direct feedback about the respondents’ comments and remarks, which was the key asset of this tool. The relatively moderate response rate also reveals the reluctance of Polish tourism enterprises to participate in research. Another reason for the low response rate, which was impossible to verify prior to the study, is the large proportion of microenterprises in the survey sample. This fact is of indirect consequence for a further aspect: the timing of the survey. The questionnaire was sent out after the end of the winter season but before the beginning of the summer season, which meant that a large percentage of the firms selected for participation had suspended their activities (a large number of autorespond answers received—more than 400—stated that the business in question was suspended). In light of this fact, the number of completed questionnaires was treated as sufficient, the more so that international journals do publish studies based on comparable rates of return (Kalliny & Ghanem, 2009; Pelletier, 2007). Poland was selected for the study due to the fact that this was the market of which the authors of the article had the best understanding, and also in view of the dynamic development of tourism there in recent years. The research was funded by a National Science Center grant pursuant to decision DEC-2011/01/D/HS4/03983.

Various indices were calculated: the percentage of enterprises using outsourcing of specified types of KIBS, the average number of services purchased by tourism sector enterprises based on numbers of paid invoices, and the index of the scope of KIBS usage by the tourism sector. Cross tabulation of the statistics was conducted to assess the interrelation between type of tourism firm, localization, size, and type and number of services used.

Sample Description

The structure of the sample is presented in Table 2. In terms of market segment, nearly 60% of participants were accommodation venues, while more than one tenth were restaurants, and a further tenth were tourism offices. The shares of the remaining subsectors amounted to only a few percentage.

Sample Description.

Source. Own elaboration.

In terms of the size of the surveyed firms, participants were mainly microenterprises with fewer than 9 employees. More than one fifth of the sample were small firms, employing 10 to 49 people. In terms of market experience, the sample was divided almost equally (about 20%) between the various age brackets of the businesses, although the youngest firms (less than 2 years old) accounted for roughly 7 percentage points more than any of the others (about 27%).

More than 60% of questionnaires were completed by the owner/co-owner of the firm, which reveals their involvement. This is further confirmed by the fact that nearly a quarter of the questionnaires were completed by managers, more than one fifth by chairmen, and more than 16% by directors.

Results

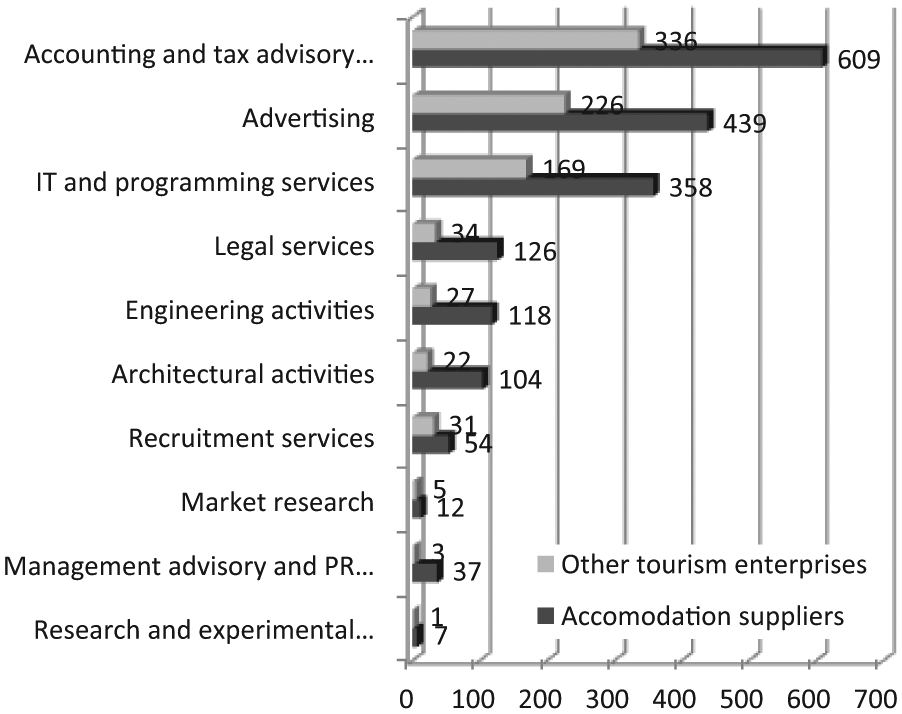

To assess the scope of the services outsourced by the tourism sector from KIBS providers in Poland, a number of indices were used. The first was the percentage of enterprises surveyed that were using specified types of KIBS in 2012. The results revealed that the three groups of services that were most commonly outsourced were in the following areas (Figure 1): 86% of all the enterprises surveyed used advertising services (of that figure, 52% were accommodation entities), 80% used IT and programming services (48% of that number were accommodation entities), and 71% accounting and tax advisory services (42% of that number were accommodation entities). Forty percent of enterprises outsource engineering services and architectural services, and nearly one-third legal services. In 2012, a quarter of the firms surveyed used outside management advisory and PR services, and one-fifth recruitment services. Market research services and research and development services were used very rarely in the surveyed sample—by less than one fifth of firms.

Percentage of surveyed tourism enterprises (accommodation and others) that outsourced KIBS in 2012.

The second index calculated was the average number of services outsourced by tourism sector enterprises in 2012. The results show that in the case of accommodation venues in 2012, the surveyed firms ordered on average about three services from the accounting and tax advisory segment (2.9), more than three services within advertising, and about three IT and programming services (2.8). There is a difference between accommodation providers and non-accommodation firms. Compared with other firms (non-accommodation entities), accommodation businesses had a higher average number of invoices per year for accounting and tax advisory services, and IT and programming services. Legal, engineering, and architectural services were used on average once a year. Once the above results were established, attention was focused on the frequency of use of the most commonly used services in the sample. Thus, the data for accounting and tax advisory services (Table 3) show that 64% of the accommodation firms surveyed bought such services 12 times a year (in 2012), while 11% had used services in this category only once in the past year. Of “other” businesses, 57% used them once a month, and 15% just once a year.

Frequency and Percentage of Enterprises Outsourcing a Given Number of Services in 2012.

Source. Own calculations.

IT services were used in a different way. Twenty-two percent of the accommodation enterprises surveyed sought them once a year, and 18% twice. About 10% of firms used IT services 3, 4, and 5 times a year, respectively. Only a small percentage of firms used outsourced IT services more often than this. Very similar results were received in the case of non-accommodation firms—27% of them had used services from this category twice a year and 15% only once. For this kind of service, we did not observe any significant incidence of payment 12 times a year (once a month).

Use of advertising services in the surveyed group followed a similar pattern to that of accounting and tax advisory services. In 2012, 22% of accommodation enterprises used them twice in the year, 14% 3 times, 11% cited 4, 5, and 10 invoices for that year. The results for other (non-accommodation) enterprises show that the most frequency with which invoices were paid was 3 times a year (20%), and in the next positions were 10 payments per year (15%) and 1 per year (13%). Only a small percentage of the researched subpopulation bought external advertising services more often and more frequently.

The index of KIBS outsourcing by the tourism sector was calculated as the cumulative number of service types outsourced by selected tourism subsectors (see Figure 2).

Index of scope of KIBS outsourced by tourism subsectors.

The results prove that the most widely used services in the survey sample were accounting and tax advisory services, followed by advertising services, and in third place IT and programming services, both by the accommodation sector and by other tourism enterprises.

The next research question was as follows:

To answer this question, cross-tabulation analysis of the statistics was conducted. Only statistically significant results (p≤ .05) were presented, as verified by the Pearson chi-square test, which is the most common test for significance of the relationship between categorical variables, allowing us to compute the expected frequencies in a two-way table.

The results, shown in Table 4, reveal some statistically significant relationships between specific features of enterprises and their KIBS use. One statistically significant feature was the size of the enterprise and its use of legal services (p = .00005, Cramer’s V = 0.3629301). As has been already mentioned, legal services are not very widely used by the tourism sector (only a quarter of the enterprises surveyed used them). However, a certain relationship may be observed: In 2012, microenterprises tended to use legal services only once or twice, whereas small and medium-sized enterprises more often used them 3 or more times (32.43% of the small and medium-sized tourist enterprises in the sample used this category of KIBS 3 or more times).

Results of Cross-Tabulation Analysis.

Source. Own elaboration.

The relationship between the size of an enterprise and its use of IT and programming services was also statistically significant in the surveyed sample (p = .01624, Cramer’s V = 0.2610752). It was observed that the share of tourism microenterprises outsourcing one or two IT and programming services per year was much higher (36%) than the share of those using three to four services (14%), or five or more services (24%). The relationship between the size of the tourism enterprise and its use of architectural services also appeared to be statistically significant (p = .00667). The results suggest that small and medium-sized firms use architectural services more frequently than once a year.

There was also a statistically significant relationship between the status of the person completing the questionnaire and the company’s use of legal services (p = .049, Cramer’s V = 0.1993368), and both the position within the company and the status of the person completing the questionnaire and the company’s use of IT services, though this was not a particularly important relationship in terms of the analysis.

Discussion and Conclusion

The results reveal that the scope of KIBS outsourced by the surveyed Polish tourism enterprises in 2012 was not very wide. This statement is based on the value of the indices calculated. Polish firms mainly outsource three types of services: accounting and tax advisory services, advertising services, and IT and programming services. In fact, this is in line with results of other studies showing that these are also the most commonly outsourced services in other countries (Chatzoglou & Sarigiannidis, 2009; Espino-Rodríguez, Lai, & Baum, 2008).

The patterns of use of the above-mentioned services by Polish tourism enterprises in 2012 differ: outsourced accounting services were used systematically, every month, while the other two types of services were sought only occasionally. It may be supposed that these firms used advertising, IT, and programming services to solve a particular problem or achieve an operational goal. This is in accordance with the transaction cost theory (Coase, 1988; Espino-Rodríguez & Gil-Padilla, 2005; Espino-Rodríguez & Padrón-Robaina, 2005; Williamson, 1998) and the resource-based theory, specifically the RBV (Barney, 1991). It must be taken into consideration that the macroeconomic conditions in 2012 were more difficult for the Polish tourism sector than those in previous years, and the results obtained reveal a tendency typical for a period of slowdown in the economy. It may be assumed that the lean management strategy (Arnheiter & Maleyeff, 2005) was implemented by the surveyed firms. It has been proved that economic slowdown affects the prioritization of goals and investments (Millar & Choi, 2011).

It should be stressed that aside from the three types of services mentioned, other KIBS services were outsourced on average very seldom, no more than once a year. The analysis of the accommodation and other tourism firms conducted shows a difference in the number of relations (expressed by the number of invoices paid per year) generated by these entities with KIBS suppliers.

Detailed insights into the outsourcing decisions of the Polish accommodation sector suggest that the level of outsourcing may be determined more by strategic decisions than simply by costs, which was also shown in other studies (e.g., Espino-Rodríguez & Gil-Padilla, 2005, Espino-Rodríguez &Padrón-Robaina, 2004), concerning the approach of hotels in the Canary Islands to Information System/ Information Technology (IS/IT) outsourcing).

The results seem to indicate that there was no sustainability of cooperation between Polish tourism enterprises and suppliers of services in these areas, at least in 2012. This somewhat contradicts the findings in the literature, which show that networks are a fundamental feature of services (Scott & Laws, 2010). This suggests that the surveyed Polish tourism enterprises have not yet reached the stage of the developed Western market, where firms are more open to external sources of innovation and cooperation (Laursen & Salter, 2006) in their creation of competitive advantage. As Chesbrough (2003) states, if restrictions on internal sources of innovation are too tight, it can reduce firms’ operating effectiveness. This is an important signal for KIBS suppliers—as a benchmark from Western markets—that the scope of cooperation should increase in the future and they should be more active in building relations and even establishing networks. There were few statistically significant relationships between particular features of tourism enterprises and their KIBS outsourcing patterns, so no features of enterprises determining KIBS usage were revealed; this was mainly determined by enterprise size. A relationship was proved between the size of an enterprise and the number of both IT and legal services it purchased externally. This confirms the pattern in other European countries of the influence of enterprise size on operating decisions (Tetteh & Burn, 2001).

An important finding of this study relevant to practitioners is the issue that there is demand among tourism enterprises on the Polish market for accounting and tax advisory services, advertising services, and IT and programming services. If suppliers are made aware of it, they can orient their activity and attempt to specialize in the tourism market.

Limitations and Future Research

The limitations of the results are the fact that the study focused only on 1 year, and the fact that a relatively small number of questionnaires were returned; this suggests that the results should be treated with some caution. This study was the first of its kind to be conducted in Eastern Europe. There is a need for further research into both the national and regional levels, with a higher level of enterprise participation in subsequent studies. The aim of future research should be to establish whether there will be a need for outsourcing in periods of economic acceleration and growth. The next step should be in-depth analysis of the relations between the tourism sector and service suppliers, and assessment of the effects of such outsourcing on both parties.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research and/or authorship of this article: This study was financed by a National Science Centre grant pursuant to decision DEC-2011/01/D/HS4/03983.