Abstract

The network of slum dweller federations known as SDI has innovated a form of local financing derived from the collective savings of urban poor groups. This addresses three shortcomings of conventional microfinance: its inability to reach very low-income people, its limited role in community mobilization for longer-term social change, and its constraints in terms of leveraging subsidies from the state and the market. SDI’s national and international urban poor funds have been used, among other purposes, for providing basic services and upgrading homes in informal settlements. Further, SDI’s model of federating urban poor communities and their funds at city, national and international levels has enabled mature federations, capable of financially sustainable projects, to cross-subsidize learning and precedent-setting projects in which full cost recovery is not feasible. This produces an outcome whereby the combined portfolios of all the national funds are able to match financial outflows with inflows. At the same time, the federations that co-manage these funds and the projects that they finance are able to escalate the production of social capital amongst the urban poor and to generate impact through changed relationships with government.

Keywords

I. Introduction

SDI is a unique network of slum dweller federations, which mobilizes communities around ever-expanding agglomerations of savings collectives that work together at city, national and global levels to build a transformative agenda for the creation of slum-friendly(1) cities in which the lives of the urban poor(2) are substantively improved. These federations now bring together over a million slum dwellers in over 30 countries throughout Africa, Asia and Latin America. The majority of their members are among the most vulnerable women, men and children in informal settlements.

This segment of the urban poor population almost never benefits from financial flows into low-income, informal neighbourhoods for the purposes of upgrading and housing improvements. It makes little difference whether these funds come from the state, the market or microfinance intermediaries.

This paper explores how and why SDI has been forced to bridge this finance gap for its network of urban poor federations. The primary purpose, however, has not been to provide access to credit as an end in itself, but rather as a means to urban transformation. The aim has not been to indebt poor households, nor to turn federation leaders into debt collectors. From the outset in the mid-1980s, SDI’s goal has been to place the organized urban poor at the heart of the politics and the economics that make all modern cities unequal and exclusionary, to organize them and unite them in such a way that they are the main drivers in transforming their slums into safe, secure, affordable and habitable neighbourhoods. This goal translates into a practical advocacy, in terms of which organized communities upgrade their own neighbourhoods, first on their own, then as part of federations and in conjunction with other stakeholders.

Because SDI has been obliged to build its own instruments (at settlement, city, national and global levels), so that very poor people living in informal settlements are able to have access to affordable finance, its savings systems have often been interpreted as conventional microcredit tools and its urban poor funds have been assessed as traditional housing microfinance mechanisms. When measured in those terms, SDI’s financing systems have a rather chequered record. More significantly, though, if SDI’s savings collectives and urban poor funds are seen through this lens – which is all too often the case – then its unique value proposition is misunderstood from the outset.

II. Why Sdi Affiliates have Developed Expertise in Community-Managed Local-Level Finance

The persistent housing finance challenge in low-income countries manifests itself in two related ways. Where adequate shelter is provided through formal processes, either by the private sector or by the state, it is generally unaffordable, especially for people at “the bottom of the pyramid” (the sub-sector of the population from which SDI draws its membership). Inversely, when poor people produce their own affordable shelter through informal processes, it is generally inadequate (and illegal).

From their inception, SDI-linked federations in 34 countries have sought to bridge this gulf. They have sought to make formal, adequate shelter affordable to the poor, mainly by trying to reduce costs by building incrementally, and by drawing state institutions into their land tenure, upgrading and housing interventions. From an actual delivery perspective, the strategy has been to start out by accumulating collective community savings and capacities, then to leverage resources from the state and then, by demonstrating the effectiveness of these bottom-up interventions, to push for the institutionalization of state support for these co-productive solutions. As opposed to a housing microfinance lens, this is the frame through which SDI systems for the financing of slum upgrading ought to be examined and assessed. The households that benefit directly from projects funded through SDI’s savings schemes and urban poor funds may regard the physical outputs, whether settlement re-blocking, infrastructure installation or housing, as ends in themselves. However, as an institution and as a tool for building a social movement of the urban poor, SDI has always regarded the projects it finances as interventions that produce, first and foremost, social and political capital for the federations that drive them.

For SDI federations, saving for self-built, incremental housing and trying to leverage state resources have always been interconnected. The innovative, grassroots finance programmes that SDI has built over the years have always been designed to advance these two objectives. SDI’s support for community-owned and -managed project implementation has not only been for the sake of one-off improvements for project beneficiaries. Its intention has been to produce solutions at scale. This has forced it to engage in the sphere of upgrading and housing finance. It is also why SDI has always insisted that informal settlement upgrading, including housing delivery, should explicitly target the securing of subsidies, especially but not only from governments, so that the lowest quartile of the urban poor is included. The leveraging of resources from other actors, especially state institutions, for specific projects is an important goal, but for SDI it is also a means to a larger end. The long-term goal of all country federations and of SDI itself is to influence policymakers in a way that affects institutional arrangements, to change policy and redirect resources to the benefit of the urban poor. It is for this reason that SDI has always regarded its projects as means by which the direct action of slum dwellers sets precedents that other agencies, especially those of the state, will want to replicate and institutionalize.

Straightforward housing microfinance, without a clear subsidy component, is by no means a panacea for the poorest households living in slums. In spite of all the ideologically driven assertions to the contrary, taking on debt is an extremely risky undertaking that desperate households and institutions are all too frequently encouraged to pursue. This widespread endorsement and promotion of housing microfinance stem, in part, from the fact that state institutions, especially in low-income countries, consistently ignore the needs of the poor, and that formal financial institutions across the board regard investments in low-cost housing as too risky. Since there are over 2 billion people living in inadequate shelter, often without tenure security, housing microfinance can enter this space, insist on 100 per cent cost recovery (including very high rates of interest), and find enough takers with sufficient income to benefit from their offerings. These takers are invariably higher-income households that generally include homeowners seeking to invest in household improvements. Microfinance rarely answers the needs of tenants or those with very low incomes.

This is why SDI, a grassroots social movement, with its roots in trying to prevent evictions by securing the rights of the urban poor, has devoted so much of its time and effort to designing and applying alternative, pro-poor systems of housing finance.

III. It Starts with the Savings Collectives

Saving is one of the defining practices of all grassroots organizations affiliated to SDI. While lending and withdrawing money occur with equal regularity, special emphasis is placed on savings. SDI’s earliest origins are in the mid-1980s in South Asia – where the microcredit movement got its lift-off at about the same time. Superficially, SDI savings networks are similar to mainstream microfinance programmes. They share some of their characteristics, making use of the strengths of these systems in delivering small loans with little delay and at comparatively low cost. As with microcredit programmes, SDI groups use group-based relational collateral and the successful repayment of small loans as a precondition for larger-scale finance. Most importantly, both microcredit groups and SDI savings and credit groups are concerned with addressing the gap caused by the reluctance, or inability, of formal-sector institutions to service the poor – especially women.

However, it is in their responses to this crucial gap that their paths diverge, because they have very different approaches to improving the material conditions of the poor.(3) Microcredit initiatives are concerned with giving low-income people access to money and financial markets, helping them save and borrow their way out of poverty. But SDI groups have chosen to use savings also as a cornerstone practice for dealing with evictions and related land tenure, basic services and shelter challenges. This has meant using microfinance not only to adjust credit markets downward but also to build material, social and intellectual cohesion in order to pressure governments into taking on the responsibility for intervening in issues of equity and redistribution.

Of course, setting up savings schemes was only the first step. All federations have a long route to travel before they develop fully fledged housing finance instruments and attract external finance on terms favourable for the very poor. For a very long time, India’s savings collectives (SDI’s first foray into this space) did not succeed in significantly leveraging external resources. These extended delays, amounting to a decade and a half before external resources were leveraged, gave the Indian Alliance enough time to develop financial management systems that worked specifically for the very poor. At the same time, they became progressively more robust until they could satisfy the vertical accountabilities demanded by semi-formal and formal financial institutions. On the opposite end of the spectrum, the South African savings groups quickly became adept at leveraging resources from the state, but their housing microfinance instruments for recovering loans remained undeveloped. Importantly, though, the savings collectives in the South African federation showed that under certain conditions it was possible to pressurize governments to recognize, support and finance organized communities of the urban poor.

IV. The Emergence of National Urban Poor Funds

Savings may be a sufficient reason for poor people to join a community collective, but are not enough to ensure ongoing involvement and participation. “Savings has to be for a purpose”, as a Malawi federation slogan pronounces. If the purpose is to provide small-scale lending opportunities that target households, such as loans for livelihoods and consumption, then individual savings groups can be appropriate vehicles. However, SDI’s main objective has always been to address shelter needs. Land tenure, services and housing (even when they are incremental) require larger investments that are beyond the savings and repayment capacities of poor households. SDI’s federal model pointed to the way to address this challenge by developing the appropriate horizontal, participatory instruments to provide finance for community-level housing projects – local urban poor funds.

The first two housing projects in the SDI network that depended on this financial intermediation were designed and managed by the Jankalayan Cooperative Housing Society in Mumbai, India and Saamstaan Cooperative in Windhoek, Namibia. In both cases the communities involved realized that their own savings would never be sufficient to pay for their housing aspirations. This made them turn to their networks in order to request loans from the pooled savings for housing of all the savings collectives in these two cities.(4) This additional capital was only enough to finance a couple of houses at a time, but it produced two very important outcomes.

First, it produced solidarity and accountability across settlements. Social and financial flows were in alignment for the simple reason that every cent of available capital was community owned, resulting in local accountabilities, transparencies and relations of trust. One of the many benefits of a network of urban poor organizations that thrive in an environment of experiental learning is that tools that can be applied in struggles against poverty are readily transportable. Emerging federations throughout the SDI network replicated this strategy. Women in a single settlement came together to save as a response to tenure insecurity or lack of services. Other settlements in the respective cities followed suit. The savings collectives federated, pooling a portion of their savings, and making this available to those collectives in need of finance, whether to stave off an eviction threat, to upgrade essential services or to make minor improvements to their dwellings. This merging of some of the accumulated funds of several geographically contiguous, self-managed, women-centred savings collectives resulted in the creation of local funds in their most fundamental form. For convenience, these arrangements can be referred to as community funds or aspiring urban poor funds.

Second, the community funds in India and Namibia (and later in all other federations) enabled local NGOs, which had entered into partnerships with the savings collectives, to approach external agencies for financial assistance. In the case of India this took the form of government guarantees and government loans. In the case of Namibia it took the form of grant funding from church-based organizations. These were the early origins of local-level funds, comprising community savings for housing, and consolidated at the city level in order to attract external finance. Saamstaan’s and Jankalyan’s ability to house their members through the financing provided by community funds that were able to leverage external finance was quickly adapted by other countries in the SDI network. The simplicity of the instruments that constituted these first urban poor funds ensured their easy replication in other countries.

Jankalayan and Saamstaan were the first upgrading projects in the SDI network to demonstrate that capital requirements for settlement-wide and city-wide interventions are more demanding and are generally beyond the means of the pooled resources of a federation of savings collectives. These aspiring urban poor funds or community funds are unable to cover larger projects. The funds available are smaller than the overall scale of need. Community funds can only resource a limited (albeit increasing) number of small-scale settlement improvements. It needs to be emphasized that this is not an indication of the non-viability of these instruments, but a structural dimension that is fundamental to their intrinsic value. In order to undertake larger projects, the federations need to look beyond their own limited resources and use their numbers, their solidarity and their organizational strength to leverage subsidized or discounted capital from other sources. Formal intermediaries (normally NGOs) use their training and their networks to raise funds for the more capital-intensive projects, historically from donor and multilateral agencies. These funds are blended with community savings and loaned through the savings collective to the households involved in the project. Once these instruments have been used at least once to blend community savings with external finance, the local-level finance facility or urban poor fund is effectively operational and the federation in question has a mechanism to address the financial needs of the very poor households in the federations that cannot access credit within the formal financial systems. The Indian, Namibian and South African federations were the first to deliver projects in which community finance was blended with capital subsidies (South Africa) or subsidized loans (India and Namibia). Other federations followed suit.

As the community leaders in these other SDI federations and their support NGOs began to explore access to external funding, they realized that conventional mortgage finance was not going to be an option. Formal financial institutions regarded slum dwellers who had very little income and no assets (in particular, no formal title deeds and no regular formal employment) as extremely high risk.(5) When the federations then turned to shelter microfinance they bumped into a different set of constraints. While microfinance institutions are not intrinsically opposed to leveraging finance from other agencies, specifically the state, for the repayment of loans, they are not at all geared for such a strategy. Indeed, their primary aim is to make financial markets work better, and many of them are suspicious of engagements with the state due to the tradition of governments not honouring their loans. They are also very risky partners when it comes to financing projects whose primary purposes are to build social capital and to set policy precedents. Furthermore, housing microfinance is generally not linked to government programmes and therefore to government funding. Since microfinance loans are most likely to be provided to individual households for the purpose of building individual assets, and are de-linked from state interventions, it is often impossible for microfinance loans to be secured for much-needed land acquisition and infrastructure investment.(6) Finally, by targeting individuals (although they are sometimes tied to group guarantees) who meet certain criteria, traditional housing microfinance always favours the better-off segments of the homeless poor.

Since microfinance institutions do not address SDI’s need to provide credit for land and services to collectives of very poor people, SDI’s “go-to” institutions for these external funds became international agencies and donor institutions.(7) At the moment that external finance is secured, normally but not always from the abovementioned sources a whole set of new demands emerges: internal procedures, control mechanisms, allocation systems and reporting structures. The successes, since 2002, in securing external finance for projects may represent a triumph of the SDI mobilization model at settlement, city, national and international levels. However, external finance is by definition vertical, and its flow connects the savings collectives, which implement and benefit from the project, to vertical lines of power and decision-making. This applies not only to the relationships with the external resource provider, but also to increasingly complex internal systems of management. Professionals and community leaders who use the SDI model to succcessfully mobilize women’s collectives at scale now face a major new challenge: how to manage vertical flows of finance without killing the social capital generated through horizontal solidarities at the community level. The critical challenge becomes one of marrying these external finance flows that are necessary for achieving scale with the practices and institutional arrangements at settlement level that were designed in the spirit of “social movementism”. How does one design and deliver projects that:

continue to serve as sites for horizontal, grassroots learning, and

continue to set precedents that others will replicate and that state insitutions will institutionalize, but

at the same time are able to go to scale and cover costs in order to attract external finance from the state, international agencies and the market?

In other words, when and how do SDI’s urban poor funds move from emergent to mature? When and how do federations switch from delivering projects that are explicitly designed to produce social and political capital, to using this social and political capital to deliver projects that are able to achieve full cost recovery and replicate positive practices across settlements at a city-wide scale?

V. Mature Urban Poor Funds and City Funds

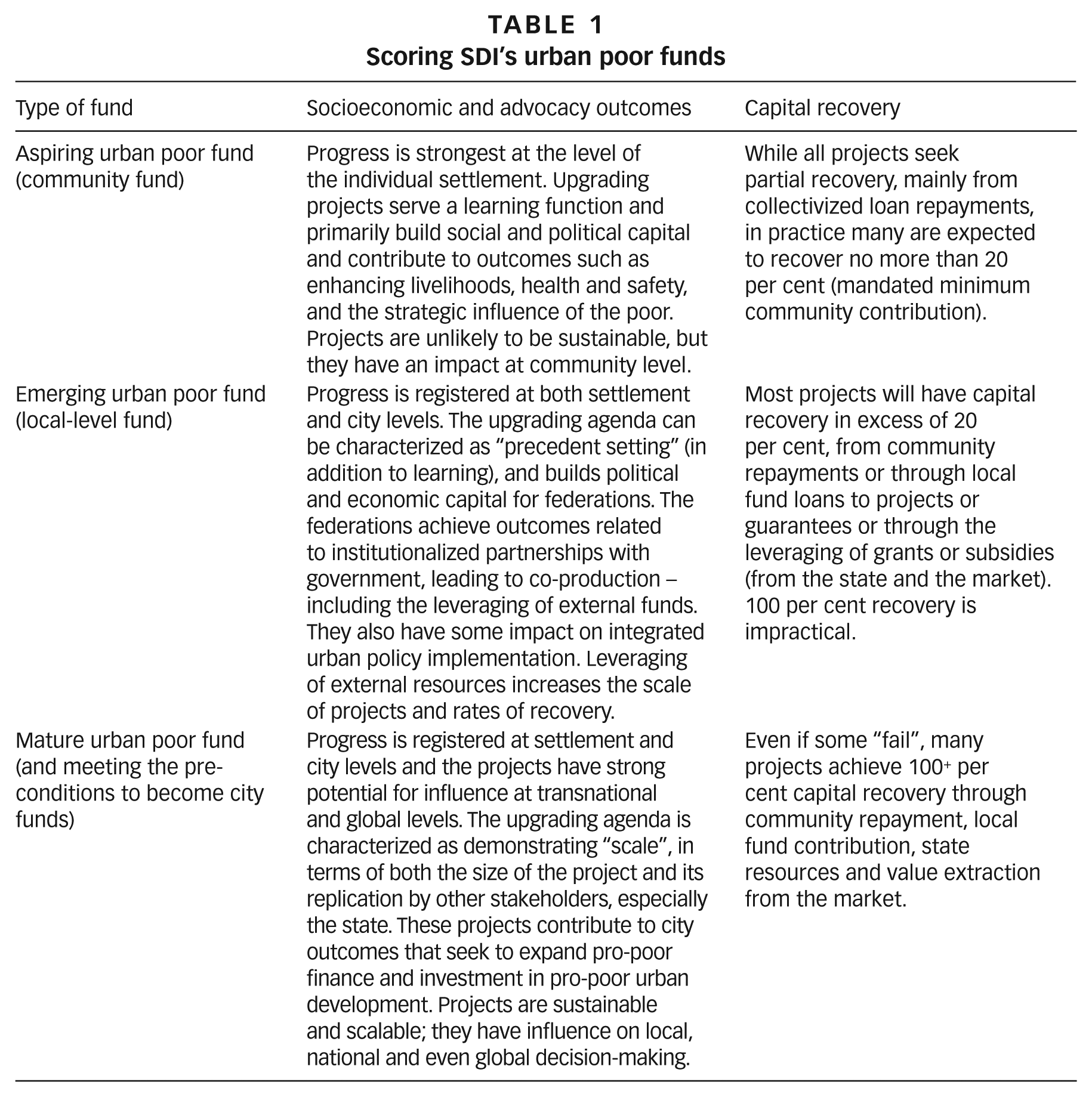

The introduction of external capital benchmarks the transition from aspiring to emergent, from community funds to local urban poor funds, and with this development comes major structural challenges. (Table 1 lists the characteristics of different types of urban poor funds, from aspiring to mature.) One possibility for every savings collective and for any national SDI affiliate is to refuse to accept external finance for investment in projects and to try using pooled community savings only. However, most settlement-upgrading projects have to bring in more resources than communities can generate themselves and, as already explained, SDI’s community funds are meant to be much more than just institutions that lend to the poor. They are institutions that are ambitiously trying to change the socioeconomic systems of our cities and our societies. Funds, therefore, need to have links with the state and need to become instruments that provide flexible finance to all organized communities of the urban poor, regardless of whether they belong to a federation or not. Government involvement (but not government control) is an essential precondition for these funds to have a large impact. It is very rare indeed for a finance facility grow beyond a few projects in a few settlements if it has to depend on community savings only,(8) even if they leverage external finance but do not force commitments of co-financing and co-production from government institutions.

Scoring SDI’s urban poor funds

However, it often is very difficult to set up this kind of city fund. Many federations are able to grow their community funds into urban poor funds by leveraging external finance, but may not be able to have them institutionalized by the state. In order for these urban poor funds to become sustainable by attracting and retaining the interest of external partners, including governments, they need to recover the funds they invest in community projects. Mature finance facilities in the SDI network are, first and foremost, those that have generated a portfolio of projects that, as a whole, are able to recover more than they invest. Cost recovery is an explicit but not primary aim, and repayment of loans by individual households is only one means to achieve this objective. The primary aim is to achieve transformational goals, not to “push the market down”. The projects they resource are designed and operated in ways that seek to make urban development outcomes inclusive and pro-poor.

There is one other extremely important financial hurdle that mature finance facilities have the potential to overcome. This is something that SDI is just beginning to explore. It relates to the ability of federations to extract value, especially the value related to land development, from the informal sector. This requires a strong federation that pools its resources and capacities at the city level (at the very least) to “disentangle” the web of exploitative social relations between politicians and slumlords, and among tenants, structure owners and landlords, in order to create land sharing (or acceptable relocation) options that can realize significant value. In general, federations that are still developing scale and muscle, and whose urban poor funds are at an emergent stage, are able to play a catalytic role in producing this value but then struggle to benefit materially from it themselves. One simply has to consider the impact that a single federation-driven project has on the land on which it takes place, and on neighbouring land, to appreciate how much value is generated by housing and related infrastructure development that is then diverted from urban poor enterprises as it is captured by other actors, individual or corporate, who do not have the interests of the urban poor at heart. Mature federations have developed the capacities to capture some of that value and use it to increase the capital base of their urban poor funds.(9)

By the end of 2017 there were only four federations in the SDI network that had demonstrated an ability to deliver land tenure, service provision or housing projects, and at the same time recover costs and even generate surpluses. These are the South African, Namibian, Kenyan and Indian federations. In all four of these countries, the finance facilities carry project portfolios that comprise learning projects, precedent-setting projects and cost recovery projects. Their urban poor funds are moving steadily to a point where they are financially sustainable and at the same time continue to achieve their social and political outcomes on behalf of their membership – the very poor. Federations in Zimbabwe and Uganda are not far behind. All other SDI groups that get involved in projects that contribute significantly to outcomes such as enhancing livelihoods, health and safety, and the strategic influence of the poor, continue to have overall rates of recovery that fall short of 100 per cent. The major challenge for these affiliates and for SDI as a whole is to continue to raise capital for these projects that are increasingly effective in achieving socio-political and socioeconomic outcomes but unable yet to be financially sustainable.

As of 2017 there are no formally constituted and fully functional city funds with active participation from SDI federations.

VI. Enter the Urban Poor Fund International (UPFI)

SDI is built on a federal model that places a premium on subsidiarity. In its early years it was little more than an instrument that enabled transnational learning between grassroots organizations and created a voice for the urban poor in the international urban development arena. It was only in 2002, six years after it was first constituted, that SDI began to provide its affiliates with small capital injections for projects that they themselves had prioritized. These funds took the form of flexible grants that were designed specifically to build and strengthen federated communities through the upgrading of slums. From the outset, the SDI Secretariat began to develop a matrix for the measurement of these projects and for the local funds that financed and managed them. This matrix and the measurement it facilitates have become more robust over time, especially in 2017, as the Secretariat professionalizes and prepares a new four-year strategic plan, but the framework has remained unchanged. The development of systems of measurement for capital grants has resulted in the establishment of a new semi-formal formation that has come to be known as the Urban Poor Fund International (UPFI), which is wholly managed by the Secretariat’s financial and project staff.

As indicated above, SDI’s national affiliates operate in many different environments and produce different results. In terms of finance and organizational form, this ranges from community funds that aspire to become urban poor funds where projects are funded by pooled community resources and where low rates of capital recovery are most likely, through emerging urban poor funds where better rates of recovery are secured through a blend of repayments and leveraging of external funds, to mature urban poor funds where 100 per cent capital recovery is possible. One hundred per cent capital recovery generally does not happen at scale if the state does not provide subsidies.

Because mature, emergent and aspiring federations have different expectations of capital recovery, in the aggregate, the Urban Poor Fund International has never been expected to recover 100 per cent. From 2007 to 2014 there was only one strategy to stabilize the national funds: net cash outflows had to be matched by inflows from donors.(10) SDI felt that it would be able to secure further inflows from donors because its investments in local funds would:

Produce many deliverable outcomes – e.g. houses, toilets, land tenure

Generate impact through changed relationships with government, policy changes, and improved climates for pro-poor initiatives

Leverage funds from other sources – such as communities, governments, international agencies and private capital

Demonstrate potential to go to scale by spreading to new environments, building new partnerships and having the methods replicated by other actors

However, a number of external factors (including a development assistance environment that has become increasingly prescriptive, demanding financial sustainability above all else) have compounded the central challenge facing UPFI. This has been to make inflows match outflows while still focusing on ventures that serve the poorest of the poor and therefore usually have a gap of non-recoverable cash.

“To keep the fund solvent even while putting capital into projects with non-recoverable costs is SDI’s central management challenge” [SDI Secretariat (2008), UPFI Strategic and Financial Plan].

The good news is that increasingly the local urban poor funds are financing urban improvement projects that: (a) maintain self-governance and autonomy, (b) draw local government in as co-producers, (c) impact on institutional arrangements and state policy, and (d) meet the challenge of making financial inflows match outflows.

How is this done? What happens to projects and local funds where 100 per cent capital recovery from local residents is unlikely? How does SDI continue to secure and distribute capital for its aspiring and emerging funds whose project portfolios have gaps of non-recoverable cash? How does it avoid the pitfall of trying to force these projects to make inflows match outflows, as all financial institutions, including housing microfinance agencies and a growing number of donor agencies, demand?

This is where UPFI has come into its own. It enables a mix of distribution that is adjusted on the basis of repayment results and available ongoing inflows. In other words, mature federations and their finance facilities, with portfolios that have 100+ per cent capital recoveries, are able to subsidize non-cost recovery projects in aspiring and emerging federations. It is expected that this cross-subsidy will also take place at the national level where, in some cases, financially viable projects already compensate for projects in which full cost recovery is not possible.

UPFI “spends” are structured as equity rather than loans. This means that the capital or cash recovered flows from the recipients (savings collectives) back to the local urban poor funds,(11) and is maintained there. Notwithstanding the reporting challenges, this is a constructive development in keeping with SDI’s commitment to devolution. UPFI’s end goal therefore is to have seeded a series of national urban poor funds (UPFs) that are autonomous and self-sustaining. Using an equity model rather than framing flows as debt is more than mere vocabulary. It goes to the heart of the relationship between UPFI and its national UPFs, and between SDI and its affiliated federations. Savings collectives are not beneficiaries and national urban poor funds are not financial intermediaries. They are partners, and UPFI becomes successful as each national fund becomes successful.

The challenges of international currency transfer mean that a physical flow of equity between affiliates is currently a rare occurrence and is likely to remain that way for some time to come. However, as far as a composite (UPFI) balance sheet is concerned, the intention is to aggregate both socioeconomic and advocacy performances and actual rates of financial recovery. SDI is now developing the systems and procedures to track and measure the capital investments it makes through UPFI to its national urban poor funds and to SDI’s desired outcomes, both tangible (e.g. houses, toilets, houses) and less tangible (e.g. new partnerships, advanced livelihoods, health and safety). Many of the variables are complex, especially when it comes to measuring material value, and this complexity is compounded by contextual differences between affiliates.(12)

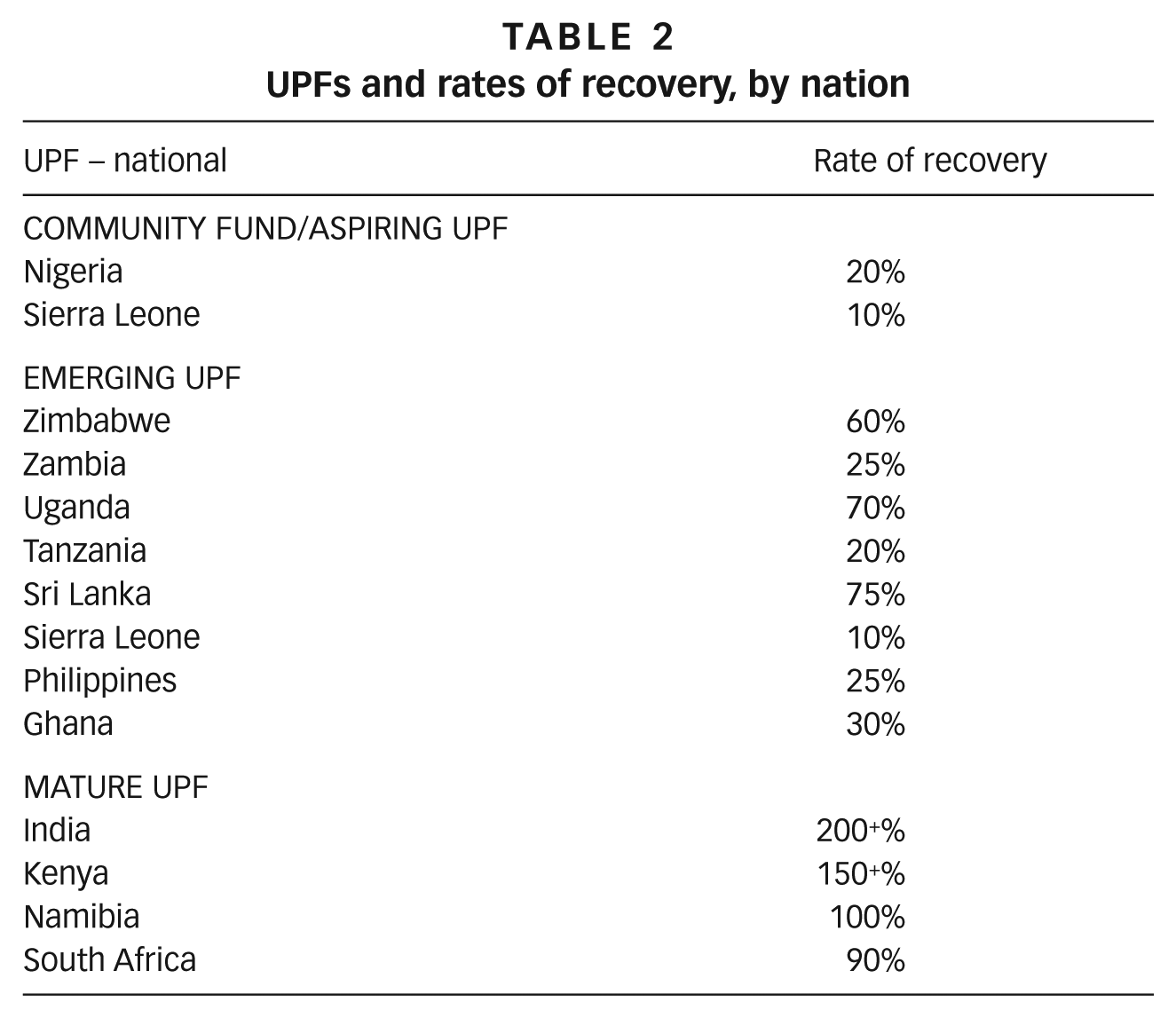

Even at this early stage, the information on capital returns makes for interesting reading. Table 2 is a very basic presentation of the rates of recovery of active local funds that are linked to UPFI.(13)

UPFs and rates of recovery, by nation

VII. Measuring Success

SDI is able to state that UPFI is something new, or at any rate that it is not a housing microfinance institution writ large; rather, it is a unique member-driven, cross-national capital pooling and capital sharing network of cohesive member organizations. Being member-based, it uses its money for investment, in the form of “commitments” to its network partners rather than microfinance loans provided to customers on a commercial basis. This difference cuts across both practice and language. Returns on investment do not necessarily take monetary form (either dividends or profits). They primarily take the form of capacitated communities; project replication through trans-settlement and trans-border learning; and policy and attitudinal changes amongst governments and donor agencies (sometimes leading to the provision of capital on a different basis to slum dweller organizations).

Every expenditure that is channelled through UPFI and its national urban poor funds is therefore part of a larger long-term housing strategy for SDI and its affiliate federations. SDI recognizes that change does not happen in equal steps but via a series of actions, each of which moves toward a larger goal. Scale, impact and leverage at national UPF level are not achieved in equal increments but as a result of a breakthrough event, and the conditions for responding to this have been prepared by previous events deriving from previous activities.

Each national UPF now measures the success of all its projects on the basis of a rate of recovery while also reporting on its social returns. National urban poor funds are at different levels in terms of their overall performance and their recovery levels. Aspiring and emerging local urban poor funds will have net cash outflows. Mature local funds will match outflows with inflows. UPFI is expected to stabilize when its outflows to its national partners are linked to recovery shortfalls. All local funds will be measured against their progress toward self-sustainability, but within an operating framework that ensures that they simultaneously strive to build the federation’s capacity to address the shelter needs of its members, the majority of whom are in the lowest economic quartile in informal settlements. This means that cost recovery, especially in the form of individual debt repayment, is but one indicator by which to measure national urban poor funds’ success. In each situation, the federation and its UPF (and therefore UPFI overall) will be assessed by its:

Political impact and clear indication of trends towards pro-poor urban development – especially at city level

Increased instances of tenure security, basic services provision and affordable housing delivery

Increased capacity to use UPFI funds to leverage public and/or private capital investments in slum upgrading

Strengthened affiliate capacity to become trustees of funds that recycle monies at the national level

Ability to develop a decentralized capitalization model, where information flows freely across borders so learning accelerates everywhere, while capital flows internationally through UPFI to the UPFNs, where it is recycled

VIII. Conclusions

We live in a world where capitalism dominates every aspect of our lives. This goes beyond dependence on markets as a means of interpersonal transactions, the modality by which resources are secured and redistributed, and the logic by which we secure our basic needs. Money has been rarefied such that financial worth is seen as an indicator of social value, social status and good citizenship. Arguments to the contrary notwithstanding, markets are no friends of the urban poor. However, it is deluded to ignore the power that capital provides to those who use it for their own ends. Land capital and other forms of value in the market can play a role in dealing with the causes of poverty by helping communities finance their own solutions to their tenure and housing problems.(14) In most countries SDI affiliates have begun to grasp this reality.

At the same time, it is important to recognize the dangers that market-based tools can present to poor communities, and to understand how to use more conventional formal systems of extraction and accumulation without damaging the collective accountability of communities and the informal systems they use to deal with these very exclusionary market forces. If this can be accomplished through the innovative financial instruments described in this paper, then SDI could point the way to the upgrading of slums and cities at a significant scale and in a manner that includes the poor instead of pushing them politically, economically and spatially to the margins.