Abstract

Corporate social responsibility (CSR) is central to debates on the legitimacy and competitiveness of family firms, yet evidence on ownership effects remains inconsistent. While socioemotional wealth perspectives highlight reputational motives, capability-based views suggest that resource constraints may limit substantive internal investments. Most prior studies focus on aggregate CSR levels and on Europe or North America, leaving unanswered whether ownership shapes the composition of CSR activities in under-represented contexts such as Latin America. This article examines 315 listed firms in Argentina, Brazil, Chile, Colombia and Mexico between 2019 and 2023. Using environmental, social and governance ratings and generalised linear models with size, age, country and sector controls, this study tests whether family ownership predicts internal versus external CSR outcomes. The authors find that non-family firms outperform in capability-intensive internal CSR, while external CSR and governance show parity. These results highlight a visibility–capability trade-off and suggest that Latin American family firms must enhance their operational capabilities to address CSR gaps.

Corporate social responsibility (CSR) in family firms (FFs) has attracted sustained scholarly attention. On one hand, socioemotional wealth (SEW) perspectives suggest that family owners engage in CSR to protect reputation and legitimacy. On the other hand, resource-based arguments highlight constraints and risk aversion that may limit substantive investments in sustainability. More recently, scholars have distinguished between external, visibility-oriented CSR (e.g., community relations) and internal, capability-intensive practices (e.g., workforce development); however, findings across regions remain mixed.

Despite these advances, two important gaps remain. First, most studies treat CSR as an aggregate level, overlooking whether ownership differences shape the composition of CSR activities more than their overall intensity. Second, Latin America remains under-represented in family business research, despite the fact that FFs dominate capital markets and operate under volatile institutional conditions. Without evidence from this context, it is unclear whether family ownership fosters substantive internal improvements or instead prefers more visible outward activities.

This article addresses these gaps by examining the composition of CSR in 315 listed firms across Argentina, Brazil, Chile, Colombia and Mexico. Using environmental, social and governance (ESG) ratings and generalised linear models with controls for firm size, age, country and sector, we test whether family ownership predicts systematic differences in internal versus external CSR. The results show that FFs lag behind non-family firms (NFFs) on internal, capability-intensive CSR, while external activities and governance are statistically comparable.

These findings make three contributions. First, they shift the focus from overall CSR levels to the composition of CSR activities, helping explain the mixed results in prior research. Second, they integrate SEW and legitimacy motives with capability-based perspectives, introducing a visibility–capability trade-off: FFs tend to meet external expectations but often underinvest in internal improvements, which may reflect limitations in organisational processes or information systems. Third, they provide rare, contextual evidence from Latin American public markets, demonstrating that ownership effects persist even under strong country and sector influences. Together, these contributions advance understanding of how family ownership shapes CSR in emerging economies and highlight capability building as a central challenge for FFs.

Theoretical Background and Hypothesis

This section grounds the study in theories that explain where ownership should matter for CSR in Latin American listed firms. The study integrates SEW and legitimacy perspectives, with their emphasis on reputation and outward signalling, with capability-based views that locate costly, process-intensive improvements inside the firm. While the broader literature often refers to CSR, this study uses ESG metrics to operationalise CSR outcomes. From this lens, we derive hypotheses about overall ESG differences, as well as internal and external ESG differences among FFs and NFFs.

CSR and Family Firms

CSR is the set of business policies and practices through which organisations take responsibility for their environmental and social impact on society (European Commission, 2011). It is often framed as discretionary activities that advance social good (De Roeck & Maon, 2018), while accounting for stakeholders’ expectations and the triple bottom line of economic, social and environmental performance (Aguinis, 2010). CSR is a strategic decision (Bundy et al., 2013). Over time, CSR actions can lead to higher financial performance and the development of a competitive advantage (Velte, 2022). This remains a key strategic priority for many organisations, serving as a source of competitive advantage (Carroll, 2015; Porter & Kramer, 2006; Saeidi et al., 2015). CSR is also a multidimensional concept (Carroll, 2021; Dahlsrud, 2008; Matten & Moon, 2008) and can be organised into external and internal domains. External CSR refers to public and visible organisational activities that affect the public, consumers and institutions (external stakeholders) (Hawn & Ioannou, 2016). Internal CSR refers to organisational activities that impact employees and shareholders as internal stakeholders (Canavati, 2018). These domains are often in tension because resources devoted to one set of stakeholders may divert attention away from the other, prompting firms to seek a balance (Berrone et al., 2010; Cruz et al., 2014; Durand et al., 2019; Hawn & Ioannou, 2016). To align our empirical analysis with this internal–external CSR framework, we operationalise CSR using LSEG (Refinitiv) ESG pillar scores—internal CSR is the mean of the following categories: resource use, emissions, workforce, human rights, management and shareholders. External CSR includes environmental innovation, community, product responsibility and CSR strategy. The complete details appear in the ‘Methods’ section.

The extant literature has found that firm ownership influences how CSR decisions are taken and that FFs and NFFs choose different CSR practices (Campopiano & De Massis, 2015; Dyer & Whetten, 2006; Pareek & Sahu, 2022; Rees & Rodionova, 2015). While the results are inconclusive on whether one type of ownership is more or less socially responsible than the other (Cruz et al., 2014; Mariani et al., 2023), recent studies have aimed to identify how ownership differs in the prioritisation of one CSR dimension over others (Rivera-Franco et al., 2024).

Socioemotional Wealth, Legitimacy and Resource-based View

According to the SEW theory, family businesses are motivated to preserve the utilities derived from the non-economic aspects of the business, such as family values, emotions and altruism (Cennamo et al., 2012; Gomez-Mejía et al., 2007; Stock et al., 2023). SEW perspectives emphasise control, identity and continuity in FFs. Hence, the family makes decisions about the family business based on the gains and losses they may incur regarding SEW, which encompasses family control and influence, emotional attachment and dynastic succession (Berrone et al., 2012; Daspit et al., 2021; Gomez-Mejía & Herrero, 2022).

Rivera-Franco et al. (2024) identified that European FFs outperform non-FFs in overall CSR and in the internal dimension of CSR and explained this phenomenon through the SEW theory. Because FFs aim to protect their SEW, they are more intentional in their CSR practices, as it enhances the image and reputation of the firm (Campopiano & De Massis, 2015; Zellweger et al., 2013), particularly in environments where the perception of corruption challenges the credibility of CSR practices (Rivera-Franco et al., 2024). In countries with high levels of corruption, external stakeholders may not value CSR practices, which can hinder the FFs’ image and reputation, and consequently diminish its SEW. Empirical research has found that FFs tend to enact CSR practices towards their employees in such environments (van Essen et al., 2015) to fill institutional voids and that internal CSR practices enhance the employees’ trust in the firm. Given the differences between Europe and Latin America in institutional enforcement, professionalisation and sector mix, this study treats Rivera-Franco’s claim with caution and explores the ownership effects on overall and compositional CSR as context-dependent and state non-directional hypotheses.

Following Suchman (1995), this study defines legitimacy as a generalised perception that an organisation’s actions are desirable, proper or appropriate within a socially constructed system of norms, values and beliefs, grounded in pragmatic, moral and cognitive bases. Organisations manage legitimacy through substantive changes to practices and symbolic displays that communicate conformity, as argued by Ashforth and Gibbs (1990). Over time, institutional pressures lead to convergence in organisational forms through coercive, normative and mimetic isomorphism, as noted by DiMaggio and Powell (1983). In the context of the current study, these mechanisms suggest that listed firms face incentives to appear responsible and, in some cases, to actually become so, while the mix of substantive and symbolic responses may vary depending on ownership. Therefore, legitimacy suggests that family owners value reputation and may favour visible, outward activities that signal responsibility to stakeholders and that they may use ESG reporting to maintain a social bond with stakeholders (Garzón Jiménez & Zorio-Grima, 2021).

From a capability-based perspective, CSR initiatives vary in the extent to which they require firms to mobilise resources and develop new routines. The resource-based view and its environmental extension, the natural resource–based view, highlight that process-intensive improvements, such as reducing emissions, improving resource efficiency or professionalising workforce and governance practices, depend on accumulated capabilities that are costly to build and slow to yield visible payoffs (Barney, 1991; Hart, 1995; Khattak et al., 2021). Similarly, the dynamic capabilities framework emphasises that such practices require continuous investment in learning, integration and reconfiguration (Teece et al., 1997). Recent evidence shows that in family businesses, innovation is likely to be constrained if not supported by professionalised control systems or training (Basly & Cano-Rubio, 2024; Román-Calderón et al., 2023). This study, therefore, conceptualises internal CSR as more capability-intensive (Dassanayake et al., 2025), in contrast to external CSR activities such as community engagement or philanthropy, which are more symbolic, visible and less dependent on internal process improvement.

In emerging markets, legitimacy expectations are context-specific (Jamali & Neville, 2011). For listed FFs, legitimacy is also intertwined with reputation and SEW (Deephouse & Jaskiewicz, 2013), a dynamic that is especially salient in Latin America (Gomez-Mejía et al., 2024). In Latin America, FFs are both SEW-intensive (highly oriented towards preserving and enhancing SEW) and SEW-sensitive (highly responsive to external cues that impact SEW, such as reputation, status and continuity) (Gomez-Mejía et al., 2024).

Hypotheses

Since these forces can yield CSR that is selective rather than uniformly higher or lower, this study examines whether there are any significant differences in the overall CSR scores of family and non-family listed firms in Latin America. CSR levels vary with sector exposure and country conditions. Prior findings on FF versus NFF CSR are heterogeneous; therefore, we posit an association rather than a directional effect. To avoid attributing contextual composition to ownership, we include year, country and sector fixed effects, as well as controls for size and age.

H1: Ownership type (FF vs NFF) is associated with overall ESG performance after controlling for size, age, year, country and sector.

H2: Ownership type (FF vs NFF) is associated with internal CSR after controlling for size, age, year, country and sector.

H3: Ownership type (FF vs NFF) is associated with external CSR after controlling for size, age, year, country and sector.

H4: Within FFs, age will be positively associated with internal CSR performance, but not with external CSR performance.

Methodology

The study examines whether and where family ownership is associated with CSR, employing a balanced and transparent design. The data set covers 63 listed firms in four Latin American countries from 2019 to 2023 (315 firm-years), categorised as FF or NFF. CSR outcomes include the ESG score; its E, S and G pillars; categories; and two theory-guided composites: internal CSR (resource use, emissions, workforce, human rights, management and shareholders) and external CSR (environmental innovation, community, product responsibility and CSR strategy). To isolate ownership effects within comparable contexts, the study estimates general linear models (GLM/ANCOVA) with year, country and sector fixed effects and controls for firm size (log assets, swapped for log market cap in checks) and firm age (log years).

Sample and Data

The sample was constructed by collecting information on a collection of listed FFs and NFFs from five Latin American countries over a 5-year period (2019–2023). The FFs were initially identified from the Global 500 Family Business Index (EY & University of St. Gallen, 2025), and NFFs were selected from the Statista report on the largest listed businesses in Latin America 2025 (Statista, 2025). The Family Business Index considers an organisation to be a family business if a family has voting control of at least 32%, has a demonstrated involvement of multiple generations and/or is at least 50 years old (EY & University of St. Gallen, 2025).

The final sample consists of 315 firm-year observations from five Latin American countries: Argentina (19%), Brazil (22%), Chile (16%), Colombia (6%) and Mexico (36%). Of these, 160 firms (51%) are classified as FFs, while 155 (49%) are NFFs. The industry distribution reflects the sectoral concentration of listed firms in the region, with the largest groups in consumer goods (40%) and materials and energy (37%), followed by industrials (11%), technology and communication (8%), real estate (3%) and healthcare (2%).

Following prior research on CSR and corporate governance, the study excluded firms in the financial and utility sectors because their regulatory environments, capital structures and incentive systems differ substantially from those of other industries. Financial firms’ high leverage and unique accounting practices, and utilities’ rate-regulated monopolistic nature and compliance-driven CSR, make them non-comparable to firms operating in competitive markets. Including these sectors could introduce bias and confound the interpretation of CSR determinants and outcomes (Armstrong et al., 2016; Fama & French, 1992; Galant & Cadez, 2017). The study also removed the observations that lacked five consecutive years of data. The final sample consisted of 63 firms and 315 observations.

Measurements

Dependent Variables

CSR performance was measured using the ESG score provided by the London Exchange Group (formerly known as Refinitiv). This database is widely used by academics, analysts and investors; it has also been used in previous studies on socially responsible practices (Dal Maso et al., 2020; Pérez-Cornejo et al., 2020; Rivera-Franco et al., 2024; Soni, 2023).

The ESG score is a composite score ranging from 0 to 100, used to assess a firm’s environmental, social and governance performance, with higher values indicating better performance. Each pillar is divided into 10 categories. These categories are the elements used to divide the scores into internal and external CSR.

Internal CSR refers to inward-looking practices aimed at employees and investors (Canavati, 2018; Hawn & Ioannou, 2016). The measure of internal CSR encompasses two categories of the environment pillar (resource use and emissions), two categories of the social pillar (workforce and human rights) and two categories of the governance pillar (management and shareholders). The resource use category represents the company’s performance in reducing the use of materials, energy or water. The emissions category represents the organisation’s commitment to reducing emissions to the environment during its operations. The workforce category evaluates a company’s policies and practices related to its employees, including diversity and inclusion, health and safety, working conditions, training and development, and employee engagement. It reflects how the firm manages its human capital to ensure fair treatment, well-being and professional growth. The human rights category assesses a company’s commitment to upholding fundamental labour and human rights standards through policies and practices, including ensuring freedom of association, prohibiting child and forced labour, respecting international conventions and applying human rights criteria in supplier selection and monitoring. These measures reflect the company’s commitment to its workforce and adherence to ethical labour practices. The management category assesses internal governance practices, encompassing board structure, independence, audit and compensation oversight, succession planning and executive compensation policies. These mechanisms strengthen accountability and decision-making within the organisation. The shareholder category measures a company’s commitment to protecting shareholder rights through policies on equal treatment, voting rights, executive pay approval and limits on anti-takeover devices. These practices strengthen internal governance and accountability by ensuring fair representation and transparency in decision-making. While prior studies (e.g., Rivera-Franco et al., 2024) classify all environmental categories as external CSR, this study follows a different approach based on the underlying focus of each category. Specifically, the study includes resource use and emissions within internal CSR, since the underlying indicators primarily capture practices directed at employees and internal operations (e.g., energy efficiency, pollution control, workplace safety).

External CSR includes customers, community and the environment (Canavati, 2018). The study’s measure of external CSR includes one category of the environment pillar (environmental innovation), two categories of the social pillar (community and product responsibility) and one category of the governance pillar (CSR strategy). Environmental innovation captures a company’s ability to develop technologies, processes or eco-designed products that reduce customers’ environmental impact. The community category measures the organisation’s efforts towards promoting public health and business ethics. The product responsibility category measures an organisation’s efforts to produce a quality product or service that protects consumers’ health and safety. The CSR strategy refers to the firm’s practices of communicating how it integrates ESGs into its decision-making processes.

Control Variables

To isolate the ownership association from contextual confounds, the study includes firm size and firm age as covariates, measured as LogAssets (in the main models and LogMktCap in robustness) and LogAge (in years since founding), to capture resource slack and organisational maturity. The study includes a full set of fixed effects for year, country and sector (entered as categorical factors; Type III SS with an intercept) to account for common shocks, country-level institutional bundles and industry-specific technology/regulatory differences. To avoid redundancy and multicollinearity, the study includes only one size proxy per model and does not pair country dummies with the institutional index; instead, institutions are examined in complementary specifications that replace country fixed effects. Continuous covariates are log-transformed to reduce skew and approximate linearity; results are robust to swapping the size proxy. Firm size is measured using LogAssets; LogMktCap is used only in robustness checks, and results are robust to swapping the size proxy.

The study also compiles the World Bank Worldwide Governance Indicators to capture institutional quality. In the main models, the study relies on country fixed effects, which provide a more flexible capture of unobserved national-level heterogeneity across our four countries. As a complementary specification, the study replaces country fixed effects with a standardised composite institutional index that aggregates six dimensions: voice and accountability, political stability, government effectiveness, regulatory quality, rule of law and control of corruption. Institutional strength varies across Mexico, Brazil, Colombia, Argentina and Chile, with Chile typically viewed as a strong performer.

Results

The authors reports results from general linear models (GLM/ANCOVA) that compare FFs and NFFs on ESG outcomes, controlling for size and age and including year, country and sector fixed effects. The study first presents descriptive statistics, then the results for the overall ESG and pillar scores, followed by the internal versus external CSR decomposition and categories.

Descriptive Statistics

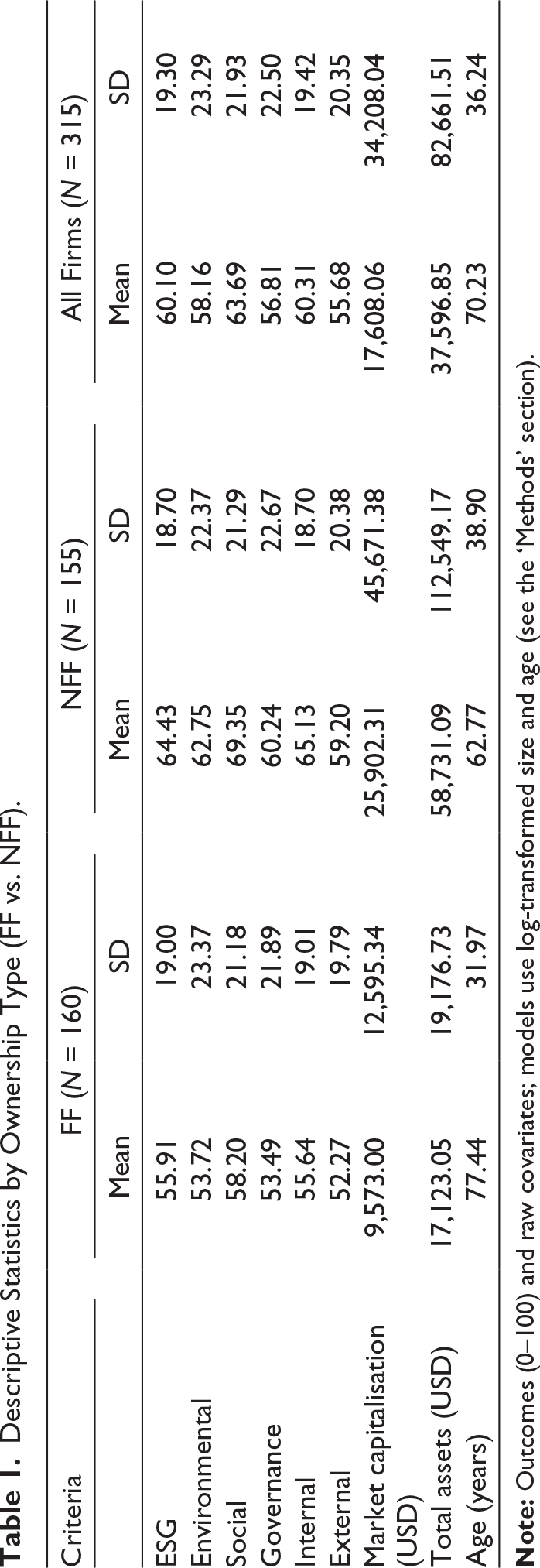

The first step in the analysis was to conduct descriptive statistics to get a better understanding of the data, as well as t-tests. The authors analysed 315 firm-years, split between NFFs (n = 155) and FFs (n = 160). NFFs score higher on overall ESG (M = 64.43) than FFs (M = 55.91), a mean gap of 8.52 points (t = 4.01, p < .001; Cohen’s d ≈ 0.45). By pillars, NFFs exceed FFs on environment (62.75 vs 53.72; t = 3.50, p < .001), social (69.35 vs 58.20; t = 4.66, p < .001) and governance (60.24 vs 53.49; t = 2.69, p = .008). Using the internal/external split, NFFs also outperform on internal CSR (65.13 vs 55.64; t = 4.47, p < .001; d ≈ 0.50) and external CSR (59.20 vs 52.27; t = 3.06, p = .002; d ≈ 0.35). Among the categories, differences favour NFFs for resource use, emissions, environmental innovation, workforce, human rights, CSR strategy and management (all p ≤ .006), while community and shareholders are not statistically different, and product responsibility is only marginally significant (p = .054). On firm characteristics, NFFs are larger on market capitalisation and total assets (both p < .001); log assets are modestly higher (p ≈ .049), whereas FFs are older (age: 77.4 vs 62.8 years; t = −3.66, p < .001; LogAge is also higher for FFs). Overall, differences are small to moderate in magnitude, indicating that, in this sample of listed Latin American firms, ownership type is meaningfully, though not overwhelmingly, associated with ESG levels (see Table 1).

Descriptive Statistics by Ownership Type (FF vs. NFF).

Overall ESG and E, S and G Pillars

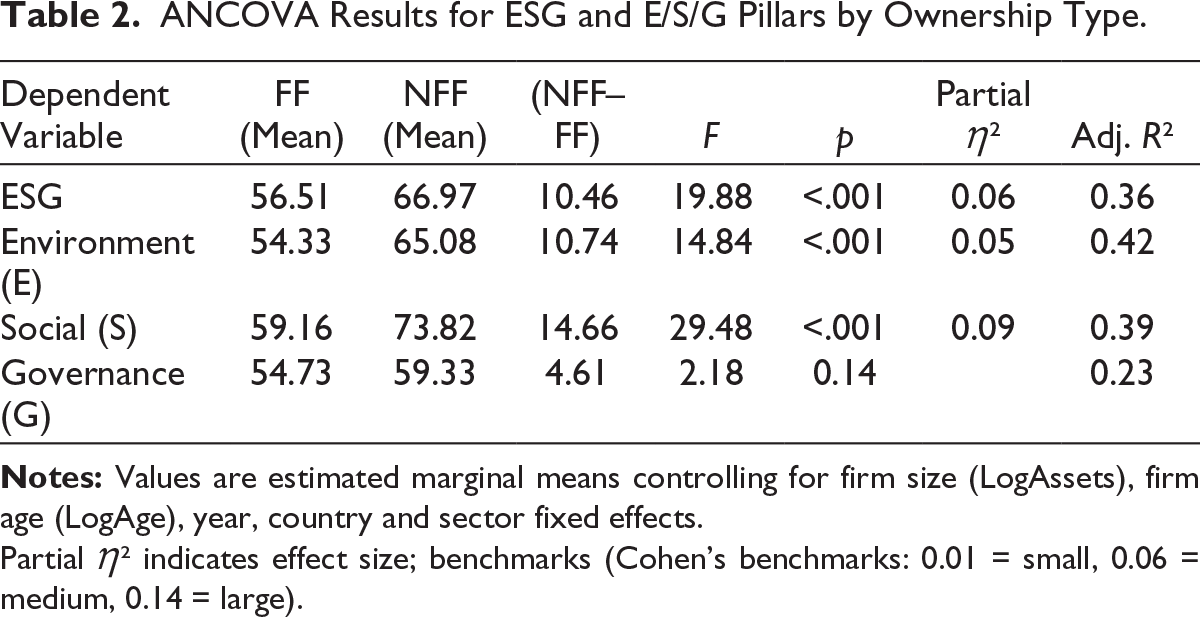

To test whether ownership (family vs non-family) is associated with overall ESG performance after controlling for size, age, year, country and sector (H1), the study uses a univariate general linear model (GLM/ANCOVA). We found that NFFs scored significantly higher on ESG than FFs (estimated marginal mean: 66.97 vs 56.51; difference = 10.46; F = 19.88, p < .001). The effect size was moderate (partial η² = 0.06), and the model explained a substantial portion of the variance (R² = 0.41). Among covariates, both firm size (LogAssets) and firm age (LogAge) were positive and significant predictors of ESG performance, while year effects were not. Country and sector fixed effects were also jointly significant. These results confirm that, in Latin American listed firms, ownership type is meaningfully associated with ESG outcomes, with NFFs consistently outperforming FFs in overall ESG performance.

For the environmental pillar, NFFs scored significantly higher than FFs after accounting for firm size, age, year, country and sector. The adjusted mean was 65.08 for NFFs and 54.33 for FFs, a gap of 10.74 points (F = 14.84, p < .001, partial η² = 0.049). This represents a moderate effect size, indicating that ownership type has a meaningful impact on environmental practices in Latin American listed firms.

NFFs also significantly outperformed FFs on the social pillar of ESG. The adjusted mean was 73.82 for NFFs and 59.16 for FFs, a gap of 14.66 points (F = 29.48, p < .001, partial η² = 0.092). This is a moderate to large effect size, indicating that ownership has a strong association with social practices, particularly those involving the workforce and human rights.

In contrast, no significant differences were found between ownership types on the governance pillar. The adjusted mean was 59.33 for NFFs and 54.73 for FFs, a gap of 4.61 points that did not reach statistical significance (F = 2.18, p = .141). This suggests a convergence in governance practices across listed firms, likely reflecting the influence of regulatory requirements (see Table 2 for the ANCOVA results).

ANCOVA Results for ESG and E/S/G Pillars by Ownership Type.

Partial η² indicates effect size; benchmarks (Cohen’s benchmarks: 0.01 = small, 0.06 = medium, 0.14 = large).

Internal and External CSR (H2 and H3)

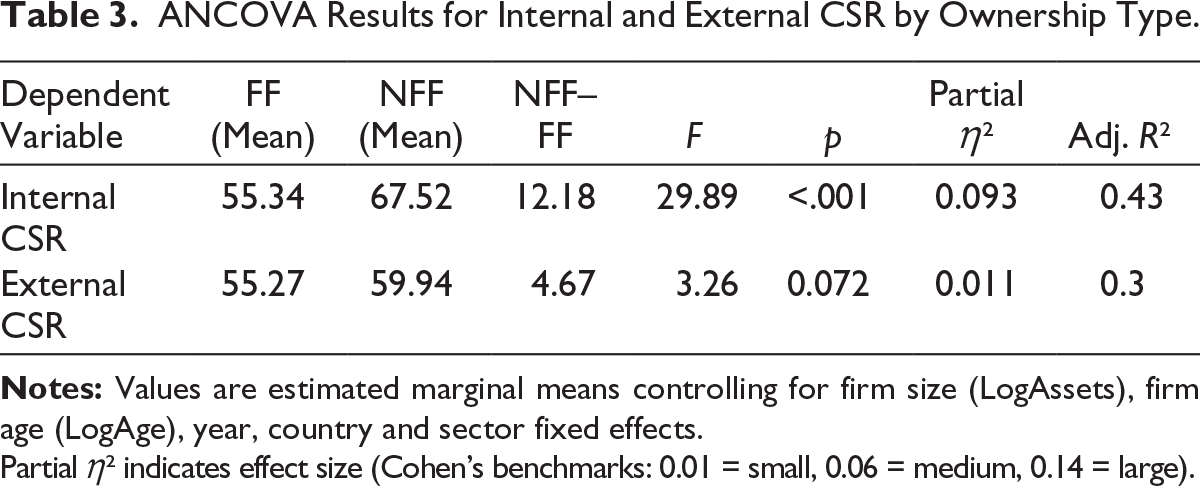

The ANCOVA results reveal significant differences in internal CSR between ownership types. NFFs reported substantially higher scores (adjusted mean = 67.52) than FFs (adjusted mean = 55.34), a gap of 12.18 points (F = 29.89, p < .001, partial η² = .093). This represents a moderate to large effect size, suggesting that ownership exerts a meaningful influence on internal CSR practices, including employee relations, workplace standards and human rights initiatives.

For external CSR, results show no statistically significant difference between FFs and NFFs. Although NFFs scored somewhat higher on average (59.94 vs 55.27), the gap of 4.67 points did not reach significance (F = 3.26, p = .072, partial η² = 0.011). This indicates that both ownership types engage similarly in external-facing CSR activities, such as community engagement (see Table 3 for the ANCOVA results).

ANCOVA Results for Internal and External CSR by Ownership Type.

Partial η² indicates effect size (Cohen’s benchmarks: 0.01 = small, 0.06 = medium, 0.14 = large).

Comparison by ESG Categories

The study conducted ANCOVA tests to identify significant differences among the 10 categories that comprise the E, S and G pillars. The environment pillar encompasses resource use, emissions and innovation. NFFs scored significantly higher than FFs in terms of resource use practices. The adjusted mean was 74.46 for NFFs and 60.02 for FFs, a gap of 14.44 points (F = 17.64, p < .001, partial η² = 0.057). This indicates a moderate effect size, suggesting that ownership type has a significant influence on energy efficiency and resource management. For emissions, NFFs again outperformed FFs, with the adjusted mean of 73.27 and 62.46, respectively. The 10.81-point gap was statistically significant (F = 14.55, p < .001, partial η² = 0.048). This represents a moderate effect size, underscoring the stronger environmental reporting and emission-reduction initiatives among NFFs. In contrast, no significant differences in ownership emerged regarding environmental innovation. NFFs reported a slightly higher adjusted mean (30.99) than FFs (27.76), but the 3.23-point difference was not significant (F = 0.55, p = .458, partial η² = 0.002). This suggests that both types of firms engage at similar levels in environmental innovation initiatives.

The social pillar comprises workforce, human rights, community and product responsibility categories. NFFs demonstrated significantly higher workforce-related CSR practices compared to FFs. The adjusted mean was 79.94 for NFFs and 63.09 for FFs, yielding a gap of 16.85 points (F = 27.62, p < .001, partial η² = 0.087). This represents a moderate to large effect size, suggesting that ownership type has a strong influence on employment practices, workplace policies and employee relations. The human rights category also indicates a significant ownership effect. NFFs scored an adjusted mean of 74.97, while FFs scored 44.46, a gap of 30.52 points (F = 86.73, p < .001, partial η² = 0.230). This is a large effect size, showing that NFFs engage far more actively in upholding and reporting on human rights standards compared to FFs. By contrast, no significant differences in ownership were observed in community-oriented CSR practices. NFFs and FFs reported similar adjusted mean (75.28 vs 75.75), with a small gap of –0.47 points (F = 0.02, p = .893, partial η² = 0.000). This suggests that both ownership types engage in community engagement activities at similar levels. Likewise, ownership type did not significantly affect product responsibility. NFFs scored slightly higher (57.46) than FFs (55.21), but the 2.25-point difference was not statistically significant (F = 0.44, p = .510, partial η² = 0.001). This indicates comparable levels of attention to product safety, quality and customer-related responsibilities across ownership forms.

The governance pillar comprises the CSR strategy, management and shareholder categories. NFFs scored significantly higher than FFs on CSR strategy. The adjusted mean was 76.03 for NFFs and 62.35 for FFs, a gap of 13.68 points (F = 15.57, p < .001, partial η² = 0.051). This reflects a moderate effect size, indicating that ownership type has a significant influence on the development and disclosure of formal CSR strategies. In management, no significant differences were observed. NFFs reported a slightly higher adjusted mean (61.93) compared to FFs (55.79), but the 6.14-point gap was not statistically significant (F = 2.38, p = .124, partial η² = 0.008). This indicates broadly similar levels of management governance practices across ownership types. Likewise, no statistically significant ownership effects were found in the shareholder dimension. FFs scored marginally higher (46.21) than NFFs (40.52), but the 5.69-point difference was not significant (F = 1.83, p = .177, partial η² = 0.006). This suggests comparable practices in shareholder rights and engagement across both ownership types.

Within-family Firm Analyses (H4)

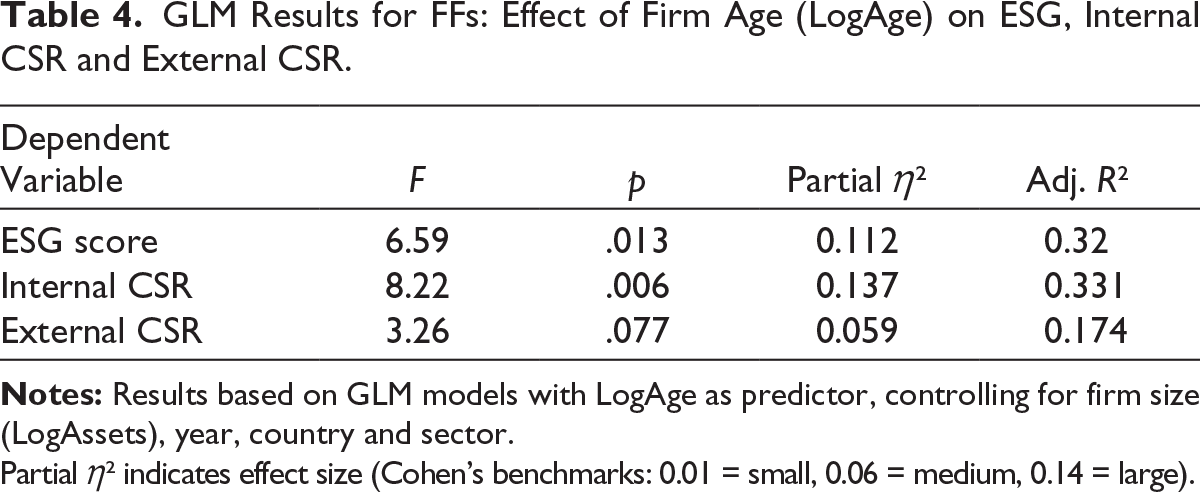

The study examined whether firm age was associated with CSR outcomes among FFs. Results show that LogAge was positively and significantly related to internal CSR (F = 8.22, p = .006, partial η² = 0.137), suggesting that older FFs are more actively engaged in capability-intensive practices such as resource use, emission reduction, workforce management, human rights, governance management and shareholder relations. By contrast, LogAge was not significantly associated with external CSR (F = 3.26, p = .077, partial η² = 0.059), indicating that community and outward-facing initiatives are not systematically related to organisational maturity. For overall ESG performance, LogAge was again significant (F = 6.59, p = .013, partial η² = 0.112), reinforcing that age strengthens ESG primarily through its effect on internal domains. Country and sector effects were consistently significant across all models (see Table 4).

GLM Results for FFs: Effect of Firm Age (LogAge) on ESG, Internal CSR and External CSR.

Partial η² indicates effect size (Cohen’s benchmarks: 0.01 = small, 0.06 = medium, 0.14 = large).

Discussion

The study locates the family–non-family CSR difference in Latin American public markets within the firm. NFFs outperform FFs in capability-intensive internal CSR, while external CSR is comparable, and governance shows parity once controls are taken into account. This composition reconciles mixed prior findings: FFs may preserve legitimacy through outward activities and formal governance, yet lag in sustained operational upgrading, which demands organisational processes, information systems and cross-functional execution. The positive age gradient within FFs suggests the accumulation of capability over time and a pathway to convergence.

FFs and NFFs in the Overall ESG Score and E, S and G Pillars (H1)

The analysis reveals that ownership type is significantly associated with ESG outcomes in Latin American listed firms, although the differences are uneven across various dimensions. NFFs consistently outperform FFs on overall ESG, with gaps concentrated in the environmental and social pillars, while governance shows no significant variation once controls are included.

The environmental pillar results indicate that NFFs achieve stronger outcomes in emission reduction, resource use and related operational practices. This supports the argument that environmental improvements require capability-intensive processes, for which NFFs may be better positioned to develop. FFs, while motivated by SEW considerations, may underinvest in these less-visible internal routines, especially in contexts where institutional enforcement is weaker.

Similarly, the social pillar gap, the largest observed difference, suggests that NFFs excel in workforce and human rights practices. This finding reinforces the view that capability accumulation, often linked to organisational scale and professionalisation, is crucial for embedding systematic employee-oriented policies. For FFs, reputational and legitimacy concerns may drive outward-facing CSR efforts, but the sustained, process-heavy investments required for social practices appear more challenging.

By contrast, the governance pillar parity suggests that FFs and NFFs converge in this domain, likely due to regulatory requirements, listing standards and external monitoring in public markets. Governance, as a more formalised and standardised area, may be less susceptible to ownership effects compared to capability-intensive CSR domains.

Taken together, these results refine the application of SEW and legitimacy perspectives in Latin America. FFs appear motivated to preserve SEW and legitimacy, but in practice, this translates more into symbolic or outward-oriented CSR than into internal, capability-intensive improvements. By contrast, NFFs, with stronger access to professionalised management and resources, achieve higher performance in environmental and social domains. This dynamic helps explain why prior research in Europe found FFs leading on internal CSR (Rivera-Franco et al., 2024), while our findings in Latin America highlight their relative disadvantage in capability-heavy ESG practices.

Internal and External CSR (H2 and H3)

The findings for internal and external CSR provide further insights into how ownership type influences sustainability practices in Latin American listed firms. The results reveal a pronounced divergence in internal CSR, with NFFs scoring significantly higher than FFs, indicating a moderate-to-large effect size. This suggests that NFFs are better positioned to implement and institutionalise capability-intensive practices related to workforce management, workplace standards and human rights. These outcomes align with arguments that NFFs benefit from greater professionalisation, formalisation and broader stakeholder accountability mechanisms, which enable sustained investment in employee-oriented policies; financial strength also acts as a catalyst for CSR performance (Basly & Cano-Rubio, 2024; Khattak et al., 2021).

By contrast, external CSR activities did not differ significantly between ownership types. This finding suggests that FFs and NFFs converge in their external CSR commitments, likely because these activities are more visible, symbolic and directly linked to legitimacy and reputation in the eyes of external stakeholders. For FFs, such outward-facing initiatives may resonate with SEW preservation motives, enabling them to demonstrate responsibility without the same capability investments required for internal CSR.

Taken together, these results reinforce the distinction between capability-intensive versus legitimacy-oriented CSR. NFFs outperform in internal domains where systems, resources and professional structures are critical, whereas FFs remain equally active in external domains that allow them to preserve reputation and legitimacy without large-scale organisational transformation. These patterns align with prior findings in emerging economy contexts, which emphasise the visibility–capability trade-off in CSR implementation (Rahmann Belal & Momin, 2009). The findings also resonate with recent evidence on emerging multinationals, which shows that resource constraints and legitimacy pressures can shift attention away from internal CSR and towards outward-facing activities (Bu & Chen, 2023). In this Latin American sample, FFs appear to follow a similar logic, privileging external legitimacy over internal capability building.

Ownership Effect on ESG Categories

The category-level analyses provide further details on the ownership–ESG relationship. For the environmental categories, NFFs significantly outperformed FFs in both resource use and emission management, with moderate effect sizes. These findings reinforce the view that capability-intensive practices, which require systems for monitoring, efficiency and operational adaptation, are more readily adopted by NFFs with stronger, professionalised structures. In contrast, no ownership difference was observed in environmental innovation, suggesting that both FFs and NFFs face similar constraints in pursuing innovation-led sustainability, particularly in emerging market contexts where technological and financial barriers are high (Del Sarto & Ozili, 2025; Torres de Oliveira et al., 2022).

Within the social categories, the strongest gaps emerged in the workforce and, especially, in human rights, where NFFs substantially outperformed FFs. The significant difference in human rights practices highlights the resource and organisational intensity required to implement robust compliance systems, which NFFs appear better equipped to sustain. By contrast, no significant differences were found in community engagement or product responsibility, areas that are more visible to external audiences. These results suggest that FFs remain competitive in outward-facing CSR domains that protect SEW and legitimacy but lag in more demanding internal practices.

The governance categories present a more mixed picture. NFFs scored significantly higher on CSR strategy, indicating greater emphasis on formalised planning and integration of sustainability into governance frameworks. However, no differences were observed in management- or shareholder-related practices, suggesting convergence between FFs and NFFs in these standardised governance mechanisms. This likely reflects the role of regulatory requirements, market oversight and listing standards, which create a level playing field across ownership types (Khatri & Kjærland, 2023; Medina et al., 2022).

Taken together, these category-level results strengthen the argument that ownership differences in Latin America are most pronounced in capability-intensive domains, such as environmental management, workforce and human rights, while symbolic or externally visible domains, such as community and product responsibility, show convergence. FFs appear to prioritise legitimacy-preserving CSR efforts over the systematic, resource-heavy investments required for deeper internal transformation. This pattern refines the SEW and legitimacy perspectives by highlighting the boundary conditions under which FFs can sustain competitive CSR practices in emerging market contexts.

The findings diverge from recent European evidence, which has shown that FFs outperform NFFs in internal CSR (Rivera-Franco et al., 2024). This contrast underscores the importance of institutional environments in shaping CSR trajectories. In Europe, strong regulatory frameworks, stakeholder protections and established governance codes create incentives and support structures that enable FFs to professionalise internal processes and build CSR capabilities over time. By contrast, the Latin American context is characterised by weaker institutional enforcement, higher informality and resource constraints, which limit the ability of FFs to develop capability-intensive practices. As a result, Latin American FFs appear relatively less equipped to sustain strong internal CSR compared to their non-family peers, but remain competitive in external CSR, where legitimacy pressures and reputational concerns play a more immediate role. This divergence suggests that the visibility–capability trade-off is context-contingent and that ownership effects on CSR must be understood in relation to the institutional infrastructures that support or constrain organisational capacity building.

Within-family Firms’ CSR Practices (H4)

The within-FF analyses provide important details about the ownership–CSR relationship. Consistent with the author’s expectations, firm age was positively associated with internal CSR performance, indicating that older FFs are more likely to invest in capability-intensive practices such as workforce management, human rights, environmental processes and governance routines. This supports the argument that organisational maturity and accumulated experience facilitate the institutionalisation of internal CSR systems, which require time, resources and formalisation to be fully embedded. By contrast, firm age was not significantly related to external CSR, suggesting that community engagement and outward-facing initiatives are not dependent on the maturity of FFs. This distinction aligns with the capability versus legitimacy trade-off: while internal CSR strengthens with accumulated organisational capacity, external CSR reflects more symbolic, legitimacy-driven commitments that even younger FFs may adopt to preserve SEW. Taken together, these results reinforce the argument that CSR trajectories within FFs grow stronger internally as firms age, while external initiatives remain largely consistent across generations.

Institutional Effects

A key finding is that country and sector effects explain substantial variance in CSR outcomes, often with large effect sizes. This finding is consistent with recent comparative work, which shows that the CSR priorities of public FFs vary systematically across national contexts, underscoring that institutional scaffolding strongly shapes category-level outcomes (Bravo Monge & Starcevic, 2025). At the same time, our analyses demonstrate that ownership effects persist even after accounting for these institutional forces. In particular, the internal–external CSR distinction holds robustly across countries and sectors, suggesting that the visibility–capability trade-off is not merely an artefact of national or industry differences, but reflects a systematic pattern associated with family ownership. In other words, institutional context sets the baseline for CSR engagement, but ownership type influences the composition of that engagement.

Contribution, Implications and Future Research

This study advances the family-business and CSR literature in four ways. First, it shifts the debate from levels to composition, showing that ownership is associated with where CSR resides: NFFs lead in internal, capability-intensive practices, while external activities are statistically comparable, and governance shows parity. Second, it integrates SEW/legitimacy with capability-based views, proposing a visibility and capability lens that explains why motives to appear responsible need not translate into operational upgrades without the requisite routines. Third, it provides contextual evidence for Latin American listed firms, utilising year, country and sector fixed effects, as well as size/age controls. This analysis also clarifies a methodological point: in small-N country panels, country fixed effects outperform linear institutional indices in isolating ownership associations. Fourth, it contributes to measurement discipline by mapping CSR into internal versus external composites (with robustness to alternative classifications) and identifies a within-family maturity effect (age leads to stronger internal CSR), yielding actionable guidance for owners and boards seeking to close the internal CSR gap.

The implications are twofold. For family owners and boards, the findings highlight the importance of investing in internal capability building that embeds ESG practices into daily operations. For policymakers, they suggest that standards and incentives emphasising operational outcomes, rather than disclosure alone, are more likely to reduce ownership-related gaps.

Several limitations merit attention. The study’s observational design cannot establish causality. Although it controls for size, age, year, country and sector, unobserved firm-level characteristics may still bias the results. Additionally, the reliance on publicly listed firms raises concerns about potential endogeneity. First, listed FFs may be systematically different from non-listed firms in ways that affect CSR (e.g., they may be larger, more diversified or more exposed to capital market pressures). Second, survivorship bias could be present, as only firms that persisted long enough to be included in ESG databases are observed. Third, they represent only a small fraction of the family business population in Latin America. Listed firms are typically larger, more internationalised and subject to stronger disclosure pressures than privately held FFs. These factors limit the generalisability of the findings and suggest caution in drawing causal inferences. Future research should examine whether the visibility–capability trade-off observed here also applies to private FFs, which may face different institutional pressures and resource constraints. In addition, the results showed that country and sector effects explained substantial variance in CSR outcomes, highlighting the importance of institutional context.

Future research should extend the analysis in three directions. First, studies could examine whether the visibility–capability trade-off identified here applies to private FFs, which face distinct resource constraints and institutional pressures. Second, scholars could explicitly test how national governance systems, cultural expectations and industry logics interact with ownership type to shape CSR, thereby enriching comparative understanding across emerging economies. Third, future work could explore moderators within FFs, such as professionalisation, innovation orientation or generational stage, that may accelerate or hinder the accumulation of internal CSR capabilities.

Conclusion

In Latin American listed firms, family ownership is associated not with uniformly higher or lower CSR, but with a different composition. NFFs lead in internal, capability-intensive practices, while external activities and formal governance are broadly comparable across ownership types. This pattern suggests that the CSR gap for FFs in the region is less about external signalling and more about building the internal capabilities that underpin operational excellence. The findings reinforce the visibility–capability trade-off and highlight that ownership effects on CSR are institutionally contingent: in weaker governance environments, FFs may be slower to professionalise internal processes. For scholars, this study contributes to understanding how ownership interacts with institutional contexts to shape CSR trajectories; for practitioners, it points to the importance of capability building as the route to closing the CSR gap.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.