Abstract

This paper examines the geopolitical dimensions of China's strategy to internationalise the renminbi (RMB) and reduce reliance on the U.S. dollar. Far from a purely financial initiative, RMB internationalisation is a strategic response to the geopolitical and economic risks of a dollar-centric order. Through instruments such as the petroyuan, bilateral currency swaps, the Cross-Border Interbank Payment System, and the digital yuan, China seeks to embed the RMB within global trade, investment, and payment infrastructures. Anchored in geopolitical frameworks such as the Belt and Road Initiative and BRICS+ cooperation, these efforts form part of a wider strategy to extend China's economic influence and reduce exposure to dollar weaponisation. While the RMB's role in global reserves remains limited, China's selective and incremental approach prioritises trade-based internationalisation over capital account liberalisation. Set against accelerating de-dollarisation and deepening multipolarity, the paper analyses how China's RMB strategy is reshaping global systems of exchange, across finance, trade, and payments.

Keywords

Introduction

Mounting frustration with the dominance of the U.S. dollar has driven BRICS+ (an intergovernmental group now comprising Brazil, Russia, India, China, South Africa, Egypt, Ethiopia, Iran, United Arab Emirates [UAE] and Indonesia) members, among others, to pursue de-dollarisation efforts, as highlighted at the 2023 and 2024 BRICS summits. Geopolitical concerns over the dollar's weaponisation through Western sanctions, combined with economic vulnerabilities caused by dollar shortages, have fuelled interest in alternatives, notably the Chinese renminbi (RMB) (Wade, 2024). These moves aim to reduce reliance on the greenback, foster local currency usage, and advance a multipolar financial order. China has been proactive in pursuing de-dollarisation through the RMB, employing mechanisms such as the petroyuan, bilateral currency swap agreements, the Cross-Border Interbank Payment System (CIPS), and the digital yuan. The RMB's role has grown significantly in the BRICS and Belt and Road Initiative (BRI) trade, as well as in sanctioned countries such as Russia and Iran, where it provides a viable alternative to the dollar.

While financial challenges persist, most notably limited convertibility, which constrains the RMB's share in global reserves, China's strategic initiatives nonetheless position the RMB as a significant contender in the de-dollarisation agenda. This paper examines the geopolitical dimensions of China's RMB internationalisation strategy. It argues that China is pursuing a cautious and incremental approach to RMB internationalisation, balancing a seemingly contradictory policy agenda: promoting internationalisation while maintaining control over its capital account to limit financial volatility. At present, Beijing is prioritising trade-based rather than financial internationalisation, expanding the RMB's use in bilateral trade settlements – particularly with sanctioned states such as Russia and Iran, as well as with BRICS partners – as a way to internationalise the currency without liberalising domestic financial markets. China's selective approach to RMB internationalisation reflects not only economic pragmatism but also a deliberate effort to hedge against potential U.S.-led “financial war” scenarios (Freymann and Heng, 2025). Unsurprisingly, some observers have dismissed the possibility of the RMB becoming a leading global currency (Kirchner, 2019; Steil and Della Rocca, 2018). However, such analyses often overlook both China's historically gradualist approach to economic reform and the intensifying geopolitical drivers behind both de-dollarisation and RMB internationalisation.

Challenging dollar dominance is not merely an economic proposition but a politically symbolic and motivated effort. China, along with the BRICS, does not seek to establish currency hegemony for itself but instead envisions a multipolar financial system (Flores, 2024). The U.S. dollar's dominance, entrenched over decades, has created deep path dependencies and institutional frameworks that support its continuing use. However, cracks are emerging in some of the geopolitical alliances that sustain it. For example, recent tensions in the U.S.–Saudi Arabia relationship – the cornerstone of the petrodollar system – raise questions about the long-term stability of their relationship. The push for de-dollarisation is also intended to counter the U.S. and other Western governments’ weaponisation of the dollar-centric financial system to sanction their geopolitical opponents (Wade, 2024). These shifts coincide with growing ideological challenges to the liberal international order, as well as rising anti-Western sentiment among countries in the Global South. While outright displacement of the dollar remains unlikely, the combined pressures of geopolitical realignments and ideological shifts are beginning to erode its foundations.

With Trump's return to the White House, the drive for de-dollarisation is gaining further momentum. His aggressive neo-mercantilist agenda – marked by a preference for tariffs, unilateralism, and sanctions – combined with attacks on democratic institutions and the rule of law at home, reinforces the perception of the dollar as a weaponised tool of U.S. foreign policy and undermines global trust in the U.S. financial system. The renewed use of financial sanctions, including secondary sanctions, has heightened concerns about overexposure to the dollar among both adversaries and neutral states. The chaotic and punitive tariff regime unveiled on “Liberation Day” on 2 April 2025 – marked by sweeping tariffs on imports from both adversaries and allies – has disrupted global trade flows and sharpened concerns about the risk of over-reliance on the dollar-centric system. At the same time, strained alliances and mounting global economic uncertainty may create openings for alternatives, such as the RMB, to gain wider adoption. In this context, de-dollarisation emerges not merely as an economic strategy but as a geopolitical response to the volatility, assertiveness and unpredictability of U.S. policies, reflecting a broader rejection of dollar-centric hegemony.

This paper explores the geopolitics and policy instruments of the RMB's internationalisation and its potential to challenge dollar dominance. It begins by outlining and evaluating the geopolitical dimensions of RMB internationalisation, focusing on the petroyuan, digital yuan, and BRICS+ and BRI trade and currency strategies. Next, it discusses the global geopolitical context and growing de-dollarisation momentum. Finally, the limits and opportunities for the RMB to become a significant international currency are addressed, along with the broader potential costs and benefits associated with the emergence of a multipolar currency order.

Policy Instruments and Mechanisms of RMB Internationalisation

China's plan to internationalise the RMB began in the first decade of the twenty-first century, particularly after the 2008 global financial crisis exposed vulnerabilities in the dollar-dominated global financial system. Key milestones in Beijing's incremental approach include the 2009 launch of the RMB Cross-Border Trade Settlement Pilot Program, which enabled selected Chinese companies to settle international trade in RMB, and the subsequent development of offshore RMB markets in financial hubs such as Hong Kong, London, and Singapore (PBC, 2009). To support these efforts, China introduced the CIPS in 2015, providing critical infrastructure to facilitate international RMB payments and reducing reliance on the Society for Worldwide Interbank Financial Telecommunication (SWIFT), enabling China and others to bypass U.S.-dominated financial payment systems (PBC, 2015). The inclusion of the RMB in the International Monetary Fund’s (IMF's) Special Drawing Rights basket in 2016 marked its acceptance as a global reserve currency, while the 2018 introduction of yuan-denominated crude oil futures, or petroyuan, expanded RMB usage in energy markets (PBC, 2016a; The Economist, 2018).

These efforts gained renewed urgency during the U.S.–China trade war, beginning in 2018, which drew further attention to the strategic risks of dollar dependence for Beijing (Amighini and Garcia-Herrero, 2023: 7). RMB internationalisation is largely shaped by concerns over national security and financial vulnerability. Faced with growing U.S. economic coercion, Chinese elites increasingly regard dollar dependence as a strategic risk, viewing partial RMB internationalisation as a hedge against the threat of “financial war” (Freymann and Heng, 2025). Although numerous policy instruments and mechanisms contribute to RMB internationalisation – including financial market reforms and the development of offshore RMB markets – this paper focuses specifically on its geopolitical dimensions, examining three principal mechanisms where geopolitics plays a central role: the petroyuan, the digital yuan, and BRICS and BRI trade and currency strategies.

Petroyuan

The introduction of yuan-denominated crude oil futures (petroyuan) via the Shanghai International Energy Exchange (INE) in 2018 marked a pivotal step in China's efforts to internationalise the RMB and embed it within global energy markets. The petroyuan establishes a yuan-based benchmark for oil pricing alongside entrenched dollar-denominated benchmarks such as Brent Crude and West Texas Intermediate. Leveraging its position as the world's largest oil importer, China aims to use the petroyuan to facilitate trade in its own currency, reducing the need for dollar conversions and lowering transaction costs for its trading partners.

Yuan-based oil trade is expanding but remains modest in terms of its scale and share in the global oil market. However, deepening institutional and financial ties suggest that a much broader adoption of the petroyuan could unfold over the coming decades. President Xi Jinping's December 2022 visit to Riyadh contributed to this trajectory, establishing cooperation on initiatives such as Saudi Arabia's Vision 2030, which seeks to leverage oil revenues to drive economic diversification and may lay the groundwork for expanded RMB use in energy and infrastructure projects (Ma, 2025). Saudi Arabia and other Gulf states are likely to expand yuan settlements cautiously, balancing relationships with the U.S. and China to pragmatically advance their interests.

China's strategic motivations for the petroyuan extend beyond trade efficiency to reducing vulnerabilities imposed by the dollar–oil nexus (Taylor, 2024a: 136). The petrodollar's role as the dominant currency for oil invoicing, established in the 1970s through agreements between the U.S. and Saudi Arabia, has underpinned the dollar's hegemonic position in the global financial system (Spiro, 1999). For China, this arrangement exposes its energy security to fluctuations in American monetary policy, which can lead to increased costs and economic instability. Mindful of these vulnerabilities, China's RMB-denominated oil futures contract provides an alternative that reduces exposure to a financialised and dollarised global commodities market.

The petroyuan has gained traction among global traders and market participants, with swift acceptance from major commodities firms such as Glencore PLC and the Trafigura Group (Bloomberg News, 2018). Within its first year, the contract became the third most actively traded crude oil future worldwide, with trading volumes equivalent to 14% of the global activity in similar futures (Jordan, Knauff and Company, 2019). The contract's adoption has been bolstered by the INE's delivery to overseas clients, including South Korea, India, Singapore, Malaysia, and Japan, and the introduction of oil options for risk management (Al Shareef, 2024). In addition, the petroyuan's closer reflection of regional supply and demand dynamics enhances its relevance as a benchmark for Asian markets. This alignment has the potential to address the “Asian premium” – the higher prices Asian importers have traditionally paid compared to their Western counterparts (Katsomitros, 2018).

Countries seeking to diversify their trade settlement currencies for strategic or economic reasons have embraced the petroyuan as a practical alternative. Bilateral agreements with oil exporters such as Russia and Iran have incorporated yuan-denominated settlements, largely to bypass Western sanctions. Discussions with Saudi Arabia and other Gulf states underscore the petroyuan's potential to shift energy trade dynamics, although challenges persist due to Gulf currencies’ dollar pegs and concerns over yuan liquidity. The BRI has also been instrumental in expanding the petroyuan's reach, facilitating yuan-based trade relationships with a wider range of partners and reinforcing China's broader strategy to elevate the RMB's role in global trade.

This growing adoption reflects not only the yuan's utility in energy trade but also the geopolitical and economic drivers motivating China's partners to reduce financial dependencies and diversify trade systems. Agreements made during President Xi's visit to Riyadh include a local currency swap agreement between the People's Bank of China (PBC) and the Saudi Central Bank, valued at 50 billion yuan (approximately $6.93 billion), to facilitate trade and investment in local currencies (Cash, 2023). Furthermore, the Shanghai Stock Exchange and Saudi Tadawul Group (the parent company of Saudi Exchange) signed a memorandum of understanding to explore cross-listing opportunities and data sharing between their capital markets (Reuters, 2023; Zhang and Ren, 2023). These developments highlight the growing financial architecture that could underpin yuan-based trade in the region.

While the petroyuan's role continues to expand, its significance lies in providing an alternative pathway for trade rather than fundamentally transforming the global energy market's reliance on the petrodollar. At the same time, China's evolving relationships with key energy exporters in the Middle East and elsewhere that foster broader economic partnerships align with Beijing's ambitions to secure energy supplies, deepen trade ties, and support the internationalisation of the RMB.

Digital Yuan

Even though its primary purpose remains domestic, the digital yuan (e-CNY), launched as a pilot project in 2020, is another component of China's efforts to internationalise the RMB (PBC, 2021). As one of the first central bank digital currencies (CBDCs) introduced by a major economy, the e-CNY aims to enhance payment efficiency, reduce transaction costs, and provide a secure alternative to existing global financial infrastructures, including those dependent on Western bank messaging networks such as SWIFT. Designed to modernise payment systems and strengthen monetary control, the e-CNY also offers capabilities for cross-border transactions, making it a potential tool for expanding RMB adoption in international trade (Kshetri, 2023; Taylor, 2024b). By integrating advanced digital technologies and providing an alternative to dollar-dominated financial systems, the e-CNY aligns with China's broader strategy to expand the global role of the RMB.

The geopolitical utility of the digital yuan has become increasingly apparent in contexts where countries seek to bypass the constraints of U.S.-dominated financial networks. The e-CNY provides an alternative for sanctioned states, again notably Russia and Iran, allowing them to conduct trade without relying on dollar-linked systems vulnerable to U.S. restrictions. Moreover, China's strategic partnerships with BRI participants and other Global South countries have created a conducive environment for the e-CNY's adoption in cross-border trade and investment. Pilot programs for cross-border e-CNY payments with nations such as Thailand and the UAE further indicate its potential to integrate into regional financial ecosystems, facilitating transactions outside traditional dollar-dominated systems (The Economist, 2022).

Although often discussed as a sanctions workaround, the international use of the digital yuan carries far broader strategic implications. Slawotsky (2022: 253) argues that if the digital yuan is successfully embedded in international payment systems, it could grant China structural power by shifting financial and technological infrastructures away from U.S.-dominated networks, thereby accelerating the erosion of dollar dominance by creating alternative digital infrastructure and reconfiguring global monetary governance to support RMB usage. However, as Chaisse (2023) shows the global regulatory landscape for cross-border digital transactions remains highly fragmented. Legal uncertainty surrounding data flows, digital foreign direct investment, and investment protections may present serious institutional constraints to any effort, such as China's, to internationalise digital currencies through globally integrated financial systems.

Despite its promise, the digital yuan faces hurdles to becoming a widely adopted international currency. Its primary usage remains domestic, and the limited international convertibility of the RMB, coupled with concerns about transparency and political control (as the PBC is a non-independent central bank subject to party–state interference), constrain its appeal among foreign users, particularly in the West (Taylor, 2024b). However, as China continues to expand bilateral agreements and refine its CBDC framework, the e-CNY could contribute significantly to RMB internationalisation. Although not initially intended as a vehicle for this purpose, the e-CNY serves as an example of how digital innovation can align with broader economic and geopolitical strategies.

BRICS+ and BRI Trade and Currency Strategies

The BRICS+ grouping and the BRI are important frameworks for advancing RMB internationalisation. Through these platforms, China has sought to increase the RMB's role in regional and global trade systems, drawing upon bilateral and multilateral agreements to encourage its use in settlements and investments. The recent expansion of BRICS to include five new members – Egypt, Ethiopia, Iran, UAE, and Indonesia – enhances the bloc's economic and geopolitical influence and could further bolster RMB internationalisation efforts. The BRI, encompassing over 140 countries, complements these efforts by promoting RMB usage in infrastructure financing and trade settlements along key economic corridors.

Within BRICS, China has promoted initiatives aimed at expanding RMB usage among member states. Bilateral currency swap agreements, such as those between the PBC and the central banks of Brazil and Russia, enable trade and financial transactions in local currencies (BBC, 2013; PBC, 2016b). These agreements serve as a key mechanism for providing offshore RMB liquidity without requiring capital account liberalisation, making them central to China's strategy of controlled internationalisation. They become particularly significant for Russia, which has settled an increasing share of its bilateral trade with China in RMB since 2022, in response to Western sanctions. Discussions at the 2024 BRICS Summit in Kazan, Russia, about establishing a BRICS reserve currency further highlighted interest in reducing reliance on the dollar, though practical implementation remains uncertain (von Essen and Ingvarsson, 2024: 4). RMB adoption within BRICS countries varies widely, yet China's status as the bloc's largest economy positions the RMB as a strong candidate for regional currency usage and cooperation.

The BRI provides additional avenues for promoting RMB adoption, particularly through infrastructure financing and trade relationships. In 2021, China's RMB settlements with BRI countries reached 5.42 trillion yuan (approximately US$763.4 billion), marking a 19.6% year-on-year increase (State Council, 2021). This growth included a 14.7% rise in the trade of goods and a 43.4% increase in direct investment settlements (State Council, 2021). China had concluded bilateral currency swap agreements with twenty-two BRI countries and set up RMB clearing arrangements in eight of them in that same year (State Council, 2021). Furthermore, in 2023, the merchandise trade volume between China and approximately 150 BRI countries reached 14 trillion yuan (Chan, 2023). This substantial trade volume is promising for the growth of RMB usage in trade and investment activities.

Chinese state-owned banks, notably the China Development Bank and the Export–Import Bank of China (Eximbank), play a pivotal role in financing BRI projects, often through RMB-denominated loans. For instance, both banks have established financing windows of 350 billion yuan each to support BRI endeavours (Xinhua, 2023). This strategy encourages recipient countries to engage in transactions using the RMB, thereby promoting its internationalisation. For example, Pakistan has increasingly adopted the RMB for several China–Pakistan Economic Corridor projects (Safdar and Zabin, 2020). By integrating the RMB into trade and investment activities across Asia, Africa, and the Middle East, the BRI facilitates the currency's expanded international role. Although not all transactions are conducted in RMB, China's Eximbank has financed over 4000 kilometres of railways, 23,000 kilometres of roads, forty airports, and thirty ports in BRI partner countries, underscoring the extensive reach of its financing activities (Wu, 2024).

The petroyuan and digital yuan play complementary roles in advancing China's financial and geopolitical objectives through BRICS+ and the BRI. Saudi Arabia has not yet adopted the yuan for oil transactions but has expressed openness to exploring this possibility (Wong, 2024). Iran and Russia are already using the petroyuan in their energy trade with China in order to circumvent international sanctions (Gardner, 2024; Prokopenko, 2024). Meanwhile, the digital yuan supports the broader internationalisation of the Chinese currency by enabling secure cross-border payments, particularly in BRI economies with underdeveloped financial infrastructure. While these initiatives are not yet transformative for RMB adoption on a global scale, they constitute strategic steps towards increasing its international role.

De-Dollarisation Trend

China's efforts to internationalise the RMB coincide with a growing global push to reduce reliance on the U.S. dollar, driven by a range of geopolitical, economic, and systemic factors. Calls for a more multipolar monetary order emerged in the first decade of the twenty-first century when China and Russia began advocating for a multipolar world, the details of which can be found in their 2005 “Joint Statement of the People's Republic of China and the Russian Federation on the International Order of the twenty-first Century” (PRC and Russian Federation, 2005). The 2008 global financial crisis exposed vulnerabilities in the dollar-centric framework, prompting more systematic efforts to diversify away from the dollar throughout the 2010s (Amighini and Garcia-Herrero, 2023: 4). These efforts have been intensified by U.S. sanctions regimes, geopolitical rivalries, and the fragmentation of the global economy, creating greater openings for the RMB's wider international acceptance.

Countries such as Russia and Iran are clearly motivated by geopolitics in their move away from the dollar, yet economic considerations are no less significant. Emerging economies often face heightened exposure to U.S. monetary policy, particularly through the impact of interest rate volatility, dollar-denominated debt burdens, and the spillover effects of inflation or recession in the U.S. The Federal Reserve's tightening cycles frequently trigger capital outflows, exchange rate depreciation, decline in equity prices, and rising bond yields, underscoring the risks of over-reliance on the dollar (Gupta et al., 2017: 3). Simultaneously, concerns about the long-term stability of the dollar, amid rising U.S. debt and inflationary pressure, have deepened scepticism.

These dynamics coincide with China's economic rise and its promotion of the RMB as a reserve currency, supported by the establishment of alternative institutions such as the New Development Bank and Asian Infrastructure Investment Bank, which challenge the dominance of Bretton Woods-era international financial institutions such as the World Bank and IMF. De-dollarisation is also driven by changes in the structure of global trade. Over the past twenty years, trade patterns have evolved to include a growing share of bilateral trade among emerging economies, alongside continued exchanges with advanced economies. For the latter, transactions are largely denominated in U.S. dollars, while the former are increasingly conducted in local currencies.

Technological innovations could further accelerate de-dollarisation. CBDCs, alongside blockchain technology and decentralised finance, provide mechanisms to bypass traditional dollar-based financial systems. However, these technologies are not without their challenges – particularly in the case of cryptocurrencies – and are best viewed as long-term possibilities. Despite the dollar's enduring dominance, underpinned by its deep liquidity and global acceptability, these drivers collectively point to a gradual erosion of its hegemony in the global economy. Currently, de-dollarisation is most evident in trade settlements, payment systems, gold purchases, and, to a much lesser extent, in the composition of foreign exchange reserves. In contrast, it remains far less pronounced in global financial markets, energy markets, and international bond markets.

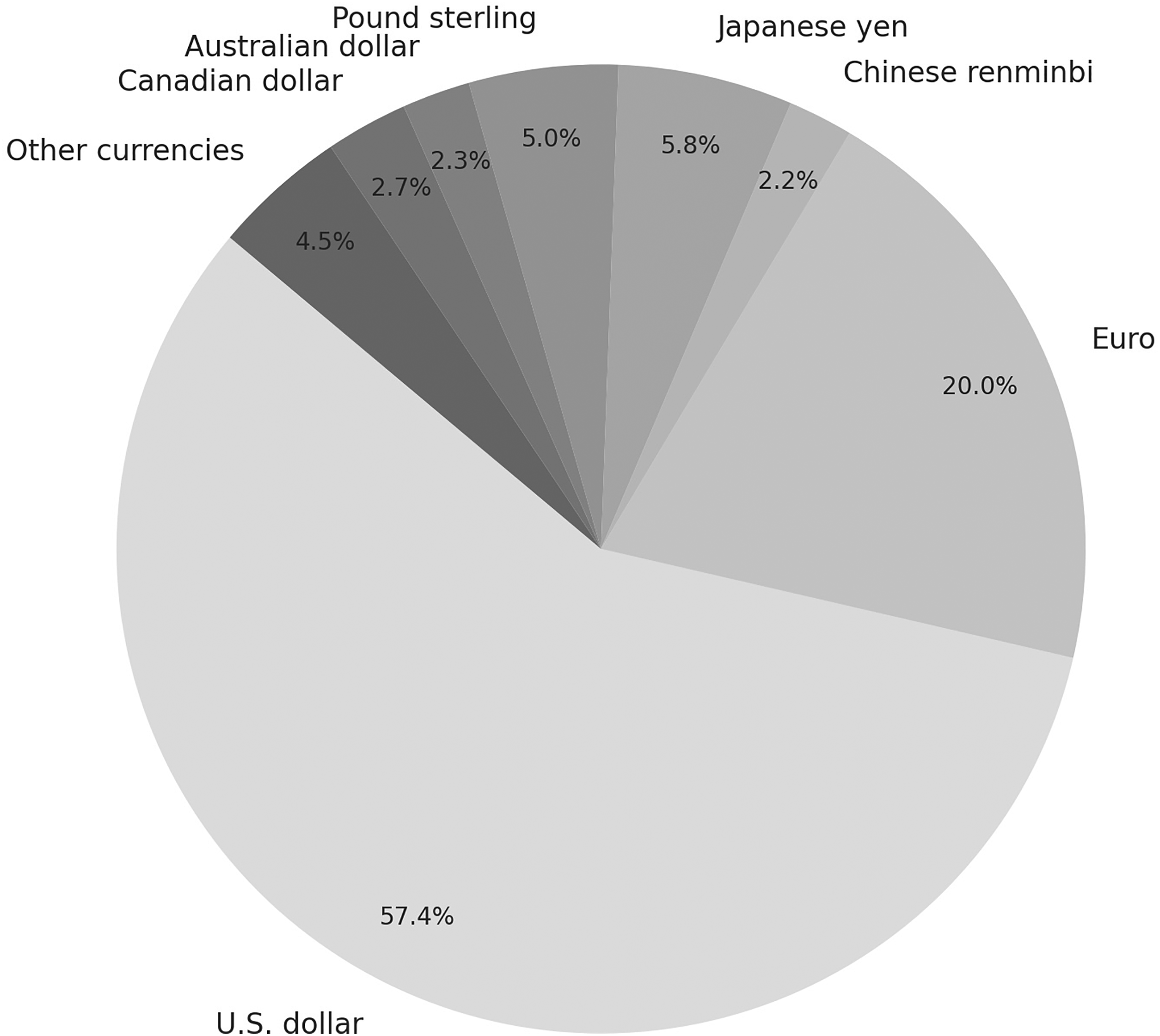

De-dollarisation in global reserves remains modest in scale but is part of a notable long-term trend. According to the IMF, the U.S. dollar's share of allocated foreign exchange reserves has gradually declined from 71 per cent in 1999 to 57.4 per cent by the second quarter of 2024 (IMF, 2024a). Interestingly, this reduction in the dollar's dominance over the past two decades has not been accompanied by significant increases in the shares of the three other members of the “big four” currencies – the euro, yen, and pound sterling (Arslanalp et al. 2022). Instead, the decline has coincided with a growing share of non-traditional reserve currencies such as the Australian dollar, Canadian dollar, Chinese RMB, South Korean won, Singaporean dollar, and Nordic currencies, reflecting central banks’ efforts to diversify their holdings (Arslanalp et al., 2022). The RMB accounted for only 2.2 per cent of global allocated reserves in the third quarter of 2024 – on par with the Australian and Canadian dollars – a modest share considering China's significant global economic role (see Figure 1) (IMF, 2024b).

Global reserve currency composition (Q3 2024).

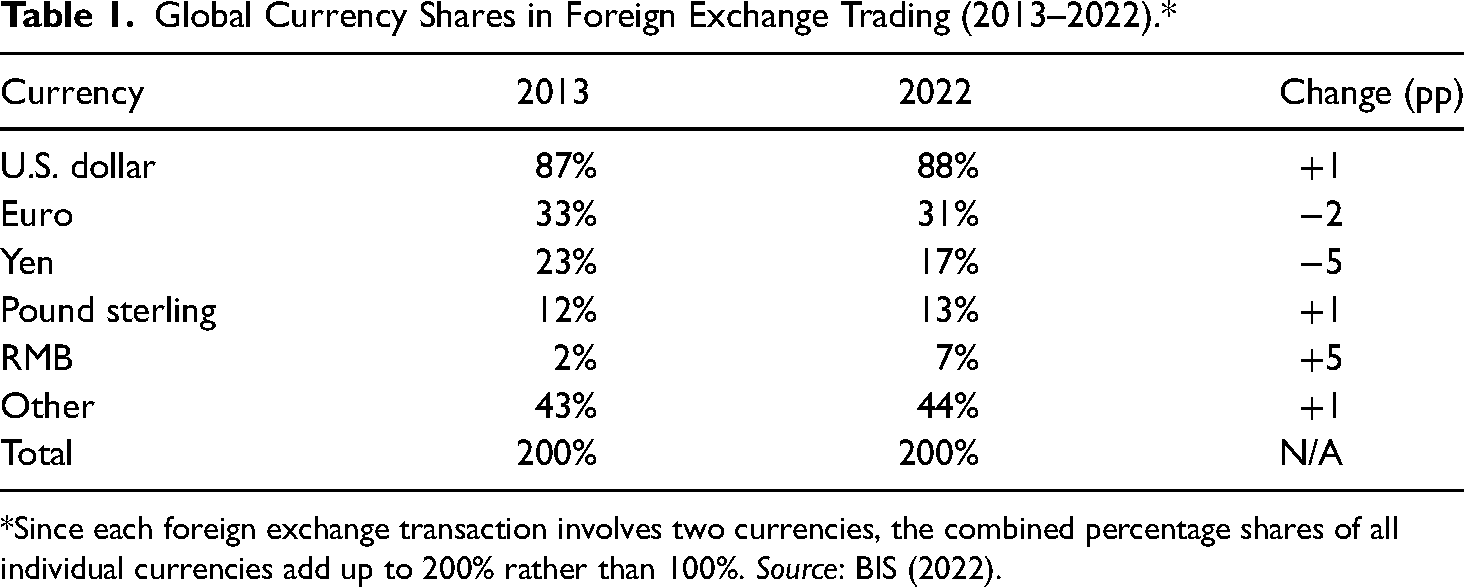

Although central bank reserves show some signs of de-dollarisation, currency trading patterns in the foreign exchange market reflect continued, and even slightly increased, dollar dominance. Data on currency used in global foreign exchange transactions from the Bank for International Settlements provides evidence for a gradual uptake of the RMB but does not support the argument for de-dollarisation in the area of foreign exchange transactions (see Table 1) (BIS, 2022). The U.S. dollar remains dominant, with its share rising slightly from 87% in 2013 to 88% in 2022. Meanwhile, the RMB experienced the largest increase from 2 per cent to 7 per cent. The euro and yen have both declined in usage (–2 per cent and −5 per cent, respectively), and the pound sterling has remained largely stable (+1%). Overall, the data highlights the RMB's growing international role but situates it within the broader context of a highly dollar-centric global financial system. While China has made inroads in advancing RMB adoption, the figures suggest that any significant challenge to the dollar's dominance in foreign exchange transactions remains a long-term objective rather than an immediate reality.

Global Currency Shares in Foreign Exchange Trading (2013–2022).*

*Since each foreign exchange transaction involves two currencies, the combined percentage shares of all individual currencies add up to 200% rather than 100%. Source: BIS (2022).

Despite its progress, the RMB accounted for only 3 per cent of global cross-border transactions in 2023, compared to 46 per cent for the U.S. dollar and 24 per cent for the euro (Amighini and Garcia-Herrero, 2023: 2). The global impact of RMB internationalisation remains modest; however, its effect on China's trade ecosystem has been more dramatic. By July 2024, 53 per cent of China's inbound and outbound transactions were conducted in RMB, a sharp rise from 40 per cent in 2021 and just 0.3 per cent in 2010 (Sandlund, 2024). Conversely, the U.S. dollar's share fell from 84.3 per cent to 42.8 per cent, illustrating China's strategic shift away from dollar reliance (Sandlund, 2024).

China has driven the RMB's cross-border adoption through initiatives such as the BRI, expanded currency swap agreements with key partners such as Saudi Arabia and Argentina, and efforts to settle more trade and investments in its currency. U.S. sanctions on Russia, which restricted dollar transactions, have greatly accelerated this trend, fostering stronger financial ties between China and Russia. Furthermore, the establishment of new RMB clearing banks in countries such as Brazil and Pakistan, coupled with Beijing's stable exchange rate policy, has encouraged broader adoption (Sandlund, 2024). As the RMB assumes a central role in China's trade payments, its growing use could have significant implications for global trade dynamics and currency preferences.

These developments reflect growing momentum behind de-dollarisation, particularly in trade settlements and cross-border payments, but they should be analytically distinguished from deeper structural shifts in global monetary power. The RMB's increased use in these transactions does not yet translate into systemic transformation at the level of global reserves or foreign exchange markets. Current trends point more towards selective diversification and hedging strategies than towards a comprehensive challenge to dollar hegemony. This distinction is important in assessing the scope and limitations of China's internationalisation efforts.

Limits and Opportunities for RMB Internationalisation

China has pursued an incremental or gradualist approach to RMB internationalisation, which is consistent with its general approach to economic policymaking and reform. Since the beginning of China's “reform and opening” era, incremental changes have allowed the country to test and adjust policies, mitigate risks, and build institutional capacity while maintaining control over the pace of reforms (Naughton, 2008). The pursuit of smaller-scale or local economic experiments has been a hallmark of this strategy, enabling China to identify successful initiatives, such as special economic zones or pilot programmes for RMB cross-border settlement, before scaling them up to the national or international level. The pace and sequence of RMB internationalisation, marked by various milestones, should be understood within this framework of gradualism.

Despite this cautious, selective, and gradual approach to internationalising the RMB, there are some major obstacles to its adoption as a significant global reserve currency, which have not been addressed to any great extent by the Chinese leadership. The first is the limited convertibility of the RMB, as China maintains a closed capital account that restricts the free flow of the currency in international markets, making it less attractive to central banks and global investors as a reserve asset. Central banks require reserve currencies to be freely convertible and easily accessible for use in times of liquidity crises or to intervene in foreign exchange markets. The lack of full convertibility creates uncertainty about the ability to exchange RMB freely, particularly during periods of financial instability. Despite the development of offshore platforms such as Hong Kong, capital controls continue to constrain the overall depth and global liquidity of RMB markets, limiting its appeal as a reserve currency for central banks.

Beijing is loath to remove capital controls not only due to concerns about financial stability and the risk of capital flight but also because of the Chinese Communist Party's (CCP) strong desire to maintain control over all aspects of the economy and financial system. Capital controls allow the CCP to closely monitor and regulate the flow of money in and out of the country, ensuring that economic activity aligns with the party's broader strategic objectives and safeguarding against potential external influences that could undermine its authority. This preference for control takes precedence over the liberalisation necessary to make the RMB a fully competitive global reserve currency. As a result, the tension between the CCP's insistence on centralised control and the demands of international financial markets is a major obstacle to RMB internationalisation.

Hong Kong plays a structurally significant role in China's RMB internationalisation strategy by serving as an offshore platform that enables currency circulation while maintaining capital controls. As the world's leading offshore RMB clearing centre, Hong Kong handles the majority of cross-border RMB settlements and hosts the most liquid offshore RMB bond market (the “Dim Sum” bond market), adding depth and accessibility to the currency beyond the mainland. Mechanisms such as Bond Connect and bilateral swap lines between the PBC and the Hong Kong Monetary Authority have embedded Hong Kong within China's broader financial architecture, facilitating cross-border flows within a tightly managed regulatory environment (GovHK, 2025).

Crucially, Hong Kong's participation in international economic law regimes under its own legal identity, distinct from mainland China, reinforces its role as a credible financial intermediary. This autonomy, grounded in the “one country, two systems” framework, provides a rule-based legal environment that appeals to international investors and facilitates RMB adoption in ways that China's domestic system, characterised by political intervention and limited legal recourse, does not (Chaisse, 2024: 9–11). This arrangement is not without limitations: growing political integration with the mainland has raised concerns about the durability of Hong Kong's distinctiveness (Chaisse, 2024: 9). As such, Hong Kong provides an important bridge rather than a destination: it facilitates RMB internationalisation within existing constraints but lacking the independent credibility, trust, and systemic openness required to elevate the RMB to a leading international currency.

Concerns about political risk and institutional trust play a key role in central banks’ reserve currency choices, with China's opaque governance, party-state-led financial system, and discretionary regulatory interventions often cited as barriers to RMB reserve adoption. Unlike the greenback, which is embedded in a system of relatively predictable legal norms and institutional checks, the RMB lacks sufficient transparency and legal insulation from political interference. As a result, many central banks remain hesitant to increase their RMB holdings, owing to limited transparency, weak legal protections, and the absence of an independent monetary authority in China.

Beyond these institutional concerns, structural path dependencies in the global financial system, China's state-managed exchange rate, shallow bond markets, and capital controls continue to limit the RMB's appeal as a global reserve currency. Nevertheless, China's position as the world's second-largest economy, its pioneering role in CBDC development, expanding BRICS and BRI partnerships, and the growth of offshore RMB platforms offer openings for broader international use. While comprehensive liberalisation remains unlikely, gradual financial reforms and selective easing of capital controls could support greater RMB adoption over time. The RMB is unlikely to rival the dollar globally in the near term, but it may increasingly function as a regional reserve currency, particularly among BRI countries in Asia and Africa, supported by currency swaps and RMB-denominated trade agreements.

Conclusion

The gradual decline of the U.S. dollar as a global reserve currency, de-dollarisation momentum, the rising share of non-traditional reserve currencies, including the RMB, and the increasing use of non-dollar currencies in trade settlements and cross-border payments all point towards a more multipolar currency system. As it stands, however, the global financial system remains dollar-centric, and any significant realignment would typically take decades – unless catalysed by major systemic disruptions. The entrenched dominance of the greenback, particularly in global finance, is underpinned by structural factors such as the depth and liquidity of U.S. bond markets – especially Treasuries – the historically widespread trust in American institutions, and the inertia accumulated over decades of dollar hegemony in global trade, finance, and reserves. Yet these expectations rest on the assumption of institutional stability and continued adherence to the rule of law within the United States. As of April 2025, Trump 2.0 is shaking those very foundations. Should this instability persist over the next four years, the pace of de-dollarisation could accelerate dramatically. What might otherwise have taken decades could, under such conditions, unfold within a single presidential term.

For the RMB to play a larger role in this evolving landscape, several changes would need to occur, such as the liberalisation of China's capital account, the deepening of its bond and financial markets, and the development of greater global trust in China's political and legal systems. Even with these changes, the transitions are likely to be gradual, as countries and institutions adapt to the risks and opportunities of a more diverse monetary framework. While such changes would be necessary for the RMB to play a larger global role, its growing share of reserves and use in regional trade and investment may already serve as stepping stones towards a system in which multiple currencies coexist, each with specific regional or functional roles. This multipolar shift would likely reflect broader geopolitical and economic realignments, underscoring the interconnectedness of geopolitics, financial power and global governance.

A final question to be pondered is whether a multipolar currency order, rather than U.S. dollar hegemony, is desirable. Views on this differ. Kindleberger (1973) argues that a single dominant currency provides stability to the global financial system by serving as a reliable anchor for trade, investment, and reserves. In the field of International Political Economy, this perspective is known as hegemonic stability theory. According to Kindleberger, the absence of a clear hegemon risks disorder, as witnessed during the Interwar period, when no country or currency was willing or able to supply the public goods essential for global economic stability, such as liquidity and a lender of last resort during crises. This argument forms the intellectual foundation for proponents of the liberal international order, who see U.S. dollar hegemony as desirable because it supports rules-based institutions, facilitates policy coordination and the maintenance of open markets, and ensures the provision of global public goods such as financial liquidity and crisis management. These mechanisms foster the predictability and cooperation that are central to the liberal system.

Critics of dollar hegemony, however, argue that it disproportionately concentrates power in the U.S., allowing Washington to unilaterally influence global financial and monetary policies to its advantage. Eichengreen (2011) suggests that a multipolar system could mitigate these imbalances by distributing power more evenly, reducing dependence on a single currency and spreading risks across multiple reserve currencies. This diversification could make the global economy less vulnerable to shocks originating in any one country. However, in the context of intensifying geopolitical rivalries, the transition from dollar hegemony to a multipolar system is unlikely to be smooth – such a shift may introduce instability, competition, and conflict. Moreover, a fragmented currency landscape could increase transactional friction and complicate the coordination of global financial policies. Whether such a system can offer stability without hegemony remains an open question.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work has received funding from the European Union's Horizon Europe coordination and support action 101079069–EUVIP–HORIZON-WIDERA-2021-ACCESS-03. Funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union or the European Research Executive Agency (REA). Neither the European Union nor the granting authority can be held responsible for them.