Abstract

Jet Airways (India) Private Limited, one of India’s finest and largest private aviation companies commanded the Indian skies until 2005. On 5th May 1993, it began commercial operations. Five of the seven airlines that had been launched since 1992 had been grounded by the year 1997. It began with a fleet of four leased Boeing 737–300 planes. In the early 2000s, it surpassed the market leader, state-owned Indian Airlines, in passenger volume. Jet Airways was granted authorization to conduct international flights in 2003. However, as a result of changing market dynamics, Jet Airways became a victim of its own success. The corporation is in billions of dollars of debt, and the company’s closure has harmed almost 20,000 people. Porter’s Five Forces Framework and SWOT Analysis have been applied to interpret the strategic trajectory explaining characteristics in its different phases. This case examines the aspects that contributed to the end of one of India’s greatest airlines. The study’s observations provide a conclusion report on the challenges encountered by airlines. Moreover, a glimpse of the rise and fall of some of the major airlines is also highlighted.

Introduction

Since the 1980s the global airline industry has experienced the trend of deregulation with the elimination of restrictions on routes, frequency and fares. The domestic airline industries, as a whole, which normally carry about two-thirds of the air passengers moved by the global airline industry, were also subject to the forces of the emerging changes in LPG (Liberalization, Privatization and Globalization). In India, after the nationalization of Air India in 1953, the Indian government heavily regulated its airline industry till the 1980s by placing restrictions on foreign private sector participation in domestic commercial airlines. India’s Open Sky Policy of 1990 and the Air Corporations (Transfer of Undertakings and Repeal) Act of 1994 freed up the Indian civil aviation industry to a great extent (Government of India, 1994). The monopoly of government-owned airlines (Air India Ltd. and Indian Airlines Ltd.) has no longer existed since then. The changes in Indian aviation were made as a response to following global trends across industries and to make adjustments to India’s approaches toward economic development. Though it is challenging to study the business history of an industry (Mohanty & Augustin, 2014), this study tries to find the rise and fall of Jet Airways over a period of time.

When the Government of India allowed private sector companies to provide air taxi service, a number of players—Jet Airways, Air Sahara, Damania Airways, East West Airlines, ModiLuft and NEPC Airlines, made entry into the civil aviation space. Out of these, Jet Airways only in its earlier avatar could serve till 2019. With the largest aviation takeover in India in 2006 (when Air Sahara was bought by Jet Airways), Jet Airways became the largest domestic player in 2007 outpacing its public sector competitor Indian Airlines. However, the acquisition caused a huge drain on the financial resources of Jet Airways. To make the matter complicated there were issues of pilots’ strikes, retrenchment, pay cuts and stiff competition in terms of low airfares from low-cost carriers (LCC), which was triggered by Air Deccan. There was a gradual passenger shift from legacy full-service (FSA–Full Service Airlines) to low-cost airlines. The competition was quite intense. Jet Airways started falling. It dropped to second place behind IndiGo in October 2017, with a passenger market share of 17.8% from 42% in 2000–2001. The downward slide continued and ultimately it resulted in bankruptcy in 2019 (Adhikari, 2018).

Before suspending operations in April 2019 due to mounting losses, Jet Airways was present in more than 65 destinations in India and across the world—Europe, the Middle East, Southeast Asia, and North America, with hubs in Mumbai, Delhi, Bengaluru, and gateways in Amsterdam, Paris, London, and Abu Dhabi. However, a series of strategic mismatches led to its closure. Lenders to Jet Airways decided to refer the company to National Company Law Tribunal (NCLT) for bankruptcy proceedings with a debt of $1.2 billion. Insolvency proceedings were initiated against Jet Airways under Insolvency and Bankruptcy Code (IBC), 2016. As per the provisions of the Code, on 24th June 2019, a public announcement was made by the court-appointed officer to manage the affairs during insolvency, inviting all claimants to submit their claims. After several rounds of bidding, the Jalan-Kalrock Consortium emerged as the successful resolution applicant for Jet Airways in June 2021, giving the airline a new lease of life and paving the way for its revival. Jet Airways’ AOC (Air Operator Certificate) was revalidated on May 20, 2022, allowing the airline to recommence commercial operations (Jet Airways, n.d.).

Historical Background and Liberalization in Indian Civil Aviation

Scheduled airline services in India began on 15th October 1932 when Air India Ltd. founder JRD Tata, a leading industrialist, flew a plane from Karachi to Bombay via Ahmadabad. It was the first airline in India, commenced operation as Tata Airlines. Tata Airlines was converted into a public company on 29th July 1946. On 8th June 1948, Air India Ltd. started its international services from Mumbai to London via Cairo. On 1st August 1953, the Indian parliament passed the Air Corporation Act 1953 and took over Air India in partial fulfilment of Industrial Policy requirements and the ideals of a mixed economy regime. Two autonomous corporations were created- Indian Airlines for domestic and regional operations and Air India for overseas services. The airline industry has a great impact on an economy as it creates jobs, facilitates geographical connections; and enables the flows of trade, tourism, and investment. The Ministry of Civil Aviation and the Office of Director General of Civil Aviation, Government of India are the main policy-making bodies for the development and governance of the civil aviation sector in India.

In civil aviation, an Open Sky Policy means liberalization and ease of access to national airports for foreign airlines with an intention to increase the tourist flow and develop the potential as a regional air hub. The Government of India with its Open Sky Policy of 1990, allowed air taxi operations from any airport throughout India. The market trend towards availing air journeys was favourable that attracted private players. These reforms ultimately made the private players quite impactful, and later on, completely changed the ways the airlines operated in the post liberalized scenario.

Until 2012–2013, Airports Authority of India (AAI) was the only major player involved in developing and upgrading airports in India. Post liberalization, private sector participation has been increasing. Major private sector players include Larsen & Toubro, Adani Group, GVK, Siemens, GMR Group. In 2004, the Indian government liberated further its aviation policy to allow scheduled Indian carriers to commence international operations—Jet Airways, Air Sahara responded to this change along with state-owned Indian Airlines.

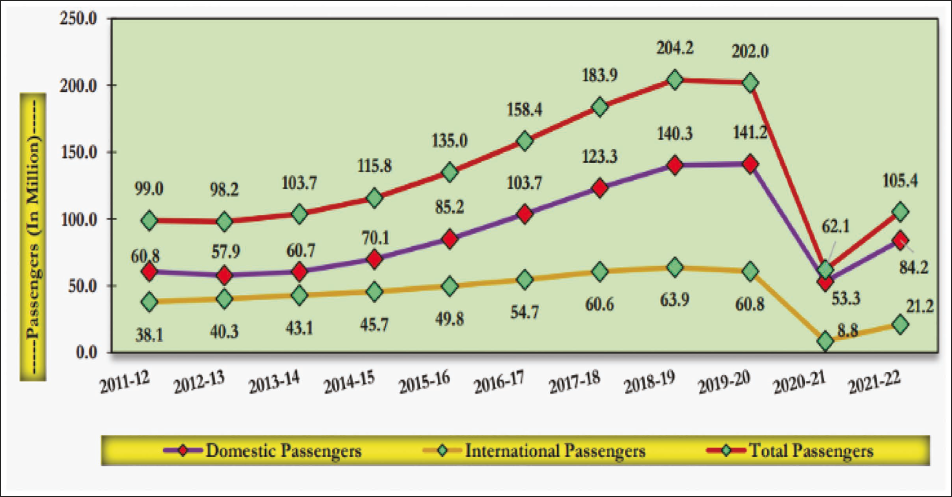

For the reforms in the aviation sector, there was a matching PLF (Passenger Load Factor). In commensuration with the supply side, demand also increased steadily, though the upward growth of air traffic in India was halted by the outbreak of COVID-19 as shown in the chart below.

Due to the COVID-19 pandemic, the global airline industry’s net losses were forecast to amount to some $118 billion in 2020, and to decrease to $38 billion in 2021 (IATA Economics, 2020). The airline industry experienced the biggest blow since the Second World War. Due to COVID-19, the drop in demand was much greater than in previous crises, such as the 2008 financial crisis, or the one caused by the terrorist attacks of September 11, 2001, in New York.

On 30 October 2022, a historic day for India, the Prime Minister laid the foundation stone of a facility in Vadodara, Gujarat for manufacture of medium size military transport aircraft under a Tata Group (Tata Advanced Systems Ltd. which has an industrial partnership with Airbus) sponsored project being executed in cooperation with European aerospace major Airbus. The aircraft can be used for civilian purposes as well. The PM envisioned that the day would not be far when India would manufacture big commercial planes with the mantra of ‘Make in India and Make for the Globe’.

Before liberalization, there was a capacity constraint, however, airfare was high. Now, in the post-liberalized scenario, India is poised to move from the current seventh-largest player in aviation market to the third-largest after China and USA within the next 10 years. All these developments apparently indicate opportunities for Jet Airways in its new avatar. However, there are important learning lessons in the rise and fall of its previous avatar.

The Rise and Fall of Jet Airways

After three and a half decades of monopoly by Air India and Indian Airlines, the Indian government reopened the domestic aviation market to private carriers in April 1989. This provided an opportunity for Naresh Goyal to establish Jet Airways (India) Private Limited in 1991. It commenced commercial operations on 5ft May 1993. By 1997, five of the seven airlines that had been launched since 1992 were grounded. It progressed rapidly and overtook the market leader; state-owned Indian Airlines in passenger volume in the early 2000s. Jet Airways obtained permission to operate international flights in 2003. Colombo, Sri Lanka, was the first such international destination. With the motto ‘We don’t fly aircraft, we fly people’, Jet Airways was flying high. From a 6.6% market share in 1993–1994, the market shares of Jet Airways rose to 42% in 2000–2001.

Possibly excited by this euphoria, the management made its first big gamble by eying Air Sahara in 2006. In order to realize its high growth aspirations, Jet acquired Air Sahara. Naresh Goyal struck a deal in 2007 to buy Air Sahara for Rs 1,450 crores. Acquiring Sahara meant a huge drain on Jet’s resources, not only on financials but on other alignments of management as well. All this happened at a time when the concept of LCC was completed two years ago in India. The domestic aviation market was growing at 30%–40% and players like Air Deccan, a new entrant in the LCC segment, were challenging the might of full-service carriers.

After the acquisition, Air Sahara’s name was not retained. Jet went for brand extension. On 16th April 2007, Air Sahara was renamed as Jet Lite which became a wholly owned subsidiary of Jet Airways. Sahara was rebranded as Jet Lite with a strategic intention of reducing frills but going beyond LCC in terms of service. Jet Airways launched another low-cost airline Jet Konnect in 2009 as a part of a strategic rebranding and restructuring exercise. The Jet-Sahara merger was expected to bring synergies and benefits like a complete parking bay; Airport infrastructure dominance; cost savings by improving economies of scale; a larger operational base; increased prime-time departures and frequencies.

Post-merger operating margin of Jet Airways dwindled from 33.2% to 5.2%; Gross Profit declined from 24.5% to 6.4% in 2009. However, the strategic management of Jet Airways attributed the declining performance to lean periods, low yield, and pilot strikes. Whatever the extraneous factors, Sahara acquisition resulted in a huge drainage of Jet fund. Moreover, the airline received serious setbacks in its HR and public relations as well.

Without getting adequately involved in the exercise, employees of Jet Airways (1900 numbers) were sacked in 2008. The retrenchment move resulted in a severe backlash not just from employees but also from the government, political parties and regulatory bodies who forced the airline to take back the sacked people. In a dramatic response, Jet Airways chairman Naresh Goyal, in a press conference said his airline would take back each and every one of the 1,900 sacked Jet employees because he understood their pain and ‘would not be able to sleep peacefully’ if he did not reverse the retrenchments.

‘I apologize for all the agony that you went through’—the statement of Mr Goyal was directed at the retrenched staff. All these ultimately resulted in public outcry, mockery and HR-PR disaster. The employees had to be reinstated urgently. ‘While the mishandling of the Jet Airways sacking and reinstatement of 1,900 employees was an HR and PR disaster, the larger implications of what happened are also worth considering. It is not just that the chairman of India’s most successful airline became the butt of jokes, it is also a question of what he knew, when he knew it, and who did the bungling.’ -Anjuli Bhargava, a Columnist remarked in this regard

To complicate matters further, there were other issues of industrial relations. The pilots went on strike. The management’s decision to refuse to take back two pilots who were sacked amounted to a cost to the company at almost Rs 15 crore a day. The passengers of Jet Airways were facing agonizing and painful times as the airline cancelled over 200 flights, though it tried to re-accommodate its stranded passengers on flights of other airlines. It readily refunded the airfare of the remaining ones who could not be re-accommodated.

All these indicate, the organizational climate was not congenial, let alone the financial inadequacies. Jet Airways suffered losses for the first time since its establishment in the financial year 2001–2002 as demand fell and costs increased. Lowering ticket fares by the competitors in the following years, Jet was forced to follow suit, hurting overall performance resulting in steep financial losses. In 2008, the airline was forced to discontinue international routes because these attracted losses due to the global economic downturn. Market share started falling more. It dropped to second place behind IndiGo in October 2017, with a passenger market share of 17.8%.

Adding to these, on 12 December 2001, an internal memo from the Indian intelligence agencies; to the Indian home ministry stated that they had evidence that Jet Airways had intermittent contact with the Indian underworld related to financial transactions. Subsequently, in 2016 (15 years later), reports surfaced that the initial investment for Jet Airways was heavily funded by the Indian underworld. The lack of financial transparency resulted in low credibility and an adverse image.

As in November 2018, Jet Airways was reported to have a negative financial outlook due to increasing losses. In March 2019 it was reported that nearly a fourth of Jet Airways’ aircraft were grounded due to factors like unpaid lease rates and non-payment of dues to Indian Oil Corporation Ltd. Lenders rejected the proposal of emergency funding. On 17 April, the airline suspended all flight operations, due to lenders rejecting Rs 4 billion of emergency funding. Lenders led by the State Bank of India were making efforts to find a resolution for Jet Airways outside India’s IBC; however, it did not yield results. The lenders resolved to seek a resolution within the IBC process and on 17 June, they decided to refer the company to NCLT for bankruptcy proceedings with debt of $1.2 billion, to find a buyer for the stranded airline or recover any of their dues from the sale of any remaining assets. The insolvency proceedings were initiated against Jet Airways under IBC, 2016 in June 2019.

As the Auditors warned, once the largest private airline in the country, Jet Airways’ wings were clipped. On 24th June 2019, a public announcement was made by the court-appointed officer (to manage the affairs during insolvency) inviting all claimants to submit their claims. After several rounds of bidding, the Jalan-Kalrock Consortium emerged as the successful resolution applicant for Jet Airways in June 2021, giving the airline a new lease of life and paving the way for its revival. Jet Airways AOC was revalidated on 20th May 2022, allowing the airline to recommence commercial operations. The Jalan Fritsch Consortium is a consortium of Mr. Murari Lal Jalan (a Non-Resident Indian based in the United Arab Emirates) and Mr. Florian Fritsch, the former being the lead Partner. Mr. Jalan will hold shares in the Corporate Debtor in his personal capacity and Mr. Florian Fritsch will hold shares therein through his investment holding company. The new management of Jet Airways is quite hopeful about its successful revival as a ‘smart full-service carrier’. Given the complexities in Indian aviation, the task is gigantic which requires an all-out holistic effort. Financial prudence is of paramount importance. Jet Airways had reported erosion in net worth for a standalone net loss of Rs. 308.24 crore for the quarter ending on 30th September 2022.

India’s aviation industry is largely untapped with huge growth opportunities, considering that air transport is still expensive for the majority of the country’s population, of which nearly 40% is the upwardly mobile middle class. Ensuring sustainability of the individual players to realize sales potential in the demand fulfilment area has remained a major concern, historically too.

To that extent, a glimpse of the rise and fall of some of the major airlines may sound helpful.

Literature Review

The following are some of the studies which can highlight the strategic implications of business models in speculative industries. The following studies will provide some useful insight.

Amit and Zott (2012), in their studies, stated that companies are increasingly adopting business model innovation as an alternative to product or process innovation. A business model is a system of interconnected activities that determines how a company conducts business with customers, partners, and vendors. Innovation can occur through adding novel activities, linking activities in novel ways, or changing parties performing activities. The authors suggest six questions for executives to consider when considering business model innovation: what perceived needs can be satisfied through the new model design, what novel activities are needed to satisfy these needs, how value is created through the novel business model, and what revenue model fits with the company’s business model.

Høgevold et al. (2015) study tests the Triple Bottom Line (TBL) construct and discusses the reasons for implementing sustainable business practices in companies and their networks. The quantitative research focuses on companies in different Norwegian industries and finds that a higher propensity for sustainable practices ensures a better organization’s ability to integrate TBL. It also provides insights into the general status of business-sustainable practices and contributes to a TBL construct.

Mohanty and Augustin (2014) state that the case research on Mahindra Group provides a comprehensive exploration of its business strategies and historical evolution using qualitative research. The study uses the Greiner model to capture the complexities and dynamics of its organizational development. The research outlines several key phases of growth in M&M’s history, as mapped onto the Greiner model. These phases include creativity, direction, collaboration, alliances, and innovation and transformation. The Mahindra Group’s journey demonstrates strategic growth and adaptability in a complex and evolving business environment. This case study provides insights into M&M’s strategic manoeuvres and serves as a valuable reference for understanding business growth in emerging markets.

Vintergaard (2004) article ‘Corporate Venturing: Recognition and Discovery of Investment Opportunities’ provides a comprehensive framework for understanding how corporate venture managers recognize and discover investment opportunities in a network environment. The article, grounded in Austrian economics, emphasizes that entrepreneurial opportunities are not pre-packaged but are recognized and discovered through a collective process involving multiple actors. The article provides a case study of PMC Porous Media Combustion GmbH, illustrating the practical application of the conceptual framework. The study finds that recognizing and discovering opportunities is a collective process involving multiple actors, including corporate venture capitalists, who have access to extensive information and resources. The article emphasizes the importance of strategic management and a networked approach in managing entrepreneurial opportunities within established firms.

Research Methodology

Qualitative research has been applied to describing and exploring the historical evolution of the strategy of Jet Airways. Qualitative research is an inquiry process of understanding a host of organizational problems, formed with words, reporting detailed views of informants. It is characterized by its aims, which relate to understanding some aspect of organizational history, and its strategies, which in general generate words, rather than numbers, as data for analysis (Mohanty & Augustin, 2014). The research method involves a comprehensive secondary study of Jet Airways and provides all the reasons and causes for the downfall of the airline. By utilizing a variety of sources, including documents, articles, case studies and archival records these studies are intended to produce a thorough analysis of the case with the help of Porter’s Five Force Framework and SWOT Analysis.

Objectives of the Study

The present study builds upon previously carried research in the aviation industry, particularly Jet Airways and has focused on the key theoretical frameworks with respect to Porter’s Five Forces Analysis and SWOT Analysis, elucidating their relevance and application to the present case study of Jet Airways.

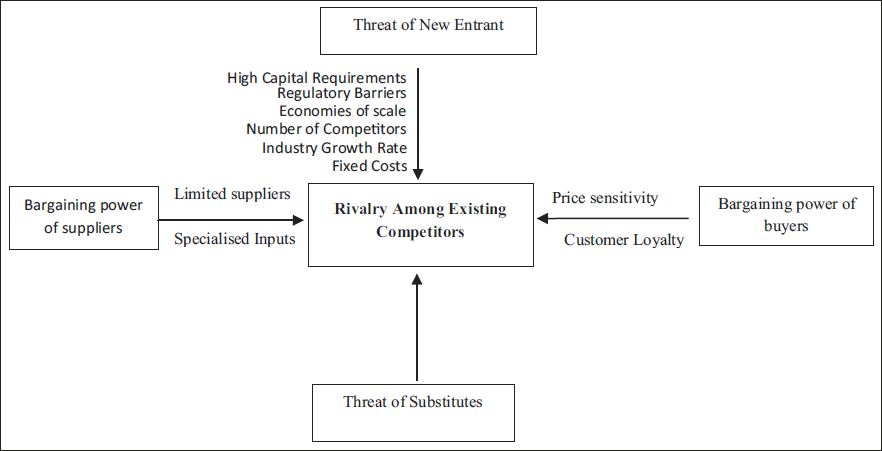

Examination of the Strategy Through Porter’s Five Forces Framework

Porter’s Five Forces framework, developed by Michael E. Porter in 1979, is a powerful tool for analyzing the competitive forces that shape industries and determine their profitability. The framework identifies five key forces that influence competition and profitability in any industry: Threat of New Entrants, Bargaining Power of Suppliers, Bargaining Power of Buyers, Threat of Substitutes, and Rivalry Among Existing Competitors.

Threat of New Entrants: This force examines how easy or difficult it is for new competitors to enter the industry. New entrants can potentially force existing companies out of the market (Porter, 2008). Some barriers to entry include increasing customer switching costs by building brand loyalty and creating unequal access to distribution channels, which hinders new entrants from achieving supply chain efficiency. Another strategy to counter the threat of new entrants is aggressive marketing through price cuts. Factors affecting this threat include capital requirements, regulatory policies and economies of scale.

Bargaining Power of Suppliers: This force assesses the power that suppliers of raw materials, components, labour, and services have over the firm. High supplier power can erode industry profitability by increasing costs. Influential suppliers can increase their own value by raising prices, reducing the quality or level of services, or transferring costs to industry participants. These actions can significantly erode the profitability of industries unable to pass these costs onto their customers (Porter, 2008). Suppliers exhibit substantial power when they are few in number, provide unique products, and can credibly threaten to move forward in the supply chain.

Bargaining Power of Buyers: This force analyzes the power of customers to influence pricing and quality. When buyers have high bargaining power, they can demand lower prices or higher quality, impacting industry profitability. In certain sectors, buyers wield significant power, particularly when the industry has a few buyers purchasing in large volumes, which is especially impactful in industries with high fixed costs. Buyers also hold substantial power when industry products are standardized, and when switching costs for buyers are low (Porter, 2008). The influence of buyers can be mitigated by increasing their switching costs, fostering brand loyalty, or differentiating products to add value and shifting purchasing decisions from being price-based to product-based (Recklies, 2015).

Threat of Substitutes: This force considers the likelihood of customers finding alternative ways of fulfilling their needs. The presence of substitutes can limit the prices that companies can charge. The threat of substitutes is significant when there is a favourable price-performance trade-off or when buyers face low switching costs. While this might appear easy to mitigate, it is often complex because firms are not always aware of all potential substitutes (Porter, 2008).

Rivalry Among Existing Competitors: This force examines the intensity of competition among existing firms in the industry. High rivalry can limit profitability as companies engage in price wars, advertising battles, and product innovations. Intense rivalry typically occurs in markets with slow growth or a large number of competitors and can also arise when firms cannot accurately interpret each other’s market signals. This situation resembles the Game Theory-Prisoner’s Dilemma Model, where cooperation is unlikely and one firm’s gain is another’s loss (Deng & Deng, 2015). However, rivalry can be positive-sum if each competitor targets different market segments (Porter, 2008).

Detailed Timeline and Analysis of Jet Airways Using Porter’s Five Forces

Jet Airways’ journey was blemished by a series of highs and lows, and it serves as a compelling example of both the opportunities and challenges that exist in the aviation industry. At first, it symbolized success in India’s domestic airline industry, but troubles started in 2018 when the airline deferred its quarterly financial results. This raised red flags for government regulators (Prasad, 2024). It faces numerous competitive challenges and threats that can impact its performance and profitability.

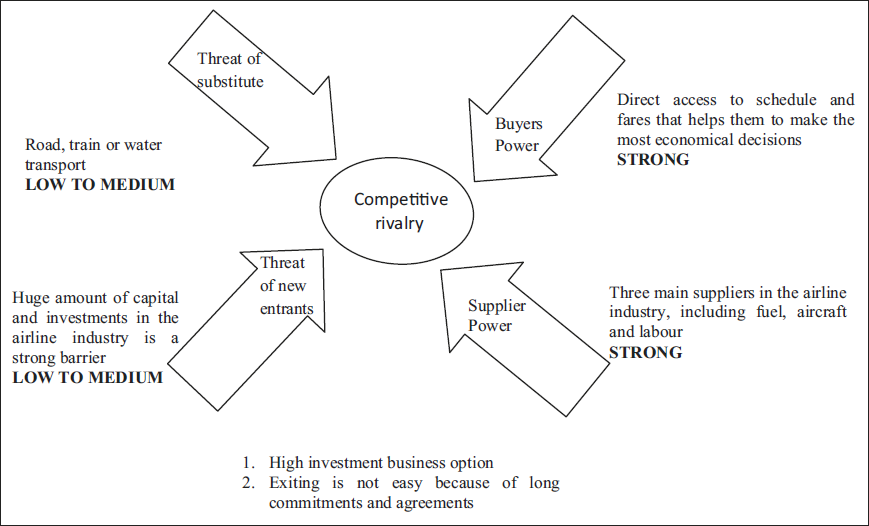

This case has examined Jet Airways’ series of highs and lows with the help of the forces of Porter’s Five Force Framework. The following Figure 1 is the review of Porter Five Forces airline industry (Airline Industry Porter’s Five Forces Analysis | EDrawMax Online, Edrawsoft n.d.):

Competition in the industry (strong force)

The threat of new entrants (low to medium force)

The bargaining power of suppliers (strong force)

The bargaining power of customers (strong force)

Threat of substitute products or services (medium force)

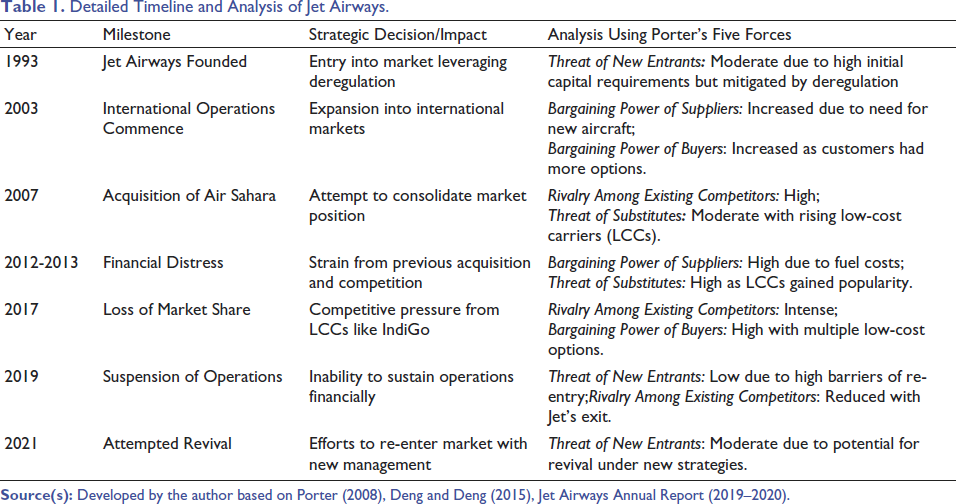

Table 1 provides a chronological overview of key milestones in the history of Jet Airways. It analyzes the strategic decisions made by the company and their impacts, using Porter’s Five Forces framework to understand the competitive dynamics at each stage.

Detailed Timeline and Analysis of Jet Airways.

The timeline of Jet Airways (Table 1) illustrates the key milestones and strategic decisions through the framework of Porter’s Five Forces framework.

Founded in 1993, Jet Airways entered the market leveraging deregulation, facing a moderate threat of new entrants due to high capital requirements.

By 2003, the airline expanded internationally, increasing the bargaining power of both suppliers and buyers due to the need for new aircraft and more customer options.

The 2007 acquisition of Air Sahara was an attempt to consolidate its market position, leading to high rivalry among existing competitors and a moderate threat from rising LCCs.

Financial distress between 2012 and 2013, exacerbated by competition and previous acquisitions, resulted in the high bargaining power of suppliers and a significant threat from substitutes as LCCs gained popularity.

By 2017, Jet Airways lost market share to LCCs like IndiGo, experiencing intense competition and high bargaining power of buyers due to multiple low-cost options.

The airline suspended operations in 2019, unable to sustain itself financially, which reduced rivalry among competitors and lowered the threat of new entrants due to high re-entry barriers.

In 2021, Jet Airways attempted a revival under new management, facing a moderate threat of new entrants with the potential for new strategies to regain market presence.

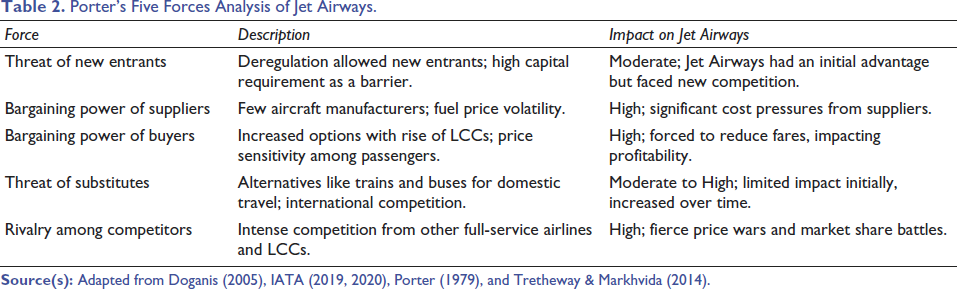

Table 2 and Figure 2 exhibits how various competitive forces have impacted the airline over time, influencing its strategic decisions and market position. (Porter, 1979; Doganis, 2005; Tretheway & Markhvida, 2014; Pfeffer, 1994; Zou & Cavusgil, 2002; DGCA, 2020; CAPA - Centre for Aviation, 2021; IATA, 2020)

Porter’s Five Forces Analysis of Jet Airways.

The threat of new entrants for Jet Airways was moderate. The deregulation of the Indian aviation sector initially made it easier for new airlines to enter the market. However, the high capital investment required for purchasing aircraft and setting up operations acted as a barrier. For instance, when Air Deccan entered the market as India’s first LCC, it heightened competition, prompting Jet Airways to modify its strategies.

The bargaining power of suppliers was significant due to the limited number of aircraft manufacturers, such as Boeing and Airbus. Additionally, fluctuations in fuel prices exacerbated cost pressures. For example, during periods of rising oil prices, Jet Airways experienced substantial increases in operating costs, affecting profitability since the airline had limited leverage to mitigate these expenses.

The bargaining power of buyers was also considerable, especially with the emergence of LCCs like IndiGo and SpiceJet. Passengers became more price-sensitive and had more options, compelling Jet Airways to reduce fares to stay competitive. This high buyer power resulted in diminished profit margins. For example, the competitive pricing introduced by IndiGo attracted a substantial customer base, forcing Jet Airways to adjust its pricing strategies.

The threat of substitutes varied from moderate to high. Initially, alternatives such as trains and buses had a limited impact on Jet Airways’ domestic routes. However, as high-speed trains and enhanced bus services became more reliable and convenient, they posed a greater threat. Additionally, for international travel, other airlines offering better prices or services became viable substitutes. For example, travellers on domestic routes between cities like Mumbai and Delhi might prefer high-speed trains over flights if they offer comparable travel times at lower costs.

Lastly, the rivalry among competitors was intense. Jet Airways faced stiff competition from both FSAs like Air India and LCCs like IndiGo. This competition resulted in fierce price wars and efforts to capture market share. For instance, during peak travel seasons, airlines would implement aggressive pricing strategies, offering significant discounts to attract passengers, thereby intensifying the rivalry. This intense competition forced Jet Airways to continuously innovate and adapt to maintain its market position.

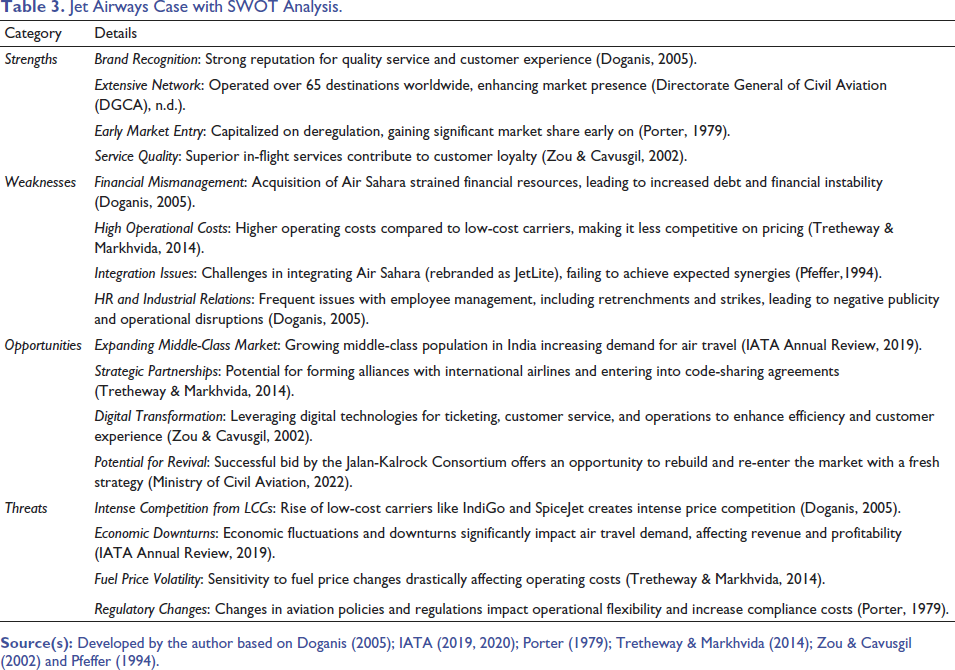

Analysis of Jet Airways Case with SWOT Analysis Framework

The present study also provides a comprehensive overview of the company’s internal strengths and weaknesses, as well as, external opportunities and threats through SWOT analysis. This framework helps to understand the strategic position of Jet Airways. Jet Airways’ journey from market dominance to bankruptcy is a multifaceted case of strategic missteps, financial mismanagement, and operational challenges. Despite strong brand recognition and an extensive network, the airline struggled with high costs, intense competition, and integration issues following the acquisition of Air Sahara.

The SWOT analysis highlights the critical areas where Jet Airways faltered and the opportunities and threats that influenced its path. The airline’s potential revival under new management presents a chance to learn from past mistakes and rebuild with a more sustainable and competitive approach.

Jet Airways’ strengths in quality service and strategic routes helped establish a robust brand and a loyal customer base. Its early entry into international markets allowed it to secure profitable routes before competitors, capitalizing on the increasing demand for international travel from India. However, weaknesses in financial management and high operational costs contributed to its downfall. Poor financial planning led to mounting debts, and high fuel costs further strained its resources. Ineffective cost management caused cash flow problems, resulting in salary payment delays and negatively impacting employee morale. Operational inefficiencies, such as frequent flight delays and maintenance issues, also damaged its reputation, pushing customers towards more reliable alternatives. Opportunities in the expanding Indian aviation market could have been leveraged by broadening services and enhancing operational efficiency. The growing middle-class population and rising disposable incomes were increasing air travel demand. Jet Airways could have pursued strategic partnerships with international airlines to enhance connectivity and share resources, thereby reducing costs and improving service quality. Conversely, threats from LCCs like IndiGo and regulatory changes posed significant challenges. The competitive pricing of LCCs attracted cost-conscious travellers, making it hard for Jet Airways to retain market share without sacrificing profitability. Regulatory changes, such as higher taxes on aviation fuel or new safety regulations, could further burden Jet Airways’ financial resources and operational flexibility.

Table 3 is a tabular representation of the Jet Airways Case with SWOT Analysis. Overall, while Jet Airways had significant strengths and opportunities, its weaknesses and threats ultimately led to its decline. Addressing financial mismanagement, reducing costs, and improving operational efficiency could have helped the airline better navigate the competitive and regulatory landscape.

Jet Airways Case with SWOT Analysis.

The New Avatar of Jet Airways and Way Forward of Indian Aviation

The LCC market share rapidly increased from 1% in 2003–2004 to 69% in 2010–2011. This is a historic lesson. The then-established players like Indian Airlines, Jet Airways, and Air Sahara initially ignored the low-cost model. However, with the increasing demand for low-cost air travel and to improve occupancy rate, they had to respond to the market trends by discounting fares but with advance bookings and high penalties for cancellation. This has implications for FSAs, which Jet Airways is contemplating in its new avatar. Despite the rise and fall of major airlines including the LCC, the aviation market has remained buoyant in the last decade also as indicated by the following Table 4.

The Aviation Market.

The government has been instrumental in developing policies to give a boost to the aviation sector. For this, UDAN-RCS scheme (Regional Connectivity Scheme-Ude Desh ka Aam Naagrik) has been launched by the government which aims to increase air connectivity by providing affordable, economically viable and profitable travel on regional routes. With the right policies and relentless focus on quality, cost and passenger service, India is likely to be well placed to achieve its vision of becoming the third-largest aviation market by the end of 2030s. Rising working groups, expanding middle-class demography, increased discretionary income, growth in external trade, policy support, increased investment for infrastructure augmentation, and increased private sector participation—all these drivers are expected to boost demand. AAI has developed and upgraded over 23 metro airports in the last few years. AAI is making heavy investments in the development of non-metro projects including unconnected places of North East India like Itanagar, Kohima, Gangtak. Indigo successfully test-landed its plane on 18-10-2022 at the newly constructed Donyi Polo Airport, Itanagar with 685 acres of land. DGCA granted an aerodrome licence to AAI in September 22 for this airport which was built by AAI at Rs. 660 crores. Government of India has launched NABH- Nirman (Nextgen Airports for Bharat Nirman initiative), which is aimed at increasing India’s airport capacity. According to various estimates, India will require investment worth Rs. 3–4 lakh crore to achieve capacity for having a billion trips per year (IBEF Report, 2022).

All these indicate a turnaround in the Indian aviation sector. Legacy carriers have built the hubs largely on the back of long-haul international connectivity. Ways have been paved for LCCs to exploit emerging regional markets. A symbiotic relationship of LCC with legacy airlines might have another rosy picture. However, historical lessons from Jet Airways in its earlier avatar and other airlines indicate a very competitive and highly complex picture to sustain the efforts of domestic airlines in India.

In this context, big question remains for Jet Airways in its new avatar—what and where to start; and how to proceed. Will the airline be able to realize its dream of ‘being India’s most people-focused and customer friendly airline’? A saying goes that many turnarounds require a forceful authority. Will it be applicable to Jet Airways? If yes, in what form? How should it evolve its turnaround strategy on various pillars like fleet expansion, route-frequency-fare, client and passenger servicing, HR, and liquidity? There are many questions to ponder and issues to analyze.

The new management of Jet Airways is quite optimistic about its future

Well-capitalised and led by seasoned industry professionals, Jet Airways in its new avatar will be India’s most people-focused and customer-friendly airline, updated for the Digital Age. It will be a ‘smart’ full-service carrier with a two-class cabin configuration, including a business class cabin designed to global standards and an evolved new-generation economy class that offers today’s customers what they most value.

The Dilemma: Path to Revival

Jet Airways, once a dominant force in India’s aviation sector, now faces a critical juncture in its quest for revival under new management. The airline must navigate several key challenges to regain its former glory. These include clearly defining its market positioning, formulating a comprehensive financial restructuring plan, effectively navigating complex regulatory landscapes, enhancing operational efficiency, rebuilding employee morale, and developing strategic initiatives to recapture market share. Each of these challenges is crucial for ensuring the airline’s sustainable recovery and long-term success. The Strategic questions for the New Management may arise; Should Jet Airways continue as a full-service carrier, or should it adopt a hybrid model to compete with LCCs?; What strategies can be employed to stabilize the airline’s finances and attract new investment? How can the airline navigate regulatory challenges to maintain operational flexibility and efficiency? What improvements are necessary to enhance service reliability and customer satisfaction? How can the new management rebuild trust and morale among the workforce? What alliances can be pursued to expand market reach and improve competitiveness? How can the airline balance immediate survival tactics with long-term growth strategies? Addressing the strategic dilemmas will be crucial for Jet Airways to reclaim its position in the Indian aviation market and ensure long-term success.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.