Abstract

In the early 1980s Argentina, Brazil, and Mexico had commercial banking sectors that were dominated by local banks. The largest countries in Latin America were subjected to common international economic pressures during both the neoliberal 1980s and 1990s – including the expansion of capital markets in the periphery and integration into the regional trade agreements NAFTA and Mercosur – and the post-1998 financial turmoil. By 2015, however, the three countries had consolidated alternative commercial banking systems: domestic private group dominated (Brazil), mixed (i.e., ownership more evenly divided among public, private domestic, and foreign banks (Argentina), and foreign bank dominated (Mexico). The article traces these alternative outcomes to the power of prereform private financial groups, the virulence of “twin crises” in the transition from fixed to floating exchange rates, and the (contingent) role played by government ideology.

Introduction

The growth and diversification of the financial sector in developing economies is at the center of the economic globalization that has swept the world since the last quarter of the twentieth century. Though the Great Recession has redeemed regulation and Keynesian interventionist tools, it is doubtful that the trend will be drastically reversed. The major features of financial globalization in emerging markets (i.e., the diversification of securities and bond markets, the free flow of capital, and the internationalization of the banking industry) seem to be here to stay. Indeed, it has been widely asserted that to effectively ride the globalization wave and attract foreign capital, governments in emerging economies have to enact reforms primarily aimed at reassuring international investors, such as anchoring domestic exchange rates, sanctioning central bank independence, and strictly adhering to the Basel requirements in the banking industry. 1 The corollary of these reforms would be the inexorable weakening of domestic financial actors, in particular public and private commercial banks that have engaged for decades in fiscal profligacy, protection, and political favors. 2

The Basel accords organize the regulatory framework on capital ratios and other issues for commercial banking worldwide.

For good reviews of this literature, see Martínez-Díaz (2009) and Stallings and Studart (2006).

However, in the three major economies of Latin America this early vision of globalization interpreters is far from taking hold. Although foreign ownership has increased almost everywhere, after two decades of thorough financial internationalization, Brazil, Mexico, and Argentina display radically different financial and banking systems. This study focuses on commercial banking, which is the former stronghold of state financial interventionism in these economies and the form most challenged by financial globalization. In Brazil, after decades of economic internationalization, private domestic financial groups are the most dynamic local players in terms of asset value and deposits. Indeed, the main Brazilian domestic group, Itaú, has internationalized to become the largest commercial bank in the Southern Hemisphere in terms of market capitalization. In Argentina public banks, along with some new local private groups, are now central players in the retail sector. In Mexico, which had an archetypical powerful Latin American financial bourgeoisie in the twentieth century, commercial banking has become almost completely internationalized in the neoliberal aftermath. For instance, by 2010 more than 80 percent of the system was in the hands of major international banks. In sum, the three largest economies of Latin America have consolidated alternative commercial banking structures in the financial globalization era: Brazil has a domestic group-dominated structure; Argentina, a mixed structure (ownership fairly evenly divided among public, local private, and foreign banks); and Mexico, a foreign bank-dominated structure.

This article seeks to describe and explain the different trajectories commercial banking systems in Brazil, Mexico, and Argentina took in order to adapt to financial internationalization, and which resulted in profoundly divergent ownership and functioning structures. The morphology of the commercial banking sector is relevant for two main reasons. First, some evidence suggests that in developing economies subject to economic uncertainties solid public and private domestic banking institutions will be more likely to expand credit for local consumers and firms across the country (Haber and Musacchio 2005; Bleger 2000). For example, the Banco do Brasil in Brazil (a mixed public/private bank) and the Banco Nación in Argentina (a public bank) account for most of the credit that flows to the agricultural sector, especially to medium and small firms. Second, and more important from a political economy perspective, the distinct outcomes of the banking structure help shape socioeconomic coalition building under neoliberalism and beyond and are relevant for understanding macroeconomic regimes. Many argue that the weight of the private banking sectors in Brazil and Mexico has been one of the factors behind the persistence of orthodox financial policy based on high interest rates since left-wing policies and ideas swept the continent. Indeed, in Brazil the political choices and alignments of the owners of the private domestic groups Itaú and Bradesco are a regular topic in the political and business press (see Bianchi and Braga 2005).

We contend that the analysis of the origins of alternative commercial banking structures should be divided into two fundamental historical stages. The first stage, which we call “exchange rate-based stabilization,” signals the period in which neoliberal governments attempted to tame high inflation through a nominal anchor. The second stage, which we call the “postliberal” or “postadjustment” period, is that where – largely as a result of international financial volatility and domestic pressures – governments free the exchange rate, often seeking an “administered flotation.” The commercial banking sectors in Brazil and Mexico underwent these two stages in very different ways. In both countries the interlude in exchange rate-based stabilization resulted in the strengthening of top domestic private financial groups in the commercial segment. In Argentina, by contrast, regulators sought banking internationalization as a way to strengthen the financial system. The Argentine government limited the intervention capacities of the Central Bank of Argentina and pushed through prudent regulations that were even tougher than the international standards set by the Basel accords, effectively weakening domestic financial actors. In Brazil the consolidation of domestic private banks continued in the postadjustment period. In Mexico and Argentina, however, the initial trends were drastically reversed after monetary stabilization and adjustment – that is, during the period of flexible exchange rates. In Mexico new regulatory changes enabled the massive expansion of the major international banks that went on to take over the main local private commercial banks. In Argentina, by contrast, the postliberal era witnessed an unlikely but extended comeback by both public and local private banks.

We have identified two variables that are crucial to understanding these alternative trajectories: (i) prereform power of the local private financial elite and (ii) the virulence of “twin crises” – that is, the simultaneous eruption of currency (i.e., capital account) and banking crises during the transition from fixed to floating exchange rates. Unlike in Argentina and other Latin American countries, in Brazil and Mexico local private banks were central actors under the import substitution industrialization (ISI) model and gathered considerable political and economic strength. Thus, they were able to politically counter the systemic denationalization tendencies triggered by the initial financial opening. Argentina, by contrast, engendered very weak local private financial groups under its inward-oriented model. These groups’ limited lobbying capacity vis-à-vis the technocratic neoliberal elite paved the way for sweeping domestic banking denationalization during the initial period of economic stabilization.

However, the strong currency and banking/insolvency crises – which signaled the end of the fixed exchange-rate regimes, the 1995 “tequila effect” in Mexico, and the December 2001 financial meltdown in Argentina – drastically changed the status quo and undermined banking “stakeholders” in both countries. Thus, the neoliberal technocracy led by President Zedillo in Mexico after 1995 radically altered policy and laid the foundations for the future denationalization of the commercial banking system. Conversely, the 2001–2002 crisis gave way to the emergence of a center-left, populist government that adopted a more interventionist financial policy. This strategy cemented a coalition between private and public domestic banks. Brazil, on the other hand, never experienced comparable twin crises: therefore, traditional private banks managed to maintain the status quo throughout the postneoliberal period.

The first part of the article discusses how our approach departs from the dominant literature on the politics of financial policy in developing economies. The second part presents the comparative-historical method we use. The third part presents a more detailed narrative of commercial bank-related financial policy and the alternative factors that shaped the outcome in each historical stage.

The Political Economy of the Financial Sector in Latin America: From Capital Account Liberalization to Varieties of Financial Systems

By the late 1980s three major issues were at stake in the area of the liberalization of finance in developing countries: (i) liberalization/deregulation of the capital account and domestic interest rates, (ii) the implementation of central bank independence, and (iii) the opening of the domestic banking system to foreign banks. Capital liberalization and interest-rate liberalization were closely tied to the short-term goals of price and exchange-rate stabilization. While the timing between exchange-rate reform, tariff liberalization, and opening to external financial flows often varied (and was hotly debated by economists), financial and interest-rate deregulation were seen as essential preconditions to cope with inflationary pressures and to reschedule debt with multilateral institutions. In the early literature the ability of mobile capital holders to threaten to exit and spark a balance of payments crisis were seen as the main triggers of capital account liberalization and exchange-rate reform – that is, the end of currency controls and of multiple regimes (Frieden 1991; Haggard and Maxfield 1996; Loireaux et al. 1997; Remmer 1998).

In Latin America the control of the money supply and the fiscal profligacy of public (especially subnational) banks were considered essential for the consolidation of price stability. Thus, for some scholars and multilateral institutions, the institutional crystallization of central bank independence and the opening of domestic banking sectors would help to stabilize sound currencies. The duration of a government's tenure and the country's need for balance of payments support (Maxfield 1997a) or the willingness of authoritarian elites in retreat to insulate economic policymaking (Boylan 2001) explained the sanctioning of central bank independence.

This early scholarship on financial openings and central bank independence in developing countries, which is generally advanced by international political economy scholars, tends to emphasize commonality – that is, how most countries were increasingly “forced” to lift capital controls and to institutionally sanction central bank independence. In contrast, the comparative politics camp began to call attention to the fact that domestic governments had more leeway to intervene with regard to the degree and timing of financial liberalization and, in particular, banking sector opening; moreover, considerable variation emerged in the politics of financial sector openings. The seminal works of Kessler (1998) and Perez (1997), for example, demonstrate that governments and domestic financial actors coalesced in order to bias the liberalization of the financial sector in favor of local banks in Mexico and Spain. For these authors, the privatization of public or government-intervened banks was a key tool for the crafting of domestic coalitions that could administer liberalization pressures. More recently, Lukauskas and Minushkin (2000), Martínez-Díaz (2009), Stallings and Studart (2006), and Epstein (2011) have similarly explored how the virulence of banking crises affect the timing and the degree of domestic financial and banking opening.

This more recent comparative political economy literature is useful to assess the different timing and styles of financial openings. Nonetheless, there is no clear explanation or conceptualization of the resulting alternative banking systems. We do not possess a theoretical or causal framework that can account for these different trajectories or for the varieties of financial and commercial banking systems that have consolidated after two decades of financial deregulation. This article is an initial effort to cover this theoretical and empirical gap.

Methods: A Comparative Historical-Institutional Approach

This study employs the comparative method based on the most similar systems design (Skocpol and Sommers 1980; Gerring 2001). Because Mexico, Brazil, and Argentina share the a common Iberian cultural background and are the three largest economies in Latin America, we held general control variables constant. As emerging developing countries, they have been exposed to roughly the same constraints from international financial markets since the early 1980s – though the cases vary, of course, with regard to the values of our explanatory variables (i.e., the type of initial banking actors, the severity of twin crises during the transition from fixed to floating exchange rates, and government ideology). These variables form the potential necessary conditions that launched these countries on their respective trajectories. 3

The identification of potential necessary conditions as a minimum claim in causal assessments based on the most similar cases design is analyzed in Gerring (2001: 211).

Comparative historical analysis provides two main advantages for our theoretical purposes. First, paying close attention to the historical sequence enables us to assess how analogous commercial banking actors in different countries undergo alternative stages of international financial pressures while expanding or shrinking their economic and political clout in the process. Therefore, we do not code the power and role played by the different state and economic actors at one point fixed in time; rather, we assess the evolution of their interaction in a classical historic-institutionalist vein (see Pierson and Skocpol 2002; Thelen 1999). In that sequence, the relevance of some variables (e.g., ideology of policymakers) is contingent on the prior existence of other factors (e.g., the onset of twin crises that fundamentally weaken stakeholders). This combination, whereby one variable only works if previously activated by some other factor, is more difficult to grasp in the large-N, econometric, and quantitative approaches that dominate the literature on banking politics (e.g., Rosas 2006). As Hacker and Pierson (2002) argue, business influence, in particular, is always relational and subjected to changes in the state and the economy, and its variation is best captured in historical sequence.

Second, the comparative historical approach allows for the qualitative distinction between two crucial periods that created alternative international pressures for domestic banks: the exchange rate-based stabilization stage (denoted by the implementation of varied forms of fixed exchange rates) and the postliberal or postadjustment moment (characterized by exchange-rate flotation). As has been widely argued, increasing levels of commercial and financial integration has underscored the salience of exchange-rate policy in the developing world, which in practice has become increasingly tied to monetary policy. Wise (2001) and Corden (2001) have posited that the transition from fixed exchange rates (based on a nominal anchor essentially oriented to tame inflation) to flexible or flotation regimes (based on the “real policy goals” approach) represents a defining moment in the consolidation of market reforms in Latin America. In general, after nominal anchors have succeeded in restraining fiscal and monetary policy, there is increased pressure for a more flexible exchange-rate regime, particularly in contexts of capital flow volatility. Indeed, the recovery of fiscal and monetary policy implicit in the (generally controlled) floating exchange-rate regimes gives policymakers greater freedom to accommodate economic interests and to adapt to sudden changes in international financial flows. In short, the transition to flexible exchanges rates by “successful” market-reforming states became both a normative goal and a political and policy imperative that could hardly be avoided (see, for example, Edwards and Naim 1997). Fixed and flexible exchange-rate regimes define two main periods of liberalization in macroeconomic terms. Both implied different opportunities and constraints in the relation between policymakers. The often-traumatic transition between these regimes is a key moment for the structure of the financial system.

Financial Internationalization and Commercial Banking: Alternative Trajectories in Brazil, Mexico, and Argentina

With the consolidation of neoliberalism under the presidencies of Salinas (1988–1994, Mexico), Menem (1989–1999, Argentina), and Franco and Cardoso (1992–1995 and 1995–2003, Brazil), each country established or consolidated a nominal anchor to control historically high levels of inflation. Whereas Argentina installed a currency board – which mandated that every peso should be backed by a dollar reserve and in practice implied that capital inflows and outflows would set the monetary base – Mexico and Brazil instituted more traditional fixed exchange-rate systems. 4 These economic schemes drastically hampered the capacity of central banks to finance the federal government and subnational states; in these three cases, however, the administrations resorted to noninflationary borrowing in capital markets.

For a comparison of the three countries as embodying similar strategies of fixed or quasi-fixed exchange-rate regimes in this period, see Frenkel and Rapetti (2010: 19–20).

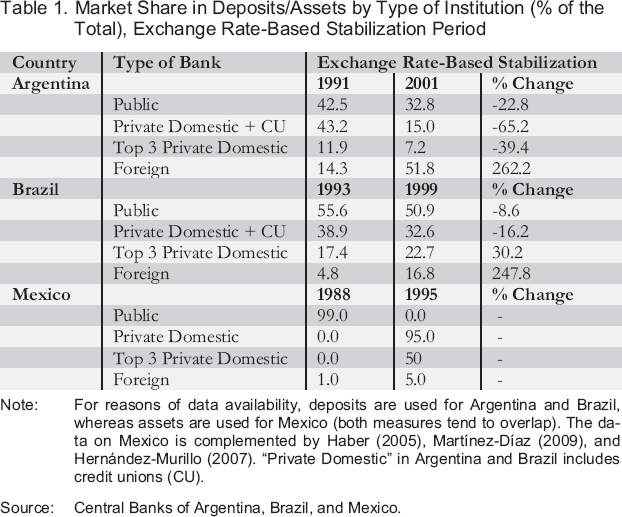

However, despite similar stabilization approaches, the impact of neoliberalism in the banking sector varied remarkably. Table 1 shows the trends in domestic banking internationalization in Brazil, Argentina, and Mexico measured as market share by type of bank in the period of exchange rate-based stabilization. In the three cases de jure or de facto central bank independence from elected authorities was sanctioned. Likewise, the capacity of central banks to act as financial regulators was notably strengthened. However, in Argentina the period of initial adjustment and exchange-rate stabilization resulted in the massive expansion of international banks. The established financial bourgeoisie and the public banks were clear losers under neoliberalism. The whole local private sector lost a remarkable 66 percent of its market share; even the largest private banks were severely weakened. Public banks also shrank by about 20 percent. It is worth noting that during this period the system witnessed a fivefold increase in deposits as a result of economic stability and growth (data in Beck, Demirgüç-Kunt, and Levine 2000).

Market Share in Deposits/Assets by Type of Institution (% of the Total), Exchange Rate-Based Stabilization Period

Note: For reasons of data availability, deposits are used for Argentina and Brazil, whereas assets are used for Mexico (both measures tend to overlap). The data on Mexico is complemented by Haber (2005), Martínez-Díaz (2009), and Hernández-Murillo (2007). “Private Domestic” in Argentina and Brazil includes credit unions (CU).

Source: Central Banks of Argentina, Brazil, and Mexico.

In Brazil and Mexico the financial sector also deepened during stabilization. Yet, the power of both state and private domestic banking actors to resist the strains of neoliberalism was much stronger. In Brazil state banks lost about 8 percent of their market share. 5 The entire local private banking sector, which had approximately the same market share as its Argentine counterpart previous to the reform, only lost 16 percent. However, the top echelons of the established financial bourgeoisie increased their market power by 30 percent. Finally, while foreign banks also made significant inroads, their overall share remained quite limited. In Mexico, the expansion of local private banks during the initial stage of neoliberalism was more spectacular and was largely a consequence of the privatization strategy of the government. The commercial banking sector was formally nationalized in 1982. As we shall see, massive state disinvestment in 1991–1992 privileged domestic financial groups. This reconfiguration of the banking system from scratch in Mexico makes the calculated percentage change in market share during the period less useful. Yet, Table 1 shows that during the initial stage of neoliberalism, the Mexican financial elite emerged as the strongest private actor by far among the three countries: in Mexico the three largest local private banks had 50 percent of the market share; in Brazil, 22.7 percent; and in Argentina, just 7.2.

It is worth stressing that we are analyzing commercial banking. Therefore, state development banks that do not take deposits, such as the Brazilian Development Bank (BNDES) in Brazil, are excluded.

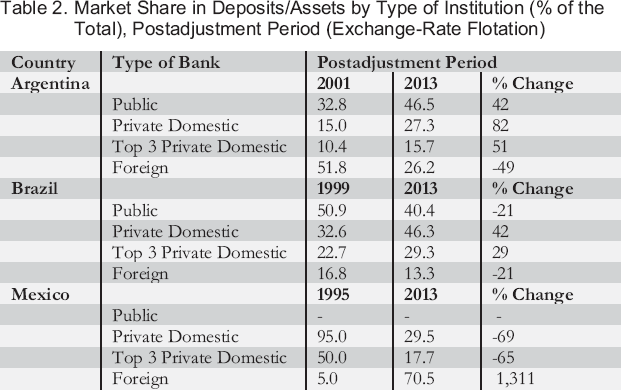

The poststabilization period (table 2) witnessed more similar trends in Argentina and Brazil, as domestic financial actors gained market share in both cases. In Argentina denationalization was largely reverted. After the 2001 crisis and under the Duhalde, Néstor Kirchner, and Cristina Fernández de Kirchner governments public banks recovered and local private banks doubled their share – though within a downsized banking system. At the same time, international banks shrank by 50 percent during the postadjustment period. Brazil witnessed more continuity in the postliberal period under President Lula, with the local private sector continuing to thrive and increasing its market share to 46 percent. Foreign banks only essentially preserved the market obtained in the early stages of neoliberalism. The contrast with Mexico is remarkable, where local banks were decimated after 1995. A series of regulatory changes paved the way for major foreign banks to make massive inroads in the country and take over the recently reprivatized banks. The public commercial banking sector, historically weak in Mexico, remained nonexistent.

Market Share in Deposits/Assets by Type of Institution (% of the Total), Postadjustment Period (Exchange-Rate Flotation)

In sum, by the end of the first decade of the twenty-first century, the trajectory of financial reform taken by these countries resulted in three distinct commercial banking systems: a domestic group-dominated system in Brazil, a mixed system (in which ownership is more evenly divided among public, private domestic, and foreign banks) in Argentina, and a foreign bank-dominated system in Mexico.

Explaining the Outcomes

What explains these different trajectories? Why were local financial actors, who were decimated under neoliberalism, able to recover in Argentina during the postadjustment period? Why was the domestic financial bourgeoisie able to thrive in Brazil under neoliberalism and beyond despite the expected inroads made by foreign banks? Finally, why did Mexico, with its archetypical powerful Latin American financial bourgeoisie in the twentieth century, witness the almost complete denationalization of its banking sector?

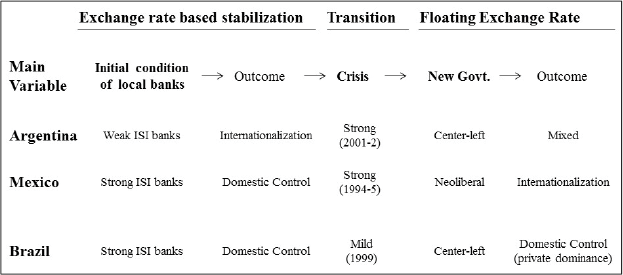

Figure 1 sketches both the historical periods and the main variables that produced the outcome of a certain banking structure. We argue that the key factor that explains the level of bank internationalization during the initial stabilization period is the power that domestic private financial elites generated under the inward-oriented model – that is, during the preneoliberal period. As we show below, Mexico and Brazil developed strong domestic financial private sectors during import substitution industrialization (ISI). In Brazil the source of this strength primarily stemmed from inflation revenues; in Mexico, from the financial elite intermediation with industry. In both countries, however, the domestic financial elite used their political connections and economic power to bias liberalization and financial asset privatization in their favor and consolidate their market power. In Argentina, by contrast, for reasons that we explain below, a domestic financial elite never took hold under the inward-oriented model. Thus, it was easy for neoliberal policymakers during the Menem presidency (1989–1999) to impose liberalization on weak actors that were already in retreat and to allow massive internationalization.

Period Exchange Rate–Based Stabilization Transition Floating Exchange Rate

Yet, in the cases where the momentous transition from fixed to floating exchange rates resulted in severe twin crises (currency and banking crises), which shook the banking status quo, the emerging governments had more leeway to recraft the domestic banking sectors, which were in desperate need of help and funds. In Mexico the orthodox neoliberal wing of the PRI, led by Zedillo (1995–2000), consistently favored international banking after the “tequila crisis” and the peso devaluation in 1994. The populist, center-left governments of Duhalde and the Kirchners (2002–2011) in Argentina, by contrast, privileged domestic public and private banks in the reconstruction of finance after the unprecedented 2001 crisis. Meanwhile, in Brazil the transition from a fixed to a floating exchange rate in 1999–2000 was relatively smooth. Thus the (federal) state and especially the private banks that managed to weather the storm of liberalization achieved dominance, though the market became more competitive. In this case, however, the ideology of the postliberal government is less relevant because the structural power of the top local private banks was unaffected by the crisis; instead, they maintained the status quo of the initial neoliberal period.

In short, these dramatic shifts in the retail banking sector, both between ISI and the neoliberal period and during the postadjustment stage in the first decade of the twenty-first century, cannot be explained solely in terms of commercial strategies vis-à-vis consumers and firms. Politics, coalitions, and the alternative impact of currency and banking crises also mattered. The next section describes in more detail the (de)nationalization trends and the role played by the factors just discussed.

The Period of Exchange Rate-Based Stabilization

Brazil: The Power of Domestic Financial Groups

In Brazil stabilization and the liberalization of the current account in the early 1990s brought about unprecedented challenges to the banking sector. As in most neoliberal experiences, the government strengthened the regulatory powers of the Central Bank of Brazil (BCB), forged ahead with a deposit insurance system, and complied with the Basel criteria for capital requirements. However, with the introduction of the Real Plan in 1994, Cardoso also implemented the Temporary Special Administration Regime (RAET), which empowered authorities to liquidate, recapitalize, or restructure and sell banks under stress. Between 1994 and 1997 the BCB went on to control about 17 percent of the banking system (40 financial institutions out of 242) – which included both public (federal and state) and private commercial banks (Stallings and Studart 2006: 226).

RAET was complemented by a series of BCB programs designed to execute the final reconversion of the different bank types into new entities. The Program of Incentives for the Restructuring and Strengthening of the Financial System (PROER) was introduced by decree in 1995 for private banks. It offered tax incentives and credit facilities for acquiring banks. The Program of Incentives to the Reduction of State Public Sector in Banking Activity (PROES) and the Program for the Strengthening of the Federal Financial Institutions (PROEF) – both launched in 1997 – established similar programs for state banks and national public banks, respectively. Of course, the main political battle was waged between the federal government and regional states, which owned faltering banks. State (i.e., provincial) banks had traditionally jeopardized the centralized management of monetary policy in Brazil and had provided governors with sources of uncontrolled spending. In 1995, in the midst of financial turbulence, RAET put the two major state banks – the bank of Sao Paulo (Banespa) and the Bank of Rio de Janeiro (Banerj) – under federal control (see Beck, Crivelli, and Summerhill 2005).

The administration initially privileged the largest local financial conglomerates in the privatization of state banks and intervened banks. Banerj and, later, the Bank of Minas Gerais and the Bank of Goias were awarded to the domestic group Itaú. Unibanco was granted the government-revamped Banco Nacional through the facilities offered by PROER. Bradesco, the third major local bank, acquired the Bank of Bahía and Credireal, a state bank in Mina Gerais. 6 It is worth noting that most of these privatized banks retained all the functions as employee paymasters and managers of provincial state administration accounts. Thus, the three main local private banks consolidated their market positions through auctions in which foreign banks were largely banned from participating. The government did, however, turn to foreign capital if local corporations could not afford or were reluctant to take over banking facilities (Rodrigues de Paula 2003). This approach enabled the administration to achieve its twofold goal of obtaining higher sale revenues and injecting competition.

The privatization of Banerj offers a good example of the coalition between the government and domestic financial groups. The government hired the domestic investment bank Bozzano to organize the sale, which finally awarded the bank to the domestic group Itaú in a bidding process in which no foreign bank could participate (Baer and Nazmi 2000: 15).

In sum, although the major Brazilian banks did not develop extensive ties with industry during ISI as did their Mexican counterparts, they were undoubtedly powerful players who had fared well under ISI. Inflation provided easy revenues as banks paid low or negative interest rates on the excess of demand deposits over reserve requirements. It also reduced the real value of liabilities and added liquidity, which made it easier for borrowers to repay loans (Baer and Nazmi 2000: 6). 7 Brazilian banks also profited from the opportunities in secondary markets, which had been opened by the reform initiated by the military regime (1964–1985). Therefore, their power was fueled by two essential revenue sources under ISI. The first source was so-called treasury operations, which consisted of trading government bonds subject to indexation. The second source was the menu of basic services through which domestic banks granted cash-starved consumers rapid access to their accounts. 8 Thus, despite macroeconomic instability, the private banking sector boomed in Brazil during the 1980s and early 1990s. Unlike in Argentina, the semiclosed economy in Brazil engendered massive private financial actors under ISI – especially Itaú, Bradeso, and Unibanco – who had developed the economic power and know-how to profit from controlled financial liberalization.

On the massive growth of Brazilian banks in the inflation period, see also Carvalho 1998 and 2000.

Indeed, unlike in other developing economies, currency substitution was never relevant in Brazil. Thus widespread indexation and payments system innovation induced the general public to maintain their funds in the domestic banking system (see Carvalho 1998: 304 and Baer and Nazmi 2000: 8).

Mexico: The Traditional Lobbying Power of the Financial-Industrial Conglomerates

The commercial banking sector in Mexico was nationalized in 1982 by the Lopez Portillo administration in an attempt to halt capital flight in the wake of the debt crisis. Yet the clash with the private sector did not last. The De la Madrid administration (1982–1988) focused on taming inflation by introducing major monetary and fiscal reforms. President Salinas (1988–1994) pressed ahead with further financial and market liberalization and dismantled the structures of financial repression by freeing up interest rates and lifting credit controls and reserve requirements on private banks. This move increased the amount of credit available to the private sector and sought to diversify financial instruments by allowing banks to issue short-term letters of credit and permitting the formation of nonbank financial holding companies (Maxfield 1997b: 11–12). Investment in commercial paper enabled banks to enter an already burgeoning market dominated by the stock brokerage houses, which had grown after the 1982 liberalizing reforms.

Despite widespread liberalization, bank reprivatization and integration into the North American Free Trade Agreement (NAFTA) were carried out in a way that accommodated and benefited the interests of the established financial-industrial elite. The privatization legislation passed in 1990 did not allow foreign banks to participate in the bank auctions and did not permit international financial enterprises to participate in financial intermediation in national markets – though the latter could perform banking functions with nonresidents. Moreover, the legislation also encouraged the formation of local financial holding companies. As Haber (2005: 2329) notes, by not breaking up the concentrated structure in which four banks controlled 70 percent of total bank assets, the Mexican government signaled to bidders that they would not have to act in a competitive environment. In order to prop up prices, accounting standards were not modified – for example, when a loan was past due, only interest in arrears was counted as not performing, and the loan could be rolled over. In sum, concentration, a lack of competition, and weak accounting standards turned banks into an attractive prize.

The traditional Mexican economic groups, whose ties with the financial sector had been sundered by the 1982 expropriation, were important beneficiaries of bank reprivatization. For example, Bancomer and Serfin – two of the largest three banks in terms of asset value – came to be controlled by the traditional economic groups Visa and Vitro, respectively. Banamex, the largest bank, was purchased by relatively new financial players that owned stock brokerage houses. Protection of course continued in the wake of the NAFTA negotiations, during which the recently empowered bankers engaged in intense lobbying. 9

In words of Kessler (1998: 48), “The same Mexican negotiators who conceded significant trade and services concessions in NAFTA fought tenaciously to with the US to guarantee that Mexican banks retained strong protection against foreign competition.” See also Maxfield 1997b.

The main factor that explains this state alliance with domestic economic groups in the reprivatization of banks was the traditional power of the financial bourgeoisie. Like in Brazil, in Mexico a private-financial elite was able to consolidate itself as a key player under the inward-oriented model. Indeed, in Mexico the state never made real inroads into the commercial banking sector and mostly operated in investment banking through Nacional Financiera (Nafinsa). Unlike in Brazil, however, this banking elite was linked with the main domestic economic groups through a complex web of cross shareholding and interlocking directories. 10 Thus, Mexican private banks profited from their primary role as financiers (and owners) of the main industrial conglomerates in an environment of tighter monetary policy and stronger currency. 11 Moreover, the influence of Mexico's banking elite (which, we should stress, was financial as well as industrial) did not cease after the nationalization of banks in 1982. As Maxfield (1997b: 106–107) contends, the neoliberal government hastened to counter the effects of nationalization on the private sector by relinquishing the control of nonbank stocks, preserving the independence of bank management, and encouraging the conglomeration of nonbank financial enterprises in a burgeoning liberalized market for portfolio investments. Thereafter, Salinas's banking policy essentially served as a coalitional fulcrum for his alliance with the main economic conglomerates that had dominated the Mexican private sector and had mostly gone unharmed during the events of 1982. 12 Some traditional families and groups changed roles and banks, but the main point is that the initial phase of financial liberalization consolidated a traditional private oligopoly. As Kessler (1998: 49) argues, the protection of local banks under Salinas was geared “to cement the PRI's partnership and alliance with Mexico's wealthiest and more powerful capitalists.”

Camp (1989: 173–190) well describes this financial-industrial elite based on interlocking directorates and argues that Mexican private bankers “have exerted an unusually significant influence over Mexican government policy” (Camp 1989: 175).

For a comparison of the Brazilian and Mexican preneoliberal financial elites in this vein, see the excellent study by Maxfield 1991.

Some new local financial players in the secondary markets, the bolseros, also had a prominent role in the bank reprivatization of 1991–92 (see Minushkin 2002). But, according to Minushkin and Parker (2002: 217), “The essential nature of the relationship between the financial sector and the government survived.”

Argentina: The Weakness of Domestic Financial Capital

The Argentine economy went through significant transformations during the 1990s, which radically reconfigured both state–market relations and domestic business groups. After taming high inflation and balancing the budget, the government implemented a broad financial reform. In 1991 the economy minister, Domingo Cavallo, launched the Convertibility Plan, which tied the peso to the dollar and limited the monetary base to the level of international reserves in hard currency; this turned the Central Bank of Argentina (BCRA) into a de facto currency board. The administration enacted a new BCRA charter and introduced innovative prudential regulations.

Moreover, the devaluation of the Mexican peso in December 1994 triggered a confidence crisis in Argentina that deepened the massive restructuring of its banking sector. The run hit wholesale banks in particular, as well as provincial, cooperative, and small retail banks. Several policies were launched to pave the way for the expansion of international banks. A privately owned deposit insurance company (Seguro de Depósitos S.A., SEDESA) and two trust funds (Fondo Fiduciario para la Capitalización Bancaria and Fondo Fiduciario para el Desarrollo Provincial) were established with the purpose of financing the merger and acquisition of small and medium-sized banks.

Stringent banking regulations and supervisory mechanisms were implemented in line with the Basel recommendations. The BCRA established high minimum-capital requirements in a horizontal manner. Private-monitoring norms and a formally noninterventionist policy that left troubled banks subject to market forces biased the prudential system in favor of the largest international financial conglomerates (Wierzba and Golla 2005). As expected, the outcome of the process was further foreignization and greater concentration of the financial system – a trend intensified by the tight monetary regime's squeeze on liquidity (Bleger 2000). The authorities reacted to these events by strengthening their commitment to convertibility institutions, thus increasing exit costs. Restrictions to liquidity fueled the dollarization of contracts. In 1994 53 percent of deposits were denominated in US dollars; in 2001, 68 percent. Dollarization ratios were even higher for loans and fueled the profitability of international banks, which faced no (apparent) exchange-rate risk. Significantly, in contrast to prudential regulations that accounted for multiple types of risk, no policies were passed to keep banks safe from an eventual devaluation.

In short, foreign entry was explicitly encouraged through a series of incentives and a very permissive legal framework. Foreign banks sought to exploit the advantages of the installed retail network. The extent of the local banking sector's retrenchment was impressive. By 2000, only one large private domestic bank, Galicia, remained open as a locally owned private entity. Out of around 38 cooperative banks, 2 remained in 2001. Unlike in Brazil, state (provincial) bank privatization was not used to strengthen major local commercial private banks strained by sectoral liberalization (Clarke and Cull 2001).

The main difference between Mexico and Brazil at this stabilization stage was the traditional weakness of the domestic financial elite. Unlike in the industrial realm, in which massive domestic economic groups flourished, in Argentina large financial groups never consolidated during ISI. The origins of the Argentine financial elite's “weakness” (Thorburn 2004: 165, 206) under the inward-oriented model were twofold. First, the early integration of Argentina into world markets during the agrarian boom of the early twentieth century paved the way for the arrival of foreign banks in a way unmatched in Brazil and Mexico. Second, the extremely unstable macroeconomic environment during the postwar period favored booming banks, which eventually collapsed in expensive failures. Unlike in Brazil during that period, where three “majors” dominated local commercial banking under ISI, in Argentina the weakness of local actors was reflected in the volatile bank rankings. Tellingly, the two major private banks in the early 1980s were liquidated and their owners imprisoned (Quintela 2005). In Brazil domestic private banks profited from and thrived under high but controlled inflation. In Argentina, by contrast, extreme macroeconomic instability (including three episodes of near hyperinflation in 1975, 1989, and 1990) and the absence of vibrant secondary financial markets precluded the consolidation (even the survival) of any major domestic financial group. Weakly integrated local financial conglomerates with tenuous links to the much larger industry-based economic groups were easily displaced during the neoliberal period; they were simply not at the policy discussion table. Moreover, the importance of cooperative banks and credit unions in the semiclosed economy (which accounted for 15 percent of the private sector in 1991 and was much less prepared to cope with international competition) signaled the prereform internal heterogeneity and atomization of the private financial sector in Argentina.

The Transition from Fixed to Flexible Exchange Rates: The Role of Twin Crises and the Postliberal Structure of Banking in Mexico, Argentina, and Brazil

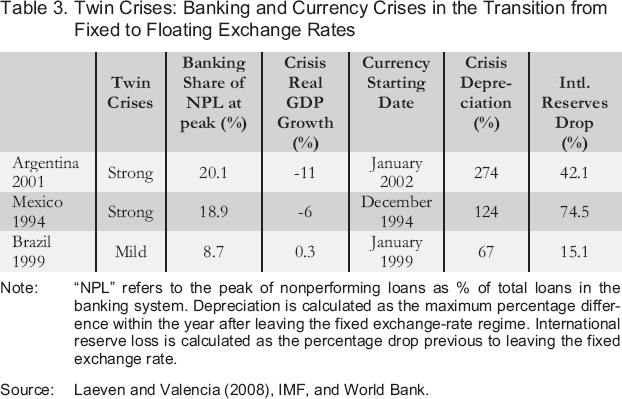

In the economics literature almost every transition out of a fixed exchange-rate regime is classified as a currency crisis (Kaminsky and Rein-hart 1999; Laeven and Valencia 2008). Here we define twin crises as the simultaneous occurrence of a currency crisis (i.e., massive capital flight that triggers devaluation) and a financial/banking crisis (i.e., an extended degree of insolvency in the banking sector). In Table 3 we try to give a sense of the severity of both of these episodes during the transition from fixed to flexible exchange rates in Argentina, Brazil, and Mexico.

Twin Crises: Banking and Currency Crises in the Transition from Fixed to Floating Exchange Rates

Note: “NPL” refers to the peak of nonperforming loans as % of total loans in the banking system. Depreciation is calculated as the maximum percentage difference within the year after leaving the fixed exchange-rate regime. International reserve loss is calculated as the percentage drop previous to leaving the fixed exchange rate.

Source: Laeven and Valencia (2008), IMF, and World Bank.

In Mexico political and economic instability throughout 1994 triggered a massive run on peso-denominated assets. The government was forced to devalue the peso by 15 percent in December. Moreover, to slow capital outflows, the administration raised interest rates to 80 percent in the first quarter of 1995. 13 Government debts and bank debts soared; according to one estimation, foreign currency liabilities of banks increased by 47 percent just in a few days (Martínez-Díaz 2009: 54). Overall, real depreciation reached 124 percent within a year, GDP fell by around 6 percent, and international reserves dwindled by 74 percent (table 3).

The bibliography on the peso crisis in Mexico is of course vast. For an overview, see Edwards and Naim (1997).

The financial institutions most affected were two of the largest and recently privatized banks, Serfin and Banamex. In view of the crisis, the new Zedillo government implemented the Banking Fund for the Protection of Savings (FOBAPROA), which enabled banks to clean their balance sheets by swapping nonperforming loans for a 10-year FOBA PROA coupon at relatively low interest rates (Haber 2005: 2342–2343). This massive bailout gave the government enormous leverage to reshape the banking industry. Zedillo belonged to the most neoliberal wing of the PRI. Indeed, when deregulation was initiated during the early 1990s, as minister of planning and budget, he opposed protection for domestic banks (Martínez-Díaz 2009: 57). As president, Zedillo announced that the fundamental recapitalization of the banking system could only come from foreign retail institutions. The first package of legislation passed in 1995 increased the noncontrolling type of shares available to foreigners and lifted ownership limits for international banks. In 1997 the Revolutionary Institutional Party (PRI) lost control of Congress in the mid-term elections, which cleared the way for a coalition between the neoliberal faction of the PRI and the right-wing Autonomous National Party (PAN). What followed was a series of reforms that lifted any ceiling to foreign entry and removed the old 20 percent limit on individual equity ownership. The domestic financial bourgeoisie was powerless to counter these reforms. The first policy package was not openly opposed by the “big three” (Banamex, Bancomer, and Serfin), which dominated the local banking association, because the foreign capital limits still protected them. By 1997, however, Serfin was experiencing increasing problems and was taken over by the government and put under the FOBAPROA program. The rest of the top local banks were also full of toxic assets and undercapitalized, which was conveniently masked by regulators’ accounting standards (Haber 2005). Given these banks precarious situations and the new liberal regulations, a cascade of foreign takeovers ensued. In the largest FDI transaction in Mexican history, Citigroup paid USD 12.5 billion for Banamex in May 2001. 14

For details of these foreign takeovers, see Thorburn 2004 and Martínez-Díaz 2009.

Once the established banking system had been shaken by the crisis, Zedillo had ample room to push forward his neoliberal view. Significantly, in 2000 Banamex, the largest local bank, tried to bid for Bancomer – a merger that would have brought about a financial “national champion,” much in the way Brazil and Spain had empowered domestic financial groups during the liberalization of their banking sectors. However, Zedillo regulators blocked the acquisition, citing the “perils of concentration,” and eased the way for Spain's BBVA to complete the takeover of Ban-comer (see Minushkin and Parker 2002). Meanwhile, the other Spanish major bank, Santander, acquired the Serfin Group. The argument is not that Mexico could have endlessly protected its banks in the context of NAFTA, but rather that the twin crises and Zedillo's neoliberal technocracy prevented the creation of strong national financial groups that could have survived and even profited from the newly liberalized order, as they did in Brazil.

Although the 2001–2002 Argentine crisis was certainly not an endogenous banking crisis, major socioeconomic turmoil erupted when Cavallo, the economy minister, announced – on the eve of a major bank run – the (partial) suspension of the convertibility of banking deposits (el corralito). Capital movements abroad were also severely restricted. President De la Rúa could not resist the social uprising that ensued and resigned. Argentina defaulted on its sovereign debt, and Eduardo Duhalde was appointed by Congress as the provisional president and inaugurated his administration by formally devaluating the peso. He was succeeded in 2003 by the democratically elected Nestor Kirchner. The consequences of the 2001–2002 crisis were devastating for the economy and the financial sector: GDP dropped 11 percent, international reserves dropped 40 percent, the peso depreciated almost 300 percent within a year, and the amount of nonperforming loans totaled a fifth of the system (table 3).

As in Mexico, though with different consequences, this major crisis had a destabilizing impact over the status quo in the commercial banking services. In contrast to the neoliberal 1990s strategy, an interventionist approach became the rule and was used to avoid bank failures. Financial restrictions on the public were intensified by the reprogramming of all the term deposits and even of some demand deposits denominated in US dollars (el corralón). The BCA charter was amended to give the monetary authorities wider possibilities of granting assistance through the discount window. The government mandated that every peso discounted to a foreign-owned bank had to be matched by a peso from the bank's “First World”-based mother companies (Yeyati and Valenzuela 2007). However, the banks’ headquarters were reluctant to back their subsidiaries with fresh capital. The government's support for established local banks contrasted with the risk-averse nature of managers accountable to foreign stockholders. Indeed, the postliberal period in Argentina witnessed the growth of a group of domestically owned private banks. Most of these new local commercial banks came from the wholesale segment. They had profited from the privatization of provincial and municipal banks and forged important political connections. In the aftermath of the 2002 crisis they acquired a group of foreign banks willing to leave the country (García 2006), although top foreign institutions remained. The publicly owned Banco Nación, the largest bank in the system, temporarily administered the fleeing institutions. It capitalized and cleaned the balance sheets of troubled banks before carrying out reprivatizations that favored a group of local bankers.

The local Macro Group is a paradigmatic case of the comeback of private banks. It jumped from a marginal position to being the 22nd largest bank (measured by deposits) in 2001 and the 6th largest bank in 2009. By 2010, it was also ranked as the second largest bank in terms of territorial reach – second only to the state-run Banco Nación. Comafi, Patagonia, and the Petersen Group banks (Bancos San Juan, Santa Cruz, Santa Fe, and Entre Ríos) are other medium-sized, fast growing banks that followed a similar trajectory. Indeed, the poststabilization period in Argentina also witnessed the organizational resurgence of the private domestic banks. The Association of Argentine Banks (ADEBA) was relaunched by Jorge Brito, the main shareholder of the Macro Group. The new association stayed close to the Kirchner administrations until 2011, supporting most of their financial policies. Of course, the benefits of this new financial interventionism to local actors were possible in a context of a more expansive economic and monetary policy. The successful renegotiation of the sovereign debt and the resumption of economic growth and exports under the Kirchner presidencies provided government with extra leverage over international financial players. In November 2008 the individual capitalization pension regime (created in 1994) was nationalized, which resulted in the transfer of considerable financial assets to state management. Many of them were liquid deposits placed in the domestic banking system, which were partially redirected toward public banks, enhancing their participation in the market.

In Brazil the crisis that triggered the end of the fixed exchange rate was much less virulent by almost any measure than in the region's other major economies. The rate of nonperforming loans, currency devaluation, and the decrease in international reserves was less than half that in Argentina and Mexico, and there was no fall in GDP (table 3). Though the local financial system was subjected to severe strains during the 1999 devaluation and again during Lula's run-up to the presidency in 2003, there was no major economic or social dislocation. Furthermore, the milder crisis in the transition to a flexible exchange rate did not affect the major banks but rather heavily favored the status quo. Thus, the dominant players of the neoliberal period – namely, the local private banks – were able to expand and takeover those institutions that could not afford international competition and those international banks that left the Brazilian markets in view of their regional and global strategies. Itaú and Unibanco (which merged in 2008) and Bradesco bought a number of smaller banks and became prominent regional actors in the financial sector. Moreover, the privatization of (provincial) state banks, which was financed by the central government and favored major local banks, continued after 1999 with, for example, Itaú purchasing the Bank of Parana (Banestado) and the Bank of Goias.

Alternative Explanations: International Trade Agreements and Bailouts

Interestingly, factors such as international trade agreements and the existence of massive foreign bailouts cannot explain the above-analyzed trends in commercial banking services. First, the resulting type of commercial banking structure was unaffected by the consolidation of alternative international trade agreements in Mexico (NAFTA) and in Brazil and Argentina (Mercosur). The initial NAFTA accords witnessed the paradoxical consolidation and protection of local industrial groups and their associated banks, as shown above. Indeed, besides the Citibank, the major banks that later took over most of the Mexican system were Spanish (BBVA and Santander) and not from the NAFTA area. This massive Spanish inroad signals the relative influence of the United States and NAFTA in Mexican banking policy. Meanwhile, the two Mercosur countries underwent diverging trends during the initial neoliberal period during the 1990s: liberal deregulation favored foreign banks in Argentina, whereas protection strengthened local banks in Brazil.

Second, the occurrence of financial bailouts also fails to explain the final banking structure. Although President Zedillo used the massive international bailout backed by the IMF and the United States after 1995 to strengthen the government's financial resources, “clean” the banking system under FOBAPROA, and advance a policy of internationalization, he could have used the bailout resources to strengthen domestic banking groups and promote financial national champions, as Brazil and Spain did under neoliberalism. This possibility, as noted before, was deliberately ruled out by the Zedillo government. The fall of local banking groups during the peso crisis was, so we argue, the precondition for their loss of political and economic clout and their ultimate demise. Similarly, the absence of an external bailout did not deter the Kirchners’ ideological convictions regarding the role of international capital. Once the dominance of foreign banks was undermined by the crisis, Néstor Kirchner's left-wing populist government used state power and the liquidity that resulted from monetary policy expansion to reshape the banking system on more nationalist grounds.

In sum, once in power after the twin crises, Zedillo and the Kirchners had access to new resources stemming from alternative sources: a massive international bailout (Mexico) and a recovered and expansive monetary policy in the context of increasing export revenues (Argentina), respectively. Both profited from a strong crisis that broke the financial status quo, which allowed them to pursue their (contrasting) ideological approaches during the reconstruction of the commercial banking sector.

Conclusions

The notion that financial internationalization leads to the fundamental weakening of domestic financial actors in emerging markets has proved to be wrong. In some cases, such as Mexico, international banks have effectively come to control most of the local financial commercial sector. In other cases, such as Argentina and Brazil, domestic banks control over 70 percent of the local commercial banking system. Only Brazil, however, has generated strong domestic financial groups that have deepened the local financial sector and are able to compete successfully in regional markets.

After initially concentrating primarily on the determinants of capital account opening, comparative political economy went on to study alternative “styles” and the timing of financial openings in emerging markets subjected to neoliberal restructuring. However, this literature has not produced an explanatory framework that can account for the different trajectories taken by financial actors and the current alternative banking systems. Moreover, when the literature on varieties of capitalism is extended beyond its original focus on advanced countries to include developing and Latin American countries (see Schneider 2013; Etchemendy 2011; Royo 2008), it is even more necessary to conceptualize and explain the different institutional configuration of markets. This article is a step in that direction.

We argue that during the period of exchange rate-based stabilization, the prereform power of domestic financial groups shaped the divergent fates of domestic private banks in Brazil, Argentina, and Mexico. Once the “new” status quo was established in the liberalized markets, however, the transition to more stable macroeconomic schemes based on exchange-rate floatation played a key role. Massive twin crises (i.e., simultaneous currency and banking crises) were witnessed in both Argentina and Mexico, severely damaging the status quo that emerged during neoliberalism – namely, foreign bank domination in Argentina and the consolidation of the traditional, prereform financial-industrial groups in Mexico. Thus, the liberal government of Zedillo facilitated foreign bank penetration in Mexico, while the populist and center-left governments of Duhalde and the Kirchners promoted the resurgence of local public and private banks in Argentina. In Brazil, by contrast, the smoother transition to a floating exchange-rate regime reinforced the private banking groups that had adapted during the initial stage of neoliberalism. In sum, the trajectory of commercial banking liberalization in the three major economies of Latin America suggests that the social and economic power of established banks trumps broader ideological trends. Only when severe twin crises destroy the status quo, as happened in Argentina and Mexico, are governments able to push ideologically defined financial policies that reshape the commercial banking system.