Abstract

One psychological barrier to putting money aside for retirement may be an inability to fully empathize with the economic woes of one’s future self. In tests of ways to lower this barrier, previous studies have had experimental participants interact with visualizations of their future selves. Despite the promise shown by such interventions in small-scale tests in the lab, little is known about their effectiveness in the real world. Our research evaluates the effectiveness of an aging filter (that is, software that creates an image of how a participant might look when older) in a randomized field study involving nearly 50,000 people saving for retirement in Mexico. The intervention, carried out over a month, modestly increased the number of account holders who made one-time contributions (from 1.5% in the control group to 1.7% in the treatment group, representing a 16% increase), as well as the value of those contributions. Although the total amount of money put aside was modest and the number of sign-ups for a recurring contribution savings program did not change significantly, this intervention proved cost-effective: It increased savings at a rate almost 500 times the cost of the intervention. Such psychologically informed interventions can effectively complement other initiatives to encourage people to save for retirement.

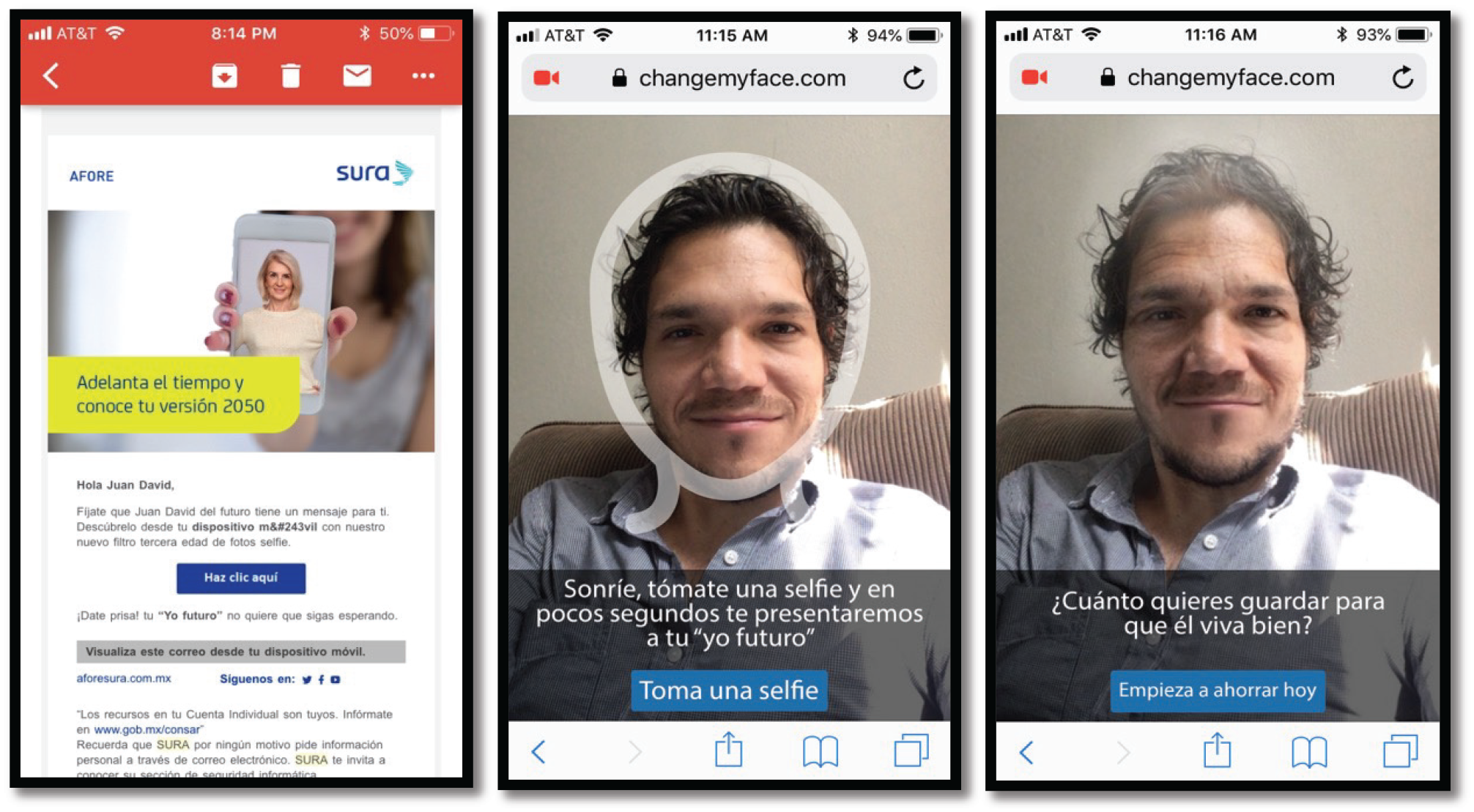

One day in August 2018, a middle-aged woman’s phone pinged with a text message from her bank in Mexico, asking if she wanted to contribute to her retirement savings plan. But the message, delivered as part of our study, did not contain just words: It also invited her to look at a photo depicting what she might look like when she is 60 years of age. Would the image help her to feel an affinity with her future self and prompt her to save more for the future? If it did, would that strategy be an inexpensive way for policymakers to encourage people to invest money for their retirement?

In many nations, retirement savings fall far below the amount considered sufficient to maintain preretirement standards of living. In Mexico, the retirement pension system changed in 1997 to a defined contribution system, in which employers are required to deposit a set amount of each paycheck into a retirement account, with employees then encouraged to make additional contributions themselves. The mandatory contributions are set by the government; as we write this article, the rate is just 6.5% of a worker’s salary. Through these mandatory contributions alone, workers are projected to receive less than 30% of their preretirement salary in retirement, far less than the traditional benchmark of 75% that is generally considered sufficient to provide a secure retirement.

More than 99.5% of Mexico’s 40.5 million registered account holders do not make any additional contributions in a given year. 1 Moreover, 60% of workers are in the informal work sector and do not have any mandatory retirement savings, making their financial futures particularly vulnerable. 2

Countries around the world take various approaches to encourage retirement saving. Some, for instance, automatically enroll workers in savings plans and require them to actively opt out if they do not want to participate. Yet even when such choice architecture interventions are used, there still may be room to increase both participation in plans and the amount saved. In Mexico, as in many other nations, increasing retirement contributions could improve the financial situations of millions.

Although some people may not save for retirement because they are struggling to pay for the essentials of day-to-day life, many are also deterred by psychological barriers. For instance, some may lack the willpower to save when facing the temptation to spend on something they want now,3,4 or they may find it hard to predict how they will feel in the future about decisions they make today. 5 In this article, we focus on a related barrier: the difficulty people have identifying with—and feeling concern for— their future selves.

Previous theoretical work suggests that people may think about their future selves—the selves who may benefit from or be punished by choices made today—as if they are other people altogether.6,7 Thinking of the future self as another person can, in theory, have a detrimental effect on long-term decision-making and planning. For example, it is easy to eat too much pizza and chips in the present moment or splurge on an unaffordable car when the future consequences of obesity or debt are thought of as “someone else’s problem.” In this light, impatience is simply a form of self-interested behavior—a person acts for the benefit of their current, present self rather than their future self.

Of course, people do at times make sacrifices for others, particularly people they feel close to, like family and friends. Therefore, it might be the case that people will make sacrifices for their future selves if they feel as connected to their future selves as they do to their friends and family. 8 This theory has been borne out by some early, small-scale studies in the lab. In one study, for example, people who felt more connected to their future selves accrued more assets in savings, even when the researchers controlled for demographic factors. 9 And in another study, high school students who felt more connected to their future selves maintained higher levels of academic performance. 10

How can the gap between current and future selves be narrowed? Consider a technique used by charitable organizations: Presenting people with salient and vivid representations of charity recipients (for example, through stories about who the recipients are and how the charity has helped them) makes them more likely than those who are not presented with such representations to make donations. 11

Drawing on that finding, researchers have attempted to increase the vividness of future selves to induce people to take better care of those distant selves. For instance, when participants were shown vivid, visual representations of their future selves in laboratory contexts, they were more likely to make contributions to a hypothetical long-term savings account 12 and opt for more ethical paths when given the opportunity to cheat. 13

Despite the promise seen in the results of such interventions from small studies conducted in lab settings, little is known about their effectiveness in large-scale field settings with real consequences. This is an important gap in the research: Field trials can help to inform the theories that motivate an intervention, 14 and achieving success in the field is critical before policymakers can justify widely deploying any intervention to address societal problems, such as inadequate saving for retirement. 15 This is the gap we set out to address in our study.

Method

We ran our field experiment in Mexico throughout August 2018 on all 48,853 clients who had retirement accounts with a specific fund administrator and used an online mobile banking app called AforeMovil to set up and make voluntary contributions to those accounts. This popular app is provided by the government regulatory commission CONSAR (Comision Nacional del Sistema de Ahorro para el Retiro) and is available to all retirement savings plan providers (known in Mexico as Administradoras de Fondos para el Retiro). We split the group in half randomly on July 25, 2018, allocating 24,427 account holders to the treatment group and 24,426 to the control group.

The two groups did not differ in terms of their members’ gender, initial savings, and age (see Table S1 in the Supplemental Material for a detailed analysis). Seventy-three percent of the account holders from the whole study group were men, and the average total retirement

savings balance was 212,200 Mexican pesos (approximately US$10,500), out of which 8,650 pesos (approximately US$420) were voluntary savings. For context, the average monthly household income per capita in Mexico at the time was approximately US$240. 16 Sixty-one percent of account holders were in the high-risk investment portfolio designed for those 36 years of age and younger, 23% were in the portfolio designed for 37- to 45-year-olds, 15% were in the portfolio for 46- to 59-year-olds, and 1% were in the portfolio for those over 60.

The intervention for the treatment group involved three main stages. First, account holders received an invitation message with a link to meet their future self. Second, those clicking the link were directed to a web page where they could take a selfie and see an age-progressed rendering of their future self (see Figure 1). A computer algorithm, made by an anonymous commercial company in collaboration with our research group, automatically aged the person’s image to approximate what they would look like in about 20 years. Third, after taking this step, account holders saw a message below their aged photo asking how much they would like to save for the person in the picture to live well, along with a link to the savings page on the app. Account holders could then choose to enroll in the recurring-deposit program, make a one-time contribution, or do both.

The results of the aging filter on a selfie

To increase the likelihood of attracting account holders’ attention, we planned to send each account holder nine invitation messages—three emails, three mobile phone text messages, and three push notifications in the app—over the course of one month. We also used three different themes along the following lines for the phrasing in the invitations: “How will you look in old age?” (aiming to spark a sense of curiosity); “message from your ‘future self’“ (aiming to grab attention through mystery); and “limited time, try it today” (drawing on a sense of urgency). 17 (See Figures S1-S7 in the Supplemental Material for the full text of the email, text, and app messages in Spanish and English.) The order of the type of communication used (email, text, or push notification) and the message theme was randomized. Whether or not account holders clicked on the links, took a selfie, or made a contribution, they received all scheduled invitations throughout the month. Because of a logistical issue, one of the planned emails was, in the end, not sent, so each account holder received a total of eight invitations.

The control group also received messages (by email, text, and push notification, at the same times as the treatment group) encouraging them to save. These messages had themes similar to those in the messages sent to the treatment group but did not mention the aging photo filter. In translation, the text messages, for example, read, “Do you want to save for retirement? Click here!”; “Have you started saving for retirement? Click here and program your savings!”; and “Don’t waste more time, click here and save TODAY for a better future.” Each control message had a link directly to the saving app.

Results

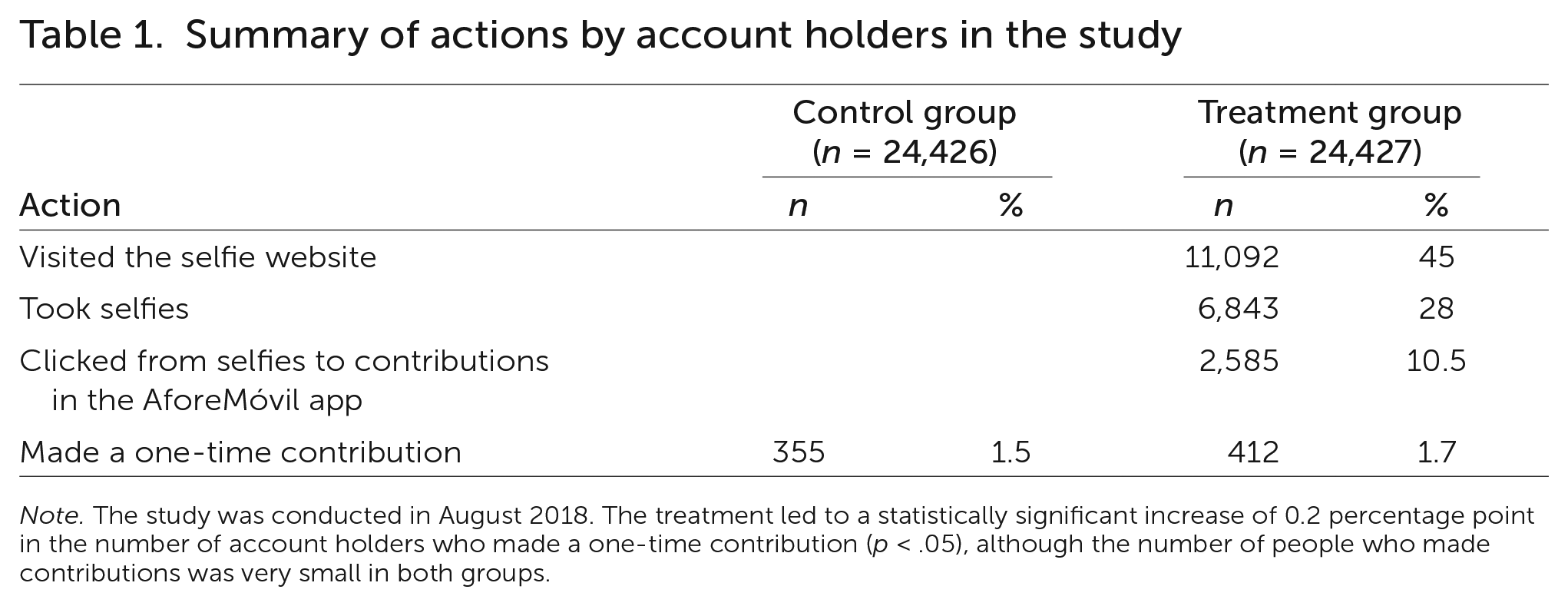

Almost half of the treatment group chose to click through to the photo filter page at least once. A total of 11,092 account holders (45% of the treatment group) at some point clicked

through, together making 32,615 visits to the web page. Of those who visited the photo filter web page, more than half took selfies: 6,843 account holders (28% of the treatment group) took a total of 13,041 selfies. Then 2,585 account holders (10.5% of the treatment group) clicked on the AforeMovil contribution link a total of 3,013 times (see Table 1).

Summary of actions by account holders in the study

Note. The study was conducted in August 2018. The treatment led to a statistically significant increase of 0.2 percentage point in the number of account holders who made a one-time contribution (p <.05), although the number of people who made contributions was very small in both groups.

In terms of engagement, email and mobile phone text messages proved more effective than the app’s push notifications at generating initial interest: 42% of first visits to the photo filter web page came from emails, 40% from text messages, and 18% from push notifications. The theme of the message also mattered: 44% of first visits came from the “how will you look in old age” communications, 39% came from the “message from your ‘future self’“ communications, and 17% came from the limited-time communications. When the effects of all communications were analyzed, we found that the same patterns held, and the differences were significant at the p <.01 level. (See Table S6 in the Supplemental Material for more details, and see note A for a discussion of the statistical terms used in this article.)

Overall, we found that men were more likely than women to take a selfie, click through to the app, and make a contribution. Also, the probability increased with the age, rising from one age group to the next. Looking at retirement account balances and salary levels, we found that the probability of completing the entire process increased with the account balance of the account holder and decreased with the salary level. (Overall, these findings were significant at p <.05; see Table S2 in the Supplemental Material for a detailed analysis.)

As we noted earlier, account holders could enroll in the recurring-deposit program, make a one-time contribution, or do both. Before starting our study, we preregistered (https://aspredicted.org/blind.php?x=uu88y4) two main outcomes—whether clients enrolled in a recurring-deposit program and whether clients made any voluntary contribution (that is, whether they made a one-time contribution or signed up for the recurring-deposit program)—as well as the magnitude of the contributions. Given the extremely low retirement savings contribution rate in Mexico, upon reflection, we realized we had failed to include a simple analysis of one-time contributions. Because this information is of practical interest, we report three outcomes: recurring-deposit sign-ups, one-time contributions, and whether account holders made any voluntary contribution.

We found no significant effects in the percentage of account holders who enrolled in the recurring-deposit program, perhaps because signing up for recurring deposits is a large commitment and thus hard to influence, nor did we find a statistically significant effect on the likelihood of making any voluntary contribution. Nonetheless, the treatment modestly increased the number of account holders who made one-time contributions to a statistically significant extent: 1.5% of the control group made contributions (355 people), compared with 1.7% of the treatment group (412 people; p <.05). (See Table 1; also see Table S3 in the Supplemental Material for a detailed analysis.) Although a 0.2% increase sounds small, this means that 16% more people in the treatment group than in the control group made contributions.

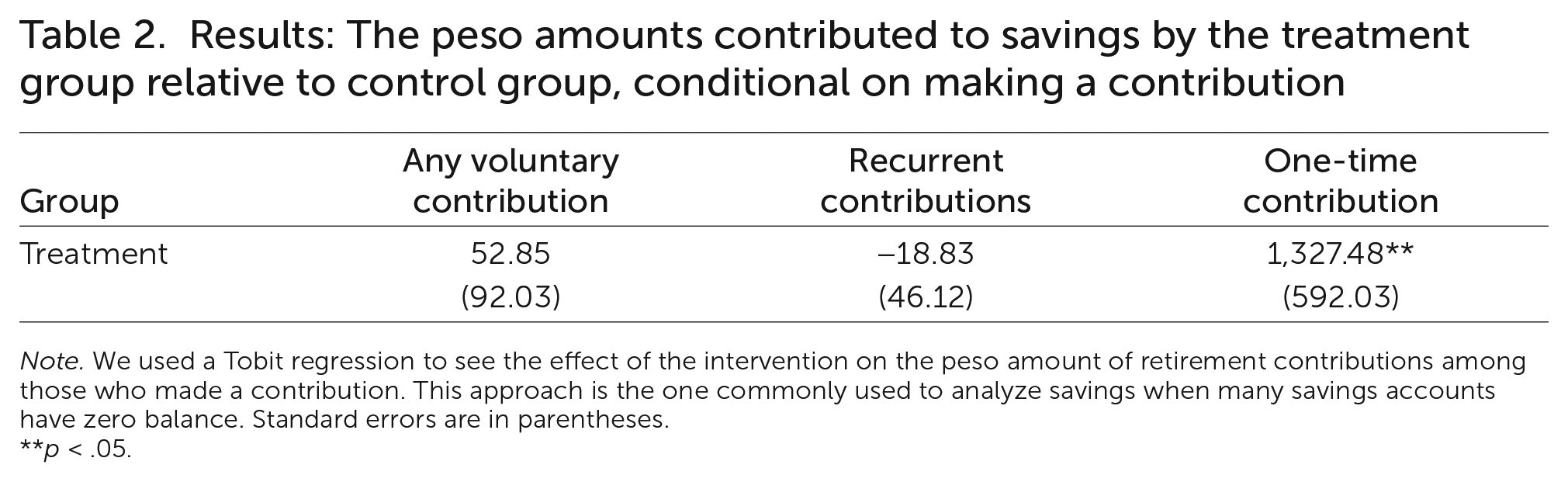

Given that over 98% of account holders in the study made no contributions to their retirement savings, any effects among the people who did contribute get diluted in simple statistical regressions, the kinds of analyses often done with this kind of data. A more informative approach is to use Tobit regression—a statistical approach that isolates the effect from the subset of people making nonzero contributions. This is the common model used to analyze savings when many accounts have a zero balance. With this approach, we found that the intervention greatly raised the average amount of single contributions (conditional on a contribution being made): The average contribution in the control group was 3,063 pesos, and the average contribution in the intervention group was 1,327 pesos higher (a 43% increase). (See Table 2; see also Table S4.) Not all people in the intervention group completed the process (in other words, not everyone who had the opportunity to take a selfie did so); this suggest that the effect we found is a lower bound of the effect of the intervention on the people who went through the intervention.

Results: The peso amounts contributed to savings by the treatment group relative to control group, conditional on making a contribution

Note. We used a Tobit regression to see the effect of the intervention on the peso amount of retirement contributions among those who made a contribution. This approach is the one commonly used to analyze savings when many savings accounts have zero balance. Standard errors are in parentheses.

p <.05.

Collectively, account holders in the treatment group contributed 54% more to retirement in August than the control group did: 1,675,974 and 1,087,422 pesos, respectively. Although these seem like large increases in money, these results should be treated with caution given the very small number of people making the contributions leading to these amounts.

Finally, we explored whether income level, age, gender, and formal employment influenced the retirement contributions made. (We used mandatory contributions as a proxy for formal employment, given that these contributions are made by employers.) We found some evidence that the intervention increased recurring savings of individuals aged 37-45 years by 305 pesos compared with the recurring savings of individuals in the treatment group who were younger than 36 years or older than 46 years (p <.05). We also found that for the people in the treatment group who made voluntary contributions, those contributions increased by about 16% per additional peso of income (p <.01; see Table S5 in the Supplemental Material for detailed analysis). In other words, those with a higher income may have been more influenced by this intervention. This pattern may reflect the fact that for many workers with limited incomes, saving even a little is a considerable burden, and this intervention may not influence such workers.

These results should be interpreted with care, however, given the large number of tested parameters in this model and the noisy nature of our income measure. Indeed, employers in Mexico widely underreport income because of tax incentives and to reduce the money they must contribute to retirement accounts.

Perhaps the most interesting aspect of the intervention is its cost-effectiveness. The development of the aging photo filter itself and the host web page cost 139,490 pesos (US$7,000). The text messages cost 0.56 peso (US$0.028) per message, in this case totaling roughly 82,940 pesos (US$4,130), and push notifications and emails had no direct costs outside of the time and effort required to administer them.

At present, about 20 million people in Mexico have retirement savings plans, 2.2 million of whom use AforeMovil. Using emails and push notifications alone to share the aging photo filter web page, it would be possible to scale this intervention to all 2.2 million current AforeMovil users for about 112,785 pesos (US$5,500) per month, given the costs of the photo filter license and AforeMovil staff time.

Extrapolating from our results that the intervention increased the number of contributors by 0.2%, we calculate that this expansion could result in an additional 4,400 contributors out of 2.2 million people, generating an increase of 53,004,600 pesos (US$2,584,782) in voluntary retirement savings in just one month. That translates to about 470 pesos in savings generated per 1 peso invested.

Discussion

Around the world, policymakers are keen to encourage people to save more for their retirement. To help, researchers have introduced a variety of interventions based on principles of social psychology and behavioral economics. For example, requiring employees to opt out of a default defined-contribution plan rather than waiting for them to opt in to such a program can increase the number of people who participate in a retirement plan. Such strategies have been shown to greatly increase the number of employees who contribute to their retirement funds. 18 Similarly, introducing an automatic escalation feature for retirement saving plans (in which workers have their paycheck contributions automatically go up each fiscal year without having to take any action) has also had a positive effect on saving rates. 19 But these effective interventions are not used everywhere. Mexico, for one, does not use them. Even in countries where they are used, employers must implement them. Also, workers across the world are increasingly turning to contract work: Some estimates predict that close to 50% of the American workforce could be contract workers by 2030. 20 So it would be useful to come up with additional ways to encourage individuals to increase their voluntary retirement fund contributions.

The treatment we implemented—exposure to age-progressed images—led to a 16% increase in the number of account holders who made one-time contributions to their retirement savings accounts (off a modest baseline) as well as an increase in the average amount they saved. Our results suggest that investing in the intervention on a large scale would be cost-effective: When scaled up across the 2.2 million account holders in Mexico, the approach could result in an additional 470 pesos saved per 1 peso spent on the intervention.

Given the complex set of factors that affect who saves what for their retirement, it is reasonable to expect that the effects of any one intervention should be small. 21

Our study did have some limitations. Because we could test this intervention only with the customers who already had the online banking app, our results may be less relevant for people who do not have the app or even a bank account, which may be true more often for people with low incomes and informal or no employment. Further, because the aging filter was hosted on an external website and not directly within AforeMovil, some account holders may have had logistical difficulties going through the steps of the whole intervention process, from taking a photo to making a retirement saving deposit. All of the results should also be treated with some caution given the large number of outcomes we analyzed, which may have inflated the chance of finding significant effects.

The design of this field study does not allow us to determine why viewing age-progressed images led people to contribute more money to retirement. In theory, such images should enhance an emotional connection to and concern for the well-being of one’s future self, as previous research has found.12,22 However, other factors could help to explain the increase. For example, the treatment may have led individuals to simply pay more attention to the savings decision, and this additional attention could have increased their contributions. If possible, future research— in the field and in the lab—should examine such alternatives.

Our study answers a growing call for psychological research to address pressing societal concerns. 23 We have shown that helping people to construct vivid, realistic images of their future selves can affect their real decisions to increase savings for the future. However this effect is accomplished, the findings suggest that from a practical standpoint, using age-progressed photos could complement existing successful strategies for increasing retirement savings.

Supplemental Material

sj-pdf-1-bsx-10.1177_23794607231190607 – Supplemental material for Saving for retirement: A real-world test of whether seeing photos of one’s future self encourages contributions

Supplemental material, sj-pdf-1-bsx-10.1177_23794607231190607 for Saving for retirement: A real-world test of whether seeing photos of one’s future self encourages contributions by Juan David Robalino, Alissa Fishbane, Daniel G. Goldstein and Hal E. Hershfield in Behavioral Science & Policy

Footnotes

endnote

A. Editors’ note to nonscientists: For any given data set, the statistical test used—such as the chi-square (x2) test, the t test, or the F test—depends on the number of data points and the kinds of variables being considered, such as proportions or means. The p value of a statistical test is the probability of obtaining a result equal to or more extreme than would be observed merely by chance, assuming there are no true differences between the groups under study (this assumption is referred to as the null hypothesis). Researchers traditionally view p <.05 as the threshold of statistical significance (also referred to as a 5% significance level), with lower p values indicating a stronger basis for rejecting the null hypothesis. Standard deviation is a measure of the amount of variation in a set of values. Approximately two-thirds of the observations fall between one standard deviation below the mean and one standard deviation above the mean. Standard error uses standard deviation to determine how precisely one has estimated a true population value from a sample. For instance, if one took enough samples from a population, the sample mean ±1 standard error would contain the true population mean around two-thirds of the time.

author affiliation

Robalino: Universidad San Francisco de Quito. Fishbane: ideas42. Goldstein: Microsoft Research. Hershfield: University of California, Los Angeles. Corresponding author’s e-mail:

author note

The authors acknowledge generous funding from MetLife Foundation and assistance with intervention design and implementation from Andrew Fertig and Marcela Cheng Oviedo.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.