Abstract

This article analyses how family firms, which constitute India’s dominant ownership category, compare with nonfamily firms in ESG (Environmental, Social, and Governance) goals adoption. To account for heterogeneity within family firms, we investigate the standalone family firms (SFFs) separately from a family business group affiliated firms (FBGFs). Results show that nonfamily firms perform better than family firms in overall ESG and E parameters. Within family firms, FBGFs perform better than the SFFs on S parameters. Our analysis urges the policymakers to create awareness, provide a roadmap, nudge the family firms, and promote action toward being ESG-conscious.

Executive Summary

The article investigates the adoption of ESG (Environmental, Social and Governance) practices among family and non-family firms in India, emphasizing the unique dynamics within family firms. Employing CRISIL’s proprietary ESG scores for 225 of India’s largest listed companies, the study reveals that non-family firms outperform family firms overall, particularly in environmental (E) parameter. Among family firms, family business group-affiliated firms demonstrate superior social performance compared to standalone family firms (SFFs), attributed to their resource availability, public scrutiny and legacy-driven motivations. The research also identifies foreign institutional investor (FII) ownership as a significant factor positively influencing ESG adoption across all firms. This suggests that FII presence encourages sustainable practices, aligning corporate behaviour with global governance standards. Despite their long-term orientation and stewardship values, family firms lag behind non-family counterparts, primarily due to a lack of awareness and structured approaches to ESG integration. The findings underscore the need for tailored policy interventions to promote ESG adoption, especially among SFFs, by addressing resource and knowledge gaps. The article calls for standardized ESG reporting frameworks to ensure transparency and comparability, enhancing investor confidence and driving corporate responsibility. It highlights family firms’ potential as ESG leaders, given their societal embeddedness and multi-generational perspective, urging immediate action to align their practices with global sustainability goals.

‘To create a better future we need to harness collective agreement to focus on net zero commitments. Our purpose is unequivocal in protecting both society and future generations from the consequences of climate change…This is inclusive capitalism in action—inaction is not an option.’ Michelle Scrimgeour, Chief Executive Officer, Legal and General Investment Management, Co-chair, COP26 Business Leaders Group. (COP26, 2021)

Deliberations and commitments of world leaders at the COP26 Summit held in Glasgow, Scotland (2021) indicate the seriousness of climate change and its consequences on the economy, society and survival of the earth itself. Climate change and concerns about the need for and process of protecting and sustaining society and the environment have grown multi-fold worldwide in recent years.

In addition to climate change, growing recognition for proactive response and prevention of long-term downturn effects of factors such as poverty, lack of diversity, corruption and pandemics on society have nudged corporations to increasingly adopt sustainability practices concerning risks broadly categorized under environment, social and governance (ESG). ESG risks are relevant for all. It impacts companies operating anywhere globally. The implications are porous, and the impact is gradual yet significant. As William Henry Gates III, co-founder of Microsoft, investor, author and philanthropist, said, ‘We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction’.

Therefore, all companies must play a role in developing a more sustainable society. Family firms have greater incentives and are better poised to take decisive action toward long-term planning of such risks. They generally have a long-term orientation, stewardship values, family members identifying with the firm, binding social ties and emotional attachment to the firm, with dynastic succession as one of their objectives (Berrone et al., 2012). Such characteristics automatically propel the family firms to care about sustainable practices. Further, their sheer numbers and dominance in most economies mean that their impact on the cause of ESG is also significant.

In this article, using the Ordinary Least Squares (OLS) regression technique, we analyse how family firms compare with non-family firms in ESG goals adoption, as measured by ESG scores developed by CRISIL (CRISIL, 2021). To account for heterogeneity within family firms, we also investigate the standalone family firms (SFFs) separately from family business group affiliated firms (FBGFs). Our results show that non-family firms perform better than family firms in overall ESG and E parameters. Within family firms, FBGFs perform better than SFFs in achieving social goals. Our results also show a positive relationship between ESG and FIIs Ownership in the firm. Family firms have the potential to lead in ESG metrics, yet, our results show that they have a long way to go.

WHAT IS ESG AND WHY MUST WE CARE FOR IT?

The birth of ESG reporting can be traced back to 2004, when the United Nations, in collaboration with the Swiss Government, launched the WHO CARES WINS initiative, which sought to integrate ESG into capital markets. Its report conveyed why institutions that were part of the initiative believed that considering ESG factors in investments would ultimately create more robust, resilient markets and better societal outcomes. The launch of the Principles for Responsible Investing under the late UN Secretary-General, Kofi Anan, in 2005 provided the framework for including ESG in investment decisions and sought to encourage investing for long-term sustainable development rather than short-term gains (United Nations, 2006).

The E in ESG depicts the inter-relationship between the activities of the company and the natural environment. It tackles the problem of climate change by evaluating various parameters such as carbon/toxic emissions, renewable energy, resource consumption and raw material procurement in an organization. It encompasses how the company affects or is affected by the environment. The S refers to social criteria covering all company stakeholder relationships, such as employees, customers and suppliers, through workplace policies, community embeddedness and CSR projects. It also addresses problems in labour relations, workplace diversity and more. The G refers to governance criteria, that is, the internal practices and procedures adopted by the company. It encompasses company management, board composition, board independence and shareholders. While ‘E’, ‘S’ and ‘G’ are measured independently, they are closely intertwined, and an action taken in any criterion also impacts the others.

ESG integration is ‘the explicit inclusion of ESG risks and opportunities into traditional financial analysis and investment decisions based on a systematic process and appropriate research sources’ (Duuren et al., 2016). The evaluation of a firm’s efforts towards ESG integration has become a predominant area of interest for socially responsible investors, who consider their values and concerns while making investment choices instead of solely considering financial factors. They like to optimize their financial returns while creating a net positive impact on society by integrating ESG factors into the decision-making process.

ESG reporting is believed to be a positive step toward achieving the 17 UN Sustainable Development Goals (SDGs) underlined by the Paris Agreement and Agenda 2030, which aims at creating a brighter, more sustainable future for our planet (Figure 1). According to Antoncic et al. (2020), a positive linkage between ESG and SDG footprint is entirely consistent with asset owners’ fiduciary duty of not sacrificing return opportunities for the future.

With socially responsible investing on the rise due to the increased awareness and sensitivity of newer generations towards problems like climate change and human rights, the ESG asset market is expected to grow to almost $53 trillion by 2025 (Bloomberg Intelligence, 2021). In fact, according to a report by CRISIL, the ESG market in India has already experienced an accelerated rate of growth, with the assets under management of the top 10 ESG funds in India valued at $1.4 billion as of 31 March 2021 and allocation of $28 billion international socially responsible investment funds to India in 2019 (CRISIL, 2021). Clearly, investment in ESG-conscious and sustainable funds has grown exponentially in the last decade, warranting this study.

THEORY

ESG-related activities were traditionally viewed as a tradeoff with profitability. It was believed that a firm’s only responsibility should be to maximize shareholders’ wealth. Diverting funds to ESG activities was believed to increase operational costs and reduce the firm’s profitability (Friedman, 1970). In recent years, however, this discourse has been changing positively towards ESG adoption and its merits. About 70 % of recent academic studies show a positive relationship between financial performance (even when measured differently) and ESG performance (Bernow & Nuttall, 2020).

Further, an ESG portfolio significantly outperforms the MSCI US Index, confirming that financial returns and a positive societal footprint reinforced each other and were not tradeoffs (Antoncic et al., 2020). The firms that have a positive ESG evaluation also tend to have a lower cost of capital and are found to provide greater returns than the market in the mid to long-term investment horizons (Antoncic et al., 2020; Bernow & Nuttall, 2020; Fulton et al., 2012). This reflects the change in thinking over the years (from ESG activities being considered a form of theft) to the emergence of ESG performance as a critical objective of corporations.

Family Versus Non-family Firms

Family businesses add an exciting dynamic to ESG and Corporate Sustainability discourse. For family-run organizations, the ability to gain legitimacy and not just the availability of resources affects the growth and survival of the business (Gracia-Sanchez et al., 2021; Westhead & Howorth, 2006). Further, family business owners are motivated by more than just financial goals (Berrone et al., 2012). The identity and image of the family are closely tied to the family business’s functioning; hence, they are personally invested in the business’s reputation, socially responsible image, the longevity of the firm and transgenerational entrepreneurship (Gomez-Mejia et al., 2007). Therefore, they are likely to be more invested in being a sustainable contributor to the ESG goals.

Proponents of the stakeholder theory also posit that a firm’s success depends on all its stakeholders, including the society, to create shared value and, therefore, its responsibility is to all stakeholders (Freeman & Gilbert, 1987). This should increase the scope of ESG in firms (Freeman, 1984: pp. 95–109; Jones, 1995; Qureshi et al., 2021). Further, the quest to build a legacy, attain legitimacy and maintain their reputation would induce family firms to adopt ESG performance goals (Dyer & Whetten, 2006). The broader literature, however, has found mixed results for the ESG performance of family versus non-family firms (Cruz et al., 2014).

In family firms, where the family’s wealth is linked to the firm’s financial performance, the family may have less of an incentive to adopt ESG goals. Through the lens of the shareholder theory, they are justified, as the primary objective of a firm is to maximize wealth for its shareholders (Friedman, 1962). While the broadening scope of corporate governance in recent times entails that the management must actively extend its interests beyond those of the firm’s capital providers to wider stakeholders (Veltri et al., 2021), the concentration of ownership and control in family firms may make the family firms the most important stakeholder for the firm. The firm’s resource dependence on other stakeholders may be limited. Therefore, the interests of other stakeholders will be subservient to that of the family owners (Singh & Mittal, 2019).

The non-family firms mainly comprise state-owned enterprises (SOEs) and multi-national companies (MNCs). SOEs typically have social welfare goals apart from financial ones (Kaushik, 1997). MNCs operating in India generally have their parent firm in developed countries that would have well-established ESG practices. The Indian subsidiaries of the MNCs try to imbibe the practices in the context of their parent company locally (Hassan et al., 2018). The other non-family firms are generally widely held by financial institutions that prefer to invest in companies with better ESG practices and hold them accountable for it.

The SOEs, MNCs and other non-family firms are often very large companies that strive to create a sustainable ecosystem around the geographical locations they operate in, which may be for a combination of factors such as the necessity to create social infrastructure and their values. They spend large amounts on developing communities around their factories, keeping the environment clean and following best practices for waste disposal due to the public, media and analyst scrutiny they always face and their long-term strategy of being socially responsible.

Therefore, non-family firms in India should outperform family firms in terms of the adoption of ESG goals. Hence, we hypothesize:

H1: Nonfamily firms will outperform family firms in the adoption of ESG goals

Heterogeneity Within Family Firms

The relationship between financial and non-financial performance of family firms and ESG practices has garnered significant scholarly attention. Studies have shown that family firms often enhance their corporate reputation through improved ESG performance (Piyasinchai, 2023; Wang, 2024), and some have demonstrated a positive impact of ESG on financial performance (Ahmad et al., 2021). Minutolo et al. (2019) argued that a firm’s ESG score can reflect strategic transparency choices, leading to increased performance. Furthermore, Maquieira (2023) noted that family firms with higher ESG scores tend to pay higher dividends, driven by their concern for stakeholder welfare. Despite this generally positive outlook on the impact of ESG performance, not all family firms are equally likely to adopt ESG practices.

Some studies have reported a negative relationship between family ownership and ESG performance (Rees & Rodionova, 2014). Conversely, other research suggests that a long-term orientation can mitigate the negative impact of family ownership on sustainability practices, encouraging ESG adoption (Memili et al., 2017). Thahira and Mita (2021) also found that family firms often prioritize strong relationships with stakeholders through non-financial information disclosure.

Therefore, the research on ESG performance of family firms suggests a nuanced relationship between family ownership and ESG practices. Few family firms may adopt ESG practices due to their long-term orientation and willingness to forsake short-term goals for the greater good in the future (Lumpkin & Brigham, 2011). While other family firms that may be more focused on profits and short-term results are not likely to adopt ESG practices.

To understand the mixed results on family firms’ ESG practices, it is crucial to distinguish between business group-affiliated firms (FBGFs) and SFFs. These two organizational structures possess distinct characteristics and implications. Standalone firms operate independently without formal ties to other entities, whereas business groups consist of legally independent firms interconnected through coordinated actions (Mahmood et al., 2011). Business groups offer unique advantages, such as internal resource allocation, value-added opportunities, employment promotion and brand strength enhancement (Bae et al., 2002). In contrast, standalone firms may face higher financial constraints and inefficiencies in capital allocation due to their isolated operational structure (Gupta & Mahakud, 2019). Moreover, business groups are often better equipped to navigate institutional voids and market failures in emerging economies, resulting in improved performance compared to standalone firms (Carney et al., 2009).

In the specific context of family firms, FBGFs are typically larger and older than SFFs (Bang et al., 2020). FBGFs are likely more focused on preserving their legacy, maintaining sustainability, enhancing their public image, and are subject to greater scrutiny. The larger size of FBGFs means that lapses in ESG consciousness are more visible to analysts and the public, which pressures these firms to adopt and maintain higher ESG standards. Conversely, SFFs may find it less costly and potentially more rewarding in terms of valuation to be less conscientious about ESG practices.

Another critical mechanism influencing ESG performance in family firms is the role of family governance structures. FBGFs, due to their size and visibility, are more likely to implement robust governance structures, including independent boards and formalized management practices, to safeguard their reputation and legacy (Dyer & Whetten, 2006). These governance structures provide necessary oversight and accountability, ensuring that ESG initiatives align with the firm’s strategic goals. Well-governed family firms can better balance the interests of diverse stakeholders, essential for successful ESG implementation (Bennedsen et al., 2015). Therefore, FBGFs are better positioned to adopt ESG practices effectively compared to SFFs. Therefore, we hypothesize:

H2: FBGFs will outperform SFFs in the adoption of ESG goals

DATA AND METHODS

Dependent Variable

ESG Scores

CRISIL released a report in 2021 that followed a proprietary ESG methodology that scored the 225 largest listed companies in India (CRISIL, 2021). The methodology covers 100 different ESG assessment parameters for which quantitative and qualitative publicly available data were used. The score ranges from 1 to 100, where 100 denotes the best ESG performance. Apart from the composite ESG scores, separate E, S and G scores were also available. Detailed methodology and framework for scoring can be obtained from the CRISIL ESG compendium (2021). The analysis uses the natural log of the ESG score and the natural log of E, S and G scores as dependent variables.

Independent Variable

Family Firms

We obtained the family and non-family classification of the 225 firms in our sample from the Thomas Schmidheiny Centre for Family Enterprise (ThS_CFE). ThS_CFE classifies a firm as a family firm based on the family members’ minimum ownership of 20% equity shares and management control or succession/business continuity. Family Dummy for the ownership classification of the firm takes the value 1 if the firm is a family firm and 0 if the firm is non-family.

Further, ThS_CFE classifies the family firms into firms affiliated with a FBGF and SFF based on business groups data from the Centre for Monitoring Indian Economy (CMIE) prowess and triangulating it with publicly available ownership and affiliation information about the firms (Bang et al., 2017). FBGF Dummy for the ownership classification of the firm takes the value 1 if the firm is an FBGF and 0 if the firm is an SFF.

Control Variables

The study includes various variables in the models to control for the possible confounding effects affecting the hypothesized relationships. Financial information on the firms in our sample is extracted from the prowess database of the CMIE, which has been used extensively by researchers studying issues in the Indian context (Chittoor et al., 2015).

Based on past research, FII ownership (%), return on assets (ROA), sales growth rate, firm age, firm size, cash ratio, research intensity, marketing intensity, investment intensity and debt-equity ratio, have been included as control variables (Antoncic et al., 2020; Bernow & Nuttall, 2020; Miller et al., 2007; Patel & Chrisman, 2014; Ray et al., 2018).

The industry in which the firm operates would also significantly influence its response to ESG and its components. Our sample is well represented by most industries as classified by the National Industrial Classification codes (2008) at a two-digit level. We include industry dummies in our models.

Table 1 provides a description of the variables used in the study.

Variables Description.

Methods

The OLSs regression model was used to examine the relationship between ESG performance and firm classification (family/non-family or FBGF/SFF). The model takes the general form as in Equations (1) and (2).

where subscripts refer to firm i and εi is the error term.

The dependent variable takes the values of natural logarithms of ESG Scores for Model 1, E Scores for Model 2, S Scores for Model 3 and G scores for Model 4.

All financial and accounting data have been winsorized at a 2% level to handle skewness and outliers. The correlation matrix of all variables was constructed, and the VIF was computed. VIF was found to be below 5. Thus, multi-collinearity does not seem to be a concern in our study.

RESULTS

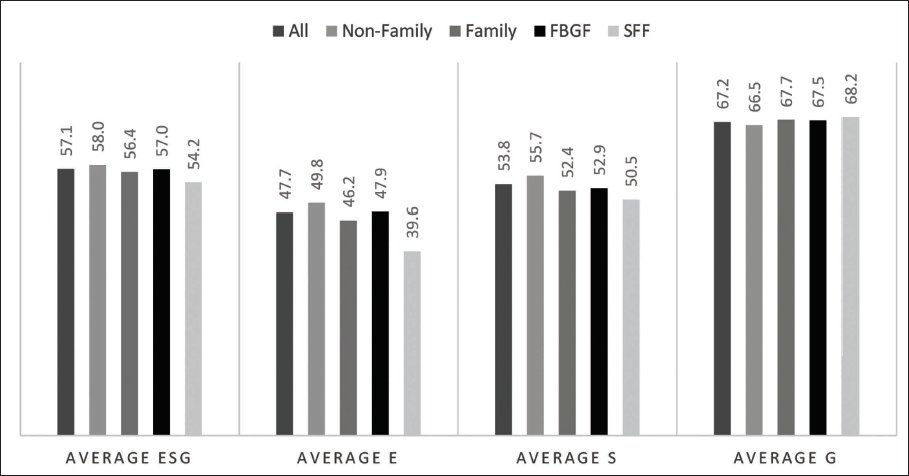

The preliminary analysis of the ESG scores and the scores of its components for different types of firms by ownership show that non-family firms have a higher average ESG score when compared to family firms, except in the G parameter, where the variation seems to be small between firm categories (Figure 2).

Average ESG, E, S and G Scores by Firm Type.

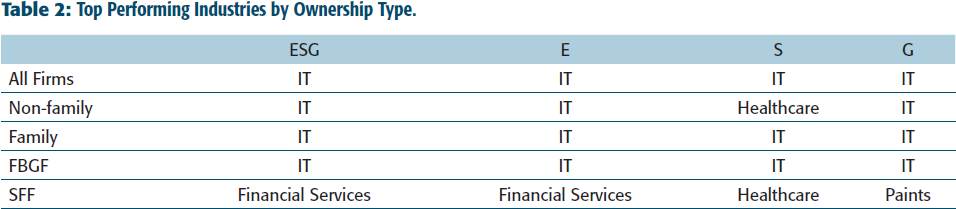

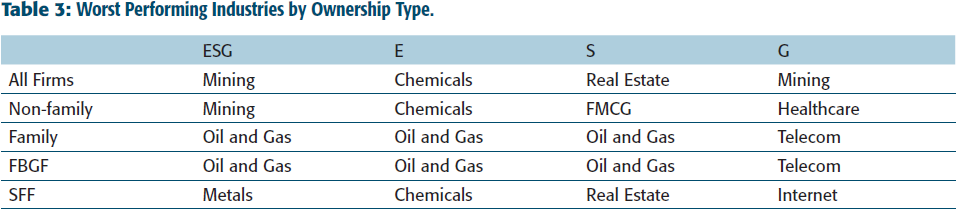

We also see that the industry in which the firm operates plays a vital role in adopting ESG goals (Tables 2 and 3). Overall, IT firms perform the best across all ownership categories and all components of ESG, except SFFs. The best-performing industry among SFFs is financial services. Mining, Oil and Gas and Chemicals dominate among the worst-performing industries. The nature of these firms makes them more susceptible to polluting the environment, not having diversity in the workforce, or getting embroiled with compliance-related issues. Once again, SFFs stand out mainly because non-family firms (mainly SOEs) and FBGFs dominate the oil, gas, mining and telecom sectors.

Top Performing Industries by Ownership Type.

Worst Performing Industries by Ownership Type.

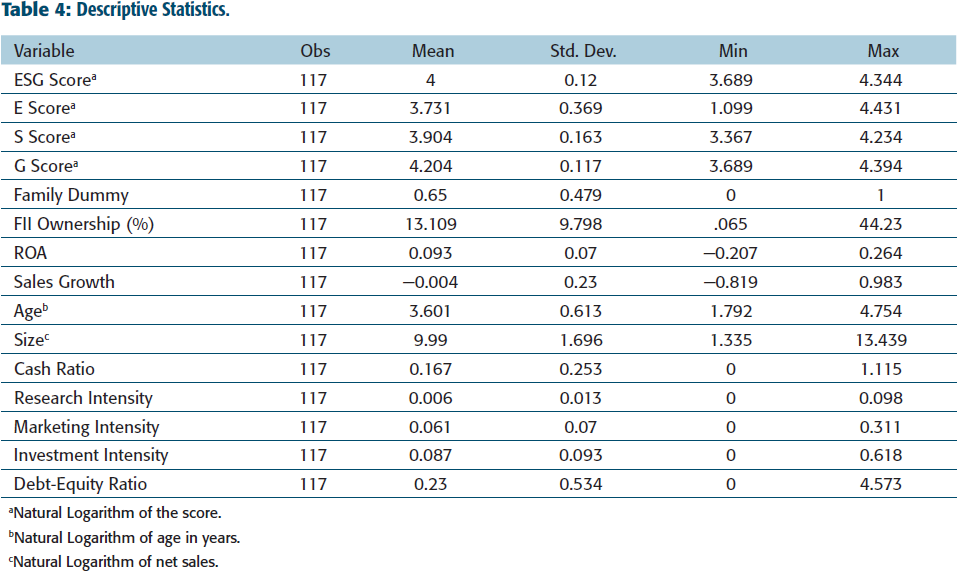

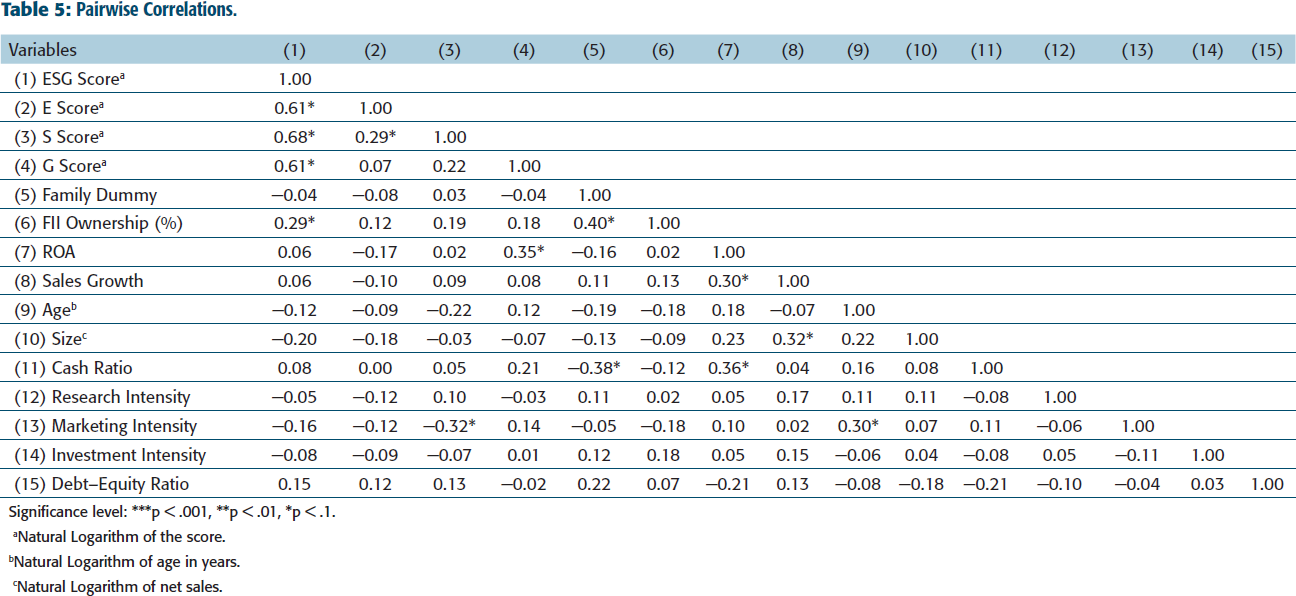

Table 4 presents the descriptive statistics of the variables used in the analysis. Many observations were lost due to the unavailability of data. However, the results were also cross-checked with univariate analysis and were found to be similar. Overall, 65% of the firms in our sample are family firms. This aligns with the percentage of family firms in the BSE500 index. Table 5 presents the pairwise correlation matrix. Ignoring the correlation among the various parameters of ESG, we find that the highest correlation is between family dummy and FII ownership (=0.4).

Descriptive Statistics.

aNatural Logarithm of the score.

bNatural Logarithm of age in years.

cNatural Logarithm of net sales.

Descriptive Statistics.

Significance level: ***p < .001, **p < .01, *p < .1.

aNatural Logarithm of the score.

bNatural Logarithm of age in years.

cNatural Logarithm of net sales.

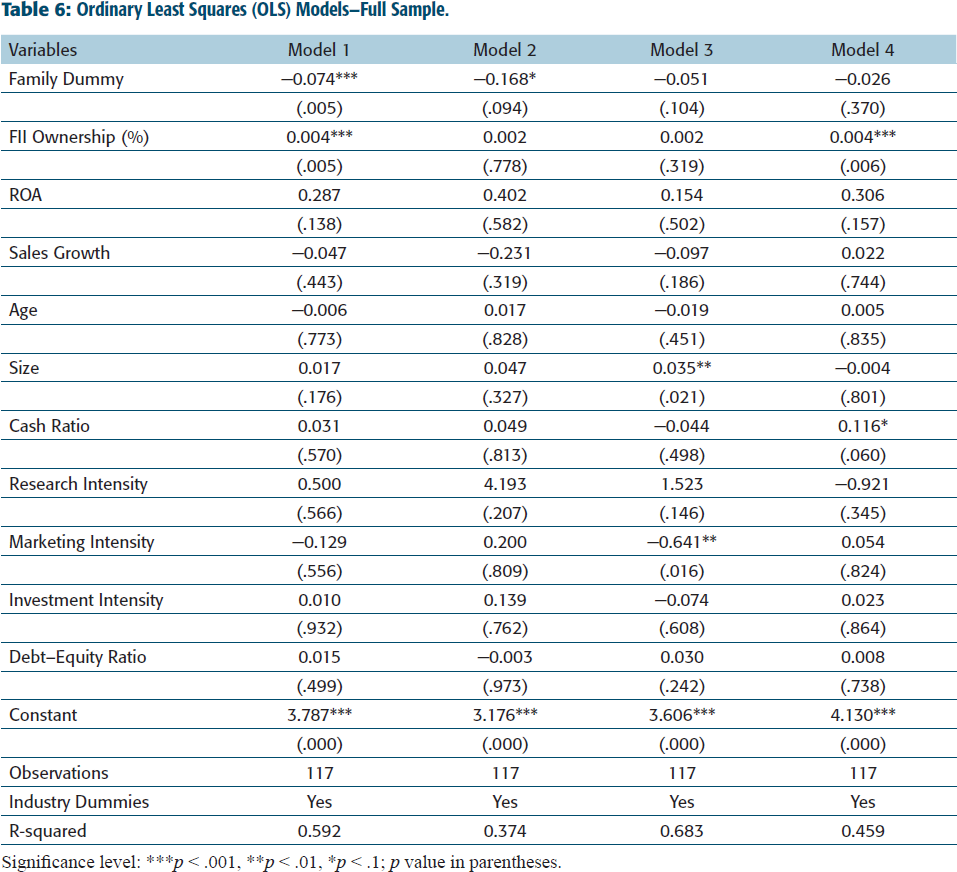

The results of our hypothesis tests are presented in Tables 6 and 7. In Table 6, we test whether the performance of non-family firms is better than that of the family firms in adopting ESG goals, measured by ESG scores and the scores of their components. Model 1 tests H1 that non-family firms will outperform family firms in adopting ESG goals. The result supports our hypothesis as the family dummy is negative and significant (β = −0.074, p = .005).

Descriptive Statistics.

Significance level: ***p < .001, **p < .01, *p < .1; p value in parentheses.

Models 2–4 test for the impact of family ownership on the adoption of each of the components of ESG, respectively. While the coefficient of the family dummy is negative for all components, only the Environment component (Model 2) is significant. The Social component is weakly significant, with a p value of .104.

The insignificance of the G component could be attributed to clearer, relatively mature and more stringent regulatory requirements on aspects such as independent directors, diversity at the board level and various disclosures about the company that is mandatory across all classes of companies, irrespective of whether they are family owned or are non-family firms. Corporate Governance norms for the listed firms in India are continuing to improve owing to various reforms (Chakrabarti et al., 2008). Large firms, which are primarily the ones rated by CRISIL, are especially leading the way in corporate governance due to their quest to be global multi-national corporations, the investments from global financial institutions looking to invest in emerging markets such as India, and the scrutiny from analysts and investors (Afsharipour, 2009). Therefore, all large firms would try to comply with corporate governance regulations irrespective of ownership.

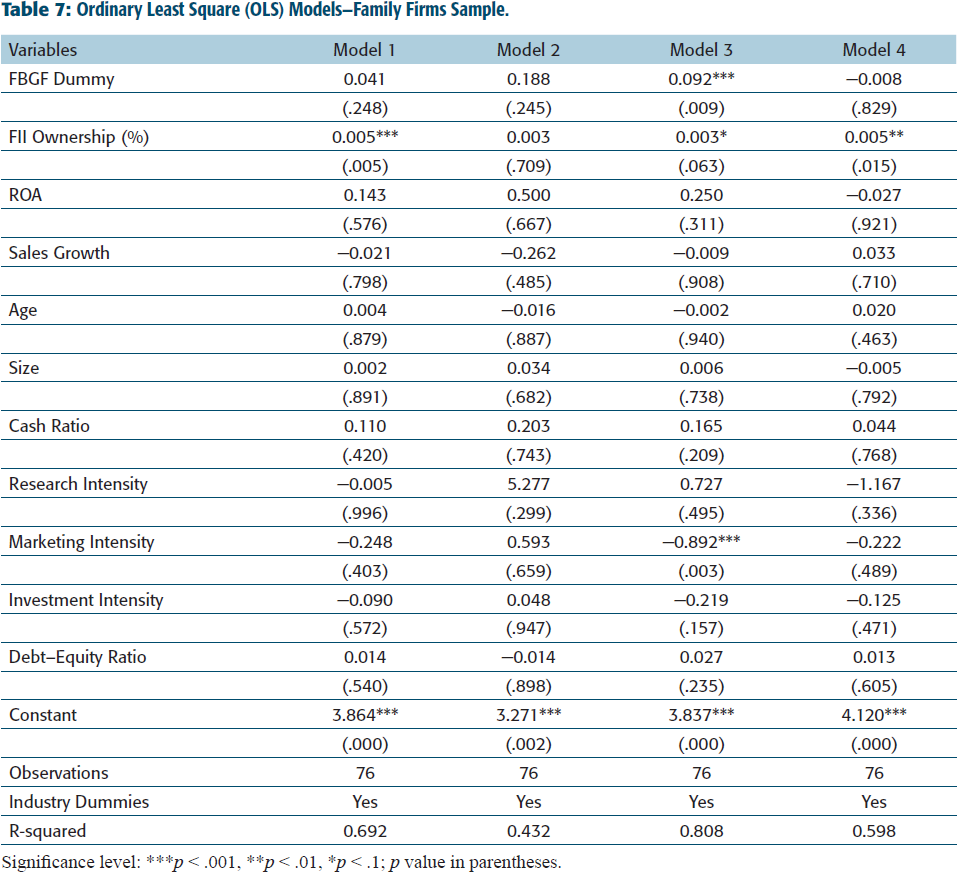

The results for the test of H2 are presented in Table 7. Model 1 tests for the impact of affiliation to a family business group on adopting ESG goals performance for a sample of family firms only. Models 2–4 test for the individual components of ESG. FBGFs perform better than SFFs in only the social component (Model 3, β = 0.092, p = .009). Since most firms in our sample are large firms, it is unsurprising that FBGFs and SFFs do not differ in governance or environmental adoption and their overall performance in ESG adoption.

Ordinary Least Square (OLS) Models—Family Firms Sample.

Significance level: ***p < .001, **p < .01, *p < .1; p value in parentheses.

However, traditionally family business group firms in India have been socially conscious, and societal giving for the betterment of society is ingrained in most families (Bhatnagar et al., 2020), especially the ones that comprise the family business groups. The belief in the concepts of Dharma and Karma, that espouse societal giving, motivate many family business group firms such as the Murugappa Group firms, Aditya Vikram Birla Group firms and the Piramal Group firms, that have the ability as well as the willingness, to spend on causes of social upliftment and empowerment (Bhatnagar et al., 2020; Krishnan, 2005).

We find a positive relationship between FII Ownership and the adoption of ESG goals (Tables 6 and 7). It indicates that (a) FII can drive the firms to adopt more sustainable practices, and (b) FIIs perhaps tend to invest in companies that are already known to have better ESG practices and are known to be well governed (Fang et al., 2015).

Ad-Hoc Analysis

We also did an ad-hoc analysis of the moderating effect of FII Ownership on the impact of family on adoption of ESG goals. We found that the moderation term is positive and significant (β = 0.006, p = .036), indicating that the presence of FII Ownership moderates the impact of family on ESG adoption positively. However, the moderating effect is insignificant for E, S and G components separately, and also for the analysis of only family firms sample.

Addressing Endogeneity Concerns

In conducting our analysis, we acknowledge the potential endogeneity concerns that may arise due to the relationship between ESG performance and firm characteristics. Specifically, there is a possibility that unobserved factors influencing a firm’s ESG performance may also be correlated with the independent variables, leading to biased estimates. To mitigate these concerns, we have employed several strategies. First, we included a comprehensive set of control variables, such as firm size, age, ROA, sales growth rate, cash ratio, research intensity, marketing intensity, investment intensity and debt-equity ratio, which are commonly associated with both ESG performance and firm characteristics. Second, we incorporated industry-fixed effects to account for industry-specific influences that could affect both ESG adoption and firm performance. Despite these measures, we recognize that endogeneity cannot be completely ruled out. Future research could benefit from employing instrumental variable approaches or panel data techniques to further address potential endogeneity and provide more robust causal inferences.

CONCLUSION

Family firms have a multi-generational long-term perspective and strong social connections, and ESG strategies need a long-term orientation. Therefore, family firms and ESG are a natural fit. Then paradoxically, why do we not find family firms scoring better than non-family firms on overall ESG, specifically environmental and social parameters?

Our findings suggest that the overall ESG adoption remains challenging for family firms compared to non-family firms. This discrepancy can be attributed to the lack of awareness about ESG parameters and their long-term implications for business sustainability. Additionally, the predominance of large firms in our sample, all rated by CRISIL, indicates that size alone does not significantly impact ESG performance.

Our study’s examination of FBGFs and SFFs yields intriguing insights into the heterogeneity within family firms concerning ESG adoption. The results indicate that FBGFs outperform SFFs specifically in the social dimension of ESG performance. This finding underscores the distinctive advantages that FBGFs possess due to their size, resource availability and legacy-driven focus on social responsibility. FBGFs, being larger and more established, are often under greater scrutiny from analysts and the public, which pressures them to adopt and maintain higher social standards. Furthermore, the historical and cultural values of many family business groups, which emphasize societal giving and community development, likely contribute to their superior performance in social metrics. On the other hand, SFFs may prioritize financial performance and operational survival over extensive ESG commitments. The contrast between FBGFs and SFFs highlights the need for tailored strategies to enhance ESG adoption across different types of family firms. Policymakers and stakeholders should consider these intrinsic differences and provide support mechanisms that address the unique challenges faced by SFFs, while leveraging the strengths of FBGFs to foster a more inclusive and effective ESG adoption across the board.

Our analysis also reveals the significant moderating effect of FII ownership on the relationship between family ownership and ESG adoption. The positive and significant interaction term indicates that the presence of FII ownership enhances the adoption of ESG practices in family firms. However, this moderating effect is only significant in the full sample analysis for ESG scores and not for individual E, S and G components separately. This suggests that FIIs play a crucial role in driving family firms towards more sustainable practices, potentially due to their governance mechanisms and the pressure they exert on firms to meet higher standards of ESG performance.

Despite the inherent advantages of family firms in terms of long-term orientation and stewardship values, our results highlight the need for a more structured approach to ESG adoption. Policymakers should focus on creating awareness and providing clear roadmaps to nudge family firms towards better ESG practices. Given that more than 90% of listed firms in India are family firms, this targeted approach is crucial.

The starting point could be to formulate a clear strategy to sensitize family firms about the long-term negative implications and the destructive effects of ignoring ESG factors. They need to realize that ESG scores reflect their level of understanding and response to the need for proactive steps towards sustainability. If family firms do not start to focus on all parameters of ESG, they may drive away their progeny, who are increasingly concerned about their future in a sustainable world.

Family firms are also known to take all stakeholders along as a family. That is precisely what ESG performance entails. All stakeholders must come together and believe in sustainable solutions. While it might necessitate changing current practices, renegotiating contracts, going back to the drawing board and perhaps facing the ire of the markets in the short run, companies will find that it is in their best interests to be proactive rather than reactive in their approach towards ESG.

ESG performance is undoubtedly becoming an integral part of company reporting. As the focus on socially responsible businesses and investment grows, investors increasingly consider integrating sustainability into their portfolios. In such a scenario, it is pertinent for the Government to have clear reporting standards. Although there are international reporting standards such as Global Reporting Initiative and Sustainability Accounting Standards Board, there are no standard parameters of measurement within these three (E, S, G) broad categories. It becomes hard to ascertain what is good and what is wrong. Also, the lack of comprehensive analysis of a company’s operations leaves us with questions such as whether it would be correct to say that Tesla is a green company even if it is involved in large-scale nickel mining.

Similarly, as the demand for responsible investing increases, so have the agencies offering such data. However, various agencies are disjointed in their data collection and analysis. For example, they differ in the choice of relevant factors, how they are measured and weighted, and where the data is sourced. Different metrics result in a considerable divergence in what makes an investment sustainable. This impacts investors who blindly follow the strategy of a single index or agency and may invest in a portfolio of companies that perhaps made a list due to a particular bias or omission.

Such loopholes pose an even bigger problem to the planet if overlooked. Not only does it give misconstrued views on the ESG actions of companies, but it also allows companies to hide behind a fabricated window of responsibility and carry on their unethical practices with no accountability. LaBella et al. (2019) mention that ESG scores are skewed towards companies with higher disclosures. Such a practice allows companies to manipulate the process since unaudited self-reports will only show companies in their best light, allowing people to overlook its other practices.

Fortunately, with the fast-growing popularity of ESG, active efforts are being taken to standardize ESG reporting worldwide. At this juncture, however, responsible investors should educate themselves on the nuances of sustainability reporting to look beyond the froth, identify what is relevant, and make unbiased conclusions. With the suitable measures in place, ESG will soon arm companies with the tools they need to be resilient in this fast-paced, dynamic world.

In essence, government and development institutions have a responsibility to move ESG onto the front burner and proactively formulate appropriate policies. Because of their unique characteristics, family businesses can potentially become leaders in ESG performance. Family firms in India have always stepped up when needed. Whether it was the era of manufacturing steel, salt or textile, or when India moved towards liberalizations, family firms led the transition to a service-led economy, or when the deadly COVID-19 struck globally, the family firms in India became the suppliers of vaccines to the world. Now, ESG has become a necessity, not an option. Moreover, we can be sure that collectively, family firms will rise to the occasion with a bit of awareness, a little nudge and the realization of a better tomorrow.

Footnotes

ACKNOWLEDGEMENT

The authors are thankful to Bharagavi Mantravadi for her research assistance.

DECLARATION OF CONFLICT OF INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.

NOTES

e-mail:

e-mail: