Abstract

M. Damodaran,1 chairman IndiGo, has a lot on his plate, and the servings are not over yet. What happened on 26 April 2019, was just a precursor to what was eventually to follow. Aditya Ghosh,2 the longstanding director of InterGlobe3 for 10 years, resigned from his position, making way for Greg Taylor4 as president and chief executive officer (CEO). Rahul Bhatia5 became the interim CEO. This, ironically, happened when the airline had bagged in traffic rights to as many as 15 countries, including France, UK and Germany. The most ill-timed dispute between the two co-founders of IndiGo, Rakesh Gangwal6 and Rahul Bhatia, which had been brewing for about a year, came out in the open on 16 July 2019, at the most inopportune moment. Rakesh Gangwal alleged violations of corporate governance rule at IndiGo7 and requested the Securities and Exchange Board of India8 (SEBI) to intervene. The feud between the founders of InterGlobe Aviation Ltd. opened a can of worms, although Gangwal was not inclined to sell or raise his stakes. Analysts wondered about the timing of the complaints to SEBI: Why now? Will IndiGo be able to come out of this predicament or follow Kingfisher and Jet Airways’ footsteps?11 Will it be yet another episode of shallow vested interests? Will this lead to the downfall of IndiGo,12 or will it survive the turbulence and keep flying like a phoenix?

Discussion Questions

Analyse the board structure of IndiGo and its implications on airline governance.

Examine the role of promoter companies in the corporate governance of the company.

Evaluate the situation for the fallout between the two promoters.

How can Damodaran restore the morale of the employees?

Advise Damodaran on streamlining the governance processes.

Introduction

The market shares of InterGlobe Aviation fell over 6%, the most in 7 months, on 27 April 2019, just before the airline announced the resignation of the company’s president Aditya Ghosh. In the quarter-end of June 2019, IndiGo’s net profit stood at $170 million, a 43-fold jump from the measly profit of $3.81 million in the previous quarter. There were speculations about the exit of Ghosh and the appointment of many senior expats into the organization. Problems had begun to mount for IndiGo since the failure of the engine of its Airbus 13 A320. IndiGo’s initial inclination to buy out Air India 14 and then its withdrawal remained a jinx. Additionally, while following up on the alleged violations of corporate governance by Bhatia, as flagged by Gangwal, SEBI sensed foul play and directed the stock exchange to furnish information on the company’s share price data last 1 month to check for any possible insider trading norms. In the meantime, the controversy around the fallout between the two promoters and its reasons began to feed the gossips.

Aviation Industry

Global Scenario

Globally, the players in the airline industry operated in a highly sensitive market. Over the past three decades, the airline industry had undergone a lot of changes; from an increase in market share of low-cost carriers to a sharp rise in fuel prices, and too many closures of airlines world over such as Alitalia, 15 Air Berlin 16 and Monarch 17 in Europe, and Kingfisher and Jet Airways in India. Despite this, an increase in commercial aircraft production signalled that there was potential for growth in the industry, with India and China dominating the commercial aerospace’s growth rate.

Indian Scenario

The aviation industry in India had emerged as one of the most promising and rising industries in the country during the last 5 years. During FY 2019, passenger traffic in India stood at 344.70 million. With the continuous increase in passenger traffic, India planned to increase the number of airports to 190–200 18 from 103 operational airports. As on July 2018, 620 airplanes were in service, which was expected to increase to 1,100 airplanes by 2027. Key investments and developments were being planned, such as the investment of $2320 million in 2018–2019 to expand and construct new airports, including those in a public-private partnership (PPP) model. 19

The Competitive Scenario

As per the India Brand Equity Foundation (IBEF) Aviation report in June 2019, India had seven major airlines operating in the country:

SpiceJet

20

: It was a low-cost airline (the second largest airline in India in terms of the number of passengers) with a market share of 13.6% as on March 2019. The airline operated 312 daily flights to 55 national and international destinations (see Exhibit 2). GoAir

21

: It was another Indian low-cost airline, owned by the Wadia Business Group. It started its operations in November 2005, and with a fleet of Airbus A320 aircraft, the airline operated over 230 daily flights to 28 destinations nationally and internationally. Jet Airways: It was an Indian airline flying internationally, which suspended all its flight operations on 17 April 2019. It held second position in India with 17.8% of the passenger market share. The company was subject to the insolvency process under the Insolvency and Bankruptcy Code, 2016. Jetlite

22

: Formerly known as Air Sahara, Jet Airways’ subsidiary. But it suspended all of its flights and ceased all operations on 17 April 2019. Air India: The government ran India’s national airline, owned by Air India Limited. The fleet flew to 94 destinations nationally and internationally. Vistara

23

: It was a joint venture of Tata Sons Limited and Singapore Airlines Limited, where Tata Sons held 51% in partnership and Singapore Airlines owned 49% stake. The company was registered as TATA SIA Airlines Limited. AirAsia India

24

: AirAsia India was an Indian low-cost carrier headquartered in Bangalore, India. It was a joint venture of Tata Sons, which held 51% stake in the airline and AirAsia Berhad had 49% stake.

About IndiGo: The Market Leader

IndiGo (InterGlobe Aviation Ltd.) was a low-cost airline based in Gurgaon, Haryana, India. It was a leader in terms of passengers carried and fleet size, reaching 48 domestic and international destinations. The airline was founded in 2006, jointly by Bhatia of InterGlobe Enterprises (IGE) and Gangwal, an expatriate from the United States. In 2010, IndiGo became the third largest airline in India, with a passenger market share of 17.3%. In January 2011, the airline secured permission to launch international flights. It went public in November 2015, with over 17,000 employees; it started with 1,100 employees. At that time, InterGlobe had a 51.12% stake in IndiGo, whereas 47.88% was held by Gangwal’s company, Caelum Investments. 25 The success of IndiGo was accounted to its effective business model that reduced costs. Its quick turn-around time ensured aircrafts flying as many as 12 hours every day.

The Journey to IPO

The IPO issue was a curious mix of Rakesh Gangwal’s art of negotiation and Rahul Bhatia’s financial muscle and operational efficiency. Because of Bhatia’s financial contribution in the shareholders’ agreement, he naturally had more power regarding the appointment of directors and senior leadership in IndiGo. Bhatia had a stake of 38.26% in IndiGo, while Gangwal owned 36.69%, with the market capitalization valued at $8,735 million. 26 While Gangwal was the driving force behind the carrier, Bhatia oversaw the financial needs of the airline. The IGE Group had stated that while Gangwal was relatively safe with equity exposure of less than $2.1 million, Bhatia and his father, Kapil, had borne financial load as a personal loan to the airline as well as personal guarantees to the banks to meet financial needs of the airline. 27 IGE Group stated, ‘Starting from the financial year 2005–2006 at a level of $20 million of personal guarantees by the financial year 2009–2010, the aggregate financial exposure of IGE, Kapil and Rahul Bhatia was well over $155 million’. 28 The Bhatias continued to extend their financial support to IndiGo until IndiGo stood on its own feet in 2012. Gangwal, on the other hand, said that he made a mistake in agreeing to the IGE Group’s rights and that ‘times, circumstances and behaviour of promoters had changed since 2015’, when IndiGo went public. 29

The Fissure Starts

Gangwal had begun to question the shareholders’ agreement and related-party transactions between IndiGo and Bhatia’s IGE. He said again and again, ‘Rahul (Bhatia) was a great friend who I had known for decades, and I gave him blind trust’. 30 In 2018, Gangwal pursued aggressive expansion to penetrate India’s aviation market and claimed to increase the Airline’s capacity to 250 from 155, while Bhatia retained a balanced and cautious approach. 31 The proposal did not go down well with IndiGo management. While Bhatia believed wide-bodied aircraft could help achieve international stature for IndiGo, Gangwal felt that narrow-bodied aircraft like Boeing 737 and codeshare agreements with other global carriers could help it gain a global presence.

An engine deal that IndiGo had to conclude was taking time, ‘to the point the company was at the risk of breach of its contract’, said an executive. 32 The deal negotiations were being driven by Gangwal, assisted by Riyaz Peer Mohamed, Chief Aircraft Acquisition and Financing Officer of IndiGo. The reasons remained unknown for the cause of the delay. Speculations were that Gangwal wanted more clarity from Bhatia on the issue of the related-party transaction. He wanted IGE to dilute its rights to nominate three non-independent directors to the IndiGo Board and the senior leadership as Gangwal had the power to nominate only one. In the meantime, two major developments also took place. Bhatia brought in Kiran Rao—who was earlier heading Airbus in India—to negotiate the engine deal. Her appointment coincided with the notice that Gangwal sent to the IndiGo board, raising issues regarding related-party transactions between IndiGo and IGE.

Further, Ronojoy Dutta was brought in as a principal consultant to float a 5-year business plan for IndiGo. Gangwal and Dutta were former colleagues at United Airlines, and shared an uneasy relationship. It was easy to see the manoeuvres. Parallel to this, the hunt was on for a new CEO. Greg Taylor, who was appointed as a senior advisor following the resignation of former president Aditya Ghosh, was chosen to be close to Gangwal. One who had also recently begun questioning the related-party transactions between IndiGo and Bhatia’s private firm. Dutta and Taylor had worked together at the American carrier United Airlines—Taylor in a junior position and Dutta was a board member.

But interestingly, Taylor’s appointment was not able to see the light of the day as it was suspiciously withheld. Taylor’s appointment needed security clearance from the government, and since that was not happening, his appointment had still not been presented to the board for approval. ‘It’s weird why his security clearance didn’t come, especially when there was no problem when Taylor first worked with IndiGo’, said an executive. 33 Prince Mathew Thomas, chief of Corporate Bureau, Money Control, stated, ‘Even though Taylor was excellent in revenue management, one part of the management wondered if Taylor had enough breadth to handle the operations of an airline’. 34 Reportedly, ‘Taylor didn’t see a future with the company after Dutta was brought in’. This notwithstanding, Taylor quit IndiGo in December 2018, his second stint since 2016–2017, paving the way for Dutta’s smooth transition from his advisory role to CEO, which was made official a month later, in January 2019.

The Exit of Aditya Ghosh

As luck would have it, IndiGo, the leading no-frills carrier, announced its president and director Aditya Ghosh’s sudden departure on 26 April 2019. ‘It is now time for me to step off the treadmill and, sometime in the near future, embark on my next adventure. I wish all my colleagues at IndiGo the very best as they move on to the next phase of growth’, he said. 35 Ghosh was with Delhi’s J. Sagar Associates, a lawyer by training, where he serviced clients that included Rahul Bhatia promoted InterGlobe Enterprise. 36 Ghosh had joined IndiGo as general counsel and was made the airline CEO in 2008, in a surprise decision by its founder, Bhatia. Undoubtedly, Ghosh, also the airline’s whole-time director and president, made IndiGo what it had become, capitalizing on his legal acumen and command over the language. He was the voice of IndiGo. Even IndiGo’s rivals had good things to say about him. ‘I have had the privilege of knowing Aditya for many years and working with him closely on issues concerning Indian aviation. He had a glorious stint. We are all proud of his achievements and those of the Airline he has worked for’, said Ajay Singh, chairman of SpiceJet, to ET Magazine. 37

Mysteriously enough, shares of IGE fell over 6%, the most in & months on 27 April 2019 (see Exhibit 3), before the airline announced the resignation of the company’s president Aditya Ghosh. Did Ghosh smell a rat, a foul play, or a deliberate leak? In an interview with CNBC TV18, Ramdeo Agrawal said, ‘while Aditya Ghosh had been one of the finest persons and the face of IndiGo, in businesses what matters is the strategy and the whole team; the company will soon be able to find a worthy leader. 38 Bruce Ashby and Gangwal built the Airline, plus Riaz Peer Mohammad (former CFO). Strategy, business model, major long-term contracts, branding, and positioning were all done by them. Aditya’s role was to grow the Airline without touching the autopilot settings’, says a top executive at another rival airline. 39 ‘Ghosh was close to Bhatia. On the other hand, Taylor comes from United Airlines, just like Gangwal’, said a senior executive from the industry. ‘He was Gangwal’s choice to be the CEO’, said another executive from the industry. 40 If Ghosh was a close aide to Bhatia, who was more powerful than Gangwal, why did Aditya Ghosh resign?

The Mess Up

On 13 June 2019, IndiGo announced a $20,000 million order for LEAP-1A engines with US-based CFM International to power its future fleet of 280 narrow-body aircraft. Calling it the ‘largest-ever single-engine order in history’, the Airline also said that ‘delivery of the first LEAP-1A-powered A320neo was scheduled in 2020’. 41 The deal soon became the bone of contention between Gangwal and Bhatia, with their relation reaching a point of no return. The decision to switch from Airbus’ to A320neo family aircraft came after reported issues with Pratt & Whitney (P&W) engines since 2017. The Directorate General of Civil Aviation (DGCA) documents reviewed by Money Control said that there were 69 engine failures in IndiGo’s A320neo fleet. With the manhandling of an IndiGo passenger in November 2017, the situation spiralled out of control. Eight of its new Airbus A320neo jets grounded in February and March 2018, hit by a string of engine snags, forcing dozens of flights to be cancelled or rescheduled.

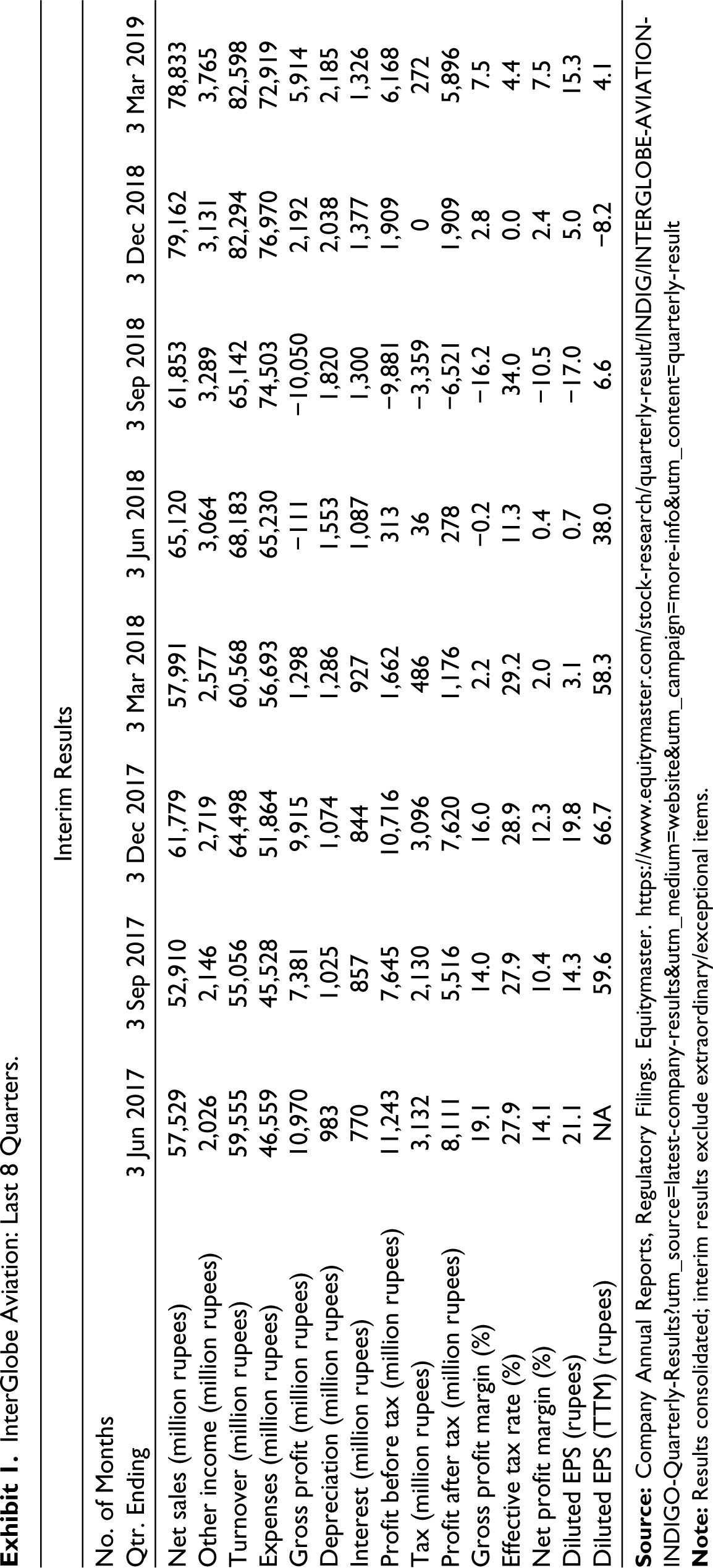

Then came Air India’s ‘Buy-in Buy-out’ episode. After the government decided to disinvest Air India, the national carrier IndiGo quickly showed its interest in bidding for the same. However, it made a hasty retreat strangely enough after the government released its Expression of Interest on 28 March 2018. The IndiGo president once said, ‘From day one, IndiGo has expressed its interest primarily in the acquisition of Air India’s international operations and AI Express. However, that option is not available under the government’s current divestiture plans’. ‘Also, as we have communicated before, we do not believe that we have the capability to take on the task of acquiring and successfully turning around all of AI’s airline operations’, he added. Trouble had been brewing from before 2018. In Q42018, the IndiGo share price plummeted to over 17% with a 73% drop in profit after tax (PAT) to $16 million compared to a PAT of $62 million a year ago 42 (see Exhibit 1). IDFC Securities also downgraded the rating to neutral and said that ‘The Q4FY18 yields have been weak as airlines have not passed on the impact of higher fuel prices (see Exhibit 4). In the past too, there have been instances when airlines have passed on the impact of higher fuel prices with a lag, giving rise to incremental pressure on margins and earnings’. 43 Mr Philip, chief financial officer of IndiGo, said that the revenue per available seat kilometre (RASK) for the quarter was $0.048 compared to $0.050 during the same quarter last year, a decline of 3.2%. ‘This decline in RASK was primarily driven by lower yields partially offset by higher load factors. While our yields were down by 5.6% to 3.31 rupees, our load factors were up by 2.8 points to 88.9%’, he said (see Exhibit 5). 44

The Washing of Dirty Linen

Gangwal stated that the company deviated from the core principles and values of governance. ‘Beyond just questionable Related Party Transactions (RPT), various fundamental governance norms and laws were not being adhered to, and this would inevitably lead to unfortunate outcomes unless effective measures are taken today’, Gangwal said in a letter. 45 In response to Gangwal’s allegation relating to RPT and appointments, calling them as governance lapses (including violation of SEBI regulations that makes it mandatory for having a woman director on Board), IGE defended its controlling rights over the airline, stating that Gangwal had limited financial risks in the airlines. In contrast, IGE had been continuously fending for IndiGo, including its negotiations with Airbus for fleet expansion, which was initially a joint undertaking. Later, IGE single-handedly fulfilled all the obligations. ‘Even more significantly, during the turbulent period of the fledgling airline, it was left to the IGE Group, as a responsible founder, to fend for IndiGo. Gangwal was missing in action at that time, and there were stages where he wanted to de-risk and pushed for the business to be sold’, 46 read a press release statement, adding that the IGE Group had consistently supported ‘without in any way diluting Gangwal’s potential upside’. ‘Do business ethics and morals permit a contracting party to walk away from its obligations at its convenience after it has enjoyed the benefits under an agreement and pretend to be a victim?’ it posed. 47

On the contrary, according to Gangwal, ‘Bhatia had built an ecosystem of other companies that would enter into dozens of related-party transactions (RPTs) with IndiGo. We are not against RPTs as long as proper checks and balances exist, and such RPTs are in the best interest of the company’. He also pointed out violations of fundamental governance norms and laws. ‘The process of appointing an Independent Chairman at IndiGo is the classic “Hobson’s choice” and a sophisticated way to circumvent SEBI rules’. 48 Countering the allegation, Bhatia pointed out that an Ernst & Young (EY) report on the RPTs of the past 5 years noted that there were no ‘substantive’ irregularities but only ‘procedural irregularities’. ‘Had EY disclosed that any RPTs were not at arm’s-length or not in the ordinary course of business, that would have been highlighted’, said Bhatia. 49 He maintained that this requisition was a ‘proxy and subterfuge’ to force a change in the governing structure of the company and an ‘unreasonable demand to dilute the controlling rights’.

No End in Sight

‘The dispute has the potential of lingering on and becoming a significant headwind for the IndiGo stock’, wrote analysts from Credit Suisse Securities (India) Pvt. Ltd in a report on 9 July 2019. 50 Resonating with the sentiment, Citi Research, on 9 July 2019, said, ‘With the conflict between the two promoters coming out in public in great detail, we do not envisage a settlement anytime soon. We think that the uncertainty regarding the final resolution could cause weakness in the stock price’. 51

What started as a hiccup was threatening to derail one of the world’s most successful airlines; questions loomed. Was this fallout between the two promoters Gangwal and Bhatia, inevitable, given the backdrop? Is it a situation of no return or the dispute between the promoters to reach an amicable solution? Will, the airline, remain the market leader or fall apart with the dispute between the promoters over CG issues, or will Damodaran be able to bridge them?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

InterGlobe Aviation: Last 8 Quarters

| Interim Results |

||||||||

| No. of Months Qtr. Ending |

3 Jun 2017 | 3 Sep 2017 | 3 Dec 2017 | 3 Mar 2018 | 3 Jun 2018 | 3 Sep 2018 | 3 Dec 2018 | 3 Mar 2019 |

| Net sales (million rupees) | 57,529 | 52,910 | 61,779 | 57,991 | 65,120 | 61,853 | 79,162 | 78,833 |

| Other income (million rupees) | 2,026 | 2,146 | 2,719 | 2,577 | 3,064 | 3,289 | 3,131 | 3,765 |

| Turnover (million rupees) | 59,555 | 55,056 | 64,498 | 60,568 | 68,183 | 65,142 | 82,294 | 82,598 |

| Expenses (million rupees) | 46,559 | 45,528 | 51,864 | 56,693 | 65,230 | 74,503 | 76,970 | 72,919 |

| Gross profit (million rupees) | 10,970 | 7,381 | 9,915 | 1,298 | -111 | -10,050 | 2,192 | 5,914 |

| Depreciation (million rupees) | 983 | 1,025 | 1,074 | 1,286 | 1,553 | 1,820 | 2,038 | 2,185 |

| Interest (million rupees) | 770 | 857 | 844 | 927 | 1,087 | 1,300 | 1,377 | 1,326 |

| Profit before tax (million rupees) | 11,243 | 7,645 | 10,716 | 1,662 | 313 | -9,881 | 1,909 | 6,168 |

| Tax (million rupees) | 3,132 | 2,130 | 3,096 | 486 | 36 | -3,359 | 0 | 272 |

| Profit after tax (million rupees) | 8,111 | 5,516 | 7,620 | 1,176 | 278 | -6,521 | 1,909 | 5,896 |

| Gross profit margin (%) | 19.1 | 14.0 | 16.0 | 2.2 | -0.2 | -16.2 | 2.8 | 7.5 |

| Effective tax rate (%) | 27.9 | 27.9 | 28.9 | 29.2 | 11.3 | 34.0 | 0.0 | 4.4 |

| Net profit margin (%) | 14.1 | 10.4 | 12.3 | 2.0 | 0.4 | -10.5 | 2.4 | 7.5 |

| Diluted EPS (rupees) | 21.1 | 14.3 | 19.8 | 3.1 | 0.7 | -17.0 | 5.0 | 15.3 |

| Diluted EPS (TTM) (rupees) | NA | 59.6 | 66.7 | 58.3 | 38.0 | 6.6 | -8.2 | 4.1 |

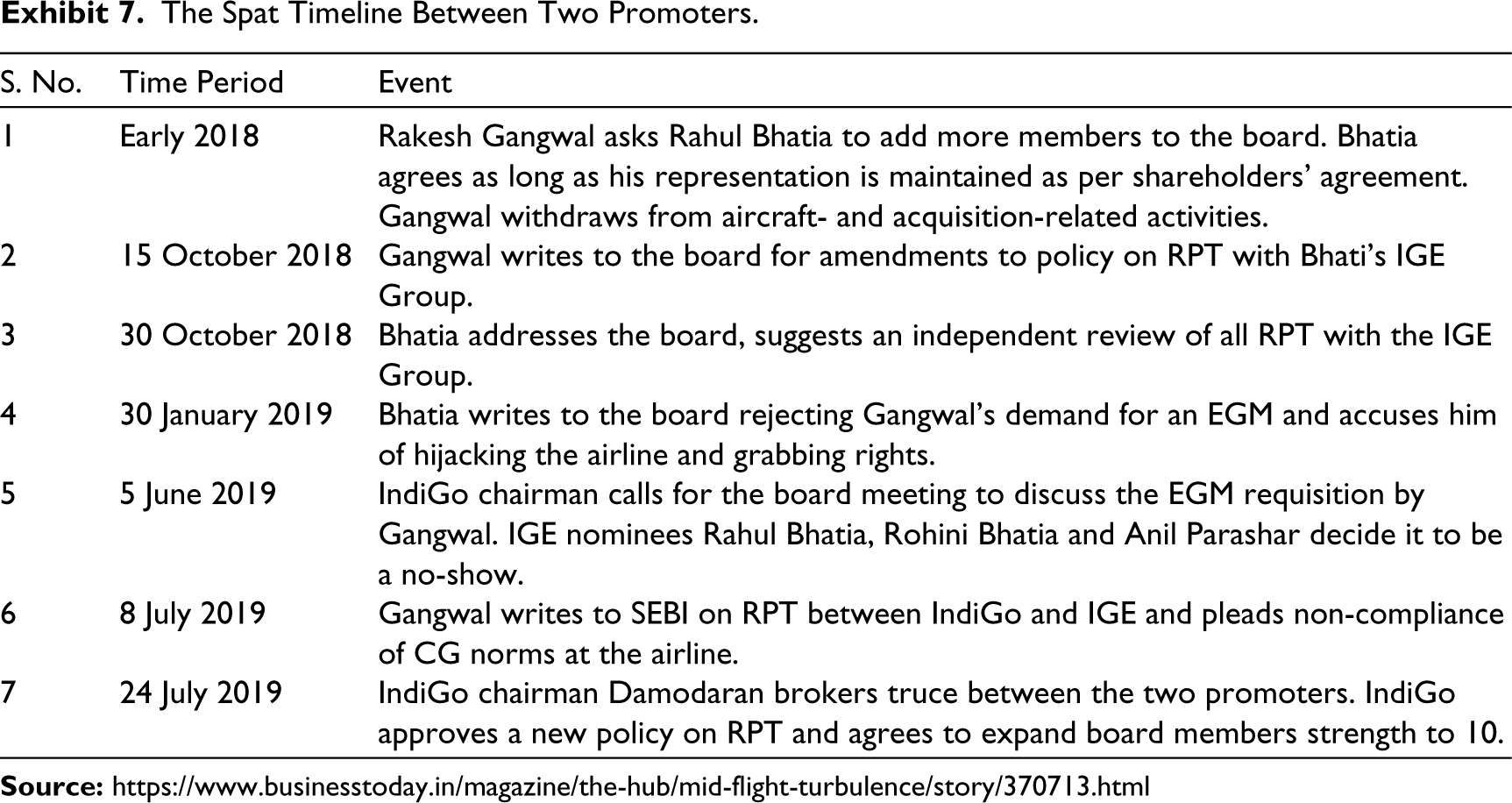

The Spat Timeline Between Two Promoters

| S. No. | Time Period | Event |

| 1 | Early 2018 | Rakesh Gangwal asks Rahul Bhatia to add more members to the board. Bhatia agrees as long as his representation is maintained as per shareholders’ agreement. Gangwal withdraws from aircraft- and acquisition-related activities. |

| 2 | 15 October 2018 | Gangwal writes to the board for amendments to policy on RPT with Bhati’s IGE Group. |

| 3 | 30 October 2018 | Bhatia addresses the board, suggests an independent review of all RPT with the IGE Group. |

| 4 | 30 January 2019 | Bhatia writes to the board rejecting Gangwal’s demand for an EGM and accuses him of hijacking the airline and grabbing rights. |

| 5 | 5 June 2019 | IndiGo chairman calls for the board meeting to discuss the EGM requisition by Gangwal. IGE nominees Rahul Bhatia, Rohini Bhatia and Anil Parashar decide it to be a no-show. |

| 6 | 8 July 2019 | Gangwal writes to SEBI on RPT between IndiGo and IGE and pleads non-compliance of CG norms at the airline. |

| 7 | 24 July 2019 | IndiGo chairman Damodaran brokers truce between the two promoters. IndiGo approves a new policy on RPT and agrees to expand board members strength to 10. |