Abstract

This article examines the links between financialization, rent increases and spatial inequality in Toronto, Canada. By drawing on qualitative data from the grey literature, corporate records and real estate events, we first find that financial landlords (REITs, REOCs, asset managers, private equity and institutions) attest to rent price increases as a strategy core to their financial structure, leading to a systematic undermining of affordability. Drawing on a Toronto-wide database of property rent levels, we then quantitatively demonstrate that financial firms charge higher rents, charge higher premiums to neighbourhood average rents and post the highest same-property quarterly rent increases, compared to other types of landlords. We analyzed the geography of financialization and rent, finding that financial firms charge the highest premiums to average rents in lower-income and racially marginalized ‘Neighbourhood Improvement Area’, (NIAs), capitalizing on the higher rent gap potential in devalued areas with lower rent levels. We conclude by stressing the importance of reining in on financial landlords, especially as they have become the largest acquirers of suites in Toronto in the past two decades.

Introduction

In Canada financialization has become a major trend in the rental housing landscape. In all kinds of rental housing – apartments, seniors housing, student housing – financial firms (i.e. firms that make housing open to investors, including private equity, institutions, publicly-listed firms, asset managers and Real Estate Investment Trusts [REITs]) have rapidly consolidated direct ownership of housing stock (August, 2020; August, 2021; Revington and August, 2020). Alongside financialization, Canada’s long-running housing affordability crisis has worsened in recent years, with house prices and rents diverging from people’s incomes (Stokes, 2021). In 93% of Canadian neighbourhoods, a minimum-wage worker cannot afford an average one-bedroom apartment (McDonald and Tranjan, 2022), with unaffordability disproportionately affecting racialized renters (SPT [Social Planning Toronto], 2020). In the City of Toronto, asking rents hit a record of $3,000 in April 2023 after six straight quarters of double-digit increases (Kalinowski, 2023), such that a Toronto household would need to make $100,000 per year to afford the average apartment (Statcan, 2021). 1 These trends have led tenant organizations (ACORN Canada, 2021), housing rights advocates (CCHR [Canadian Centre for Housing Rights], 2023a; AHSL [Affordable Housing Solutions Lab], 2023) and researchers (August, 2021; St-Hilaire et al., 2024) to associate financialization with rising housing costs and reduced affordability. However, data demonstrating this connection is hard to come by, even as financialization has moved from a scholarly concern into mainstream public debates.

Globally, researchers are exposing financial firms for buying up affordable housing, evicting at high rates and driving up rental costs (Gabor & Kohl, 2022). In 2019, United Nations representatives challenged Blackstone – the world’s largest private equity group – for violating the human right to housing (UN [United Nation], 2019). In Canada too, the media, public and policy makers are beginning to highlight the incongruities between the Right to Housing (recently affirmed in Canadian legislation), and the treatment of housing as an investment product by financial firms. In 2022, Canada’s newly appointed Federal Housing Advocate (OFHA [Office of the Ferderal Housing Advocate], 2022) commissioned a series of reports, and in 2023 Canada’s National Housing Council launched its first ever Review Panel, examining the financialization of rental housing. Critiques of financialization have inspired a backlash from the industry and its supporters. In defense of Blackstone, Forbes published a 2023 piece claiming that ‘private equity did not cause the housing crunch’ (Westenhaver, 2023). In Canada, the Financial Post re-printed an article defending financial ownership of apartments (Taylor, 2022), and in 2023, Canada’s five-biggest REITs attempted to rebrand as providers of affordable housing. 2 As tenants and advocates call for policies to rein in financial landlords and the industry pushes back, there is a need for clear findings on the impacts of the financialization of housing. In this paper, we look specifically at the relationship between financial ownership of apartments and rent prices, and how this maps on to Toronto’s uneven geography of racialized inequality.

The paper begins by surveying the literature on the financialization of rental housing and how theory predicts that financial firms will raise rents more aggressively than other owners. Next, we qualitatively examine comments related to rents made by financial firms themselves, drawing on company records and other sources. We find that in line with theories of financialization, financial firms claim to generate revenues from rents more intensively than their competitors. Next, we used four quantitative approaches to analyze a uniquely composed dataset which links landlord ownership with building-level rent data in Toronto to test whether financial firms have raised rents more than other types of owners. First, we found that financial firms in Toronto charged the highest ‘rent premiums’ to average rents, asking 44% more per month (or CAD$670 more) than average neighbourhood rents (over 2022–2024), a much higher premium than other landlord types. Second, we found that financial firms increased same-property rents at faster rates than their counterparts – imposing an average 5.0% increase per quarter ($96). Third, using a multiple linear regression model, we found that ‘financial’ landlord as a variable had the largest impact on rent levels, rent premiums and same-property quarterly rent changes among landlord types. Fourth, we spatially analyzed rent increases, finding that financial firms charged the highest rent premiums in the city’s 31 ‘Neighbourhood Improvement Areas’ (NIAs) – areas with higher levels of low-income and racialized residents, identified by the City of Toronto (2020) for having the most ‘inequitable outcomes’. 3 We conclude that while all private landlords aim to profit from rental housing, financial landlords are most aggressive in driving up rent prices, particularly in the most marginalized districts.

Financialization, profit-making and rent increases in rental housing

Financialization refers to a shift in the economy in which finance capital has assumed a dominant role and profits are increasingly made through financial rather than productive channels (Durand, 2017). According to Aalbers (2016) it involves ‘the increasing dominance of financial actors, practices, measurements, and narratives, at various scales, resulting in the structural transformation of economies, firms (including financial institutions), states, and households’ (p. 3). Globally, financialization has been associated with the rise of inequality, facilitating the transfer of income to the wealthiest ‘one percent’ (Piketty, 2017), and into the hands of owners of assets (Adkins et al., 2020); a process that has been ‘highly detrimental to significant numbers of people around the globe’ (Epstein, 2005: 5). While critics of the concept of financialization have pointed to its vague and expansive definitions (Christophers, 2015), and argued that it is nothing new (Koddenbrock et al., 2022), Sassen (2012) argues that the current, new age of global finance has been driven by the deregulation of capital markets, the formalization of the private institutions in the operations of global markets, and the role of info-tech in the proliferation of new financial tools and vehicles.

The financialization of housing involves the treatment of housing as a commodity and financial asset, rather than a home and basic human right (Rolnik, 2019). It is defined by the increasing role of financial firms and vehicles (such as private equity, Real Estate Investment Trusts [REITs], publicly-listed firms, institutions and asset managers) in the ownership of housing debt (mortgages) and housing itself – including single-family rentals (Charles, 2020; Fields, 2018), multi-family homes (August, 2020; Fields, 2017; Teresa, 2019; Lima, 2020), long-term care and retirement homes (August, 2020; Horton, 2020), student housing (Revington and August, 2020), mobile homes (Sullivan, 2018; Kolhatkar, 2021), cooperative and social housing (Fields and Uffer, 2016; Wainwright and Manville, 2017) and new-build construction (Gaudreau, 2020; Nethercote, 2020). One measure of the growing financialization of housing is the increasing concentration of homes in the hands of financial firms. Since the 1990s, researchers have identified this trend – in New York (Fields, 2017), Los Angeles (Graziani et al., 2020) and in Canada – where financial firms have consolidated 20%–30% of multi-family housing stock and 33% of seniors housing (August, 2020).

It is common to ask if financial landlords are different from other private landlords, who similarly run profit-driven businesses. Theory suggests that financial landlords are more extreme in their pursuit of profits. The ascendancy of finance is associated with the rise of assetization – the transformation of things (such as housing, infrastructure, public goods, data, and more) into assets that produce an income stream for their owner and to which financial logics are applied (Birch and Ward, 2022; Langley, 2021). The pursuit of financial metrics and ‘shareholder value’ (Ashwood et al., 2022; Prechel and Touche, 2014) drives managers to maximally extract value from their investments, and ultimately from the workers, customers, buildings, land and environment associated with them, to the detriment of other objectives (affordability, quality of life, labour conditions, etc). The very structure of financial firms compels managers to aggressively seek returns. Most Canadian multi-family REITs, for example, operate with the same objectives: to deliver stable monthly tax-deferred payouts to investors and to grow net asset value. 4 If their asset value (and share value) goes down, they will lose investors and fail. Executive compensation is typically linked to firm performance, giving additional incentive to leadership to maximize profits. Similarly, private equity fund managers must deliver returns that exceed certain benchmarks or face financial penalties. The structural compulsion to pursue financial performance metrics differentiates these types of firms from non-financial landlords. Because they are not beholden to external investors, a small landlord or private company might choose to keep rents affordable and accept a lower profit margin. This is not an option for financial firms. Financial firms also differ from other landlords in terms of their sophistication and use of technology. Financial firms have complex corporate structures that distribute risk and profits across legal boundaries (Ashwood et al., 2022), and use platforms and data that facilitate acquisitions and optimize costs and revenues (Fields, 2019). According to Nethercote (2023), financial firms leverage data to create ‘sophisticated renter profiles’, and extract as much money from renters as possible. While there will always be variation in the behaviour of landlords across various categories, we expect financial firms as a class to set high rents and raise them aggressively.

Researchers have found evidence that financial firms are aggressive in their property management strategies (August, 2020), with negative effects on tenants. Their business strategies have been associated with under-maintenance and property neglect (Teresa, 2016; Fields, 2017), increased cost burdens (St-Hilaire et al., 2024), harassment (Crosby, 2020) and displacement (Walks and Soederberg, 2021). In the US, financialization is associated with increased rates of eviction and dispossession (Seymour and Akers, 2021), with worse impacts on racialized and Black renters (Fields and Raymond, 2021; Raymond et al., 2021). In Canada, financial firms have been found to file for evictions at the highest rates (August and Mah, 2024; Buhler, 2023). ACORN Canada (Jhamb & Duncan, 2022) surveyed 606 tenants and found that people in financial-owned properties had higher rates of disrepair, of perceived unfair treatment and of feeling threatened when filing complaints, along with more trouble getting work done compared to tenants of other types of landlords. In addition, properties owned by financial firms in Toronto have higher rates of Above-Guideline Increases (AGIs) to rents (Zigman and August, 2021).

A central concern – and the focus of this paper – is that financial firms charge higher rents. Researchers have demonstrated this link at a high level. In Europe, Dewilde and De Decker (2016) found that countries with more financialized housing regimes had worse affordability for low-income owners and renters. In Canada, Zhu et al. (2021) identified financialization as a key factor associated with worsened affordability for low- to moderate-income renters. St-Hilaire et al. (2024) have found that neighbourhoods in Montreal with higher percentage of financialized landlords had higher levels of both average sitting and asking rents. Beyond broad-level trends, there are few studies that look explicitly at financial firms in rental housing – building by building – to see if there is a difference in their rent-raising behaviours compared to other firms – an approach that would demonstrate this link more decisively. One exception is García-Lamarca (2021), who found that in Barcelona, REIT-owned properties had rents far above average neighbourhood rents, and properties owned by Blackstone were listed for 38% more than similar apartments (p. 1418). 5

Finally, we focus in this work on the geography of financialization and rent increases in Toronto, which highlights the varied impact of landlord profit-making strategies in the contexts of race class, and social difference. Scholars of racial capitalism and urbanization have identified how capitalist value extraction from property is predicated on racial difference (Dantzler, 2021), and how the financialization of housing both capitalizes on and reproduces racial inequality (Fields and Raymond, 2021). Racialized households are not only targeted for predatory lending and dispossession (Immergluck, 2022), but can be gouged for higher rents (or displaced outright) as real estate actors close the profitable rent gap created by the devaluation of property in racialized communities. While still an emerging field, scholars have have found connections between financialization of rental housing and uneven racial impacts (Raymond et al., 2021). In South Africa, for example, Migozzi (2023) examined racial capitalism, platform capitalism and the rise of corporate landlords to find that firms using racially-based algorithms disproportionately extracted profits from Black renters.

Qualitative analysis – What financial firms say about rent increases

Literature and theory on financialization (discussed above) suggest that financial firms may pursue rent increases more aggressively than other types of landlords. We also expect financial firms to raise rents more aggressively because they say they do. In this section, we discuss qualitative findings from public filings, documents and other commentary by financial owners of rental housing in Canada, 6 in which they boast to investors about their high rent increases, and even point to their structure as unique in extracting higher rents more efficiently.

The operating strategy of financial firms in rental housing makes money for investors quite simply – by driving up revenues and driving down expenses. Rents (and other fees) are their source of revenues, and so raising rents is central to maximizing profits. Rents can be raised on sitting tenants in the Province of Ontario (where Toronto is located) once per year, by a provincially-set ‘guideline’ amount. 7 Rent control is suspended, however, if units become vacant, making it profitable for firms to replace existing tenants with someone new. To drive high profits, financial firms pursue ‘suite turnovers’ leading to vacancies that allow them to raise rents ‘to market’. In addition, rents can be raised using ‘Above Guideline Increases’ (AGIs), a loophole in legislation allowing for additional increases if landlords invest in certain major capital repairs. Financial firms pursue rent increases in all these ways as part of ‘repositioning’ or ‘value-add’ strategies, which often include renovations to further lift rents, particularly in gentrifying areas.

Many financial firms we analyzed explicitly identified strategies to increase rents maximally upon vacancy. For example, private equity firm Conundrum Capital (operating under the Q Residential brand) outlined a 2019 growth plan to ‘move current in-place rents to market rent upon suite turnover’ (Conundrum Capital Corporation [Continuum Residential REIT], 2019: ix), aiming for a 30% ($368) increase on average, despite that year’s provincially allowable increase of 1.8%. Notably, the firm cited ‘rental revenue growth’ as the only driver of cash flow increases for their company. Similarly, CAPREIT, Canada’s second-largest landlord with over 47,000 suites, increased its rents ‘on turnover’ in 2022 by 12%, fully ten times higher than the provincially set guideline increases for that year (CAPREIT, 2022: 1).

Canada’s largest landlord, Starlight Investments, suggested that financial firms are unique in their strategies to maximize rent increases. With a portfolio of over 60,000 suites, Starlight is a private asset manager with a range of funds, joint ventures and partnerships with major institutions and investors (including US-based Blackstone Group). In 2019, the firm published a ‘white paper’ on returns in multi-family housing, making the case that landlords with ‘scale, operational expertise, and capital’ (characteristics associated with financial landlords) were uniquely able to extract maximum growth from apartments using a ‘value-add strategy’, and pointed to two publicly listed firms (Minto REIT and Interrent REIT) using the same approach (p. 3). The value-add strategy described by Starlight goes beyond simply raising rents and fees (for laundry, parking, storage, etc), to include ‘active management’ that generates – according to the company – ‘two times the returns’ (Starlight Investments, 2019: 3). To illustrate, Starlight offered a case study of one property where their ‘value add strategy’ was applied (including renovations), and rents were increased by $411 per month (or 31%).

Minto REIT (owner of 8,300 suites in Canada as of 2022) boasted in 2018 of charging ‘the highest in-place rent among public peers’ (Minto REIT, 2018: 8). Minto’s growth plan was to use an ‘intensive, active management approach’ (p. 9), involving raising rents to market levels, using above-guideline-increases (AGIs) in Ontario, and repositioning properties – noting that ‘renovation opportunities pursued by management are intended to drive and enhance revenue’ (p. 10). The firm also described using ‘test suites’ to see just how high rents could be raised. Another major player, Timbercreek Asset Management (rebranded in 2020 as Hazelview), described using a ‘value-add renovation and repositioning’ approach, ‘with the objective of increasing monthly rents and potentially generating significant gain upon divestiture’ (2012: 7). 8 Investments in the ‘cosmetic appeal’ of buildings were intended to put them into a ‘higher market’. In 2011, CEO Ugo Bizarri told the Financial Post that their value creation strategy ‘leads to the opportunity to raise rents when tenants leave’ (Critchley, 2011).

Rent increase strategies have spatial dimensions as well, as firms find it profitable to capitalize on gentrification pressures to increase rents, often in areas with higher proportions of racialized renters and newcomer households – where rents have often remained low. Investment management firm Fiera described in 2019 how they were able to achieve 40% rent increases ‘upon turnover’ after repositioning a building in Toronto’s gentrifying Black Creek community, an area with above-average concentrations of visible minority and immigrant households (City of Toronto, 2016). According to VP Peter McFarland: ‘We are gutting a unit each time a tenant moves out. . . and renovating and re-leasing to new tenants who are able to afford that kind of pricing. It’s worked very well, and it’s gotten us the overall return objective that our fund has’. 9

Financial firms explicitly differentiate themselves from so-called ‘legacy’ owners – longer-term operators or rental housing who are not seeking to maximize investments in the same way. Nick Macrae, Senior VP of private equity firm Woodbourne described in 2023 that ‘a lot of legacy managers. . . have a different operating model’. Some non-financial operators agree. Interviewed in 2014, Paul Minz, of 50-year-old family-run Toronto firm M&R Properties compared his firm directly to REITs, noting that ‘the mindset is different. They are driving by financial decisions rather than by seeing the building as a core asset’ (CAM [Canadian Apartment Magazine], 2014). He added that at his firm, ‘we are never pressured to sell or finance, we want to optimize and take care of our buildings’ (CAM [Canadian Apartment Magazine], 2014).

Quantitative analysis of rent increases in Toronto

Data and methods

Even if financial firms claim to raise rents more ‘efficiently’ than others, it is worth seeing what rent data reveal. In this section we examine rents in Toronto by property, landlord and landlord type. In Canada, building-level information on rents and ownership has not traditionally been available. For this project, we drew on the new proprietary GTA Multi-Family Database by Altus Group, a real estate analytics company. This database includes asking rents for available/vacant apartments by size (bachelor up to four bedrooms) in the Greater Toronto Area (GTA), for all properties with over 12 units, updated quarterly. We used this database to collect rent data for ten quarters, starting with Q1 2022, through Q2 2024, for a total 1,602 unique properties, including 1,248 with multiple quarters of data, for a total of 8884 unique property-rent observations. 10 Our dataset included industry-defined information on ‘building class’, which rated properties on a scale from A (for highest quality) to D (for lowest quality), based on quality, age, construction and finishes.

For each property we assigned ownership and landlord type. To identify the owner, we used proprietary databases (Urbanation Property Sales, Altus GTA Multi-Family, Altus Commercial Sales) and other sources (Municipal Property Assessment Corporation (MPAC) data; web-searches and company websites, data filed with Canada’s Securities Administrators (sedar.ca), and industry publications). We researched each owner and categorized them as:

We assigned owners to the highest suitable category. For example, a ‘multiple owner’ with a branded website would be identified as a ‘chain,’ and an owner identified as a private equity firm would be listed as ‘financial’ – even if it had only one property. Our categories focus on the owner, not the property manager. Our ‘chain-managed’ category, however, was created to acknowledge (following Gomory, 2022) that small owners may have different behaviour if they use professional property management. For this reason, we separated properties held by single- and multiple-owners using chain managers from those managing the properties on their own.

We used four quantitative approaches to address our research question. First, we compared ‘asking rents’ of individual properties (using Altus data) to the average ‘existing rents’ in their neighbourhood using Canada Mortgage Housing Corporation (CMHC) data, controlling for unit size. 12 CMHC’s ‘existing rent’ data includes prices for all occupied units, while ‘asking rent’ data is only for vacant units. Average ‘asking rents’ are therefore always higher than ‘existing rents,’ and represent the market that a tenant seeking housing would encounter (Boeing and Waddell, 2017). We thus expected the difference to be higher for all landlords but hypothesized that financial firms would charge a bigger ‘premium’ to neighbourhood average rents than other landlord types. Second, we used longitudinal quarterly rent data to look for patterns in same-property rent increases. Our data spanned ten quarters (Q1 2022–Q2 2024), including 1,248 properties with more than one data point. 13 We calculated the quarterly increases between each property with two consecutive points, and calculated an average increase for that property by averaging the quarterly increases. 14

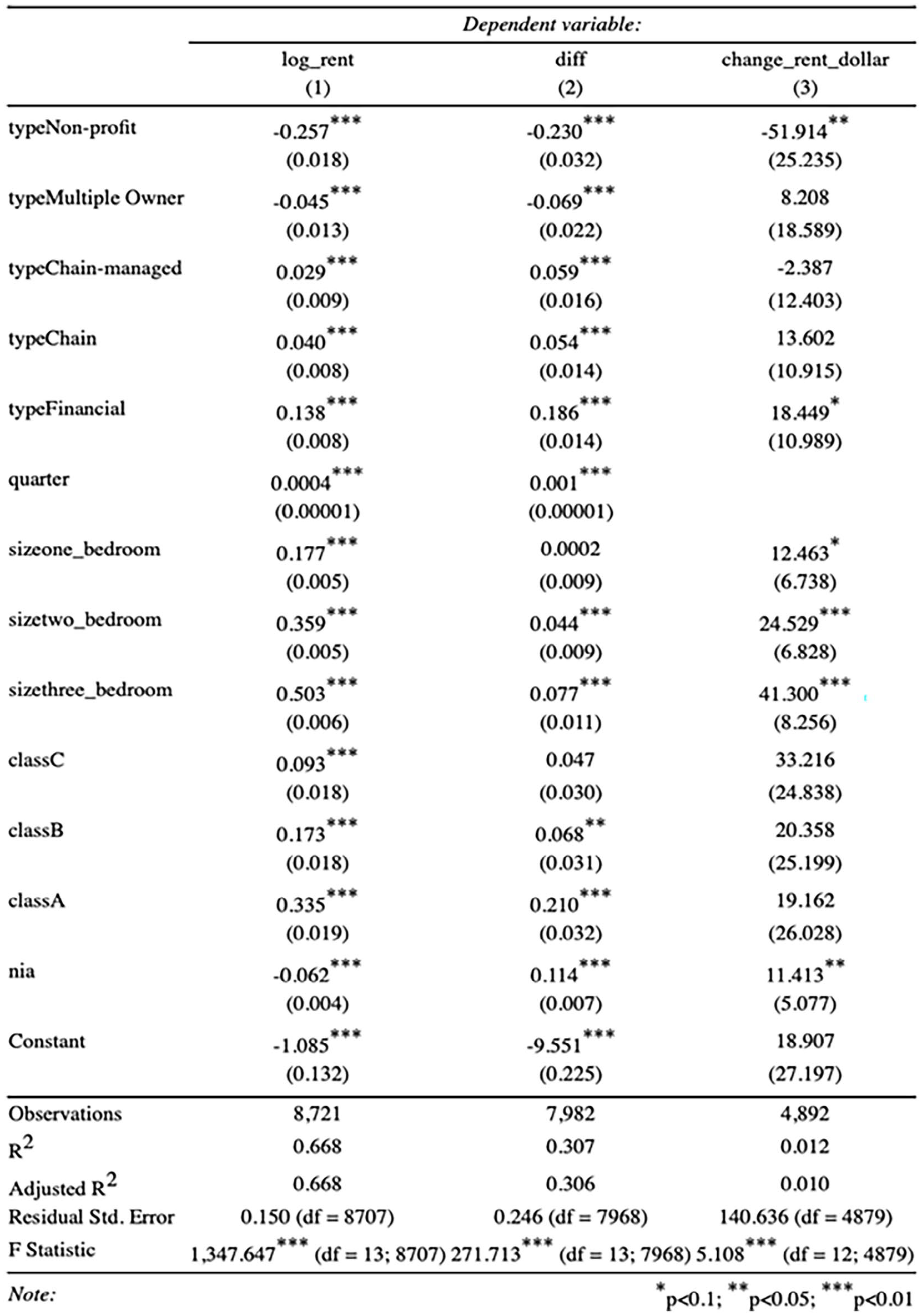

Third, we conducted three multiple linear regression models. Our dependent variables were logged asking rents (log_rent), rent premium (diff) and quarterly same-property rent change (change_rent_dollar). Our independent variables included landlord type (type), building class (class), unit size (size), quarter during which data was collected (quarter) and if the building was in a Neighbourhood Improvement Area (nia). The independent variables are categorical except for quarter (a date variable) and nia (a binary variable). We converted type, size and class to factor variables, with ‘Single owner’, ‘Bachelor’ and ‘D’ being the implicit levels of the three variables. 15 The three regression equations are the following:

Fourth and finally, we examined the geography of financialization and rent by linking our rental price data to: (1) spatialized after-tax household income (2021 census), (2) percentage of visible minority population (2021 census) 16 and (3) property location in a Neighbourhood Improvement Area (NIA).

Rent premiums: Comparing property rents to CMHC average neighbourhood rents

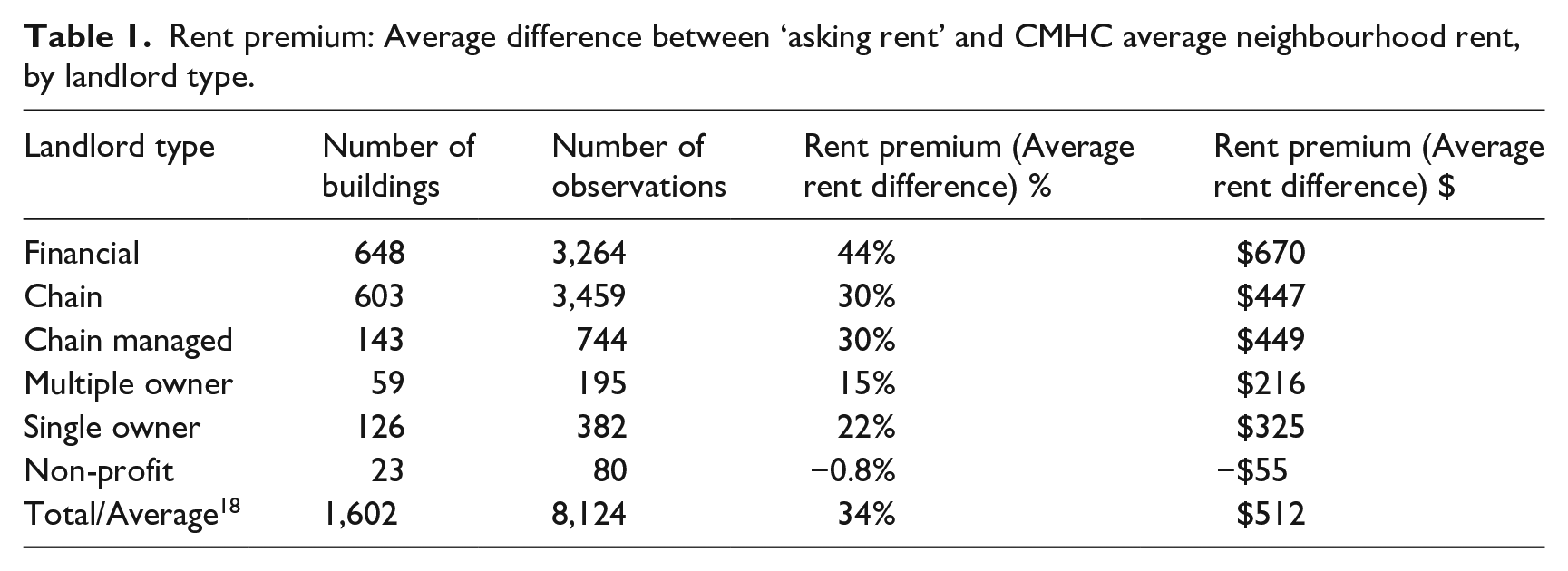

Our research identified that financial firms acquired 100,076 suites (38%) sold in Toronto between 1980 and 2020 and have totally dominated sales in recent years – snapping up 85% and 91% of suites sold in 2019 and 2020. 17 What, if any impact, has rising financialization had on rent levels? We found that financial firms charged an average asking rent of $2,383, 8.9% higher than our dataset average and far higher than $1,825, a rent level that would be affordable (at 30% of after-tax household income) for the median Toronto renter (CMHC, 2024). These rents diverged from local averages: our analysis showed that properties owned by financial landlords had the highest differences between asking rents and neighbourhood rents (Table 1), charging an average 44% premium ($670 more per month) to neighbourhood averages. This was higher than the premium charged by chains (30%) and chain managers (30%) – types of operators with corporate management and often large portfolios. Smaller-scale operators charged lower premiums, including multiple owners (15%) and single owners (22%). Non-profit landlords by contrast, charged a $55 discount to neighbourhood averages.

Rent premium: Average difference between ‘asking rent’ and CMHC average neighbourhood rent, by landlord type.

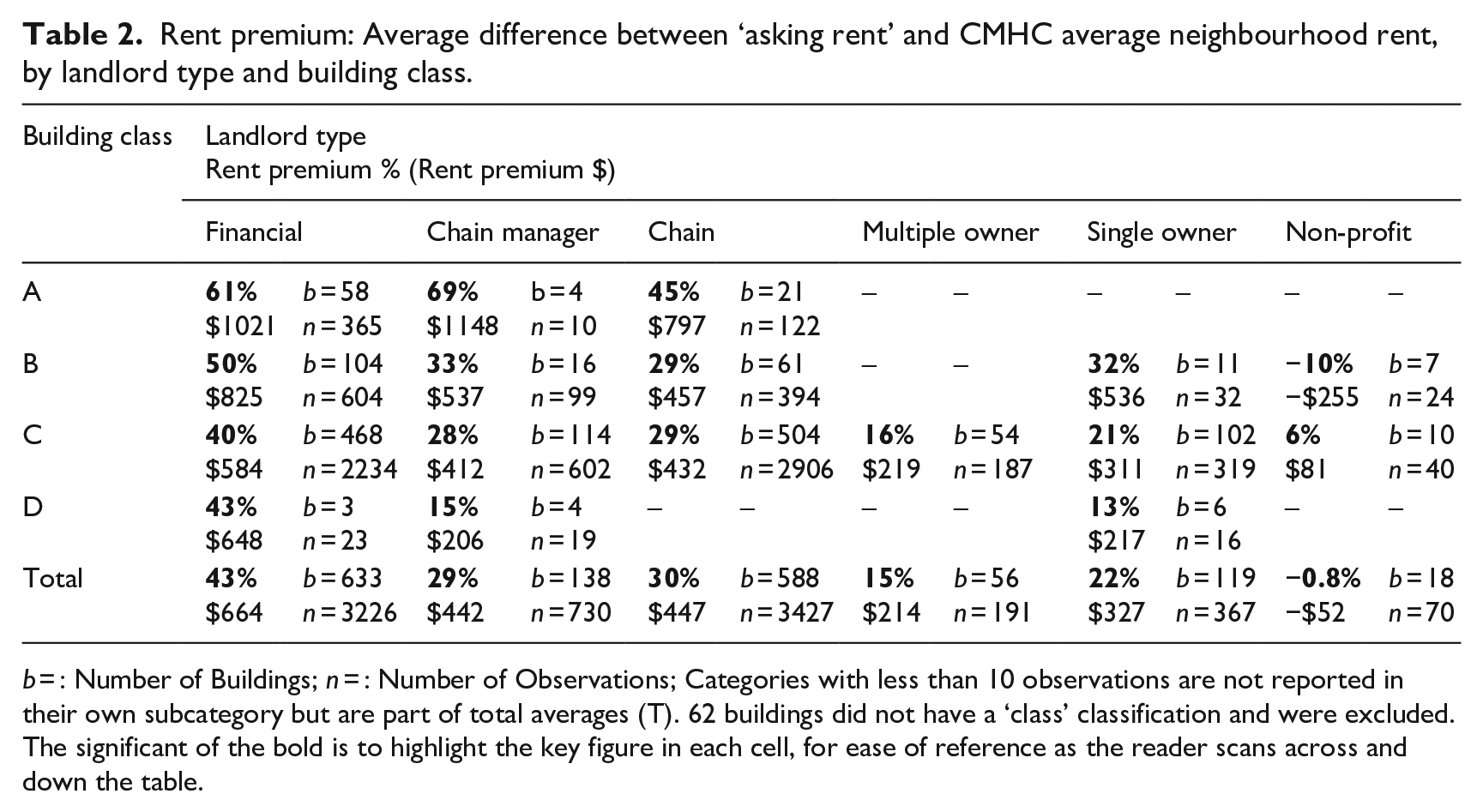

Perhaps financial firms simply own higher quality buildings, justifying higher levels of rent. To test this, we examined rent premiums by landlord-type and building class (Table 2). We found, first, that every type of landlord charged higher premiums for higher quality buildings (as show by reading down each column). This is to be expected – owners charge more for new or luxury buildings. Second, we found that financial firms charged the highest rent premiums when comparing buildings of the same class (i.e. reading across each row), for nearly every category. 19 For example, in ‘C-class buildings’ (the category with the most buildings), financial firms charged a 40% premium, higher than chain managers (28%), chains (29%), multiple owners (16%) and single owners (21%).

Rent premium: Average difference between ‘asking rent’ and CMHC average neighbourhood rent, by landlord type and building class.

b = : Number of Buildings; n = : Number of Observations; Categories with less than 10 observations are not reported in their own subcategory but are part of total averages (T). 62 buildings did not have a ‘class’ classification and were excluded. The significant of the bold is to highlight the key figure in each cell, for ease of reference as the reader scans across and down the table.

We ranked rent premiums by company to further examine rent increase behaviour. The firm that charged the biggest premium in our sample ($1,961 more than average rents – a 118% premium), was private equity firm Woodbourne. Woodbourne entered Canada in 2007 with a goal to apply US-style asset management to Canada’s multi-family sector. The firm owns both old buildings, which are subject to a repositioning program, and new buildings, in which higher uncontrolled rents can be charged. Quite notably, Woodbourne has publicly confirmed that it uses YieldStar software by RealPage Inc., which allows for ‘dynamic pricing’ of rentals, and which is subject to an ongoing class-action lawsuit in the US for allowing landlords to illegally collude to increase rents (Abraham, 2023). According to the lawsuit, YieldStar also sets prices artificially high and encourages landlords to leave units vacant to restrict supply. Woodbourne VP Nick Macrae stated that YieldStar allows the firm to ‘really optimize net operating income, which is different than maximizing occupancy’ – a comment that suggests the firm may indeed hold units vacant to maximize revenues.

Another firm that charged high premiums to neighbourhood rents (75% or $1,312) was asset manager and developer Fitzrovia. Fitzrovia’s portfolio includes new Class-A properties that are not subject to rent controls. In 2022, CEO Adrian Rocca 20 described Fitzrovia’s approach to ‘really push top-line revenue’, noting that ‘you need to drive rent’ to gain operating leverage in the multi-family asset class. His firm was achieving ‘tremendous growth on rental tone’, as he put it, when units turned over in their portfolio. Rocca described Fitzrovia as ‘data driven’, using focus groups and revenue optimization tools to charge the maximum amount possible. 21

Other firms that have (or may have) adopted YieldStar software also charged high premiums. Quadreal, the real estate arm of a BC-based pension fund, charged the fifth highest premiums in our sample (68% or $1,261) and may use YieldStar. 22 Institutional firm GWL (insurance company Great West Life), which charged a 45% (or $841) premium to neighbourhood rents, was the first Canadian firm to adopt YieldStar software. According to Realpage News (2017), GWL’s properties using the YieldStar platform ‘outperformed by up to 4% in rental revenue relative to the control group’ over an eight-month pilot test of the software.

What else do high rent premiums tell us about landlord strategies? First, because they indicate higher rent than the surrounding area, they are often associated with new Class A buildings. Indeed, many owners charging high premiums in our sample were institutional investors (pension funds, insurance companies), which typically acquire luxury rentals to ensure steady, low-risk, income-oriented returns. Second, high premiums can indicate rent gouging and gentrification as landlords raise rents in lower-income communities, often as part of a repositioning strategy – patterns examined further in our spatial analysis.

Longitudinal analysis: Comparing same-property rents over time

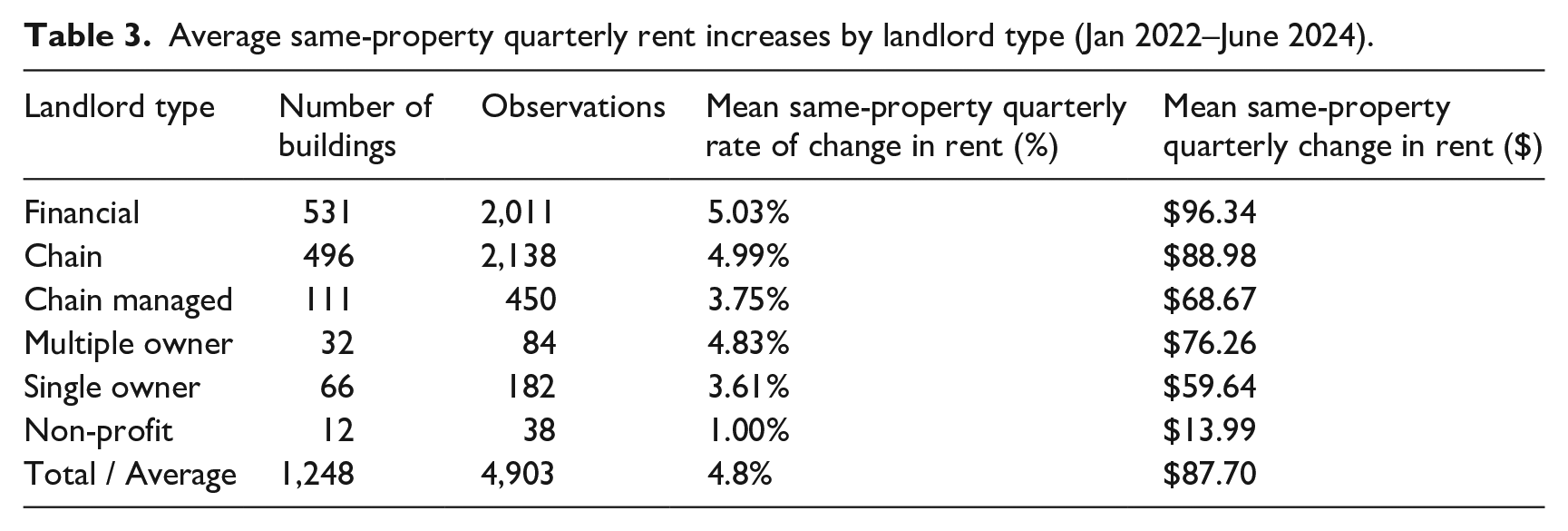

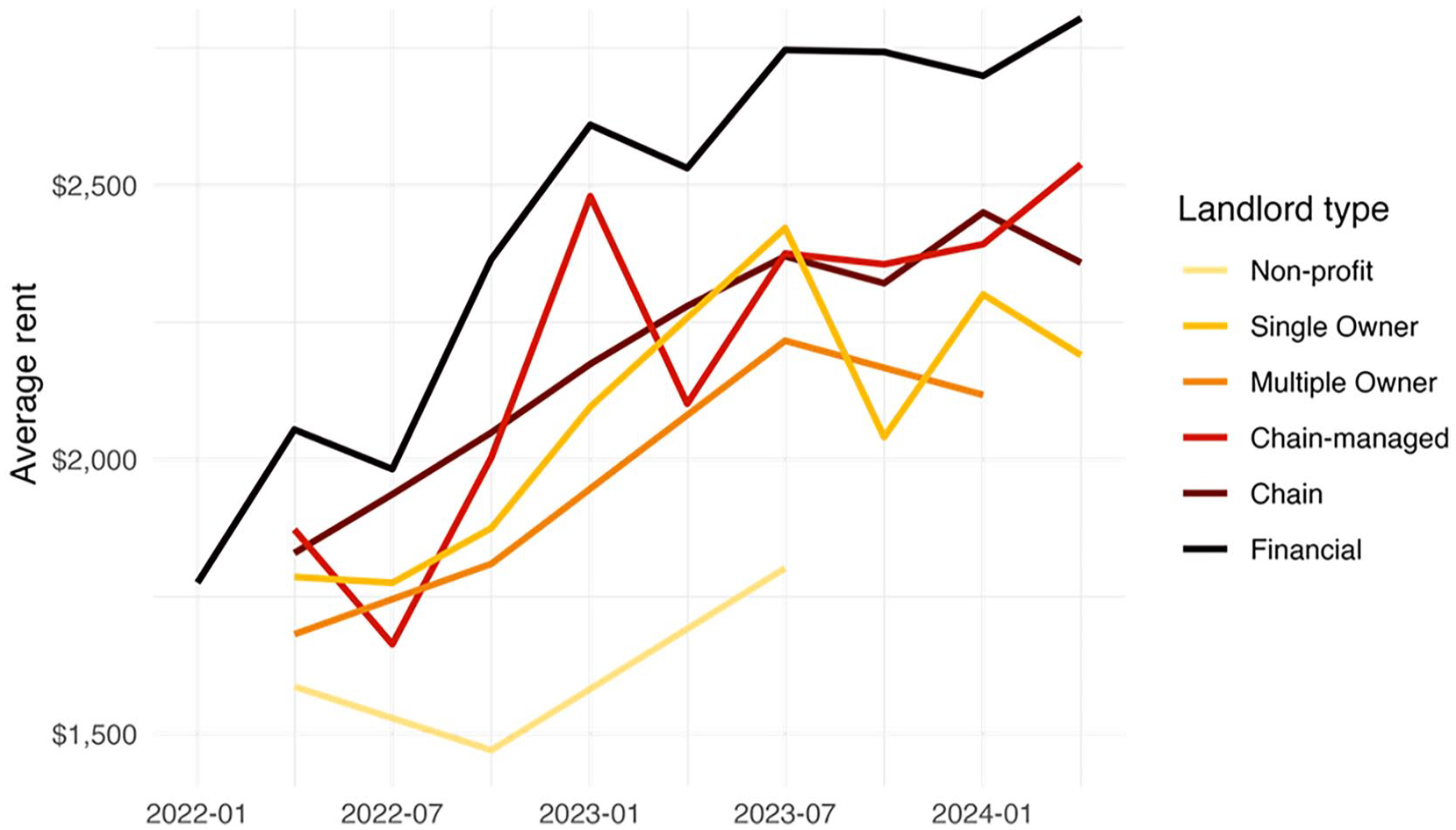

We examined same-building rent increases using a longitudinal dataset of 1,248 properties with rent data for more than one quarter (Table 3). We found that financial firms increased rents most aggressively – by an average of 5.0% ($96) per quarter. This was higher than chains ($89), chain managers ($69), multiple owners ($76), single owners ($60) and non-profits ($14). While the increases in Table 3 appear comparable in terms of percent change, financial firms charged higher rents across the board, meaning that similar percent change reflected higher dollar value increases (Figure 1).

Average same-property quarterly rent increases by landlord type (Jan 2022–June 2024).

Average quarterly rents by Landlord Type, January 2022–March 2024.

We associate high same-property rent increases with a strategy of value-add repositioning, often targeting lower-cost (Class C) properties where firms see the most runway (to use an industry term) to raise rents. These are areas where landlords capitalize on the rent gap (to use an academic term) between low existing and high potential rents (Smith, 1987). Financial firms may create conditions for pushing ‘potential’ rents even higher, drawing on supply constraints, superior market intelligence, technology and capital to create (and close) a bigger rent gap. The financial firms in our sample that posted high same-property increases included REITs, asset managers and institutions – financial landlords that often use value-add repositioning. Meanwhile, fewer institutional owners of Class-A properties had high same-property rent increases, possibly because properties with top-of-market rents have less ‘runway’ for increases on turnover.

One financial firm in our sample with very high same-property increases was Crestpoint Realty Investors, which drove rent increases of 9% ($148) per quarter across the 10 properties in our sample, equivalent to 36% (or $592) per year. Crestpoint’s properties were all ageing C-class apartments in Toronto’s gentrifying Parkdale neighbourhood, traditionally a low-rent destination. A boutique investment arm of a financial firm, Crestpoint’s goal is to create ‘strategic cash flow and long-term returns’ through ‘hands-on strategic asset management’ (Crestpoint, 2024). According to CEO Kevin Leon, Crestpoint is ‘pretty good at arbitraging the market . . . identifying situations where they’ve been poorly managed, or under-market rents and able to take advantage of that with active management’. 23 In other words, the firm targets low-cost rentals as ‘dislocations’ and drives value for shareholders by systematically closing the gap between existing and potential rents in the gentrifying community.

Multi-linear regressions: Financialized ownership and rents

To strengthen our findings, we conducted three multi-linear regression analyses (Figure 2), which showed a strong and significant relationship between financial ownership and rent levels, rent premiums, and quarterly same-property rent increases. Model 1 examined rent levels (represented as logged rents), and shows intuitive connections, such as higher logged-rents over time (quarter), in bigger units (bedroom size), and in higher quality buildings (e.g. class A has a coefficient of 0.335 vs class C with a much lower coefficient of 0.093). Ownership by financial firms was associated with the highest logged-rent of all landlord types (0.138 higher than single owners, p < 0.01), much higher than the next-highest type – chain-managed – which had a logged rent of 0.040). To put in terms that are easier to understand, if a unit held by a Single Owner (owner of one property) was listed at our dataset’s average rent – $2,187, the expected rent of the same unit would be $2,510 if it were owned by a financial firm (i.e. 0.138 log higher), a $323 difference. Model 1’s adjusted r-squared is 0.668 with all variables at p < 0.01, indicating a strong model fit. Model 2 examined rent premiums (the difference between asking and neighbourhood average rents) finding that the premium charged by financial firms was 18.6% higher than that charged by single owners (our comparator in this model). This was far higher than the next-closest landlord type, chain managers (which charged a 6.0% higher premium than single owners). Lastly, Model 3 found that financial landlords charged the highest same-property quarterly rent increases ($18.45, p < 0.1). We also conducted a binary regression model, 24 which associated having a financial landlord with a 14.6% (p < 0.01) higher rent premium and a $9.25 (p < 0.05) higher same-property quarterly rent increase, compared to all other (non-financial) landlords.

Multiple linear regression results predicting log rents, rent premiums and quarterly rent changes.

The social geography of rent increases

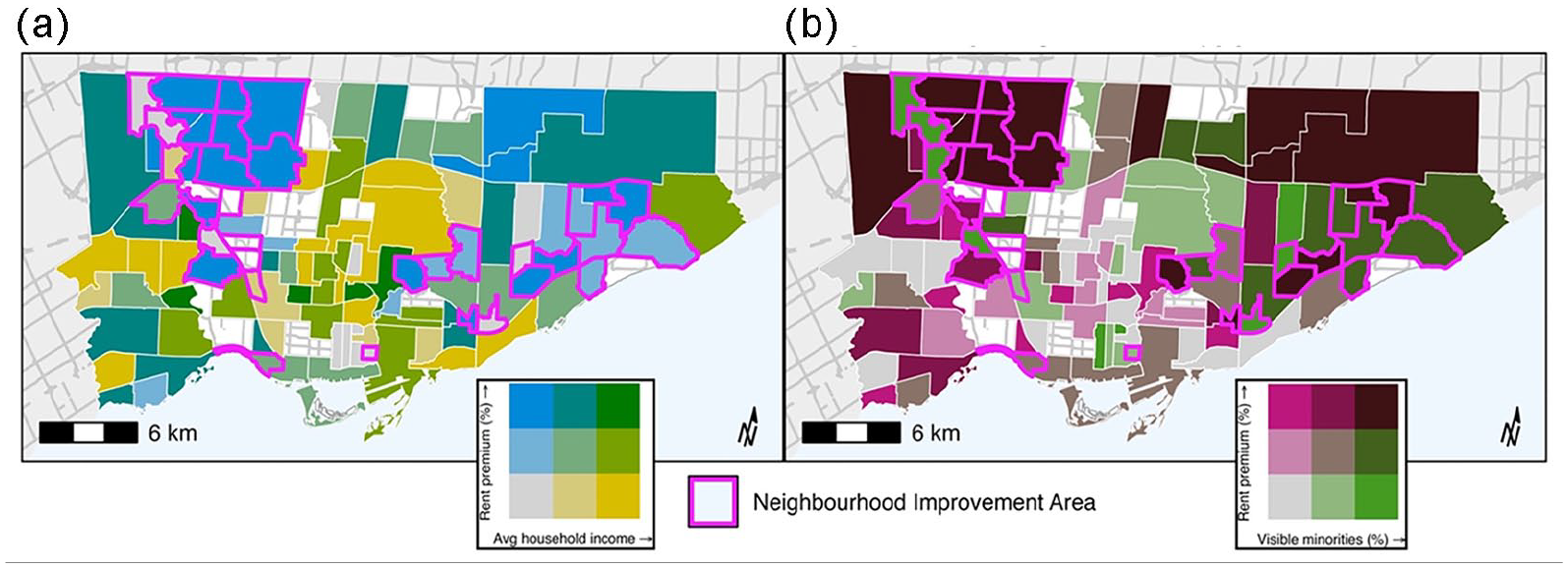

Finally, we examined the geography of financialization and rent increases in Toronto, to explore links between racialized spatial inequality and financialized value extraction (Fields and Raymond, 2021). We mapped the average rent premiums by neighbourhood for financial landlords and found that areas with high premiums are concentrated in the inner-suburban parts of Toronto associated with the suburbanization of racialized poverty (Hulchanski, 2005). This is also where the bulk of the City’s NIAs – areas identified for having statistically higher inequity – are located. We created two bivariate maps to visualize these patterns. The first (Figure 3a), combines data on rent premiums by financial landlords and average household incomes. This shows that NIAs were often shaded blue, indicating a combination of high rent premiums, and low incomes. The map also reveals a clear section of yellow-shaded census tracts, richer areas where rent premiums are comparatively lower – likely because high existing rents provide less ‘runway’ for firms to charge big increases.

Panel (a) Bivariate map of average rent premiums of financial landlords by neighbourhood and Panel (b) Bivariate map of rent premiums and percentage visible minority population.

Our second bivariate map (Figure 3b), combines data on rent premiums by financial landlords and visible minority population. In many of the areas that stand out for having low-incomes and high-rent premiums, there are also high percentages of visible minority populations. Particularly in NIAs and the inner suburbs, we see many dark purple-shaded census tracts, indicating areas where high rent premiums collide with high proportions of visible minorities. These maps suggest that in low-income and racialized communities, landlords seek bigger revenue gains from devalued rental properties, using repositioning and ‘value add’ strategies to extract higher rents and fees from lower-income renters (August and Walks, 2018).

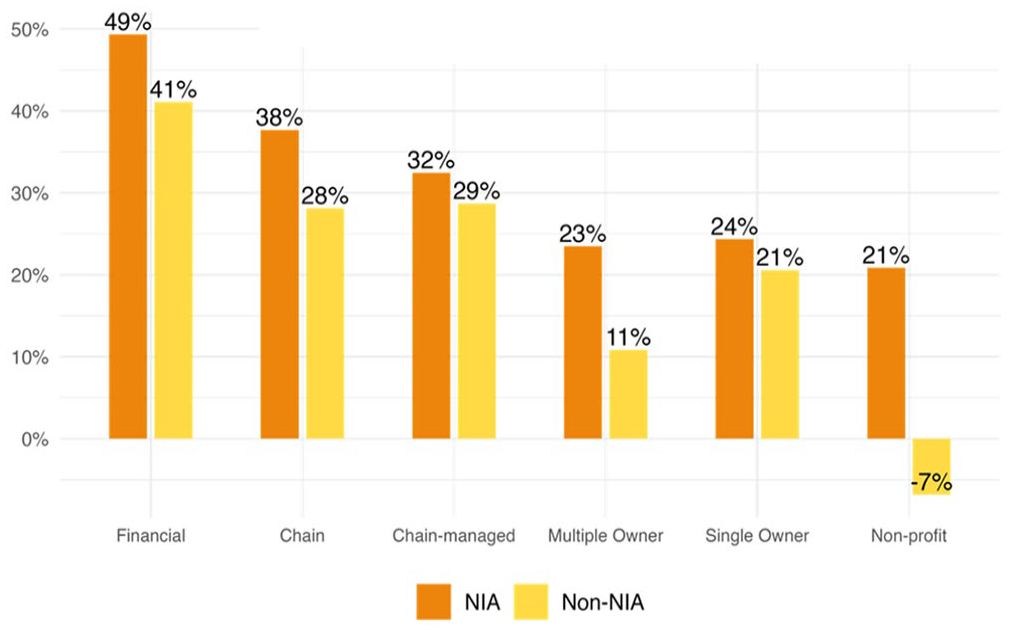

We found similar patterns of high-rent premiums being charged in NIAs with all landlord types (Figure 4). In all cases, landlords charged a higher premium to neighbourhood rents in NIAs when compared to non-NIAs. Still, the biggest rent premiums in NIAs were by financial firms – who charged, on average, 49% more than CMHC average rents in NIAs (compared to charging a 41% premium in non-NIAs). In other words, financial firms charged a 20% higher premium to residents in the city’s most inequitable areas. Our multi-linear regression confirmed these findings (Figure 2). While rent levels in NIAs tended to be lower overall (Model 1, p < 0.01), both the rent premiums and same-property quarterly rent increases (Model 2, p < 0.01 and Model 3, p < 0.05), were higher in NIAs than in non-NIAs, demonstrating that upon turnover, landlords tend to charge proportionally higher rents in NIAs than other neighbourhoods, capitalizing on higher rent gaps in marginalized neighbourhoods.

Rent premiums by landlord type in NIA and non-NIA neighbourhoods.

An example of a financial firm capitalizing on gentrification to raise rents in a racialized community was identified in our qualitative analysis a proprety acquired by Woodbourne in Toronto’s Weston area, an NIA with a high proportion of Black residents (Lewis, 2022). President Jack Herman 25 described it as ‘not a normal area you’d think about for a brand-new apartment’, and a place that ‘didn’t have much community around it before’. The firm bought in anticipation of incoming new transit, ‘applied our management techniques and increased the rent in the old building’. In 2021 the property was sold to Dream Unlimited, a financial firm with four REITs, an asset management business and $18 billion assets under management. Dream was one of top rent increasers in our study, raising rents by 13% ($204) per quarter across its Toronto-based properties (equivalent to 52% or $816 per year).

Conclusion

In 2021, Blackstone CEO Jonathan Gray – accused by the UN in 2019 of contributing to the global housing crisis – told landlords at Toronto’s Real Estate Forum how much he liked investing in Canadian housing. ‘Canadian housing people’, he told them: ‘diamonds are at your feet’. Meanwhile, rapidly declining affordability in the country is driving housing insecurity, evictions (Mah and August, 2022; CCHR [Canadian Centre for Housing Rights], 2023b) and homelessness (Cook and Crowe, 2022). While tenants face a crisis, the shareholders and senior executives in financial firms investing in rental housing gather diamonds. At the end of 2022, CAPREIT reported ‘record breaking’ annual returns, based on ‘rental uplift’ of 15 percent (CAPREIT, 2022). Minto REIT’s year-end report touted gains that were near the highest in the company’s history and promised investors a strong ‘outlook for our rental markets’ based on a ‘widened affordability gap’ (Minto REIT, 2023). In Toronto, the affordability crisis in rental housing appears to be linked to the profit-making strategies of financial firms, which extract more from tenants through rent increases, drive worsening affordability and use the earnings to enrich shareholders and company executives.

This article has investigated the link between the financialization of rental housing and the growing affordability crisis in Canada. Theorists expect that financialization – on the rise in Canada since the 1990s, will lead to higher rent levels because financial firms are structured to maximize profits more aggressively than other types of firms, driven both by their desire for profits (for executives and shareholders) and by their fear of losing investors if growth targets aren’t met. While other types of landlords are also profit-motivated, they are not structured with the same single-minded objective for growth. We argue that financial firms are more aggressive in pursuing rent increases because they say that they are: the firm themselves state that their growth is driven by raising rents, and that they pursue more aggressive increases – linking these to investor returns. Finally, we show that financial firms raise rents higher than other types of landlords by looking at building-level rent data in the City of Toronto. We found (1) that financial firms charged the highest average rent premiums when compared to average neighbourhood rents, (2) that financial firms charged the highest average same-property quarterly rent increases and (3) that ‘financial landlords’ was the landlord type most strongly correlated with higher rent levels in the city.

We also found a pattern in which higher rent premiums were charged in low-income and marginalized neighbourhoods. While higher premiums are expected in brand-new properties, the highest premiums were in communities with high levels of inequity and racially marginalized renters. Our data on same-property quarterly rent increases identified properties and communities where landlords are creating and capitalizing on rent gaps, using value-add repositioning strategies to push up rental prices in traditionally lower-cost areas. While property owners have historically used racial difference to generate and capitalize on rent gaps (at the expense of racially marginalized households), this research supports Fields and Raymond’s (2021) argument that financial firms are intensifying and extending these patterns, supported by large-scale data analysis and the likely use of property technology (Eschner, 2023).

Financial firms are leading the industry in raising rents and worsening housing affordability. This matters because they continue to dominate in apartment ownership, acquiring almost all suites sold in Toronto in recent years. Our findings suggest that the more they own, the worse affordability will get. We echo policy recommendations to rein in financial firms in the interests of promoting affordability (Farha et al., 2022; August, 2022). Notably, our findings should not be taken as an endorsement of non-financial landlords (Bano, 2024), who similarly (although not to the same degree) engage in rent-raising behaviours. As financial firms set the standard in the industry, other firms will increasingly follow their lead – adopting the strategies and technology associated with high rent increases. Ultimately, the social relation between tenants and landlords ensures exploitation and the solution involves regulating rental housing, expanding tenant protections and replacing for-profit ownership with social housing – efforts that will support tenants and housing equality regardless of landlord type.

Footnotes

Acknowledgements

The authors would like to thank Alan Walks, Julie Mah, David Wachsmuth, David Hulchanski and Richard Maaranen. The authors are grateful for the generous feedback of the three anonymous reviewers and EPA editor Desiree Fields.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper was funded by Neighbourhood Inequality, Diversity, and Change (SSHRC 895-2011-1104) project, and the Ontario Early Researcher Award. Cloé St-Hila was also supported by the Fonds de Recherche du Québec, and a Vanier Canada Graduate Scholarship (CGV-186949).