Abstract

While scholarly and public attention on institutional investors in rental housing is considerable, studies that quantify the relevance of such actors are still rare. This article measures institutional investor ownership in a European city with one of the highest shares of social housing: Vienna, Austria. We present a novel approach to measure institutional investor ownership that combines land registry data with the international company database ORBIS and Vienna’s local housing register. This provides unique ownership data for the entire housing market at the property level. We measure the role of institutional investors in different rental tenures and further distinguish between direct and indirect property owners, between national, EU, and non-EU investors, and conduct a geographical analysis of investment hotspots. We make three broader contributions: First, we widen the geography of research on institutional investment by considering a highly regulated housing market context. Second, we demonstrate that a large social housing stock does not per se prevent a significant presence of institutional investors. Third, we introduce a method that may be used in other cases and contexts.

Keywords

Introduction

There is growing attention among researchers, housing activists, and policy makers on the role of institutional investors in rental housing (Gabor and Kohl, 2022). Such investors, inter alia in the form of private equity firms, hedge funds, banks, pension funds, and insurance companies (Gabor and Kohl, 2022) have gained importance in a number of economic sectors in recent years. Housing, and rental housing in particular has become a major target in this respect. It is perceived as a stable and safe asset class, especially in cities, where housing demand and market pressures are high. Indeed, recent research suggests that in Europe alone, the biggest investors together manage at least 1 million rental apartments in a total of 10 countries (Holm et al., 2023: 13). 1 Ownership by institutional investors has been associated with declining affordability and worsening housing conditions (Fields and Uffer, 2016; Holm et al., 2023; Raymond et al., 2016), raising critical concerns about this development (Soederberg, 2018).

Scholars have investigated the emergence of institutional investors, initially focused on Germany (Holm, 2010a, 2010b) and the United States (Fields, 2015), yet more recently expanding to a wider range of European (Belotti and Arbaci, 2021; Bernt et al., 2017; Beswick et al., 2016; Byrne, 2020; Janoschka et al., 2020), Global South, and East contexts (Aveline-Dubach, 2022; Chen et al., 2022; Guerreiro et al., 2022; Migozzi, 2020). While thus tracing the expansion into rental markets in ever more terrains, this research, furthermore, has demonstrated the variegated ways in which a global pool of investors enters local real estate markets. Institutional investors have become increasingly important across more contexts, yet they interact in complex ways with pre-existing housing policies and regulatory landscapes, calling for context-specific case studies and analyses that account for local market and institutional structures (Holm et al., 2023: 9).

This article responds to this call by examining institutional investors in the rental market in a city that has so far not been in the focus: Vienna, Austria. The aim is to provide a fine-grained empirical analysis of ownership patterns to establish the role of institutional investors in different rental tenures. The results are interpreted against the background of policies, institutional constellations, and path dependencies that have directed such investors to and away from different tenures.

We make three broader contributions: First, we widen the geography of research on institutional investors in urban rental housing by considering a case of strong housing policy intervention. Despite growing attention to a greater number of contexts, the geographical reach of scholarship still remains limited. Indeed, particularly at the city level, much ink is spent on a small number of cities, such as Berlin (Fields and Uffer, 2016), New York (Fernandez et al., 2016), and London (Beswick et al., 2016; Bourne et al., 2023), all of which have experienced comprehensive privatization and deregulation of their housing stocks (Beswick et al., 2016; Kadi and Ronald, 2016; Kadi et al., 2021a).

By contrast, Vienna provides a much more regulated context, with an exceptionally high share of social housing (43% in 2021) and moderate degrees of housing privatization (Kadi, 2015), enabling us to consider institutional investors in a case where the state, at both national and local levels, continues to play a strong redistributive role in the housing market. Our results show that institutional investors own a significant share of Vienna’s rental housing stock, supporting the claim that such actors are expanding into ever wider terrains (Aalbers et al., 2020b; Rolnik, 2020 [2019]). At the same time, we demonstrate considerable within-case differences between rental tenures, calling for greater attention to the urban variegation of rental housing investment.

Second, we show that a large social housing stock does not per se prevent a significant presence of institutional investors. The sector is often considered a major barrier to institutional investors and housing financialization more broadly, as long as it is not privatized and transformed into private rental housing. In this line, social housing provision is also discussed as one of the most promising ways to de-financialize housing (Wijburg, 2021). However, institutional investors may play a considerable role even in a housing system with a high share of social housing: First, they may own private rental housing; second, they may be invested in privately organized social housing providers (cf. Belotti and Arbaci, 2021). We show how both mechanisms are present in Vienna, while also demonstrating stark differences in investor relevance between different social housing tenures.

Third, we provide an innovative method to measure institutional investor ownership. Existing studies typically draw on company case studies, commercial databases for selected market segments, or specific investment instruments. Acknowledging their limitations, we instead combine land registry data with the international company database ORBIS and Vienna’s local housing register to gauge the role of institutional investors at the property level for the entire housing market. We focus on rental tenures and additionally distinguish between direct and indirect property owners, between national, EU, and non-EU investors, and conduct a geographical analysis of investor hotspots. We draw on the existing literature on institutional investors and rental housing alongside a policy analysis and a systematic reading of newspaper articles and studies about Vienna’s housing market to identify the institutional factors that incentivize and disincentivize investors to enter different rental tenures.

Reflecting the strong role of the social housing sector, Vienna is often taken as an example of decommodification rather than of marketization and commodification (Kadi and Lilius, 2024; Premrov and Schnetzer, 2023 but see Kadi, 2024). The broader literature on housing financialization has pointed to the limited role the latter plays in the Austrian housing system, related to low levels of home ownership and mortgage rate to gross domestic product (GDP) (Schwartz and Seabrooke, 2008: 245), the absence of mortgage-backed securities (Springler and Wöhl, 2020), the strong public commitment to housing provision (Springler and Wöhl, 2020), or the high share of decommodified housing (Musil et al., 2024). Recent structural changes have provided more attractive investment opportunities in Vienna’s market, however. This, as discussed below, includes rapid population and house price growth, a low interest rate environment in the post-GFC period (until the recent upsurge in interest rates), as well as limited investment flows into the housing stock in earlier decades. While existing research has acknowledged these broader shifts (Kadi and Matznetter, 2022; Musil et al., 2024), fine-grained analyses of institutional investor ownership are so far absent.

Our analysis is guided by two research questions: First, what is the significance of institutional investors in different tenures of the rental market? Second, which policies, institutional constellations, and path dependencies direct institutional investors to and away from specific rental tenures?

We start with a conceptualization of institutional investors in rental housing. Second, we introduce the Vienna context and discuss recent structural shifts that make a growing influence of institutional investors on the rental market more likely. Third, we lay out our data and methods. Fourth, we present the results of our quantitative data analysis. Fifth, we present the results of our policy analysis. Sixth, we discuss and, seventh, close with a short conclusion.

Conceptualizing institutional investors in rental housing

Albeit, or perhaps because increasingly growing in scale, research on institutional investors in rental housing is not limited to one discipline. Relevant studies are spread over the fields of urban studies, housing studies, geography, and political economy, among others. The common denominator is the multi-disciplinary literature on housing financialization, in which research on the issue is mostly embedded.

Financialization has been broadly defined as “[t]he increasing dominance of financial actors, markets, practices, measurements and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states and households” (Aalbers, 2016: 2). The housing financialization literature initially focused on the link between the financial sector and the home ownership sector. The subprime mortgage crisis, the rise of mortgage-backed securities, and the subsequent Global Financial Crisis became a central concern in this regard (see, e.g. Aalbers, 2016; Schwartz and Seabrooke, 2008). The focus on institutional investors was already present in this literature. The financialization of mortgage markets is considered a debt-driven strategy of asset accumulation on behalf of institutional investors, via securitization and debt management arrangements (Janoschka et al., 2020; Wyly et al., 2009). Indeed, in this way, housing financialization, from the very start, was already interlinked with this particular actor type.

The focus on rental market and institutional investment is a more recent shift in the literature (Aalbers, 2023; Aalbers et al., 2017; Gabor and Kohl, 2022). Institutional investor is an umbrella term that includes different actors, depending on whether a broader or a narrower definition is adopted. Such investors are generally defined as legal entities that act as “intermediary investors,” that is, actors that manage and invest other people’s money (Çelik and Isaksson, 2014: 96). 2 This includes investment funds, insurance companies, pension funds, sovereign wealth funds, private equity funds, hedge funds, and exchange-traded funds (Çelik and Isaksson, 2014). Narrow definitions exclude the traditional banking sector, assuming varying business strategies and stricter regulations in the latter (Bessler and Rapp, 2022), in contrast to broader definitions (e.g. Von Schickfus, 2021). The recent literature on housing has, additionally, focused specifically on real estate investment trusts (REITs) (Aalbers et al., 2023). We adopt a broader definition in our analysis, as our interest is in gaining a comprehensive overview of the significance of institutional investors.

As owners, institutional investors can be directly and indirectly involved in rental housing 3 (Holm et al., 2023). Direct, when they own a property, or indirect, when they own (parts of) the company that owns the property. The latter may be motivated by a variety of reasons, including tax avoidance or anonymity (Bourne et al., 2023). From a public policy perspective, capturing both direct and indirect levels is relevant. Such an approach is, at the same time, methodologically more challenging, for example, because it typically requires the use of different data sources. Indeed, many studies are limited to the level of direct ownership (see, for example, Holm et al., 2023). We introduce below our method to capture both levels. Meanwhile, we account for the fact that investors may be national or international investors. Doing so provides relevant insights about the room for maneuver for (national) regulation. We therefore also analyze investor origin, distinguishing national, EU, and non-EU investors for different rental tenures.

Institutional investors may enter the rental housing market as owners through different means. Early analyses highlighted the stock acquisition of social rental housing through investors as a “window of access” (Holm, 2010a, 2010b). Subsequent work focused on the private rental sector, and how investors purchased rent-regulated units, circumventing regulation to maximize returns (Fields and Uffer, 2016). Scholars also highlighted the connections of financialized home ownership and rental housing investment. In contexts like Spain, Ireland, or the United States, the state amassed and then resold distressed properties from domestic banks to institutional investors and individuals to boost the supply of private rentals (Byrne, 2016; Gil García and Martínez López, 2023; Waldron, 2018). Recent work has shown how the investment terrain has widened even further. It now inter alia includes new housing construction through build-to-rent models (Nethercote, 2020), student housing, care-homes, and single-family homes (Plank et al., 2023). Rather than being limited to one tenure, different parts of the rental market have thus become encroached by institutional investors.

While varying levels of investment in one rental market are typically not in the focus, we examine institutional investor ownership in different rental tenures. We build on the existing literature alongside an analysis of Vienna’s policy landscape to identify the institutional factors that have driven investors to and away from different tenures. To do so we draw on concepts that have been used to account for investor presence in urban rental markets: the rent gap concept (Christophers, 2021), the commodification gap (Bernt, 2022), as well as the notion that investment into newly built rental property is incentivized by a portfolio diversification strategy (Sanderson and Özogul, 2022). Doing so provides us with a conceptual language to make sense of our tenure-specific findings for Vienna.

Our analysis feeds into current policy debates. Housing and finance have long been tightly interwoven. As a capital-intensive good, housing requires access to finance at the point of production and subsequent stages of the transaction (Aalbers et al., 2020a). The relationship between the two sectors has, however, transformed in recent decades. Rather than the housing sector turning to finance to secure the necessary funding, housing has increasingly come to support financial markets in their search for lucrative investments (Aalbers, 2017), with the state being complicit in this shift in many contexts (Gabor and Kohl, 2022; Ryan-Collins, 2021). Several rounds of financial market deregulation, touted as a promising route to expand the housing supply and distribute housing assets (Arundel and Ronald, 2021), have enabled financial markets to operate more widely and with less restrictions (Ryan-Collins, 2021). The Global Financial Crisis has triggered a temporary pushback against this political optimism, yet calls for more restrictive regulations for financial actors have gained momentum in a number of contexts more recently, particularly in rental housing (see, for example, Christophers, 2021; Gabor and Kohl, 2022; Hoffrogge and Junker, 2022). Such interventions rely, however, on fine-grained empirical research, underlining the importance of our analysis below.

The Vienna context

Vienna and Austria, more broadly, have so far been curiously absent from debates around institutional investors in rental housing. Global financial markets have traditionally had a limited role in the Austrian housing system. Austria has one of the lowest home ownership rates in Europe and mortgage-backed securities are prohibited (Springler, 2008: 289). Covered bonds drive the mortgage system, yet the tendency to include low-income households is limited, as the risk cannot be sold-off by commercial banks (Springler and Wöhl, 2020). More directly relevant to our analysis, Austria, and Vienna in particular, has long shown a strong public commitment to affordable housing provision, with rent regulation applying to parts of the private rental market and, by international comparison, a large share of the housing stock constituted of social housing (Springler and Wöhl, 2020). Furthermore, privatization has been limited, particularly when compared with contexts like Germany, which is often considered in the same welfare/housing regime type (Kadi et al., 2021b). Finally, REITs cannot be registered legally in Austria, albeit investment by foreign Trusts is possible.

While these factors have mitigated the integration of global financial markets with Vienna’s housing market, we demonstrate in our analysis that, still, institutional investors have come to play a considerable role. While differences are evident between tenures, which we explore below, four macro-level factors have made investment generally more attractive.

First, Vienna has seen rapid population growth. While the number of residents had been declining for much of the post-war period and restarted to grow again only from the 1990s onwards (Kadi and Matznetter, 2022), over the last decade alone, the city has added over 200,000 residents—close to the size of the second largest city in Austria, Graz. With further growth projected in the coming years, this provided increasingly attractive investment conditions.

Second, market conditions in Austria and Vienna have been strongly impacted by the macro-economic environment. Being part of the integrated European monetary system, the quantitative easing policy of the European Central Bank and the low interest rate policy over the last decade have lowered capital costs and triggered investment into different sectors, among them rental housing (Springler and Wöhl, 2020).

Third, Vienna has seen rapid house price growth. Between 2004 and 2022 alone, house prices for residential properties have increased by 174 percent, whereas the consumer price index only increased by 49 percent (OENB, 2023). One implication has been a rising demand for rental housing among those unable to afford home ownership.

Fourth and finally, Vienna has long seen limited investment flows into the housing stock (Kadi and Matznetter, 2022), disincentivized by low population growth and relatively strict rent regulation. Ongoing depreciation of the housing stock, however, also provided the chance to close growing rent gaps, particularly in the context of inexpensive credit, high population growth, and, as we will discuss below, relaxed rent regulation in parts of the market.

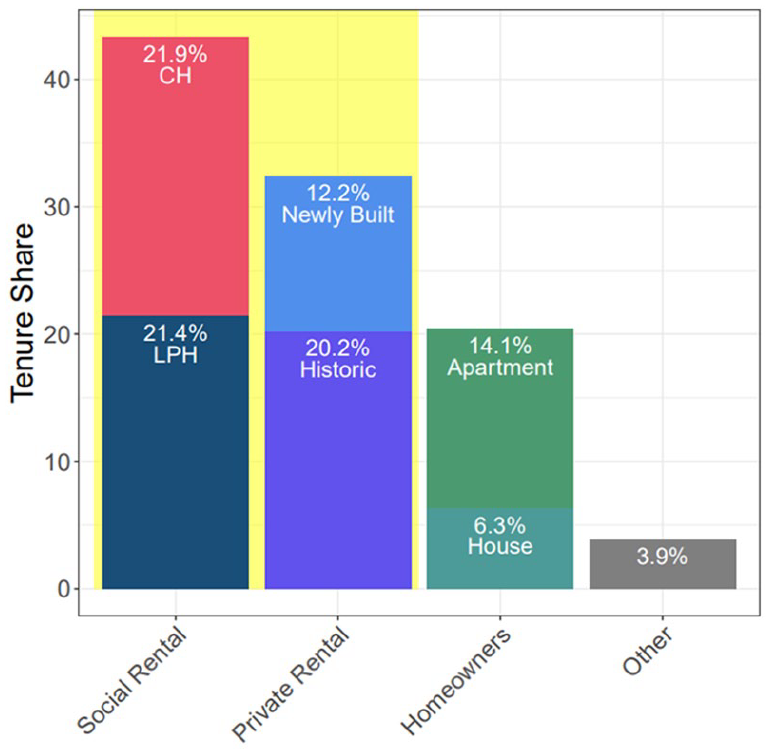

These macro factors need to be considered along with the unique structure of Vienna’s housing system (see Figure 1). With 43 percent, the city has one of the largest social housing tenures among all European capital cities (Kadi, 2015). About half of it is city-owned and administered council housing. The other half is owned and administered by limited-profit housing providers, that is, private entities that provide inexpensive housing in exchange for tax incentives and subsidies (Mundt and Amann, 2010). About one-third of all housing units belong to the private rental tenure. It includes a historic stock (built before 1944), which is rent-regulated and makes up around two-thirds of all units, and a newly built stock (built after 1944), which is not rent-regulated and accounts for the remaining third of the private rental stock. Finally, the home ownership sector comprises around 20 percent of all units. In our analysis, we consider all four rental tenures: council housing, limited-profit housing, historic private renting, and newly built private renting. As we show, the significance of institutional investors differs considerably between tenures, reflecting varying institutional conditions that drive such owners to and away from different tenures.

Vienna’s housing tenuresa.

Vienna’s housing system consists of a complex set of regulations in a multi-level governance structure with a diverse set of actors. Consequently, different regulations at various levels as well as actors also impact institutional investment. At the national level, it is particularly the Tenancy Law, the Limited-Profit Housing Act, and the regulation of financial/credit markets. At the local level, planning acts, which, for example, regulate the use, construction, and demolition of buildings, as well as the provision of housing subsidies are specifically important. In terms of actors, alongside the national actors and the local state, there is a complex web of outsourced institutions and public enterprises (such as Wiener Wohnen, which administers council housing), and intermediary institutions, particularly the limited-profit housing associations. The associations are organized as private entities but operate under a comprehensive regulatory framework that mandates them to provide affordable housing with a long-term place-based mission (Kössl, 2019). We draw on these specifications in our analysis of the factors that promote and impede the entrance of institutional investors in different tenures.

Data and methods

How to gauge the relevance of institutional investors in rental housing empirically? There are three common approaches. First, company case studies that consider one or more companies and their operation. See, for example, Janoschka et al. (2020) and Christophers (2021). Second, studies that draw on commercial databases to measure institutional investors in a specific market segment. See, for example, Romainville (2017) on new construction projects and Guironnet et al. (2023) on recently traded properties. Third, studies that draw on a specific investment instrument. See, for example, Aalbers et al. (2023) on REITs.

All three approaches have limitations. The first is unable to draw conclusions about the role of institutional investors beyond the companies considered. The second misses all that is going on beyond the specific segment considered (e.g. existing stock, those properties that were not recently traded). The third falls short in considering investments outside of the specific investment vehicle studied. None of the approaches, thus, provides insights into the entire housing stock.

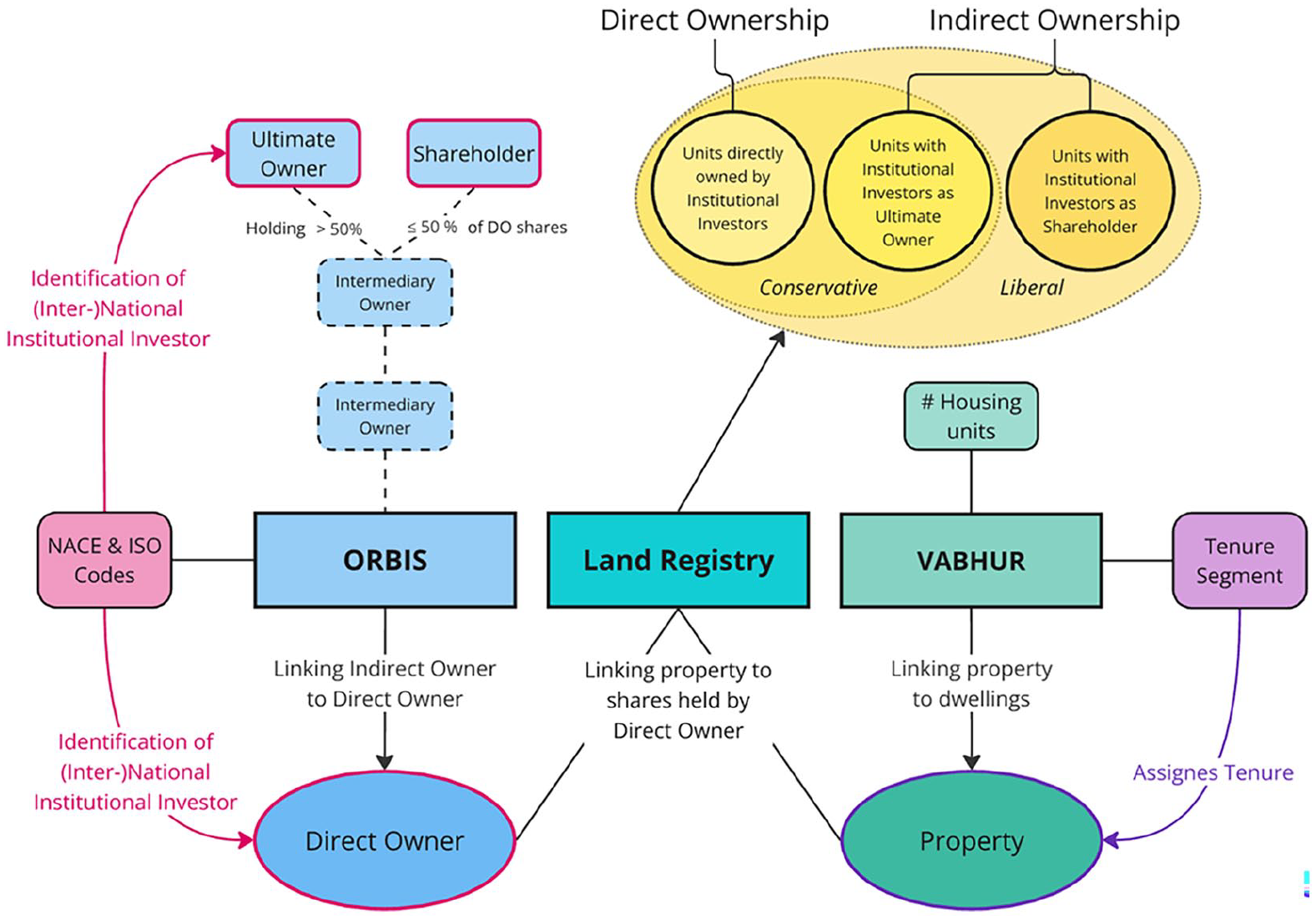

One of the few studies that does so is St-Hilaire et al. (2024). It draws on tax records for the case of Montreal to quantify what the authors call “financialized landlords.” Tax records are, however, not widely available to researchers in many contexts, including in Vienna. Here, we instead draw on land registry data, which has recently also been used in property ownership research in other contexts (see, for example, Paccoud et al., 2021). We amend it with the ORBIS company database and the local housing register VABHUR. This provides us with a unique dataset about property ownership at the plot level, including all owners (as long as they are a company and not an individual) and their classification in a standardized classification of economic activities. It also differentiates between direct and indirect ownership (including both majority owners and other shareholders), specifies the nationality of all company owners, and furthermore, the tenure each property belongs to.

Figure 2 gives an overview of the data structure and how it is utilized to identify housing units held by institutional investors.

Data analysis framework.

The land registry (Grundbuch) provides a property ID, subdistrict code, name of the company or companies that own the property, 4 company register number (not available for all owners), and share of property owned by each company. It covers all 128,220 Viennese properties (Liegenschaften). 5 Property, in this context, refers to a plot of land. A property can contain several buildings, each of which can again contain several housing units.

To uncover indirect ownership, we linked the land registry to the ORBIS company database. We did so for all 20,800 companies that appeared as direct owners in the land registry by systematically searching ORBIS for the company register number, or, if unavailable, the company name. We used the matching function in ORBIS and manually linked around 1000 cases in which the automatic matching did not work (e.g. due to spelling errors in the company name).

For all cases with indirect owners, we extracted the name/company register number of the owner that functions as the majority owner (ultimate owner in ORBIS parlance) or the name and equity shares of the shareholders that own the direct owner. We traced all shareholders starting from the direct owner and up to 15 levels above. 6

Our identification of institutional investors rests on the classification of economic activities in the statistical nomenclature of the European Union (NACE, Nomenclature statistique des activités économiques dans la Communauté européenne). We extracted the NACE code for all companies that function as direct owner, majority owner, or shareholder from the ORBIS database. If a company belongs to the finance and insurance sector, following the NACE Code, we classify it as an institutional investor (see for a similar approach, for example, Romainville, 2017). 7 We use the codes 64 to 66.30, 8 that is, companies belonging to three super-categories “Financial service activities, except insurance and pension funding,” “Insurance, reinsurance and pension funding, excluding compulsory social security,” and “Activities auxiliary to financial services and pension funding.” In addition, we treated all private foundations (Privatstiftungen) operating under the Austrian Private Foundations Act (Privatstiftungsgesetz, 1993) as an institutional investor. Although they were typically already identified as such based on their NACE classification, implementing an explicit string search for the term “Privatstiftung” across direct and indirect owners enabled us to capture additional cases without an ORBIS match. There were 3628 cases in the database for which we found no information in ORBIS. A manual check of a subsample of 300 cases revealed that many of them are societies and religious institutions. They were considered to be no institutional investors.

Based on this scheme we looked for institutional investors at three levels: first, as direct owners, second, as majority owner of the direct owner, and third, as owner of certain shares of the company at the second, third, or another level above the owner. There seems to be no general agreement in the literature about which measure is the right one for gauging indirect ownership. Whereas some draw on the majority owner, others emphasize the strategic influence shareholders can have (e.g. Christophers, 2023). 9 For our analysis, majority and shareholder measures can be seen as upper and lower bounds of indirect ownership, respectively. We refer to them as conservative and liberal measures. Meanwhile, the direct ownership measure provides a benchmark and serves to evaluate the importance of indirect ownership. Our measures are cumulative: the indirect ownership (conservative) category includes all cases in which either the direct owner is an institutional investor or the majority owner. The indirect ownership (liberal) category includes all cases in which either the direct owner, the majority owner, or a shareholder are institutional investors.

We extracted the nationality of the owners from the ORBIS database per its ISO code (i.e. whether they are registered in Austria or in another country). We did so for all direct and indirect owners (conservatively measured). Hence, we classified units as owned by international institutional investors if the owner at the land registry level is a foreign entity or if the respective entity is indirectly owned by a majority owner in a foreign jurisdiction. We further differentiated between owners from other EU countries and from outside the EU.

Finally, we linked the database to the local housing register VABHUR. 10 It includes information about the primary usage of a property which is used to filter for residential properties. Furthermore, it reports the number of units per building. This is necessary as the land registry only provides ownership shares for different owners in the property. In addition, the register provides information about the majority tenure of the housing units in each building (rented, self-use of owners, unknown), as well as a broad classification of property owners (natural person, limited-profit housing associations, City of Vienna, company, unknown). This enabled us to relate the land registry and ORBIS information about property ownership to rental tenure categories. 11

A number of limited-profit housing units are built on leased land (Litschauer et al., 2023). Consequently, the land registry states the name of the land lessor not the housing association. We identified the correct tenure category for these units based on the ownership data in the VABHUR register. The absolute number of units in our database closely matches the number of units stated by the umbrella organization of limited-profit housing associations (AFLPHA, 2021), corroborating our approach. Overall, we were able to assign 97.4 percent of all housing units in the city to a tenure category.

One additional challenge was that for those units that were assigned to limited-profit housing based on the VABHUR only, we did not know the name of the actual limited-profit housing provider (only available from the land registry). These were treated as not owned by an institutional investor by default. Therefore, we are likely to underestimate the actual share of institutional investors within LPH.

Institutional investors in Vienna’s rental housing market

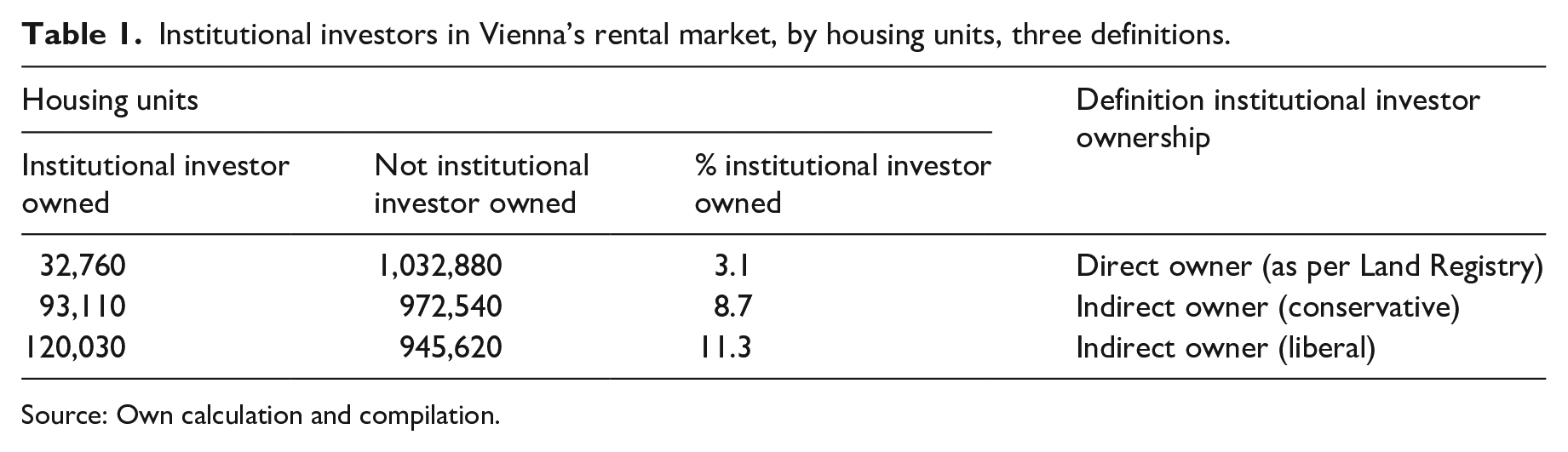

At the level of direct ownership, about 32,760 housing units in Vienna belong to institutional investors. This amounts to a share of 3.1 percent of the 1.07 million units in 2022. When we also consider indirect ownership, in a conservative measure, around 93,110 units belong to investors, that is, 8.7 percent of all units. If we adopt an even wider definition that also includes investors as minority shareholder of a property owner, this increases to 120,030 units, or 11.3 percent of all units (see Table 1).

Institutional investors in Vienna’s rental market, by housing units, three definitions.

Source: Own calculation and compilation.

This already demonstrates two things: First, institutional investors play a considerable role in the housing market, especially when direct owners, majority owners, and shareholders are considered. Together such actors are invested in more than every tenth housing unit in the city. Second, when the different definitions are considered, we can see that institutional investors often function as indirect rather than direct owners. This lends support to our methodological choice to investigate both ownership levels.

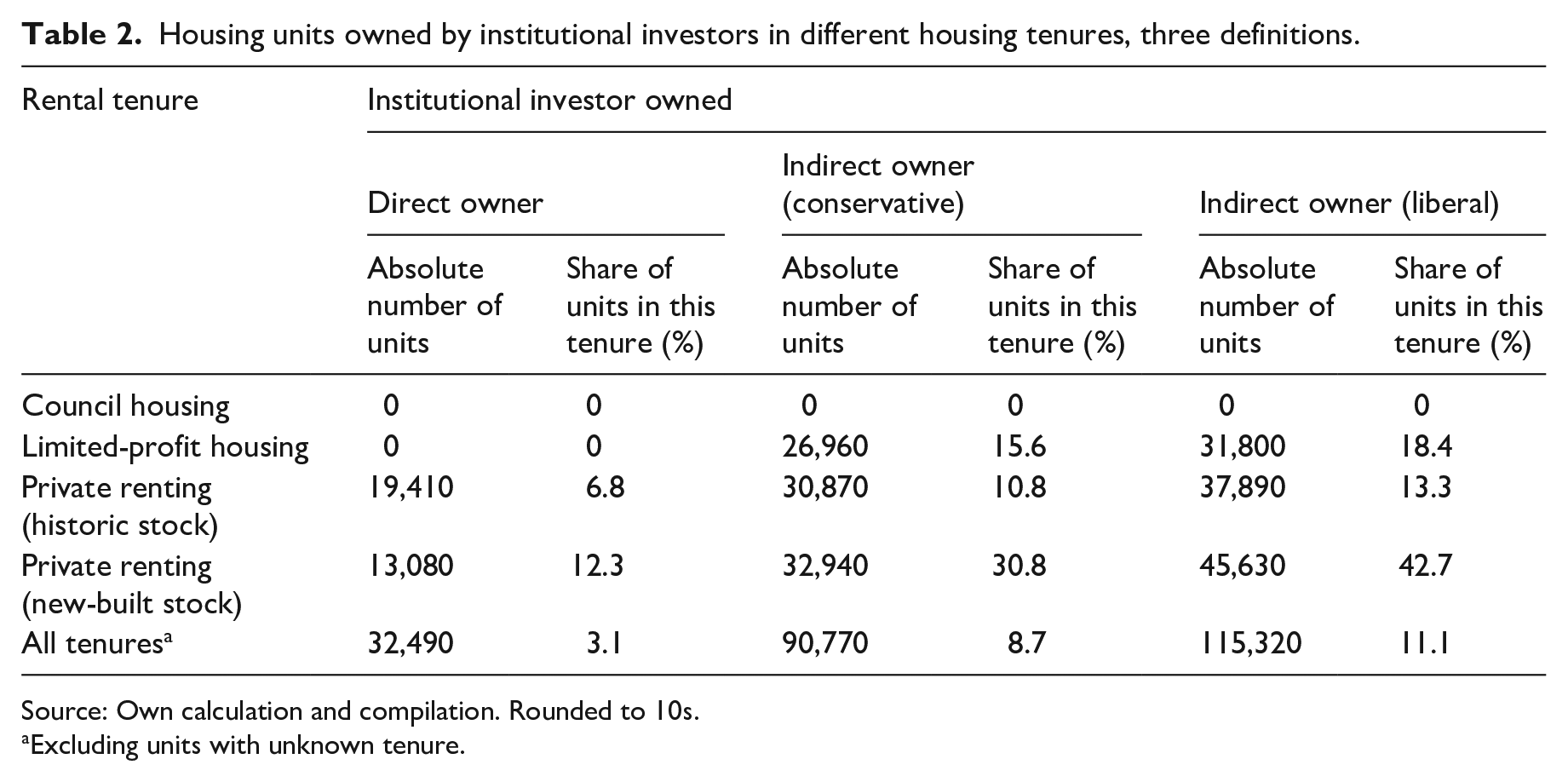

What role do institutional investors play in different rental tenures? In council housing, institutional investors are not invested in the stock (Table 2). This holds by definition for all three types of ownership considered, as this stock is fully publicly-owned. In limited-profit housing, the second social housing tenure, this also holds true for the level of direct ownership. At the level of indirect ownership, however, institutional investors play a sizable role, owning some 15 percent of the stock. This share further increases when a liberal, shareholder definition is applied. The increase is moderate, however, to around 18 percent. Most institutional investors in limited-profit housing are thus majority owners of the companies that hold the housing stock. Compared with other housing tenures, the relevance of investors in limited-profit housing is remarkable. It has the second-highest share among all tenures at both levels of indirect ownership.

Housing units owned by institutional investors in different housing tenures, three definitions.

Source: Own calculation and compilation. Rounded to 10s.

Excluding units with unknown tenure.

In the historic private rental stock, the pattern looks again different. Some 7 percent of the stock is investor owned at the level of direct ownership. The share increases when conservative and liberal definitions are considered, but only moderately. In contrast to limited-profit housing, a sizable number of investors in this tenure thus function as direct rather than indirect owners. At the level of direct ownership, the tenure has the second highest share of investors. At both levels of indirect ownership, it has the third highest share.

The newly built private rental stock, finally, has the highest share of investors for all three definitions and the steepest increase from direct to indirect forms of ownership. More than one-tenth of all units in the tenure are directly owned by institutional investors (12.3%). This increases to almost every third unit at the level of majority ownership (conservative measure) and to 42 percent at the level of shareholder ownership. Thus, compared with the historic private rental stock—the only other tenure that has direct ownership of institutional investors—the tenure has almost twice the share of investors at the level of direct ownership. The difference between direct and majority ownership in the tenure is higher than for all other tenures in terms of percentage point increase. The same holds for the difference between majority and shareholder ownership. Thus, institutional investors play the most significant role in newly built private renting, both as direct owners and as indirect owners, regardless of the level considered.

As for our analysis of the housing market overall, these results underline the usefulness of our approach. Given the pronounced difference between conservative and liberal measure, the newly built private rental stock in particular highlights the insights gained from different definitions of indirect institutional ownership. The same can be said for the limited-profit housing stock regarding the usefulness of distinguishing between direct and indirect ownership.

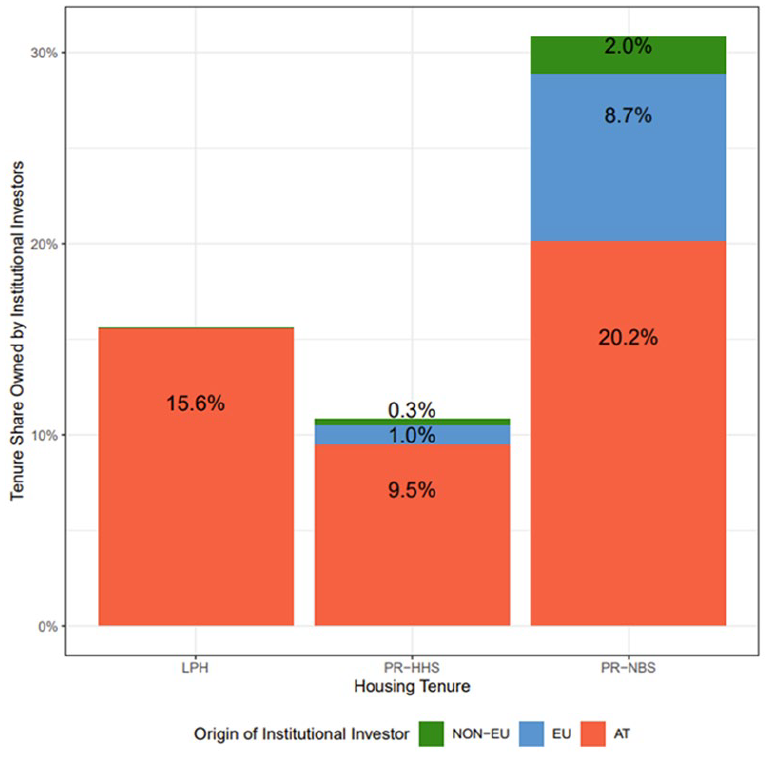

The analysis of investor origin further underlines the differences between tenures. We analyzed the level of indirect ownership (conservative) for all three tenures in which institutional investors are present according to this definition: limited-profit housing and both private rental tenures (Figure 3).

Share of housing units owned by institutional investors in different housing tenures, by investor origin.

The overall picture is that institutional investment in rental housing in Vienna is a predominantly national affair. Most of the investor owned housing in all three tenures is in the hands of national owners. There are, however, relevant differences. In limited-profit housing, no EU/Non-EU investor is active. In the historic private rented stock, around nine-tenth of all units that belong to institutional investors are nationally owned, while the remaining tenth is owned by EU investors and a marginal share (0.3% of all units in the tenure) by non-EU actors. The ranking remains the same for the newly built private rental stock, but the quantities differ. Around one-third of the investor owned units are in the hands of non-Austrian owners. Most of them, around 9 percent belong to EU owners and the remaining 2 percent to non-EU owners. While national investors thus dominate the investment landscape, the relevance of international actors differs quite strongly, from playing no role in limited-profit housing to owning around one-tenth of the investor owned units in the historic private rental stock to holding around one-third of such units in the newly built private rental stock.

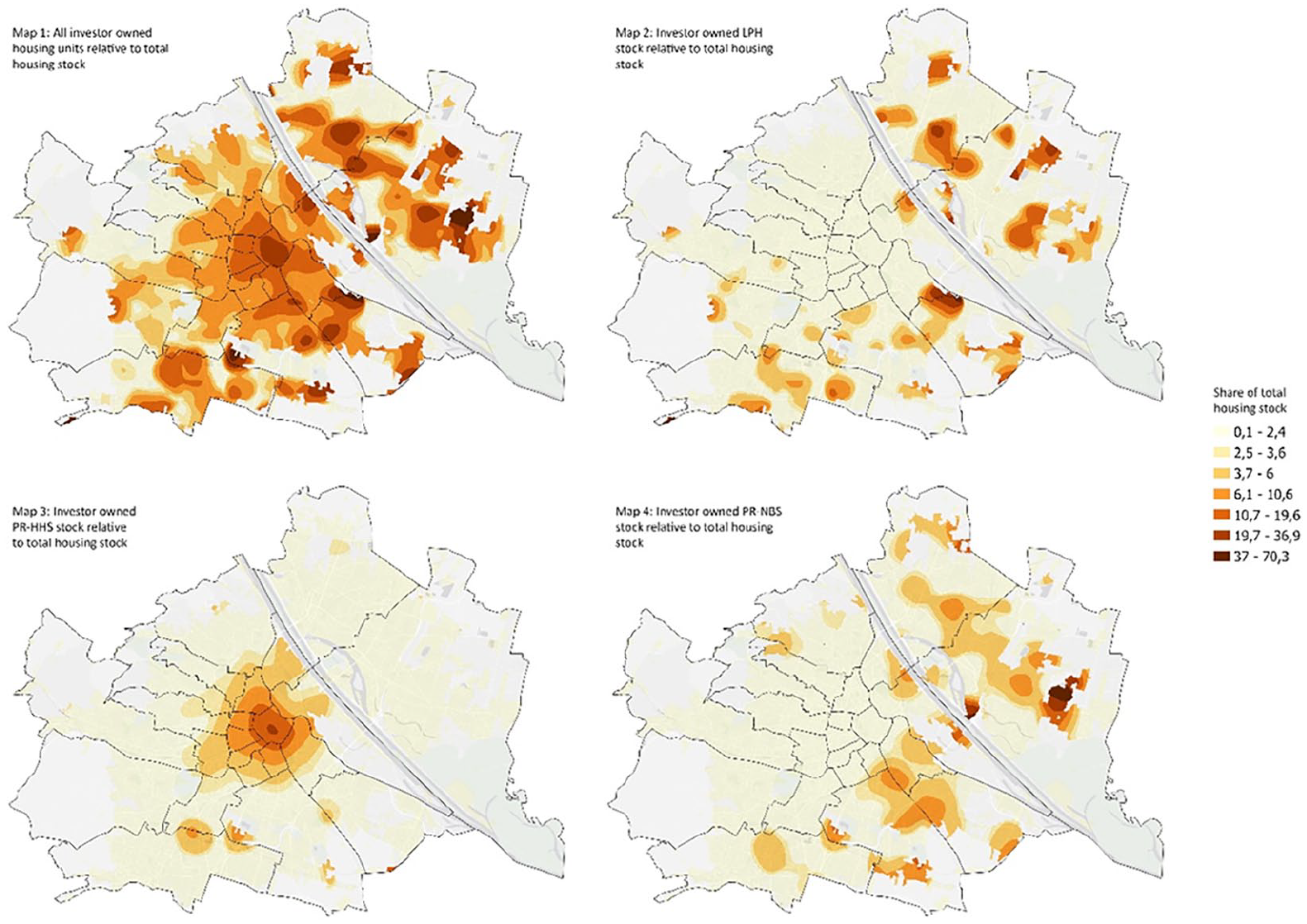

Our geographical analysis underlines the relevance of institutional investor ownership, but confirms significant differences between tenures also in spatial terms. We mapped the share of institutional investor owned housing per tenure relative to the total housing stock. We used a kernel density model with a radius of 1 km. The result is a value between 0 (no investor ownership) to 100 (complete investor ownership). Again, we focused on the level of indirect ownership (conservative) and on the three rental tenures with institutional investors (see Figure 4).

Kernel density mapping of the share of housing units owned by institutional investors (as direct or indirect majority owner) relative to total housing stock.

Map 1 shows all investor owned housing relative to the total housing stock. It reveals a range between areas with very little such units, particularly in the more peripheral parts of the city, and higher values in the inner city and the North-West, as well as the South. There is less investor presence in the Western part of the city—traditionally areas with higher social status and greater numbers of owner-occupied units.

Maps 2–4 zoom in on the three rental tenures with investor ownership. Map 2, on LPH, shows that investor owned housing there is much more peripherally located than in the housing market overall. We find concentrations in the South-East and the North-East in particular. The dark color in many of these areas also indicates that such units make up a significant part of the housing stock there. Map 3, on the historic private rental stock, shows a very different geography. Institutional investor ownership is concentrated in the inner city, with the highest values in the city center and decreasing with distance from the center. Finally, the newly built private rental tenure contrasts again sharply with this. Investor owned units are much more peripherally located in the South, South-East, and particularly the North-East of the city. Apart from the two hotspots in the North-East, the units also make up a smaller share of the housing market in the surrounding areas than in LPH.

These differences largely reflect the varying geographies of the three tenures. LPH is mostly concentrated in the outer districts. The LPH estates are often quite large-scale compared with the lower density housing in the surrounding areas, promoting a dominance of investor owned housing in the spatial units considered. The historic private rental stock, by contrast, is much more centrally located, in the historic part of the city, and hardly present in the outer districts. Meanwhile, the newly built private rental market is again more peripherally located and particularly to be found in new urban development projects like in the North-East of the city, where we can see strong concentrations.

Taken together, this adds to our previous findings. Institutional investors do play a sizable role in the housing market, but there are strong differences between tenures, not only in terms of the share of housing units owned, the level of ownership at which this ownership is exerted, the degree of international ownership, but also in terms of the investment geography. Institutional investors impact on urban space in different tenures in different ways.

Institutional factors driving investors to and away from different rental tenures

Abstracting from the tenure-specific differences in terms of investor origin and geography, what are the institutional mechanisms and specificities that can help us understand the presence and absence of investors in different tenures? What are relevant factors, beyond the above-discussed macro-level factors that have incentivized investment into Vienna’s rental market, that is, rapid population growth, rising house prices, a housing stock with limited investment in preceding decades, and the availability of cheap credit?

Christophers (2021) draws on the rent gap to account for the entrance of institutional investors into urban rental markets. He contends, drawing on the case of Blackstone, that such actors aim to close the gap between the “capitalized” and “potential” ground rent through a “buy it, fix it, sell it” model: They purchase real estate, renovate it, and let or sell it at a net overall profit. For the strategy to work successfully, there is not only a need for buoyant demand that pushes up potential ground rents and earlier rounds of disinvestment that pushes down capitalized ground rents. There must also not be any institutional constraints that impede the closure of rent gaps (Christophers, 2021: 700).

The absence of institutional investment in Vienna’s council housing can be usefully interpreted through this lens. In the context of rapidly growing housing demand in the city, rounds of disinvestment in council housing along with low rent setting have created a sizable gap between what is currently earned with these estates and what could potentially be earned under “highest and best use.” There is, however, an insurmountable barrier for institutional investors. Vienna, in contrast to several other European cities, has not sold any council housing units (Kadi and Lilius, 2024), nor has it considered to invite institutional investors as (minority) shareholders. While in cases like Berlin, such a privatization has been a primary means for institutional investors to enter the market and adopt their business model (Holm et al., 2023), in Vienna, this door has remained closed. Hence, institutional investors had no legal room to acquire ownership.

Such institutional constraints to close rent gaps also exist in historic private renting. Most importantly, rent regulation applies to the units, along with relatively high degrees of tenure security (Kadi, 2024). Hence, potential ground rents are pushed down, disincentivizing investment. There are, however, regulatory loopholes and changes that have made investment in the sector more lucrative. Bernt refers to this as the commodification gap: Investors are incentivized by such loopholes or changes that allow them to get units out of regulation and maximize returns, turning units from partially decommodified into more commodified forms (see also Fields and Uffer, 2016). In Vienna, this has two dimensions (Kadi, 2024).

First, rent regulation was significantly deregulated in the mid-1990s. Essentially, this facilitated higher rents setting and regularly raising rents, even without substantial upgrading of the unit. One element was the introduction of so-called “location bonuses.” They allowed, for the first time, to ask higher rents in areas with higher land prices. While housing in parts of the city was exempted, the bonuses enabled landlords to regularly raise rents along with general market developments. Relaxed rules to issue temporary rental contracts further facilitated this, as rents could regularly be adapted with new contracts (Kadi, 2024).

Second, legal loopholes exist to get units out of rent regulation. This includes, for example, the possibility to demolish buildings. Until recently, few restrictions applied to demolitions. The incentive for investors is that rent regulation only applies to the historic housing stock. When an older building is thus demolished and replaced with a new one, much higher rents can be asked (Kadi, 2018). The City of Vienna, in 2018, introduced stricter regulations to curb demolitions. Another loophole is that private rental multi-story buildings can be split up legally and individual units can be sold off to new owners. This process, in German called Parifizierung, enables owners to increase returns resulting from tenure conversion. Rapidly rising house prices in the post-2008 period incentivized investors to engage in this business model (Kadi, 2024; Musil et al., 2024).12,13

While closing the gap between partially decommodified and commodified status through these three means provided an attractive investment opportunity, the high degree of complexity in the Austrian Tenancy Law also meant that investors needed to acquire significant amounts of local knowledge, which dampened attractiveness and can help understand why the level of investment remains lower than in newly built private renting.

There, a key difference to the historic private rental stock is that no general rent regulation applies. While some parts constructed with housing subsidies are temporarily rent-regulated, the tenure overall fills a more upmarket niche in Vienna’s highly regulated housing supply. Until the early 2000s, construction in newly built private renting remained limited in the context of stagnating population and a strong focus on subsidized housing provision, for example, through city-owned council housing. The tenure played a marginal role, with most housing demand covered by other tenures.

Since then, rapid urban growth and a lack of supply drove construction, facilitated by the absence of strict rent regulation. The stock inter alia includes Build-to-Rent properties, along with high-end student housing and serviced apartments for young professionals (Franz and Gruber, 2022; Plank et al., 2022). 14 Ultimately, newly built private renting provides a rare investment opportunity for more upmarket housing, facilitated by demographic developments and limited alternative housing options in this price segment. While investors can increase returns through adapting rents to general market developments, for example, through regularly issuing new temporary contracts, they can also purchase and resell properties in the context of a highly dynamic property market. Meanwhile, investment is advertised as a portfolio diversification strategy (Arnold, 2022), where stable rental income streams are used to balance more high-risk investments in other assets (see for this argument in an international context (Australian Government, 2023; Sanderson and Özogul, 2022).

This leaves us with limited-profit housing. Institutional investors do not own any units directly, but 15.6 or 18.4 percent of the stock indirectly, depending on the applied definition. A key to understanding this is that limited-profit housing providers are, as discussed above, private entities. While around half of the 185 providers in Austria are organized as cooperatives (Genossenschaften), the other half are limited or public limited companies, in which investors can acquire ownership. Over the last decades, they have increasingly done so. The associations have a very good financial standing and investments are considered relatively low risk. The possibility to extract high returns is, however, strictly limited by law, dampening attractiveness in this regard (Bauer, 2006: 25). 15 There is also no possibility that rents are raised to increase returns (Bauer, 2006: 25).

There is another incentive, however. Banks and insurance companies, who are the main investor types in the tenure, can invest in order to secure clients and expand their traditional business area (Bauer, 2006; Koeppl et al., 1990: 63; Orner, 2020). Any limited-profit housing provider requires financing for new housing projects, and insurances, for the houses built. The Limited-Profit Housing Act regulates who can own limited-profit housing providers and, for example, prohibits that owners with ties to the construction industry function as owner, so as to avoid potential conflicts of interest. No such rules exist, however, for the financial industry. Accordingly, it is possible that a bank functions as the owner of a provider, yet at the same time provides the financing for its (current and future) operations. A similar logic applies to the insurance sector and the provision of insurances. Institutional investors can thus invest in the tenure in order to shape their own market and expand their traditional business area (Orner, 2020). This, more indirect mechanism, provides an incentive to engage with the tenure.

Discussion

How do these findings relate to what we know about the role of institutional investors in urban rental markets? If the literature suggests that institutional investors encroach an ever wider terrain of rental markets (Aalbers et al., 2020b; Guironnet et al., 2023; Rolnik, 2020 [2019]), our findings lend support to such an argument. Going beyond the limited geographical scope of existing studies, and drawing on a contrasting case, we show how institutional investors have also come to play a significant role in the case of Vienna. Despite a much more regulated housing policy context, they are invested in more than every tenth housing unit, either as direct owner, majority owner, or shareholder. Even if we just consider the direct and majority owners, it is roughly every thirteenth unit.

That said, our findings also call for nuance in such an argument. The analysis demonstrates considerable differences between tenures. First, the share of units affected differs considerably, for example, when the council housing sector, without any investors, and the other three rental market tenures are compared. Second, not only does the overall share differ, but also the way how ownership is predominantly organized, with, for example, limited-profit housing only having indirect owners, whereas the historic private rental stock having a strong presence as direct owners and the newly built private rental sector having high shares compared with other tenures across direct, majority owners and shareholders. Third, in terms of investor origin, despite an overall dominance of national actors, international owners play a varying role: no ownership in limited-profit housing, a limited share in the historic private rental stock and a sizable role in newly built private renting. Fourth, the geography of institutional investors, and thus also the spatial implications, differs substantially between tenures. Fifth and finally, there are distinct institutional constellations that have directed investors to and away from different tenures. Even if our findings thus suggest that institutional investment plays a significant role also in Vienna, they equally underline how their presence and manifestation vary considerably within the rental market.

Such an argument, about expansion and variegation of institutional investors, is not per se new. Indeed, as discussed at the start, the context-dependency of such investments has been highlighted, with, for example, Bernt et al. (2017) arguing that they unfold in “path-dependent, uneven and contingent” (p. 555) ways. Our argument is similar but operates on a different spatial level. Whereas existing studies emphasize differences between cases, our findings highlight within-case variation, in particular related to rental tenures. Several other studies have also focused on the level of rental tenures in one case (e.g. Christophers, 2021; Fields and Uffer, 2016). They have typically focused on one tenure only, however, unlike our analysis, which has instead foregrounded differences between tenures.

Emphasizing such differences in institutional investments within one case is not about academic hair-splitting. If institutional investor ownership impacts housing conditions and outcomes (Fields and Uffer, 2016; Holm et al., 2023; Raymond et al., 2016; Soederberg, 2018), such differences are crucial to understanding real-life housing experiences and policy implications. Indeed, our findings suggest that there is much to investigate when it comes to the urban variegation of institutional investment and our analysis provides a first step in this direction, both related to the quantitative importance as well as the underlying institutional mechanisms.

Our results also relate to debates around the relationship between social housing and institutional investors. While stock acquisition and the subsequent transformation of social housing into private rental housing has become a key “window of access” for investors into housing markets (cf. Fields and Uffer, 2016), the presence of the sector, without stock acquisitions, is often assumed to, conversely, constitute a major entry barrier (cf. Wijburg, 2021). Our results, drawing on one of the cities in Europe with the highest rates of social housing, suggest that the sheer presence of a sizable social housing does not necessarily keep away such actors. The details matter, however.

First, the absence of investors from council housing demonstrates how indeed, such a sector, if remaining in public ownership, can be an insurmountable barrier. Second, investors can, however, be invested in other tenures, such as, in Vienna, the private rental market. Third, they can also be invested in privately organized social housing providers, as is the case with limited-profit housing associations. The possibility for investors to extract value from the latter is strictly limited and there is thus no direct threat to the status of social housing as an affordable housing segment, as was the case with the stock acquisition by financial actors in cases like Berlin (Holm et al., 2023). For investors, investment in the providers rather serves as a means to strengthen their traditional business activities in the realm of financing and insurance provision. Nonetheless, investors hold a significant share of the housing stock, despite the large share of the tenure in the city. This lends support to arguments that the link between social housing and institutional investors is more complex than often assumed (Belotti and Arbaci, 2021) and also underlines that the tenure is not by definition immune to processes of housing financialization (Aalbers et al., 2017), although the case of LPH seems to constitute a special variant of it.

While our study provides an in-depth look at the significance of institutional investors in different rental tenures, it does not address questions about the impacts of such investors on housing conditions. If the existing literature (see Fields and Uffer, 2016; Raymond et al., 2016; Soederberg, 2018) has suggested detrimental consequences for affordability and housing problems—even though empirical studies have so far arguably remained scarce and limited to selected rental tenures and regulatory contexts—our analysis does not allow to make any empirical inferences for the Vienna case. Our findings about the factors that incentivize investors to enter different tenures indicate, furthermore, that the business models and hence also the potential impacts of investors may well differ between tenures. While not within the scope of this study, our findings nonetheless provide a necessary first step to explore such questions further. Meanwhile, our dataset provides a promising tool to do so, given its property level data that can be linked to housing outcome variables on the micro level.

Concluding remarks

This study contributes to understanding the significance of institutional investors in urban rental housing markets. This is crucial to evaluate the impacts of this actor type on housing markets and conditions and develop appropriate policy responses. Going beyond existing approaches, we have drawn on a novel method to analyze ownership patterns of institutional investors in different tenures in Vienna—one of Europe’s cities with the highest share of social housing. Combining land registry data with the international company database ORBIS and Vienna’s local housing register for a property level measurement of investor ownership showed that such investors have become of significant relevance also in a highly regulated housing market context like Vienna. Yet this relevance differs considerably between tenures: In terms of the share of properties owned, the level of ownership at which institutional investors are invested, the origin of investors, the geography of investment, as well as the institutional mechanisms that promote or impede investor presence. Based on this, and mirroring arguments about contextual variegation of institutional investment in rental housing between cities, we call for greater attention to the urban variegation of such investments within cities. We also demonstrate that a high share of social housing does not prevent institutional investors to enter a housing market and, based on our case, demonstrate two mechanisms for how a large social housing stock may coexist with significant investor presence. Our land registry-based approach may be adopted in other cases and contexts. The perhaps most critical aspect for transferability is the availability of detailed ownership data at the plot level. Comparable data has, however, recently been used by researchers in other countries and it is in these contexts where our approach may be most easily replicable (see, for example, Bourne et al., 2023; Casanova Enault et al., 2023; Hochstenbach, 2024; Paccoud, 2020).

Footnotes

Acknowledgements

All three authors contributed substantially to the paper. Justin Kadi had the lead in theoretical conceptualisation and writing. Selim Banabak had the lead in the conceptualisation of the database, data preparation and formal data analysis. Leonhard Plank contributed to data aquisition and conceptualisation of the database. We thank Robert Kalasek for support with the GIS mapping, Anna Kalhorn for support with the construction of the database, and the City of Vienna, Department of Economy, Labour and Statistics for the provision of the local housing register data. A previous version of this article was presented at the workshop “Institutional Investment in Urban Housing Markets: Global Trends, Local Manifestations and the State” in Brussels in November 2023. We thank all workshop participants for useful suggestions. The same goes to two anonymous reviewers and the journal editor.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.