Abstract

Some studies have provided empirical evidence that firms’ high growth rates just before economic crises are negatively associated with resilience. Other authors have observed that firms that grow fast in the early phases of an external crisis are generally more resilient. This countercyclical behavior is less common in small- and medium-sized enterprises (SMEs), and literature has not delved into the underlying factors that facilitate SMEs’ countercyclical strategies. Firm exploration is defined as a firm’s willingness to experiment, take risks, be flexible, and accept variation. Our thesis is that exploration acts as a countercyclical factor by slowing down a firm’s growth before the external shock takes effect, favoring growth during the crisis, and providing better resilience outcomes. We find support for our hypotheses from a sample of 2,081 manufacturing medium-sized enterprises.

Keywords

Introduction

Economic downturns are to firms what curves are to F1 cars. Some are extremely difficult, such as Loews, the legendary 180° turn for F1 cars in Monaco, or the recent Great Recession (2008–2012) for firms. These curves force drivers to brake hard before turning, whereas other curves are easy and can be taken at full speed. Braking just in time is the key to entering sharp curves safely and allowing the driver to recover speed inside the turn and exit it without losing too much time.

Like a racecar overcoming curves, firms face mild, moderate, and highly complex external crises. In recent years, at least two crises have been global in scope: the Great Recession, triggered by the global financial collapse, and the recent COVID-19 pandemic. These crises have posed a huge challenge to many of world’s firms, especially small- and medium-sized enterprises (SMEs), which have suffered most from their effects. 1 These rare and stressful events, which can undermine the stability and security of any organization, have brought firms’ resilience outcomes, that is, their capacity of resisting and recovering (Annarelli & Nonino, 2016; DesJardine et al., 2019) to the frontline of current research (De Smet et al., 2020; Iborra et al., 2020; Wenzel et al., 2020).

Drivers know that they have to brake before the most difficult turns, which allows them to accelerate progressively inside the curve and exit it accelerating. This is how they handle tight curves efficiently. In this work, we argue that firms can achieve good resilient outcomes in a similar way. Entering the curve at too high a speed, because of braking too late or not braking at all, means that the driver has to brake inside the curve and exit it slowly or end up in a crash. When entering economic downturns, some firms slow down their growth, others accelerate fast increasing their growth, and others, apparently, do nothing.

Regarding firms’ behavior before recession, some studies have provided empirical evidence that firms’ high growth rates just before a recession starts are negatively associated with their resilience to the crisis (Burger et al., 2017; Geroski & Gregg, 1993; Knudsen, 2011). On the contrary, with regard to behavior in the early stages of an external crisis, other authors have observed that fast-growing companies generally prove to be less vulnerable, that is, more resilient (De Smet et al., 2020; Geroski & Gregg, 1996; Higson et al., 2004). In addition, there is evidence that high pre-crisis growth is rarely associated with high growth within the crisis (Geroski & Gregg, 1996). Consequently, like good drivers, firms that reduce growth before an economic downturn can grow more during the first stage of the crisis and end up with better resilience outcomes.

Despite the fact that these countercyclical behaviors appear to be key to understanding SMEs resilience after a global and external crisis, researchers have not addressed the underlying factors of countercyclical strategies; in other words, they have not identified the variables which could explain how some SMEs are able to “brake before the curve and then accelerate inside,” as well as how this capability influences the firm’s later performance. To answer this question, in this article, we take a closer look at these factors, focusing on exploration, which is an essential and characteristic component of organizational ambidexterity in SMEs and one of the dynamic capabilities that is more associated with resilience.

Organizational ambidexterity is defined as the ability of an organization to be simultaneously efficient in its management of current business requirements—also called exploitation orientation—and adaptive to changes in the environment, known as exploration orientation (Duncan, 1976). Previous research has argued that organizational ambidexterity is a dynamic capability that (1) requires the development of sensing, seizing, and transforming activities (Luger et al., 2018; Teece, 2020; Vahlne & Jonsson, 2017); (2) plays a significant role in integrating the contradictory demands of exploration and exploitation (Lubatkin et al., 2006); and (3) enhances SMEs’ resilience (Iborra et al., 2020).

In a crisis, SMEs usually monitor their operations closely and ensure costs are contained. This tendency of companies toward exploitation is natural, given the observable and short-term returns compared to those of exploration (March, 1991). While exploitation will make it easier for SMEs to minimize losses through downsizing or reducing unnecessary costs (Schmitt et al., 2010), in this article, we argue that SMEs’ exploration may help them break through inertial behaviors and adapt to external changes (Schmitt et al., 2010), providing the chance for achieving countercyclical behavior.

Economic downturns have a huge impact on the economy and society (Knoop, 2004). Many firms, mainly SMEs, which potentially have a long-term future, do not withstand the difficulties caused by crises because they tackle them with the wrong strategy or under bad internal conditions (Geroski & Gregg, 1996). How to effectively manage a firm through business cycles remains one of the most important but overlooked areas in research (Lagesh et al., 2018).

In this article, we aim to deepen the knowledge around this topic, addressing issues that have not yet been studied regarding firm growth and resilience in crises. We particularly focus on how exploration affects pre-crisis and crisis growth, on the relationship between pre-crisis and crisis growth, and SME resilience outcomes, that is, SMEs’ resistance to crises and how they recover from them. Our central thesis is that exploration in SMEs acts as a countercyclical factor, slowing firm growth before the external shock hits and favoring growth during the crisis, which then leads to better resilience outcomes. We tested our hypotheses on a large sample of 2,081 manufacturing medium-sized enterprises using multivariate techniques. The data confirm our hypotheses.

Our research contributes to the literature on firms’ resilience, highlighting the role of countercyclical behavior in the face of external shocks. Furthermore, our study offers evidence for the influence of such behavior on SME resilience, since small- and medium-sized firms are able to reduce their growth before the crisis and then increase it during the crisis, or in other words, “brake before the curve and then accelerate through it.” We also contribute to the dynamic capabilities literature emphasizing the importance of exploration as a driver of countercyclical behavior and providing empirical evidence for it.

In addition, our results have several implications for managers: first, because they highlight the essential role played by dynamic capabilities in managing growth before and during crises; second, because they stress the importance of creating a long-term vision when managing a firm’s finances and strategy; and third, because exploration-oriented SMEs are able to anticipate turnaround strategies ahead of the recession phase.

The article is structured as follows. In section “Literature review and hypotheses,” a literature review and the hypotheses are presented. The descriptions of the context, data set, research methodology, and results are provided in section “Methods.” Finally, section “Discussion and conclusion” discusses the findings and offers the conclusions, implications, and future research directions.

Literature review and hypotheses

Our study is situated within the theoretical and empirical research framework on the growth of firms exposed to external economic shocks. In addition, it examines their capacity to adapt, resist, and recover in that context. These shocks are cyclical, affecting most of a nation’s industries, and typically give way to two phases, recession and recovery, which are preceded by a growth phase.

Firm growth has been explained by several general theories. In the study of the relationship between growth and failure to make the changes needed in crises and to overcome them, theories such as organizational inertia theory and the dynamic capabilities approach are often cited.

According to the inertia theory, inert organizations resist change because of both resource rigidity—that is, failing to change their resource investment patterns—and routine rigidity—that is, failing to change the organizational processes that use those resources (Gilbert, 2005). Bolle and Kårbø (2015) explain that

during recessions, firms are faced with the sudden need for adaptation. This change might be temporary, given that recessions have limited duration, but adaptation might still be required. Fast growers might be particularly vulnerable if their quick growth has induced high inertia pressures. (p. 127)

According to the dynamic capabilities approach, dynamic capabilities make it possible to foresee the crisis, design a response, and implement the necessary changes before and when it arrives, mitigate its effects (Teece, 2014). Thus, one explanation for high growth before the bubble bursts is that firms do not appear to anticipate shocks (Geroski, 1999), nor the severity or scope of their blowback effects (Phan & Wood, 2020) because of a lack of, or low level of, anticipatory capacity in them. Also, many firms’ lower resilience in crises is understandable because of their lack of dynamic capabilities and their incompetence in designing and executing effective responses (Makkonen et al., 2014).

SME growth and resilience

The literature supports the hypothesis that pre-recession growth and good performance in crises are negatively correlated, mainly because of poor performance during the recession phase. However, the strong random component in the evolution of business growth has become evident (Coad, 2007a, 2007b). Lien (2010, p. 5) claims that fast growth occurring late in a boom leads to a longer contraction in the recession period, which makes it harder to recover the previous sales levels after the crisis. Also, Burger et al. (2017) found that demand reductions in firms with high growth rates in the pre-recession period affect their resilience outcomes.

Regarding the rationale for that hypothesis, Knudsen (2011) states that

high pre-recession growth rates make firms more vulnerable to recessionary pressures because the marginal customers who enter a market in the later stages of a boom and cause the growth are likely to be the first to exit the market when the good times end. Therefore, the contraction in demand is likely to be larger for firms with higher pre-recession growth, which makes them more vulnerable to recessions. (p. 5)

Growing a lot before a crisis implies that firms must assume certain inefficiencies that can be detrimental when hard times come. In practice, all firms go through more or less temporary episodes of inefficiency, particularly when undertaking major investments (including takeovers) or growing very rapidly (Geroski & Gregg, 1996, p. 552). For this reason, if the selection pressures created during a recession are brought to bear on the short-run efficiency differences between firms, those firms that grow rapidly in the pre-recession period and have to cope with adjustment costs may be affected, as these costs make them temporarily inefficient (Geroski & Gregg, 1996).

Finally, due to the managerial constraints that hinder firm growth—what is known as the Penrose effect, which suggests that corporate growth rates are not persistent over time (Mahoney & Pandian, 1992)—, high pre-crisis growth is rarely associated with high recession growth (Geroski & Gregg, 1996, p. 556).

Empirical evidence seems to confirm the above hypothesis. Geroski and Gregg (1993) found that in the UK recession of the early 1990s, firms with higher pre-recession growth were more severely affected. Probit regressions performed by these authors in another study, identifying failing firms, revealed that pre-crisis growth was positively and significantly related to the probability of going into receivership (Geroski & Gregg, 1996). In a Norwegian study, Knudsen (2011, 2019) found that during the Great Recession, higher pre-crisis growth levels made firms more vulnerable and more likely to experience reduced demand. In another study of Norwegian companies in the same period, Bjørkli and Sandberg (2012) provided evidence that those which had grown to high levels during the pre-crisis years were more vulnerable to the crisis in terms of their competitive advantage. Peltonen (2014) analyzed the performance implications of procyclical and countercyclical strategies of Finnish software SMEs in the period 2008–2012 and found that countercyclical strategies led to a better sales compound annual growth rate. And a recent study by Burger et al. (2017) for several countries during the Great Recession confirmed the hypothesis that firms with a high pre-recession growth rate were more likely to experience lower demand for their products.

It is known that crises, which entail reductions in demand and restrictions on access to finance, hit SMEs particularly hard and significantly reduce their resilience. Several studies have shown that SMEs are more sensitive to cycles (Burger et al., 2017; Hardwick & Adams, 2002; Peric & Vitezic, 2016) and more dependent on external financing (Gertler & Gilchrist, 1994). The latter authors studied the cyclical behavior of SMEs and large manufacturing firms concerning monetary policy over a broad time span and found that, following tight money, SMEs’ sales declined faster than large companies’ sales over a period of more than 2 years. According to them, the differential response of SMEs to tight money is due to both the direct impact of monetary policy and its indirect impact, causing an overall decline in economic activity because, as they state, SME growth is more sensitive to movements in the economy (p. 33). It follows that the greater the pre-crisis growth, the harsher the effect of the financing constraints, and therefore, the lower the growth during the recession, which undermines resilience outcomes.

The Penrose effect has been supported in the case of SMEs, which have less managerial capability than large firms to maintain pre-recession sales levels. For example, Bolle and Kårbø (2015) used annual financial statement data from around 20,000 Norwegian firms from 1999 to 2012 to study two recessions: the 2001 dot-com crisis and the Great Recession. They found that fast growers experienced negative effects from their growth during the most severely affected years, 2002–2003 and 2009.

These reflections can be summed up in the following proposition: SMEs are very sensitive to economic downturns, but countercyclical growth favors their resilience outcomes. Here, we will operationalize this by establishing the following hypotheses.

H1. The higher an SME’s sales growth just before the start of an economic crisis, the lower the sales growth in the recession phase. (Marginal customers’ market exit and Penrose effect hypotheses)

H2. The higher an SME’s sales growth just before the start of an economic crisis, the lower the resilience outcomes. (Pre-crisis inefficiency hypothesis)

Exploration in SMEs as an antecedent of countercyclical behavior

Knudsen (2019) proposed and provided empirical evidence that innovative (explorative) firms are more resilient in crises because of their dynamic capabilities. One way to cope with external shocks is by trying to anticipate them. Usually, SMEs do not have enough resources, for example, in terms of a business intelligence department, or to invest in anticipating external shocks. However, some researchers have found that some SMEs are able to develop specific sensing, seizing, and reconfiguring capabilities (Teece, 2007); that is, they are able to explore their environment and discover new opportunities, take advantage of them effectively, and change or reconfigure themselves. Moreover, some SMEs become ambidextrous (Cao et al., 2010; Lubatkin et al., 2006; Tushman et al., 2011), that is, they are able to undertake exploitation and exploration activities simultaneously, with the first ability being related to concepts such as refinement, efficiency, and productivity, while the latter is associated with variation, risk, experimentation, and flexibility (March, 1991).

Available empirical evidence also shows that ambidextrous SMEs typically achieve resilience because they can pick up the signals of change in the environment, seize opportunities, recognize threats, challenge organizational inertia, and reconfigure themselves (Iborra et al., 2020). We argue that it is reasonable to think that SMEs’ ability to anticipate demand shocks and deploy countercyclical strategies as the best way to face crises may rely more on their exploration than on their natural tendency to exploit. In this sense, Walrave et al. (2012) argue that exploration implies that managers engage in discovery actions and in detecting business opportunities. More importantly, they will be more focused on the future rather than on the past or present environment, that is, detecting changes in the environment and adapting the company to the requirements imposed by the recession. Exploration can help SMEs to detect external changes, overcome inertial behaviors, and align their strategies with the environment (Schmitt et al., 2010).

Furthermore, just as organizational inertia does not favor commencing reforms before a crisis, once the company enters one, the rigidities arising from inertia will also prevent the company from making the necessary changes to adapt to the new situation, resulting in a more pronounced downturn (Bolle & Kårbø, 2015). Here too, exploration will help firms to break inertia, foster change, and take advantage of new opportunities.

In summary, we argue that SMEs with exploratory capabilities are better at coping with disruption and change because they are quicker to identify problems and develop alternative action plans, and as a result, they implement countercyclical measures in the early stages of the crisis (recession phase) using innovative, agile, and novel approaches (Iborra et al., 2020). Furthermore, exploration is an enhancer of managerial capabilities, which reduces the negative impact of the Penrose effect. Explorative firms are also better prepared than non-explorative firms, who do not replace customers lost during the first phase of the crisis with new customers by offering new products or adapting to meet their needs. As Walrave et al. (2012) argue, exploration enables firms to uncover opportunities that could be relatively scarce during a recession. In this respect, in an economic downturn, the decreased level of munificence in terms of less readily available finance means that business opportunities are less common (Sidhu et al., 2004), and hence, for non-explorative SMEs more difficult to exploit.

In addition, explorative SMEs are better able to break out of inertia since they are more flexible in changing their strategy and structure to increase their resilience outcomes. It can be thus argued that exploration is a precursor to countercyclical behavior in SMEs, and therefore, we can propose the following hypotheses:

H3. Explorative SMEs grow less before an economic crisis begins. (Shock anticipation. Dynamic capabilities hypothesis).

H4. Explorative SMEs grow faster in the recession phase of an economic crisis. (Identification and exploitation of opportunities. Dynamic capabilities hypothesis).

Methods

Sample and context

We tested our hypotheses on a large sample of Spanish manufacturing firms that faced the Great Recession. The global economy was shocked by this crisis, which offers a natural experiment to investigate the relationships between firm growth, exploration, and SME resilience under challenging circumstances. During this period, SMEs experienced a greater negative impact than large companies did (Bourletidis & Triantafyllopoulos, 2014). Along with the problems derived from reduced demand, there was also a sharp reduction in access to credit. These two factors were particularly difficult for SMEs in European countries such as Spain (European Central Bank, 2013, 2019), which were confronted, much more than large firms, with problems of late payments and lending obstacles (Cowling et al., 2012; Ma & Lin, 2010). This makes this kind of enterprise and this country a good context for testing our hypotheses.

It is commonly accepted that the starting date of the Great Recession was September 2008 (DesJardine et al., 2019). According to national statistics (Spanish National Institute of Statistics, www.ine.com), the recession in Spain took a W-shape, with a midway recovery in gross domestic product (GDP) in 2010. Consequently, in this study, we narrow the first stage of the crisis, that is, the recession phase, to the year 2009, and we analyze the outputs in terms of resilience with data from 2010.

The sample comprised 2,081 active firms. We used the SABI© and ORBIS® databases to obtain the sample data set. This consisted of all Spanish manufacturing firms with 50–250 employees included in these databases and reporting sales of €10–50 million in 2008. We use medium-sized firms since their accounting information is often more reliable than that of micro and small-sized firms. 2 Also, the final sample only included manufacturing firms that had been active from 2000 to 2010. We focused on the manufacturing sector due to the way in which we measure the exploration variable based on brands and patents.

Variables

Gyanwali (2018) claims that annual sales turnover is one of the indicators most commonly used to measure business growth in profit-making organizations, and Weinzimmer et al.’s (1998) research revealed that 83% of studies carried out between 1981 and 1992 used annual revenue to measure firm growth. The literature on resilience in recessions also uses the annual change in sales as a proxy for growth. For example, Geroski and Gregg (1993, 1996) measured pre-crisis growth as growth in sales data (1986–1989) to study the UK recession in the early 1990s, and Knudsen (2019) used firm sales growth between 2006 and 2007 to study the Great Recession. Here, because 2008 was a fiscal year of transition to the crisis, we used the ratio [Sales2008 + Sales2007]/[2 × Sales2006] to measure Pre-Recession Growth. The recession bottomed out in 2009. Consequently, we used the ratio [Sales2009]/[(Sales2008 + Sales2007)/2] to measure the Recession Growth variable.

The literature has usually considered two dimensions of resilience (Buyl et al., 2019): a system’s ability to survive a major disruption and its capacity to “bounce back.” Previous research has measured these dimensions through variables such as survival (e.g., Dolz et al., 2019; Iborra et al., 2022), sales recovery (Geroski & Gregg, 1993, 1996; Knudsen, 2019), employment (Iborra et al., 2020), or profitability (Salvato et al., 2020).

In this article, we measured the resilience output using Altman’s Z-score. This score is an indicator of the financial health of the SME and a predictor of bankruptcy risk (Altman & Sabato, 2007; McGuinness et al., 2018). Other papers on firm resilience (Bravo & Hernández, 2021; Martínez, 2018; Pal et al., 2011; Singh & Rastogi, 2022) and on resilience in the SME context (Pal et al., 2014) use this score as a resilience outcome; and previous work has shown that it is one of the best indicators of long-term performance of firms (Carton & Hofer, 2006).

Altman’s Z-score for private manufacturing firms is based on the following formula: Zʹ = (0.717 × working capital/total assets) + (0.847 × retained earnings/total assets) + (3.107 × earnings before interest and taxes/total assets) + (0.420 × book value of equity/total liabilities) + (0.998 × sales/total assets). The higher the score, the better the health of the company and the lower the risk of bankruptcy.

In this study, we calculated Altman’s Z-score for a set of unlisted manufacturing companies in 2008 and 2010, and the resilience outcome as the difference between these scores (Resilience Outcome = Z2010–Z2008). The resilience score has already been calculated this way before (Bruno & Shin, 2020). Therefore, Resilience Outcome measures the improvement (recovery) in financial health and the reduction in the risk of bankruptcy in 2010 compared to 2008.

Other common measures of resilience outcomes in the literature include recovery of sales, employment, and assets. We discarded sales recovery as an outcome measure to avoid endogeneity problems since the recovery of sales in 2010, by definition, also includes its recovery in the recession phase (2009). Neither employees nor assets were used. Growth in employment and assets is correlated with sales, but their dynamics make growth analyses difficult (Knudsen & Lien, 2019; Weinzimmer et al., 1998). For example, the best companies can boost sales by improving productivity without increasing employment, and the mix and amount of assets may be altered by outsourcing processes and productivity.

Some studies measure resilience based on profitability. We use it through Altman’s Z-score, as this indicator includes it in its formula, it being the factor with the highest weight.

We performed additional robustness analyses to measure resilience using Survival. This variable is commonly employed in resilience studies (e.g., Dolz et al., 2019; Iborra et al., 2022).

Exploration is the independent focal variable. Previous studies based on secondary data have used exploration measures based on R + D investment (Auh & Menguc, 2005; Han & Celly, 2008; Menguc & Auh, 2008), the number of patents (Sarkees et al., 2014), or the launch of new products (He & Wong, 2004). According to Iborra et al. (2020, p. 8), investment in R + D is not easy to obtain from firms’ accounts; however, patents are well collected in international databases and do reflect the output of the exploratory process. On the contrary, as the launch of novel products requires, in most cases, content analysis, an alternative to this indicator is new brands since product launches usually involve trademark registration. Thus, we used the procedure for measuring this construct in manufacturing SMEs, as proposed by Iborra et al. (2020). These authors employed a 4-year variable based on the number of new patents and brands. Our measurement covers the years 2000 to 2007 (new patents and brands released in those years). As in Iborra et al. (2020), the variable is constructed with the average of new patents and brands centered on the median of the firm’s industry. Measures based on patents and brands require averaging over several years because these items show erratic trends due to their scarcity in SMEs (many years give results of zero, even in innovative firms with regular patent and brand activity).

Following the literature on growth and resilience (e.g., Cowling et al., 2015; Fort et al., 2013; Geroski & Gregg, 1993; Iborra et al., 2020; Mahajan & Singh, 2013), we also included firm Size, measured by the log of the sales in 2008, Age in 2008, and Pre-crisis Financial Performance in 2008 as control variables.

Regarding the latter, the Great Recession had a considerable negative impact on firms’ performance, and consequently, its impact was more dramatic for underperforming firms than for well-performing firms (Bjørkli & Sandberg, 2012). More bankruptcies and defaults were observed among firms that performed poorly in the years leading up to the crisis, especially in terms of their financial performance (Iborra et al., 2020). Thus, we also controlled for pre-crisis financial performance in 2008 using the Altman Z-score model. In addition, since the Altman Z-score contains several efficiency indicators, Pre-crisis Financial Performance in 2008 also allows controlling for the effects of the pre-crisis exploitative orientation.

To confirm that exploration has a positive effect in stages away from the crisis, in addition to controlling for Pre-crisis Growth, we introduced a variable called Sales Trend. This variable is the linear regression slope of each firm’s normalized sales for the years 2000 to 2006. This way of measuring growth is recommended when the analysis period spans several years (Weinzimmer et al., 1998).

Hypothesis testing

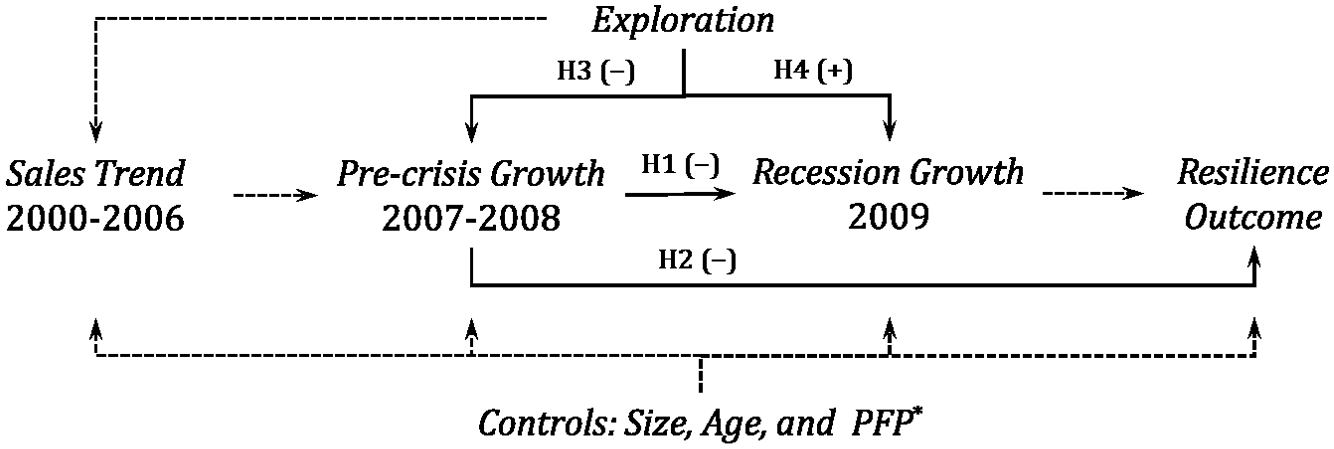

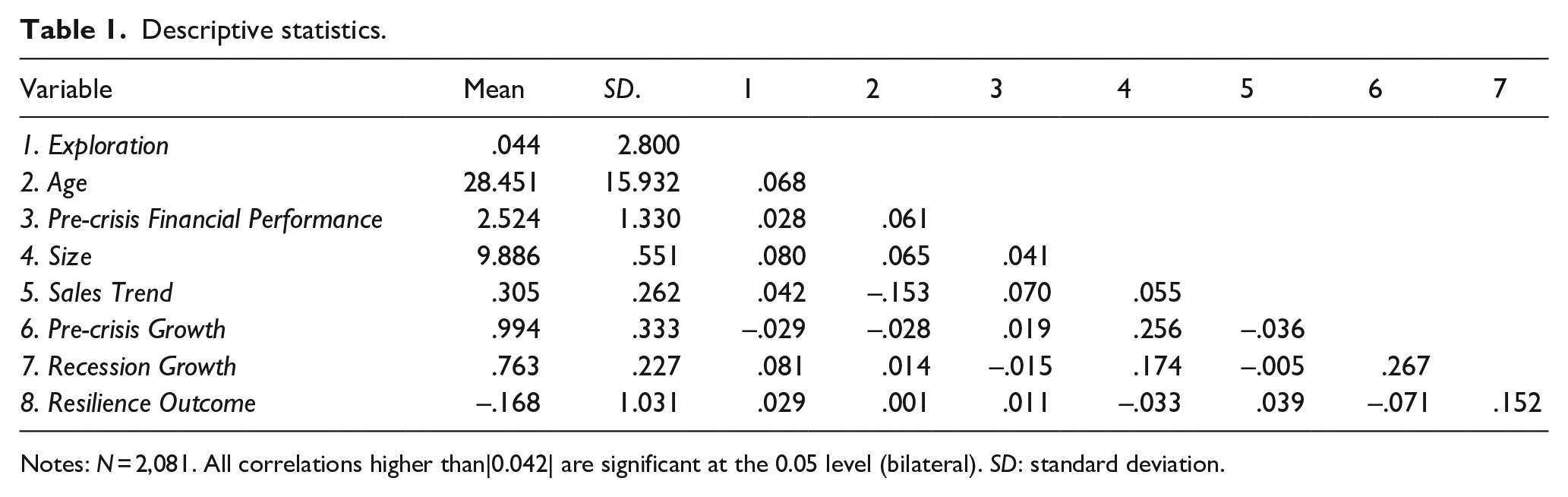

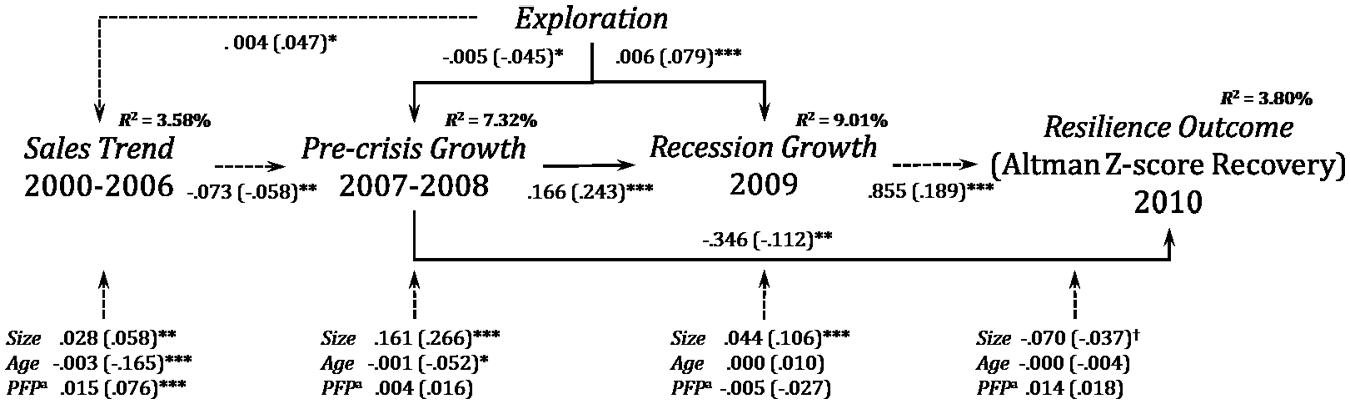

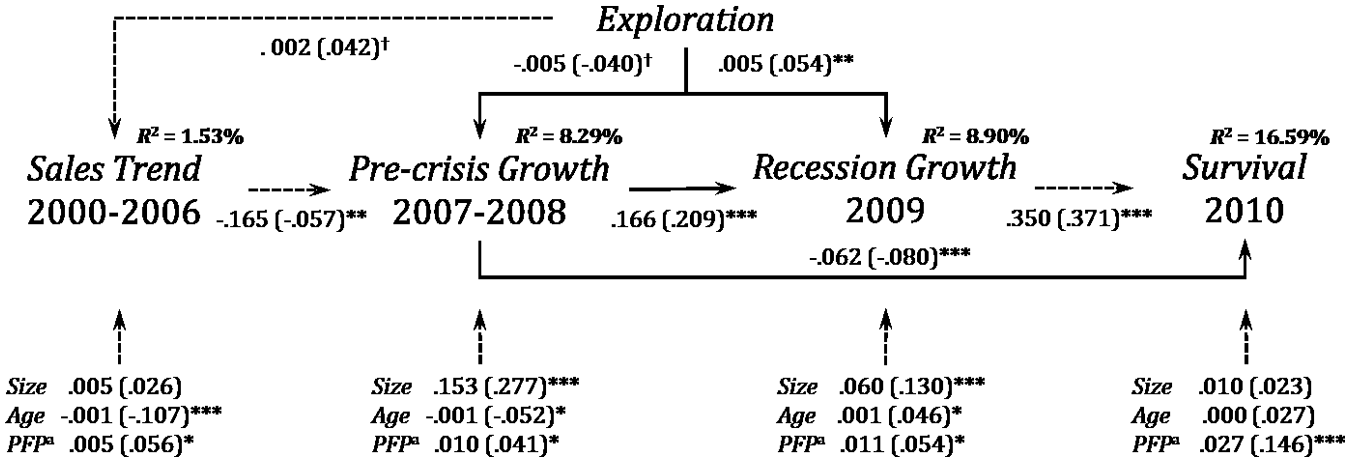

Figure 1 shows the model that will be used to test our hypotheses (solid lines). Given the existence of four dependent variables, we estimated the whole model by applying structural equation modeling (SEM) techniques using the maximum likelihood method. Table 1 shows the means, standard deviations, and correlations of the variables. And Figure 2 reports the structural model results obtained using IBM SPSS Amos 26 Graphics software.

Testing model.

Descriptive statistics.

Notes: N = 2,081. All correlations higher than|0.042| are significant at the 0.05 level (bilateral). SD: standard deviation.

Tested model.

The model fitted the data well, and the goodness-of-fit indicators were within the usual parameters required by the literature (χ2 = 3.226, df = 3, p = .352 > .05; comparative fit index (CFI) = .999 > .90; root mean square error of approximation (RMSEA) = .007 < .08; Byrne, 2010). As discussed in the literature review, growth has a very large random component, so results with high statistical power on growth variables were not expected. Our independent and control variables are able to explain a low but significant variance in the dependent variables. Specifically, the R2 for Sales Trend is 3.58%, for Pre-crisis Growth, 7.32%; for Recession Growth, 9.01%; and for Resilience Outcome (Altman Z-score recovery), 3.80%.

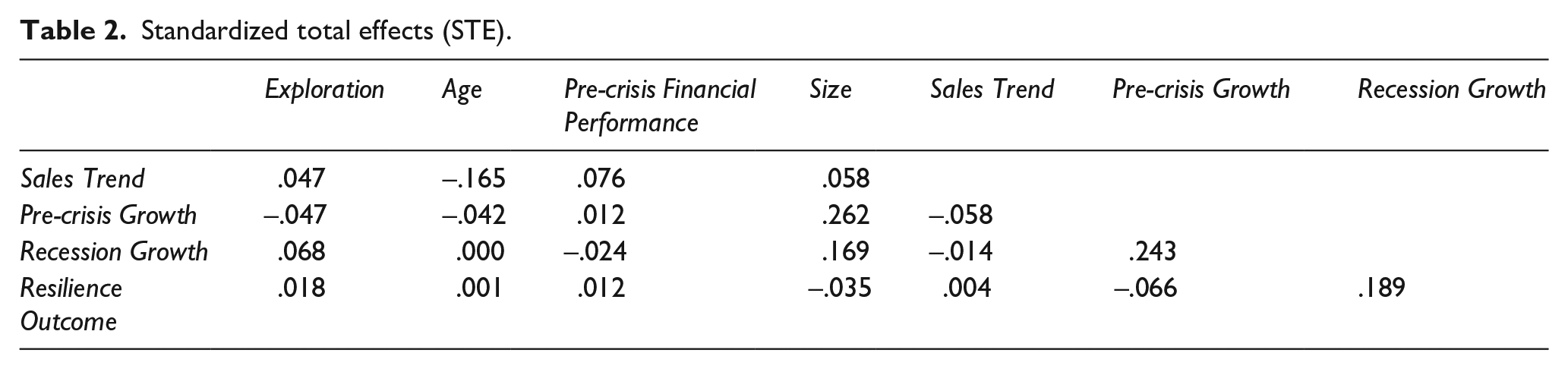

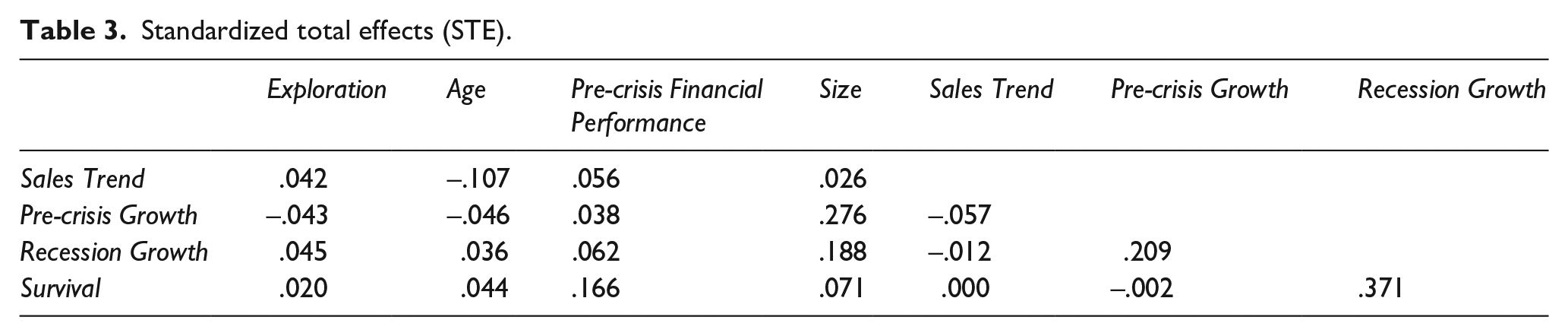

Table 2 shows the standardized total effects (STE) on dependent variables. The variables that most favor resilience are Recession Growth and Exploration, with STEs of .189 and .018, respectively. And those that most harm resilience are Pre-crisis Growth (STE = –.066) and Size (STE = –.035).

Standardized total effects (STE).

In general, our results support the hypotheses of this study. The underlying assumption that countercyclical growth favors resilience is partially supported, as pre-crisis growth negatively influences resilience outcomes (STE = –.066, see Table 2). Hypotheses 1 and 2 predict a negative indirect effect (H1) and a negative direct effect (H2) of pre-crisis growth on resilience outcomes. Contrary to expectations, the indirect effect has the opposite direction to that predicted and is statistically significant (β = .243, p < .05). However, the direct effect on the Resilience Outcome variable has the expected sign and is also significant (β = –.112, p < .05). Although the indirect effect is positive (standardized indirect effect = .243 × .189 = .046), the impact on resilience outcomes is lower than the negative direct effect (standardized direct effect = –.112), together implying a negative STE = –.066, which indicates that pre-crisis growth is negatively associated with resilience outcomes. Thus, our data reject H1 and support H2, but they also support our proposition (i.e., countercyclical growth favors resilience). We will return to these results in our discussion section.

Hypothesis 3 states that exploration has a negative effect on pre-crisis growth. As predicted, the parameter associated with this path is negative and statistically significant (β = –.045, p < .05). It should be noted that this result is influenced by the firm’s size. As can be seen in Table 1, the correlation between the Exploration and Pre-crisis Growth variables is –.029, which is not significant. Nevertheless, when this correlation is controlled for size, the partial correlation between the Exploration and Pre-crisis Growth variables rises to –.051, which is substantial (p < .05) and is the cause of the significance of the regression coefficient associated with this path. Hypothesis 4 proposes that exploration is positively related to recession growth. As expected, the effect of exploration is positive and statistically significant (β = .079, p < .05). Thus, hypotheses 3 and 4 are supported.

Regarding the control variables, Size appears to be a clear predictor of growth but not of resilience. The variable Age of the firm has a negative effect in the years before the crisis, but its impact is not significant in the recession nor in the recovery years. Surprisingly, firms’ financial health in 2008 did not influence growth during the recession nor influence resilience outcomes.

Robustness check

In addition, we tested whether our results were robust to other commonly used resilience measures. We ran another model using the Survival variable in 2010 to measure the Resilience Outcome variable (Figure 3). In this model, Survival took two values: 1 if the firm was active in 2010 and 0 if the firm went into receivership, exit, or liquidation process during 2009 or 2010. To include companies that did not survive in 2009 or 2010, we relaxed the sampling criteria, requiring that they only have data from 2000 to 2008. The newly collected sample contained 2,139 firms.

Alternative Model (Survival as Resilience Outcome).

The results are compatible with those shown in Figure 2. The revised model has an acceptable fit (χ2 = 10.703, df = 3, p = .013, CFI = .991, RMSEA = .035), with an R2 linked to Survival of 16.59%. These results continue to support the hypotheses proposed here, and the STEs of the Exploration variable (Table 3) rise to 0.020 (in the main model shown in Figure 2, the STEs are 0.018).

Standardized total effects (STE).

It is interesting to note that in the revised model, Pre-crisis Financial Performance influences all growth variables and the Resilience Outcome variable. This result is different from that of the main model (Figure 2) and can be explained by the fact that the sample here includes firms that died in 2009 or 2010.

Discussion and conclusion

Discussion and academic contributions

Previous research has shown the relationship of both pre-crisis and recession growth with resilience achieved through countercyclical strategies (Peltonen, 2014), but so far, it has not dealt with the factors that can explain how SMEs can reach these countercyclical behaviors simultaneously. In this article, we put forth the hypothesis that exploration is an antecedent of SME resilience to external shocks since it fosters the adoption of countercyclical strategies, for which we have found supportive evidence.

Exploration may serve to both slow down the pre-crisis growth of firms and accelerate their growth in the recession phase so that they can emerge from the recession with better results. In terms of the recession phase, our results fit with those of Walrave et al. (2012). Their findings from a sample of 86 companies (66 in the United States and 20 in Europe) and 1,720 valid observations over 20 quarters suggest that more attention to exploration during the recessionary period is linked to better performance outcomes.

In addition, other studies have shown that strong growth before a bubble bursts is related to greater suffering during a recession (Burger et al., 2017; Geroski & Gregg, 1993; Knudsen, 2011) and that firms which adopt pre-crisis strategies with a strong emphasis on innovation are less likely to experience reduced demand in the recession period (Knudsen, 2019). Our results support these findings, providing new evidence. On one hand, Hypothesis 3 demonstrates that exploration is a factor that limits pre-crisis growth, achieving its stabilization. On the other hand, our evidence supports the hypothesis that exploration helps reduce the impact of a recession and favors growth in this phase of the crisis.

Furthermore, our results strongly support the positive effects of countercyclical behaviors on performance outcomes and, specifically, on recovery and survival during the 2008 crisis. In this regard, we confirm the negative relationship between pre-crisis growth and resilience outcomes. This finding is consistent with evidence found by Geroski and Gregg (1993, 1996) for the UK recession of the early 1990s and also with Peltonen’s (2014) research, who showed for software SMEs that growing fast in the pre-crisis period is negatively related to performance outcomes. These findings are in line with the greater vulnerability of fast-growing SMEs identified by Knudsen (2011, 2019), Bjørkli and Sandberg (2012), and Burger et al. (2017).

However, we have obtained a result that contradicts our expectations. Our prediction was that pre-crisis growth had a negative effect on recession growth and, through the latter, a negative indirect effect on resilience outcomes. Our results support the opposite, as growth before the crisis is positively related to growth in a recession. This contradicts the theory of marginal customers, which states that customers who emerge in the bubble are the first to disappear in the recession, so firms that grow with these customers before the crisis suffer more during the recession (Knudsen, 2011; Lien, 2010). It also contradicts the Penrose effect, which predicts negative correlations between pre-crisis and recession growth (Geroski & Gregg, 1996; Mahoney & Pandian, 1992).

A possible explanation may be that the prevalence of marginal customers in our sample is low. Our sample is made up of Spanish manufacturing firms. The Purchasing Managers Index for Spanish manufacturing began to decline in 2007, with negative figures (PMI < 50) during 2008. It is therefore likely that 2007 and 2008 were years in which the outflow of marginal customers was already being felt. On the contrary, the firms that managed to survive in 2009 took the place of those who died that year, allowing some firms with solid growth in 2007 and 2008 to continue growing because of the exit of firms in 2009.

Another possible explanation is that customers in this type of sector, where B2B relationships are common, value the supplier’s solvency. This is because, during a recession, the supply guarantee becomes especially crucial. From outside, it is difficult to determine if a supplier’s solvency is close to its image, which is highly influenced by its growth. Hence, it is possible that firms that grew the most before the recession benefited from an improved reputation that allowed them to maintain and increase their customer base.

Finally, the Penrose effect suggests a negative correlation between growth rates in successive periods and argues that a firm’s ability to grow is limited by its resources, especially its internal management system, which acts as both an accelerator and a brake on the growth process (Mahoney & Pandian, 1992). Therefore, one interpretation of our findings is that firms acquired new managerial resources in the pre-crisis period, which fueled growth afterward. In our sample, we found that firms hired more people during the bubble, however, it is unknown if they were managers.

Regarding effect size and statistical significance, according to Sun et al. (2010), effect sizes must be interpreted by directly comparing them to prior effect sizes in the related literature (for example, Iborra et al., 2020; Mayr et al., 2017). Also, in this regard, Tonidandel and LeBreton (2011) state

a large effect in one situation can be pretty meaningless, while a tiny effect in a different situation could be extremely important from a practical standpoint. Any interpretation of a particular effect needs to take the specific context into account. (p. 8)

In this study, Hypotheses 2, 3, and 4 obtained statistical support, although the effect size of the parameters is small. This result is not surprising considering that firm growth in an external shock context is a consequence of many external and internal factors and that available empirical tests have recognized the strong stochastic element in this explanation (Burger et al., 2017; Coad, 2009; Malinić et al., 2020). This explains the small R2 associated with the dependent variables of the tested models (Figures 2 and 3). However, our large sample size allowed us to identify low-impact, albeit statistically significant, relationships. As can be seen in Figures 2 and 3, and Tables 2 and 3, the 2010 resilience outcome was dependent on pre-crisis growth at the peak of the boom and highly dependent on the recession growth. It follows that a firm will likely be more resilient if it moderates its pre-recession growth and expands during the early stages of the crisis. But from the point of view of the effect size, the impact of stabilizing growth before a recession is undoubtedly very small compared to the impact of growth during the recession. In fact, the real countercyclical behavior is growing during a recession.

Our results show that SMEs with high doses of exploration were slightly more cautious during the pre-recession phase. Moreover, they favored growth during the recession, which is a key factor in resilience. Although exploration does not have a large statistical effect on pre-crisis and recession growth, it is an essential factor in understanding the recovery of key financial parameters included in the Altman Z-score, as well as in understanding survival. Our results also support the conclusion that exploration has an impact on growth during a recession, highlighting that it is probably more important to look for opportunities and know how to take advantage of them during a recession than to anticipate their arrival.

Implications for practice

Our results offer implications for managers: first, by highlighting the vital role played by dynamic capabilities in managing growth before and during a crisis, and second, by underlining the importance of developing a long-term vision when strategically managing a firm. Our study supports this line of research by uncovering evidence that developing the ability of exploration provides SMEs with some protection against foreseeable external shocks and with early resilience in crises. SMEs should develop this ability in good times, even though it may not be as profitable in the short term as an exploitation-oriented strategy.

The economic cycles inherent in capitalism are great enemies of the development of exploration capability. In the bubble and during the recession, managers may be tempted to reduce the emphasis on exploration. SMEs with limited resources are particularly affected by the ease with which they can grow through doing business as usual during the bubble years, which prevents resources from being diverted to “other things” (exploration). This is because the cost/benefit analysis of investing in exploitation (doing business as usual) or exploration (doing new things) clearly benefits the former. Likewise, the need to survive in a recession activates retrenchment strategies, and the first to be reduced are those related to exploration (e.g., R&D, market research, etc.). Therefore, managers must prevent the firm’s exploration effort from slacking off in the bubble and recession. This is where the role of the board of directors can be of significant help since they can guarantee that managers will not reorient the company toward exploitation during these two phases of the economic cycle.

Recent literature on turnaround has argued that retrenchment and recovery strategies should be used simultaneously when the firm faces a crisis (Schmitt & Raisch, 2013), rather than retrenchment first and then recovery (Pearce & Robbins, 1993). This is due to the fact that an initial focus solely on retrenchment during a recession may reduce the firm’s ability to innovate and restrict or inhibit effective recovery activities following the recession (Dolz et al., 2019, p. 126). Exploration-oriented firms are more able to combine both strategies. Thus, if they initiate retrenchment and recovery at the same time as soon as they predict the peak of the bubble, they can improve their results in terms of resilience.

Further research

In this article, we analyzed the role of exploration in fostering countercyclical strategies in firms facing economic crises. Despite crises being to some extent predictable, companies are very frequently unable to foresee the exact moment of their arrival nor the severity and scope of their blowback effects (Phan & Wood, 2020). When these kinds of crises occur, exploration can contribute positively to the resilience of SMEs, given that a greater capacity for anticipation is effective in the face of any event with a certain degree of predictability.

The recent coronavirus pandemic caused a different type of crisis, which was completely unexpected, even though, for some time, some gurus had been warning of a pandemic (e.g., Bill Gates or Michael T. Osterholm). One wonders whether, in this kind of crisis, exploration is just as useful for firms’ resilience or whether it merely enables faster adaptation without the need for anticipation. We will have to wait for some time until the pandemic is over and data are available for exploring this promising line of research.

Our hypotheses have been tested on a large sample of manufacturing SMEs. As a result, even though the associations found between variables are weak, they are statistically significant. Nevertheless, future studies should use more refined measures based on survey scales to investigate the countercyclical effects of exploration. Our measure of exploration based on patents and brands leaves out many firms that are genuinely explorative firms. New research that measures exploration more accurately should uncover more powerful relationships, which would also be an opportunity to conduct surveys that include both exploration and exploitation measures. This would allow researchers to test the combination of these two orientations, known as organizational ambidexterity, which is also a cause of countercyclical behavior.

Finally, although we found statistically significant associations between the independent and dependent variables, our empirical method does not allow us to interpret the results in a strictly causal manner. Thus, further qualitative and quantitative research will be necessary.

Conclusion

In this article, we have obtained evidence that firms with an exploration orientation are better able to handle and survive economic crises, such as the recent Great Recession. On one hand, exploration orientation makes firms more cautious in the bubble phase, as they are more informed, which leads them to reduce their level of activity during the pre-crisis years. On the other hand, firms that engage in exploration are more adaptable and better able to spot growth opportunities during economic downturns, which means that their sales are not too badly affected. All of this allows them to emerge from the recession stronger, and they are more likely to survive than those firms which are not explorative.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Conselleria d’Innovació, Universitats, Ciència i Societat Digital, Generalitat Valenciana AICO/2021/309.