Abstract

This article analyzes the relationship between female directors and corporate reputation with a Spanish sample for the period 2008–2017. We also examine two background characteristics of women directors: their busyness and their educational background, suggesting that differences can exist among women according to their level of success (measured by the number of directorships) and their education. Our analyses show that female directors improve corporate reputation, but that neither women with multiple directorships nor the educational background of female directors increases corporate reputation, perhaps because stakeholders appreciate general attributes associated with women rather than the cognitive attributes of females on boards.

Introduction

Corporate reputation measures the collective judgment of an organization held by its stakeholders (Brammer & Millington, 2005). The benefits of corporate reputation (such as higher performance or better employee profile) have increased academic interest and debate regarding the factors that can influence its value (Deephouse et al., 2016). According to Gabbioneta et al. (2007), governance structure (including boards of directors) is likely to be one of the key drivers of corporate reputation because of its capacity to influence stakeholder perceptions. The composition of boards of directors is one of the main corporate governance characteristics, with many papers showing the effect of gender diversity on firm outcomes. According to the literature, the presence of women on boards is linked to lower conflicts, better boardroom discussion (Huse et al., 2009), and increased understanding of the marketplace (Robinson & Dechant, 1997) as well as an improved image of the firm through positive effects on customer behavior (Smith et al., 2006). However, the evidence regarding the effect of women directors on reputation is still scarce and inconclusive.

One of the few papers on gender diversity and reputation is the work by Bear et al. (2010), who showed that female directors increased firm reputation by enhancing corporate social responsibility (CSR) strength ratings. Previously, Brammer et al. (2009) also found that female directors have a reputational effect, but only in those sectors that operate close to final consumers. However, Miller and Triana (2009) did not find any relationship between board gender diversity and corporate reputation, although they did find a connection between racial diversity and reputation. These papers are based on data from Anglo-Saxon countries and are dated from a period of time where recommendations and quotas were not common and awareness regarding gender equality in society was less prominent.

Whereas previous studies have examined the mere presence of women directors without analyzing differences among females, this article also studies whether the appointment of “specific female directors” can be considered as signals to the market that have reputational effects. According to the concept of gender diversity, more focused on the perspectives of “skill” than “representation,” women may bring different skills, viewpoints, expertise, and knowledge, therefore their effects on firms may be different. In this respect, recent literature on board composition emphasizes the differences among board members in socioeconomic, professional, and educational backgrounds (van der Walt & Ingley, 2003). Following the signaling theory, we note that since gender board quotas are only one type of quota, other visible diversity traits (e.g., educational and professional background) should be also examined as they are important signals to the market (Terjesen et al., 2009). This fact, together with inconclusive evidence, leads us to the necessity for further and more in-depth research.

The primary purpose of our article is to shed light on the following questions: (1) Do stakeholders value the appointment of women directors? (2) Are the education and professionalization of these women considered visible signals by stakeholders? Hence, using the signaling theory, we first analyze the role of gender diversity on firm reputation. In a second step and still under the signaling theory, we go beyond the surface of gender diversity and examine two background characteristics of women directors that can be also relevant signals to gain reputation: female busyness and female educational background, suggesting that the appointment of busy women directors and those with a high educational profile can be positively valued by stakeholders. These research questions are examined with a Spanish sample for the period 2008–2017.

We focus on Spain; an interesting setting for several reasons. First, the 2007 Spanish Gender Equality Act stated the recommendation to reach quotas of 40% by 2015 for publicly traded firms with more than 250 employees. Then, Spain is one of the first European countries that recommended specific quotas for female directors in listed firms and with several corporate governance codes with recommendations regarding gender diversity. Despite the figures are still under the aims (in 2017, there were still 18% of listed companies with no women on their boards and the average of non-executive women directors was 22%), the growth of female directors by Spanish firms has been noticeable. However, because the Spanish law was a soft law with no sanctions in case of no compliance, many think that the main reason to appoint females directors by Spanish listed firms has been to accomplish social legitimacy and gain reputation among the public. Second, in contrast to the Anglo-Saxon capital markets, Spain’s capital markets are characterized by high ownership concentration and a low investor protection level, where the board of directors is the prevalent mechanism of control (García-Meca et al., 2017). Finally, in Spain, there is a reputational index comparable to other measurements of reputation published in top journals, such as Fortune (Delgado-García et al., 2010). Therefore, analyzing the incidence of gender diversity in the reputation of firms established in a country with soft-law gender quotas, high ownership concentration, and low investor protection makes this research interesting and valuable.

Our results provided by logit regressions evidence a significant effect of female directors on reputation, confirming the signaling theory, but we do not find differences on the effect that women directors have on corporate reputation according to their educational profile or busyness. This study contributes to the existing literature in several ways. First, it adds evidence to the very scarce literature analyzing the impact of gender diversity on firm reputation (e.g., Bear et al., 2010; Brammer et al., 2009; Miller & Triana, 2009). Second, we contribute to the relevance of the signaling theory on gender diversity studies, noting that one of the main reasons to appoint female directors by Spanish companies is the visible signal to the market because of their effects on firm reputation among stakeholders. Third, we further contribute to the gender diversity literature by examining specific attributes of female directors, delving into the question of whether stakeholders value female differences in personal styles, skills, and business knowledge when women are on boards.

Theoretical framework and hypotheses

Based on Fombrun and Shanley (1990), corporate reputations “represent the public’s cumulative judgments of firms over time” (p. 235). Companies are likely to have as many reputations as there are distinct stakeholder groups, and for this reason, Bromley (2002) indicates that surveys with large and heterogeneous samples of respondents portray a “meta-reputation.” Therefore, the concept of reputation derived from a survey like that of Fortune mostly reflects the reputation of an organization’s effectiveness (Brammer et al., 2009) since it is basically an overall index of success.

Managers try to influence other stakeholders by signaling their firms’ outstanding advantages compared to those of competing firms (Fombrun & Shanley, 1990). Companies try to signal their salient characteristics to maximize their reputation. At this point, the role of boards is crucial since they monitor management activities and strategies and provide resources to the firm. Effective monitoring may improve firm performance (Hillman & Dalziel, 2003), thereby enhancing corporate reputation.

Diversity within organizations has also been the subject of great attention among researchers. Diversity can be addressed from the demographic (observable) and from the cognitive (non-observable) dimensions. Following van der Walt and Ingley (2003), “the concept of diversity relates to board composition and the varied combination of attributes, characteristics, and expertise contributed by individual board members in relation to board process and decision-making” (p. 219). Demographic diversity is based on detectable attributes, such as race, gender, or age, while cognitive ones relate to education, technical skills, and occupational or functional background.

In this study context, Spain is a civil law country with a high ownership concentration, a lack of liquidity and a legislative framework attempting to improve the corporate governance of listed firms (García-Meca et al., 2017; Ruiz-Mallorquí & Santana-Martín, 2009). In countries with poor investor protection, companies need a strong reputation to raise funds (La Porta et al., 2000). In this situation, the presence of women on the boards frequently may not be effective because of the weakness of corporate control. However, controlling shareholders may try to improve firm reputation signaling the presence of female directors.

Byron and Post (2016) indicate that female board representation is likely to be associated with strategic decisions for a wider range of corporate stakeholders. Both a male and a female stereotype exist. Traits associated with males are aggressiveness, ambition, dominance, or independence, whereas femininity is associated with compassion, sensitivity to the needs of others, understanding, and warmth (Eddleston & Powell, 2008). Accordingly, Brammer et al. (2009) contend that female directors may influence the perceptions of external agents about a board’s functioning more effectively. Miller and Triana (2009) suggest that diverse boards may signal that the firm is well-positioned to succeed in a diverse market and will be able to advise the firm executives effectively. We can also expect that individuals high in femininity in the boardroom favor relationships with stakeholders, such as employees and customers (Daily et al., 1999; Singh & Vinnicombe, 2004). Through board diversity, firms signal effective interaction with markets in the hope of enhancing their firm’s reputation.

In the same way, as indicated by van der Walt and Ingley (2003), board diversity is associated with the idea of being a good corporate citizen, being seen as non-discriminating and complying with diversity norms. Organizations working within the rules gain legitimacy and ultimately, reputation (Miller & Triana, 2009). Thus, diverse boards are useful for signaling support for women. As Bernardi et al. (2002) find that companies with higher percentages of female directors are more likely to display their pictures in their annual reports, this implies support for the argument of signaling. Thus, the presence of female directors may improve the perceptions of external constituents to the extent that firms show adherence to norms and support for women. Consequently, diverse directors can enhance corporate reputation through signaling the attractiveness of the firm. In summary, we hypothesize:

H1: Board gender diversity improves corporate reputation.

There is a debate on the costs and benefits of individuals holding multiple board seats. Ferris et al. (2003) call the hypothesis that predicts that serving on multiple boards might over commit an individual the busyness hypothesis. As a consequence, they posit that individuals with multiple directorships might shirk their responsibilities, thereby reducing their monitoring of management and, as a result, the value of the firm. As indicated by Fich and Shivdasani (2006), several studies show that the number of boards that outside directors sit on is linked to the performance of the firms, although too many directorships may lower the effectiveness of outside directors. However, Jiraporn et al. (2009) have created the term reputation hypothesis to refer to the advantages that multiple directorships provide in developing managerial expertise. In this context, Perry and Peyer (2005) indicate that when executives have strong incentives, outside directorships can enhance firm value, possibly through learning or networking opportunities or through the signaling of managerial quality. Therefore, whereas academic literature uses the number of board seats held by outside directors as a proxy for director reputation (Shivdasani, 1993; Vafeas, 1999), other research indicates that busy outside directors weaken firm performance (Core et al., 1999; Fich and Shivdasani, 2006).

In the case of female directors, while women directors serving on multiple boards may neglect their monitoring functions, the presence of busy female directors may be more clearly perceived as a signal of reputation. Directorships provide status and visibility, that is, “saliency” in the business community (Hillman et al., 2002). Female directors already serving on a corporate board demonstrate a certain level of expertise, novelty, and increased attractiveness for subsequent directorships. They can also provide a valuable network, which along with their communicative advantages and specific leadership style can favor firm outcomes. Consequently, firms attempting to gain reputation and credibility by being receptive to diversity (Bernardi et al., 2002) may select female directors serving in other companies (successful women) to benefit from their salience and their expertise and the perception that there is no “lack of fit” for directorships.

In sum, hiring successful female directors may be a signal to highlight that company is especially well prepared to face the challenge of diverse markets at the same time that it respects women’s rights. Thus, the question we ask ourselves is not whether women with multiple directorships further increase firms’ reputations with respect to male directors, but if the differences in reputation after the appointment of female directors are conditioned by their success, measured by their holding of multiple board seats. Therefore, we pose the following hypothesis:

H2: Busy women directors improve corporate reputation.

Recent studies suggest that not all women directors are equally good advisors or monitors and that several characteristics of women directors can have greater importance. One of these attributes is related to educational background. In this respect, the European Commission calls for a more professional board of directors to ensure the board’s understanding of the firm’s financial objectives, the complexities of global markets, and the impact of the business on different stakeholders (European Commission, 2011). Educational level provides information about a person’s knowledge, skill base, cognitive preferences, and values (Hambrick & Mason, 1984). According to Lewis et al. (2014), differences in education arise not only because of the training provided by the education itself (i.e., MBA) but also due to selection bias (i.e., who chooses to get an MBA degree). In this regard, prior research suggests that the educational background of firm executives influences firm outcomes, such as firm performance or innovation (Finkelstein et al., 2009). Findings also confirm that CEOs with MBAs are more likely to increase voluntary environmental disclosure to enhance corporate environmental reputation and legitimacy (Lewis et al., 2014).

Very few scholars have addressed how educational background can influence the role of women directors and their effect on firm outcomes, but women’s effects can be influenced by individual differences in personal styles, skills, connections, and business knowledge (Hambrick & Mason, 1984). According to Adams and Ferreira (2009, p. 297), the mere presence of female directors on boards is not sufficient to have an impact on business decisions, but board gender diversity has to include a qualified board. Consequently, women directors should not be considered to be a homogeneous group. It is necessary to consider differences among them according to their human and social capital (i.e., level of education). We assume, according to the resource dependence view, that women directors with high qualifications provide the company with valuable resources related to their greater level of “human capital.” In particular, women with high educational backgrounds are more skilled and can possess a greater ability to recognize opportunities and take advantage of them (Geletkanycz & Black, 2001). They can also possess a greater ability to consider new ideas and the capacity to process information (Hsu et al., 2013). Therefore, stakeholders can value the appointment of these directors because they are able to anticipate industry conditions, evaluate risk, and overcome information challenges. With respect to the signaling theory, hiring female directors with a high educational profile can also be a signal of firm sensitivity to the needs and requirements of particular stakeholders (Daily et al., 1999). Regarding the latter, the hiring of women with high educational profiles can be a signaling factor that significantly conditions the opinion of stakeholders and, therefore, affects a firm’s reputation by overcoming the constraints related to the hiring of women directors motivated by quotas or mere public image. The appointment of these women can enhance the perception that female directors provide valuable resources that help corporate decision-making due to their specific knowledge.

Therefore, we consider that although the mere presence of women can be enough to improve a firm’s reputation, stakeholders’ perceptions of the company can be enhanced by the appointment of “highly qualified” female directors. According to the above arguments, women directors with advanced degrees may provide unique attributes to firms that can enhance the effectiveness of the board of directors. This appointment can be also used by the firm as a visible signal among the public to improve its image and reputation due to the company can be seen as well-positioned to meet market needs. Thus, we hypothesize:

H3: Highly educated women directors improve corporate reputation.

Research methodology

Sample selection and data sources

This study focuses on 141 non-financial firms listed on the Spanish stock market to examine the relationship between female directors and corporate reputation for the period 2008–2017. All financial firms have been excluded from the sample due to the fact that they are under special scrutiny by financial authorities, which constrains their directors’ role, and also because their accounting information is not comparable to the rest of the firms in the sample (García-Meca et al., 2017; López-Iturriaga et al., 2015). We also eliminate the firms whose financial or board data are not available. The final sample is based on three data sources. First, it is based on the Spanish Monitor of Corporate Reputation 1 ranking (MERCO) to identify the most reputable companies. Second, the financial and accounting information comes from the SABI 2 database, which comprises general information and contains data from the financial statements included in the Spanish Companies Registration Office of over 2 million Spanish companies and more than 500,000 Portuguese companies. Finally, we focus our research on board characteristics with data which were hand-collected not only from the web page of the Spanish National Stock Market Commission (CNMV) but also through corporate websites. The final sample consists of an unbalanced panel of 1,240 firm–year observations. 3

Methodology

To study the effects of our independent variables on company reputation, and due to the fact that we are dealing with a binary dependent variable, we base our analysis on a logistic specification to determinate the probability of companies being included among those most reputable. However, this procedure can provide biased estimates in the presence of omitted firm-specific variables (Hsiao, 2014). It is for this reason that ex post, a logistic regression with fixed effects is presented, which is robust to the presence of unobservable individual heterogeneity, avoiding biased results (Fich & Shivdasani, 2006).

After this, and with the main aim of addressing selection effects and reducing the degree of observable heterogeneity between the firms included in and those outside of the MERCO ranking, we use the nearest neighbor technique of the propensity score matching (PSM) procedure (Heckman et al., 1998).

In all the cases, the variables have been lagged by 1 year to avoid endogeneity problems (Chen et al., 2017).

Data description

Dependent variable: corporate reputation

Our dependent variable is corporate reputation (Reputation). It is a dummy variable which indicates if the company is included in a yearly ranking of the 100 most highly reputed firms in Spain. These companies are determined using the firms comprised in the Spanish Monitor of Corporate Reputation, which is the only monitor which annually evaluates the reputation of Spanish firms, creating a reference in terms of the assessment and the management of their reputations (Fernández & Luna, 2007). It has often been used in previous research (Delgado-García et al., 2010, 2013; García-Meca & Palacio, 2018; Sánchez & Sotorrío, 2007).

To create the ranking, a market research institute collects data from a sample of managers of large companies who are asked to answer a questionnaire. It evaluates six dimensions (economic and financial results, quality of product/service, internal reputation or talent, ethics and CSR, international dimension of the company, and innovation), which are averaged into an overall reputation score for each company. Based on these responses, a provisional ranking of firms is drawn up and only the 100 companies with the highest scores are evaluated by experts (financial analysts, consumer associations, NGOs, influencers, economics and business professors, among others). A final evaluation is carried out by analysis and research technicians who, by means of a merit questionnaire, verify the reputation attributed to each company, following criteria approved by the main indexes, such as the Dow Jones Sustainability Index or the Global report Initiative. A maximum of 10,000 points is given to the top company in the ranking and the bottom one receives a maximum value of 3,000 points.

To prevent our final study sample from being limited, we base our study on a sample consisting of all the companies included in the Spanish National Stock Market Commission (CNMV), where the dependent variable is a dummy variable taking the value 1 if the company is included in the MERCO ranking and 0 otherwise.

Independent variables

Based on previous results (Campbell & Minguez-Vera, 2008), we define Women as the percentage of women sitting on boards, calculated as the number of female directors divided by the total number of directors.

The variable Education represents the proportion of women on the board who have completed post-graduate studies. Research suggests differences in decision-making between executives with MBAs and executives without MBA degrees (Finkelstein et al., 2009).

Busy women directors measure the proportion of women on the board who work for several boards. Specifically, they are considered to be busy if they serve on three or more boards (Benson et al., 2015).

Control variables

To avoid biased results, we control for a number of factors whose effect on corporate reputation has been well established by previous literature and allows us to ensure the validity of the relation between our variables.

Firm size (Size) is the logarithm of total assets of the company. Large companies undergo continuous examination by their stakeholders, so they clearly have to make an effort to maintain and improve their reputation (Cordeiro & Sambharya, 1997; Dunbar & Schwalbach, 2000; Roberts & Dowling, 2002).

Following Brammer et al. (2009), return on assets (ROA) is calculated as the proportion of operating income before interest and taxes, divided by total assets. It shows how the firm is able to generate earnings with its available assets. As explained in previous research (see Delgado-García et al., 2010), when a firm is able to achieve a higher value, the possibilities of satisfying future demands of stakeholders increase. Stakeholders will use previous firm performance to estimate future performance, and a higher expected value will lead them to presume the satisfaction of their interests. It is expected to affect corporate reputation in a positive way.

Financial leverage (LEV) is measured by the ratio of total debt to total assets (Brammer et al., 2009). Since leverage is an indicator of a firm’s risk, previous research predicts a positive association between leverage and insolvency risks (Brammer & Millington, 2005), which impacts negatively on corporate reputation.

Board size (Bsize) is measured as the natural log of the number of directors serving on the board during the year (Benson et al., 2015). In previous literature, board size has been associated with corporate reputation in a positive way (Musteen et al., 2010) because it is considered to be an important indicator of firm quality. A larger board size is more desirable since it provides board members with more opportunities to connect with external knowledge, skills, and networks (Forbes & Milliken, 1999; Rhee & Lee, 2008).

Duality means that the company CEO also holds the board chairperson position (Michelon & Parbonetti, 2012). It is measured as a dummy variable that equals 1 if the CEO is also the chairman of the board and 0 otherwise. Duality is often associated with weak governance. According to the institutional theory, a negative relationship between CEO duality and corporate reputation can be expected (Musteen et al., 2010).

Ownership concentration (Ownership) is measured as the total percentage of shares controlled by the largest and second largest shareholders. Previous research finds that corporate reputation is negatively affected when the largest shareholder has a high proportion of ownership concentration (Delgado-García et al., 2010).

Finally, we control for industry, year, and firm-specific fixed effects using dummy variables. Table 1 presents the variable definitions.

Variable definition.

LEV: leverage; ROA: return on assets.

Accordingly, to study the impact of female board member characteristics on corporate reputation, we estimate the following baseline model

where the firm is represented by i, the time period is denoted as t, and ε it is the random error for each observation (Pindado & Requejo, 2015).

Results

Descriptive statistics

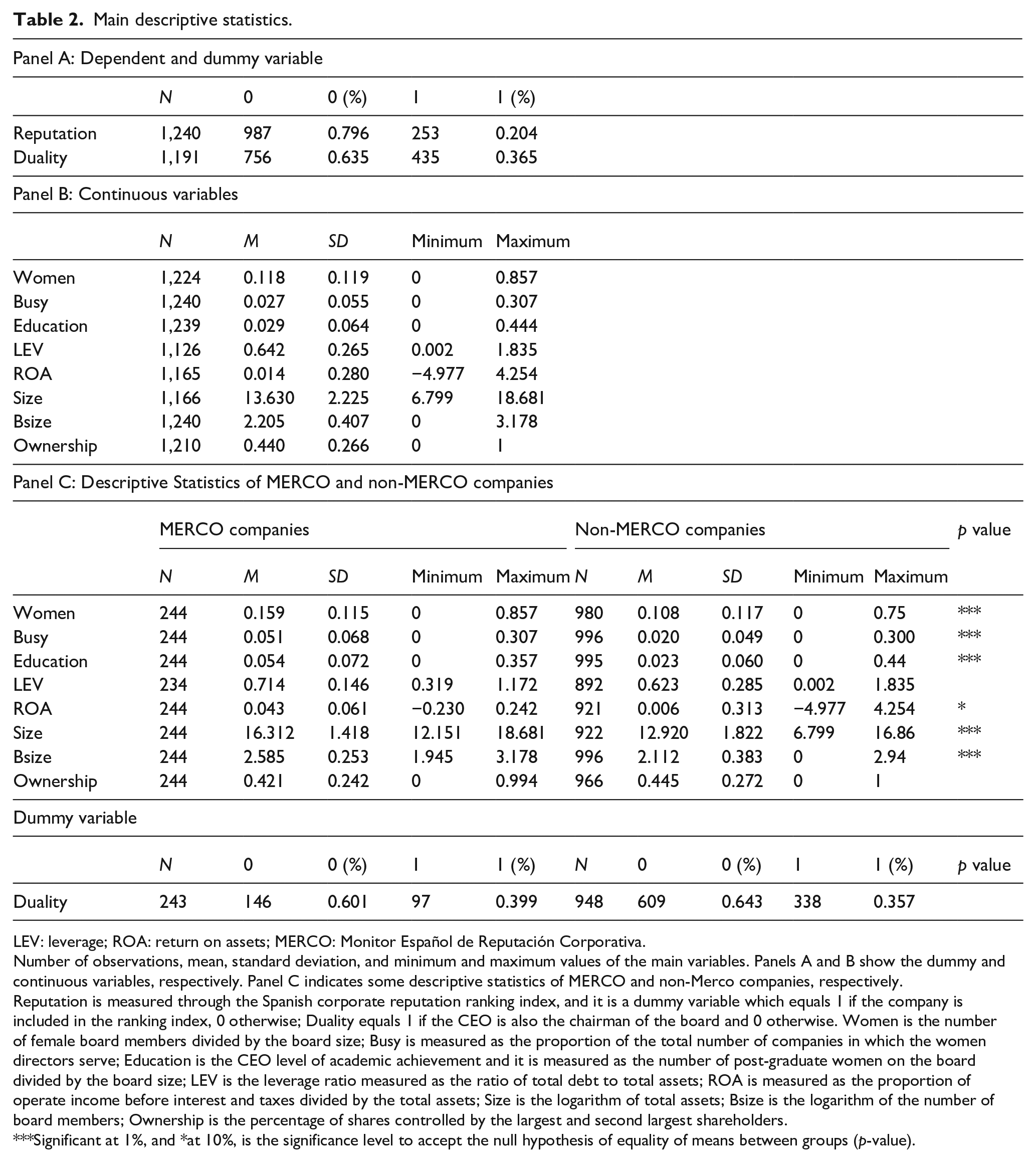

The descriptive statistics of the main variables are reported in Table 2. Panel A shows the values of the dependent and the dummy variables. The results show that 20.4% of the observations in our sample are included in the MERCO ranking (Reputation) and 36.5% of the directors in the sample are also chairmen of the board (Duality). Panel B shows the continuous variables. The mean percentage of women on boards is 0.118. However, 0.027% corresponds to Busy and 0.029% is the post-graduate women percentage (Education). The LEV mean is 0.642 and the ROA is 0.014. Company size, expressed in a logarithm of total assets, is 13.630 and the board size, expressed in a logarithm, is 2.205 members. Finally, ownership presents a mean of 44%. Panel C shows the descriptive statistics for companies included and not included in the MERCO ranking, respectively. It shows that MERCO companies present a higher number of women and busy women. In general, they are larger than non-MERCO companies, which can be translated into higher leverage, ROA, and board size. Mean difference tests are also run. The results show that both groups are not homogeneous, as there are differences between almost all the variables.

Main descriptive statistics.

LEV: leverage; ROA: return on assets; MERCO: Monitor Español de Reputación Corporativa.

Number of observations, mean, standard deviation, and minimum and maximum values of the main variables. Panels A and B show the dummy and continuous variables, respectively. Panel C indicates some descriptive statistics of MERCO and non-Merco companies, respectively.

Reputation is measured through the Spanish corporate reputation ranking index, and it is a dummy variable which equals 1 if the company is included in the ranking index, 0 otherwise; Duality equals 1 if the CEO is also the chairman of the board and 0 otherwise. Women is the number of female board members divided by the board size; Busy is measured as the proportion of the total number of companies in which the women directors serve; Education is the CEO level of academic achievement and it is measured as the number of post-graduate women on the board divided by the board size; LEV is the leverage ratio measured as the ratio of total debt to total assets; ROA is measured as the proportion of operate income before interest and taxes divided by the total assets; Size is the logarithm of total assets; Bsize is the logarithm of the number of board members; Ownership is the percentage of shares controlled by the largest and second largest shareholders.

Significant at 1%, and *at 10%, is the significance level to accept the null hypothesis of equality of means between groups (p-value).

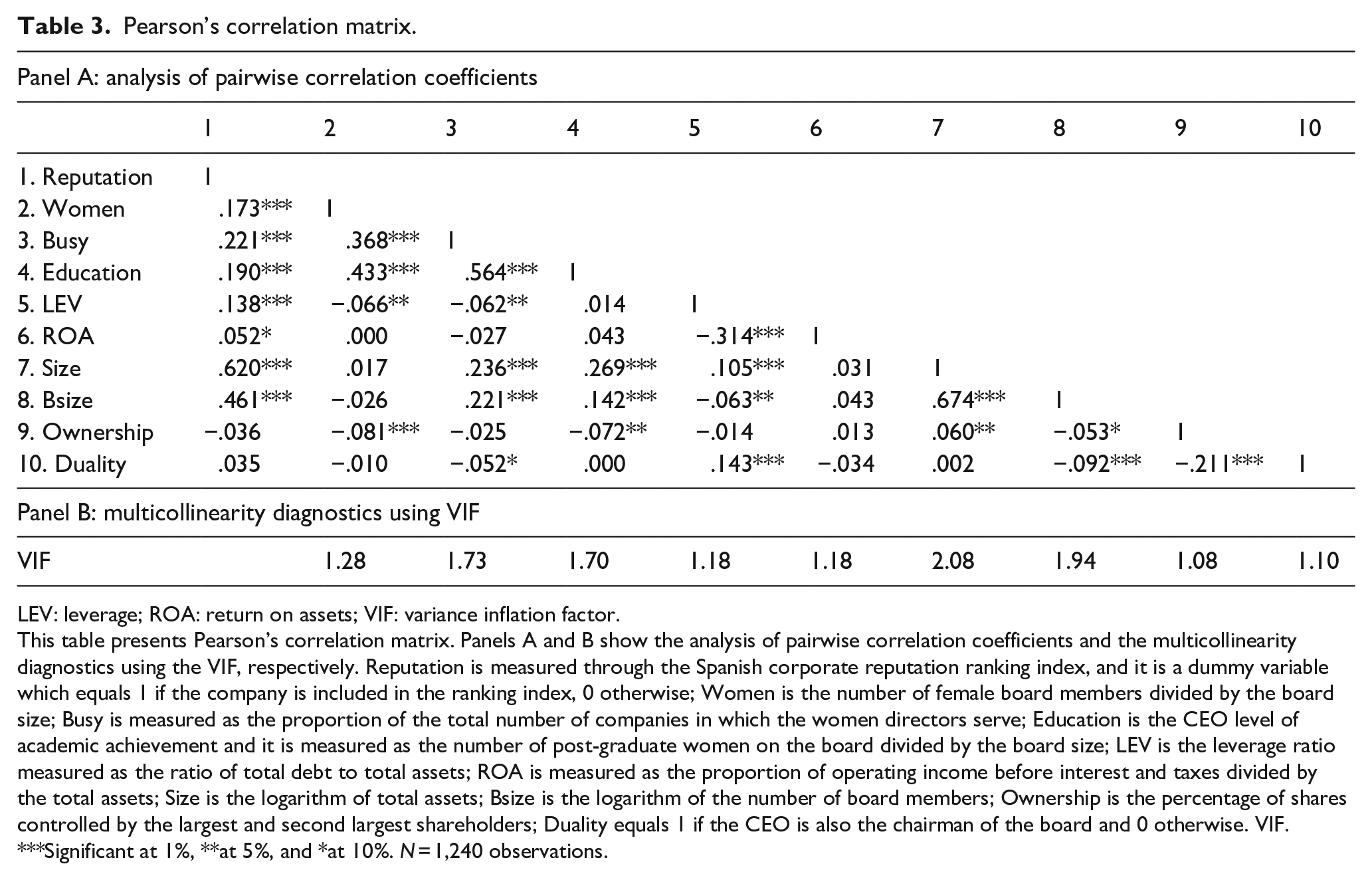

Table 3 presents the Pearson correlation matrix to test for multicollinearity. The correlation between the pairs is low and not significant. None of the correlation coefficients is high enough (>.80). In addition, we perform the variance inflation factor (VIF), which measures the degree to which the explanatory variables are explained by other explanatory variables. We notice that all VIFs are below 10, which is the traditional rule of thumb value (Cohen et al., 2003). Accordingly, we conclude that the models are free of multicollinearity problems. 4

Pearson’s correlation matrix.

LEV: leverage; ROA: return on assets; VIF: variance inflation factor.

This table presents Pearson’s correlation matrix. Panels A and B show the analysis of pairwise correlation coefficients and the multicollinearity diagnostics using the VIF, respectively. Reputation is measured through the Spanish corporate reputation ranking index, and it is a dummy variable which equals 1 if the company is included in the ranking index, 0 otherwise; Women is the number of female board members divided by the board size; Busy is measured as the proportion of the total number of companies in which the women directors serve; Education is the CEO level of academic achievement and it is measured as the number of post-graduate women on the board divided by the board size; LEV is the leverage ratio measured as the ratio of total debt to total assets; ROA is measured as the proportion of operating income before interest and taxes divided by the total assets; Size is the logarithm of total assets; Bsize is the logarithm of the number of board members; Ownership is the percentage of shares controlled by the largest and second largest shareholders; Duality equals 1 if the CEO is also the chairman of the board and 0 otherwise. VIF.

Significant at 1%, **at 5%, and *at 10%. N = 1,240 observations.

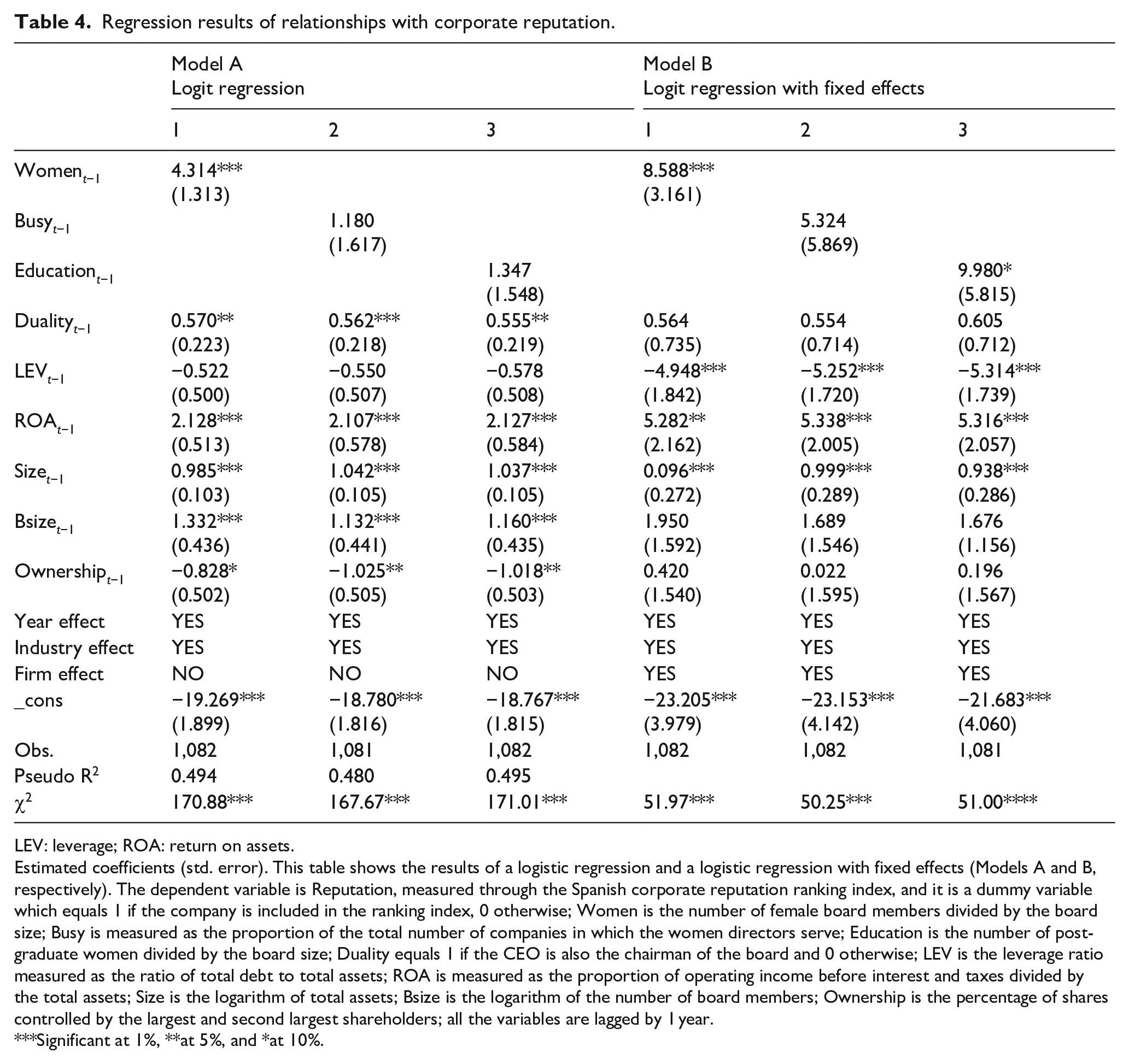

Regression results

Table 4 presents the results for the regressions explaining company reputation, measured as a dummy variable. Models A and B present an ordinary least squares (OLS) logit regression and a logistic regression with fixed effects, respectively, with all the variables lagged by 1 year to avoid endogeneity concerns. Both models show a positive and significant relationship between the proportion of women directors on boards and corporate reputation, confirming that demographic diversity has a positive influence which enhances corporate reputation (Brammer et al., 2009).

Regression results of relationships with corporate reputation.

LEV: leverage; ROA: return on assets.

Estimated coefficients (std. error). This table shows the results of a logistic regression and a logistic regression with fixed effects (Models A and B, respectively). The dependent variable is Reputation, measured through the Spanish corporate reputation ranking index, and it is a dummy variable which equals 1 if the company is included in the ranking index, 0 otherwise; Women is the number of female board members divided by the board size; Busy is measured as the proportion of the total number of companies in which the women directors serve; Education is the number of post-graduate women divided by the board size; Duality equals 1 if the CEO is also the chairman of the board and 0 otherwise; LEV is the leverage ratio measured as the ratio of total debt to total assets; ROA is measured as the proportion of operating income before interest and taxes divided by the total assets; Size is the logarithm of total assets; Bsize is the logarithm of the number of board members; Ownership is the percentage of shares controlled by the largest and second largest shareholders; all the variables are lagged by 1 year.

Significant at 1%, **at 5%, and *at 10%.

Results in Column 2 of both models present a positive but not significant relationship between busy women directors and corporate reputation. This indicates that cognitive diversity of women directors measured as the appointment of women serving on multiple boards does not imply a contribution to a company’s reputation.

However, in the last column of Model B, we can appreciate a mild positive effect of the high educational profile of women directors and firm reputation, which suggests that the higher educational level of women directors can influence firm outcomes, such as its reputation (Finkelstein et al., 2009).

With regard to the control variables, ROA and Size present positive and significant signs, as expected. These results also note that larger companies, and those with high returns on assets, present positive effects on corporate reputation. The opposite effect is presented for the remaining control variables.

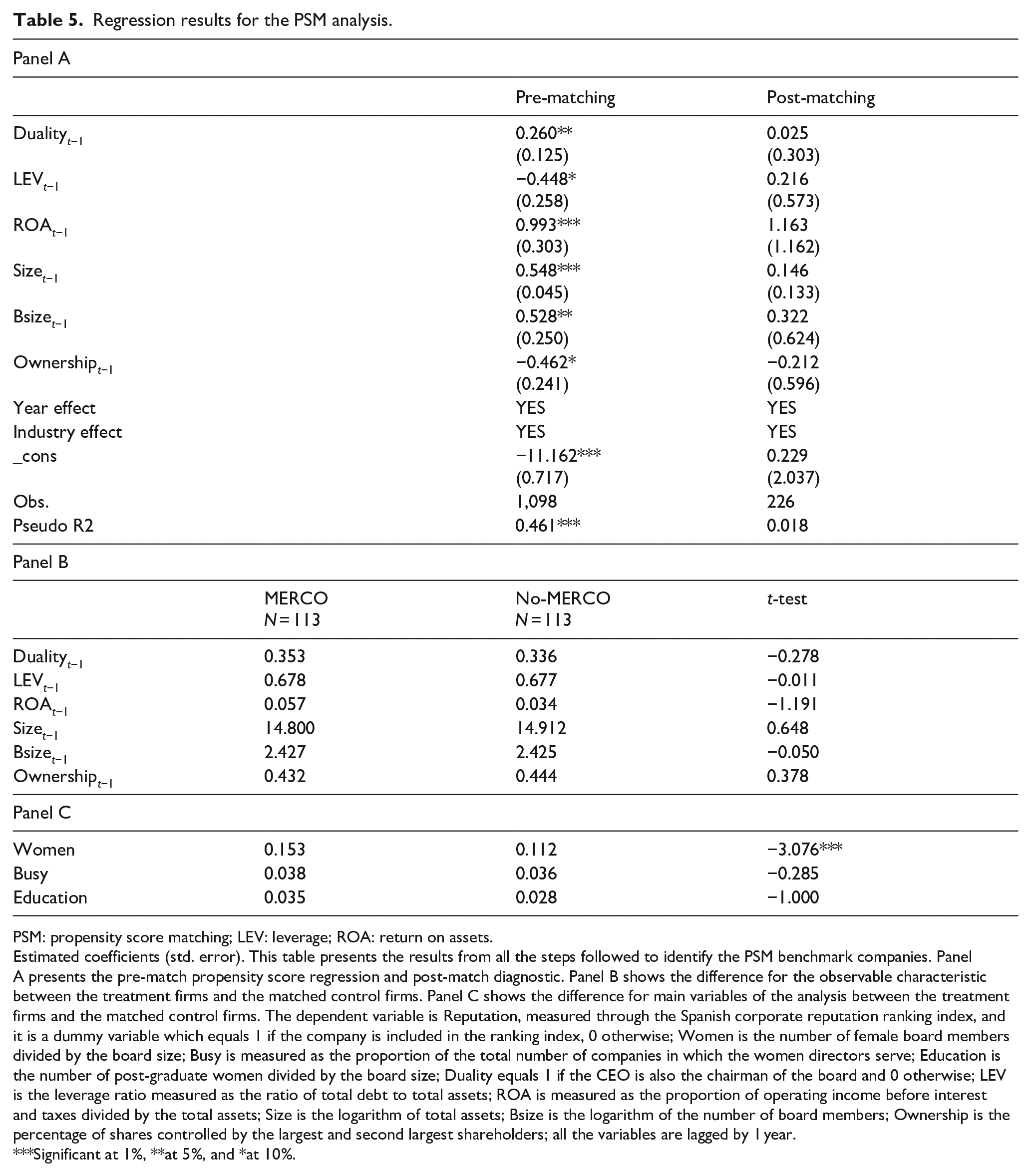

To continue, and with the main aim of addressing selection effects and reducing the degree of observable heterogeneity between the firms included in and outside of the MERCO ranking, we broaden our analysis based on pair-matching techniques. To start with, we calculate the predicted value from a logit regression based on a set of firm characteristics that should reflect the likelihood of a given firm to be included in the MERCO ranking. They are the same variables as those used in Table 4, to compare the companies with and without reputation. In Table 5, we can see that more highly reputed companies present higher CEO duality, are less leveraged, have better ROA, size, and board size, and have lower ownership concentration. The pseudo R-squared for the regression presents a value of 0.461.

Regression results for the PSM analysis.

PSM: propensity score matching; LEV: leverage; ROA: return on assets.

Estimated coefficients (std. error). This table presents the results from all the steps followed to identify the PSM benchmark companies. Panel A presents the pre-match propensity score regression and post-match diagnostic. Panel B shows the difference for the observable characteristic between the treatment firms and the matched control firms. Panel C shows the difference for main variables of the analysis between the treatment firms and the matched control firms. The dependent variable is Reputation, measured through the Spanish corporate reputation ranking index, and it is a dummy variable which equals 1 if the company is included in the ranking index, 0 otherwise; Women is the number of female board members divided by the board size; Busy is measured as the proportion of the total number of companies in which the women directors serve; Education is the number of post-graduate women divided by the board size; Duality equals 1 if the CEO is also the chairman of the board and 0 otherwise; LEV is the leverage ratio measured as the ratio of total debt to total assets; ROA is measured as the proportion of operating income before interest and taxes divided by the total assets; Size is the logarithm of total assets; Bsize is the logarithm of the number of board members; Ownership is the percentage of shares controlled by the largest and second largest shareholders; all the variables are lagged by 1 year.

Significant at 1%, **at 5%, and *at 10%.

The second step, following Chen et al. (2017), is based on the nearest neighbor approach to ensure that reputed companies (the treatment group) are similar to the less reputed ones (the control group). This means that each reputed firm has been matched to a company not included in the MERCO ranking. After matching, our propensity score matched sample comprises 226 firm–year observations. To ensure that firms in the treatment and in the control group have the same observable characteristics, we re-estimate the logit model for the propensity score matched sample. Table 5, Panel A displays the results in the second column, showing the similarity between both groups. As shown, none of the coefficients is statistically significant, indicating that there are no differences in reputation between the two groups.

Panel B of the same table studies the difference in the observable characteristics between the treatment firms and the matched control firms. Predictably, there are no differences between the groups, which shows that the PSM removes all observable differences between them. Panel C shows that in the matched sample, there are significant differences in corporate reputation between firms with and those without women directors, and it confirms Hypothesis 1. However, the coefficients for busy and educated women remain insignificant, which indicates that having busy or highly educated women on boards does not influence corporate reputation. This runs contrary to our Hypotheses 2 and 3.

To conclude, we can confirm that board gender diversity is positively related to corporate reputation and that the presence of busy women directors has no effect on it. Meanwhile, the influence of highly educated women directors on reputation is inconclusive, making further analyses necessary.

Additional analyses

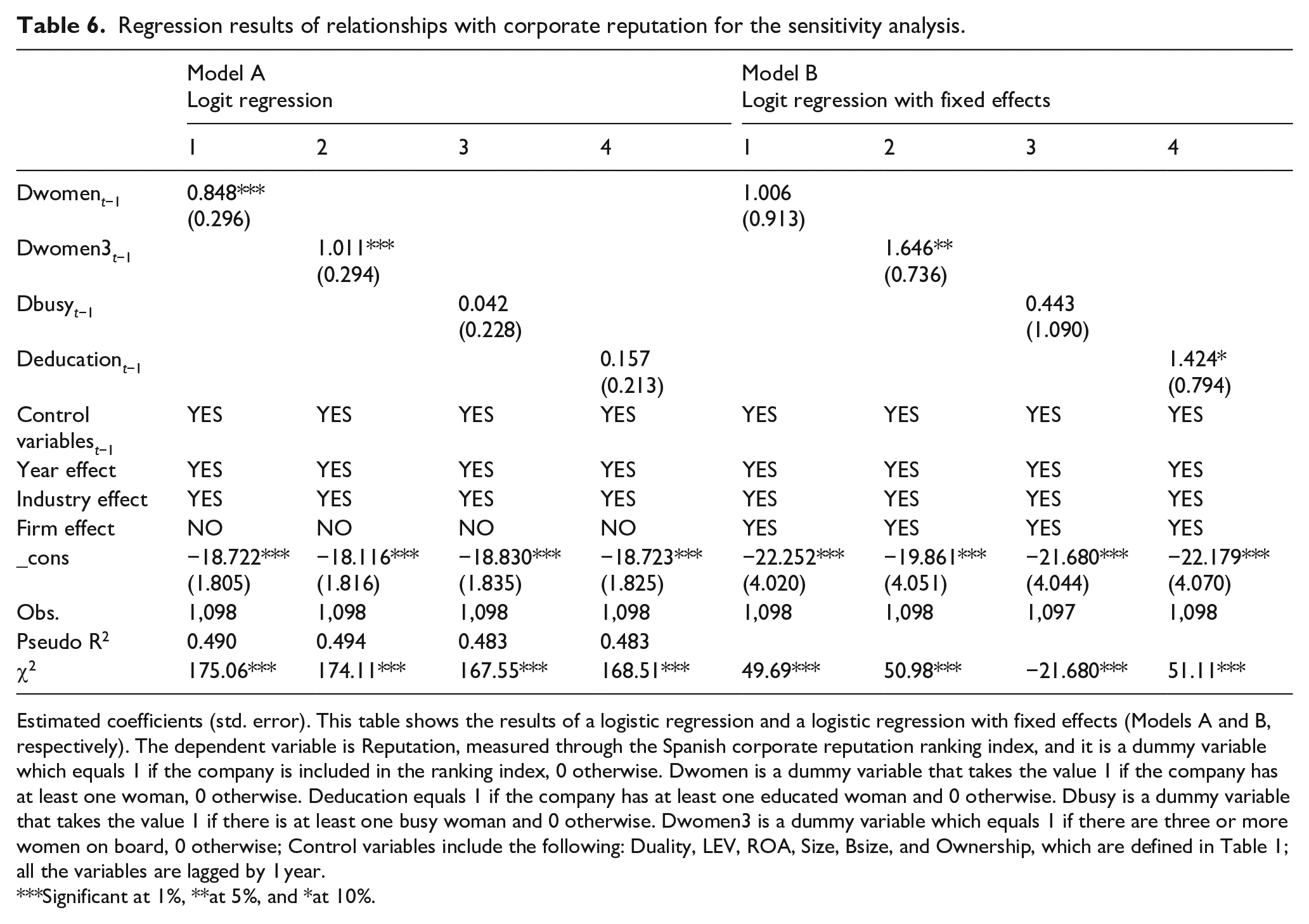

It is in this section where we extend our analysis by considering alternative measures to our independent variables. However, we define new dummy variables, Dwomen, Deducation, and Dbusy, and those take the value of 1 if the company has at least one woman, one educated woman, and one busy woman, respectively, and 0 otherwise. Control variables remain unchanged. As before, all the variables are lagged by 1 year to mitigate endogeneity concerns.

Moreover, previous studies in this area have focused not only on the presence of women but also on their number sitting on boards, suggesting the need for a critical mass (Erkut et al., 2008; Torchia et al., 2011). In this regard, previous literature tells us that boards with three or more women are different from those composed only of men, and the communication between the board and its stakeholders is more effective (Terjesen et al., 2009). Subsequently, we have used an alternative measure for the variable women by creating a dummy, Dwomen3, which takes the value 1 if there are three or more women on board and 0 otherwise.

We conduct the new estimation in Table 6. First, Model A is based on a logit regression. Second, to control for the unobserved heterogeneity which can be present in the first model, Model B uses a Logit regression with fixed-effect estimates. Finally, we run some difference in means tests to check the differences in the previous matched sample.

Regression results of relationships with corporate reputation for the sensitivity analysis.

Estimated coefficients (std. error). This table shows the results of a logistic regression and a logistic regression with fixed effects (Models A and B, respectively). The dependent variable is Reputation, measured through the Spanish corporate reputation ranking index, and it is a dummy variable which equals 1 if the company is included in the ranking index, 0 otherwise. Dwomen is a dummy variable that takes the value 1 if the company has at least one woman, 0 otherwise. Deducation equals 1 if the company has at least one educated woman and 0 otherwise. Dbusy is a dummy variable that takes the value 1 if there is at least one busy woman and 0 otherwise. Dwomen3 is a dummy variable which equals 1 if there are three or more women on board, 0 otherwise; Control variables include the following: Duality, LEV, ROA, Size, Bsize, and Ownership, which are defined in Table 1; all the variables are lagged by 1 year.

Significant at 1%, **at 5%, and *at 10%.

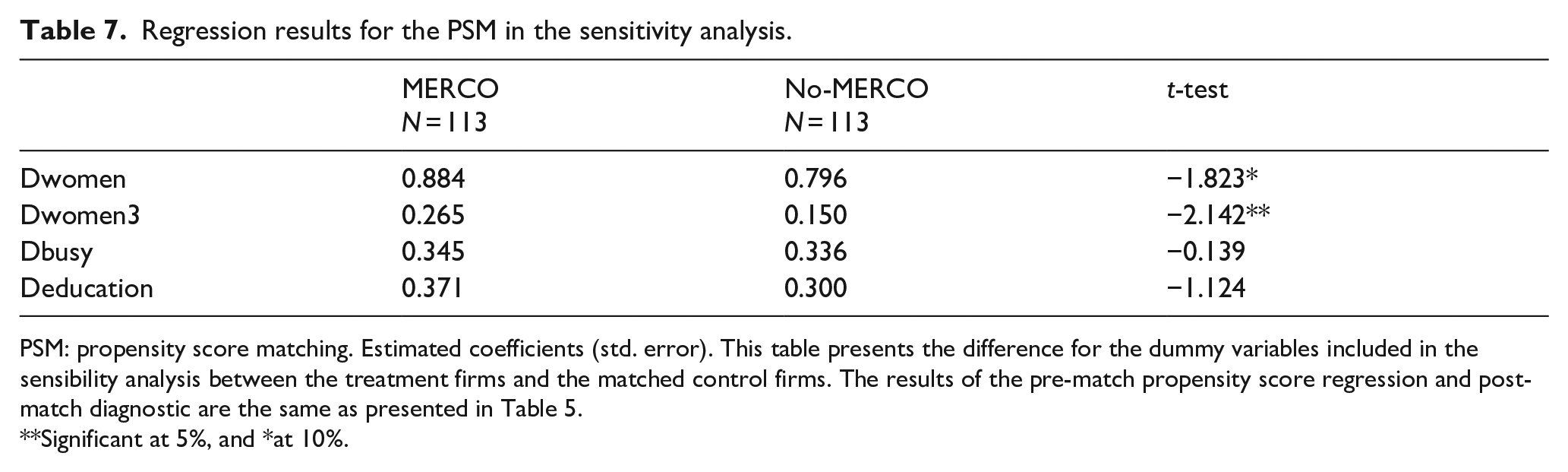

The results show that our main outcomes are qualitatively the same, confirming that after controlling for endogeneity and unobserved differences across firms, female directors influence Spanish firms’ reputations but their busyness does not. Regarding the education level of women directors, it shows weak evidence of a positive influence. Finally, Table 7 indicates that when similar companies are matched using the PSM procedure, only Dwomen and Dwomen3 are significant.

Regression results for the PSM in the sensitivity analysis.

PSM: propensity score matching. Estimated coefficients (std. error). This table presents the difference for the dummy variables included in the sensibility analysis between the treatment firms and the matched control firms. The results of the pre-match propensity score regression and post-match diagnostic are the same as presented in Table 5.

Significant at 5%, and *at 10%.

Discussion and conclusion

Drawing on the signaling theory, companies are proud to show their adaptation to new times. As companies signal that they include female directors on their boards (Bernardi et al., 2002), we can infer that a diverse board may signify that boards function more effectively.

Previous research on females and corporate reputation had small samples. Examples include Fuentes-Medina et al. (2018) with 49 observations from Spanish firms during 2012; Bear et al. (2010) with 51 observations from the health care industry during 2009; Brammer et al. (2009) with 199 firms during 2002; and Miller and Triana (2009) with 326 companies during 2004. Our panel data study 141 non-financial listed firms during 2008–2017, with a total of 1,240 firm–year observations. After controlling for industry, year, and firm-specific fixed effects, as well as endogeneity issues, our results indicate that the more women there are on boards, the better the corporate reputation is.

The signaling theory, in a context of asymmetric information, indicates that firms convey important information through observable signals. The public receives signals not only from the firms themselves but also from the media or from other channels (Fombrun & Shanley, 1990). The percentage of women on boards has doubled during the period under study. According to the Spencer Stuart Board Index, during this period, Spanish firms have gone from 57% of companies having some female directors (37% in 2005) to 92%. This increase in the number of women directors has probably improved the perception of corporate reputation by the public. But it is also worth noting that we study a key period where, in general terms, the 2007 Spanish Gender Equality Act has been followed by both the support of different governments and the active role of the media, who have promoted the incorporation of women on boards.

In Spain, the public has received signals about the importance and benefits of female presence. The signaling theory suggests that companies adopting governance practices perceived as desirable are likely to be more favorably viewed by stakeholders (Musteen et al., 2010). Through the presence of women, Spanish firms have signaled adherence to norms and even positive working conditions (Miller & Triana, 2009), while public policies and mass media have contributed to the greater visibility of women’s roles. In addition, our results are consistent with those of Konrad et al. (2008) or Torchia et al. (2011) since companies with three or more women in the boardroom enjoyed a significantly better reputation than the rest.

However, although we find some weak evidence that highly educated female directors improve corporate reputation; the PSM methodology does not support this hypothesis. Furthermore, we do not find any relationship between busy women directors and corporate reputation.

Williams and O’Reilly (1998), after analyzing over 80 studies, claimed that “simply having more diversity in a group is no guarantee that the group will make better decisions or function effectively.” In fact, Brammer et al. (2009) or Miller and Triana (2009) did not find strong evidence to support the relationship between gender diversity and corporate reputation. However, during our study period, the Spanish public has been receiving clear messages indicating that social equality or ethical reasons require diversity on boards of directors. As a result, companies hiring women directors would signal adherence to norms. In addition, having a diverse board signifies that the firm is properly prepared for modern times, and, consequently, for facing a diverse market.

In our opinion, awareness regarding gender equality is greater in our society now than it was before. Our results suggest that neither women with multiple directorships nor greater educational background conclusively increase corporate reputation, perhaps because stakeholders appreciate the general characteristics associated with femininity rather than cognitive attributes. That is, feminine traits are perceived to be important to better understand the business environment, which is guaranteed by board gender diversity.

We make a contribution to the scarce accounting literature on gender and reputation, by conducting a thorough investigation that covers both several specific attributes of female directors and the use of rigorous methodology. Our research concludes that having women directors on the board increases corporate reputation. Nevertheless, we are aware that our study is limited to Spain. Further investigation is necessary to analyze other countries. Moreover, previous research was conducted when society was not so aware of the importance of the female role. Consequently, only recent studies can show whether other countries appreciate the increase in reputation of firms that promote women on their boards in the same way as Spain.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.