Abstract

This case talks about Vistara, an airline brand registered under the name of Tata Singapore Airlines (SIA) Airlines Limited, which started as a joint venture between Tata Sons and SIA Limited in 2013. While the company was founded with the intent to expand, as suggested by its brand name, the airlines has failed to register positive returns ever since its inception despite a 190% compound annual growth rate (CAGR) in total revenue from financial year 2016 to financial year 2020. While company’s ratios have shown a dismal performance over the years, its competitors and the market leader have shown better performance or at least some form of leadership in one of the operating aspects. In an industry plagued with problems such as fluctuating crude oil prices, rising maintenance and leasing costs, and other operating costs, most of the airline companies have registered losses in recent years, the magnitude of which has further aggravated due to COVID-19. Vistara will need to revisit its short-term and long-term strategies to expand its position in the Indian as well as the international aviation market.

Learning Outcomes

There have been at least two or three rounds of equity infusion by the promoters, this clearly indicates that the original business plan was flawed

—Koushik Jagathalaprathaban, Partner, AT-TV

Develop an understanding of the functioning of the Indian aviation industry.

Understand Vistara’s bottlenecks in registering profitability and think holistically in terms of possible solutions to the problem from financial and strategic perspectives.

Appreciate the importance of a good business model in the sustainability of a business in an extremely volatile and competitive business environment.

Introduction

Tata Singapore Airlines (SIA) Airlines Limited, popularly known by the brand name ‘Vistara’ registered a loss of ₹1,814 crores in the financial year 2019–2020. This was the largest figure of loss for Vistara since the company’s inception of operations in early 2015. While many aviation experts remain puzzled over the company’s business model and strategy, the company’s management remains largely positive over the company’s future growth prospects. The company’s financial health has deteriorated considerably, with increased operating expenses significantly affecting the company’s bottom line. The trends suggest that the company has been losing money consistently, while consuming huge amounts of capital per year, mostly funded by its parent companies, Tata Sons and SIA.

Aviation Industry Outlook

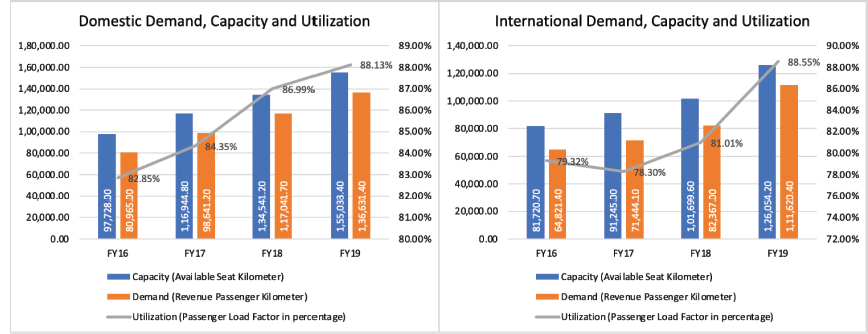

The aviation industry encapsulates several aspects of air travel and activities, and it has gradually escalated to hold an integral place in the economy. It not only includes airline services (passenger as well as cargo and mail) but also manufacturing of aircraft, their maintenance, etc. India is set to become the world’s third largest airline market by 2024 after overtaking the UK (Indian Airports Analysis, 2020). The domestic passenger traffic saw a growth of nearly 13% compounded annual growth rate (CAGR) from financial year 2016 to financial year 2020, while international traffic grew at 5% CAGR in the same period. Freight traffic also registered a growth of 5.32% CAGR in the same period.

Looking at Figure 1, the domestic connectivity of airlines in India has been growing steadily since financial year 2016. However, capacity utilization in the international segment saw a decline in financial year 2017 due to decline in foreign tourist arrivals, owing to slowdown in the services sector, but it later surged to 88.55% in financial year 2019. It can be said that the growth in demand was much more than the growth in supply, which resulted in greater utilization of airlines in financial year 2019.

The sector has not been performing as per the expectations of its stakeholders since 2018. Lack of trained staff for airline companies often leads to operating inefficiencies, and the industry struggles to retain talent. Intense competition is one of the leading factors causing declining wage prices, besides affecting the prices of air tickets. Inefficiencies caused due to obsolete airport infrastructure and air traffic control foundation also add to the woes of the sector. Although privatization of airports is underway, the results are expected to be seen only after a few years.

Due to COVID-19, the aviation industry has suffered in several different ways and with airline services being the most affected. It is expected that the losses due to reduced air traffic would go up to US$113 billion. The COVID-19-affected areas have seen a 30% drop in bookings because of which the number of flights dropped by 20%–30%. Internal traffic growth is also largely affected when local commuters postpone or cancel their travel plans (Aviation, 2020).

The Airports Authority of India (AAI), responsible for overseeing the management and maintenance of aviation infrastructure in India had reported a reduction in its revenue by 92% from April 2020 to June 2020 as compared to 2019 values. The Investment Information and Credit Rating Agency India Limited (ICRA) expects financial year 2021 to see a decrease of approximately 41%–46% in domestic passenger traffic and approximately 65%–72% in overseas passenger capacity. Therefore, the revenue of the Indian aviation industry is expected to see a sharp decline. Profits from this industry will also be affected by low revenues and high fixed costs (Ray & Shah, 2020).

For Indian carriers, Q1 is generally seen to be the strongest period, while Q2 the weakest. With the shutdowns/lockdowns playing in Q1, any gradual improvement in the revenues of the Indian aviation industry is expected to be seen only from Q3 of financial year 2021. (How Bad is the Impact of Coronavirus, 2020)

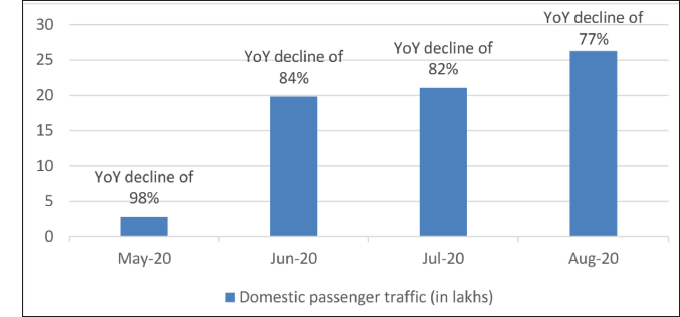

Figure 2 suggests a decline in the domestic passengers from May 2020. The pandemic struck harder during May 2020, which caused a decline of 98% of passenger numbers, year-on-year (y-o-y). However, as the Indian carriers restarted their operations in a calibrated manner, domestic operations stood at 45% capacity by the last week of June, which led to the y-o-y decline in passengers from 98% in May 2020 to 77% in August 2020.

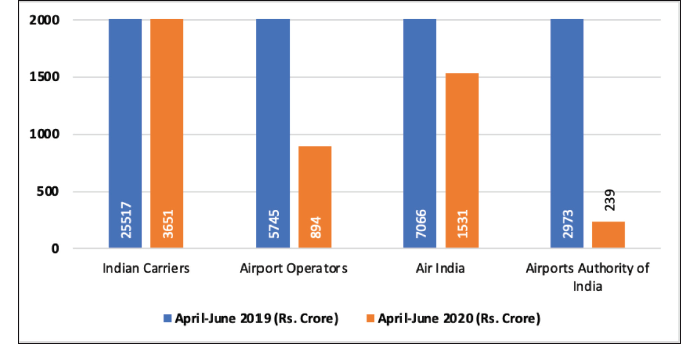

Figure 3 shows that the aviation revenue was impacted significantly due to the COVID-19 pandemic. On a y-o-y-based analysis, it is seen that there was a decline of revenue by a huge margin across all subdivisions of the Indian aviation industry. Employment also declined in airline companies, airports, ground-handling agencies and cargo operators.

Introduction to Vistara

Vistara is a full-service airline that was initiated as a joint venture between Tata Sons (India) and SIA with stakes of 51/49. The company offers full-service flights and was launched its operations in January 2015.

The Tatas and SIA were keen to enter the Indian aviation market together and made attempts to do so in 1994 and 2000, which ended in failures. To understand the Tata group’s interest in re-entering the airline business, one must go back to the 1990s. With economic liberalization just round the corner, the airline sector also was one that had generated much interest. In 1994, the prime minister of Singapore met the prime minister of India, where the introduction of an Indian joint venture with SIA was also a part of the discussion. Multiple meetings followed, including some where the chairman of the Tata group was present. A formal proposal was floated in 1995 and then again in subsequent years. Yet, these proposals never saw the light of day. Indeed, in 2010, in a speech, the chairman of the Tata group construed that Tata’s interest to enter the airlines sector was impeded by three governments, and as many prime ministers, and that the group would only enter via clear and transparent dealings. Another interesting fact was that the group was quite clear on SIA as a joint venture partner. An opportunity presented itself in 2011 when the government revised the foreign direct investment (FDI) guidelines for the aviation sector that allowed 49% of private sector investment in the aviation sector, which led to a successful alliance between the two companies. On 5 November 2013, Tata SIA Airlines Limited, the holding company of Vistara, was incorporated and its first flight took off on 9 January 2015 (Mittal & Gupta, 2020).

This joint venture also addressed the challenges faced by SIA. SIA only had 4% of the international traffic share from India before 2015. Post liberalization of the aviation sector, SIA was able to create a domestic, localized brand with the assurance of a financial influence in a sector that required heavy capital investments.

Vistara is a full-service airline, which is different from Air Asia India, another joint venture of Tata with Malaysia’s Air Asia that operates as a low-cost airline.

From its inception till early 2019, the airline focused only on domestic operations with an emphasis on point-to-point operations. In August 2019, it announced international operations from Mumbai and Delhi to Singapore. It, currently, serves eight international destinations, which include London, Dhaka, Dubai, Bangkok, Doha, Colombo and Kathmandu, apart from Singapore.

Vistara had a lively 2020, adding many new planes and routes despite the precarious circumstances. The airline notably took delivery of its first 787-9 Dreamliner and A321neo fleets this summer. The additions bring Vistara closer to its goal of 70 aircraft by 2023 and fulfilling its long-distance ambitions (Pande, 2020).

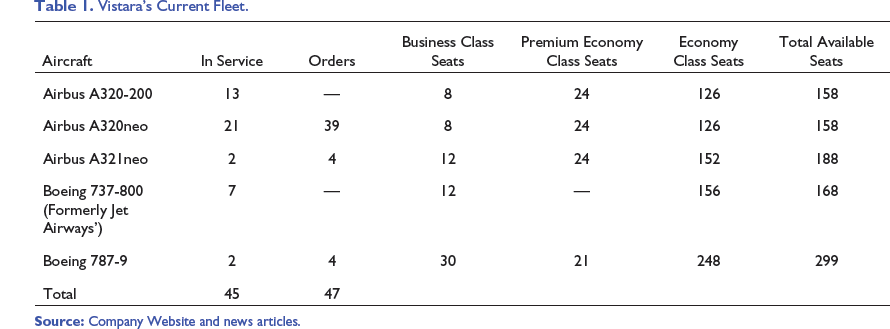

Vistara’s Current Fleet.

Value Proposition

Value proposition may be defined as ‘a clear, simple statement of the benefits, both tangible and intangible, that the company will provide, along with the approximate price it will charge each customer segment for those benefits’ (Lanning & Michaels, 1988).

Vistara Product Strategy

Flight services is the core service offering of Vistara. Its marketing mix consists of three types of seat offerings at different prices (price discrimination–revenue maximizing strategy).

In addition, the travellers are provided with quality vegetarian and non-vegetarian meals. Vistara updates its in-flight meal menus more frequently than its competitors to satisfy its customers. For all flights, Vistara offers in-flight entertainment, where passengers having the Vistara app can connect to the in-flight Wi-Fi and enjoy music, movies, serials, etc.

Vistara Price/Pricing Strategy

Unlike its competitors that offer deep discounts, Vistara neither offers cheap tickets nor discounts. Its pricing principle is derived from its parent SIA, which follows a premium pricing model. Vistara is also the first airline in India to offer a value-based frequent flyer programme called ‘Club Vistara’, where loyalty points are accrued based on customer expenditures on fares in contrast to a loyalty programme based on total miles travelled. In other words, a registered Club Vistara member gets points based on the money he/she has spent on travelling. The advantage of such a system lies in the fact that it takes into consideration fluctuating air ticket prices so that the customer does not miss out on points. In other words, the more a passenger spends, the more points they get, a feature not available in a miles-based rewards system (points based on distance travelled). Another advantage is that all Club Vistara members, irrespective of the class they may choose to travel, get priority services (check-in, boarding and baggage handling), lounge access and increased baggage allowance (Vistara, 2021). Vistara does not have any hidden pricing strategy and follows uniform pricing rules, based on market dynamics.

The airline had adopted the system of charging higher prices much before the journey dates, which was ultimately reduced as the journey date came closer due to low seat occupancy. This contrasted to other airlines, which initially charged low prices but increased them as seats were occupied. This was one of the reasons for Vistara’s low performance over the years in terms of customer acquisition.

In the initial days, selling the premium economy seats, whose prices were 75% higher than economy seats, was a challenge as little attention was paid to policies of premium economy by airline companies. These seats got sold only after the economy class filled up. It is always advisable for an airline to discount early if it has such a policy.

Vistara Place and Distribution Strategy

Vistara’s hub is at Indira Gandhi International Airport (IGI), New Delhi. The company has rapidly expanded its footprint, both in terms of network and in terms of service proposition. As per the company’s website, ‘Vistara currently serves 36 destinations with over 200 flights daily operated by a fleet of 33 Airbus A320,1 Boeing 787-9 Dreamliner™, 1 Airbus A321neo and 7 Boeing 737-800NG aircraft. It has already flown more than 20 million customers since starting operations’ (Vistara, 2020). Flight tickets can be booked through its website (

Vistara Promotion and Advertising Strategy

In its initial days, Vistara had to face constraints due to a small marketing team because of which it was not able to market itself effectively. However, they soon realized their mistake and worked extensively on brand promotion and advertising. Apart from the traditional forms of marketing such as billboards, television or print media, Vistara also started focusing on social media marketing through creative and innovative content. Another form of marketing was internal marketing, where the employees were well trained and followed dress codes to project an image of sincerity, discipline and a customer-friendly attitude.

‘Fly Higher’ Brand Campaign

The Fly Higher campaign was built on Vistara’s tag line ‘Fly the New Feeling’, with an aim to enhance customer loyalty by assuring them of the level of class, quality and attention to detail in the skies in accordance with different spheres of their lives such as career, lifestyle and travel choices (Sengupta, 2018).

The campaign was based on wide-ranging customer insights, suggesting that customers today do not intend to settle for less than the best. This is evident from the living standards of present-day Indians who not only choose challenging careers and create their own success stories but are also willing to spend luxuriously on holidays, food, shopping etc. and look forward to the best quality and service in everything they select. However, when it came to flying, there was an aversion for full-service experiences. Vistara challenged this hesitation by giving flyers a reason to select their airline too with the same discerning eye to quality and customer experience: ‘Why settle for second best when you can fly the best?’

The new integrated campaign went on air on 14 December 2018 and ran for nearly 75 days from the launch. The campaign was deployed across multiple platforms, including cinema print, outdoor, digital media and TV, aiming to cater to a wide range of travellers.

The Yogic Safety Promotion

Full-service carrier, Vistara released its first-ever in-flight safety video in August 2020 that was displayed in its brand-new Airbus A321neo and Boeing 787-9 Dreamliner aircrafts. It showcased safety instructions by mixing various yoga asanas or postures with an aim to create a visual appeal and hold the interest and attention of customers. It aimed to take customers on a relaxing journey to some of the most scenic and off-beat locations across the length and breadth of India and project India as a travel destination. Vistara also added that it was the first time that an airline of Indian origin had gone beyond aircraft cabins to illustrate in-flight safety. The safety messages were also conveyed through sign language in the video.

According to Vinod Kannan, Vistara’s Chief Commercial Officer, ‘There was no better way to show Vistara’s Indian roots and its global, contemporary outlook than this. Yoga is one of India’s greatest gifts to the world, practiced by hundreds of millions of people, and our country’s diverse landscape continues to surprise natives and visitors alike. The video combines both these aspects with important safety briefing to help travellers remain not just safe, but also arrive feeling fresh at their destinations’.

However, in spite of the company’s innovative advertisement campaigns and promotion strategies, the generation of customer value has not reflected in the company’s financial statements.

Financial Analysis

Vistara has been struggling continuously to generate positive returns due to intense competition, volatility in crude oil prices and the depreciation of the rupee against the US dollar.

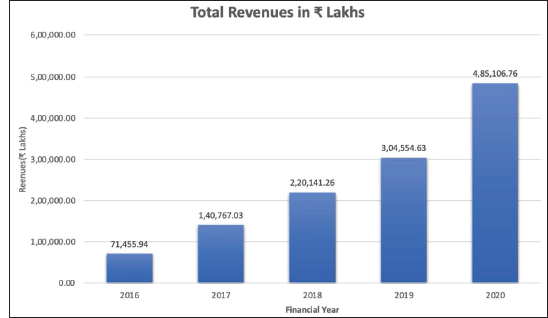

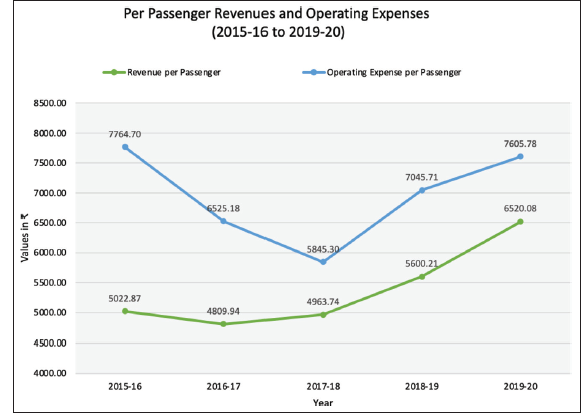

Although Vistara’s revenues have grown at 190% CAGR from 2016 (Figure 4), its earnings before interest, taxes, depreciation and amortization, (EBITDA); earnings before interest and taxes (EBIT); and profit after tax (PAT) margins are constantly below zero even as its parent companies are continuously pumping in equity capital y-o-y. Aviation turbine fuel (ATF) costs, aircraft lease rents, and repair and maintenance costs have also seen a higher increase as compared to the increase in revenue. This is also observed in the per passenger metrics of Vistara from 2015–2016 to 2019–2020, where the revenue per passenger and operating expense per passenger saw a decrease in the gap till 2017–2018, but since then, the gaps have somewhat widened, owing to increased losses for the airline company (Figure 5).

Vistara somewhat benefitted from the downfall of Jet Airways in April 2019 as it got access to the latter’s airport slots and premium class traffic. It also inducted seven Boeing 737 aircraft flown by Jet Airways and increased its fleet from 22 to 40 by March 2020. The number of destinations rose from 24 to 36, including 5 foreign destinations by the end of financial year 2019–2020.

Coming to the financial aspect, it is startling to see that the company recently took a lot of long-term debt, increasing the debt equity ratio from 0 to 1.1 in financial year 2020.

Vistara also increased its equity by infusing more capital, which will help the airline maintain liquidity as it has had to dip into cash reserves post the pandemic to cover fixed costs and payments to aircraft lessors. Domestic flights were suspended until May 25, after which travel restrictions were eased gradually. The ban on flights led to a significant revenue erosion for the airlines. But repeated infusion of capital without trying to improve or change the business model does not present a picture of sustainable growth for the airline.

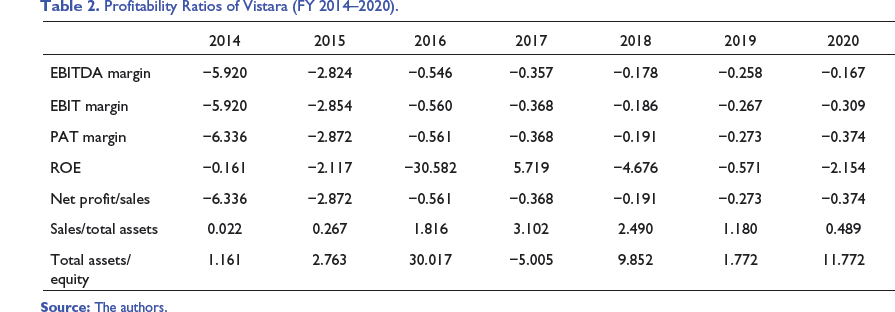

Profitability Ratios of Vistara (FY 2014–2020).

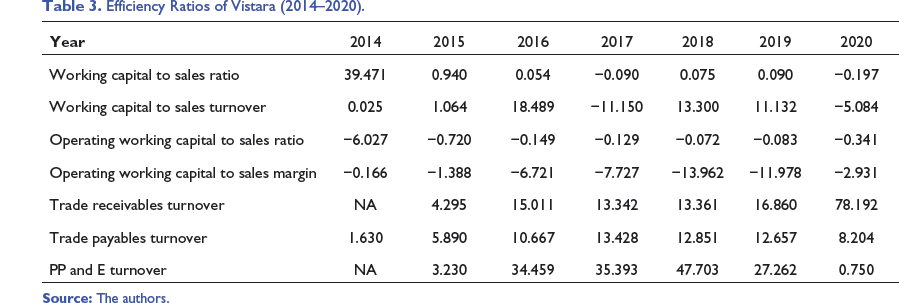

Efficiency Ratios of Vistara (2014–2020).

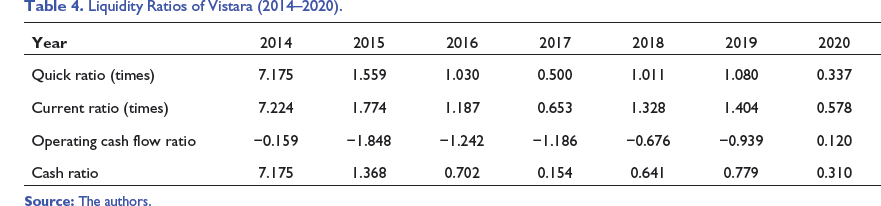

Liquidity Ratios of Vistara (2014–2020).

Vistara is operating in a tight liquidity condition (Table 4) and the recent capital infusion of ₹5.85 billion is a step to rescue Vistara from mounting liabilities and poor liquidity health.

Generally, the time gap between the initiation and achieving the break-even point in sales for an airline company in India is 18 months to 36 months, with consideration of the high-cost structure of aviation in the country, including expensive jet fuel and high airport charges.

It seems that given the current scenario, it would take not less than 4–5 years for the airline to turn profitable or break-even, given rising operational and jet fuel costs, worsened by intense competition.

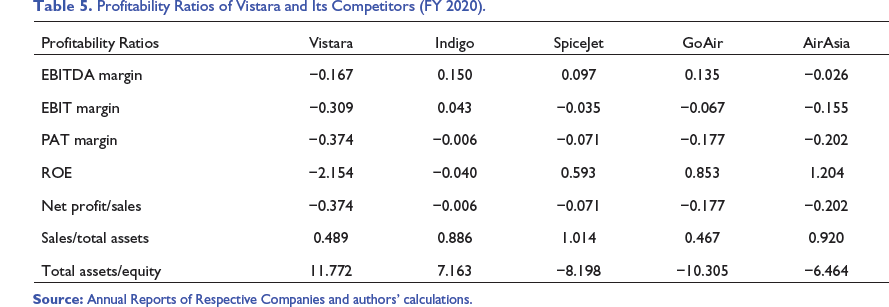

Profitability Ratios of Vistara and Its Competitors (FY 2020).

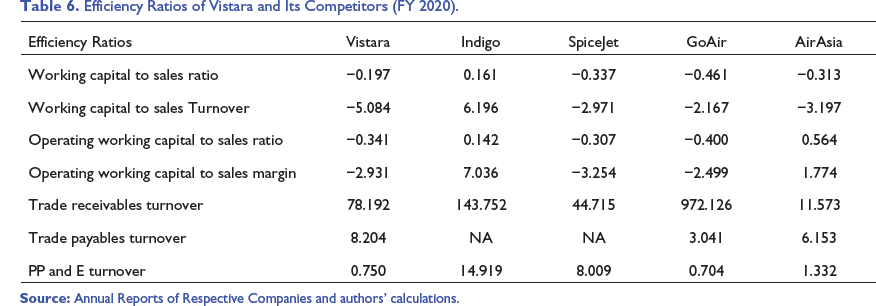

Efficiency Ratios of Vistara and Its Competitors (FY 2020).

In terms of efficiency, Vistara has performed better than most of its competitors but lags behind Indigo (Table 6). The operating working capital ratio of Vistara is worse than its competitors, but it is only better than GoAir. Similar situation exists in case of PP and E turnover.

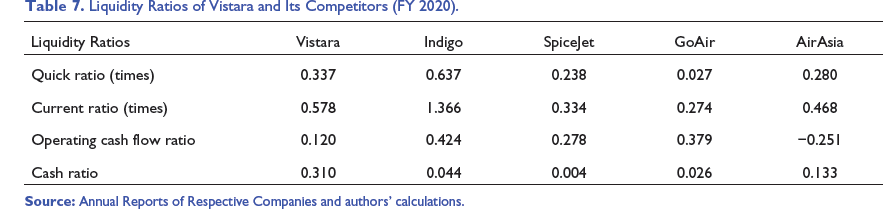

Liquidity Ratios of Vistara and Its Competitors (FY 2020).

Debt and Solvency Ratios of Vistara and Its Competitors (FY 2020).

Compared to its peers, Vistara has much higher liabilities to equity, debt to equity and debt to capital ratios, which may cause issues in the future (Table 8). Even its debt to capital ratio is high (next only to GoAir), which may increase stress on the company’s balance sheet. Most of Vistara’s liabilities are long-term liabilities that would require significant capital or revenue generation to be paid off.

Price to Sales Valuation

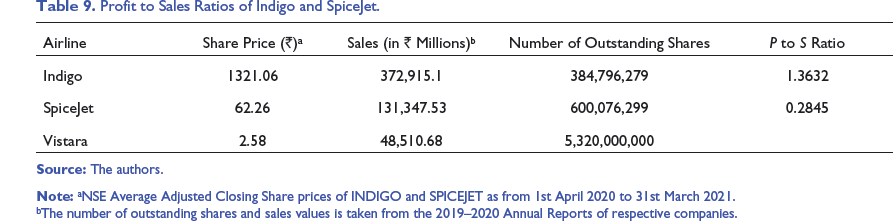

Profit to Sales Ratios of Indigo and SpiceJet.

aNSE Average Adjusted Closing Share prices of INDIGO and SPICEJET as from 1st April 2020 to 31st March 2021.

bThe number of outstanding shares and sales values is taken from the 2019–2020 Annual Reports of respective companies.

Since Price to Sales ratio = Market Capitalization/Revenue = (Share Price * Number of Outstanding Shares)/Revenue

If we consider the P to S ratio of SpiceJet, we can calculate the probable share price of Vistara. The sales for Vistara in FY 2020 was ₹48510.68 million and, from the number of outstanding shares, the price comes out to be ₹2.58 per share (Table 9).

Competitors

Comparative Analysis of Traffic Data

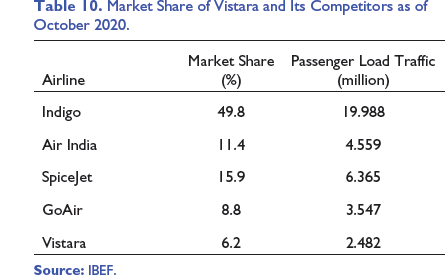

Market Share of Vistara and Its Competitors as of October 2020.

Indigo’s success in the industry mostly stems from its brand value that projects an image of reliability. Indigo has the record of having most of the flight departures and arrivals on time, as compared to others (On-time Best Domestic Airline, 2021). As can be seen in Figure 6, the passenger load of Indigo has seen a much sharper rise, compared to its rest of the peers, while Vistara has struggled and even saw a decline as compared to Air Asia India, another of Tata’s joint ventures. This may suggest a form of cannibalism, where the market share of one joint venture is lost to another.

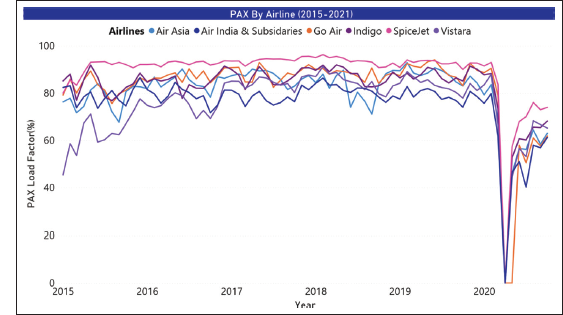

PAX refers to the number of passengers carried by an airline. It gives a measure of how many seats in an airline’s flight are occupied by passengers. As can be seen in Figure 7, SpiceJet has the highest average PAX from 2015 to 2020, which means it is most efficient in filling up the seats on its flights. This is followed by GoAir (which only has a market share of 8.8%) and Indigo (market leader), which have also maintained a good PAX over the years. It indicates that the operational strategies of these airlines are efficient. However, when it comes to Vistara, it has performed only better than Air India.

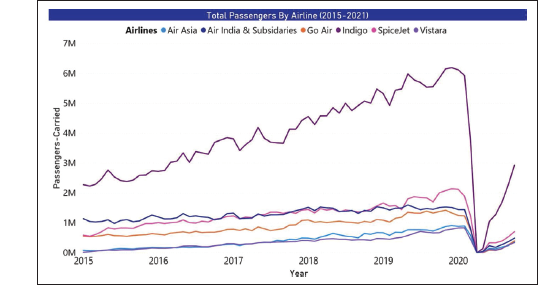

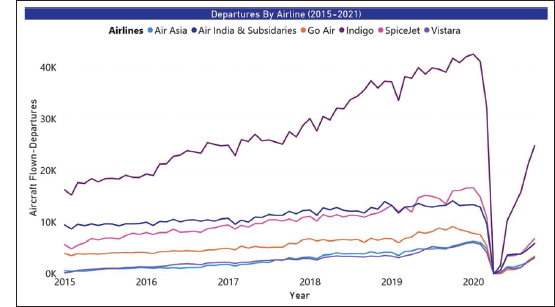

The number of departures is driven by total flights of an airline company departing in a particular time period. Increasing number of departures may be due to either increased frequency of flights or introduction of new routes or both. Looking at Figure 8, we can say that Indigo has again dominated the market due to its vast domestic air network in India. From 2015 to early 2019, Air India remained in the second position but later, lost it to SpiceJet. Vistara and Air Asia remained on the lower end of the graph, which also indicates a slow rate of expansion as compared to others.

In summary, it can be said that due to Vistara’s flawed business model, it has not been successful so far in achieving leadership in any of the performance metrics.

Air India

Air India is India’s national carrier. It was initially launched by J.R.D. Tata with the name ‘Tata Airlines’ in 1932 and later renamed as ‘Air India’. However, in 1951, the airline was nationalized, keeping in line with the socialist policies of the then Indian government. Due to lacklustre performance of the airline for the past few years and increasing pressure on the government exchequer, the central government has decided to privatize the airline. However, irrespective of its problems in the management, the airline had three advantages—financial backing from government to cover up losses, being the preferred airline for all government employees and membership of Star Alliance that permitted the airline to avail code-share benefits of other members of the alliance. However, its major problems pertain to the use of outdated technology, lack of change in mindset and lack of customer satisfaction. With privatization on the cards, things are expected to improve. As of December 2019, Air India flew to 57 domestic destinations and 45 international destinations with a fleet size of 125. Its primary hub is in Delhi with a secondary hub in Mumbai.

Air Asia India

Air Asia India is another joint venture of Tata Sons (51%) with Malaysia-based Air Asia (49%). It started its operations in 2013 and currently operates out of Bengaluru’s Kempegowda International Airport and has secondary hubs in Mumbai, Delhi and Kolkata. Unlike Vistara, it is a low-cost carrier. Its operating expertise comes from the parent company Air Asia, which is famed for operating with the lowest cost per seat per available seat per kilometre and has consistently maintained its record for being the world’s best low-cost carrier. The benefit it obtains from Tatas is their expertise in knowing the Indian market and leverages the creditworthiness among the supply chain partners. It operates only Airbus A320-200s and A320neos with an aim to reduce maintenance and other operating costs. Due to COVID-19 and a history of losses for the joint venture, it was speculated that the Tatas may have to choose one joint venture over the other. In December 2020, there were speculations that the Tatas may increase the ownership of the airline to 87%. It operates a total of 33 aircraft with 200 daily flights per week, covering 21 destinations across India (AirAsia India Emerges No. 1, 2020).

Indigo

Indigo is owned by Interglobe Aviation Limited and is India’s leading airline in terms of market share (49.8%). It operates as a low-cost airline with a no-frills approach. In other words, apart from availing flight services, a passenger must pay extra for all other services, including food and beverage. There is no in-flight entertainment in its flights. The only disadvantage of such a model is the initiation of deep discounting and price wars its model could lead to. However, for passengers willing to spend less for flights, Indigo is a great option. It has a fleet of 262 aircraft, which cover 63 domestic destinations and 37 international destinations (Explore our Destinations, 2021). It has code-share agreements with Qatar Airways and Turkish Airlines. It has its primary hub at IGI Airport, Delhi.

Since its net profit declined by 93% as of March 2020, it had to dip into cash reserves due to the COVID-19 pandemic. But it has recovered to 70% of its operating efficiency and operates 1,000 daily flights as of December 2020 (Press Trust of India, 2020).

The airline has the following value proposition: ‘On-time, Low Fares, Courteous and Hassle Free flight experience’ (Interglobe Aviation Limited, 2020). It is the only Indian airline to be ranked among the top 20 airlines of the world for on-time performance, 3 times in a row (OAG Punctuality League, 2020).

SpiceJet

As per the company’s annual report:

FY 2019-20 has been nothing short of challenging. From setback in our growth strategy due to global grounding of Boeing 737 Max fleet to rise in ATF prices, from rupee depreciation to shutdown of airline operations due to onset of COVID-19 pandemic, the challenges were manifold.

SpiceJet is only second to Indigo in terms of market share (15.9%). It was founded in 2005 and operates a variety of aircraft under its fleet for both passenger travel and cargo shipping, the latter under the brand name ‘SpiceXpress’. As of March 2020, it was India’s largest cargo operator in terms of domestic and international cargo operations and has dominated India’s regional connectivity segment (connecting smaller towns with bigger cities, a feature not performed by Indigo). Although there is not much difference from Indigo in terms of passenger services strategy, the airline has capitalized much on cargo shipping business. It has a low-cost carrier model, which makes it quite prone to competitive pricing. However, due to high average PAX values and a diversified business strategy, it can compete in the Indian aviation industry. The airline operates Boeing 737-Max and Q400 Bombardier aircraft and is the best choice for short-to-medium haul flights. It has code-share agreements with Emirates and Gulf Air. It has a fleet size of 105 and operates 240 daily flights on 47 domestic and 10 international routes (SpiceJet Limited, 2020).

Go Air

Go Air is owned by the Wadia Group and was founded in 2005. It is also a low-cost carrier that operates 27 domestic and 9 international destinations. As of September 2020, it operated 600 daily flights. As per the company, its business model is based on ‘punctuality, affordability and convenience’, quite similar to Indigo (About Us, 2021). It currently has a fleet size of 55 (mix of Airbus’ A320-200s and A320neos), with 144 orders of Airbus A320neos in place. With a small market share and competition against Indigo and SpiceJet, the airline has little to differentiate. The company’s website mentions the following:

GoAir, India’s fastest growing airline, has once again recorded the best On-Time Performance (OTP) at 67.6% as per the latest report of November 2019 month released by the Director General of Civil Aviation (DGCA). The airlines also has one of the highest load factors in November 2019. As per DGCA report, the load factor in November was 92.7% as against 83.1% in October 2019.

However, in recent times, the airline has tried to adopt a differentiation strategy by offering adjacent seat on the same passenger name record (PNR) with an aim to provide additional safety. It also offers online doctor’s consultation in association with on-demand healthcare platform MFine.co. According to the press release:

Visiting a hospital or dispensary for consultation could be risky, whereas the MFine app connects the passenger to top doctors in the city from the most trusted hospitals. Passengers can consult with experts across 30+ specialities including physician, orthopedician, diabetologist, paediatrician, gynaecologist, skin & hair specialist, dietitian, dentist, heart specialist, ophthalmologist, ENT specialist, et al via chat, audio or video call. The MFine app can also help GoAir passengers get consultation for COVID-19 symptoms. If there are any symptoms of flu or any viral infection, then passengers can get their symptoms assessed by an expert doctor.

Way Forward

‘Airline branding is a challenge because it builds from the customer experience: thousands of passengers taking thousands of flights, and thus consistently delivering on the brand promise is difficult’.—Tim Calkins, clinical professor of marketing, Kellogg School of Management, Northwestern University.

Despite Vistara’s unique value proposition, it failed to generate the desired outcomes, the fundamental problem lying in its business model. The single most important factor affecting the company’s profitability is operating expense. Equity infusion by parent firms is not a sustainable strategy in the long run. With the outbreak of COVID-19, it seems the break-even point for Vistara will be delayed even further. Therefore, this calls for the company to revisit its business model and strategy in such a manner that the customer value should be reflected in the firm’s financial statements. Effective risk management strategies should be formulated and executed on a priority basis. Focus on improving operating efficiency and the management of operations will also play a key role in improving business performance. With no government bailout in sight, it is left up to the airline companies to plan their recovery. The same applies to Vistara. To increase its market share, it needs to change its marketing strategy, which is the need of the hour. One of the possible solutions could be to incentivize people to choose Premium Economy, and it needs to be carried out in a such a manner to ensure a behavioural shift from Economy to Premium Economy, rather than Business Class to Premium Economy. This essentially implies survival of the Premium Economy Class without dilution of the Business Class yields. Another area of focus for the airline would be on improving PAX values. It needs to ensure that all its flights’ seats are occupied without compromising too much on ticket prices and quality. Due to the COVID-19 situation and uncertainty looming, the aviation sector is most likely to take a few more months to bounce back (Bhargava, 2020). In such a scenario, it will be more appropriate for Vistara to reduce its debt holdings and focus only on equity-based funding, as it had been following since its inception. The recent capital infusion into Vistara by Tata Sons through the rights issue is a significant move in this context. Another strategy could be to defer deliveries of its aircraft. Looking at things from a long-term perspective, it would be wise and prudent to define a minimum cash reserve policy, considering a volatile industry. That would be a step ahead to reduce risks. Despite losses due to the COVID-19 pandemic, the airline has gained the opportunity to revisit its overall business model and strategy and its contracts with other back-end players that lead to increased cost burden on the company.

Footnotes

Acknowledgement

Foremost, we would like to thank the almighty, divine and Supreme Lord who has bestowed upon us good health and blessings in preparing this case.

We would also like to thank Dr Sakshi Sharma, Assistant Professor, Atal Bihari Vajpayee School of Management and Entrepreneurship, for her continuous and utmost guidance, patience, motivation, enthusiasm, mentorship and support in the preparation of this case. We could not have imagined a better mentor for the case study preparation.

Lastly, we thank our parents, friends and benefactors who have rendered support to us during the drafting of this case.

Declaration of Conflicting Interests

Funding

The authors received no financial support for the research, authorship and/or publication of this article.