Abstract

In this essay, we connect the United Nations’ Sustainable Development Goals (SDGs)—an extensive collection of society-level goals and targets aimed at addressing grand challenges and achieving global sustainability by 2030—to firm-level sustainability and Environmental, Social, and Governance (ESG) factors. In doing so, we highlight the importance of connecting the SDGs with the concept of double materiality—stakeholder materiality and financial materiality. Our assessment helps businesses navigate the intricate sustainability space and understand the ways in which their sustainability interventions can help solve the ESG grand challenges encapsulated in the SDGs. We conclude the article by introducing the five research articles that are part of the special issue “Our house is on fire! The role of business in achieving the Sustainable Development Goals” and suggesting a path for the future that revolves around creating standardized “sustainability balance sheets” in business.

Keywords

Introduction

In 2015, the United Nations launched the Sustainable Development Goals (SDGs)—a compilation of 17 societal-level goals, 169 targets, and 231 indicators—aimed at achieving global sustainability by 2030 (United Nations, 2015). The SDGs have been described as the most comprehensive framework ever formulated to address global societal grand challenges (Kolk et al., 2017; Sachs et al., 2019; Wettstein et al., 2019), including environmental (e.g., natural-resource depletion, biodiversity loss, and climate change), social (e.g., world hunger, growing inequalities, systemic racism, human-health deficiencies, and education deficits), and governance grand challenges (e.g., gender gaps, corruption, and war). Although the SDGs are set as macro-level goals for countries and governments, businesses are considered central actors in their achievement (Montiel et al., 2021; UN, 2015; van Zanten & van Tulder, 2021).

The SDG framework has been accompanied by growing interest in the role of business in achieving sustainability, and a multitude of concepts and frameworks focused on this issue have appeared in recent years (Antolín-López et al., 2016). One such concept is “corporate sustainability” (Bansal, 2005), which reflects the idea of ensuring sustainability in business practices—“sustainability” from this point on. As the financial markets have begun to recognize the importance of pursuing sustainability outcomes in business, the concept of materiality has gained traction in connection with environmental, social, and governance (ESG) factors (MacNeil & Esser, 2022). “Materiality” is traditionally used in finance to refer to the factors that may have consequences for financial performance (Jebe, 2019). Companies must provide investors with information on these factors, as they are key for investors’ decisions. Since ESG factors were recognized as able to affect financial profitability, the financial materiality of ESG factors has gained increasing attention, which has spurred the proliferation of ESG data providers and metrics (van Zanten & Huij, 2022). Moreover, relevant stakeholders, such as non-governmental organizations (NGOs) and regulators (e.g., European Commission, 2019), have warned that a narrow notion of materiality focused solely on financial aspects is worrying, and that any such view should be supplemented with information on social and environmental impacts to ensure the achievement of global sustainability.

In this special issue, we aim to advance our knowledge on the role of business in solving grand challenges and achieving the SDGs by 2030. In this regard, a reflection on how societal-level goals fit with existing firm-level sustainability logics, including the concept of ESG and the notion of double materiality, which encompasses materiality based on both (1) financial and (2) stakeholder aspects, seems appropriate. To demonstrate this connection, we provide examples of how firm-level ESG factors correlate with specific societal-level SDGs and related targets. Furthermore, we introduce the five articles that are part of this special issue entitled “Our house is on fire! The role of business in achieving the Sustainable Development Goals.” Finally, we introduce the concept of the sustainability balance sheet.

The United Nations’ SDGs

By mid-2022, it was difficult to navigate any type of corporate external communications, such as company websites or annual reports, without bumping into the colorful rainbow of the 17 SDGs: (1) no poverty; (2) zero hunger; (3) good health and well-being; (4) quality education; (5) gender equality; (6) clean water and sanitation; (7) affordable and clean energy; (8) decent work and economic growth; (9) industry, innovation, and infrastructure; (10) reduced inequalities; (11) sustainable cities and communities; (12) responsible consumption and production; (13) climate action; (14) life below water; (15) life on land; (16) peace, justice, and strong institutions; and (17) partnerships to achieve the goals.

Although they were first released in 2015, the SDGs are a product of the UN’s long-standing efforts attempt to advance global sustainability. Two pivotal antecedents of the SDGs are worth mentioning. In 1987, the Brundtland Report introduced the concept of “sustainable development” as development that meets the needs of current generations without jeopardizing the needs of future generations (World Commission on Environment and Development, 1987). The premise is that not all development is good for society and the planet, and that long-term considerations must be added to the equation. In other words, any development approach that adopts a short-term focus will likely compromise the likelihood that future generations will be able to lead a healthy life on Earth.

The SDGs were preceded by the Millennium Development Goals, a set of nine broad goals introduced in 2000 to advance sustainable development, mainly in developing regions, by 2015 (UN, 2000). After the partial success of the Millennium Development Goals in addressing some of the most critical global sustainability issues, such as world hunger and access to health care (Griggs et al., 2013), the United Nations expanded its catalog of goals to be more inclusive, not only in terms of participating countries but also with respect to societal actors, including governments, civil-society organizations, and the private sector. For example, SDG 8 on decent work and economic growth and SDG 12 on responsible consumption and production are closely connected to business activity. In fact, businesses are regarded as critical actors with the potential to advance global sustainability under each of the 17 SDGs. Therefore, it is crucial to understand how businesses can embed the SDG framework in their core activities and discern whether the 2030 Agenda indeed promotes substantive changes in business to advance global sustainability.

However, the role of business in advancing the SDGs is unclear, as the goals are set at the societal or country level. As such, businesses may assume that governments are the sole actors responsible for advancing the 2030 Agenda. This assumption is flawed, as businesses have the potential and the responsibility to advance global sustainability, especially as they have contributed to creating negative externalities in society and the natural environment (Montiel et al., 2021). In addition, businesses have the expertise, resources, and capabilities needed to help accelerate the sustainability transitions required to achieve the SDGs by 2030. Therefore, we require an understanding of how businesses can embed the framework of the SDGs in their core activities and discern whether the 2030 Agenda is actually promoting substantive changes in business to advance global sustainability.

Double materiality: linking ESG, sustainability, and SDGs at the firm level

The concepts of materiality and double materiality

“Materiality,” which is a crucial concept in finance, refers to the information that companies must provide to investors. More specifically, “information is material if omitting it or misstating it could influence decisions that users make on the basis of financial information about a specific reporting entity” (IASB, 2010, p. 17). When businesses provide ESG data to investors based on this definition of materiality, they generally focus on factors that might affect the company financially—that is, the risks and opportunities that ESG factors may generate for the company. This conceptualization of materiality corresponds to the notion of financial materiality and mainly targets investors.

However, stakeholders (e.g., governments, employees, customers, NGOs, and communities) are also concerned about the external impact of companies on society and the natural environment. When companies provide information about their external impacts, they are responding to the need for stakeholder materiality. Despite the fact that stakeholder materiality is mostly aimed at stakeholders, many investors have begun to use this information in their investment decisions. Therefore, financial materiality and stakeholder materiality have been termed “double materiality.” We posit that the double materiality perspective provides a complete picture of the relationship between business and global sustainability, and the external impact of business activities.

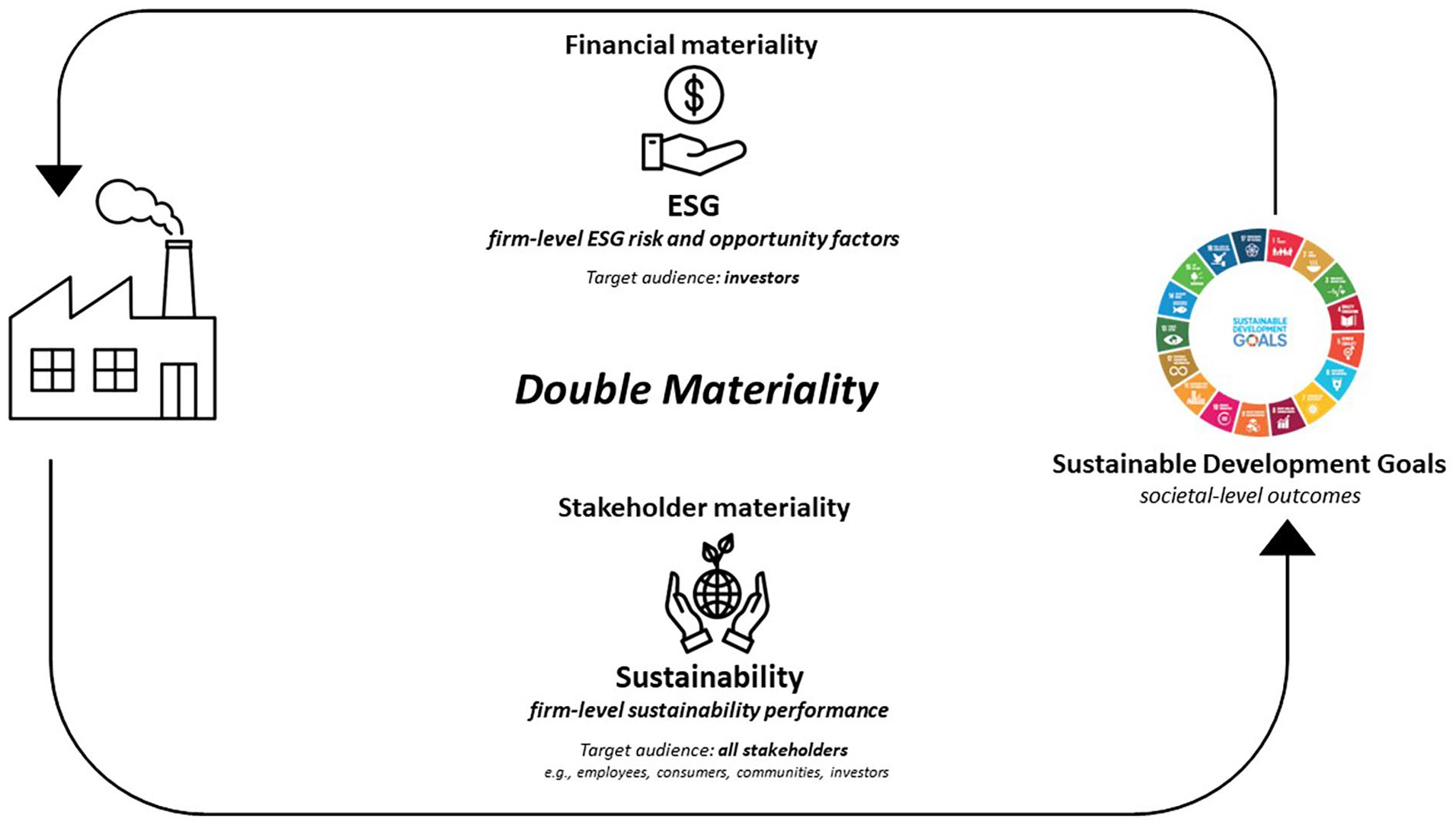

Figure 1 illustrates how the double materiality perspective acts as a mechanism that links ESG, sustainability, and the SDGs. The top arrow indicates how societal-level SDGs and SDG targets have become relevant to investors by considering them in their investment decisions, thus making them financially material for the company. Such societal-level information is generally collected using ESG factors at the firm level, which are increasingly being used in investors’ due-diligence processes. The bottom arrow represents companies’ efforts to improve their firm-level sustainability performance. Such efforts, if substantively implemented, benefit firms’ stakeholders including employees, consumers, communities, and even investors, and advance the SDGs. This bottom section represents stakeholder materiality. Thus, financial materiality and stakeholder materiality compose the double materiality perspective.

Double materiality as the link among sustainability, ESG, and the SDGs.

Even if we differentiate between the two types of materiality with different audiences, recent studies have shown that pursuing what is good for society positively affects investors in the long term (e.g., Ortiz-de-Mandojana & Bansal, 2016). Double materiality represents the joint consideration of financial materiality and stakeholder materiality, and can be used as a framework to reconcile investors’ interests in sustainability with the business’ external impact on the natural environment and society.

Sustainability and stakeholder materiality

The role of businesses in society was initially recognized in the 1950s with the introduction of “corporate responsibility.” The concept focused on the responsibility of business for its actions in society and its immediate environment (Carroll, 1979). The idea that businesses not only had to keep shareholders’ interests but also those of other stakeholders in mind started to gain traction (Freeman, 1984). In the 1980s, stakeholders increasingly began paying attention to the adverse effects of business operations on the natural environment in the form of, for instance, pollution, natural-resource depletion, and biodiversity loss, creating a conversation on corporate sustainability that grew in parallel with the conversation on corporate social responsibility (Bansal & Song, 2017; Montiel, 2008). In 1987, the World Commission on Environment and Development (1987) introduced the term “sustainable development” as development that does not jeopardize the life of future generations in its Brundtland report. This boosted the attention paid to this issue among scholars, practitioners, governments, and society in general. Since then, scholars and practitioners have developed various definitions to incorporate sustainable development into the business context and business operations.

Initially, most definitions of sustainability focused on the effect of business operations on the natural environment in connection with, for instance, environmental management (e.g., Klassen & McLaughlin, 1996), environmental strategies (e.g., Russo, 2003), ecological sustainability (e.g., Shrivastava, 1995), or sustain centrism (e.g., Gladwin et al., 2006). Later, scholars expanded their sustainability definitions to include the effects of business operations on economic, societal, and environmental systems (Bansal, 2005; Hart & Dowell, 2011; Schaltegger et al., 2013; Sharma, 2014). For example, Valente (2012, p. 586) pointed out that businesses needed to find ways to connect social, economic, and ecological systems using “coordinated approaches that harness the collective cognitive and operational capabilities of multiple local and global social, ecological, and economic stakeholders operating as a unified network or system.” However, despite these developments, we lack a universal definition of business sustainability—a fact that reflects the concept’s complexity and ambiguity (Meuer et al., 2020; Montiel & Delgado-Ceballos, 2014). In general, scholars seem to agree that sustainability is a tri-dimensional construct based on economic integrity, social equity, and environmental integrity (Bansal, 2005), which is also referred to as the 3Ps approach to business (i.e., profit, people, planet) or the “triple bottom line” (Elkington, 1997; Hart & Milstein, 2003). In essence, sustainability is seen as an ultimate goal for businesses, as many wish to claim that their operations do not negatively affect society or the natural environment. However, recent discussions suggest that businesses have the potential to positively affect social-ecological systems by engaging in regeneration, which shifts the focus away from a business logic and toward a systems logic (Hahn & Tampe, 2021).

The concept of firm-level sustainability, which centers on the positive and negative consequences of business activities for society and the natural environment, fits the stakeholder logic. Stakeholder materiality relates to the “impact of [the company’s] activities” (European Commission, 2019, p. 10). Given this notion of materiality, we can posit that ESG grand challenges are material to businesses, and that integrating this logic into business operations can ultimately contribute to the achievement of global sustainability and the SDGs. In fact, stakeholder materiality increases the pressure for businesses to consider not only the risks and opportunities for investors but also issues relevant for all stakeholders (e.g., employees, communities, consumers, and investors), such as ESG concerns.

ESG and financial materiality

The term “ESG” first emerged in finance and mainly targeted business investors. It was first coined in the report “Who Cares Wins: Connecting Financial Markets to a Changing World,” compiled by UN Global Compact and published in December 2004 (Global Compact, 2004). The report, which aimed to integrate ESG criteria into the financial sector, provided recommendations and guidelines for incorporating ESG-related risks and opportunities into financial-market analyses, investments, and research. It was publicly endorsed by a group of 20 financial actors, including banks (e.g., Deutsche Bank, HSBC, Morgan Stanley, and the World Bank Group), asset managers (e.g., Henderson Global Investors, ISIS Asset Management, and RCM), asset owners (e.g., Allianz SE and Aviva PLC), securities brokerage agencies (e.g., AXA Group, CNP Assurances, and KLP Insurance), and rating agencies (e.g., Calvert Group, Goldman Sachs, and Innovest). The report was a joint initiative among the former UN Secretary-General Kofi Annan, the Swiss Government, and the International Finance Corporation (IFC). However, 1 year later, the publication of the “Freshfields Report” by the United Nations Environmental Programme Finance Initiative (UNEP-FI, 2005) served as a milestone for the acceptance and spread of ESG criteria in the finance field. The report used a legal framework for integrating ESG issues into institutional investment. However, the central relevance of the report arose from the fact that it provided the first evidence of the financial materiality of ESG factors.

Although ESG evolved from the concept of sustainability, the focus has shifted from the external impact of business activities on society and the natural environment toward the risk and return implications for financial investors of not effectively addressing ESG factors (MacNeil & Esser, 2022). In fact, the main goal of integrating ESG criteria into investment decisions is to align social and environmental benefits and impacts with financial returns by identifying risks and opportunities related to ESG that are likely to affect investors’ and shareholders’ returns (Eccles et al., 2020). In other words, ESG may be characterized as the “financialization” of sustainability.

The emergence of ESG rating agencies and ESG-related products, such as metrics and indices, has contributed to the broad adoption of the term “ESG” from a financial materiality perspective. For example, the MSCI ESG ratings aim to account for a business’ management of financially relevant ESG risks and opportunities, including exposure to ESG risks, and how well it manages those risks compared to its industry peers (MSCI, 2022). This approach stands in contrast to the stakeholder materiality perspective, which aims to integrate ESG factors to minimize negative effects on society and the natural environment, and to create a positive societal impact (European Commission, 2019).

Even if the rise of the ESG’s financial materiality has helped ensure that social and environmental issues are integrated into financial-market valuations, this vision has only led to partial integration of sustainability at the firm level (i.e., only those parts that affect profitability), while the rest has been left out. For example, a business that pollutes might not be penalized in ESG factor analyses based on financial materiality if the regulations of the country or sector in which that business operates do not have regulations in place to address such pollution. Thus, there is no real risk that this pollution will affect the company financially. Nevertheless, as markets and public policies evolve, and require companies to be sustainable, a business’ positive or negative impact on the environment and society will increasingly translate into financially significant business opportunities and risks. As this overlap emerges, regulators must encourage the publication and assessment of indicators more representative of the business’ effects on the environment and society. This was the focus of the European Parliament’s Directive 2014/95/EU, which is also called the Non-Financial Reporting Directive (NFRD). According to the Guidelines on Reporting Climate-Related Information, the NFRD mandates cover both financial materiality and stakeholder materiality—that is, the double materiality perspective (European Commission, 2019).

Connections between firm-level metrics and societal-level SDGs

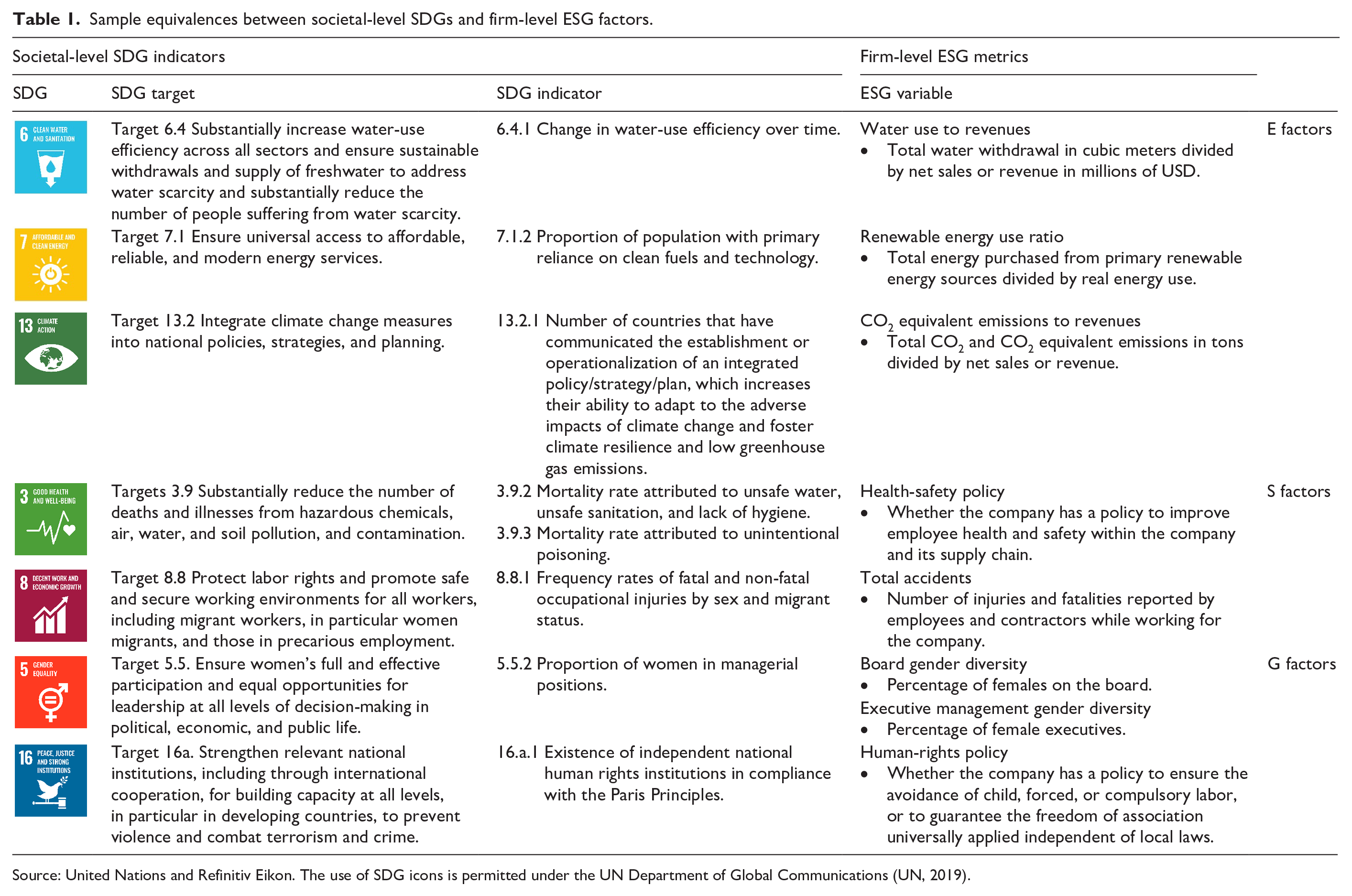

An important issue when talking about companies’ contributions to the SDGs is ensuring that the measures adopted at the micro level effectively capture companies’ sustainability and that their ESG performance advances global sustainability. In this section, we highlight a few examples of ESG indicators that may be useful for measuring the sustainability impact of companies and their potential contributions to achieving the SDGs. Specifically, we provide equivalences between firm-level ESG factors and societal-level SDG indicators. We rely on metrics from Refinitiv Eikon, which provides ESG data on more than 9000 global companies across 76 countries and covers more than 80% of global market capitalization. The Refinitiv Eikon analysts collect more than 450 annual ESG metrics for each company from publicly available information sources, such as company websites, annual reports, and sustainability reports (Refinitiv Eikon, 2022). Refinitiv is an ESG data provider that is widely used by financial analysts and academic researchers. Refinitiv Eikon also provides ESG ratings based on its evaluation of materiality for each industry group.

Table 1 includes a selection of ESG indicators and their equivalences to SDG indicators. These examples exclude ratings to avoid incorporating Refinitiv’s materiality assessment. Instead, we propose indicators based on metrics that are as close as possible to the original values of the impact to be measured. We include a column that identifies whether the issue in Refinitiv is more closely related to E, S, or G. However, this distinction is not always easy to determine, that is, a bit imprecise. This is the case, for example, for “environmental partnerships,” where the proposed indicator could simultaneously be classified as belonging to all three types of ESG factors. The selected indicators could also be evaluated in terms of their ability to capture double materiality. For example, in SDG 13, which focuses on taking urgent action to combat climate change and its impacts, we draw attention to the “CO2-equivalent Total” indicator because of its ability to capture both the financial risk to the business of high emissions and the threat to the planet and society that the business may pose. This indicator should always have a priority weight in the design of double materiality valuations. Other examples of indicators that capture double materiality are “Accidents Total” in the business (SDG 8 on Decent Work) and “Water use to Revenues” (SDG 6 on Clean Water and Sanitation). In contrast, other indicators have a clear positive effect on society but are less connected to the business’ profitability, at least in the short term, such as the existence of partnerships in SDG 17.

Sample equivalences between societal-level SDGs and firm-level ESG factors.

Source: United Nations and Refinitiv Eikon. The use of SDG icons is permitted under the UN Department of Global Communications (UN, 2019).

In any case, we believe that it is essential to stress that choosing a few highly relevant (material) indicators can be helpful for developing a clear picture of a business’ impact on society and the natural environment. The excessive use of aggregated indicators incorporating a large amount of diverse and weighted information (e.g., some of the aggregated global ESG indicators provided by rating agencies) has led to criticisms and mistrust of the validity of firm-level ESG metrics. For example, The Economist (2022) claims that a focus on ESG factors “that won’t save the planet” confuses investors (Pucker & King, 2022), as it does not lead to a meaningful impact on society and the natural environment (Pucker & King, 2022; van Zanten & Huij, 2022).

Essays in this special issue

In this special issue, we are pleased to present five essays analyzing the role of business in advancing the SDGs. The five contributions provide insights from different parts of the world, including Spain and Colombia.

The first essay, “Agglomerations around natural resources in the hospitality industry: Balancing growth with the Sustainable Development Goals,” explores the tensions between business growth and environmental preservation, as seen in tourism agglomerations located near natural resources. The authors’ analysis of the location decisions of 295 luxury beach hotels in Spain between 1960 and 2015 advances our knowledge of how the tourism industry can work toward achieving SDGs, especially SDG 8, SDG 12, and SDG 14. The second essay, “Where smart meets sustainability: The role of smart governance in achieving the Sustainable Development Goals in cities,” examines the trade-offs in simultaneously advancing economic growth, social equality, and environmental performance in urban contexts. Using a sample of 128 cities worldwide, the authors conclude that smart governance plays a key role in promoting SDG 11, SDG 16, and SDG 17 at the city level.

The third essay, entitled “The impact of the United Nations Sustainable Development Goals on corporate sustainability reporting,” analyzes 164 large corporations that have been ranked as the best sustainability performers. The authors use the lens of normative pressure to explore how the SDGs affect sustainability reporting and to identify differences in industries, natural-resource intensity, and geo-institutional contexts. The analysis reveals variations among companies based on institutional characteristics. The fourth essay, entitled “Business for peace: How entrepreneuring contributes to Sustainable Development Goal 16,” uses emancipatory entrepreneurship theory to study the role of entrepreneurial ventures in advancing this SDG. The research team developed four qualitative cases of ex-combatants in Colombia to identify activities that simultaneously achieve peace and wealth. The last essay, “The roles of multinational enterprises in implementing the UN Sustainable Development Goals (SDGs) at the local level,” examines 349 multinationals to explore the different roles that these actors can play in implementing the SDGs at the local level.

These studies take different approaches to analyzing connections between business and the SDGs. They do not rely solely on firm-level data, as they also entail societal-level analyses that bring us closer to the system approach needed in sustainability research (Grewatsch et al., 2021)

Moving forward: the sustainability balance sheet

The United Nations’ ultimate objective when it launched the 2030 Agenda and the 17 SDGs was to tackle the grand challenges of our era, including poverty, climate change, biodiversity loss, and systemic inequalities. Undoubtedly, the success of this new plan requires collaboration among many actors, such as governments, intergovernmental organizations, non-governmental organizations, and society at large. Businesses must play a central role in implementing the SDGs. However, we must translate societal-level SDGs and SDG targets into firm-level goals if we are to achieve the SDGs. For example, SDG 8 on decent work and economic growth, and SDG 12 on responsible consumption and production are closely connected to business activities. In fact, businesses are regarded as critical actors with the potential to contribute to the targets under each of the 17 SDGs.

Double materiality’s increasing popularity has triggered the need for companies to consider the impact of their activities on all stakeholders (stakeholder materiality), and the risks and opportunities for their investors (financial materiality). Although an increasing number of investors are demanding a stakeholder materiality analysis before evaluating any business plan or model, some are not concerned about these factors. The latter do not see a clear effect of these factors on businesses financial profitability, at least in the short term. Thus, when providing information about their impacts, businesses must consider whether to adopt a financial materiality or a double materiality perspective.

We believe that double materiality allows businesses to engage investors and shareholders in ESG integration, while simultaneously contributing to sustainable development and helping to achieve the SDGs. Double materiality serves as a framework that can help a company design its sustainability practices in a way that takes the interests of all stakeholders into account and reconciles the “opposing” positions of investors (financial materiality) and other stakeholders (stakeholder materiality) in relation to sustainability.

Although ESG indicators are closely linked to financial materiality, we have highlighted several examples in which these indicators encompass double materiality and have the potential to capture the company’s role in achieving the SDGs. However, many firm-level ESG and ratings are complex and cumbersome. ESG data providers cover hundreds of variables, but some of them lack relevant data. We recommend that the ESG industry and researchers focus on simplifying and standardizing ESG to encompass those factors that are material to the business (i.e., financial materiality) and those factors that are vital for achieving the SDGs (i.e., stakeholder materiality). Efforts to consider “double materiality” are pivotal not only for the sustainability of modern business but also the sustainability of our planet.

We also point to the debate on whether ESG ratings are effective for measuring the impact of companies on society and the environment. The crucial issue is that ESG metrics do not fully capture how businesses contribute to addressing all societal-level sustainability challenges. For instance, a company could improve its ESG rating on “Water use to revenues USD” using more water while simultaneously increasing revenues, which would not necessarily contribute to Target 6.4 or Indicator 6.4.1 on water-use efficiency. In addition, although we believe it is appropriate to have some global indicators, such as emissions, we recommend the development of industry-specific indicators depending on the industry’s main activities and their impacts.

In sum, we envision the development of a “sustainability balance sheet” that captures businesses’ double materiality and makes it easier to compare two competing companies. Such sustainability balance sheets would require the simplification and standardization of all existing ESG and sustainability indicators at the firm and societal levels. These balance sheets would also need to account for the short-term and long-term impacts of business activities on ESG factors, while also considering how ESG factors can affect a company’s overall performance. Table 1 can be considered as a starting point for the sustainability balance sheet of a sustainable future.

Footnotes

Acknowledgements

The authors would like to thank Gregorio Martín-De Castro, Martina Linnenluecke, Junghoon Park, and J. Alberto Aragón-Correa for detailed comments on previous versions of this article. We particularly thank Juan Carlos Bou Llusar for his support in the development of this Special Issue.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Javier Delgado-Ceballos and Natalia Ortiz-de-Mandojana, would like to acknowledge the financial support from the Spanish Ministry of Science and Innovation PID2019-107767GA-I00. Likewise, Raquel Antolín-López would like to acknowledge the financial support from the Spanish Ministry of Science and Innovation, Agencia Nacional de Investigación-AEI, and the European Regional Development Fund-ERDF/FEDER-UE: R&D Projects PID2020-119663GB-I00 and and UAL2020-SEJ-D1872. Finally, Ivan Montiel thanks the Lawrence N. Field Center for Entrepreneurship at Baruch College, City University of New York.