Abstract

Purpose

Fintech provides material capital for educational investment and holds practical significance for achieving equity in education.

Design/Approach/Methods

Drawing on the indexes of fintech development and educational inequality, this study uses a variety of methods such as fixed effect models to explore the influence of fintech on education equity.

Findings

Results show that fintech can significantly advance educational equity, particularly in regions with lower levels of educational input, educational output, and economic development. Mechanism analysis reveals that fintech facilitates the sharing of educational resources through the application of digital financial platforms. It also drives the development of information technologies for education by promoting the creation of new infrastructure. Fintech can strengthen niche marketing and increase the use of financial services to narrow the digital divide, thereby reducing educational inequality. Moreover, fintech indirectly addresses educational inequality by increasing household income, household consumption, and public education expenditure.

Originality/Value

In the pursuit of educational equity, the positive influence of fintech should be harnessed by increasing investments in new infrastructure creation, advancing fintech e-learning platforms, and promoting the equal distribution of educational resources.

Keywords

Introduction

Equality of educational opportunity, particularly educational equity, is a fundamental prerequisite for fostering individual initiative and a decisive factor in reducing income inequality (Youness & Hamzaoui, 2017; Yuan et al., 2022). The promotion of educational equity helps create an environment for fair and high-quality education, facilitating the overall development of individuals. Addressing the multifaceted and diverse needs of people across various social strata, this endeavor promotes collective material and spiritual prosperity while providing a robust foundation for the construction of an education power. In China, this concept is called “common prosperity,” and related policies aim to achieve a fair distribution of wealth and reduce the wealth gap.

In terms of cake theory, fintech plays an important role in increasing the size of the cake and dividing it. As a technology-driven financial innovation application, fintech uses emerging technologies—such as the Internet of Things (IoT), artificial intelligence, blockchain, cloud computing, and big data—for innovative applications in traditional financial fields, including payment, credit, and wealth management. Fintech can break through the bottleneck of unbalanced economic structure, industrial structure, and regional development, and improve high-quality economic development—thereby producing a “bigger cake.” Fintech can also promote the availability and utilization of resources to better “divide the cake.” Therefore, fully understanding the impact of fintech on education equity is key to building a powerful country in terms of education, science and technology, and talent.

Fintech significantly impacts household income consumption at the micro level and income distribution at the macro level. More specifically, at the micro level, with the adoption of the latest technologies such as big data and cloud computing, fintech can notably improve households’ business engagement, success probability, and entrepreneurial performance—increasing household income by promoting employment, especially nonagricultural employment (Zhang et al., 2019). Fintech also makes financial services more accessible and convenient and promotes the growth of household wealth and consumption upgrading. At the macro level, it improves the level and efficiency of allocating financial resources, which significantly promotes high-quality economic development and helps narrow the income gap between developed and underdeveloped regions and groups (Dupas & Robinson, 2013). However, little research has been conducted on the allocation of educational resources, especially with respect to its impact on educational equity, the digital divide, and its crowding-out effect.

While equity in education embodies the basic values of the modernization of education, markedly few studies have explored the influence of fintech on educational equity. Studies have tended to focus on the factors influencing educational equality, including those related to the family background (e.g., personal income and household registration), individual factors related to endowments (Cole et al., 2011; Dee, 2005; Lavy & Sand, 2018), as well as factors related to urban–rural differences and regional economic imbalances (Youness & Hamzaoui, 2017). Educational informatization also has a significant impact on educational equity. In this regard, Internet accessibility holds practical implications for promoting the sharing of educational resources, social integration, and educational equity (Biagi & Loi, 2013; Volman & van, 2001). Accordingly, advances in fintech significantly benefit regional education informatization, promoting the balanced development of regional education in four domains: the environment, resources, opportunities, and quality. However, despite the importance of fintech, few have quantitatively analyzed its influence or provided theoretical evidence regarding its influence mechanism.

This study addresses two gaps in the literature and presents policy suggestions based on its findings. First, it provides new empirical evidence on educational equity by exploring its relationship with fintech. Studies in this area have primarily focused on the qualitative analysis of individual endowments, distribution of educational resources, and family background. In a departure from this trend, this study examines the impact of the development of fintech on the allocation of educational resources based on the current level of education informationization, thus providing insights into educational equity from the perspective of the digital economy. Second, this study examines the influence mechanism of fintech on educational equity. While existing research has investigated the influence of fintech on income distribution, this study focuses on educational equity and explores the influence mechanism of fintech on household income expenditure, educational investment, and the digital divide. Third, based on the results of this comprehensive analysis, this study provides policy recommendations and potential solutions to promote educational equity using fintech and its related benefits.

Theoretical framework and hypotheses

Direct influence of fintech on educational equity

Improvement in the sharing of educational resources with digital financial platforms

Fintech plays a key role in achieving educational equity by promoting smart education, e-learning, and information technology for education. With the implementation of digital financial platforms, fintech offers a diverse environment for sharing educational resources and advancing new educational approaches such as smart teaching and experiential learning. It also provides a broader range of financial services to support basic education, with the introduction of fintech e-learning platforms driving both educational reform and innovative financial practices. Furthermore, fintech facilitates the construction of integrated digital financial platforms, offering a diverse and convenient environment for accessing out-of-school educational resources, thus promoting the effective sharing of educational resources.

Through digital financial applications, fintech provides inclusive financial services to low-income groups, thereby enhancing educational equity. Characterized by low transaction costs and wide accessibility, digital finance improves households’ access to formal credit. Fintech has a greater marginal effect on underdeveloped regions. Employing digital technologies such as big data and cloud computing, fintech offers targeted financial solutions to specific groups. In doing so, fintech can enable equal access to financial services for people in remote and less economically developed areas. It also reduces educational inequality by encouraging educational funds for less advantaged groups.

Advancing information technologies for education by promoting new infrastructure creation

The creation of new infrastructure is an effective pathway for advancing the digital transformation of education and the development of high-quality education. To promote education informationization, fintech offers various products like “smart campus” and “campus payments” to build a more mobile, digital, and intelligent educational ecosystem. Fintech also improves educational equity by promoting new infrastructure creation, education informationization, and the sharing of educational resources. The implementation of digital technologies such as IoT and cloud computing is conducive to educational digitalization and offers a solution to underdeveloped regions lacking high-quality teaching resources. In short, fintech has a significant spillover effect on the development of new infrastructure by improving the models and capabilities of financial services.

Reduction in the digital divide

The development of fintech has both advantages and disadvantages. On the one hand, it promotes inclusion, convenience, and efficiency, which is conducive to narrowing the digital divide. By expanding resource accessibility to less advantaged individuals, fintech has a stronger marginal effect on underdeveloped regions in terms of narrowing the digital divide and reducing educational inequality. On the other hand, the adoption of fintech imposes higher demands on infrastructure, financial ecosystems, and people's cognitive abilities, potentially resulting in larger regional disparities, service shortages, higher potential risks, and the uneven distribution of financial resources—leading to the so-called Matthew effect, whereby the rich get richer and the poor get poorer. As such, the digital divide not only compromises the economic well-being of individuals experiencing information poverty but exacerbates income disparities between different social strata, thereby widening the gap in educational investment and negatively impacting educational equity. Based on the foregoing, this study proposes the following hypothesis:

Indirect influence of fintech on educational equity

Increase in household income and consumption

The development of fintech significantly influences poverty reduction by increasing household income. Household income plays a critical role in promoting educational equity. Households face various types of constraints related to credit, information, and knowledge. Fintech can reduce such constraints by creating employment and business opportunities as well as increasing household income. Its influence on household income is particularly strong among those with low endowments. The advancement of fintech is also conducive to consumption upgrading with better consumption patterns and more experiential consumption. By providing more accessible and convenient financial services, fintech can increase property income and strengthen the risk management capabilities of households, further promoting total household spending and consumption upgrading in turn. Fintech has a particularly strong impact on advancing educational expenditure on human capital development (Chen et al., 2021), increasing equal opportunities and driving equity in education.

Increase in public education expenditure

Fintech can promote educational equity by increasing public education expenditure, particularly for underdeveloped areas. Public education expenditure is crucial for the allocation of educational resources, improvement of educational standards, and reduction in overall disparities in education. In addition, fintech can facilitate economic progress and stabilize regional fiscal revenues, which supports the development of local infrastructure in key sectors such as science, education, culture, and healthcare. In particular, the wide adoption of fintech aids the establishment of new financial service models, which can further support new infrastructure creation and increase investment and fiscal expenditure on education, thereby driving educational equity. Fintech also helps reduce uneven regional development by optimizing the allocation of educational resources across regions. The development of fintech improves the industrial structure of underdeveloped areas with higher economic and cultural standards as well as higher educational input. Moreover, it can drive digital transformation, thereby reducing inequality in education. Accordingly, this study proposes the following hypothesis:

Research methods

Data

This study utilized 2004–2019 fintech data as well as provincial and municipal statistics on education and households in China. Fintech data primarily comprise fintech-related keyword search results from Tianyancha, a Chinese business data and investigation platform (Song et al., 2021). Provincial and municipal statistics were obtained from the Wind economic database, which provides various types of data—including population education level, urban population ratio, and government expenditure on education—for 31 provinces and cities in China between 2004 and 2019. County-level data regarding the numbers of teachers and pupils in primary and junior high schools, the number of regular high schools, and the regional gross domestic product (GDP) per capita were obtained from the China Regional Economy Research Database in the China Stock Market and Accounting Research database.

Parameters and indices

This study measured inequality in education using the education Gini coefficient, which can be calculated using Equation 1:

Following Song et al.'s (2021) approach, this study measured the level of fintech development in a prefecture-level city using the number of fintech companies in that city. First, company registration information was obtained from the Tianyancha platform using the following keywords: “fintech,” “cloud computing,” “big data,” and “blockchain.” Query results containing these keywords in the company name or business scope were retained for analysis. To reduce inaccuracies caused by shell companies in the query results, companies that had been in operation for less than a year or had an abnormal operation status (e.g., suspension, dissolution, revocation) were excluded from the analysis.

Based on the business scopes of the sampled fintech companies and the classification of fintech business models by the Basel Committee on Banking Supervision, this study performed fuzzy regex matching on the fintech-related keywords (e.g., finance and clearing) within the business scopes. Matched samples were retained to calculate the number of fintech companies per year and the level of fintech development (Fintech) for prefecture-level cities and provinces. The Fintech index is the logarithm of the number of fintech companies per year, with a higher value reflecting a higher level of fintech development in the region.

Accordingly, in this study, the education Gini coefficient is calculated using Equation 2:

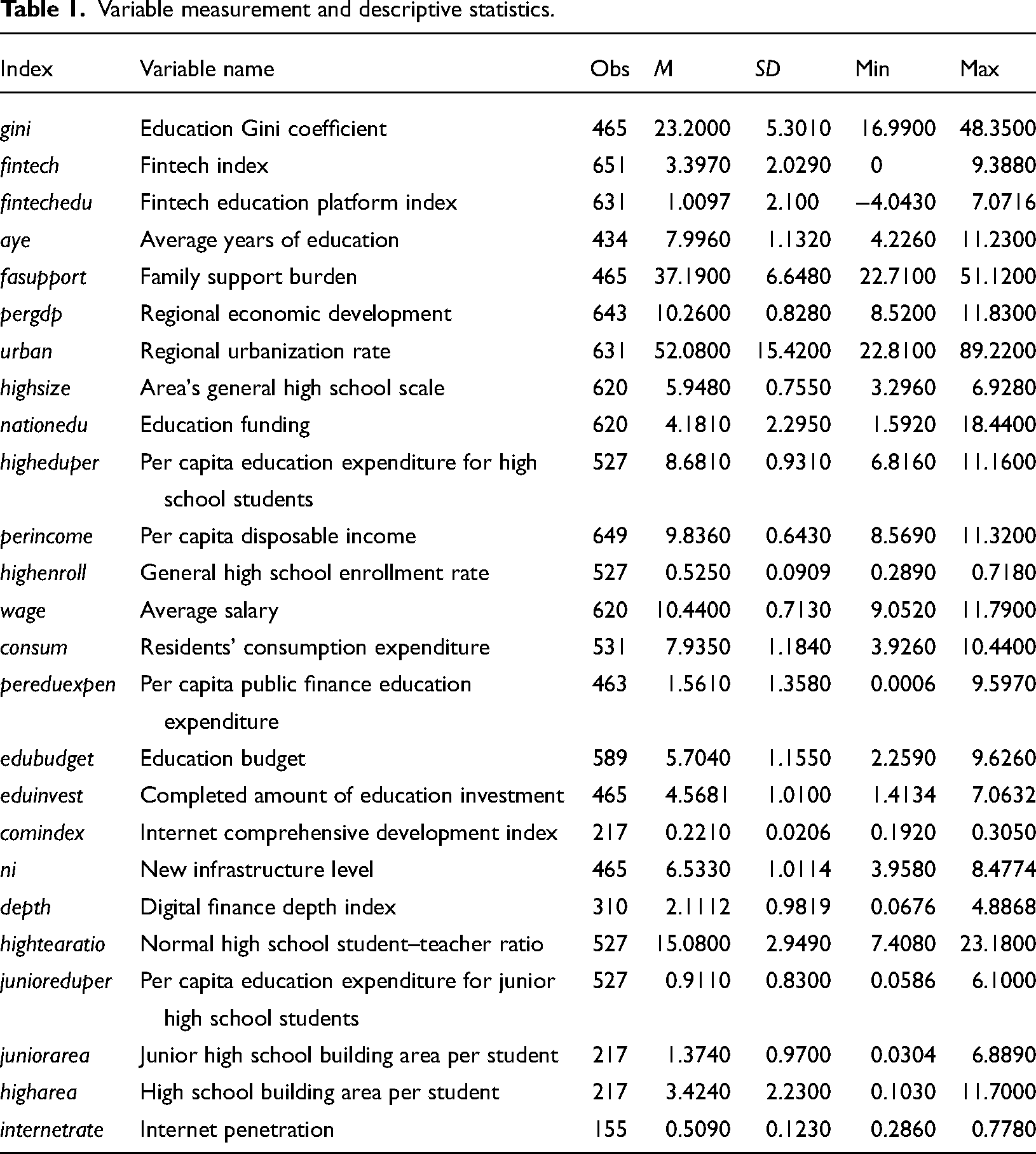

Table 1 presents the measurement and the descriptive statistics of the variables used in this study.

Variable measurement and descriptive statistics.

Impact of fintech on education equity

Benchmark test results

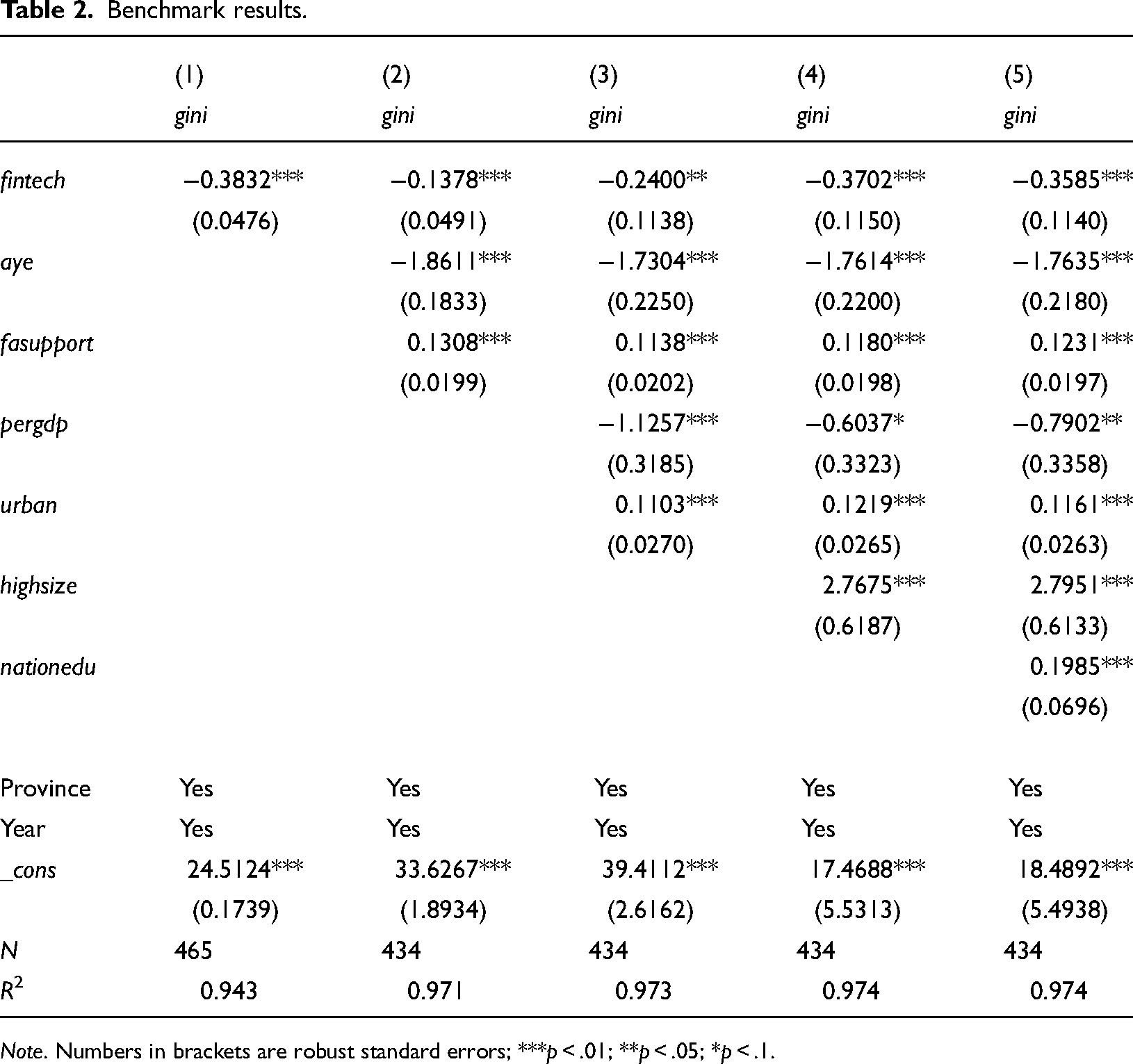

Table 2 presents the results of the benchmark tests. All estimated values for fintech are significantly negative at a 1% confidence level, indicating that the development of fintech can reduce the education Gini coefficient and promote educational equity. Fintech development helps lower the barriers to credit, reduce households’ credit constraints on education expenditure, and encourage household savings, promoting educational expenditure and equity in turn. Moreover, fintech technologies like IoT and cloud computing play a crucial role in driving the digital transformation of the education sector. By reducing information asymmetry, fintech narrows educational disparities across regions and increases resource equity. It also encourages public education expenditure, thereby promoting educational equity across regions.

Benchmark results.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

Heterogeneous influence of fintech on educational input

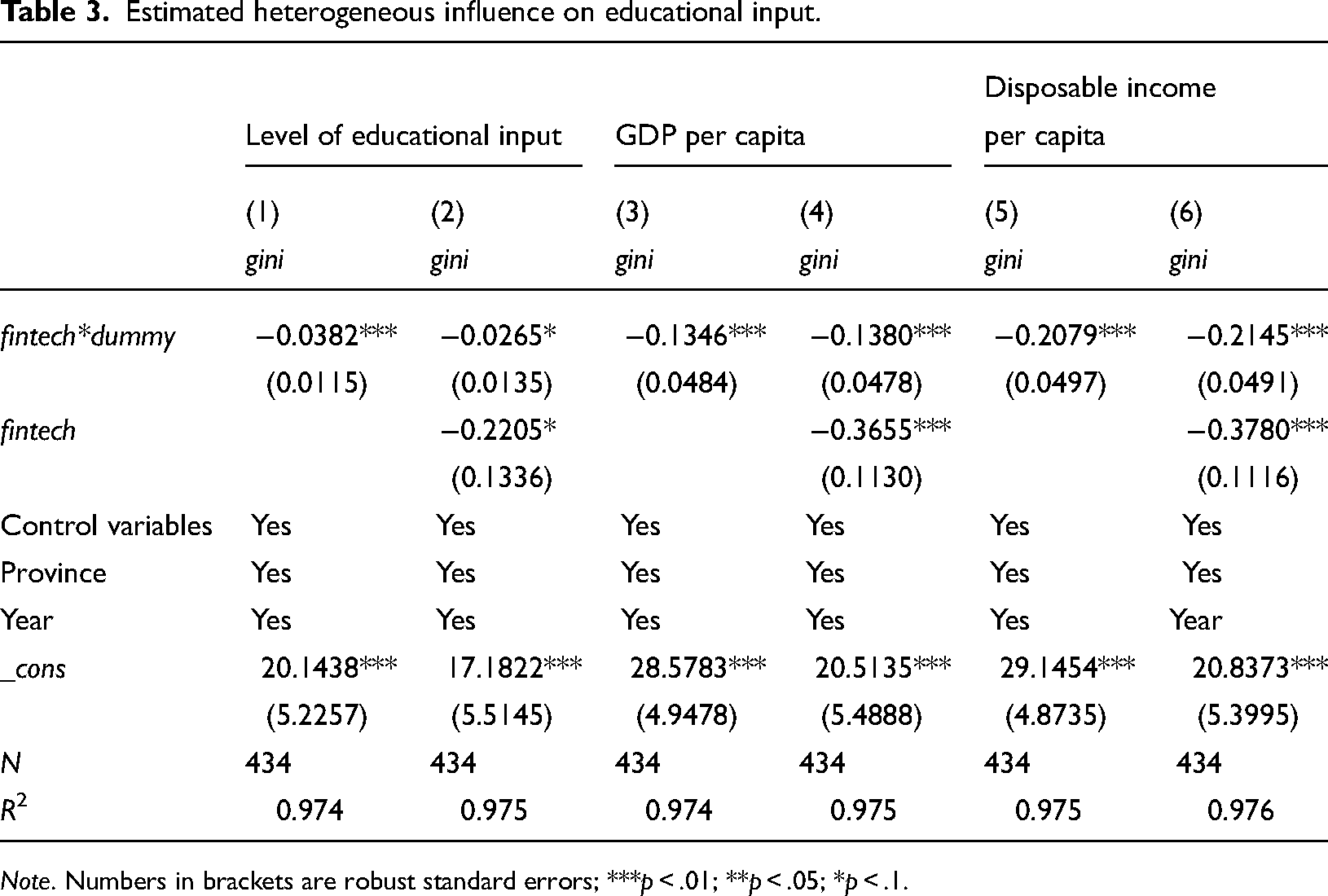

The effect of fintech on promoting educational equity is closely related to educational input and economic development. Therefore, this study examined the heterogeneity of the effect of fintech on educational equity with respect to educational input. Educational input reflects the level of government spending on public education, which this study measures using the public education expenditure per capita for regular high schools. The level of economic development in a region is characterized by its GDP per capita and disposable income per capita. This study also used dummy variables, with the dummy equal to 1 if the variable is less than the median, and 0 if not.

As Table 3 shows, fintech had a stronger effect in mitigating educational inequality for regions with less educational input and slower economic development. Fintech can strengthen niche marketing, unlocking the potential for regional consumption and investment and thus effectively mitigating educational inequality in underdeveloped regions with less educational investment and economic growth.

Estimated heterogeneous influence on educational input.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

Heterogeneous influence of fintech on educational output

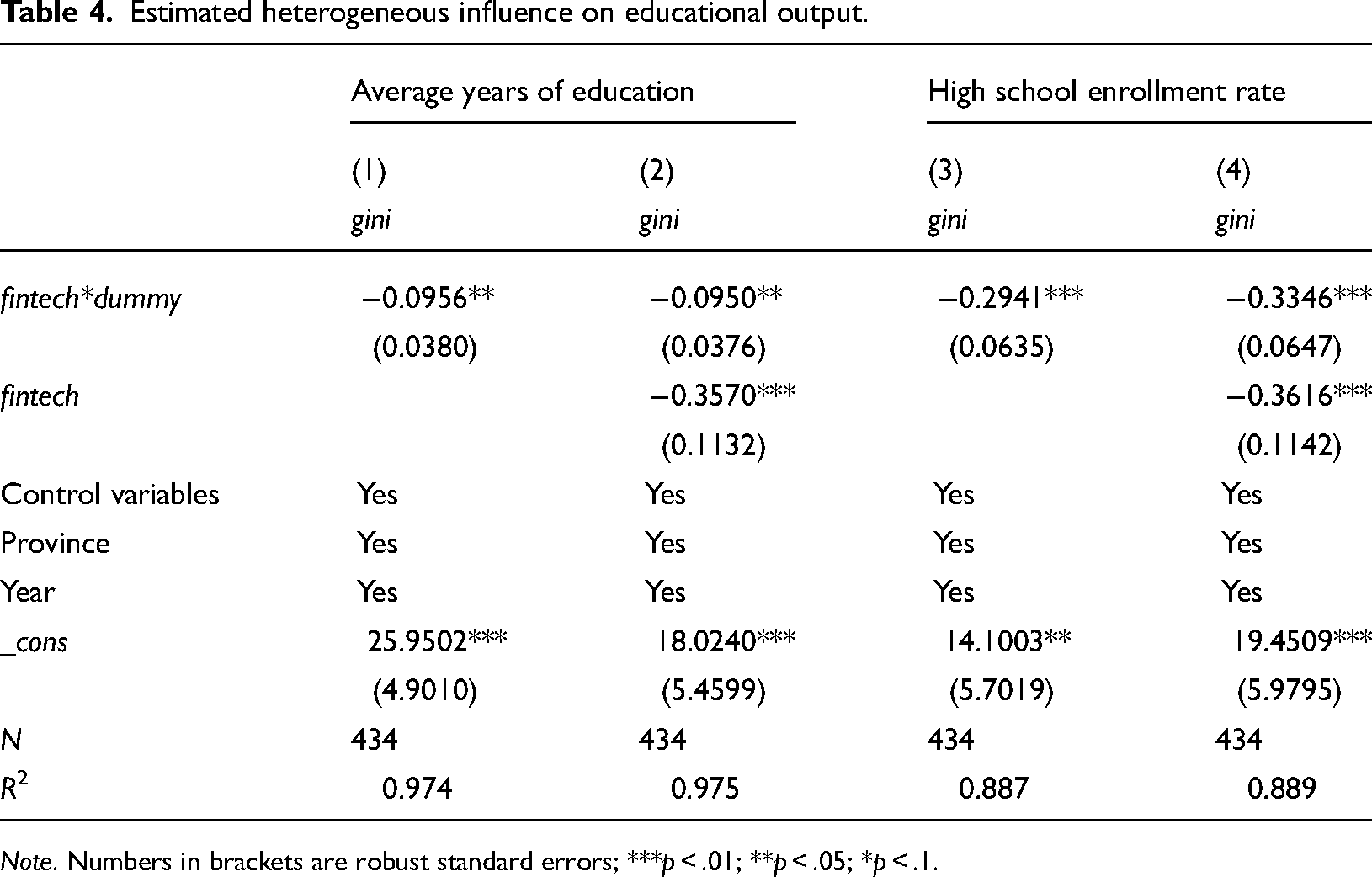

Educational output reflects the overall level of education as well as the scale and speed of educational development in a region. Therefore, this study analyzed the heterogeneity of the influence of fintech on educational equity with respect to educational output, which is characterized by average years of education and regular high school enrollment rates. Similar to the above, dummy variables were used in the analysis, where the variable holds a value of 1 if it is less than the median, and 0 if not.

As the results in Table 4 show, fintech had a stronger effect in mitigating educational inequality in regions with a lower average of years of education and high school enrollment rates. Regions with lower levels of educational output often have lower levels of economic development. To reduce inequality in education, fintech significantly improves the educational output of less economically developed areas by providing a broad range of financial products and increasing the breadth and depth of financial services.

Estimated heterogeneous influence on educational output.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

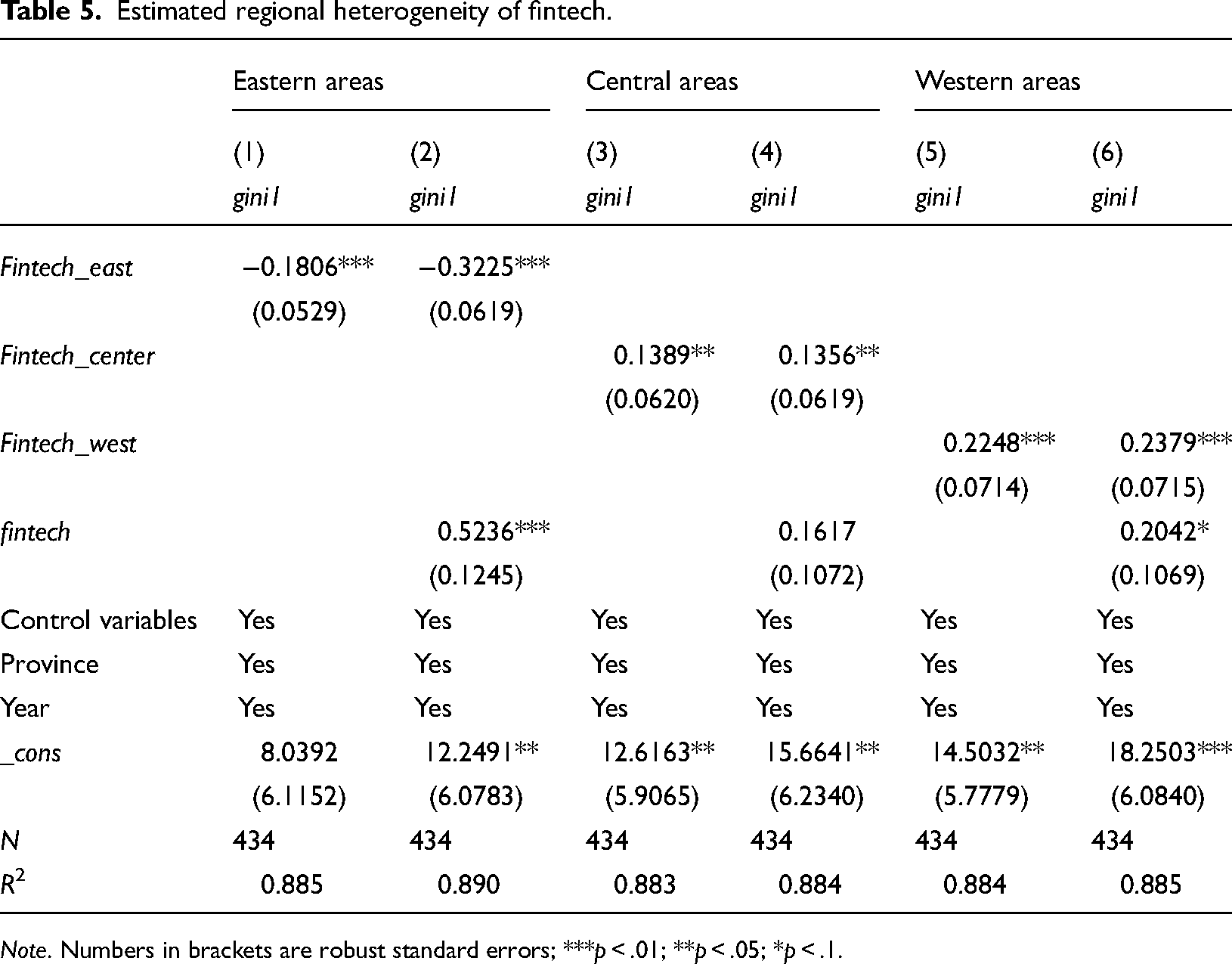

Regional heterogeneity of fintech

This study also investigated the regional heterogeneity of the effect of fintech on educational equity. Regional heterogeneity in educational output is characterized by the education Gini coefficient. In conducting regression analysis, this study set dummy variables for the eastern, central, and western areas of China.

As the analysis results in Table 5 show, fintech had a stronger mitigating effect on educational inequality in the central and western areas than in the eastern areas. More specifically, in less economically developed areas, fintech improved educational equality by promoting infrastructure development, particularly in terms of the widespread implementation of information technologies in education.

Estimated regional heterogeneity of fintech.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

Influence mechanism analysis

This study investigated the influence mechanism of fintech on educational equity using the following model:

Direct influence of fintech on educational equity

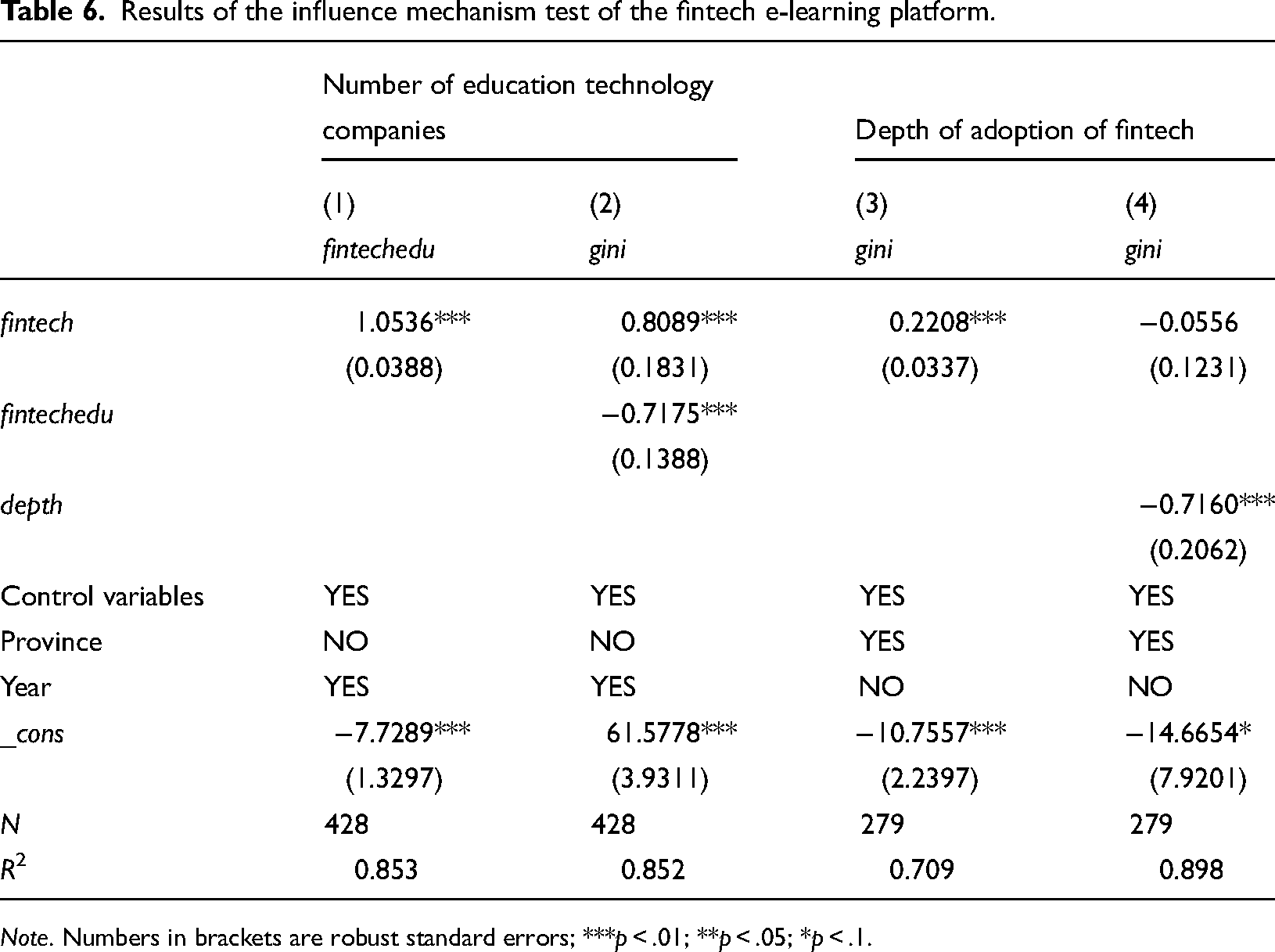

Adoption of the fintech e-learning platform

Using the latest generation of digital technologies, fintech drives the transformation of both traditional and smart education and promotes web-based business and innovation for education. Through e-learning platforms, fintech offers a broader range of financial services to support basic education, advancing both education reform and financial innovation and enhancing educational equity by increasing the sharing of educational resources. In this study, the level of regional fintech e-learning was measured by the number of fintech-related education technology companies at the provincial level, denoted as fintechedu. 1 This study evaluated the adoption of financial services using the depth index, which is a primary indicator of the digital financial inclusion index.

Table 6 shows the positive impact of fintech on various aspects of education, including smart education, e-learning, and educational information technology. By building a diversified platform for the sharing of educational resources, fintech advances educational equity. Moreover, the application of digital financial platforms reduces educational inequality by expanding the accessibility of financial services to low-income individuals, enabling them to overcome financial barriers and secure educational funds for their children.

Results of the influence mechanism test of the fintech e-learning platform.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

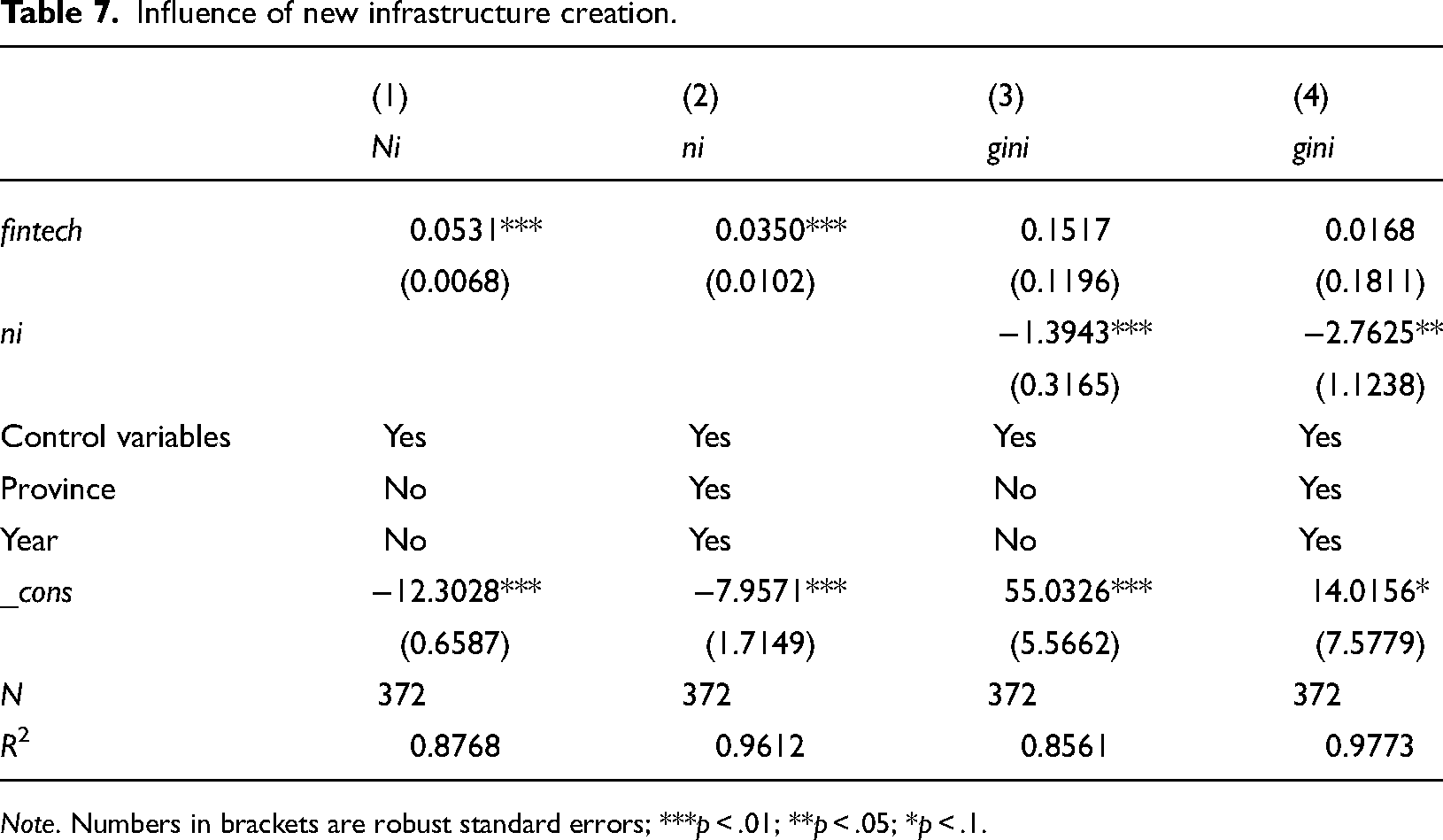

Influence of the creation of new infrastructure

The creation of new infrastructure is an effective pathway for advancing the digital transformation of education and the development of high-quality education. Establishing educational platforms is conducive to the sharing of educational resources, which can promote education equity in turn. As fintech innovates financial services through the application of technologies, it has a significant spillover effect on the development of new infrastructure. Accordingly, this study proposes a new index to evaluate the level of new infrastructure creation, 2 namely, ni.

As the results in Table 7 indicate, fintech can restrain inequality in education by promoting new infrastructure creation. Web accessibility has practical implications for promoting the sharing of educational resources and ensuring equity in education. The efficiency of asset allocation has been greatly improved following advances in the latest generation of information technologies, such as IoT, big data, and cloud computing. This also drives innovation and promotes the dissemination of knowledge in low-cost and efficient ways, which is beneficial for improving equity in education.

Influence of new infrastructure creation.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

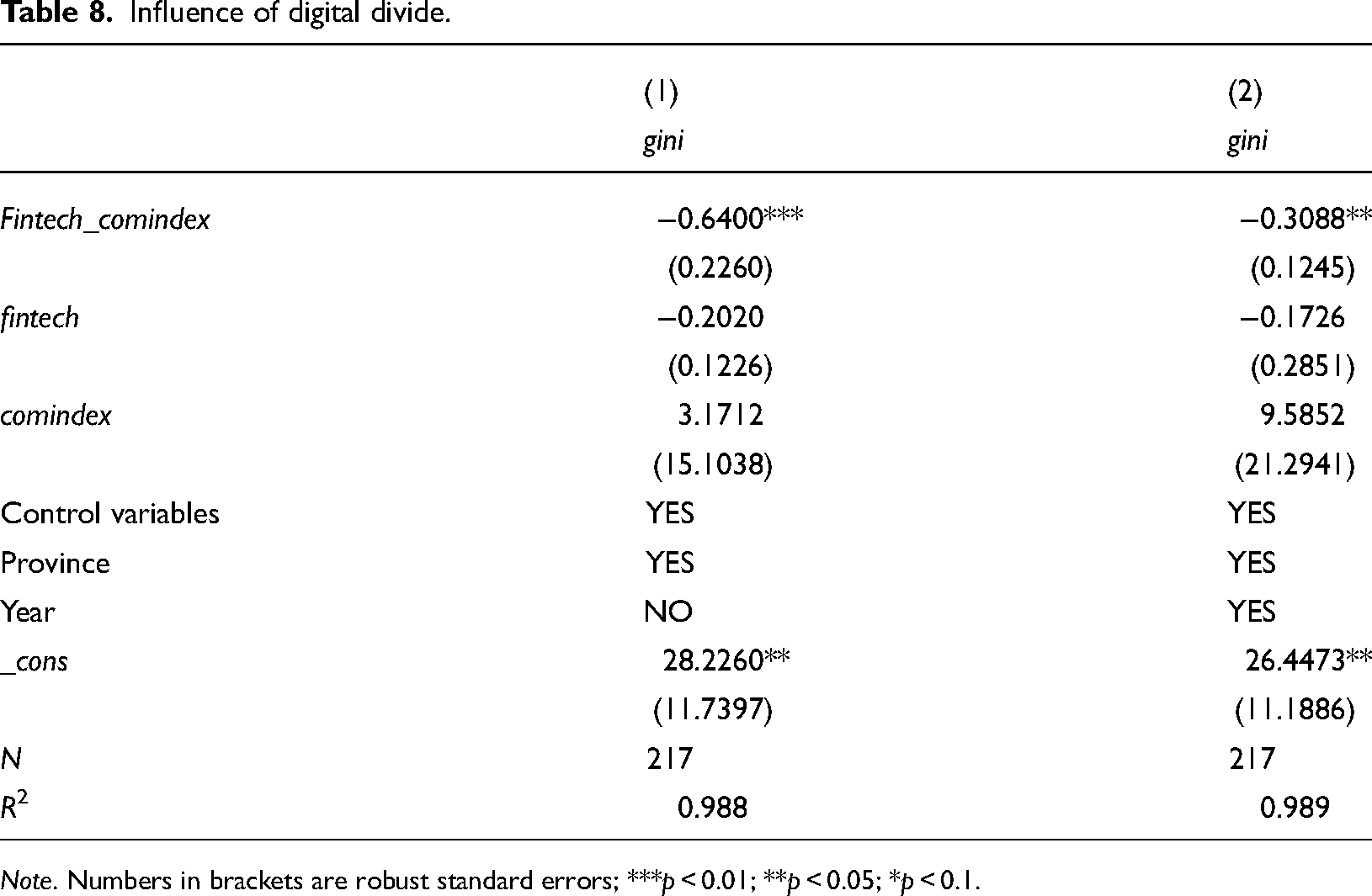

Influence of the digital divide

To examine the positive and negative effects of fintech and the digital divide on educational equity, this study constructed an analytical framework to investigate the interaction effects between variables. In this respect, the digital divide was measured using the comprehensive internet development index at the provincial level, denoted as comindex. 3

The results presented in Table 8 show that fintech had a stronger moderating effect on educational inequality in regions with lower levels of internet development and a larger digital divide. Fintech offers an open path to financial equality and freedom. Users from diverse backgrounds can utilize the vast amount of data it provides, which can promote service integration, encourage the digital transformation of education, encourage the creation and sharing of high-quality educational resources, mitigate the impact of the digital divide, and bolster educational equity.

Influence of digital divide.

Note. Numbers in brackets are robust standard errors; ***p < 0.01; **p < 0.05; *p < 0.1.

Indirect influence of fintech

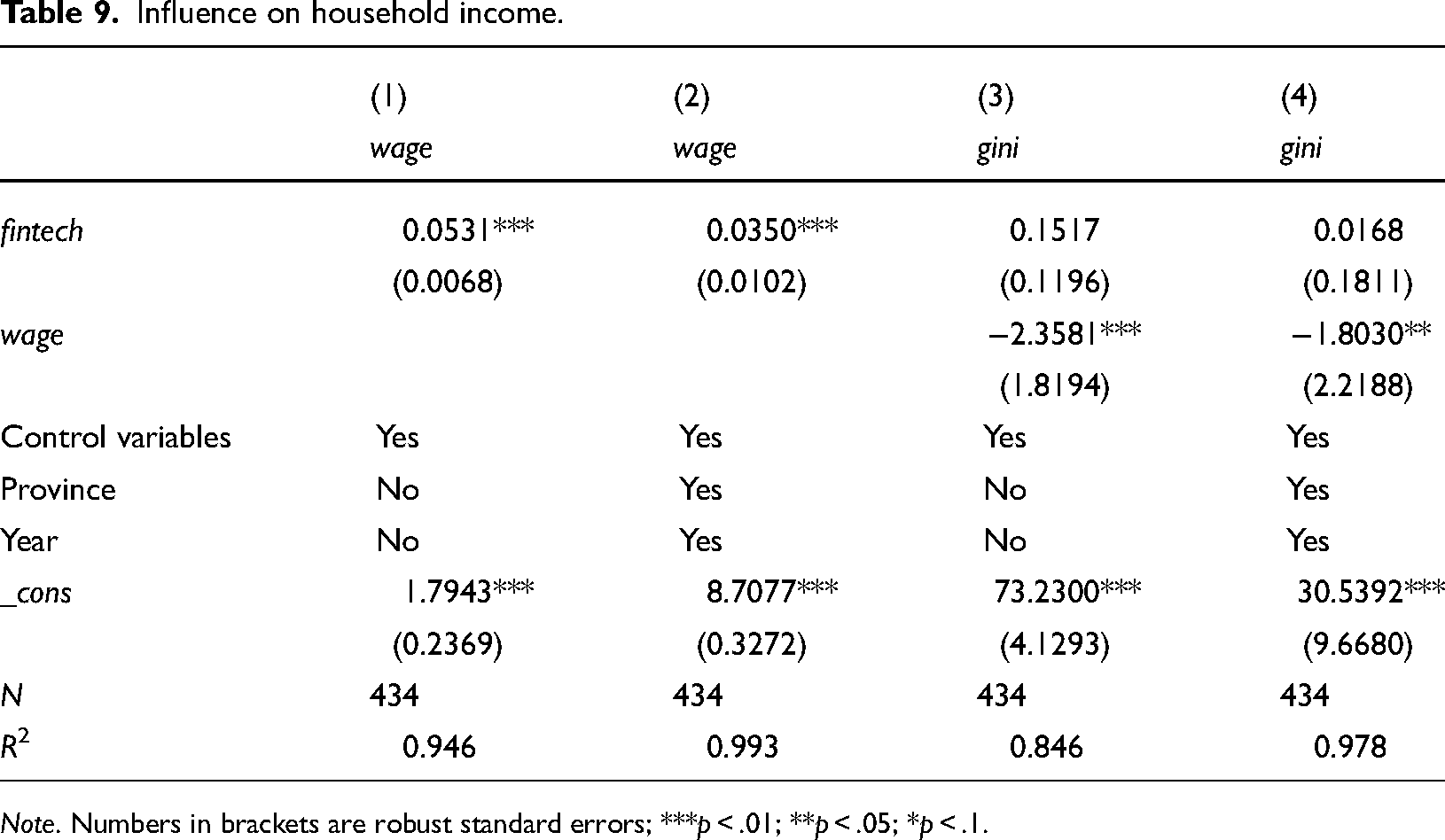

Influence on household income

Household income plays a significant role in improving educational equity in the long term, with the effect of fintech on improving household income found to be stronger among families with low endowments. In this study, household income was measured using the average wage of individuals employed in urban units.

As Table 9 shows, fintech can reduce inequality in education by increasing household income. Fintech can greatly promote household participation in financial markets by reducing participation costs, increasing accessibility, and broadening the channels for information acquisition. Furthermore, fintech encourages more diversified and efficient household asset portfolios, while portfolio optimization can effectively increase household wealth accumulation, thereby promoting equity in education. Fintech can also promote educational equity by enhancing the educational expectations of parents in a number of ways, such as increasing their expected rate of return on education and influencing family preferences for education.

Influence on household income.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

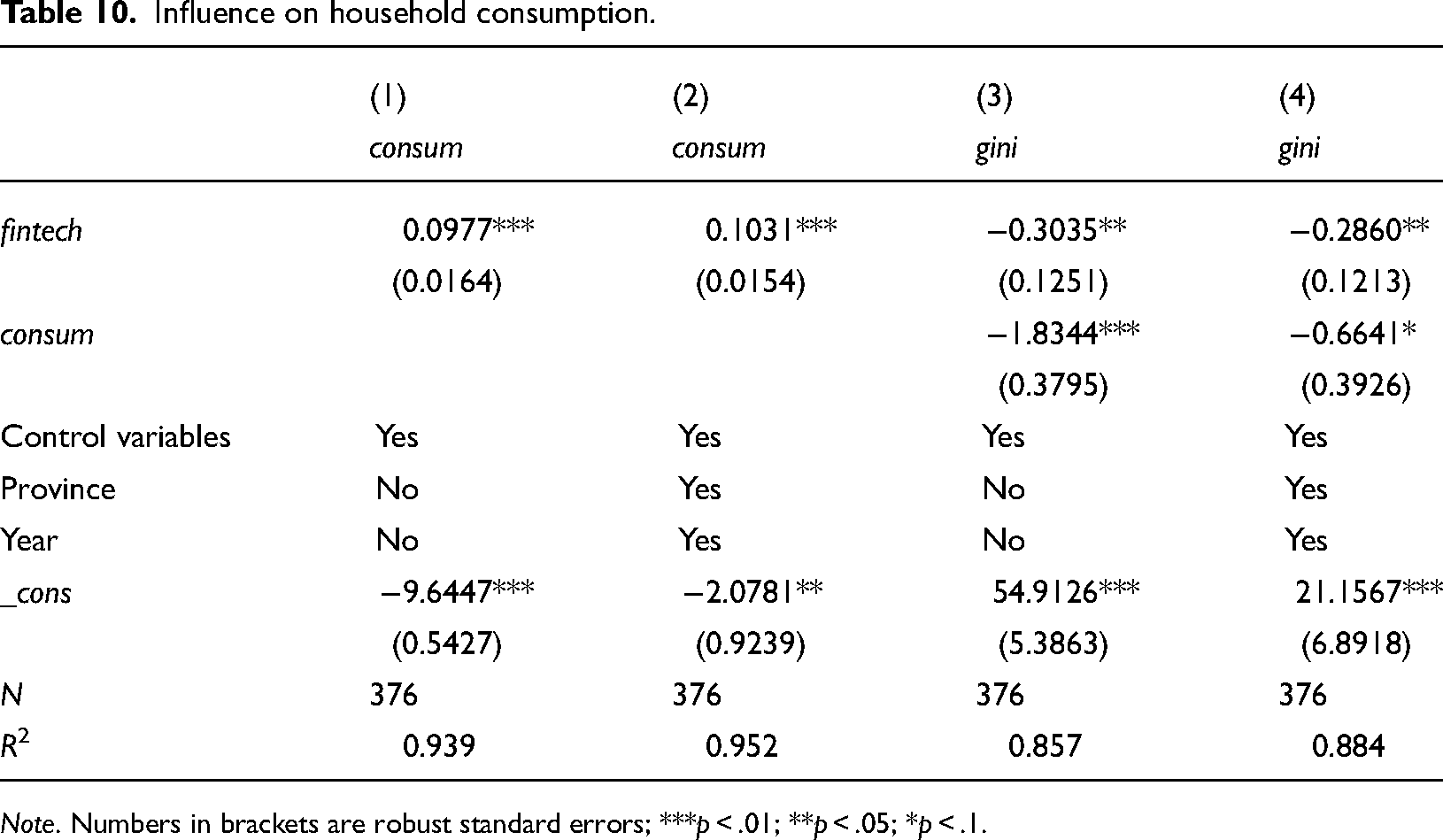

Influence on household consumption

Household consumption is a crucial indicator of the living standards of households. Consumption upgrading can increase not only residents’ business input but also their educational input and future income. In this study, household consumption was measured using the logarithm of consumption expenditure by resident households.

As the results in Table 10 demonstrate, an increase in household consumption can significantly restrain inequality in education. As a result of fintech development, consumers can enjoy more accessible and convenient financial services. More efficient business models lead to an increase in total household spending and a more refined consumption structure, increasing educational expenditure and educational equality.

Influence on household consumption.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

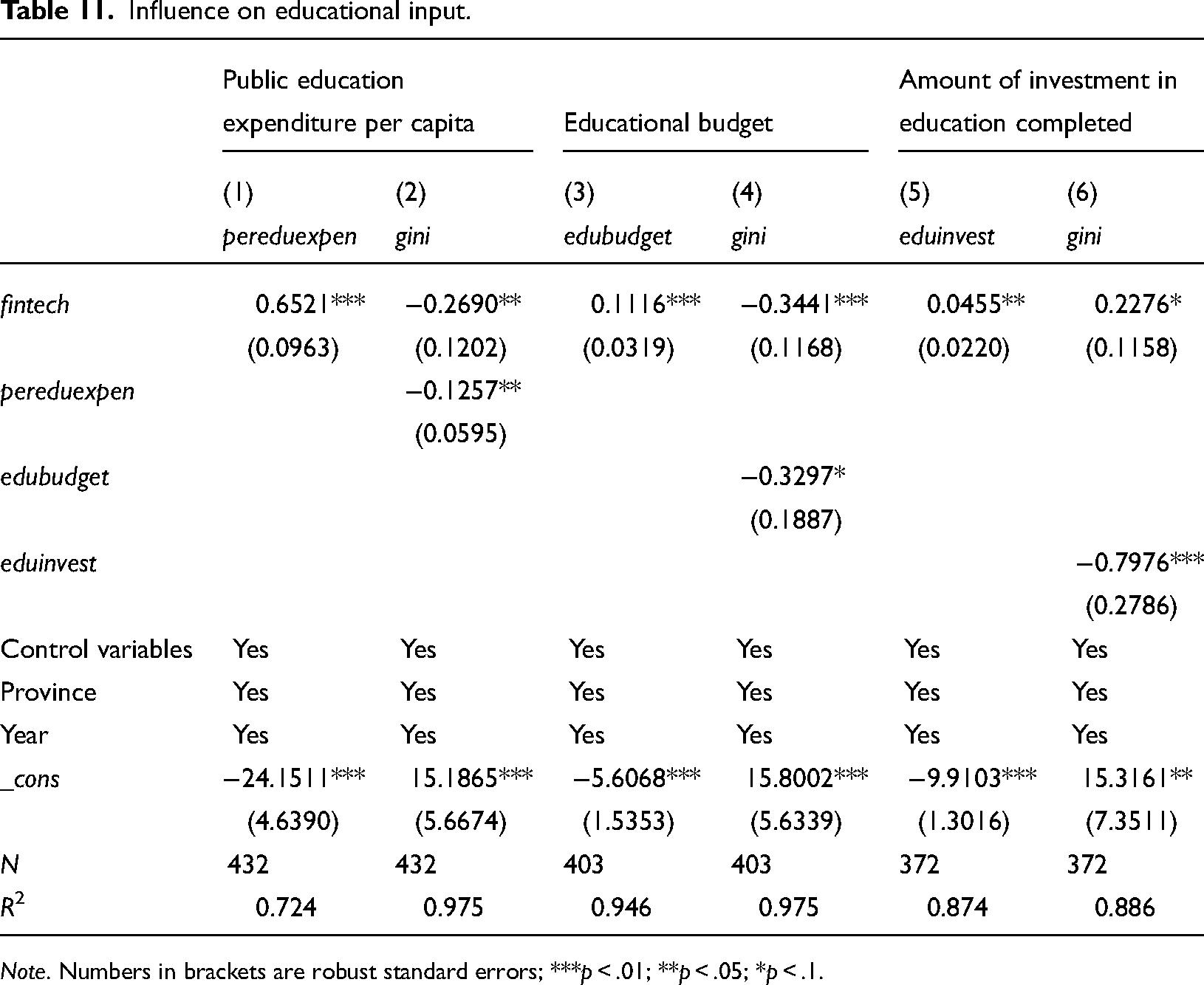

Influence on educational input

Another variable that may have a significant impact on educational equity is government spending on public education, such as educational resources, educational funds, teaching force, and educational content. This study measured regional educational input using public education expenditure per capita, the educational budget, and the amount of investment in education.

As the results in Table 11 show, fintech can reduce inequality in education by increasing regional educational input and optimizing educational resources. Greater investment in public education resources offers an effective solution to the unequal distribution of educational resources caused by external factors such as personal endowment and family environment. In addition, by stabilizing local fiscal revenue and promoting new infrastructure creation, fintech drives investments in related areas, thus promoting education equity.

Influence on educational input.

Note. Numbers in brackets are robust standard errors; ***p < .01; **p < .05; *p < .1.

Conclusions

Through our empirical research, we find that fintech can effectively promote education equity, particularly in regions with less educational input and output, such as the central and western areas of China. Further, our mechanism analysis shows that fintech promotes educational equity both directly and indirectly. More specifically, fintech has a direct positive influence on educational equity through fintech platforms, the creation of new infrastructure, and the narrowing of the digital divide. Meanwhile, fintech indirectly addresses educational inequality by increasing household income, household consumption, and public education expenditure. Accordingly, we propose that this study has the following three policy implications.

First, the study suggests that we should accelerate investment in new digital infrastructure and amplify the positive influence of fintech and other applications in the digital economy on education equity in emerging countries like China. Along these lines, we should actively promote the development of fintech infrastructure to expand its coverage. We should also accelerate the construction of a “government-guided, enterprise-based, market-operated” multifinancing system, encourage social capital to enter new infrastructure and alleviate the problem of insufficient funds for new infrastructure. In particular, in areas with a large digital divide, it is necessary to promote the introduction of big data, cloud computing, and other technologies; expand the coverage of inclusive finance; benefit new business entities, people living in poverty, and other “long tail” groups; and drive household income and consumption to promote educational equity.

Second, the study suggests that we should pay attention to the equalization of educational investment and optimize resource allocation for education, not just in China but across the international landscape. Policies should be designed to rationally guide the allocation of educational resources, reduce the gap in educational inequality between regions, continue to increase transfer payments to provinces with high education inequality and improve the basic driving forces of educational equity. At the same time, we should improve the treatment and welfare of teachers in underdeveloped areas, improve the quality and stability of teachers, and strengthen the software guarantee for educational fairness.

Third, the findings evidence that we should improve talent provision for the digital economy and reinforce digital innovation in education—this recommendation is applicable to China and nations worldwide. On the one hand, we should optimize the structure of the disciplines, deepen the reform of talent training models, and cultivate more talents in key areas. This requires deepening collaborations between industry and academia, vigorously cultivating digital economic and technical talents, and providing high-end human support for new infrastructure creation to achieve breakthroughs in core technologies. On the other hand, we should make full use of digital technology, improve the construction of platforms for sharing high-quality educational resources with more people, enhance our ability to support regional development and narrow the digital divide across regions.

Footnotes

Contributorship

Lianxing Yang conceived the idea for this research, critically reviewed the entire manuscript, and led the writing process. Yunzhe Hong collected and processed the data and drafted the manuscript. Both authors contributed to the manuscript.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.