Abstract

While attention has been paid to how politico-legal reforms have enabled or inhibited the entrance of institutional investors, less is known about how these providers impact or challenge existing actors, regulations, processes, and institutional arrangements within local housing systems. This article departs from the case of Sweden: it has been discussed how institutional investors have been enabled by the country’s soft rent regulation, which is based on a collective bargaining process between all providers and the Swedish Union of Tenants (SUT) and allows for sharp rent increases after renovation. We show how in the Swedish case large institutional investors exploit existing institutional arrangements and challenge the norms that underlie the functioning of the rental housing system. To explore and illustrate this process we rely on the theory of incremental institutional change and complement it through the conceptual metaphor of “gaming.” We argue that housing systems can be understood as playing fields in which different actors employ tactics to defend or advance their interests, without, necessarily, the need to formally change the rules of the game. We suggest that more attention should be paid to institutional investors’ active engagement with local housing systems over time, beyond dichotomies of enablement or inhibition.

Introduction

In the last days of March 2023, news broke that the Nordic institutional investor Heimstaden is demanding a reopening of the yearly rent-setting negotiations in Malmö, Sweden’s third-largest city. Rents in Sweden are set through a collective bargaining process between The Swedish Union of Tenants (SUT) and the individual companies. Legitimized by global inflation and skyrocketing interest rates, the local negotiations for that year had ended in a historically high increase of 5 percent. But Heimstaden, Malmö’s and Sweden’s leading private rental provider, was not satisfied, demanding another 2 percent increase to be effective as of July 2023. Other providers, among them a Swedish pension fund, a local stock-listed company, and the German-listed rental property giant Vonovia (operating as Victoriahem in Sweden) followed suit. As SUT did not agree to the second increase, the landlords 1 involved in the quibble raised the rents in the meantime, with most tenants paying the additional bill. They also threatened to file complaints against all non-paying tenants with the regional Rent Tribunal, a legal authority set to solve rent disputes. In 2023, SUT Malmö had managed to fight back, forcing the four landlords to an agreement to compensate tenants who had already started to pay the new rent and back off from further complaints. Calling back for a second increase after negotiations have been concluded, is legal, however, an uncommon practice in the Swedish context (Bendzovski cited in Hyregästföreningen, 2023). When we asked the chairman of SUT Malmö, why he thought these particular landlords chose this rather confrontational path, his sober answer was “they are testing the system, they want to see how far they can go” (Interlocutor 1).

The question of how far institutional investors can go in the Swedish rental housing system is the question inspiring this article. Christophers (2013) described Sweden’s housing system as a “hybrid monstrosity,” that is retaining some of its protective features such as the above-mentioned yearly rent negotiations and a relatively resilient municipal housing sector (Blackwell and Bengtsson, 2023), while also being one of the most liberalized systems in Europe with little to no state involvement. This hybridity, as we show in this article, produces a unique field for institutional investors, who, as the case of Malmö illustrates, exploit existing regulations efficiently while also challenging the institutional arrangements and underlying norms governing the rental housing sector.

To conceptualize the interactions of institutional rental housing investors with the Swedish housing system we rely on the framework of incremental institutional change developed by Kathleen Thelen, Wolfgang Streeck, and James Mahoney (Mahoney and Thelen, 2010; Streeck and Thelen, 2005). Thelen et al. have argued for a shift in focus from more radical toward more incremental, gradual, and possibly accumulative institutional change. Research on incremental change has shown that institutions and how they work are ambiguous: rather than static, institutions are evolving structures that are “the object of ongoing skirmishing” (Streeck and Thelen, 2005: 19) between actors with different, sometimes clashing interests. The skirmishing is what this article seeks to zoom in on. To do so, we complement the incremental change framework by mobilizing the conceptual metaphor of “gaming.” We suggest that an integration of the notion of gaming into an institutional analysis of rental housing financialization helps us to think about rental housing financialization, not solely as an outcome of certain institutional and/or political arrangements but as an ongoing, dynamic, and relational process that unfolds over time. We centralize the relations between institutional investors and SUT and focus on the rent negotiation process as a playing field in which actors try to advance their interests.

Our article contributes to the existing literature in multiple ways: first, this article contributes to furthering our understanding of how rental financialization unfolds in specific institutional settings. Second, paying attention to the interactive dimension of rental housing financialization adds to the theorization and analysis of institutional change: by mobilizing the conceptual metaphor of gaming, we specify how the process is not linear with financialization either happening or not, but shaped by an ongoing back-and-forth between different actors. Finally, we show that institutional investors’ involvement in local housing markets could have effects beyond affordability, namely the challenging and, at times, alteration of the housing system’s underlying arrangements and norms.

We first present the theoretical framework and then provide a contextualization to the Swedish case. Our empirical material is based on semi-structured interviews conducted in 2022 and 2023, with current and former negotiators and staff in senior positions at SUT (10), both on national and region levels including Stockholm, Gothenburg, and Malmö, and representatives from public and private housing companies (3). 2 We also draw on a pilot study of the changing landscape of rental housing in the context financialization that was conducted between 2020-2021 in Husby, Stockholm, with a focus on everyday life experiences and the role of local tenants’ organization and SUT in ameliorating housing conditions (Kadıoğlu and Kellecioğlu, 2023; Kadıoğlu et al., 2022). The material is presented in four sections, consecutively discussing the conditions, renovation strategies, and negotiation tactics of institutional investors. The last empirical section considers the reasons for the recent escalation of the conflict. The article ends with a brief conclusion discussing the main findings, theoretical contribution, arguments, and pathways for future research.

Understanding incremental institutional change

In the 2000s, historical institutionalists Thelen, Streeck, and Mahoney (Mahoney and Thelen, 2010; Streeck and Thelen, 2005) challenged dominant models of path dependency by suggesting a theory of incremental institutional change. Their theory is based on a non-static conception of institutions, perceiving them as ambiguous entities whose evolution is dependent not only on the (changing) rules that govern them but on the ways these rules are interacted with. This can take the form of actors’ reinterpreting, subverting, circumventing or even ignoring some institutional rules, which, in turn, may result in lasting changes over time. This, less reified, view of institutions, opens the possibility for a more nuanced analysis of political and societal transformations.

Many examples of incremental change can be found within the context of economic regulation and deregulation. While there is broad academic consensus that the forces of globalization and liberalization do not simply “wash over” countries and their national and local institutional arrangements (Peck & Theodore, 2007), there is less understanding of the different modalities of change beyond severe exogenous shocks. Anderson (2015), for example, suggests that incrementalism has been characteristic of reforms to Germany’s welfare system. Similar to our case, Sweden, this may largely be due to the consensus and negotiation-driven German political culture. To create a conceptual framework for the analysis of incremental institutional change, Streeck and Thelen (2005) have identified five modes of change:

Displacement (slow supersession by a new set of rules/arrangements),

Exhaustion (breakdown or non-use of rules causing their withering away),

Layering (new rules/arrangements attached to the old structures),

Drift (neglect/non-maintenance in the context of external change),

Conversion (repurposing of old rules/arrangements).

In housing research, the use of Thelen et al.’s incremental change model is less prominent than in other fields of welfare research (see Béland, 2007; Thelen, 2009). Bengtsson and Kohl (2020) ascribe this to two factors: first, housing’s material durability makes the application and differentiation of the five modes of change difficult. Second, in many cases, housing provision has always heavily relied on market provision—for example, private and public finance and ownership have always been “layered.” Finally, in a more general critique, Bengtsson and Kohl (2020) note that especially drift, layering and conversion are difficult to distinguish from one another—in reality, these three processes are often connected. There is thus a substantial risk of concept stretching and subjective interpretation when employing this typology.

In this article, we scrutinize the financialization of rental housing from the perspective of historical institutionalism and, more specifically, incremental institutional change. Considering the limitations of this model, we focus on incremental change as a starting point while maintaining that the different modes of change are not mutually exclusive, reified categories but, in a longer-term perspective, might occur subsequentially or even concurrently within the same process. Even when used less rigidly, we suggest that the modes of change are useful for describing more subtle changes in housing systems that often occur alongside, in conjunction, or in the aftermath of critical junctures (see also Blackwell, 2021). As we discuss below large, institutional investors may play a particularly significant role in triggering incremental change.

Rental housing financialization and incremental change

The field of rental housing financialization has grown remarkably over the last decades. Scholars have shown how institutional investors maximize profit by engaging in a variety of strategies: in some circumstances, they might, for example, exploit welfare arrangements such as taxpayer-guaranteed rent flows linked to tenants eligible for housing benefits (Bernt et al., 2017). In other cases, the location might determine the specific tactic—investors may “squeeze” poorer tenants in less favorable locations in the city out of revenues by increasing ancillary costs while pursuing aggressive building upgrades in gentrifying areas (August and Walks, 2018). In settings where regulations allow for rent increase after renovations and/or energy retrofitting, demand for rental is high, and gentrification sufficiently spread throughout the city, these upgrades may turn into a more generalized strategy, also covering less attractive neighborhoods. Bernt (2022) has recently described this as the exploitation of a legally engineered “modernisation gap.” Scholars have also shown that institutional investors employ strategies to demobilize tenants through divide-and-rule tactics or inconsistent and untransparent communication (Crosby, 2020; Fields, 2017).

Most institutional analyses of rental housing financialization, however, tend to focus on the politico-legal conditions (such as privatization, loopholes in rent regulation etc.) that enable or disable the entrance and profit-maximizing behavior of institutional investors—in other words: that institutional investors either find favorable conditions and make use of them or they do not. However, housing systems, are not coherent, some rules or arrangements might be favorable to the growing influence of financial markets, others might not. As van Gent (2013: 508) reminds us, sets of institutions may be “the outcome of different political struggles in different eras.” So are old institutions oftentimes not fully replaced by new ones leading to institutional layering. Similarly, the role of long-standing institutions might change without them being abolished (i.e., conversion).

We suggest that the entrance of institutional investors may even further complicate the picture. Christophers (2022), drawing on the example of the US private equity firm Blackstone, has, for example, noted that the inherent capacities of large institutional actors, such as capital-access, size, as well as a multiscalar and deterritorialized mode of operation, have a discernible impact on not only if, but how, existing arrangements are engaged with. These investors do not simply exploit already-existing market conditions and systems, but advance strategies that, while specific to the local context, match their financial organization and capacities. This echoes van Gent’s (2013: 508) suggestion that “ultimately, an institution is defined by the interaction between those that make the rules and those whom the rules concern.” In other words: if the way the housing system is interacted with changes, this might also, in the long run, change its institutions. We suggest that what needs to be further specified, beyond the different types of incremental change, is the interactive process between those who make the rules and those who are subjected to them. For this, we mobilize the conceptual metaphor of gaming.

Making moves: analyzing the interactions between institutional investors and housing systems

As discussed in the previous sections, taking a less reified view of institutions as objects of constant “skirmishing,” redirects our attention to not only the type of change that could be the result of this skirmishing but also the way different actors engage with institutions and what happens along the way. As Mahoney and Thelen (2010: 8) hold, institutions are “fraught with tension” because they organize distributional outcomes that disadvantage or benefit actors at given moments in time. Rather than assuming that the distributional outcomes of housing institutions are just accepted by relevant actors, we suggest that more attention must be paid to the specific strategies employed by institutional investors to not only exploit but also circumvent, subvert, selectively ignore, or mobilize a certain set of rules over another within a housing system, and to discuss what the consequences are for the system.

To further illuminate what is referred to as “skirmishing,” we employ the conceptual metaphor of “gaming.” As Rogers (2023) notes in a recent commentary, conceptual metaphors have some tradition in urban studies. We adhere to the notion that conceptual metaphors are not just modes of linguistic expression, but modes of thought that can hold explanatory power (Lakoff and Johnson, 1980). The use of the gaming metaphor in describing processes of financialized accumulation is by no means new: Strange (2015) famously referred to western financial systems as “vast casinos” with few rules and regulations to constrict players, losses, or wins. Haiven (2014) referring to the financialization of the online gaming industry employs the term “Pokéconomy” to explicate how financialization entails a blurring of the boundaries between work and play, speculation, and gambling. Wijburg et al. (2018), in turn, suggest that listed housing companies in Germany “game” rental regulations through specific renovation strategies. However, in housing research, gaming metaphors are mostly used anecdotally and not further explored. We suggest that an integration of the notion of gaming into an institutional analysis of rental housing financialization can be productive because it helps us to think about rental housing financialization, not solely as an outcome of certain institutional and/or political arrangements but as an ongoing, dynamic and relational process that unfolds over time.

Under the overarching metaphor of gaming, we will mobilize the notions of “rules of the game” to describe the politico-legal setting(s) in which institutional investors find themselves in Sweden, “players” and “positions” to refer to the main actors that negotiate and organize distributional outcomes within the housing system, and “moves” to describe the back-and-forth of these players within the context of a given game plan. Finally, we describe transformations that have been instrumental in changing the institutional setting (i.e., the game plan) as “game changers.”

Neoliberal reforms and the dismantling of public housing

The Swedish housing system has been built on the ideals of a universal housing regime and goals of tenure neutrality—a path that was set out by the social democrat’s national housing policy in 1947 (SOU, 1947:26). A large part of post-war housing construction was subsidized non-profit public rental housing, owned by the municipalities, and available to everyone within a unitary housing system (Kemeny, 2006). The peak of housing construction came with the launch of the Million Program in 1965, a massive publicly subsidized construction boom, leading to the erection of more than one million dwellings within a decade, for a population of then eight million and under heavy involvement of municipal housing companies (hereafter MHCs).

The Swedish rental system today is governed by a form of soft rent regulation based on annual negotiations between SUT and the various landlords. This system is a replication of the Swedish corporatist model on the labor market where deals between labor unions and the employers’ organization are set without the interference of politicians or the state (see Rolf, 2021; the Saltsjöbaden Treaty of 1938). Since 1968 negotiations have been based on the so-called use-value system: use-value calculations are based on a complex set of parameters according to which rents are to be negotiated and set. Factors, such as, for example, the size of the apartment, but also appliances such as a washing machine or floor heating are considered. Since its inception, the use-value system has been criticized extensively, from pro-market actors for being untransparent and disconnected from market value, and from critical housing researchers, left politicians, and activists for its exploitability (Polanska et al., 2019). The main loophole in the system is that while regular and structural maintenance is to be included in the rent, renovations, if they are determined to raise the standard of the apartment, can result in sharp rent hikes. While the annual negotiated increase during recent years has been around 1–2 percent, renovations have been shown to lead to increases of around 50 percent, frequently resulting in displacement (Boverket, 2014). One could suggest that this loophole has opened up possibilities for landlords to “game” the Swedish rental system by engaging in “predatory” (Polanska et al., 2024) renovation practices and also led to a form of institutional drift in which rent setting has somewhat lost its regulatory power. Particularly affected are the Million Program housing areas in which institutional investors have a significant proportion of their housing (Mangold et al., 2023). These areas have reached or passed their 50-year life cycle and are in dire need for comprehensive renovations, also because previous owners have often neglected timely interventions (Thörn et al., 2023).

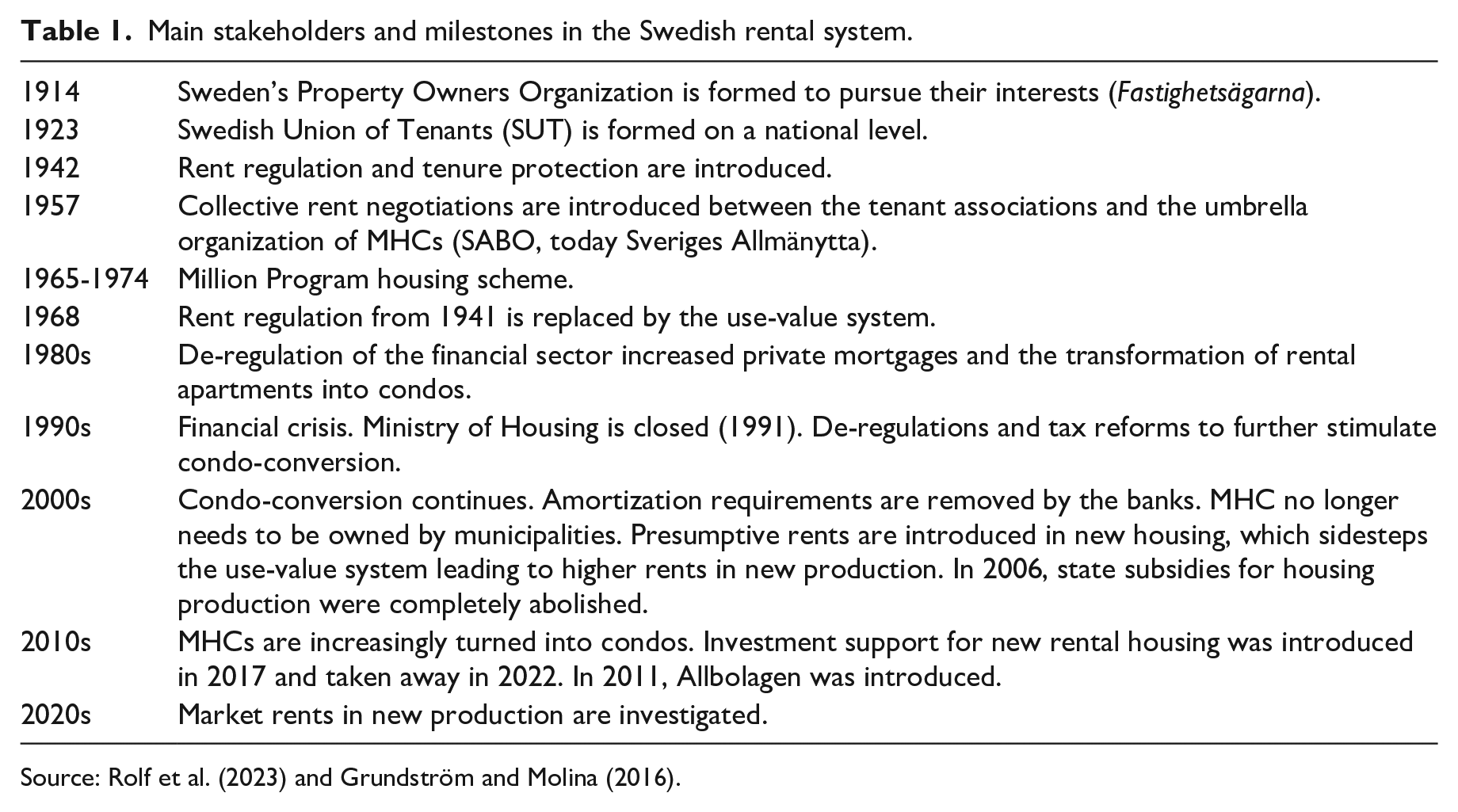

While the 1968 introduction of the use-value system has already had a substantial effect on the rental housing sector, a series of neoliberal reforms since the aftermath of the Million Program have further weakened the position of tenants. After earlier reforms to foster home ownership, the cutting of subsidies, and taxation of MHCs maintenance funds, a law called Allbolagen (i.e., “the public housing act”) was introduced in 2011. Allbolagen came about after Sweden’s Property Owners Organization (Fastighetsägarna), which includes most private landlords, complained to the European Commission, suggesting that Sweden’s rental system gives an unfair advantage to MHCs, violating EU competition laws (Elsinga and Lind, 2013). As Ösgård and Wallstam (2023) note, while SUT and the umbrella organization of MHCs (formerly SABO, now Sveriges Allmänytta) opposed, they did not substantially resist and drafted an alternative proposal that, with some alterations, accommodated the private providers’ claims. While before 2011, MHCs had a norm-setting role in the rent-negotiating process, giving tenants a somewhat stronger hand in negotiations, Allbolagen abolished MHCs’ privilege giving other providers leeway to push for higher rents. Moreover, MHCs were commissioned to conduct themselves “business-like” (i.e., profiteering), bringing them much closer to the conduct of private landlords. SUT today has a somewhat difficult and ambiguous position regarding both the use-value system and the more recent neoliberal reforms: the organization has been cautious not to deride the system, despite its apparent weaknesses, since it is their main tool to influence the rental market, legitimize their own position as the legal representative of tenants in Sweden and avoid the step toward non-negotiated market rents. Table 1 summarizes the main institutional changes in the Swedish housing market since the early 1900s.

Main stakeholders and milestones in the Swedish rental system.

Source: Rolf et al. (2023) and Grundström and Molina (2016).

The setup: a new game plan and the rise of institutional investors

As Blackwell (2021) discusses some of the challenges to Sweden’s housing system and the provision that we see today, date back to regulations in housing finance and the structure of the construction sector already from the 1970s onward. It can thus be argued that the shortage of supply and access to affordable housing across virtually all Swedish cities today both have a long forerun in earlier contradictions and have been reinforced through the neoliberal reforms of the 1990s and 2000s. In this sense, we understand Allbolagen at once as the path-dependent result of a stepwise deregulation of Sweden’s once universalist housing system (Bengtsson & Ruonavaara 2017), as well as a game-changing legislation in terms of both rules and players. In the language of institutional change, Allbolagen could be said to have resulted in a form of institutional layering in which new rules (i.e., the loss of MHC norm-setting role, the need to act “business-like”) were added on top of still existing old institutions and rules (i.e., the continuation of a unitary housing market, rent setting). Curiously, SUT, at that time, did not perceive this as particularly consequential to the system thinking that the rent-setting process and a relatively resilient public housing sector, would keep SUT in its strong position. This also explains why there was only little resistance from within the organization:

SUT made a big mistake, thinking this won’t change much, but it led to a complete system change. Now there is no roof for what landlords can ask for, no stopping mechanism. (Interlocutor 5)

It can be stated that Allbolagen, at least over time, has contributed to effectively converting public housing’s role from one of ensuring the availability of affordable housing to “just another” market player:

Before we could negotiate with them [MHCs] and they would show us their numbers and say we did this and this. Now we cannot even demand the numbers anymore because it is a business secret. (Interlocutor 2)

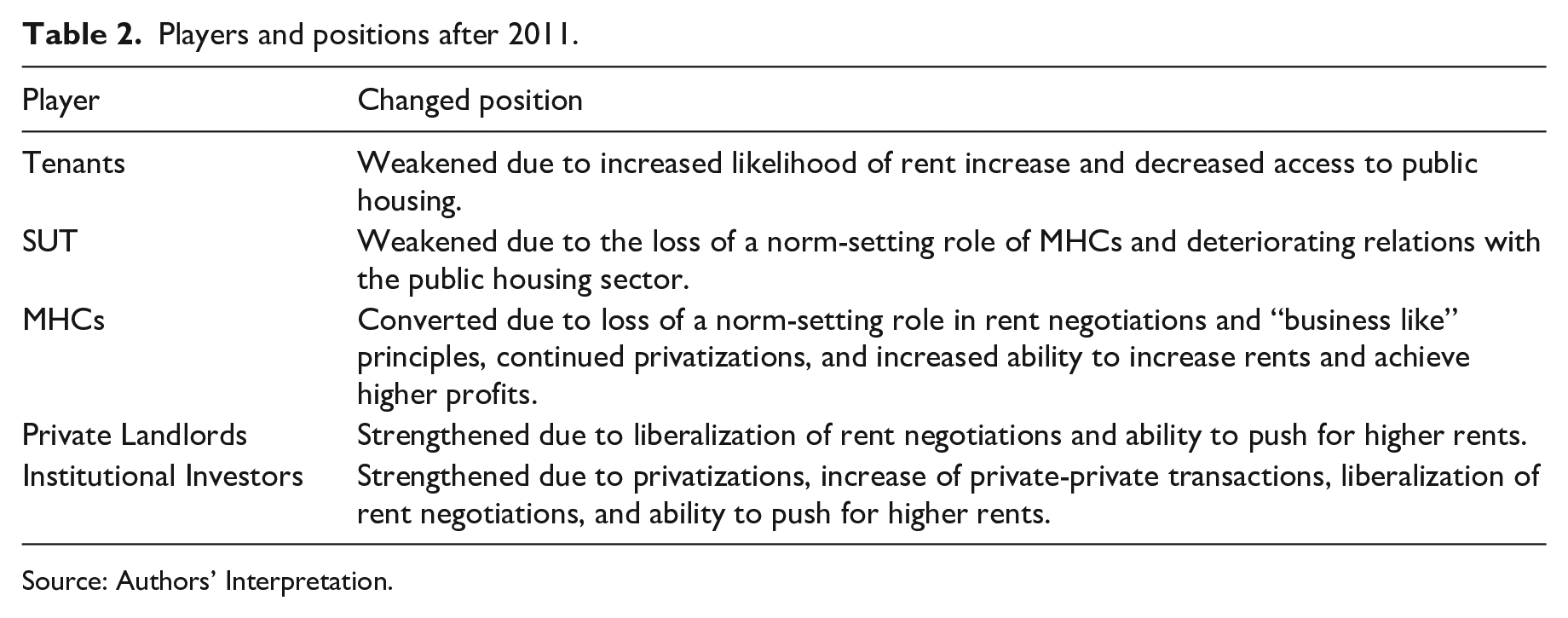

But the legal reform not only changed the rules and positioning of different actors in the system, it also fueled transactions to and between larger, often transnational, institutional investors (see Table 3). Grander and Westerdahl (2024) have shown that while, before 2011, most privatizations were in the form of condo-conversions, after 2011, sales to larger, private landlords from both MHCs and smaller private landlords increased. Some municipalities divested all their public housing stock and many MHCs changed their letting practices, not accepting, or lowering the number of tenants receiving social benefits (Grander and Frisch, 2022) (see Table 2).

Players and positions after 2011.

Source: Authors’ Interpretation.

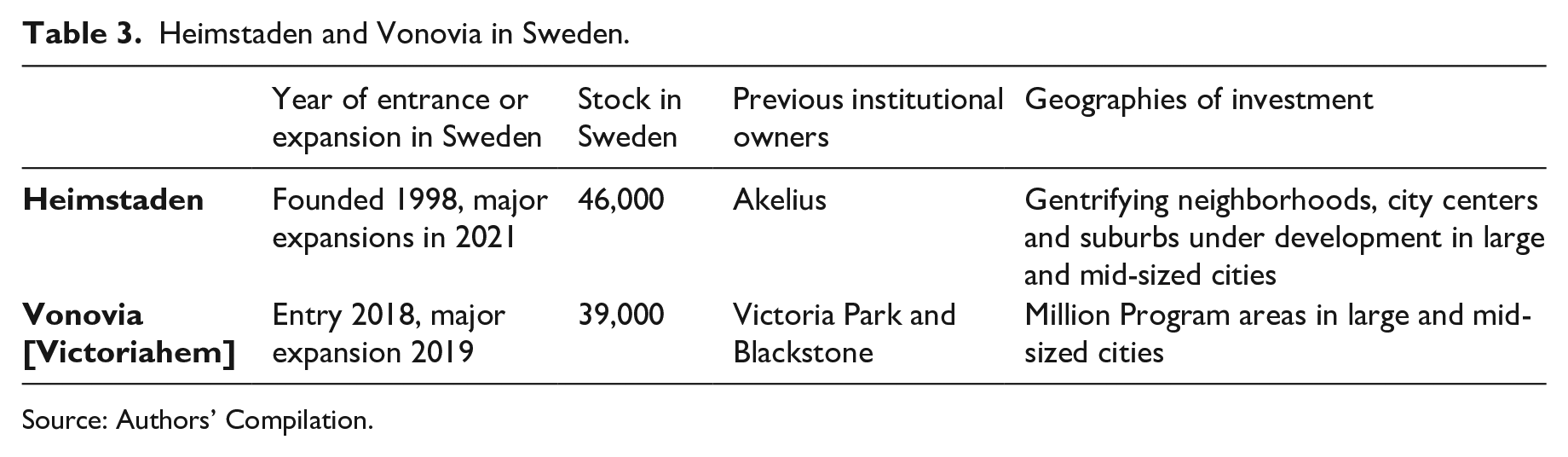

The two dominant institutional players today are the listed companies Heimstaden with headquarters in Malmö, and the German real estate company Vonovia, operating as Victoriahem in Sweden (see Table 3). Heimstaden and Vonovia are Sweden’s largest and second-largest private landlords, respectively. Most of the housing stock acquired by the two companies had been in the hands of other institutional investors, notably the listed Swedish company Akelius, the Malmö-local listed company Victoria Park, and the US private equity fund Blackstone. While Akelius is one of the earlier, pre-crisis, players, starting to buy property in Sweden already in the mid-1990s and expanding to Germany in 2006, Victoria Park entered in 2012 and Blackstone in 2016. Both companies mostly own stock in growing urban centers, with Vonovia having concentrated a large share of its stock in the Million Program areas.

Heimstaden and Vonovia in Sweden.

Source: Authors’ Compilation.

However, Heimstaden and Vonovia also benefited from privatizations taking place after 2011, in light of the pressure on MHCs to increase profit and renovate their remaining stock (Grander, 2018). Both companies become part of a local public–private merger in Malmö Rosengårds Fastigheter, which is owned in equal shares by the two companies, the MHC MKB and the Nordic listed company Balder. The merger was the result of a large-scale privatization of stock that was previously owned by MKB, corresponding to 7 percent of the total public housing stock in the city (Gustafsson, 2022).

All in all, Allbolagen can be described as a game-changing intervention in a long string of neoliberal reforms that have gradually but steadily dismantled the universalist features of the country’s housing system and made Sweden an increasingly attractive market for institutional investors. In the next section, we discuss how this new setup not only fueled the entry and expansion of institutional investment into rental housing but also introduced new renovation and negotiation tactics.

Gaming the Swedish rental system: concept renovations

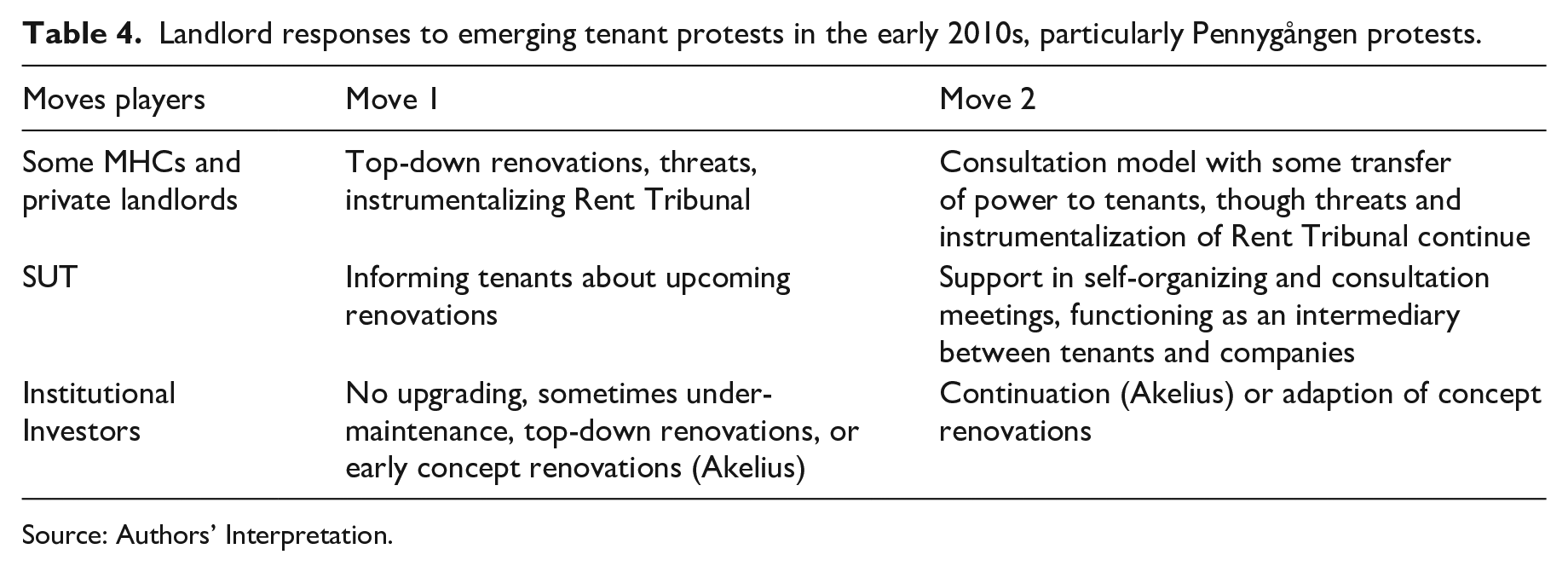

As described above, due to the cumulative changes in the Swedish housing system, SUT and tenants over the last decades already since the 1970s have lost considerable power. One move that, however, is, until today, still possible is that tenants can use their right to reject standard-increasing renovations. Landlords, private and public, have circumvented this by taking tenants to the Rent Tribunal, or threatening to do so. Rent Tribunals are regional court-like instances that decide on rental disputes. Studies have shown that around 90 percent of these cases are decided in favor of the landlord (Baeten et al., 2017; Polanska, 2023). These “renovictions” (Molina and Westin, 2012) have triggered collective countermobilization by tenants and activists. This has had profound effects on private and public housing companies as well as on SUT, in some cases forcing a change of tactics: one example was a long tenant-led struggle in Gothenburg’s Pennygången neighborhood against the Swedish, family-owned provider Stena Fastigheter in 2012. The company eventually backed down from the planned 65 percent increase, offering a consultation model with different renovation options to tenants (Thörn, 2020). Some MHCs had established similar models beforehand, also upon tenant protest (Thörn and Polanska, 2023). Moreover, as Thörn et al. (2023: 15) report, in conjunction with pressure from tenants, SUT itself reorganized the way it approached renovations, going from a more passive stance of informing tenants to actively supporting them to self-organize. While these consultations have not provided a straightforward solution to renovictions and have also been criticized, the tenant protests forced both housing companies and SUT to re-strategize (Thörn and Polanska, 2023). The “drifting” pathway of the Swedish rent setting might thus have been to some extent altered by tenant resistance that forced, at least some, landlords into a new engagement with the rules that govern the renovation process.

However, publicly listed Akelius, Heimstaden’s predecessor, did not follow this move. Instead, the company employed so-called “concept-renovations” (konceptrenovering), meaning upgrading apartment by apartment, as tenants move out with an excessive focus on internal upgrading rather than structural renewal (Mangold et al., 2023). This can, for example, take the form of installing new appliances or floor heating. Akelius had started to upgrade vacated apartments successively in Berlin in 2007, and in the early 2010s, just in the aftermath of Allbolagen, started to apply the same renovation strategy in Sweden (Olsén & Björkvald, 2019: 9). It thereby managed to kill four birds with one stone while staying in the legal framework: (1) circumventing social unrest, (2) targeting areas of the apartment which are known to legitimize sharp increases in use-value, such as bathroom and kitchen renewal, while forgoing costly structural work, (3) maintaining cash flow from other tenants in the building, and (4) maintaining the market value of unrenovated apartments in the form of unrealized value gains. While scholarship engaging with renovations in Sweden has mentioned concept renovations as popular strategy among institutional investors (Christophers, 2022: 12; Gustafsson, 2021: 6) and while the issue has been problematized in parliamentary debate and by public authorities (Boverket, 2021; Riksdagens protokoll, 2021/22:30), the wider consequences of the systematic use of concept renovations for the Swedish housing system are less understood. First, Akelius’ “discovery” was soon emulated by other landlords whose stock was of sufficient size, most of which are institutional (Mangold et al., 2023; Olsén and Björkvald, 2019):

The system had been the same all the time [allowing for rent-increase after renovation] [but] he figured it out. It was a combination of Akelius seeing this business model that was different and [what had happened] in Pennygången, and the problems that the landlords had with tenants not wanting a total renovation. So, it were these two things combined and then I think that business model went international. (Interlocutor 6)

In other words: Akelius’ move, that is, a novel engagement within an already existing set of rules, not only led to more renovations and rent increases in the company’s own housing stock but affected the sector more broadly, changing other landlords’ behavior and leading to a more profound challenge for SUT and rent negotiations. While Akelius has described its own investment activity in Sweden and in other countries as “cherry picking”—that is, buying properties with a potential for luxury upgrades, for example, in gentrifying neighborhoods in urban centers (FastighetsSverige, 2014), Victoria Park and Blackstone subsequently used concept renovations in the low-income suburbs of Malmö and Stockholm. Vonovia and Heimstaden—the two companies that took over the portfolio of these providers in 2018/2019 and 2021, respectively, continued to operate the same way. To sum up, institutional investors invented new strategies to game rent regulations and tenant resistance (see Table 4).

Landlord responses to emerging tenant protests in the early 2010s, particularly Pennygången protests.

Source: Authors’ Interpretation.

Stranding apartments, dividing tenants

The spread of concept renovations as a “move” among institutional investors and some other landlords also impacted the rent negotiation processes—in conjunction with post-renovation demands for sharp rent increases, the number of so-called “stranded apartments” increased as well. Stranded apartments are apartments for which no agreement could be reached during rent negotiations. The negotiation is then interrupted, and landlords often start to charge higher rent to tenants. If they refuse, the case might end up at the Rental Tribunal, where the landlords are likely to win (Polanska, 2023). The stranding of apartments is not new but has become more widespread and has been systematically used among institutional investors. Significantly, SUT again identified Akelius as a tone-setting player:

Landlords now do this in general, but I would say Akelius started it. They were on the forefront. But Victoriahem will do it, Balder [a Nordic-based, listed company] will do it, any big company. (Interlocutor 7) Private landlords, [. . .], they found a way to circumvent the rent negotiation system. And the scale . . . I mean the number of apartments that is not negotiated, SUT is not really keeping track of that but me as a negotiator. I had masses and especially in Victoriahem [. . .] there is some landlords who have put this system into . . . you know it’s like a system. To me this seems like a major issue [. . .] but I think there is a big dark number. (Interlocutor 3)

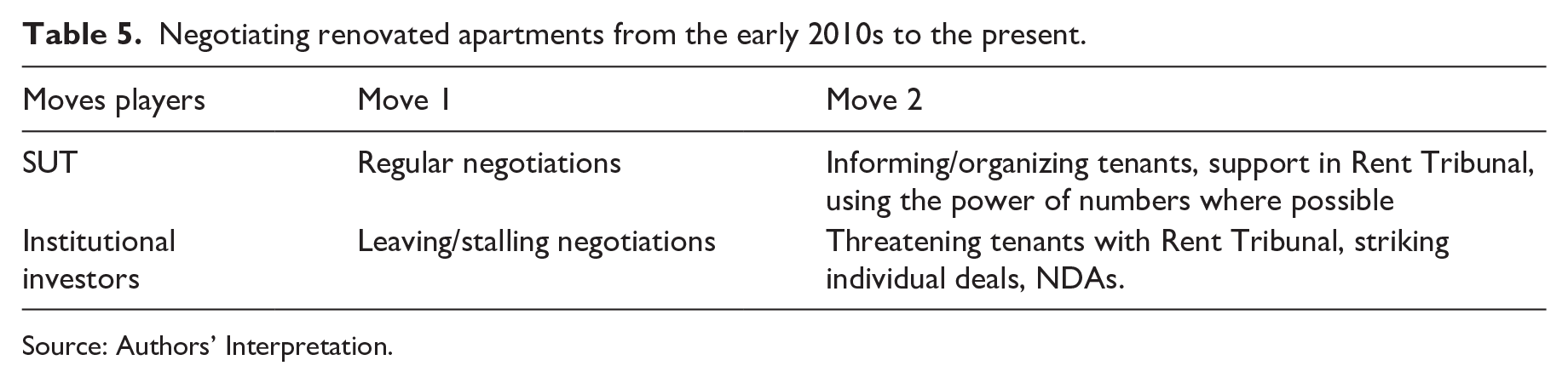

Stranding apartments effectively undermines rent negotiation: when landlords charge the rent they initially demanded to tenants, many tenants start paying, either out of fear and/or a lack of knowledge around their rights (Interlocutor 8). Significantly, many renovations take place in housing stemming from the Million Program era, which is today often inhabited by low-income, racialized populations with an already considerably weaker position on the housing market (Listerborn et al., 2020). If a new rent is approved by the tenant, even for an unnegotiated apartment, that agreed-upon rent is locked in and sets a precedent for the next round of negotiations (see Table 5). The more apartments that fall out of negotiations, the more likely are thus even steeper and more rapid rent increases overall:

The problem is that the company will buy the tenant, who attempts to go to the rent tribunal, out. I will have a tenant who tells me, “I want you to help me with my rent” and I will say “great let’s go to court” [. . .]. What happens then is that [the company] calls up the tenant and says “hi there, we hear you want to go to court. There is 19 months waiting [. . .] and if they go anywhere near what you want, we will also take it to the next instance. So, another year there . . . so [if you drop this] you won’t be seeing another rent increase for the next 2,5 years or we could give you an unrenovated apartment or we see that there is not a washer-dryer combo in your apartment [. . .] or something else you want” . . . or they make a direct agreement on a lower rent but make [the tenant] sign an NDA [non-disclosure agreement]. They’ve done this quite efficiently. (Interlocutor 7)

Negotiating renovated apartments from the early 2010s to the present.

Source: Authors’ Interpretation.

The use of non-disclosure agreements (NDAs) further points to a new quality of aggression within the rent negotiation process. While, once again, these steps are legal—that is, within the rules of the game—given that tenants and companies are allowed to set rents out of the collective agreements, they strain the norms that underlie the process. This is an illustration of how the way institutions (in this case rent negotiations) are interacted with can differ significantly depending on the actors whom the rules concern. This, in turn, forces the actors that embody these institutions and rules to also change the way they play:

We had some success dealing with this, for example we got Victoriahem back to the negotiation table. [We do this by] picking a place where the court case would be good for us, (i.e.) where we had negotiated apartments of the same quality in the vicinity. And basically, they had renovated so many apartments, it was like 200 apartments in that complex. 70 of those were stranded—so we started to massively go out to these tenants, so I had like 30 tenants, realizing that this is the only stock Victoriahem owns around here so there will not be able to offer tenants a cheaper alternative. [. . .] Then, because I was negotiating multiple apartments at once, I did not have to tell Victoriahem which apartments I am negotiating. Then they agreed to re-negotiate. (Interlocutor 7)

This back-and-forth requires additional human and financial resources from SUT’s side, meaning that the more systematically apartments are stranded, the more likely it is also that the organization will not be able to follow up on each case (Interlocutor 3). This means that the resources for the players in the game are increasingly unequal.

Game over? Playing in times of crisis

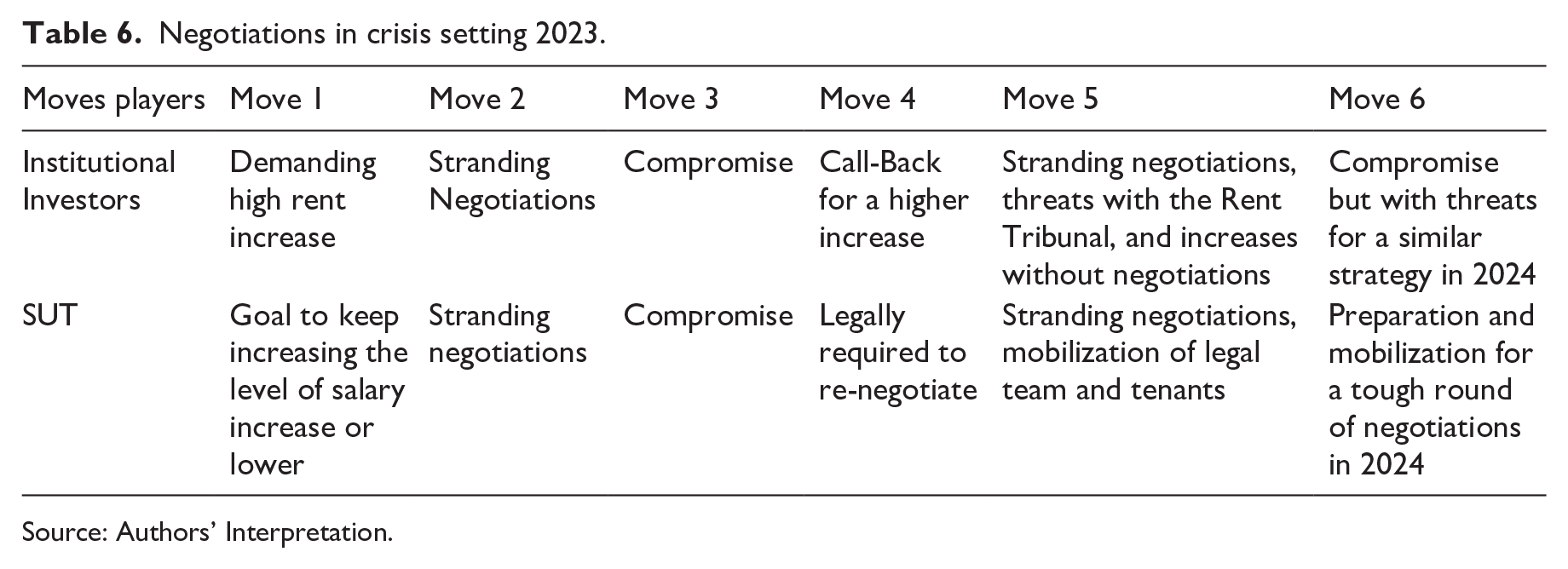

Considering the critique of the use-value system and the increasing frequency of stranded negotiations, Fastighetsägarna, Sveriges Allmänytta, and SUT struck a deal in mid-2022 to introduce a more transparent, national, system for negotiations, including considerations for differences in local costs for items such as electricity and water (Hyregästföreningen, 2022). The agreement, referred to as the tripartite agreement, is a typical example and continuation of Sweden’s self-regulatory rental housing system and can be understood as an attempt to reinforce the rules of a game that seems to be increasingly dysfunctional. This may, once again, be seen as a form of layering in which the old system is not replaced but complemented, one could argue also with the intention to save what is left of it. However, as the first year in which the new agreement was applied showed, rather than providing a foreseeable game plan, the conduct of institutional investors remained rather unpredictable and contributed to what we understand as an escalation of negotiations:

In late 2022 Fastighetsägarna had initially suggested a rent increase of 10% citing increased operating costs and inflation. During negotiations, an exceptionally high number of apartments got stranded across Sweden (Hem & Hyra, 2022). In most cases the dust settled after a couple of months, ending up in a higher-than-average rent increase of 4% throughout the country, which was aligned with the salary increase agreed upon that year by trade unions and employers (4,1%).

The Malmö case, however, stood out for several reasons: first, the agreed-upon increase was already higher than average (5%), which was, following the tripartite agreement, in part legitimized by the high electricity prices in the region. Second, the landlords demanded a second increase after negotiations had been settled. As mentioned in the introduction, this is legal within the first 6 months after negotiations, but is an uncommon and somewhat confrontational move.

Our interlocutors suggested that Heimstaden tried to convince other providers to call back for negotiations to forge a united front but was only partially successful (Interlocutors 6 and 9). At the end, six landlords plunged forward in March 2023, two of which retracted their demand by June. One was the private–public merger Rosengårds Fastigheter to which the local MHC, MKB is a 25 percent party. While an MKB representative we interviewed did not want to confirm their role in the process, SUT representatives noted that it was the public provider that urged Rosengårds Fastigheter to settle (Interlocutor 9). Rosengårds Fastigheter chairperson’s recollection of the process aligns with the view that it was the two large, corporate landlords in Malmö that pushed the process:

We discussed it in the board and two out of four [out of the four owners MKB, Balder, Vonovia and Heimstaden], it was Heimstaden and Victoriahem who suggested it, and then we said ok let’s discuss. [. . .] Then there was no solution [after a first talk with SUT] and we decided [not to go further] because we cannot see a good solution for our tenants. At the same time, [. . .], it’s also important to say that we never did like some companies, also some of our owners, that have the strategy to renovate to increase the rent [. . .]. [Also] I mean our company is so small and we don’t have that much of loans and of course we have said the interest is four times as high, but we are not in the same shoes as many of the big ones. (Interlocutor 10)

The four remaining landlords went ahead and charged tenants with the new, higher rent. SUT sent out letters and went door-to-door urging tenants not to pay (see Table 5); nevertheless, 70–80 percent of tenants started to pay the unnegotiated rent. The landlords subsequently threatened to take non-paying tenants to the Rent Tribunal (Hem & Hyra, 2023c). SUT, on both the local and national levels, interpreted the conduct of institutional investors as more than a one-time disagreement, and saw it as an insult on the system:

There are more and more actors that don’t have the “Swedish way” [i.e., that do not act according to established norms of conduct underlying the Swedish system], so we need to be there like [. . .] guards, to protect our system. (Interlocutor 5)

As Streeck and Thelen (2005: 15) note, “less than perfectly socialized actors,” to which we can count transnational institutional investors, might have little inherent motivation to follow normative rules of conduct for their own sake. These more subtle, incremental changes in the system might, over time, culminate in more tangible shifts—we suggest that it is not a coincidence that the Malmö incident occurred in an already tense political environment: in September 2022 a right-wing coalition, which members had already been vocal supporters of market rents, won the general election. Only 2 weeks later, Heimstaden’s political spokesperson, who is also a member of the party currently leading the conservative government, published a debate piece arguing that it is “time to talk about social housing,” implying an effective abolishment of Sweden’s unitary rental housing system (Persson, 2022). While these debates are still relatively marginal in the wider Swedish context (Interlocutors 9 and 11), they provide an understanding of the political arena in which the providers picked their battle with SUT:

They are testing the boundaries in a good moment in time with a conservative government—they have a chance of pushing the market in this political environment. (Interlocutor 9)

However, the guardians of Swedish rent setting did not remain passive: SUT’s central organization became involved, declaring the providers’ conduct to be “insanely inappropriate” (Bergström in Hem & Hyra, 2023b) and supporting the local organization in setting up a case against the landlords. In August 2023 SUT doubled down by asking providers to compensate all tenants who had already paid, amounting to 63 million SEK (approximately 5.5 million EURO), around 5000 SEK (approximately 430 EURO) per apartment. In mid-October, news broke that the four landlords are backing off and paying tenants would receive compensation (Hem & Hyra, 2023a). However, the settlement came with a simultaneous threat. The companies informed non-paying tenants that they should expect a “substantial” rent adjustment from 1 January 2024 (see Table 6).

Negotiations in crisis setting 2023.

Source: Authors’ Interpretation.

In turn, the local listed housing company Trianon that had been part of the dispute and owns around 3700 units in the city, mostly in Million Program areas, remarked that “the war is over, but there is no peace, possibly a truce” and pondered whether next time the companies could just circumvent the collective bargaining altogether by approaching tenants individually (Hem & Hyra, 2023a). This would mean the de facto establishment of market rents and possibly set a precedent for providers in other municipalities, which would signal the end of Sweden’s corporatist rental system. It remains to be seen whether this will be the case, if so, one could argue that decade-long processes of institutional drift and layering of the Swedish rent-setting system will have eventually culminated in its exhaustion.

Conclusion

Drawing on the framework of incremental institutional change provided by Thelen et al., this article discusses a case of rental housing financialization in an “institutionally rich” (van Gent, 2013: 505) environment—that is, in a housing system that is governed by a complex set of rules that are layered as the result of ongoing struggles, compromise as well as external factors. Specifically, we engaged with the rent negotiation process and the relations between institutional investors and SUT. SUT is still, arguably, the most powerful tenants’ union in the world (Rolf, 2021). However, while the core mandate remains and SUT still negotiates almost all rental housing stock in the country, decades of incremental and radical deregulation have slowly but steadily undermined the organization’s power. This, in turn, has given powerful players, in this case, institutional investors, the chance to “skirmish” (Streeck and Thelen, 2005: 19) around the institutional rules and norms that circumscribe the Swedish rental system. We zoom in on this skirmishing by mobilizing the conceptual metaphor of “gaming”—gaming in this case refers to the tactical moves between the different actors (players) within the Swedish rental housing system. We show that large institutional investors, in our case, chiefly Heimstaden and Vonovia, mobilize their financial and organizational capacities to not only exploit already-existing loopholes in rent regulation (as other landlords do as well) but also to actively strain the system by implementing new moves such as the systematic use of new, selective renovation strategies or aggressive negotiation tactics, including letting tenants sign NDAs and/or circumventing rent negotiations altogether. We suggest that these today possibly less visible shifts in the ways rents are negotiated and set, might over time, provoke more tangible changes within Sweden’s rental housing provision and soft rent regulation system. Our findings thus confirm Blackwell’s (2021) suggestion that the neoliberalization of Sweden’s housing system as well as the current undersupply of affordable housing in the country is both: a result of critical junctures, such as some of the reforms in the 1990s and 2000s, and a culminative effect of more incremental changes that today allow powerful landlords, such as Vonovia and Heimstaden, to further strain the system while remaining within the legal framework.

The Swedish case shows that the process of rental housing financialization cannot solely be understood by examining formal rules and regulations or political decisions but requires a closer reading of how institutional investors interact with existing—old and new—arrangements and actors. Changes in housing systems do not necessarily have to be the result of radical decisions and clearly visible shifts but can accumulate over time, also depending on how rule-takers—in this case, housing providers—behave.

We suggest that analyzing different moves and countermoves can provide a fruitful framework to think about how the interactions between institutional investors and housing systems might affect the future pathway of the system and its institutions. In our case we ponder whether institutional investors’ moves could, eventually, contribute to the legitimization of means-tested social housing in Sweden (with the argument that the system has become dysfunctional and does not guarantee affordable housing) or the de facto, if not de jure, abolishment of the rent-setting system altogether. These accumulative changes are particularly relevant for (post-) welfare contexts (Baeten et al., 2015), where neoliberal reforms are often layered on top of old rules and institutions, existing institutions remain but their roles are converted or certain processes within the system lose their functionality, that is, they drift away. The article, we hope, also opens up a discussion on resistance: as SUT’s countermobilization on both the national and the local level showed, unexpected moves by institutional investors are not necessarily taken passively—institutions that embody the rules and norms of the system may strike back. A close look at these interactions and how they unfold in national and local contexts can thus provide rich insights into how to confront predatory tactics by institutional investors and—possibly—open pathways to other, more tenant-friendly types of incremental or radical change.

Footnotes

Acknowledgements

We would like to thank the two anonymous reviewers for their valuable comments. This article benefited from discussions with numerous colleagues. We especially want to mention Andrej Holm, Eniko Vincze Alicia Smedberg, and Maria Wallstam. Our greatest gratitude goes to the Swedish Union of Tenants.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.