Abstract

This study investigates how the Psychological Capital (PsyCap) of small and medium enterprises (SME) leaders has influenced their strategic responses, ultimately impacting the performance of their companies, during the COVID-19 pandemic. Embedded within research on behavioral micro-foundations in strategy, and based on the resource-based theory (RBT) of the individual entrepreneur as well as positive organizational behavior literature, we hypothesize that SME leaders’ psychological resources can act as a strategic advantage during crises by making them adopt cost-cutting and investment measures for their companies performance. By using a sample of 372 SMEs, we find that while leaders mostly use both measures, leaders with a high PsyCap prefer adopting investment measures, which positively influences the performance of their companies during a crisis. However, adopting cost-cutting measures lowers performance. We contribute to the entrepreneurship literature by using PsyCap in the context of the RBT of the individual entrepreneur and shedding light on which measures sustain or increase SMEs’ performance during a crisis.

Introduction

Research on measures to manage and overcome crises as a business leader of a small and medium-sized enterprise (SME) has gained momentum since the COVID-19 pandemic disrupted the global equilibrium in 2020. As a result of the global health crisis, many companies faced the same problems, such as lockdowns, temporary closing of non-essential businesses (Cowling et al., 2020), closed borders, and enforced social distancing. Global supply chains failed (Madhok, 2021), and the very existence of entrepreneurs and their businesses remain endangered due to the measures that were necessary to contain the virus (Kraus et al., 2020; Kuckertz et al., 2020). In these times, companies are forced to rapidly react and adapt to an ever-changing environment (Colpan, 2008; van der Vegt et al., 2015) to at least maintain their performance. Responses usually range from investment measures, such as offensive expansion into new niche markets, to more defensive cost-cutting measures, such as layoffs and investment reductions (Latham, 2009; Lopez-Cabrales & Denisi, 2021). Besides, responses often depend on the competitive advantages as well as the physical and intangible resources of companies (Ghemawat, 1986; Latham, 2009).

However, crisis research, so far, has mainly focused on business measures and physical resources needed to reduce the impact on a firm’s performance, neglecting the importance of individual actors in such times. We argue that Alvarez and Busenitz’s (2001) extension of the resource-based theory (RBT) of the firm (Barney, 1991), focusing on the individual entrepreneur, offers a suitable theoretical lens to broaden the knowledge, especially in the context of SMEs. We thus place our article in the discussion surrounding behavioral micro-foundations of strategic management (Guerras-Martín et al., 2014; Molina-Azorín, 2014), and here particularly in the field of psychological and cognitive aspects of individuals that influence firm strategy (Hodgkinson & Healey, 2011; Molina-Azorín, 2014; Roundy & Lyons, 2022). In SMEs, most strategic decisions are usually made by the leader(s), and it is widely acknowledged that this leader centrality has a direct and extreme influence on the behavior of businesses (Blackburn et al., 2013; Dyer, 1988; Hansen & Hamilton, 2011; Jennings & Beaver, 1997; Kelly et al., 2000; Schein, 1983; Zhou et al., 2017). In addition, their decisions may not only cause the loss of financial resources (in the worst case, their company may not survive), but might also lead them to lose their independence or self-confidence, increasing stress, fatigue, and fear (Doern, 2016). As such, the lack of empirical research that deals with underlying factors focusing on the role of individuals (Foo, 2011; Miocevic, 2021) and their decision-making regarding certain strategic choices is surprising. Some studies attempted to focus on psychological constructs to explain the behavior and decision-making of SME leaders (EstradaCruz et al., 2019; Simsek et al., 2010; Wang et al., 2016). Miocevic (2021) provided the first empirical evidence that positive and negative emotions within leaders shape their response intentions in a way that positive emotions significantly influence investment, while negative emotions influence divestment. In line with this, we theorize that the selection of investment versus cost-cutting measures during times of adversity is based on the psychological mindset of SME leaders (Bullough et al., 2014; Latham, 2009).

Thus, the purpose of this study is to address the following research question, “Does psychological capital of SME leaders influence both the direction of strategic response that is taken during a crisis and performance of these firms?” Scholarly research has identified the concept of Psychological Capital (PsyCap) to reflect the nature and state of psychological resources in individuals. Thus, PsyCap represents an individual’s positive mental condition (Luthans, Avolio, et al., 2007) that comprises four psychological resources of hope (Snyder et al., 1991), efficacy (Bandura, 1997), optimism (Seligman, 1998), and resilience (Masten, 2001). As the PsyCap of an individual is malleable (Luthans, Avolio, et al., 2007) and conducive to development (Dello Russo & Stoykova, 2015), it offers great potential for management research (Luthans & Youssef-Morgan, 2017). Recently, studies on entrepreneurs’ PsyCap have been conducted (Baron et al., 2016; Hmieleski et al., 2015; Jensen, 2012), showing that it reduces their perception of stress and ultimately contributes to well-being and fosters desirable outcomes (Baron et al., 2016; Jensen, 2012). To test our hypotheses, we use partial least squares structural equation modeling (PLS-SEM) on a data set of 372 SMEs.

Our research contributes to the discourse of contemporary entrepreneurship literature by first adding to the literature on micro-foundations of strategic management (Molina-Azorín, 2014), which is embedded in RBT (Foss, 2011). Here, we emphasize the RBT of the individual entrepreneur (Alvarez & Busenitz, 2001), more precisely the SME leader, by showing that positive psychological characteristics of SME leaders contribute to the strategic advantages of their businesses. On one hand, we find a direct positive link between the SME leaders’ level of PsyCap and performance of their companies during the recent COVID-19 pandemic. On the other hand, we show that the relationship between PsyCap of SME leaders and performance is mediated by the implemented strategic measures. Second, we add to the positive psychology literature by showing that the level of psychological resources influences the mix of strategic responses during a crisis. SME leaders with a higher PsyCap emphasize implementing investment measures during a crisis, whereas SME leaders with a lower PsyCap emphasize cost-cutting measures. We observe a positive relation between investment measures and performance, while cost-cutting measures impact performance negatively. Thus, by investing in improving their PsyCap, SME leaders can contribute to strengthening the sustained competitive advantage of their firms, which is not restricted by size, financial resources, or network capabilities. Our findings ultimately contribute to understanding why some companies might perform better in adverse circumstances than others.

Theoretical background and hypothesis development

A long tradition of research suggests that sustained competitive advantages are crucial for firms’ success and become even more important in crises. Embedded in RBT (Barney, 1991), it is broadly acknowledged that firms’ idiosyncratic resources establish sustained competitive advantages (Crook et al., 2008). However, SMEs face greater constraints compared to larger companies, stemming from limited access to traditional resources, such as physical, financial, and human resources (Bartz & Winkler, 2016; Fort et al., 2013; Smallbone et al., 2012). This so-called liability of smallness (Aldrich & Auster, 1986) makes gaining some advantages more difficult to almost impossible. Nonetheless, their smaller size enables them to gain other idiosyncratic resources, which can become even more important in the task of combating exogenous crises (Beliaeva et al., 2020). Due to their size, SMEs are usually more flexible, less formalized, and have flat hierarchies, which promote and enable a quick reaction to adverse events.

Besides, in entrepreneurship research, it is broadly acknowledged that strategic responses in SMEs are concentrated within their leaders, thus giving them a pivotal role and the opportunity to shape the behavior of these companies (Blackburn et al., 2013; Hansen & Hamilton, 2011; Jennings & Beaver, 1997; Kelly et al., 2000; Kotey & Meredith, 1997; Roundy & Lyons, 2022; Schein, 1983). For example, Smallbone et al. (1995) show that high growth in SMEs is more influenced by managers’ behavior than by firm characteristics such as age or size, while Wiklund and Shepherd (2003) show that the growth of small businesses is directly linked to personal growth intentions of their leaders. The idea of leader centrality within SMEs, and thus putting individuals at the core of explaining organizational behavior, goes in line with the literature on behavioral micro-foundations in strategic management (Guerras-Martín et al., 2014; Molina-Azorín, 2014; T. C. Powell et al., 2011; Roundy & Lyons, 2022). While strategic literature for a long time focused on the firm level concerning strategy, since the early 2000s scholars have started to consider the role of individuals in this regard (Felin & Foss, 2005; Molina-Azorín, 2014). Scholars in this line focus on psychology and organization behavior research aiming at developing realistic assumptions about strategy and human behavior (T. C. Powell et al., 2011) and thus explaining why and how companies differ from one another. In doing so, the research on behavioral micro-foundations in strategic management is closely tied to the RBT, as it considers internal resources and capabilities of individuals that create a unique bundle of resources with the potential of creating competitive advantages (Foss, 2011; Molina-Azorín, 2014). Consequently, it is not surprising that Alvarez and Busenitz (2001) extend the RBT by empathizing with the long-overlooked role of individual entrepreneurs as a strategic resource in entrepreneurial businesses. They show “. . . how individuals sometimes embody bundles of heterogeneous resources that allow them to repetitiously create new entrepreneurial opportunities through the firm” (Alvarez and Busenitz, 2001, p. 771).

As Hodgkinson and Healey (2011) stress, the stream of behavioral micro-foundations in strategic management has to a large extent focused on behavioral and cognitive factors, and overlooked emotional and affective factors to a large part. They argue that this contributes to a distorted picture of how individuals influence strategy within companies. While in the past years, an increase in research on the role of emotions in strategic management can be observed (Brundin et al., 2022; Daniels, 1998; Huy, 2012), we argue that research into micro-foundations of strategy needs an even broader view. In psychology, various psychological characteristics of individuals can be grouped on the so-called state-trait continuum, referring to the degree of the characteristic being subject to malleability (Luthans & Youssef, 2007; Luthans & Youssef-Morgan, 2017). On the state-trait continuum, emotions are located on the very left side of the continuum, being pure states that are temporary, changeable, and volatile. Moving to the right side of the continuum, the psychological characteristics get more permanent with state-like resources that are more stable than states but still malleable and open for development (e.g., PsyCap). Next, the trait-like characteristics are relatively stable within an individual and are not easy to change (e.g., Big Five personality traits). On the far right of the continuum are pure traits, that are not open to development as they are mainly genetically based (e.g., intelligence) (Luthans, Avolio, et al., 2007; Luthans & Youssef-Morgan, 2017). We stress that especially the research on behavioral micro-foundations for state-like characteristics is still lacking, but offers, like the research on emotions, the potential to explain the role of individuals in strategy.

Simultaneously to the increase of research into behavioral micro-foundations, scholars in RBT have started to explore new resources on the firm as well as the individual level, that have the potential for creating sustained competitive advantages. Those resources encompass social capital, technological capital, positive organizational behavior (POB), and PsyCap (Luthans & Youssef, 2004). The latter two can be considered as psychological micro-foundations influencing organizational behavior, and thus serve as a potential unique resource in the sense of RBT (Luthans & Youssef, 2004; Newman et al., 2014).

POB as a research stream focuses on “. . . the study and application of positively oriented human resource strengths and psychological capacities that can be measured, developed, and effectively managed for performance improvement” (Luthans, 2002a, p. 59) and has been used in broad management research for almost two decades (Luthans, 2002a; Newman et al., 2014). PsyCap, as a sub-research field of POB, is defined as “[. . .] an individual’s positive psychological state of development [. . .]” (Luthans, Youssef, & Avolio, 2007, p. 3) and represents a higher-order core construct of the four psychological resources of hope, (self-) efficacy, resilience, and optimism (Luthans et al., 2005; Luthans, Avolio, et al., 2007).

Hope is contextualized by a set of two cognitive factors that interact reciprocally: agency and pathways. Whereas agency represents an individual’s belief in his or her capability to initiate and control required measures to reach his or her goal, pathways reflect the capability to imagine and generate different ways to achieve them (Snyder et al., 1991, 1996) Thus, hope describes a psychological state of goal-directed willpower and the ways to reach those. In the context of organizations, individuals with a high level of hope have several work-related long- and short-term goals, which they are motivated to reach by creating different paths (Hmieleski et al., 2015).

The psychological resource of efficacy reflects the personal assessment of an individual’s capabilities and thus the confidence in their abilities (Bandura, 1982; Stajkovic & Luthans, 1998). The concept is rooted in social cognitive theory (Bandura, 1997, 2012) and reflects the degree to which a person can mobilize his or her cognitive abilities and motivation to master tasks (Bandura, 1982). This enables individuals with a high level of efficacy to pursue more ambitious goals for showing a strong reliance on their abilities than those with low efficacy (Bandura, 2012).

Resilience in a work-related context provides the ability “[. . .] to rebound, to ‘bounce back’ from adversity, uncertainty, conflict, failure or even positive change, progress and increased responsibility” (Luthans, 2002b, p. 702). Individuals with high resilience are better able to tolerate adverse circumstances and aim to resolve a situation (Luthans et al., 2006; Luthans & Youssef, 2004).

Finally, the psychological resource of optimism (Seligman, 1998) refers to people dealing with adverse situations with an optimistic mindset. Optimistic people expect favorable outcomes and in doing so face obstacles in a constructive manner (Scheier et al., 2001). This resource can, therefore, be described as “a positive explanatory style that attributes positive events to internal, permanent, and pervasive causes, and negative events to external, temporary, and situation-specific ones” (Luthans & Youssef, 2004, p. 153). Accordingly, individuals experiencing a high level of optimism seem to adapt more easily to changing environments and adverse developments (Luthans et al., 2006).

What makes PsyCap so interesting for organizational behavior research is that it represents a state-like concept, meaning that it can be cultivated even through small interventions (Dello Russo & Stoykova, 2015). This also differentiates it from concepts, such as the big five personality traits, which mostly remain stable in an individual’s lifetime, and thus are resistant to development (Luthans, Avolio, et al., 2007).

High PsyCap has been linked to several desirable work-place-related outcomes such as individual performance, attitudes, and behaviors of employees (for a comprehensive overview, see the study by Newman et al., 2014). After examining the PsyCap of employees, scholars started to investigate the construct in the context of entrepreneurs and business owners. Jensen and Luthans (2006) find that SME leaders’ PsyCap positively influences their self-assessed authentic leadership behavior, allowing them “to not only survive but thrive within a challenging and dynamic environment” (Jensen and Luthans, 2006, p. 266). Besides, Rego et al. (2019) show that leaders with a high PsyCap energized their staff members and might have positively enhanced their performance. Furthermore, Hmieleski et al. (2015) find that PsyCap of entrepreneurs seems to be of particular importance for creation contexts, which are characterized by dynamic conditions of an industry facing a high level of uncertainty, similar to crisis contexts. These scholars find a positive influence of entrepreneurs’ PsyCap on firm performance in such contexts. In line with these findings and the above discussion concerning RBT and SME research, the relevance of individual SME leaders’ PsyCap as a source of sustained competitive advantage during crises becomes evident. In our study, we follow the theoretical perspective suggested by the extension of RBT, focusing on the PsyCap of individual SME leaders in crisis contexts.

PsyCap of SME leaders and their strategic responses during crisis

An exogenous crisis poses difficult circumstances for companies, as the external context changes in the sense that companies cannot influence the changes taking place within their environment (Cowling et al., 2018; Latham, 2009). The consequences of these changes in a company’s context can throw out of balance the well-adapted and aligned value chains and cost structures (Madhok, 2021). Meanwhile, these consequences can be due to changes in a company’s business environment, customers’ needs, or even society as a whole (Colpan, 2008). Hence, for companies, crises entail an inherent compulsion to change. Complicating matters further, the unbalanced environmental context also modifies the opportunity structure available (Kuppuswamy & Villalonga, 2016). To survive in challenging circumstances, SME leaders must act and grasp the opportunities posed by changing circumstances (Grégoire et al., 2010; Kraus et al., 2020; Vaghely & Julien, 2010). In light of the ubiquitous influence of SME leaders, which means they often have to make decisions about strategic orientations very promptly when facing crises, it is essential to understand different perceptions and reactions of SME leaders in the context of crisis (Herbane, 2010; Jones & Macpherson, 2006). This decision-making process is often characterized by a lack of information, which increases uncertainty (Herbane, 2010; Vargo & Seville, 2011) and raises pressure on leaders. They not only have to deal with unexpected losses in the business dimension, which in a worst-case scenario can lead to bankruptcy, but also personal losses such as a decrease in independence, self-esteem, and private liquidity as well. However, leaders that can build on a rich resource base, also in terms of personal and psychological resources, are better able to avoid these losses (Doern, 2016).

Consequentially and in light of the RBT according to Alvarez and Busenitz (2001), we argue that an individual leader’s psychological resource base can act as a sustained competitive advantage during times of adversity. We, thus, stress that SME leaders’ mental state in times of adversity and their individual perception of crisis (Herbane, 2010) can become a crucial resource during this time, as psychological characteristics seem to influence not only the personal well-being of leaders but also their behavior, which ultimately reflects in their companies’ ability to deal with a situation (Vargo & Seville, 2011, p. 5620).

According to research, psychological factors influence the choices of individuals in various areas and thus have an impact on their decision-making and behavior (Huijts et al., 2012; McGuire, 1976; Molina-Azorín, 2014; Roundy & Lyons, 2022; Thompson, 2014). Translating this context to entrepreneurship research seems to be of particular relevance for SME leaders because their centrality influences their companies to an extraordinary extent (Zhou et al., 2017). Moreover, time pressure caused by changed environmental conditions in a crisis inevitably makes it necessary for leaders to make a decision so that their organizations’ behavior can be adapted to the changes (van der Vegt et al., 2015).

Management scholars stress the importance of a positive psychology approach to enhance our understanding of SME leaders’ responses during such times (Giones et al., 2020; James et al., 2011; Pearson & Clair, 1998). First results by Milosevic et al. (2017) underpin the importance of research in this direction: In their study, they investigated how leaders leverage their PsyCap to navigate through a crisis and analyzed Sir Winston Churchill’s behavior during World War II. They find that PsyCap in leaders represents a crucial element when leading through such times, as the composition of psychological resources “fuel activities needed to persevere and overcome a crisis” (Milosevic et al., 2017, p. 140). From this, we theorize that the decision SME leaders make about the strategic alignment of their companies in such circumstances is influenced by their level of PsyCap.

The responses considered can be divided into two options (neither of which are mutually exclusive but can be highly effective in combination): investment measures and cost-cutting measures. The first option involves making strategic adjustments during a crisis and implementing externally focused investment measures (Hofer, 1980; Latham, 2009). These measures include revenue-generating and market-oriented actions, seizing opportunities, such as an aggressive expansion into new niche markets, diversification, competitive actions, entrepreneurial actions, or improving product quality (Kottika et al., 2020; Lonial & Carter, 2015; Shen et al., 2018; Smart & Vertinsky, 1984). However, implementing such measures depends on an entrepreneur’s capacity to recognize such opportunities (Wall & Bellamy, 2019). As individual resources of entrepreneurs influence their ability to recognize opportunities (Alvarez & Busenitz, 2001), we argue that a high PsyCap, which reflects an individual’s positive psychological state, positively influences such decisions.

Smart and Vertinsky (1984) theorized that in times of crisis, even risk-takers would rather take cost-cutting measures, as uncertainty in such situations does not outweigh the benefits gained from risky choices. According to them, people high in the psychological resource of optimism engage in investment actions because they tend to see the turbulent environment as only a temporary setback, which they counteract by trying to control the situation. Adding to that, SME leaders, high in hope and optimism, prefer to implement strategic directions that foster growth (Wall & Bellamy, 2019). Kottika et al. (2020) show that in the context of a crisis, entrepreneurs with a positive mindset tend to engage in investment measures such as becoming more competitive, more customer-oriented, or adopting innovation. This indicates that entrepreneurs, who grasp opportunities, seem to have a high level of PsyCap. Given that investment measures are largely focused in an external direction, that is, involving the use of resources in an uncertain environment (Chattopadhyay et al., 2001) with no certainty of recovering the investment, we argue that a strong link between a high level of positive psychological resources and investment measures can be expected.

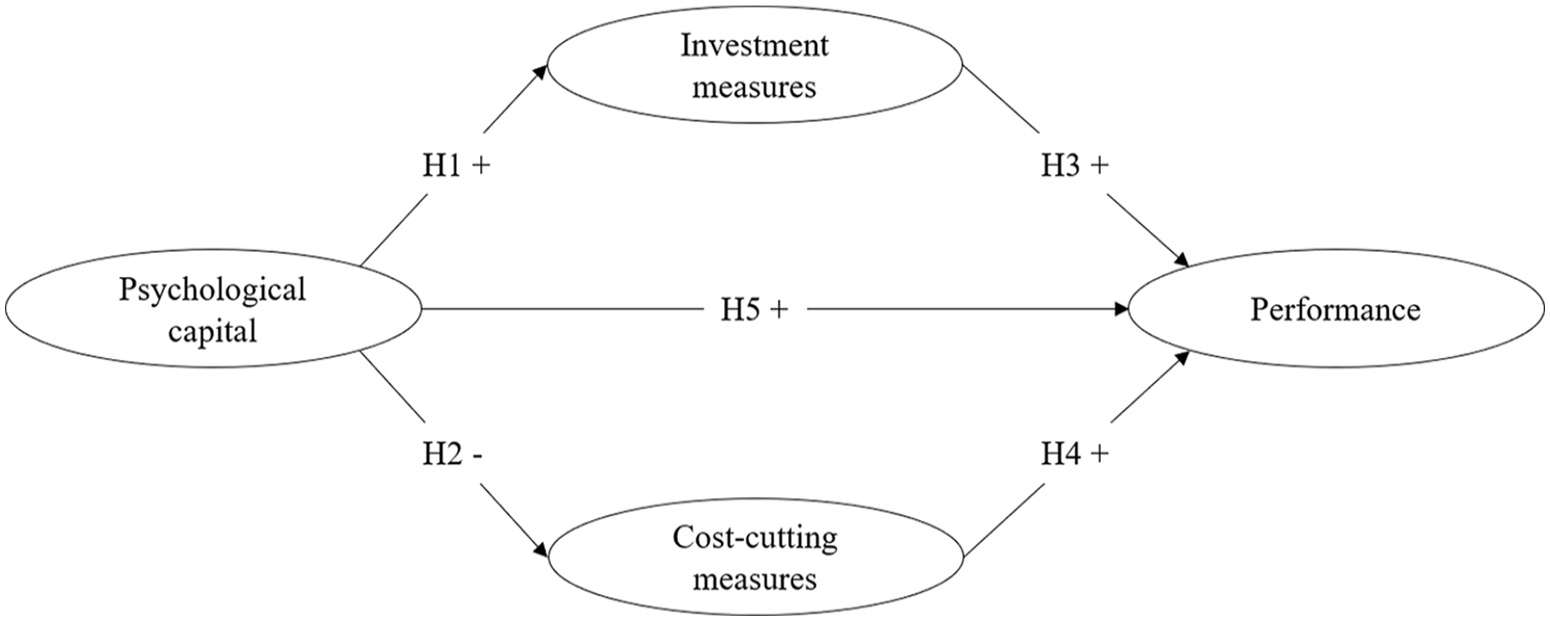

Hypothesis 1 (H1): SME leaders that exhibit a high psychological capital are likely to implement investment measures during a crisis.

The second option, contradicting the external-focused investment measures, is to implement strategic measures that are focused on internal affairs by aiming at aligning a company’s structure to its situation (Cater & Schwab, 2008; Morrow et al., 2004). Such measures are considered to be rather conservative (Chattopadhyay et al., 2001; Hofer, 1980; Latham, 2009), and they typically include retrenchment, layoffs, and cost-cutting in different areas such as marketing, purchasing, and product development (Collett et al., 2014). Usually, such measures entail less risk than investment measures, as their purpose is the realignment of a company’s structure without raising capital in any form (Morrow et al., 2004). Wall and Bellamy (2019) find that individuals who are less optimistic and less hopeful about a crisis tend to act more carefully and stay within the range of actions that are already known. In addition, less optimistic individuals are more afraid of failure in threatening situations (Engel et al., 2019), leading to more conservative responses. Thus, SME leaders who cannot draw on strong and positive psychological resources might refrain from seizing opportunities in crises and instead focus on internal affairs and adapting structures by cutting costs within an organization. In this context, Bullough et al. (2014) show that entrepreneurs with low levels of PsyCap resources of resilience and efficacy are less likely to take entrepreneurial actions. In consequence, we argue that leaders with a lower level of PsyCap resources prefer to implement cost-cutting measures.

Hypothesis 2 (H2): SME leaders that exhibit a low psychological capital are likely to implement cost-cutting measures during a crisis.

Measures to mitigate crises and their effect on performance

The survival of SMEs during adverse times is inevitably linked to their performance (Robbins & Pearce, 1992, 1993). As argued above, crises confront SMEs with the inherent need for change. Thus, SMEs and their leaders must act and seek opportunities to align with the changing environmental circumstances and maintain performance. This leaves them with uncertainty, fatigue, and stress, as they fear for their existence in terms of running out of money (Doern, 2016). Thus, they succumb to being the victim of a crisis, rather than actively engaging with an opportunity. Instead of being passive, if they are active in such situations, they will harness opportunities, which are intended to stabilize the performance (Beliaeva et al., 2020). When they start losing customers and stop being profitable, SME leaders need to find the right alignment strategy for their situations (Eggers, 2020). In doing so, they can draw on the two measures discussed above, both of which generally serve to strengthen a company’s performance.

Even in non-crisis circumstances, there is an inherent need for SMEs to harness investments, grow, expand, or simply stay competitive. If companies stop investing, they may stagnate or get outpaced by their competitors (Klein, 2008). It is evident that during a crisis the need to implement investment measures might become more important (Zúñiga-Vicente et al., 2019), as the equilibrium that usually exists within a company structure gets disrupted (Cowling et al., 2020). The circumstances of an external crisis change the business environment for companies. Consequently, established processes and cashflows of such companies may fail to generate their performance goals. Thus, SMEs must act, change, and find opportunities, which means they must invest to not succumb to being the victim of their circumstances. Research shows that SMEs are more prone to implementing investment measures in comparison to cost-cutting measures during a crisis (Shama, 1993; Smallbone et al., 2012). This draws from the fact that smaller companies exhibit special characteristics, such as low formalization, less bureaucracy, as well as informal knowledge transfer (Schulze et al., 2001; Sirmon & Hitt, 2003; Zahra, 2012). Therefore, they can react in a more flexible and fast way to the changing market demands and seize opportunities. By implementing investment measures, they can boost their performance during adverse times (Bartz & Winkler, 2016; Beliaeva et al., 2020; Lonial & Carter, 2015; Shen et al., 2018; Smallbone et al., 2012). Hence, we propose that flexibility and the concentrated decision-making power of SMEs help to adapt faster throughout a crisis and grasp business opportunities by investing, which ultimately improves their performance (Zhou et al., 2017).

Hypothesis 3 (H3): SME leaders that implement investment measures during crisis exhibit higher performance in their companies.

Another feasible step to take during a crisis is to realign a company’s internal affairs to changing circumstances by trying to reduce the use of resources (Cater & Schwab, 2008). SMEs use such cost-cutting measures as well (Chu & Siu, 2001; Collett et al., 2014; DeDee & Vorbies, 1998). When a company implements “rightsizing” or cost-cutting approach (Hitt et al., 1994), it does not imply that it is less efficient than companies that take investment measures—retrenchment can stabilize a company’s financial situation especially when an industry is declining (Morrow et al., 2004).

Usually, companies implement cost-cutting measures to increase their efficiency, productivity, and competitiveness, or aim for strategic realignment (Hitt et al., 1994). Considering the broad literature about downsizing, we find that implementing cost-cutting measures does not always have a positive effect on the company’s performance (Cascio & Young, 2003; Guthrie & Datta, 2008) or results seem to be mixed (Cascio et al., 1997; De Meuse et al., 1994; Sheaffer et al., 2009). However looking at the samples, the context, and the way that the downsizing activities were measured, we find that most of the studies take place in large publicly held companies, during stable times (i.e., not in times of economic crises) and the downsizing is mostly measured by the change in employee numbers between 2 years (Cascio et al., 1997; Cascio & Young, 2003; Guthrie & Datta, 2008; Sheaffer et al., 2009). Especially the latter is to be seen as problematic, as this measure does not include an indication of whether the employee changes were on a voluntary level (i.e., employees choose to go, due to personal reasons) or if they were forced by the management (Cascio & Young, 2003). Besides this, in relatively stable economic contexts as well as in publicly held companies, the reasons for deciding to implement cost-cutting measures differ severely than in the context of our study. As our study focuses on a global crisis and SMEs, we argue that our study needs a narrower focus on the special context we are surveying.

If the motivation for implementing cost-cutting measures stems from a crisis, companies usually aim to “right-size” in such a way that their performance at least resembles that of the pre-crisis period (DeDee & Vorbies, 1998; Hofer, 1980). However, it must be noted that not every SME is suited for implementing cost-cutting measures in the same way, as size does play a significant role in this regard. The smaller a company, the lesser its scope to cut costs without affecting its business activity in a manner that negatively impacts its performance (Chu & Siu, 2001; Fisher et al., 2004). In non-crisis situations, the internal processes of an SME are usually adjusted in a manner that there is a balance between cost structures, business activities, and performance. However, as a result of a crisis, SMEs are forced into a situation where this balance can no longer be maintained (Cowling et al., 2020; Hofer, 1980), as the changed environmental conditions lead, for example, to customers leaving a company or to significantly lower demand. This affects the revenue of a company, while its cost remains the same (Eggers, 2020).

However, by implementing cost-cutting measures, companies aim to rationalize business activities and cost structures, which can have a positive effect on their financial performance (Hofer & Schendel, 1978; Robbins & Pearce, 1992). Activities that do not correspond to this core focus are discontinued to save unnecessary costs. Consequently, the objective of such cost-cutting measures is to increase the efficiency of an organization, thereby maintaining or increasing its performance (Hofer, 1980). Therefore, we propose the following hypothesis.

Hypothesis 4 (H4): SME leaders that implement cost-cutting measures during a crisis exhibit higher performance in their companies.

PsyCap of SME leaders and the performance of their companies

The entrepreneurship literature assumes that the characteristics, behaviors, and actions of entrepreneurs are a reflection of their firm’s performance (Covin & Slevin, 1991; Hmieleski et al., 2015). This assumption follows the logic of Alvarez and Busenitz (2001), who postulate based on RBT that an entrepreneur represents a strategic competitive advantage. The sum of entrepreneurs’ characteristics and behaviors can, therefore, have a direct or indirect influence on the performance of their companies (Hambrick, 2007). In SMEs, leaders are inseparably intermingled with their companies and thus perform a crucial role. For example, we know that entrepreneurs influence their companies’ culture (Schein, 1983). In addition, their characteristics and motivations have been proven to influence the growth of their companies (Baum et al., 2001).

Given that the literature refers to PsyCap as a sustained competitive advantage (Luthans & Youssef, 2004; Toor & Ofori, 2010), we will follow this reasoning. According to Barney (1991), sustained competitive advantages can be acquired when firms exploit their internal idiosyncratic strengths as a means to respond to environmental opportunities. For a resource to act as a sustained competitive advantage, it needs to fulfill four criteria, namely, it must be valuable, imperfectly imitable, rare, and non-substitutional.

PsyCap is valuable due to the following reasons. It has already been connected to firm performance on multiple occasions. According to Grözinger et al. (2022) organizational PsyCap (OPC), which is a higher-level construct of individual PsyCap, does show a positive and significant influence on firm performance. The individual PsyCap of entrepreneurs has been connected to enterprise performance by Gao et al. (2020). Results show that all dimensions of the individual PsyCap are positively correlated to performance. However, Barney (1991) also states that context matters and resources are not valuable in general. Thus, the question remains if individual PsyCap is valuable within a crisis context. Here it is noteworthy, also shown by Grözinger et al. (2022), that OPC fosters creative innovation during times of crisis, which is an essential part to overcome such situations. Furthermore, Luthans et al. (2010) presented first evidence, that PsyCap helps individuals’ problem-solving abilities, which is essential in crises. As such, we argue that PsyCap is valuable in times of crisis according to Barney’s (1991) definition. PsyCap is also imperfectly imitable. The composition of PsyCap resources within an individual is unique to the person in question, as it emerges from a complex interaction of a sum of influences, like their social environment, experiences, and psychological processes (Luthans & Youssef, 2004). Thus, it meets Barney’s (1991) proposed conditions for a resource being imperfectly imitable. As PsyCap of an individual not only consists of a mix of four different psychological characteristics (Luthans, Youssef, et al., 2007) but also develops through a mix of different factors, it can be considered a rare resource according to Barney’s (1991) reasoning. Besides, PsyCap also meets the criterion of being non-substitutable, as the four psychological resources which form PsyCap are unique psychological characteristics of human beings (Bandura, 1997; Masten, 2001; Seligman, 1998; Snyder et al., 1991).

A high PsyCap of a person indicates that this individual is functioning optimally (Luthans, Youssef, & Avolio, 2007), which influences personal performance (Avey et al., 2010, 2011; Luthans, Avey, et al., 2008; Luthans, Avolio, et al., 2007; Luthans et al., 2010, 2005; Luthans, Norman, et al., 2008; Peterson et al., 2011). Exemplary empirical studies find a positive relationship between PsyCap of employees and factors, such as their individual job-level performance (Luthans, Avolio, et al., 2007), manager/supervisor-rated performance (Avey et al., 2010; Peterson et al., 2011), and creative performance (Rego et al., 2012).

Combining the perspectives that PsyCap can be a sustained competitive advantage for companies and the significant influence that SME leaders have on their companies, it is reasonable to assume that the PsyCap of SME leaders has a direct influence on the performance of their companies in a crisis. First results in this context were provided by Hmieleski et al. (2015). Building on the notion of creation versus discovery contexts, these scholars show that higher PsyCap of entrepreneurs positively influences performance in the creation context. Such contexts are characterized by dynamic conditions and a high level of uncertainty, like crisis contexts. This suggests that the PsyCap of entrepreneurs is especially valuable in uncertain and dynamic environments to facilitate performance in difficult times. Thus, we argue that if SME leaders can utilize a high PsyCap in crisis by increasing their individual performance, it will positively influence the performance of their companies.

Hypothesis 5 (H5): The greater the PsyCap of an SME leader, the better the firm’s performance during a crisis.

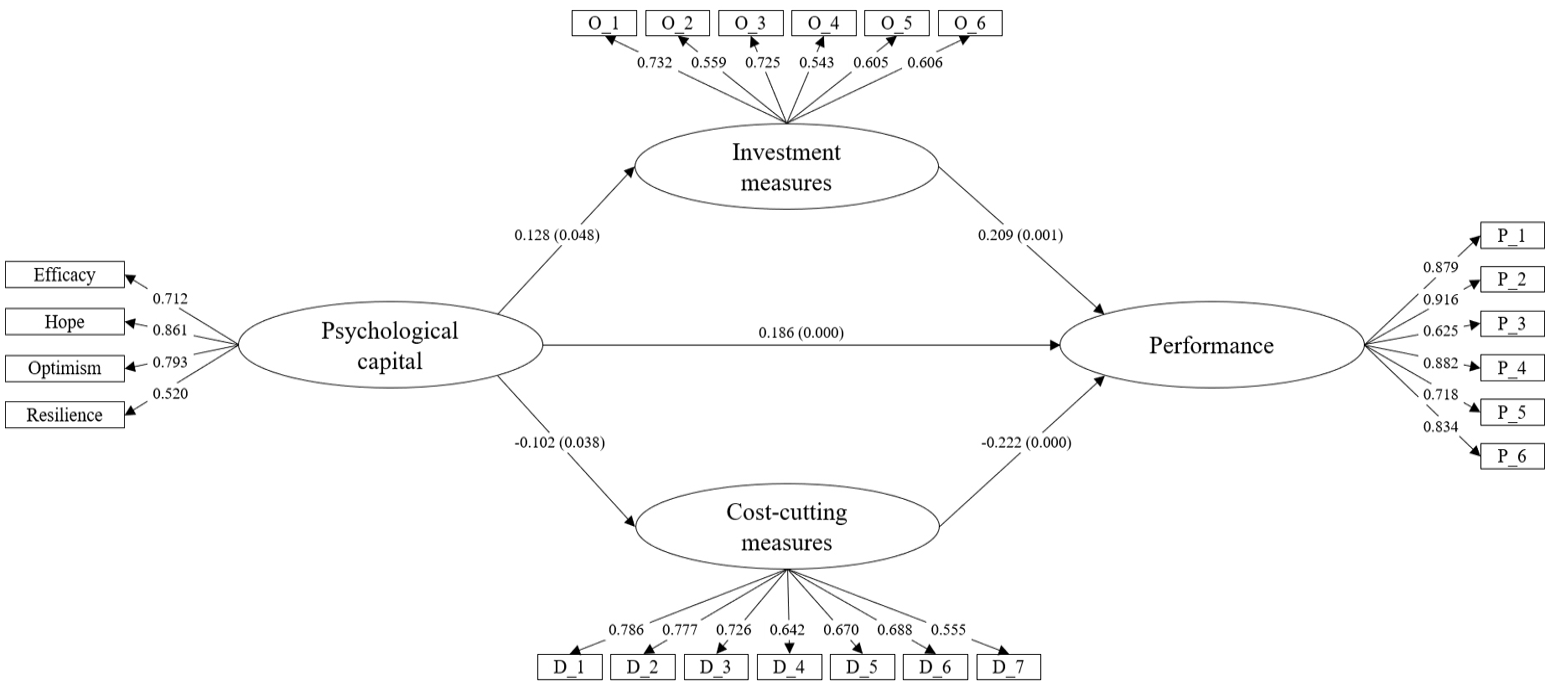

Figure 1 shows an overview of all hypotheses and their presumed relationships.

Hypotheses.

Method

Data set and sample of study

In July 2020, we conducted an online survey to test our hypothesis. We decided to focus only on one country, as various countries were affected differently by the COVID-19 crisis. We decided to choose Germany due to its important economic role and the nationwide equal political countermeasures against the crisis in the months studied. We sent e-mail invitations for participation in our study to 20,000 companies overall, which we extracted from the Amadeus database (Buerau van Dijk, 2020). The questionnaire was addressed to managers and owners of the companies. First, they were addressed as such in the cover letter, and later they were questioned about several aspects, including their position in the companies. The questionnaire was started by 1,501 people. Of them, 696 people completed it. Based on the completed questionnaires, the response rate was 3.48%. To consistently perform our analyses with the same number of cases, we used a filter that excluded all cases from our final sample where filled questionnaires had missing data or where the questionnaire was not filled out by the owner or manager of a company. To only include SMEs, we excluded firms with more than 249 employees (European Commission, 2003). This resulted in a final sample of 372 owners or managers, of which 231 are both owners and managers.

Our analysis included a test for non-response bias. Consequently, we performed an analysis to determine if the responses of the first respondents differed from those of the last respondents. As a result, we split the data set into three sections according to the response time and compared the three categories. We observed no statistically significant differences regarding our explanatory variables (Armstrong & Overton, 1977; Chrisman et al., 2004; Dehlen et al., 2014).

To confirm the representativeness of our sample, we first compared respondents to the original draw to which we sent the survey. For this, we only used firms with fewer than 250 employees in both data sets and compared the distribution of the number of employees and the industries. No significant differences were found between the data sets regarding the number of employees. Regarding the distribution of industries, the mean value for the service industry also did not differ significantly between the two samples. However, the mean values for manufacturing and other industries differ significantly. The effect size of these differences can be classified as small, with values below 0.2 (Cohen, 1988). In detail, the respondents assigned themselves somewhat more to the other industry (+4.0%) and somewhat less to the manufacturing industry (–3.7%). This may also be the case, because the assignment is not always easy for the respondents, as their companies are often active in several industries at the same time, or the assignment can be very complex. We also compared our data set with descriptive data from other published articles about surveys of SMEs in Germany. Regarding the age of the respondents, comparable values can be found in previous studies (49.4 years in our study compared to 45 years in the study by Dehlen et al. (2014) and 51.6 years in the study by Zellweger et al. (2012)).

Counteracting any potential common method bias, we took several preventive measures (Fuller et al., 2016). First, we assured all participants anonymity and scientific integrity to obtain honest answers and counteract a possible influence through effects such as social desirability (Podsakoff et al., 2003). Furthermore, we phrased the questions in a manner that did not allow conclusions to be drawn about the researchers’ expectations. In addition, the question sequences were randomized for the participants (Podsakoff et al., 2003).

Variables

We use a respondent’s self-assessment of a firm’s performance. Prior research shows that this approximation can be used as an equivalent substitute for measuring performance, as self-assessment is substantially akin to performance measurement via key figures (Dess & Robinson, 1984; Eddleston et al., 2007; Love et al., 2002). Purposefully, we asked respondents in our survey to assess the performance of their companies in six areas compared to their competitors since the beginning of the COVID-19 crisis in January 2020. We employed a 5-point Likert-type scale ranging from “much worse = 1” to “much better = 5” for the measurement. Concerning the six areas, we asked for information on (1) sales, (2) revenue, (3) number of employees, (4) net profit margin, (5) market share, and (6) cash flow. These parameters were used for measuring performance in several studies and thus provided a reliable foundation for our analysis (Eddleston et al., 2007; Naldi et al., 2007; Smolka et al., 2016; Wiklund & Shepherd, 2003, 2005).

We measured PsyCap with the validated self-form of the Psychological Capital Questionnaire (PCQ) by Luthans, Youssef, & Avolio (2007). 1 As we collected our data in Germany, we translated the instrument into German with the special permission of the publisher. We used the original questions for translation to German and validated the correctness of the translation by a bilingual native speaker. The questionnaire consisted of 24 questions representing the four dimensions of hope, efficacy, resilience, and optimism, as described by Luthans, Youssef, & Avolio (2007). We, therefore, asked the respondents to assess how much they agree with a statement about their behavior and thinking in a special situation. For this purpose, we used a 6-point Likert-type scale 2 as proposed by the original authors, ranging from “strongly disagree = 1” to “strongly agree = 6.” We then calculated the respective answers to a mean value for the respective dimension. The computed values were used as indicator variables for the PsyCap construct. Cronbach’s alpha for the dimensions of hope, efficacy, resilience, and optimism varied between 0.701 and 0.862.

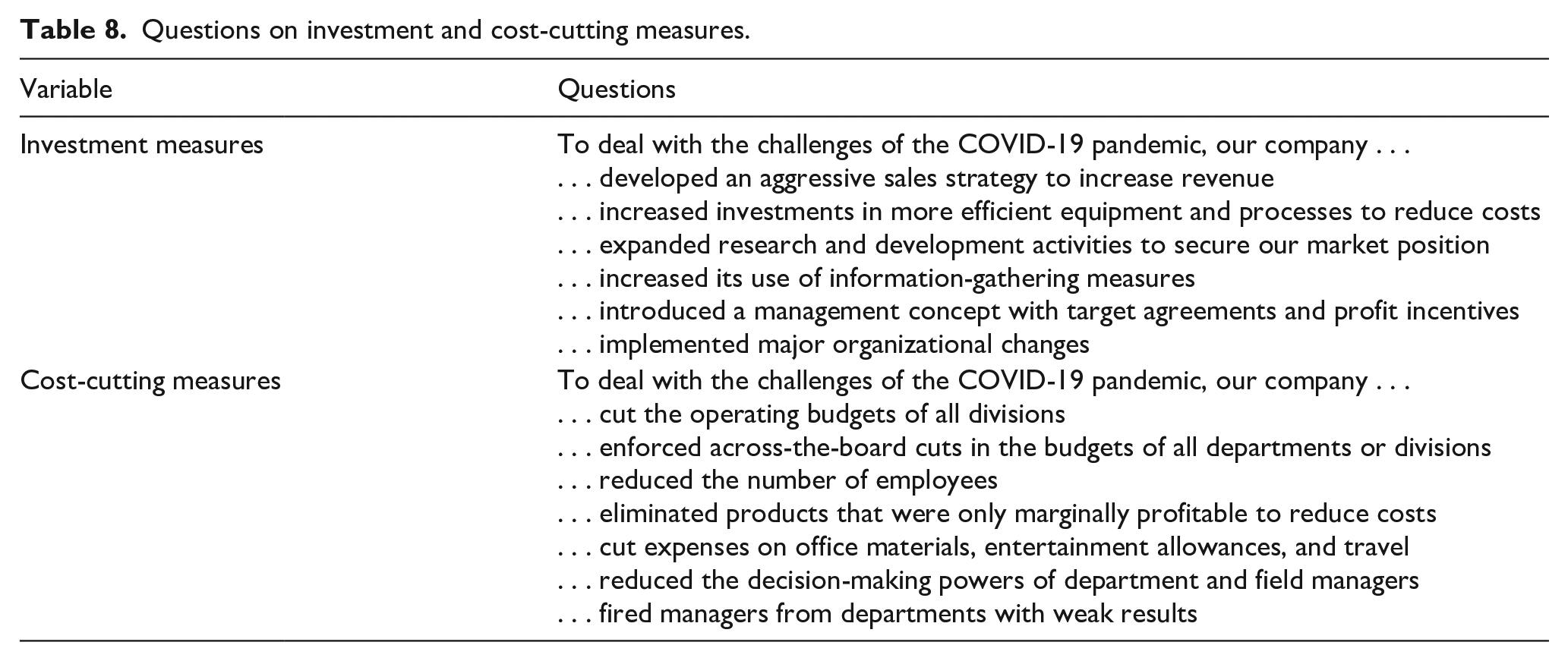

As additional latent variables in our model, we used investment and cost-cutting measures taken by the surveyed companies during a crisis. The set of potential options for strategic responses went back to the suggestions of Smart and Vertinsky (1984), an exemplary study that examined how strategic measures in a crisis are related to the environment of a company. We adapted the questions to the COVID-19 circumstances by introducing questions as follows: “To deal with the challenges of the COVID-19 crisis, our company has . . . ” The respondents, then, had to rate a statement on their company’s strategy during the crisis on a 5-point Likert-type scale ranging from “strongly disagree = 1” to “strongly agree = 5.” Finally, based on our literature analysis, we sorted the questions according to cost-cutting and investment measures and checked this classification by factor analysis. The investment measure consisted of: (1) aggressive marketing strategy, (2) investments in more efficient plants and processes increased, (3) research and development activities expanded, (4) information acquisition intensified, (5) management approach with target agreements and profit incentives introduced, and (6) major organizational changes. The cost-cutting measures included (1) cutting back the operating budgets of all divisions; (2) across-the-board cuts in the operating budgets of all divisions or departments; (3) staff reduced; (4) products that are only marginally profitable eliminated; (5) cut back expenses for office materials, entertainment allowances, and travel; (6) authority of field managers and department heads reduced; and (7) managers whose divisions have poor performance fired (Smart and Vertinsky, 1984).

Control variables 3

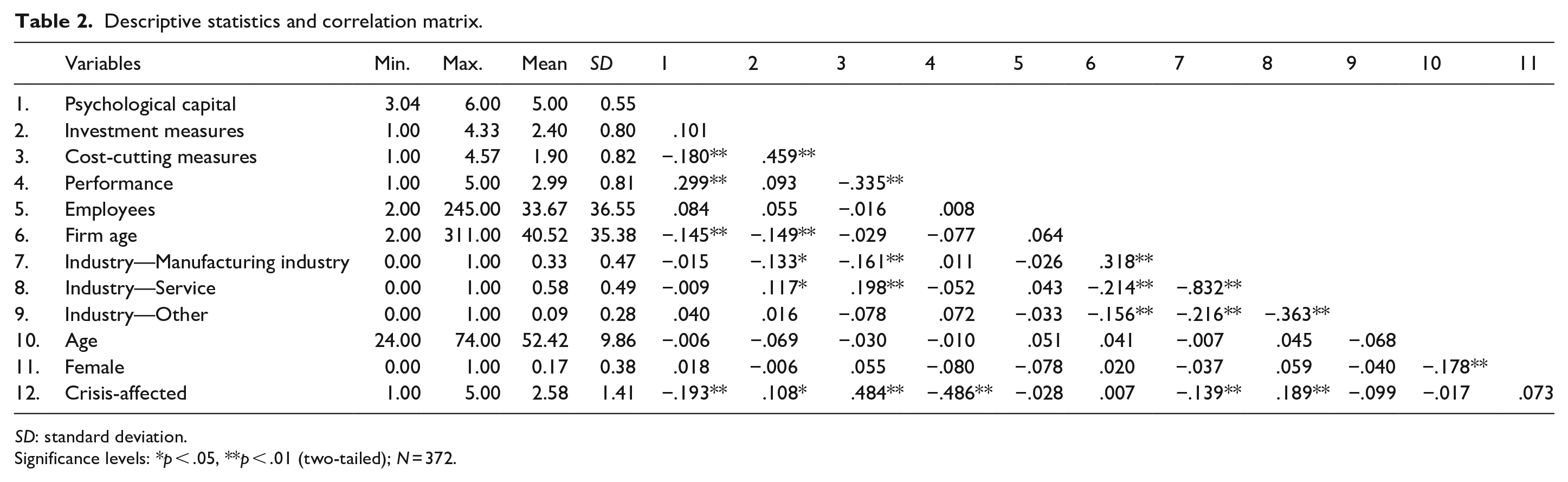

In our analysis, we included several control variables, which have been established in the literature, to influence firm performance. We used the number of employees as an indicator of firm size, which has a significant impact on the performance of companies (Smolka et al., 2016). By including the age of the firm, we controlled for the possible effects of experiences with previous crises, on the choice of measures used and performance during the COVID-19 crisis (Smolka et al., 2016). To control for industry influences (Chrisman et al., 2004), we surveyed the aggregated 10 categories version of the top-level industry allocation according to the statistical classification of economic activities in the European Union (Eurostat, 2008). For our analysis, we further aggregated these 10 categories and added dummy variables for major economic sectors, including the manufacturing industry, service sector, and a miscellaneous sector called “other.” We also analyzed the basic features of the respondents and used their age and gender in our analysis. Gender was added as a dummy variable called female. Finally, we examined the extent to which companies were affected by the crisis, as the crisis-affectedness should force companies to take strategic measures. Therefore, respondents had to rate the statement that the “company is severely affected by the COVID-19 crisis” on a 5-point Likert-type scale ranging from “strongly disagree = 1” to “strongly agree = 5.” Table 1 shows an overview of all variables, while Table 2 provides the descriptive statistics and correlation matrix.

Variable description.

COVID: coronavirus disease.

Descriptive statistics and correlation matrix.

SD: standard deviation.

Significance levels: *p < .05, **p < .01 (two-tailed); N = 372.

Data analysis

We decided to use SEM as it allows us to examine multiple causal relationships between latent variables simultaneously (Astrachan et al., 2014; Williams et al., 2009). Moreover, it allows us to consider multilevel relationships as well as relationships between dependent variables (Astrachan et al., 2014; Shook et al., 2004). We specifically chose the PLS-SEM method because it is the appropriate methodology for our model, which is relatively complex due to a large number of constructs, variables, and relationships. Our latent variables are not normally distributed and the sample size of 372 cases is not particularly large (Hair et al., 2019). We utilized the software SmartPLS 3.3.3 for our analyses with the calculation settings recommended by Hair et al. (2017). We used the path-weighting scheme with the standard start weights, a stop criterion at 10-7 as well as a maximum number of 300 iterations for the standard PLS-SEM algorithm. For bootstrapping, we calculated 5,000 subsamples with the full bootstrapping option, bias-corrected and accelerated (BCa) bootstrapping, and used a two-sided significance test with a significance level of 0.05.

We controlled for potential endogeneity issues by following the recommendations of Hult et al. (2018) and tested for potential endogeneity using the Gaussian Copula Approach. We checked that our variables, which potentially exhibited endogeneity, were non-normally distributed by running the Kolmogorov–Smirnov test with Lilliefors correction, which is the condition for the Gaussian Copula Approach (Hult et al., 2018). The results of the Gaussian Copula Endogeneity Assessment show that none of the Gaussian copulas in the models were significant, which proves that there was no endogeneity issue.

Results

Table 2 provides the descriptive statistics and correlation matrix.

Outer model reflective measurements

The reflective measurement constructs in our model are represented in Tables 3 and 4. All used constructs (i.e., latent variables) are reflective ones, for which we selected mode A in Smart PLS to determine the construct values, following the recommendations of Hair et al. (2017) for the PLS algorithm. This mode used the covariance between indicators and the latent variable to determine construct values. Nevertheless, to prove our results, we also performed our calculations with sum values for latent variables (i.e., identical weights for all indicators) and obtained comparable results. We followed the structured approach proposed by Hair et al. (2019), checking for Cronbach’s alpha, average variances extracted (AVE), and composite reliability. All reported measurements are well within the recommended borders, except for the AVE of investment and cost-cutting measures. However, the AVE is acceptable in this case, as the composite reliability and Cronbach’s alpha for all constructs are significantly high, and thus the convergent validity of the constructs is acceptable (Fornell & Larcker, 1981; Hair et al., 2017).

Cronbach’s alpha, composite reliability, and average variances extracted for reflective measurement models.

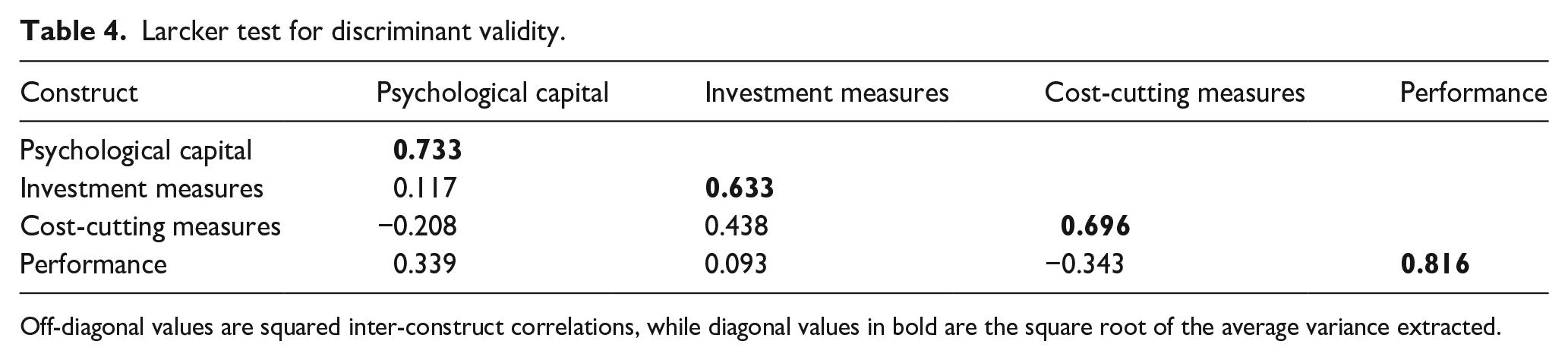

Larcker test for discriminant validity.

Off-diagonal values are squared inter-construct correlations, while diagonal values in bold are the square root of the average variance extracted.

To test for discriminant validity, we verified that all cross-loadings were smaller than indicator loads, which serves as a confirmation of discriminant validity for our model. In addition, we used the Fornell–Larcker criterion, which is fulfilled as shown in Table 4 (Fornell & Larcker, 1981).

Hypotheses testing

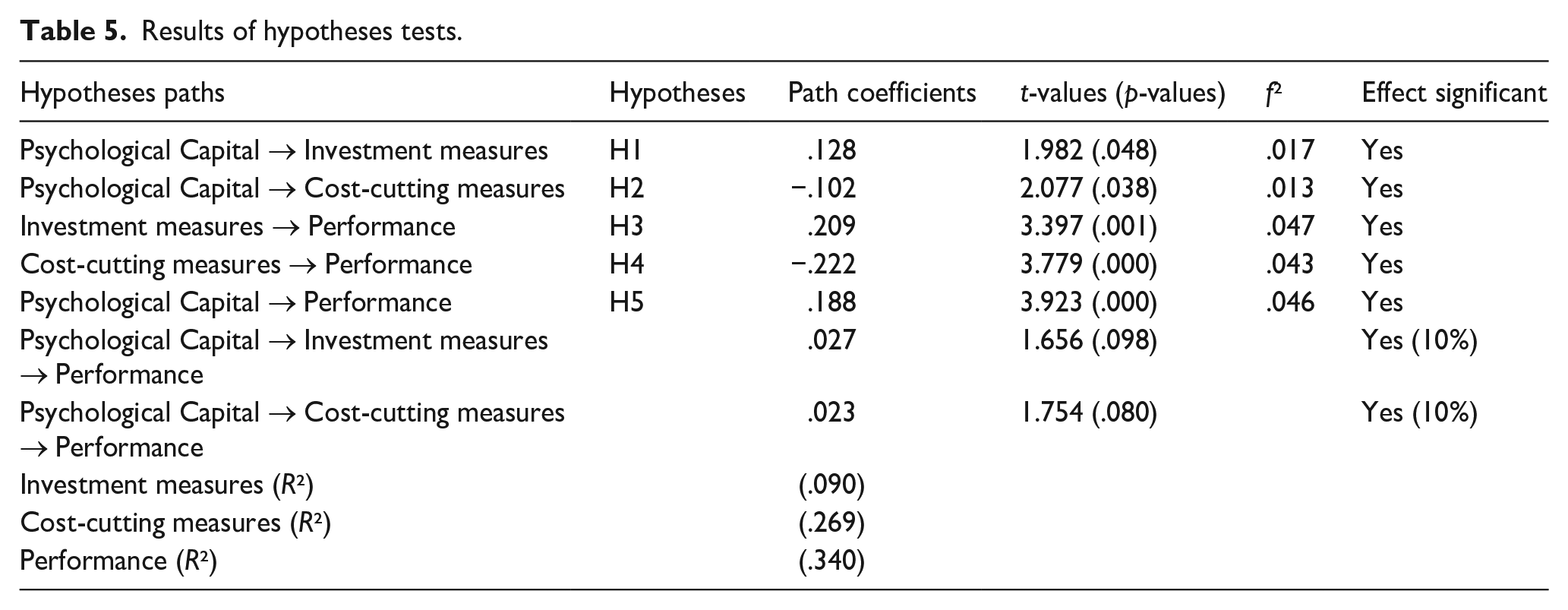

Figure 2 shows our model, the results, path coefficients, and p-values. Table 5 gives a more in-depth overview, also displaying the t-values, f², and q2 effect size.

Partial least squares structural equation model (PLS-SEM).

Results of hypotheses tests.

Reviewing our hypotheses for the influence of PsyCap on the usage of investment measures, we observe a positive effect (.128, p < .048), confirming Hypothesis 1. The assumed negative effect of PsyCap on the usage of cost-cutting measures (–.102, p < .038) is also supported and Hypothesis 2 is confirmed. The presumed positive effect of the application of investment measures on performance (.209, p < .001) can be confirmed, and thus Hypothesis 3 is accepted. In contrast, we observe a significant negative effect of the application of cost-cutting measures on performance (–.222, p < .000), and therefore Hypothesis 4 is rejected. Furthermore, a direct positive effect of PsyCap on the performance of the company (.186, p < .000) is identified, which confirms Hypothesis 5. The model also provides the opportunity to look at the indirect effects of PsyCap on performance across the mediators. The influence of the PsyCap via the mediator investment measures on performance (.027 p < .098) and the influence of the PsyCap via the mediator cost-cutting measures on performance (.023 p < .080) can be observed. A significant influence of the control variables can be largely excluded. Firm’s age has a negative influence on the use of investment measures (–.146, p < .05). In the analysis, we also included how much the respective companies are affected by the crisis. As expected, the crisis-affectedness shows a strong negative impact on the performance in the crisis (–.366, p < .000). At the same time, the higher the degree of affectedness by the crisis, the more investment (.151, p < .05) and cost-cutting measures (.452, p < .000) are pursued, whereby the influence of the degree of affectedness by the crisis on cost-cutting measures is significantly stronger.

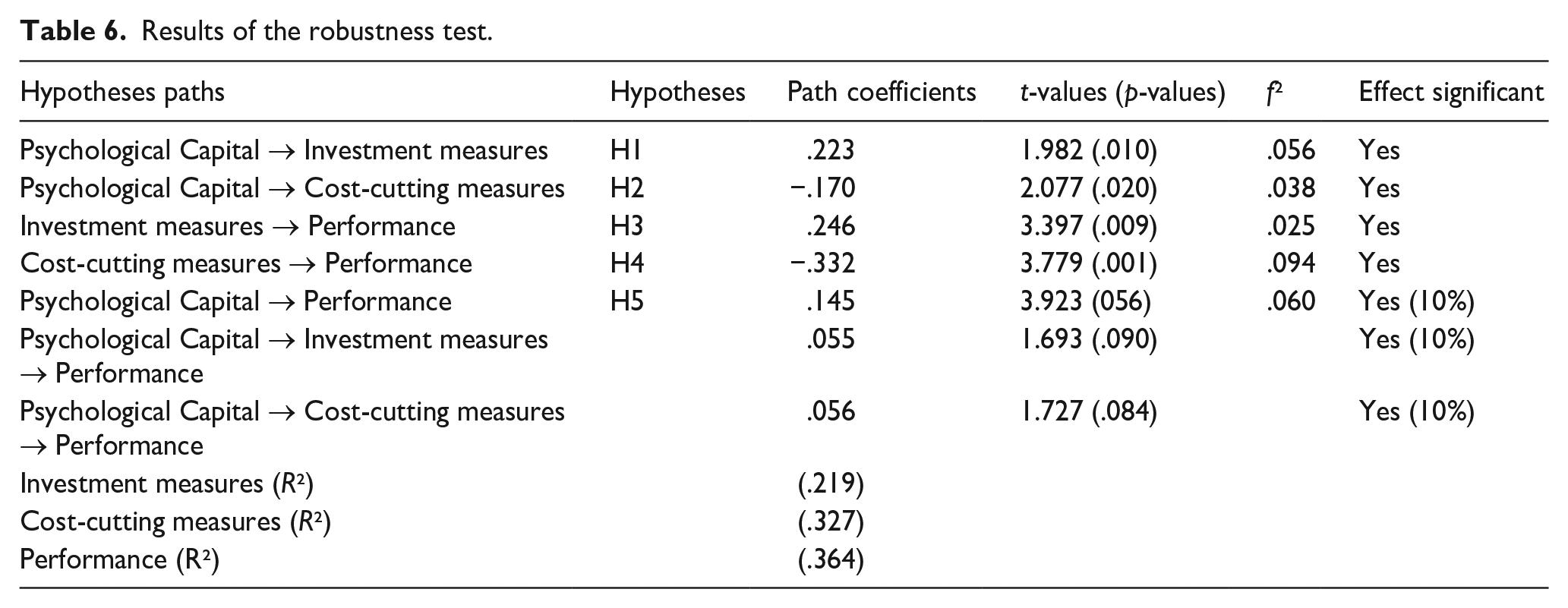

Robustness test

To prove the robustness of our results, we performed the analysis again with a subsample that included only companies with fewer than 50 employees and where the respondents are both managers and owners of the company (N = 127). As shown in Table 6, the obtained results and effects are comparable in their direction, size, and significance. Only the direct effect of PsyCap on performance is slightly below the 5% level of significance for this subsample.

Results of the robustness test.

Discussion

Crises pose a tremendous threat to the survivability of companies (Kuckertz et al., 2020). In crises, executives must make quick decisions, often under great uncertainty, and implement strategic measures, which entail different effects on a company’s performance (Latham, 2009; Petzold et al., 2019; Smart & Vertinsky, 1984). Based on the RBT of the individual entrepreneur (Alvarez & Busenitz, 2001), and in light of research on behavioral micro-foundations in strategy (Guerras-Martín et al., 2014), we argue that especially in SMEs, executives perform a central role that influences strategic responses and success of companies (Blackburn et al., 2013; Hansen & Hamilton, 2011; Jennings & Beaver, 1997). So far, we do not know much about which factors influence the choice of strategic responses taken by those executives in such periods (Herbane, 2010; Trahms et al., 2013). However, research suggests that psychological factors and, in the context of our study, positive psychological factors, may play a crucial role (Miocevic, 2021; E. E. Powell & Baker, 2014; Simsek et al., 2010) in providing a strategic advantage for firms. This idea is in line with the research on behavioral micro-foundations in strategic management, which aims at understanding how psychological and cognitive aspects within individuals influence strategy in companies (T. C. Powell et al., 2011). Thus, the goal of this study is to investigate how PsyCap of SME leaders affects the mix of strategic responses taken by their companies during a crisis.

In our analysis, we find partial support for our assumptions, as four of our hypotheses (H1, H2, H3, and H5) are accepted, but H4 is rejected. Thus, we contribute to the contemporary literature on behavioral micro-foundations in strategy as well as entrepreneurship literature in general as we show that SME leaders’ PsyCap influences strategic decision-making of their companies during a crisis, thus acting as a sustained competitive advantage in this circumstance. PsyCap of SME leaders, which represents their positive psychological state and consists of the four psychological resources of hope, efficacy, resilience, and optimism, was shown to be related to several desirable outcome variables (Baron et al., 2016; Jensen & Luthans, 2006; Rego et al., 2019). With our study, we contribute to the positive psychology literature by showing that PsyCap partly predicts the strategic orientation chosen by SME leaders to cushion the effects of crises within their companies. Furthermore, our study provides a deeper understanding of how psychological differences within individual SME leaders affect strategic decisions during a time of distress. By providing these results, we introduce state-like psychological resources (Luthans & Youssef, 2007; Luthans, Youssef, et al., 2007) to the debate in strategy research on behavioral micro-foundations (Guerras-Martín et al., 2014; Molina-Azorín, 2014).

PsyCap has a significant and positive relationship with investment measures (H1), meaning that SME leaders who exhibit a high PsyCap are more likely to deploy investment measures and less likely to implement cost-cutting measures. In addition, with H2, we display a significant negative relationship between PsyCap and cost-cutting measures, which shows that SME leaders exhibiting a low level of PsyCap tend to implement more cost-cutting measures and are less likely to implement investment measures. With these results, we follow the call of Herbane (2010) in understanding how different perceptions of SME leaders during crises translate into behavior. In the COVID-19 context, positive and negative emotions significantly influence SME leaders’ decisions regarding investment and divestment, respectively (Miocevic, 2021). We broaden this understanding by showing that SME leaders with a high PsyCap tend to implement more investment measures and fewer cost-cutting measures (H1). These results can be explained in such a way that individuals high in psychological resources might frame a crisis in a more positive light by thinking of it as a temporary state (Smart & Vertinsky, 1984), which holds opportunities for growth (Kottika et al., 2020). We show that the individual resources of entrepreneurs influence their opportunity recognition (Alvarez & Busenitz, 2001), and therefore SME leaders with a high PsyCap tend to prioritize seizing those opportunities by investing. In contrast, we show that SME leaders exhibiting a lower level of PsyCap might perceive a crisis as threatening to the survival of their companies and act more carefully by focusing on defensive cost-cutting measures (Wall & Bellamy, 2019) rather than investment measures (H2). Furthermore, we add to the results of Milosevic et al. (2017), which show that leaders leverage their PsyCap to navigate through crises. We support this notion by delivering evidence that PsyCap of SME leaders especially matters in contexts of crisis, giving a more nuanced understanding of underlying psychological resources that influence strategic responses of SMEs during a crisis. While we find evidence for those significant relationships, the results should not be interpreted in the sense that high-level PsyCap leaders only take investment measures and low-level PsyCap leaders only take cost-cutting measures. The interpretation must be nuanced here, as we explain which measure choice is more pronounced in which group of SME leaders.

As the environment of SMEs changes due to major exogenous crises, their opportunity structure changes. During a crisis, one of their major concerns is to maintain or improve performance, as it is inevitably linked to survival (Robbins & Pearce, 1993). To do so, SMEs must recognize new opportunities posed by circumstances and act on them to stay vital. While SMEs face size-related obstacles when choosing a strategic orientation, during crises, they should take advantage of low levels of formalization and bureaucracy as well as informal knowledge transfer (Schulze et al., 2001; Sirmon & Hitt, 2003; Zahra, 2012). This gives them the ability to quickly adjust to changing circumstances (Bartz & Winkler, 2016; Beliaeva et al., 2020) and seize opportunities by investing (Shama, 1993; Smallbone et al., 2012). We show that investment measures have a significant, positively correlated relationship with performance during a crisis (H3).

Another strategy usually adopted by SMEs to maintain their performance during a crisis is “rightsizing” their internal affairs by implementing cost-cutting measures (Hitt et al., 1994). While the broad literature on cost-cutting measures shows mixed results regarding the implementation of such measures and the performance of the companies (Cascio et al., 1997; Cascio & Young, 2003; De Meuse et al., 1994; Guthrie & Datta, 2008; Sheaffer et al., 2009), these studies do not apply to the context of our study. The broad literature usually studies the impact of cost-cutting measures on performance in stable economic conditions, as well as in big publicly traded companies. As our study focused on a global heath-crisis context and SMEs, studies in this regard imply that cost-cutting measures can improve the performance of SMEs during crises (Chu & Siu, 2001; Collett et al., 2014; DeDee & Vorbies, 1998). However, we find that cost-cutting measures show a negative relationship with performance of SMEs (H4).

The reasons for our findings can be manifold. As early research shows, some companies might not meet their intended goals concerning cost-cutting measures, especially if they are implemented as a reaction to a threat (Hitt et al., 2004). Besides, Robbins and Pearce (1992) described two phases when implementing cost-cutting measures—the actual phase of cutting costs is followed by a recovery stage. Thus, it might be that the companies in our sample were still in the first phase of the process and the time delay effect, which reflects in performance recovery, had perhaps not kicked in yet. Another reason could be that the companies in our sample might not have the latitude to “right-size” in a manner that positive effects of cost-cutting measures can be achieved (Chu & Siu, 2001). However, with our findings, we address considerable ambiguity stemming from the fragmented research on the diverse reactions of SMEs during times of adversity, showing that from a performance perspective, investment measures represent the better option to face a global crisis.

We also find evidence that PsyCap can be used as a resource to overcome difficult times, as a high PsyCap of SME leaders is conducive to better performance (H5). We, thus, highlight the role of an individual SME leader’s psychological resources as a source of sustained competitive advantage by contributing a new perspective to the RBT of the individual entrepreneur (Alvarez & Busenitz, 2001). Our findings are in line with the results of Hmieleski et al. (2015), who show that high PsyCap of entrepreneurs matters, especially in a creation context that is marked by conditions of uncertainty and high risk in an industry. They find that PsyCap positively influences the performance of companies in creation contexts, and we have broadened this knowledge to a crisis context. We find a positive relationship between the PsyCap of SME leaders and performance of their companies in crisis. As Hmieleski et al. (2015) also find that in discovery contexts (stable conditions within an industry accompanied by risk), PsyCap of small business leaders does not have a significant influence on performance, we stress that psychological resources could be of particular relevance in a crisis context. However, this effect is not surprising for two reasons. First, research shows that SME leaders that can rely on a broader resource base in terms of personal and psychological resources are better able to avoid losses during times of crisis (Doern, 2016). In our study, this translates into SME leaders having a broad psychological resource base in terms of hope, efficacy, resilience, and optimism that helps them to enhance their performance. Second, as SME leaders with a high PsyCap might perceive a crisis in a more positive light, they tend to frame the situation accordingly when articulating it to their employees by encouraging them in challenging and uncertain times (Penrose, 2000). Studies indicate that positivity of SME leaders spreads to their employees (Rego et al., 2019; Wall & Bellamy, 2019).

Besides our main findings, we also show a strong negative relationship (–.366, p < .000) between the perceived affectedness of a crisis by leaders and the performance of their companies and a significant relationship between crisis-affectedness and the implementation of investment (.151, p < .05) and cost-cutting measures (.452, p < .000).

These strong effects are interesting in the context of our study but not surprising. Crisis-affectedness as a variable, which reflects the external influencing factors in our study, seems to play a big role in the studied context. As illustrated by the COVID-19 pandemic, crises are highly challenging situations for all those affected with a very strong influence on personal actions (Cowling et al., 2018; Herbane, 2010). Thus, concerning SME leaders and the overall economy, crises also have a direct influence on the economic situation of companies and the overall economic system. In particular, a crisis such as the COVID-19 pandemic affected large parts of the economy (Kuckertz et al., 2020; Madhok, 2021), and therefore a strong effect on the performance of SMEs is not surprising. An individual company and entrepreneur can only influence their situation in such a global crisis up to the point that their external environment permits (Cowling et al., 2018; Latham, 2009). The good news, especially for SME leaders, who must deal with additional constraining factors due to their firms’ size (Fort et al., 2013; Smallbone et al., 2012) and could, therefore, see themselves as incapable of acting in such situations, is that nevertheless there are levers that can buffer the effects of these mechanisms to a certain point.

Besides, we also find the effects of crisis-affectedness on the implementation of investment (.151, p < .05) and cost-cutting measures (.452, p < .000), with the latter being relatively strong. In general, this result underlines the reasoning that crises entail an inherent pressure for players to act (Colpan, 2008; van der Vegt et al., 2015). The greater the impact of a crisis on an organization, the greater the need for action and thus countermeasures. In light of our results, the interpretation of the strong positive effect of crisis-affectedness on cost-cutting measures is particularly interesting: the more an SME leader and his or her company is affected by a crisis, the more he or she resorts to cost-cutting measures. In contrast, our main findings suggest that investment measures are a more effective way to respond to a crisis than cost-cutting measures. The tendency to use cost-cutting measures when a crisis is more severe can therefore indicate a heuristic or psychological bias, which may imply that SME leaders do not take advantage of opportunities related to investment measures. Although further research is needed to ensure that this is the case, it is important to recognize this relationship. Our findings show that the more an SME is affected by a crisis, the more important it is for its leader to strengthen his or her own PsyCap.

Conclusion, implications, and limitations

Crises such as the COVID-19 pandemic pose a great threat to SMEs (Alvarez & Barney, 2020) whose survival can be endangered due to their limited financial resources. The unique advantage of SMEs during such times lay in their flexibility and the centralized decision-making ability of their leaders, which helps them quickly adapt to the changing circumstances. In the context of research on behavioral micro-foundations in strategic management, we argue that the central position of SME leaders in such a situation represents an important factor in understanding strategic responses (Roundy & Lyons, 2022; Zhou et al., 2017), as crises pose difficult times for both companies and their leaders. In our study, we argue that psychological resources, such as the SME leaders’ PsyCap, play a crucial role as its influence on strategic responses (investment vs cost-cutting) ultimately influences the performance of companies during a crisis. We find empirical evidence for our proposed model and thus contribute to a more nuanced understanding of strategic responses during a crisis and the important role of the psychological state of SME leaders. Furthermore, by showing SME leaders’ PsyCap effects on performance, we contribute to the understanding of SME leaders and their PsyCap as a unique intangible resource for sustained competitive advantage of SMEs in times of adversity in the sense of RBT.

Our findings have significant implications for practitioners. With our study, we show that the individual psychological state of SME leaders influences their choice of strategic measures taken during difficult times, ultimately influencing the performance of the companies, and thus potentially increasing the chances of survival of the companies in adverse circumstances. This is especially interesting for SME leaders as Luthans, Avolio, et al. (2007) show that PsyCap is a state-like concept that can be altered with appropriate psychological measures in such a way that an individual’s PsyCap increases (Dello Russo & Stoykova, 2015). These findings suggest that SME leaders should become aware of the power of positive psychological resources, to navigate crises and attempt to develop them before crises occur. The findings also imply that coaches and psychologists working with SME leaders should develop appropriate measures to help their clients raise their PsyCap. In addition, our findings suggest that choosing investment measures during crises represents the preferable strategy for SMEs, as those show a positive effect on the company’s performance, while choosing cost-cutting measures leads to lower performance.

However, like every empirical study, our research suffers from limitations. For example, it cannot be generalized that implementing investment measures is always the better alternative for SMEs. Such an analysis would require long-term data and information from different crisis settings. Besides, we strongly believe that a mix of investment and cost-cutting measures can lead to positive outcomes. One may conceive situations in which a reverse or simulative relationship exists between measures taken and performance. For example, when performance is high, more offensive measures are chosen; or when performance is low, more defensive measures are chosen. In addition, it must be mentioned that we cannot make any statements as to the extent to which the PsyCap of an individual SME leader has changed due to COVID-19. As PsyCap is relatively stable over time, we assume that no significant changes happened due to the crisis; however, we cannot control that. In our study, we also could not control how in management teams the PsyCap of all leaders may interact and influence the choice of measures and performance. More research on the impact of PsyCap in team interaction and its influence on decision-making is needed. Furthermore, our study is limited to Germany. As the measures implemented by governments to prevent the spread of COVID-19 differed across countries (Villanueva & Sapienza, 2021), different results might occur in other cultural settings. However, we believe that focusing on one country served the purpose of our research because all companies in Germany were confronted with the same business and political environment, which enabled comparison. Nonetheless, more studies in different cultural contexts can contribute to a more nuanced understanding of how PsyCap can act as a sustained competitive advantage for SMEs. Besides that and in line with the suggestion for further research by Memili et al. (2013), we do believe that SMEs are not the only ones who can benefit from developing a sustained competitive advantage through their PsyCap. An interesting research avenue could, for example, be the comparison between family businesses and non-family businesses. Due to their idiosyncratic identity, family businesses might offer a more nurturing environment for leaders’ PsyCap than non-family businesses.

Footnotes

Appendix 1

Questions on investment and cost-cutting measures.

| Variable | Questions |

|---|---|

| Investment measures | To deal with the challenges of the COVID-19 pandemic, our company . . . . . . developed an aggressive sales strategy to increase revenue . . . increased investments in more efficient equipment and processes to reduce costs . . . expanded research and development activities to secure our market position . . . increased its use of information-gathering measures . . . introduced a management concept with target agreements and profit incentives . . . implemented major organizational changes |

| Cost-cutting measures | To deal with the challenges of the COVID-19 pandemic, our company . . . . . . cut the operating budgets of all divisions . . . enforced across-the-board cuts in the budgets of all departments or divisions . . . reduced the number of employees . . . eliminated products that were only marginally profitable to reduce costs . . . cut expenses on office materials, entertainment allowances, and travel . . . reduced the decision-making powers of department and field managers . . . fired managers from departments with weak results |

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.