Abstract

In recent decades, institutional investment in rental housing has expanded into a wider range of localities and rental market segments, thereby further pushing the financialization of rental housing. As investment in single-family homes, multi-family apartments, student housing, (former) social housing, co-living, mobile homes, nursing and care homes, Built-to-Rent developments, and short-term rentals is increasing, niche asset classes are being mainstreamed into the capital flows of global real estate markets. However, there is little research that, on one hand, goes beyond ‘mature’ and ‘primary’ institutional markets where rental housing financialization has emerged under rather exceptional conditions (such as mass-privatization of social housing and severe consequences of the Global Financial Crisis), and on the other hand, attempts to gauge institutional investment across the rental market, including across niche asset classes. Through an in-depth case study of the Brussels Capital Region, we examine how and under which market and policy conditions institutional investment flows into an emerging institutional market where investment primarily takes places in niche asset classes. While recent studies have argued that institutional investment in rental housing is limited and, therefore, financialization still a marginal phenomenon, we argue that an in-depth market-wide analysis of institutional investment strategies is necessary for understanding how and to what extent rental housing financialization takes place. Finally, we argue that the patterns of emerging financialization we observe in Brussels may be applicable to other cities as well.

Introduction

European rental markets are under intense and increasing pressure from corporate landlords and institutional investors. In their search for profitable housing products, new markets and investment opportunities, investors are expanding into a wider range of European cities and property types, often encouraged by state policies. This process is boosting rental prices and exacerbating affordability problems in many cities around the world, signalling a new wave of financialization of rental housing (Byrne, 2020; Fields and Uffer, 2016; Holm et al., 2023; Wijburg et al., 2018). Financialization, in general terms, refers to ‘the increasing dominance of financial actors, markets, practices, measurements, and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states, and households’ (Aalbers, 2016: 2). This definition implies that financialization is made up of different processes, located at multiple scales. It means that it is not easy to study financialization in its totality. We here focus on the increasing dominance of institutional investors – as a specific type of financial actors – in the Brussels rental housing market resulting in a structural transformation of that market. Rather than arguing that institutional investors are now dominant in the Brussels market, we focus on their emergence in specific niche asset classes and what this means for the structure of the rental housing market.

Previous studies on rental housing financialization have primarily focused on contexts that play a major role in the global real estate markets, pointing to two ‘special conditions’ that have led to large-scale acquisitions as an institutional investment strategy: on one hand, the run-up and aftermath of the 2007-2009 Global Financial Crisis (GFC) in core crisis-hit countries such as the United States, Spain and Ireland, and on the other, the mass privatization of social housing, primarily in Germany (Aalbers and Holm, 2008; Byrne, 2020; Fields and Uffer, 2016). However, little is known about other contexts which, despite their minor role in the global residential market and the absence of such exceptional conditions, show an institutional rental market ‘in the making’ and an emerging pattern of rental housing financialization.

To address this research gap, we have conducted an in-depth case study of the Brussels Capital Region (BCR). Despite the political status and global position of Brussels as the de-facto ‘capital of Europe’, the ‘special conditions’ do not apply. The effects of the GFC on the Belgian housing market have been limited due to risk-protection policies for homeowners (Winters and Van Den Broeck, 2016) and the relatively less financialized nature of homeownership and mortgage markets (Fikse and Aalbers, 2021), and there has been no large-scale privatization of social housing or nursing and care homes. Against this background, institutional investors have generally paid little attention to the Brussels rental market, in spite of international consultancies promoting the city as a key investment prospect thanks to its rental price increases and large international population (PwC and the Urban Land Institute, 2022).

While recent studies on Brussels have argued that the financialization of rental housing is still a negligible phenomenon (Périlleux, 2023), we observe the emergence and consolidation of new domestic investment funds, as well as first acquisitions by international institutional investors new to the residential market. In addition, established investors have seen significant portfolio growth, and new niche markets have emerged (see Casier, 2023). Although the current inflationary context of rising interest rates is forcing investors and developers to slow-down their activities, a growing group of institutional investors is looking for opportunities to expand their portfolios with properties from Brussels and other Belgian cities. In doing so, their investments target the niches of the private rental sector (PRS) which means that, in line with financialization processes observed elsewhere, key entry points for institutional investors in Brussels are niche asset classes such as student housing, nursing and care homes, co-living, social housing, and multi-family Built-to-Rent (BTR; Aveline-Dubach, 2022; Casier, 2023; Nethercote, 2020; Revington and August, 2020). In this sense, we argue that Brussels is an indicative case of an emerging institutional market and rental housing financialization.

Building on policy and document analysis, and 21 semi-structured expert interviews with investors, asset and property managers, politicians and public officials, and civil society organizations, the aim of our paper is twofold: to understand how processes of rental housing financialization take place in cities outside the mainstream of global residential investment markets; and to analyse how the expansion of institutional investors into a wide spectrum of residential asset classes is taking place. This paper begins by examining the role of niche asset classes in rental housing financialization and defining the market and policy conditions under which financialization is taking place. After discussing our research and data collection methods, we turn to a brief contextualization of our case study, outlining the structural features of the Brussels policy context and its housing system. Next, we analyse the emerging Brussels investor landscape, the key niche markets, and their underlying investment dynamics. In the final section, we outline our contribution to the literature on the financialization of rental housing and open new avenues for future research on institutional investors.

Emerging financialization and niche markets

Institutional investment in niche asset classes

With demand for private rental properties rising (Aalbers et al., 2021; Byrne, 2020), housing has become a profitable asset in investors’ portfolios and a key factor in diversifying business activities and spreading financial risks. Moreover, the range of investors active in housing has increased, and their business strategies have changed over time. Whereas before the GFC the main commercial players were mostly hedge and private equity funds that looked at housing as a short-term investment opportunity and therefore made acquisitions of units for resale (Fields and Uffer, 2016), a shift in investment strategies is noticeable since the GFC. The changing conditions of access to credit and external finance, driven first by the GFC and afterward by the pandemic and the recent energy crisis, triggered an increasing amount of institutional investors to enter urban markets by purchasing existing housing stocks to convert into rental housing, or by acquiring newly constructed buildings to let (Nethercote, 2020; Wijburg et al., 2018). Moreover, institutional investors’ strategies are increasingly geared towards long-term expectations on cash flows and capital gains, and a new focus on real estate services, such as property and asset management.

In this context, institutional investment is expanding into a wider range of niche market segments, which can be distinguished from regular apartments based on the target tenant group, characteristics of the property, location, public policy regime, sector-size compared to the rental market, property management and related services (August, 2022; Casier, 2023; Revington and August, 2020). In the past decades, institutional investment has expanded from single- and multi-family properties to (former) social housing, Purpose-Built Student Accommodation (PBSA), nursing and care homes, mobile homes and recreational vehicle (RV) sites, BTR developments, and temporary accommodations and short-term rentals. In other words, these niche asset classes have been ‘mainstreamed’ into the capital flows of institutional investment (Wijburg et al., 2018) and are increasingly treated as ‘just another asset class’ (Van Loon and Aalbers, 2017).

As such, niche asset classes have come to fulfil six key functions in the geographical and sectoral expansion of institutional investment. First, by targeting housing needs specific to local contexts (e.g. PBSA in college towns and cities) niche asset classes help to open up new, ‘secondary’ localities which ‘may be overlooked by conventional real estate investment’ (Revington and August, 2020: 870). Second, their often-higher yield expectations provide an alternative to less profitable real estate sectors, and thus a convenient possibility for capital switching in times of lower returns in non-residential asset classes (Revington and August, 2020). Third, niche investment functions as a stepping stone to large-scale investment in other market segments, and to launching new housing investment products, as it allows investors to build in-house context-specific knowledge necessary for expansion in unfamiliar markets (Brill and Özogul, 2021). Fourth, niche asset classes open up previously inaccessible segments of rental housing stock, as the characteristics of certain property types might fit the specific demands of niche rental populations and the work of local operators to bundle otherwise dispersed small-scale properties for large-scale institutional investment. This is especially the case for co-living (Casier, 2023) and student housing. Fifth, niche rental products rely on highly specialized property management, which is often undertaken by external operators. This helps to de-risk investments as commercial risks are off-loaded. Sixth, niche forms of housing production, such as BTR (Nethercote, 2020) and PBSA (Revington and August, 2020), create investment products in markets that otherwise lack the high-quality, large-volume properties that institutional investors demand. In this regard, real estate developers, that engage in close collaboration with institutional investors to provide a specialized housing product, play a key role in facilitating the entry of institutional capital into rental markets.

However, while this geographical and sectoral expansion of institutional investment is unfolding, there is little research that, on one hand, goes beyond ‘mature’ and ‘primary’ institutional markets – such as the United States, Canada and Germany – and on the other hand, attempts to gauge institutional investments across the spectrum of residential asset classes in one city. Aside from a few studies with a wider market scope (Aalbers et al., 2023; August, 2020; Fernandez and Aalbers, 2020; Holm et al., 2023; Tulumello and Dagkouli-Kyriakoglou, 2021), most studies of rental housing financialization focus on one asset class in one or two cities. We argue that a market-wide focus on the function of niche asset classes in institutional investment strategies is necessary for understanding how rental housing financialization proceeds outside the mainstream of global residential investment markets, and outside of ‘exceptional’ contexts in which institutional investors have previously thrived. In the following section, therefore, we dive deeper into the conditions under which niche investments emerge.

The creation and state facilitation of niche markets

The emergence of new asset classes depends heavily on the active creation of new markets and housing products by investors and other market actors, including state actors. By bundling large numbers of properties into real estate portfolios, promoting the newly classified product, and enabling financial investment through private or publicly listed funds, investors open up new investment opportunities in previously inaccessible rental segments. Notable examples of this process are the rise of PBSA in Canada (Revington and August, 2020; Revington and Benhocine, 2023), the securitization of single-family rental housing in the United States (Charles, 2020; Fields, 2018), the entry of Real Estate Investment Trusts (REITs) and institutional investors in the market of mobile homes and RV parks in Canada and the United States (August, 2020; Taylor and Aalbers, 2024), and the emergence of co-living in Amsterdam and our case study Brussels (Casier, 2023; Ronald et al., 2023). In addition, more recent accounts of assetization and market formation highlight the crucial function of digital technologies, such as online communication and bidding platforms, in enabling the development of large asset portfolios and smoothening property management (Fields, 2022; Shaw, 2020).

Importantly, market-making efforts work in tandem with various forms of state facilitation of institutional investment into housing. Indeed, international, national and local state interventions in property and financial markets create beneficial investment conditions that help to secure the profitability of the development and promotion of new housing products, and of investments into previously inaccessible market segments (Aalbers et al., 2023; Gabor and Kohl, 2022). On one hand, states have ‘shaped the conditions’ for the ‘massive transfer of ownership’ of formerly decommodified housing stock to private landlords by withdrawing from social service provision and reregulation of rental markets, particularly in the case of social housing and nursing and care homes (Aalbers et al., 2023: 18; see also Aalbers and Holm, 2008; August, 2022). On the other hand, states facilitate institutional investment more directly by installing beneficial tax regimes (such as REITs) and financial-legislative frameworks that promote public-private partnerships (Belotti and Arbaci, 2021; Gotham, 2006). In particular, REITs enable large-scale global institutional investment streams into housing as they provide stable rental income flows, thanks to easy access to growth capital through stock exchanges, and dividend pay-outs under high fiscal discounts. Other direct forms of state facilitation, such as rental subsidies, guarantees on social security payments, and the underwriting of student loans further secure the stability of such income flows (Aalbers et al., 2023).

Data and methods

The overall aim of our paper is twofold: to understand how processes of rental housing financialization take place in cities outside the mainstream of global residential investment markets; and to analyse how the expansion of institutional investors into a wide spectrum of residential asset classes is taking place. In contrast to the existing literature that has a ‘dominant temporal focus on pre- and immediate post financial crisis’ (Nethercote, 2020: 851), our work focuses on the period from 2016 to today, when new institutional actors entered the Brussels rental investment market specifically before, during and right after the pandemic. This development is driven by the beneficial low-interest financial climate up until the Russian invasion of Ukraine, and by the uneven impact of the pandemic on non-residential asset classes such as offices and retail, triggering investors to turn to other ‘alternative’ property types such as housing. Based on a qualitative research design, our in-depth case study of Brussels, conducted from January 2023 to May 2024, sheds light on the structural housing market features and political-economic conditions that shape the entry of institutional investors into urban rental markets. It also provides further evidence on the function of niche asset classes in the expansion of institutional investors into new rental markets.

Our data include both primary and secondary sources. For our analysis of the investor landscape and institutional investment strategies, we examined local real estate consultancy studies, recent annual financial reports of all Belgian residential REITs, press releases, and business news reports on the activities of investors and developers in the Brussels rental market. In addition, we attended two real estate and finance conferences in Brussels in September and November 2023: Realty, which annually brings together real estate operators and policymakers to present and discuss development and investment opportunities in Belgium and Brussels; and Finance Avenue, an event organized by two specialist Belgian newspaper, L’Echo and L’Investisseur, at which financial, real estate professionals and experts present and promote investment opportunities to private investors.

To identify the key investors, we first used the 2023 Investors Directory by Expertise, an important news outlet and reference for real estate professionals in Belgium. The Directory, which presents the results of a survey of 255 real estate investors active in Belgium, allowed us to identify the top 10 largest investors and market leaders for each niche segment. As the report does not include investors with a portfolio value less than 181 million Euros, we then carried out a thorough search of business and regular media, including all the major Belgian business newspapers. This resulted in a selection of newly established domestic funds, international fund and asset managers, investor-developers, and institutional investors. Finally, we verified the data gathered through document analysis and desk research during our interviews with investors.

The portfolio data presented in Tables 1 and 2 are based on annual financial reports, unless stated otherwise. The data in Table 3 on size and type of capital and investment were collected from company websites and press releases, business news publications, and interviews with company managers. Where information on the purchase/ownership of a building, the location or the number of units per building was not explicitly mentioned on the companies’ websites, evidence was collected either by matching pictures on company websites with Google Street View images or property management websites, and by examining LinkedIn posts on new purchases. In other cases, missing information was gathered through site visits.

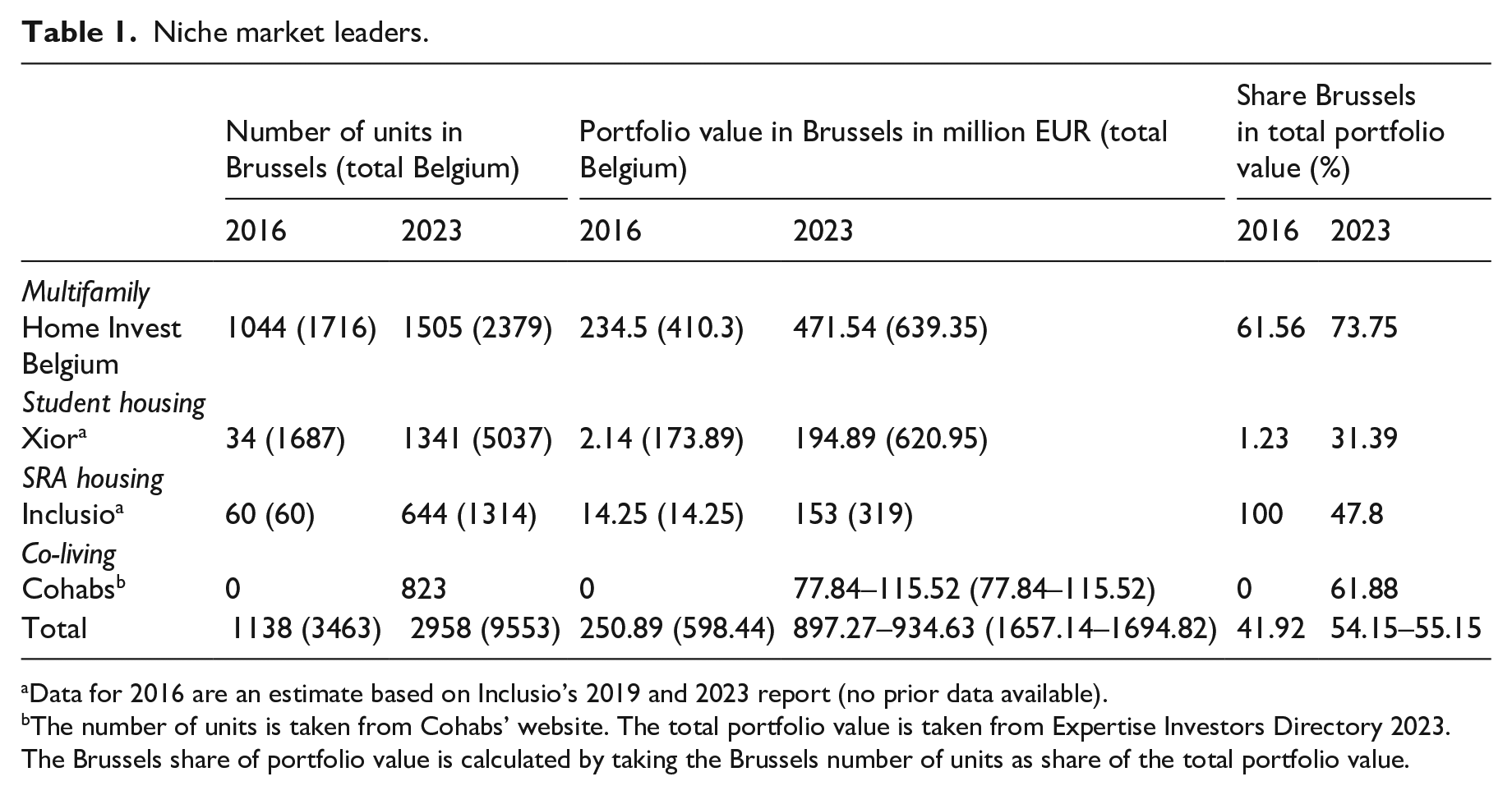

Niche market leaders.

Data for 2016 are an estimate based on Inclusio’s 2019 and 2023 report (no prior data available).

The number of units is taken from Cohabs’ website. The total portfolio value is taken from Expertise Investors Directory 2023. The Brussels share of portfolio value is calculated by taking the Brussels number of units as share of the total portfolio value.

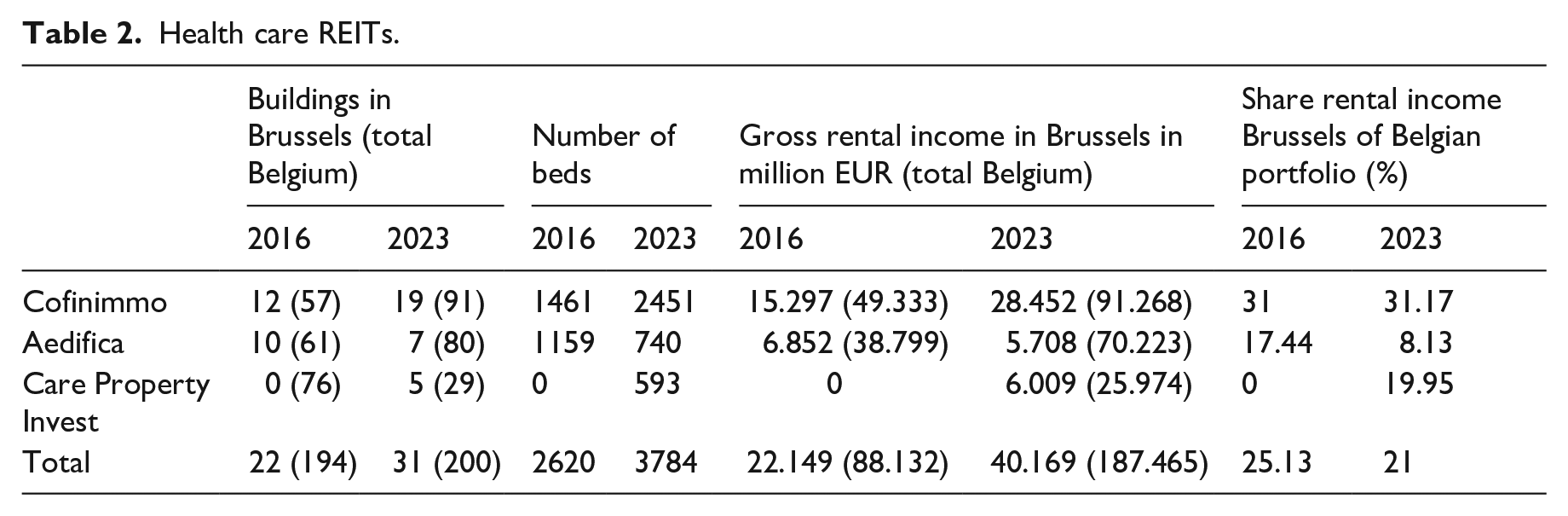

Health care REITs.

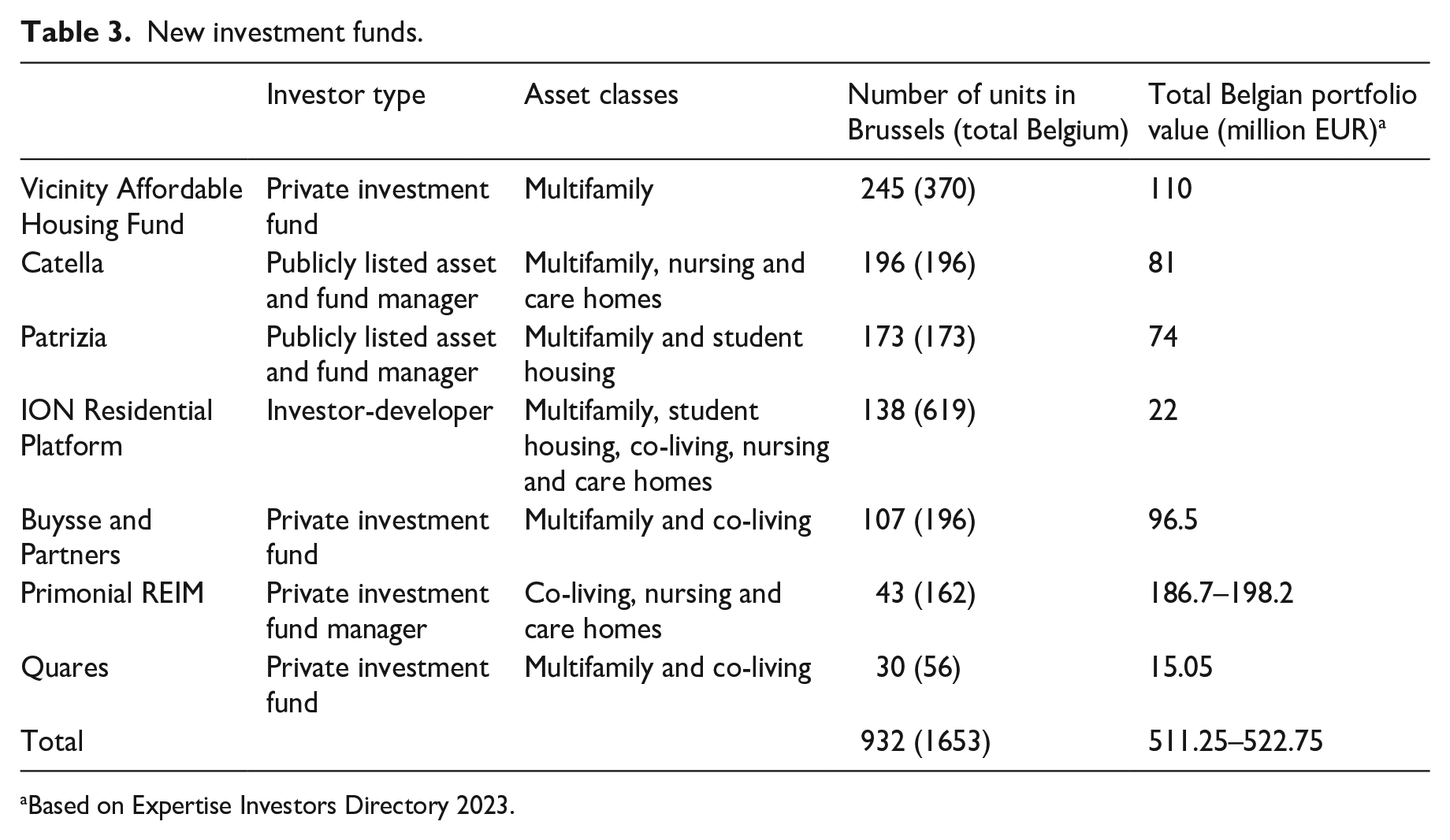

New investment funds.

Based on Expertise Investors Directory 2023.

We are aware that this data collection method may lead to biases. First, our selection of investors based on media publications runs the risk of highlighting actors that seek media attention, while missing investors that are usually less keen to attract media coverage, such as banks, insurers and pension funds. Second, for data on portfolio size, we had to rely on what investors have publicly shared, which could mean that the data are incomplete or not up to date. However, considering that the oldest purchase included in the data set was made in 2020, and the investors in question all pursue a long-term oriented buy-and-hold strategy, we believe it is unlikely that many properties have been sold in the meantime. More recent purchases, however, could have been overlooked as these have not been made public yet. All portfolio data (except for the portfolio value in Table 3) were last updated in May 2024.

Throughout 2023, we conducted 21 semi-structured interviews with investors, developers, consultants, asset and property managers, lobby organizations, policymakers and civil servants. Our interview guide included general questions about the Brussels rental housing market and real estate industry, as well as specific questions tailored to the profile and expertise of the interviewees. The selection of interviewees was based on the document and policy analysis carried out in the earlier phase of the fieldwork as well as a review of previous academic, journalistic and civil society research on investors and developers in Belgium. Occasionally, new contacts were made through snowballing, especially with market actors.

Housing policy conditions and the PRS in Brussels

Housing and policy conditions

Like many other capital cities in Europe, Brussels is a city of renters in a nation of homeowners. Over the course of a century, the promotion of homeownership based on fiscal support for first-time buyers and other non-fiscal policy support measures has gradually transformed Belgium to a majority homeowner society, counting 66 per cent owner-occupancy, 23.5 per cent private rental, and 8.9 per cent social housing (Housing Europe, 2023). 1 However, homeownership rates are much lower in Belgian cities and Brussels is emblematic in this regard. While 51 per cent of the total stock consists of private rental housing, around 40 per cent are owner-occupied dwellings. The remainder, about 9 per cent, could be considered social rental housing, which includes public housing, owned by the Brussels Regional Housing Company, and privately owned rental housing, let out by social rental agencies (SRAs) at below-market prices thanks to major federal and regional subsidies and fiscal benefits (Franklin et al., 2022; Kahane et al., 2019). 2 This tenure composition has been rather stable for the past 12 years (Heylen, 2023), as entry to homeownership has stalled for first-time buyers who are increasingly unable to qualify for mortgage loans and for lower-income groups who have been priced out in the past 20 years (Warisse, 2022), but has slightly increased for groups for which the homeownership rate was already relatively high. At the same time, there is no sign of significant private rental growth as is seen in other European homeowner countries (Aalbers et al., 2021; Lennartz et al., 2016), and social housing production is desperately lagging behind the huge demand for affordable alternatives (Bauwelinckx et al., 2017).

In this context, Brussels is facing a severe housing crisis characterized by mounting affordability issues across tenure forms (De Keersmaecker, 2018; Kahane et al., 2019). Since the late 1990s median apartment prices have increased – by more than 30 per cent in the past 10 years – while the average disposable income of Brussels residents hardly increased (Bisa, 2023; Statbel, 2021). Similarly, private rental prices have increased by 20 per cent over inflation-based rental indexation between 2004 and 2018 (De Keersmaecker, 2018). Currently, affordability issues have exacerbated to the point that people are pushed into poor quality housing that does not meet their needs (Dessouroux et al., 2016), and working class and middle-income households are increasingly leaving the city in search for more affordable housing elsewhere in Belgium (De Laet, 2018; Surkyn et al., 2020).

The Brussels private rental sector

The Brussels PRS primarily accommodates low-income households unable to afford homeownership and without access to the small and insufficient social housing sector, but also a significant group of high-skilled migrants attracted by the international political functions of the city (Casier, 2023; Dessouroux et al., 2016). The flexibility, high turnover, and higher incomes of the latter group have attracted the attention of institutional investors. Yet, 54.8 per cent of private rented housing in Brussels is owned by private landlords that hold between one and five units, whereas corporate landlords hold only 13.4 per cent of the PRS stock. Large corporate landlords owning more than 50 units amount to only 1.2 per cent of the PRS stock (Périlleux, 2023). However, these numbers date from 2015 and – as we demonstrate – there is reason to believe that the share of corporate ownership has increased, large portfolios (>50 units) are becoming more common, and the largest portfolios have grown significantly.

This small share of corporate PRS ownership has several reasons. First, the long-standing ideal of homeownership and the persistent policy support for first-time buyers and property owners have boosted individual homeownership and manifested private renting as the culturally less desirable, and fiscally less attractive tenure form, thereby steering demand away from private rental housing (Fikse and Aalbers, 2021; Romainville, 2010). Second, fiscal support for secondary property ownership has spurred high-earning households to invest in Buy-to-Let (BTL) instead of other assets, in order to compensate for low pension incomes, or simply as a strategy for wealth accumulation (De Decker and Dewilde, 2010; Wind et al., 2020). To illustrate, in Brussels 76 per cent of second property investments are estimated to be BTL, of which apartment acquisitions make up almost half (BNP Paribas Fortis, 2022). Finally, the Brussels rental housing stock primarily consists of older, 19th- and 20th-century houses and apartment blocks, while housing production has focused on individual ownership and Built-to-Sell (BTS) developments (Dessouroux et al., 2016), as the higher profit margins on individual sales trigger developers to produce for the private market. This has left few opportunities for institutional investors to enter the market through large-scale portfolio acquisitions. In short, institutional investors are faced with a market and housing system that has not been in line with their demands.

Furthermore, the Brussels private rental market is characterized by a liberal regulatory framework with weak tenant protection in terms of tenancy security, price regulation and conflict resolution (De Decker, 2001; Godart et al., 2023; Van Criekingen, 2008). As one of the three Belgian regions, Brussels is made up of 19 municipalities and one regional government. Key housing competences such as rental law and regulation, and social housing allocation policy are strictly regional competences, but several fiscal and subsidy measures, such as rental income tax, some building subsidies, property taxes, Value Added Tax (VAT), and REIT regimes are set at federal level. Municipalities are forced to follow regional housing legislation, but do issue local zoning plans and are responsible for delivering building permits and charging planning gains, despite planning authority being more regionalized (Conte, 2021). In sum, the fragmented governance structure distributing housing competences over three layers of government limits the power of the state to intervene in the PRS. As a result, policy responses to institutional investors have so far been piecemeal and incoherent, also as support for homeownership continues to be prioritized.

The changing Brussels investor landscape

Key niche asset classes

In order to understand the current expansion of the institutional investor landscape we focus on corporate residential investors that make direct investments in different types of rental housing. This results in a range of investors that share similar investment objects, but differ in terms of their spatial scale of operation, social composition, and financing (Özogul and Tasan-Kok, 2020). Overall, the key corporate residential investors we identified are REITs, domestic investment funds (backed by institutional capital or wealthy families and high net-worth individuals), international asset and fund managers, investor-developers (partly sourcing form their own pipeline) and, finally, domestic banks, insurers and pension funds operating their own investment funds.

These different types of investors target the niche asset classes of student housing, co-living, BTR, SRA housing, and nursing and care homes. Each of these PRS subsegments functions differently and investors follow different business models accordingly. For student housing, investment takes place in PBSA as well as renovation or conversion of existing building stock into student housing. The student housing market is popular with individual BTL investors, but several sources do note the increasing professionalization – or perhaps institutionalization – of student housing landlords, and the increasing activity of private developers on the market (Albea et al., 2020; Sansen and Van den Broeck, 2024). The rapid growth of Xior, a REIT specialized in student housing and the biggest student housing landlord of Belgium and Brussels, is clear evidence of this trend (see Table 1).

In the Brussels co-living market, both BTL and institutional investors are active, investing primarily in 19th- and 20th-century single-family houses converted to co-living units, but increasingly in new-build co-living projects as well. Investment strongly relies on collaboration with local operators which manage co-living properties, and in some cases also own large portfolios themselves. A case in point is the Belgian operator and landlord Cohabs, which has acquired several hundreds of properties in Brussels with the help of domestic private equity and international institutional investments. The co-living sector has boomed in the past 9 years, developing from virtually non-existent in 2015 to close to 3000 units today (Casier, 2023). The absence of a coherent, region-wide response to co-living investment has only facilitated this rapid expansion, as the unclear regulatory status of co-living has allowed investors to convert single-family housing to dense co-living properties without permit and make use of flexible tenancies.

Multi-family BTR has been part of the Brussels investment market for decades, evidenced by the long-standing presence of Home Invest Belgium, the largest Belgian residential REIT, holding the largest multi-family portfolio in Brussels (see Table 1). However, this segment of the market is small and it only started expanding and professionalizing recently. Major players are financialized developers who are responsible for nearly half of the Brussels housing production (Romainville, 2017), which increasingly collaborate with institutional investors looking for ‘investment product’. Federal fiscal policy took a turn towards promoting BTR in June 2024, when the Federal Minister of Finance reformed a long-standing VAT discount for redevelopments and gave institutional investors access to the discounted tariff, a measure strongly advocated for by many of the investors discussed here (Quares Residential Investment, 2023).

The SRA, and nursing and care homes markets are outliers, as they are heavily regulated and business models largely rely on state subsidies. The SRA sector was originally founded to ‘socialize’ the PRS, but has in the past 8 years or so also become an investment market for BTL and institutional investors. SRAs mediate between tenant and landlord, offering tenants temporary leases for below-market prices and with social support, enabled by state subsidies and housing allowances. In return for accepting lower returns, landlords receive fiscal benefits such as VAT discounts and tax exemptions, complete rental income guarantee, and discharge of nearly all property management responsibilities. Especially the emergence of new-build SRA housing (Adler, 2020) has spurred the creation of SRA investment products for BTL investors and has attracted corporate landlords, among which the REIT Inclusio, which since its establishment in 2011 has become the largest Belgian and Brussels SRA landlord (see Table 1).

In the case of nursing and care homes, supply is capped as the number of care beds is limited by regional permitting. The management of care beds is divided between public, not-for-profit and private operators, with private and not-for-profit actors taking up 76 per cent of the number of beds (Infor-Homes, 2023). The business model of institutional investors relies on close collaboration with private and not-for-profit operators, 3 which take on long-term leases (20, 25, 27 years), including the responsibility for paying taxes, insurance and maintenance costs, and operational management of the facility (also known as triple net contracts). This way many investment risks are offloaded on the operators and a stable, long-term rental income for landlords is secured. Furthermore, private profits of nursing and care home landlords are massively subsidized as a large part of the income of operators depends on social security payments, and the Belgian REIT regime provides major tax benefits for health care property (Centre for International Corporate Tax Accountability and Research (CICTAR), 2023). Currently, the Brussels market is strongly consolidated, and expansion mostly relies on acquisitions of existing properties.

Niche investments and portfolio expansion in an ‘immature’ market

In the past two decades, the Belgian institutional housing investor landscape has been dominated by a handful of REITs investing in multi-family, nursing and care homes, student housing, and SRA housing. Given their long track record in Belgium, these REITs hold a leading position in their market segments and are the largest players in the country’s residential market in terms of number of units and portfolio value (Expertise, 2022). However, with residential investment almost doubling since 2018 (Expertise, 2022), several new domestic investment funds and large international asset and fund managers have entered the market (see Table 3), often with a national coverage yet a clear inclination towards Brussels because of its international character, large tenant base, and high property and rental prices. All have made one or more acquisitions, and in some cases have capital raised to invest more. In general, their target is regular multi-family rental housing. As one investor describes it, their focus is on ‘the mass of the rental market . . . so basically the unregulated segment of the market, anything between social and luxury housing’, with a clear preference for ESG-compliant (i.e. ‘Environmental, Social, and Governance’) high-quality properties. Because of the lack of such properties in Brussels, this quickly pushes investors to BTR or extensively renovated or converted properties. At the same time, several funds are diversifying their investment strategies, acquiring nursing and care homes or including externally operated co-living in their BTR projects. Several funds have student and SRA housing on their radar but have not made such acquisitions (yet), primarily because large established players represent a ‘barrier for market entry’ in the case of student housing (e.g. Xior), or due to lower profits in the case of SRA housing. As one investor summarized: ‘the yield is not there . . . and it won’t be there with the current system [of state subsidies]’ (Interview with investment manager).

Despite different focal points in the investment strategies of the interviewed investors, three trends stand out. First, all institutional investors have long-term expansion strategies. Although there is no evidence of PRS growth since 2011 (Heylen, 2023), they all expect the current demand for private rental housing to increase in the future, both in Brussels and other Belgian cities, an outlook based on the growing unaffordability of homeownership for young households, the rise in small households, the ageing Belgian population, a growing student population, and the unmet demand for social housing. Therefore, their investments should be seen as an attempt to push PRS growth and position themselves in advance of that presumed structural housing system change.

Second, all investors perceive Brussels as an ‘immature’ institutional market compared to other European cities, characterized by low liquidity, scarce supply of investment properties, poor transparency in terms of pricing, low rental and property prices, and the absence of property managers that can meet the demands of institutional investors. At the same time, the ‘immaturity’ of the market explains the strategic appeal of Brussels for new funds and international players. Making an early entrance in an ‘immature’ market with low rental and property prices and limited competition is key to obtain long-term gains on rental and property price increases. As one institutional investor explained:

If the market is less institutionalized, and there are less parties active and less capital has flowed in, but we do believe that the fundamentals are right and institutionalization will proceed, then we think we’ll reap the benefits of having investments there.

This also explains several investors’ rent-gap seeking strategy of focusing on lower-priced yet gentrifying neighbourhoods. As different interviewees noted, their preference goes out to ‘growth neighbourhoods [with] rental upside over ten years’ which allows for a strategy based on ‘yield on the potential rent’. In short, we see a clear pattern of long-term, low-risk investment strategies aiming to optimize the financial gains of stable rental income. Investor-developers that hold BTR developments for a shorter period of time slightly deviate from this long-term approach. They often source their investment funds with their own developments, and hold these either for a period of 5–10 years before selling, or in some cases do hold these for the longer term.

Third, for most asset classes one clear market leader in terms of portfolio size and value dominates the market (see Table 1). For all asset classes this position is held by REITs, except for co-living where the Belgian private firm Cohabs (backed by several institutional investors, among which AG Real Estate, a subsidiary of AG Insurance) leads the charts. For nursing and care homes, three REITs, Aedifica, Cofinimmo and Care Property Invest, dominate this segment (Expertise, 2022), as together they own 33.17 per cent of private and not-for-profit beds in Brussels (Table 2).

In multi-family, the REIT Home Invest Belgium has, over the past 24 years, built-up the largest residential portfolio in Belgium and Brussels, making it not only market leader, but also the largest corporate landlord in Brussels. Two other REITs, Xior and Inclusio, are, respectively, the largest investors in student housing and SRA housing. Looking at the size of these market leaders in comparison to other more financialized rental markets such as Germany, the United States or the Netherlands, it becomes clear that despite their leading position, their share of the Brussels PRS is small. However, in the past 5 years, Home Invest Belgium expanded its portfolio by almost 50 per cent, Inclusio grew more than tenfold, and Xior grew from close to zero to 1341 units (Table 1). The consolidated and highly regulated nature of the nursing and care home market and the recent scandals with operators explain the more moderate growth of health care REITs. Finally, Cohabs was founded only in 2016 and in the subsequent years grew out to become market leader with 823 co-living units and a portfolio value estimated between 125 and 186 million Euros (Expertise, 2022). The rapid growth of several of these companies in the past 7 years demonstrates that, despite their relatively small portfolios, niche market investments are increasing, and institutional investors are bolstering their position in the PRS.

Pushing for institutionalization

Although more domestic and international institutional investors have entered the market in recent years, and established REITs have expanded their portfolios, the institutional market remains small and could still be considered emerging. However, evidence shows that the institutional investors already active in Brussels push the market towards a more ‘mature’, institutionalized and professionalized state, which is crucial for explaining the emergence of financialization in Brussels and elsewhere.

This push for institutionalization can be illustrated by the following two trends identified in the housing financialization literature. First, we observe a gradual shift from BTS to BTR developments, which is pushed for by institutional investors and developers collectively. In Brussels, this new interest in BTR represents a clear break with the past, when developers were mainly focused on individual sales. As stated on the website of Immobel (2021), one of the major Belgian developers, this new emphasis on BTR marks ‘a response to the increased institutionalisation of the market’ and ‘the transformation from a private rental market to a rental market dominated by professional stakeholders’. Developers and institutional investors regularly justify this shift in two ways. On one hand, they refer to the quality and sustainability of their apartments, thereby suggesting they contribute to resolving the lack of decent and adequate housing in the city. On the other hand, this shift to BTR allows them to minimize their risk by securing their margins in a single deal. As one of the largest Belgian developers noted: ‘We would like the worst-case scenario to be that we sell to the private market, after we have tried selling to an investor’. To this end, developers have started collaborating with institutional investors from the start of a project to meet their needs:

The idea is always to try and sit down as early as possible with one or two investors, if you want to try and find a deal together, and conceptualize the project, because it has an impact on your planning. (Interview with developer)

We also observed that some developers that have traditionally been active in the office market have gradually diversified their activity, including the development of residential complexes and the conversion of office space into BTR and mixed-use developments. Given the oversupply of office buildings in Brussels (Dessouroux, 2010), conversion is topical. It has returned to the political agenda during and after the pandemic due to teleworking, as it is seen as a good solution to deal with the high vacancy rate of the office stock and to address the housing shortage (perspective.brussels, 2022; Raynaud et al., 2024). At Realty, for example, the regional planning agency held a session on the subject, presenting experiences, opportunities, and challenges related to regulation and building permits. The diversification of developers’ activity and the political emphasis on office conversion have created the conditions for new block acquisitions in Brussels. Key examples are the purchase by Quares in 2021 of a student housing block currently being developed by Immobel and BPI Real Estate as part of a highly controversial mixed-use project in the centre of Brussels (Benzaouia and Charlier, 2023), and the acquisition by ION of a rental apartment and co-living block from Eaglestone in 2023 (ION, 2023).

Second, the institutionalization of the rental market, as illustrated in BTR, drives its professionalization. As one consultant put it, the relationship between market institutionalization and professionalization ‘is a bit like the chicken and the egg, because once there will be these investments you will also see property managers’. Large property acquisitions require specialized services such as property management, which is now a key dimension to make asset classes ‘investible’ and profitable in the long-term. In addition to long-term leases, which provide a steady income for institutional landlords, professional operators offer a wide range of services, from tenant screening to day-to-day building maintenance, from rent collection to property marketing, from tax payment to ESG-compliance reporting. The lack of property management attuned to institutional demands, as mentioned by nearly all our interviewees, is a case in point. Interviewees perceive Belgium to lag behind other countries where these professional services have grown significantly over the last decades:

We have a few good property managers in Belgium, local ones. [. . .] The issue with the local managers is that they do a good job with the boots on the ground, I have no doubt about that. The problem is that we need a lot of extensive reporting on ESG and financial information. And most of the Belgian managers are not used to doing this reporting and simply do not have the capacity to do this. (Interview with asset manager)

In Brussels we observe two exceptions in which external property management is more developed: co-living, and nursing and care homes. The two markets have been boosted by the presence of operators with a strong tradition outside Belgium: Orpea, Korian and Armonea in senior living; and Cohabs, Colonies and Habyt in co-living. The presence of these operators can potentially facilitate low-risk entry of REITs into new niche segments. The largest multi-family REIT in Brussels, for example, bought a co-living block in the centre of Brussels because: ‘You have a higher net yield, [. . .] because a lot of the risks are taken by the operator. But it was an opportunity for us to test it’ (Interview with investment manager).

As a consequence, players either internalize property management (Home Invest, Xior and some domestic investment funds) or outsource to the few professional property managers in the market (Patrizia and Catella). Institutional investors and investor-developers that are well-embedded in the local context have a competitive advantage, as they have long-standing experience in the Belgian and Brussels market and have developed in-house property management departments. Market operators and consultants miss no opportunity to emphasize the need to professionalize the market, not only during interviews but also during public events, such as real estate meetings and conventions. Of course, professionalization not only feeds the institutionalization but also the financialization of the market.

While these trends persist, the recent rise in interest rates and construction and energy costs (European Construction Industry Federation (FIEC), 2024) has slowed down development and institutional investment activities, in particular during and in the aftermath of the pandemic. Under the current costs of borrowing, banks are more selective:

Now, for the first time in 30 years [. . .] free money is not available anymore. If you want to sell something, the buyer wants a higher yield, because it costs more to finance, so it means that the price will go down a bit. (Interview with property manager)

In general, the rise in interest rates and construction costs has direct consequences for the investment possibilities of investors, who are strongly dependent on the expansion of the BTR offer for their market entry: ‘We have gone up 32 percent in construction costs [. . .] which means it’s pushing up prices, which means it will be more difficult to build, which means there will be less on offer’ (Interview with developer). Several smaller funds that primarily invest with private capital from wealthy individuals and families note that they can still make acquisitions, but the larger institutional investors have adopted a ‘wait and see’ approach. Altogether, this leads to the current situation in which institutional investors and developers are trying to push the emerging BTR market to a more established position, yet are constrained by the financial and economic conditions that limit the sector’s growth potential.

Conclusion

Brussels is not a case of massive institutional investment in its housing market, but it is a case of increasing investment in niche asset classes such as student housing, nursing and care homes, co-living, and SRA housing. We argue that this pattern of rental investment may be more typical of rental housing market financialization in Europe and elsewhere than more widely documented cases of mass-privatization and post-crisis financialization of housing. In other words, emerging financialization takes place in niche asset classes rather than in mainstream rental housing. This means that overall, institutional investment volumes in the PRS are increasing yet remain small. Only a small segment of the PRS is more financialized, but these niches are progressively financializing and can be the launching grounds for a further financialization of the housing market, as they contribute to developing a more ‘mature’ housing investment market.

We hypothesize that the following patterns of emerging rental housing financialization we observe in Brussels may be present in other cities as well (see section ‘Emerging financialization and niche markets’ as well as other papers in this Special Issue). First, the characteristics that make the Brussels rental market not well attuned to the demands of institutional investors also apply to other cities where developers have traditionally developed for homebuyers and BTL investors, and the existing stock is often of poor quality and heavily fragmented in terms of ownership. Second, the ‘immature’ market from the standpoint of institutional capital is both a barrier for investment and an opportunity to be exploited by select market players. Third, niche markets provide investors and developers with chances for growth in an otherwise limited market. New players that initially have a small market share can become market leaders in their specific niche segments in just a few years. Fourth, the arrival of institutional investors goes hand in hand with a push for professionalization of the market in order to lay the groundworks for further expansion of investment. Professional service providers, such as property managers and operators, play a key role in this process and prepare the market for its assetization and financialization. Fifth, the expectation by market players that the PRS will grow in the face of unaffordable homeownership and inaccessible social housing drives institutional investment and the emergence of new markets. Investors and investor-developers are jointly pushing the BTR market, for example, to create more large-volume and often higher-priced investment properties, and this asset class is becoming a key entry point for institutional investors into the PRS.

The question is if (some of) these patterns are visible in other cities – European and non-European – as well. Future studies would need to scrutinize if the financialization of niche asset classes is indeed a first step towards a larger and more widespread financialization of the rental housing market – in Brussels but also elsewhere. Although Brussels is not an ‘ordinary city’ (Amin & Graham, 1997; Robinson, 2002), it could be argued that the patterns of emerging financialization observed in Brussels, but also in many of the other cities discussed in this Special Issue, are a form of ‘ordinary housing financialization’ in European cities. Urban studies should not just focus on ordinary cities but also on the ordinary, or common, form of processes often studied in more extraordinary, or exceptional, circumstances. Yet, whereas studies on niche markets in other cities are often seen as different from well-published housing financialization cases, we hypothesize that the emerging financialization of niche rental assets is the more common, more ordinary, form of housing financialization in a wide range of cities in Europe and beyond.

The local and regional state response to emerging housing financialization in Brussels and Belgium has been piecemeal, incoherent and typically not targeted at the business models of institutional investors. To date, there have been no policy initiatives that explicitly recognize the possible impact of increased institutional residential investment on the affordability and accessibility of Brussels’ rental housing. On one hand, residential investments are de-risked particularly by fiscally beneficial REIT regimes for residential and senior living and heavy subsidies for SRA housing. On the other hand, there are no regional housing policies or planning instruments that are explicitly aimed at and designed in response to the strategies and business models of institutional investors, despite the urgent need to close regulatory gaps which have enabled the rise of new financial products (for example, in the case of co-living). Therefore, we also call for more studies that analyse policy responses to housing financialization, to understand if the (lack of a) Brussels’ policy response is also typical for emerging rental housing financialization, or if this is typical for the case of ‘fragmented Brussels’ (see Terhorst and Van de Ven, 1997).

Indeed, while the continuing penetration of finance into urban rental markets is a global phenomenon, the empirical literature shows this to be a highly context-specific process (Aalbers, 2017; Holm et al., 2023) that involves the active creation of new asset classes and the exploitation of local housing conditions, policy regimes and crisis situations (Aalbers, 2017; Beswick et al., 2016; Casier, 2023; Fields, 2018; Revington and Benhocine, 2023). How investors enter urban rental markets, through what type of investment, in which kind of properties, in which cities, and with what type of strategies, will depend on the political, policy, market, and housing conditions on the ground. In particular, housing-related path dependencies, local traditions in rental housing provision, and fiscal, housing and planning policies at the international, national and local level strongly impact on the possibilities for institutional investors to enter specific markets (Gabor and Kohl, 2022; Holm et al., 2023). Our findings, therefore, call for a shift in the empirical focus of rental housing financialization literature away from high-profile cases and major capital cities, towards cases of more common, perhaps even ordinary, housing financialization in both European and non-European cities.

Footnotes

Author’s Note

Veronica Conte is also affiliated to Research Foundation Flanders – FWO, Belgium.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding and acknowledgements

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research builds on the project ‘Housing policy under the conditions of financialization. The impact of institutional investors of affordable housing in European cities (HoPoFin)’ funded by the SciencesPo Cities, Housing and Real Estate Chair. We would like to thank all the other participants of this project, the participants of the workshop in preparation of this Special Issue, the members of the Real Estate/Financial Complex (REFCOM) research group in Leuven, and the editors and reviewers of this journal for their valuable feedback and input. In addition, the authors would like to acknowledge the financial support of the KU Leuven/CELSA Research Fund (grant no. CELSA/22/0011) and the Research Foundation Flanders–FWO (grant no. 3E210601).