Abstract

This article centers the role of digital technologies in extending financial accumulation into new sectors of the US housing market in the wake of the global financial crisis. I argue that while post-crisis market conditions provided an opportunity for large investors to acquire foreclosed single-family homes, convert them to rental housing, and roll out an new asset class based on bundled rent checks, these conditions were insufficient on their own. Digital innovations coming to prominence since the 2008 crisis were required to automate core functions, such as rent collection and maintenance, in order to efficiently manage large, geographically dispersed property portfolios. New information technologies enabled investors to aggregate ownership of resources, extract income flows, and securely convey these flows to capital markets. Such advances have, therefore, given rise to the “automated landlord”, whereby the management of tenants and properties is increasingly not only mediated, but governed, by smartphones, digital platforms, and apps, and the data and analytics these devices and infrastructures gather and enable. This article shows how technological transformations actively participate in the ongoing, dynamic process of financial accumulation strategies, and contends that digital technologies, therefore, also comprise a crucial terrain of struggles over housing’s place in contemporary capitalism.

Introduction

A 2012 New York Times article titled “Investors Are Looking to Buy Homes by the Thousands” (Rich, 2012) followed a home inspector, armed with a clipboard and a tablet computer, through a series of foreclosed homes he was evaluating on behalf of Waypoint Real Estate, one of the large investors seeking to transform the business of single-family rental (SFR). 1 After plugging the notes from his clipboard into a software program on the tablet, the inspector obtained an estimate of the renovation costs needed to get a vacant property ready to rent. A “blistering pace” of 20 minutes per home was “necessary to keep up with Waypoint’s appetite” for speedy acquisitions “in a business that some deep-pocketed investors are betting is poised to explode” (Rich, 2012). Later, the renovation costs and other data points would be plugged in to a proprietary algorithm to calculate bids on foreclosed properties up for auction. As one of the company’s founders explained, bespoke computer systems and algorithms based on rental market data, maps, and field observations were central to realizing an ambition to “treat it [the SFR business] like a factory and create a production line” to acquire, renovate, and rent out foreclosed homes (executive quoted in Rich, 2012).

Single-family homes have long been a significant part of the rental market in the USA (Goodman and Kaul, 2017). But until recently they had never been owned and managed at scale, likely due to the cost and inefficiency (compared to apartment buildings) of managing large pools of scatter-site, spatially heterogeneous properties (Mills et al., 2017). The predominance of small-scale investors and fragmented ownership patterns within SFRs has worked against the possibility of structured finance opportunities such as securitization. However, this started to change in 2012. Large supplies of discounted property, constrained mortgage credit, and increased rental demand characterizing the US housing landscape after the height of the crisis presented an opportunity for private-equity-backed investors to assemble large, geographically dispersed portfolios and issue securitizations backed by rental income flows (Mills et al., 2017). The SFR market has undergone a structural change marked by an institutional concentration of ownership, facilitating the rollout of a new financial asset class. But, as the article “Investors Are Looking to Buy Homes by the Thousands” suggests, advances in digital technologies have been vital to capitalizing on the opportunity posed by post-crisis market conditions, and, consequently, to adapting property-led financial accumulation strategies for a new segment of the rental market.

A growing body of research confirms rental housing as an increasingly important site of experimentation for financial actors and logics (August and Walks, 2018; Fields, 2018; Wijburg et al., 2018). Primarily pursued from the perspective of critical political economy, this work generally neglects recent prominent transformations in information technology (such as the rise of big data, artificial intelligence, and cloud and mobile computing), despite their potential role in financialization, e.g. fostering greater transparency and comparability of assets. In a different theoretical register, social studies of finance have long documented how information technology has fundamentally remade the spaces, practices, and cultures of financial markets (e.g. MacKenzie, 2016; Zaloom, 2006), but rarely consider housing a “key object of financialization” (Aalbers, 2017: 542; though see MacKenzie, 2011; Poon, 2009 for relevant contributions). There is significant scope to expand research on the relationship between information technology and financialization (Currie and Lagoarde-Segot, 2017). Indeed, in overlooking digital technologies, scholars concerned with the treatment of housing as a financial asset miss an avenue of analysis vital to grasping how financialization is practically realized (though see Rogers, 2017a, 2017b for an exception).

This article centers the role of digital technologies in extending financial accumulation into new sectors of the housing market in the wake of the global financial crisis. The language of the factory and the production line animating Waypoint’s vision inspires my analysis. This terminology hints at the larger supply chain involved in extracting SFR income and organizing its movement to financial markets. How are digital technologies mobilized in this supply chain? What implications does this kind of analysis have for how we understand housing financialization? What can we learn here about contemporary social struggles over housing?

To answer these questions, I draw on three conceptual points of reference. Mezzadra and Neilson’s (2013, 2015) concept of operations of capital provides a wider analytic framework. This concept revolves around the logics of finance, extraction, and logistics that, together, define contemporary capitalism (Mezzadra and Neilson, 2013), and allows a focus on the socio-technical constitution of contemporary capitalism (a chief strength of social studies of finance) without sacrificing attention to its general tendencies (a core concern of critical political economies of financialization). I further mobilize economic sociology on Fordist-style vertical integration of financial firms (Goldstein and Fligstein, 2017) and expansive interpretations of logistics and extraction, respectively emphasizing the reorganization of economic space around the imperatives of circulation (Chua et al., 2018; Danyluk, 2017) and the application of “prospecting logics” to society (Mezzadra and Neilson, 2017: 194). These additional reference points are crucial to elucidating the organizational strategies pursued by investors like Waypoint, and how these strategies have made it possible to rework housing financialization in anticipation of a potentially post-homeownership society.

The central argument of this paper is that advances in digital technology have been essential to creating a new financial asset for the post-crisis era. In the process, such advances have given rise to what I term the “automated landlord”, whereby the management of tenants and properties is increasingly not only mediated, but governed, by smartphones, digital platforms, and apps, and the data and analytics these devices and infrastructures gather and enable. While post-crisis market conditions provided an opportunity for large investors, these were insufficient on their own. Digital infrastructures coming to prominence since the 2008 crisis (including platforms, tablets, and smartphones, along with new sources and scales of data and approaches to analytics) were required to automate core functions, such as rent collection and maintenance, “enabling property management at scale” (National Rental Home Council, 2019). New information technologies enabled investors to aggregate ownership of resources, extract income flows, and securely convey these flows to capital markets. This article shows how the process by which financial capital “has reshaped post-industrial societies around rentiership based on assets” (Ward and Swyngedouw, 2018: 1078) is an ongoing, dynamic one, in which technological transformations actively participate. Therefore, such transformations also comprise a crucial terrain of struggles over housing’s place in contemporary capitalism.

The remainder of this article unfolds in four sections. In the following section, I flesh out the analytic and conceptual framework, anchored by operations of capital (Mezzadra and Neilson, 2013, 2015), critical geographies of logistics (Chua et al., 2018; Danyluk, 2017), and work on firm organization and conceptions of control from economic sociology (Goldstein and Fligstein, 2017). I then discuss the rationale for researching a phenomenon affecting a small share of the rental market, and the methods employed in this study. The main body of the paper introduces the SFR asset class and highlights the logistical-extractive digital interventions necessary to its realization. In the paper’s conclusion, I focus on the wider implications of the rise of the automated landlord for contemporary housing politics.

An analytic of operations

The aim of this paper is to analyze the role of digital technologies in reconfiguring housing financialization in the post-2008 era. The concept of operations of capital proposed by Sandro Mezzadra and Brett Neilson (2013, 2015) guides this analysis for two reasons. The first is its capacity to speak across the divide between critical political economy and social studies of finance (Ouma, 2016). Mezzadra and Neilson (2015) emphasize that “the operation always refers to specific capitalist actors while also being embedded in a wider network of operations and relations that involve other actors, processes and structures” (2015: 6). Rather than privileging one level of analysis over the other, this perspective is concerned with “capital in particular material configurations” and “the articulation of operations into larger and changing formations that comprise capitalism as a whole” (Mezzadra and Neilson, 2015: 7). The emergence of new asset classes is a historically and geographically situated process, dependent on material and practical circumstances and calculative devices and techniques. These specificities matter because they constitute important sites of potential friction and struggle (Mezzadra and Neilson, 2015). But it remains important to capture how such instances of financial economization are embedded in and define the wider capitalist political economy. Operations of capital is a framework capable of traversing between the specific and the systemic, enabling my analysis of how financial actors have deployed digital technologies to reinvent the SFR market, and what this tells us about the politics of housing a decade after a crisis of capitalism predicated on financialization.

Second, Mezzadra and Neilson’s (2015) emphasis on extraction, finance, and logistics as “contiguous and interrelated domains” of activity (2015: 6) opens up new avenues of analysis— namely, extraction and logistics—that are at once beyond finance and necessary to its functioning. Whereas finance involves “abstract processes of control and manipulation” over economic production and everyday life to capture future value, extraction brings forth “the raw materials that drive capital’s creative destruction”, and logistics “organizes capital in technical ways that aim to make every step of its ‘turnover’ productive” (Mezzadra and Neilson, 2013: 12). Thus, while decades of political economic restructuring have made financial markets and logics increasingly important to capitalism by enabling the “emergence of powerful corporate monopolies, empowerment of investors, and their drive to create profitable assets” (Ward and Swyngedouw, 2018: 1080), contemporary capitalism cannot be reduced to finance. Rather, it is the intersection of finance with extraction and logistics that today defines capitalism and its expansion into new frontiers (Mezzadra and Neilson, 2013, 2015). As such, attending to logistics and extraction can enrich our understanding of financialization and multiply sites of political possibility.

Therefore, extraction, finance, and logistics participate in and are contingent upon one another. Finance depends on “the constant searching out, or construction of, new asset streams, usually through a process of aggregation” (Leyshon and Thrift, 2007: 98; Ward and Swyngedouw, 2018). This “searching out” points to extractive activities, understood not only in terms of the material removal of natural resources from the earth, e.g. mining, but as a broader application of “prospecting logics” across a range of social activities and geographic terrains (Mezzadra and Neilson, 2017: 194). Indeed, Leyshon and Thrift (2007: 98) draw parallels between the stable flows of income on which contemporary financial innovation depends, and “gold [as] … a source of value” for the financial system of generations past. As a result of neoliberal restructuring, today it is land, housing, and infrastructure that serve as key asset streams for finance, and which are therefore subject to prospecting logics (Allon and Barrett, 2018; Ward and Swyngedouw, 2018).

As with extraction, we can think of logistics in an expansive sense. The logistics revolution of the past 50 years fundamentally changed the way economic circulation is managed (Bernes, 2013; Cowen, 2014; Danyluk, 2017). Advances in transportation (ranging from containerization to drone delivery), information technology (e.g. radio-frequency identification tags to provide real-time inventory updates, Amazon’s robot-enhanced fulfillment centers), and transformations of territory (such as large-scale infrastructure projects remaking ports and establishing transport corridors) enable the acute calibration of today’s complex global supply chains (Chua et al., 2018; Cohen, 2014; Danyluk, 2017). But, as Chua et al. (2018) argue, logistics is not reducible to a mundane science of cargo movement or a discrete industry among others … it is better understood as a calculative rationality and a suite of spatial practices aimed at facilitating circulation—including, in its mainstream incarnations, the circulatory imperatives of capital and war. (618)

I draw upon these expanded understandings of extraction and logistics to examine the role of recent advances in digital technology in post-crisis housing financialization. These “mutually implicated” (Mezzadra and Neilson, 2015: 3) domains share in common an increasing dependence on digital data and infrastructures and processes of algorithmic calculation. Private-equity-backed investors in the SFR market relied on logistical-extractive digital interventions to realize a new asset class in the wake of the 2008 crisis, seeking to become automated landlords. However, the organization of new rental companies was also a crucial ingredient in this process. As Goldstein and Fligstein (2017) argue in their work on firms involved in producing subprime mortgage-backed securities, 20th-century Fordist logics of mass production and vertical integration are relevant to financialization in the 21st century. They show how financial firms adopted an industrial model in which the value chain from mortgage origination to securitization to sales was internalized. This model ensured access to a steady supply of raw materials (mortgages) for the mass production of financial assets, eliminated middlemen, and enabled rent extraction (in the form of fees) throughout the process (Goldstein and Fligstein, 2017). The key actors effecting the financialization of SFR have pursued a similar strategy of vertical integration, enabling them to achieve economies of scale and control costs along the supply chain. Such vertically integrated firms have been best positioned to benefit from using digital tools that emerged in the tech boom of the past decade.

In the sections to follow, I analyze how vertically integrated SFR companies have deployed logistical-extractive digital interventions to, in the words of Waypoint Real Estate’s founder, “create a production line” capable of extracting aggregated rental income flows and packaging them as securities for sale to investors. By attending to the particular ways housing financialization has been reworked to suit the post-2008 political economic context, this account provides another angle from which to consider the possibility of frictions and moments of struggle within this process. Before turning to this analysis, I establish the rationale for this research and explain my methods.

Research rationale and methods

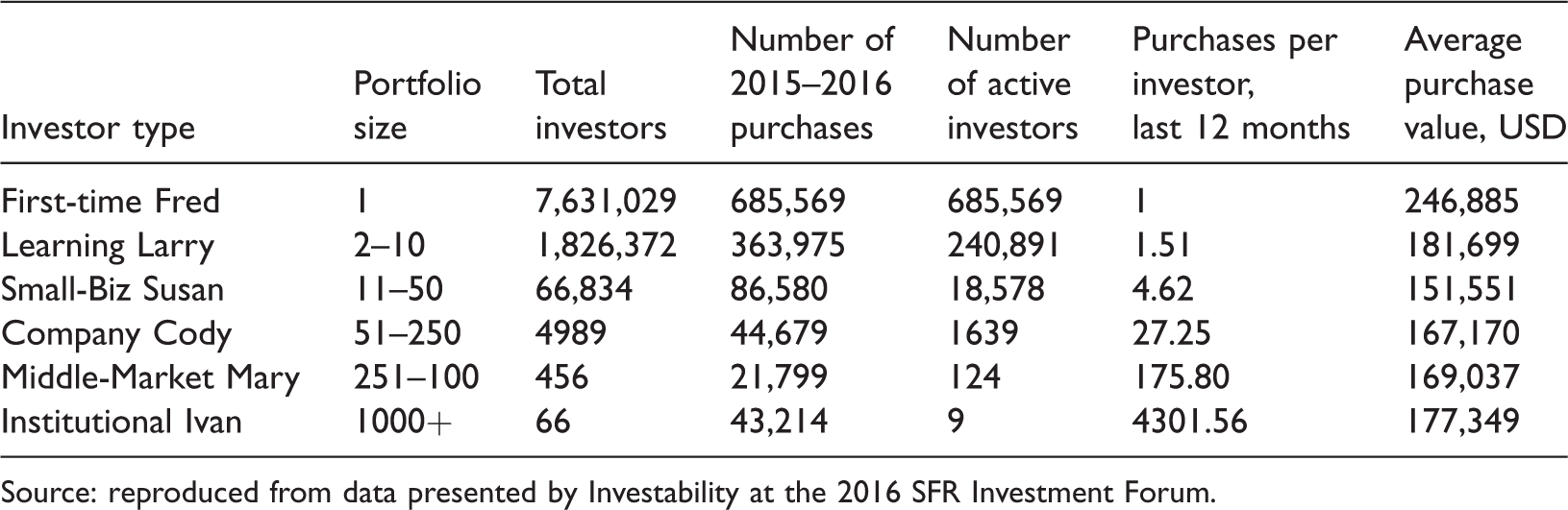

The SFR industry is in the midst of a fundamental transition. Single-family homes have accounted for a large share (approximately 40%) of rental units for decades, but the number of SFR units has grown significantly since the US foreclosure crisis (Goodman and Kaul, 2017). Bordia (2017) estimates the SFR inventory expanded from 11.2 million in 2006 to 15.4 million in 2016. This increase is largely attributable to tenure conversion as formerly owner-occupied single-family homes became rental units (Joint Center for Housing Studies, 2015). Coincident with this process is the emergence of large-scale ownership of SFR homes by financial actors. The presence of institutional investors is new in the SFR market (Mills et al., 2017), and the majority of SFR investors still own fewer than 10 properties (Table 1). At most, institutional investors own and operate 300,000 SFR homes, roughly 2% of the market (National Rental Home Council, 2019). Nevertheless, financial actors serving as SFR landlords are worthy of study because they carry weight beyond their quantitative market share in several ways.

SFR investor segmentation (incudes SFR detached, condo, and townhouses, excludes 2–4 unit homes).

Source: reproduced from data presented by Investability at the 2016 SFR Investment Forum.

First, the interest of large-scale investors in SFR introduces an ensemble of new players – including private equity funds, credit rating agencies, technology firms, and non-bank lenders – into a market that has operated, more or less, as a financial backwater for its entire history. Even if the share of ownership by institutional investors remains small, the narratives of SFR and proliferation of business models associated with their entrance to the market are not necessarily limited to such actors and the properties they own. For example, institutional investors’ need to estimate rents across a variety of markets enabled the emergence of data providers specific to SFR (Fields, 2018), but this mode of seeing the market is now widely available to all kinds of actors in the space. The role of institutional investors in SFR entails new ways of framing and valuing homes and new logics and forms of knowledge about SFR investment; these have the capacity to circulate and take root beyond institutional actors.

Second, the SFR asset class represents a novel innovation in financial engineering. SFR securitization involves elements of both residential and commercial asset-backed securities and may thus be understood as a hybrid product (Fields, 2018; Raymond, 2014). Despite the currently small scale of SFR securitization relative to the size of the addressable market, such financial innovations are mobile and flexible, subject to being reworked in incremental ways as they are shifted into different geographical contexts (Wainwright 2015: 1644). Situated accounts of the processes surrounding the emergence of new financial products matter because they provide a reference point from which to understand potential future iterations.

Third, the corporate entities carrying out the institutionalization of SFRs wield political power associated with their access to capital and in-house financial and legal expertise. They utilize these resources to maintain and extend their market advantage. For example, Blackstone, the investment firm behind Invitation Homes, the largest SFR landlord, contributed nearly US$7 million (accounting for one of every seven dollars of support) to back a 2018 campaign opposing a California ballot proposition to extend rent control to single-family homes (Dayen, 2018). Large SFR companies also employ specialists in negotiating tax appeals to petition for property tax valuation reductions, helping to maximize revenues by minimizing contributions to the local tax base (Epstein, 2017). Several of the SFR companies with nationwide brands have established a trade group, the National Rental Home Council, to represent the interests of large-scale landlords and related vendors and service providers in the media and to policymakers. Such efforts show how institutional investors in SFRs have implications for the public beyond the tenants actually living in their properties.

On the basis of the above rationale, this paper provides insight into the changes underway within the SFR sector. I focus on the largest SFR landlords (those with national footprints, including Invitation Homes, American Homes 4 Rent, Waypoint Homes, Progress Residential, and Tricon American Homes) and a small number of technology companies that cater to such investors. My analysis employs ethnographic data, semi-structured interviews, and desk research. I conducted participant observation at three SFR investment forums in the USA over 2015–2016. At the forums, I attended panel discussions on topics such as rental turn management; marketing to large institutional private players; rental process simplification and automation; securitized debt investors; acquisition strategies; and demographics of single-family renters. I also interacted informally with attendees and vendors during coffee and lunch breaks, receptions, and offsite networking events. My conference badge clearly stated my institutional affiliation, allowing me to identify myself as a researcher studying the transformation of SFRs when interacting with other attendees.

In addition to participant observation, semi-structured interviews and desk research inform the analysis. I initiated contact with a number of attendees before each forum, using an application made available by the conference organizers or LinkedIn, to request meetings to discuss my research. Through this process, networking at the forums, and referrals provided by contacts, I completed 12 semi-structured interviews ranging from 30 to 90 minutes in duration with key actors in the SFR industry. 3 Participants primarily included non-traditional SFR actors, such as software developers, founders and staff of digital platforms geared to the SFR sector, founders and chief technology officers (CTOs) of nationwide SFR companies, rental market analytics providers, and representatives of credit rating agencies. Recordings of panel discussions made available on the investment forum website complement interview data. Ongoing desk research is vital to understanding the pace and extent of transformations within the SFR industry in recent years. Monitoring coverage in popular and business media, finance industry and think tank analyses, tech industry news, and relevant academic research provides crucial background and context for this research.

Operations of capital in a financial backwater

An asset class for a rentership society

Even as single-family homes were incorporated into capital markets through mortgage securitization, the SFR sector existed as a backwater cut off from structured finance. But in 2013 it became the site of a new financial asset class via the securitization of rental income flows (Rahmani et al., 2014). As of this writing, 14 companies have completed 54 SFR securitizations that include approximately 195,000 properties. 4 Of these issuances, 45 were single-borrower securitizations completed by large-scale landlords that own and operate portfolios consisting of several thousand properties (in the case of Invitation Homes, over 80,000 5 ). Single-borrower securitizations account for 168,000 SFR properties and have leveraged approximately US$25 billion in debt based on rental income anticipated over the two to five years from issuance. The nine remaining issuances are multi-borrower securitizations of loans made by non-bank, private-equity-backed lenders to smaller-scale landlords, leveraging approximately US$2 billion in debt. Five SFR companies have also gone public as real estate investment trusts (REITs), most recently Invitation Homes, whose early 2017 US$1.5 billion initial public offering was particularly notable for the US$1 billion backing provided by government-sponsored enterprise Fannie Mae (Dezember and Timiraos, 2017). The penetration of SFR by capital markets through selling debt to bondholders (securitization) and raising equity from shareholders (REITs) signifies SFRs as a new space of housing financialization for a post-2008 era of declining homeownership rates (Fields, 2018; Mills et al., 2017; Rahmani et al., 2014). 6

The emergence of SFR financialization suggests the “rentership society” heralded by some finance industry analysts (Chang et al., 2011) may be in formation. Rental units have fulfilled nearly all US housing demand since 2010, and SFR is the fastest-growing segment of the rental market (Strochak, 2017). By 2050, the combination of rising housing costs relative to income, ongoing constraints in mortgage credit, and persistent racialized wealth and income disparities could lead to a US homeownership rate below 50% (Acolin et al., 2016). In seeking out sources of future value based on flows of rent payments in place of mortgage payments, the SFR asset class anticipates the possibility of a return to a majority-renter society not seen in the USA since the early1940s (US Census Bureau, 2011). To slightly recast Arvidsson’s (2016: 3) framing of the social logic of the derivative, the advent of SFR landlords with national reach reconfigures the social relations of rent in ways amenable to the demands of financial accumulation. That is, securitization of rental income from single-family homes affords the present realization of future value, to be extracted from tenants, who are now indirectly bound into relationships with bondholders and shareholders (Bryan and Rafferty, 2014). While financial accumulation centered on housing after the 2008 crisis is thus persistent, the SFR asset class demonstrates the important role of prospecting logics to extract new sources of raw materials for financial products, and logistical processes to securely convey these materials to capital markets.

Governing the SFR supply chain

While SFR homes are place-bound and cannot “be hurtled instantaneously through space”, the notion of the supply chain that animates logistical processes is nonetheless relevant to the SFR market (Cowen, 2014; Danyluk, 2017: 9). The sale of securities to bond investors represents the end point of a supply chain that begins with establishing sources of supply—in this case, rental income from single-family homes. The formation of the SFR asset class has depended upon the practical ability to acquire suitable properties at scale, rehabilitate them, lease the properties to tenants able to provide monthly rent checks, and manage operations and turnover—all while maintaining a regular flow of rent checks to bondholders.

Here, vertical integration has served as a crucial organizational form. As a market tactic by financial firms, vertical integration is shaped by what Goldstein and Fligstein (2017) refer to as an “industrial conception of control” (485) in which firms see internalized supply chains and scale economies as the most profitable route to the production of financial instruments. This organizational model enables larger operators to exert greater control over, and standardization of, key processes in the SFR asset supply chain (managing director of credit rating agency; Invitation Homes, 2017b). For example, the biggest SFR companies “all have deals with Lowes and Home Depot … special paint blends and so forth, really systematizing rehab to make turnover efficient and save money by buying in bulk” (managing director of credit rating agency). Because “new markets draw on conceptions of control from nearby markets”, it is possible the proximity of mass-produced, mortgage-backed securities by vertically integrated financial firms served as a model for the firms behind the SFR asset class (Call, 2017; Fligstein, 1996: 665; Goldstein and Fligstein, 2017).

In turn, information technology platforms enable vertically integrated SFR operators to govern this supply chain. As the former CTO of a large-scale SFR company stated, “one of the biggest things is just knowing where your stuff is, knowing the status of things. We like to think of our business as a manufacturing line; it’s this linear process that has to happen.” The challenge for such operators – and, thus, the importance of investing in technology – is “if you have 20,000 assets all over the country, how do you know which asset is in which phase?” (former CTO, SFR company). Bespoke technology platforms support such visibility into workflows and makes field operations transparent to executives. From an upstream perspective, this visibility and transparency is desirable to credit rating agencies, the banks putting together securitizations, and investors, because it demonstrates an ability to meet reporting requirements and, across different operators, lends the ability to generate a larger body of data about the asset class as a whole (Fields, 2018).

In-house technology platforms as a means of “knowing where your stuff is” bring the operation of logistics into focus – visibility and transparency are, as Bernes (2013) notes, prominent “watchwords of the logistics industry.” Logistics governs and coordinates supply chains to afford the circulation of commodities, promoting flow and motion in an effort to eliminate any profit-impeding friction (Bernes, 2013; Danyluk, 2017). The apparently technical nature of logistics can obscure the fact that is deeply political, remaking space on behalf of capital accumulation regimes that intensify unequal power geometries (Chua et al., 2018; Cowen, 2014; Danyluk, 2017). Though logistics typically deals with the “science of circulation” by which transport and communications enable the physical flow of goods (Cowen, 2014: 25; Danyluk, 2017), here we are concerned with the circulation of rent checks from tenants to large-scale SFR landlords and eventually to bondholders or shareholders. For rent payments extracted from tenants of single-family homes to serve as the raw material for new financial products, a set of calculative interventions was required to establish and protect sources of supply and coordinate the smooth flow of rental income from tenants to capital markets. Therefore, one way we can understand the violence of logistics is through their close association to contested processes of extraction.

For financial markets, the post-2008 context has called for applying prospecting logics to “new attributes of households” beyond mortgage payments in order to open new seams of assets for financial products (Bryan and Rafferty, 2014: 895). The imaginary of the SFR “manufacturing line” highlights how institutional landlords sought to render erstwhile sites of dispossession and the intimate terrain of the home as homogenous and “equivalent, exchangeable, interchangeable” space (Lefebvre, 2009, cited in Chua et al., 2018: 622). Employing logistical-extractive interventions that include algorithmic underwriting and intelligent and automated workflow management techniques, large-scale investors have selectively re-aggregated repossessed homes and coordinated operational processes so as to “grab value” (Andreucci et al., 2017) by re-opening spaces of financial accumulation in the wake of crisis.

Logistics to extract rental income

The advances in mobile and cloud technology and data analytics seen in the 2010s, and the way these developments drove down the cost of developing custom business technology infrastructure (Owens, 2015), are vital to the operation of extraction and logistics underlying the SFR asset class. For example, Waypoint Real Estate emphasized how their use of “lean startup methodologies on cloud computing platforms” let them “quickly deliver applications that create scale” needed to start up the SFR asset manufacturing line (Nazar, 2011). Indeed, financial assets are only viable insofar as they assemble together a group of often-dispersed and fragmented income streams, nonetheless understood to be similar: they depend on bundling and commensurability (Leyshon and Thrift, 2007; Martin, 2013). According to American Homes 4 Rent (2018), the difficulty of efficiently acquiring individual homes was a fundamental reason SFR companies with a national presence did not develop sooner. But SFR companies overcame this obstacle through developing what they term an “acquisition engine” (American Homes 4 Rent, 2018: 1) or “acquisition platform” (Invitation Homes, 2017a: 7), organized around data fed into a proprietary underwriting algorithm. These data might encompass “neighborhood desirability, proximity to employment centers, transportation corridors, community amenities, construction type, and required ongoing capital needs” (Invitation Homes, 2017b: 7). The algorithm uses these data in combination with target yield and other investor specifications to identify desirable properties and generate prices. Such software allowed SFR companies to scale-up portfolios rapidly and deploy capital to the right submarkets and neighborhoods (Mills et al., 2017). Acquisition algorithms represent the logistical architecture by which finance capital was able to access sources of raw material, thereby expanding its frontiers.

Underwriting algorithms widen the scope of potential acquisitions while reducing the time needed to evaluate and purchase properties. They give investment funds “a way for our guys, our buying guys, to not have to drive to every house,” instead managing a queue from their desktop and making the acquisition process faster. The logistical focus on capital turnover comes to the fore here: How quickly can we make an offer so we could tie up a property? If we could do it within minutes of it listing, that was a value-add that technology would create, allowing us to get competitive advantage at quick- acquiring properties just through our speed of evaluation and underwriting. (Former CTO of SFR company)

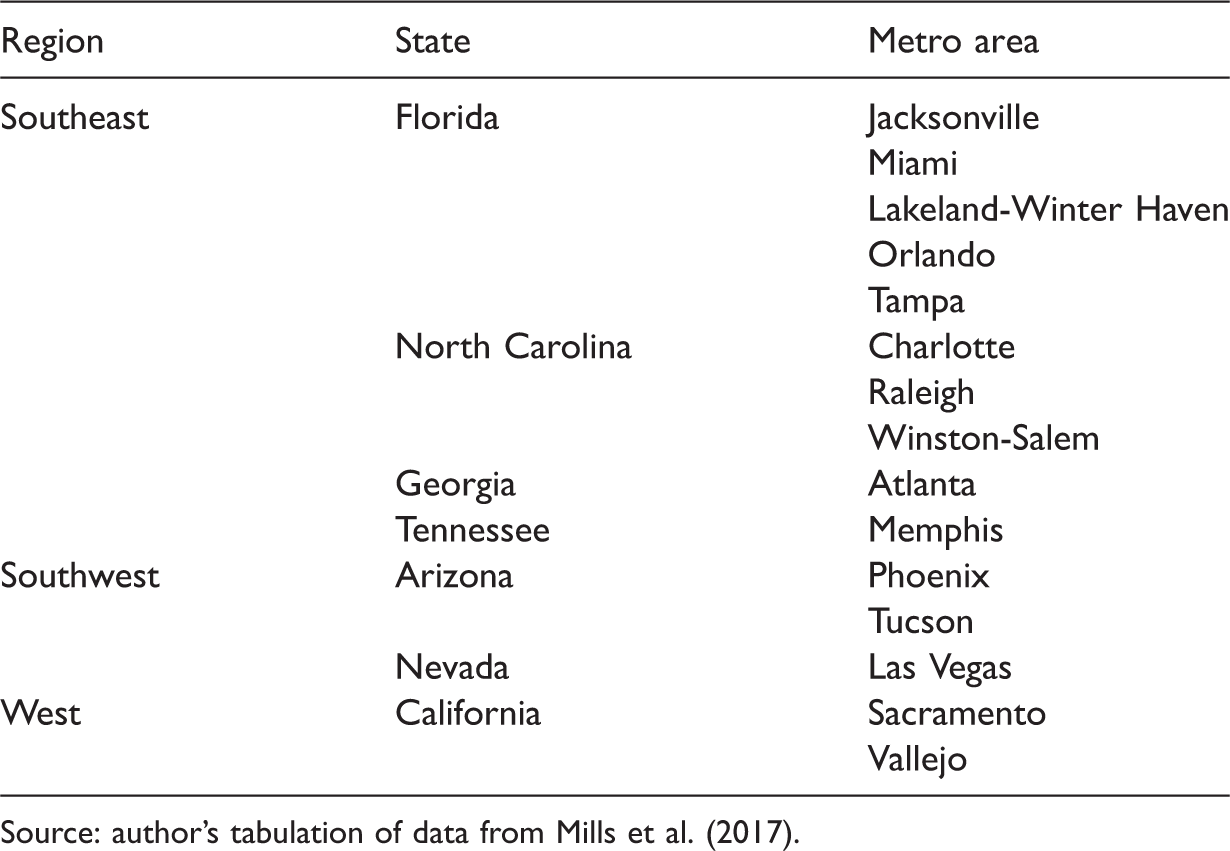

As the industry initially ramped up in 2012–2014, this set of relations drove rapid, geographically targeted capital deployment, establishing property rights capable of being “mobilized to extract value” (Andreucci et al., 2017: 2, emphasis in original). Large-scale investors established portfolios in a relatively small number of markets over this period: just 15 metropolitan areas in seven states made up the top 10 markets for acquisition across all three years, with a marked focus on the southeast and southwest regions of the country (notably Atlanta and several markets in Florida, see Table 2) (Mills et al., 2017). 7 Compared to other investors in single-family homes, large-scale investors were much more likely to purchase homes built since 2000 (48% of purchases by large-scale investors versus 17–23% of purchases by other investors; Mills et al., 2017).

Top metropolitan areas for purchases by large-scale investors, 2012–2014.

Source: author’s tabulation of data from Mills et al. (2017).

Indeed, the geographic focus of acquisitions by such investors overlaps significantly with the geography of the Sunbelt construction boom of the 2000s (Aalbers, 2009; Rudolf, 2009). Assembling geographically dense portfolios of relatively new homes could ease some of the frictions associated with managing large numbers of scatter-site properties because more recently built properties may be more similar to one another than older homes, potentially simplifying processes of rehabilitation and maintenance. This drive toward commensurability, or “making things the same” (MacKenzie, 2009), is at the heart of all financial markets. Nevertheless, the problem of incommensurability—the uniqueness of each single-family unit and their spatial dispersion within market areas—represents a potential drag on capital turnover time.

Automating operations

Underwriting algorithms served to start up the SFR asset assembly line, but institutional investors’ ability to manage large portfolios spread across the country was a source of concern (and skepticism) from capital markets as to the viability of the SFR asset class (Neumann, 2012; Raymond, 2014). Despite the density of SFR acquisitions within sub-markets, managing repairs and maintenance of scattered houses differs substantially from the centrally located and standardized (multifamily, office, or retail) units underlying commercial mortgage-backed securities (former director of operations, SFR company). Vertically integrated SFR landlords have been able to use in-house technology platforms to establish operational efficiencies that ensure the timely and secure movement of rental income along the supply line. Such systems also serve as a signal to investors and capital markets that SFR companies are able to exert control over property management and operating costs (former CTO, SFR company).

The surge in digital technology, especially smartphone adoption, coinciding with the institutionalization of SFR has helped large-scale operators automate interactions with tenants. Digitally mediated landlord-tenant relations are a response to the obstacle of distance inherent in attempting to centrally operate large and dispersed property portfolios. All SFR landlords with national brands have regional offices in major markets; indeed, they deem such local presence a crucial factor in exerting greater control over property management (Invitation Homes, 2017). Nevertheless, regional offices may be located quite far from properties – some states may have only one, or none. For example, in seven states where American Homes 4 Rent has properties, it does not have a property management office. Tenant-facing digital technologies serve to enact presence and immediacy in landlord–tenant relations otherwise marked by distance.

Such technologies comprise a vital node in the circulation of rent checks between Main Street and Wall Street because they drive down costs and create efficiencies for landlords. All large-scale operators provide online portals (often available as mobile apps) for prospective tenants to search and apply for properties and for current tenants to pay rent and submit maintenance requests, (partially) replacing the phone call or the face-to-face interaction. Keyless entry systems enhance the productivity of leasing agents by allowing prospective tenants to use a lockbox code sent to their smartphone to view properties themselves: “[before self-viewing] we used to think one agent doing 12 leases a month was just total domination, a huge win … [after] I’d say we were routinely seeing people doing 30 leases a month” (former CTO, SFR company). Digital technologies also let SFR landlords devolve tasks to current tenants. At a 2016 investment forum, one chief executive observed, “tenants are happy to do a lot of work property managers do themselves.” One example is submitting maintenance requests with photos through a mobile app, potentially avoiding sending a contractor to the site to diagnose the problem, or making their time on site shorter. Landlords also use their websites to coach tenants in home maintenance with blogs and embedded videos (Figure 1), effectively cultivating a subjectivity of ownership that offloads responsibilities onto renters. Similarly, Waypoint Homes briefly experimented with a loyalty and rewards system called “Waypoints”, in which tenants earned points for behaviors aligned with the interests of landlords (such as renewing their lease), which could then be exchanged for rewards that, in many cases, added value to rental properties (e.g. appliances, smart home hardware) (Fields, 2017; Nazar, 2014). Finally, Invitation Homes offers tenants smart home technologies to control temperature and door locks from their smartphone for a monthly fee, but, once installed, smart home hardware supports light-touch management of vacant properties during the turnover process (managing director of credit rating agency). Through this range of automated and digitally mediated interactions with tenants, SFR landlords introduce speed (e.g. in processing rent payments and leasing properties) and cost and labor savings (i.e. by shifting the work of property viewings and home repairs to tenants) that smooth out points of potential disruption in the flow of rental income to capital markets.

Sample of Invitation Homes “Maintenance & How To” videos, November 2018 (https://www.invitationhomes.com/video_category/maintenance-how-to/).

Further digital measures are directed at the contractors carrying out repairs and maintenance on SFR homes. The widespread availability of mobile computing and the geo-locative capabilities it affords provide a source of what Neilson and Rossiter (2011) term “biopolitical technology”, targeting bodies and subjectivities so as to secure the supply chain and render it transparent (Bernes, 2013; Cowen, 2014). Recent technological advances have dramatically expanded the opportunities for the surveillance of workers by employers in a range of workplaces, making headlines in 2015 after a woman was fired for deleting an employee tracking app from her smartphone (Ajunwa et al., 2017). This kind of tracking is particularly salient to large-scale scatter-site SFR portfolios because of the high potential (versus multifamily housing) for overhead inefficiencies in maintenance to “make or break profitability” (former director of operations, SFR company). Digital surveillance of contractors provides a means of holding together the intensely local and granular nature of property management and maintenance, dispersed as it is across the thousands of homes in a dozen or more markets in which any one large-scale SFR operator is active, with a centralized corporate strategy and infrastructure.

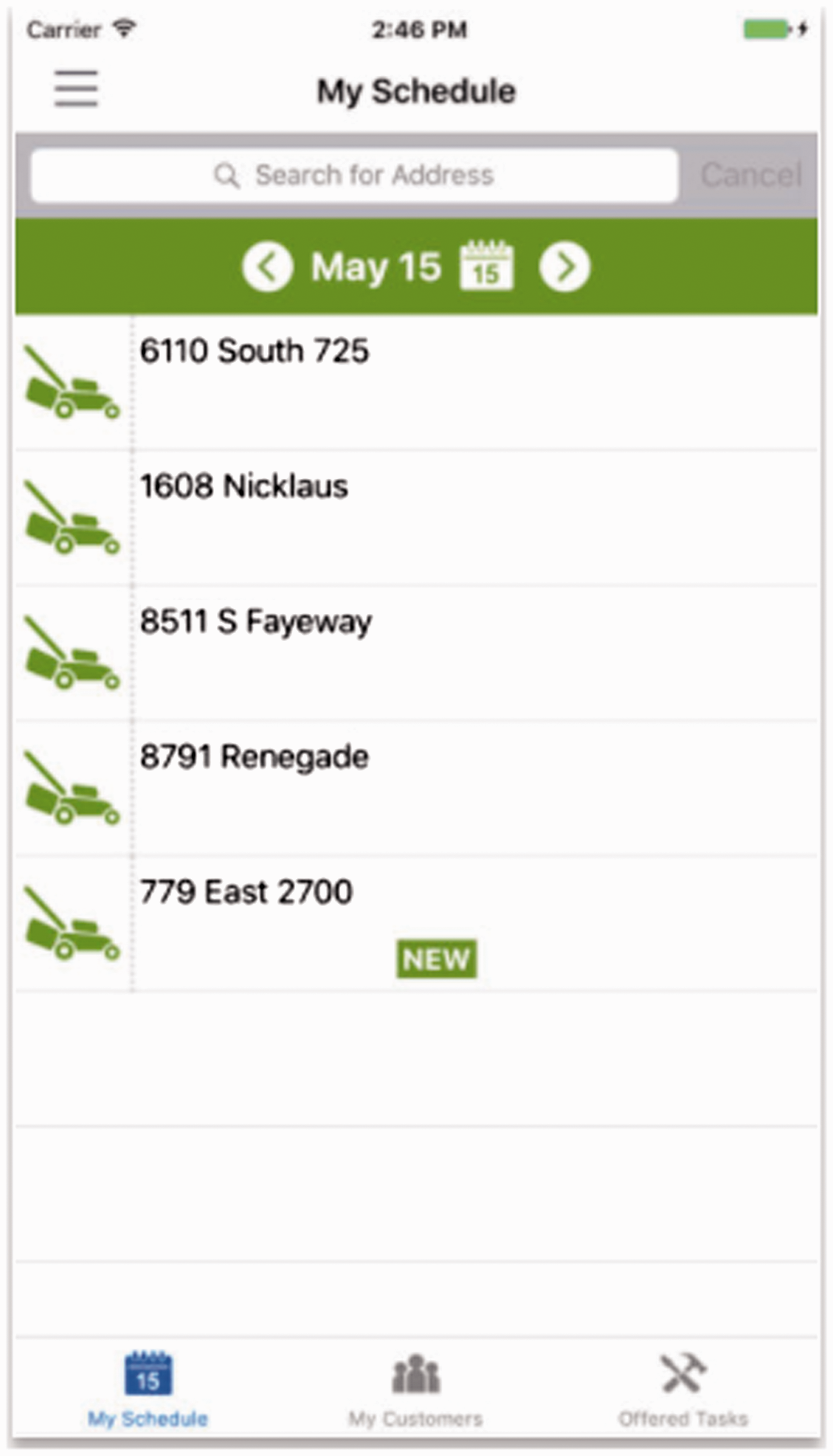

Echoing the concern of scientific management with the bodies of workers and their movements (Cowen, 2014), contractors completing repair and maintenance work on behalf of institutional landlords are compelled to use smartphone apps with geo-locative technology. In addition to optimizing routes to minimize billable time spent on the road (see Figure 2), the apps require contractors to check in and out at job sites and upload before and after photos of their work. As the chief executive officer (CEO) of a property maintenance platform whose customers include large-scale SFR companies explained:

Screenshot of sample work order route from app for maintenance vendors.Source: Apple App Store.

I can count on every one of our contractors having a smartphone, and therefore we can communicate with them in a fairly sophisticated way by laying down their routes in front of them, because all smartphones have GPS [Global Positioning System] instrumentation. We can collect photos as evidence of work being performed. All the audit data can be rolled up in that, not just photos but also in GPS and timestamp when they’re on site.

Thus, digital tracking of SFR contractors gives distant landlords visibility into their portfolios that can be used to “make the day of the guy swinging the hammer more efficient” (former director of operations, SFR company). In other words, the photographic evidence and metadata about time and location created as contractors carry out their work provides a check on carelessness, inefficiency, or fraud (CEO of property maintenance platform). Such techniques constitute what we could term “discipline by metadata” because deviations from the job route and billable hours on job sites may be checked against metadata from the app. In effect, digital tracking and governance of SFR maintenance work seeks to standardize the costs of operating geographically dispersed property portfolios through maximizing the efficiency and compliance of contractors.

Experiments in easing the frictions of circulation

Despite the effort by the SFR industry to deploy logistical interventions to ensure smooth, rapid capital turnover, disruptions and blockages are unavoidable. Here, the accumulation of data emerges as a chief advantage of vertical integration: keeping property operations in-house also keeps field data in-house, creating opportunities for analysis and experimentation to ease the inevitable frictions of circulation. As the CEO of one SFR company observed at a 2016 investment forum, “we larger operators end up becoming data and logistics companies” due to the “massive amounts of data” on consumer preferences, product quality, and operational processes call centers and technology platforms enable them to collect. Internal technology platforms add value to large-scale SFR because they may be used to optimize operations. For example, the former director of repairs and maintenance operations for one SFR company explained how an analysis of maintenance requests at different rent levels motivated a decision to equip properties renting at lower rates with fewer amenities, because the data showed they tended to generate more maintenance requests. Technology platforms also let operators evaluate the results of such experiments because they can “look at the real data.” [For example] it’s taking us seven days to re-key every house after we buy it; why is it taking so long? That shouldn’t take so long. So we could focus on little time-cycle issues like that, then start to drive them down because we had the visibility to see if the solution we came up with was actually implementing the intended change. (Former CTO, SFR company)

As the SFR industry has matured, new points of friction have emerged, including the problem of buying and selling tenanted properties. This problem emerged as the industry grew and various operators have sought to either cull their portfolios, disposing of properties that no longer meet their investment objectives, selectively add to their portfolios to achieve greater economies of scale in key markets. In both instances operators lose potential rental income (vacating properties before sale or finding tenants for vacant properties) and face added costs (broker and agent fees, marketing costs, and rehabilitation). While this friction barely existed before 2008, it has since necessitated the development of logistical infrastructures in the form of online trading platforms that coordinate the transfer of property rights from one investor to another, while keeping tenants in place and cutting out the need for traditional real estate brokers and agents. The motivation underlying such platforms thus resonates with the circulationist emphasis of just-in-time production and its view of “everything not in motion as a form of waste, a drag on profits” (Bernes, 2013). Indeed, with stated aims of “enabling investors to treat their real estate investments more like stock portfolios” and “bringing transparency and efficiency to create a better way to transact” (Roofstock, 2017), SFR trading platforms embody the ideals of visibility and liquidity by which the contemporary logistics industry operates (Bernes, 2013; Cowen, 2014) (see Figure 3).

Property organized into categories on SFR trading platform.Source: Roofstock website. https://www.roofstock.com/investment-property-marketplace

Conclusion

This article analyzed how institutional investors have deployed the tools of the post-2008 tech boom— including mobile computing, new sources of data and analytics, and digital platforms— to exploit favorable US housing market conditions and launch a new financial asset class based on bundled income flows from SFR homes. Indeed, digital technologies were absolutely vital to realizing the vision of the SFR supply chain articulated by private-equity-backed investors. An assemblage of proprietary algorithms, data, tablet computers, home inspectors, “buying guys” at foreclosure auctions, and corporate executives made it possible to initiate this assembly line by scaling up geographically dense property portfolios in target markets. Tenant-facing digital engagement, internal technology platforms, and digital tracking of contractors carrying out property maintenance work together to automate and standardize the operation of these portfolios so as to expedite and secure the flow of rental income along the supply chain to capital markets. Investors are able to target blockages and disruptions in a data-driven way due to the portfolio intelligence built up via their technology platforms, and through developing novel logistical infrastructures such as trading platforms for occupied properties. Moreover, these interventions have been a crucial part of projecting competence to capital markets so as to instill their faith in an untested asset class. However, full automation of the role of the landlord is unlikely due to the idiosyncrasies of both tenants (such as those who insist on paying by check rather than an online portal, or speaking to a person over the phone rather than a chatbot) and properties (such as the particular way the cause of a sticky lock needs to be diagnosed and repaired). Rather than implying that an ideal of full automation has – or can be – achieved, the concept of the automated landlord advanced in this article points to how digital technologies augment the capacities of landlords in ways that also reshape the realities of what it means to be a renter.

Arguing that researchers concerned with housing financialization have overlooked the role such technologies play in this process and that social studies of finance tend not to address housing, I claimed a focus on socio-technical processes was necessary to better understand the politics of housing a decade beyond the global financial crisis. In one sense, the operations of capital analyzed in this article are specific to the rearticulation of financialization in the US housing market. Digital tools and techniques constitute a core component of the operations of capital in housing markets. They support extraction by working to establish a supply of raw materials (here, rent checks) and work logistically by lending calculative power to govern and accelerate capital turnover, thereby making it feasible for financial actors to capitalize on future value in the realm of housing in ways not thought possible before 2008. But while the SFR asset class is young and the share of the SFR market controlled by large-scale landlords small, my analysis also highlights crucial tendencies about contemporary capitalism more broadly, and, therefore, offers insights about social struggles over housing in that context.

Despite the scale and severity of the 2008 crisis, housing assets today remain “foundational” for strategies of financial accumulation (Allon and Barrett, 2018: 125), though such strategies now extend to rental housing more than they did a decade ago (August and Walks, 2018; Fields, 2018; Wijburg et al., 2018). Underlining the integral role of digital infrastructures, devices, datasets, and analytics in reaffirming housing as a liquid asset demonstrates how new technologies (from the surveyor’s chain to the underwriting algorithm) inevitably reshape how we “practice ownership, use, and exchange of the earth” (Shaw, 2018: 6). Furthermore, if we recognize housing as a crucial vector of social inequality and “the immense power and capital at stake in real estate markets” (Marcuse and Madden, 2016; Shaw, 2018: 6), digital technologies must be understood as part of the terrain of current and future housing politics. This proposition is especially apparent in the SFR market because of how such tools allowed investment firms with global reach (such as Blackstone) to exploit the dispossession associated with the US foreclosure to forge a new asset class. But the politics of digital transformations of housing extend far beyond SFR: the application of digital advances to housing is seen as a tremendous market opportunity because of the size of the real estate sector in advanced economies (Baum, 2017; Maarbani, 2017). 8

As part of how we use and interact with space, the digital is materially grounded in everyday life and inseparable from the power relations therein (Graham et al., 2013; see also Eubanks, 2018). Whether we consider smart home devices marketed to landlords as a way to monitor their investments and surveil tenants, platforms whose revenue depends on generating bidding wars between tenants in tight rental markets, start-ups that use online activity to profile and rank tenants, or the ability for landlords to exclude “undesirable” market segments from viewing rental listings on Facebook Marketplace (Angwin and Parris Jr., 2016; Childs, 2016; Hall, 2018), digital technologies clearly have the potential to exacerbate what are already fundamentally uneven power dynamics in the realm of rental housing. But is this only a shift in intensity, a ratcheting up of existing politics?

I would argue there is something new here, and that it relates to what Fourcade and Healy (2017: 9) term the “information dragnet.” They argue that while the use of data to sort, score, and facilitate decision-making in the market has a long history, today we are in “a new era of data collection and analysis” (Fourcade and Healy, 2017: 11). This era is marked by the simultaneity with which aggregated and individualized records can be managed, the continuous nature of data collection and its capacity to stubbornly follow individuals as they move between platforms and the non-digital world, the status of (even public) data itself as a commodity, and the automation of so much classificatory work—obscuring the human agency in these processes. The information dragnet is the means by which stores of data are amassed (e.g. as we shop, search, socialize, consume services, and so forth), in turn setting in motion the algorithmic “sorting and slotting of people into categories or ranks” to extract profits (e.g. as a desirable tenant willing to pay for extra amenities, or an undesirable one who may be charged a higher security deposit) (Fourcade and Healy, 2017: 14). These categories carry economic rewards and punishments that contribute to socio-spatial stratification (Fourcade and Healy, 2013, 2017). The rise of the automated landlord means that current struggles to build tenant power vis-a-vis landlords in cities around the world (Axel-Lute, 2018; Card, 2018; Gray, 2018) must both develop tactics for confronting the operation of the information dragnet, and start envisioning how digital technologies might be used toward housing justice, rather than housing commodification.

Footnotes

Acknowledgments

Drafts of this paper were presented at the ISA-RC43 conference in Hong Kong, the ISA RC21 conference in Leeds, the Royal Geographical Society annual conference in London, the American Association of Geographers conference in San Francisco, the Economic Worlds seminar series in the School of Geography at the University of Nottingham, and the Information School seminar series at the University of Sheffield. I extend my gratitude to participants in these venues, and to Shaun French and Chris Muellerleile, for feedback on the work in progress, as well as the constructive feedback from three anonymous reviewers on earlier drafts.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by a British Academy/Leverhulme small grant (grant number SG153338).