Abstract

Research on firm’s motivation to undertake search behaviors in situations of positive and negative performance feedback is limited in empirical literature. In addition, the role of institutionalized corporate governance mechanisms in mediating firm’s aspiration-driven search behaviors is yet to be explored. Therefore, this study aims at examining whether firms around the world facing positive and negative performance feedback undertake different search behaviors. Furthermore, we test whether firm’s corporate governance mechanisms strengthen such search behaviors. This study reports that negative performance feedback positively influences firm problem-driven search behaviors, whereas positive performance feedback positively impacts its innovative search behaviors. Furthermore, we find a significant negative moderating influence of board strength, while a mixed positive influence of board effectiveness on firm performance feedback to carry out distinctive search behaviors. Therefore, we think that these findings would help the regulators and policy makers to strengthen their existing corporate governance mechanisms and regulations.

Introduction

There are inconclusive theoretical underpinnings about the search behaviors of firms facing differential performance feedback situations. On one hand, behavioral theory (BT) (Cyert & March, 1963) prescribes below-average firms’ problem-driven (i.e., problemistic) search behaviors 1 for alternative solutions. On the other hand, the Ansoffian view (Ansoff, 1979) opines that a necessary strategic thrust (henceforth ST) for a firm is primarily due to aspiration attainment discrepancy, that is, dependent on positive performance feedback. Thereby, Ansoff (1979) argued for exploratory or innovative search behaviors. 2 Therefore, a better understanding of the drivers and domain of search behaviors and the types of strategies firms might select under differential performance feedback situations, may be conditioned on their goal difficulty and aspiration attainment discrepancy. We draw our primary motivation from the premise that how a firm’s differential performance feedback driven by its internal capabilities and external conditions propels its innovative and problem-driven search behaviors.

BT predicts that firms with negative performance feedback 3 would trigger problem-driven search behaviors and, therefore, organizational change. This conjecture is supported in studies such as research and development consortia of high-tech firms (Bolton, 1993), innovations and investment in shipbuilding (Greve, 2003a), and R&D expenses of manufacturing firms (Chen, 2008; Chen & Miller, 2007). On the contrary, Audia and Greve (2006) showed that negative performance feedback lowers search behaviors in small firms, and it either has no significant effect or increases search, that is, risk-taking behaviors in large firms. Vissa et al. (2010) found that organizational form (business-group affiliated firms vs. unaffiliated firms) influences responsiveness to performance feedback contingent on the type of search domain (market or R&D). All these empirical studies suggest that richer theoretical insights into the linkage between performance feedback and a firm’s decision outcomes lie in investigating the moderating/mediating factors affecting this relationship.

In addition, the inconsistent empirical results (see Audia & Greve, 2006; Chen, 2008; Gaba & Joseph, 2013; Iyer & Miller, 2008; and so on) of firm’s performance feedback and search behaviors have also prompted us to investigate whether institutionalized corporate governance (CG) mechanisms in firms around the world with cross-economic, cross-regulatory, and cross-cultural heterogeneities strengthen such relationships, and, therefore mitigate the empirical contradictions. As reported, negative performance feedback would increase the participation of firm boards in the power to influence a firm’s decision-making (Tuggle et al., 2010). Boards typically influence firms through each of these three primary mechanisms—by monitoring management with the interests of owners or other external stakeholders in mind, by securing resources for the firms, and by providing advice to management (Krause et al., 2013). Empirical literature (Kumar & Sivaramakrishnan, 2008; Pathan, 2009; and so on) also argues that the effectiveness of the firm board, that is, monitoring firm managers and limiting their opportunistic behaviors, and the strength of the firm board, that is, providing resources and advice due to diversity, depend on its constructs. As there is a limited theoretical argument as to the most important CG mechanisms in our context, we make a conscious selection of firm-board variables here based on those emphasized most in the empirical literature (see Dasgupta, 2021; Kumar & Sivaramakrishnan, 2008; Pathan, 2009; and so on) as a proxy of “board strength” (representing board composition or diversity [i.e., structure]) and “board effectiveness” (representing board functioning [i.e., process]), namely independent directors and women directors, and board size and number of meetings, respectively. We measure board strength and board effectiveness by more independent directors and greater presence of women directors, a large board size, and a higher frequency of board meetings. This is because a higher number of independent and women directors on a firm board would make the firm’s decision-making more prudent and less subjective due to divergent views, and therefore, such strategic behaviors would be very strong. On the contrary, a large board comprised of members from different fields and with different views and a high frequency of meetings would improve the quality of managerial decision-making by stricter monitoring, resource capabilities, and better managing of business complexities.

Therefore, overall, we draw our secondary motivation from the fact that there is still a need for research examining whether problem-driven or innovative search behaviors are affected by a firm’s negative or positive performance feedback, which might be caused by the underlying fragile CG practices in such firms. Accordingly, it is compelling to investigate here how institutionalized CG mechanisms can moderate a firm’s search behaviors under positive and negative performance feedback situations.

Furthermore, prior methodological studies on aspiration had used direct internal measures of firm aspiration. For instance, Lant (1992) and Mezias et al. (2002) both estimate models with actual aspiration measures but did not compare multiple aspiration formulations. Besides, their results might not generalize to corporate-level data, as Lant (1992) uses data from experiments using business school students, and Mezias et al. (2002) use budget targets of the branch banks. In separate works, Washburn and Bromiley (2012) study the auto manufacturer to compare alternative aspiration models, but the implications of their results for aggregate studies are unclear. While these articles make significant contributions, a perceptible comparison of different aspiration measures has long been overdue. Therefore, we have also attempted here to fill this gap by examining the impact of the firm’s historical aspiration (HA), social aspiration (SA), and weighted aspiration (WA)-based performance feedback on its search behaviors in both positive and negative performance feedback situations in a multicountry context.

Overall, in general, we contribute to the existing literature on finance and strategy in three ways. First, this study reports that negative performance feedback positively influences firm problem-driven search behaviors, whereas positive performance feedback positively impacts innovative search behaviors. We, therefore, augment the BT (Cyert & March, 1963) and didn’t substantiate the Ansoffian (Ansoff, 1979) view of negative performance feedback firms. However, Ansoffian’s (Ansoff, 1979) ST viewpoint is exclusively evident for positive performance feedback firms in undertaking innovative search behaviors. So, our initial conjecture of differential performance feedback situations impacting a firm’s search behaviors differently is henceforth proved. Second, we find a strong negative moderating influence of a firm board with board strength and a mixed positive influence of a firm board with board effectiveness on a firm’s performance feedback to undertake search behaviors. More specifically, an effective firm board not only strengthens the firm’s problem-driven search behaviors but also shows a mixed impact on innovative search behaviors under our aspiration measures. In addition, we also find that higher independent directors’ presence on a firm board negatively moderates the firm’s performance feedback to undertake search behaviors. Similarly, we report that board size negatively impacts a firm’s performance feedback to undertake their problem-driven search behaviors. On the contrary, higher women directors’ presence has a significant positive influence on such firm actions. The results of the meeting frequency also show a significant favorable influence on firm performance feedback to undertake its problem-driven and innovative search behaviors. Therefore, we substantiate that each of these CG mechanisms has its unique moderation impact on a firm’s performance feedback to undertake different search behaviors distinctively. Third, to mitigate the conflicts arising from different aspiration measures driven by performance feedback, we classify our firms into two divisions, that is, positive and negative performance feedback firms. Subsequently, we prove that negative performance feedback positively influences below-average firm problem-driven search behaviors, whereas positive performance feedback positively impacts innovative search behaviors.

The remaining portion of this article is organized as follows: “Theory and hypotheses” talks about the relevant literature and developed hypotheses; “Data, variable construction, and methodology” presents data and methodology; “Results and discussions” presents the results and discussions; and “Conclusion” concludes our article with the relevant implications, followed by references and tables.

Theory and hypotheses

Theoretical overview

Firms undertake search behaviors when their performance falls below their historical performance levels (i.e., HA) and the performance of other referent firms such as industry peers (Cyert & March, 1963, 1992; DasGupta, 2022; Greve, 2008; March & Simon, 1993) (i.e., SA). Several authors have also used a weighted average of self- and social-referent measures to give one aggregate measure (Greve, 2003a; Mezias et al., 2002; Shinkle, 2012) (i.e., WA). Given BT’s focus on the search choices made by the firm’s decision-makers and agency theory’s focus on monitoring the role of the firm board (e.g., Fama, 1980; Kumar & Sivaramakrishnan, 2008; Pathan, 2009; and so on), we further contend that the institutionalized CG mechanisms would be critical mediating factors to strengthen or weaken firms’ performance feedback-search behavior associations. We substantiate our CG mediation arguments further from the empirical angle of the “monitoring hypothesis” (see Brick & Chidambaran, 2008; Fama, 1980; Pathan, 2009) whereby we presume that “board strength” and “board effectiveness” comprising of a higher number of independent directors and women directors, and, large board size and higher number of meetings, respectively, would strengthen firms’ performance feedback-search behavior associations.

Firm’s performance feedback and search behaviors

The BT (Cyert & March, 1963) of the firm suggests that in situations when performance declines far below the aspiration level, that is, negative performance feedback conditions, the firm’s managers initiate search behaviors for solutions, referred to as “problem-driven” search behaviors. The intent is to reverse the decline and improve future firm performance (Greve, 1998, 2003a). Thereby, greater search behaviors would only occur when due to lower performance firms attain negative performance feedback, and such behaviors would diminish as performance improves and thereby firm reaches the positive performance feedback zone (Greve, 1998). Therefore, we expect a firm to undertake higher “problem-driven” search behaviors under a negative performance feedback condition. This guides us to the following hypothesis:

We further argue that there is an agency problem in managerial decisions concerning R&D intensity in response to the firm’s performance feedback. The basis of our argument is grounded on the agency theory perspective that managers are risk-averse and self-interest-seeking (Amihud & Lev, 1981). The fact is that an increase in R&D intensity does not have an immediate positive impact on a firm’s performance given that returns to R&D investments tend to be distant and uncertain (Scherer & Ross, 1990). Rather, it can make firm performance vulnerable because of the increase in operating expenses of the firm. Accordingly, to strengthen short-term firm performance, managers are most likely to search for opportunities to reduce such expenses that do not have an immediate negative impact on revenues. There is also evidence that firms use reductions in R&D expenses to boost earnings after a leveraged buyout (Long & Ravenscraft, 1993). Therefore, we argue that managers might also use reductions in R&D expenses to increase the chances of improving positive performance feedback for their firms through improved performance especially when they are having average to below performance. Therefore, we expect a firm to undertake higher “innovative” search behaviors under a positive performance feedback condition. This leads us to the following hypothesis:

CG, firm’s performance feedback, and search behaviors

In addition to theoretical propositions (see Section 2.1), the inconsistent empirical results (see Audia & Greve, 2006; Chen, 2008; Gaba & Joseph, 2013; Iyer & Miller, 2008; and so on) of firm’s performance feedback and search behaviors have prompted us to investigate whether the institutionalized CG mechanisms in international firms with cross-economic, cross-regulatory, and cross-cultural heterogeneities mediate firm’s performance feedback-search behavior relationships and thereby solving the empirical contradictions. We expect that the negative performance feedback condition would increase the firm-board involvement in the power to influence the firm’s decision-making (Tuggle et al., 2010). Boards typically influence a firm’s search decisions through each of these three primary mechanisms—by monitoring management with the interests of owners or other external stakeholders in mind, by securing resources for the firms, and by providing advice to management (Krause et al., 2013).

The agency costs inherent in the separation of ownership and control would be reduced by monitoring of the board of directors, and, thereby, might improve firm performance and accordingly firms would move to positive performance feedback situations (Fama, 1980; Zahra & Pearce, 1989). In addition, the resources’ functioning of the board encompasses providing expertise and advice (Baysinger & Hoskisson, 1990), administering advice and counsel (Lorsch & Maclver, 1989), and aiding in the formulation of strategy and other important firm decisions such as search behaviors (Judge & Zeithaml, 1992). Therefore, all these board mechanisms are extremely important in strengthening interrelationships between firm performance, performance feedback, and search behaviors. In this context, Haxhi and Van Ees (2010) also argue that, in reality, firm boards might be less concerned with solving conflicts of interest, rather, more concerned with solving problems of performance variability (causing negative performance feedback), coordination, and managing the complexity and uncertainty associated with strategic decision-making such as “innovative” search behaviors (Rindova, 1999; Roberts et al., 2005).

Empirical literature (Kumar & Sivaramakrishnan, 2008; Pathan, 2009; and so on) also argues that a firm’s board effectiveness, that is, monitoring the firm’s managers and limiting their opportunistic behaviors, and board strength, that is, providing resources and advice due to diversity, depend upon its constructs. Our proxies of board strength and board effectiveness are more independent directors and higher women directors’ presence, and, large board size and higher frequency of board meetings. This is because a higher number of independent and women directors on a firm board would make the firm’s decision-making more prudent and less subjective due to divergent views and thereby such strategic behaviors would be very strong. On the contrary, a large board comprised of members from different fields and with different views and a high frequency of meetings would enhance the quality of managerial decision-making through stricter monitoring, resource capabilities, and managing business complexities better.

Board strength (board diversity) in a firm is extremely important for it to be effective. Such diversity would also be resulting in better firm performance, quality of earnings, and/or lower risk-taking propensity by managers (see Fama & Jensen, 1983; Kumar & Sivaramakrishnan, 2008). All these could mediate performance feedback. We argued in line with the reputation hypothesis, independent directors would support investments in less risky projects which help firms in avoiding losses and thereby protect their image (Pathan, 2009). This also might create performance feedback situations in comparison with social peers. In addition, such firms would maintain at least the status quo in terms of their performance and would also maintain positive performance feedback, due to strict monitoring of managerial activities. Based on the monitoring hypothesis, we can also argue that the presence of a higher percentage of independent directors on firm boards is expected to reduce their risk-propensity regarding “innovative” search behaviors. Empirical evidence supports the above argument by suggesting a negative relationship between the presence of independent directors on firm boards and their such search behaviors (see Brick & Chidambaran, 2008; Pathan, 2009). This argument is grounded on the assumption that the cost of information becomes higher for nonexecutive directors (Boone et al., 2007) as only limited information is available to the firm’s managers; thereby, the information asymmetry increases.

On the contrary, Adams and Ferreira (2009) observe that women directors’ presence influences monitoring policy. Empirical literature (see Jianakoplos & Bernasek, 1998) also shows that in terms of search preferences men are more likely to take higher risks than their women counterparts. Accordingly, most studies (Adams & Ferreira, 2009; and so on) argue women on boards are tempted to exercise excessive monitoring in profitable firms following riskier decisions that in turn might decrease shareholder value. A large body of empirical evidence is also found on whether the presence of women on firm boards increases the propensity to search or favors risk taking (see Faccio et al., 2016; and so on). Most of these studies present a decline in search behaviors in women-dominated firms across countries which also implies performance feedback for them. On the contrary, many empirical studies (see Hutchinson et al., 2015; and so on) document the positive influence of women directors on firm performance across countries and industries. Higher present performance would automatically drive positive performance feedback for the present. However, in such cases, in women-led firms thereafter mostly search behaviors (mostly “innovative”) would be decreased. This leads us to the following hypothesis:

We argue that board effectiveness in monitoring and advising firm managers determines its strength, and such a firm board is representing the firm’s shareholder’s interest more. Following De Andres and Vallelado (2008) and Erkens et al. (2012) among others, we also argue that “board effectiveness” symbolizes large board size and a higher frequency of board meetings. Our argument here that the number of directors serving a firm board is relevant to the outcome of the board’s decisions of search behaviors is in line with the assumptions of the agency theory (Jensen & Meckling, 1976). In addition, board size and its negative relation to firm performance due to nimbleness, cohesiveness, less communication, and coordination costs as well as less “free-riding” director problems with smaller boards (Jensen, 1993) are the most common findings in the literature (Yermack, 1996; and Hermalin & Weisbach, 2003). However, Yermack (1996) observes that small boards would be more likely to ratify riskier R&D-intensive investment projects that can ultimately increase the overall firm risk and might cause volatile operating performance. Thereby due to performance volatility, negative performance feedback situations cannot be ruled out for firms with small boards. Accordingly, it would intent and carry out problem-driven search behaviors which imply that small board size does have a positive influence on such behaviors. On the contrary, several studies observed that we need larger boards in large firms to reflect the complexities of their business models (see Coles et al., 2008), to monitor CEO functioning better (Forbes & Milliken, 1999), and to increase the pool of resources and expertise available (Van den Berghe & Levrau, 2004; see also impact of resource dependency theory [see Pfeffer, 1972] on CG [Nicholson & Kiel, 2007]). Coles et al. (2008) find that firm performance increases with board size for complex firms. Cheng (2008) also shows that US firms with larger boards are associated with higher performance and lower performance volatility. Jackling and Johl (2009) find that board size impacts firm performance positively for Indian firms. Large board size negatively impacts a firm’s search behaviors due to the diversification of opinions effect (Sah & Stiglitz, 1986, 1991). Similarly, it would impact the performance feedback of the firm through improved performance.

We also argue that effective monitoring and intensity of board activities (in line with resource dependency theory [Pfeffer, 1972]) can be possible with a higher frequency of board meetings which might be an important way to improve “board effectiveness” (Adam & Ferreira, 2009). This also takes into account the internal functioning of the board (De Andres & Vallelado, 2008) and how boards operate. As frequent meetings provide board members with the chance to meet and discuss and exchange ideas regularly on how they wish to monitor managers and firm strategies such as search behaviors, we expect that the more frequent the meetings are, the closer the optimum control over managers is.

Ntim and Osei (2011) suggest that more frequent board meetings tend to generate higher financial performance which would cause positive performance feedback. It further strengthens when previous stock performance is considered, suggesting that operating performance rises in the subsequent periods with a high number of meetings (Francis et al., 2012). On the contrary, the literature also suggests that boards with frequent meetings possess less market value (Vafeas, 1999, p. 140) and negative entrepreneurial activities in firm Johl (2006). Jensen (1993) questions the activeness of boards in such cases and reports poor performance leading to problem-driven search behaviors. Bhagat et al. (2015) emphasize the number of risk committee meetings as the driver of market performance which implies strong risk governance or balanced risk taking by firms. Thus, we argue that a high frequency of board meetings would also influence the performance feedback situations of the firm positively by improving the stability of the base operating performance. This leads us to the following hypothesis:

Data, variable construction, and methodology

Data and sample

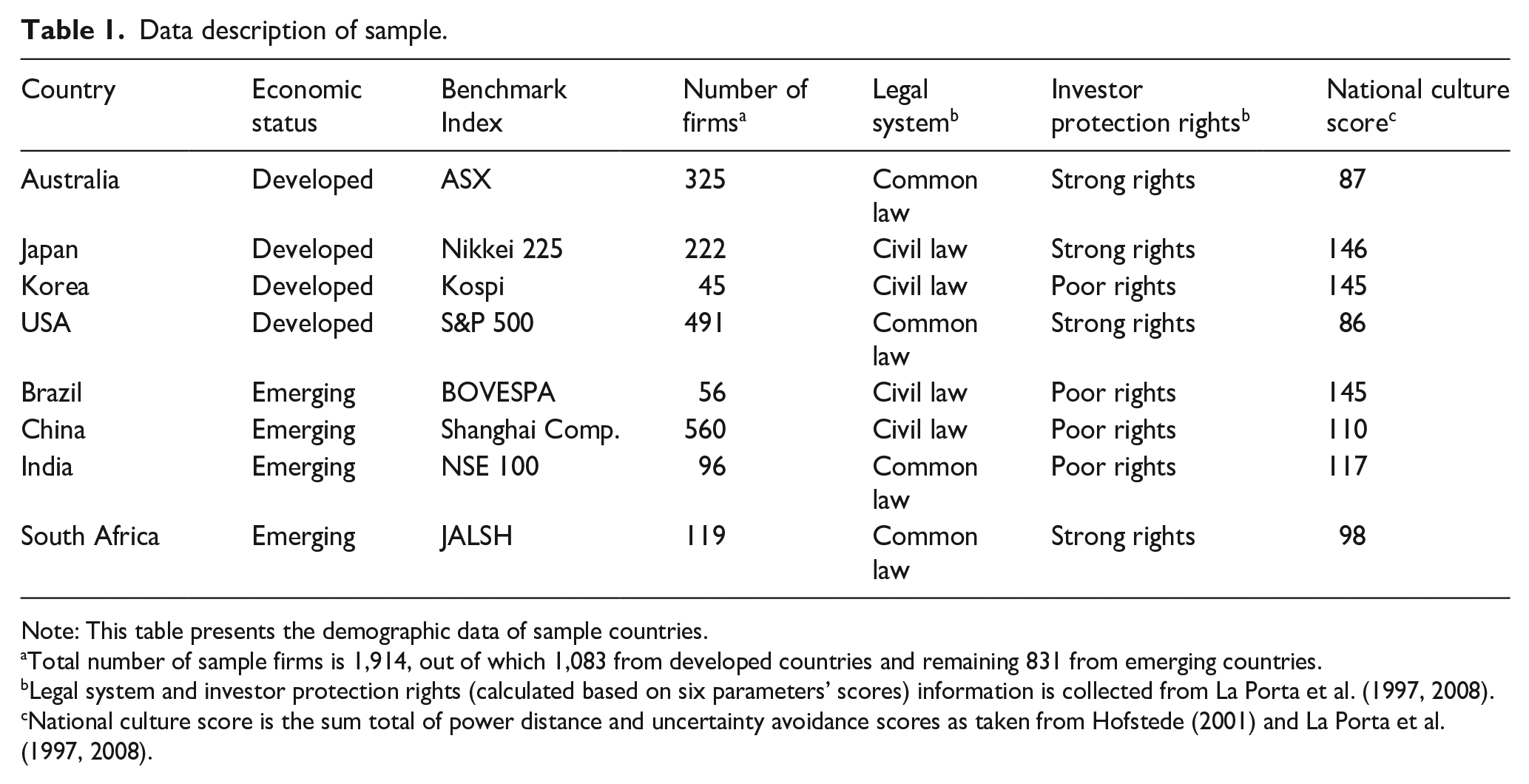

The empirical setting for our study starts with a large set of firm-level panel data for eight countries comprising of both developed (the United States, Australia, Korea, and Japan) and developing (China, India, Brazil, and South Africa) countries during the period 2008 to 2017 (details given in Table 1). To prepare the sample data, we filter the data for the nonfinancial firms from each country’s firm-level dataset. This resulted in 1,914 firms out of 2,142 firms in the final sample for the analysis. These 1,914 firms include 1,083 companies from four developed countries and remaining 831 firms from four Brazil, Russia, India, China, and South Africa (BRICS) countries representing the emerging countries here. We exclude the fifth BRICS country, that is, Russia for data unavailability. So, finally, we investigate 1,914 firms comprising of 19,140 firm years for all studied variables. We have used the Bloomberg database for sourcing the dataset.

Data description of sample.

Note: This table presents the demographic data of sample countries.

Total number of sample firms is 1,914, out of which 1,083 from developed countries and remaining 831 from emerging countries.

Legal system and investor protection rights (calculated based on six parameters’ scores) information is collected from La Porta et al. (1997, 2008).

National culture score is the sum total of power distance and uncertainty avoidance scores as taken from Hofstede (2001) and La Porta et al. (1997, 2008).

Variable construction

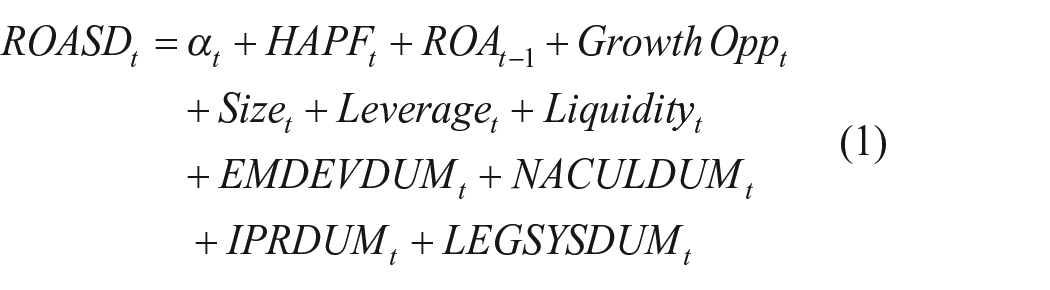

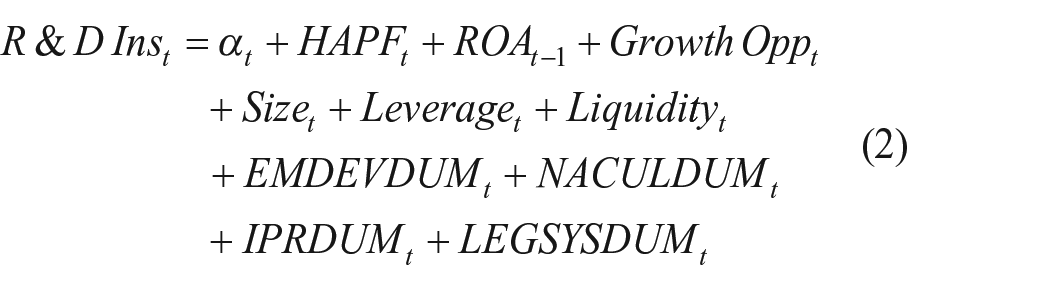

We present a detailed layout of the variable construction in this section. Our sample primarily comprises of three sets of variables along with set of control variables. The first set of variables pertains to problem-driven search behavior contexts 4 (i.e., the return on assets standard deviation [ROASD]) and innovative search behavior (i.e., the research and development intensity [R&D intensity]). ROASD is calculated by rolling standard deviation of the preceding 3 years’ return on assets (ROA) in each calendar year. For robustness purpose, following Bhagat and Bolton (2008), we calculate ROA as operating income before depreciation divided by total assets and then calculate its SD. 5 Consistent with prior studies (e.g., Chen & Miller, 2007; Gentry & Shen, 2013; Gupta, 2017), we have measured R&D intensity as the percentage of firm’s R&D expenses over sales during each calendar year. This represents the innovative risk behavior here. We also conduct the analysis using only firm observations that reported R&D expenses.

The second set of variables refers to firm’s performance feedback in regard to firm’s historical aspiration performance feedback (HAPF), social aspiration performance feedback (SAPF), and weighted aspiration performance feedback (WAPF). We measure HA as firm’s ROA during the prior year and SA as the cross-sectional median ROA of all other firms within the same industry during that year. Performance feedback is the difference between firm’s ROA and HA, and the difference between firm’s ROA and SA, respectively. We follow Cyert and March (1963) and Greve (2003a) to compute WAPF as a blend of the firm’s historical and SA levels.

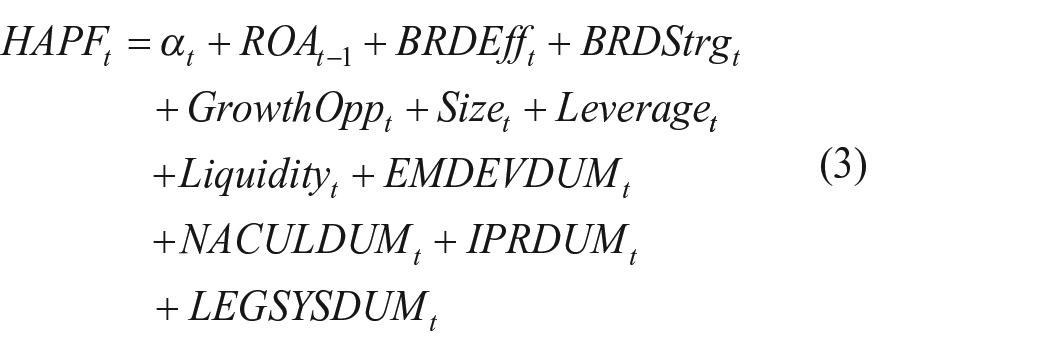

The third set relates to the CG variables, that is, board strength and board effectiveness. We measure board strength by combining higher percentage of independent directors and women directors scaled by board size (i.e., number of directors). On the contrary, our board effectiveness represents large board size and high frequency of board meetings. We also report the mediation impact of each of these individual mechanisms to substantiate our main findings in firm’s performance feedback–search behavior relationships.

Finally, we use a set of control variables 6 (lagged ROA, growth opportunity, size, leverage, and liquidity) and set of dummy variables pertaining to country heterogeneity (i.e., developed and emerging market, national culture, investor protection rights, and legal system [see Table 1 for details]). The extant literature (see Coles et al., 2008; Fisher & Hall, 1969; John et al., 2008; H. Li et al., 2013; and so on) supports inclusion of the control variables bears impact of individual firm’s heterogeneities on its search behaviors and performance feedback. For instance, the growth opportunities available before the firms can drive them in search behaviors especially in innovative contexts.

The institutional, cultural, and economic environments of a country have also been shown (see La Porta et al., 1998, 2008; H. Li et al., 2013; and so on) to affect firm’s search behaviors. Therefore, here we include dummy variables based on their legal system (civil vs. common law) and economic status (developed vs. emerging) and also control for the investor protection rights and national culture prevailing in individual countries. We create development dummy (

Model development and methodology

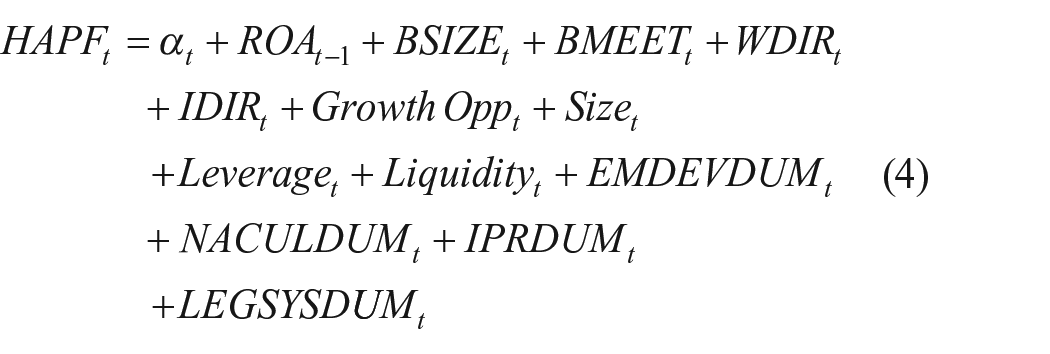

Based on our first hypothesis relating to firm’s HAPF and its problem-driven search behaviors, we test the following equation:

To test the second hypothesis relating to HAPF and its innovative search behaviors, we test the following equation:

Also, we conduct above analyses for firm’s SAPF and its WAPF. Then, suspecting that firm’s performance feedback could be endogenous and influenced by the CG variables, we model and test the following equation for our third and fourth hypothesis:

The above model is also studied using individual elements of board strength and board effectiveness as:

To present a very robust understanding on the issue, we adopt a comparative approach among several methodologies for exploring the relationship between firm’s performance feedback and search behaviors. Therefore, we compare results derived from four specific methodologies, that is, Panel-OLS, Fixed effect (FE) model, dynamic OLS, and Panel system Gaussian mixture model (GMM). The advantages over each of them are presented in this section. To start with, we use the Panel-OLS for a basic general finding. However, while studying such relationship for the diverse set of firms belonging to developed and emerging economies, we focus on three types of endogeneity issues, that is, unobserved heterogeneity, simultaneity, and dynamic endogeneity.

First, it has been noticed in empirical literature that unobserved heterogeneity results, in presence of omitted variables, affects both the independent variables and the dependent variable. In such a case, the use of FE estimation is recognized to be a robust approach. However, in the presence of dynamic endogeneity, such FE models result in biased estimation. The rationale behind such biased estimation is due to the fact that the current observations of the regressand (such as firm’s performance feedback and growth opportunities) are not independent of the previous values of the dependent variable (i.e., variability of firm performance or R&D intensity). Considering this dynamic endogeneity, we use dynamic OLS. Second, we encounter the issue of simultaneity which arises when the variables under study are jointly determined, that is, in our case the search behavior depends on firm’s performance feedback. In such a case, a simultaneous equation model is expected to correct the inconsistency. However, such model demands for strict exogeneous variables which are again extremely tough to identify in the corporate finance and international firms setting. Third, the issue of dynamic endogeneity, that is, dependence of the explanatory variables on the lagged values of the dependent variable in the presence of unobservable effects needs to be addressed. To the best of our knowledge, the dynamic endogeneity issue is not addressed in empirical literature concerning to firm’s performance feedback and search behaviors relationships.

Therefore, to address the dynamic and other types of endogeneity issues, we use the dynamic panel GMM estimation motivated from Arellano and Bond (1991). The Arellano and Bond (1991) methodology converts the level equation to a differenced equation with the predetermined instrument values. The differenced equation suffers from the measurement error issues because differencing the variables reduces the variation in the data and hence reduces the power of the tests. In addition, the independent variables in their level form weak instruments for the differenced equation. Therefore, we use a system GMM (given by Arellano & Bover, 1995 and Blundell & Bond, 1998) which includes the level equation along with the difference equation. In such a case, the first difference becomes the instrument variables in the level equation and the system GMM is represented as follows:

where Y is the regressand (the variability of ROA [i.e., ROASD] and R&D intensity) in their level form and y is the first difference of the regressand. The first difference and level explanatory variables in the equation are given by x and X, respectively. Similarly, Z and z are the set of control variables such as size, leverage, liquidity, growth opportunities, and four dummies for developed or emerging country, investor protection rights, legal system, and culture in our case. To account for dynamic specification, we use k order of lags for the dependent and independent variables. Also, to achieve asymptotic efficiency, we use two-step GMM instead of one-step. To check for the validity of the GMM models, we report the first and second order serial correlation under the null that there is no serial correlation. Furthermore, we report the Hansen statistics for over-identification restrictions under the null that the instruments used here are valid and robust.

Results and discussions

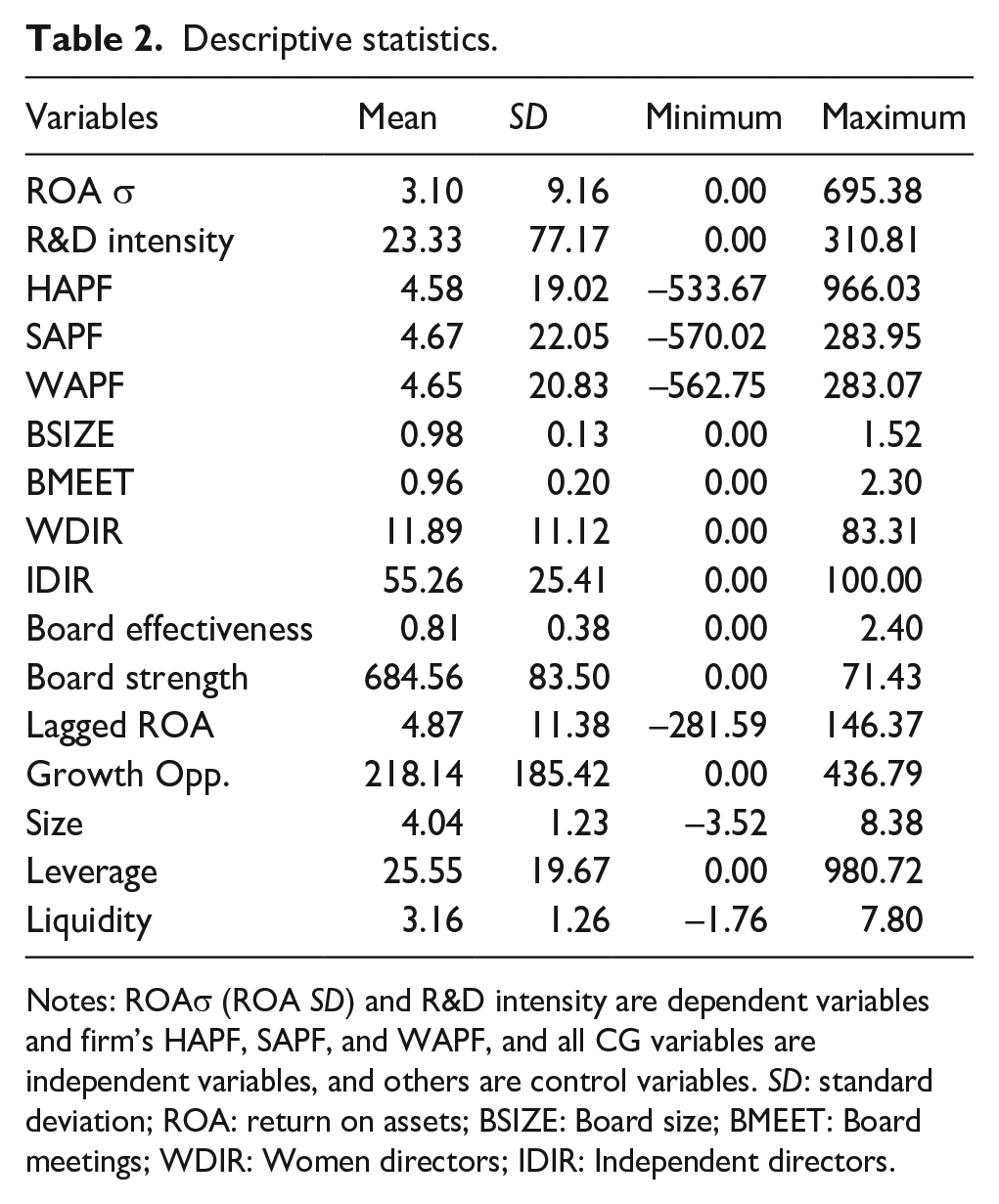

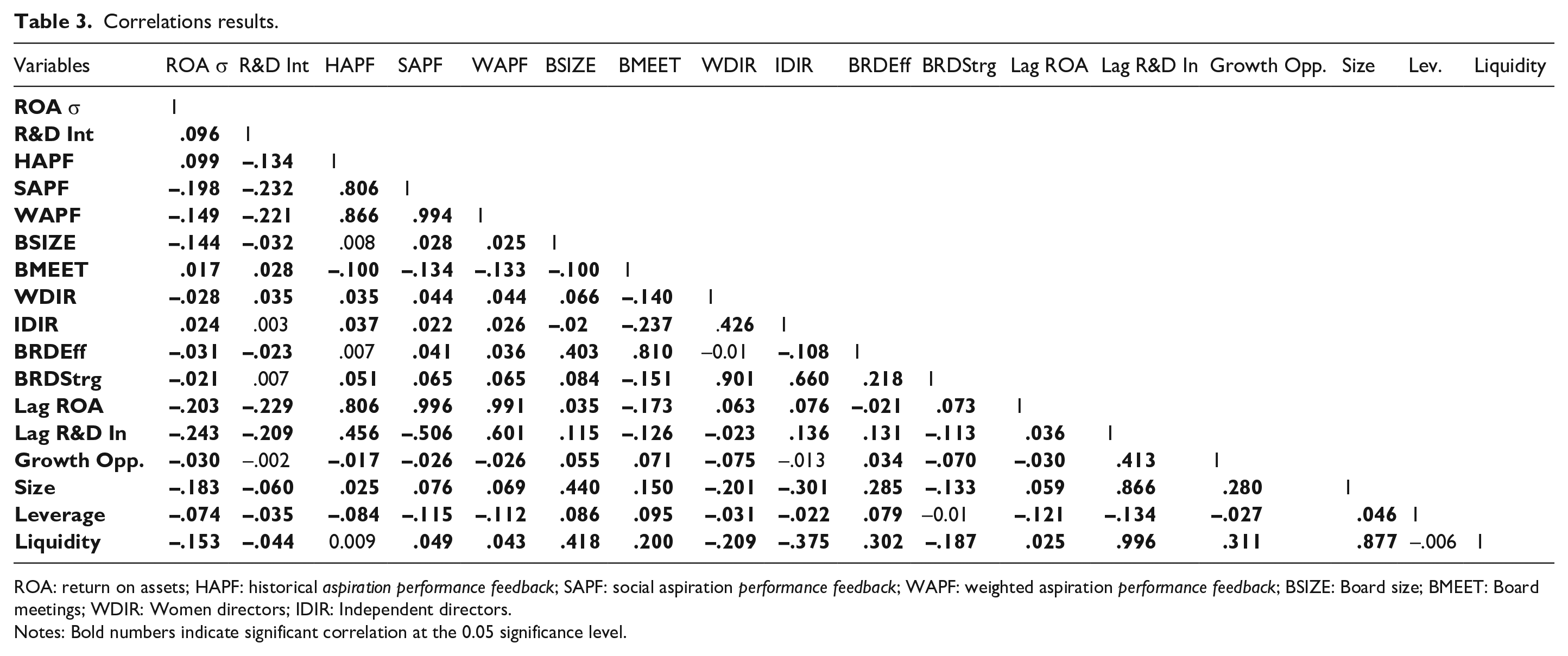

Descriptive and correlation results

We report the descriptive statistics and correlations for the 19,140 observations in Tables 2 and 3. As the historical and social (0.806***), historical and weighted (0.866***), and social and weighted (0.994***) aspiration performance feedback variables show high correlations, we estimate separate models using historical, social, and WA levels. Greve (2003b) suggested that managers might prefer SA level when they believe that their firm is comparable to others in an industry but prefer HA level when they view their firm as being unique. By estimating separate models for HAPF, SAPF, and WAPF, we also avoid including redundant indicators that could distort parameter estimates (Gordon, 1968).

Descriptive statistics.

Notes: ROAσ (ROA SD) and R&D intensity are dependent variables and firm’s HAPF, SAPF, and WAPF, and all CG variables are independent variables, and others are control variables. SD: standard deviation; ROA: return on assets; BSIZE: Board size; BMEET: Board meetings; WDIR: Women directors; IDIR: Independent directors.

Correlations results.

ROA: return on assets; HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; BSIZE: Board size; BMEET: Board meetings; WDIR: Women directors; IDIR: Independent directors.

Notes: Bold numbers indicate significant correlation at the 0.05 significance level.

Our descriptive results (see Table 2) show that R&D intensity is more volatile across firms in comparison with income stream volatility (ROASD). This is since innovative search behaviors undertaken by firms are mostly opportunistic and require both growth opportunities and available slack resources. On the contrary, problem-driven search behaviors are situations-driven and necessary for firms facing declining operating performance, that is, mostly having negative performance feedback. Our aspiration measures are similarly volatile which justifies inclusion of all in this study. On the contrary, though board effectiveness is stable, but presence of board strength is extremely volatile (σ of 83.5%). The independent directors’ presence is not stable which might imply that in many of our sample firms, CG mechanisms are not strictly adhered to. This might cause the value-reducing innovative search behaviors especially in case of positive performance feedback firms.

The correlations (see Table 3) show that performance feedback measures have a significant negative association with both firms’ problem-driven and innovative search behaviors. These are further mediated by board strength and board effectiveness of firm boards. We find that board size in individual capacity impacts search behaviors negatively. On the contrary, board meetings and independent directors’ high percentage positively influence such behaviors. However, women directors’ high percentage in firm boards provide us conflicting direction. On one hand, it weakens problem-driven search behaviors, however, initiates innovative search behaviors in firms. Both board strength and board effectiveness have a significant positive association. Lagged ROA, lagged R&D intensity, and growth opportunity variables all are having a significant negative association with search behaviors. Our control measures also show strong significant evidence to impact our main variables. All these relationships imply that their inclusion in our models would further substantiate our main findings.

Preliminary multivariate results

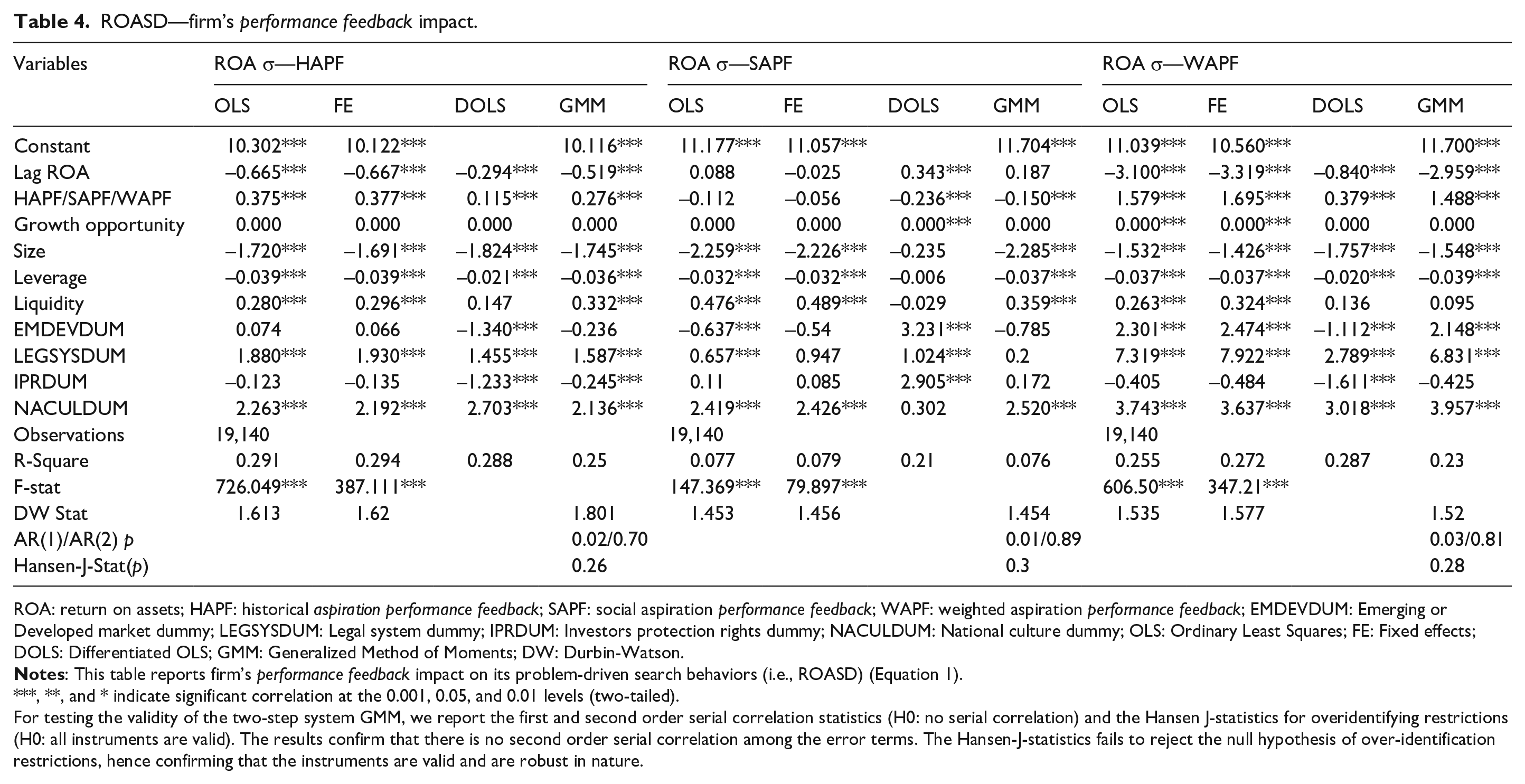

Tables 4 and 5 present the results for our models corresponding with Equations 1 and 2 about performance feedback of firms considering the full sample. Firm’s HAPF and WAPF across our methods shows a positive impact on firm’s innovative search behaviors. Accordingly, we confirm our Hypothesis 2. Furthermore, we find that the firm’s SAPF has negative influence on firm’s problem-driven search behaviors, accepting Hypothesis 1. However, we report some conflicting results, that is, the firm’s SAPF has significant negative impact on its innovative search behaviors.

ROASD—firm’s performance feedback impact.

ROA: return on assets; HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; OLS: Ordinary Least Squares; FE: Fixed effects; DOLS: Differentiated OLS; GMM: Generalized Method of Moments; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

For testing the validity of the two-step system GMM, we report the first and second order serial correlation statistics (H0: no serial correlation) and the Hansen J-statistics for overidentifying restrictions (H0: all instruments are valid). The results confirm that there is no second order serial correlation among the error terms. The Hansen-J-statistics fails to reject the null hypothesis of over-identification restrictions, hence confirming that the instruments are valid and are robust in nature.

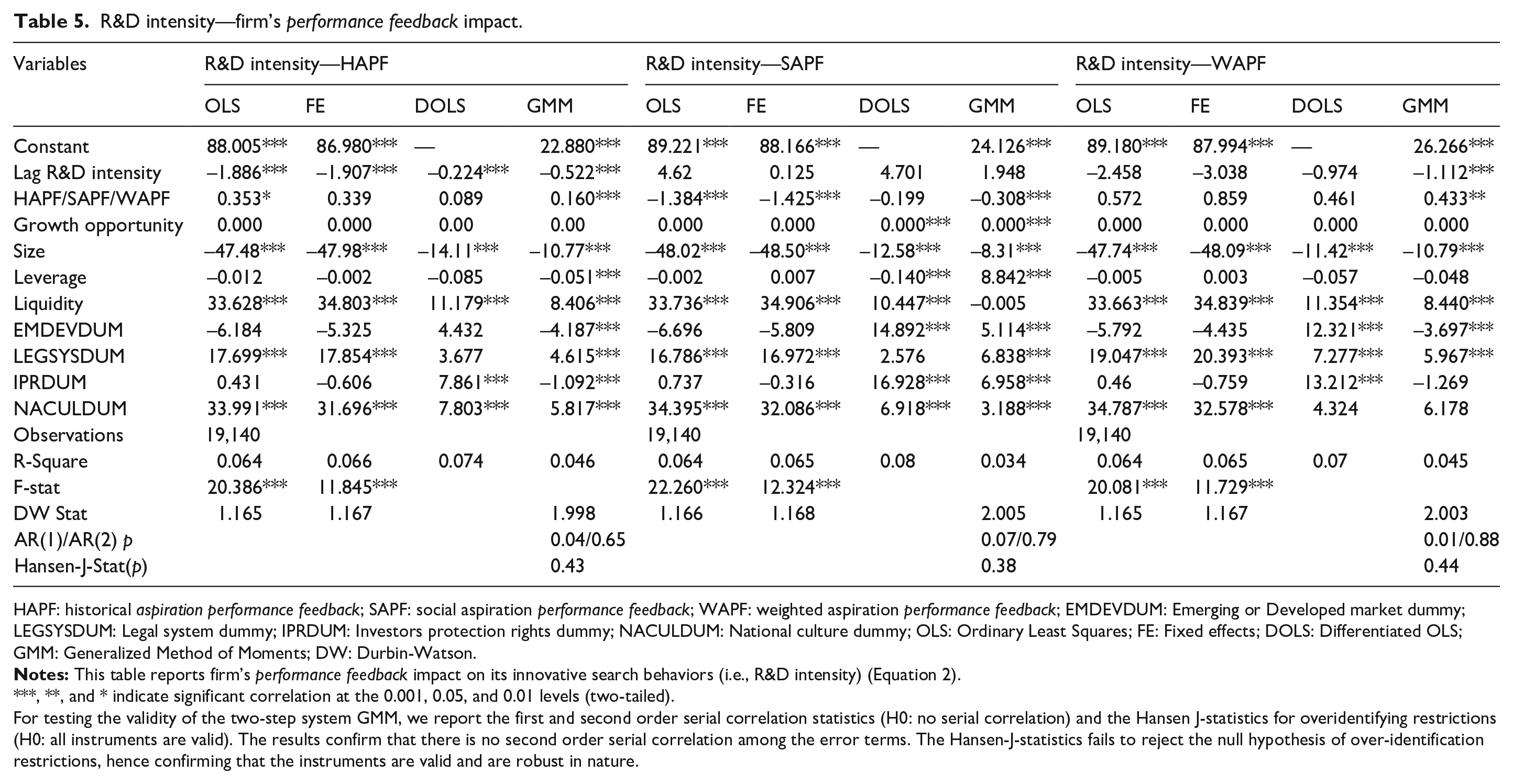

R&D intensity—firm’s performance feedback impact.

HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; OLS: Ordinary Least Squares; FE: Fixed effects; DOLS: Differentiated OLS; GMM: Generalized Method of Moments; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

For testing the validity of the two-step system GMM, we report the first and second order serial correlation statistics (H0: no serial correlation) and the Hansen J-statistics for overidentifying restrictions (H0: all instruments are valid). The results confirm that there is no second order serial correlation among the error terms. The Hansen-J-statistics fails to reject the null hypothesis of over-identification restrictions, hence confirming that the instruments are valid and are robust in nature.

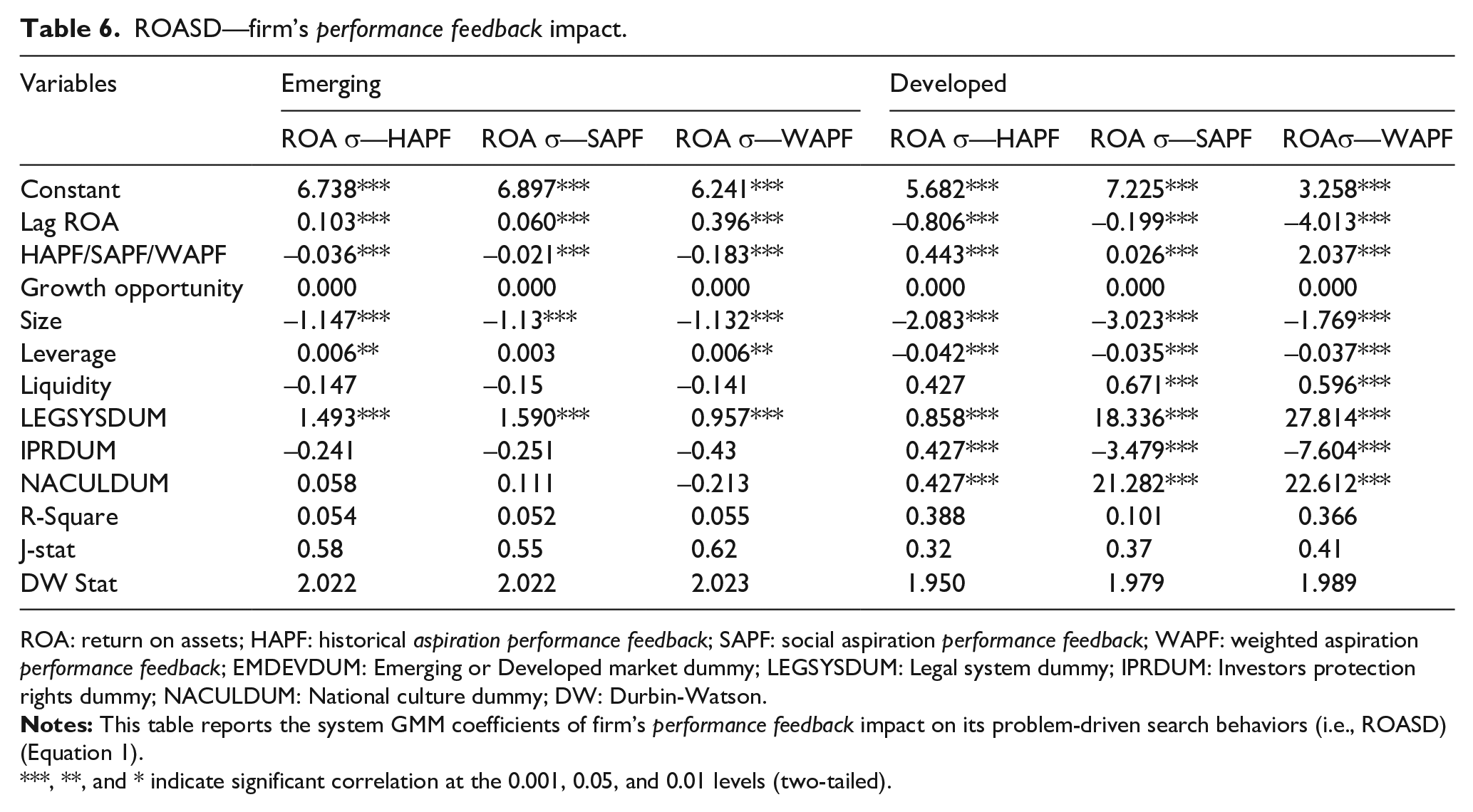

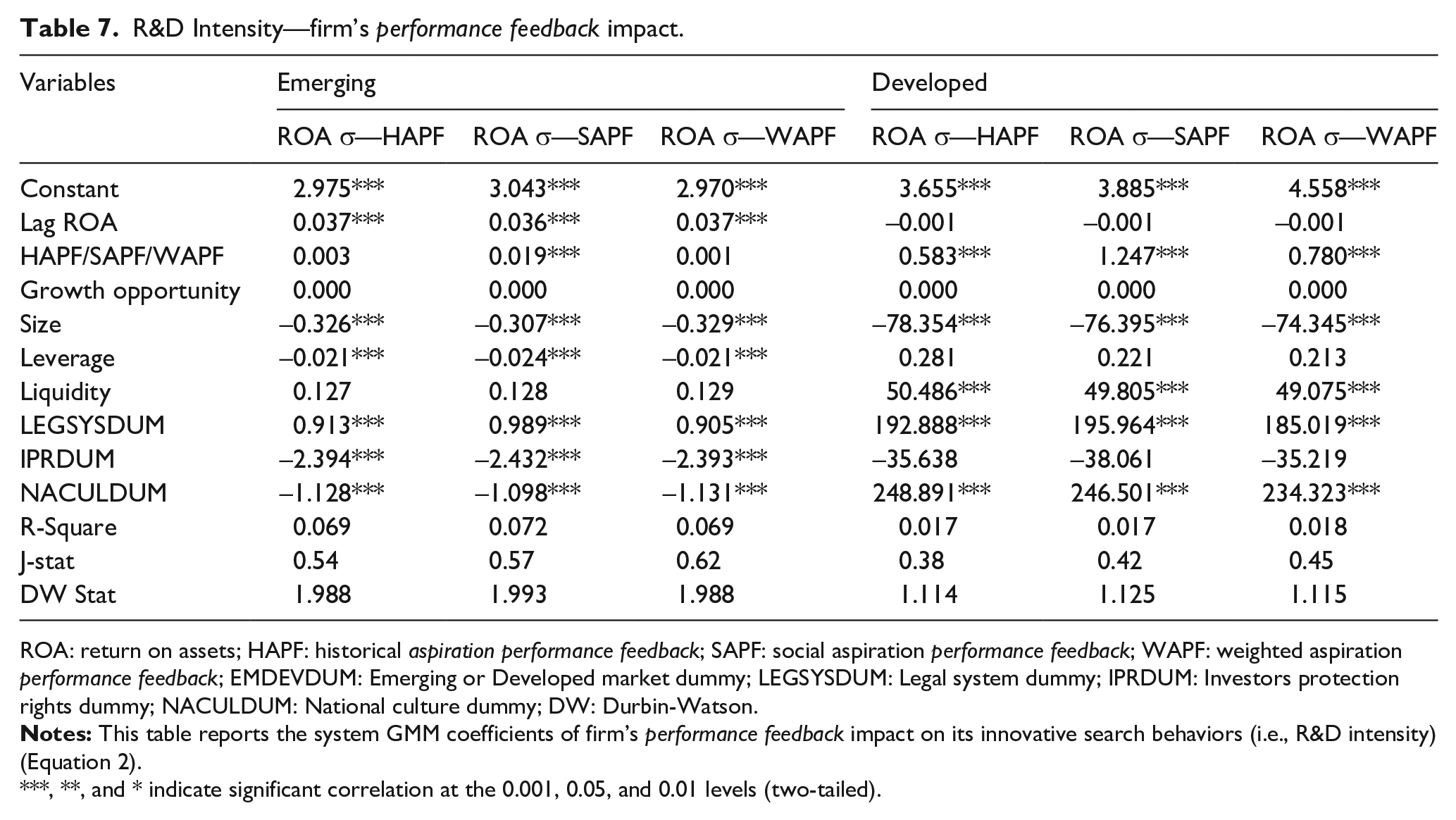

To study the performance feedback of developed and emerging market firms sample separately, we report only the generalized method of moments results of Equations 1 and 2 in Table 6 for problem-driven search behavior (i.e., ROASD) and Table 7 for innovative search behavior (i.e., R&D intensity), respectively. The results confirm that while the firm’s HAPF and SAPF influences firm’s problem-driven search behavior negatively for emerging market firms accepting our Hypothesis 1, it is positive for developing markets firms. For WAPF and problem-driven search behavior, the influence is negative for developed market firms accepting Hypothesis 1 and positive for emerging market firms. However, for the innovative search behavior (i.e., R&D intensity), the firm’s HAPF, SAPF, and WAPF has positive influence across both developed and emerging market firms accepting our Hypothesis 2. Thus, we find qualitatively similar results to problem-driven and innovative search behavior and the firm’s HA, SA, and WAs in line with our overall results.

ROASD—firm’s performance feedback impact.

ROA: return on assets; HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

R&D Intensity—firm’s performance feedback impact.

ROA: return on assets; HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

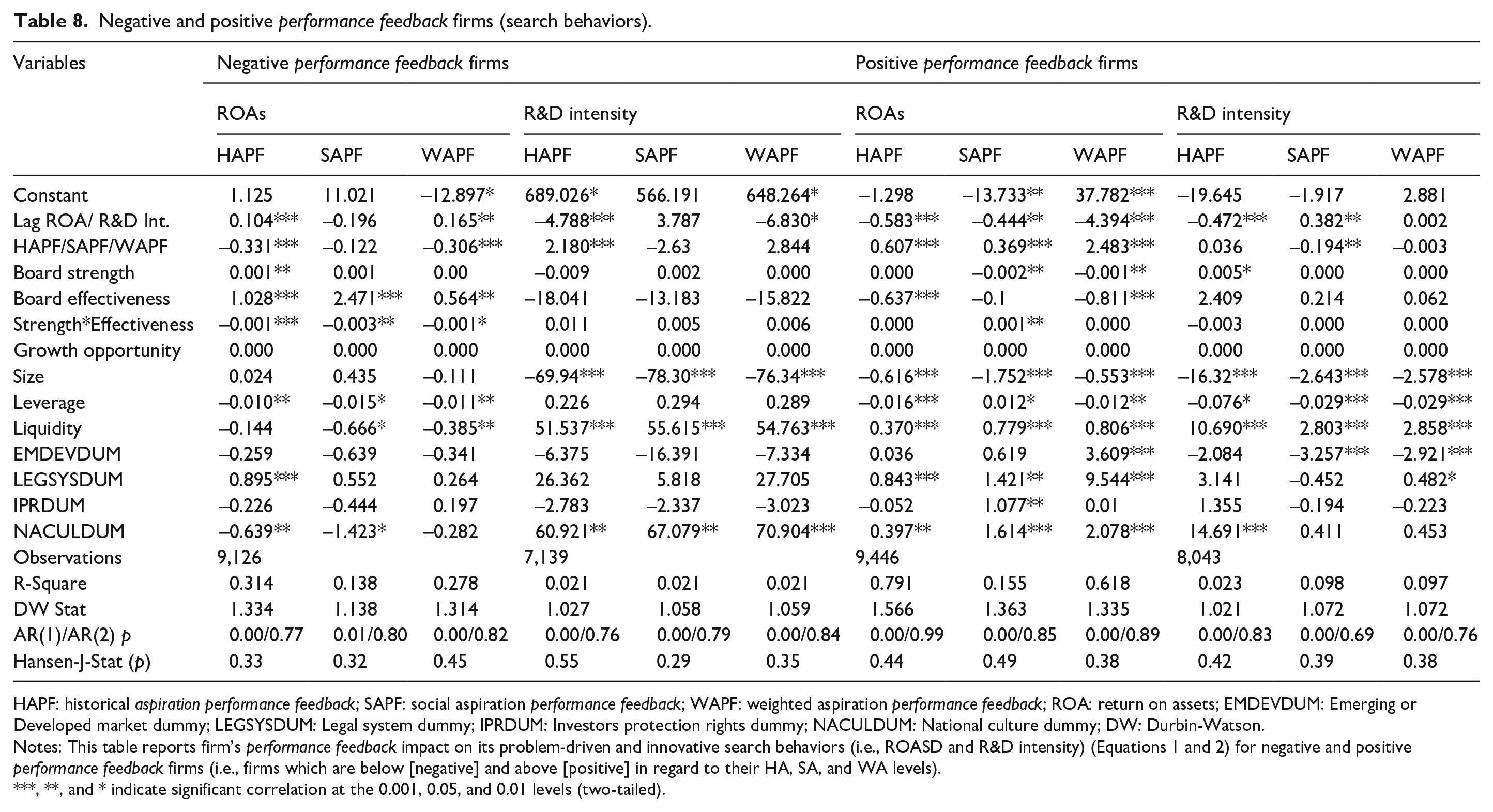

To examine the reasons behind such conflicting results under different aspiration measures driven performance feedback, we further classify our firms into positive and negative firms based on their performance feedback 9 under each of our aspiration measures. We report these results in Table 8.

Negative and positive performance feedback firms (search behaviors).

HAPF: historical aspiration performance feedback; SAPF: social aspiration performance feedback; WAPF: weighted aspiration performance feedback; ROA: return on assets; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

Notes: This table reports firm’s performance feedback impact on its problem-driven and innovative search behaviors (i.e., ROASD and R&D intensity) (Equations 1 and 2) for negative and positive performance feedback firms (i.e., firms which are below [negative] and above [positive] in regard to their HA, SA, and WA levels).

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

Intriguingly, we find that positive performance feedback firms are significantly positively impacted by their performance feedback condition to undertake more problem-driven search behaviors. On the contrary, their positive performance feedback condition has a significant negative impact on their innovative search activities. Therefore, we reject both Hypotheses 1 and 2 for these firms. On the contrary, in case of negative performance feedback firms, their performance feedback condition has a significant negative association with their problem-driven search activities. This implies that firms in this cluster which are at the bottom, that is, having an extremely negative performance feedback condition would undertake higher problem-driven search behaviors and vice versa. Our results also corroborate that firms with negative performance feedback are having a significant positive influence in undertaking innovative risk behaviors. We, therefore, accept both Hypotheses 1 and 2 only for negative performance feedback firms.

In all our models across methods, we find that previous year’s (lagged) firm performance had a negative influence on firm’s search behaviors. However, in case of firms with negative performance feedback condition, such performance has a significant positive influence on their problem-driven search activities. Growth opportunity has a significant positive impact on firm’s search behaviors. However, in case of negative performance feedback firms, we didn’t incorporate this control variable as they are fighting for survival and not pursuing growth. Large-size firms are also less interested in search behaviors. In addition, leverage has a negative impact on firm’s search activity across our results. On the contrary, liquidity is positively influencing firm’s search behaviors authenticating slack search theory. However, in case of firms with negative performance feedback, liquidity is a concern in case of problem-driven search behaviors.

In all our results, the national culture and legal systems of respective countries are strongly influencing firm’s search behaviors. Only in case of negative performance feedback firms, these are negatively influencing their problem-driven search activities which imply that it might be due to inbuilt strong legal systems and risk-averse national culture that these firms could not undertake such actions frequently.

Table 8 also reports the influence of firm-board strength on firm’s search behaviors for negative and positive performance feedback firms. We find that board strength significant positively impacts firm’s problem-driven search behaviors for negative performance feedback firms. On the contrary, for positive performance feedback firms it has a significant negative influence, however, for these firms, it further strengthens innovative search behaviors. Therefore, we accept Hypothesis 3 for both positive and negative performance feedback firms. In addition, we find that board effectiveness significant positively impacts firm’s problem-driven search behaviors for negative performance feedback firms. On the contrary, for positive performance feedback firms it has a significant negative influence; however, in case of innovative search behavior for both type firms, we didn’t find any significant influence. Therefore, overall, we accept Hypothesis 4 only for negative performance feedback firms.

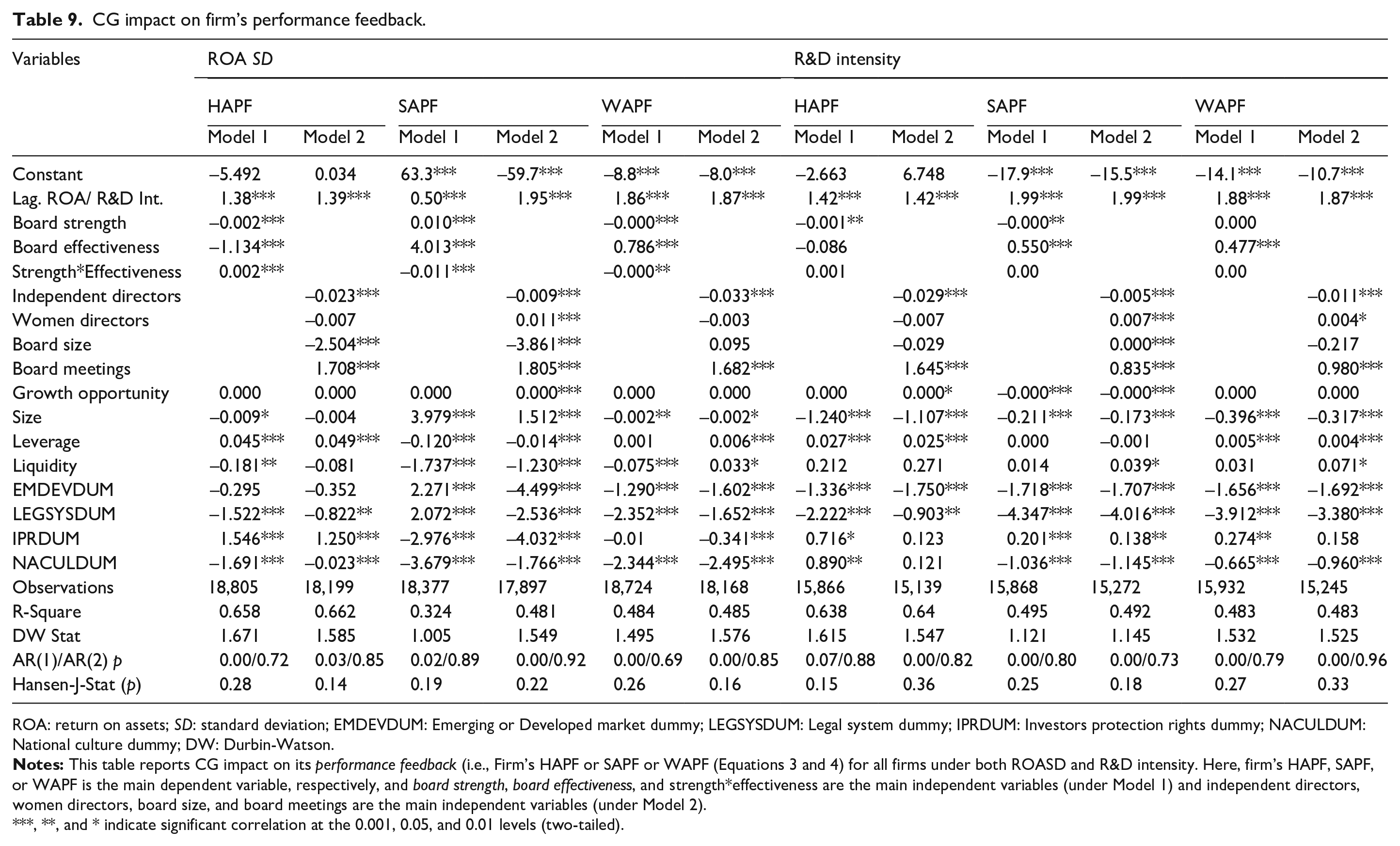

In Table 9, we report the impact of CG mechanisms on firm’s performance feedback condition in undertaking search behaviors under different aspiration measures. Interestingly, we find that board strength in a firm influences its search behaviors significant negatively by negatively impacting performance feedback condition under two of our three firm-aspiration measures. We thereby accept Hypothesis 3. Similarly, when we examine the individual elements of a firm-board strength, we find that higher presence of independent directors overwhelmingly impacts firm’s performance feedback condition significant negatively. This implies that independent boards weaken firm’s risk behaviors. On the contrary, women directors show positive influence to such performance feedback condition which drive especially firm’s innovative search behaviors. On an overall basis, we can argue that the hypothesized mediation effects of board strength on firm’s performance feedback condition in undertaking search behaviors are fully validated. In addition, we find that board effectiveness of a firm board has a positive impact on firm’s performance feedback condition to undertake both problem-driven and innovative search behaviors. Therefore, we accept Hypothesis 4. However, when we examine the individual elements of board effectiveness, we observe that board size is actually impacting firm’s performance feedback condition significant negatively in case of their problem-driven search behaviors. This implies that higher number of directors in the firm-board weaken firm’s search behaviors. On the contrary, meeting frequency results are showing overwhelming significant positive influence on firm’s performance feedback condition under our aspiration measures for both problem-driven and innovative search behaviors. So, on an overall basis, we can substantiate that the negative mediation effect of board effectiveness on firm’s performance feedback condition in undertaking search behaviors is fully evident.

CG impact on firm’s performance feedback.

ROA: return on assets; SD: standard deviation; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

Furthermore, we find from Table 9 results that board strength and board effectiveness have a significant negative influence on firm’s performance feedback condition in two out of three aspiration measures. Interestingly, the interaction effect of board strength and board effectiveness (see Table 8) positively impacts problem-driven search behaviors of positive performance feedback firms. On the contrary, it has a significant negative influence for negative performance feedback firms in line with overall results. Accordingly, we can conclude that both board strength and board effectiveness impacts can be of conflicting nature in moderating firm’s performance feedback and search behaviors relationships.

In all our results, the economic status, national culture, and legal systems of respective countries are strongly influencing firm’s search behaviors negatively. However, in case of positive performance feedback firms, both national culture and legal systems are having a positive influence toward such search behaviors.

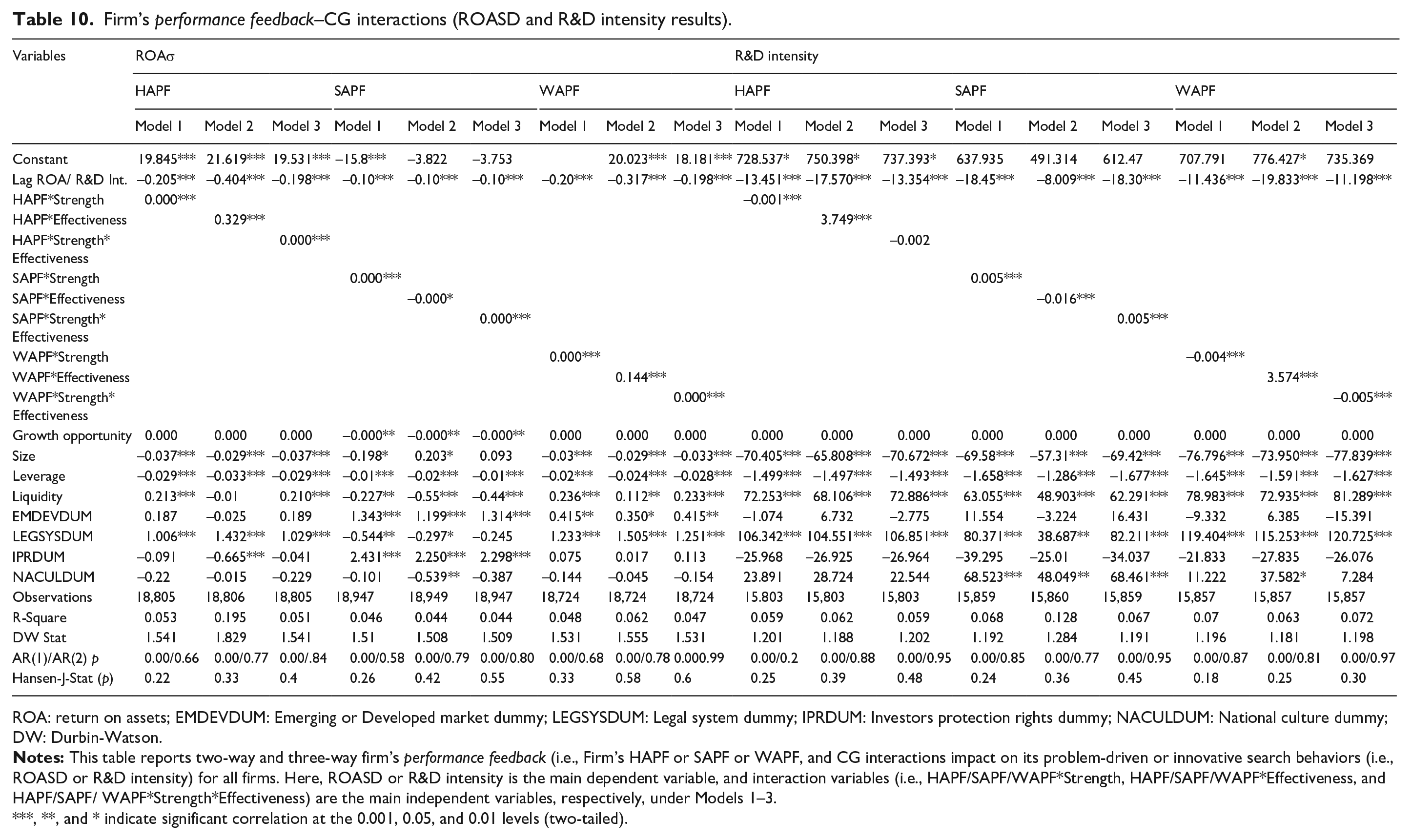

CG mediation impact on firm’s performance feedback-search behavior relationships

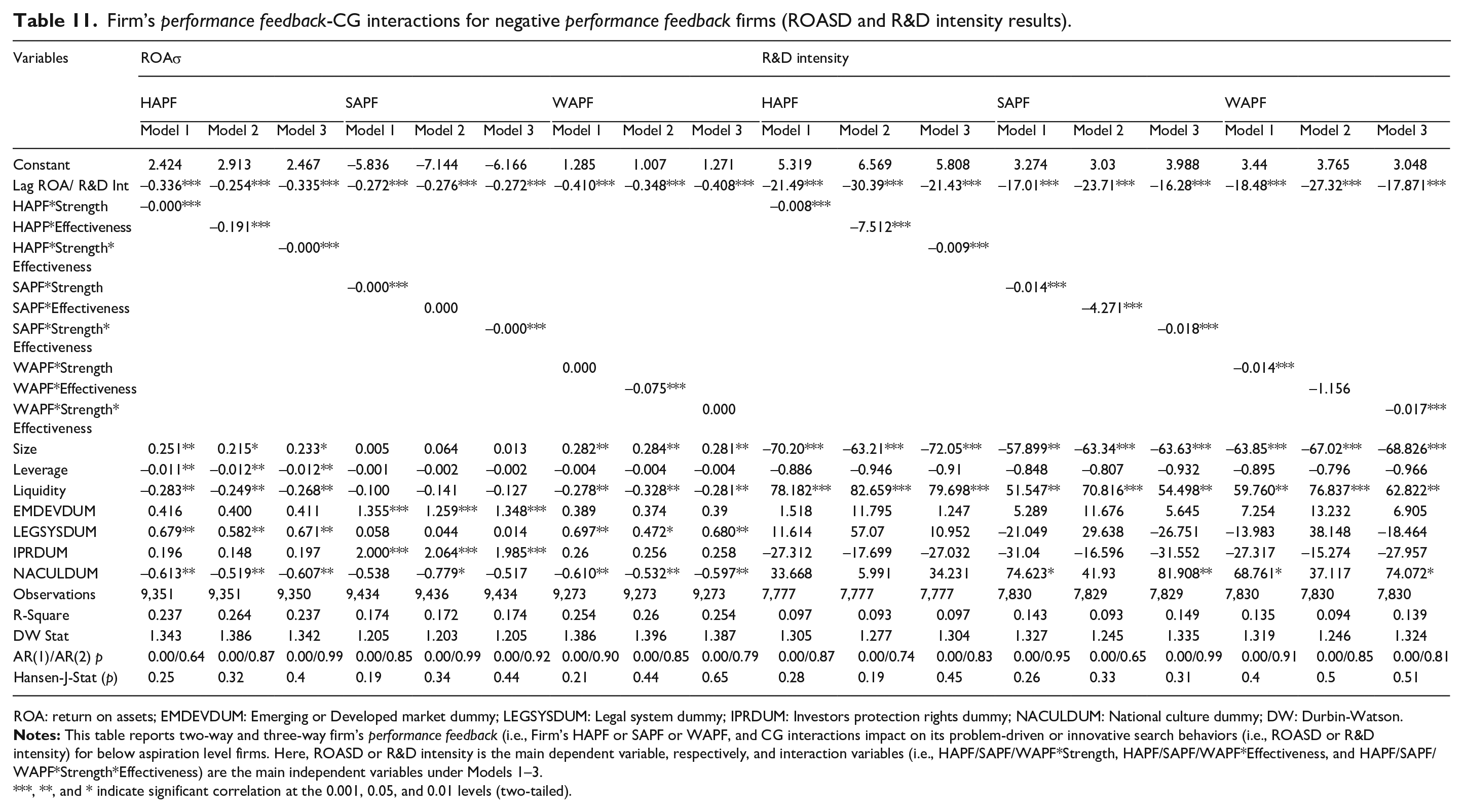

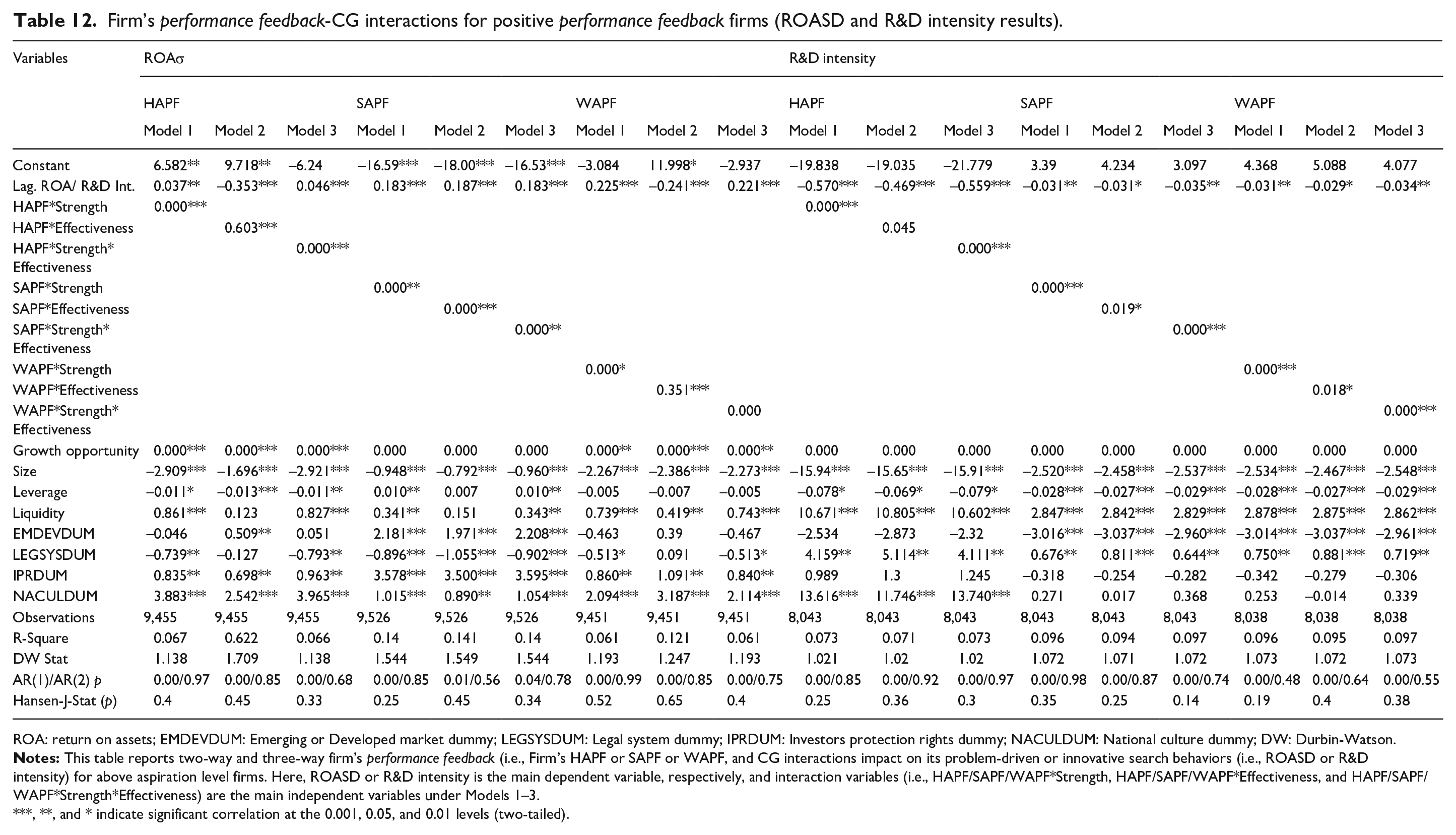

We perform two-way and three-way interaction analyses. Six variables are constructed for the two-way interaction analysis, that is, Board strength × HAPF, Board effectiveness × HAPF, Board strength × SAPF, Board effectiveness × SAPF, Board strength × WAPF, and Board effectiveness × WAPF, to further capture the effect of the CG in mediating firm’s performance feedback condition to undertake search behaviors. The results are reported in Table 8. Interestingly, under all interactions the coefficients are positive and significant for the two measures of search behaviors. It implies that both board strength and board effectiveness mediate firm’s performance feedback condition to undertake search behaviors. These results are in line with Hypotheses 3 and 4. These results are further validated by the two-way interaction results for positive and negative performance feedback firms (see Tables 10 and 11). The negative coefficients across aspiration measures for such negative firms authenticate that both board strength and board effectiveness of a firm-board moderate firm’s problem-driven and innovative search behaviors. On the contrary, for positive performance feedback firms, the positive coefficients imply that if growth opportunities prevail both board strength and board effectiveness significant positively mediate such performance feedback conditions to undertake both problem-driven and innovative search behaviors. These further validate Hypotheses 3 and 4.

Firm’s performance feedback–CG interactions (ROASD and R&D intensity results).

ROA: return on assets; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

Firm’s performance feedback-CG interactions for negative performance feedback firms (ROASD and R&D intensity results).

ROA: return on assets; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

From our three-way interaction analyses variables, that is, Board strength × Board effectiveness × HAPF, Board strength × Board effectiveness × SAPF, and Board strength × Board effectiveness × WAPF, we also report significant positive coefficients (see Tables 10–12). All these imply that CG mediates the influence of firm’s performance feedback on its search behaviors. The negative coefficients across aspiration measures under our three-way interaction results further substantiate that for negative performance feedback firms, board strength and board effectiveness of a firm-board combinedly moderate firm’s problem-driven search behaviors. For positive performance feedback firms, we report significant positive combined effect of board strength and board effectiveness, which further strengthens their innovative search behaviors.

Firm’s performance feedback-CG interactions for positive performance feedback firms (ROASD and R&D intensity results).

ROA: return on assets; EMDEVDUM: Emerging or Developed market dummy; LEGSYSDUM: Legal system dummy; IPRDUM: Investors protection rights dummy; NACULDUM: National culture dummy; DW: Durbin-Watson.

, **, and * indicate significant correlation at the 0.001, 0.05, and 0.01 levels (two-tailed).

Conclusion

The primary objective of this study was to examine how a firm’s differential performance feedback driven by its internal capabilities and external conditions propels its innovative and problem-driven search behaviors. We report that negative performance feedback positively influences firm problem-driven search behaviors, whereas positive performance feedback positively impacts innovative search behaviors. We, therefore, augment the BT (Cyert & March, 1963) and didn’t substantiate the Ansoffian (Ansoff, 1979) view of negative performance feedback firms. However, Ansoffian’s (Ansoff, 1979) ST viewpoint is exclusively evident for positive performance feedback firms in undertaking innovative search behaviors. According to us, this might be due to the internal environment, structures, and policies and also the external environment including the economic, legal, and country-specific risk-oriented national culture.

Therefore, in line with our secondary objective, we further examine how the internal CG mechanisms moderate a firm’s performance feedback condition to influence its search behaviors. We investigate the mediation impact of board strength and board effectiveness of firm boards comprising of higher percentage of independent and women directors, large board size, and higher frequency of board meetings, respectively. We find a strong negative influence of board strength whereas a significant positive influence of board effectiveness on a firm’s performance feedback condition to undertake search behaviors. More specifically, an effective firm board augments the firm’s problem-driven search behavior, but shows a mixed impact on innovative search activities under our aspiration measures. Our findings substantiate the reputation hypothesis (Pathan, 2009) and the monitoring hypothesis (Brick & Chidambaran, 2008; Pathan, 2009) for firm boards. Furthermore, we find board effectiveness through its advisory function and resource provider responsibility (De Andres & Vallelado, 2008; Erkens et al., 2012) take a catalyst role in problemistic search behaviors of negative performance feedback firms. The interactions’ impact of both board strength and board effectiveness further strengthens our above mediation impact results. These results, however, prompt us to study in-depth individual CG mechanisms’ impact on our studied associations.

On an overall basis, we find that higher independent directors’ presence on a firm board negatively mediates the firm’s performance feedback condition to undertake search activities. This proves the reputation hypothesis (Pathan, 2009) impact in our cross-country context. Similarly, we report that board size is impacting a firm’s performance feedback significantly negatively in the case of their problem-driven search behaviors. This reports the presence of diversification of opinions effect (Sah & Stiglitz, 1986, 1991) in studied firms. However, higher women directors’ presence has a significant positive influence on this action. This is due to excessive monitoring (Adams & Ferreira, 2009) that the women directors do on firms’ strategies. Also, meeting frequency results are showing a significant positive influence on a firm’s performance feedback under our aspiration measures for both problem-driven and innovative search behaviors. This is in contradiction with existing empirical evidence such as Francis et al. (2012). So, it is evident that each of these CG mechanisms has its unique mediation impact on a firm’s performance feedback condition to undertake different search activities distinctively.

The study results are also generalizable across countries as we include four emerging and four developed countries with divergent legal systems and national cultures. In all our results, the national culture and legal systems of respective countries are strongly influencing firms’ search behaviors and such performance feedback conditions. Only in the case of negative performance feedback firms, are influencing negatively their problem-driven search activities and positively their innovative search behaviors which implies that it might be due to inbuilt strong legal systems and risk-averse national culture that these firms could not undertake such actions frequently. So, these national characteristics do mediate the firm’s performance feedback condition’s impact on its search behaviors for these firms.

Theoretical, managerial, and policy implications

Overall, our findings would help the regulators and policymakers to strengthen their existing CG mechanisms and regulations as we prove that these are strong pillars of controlling firms in their search behaviors and enroot performance feedback. Accordingly, shareholders’ interests could get protected which would further mitigate the rising agency issues and corporate frauds across the world. Though we try to control most internal and country-specific characteristics and also most critical CG mechanisms in line with the existing literature, drivers such as CEO duality, executive compensation, and shareholdings pattern could have a significant bearing in our CG mediation in a firm’s performance feedback-search behavior associations.

Furthermore, firm managers can use our findings to use search behaviors in a better way in line with the existing internal and external firm-level conditions in mind. They should also understand that based on performance feedback conditions, they need to adopt their strategic behaviors, for example, if the firm falls below its aspired level, it should indulge in more conservative problemistic searches rather than exploratory or innovative searches. This finding has incrementally contributed toward the BT of the firm’s tenets. Firm managers should also cater for the internal CG mechanisms requirements and regulations in this regard. This in turn would avoid any future chances of bankruptcy for their respective firms.

However, future researchers could also look into the solutions to the above conflicts from the firm’s accounting conservatism or earnings management dimensions and/or empirically tested slack search behaviors contexts along with institutional contexts such as legal origin or national culture in-depth. This is one of the limitations of this study that we didn’t examine institutional characteristics in detail here.

Footnotes

Acknowledgements

We acknowledge the suggestions received from our peers at different points of time while preparing this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.