Abstract

This paper presents the findings of a two-year study of community finance systems (including community-based savings and loan groups, and larger city-based funds) that are operated by established urban poor community organizations in five Asian countries (Cambodia, Nepal, Philippines, Sri Lanka and Thailand), with support from their partner organizations. These five groups are the principal national urban poor organizations in their respective countries, and their community savings and city funds – as well as their other development initiatives – have all grown to national scale. The study, in which the chief researchers, data-gatherers and analysts were community members themselves, was managed by the Asian Coalition for Housing Rights (ACHR). It was conceived as an opportunity to look in greater detail at the different models of community finance these important groups have developed, in their very different national contexts, and to compare their various aspects, draw out some key elements and lessons, and see how these people-driven finance systems can be strengthened, scaled up and brought into the formal finance and development structures in their countries.

Keywords

I. Introduction

Half a billion people now live in informal settlements in Asian cities, and their numbers are increasing. Conventional systems of finance – public and private – are not reaching these families, and without access to loans, they lack the means to address their needs.(1) What little formal finance has reached them, through government programmes and microfinance schemes, has followed the top-down mode of conventional banking, which does not enable low-income households to work out solutions as a group. The community savings and fund process in Asia has grown over the last 30 years into a large movement that challenges these practices and shows that the vacuum left by commercial and government formal finance can be filled. Community finance offers low-income communities important financial tools to address both their individual and collective needs.

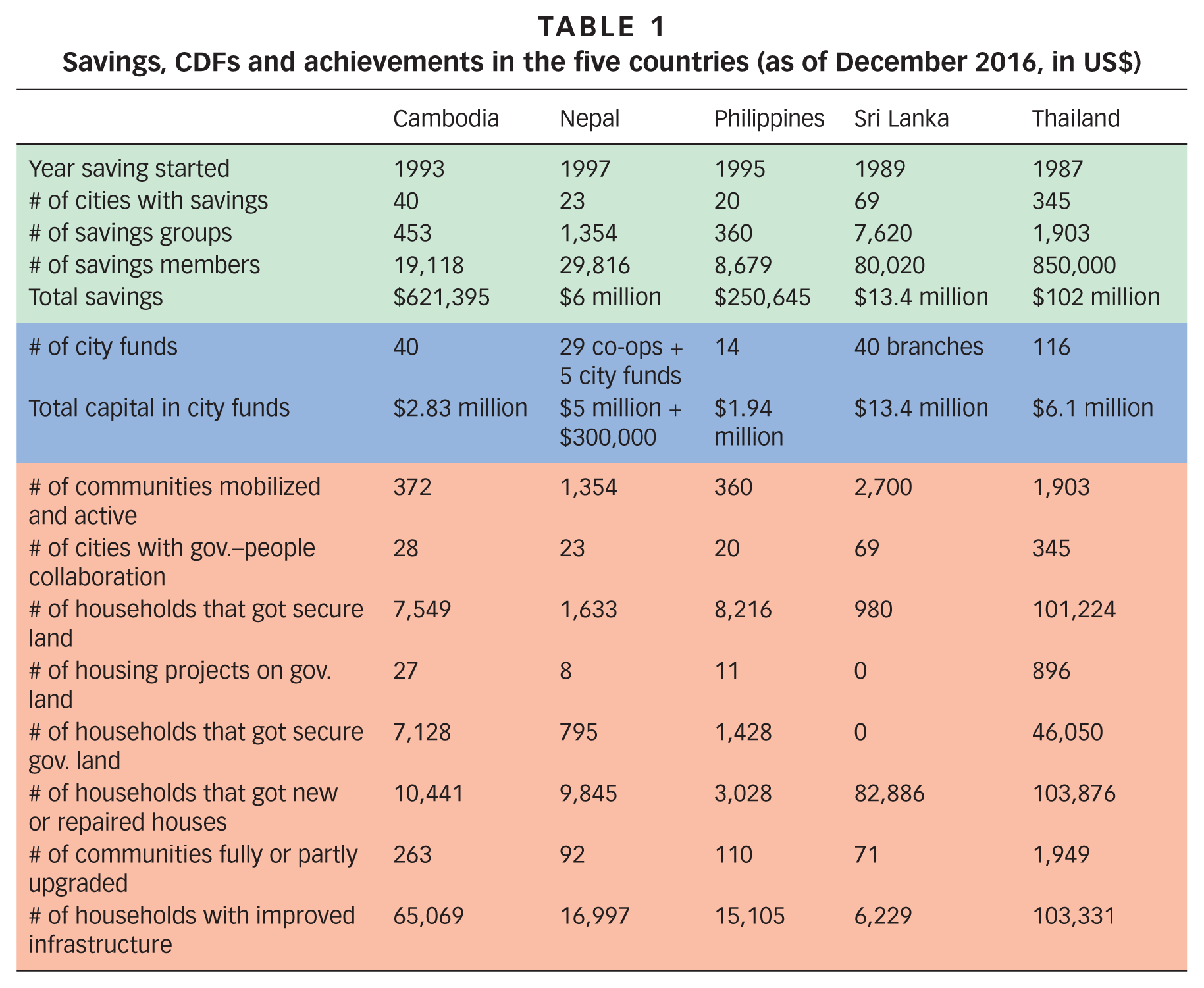

This paper presents findings from a study of community finance in five countries: Cambodia, Nepal, the Philippines, Sri Lanka and Thailand.(2) These examples have been selected because of their depth (period over which this has taken place), breadth (number of communities involved) and diversity of approaches (Table 1 on page 4).

Savings, CDFs and achievements in the five countries (as of December 2016, in US$)

Community finance provides a locally managed pathway to address poverty and challenge inequalities. In Nepal and Sri Lanka, community development funds (CDFs) and savings groups are managed entirely by women. In Sri Lanka, men are not allowed to join local groups, and the few who participate in Nepal may not make decisions. There are no gender restrictions in the Philippines, Cambodia or Thailand, but women significantly outnumber men here too.

Although four of the countries also have national funds, this study focuses mostly on the CDFs at city level – the layer that can bridge the enormous gap between informal urban poor systems and the formal world. These city funds emerged because of the limits to what small savings groups can achieve, especially when addressing housing needs. Housing requires larger-scale finance. City funds emerged after the creation of national funds in the Philippines, Thailand and Cambodia, but in Sri Lanka and Nepal, savings groups and CDFs developed simultaneously.

II. The Contribution of Community Finance to Development

Community finance is a process that includes both community savings groups (i.e. local self-managed savings and loans within a small social group or settlement) and larger community funds, which combine the monies of more than one savings group and may include capital contributions from development agencies and/or government.(3)

Community finance enables low-income communities to be pro-active, exploring, testing and developing solutions that work for them, rather than depending on government and/or NGOs. The savings these groups collect may not be sufficient to address all their needs, but it builds a community’s collective identity and development capacities, and enables it to leverage additional resources from government.

Community finance brings people together to design and manage a collective resource, with engagement, discussion and learning. The small sums they regularly save together grow into a larger financial pool that allows groups to leverage other resources and to secure and manage investments in housing, infrastructure improvements or community enterprises. Community finance provides groups with access to much-needed loans on terms they agree to, in an immediate, flexible, unbureaucratic process that allows communities to craft concrete solutions, without waiting for anybody’s permission. As membership and collective financial strength grow, funds form first at settlement level, and then at the city scale. These city funds strengthen the power of their member communities to negotiate with the state, landowners, professionals and commercial banks, and to address the larger structural imbalances in their cities, from the bottom up.

Community finance is very different from microfinance, and it is different from the multitude of small-scale savings initiatives that exist in low-income communities.(4) It begins with the collective. Local groups pool their small savings and decide together how to use those funds for various purposes. As the saving continues and loans are repaid, their internal fund grows and their lending power increases. Other benefits also emerge – bonds of friendship and stronger capacities to resolve problems collectively and care for weaker members. The collective financial capital strengthens the group’s social capital, and the two grow together. This collective aspect is not present in microfinance, where reliance on individual loans reproduces the vertical, bilateral relationships of conventional banking, between the provider and individual borrower. Even when microfinance includes savings and uses peer groups, the focus is on making sure repayments take place, not on collective priorities or the larger structural issues that cause poverty and exclusion. When the goal is finance for low-income people, if only individuals are considered, there is the risk they will fall victim to the larger system where competition is the rule, and where they cannot compete. The real wealth of low-income people is their collective wealth – not only their pooled finance, but their collective thoughts, ideas, protection, mutual support and negotiating clout. Access to finance has to go with this collective process and has to build on that collective wealth – the two things go together.

As city-wide CDFs have emerged, the contribution of community finance to development has become clear. Community finance:

a. What has been achieved to date?

Community finance systems in Asia have channelled housing and land loans, infrastructure subsidies and small grants to low-income communities, enabling them to upgrade housing and basic services like roads, drains, water supply, streetlights and playgrounds.

III. Methodology

Since 1989, the Asian Coalition for Housing Rights (ACHR) has been a key supporter of Asia’s community finance movement, providing a regional learning platform, helping to strengthen and scale up community finance activities in 19 countries, and supporting key groups to refine their process and diversify their activities.(5) ACHR has also supported city-wide informal settlement upgrading using CDFs. This paper summarizes an ACHR study that had the following objectives:

To gather detailed information about people-driven finance systems in several countries

To build the capacities of low-income communities and their support organizations to understand, support and build their community finance systems

To increase understanding among stakeholders in the formal financial systems about the vital role of informal financial systems

To link these community finance systems (particularly city-based CDFs) with larger-scale formal finance, so that community-driven development can scale up

The five study countries were identified through discussions in regional meetings and with the agreement of other groups. Selection criteria included: country-wide scale, with CDFs operating in many cities; implementation of some city-wide upgrading or housing development, using CDFs as the financial mechanism; and the existence among the five countries of a range of strategies and organizational structures.

In 2015, representatives from the five study countries met to discuss the objectives, methodology and process of the study. Study teams in each country were set up, with a coordinating team at the ACHR secretariat. Teams from six other countries joined this meeting as observers. In October 2015, the five country teams met to share their contextual analyses. A survey questionnaire was drafted and finalized to help standardize the information collected in the chosen cities. In August 2016, 40 community leaders and representatives from their support NGOs (from the five study countries and seven other countries) explored the findings that had come up so far, and discussed how community-driven finance could best contribute to Asia’s community movement. Country teams then finished their surveys and reports, and the core team chased final data, distilled key points from the five countries and completed the final report in February 2017.

Most work on this study – organizing meetings, filling in questionnaires, gathering survey information – was done by community members in the five countries, with support from their NGO partners. As in another ACHR study on poverty lines,(6) the rationale was that the people who manage and use Asia’s community funds are the real “experts”. This study was an opportunity for these community researchers – and their organizations – to collectively examine the finance systems they manage, document their knowledge, and open up new areas of exploration for refining and strengthening these systems. The interaction between city and country teams, interrogating each other’s findings, added rigour to the process. This study adds to a growing body of analysis and reflection on different aspects of poverty by the urban poor themselves.

IV. What has been Learned?

a. Savings groups – the collective processes that come with the money

All five countries have tackled the question of how large an ideal savings group should be. The Women’s Co-op (originally called Women’s Bank) in Colombo says that 5–15 is a good size for sitting together, discussing and making decisions. There are important strategic reasons for savings groups to be settlement-wide, but they can grow large and unwieldy. In Thailand and the Philippines, large settlements have been divided into a number of savings sub-groups of 10–20 members living close to each other. In Thailand, these sub-groups often operate as independent savings groups and undertake other development activities.

All five countries recognize that meetings are more than just occasions for savings and loan transactions. They also bring people together to share news and build solidarity and social strength. Weekly savings meetings have always been compulsory for all members in Sri Lanka. The more pluralistic systems in Thailand, Nepal, Cambodia and the Philippines have resisted strict rules and let local groups decide how often to meet. Almost all meet at least once a month.

The grandmothers of Asia’s savings movement, Mahila Milan in Mumbai, started their first savings groups among women living on pavements in Byculla. Daily door-to-door collection by each savings group leader made it easier for these women, all daily workers, to save small amounts. It also allowed the leader to hear each member’s news, and convey problems and loan requests to the area resource centre. For many Asian savings groups, these Byculla Mahila Milan members were their first teachers.(7)

When the Women’s Co-op began a few years later, members brought their savings to small group meetings every week. Those meetings were a lifeline for women who had been isolated by poverty and drained of confidence – a chance to talk with friends and peers, hear each other’s troubles, pass on neighbourhood gossip and offer each other moral support, along with small loans.

Over the years, groups in Thailand, Cambodia and Nepal found that combining frequent savings transactions with regular meetings helped build the group’s solidarity and power. They moved almost seamlessly from talking about savings and loans to talking about land, housing, settlement upgrading and welfare. In Thailand, which chafes at rules, some groups save during meetings, some drop off the savings at the community office, and some collect from members door-to-door. In the Philippines, most members just drop off their savings at the community office or the treasurer’s house.

Many groups agree that rules about minimum savings amounts can be a healthy discipline and motivation, but that minimums must be low enough to match varying earning patterns and leave nobody out.

b. The organizing logic and structures of inclusion

Like the savings and credit systems, the CDFs follow one of three forms: they may be area/settlement-based, membership-based or issue-based. Different forms of collectivity embody different priorities and understandings of development processes (although the study groups recognized that different strategies can achieve the same ends, and that this was not a contest).

c. Lending purposes

As savings processes in these countries have matured and grown, all have added new savings options, to answer different member needs or for bigger projects in the community and the larger network. Many now have longer-term savings for housing (Philippines, Thailand), interest-earning savings accounts (Sri Lanka, Nepal), special savings for children and youth (Nepal, Sri Lanka, Thailand), savings as shares in CDFs or national funds (Cambodia, Philippines, Sri Lanka and Thailand), and savings in community welfare and insurance schemes (all five).

They have also added new types of loans, designed to fit the informal, non-standard lives of low-income community members, with flexible finance and as little fuss and bureaucracy as possible. CDFs that get “stuck” with a narrow range of loan products seem to face more problems. The more dynamic CDFs have developed innovative demand-driven savings and credit lines:

In Cambodia they offer loans that boost the incomes of low-income families living on the semi-rural outskirts of cities by developing individual and collective farming, fisheries and animal-raising projects, as well as informal transport businesses in underserved areas of the city.

In Nepal the cooperatives give loans to women to build toilets and cover the costs of sending family members abroad for better employment. Members can save in a disaster management fund, which each cooperative can use in case of fires, floods or earthquakes. After the April 2015 earthquake, these funds provided immediate support to affected communities. The cooperatives also have welfare funds (for births and funeral rites), community development funds (for small-scale upgrading), and bad debt funds (for late loan repayments).

In the Philippines, savings and credit funds help disaster-hit communities to collectively repair houses and start earning again.

In Sri Lanka, there is a fund for relief work in flood-affected communities and to support development projects that include non-members.

In Thailand, the CDFs give loans for community enterprises, such as a communal rice farm and a bottled water plant.

The Thai study group distinguished among CDFs with only one activity (usually a welfare fund), those with two activities (typically a welfare and housing security fund), and those with three or more activities. Only those with three or more had growing membership, capital or activities. The very active CDF in Chum Phae had the fastest-growing capital and membership. Its activities included a livelihood loan fund for the city’s lowest-income families, a housing loan fund for families that could not access CODI(8) loans, a fund for resolving informal debts, three welfare programmes (for children, the elderly and everyone else), a housing insurance fund, a cement block-making factory, a communal rice farm, community enterprises to bottle drinking water and grow mushrooms, collaborations with the city, and programmes for children, youth and the elderly. Another top-scoring CDF in Bangkok’s Bang Khen District had a special fund for environmental protection, since many of its communities live beside a polluted canal, as well as a fund to help motorcycle taxi drivers buy their own motorcycles and start transport businesses.

The conclusion was that the more programmes a CDF offers, the more successful it is likely to be. This reinforced the fundamental understanding that a CDF is a tool to help community networks creatively address any needs that come up, not simply a source of finance.

Critical to developing innovative lines of credit is the organizational process. The Women’s Co-op has a system (“Everyone is a leader”) that makes every member of every savings group responsible for one of its “sector” programmes – health, education, culture, housing, children, welfare or accounting. Each “branch” (composed of 8–30 groups) uses part of the interest income – and member contributions – to run its own insurance fund, welfare fund, rescue fund and healthcare fund to provide free or subsidized medical care for members and their families. Branches also manage a national health programme (with their own hospital, mobile clinics and nurse training programmes), a life insurance programme, and a variety of advisory services for housing, land tenure, education and dealing with government agencies.

d. Collective or individual lending

While all decision-making is collective, the emphasis on collective lending varies:

Cambodia has a mix of collective and individual loans. Loans for housing, land, upgrading and livelihoods are usually managed by savings groups, but some loans (for toilet construction and agriculture projects) are to individual members.

In Nepal, loans for housing and group enterprises are made to groups, but most loans are made to individual members.

The national fund of the Homeless People’s Federation of the Philippines (HPFP) makes group loans for housing, land and infrastructure improvements, while loans for income generation projects, emergencies and other family needs are to individuals.

Loans from Sri Lankan Women’s Co-op savings groups and branches are all made individually to members.

Each CDF in Thailand sets its own rules, but all firmly agree on no individual loans. CDFs lend only to communities and networks, which on-lend to members, with the community or network managing the repayments. Thai CDFs also lend to other CDFs.

e. Structure of funds

Each country’s CDF system has developed its structure to accomodate particular aspects of its national context, and in some cases to follow formal financial sector regulations. There are three categories.

This decentralized structure facilitates the active participation of the grassroots women members, and the savings groups are very strong. Savings provide the only source of lending capital and the co-op does not borrow elsewhere or receive significant donor funding. In addition to savings and loans, the co-op provides other services as detailed above.

The federation provides a national and regional support system for the network of city-wide community networks and their city-based CDFs. It issues policies and guidelines about lending and operational issues, and staff from the centre and the regional ARCs visit cities to help with training and monitor debt collection. But the savings groups and CDFs set their own lending priorities, loan terms and conditions, and decide about fund management and project implementation.

In all three countries, loose national networks link the city-based networks and cooperatives for learning and mutual support. In Thailand and the Philippines, regional networks serve a supporting, linking and cross-learning function for the cities.

f. Management and decision-making

All the savings models keep savings in constant circulation in loans to members – not in a bank or a locked box – but money is managed differently. In Sri Lanka, Thailand and Cambodia, the small group savings stay in the group for internal lending. Only deposits made specifically for the branch (in Sri Lanka) or the CDF (in Thailand and Cambodia) go there. The savings group controls as much of its money as it chooses and decides who gets loans and on what basis. In Nepal, all member savings go straight to the five-ward cooperative, where loan decisions are made. In the Philippines, most savings groups, whether registered as HOAs or CAs, keep the savings in their association’s bank account, or keep part in the federation’s regional office.

The savings groups in Nepal and the Philippines follow rules and procedures imposed by government agencies. They are registered under the Cooperative Division rules in Nepal and HOA and CA rules in the Philippines. In Sri Lanka, the Women’s Co-op is registered as a national-level cooperative, but has negotiated flexibility for its internal rules and procedures, which are set nationally. Within this national framework, every savings group and every member takes on a decision-making role in some vital community development activity. In pluralistic Thailand, each savings group, community, CDF and network sets its own rules. Cambodia follows this looser model, but rules tend to follow a similar pattern.

Lending decisions also differ. In Nepal, they are made by a special loan committee in the cooperative, not by the savings group. A visiting team from Thailand found this system too centralized and asked whether it meant that savings groups lack power. The Nepalese explained that savings groups send their recommendations on loan requests to the cooperative committee, which usually follows them. Within the less centralized systems in Thailand, Sri Lanka and Cambodia, small group loan decisions are made entirely by members. Larger loan decisions using branch and CDF monies are made by the branch (in Sri Lanka) or the CDF (in Thailand and Cambodia).

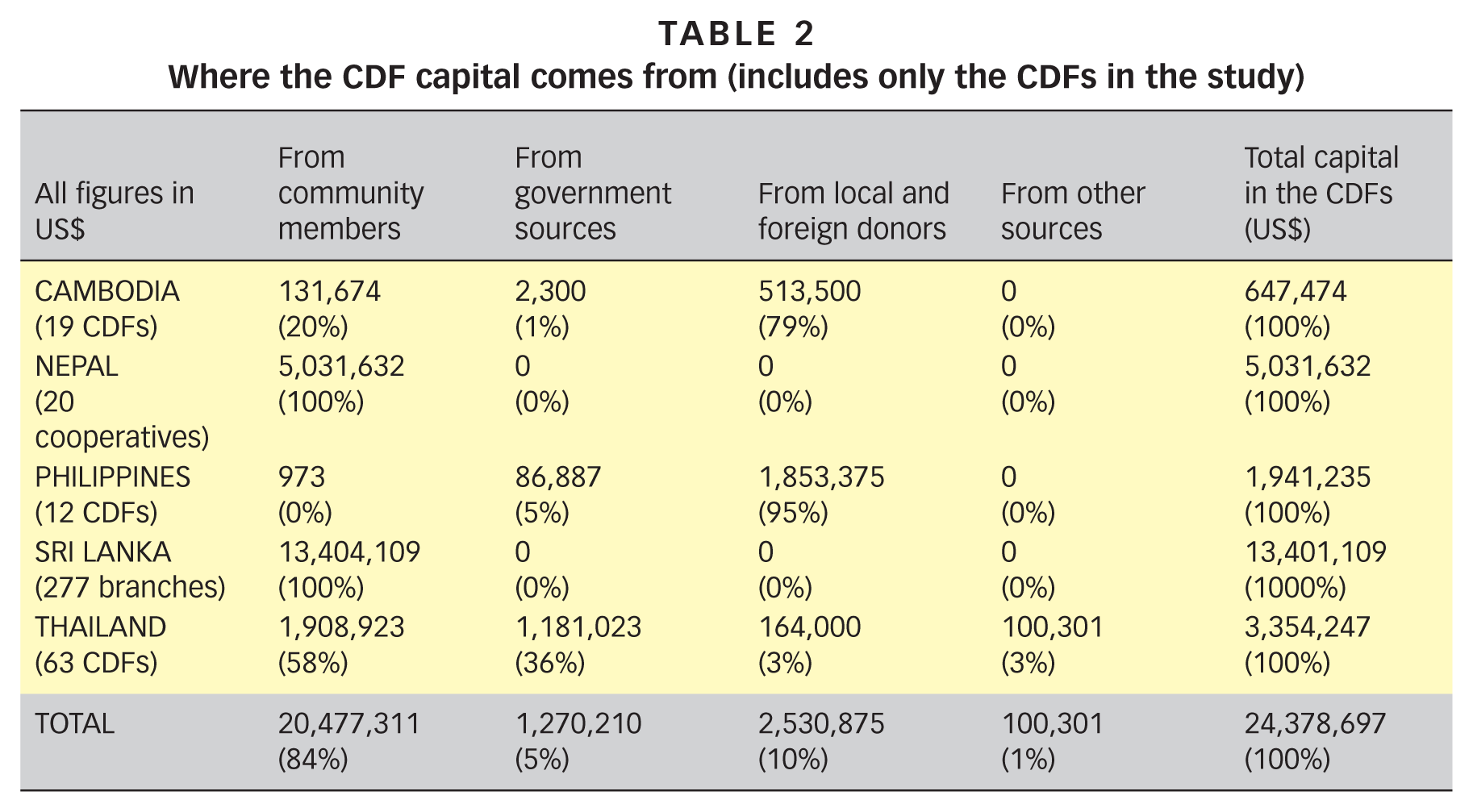

In both Cambodia and the Philippines, CDFs have received considerable grant funding for housing and upgrading in recent years (Table 2 on page 15), but they struggle with weak savings and lending systems and limited opportunities for members to participate in regular meetings and other activities. This easy, external project finance may have contributed to these problems.

Where the CDF capital comes from (includes only the CDFs in the study)

Cambodia

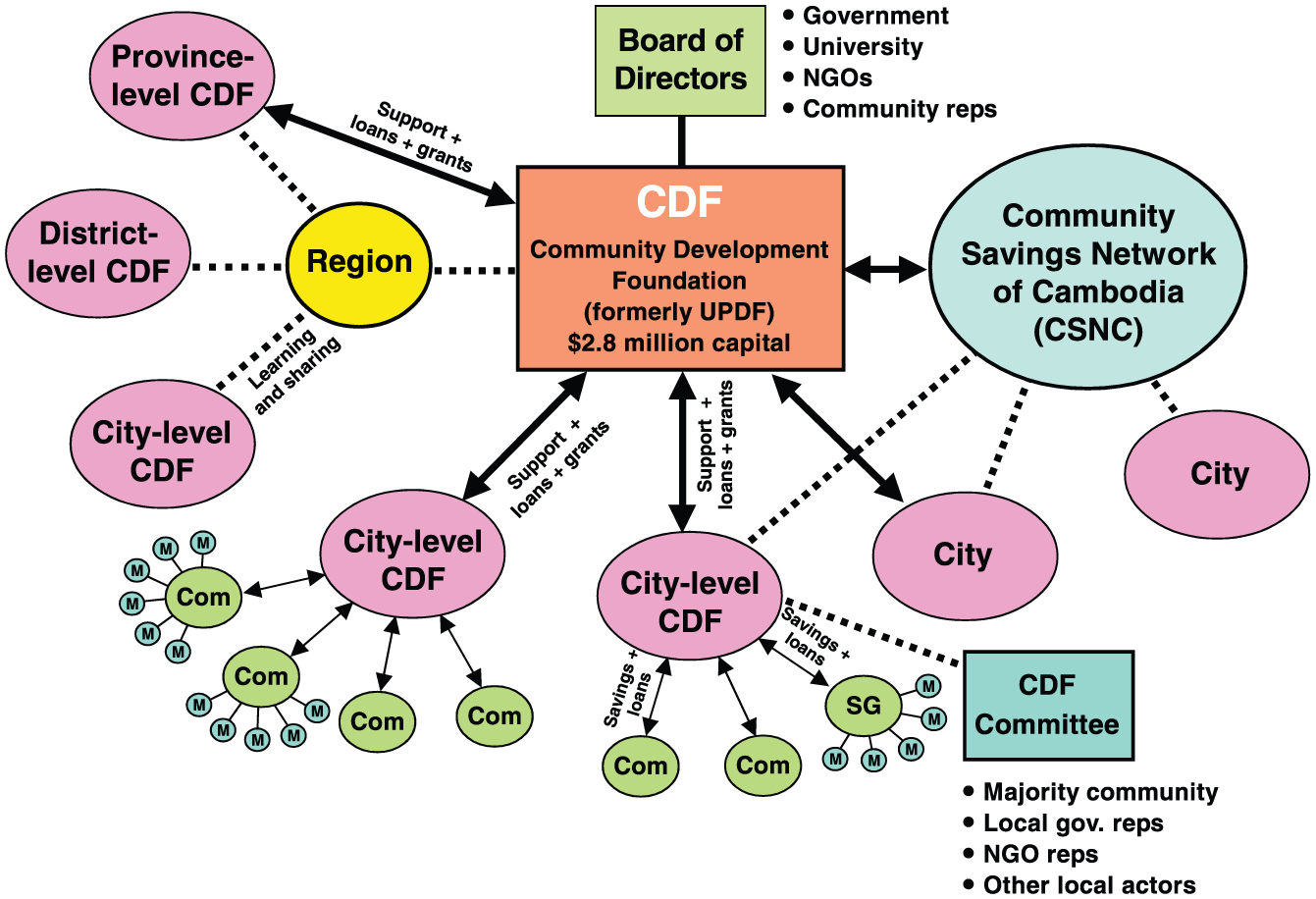

The CDFs in Cambodia link all the community savings groups in that city (Figure 1). The capital comes from community savings group contributions (shares and pooled savings), local government, the national Community Development Foundation and international donors. Each CDF sets its own rules, loan terms and lending priorities. Many CDFs try to build collaboration in their management structures and are managed by committees with a majority of community leaders, but also local government officials and other supportive local professionals and agency representatives. The CDFs provide a “bridge” between low-income communities and their local authorities, and catalyse and support collaboration on substantive issues like land, housing and infrastructure.

Cambodia CDFs

Nepal

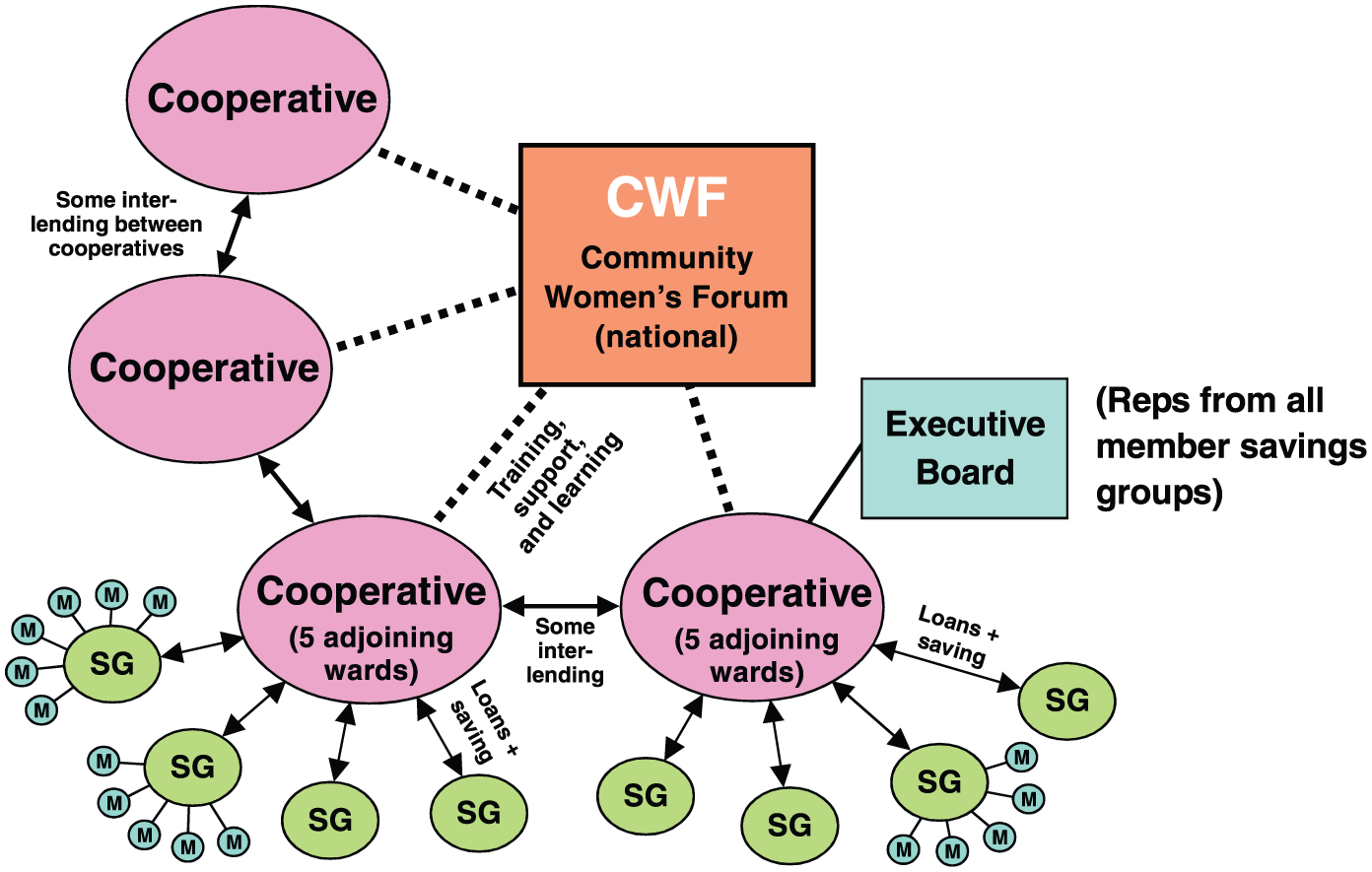

In Nepal, each women-led savings and credit cooperative pools all member group savings into a single revolving loan fund, which offers loans to members only on terms set by each cooperative (Figure 2). Savings groups choose a coordinator to collect the savings and loan repayments, and to coordinate with the cooperative. Each cooperative is governed by a board of representatives elected by the savings groups, and managed by three sub-committees responsible for education, accounting and loans, with an annual meeting for all members. Elections are held every two years, and an easily accessible office is located in the community. Beyond these government-imposed procededures, cooperatives are free to set their own priorities and lending rules. The cooperatives are independent, but do some inter-lending. Since 2007, they have linked together under the national Community Women’s Forum network, a learning and support platform.

Nepal saving & cooperative societies

The community savings are the sole source of capital for the cooperatives. Urban community support funds (UCSFs) operate alongside these cooperatives in five cities, and combine funds from local government, the cooperatives and donors, adding a more collaborative city-wide finance mechanism for the urban poor in those cities. The UCSFs, jointly managed by the cooperatives, local community organizations and the municipalities, have been used primarily to finance housing and land acquisition projects in communities facing eviction and involuntary resettlement.

Philippines

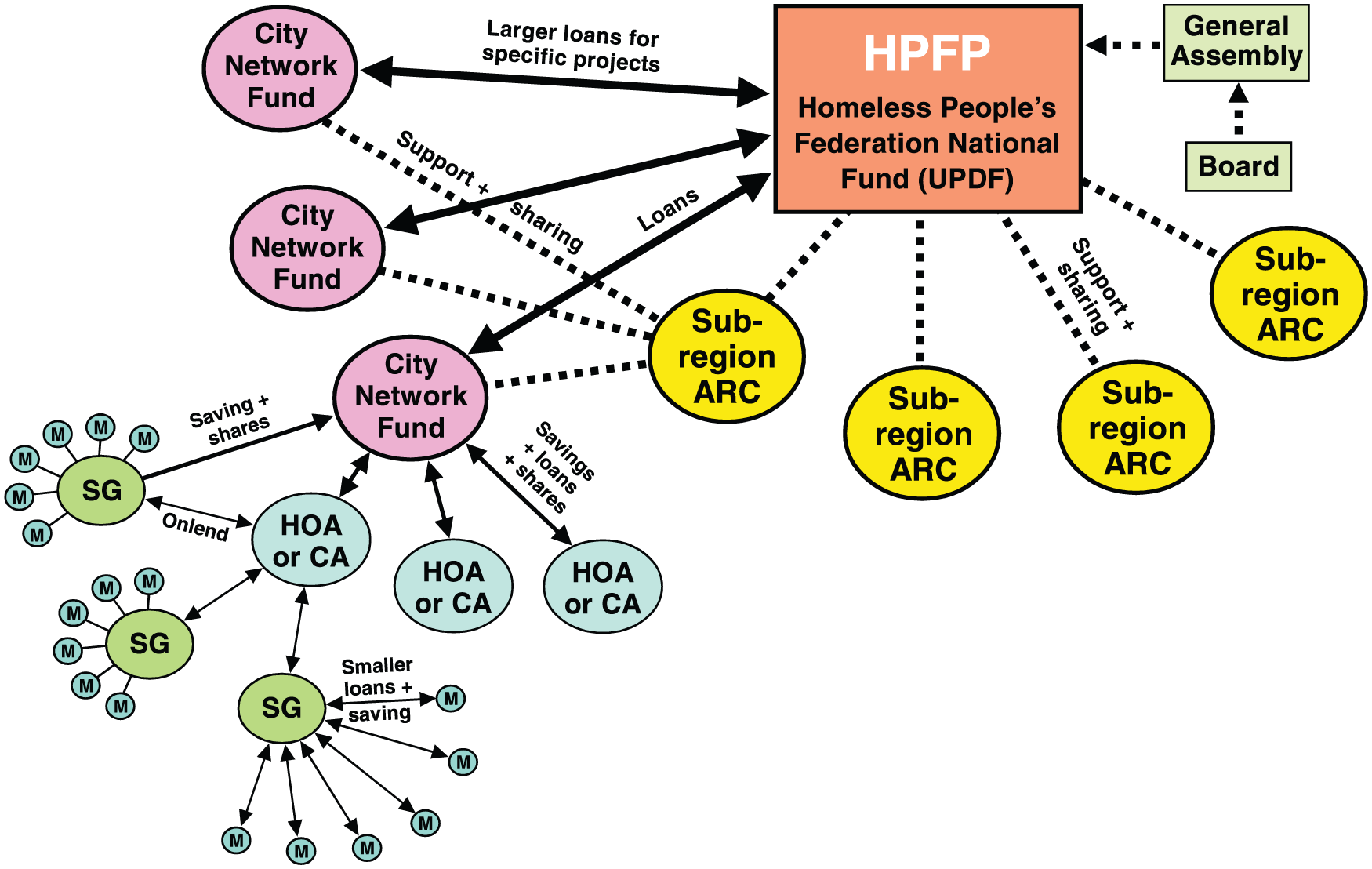

The CDFs in the Philippines (here called city network funds) are managed entirely by committees of savings group members who are part of the Homeless People’s Federation, which is divided into five regions around the country, each with its own federation office and with an area resource centre (ARC) in each city (Figure 3). The ARCs began as the points where all savings were collected and loans decided upon, but over the years, as communities took over the savings process, the ARCs evolved into points of assistance, information sharing and accounting support. Lending capital in the CDFs is drawn partly from shares and pooled savings from the member savings groups, and partly from donor funds earmarked for specific housing projects. The CDFs are financially and administratively autonomous. The national Urban Poor Development Fund, which provides an institutional umbrella for these city-based CDFs and channels outside funds to them, is managed by a board composed of federation leaders (the majority), with representatives from local government and the federation’s support NGO PACSII.

Philippines CDFs

SRI Lanka

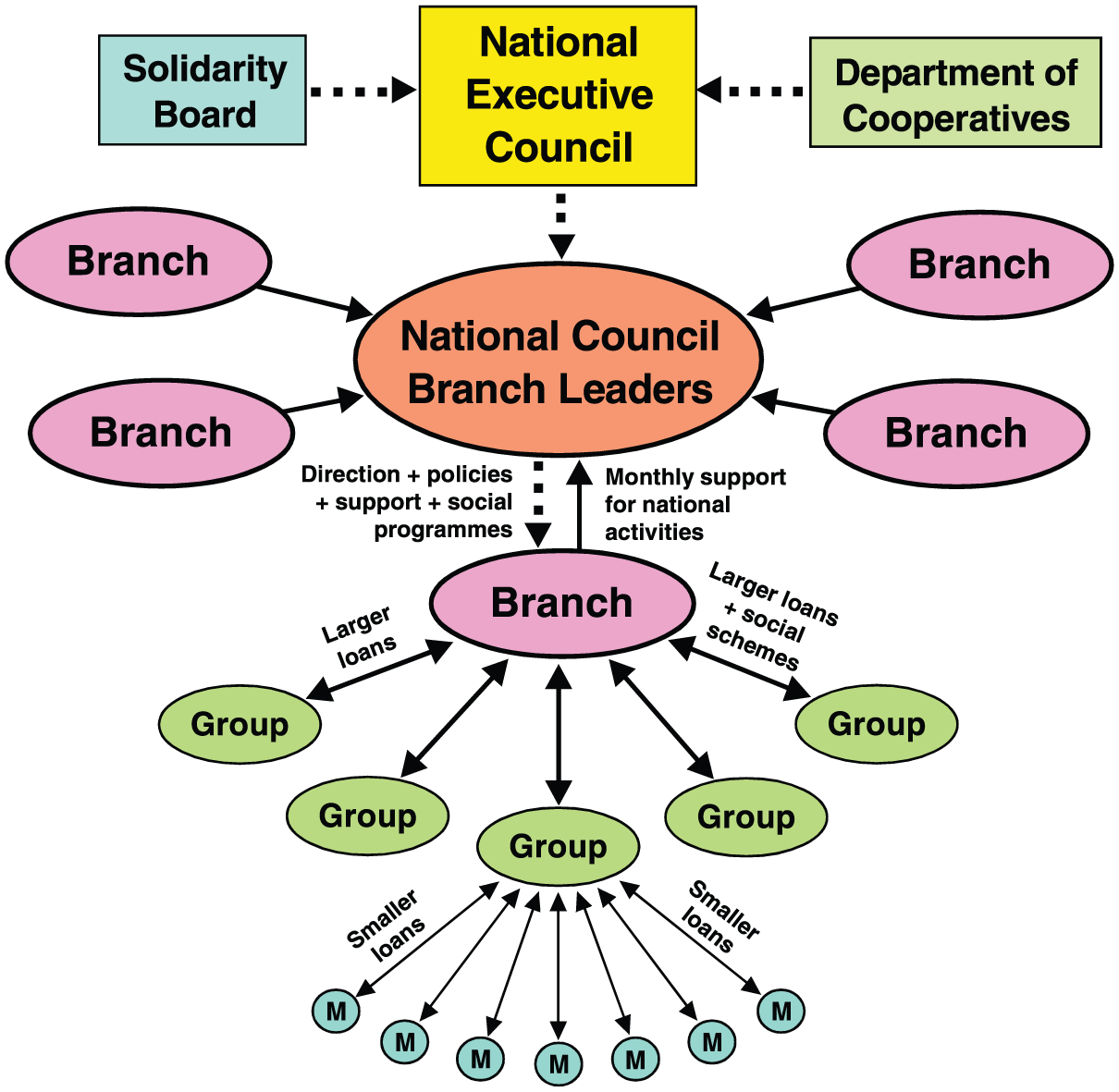

In the Sri Lankan Women’s Co-op system, the basic unit is the small savings group of 5–15 members, each of whom takes a leadership role in one sectoral task (Figure 4). Group lending decisions must be unanimous. Each group chooses a representative to the branch level, where these group leaders elect the management committee, which decides on branch-level loans and other matters. All capital is provided by members’ savings, some of which are kept within the group for internal lending. Larger amounts are sent to the branch, which operates like a larger revolving loan fund, as well as managing a variety of welfare and health programmes. Branches elect the National Executive Council, the decision-making body on policy and operational guidelines.

Sri Lanka Women’s Co-op

Both groups and branches have complete decision-making power over the money at their level, and no money leaves the branch. There is no centralization of the funds. The national leadership is funded by small monthly contributions from members.

Thailand

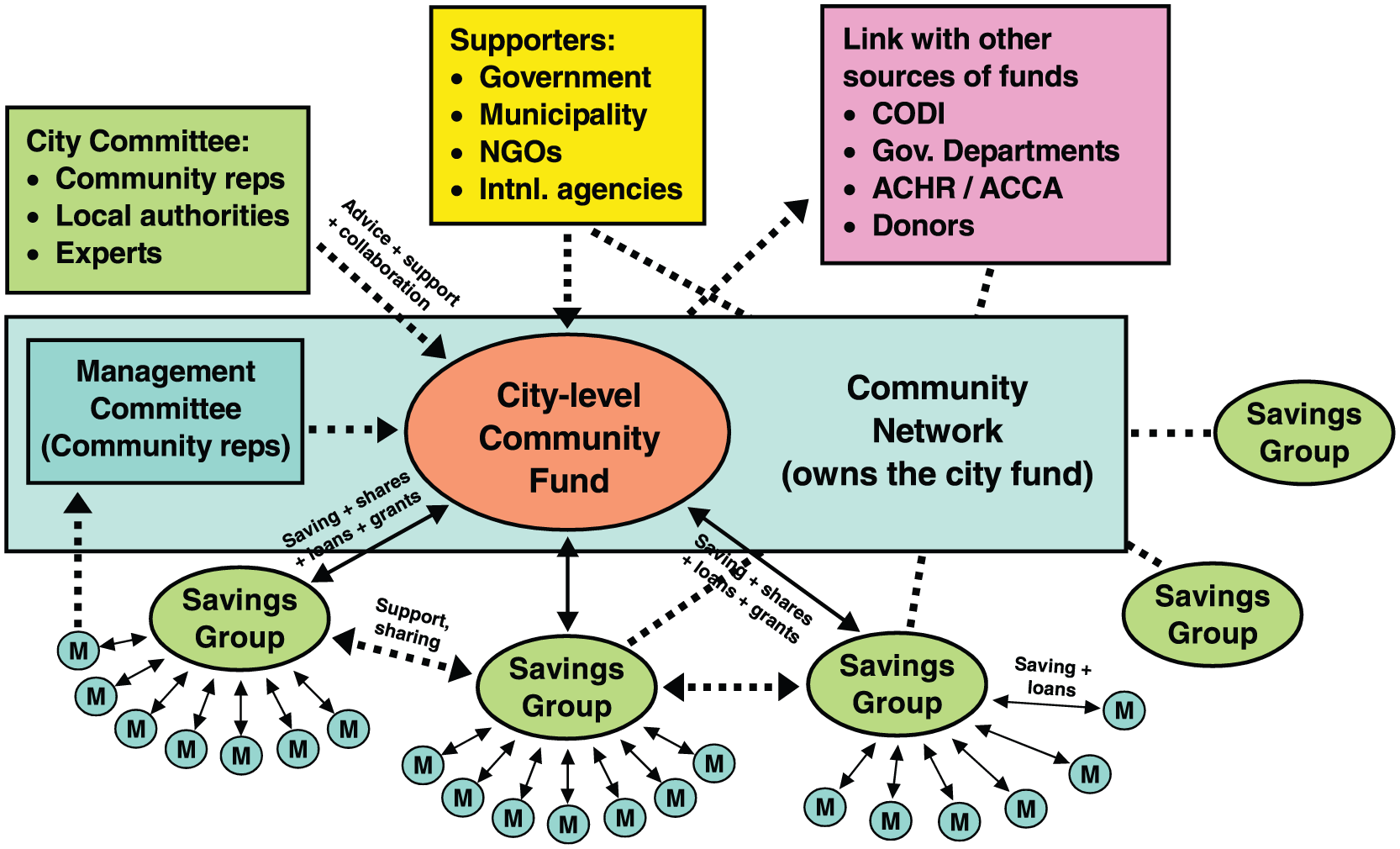

The CDFs are a recent addition in a country where one of Asia’s strongest, most progressive national government funds, CODI, has long been the main support system for Thailand’s community-driven development movement (Figure 5). The CDFs add a more autonomous and more city-oriented financial tool to that movement. Each CDF decides how to manage its operations, with decisions being made by local community networks and their member communities and savings groups. The CDF committee sets all regulations for the city fund, including loan priorities and terms and accounting procedures, and usually sets up sub-committees on housing, infrastructure, welfare, information and social issues. The lending capital blends savings and shares from member communities, donor grants and funds from CODI in the form of grants for welfare and insurance funds, and bulk loans for community upgrading projects and other purposes. There is no template for CDF operation. Each city network has complete freedom to manage its fund, according to the needs and conditions of communities in that city. As a result, each CDF is a unique community institution.

Thailand CDFs

Most cities with active CDFs also establish a parallel city committee, which includes network leaders (the majority), with representatives from the local government, NGOs, universities and other stakeholders. The city committee and CDF committee work closely together, and both usually meet once or twice a month. This two-part structure expands opportunities for collaboration and understanding, while preserving community control over the funds. In these ways, the CDFs, which have no legal status yet, are recognized and supported by the authorities.

g. How are activities funded and where does the money come from?

The lending capital in Nepal’s cooperatives and Sri Lanka’s Women’s Co-op branches is 100 per cent from member savings and shares – there are no outside funds. In Thailand, 58 per cent of CDF capital comes from community members (savings, shares, welfare and insurance fund payments), 39 per cent from CODI (seed grants for various purposes and bulk loans) and international donors, and 3 per cent from interest earned on loans. In Cambodia and the Philippines, by contrast, lending capital comes mostly from international donors (79 per cent in Cambodia and 95 per cent in Philippines), with much smaller contributions from community members (20 per cent in Cambodia and less than 1 per cent in Philippines), and from government (1 per cent in Cambodia and 5 per cent in Philippines) (see Table 2).

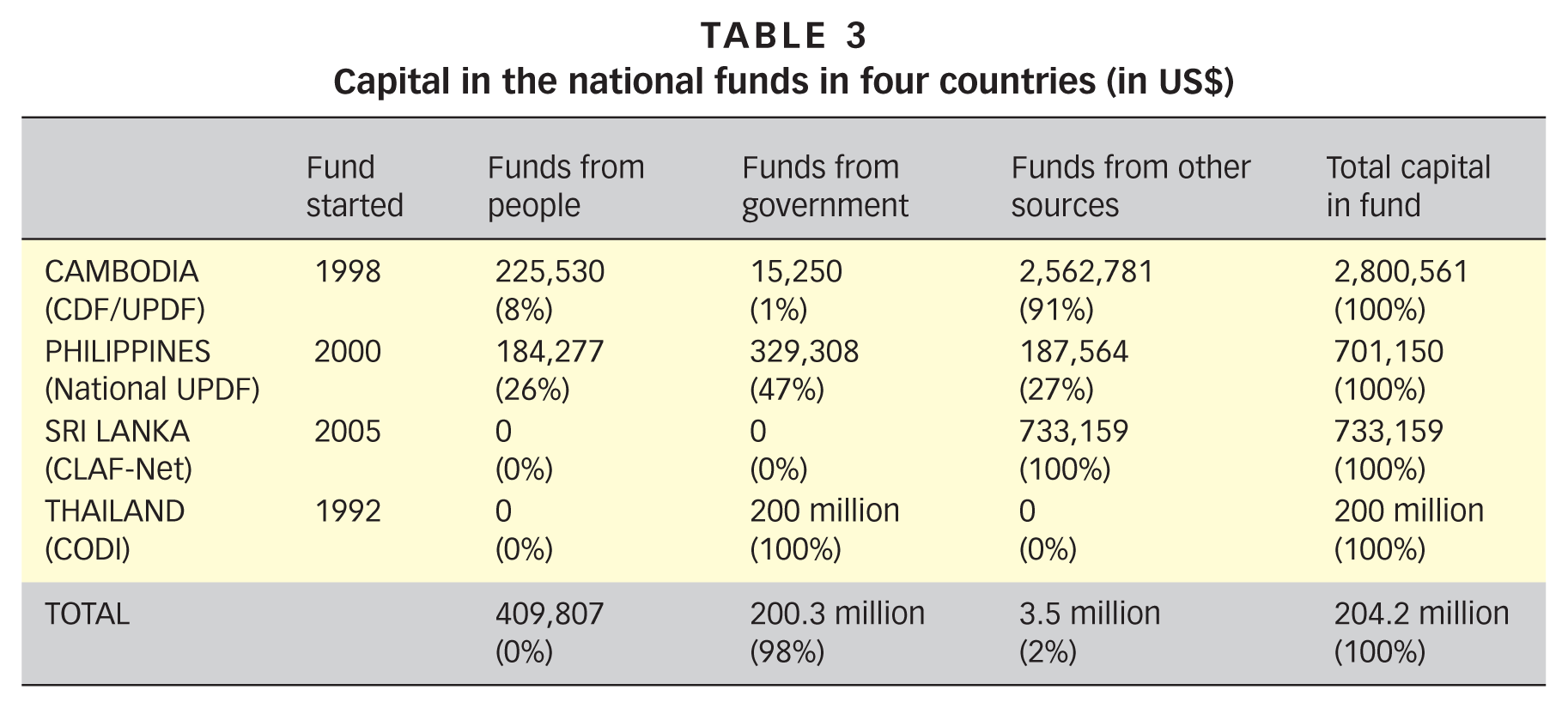

However, CDFs are only a part of this story. In four countries (excluding Nepal, where the national fund has only just gotten started), national funds also support savings group and city-level activities, including the CDFs. In Thailand, for example, the national fund CODI (which is a public government organization) is now actively supporting the city-level CDFs with seed capital grants and by channelling bulk loans to communities through them. In Sri Lanka, the national CLAF-Net Fund, which was set up after the 2004 Asian tsunami as a collaboration among ACHR, the Women’s Co-op and other local groups, initially gave livelihood and house repair loans to tsunami-hit communities. But later, with subsequent capital grants from ACHR and other donors, it began providing supplementary loans for housing and other purposes, mostly to Women’s Co-op members.

The sources and amounts of capital, for these four national funds, are listed in Table 3.

Capital in the national funds in four countries (in US$)

The more communities invest their own resources in their CDFs, the more ownership they feel, and the more motivated they are to save, repay loans and make sure their funds grow. A low dependency on other resources makes people more serious about their own resources. Sri Lanka and Nepal demonstrate this; they are 100 per cent self-funded, and have a 100 per cent loan repayment record, as well as fast-rising membership and savings.

When outside grant funding and outside-driven processes overwhelm community contributions, people lose their sense of ownership and responsibility, saving slows down, repayment problems grow, and the whole community-driven development process stagnates. We see this most dramatically in the two countries with serious loan repayment problems and declining savings membership, Cambodia and the Philippines, which also have the most precarious, donor-dependent support systems and the lowest level of community investment in the CDFs. Both countries have experienced crises recently as external donors held up funding for several years while NGO-level accounting and auditing problems were sorted out. At the same time, external grant funding for housing and upgrading projects was flowing into their CDFs. As a result, some very good housing and upgrading projects were planned and implemented, but activities for other members slowed down, morale diminished, savings plummeted, loan default rates zoomed, and the community movements in both countries lost ground.

Community finance systems across Asia are, of course, in great need of outside capital to allow communities to take their housing, upgrading and other development initiatives to scale. But these striking figures show us that a sense of ownership is essential if communities are to make best use of the CDFs they manage and to see them as vital tools in their own self-development.

Cambodia and the Philippines are struggling with considerable problems. But leaders from the other community movements are quick to acknowledge that they have gone through similar crises. Khun Prapaat, an experienced community leader from Bangkok’s Bang Khen District, offered this experience: “We faced similar problems in Bang Bua. There was corruption, the leader had problems, the community lost trust and stopped repaying their loans, everybody was fighting. It got very bad. So we asked the network to come help. At first, they did the same thing you are trying to do in the Philippines: the network leaders went around in person, collecting loan repayments from the members. After a while, though, they felt that wasn’t the right way and didn’t really understand the dynamics inside the communities. So they brought all the people into a discussion, to understand where the problems were, and to see how to reorganize the whole thing. After some time, the community people reorganized, resolved the problems and took charge again. And in the process, they brought their development to a new stage.”

h. Linking to formal systems and government

In all five countries, the savings began with purely informal groups, but in some countries more formal structures have now developed, such as the government-registered cooperatives in Nepal and Sri Lanka, which provide a legal umbrella for the savings and lending process. In Thailand and the Philippines, the savings groups that negotiate land tenure and plan their housing and upgrading projects have had to register as legal entities like housing cooperatives (in Thailand) or as homeowners’ associations and community associations (in the Philippines). This imposes rules and top-down structures that can frustrate and undermine people-driven and bottom-up community processes like savings, even if the savings are kept separate and informal, as in these two countries. The savings process in Cambodia – in fact the entire community movement – remains informal and untouched by regulation, but savings networks there have managed to collaborate with various levels of government and secure substantial amounts of land and resources for housing.

Closer engagement with government provides many opportunities,(9) but there are also challenges with formalizing a community process. The CDFs are an institutional mechanism that can bring communities and city governments together. This is crucial when it comes to low-income housing, which requires changing practices with respect to structural city issues like land use, zoning, basic services, building regulations and standards, service grids and house registration. When low-income communities upgrade their shelter to formal, legal housing, they engage with all these formal structures, which necessarily means engaging with state institutions.

The Cambodian study team found strong collaboration with local governments in most of the study’s 19 CDFs, many of them jointly managed. Community members bring local officials onto their managing committees, sometimes ceremonially and sometimes very actively, as in Serey Sophoan, where the mayor has long been a champion and supporter of the people’s process. Partnering with local governments is a key part of the savings networks’ programme, and has resulted in state contributions to CDF capital, free space in city halls for CDF offices, infrastructure investments and free government land in housing projects. Between 2008 and 2014, local governments gave land worth US$ 8.6 million to 15 of the 19 housing projects supported by the Asian Coalition for Community Action (ACCA) programme, which housed 3,407 low-income families. The national CDF fund has also worked closely with the Phnom Penh Municipality and for many years received monthly donations from the prime minister.

The Nepalese women’s cooperatives are run independently, but register with the government and comply with the regulations of the Cooperative Division. Nine of the 20 co-ops in the study reported that their local governments had supported their formation, and 10 reported improved government policies and attitudes towards the urban poor. But many reported early difficulties before positive relations were established.

All the Philippine Homeless People’s Federation groups have made efforts to link with local governments and include them in the development process. In some cities, relationships have become friendly and productive, and in rare cases, public land has been given free for urban poor housing projects, or public infrastructure projects started by communities have been continued by municipalities. One complaint was that government finances usually came only after projects had been implemented.

In Sri Lanka, as in Nepal, being legally registered has brought the Women’s Co-op’s savings and credit system under the government umbrella. In a way, this means infiltrating the government system with a bottom-up and people-driven system, and it has opened doors for negotiation and collaboration. In some cities supported by ACCA, like Nuwara Eliya and Moratuwa, local Women’s Co-op branches have worked with the local authorities and local NGOs to set up joint committees that meet regularly to find solutions for issues such as land tenure, eviction, basic services and housing. Nandasiri Gamage, who helped found the Women’s Co-op and remains its senior advisor, describes the organization’s strategy this way: “If you build a great big mill to manufacture something, everyone can see its size and its wealth and productivity. But if you make instead 1,000 small workshops, nobody can see them all at once, nobody can destroy them, and no politician can catch them. Women’s Co-op is like that.”

Although the Thai CDFs have no legal standing, many have cultivated good relationships with local authorities and have been able to leverage technical and financial support for their activities and projects. Each CDF is managed by a committee of community members and network leaders. Most cities with active CDFs establish a parallel city committee bringing together community and network leaders with representatives from local government, NGOs, universities and other supportive stakeholders. These committees work closely together and this structure expands opportunities for collaboration and understanding, while preserving community control over the funds. The Bang Khen District CDF has shrewdly invited representatives onto its city committee from several national government agencies with direct bearing on the district’s housing projects, but keeps the CDF under community management. The national government link is mainly through CODI, which has supported the CDFs all along with seed grants to start welfare and housing insurance funds; passing loan and grant funds for Baan Mankong housing projects for that city through the CDF; and giving bulk loans at 3 per cent a year to support whatever projects the communities in that city want to undertake.(10)

V. Conclusions: Constraints to Scaling Up These Community Finance Systems

The community finance systems described in this paper – from the small savings groups to the larger city and national funds – all show us that organized low-income communities can bring about enormous change in their own lives and communities and cities, cheaply, effectively and at scale, even with only modest amounts of finance within their control. And in the process, they show us a more human, communal and outward-reaching way to live together and support each other, in an increasingly harsh, lonely, individualistic world. But these unconventional finance systems face some big challenges on the question of growth, which these countries are struggling with in different ways.

Our capitalistic, individualistic ways of thinking and doing things are so potent that they often overwhelm the human and social aspects of community finance, reducing it to a strictly economic mechanism that only helps low-income households join the long queue of would-be credit customers. This may address their individual needs, but it misses the more significant, transformative aspects. Community finance makes people the subject, no matter how little money they have. By pooling people’s resources, it builds their financial strength and offers a set of flexible, powerful tools for realizing new development options. These tools are not only financial – they build upon the human qualities of people’s relations within their communities, strengthen social support systems, and allow people who are powerless as individuals to bring about change together. This is a richly social process and it begets innumerable individual and social benefits, which in turn empower, transform and improve lives in many other ways. By making people the subject – rather than simply the object of individual access to credit – community finance can play a significant role in reducing poverty and making our societies more equitable and democratic.

For community finance to deepen and spread, there is a need for legal structures to support, protect and legitimize this work, facilitating acceptance by and collaboration with the formal financial and governance systems. Different countries have different political contexts and legal systems. But in countries where there are regulatory structures governing cooperatives or credit unions, and community finance has sought to work within those structures, the experience has invariably been bad. These laws tend to impose structures that compromise and undermine rather than support people’s power to manage finance in ways that work best for their needs and that are appropriate to their realities. Unless the groups are strong enough to influence these structures to be more appropriate, they end up losing their own system and adopting the practices of top-down government structures. Can community finance expand its bottom-up systems and balance and negotiate its processes within top-down legal structures?

When a small group of people form a savings group, it is uncomplicated – everyone knows each other, and the scale is not too big. That allows the more human, democratic aspects to flourish. That is power from below. But when those savings groups link into larger funds and networks at city, regional or national levels, there comes a need for structures of representation, coordinating teams and leadership. Ideally, this leadership should facilitate the process in ways that allow the power to remain with the members and small groups, on the ground. But facilitating bottom-up power is no easy thing, and we have very few examples of how to do that. Again and again, we see that without any vigilant balancing mechanism, the coordinators start making decisions for the other levels; there is a tendency towards centralization, the bottom-up groups are weakened, and the whole process gets stuck. We live in an overwhelmingly top-down world, and our structures and models tend to take on top-down patterns. A similar imprinting takes place when community finance systems try to link with the larger system for resources and new possibilities – particularly the formal finance system. The cost is often the loss of freedom and the erasure of bottom-up power. This is the particular challenge of community finance, which should be a system that gives power to the people on the ground, so that they keep it.

Footnotes

1.

Solo, T M (2008), “Financial exclusion in Latin America or the social costs of not banking the urban poor”, Environment and Urbanization Vol 20, No 1, pages 47–66.

3.

Boonyabancha, S and D Mitlin (2012), “Urban poverty reduction: learning by doing in Asia”, Environment and Urbanization Vol 24, No 2, pages 403–422; also Mitlin, D (2011), “Shelter finance in the age of neo-liberalism”, Urban Studies Vol 48, No 6, pages 1217–1234.

4.

Satterthwaite, D and D Mitlin (2014), Reducing Urban Poverty in the Global South, Routledge, London and New York; also Boonyabancha, S, F N Carcellar and T Kerr (2012), “How poor communities are paving their own pathways to freedom”, Environment and Urbanization Vol 24, No 2, pages 441–462.

5.

See reference 2; also ACHR (2015), 215 Cities in Asia: Fifth yearly report of the Asian Coalition for Community Action, Asian Coalition for Housing Rights, Bangkok; and Archer, D (2012), “Finance as the key to unlocking community potential: savings, funds and the ACCA programme”, Environment and Urbanization Vol 24, No 2, pages 423–440.

6.

Boonyabancha, S and T Kerr (2015), “How urban poor community leaders define and measure poverty”, Environment and Urbanization Vol 27, No 2, pages 637–656.

7.

Patel, S and C d’Cruz (1993), “The Mahila Milan Crisis credit scheme: from a seed to a tree”, Environment and Urbanization Vol 5, No 1, pages 9–17; also Patel, S, A Viccajee and J Arputham (2017), “Taking money to making money: SPARC, NSDF and Mahila Milan transform low-income shelter options in India”, Working paper, International Institute for Environment and Development, London.

8.

CODI is a national government fund, the Community Organizations Development Institute, that offers support to savings groups through soft loans and grants for upgrading and other community-driven development initiatives. For housing and land loans from CODI, community groups must register themselves as housing cooperatives.

10.

Archer, D (2012), “Baan Mankong participatory slum upgrading in Bangkok, Thailand: Community perceptions of outcomes and security of tenure”, Habitat International Vol 36, No 1, pages 178–184; also Boonyabancha, S (2009), “Land for housing the poor - by the poor: experiences from the Baan Mankong nationwide slum upgrading programme in Thailand”, Environment and Urbanization Vol 21, No 2, pages 309–330.