Abstract

The purpose of this article is to empirically explore (1) the impact of political ties on international joint ventures’ (IJVs) R&D strategy and (2) the moderating effects of market turbulence and governmental policy turbulence on the relationship between IJV political ties and R&D investment in China. Our sample consists of 1,344 observations taken from 224 IJVs over a period of 6 years (2012–2017), and we applied hierarchical moderated regression analysis (HMRA) with panel data to analyze our three hypotheses. Our findings show that IJVs with political ties tend to invest more in R&D than their counterparts without political ties. Interestingly, this positive relationship grows stronger with high market turbulence, but wanes under high governmental policy turbulence. While the issues regarding the importance of political ties to IJVs competing in China have been discussed, the issues related to why political ties influence IJV’s decisions on R&D investment have been largely overlooked. Hence, this study applies the environmental contingency view to fill this gap and shows how asymmetric contingencies for market turbulence and governmental policy turbulence occur in this context.

Keywords

Introduction

A flattening world (Friedman, 2005) has intensified global competition, constrained operating margins, and made technological innovation critical to the survival and success of international joint ventures (IJVs; Oxley & Sampson, 2004; Williams & Du, 2014). The criticality of such innovation for IJVs is somewhat ironic given that early IJVs were often intended as a tool for global sourcing and supply chain cost savings. Such IJVs were targeted toward developing nations to take advantage of lower labor costs. As many such economies transitioned from underdeveloped to emerging economies, cost advantages eroded and many IJVs turned to technology innovation as a strategy for identifying new market opportunities (Lee & Marvel, 2009). IJVs that are successful at creating new innovation strategies are more likely to develop new products, services, or technological processes which ultimately lead to competitive advantage and superior performance in emerging economies (Kyläheiko et al., 2011).

Given the increasing importance of technology innovation for IJV success, it is somewhat surprising that the existing literature on IJVs in emerging markets appears to be characterized by competing logical arguments and conflicting empirical results. Some studies suggest that IJVs should invest more on R&D projects in emerging economies (Un & Rodríguez, 2018; Zhang et al., 2007). They point to market liberalization and economic growth in emerging markets that create attractive opportunities for foreign companies. IJVs with local partners represent an important entry mode to explore these opportunities and respond to local market requirements. R&D investment is helpful for IJV’s growth and expansion by facilitating the adaptation of existing technology to local needs and by creating new technology through access to local knowhow. In addition, foreign partners typically provide advanced technological, marketing, and managerial capabilities for emerging market IJVs in exchange for local human capital, business connections, and knowledge of the local market (Shu et al., 2017). By combining these advantages, IJVs are expected to penetrate emerging markets and generate profits from their advanced technologies more efficiently.

Other scholars suggest that IJVs might invest less in R&D in emerging economies for two primary reasons. First, IJVs’ R&D achievements may be leaked to local firms due to weak and ineffectual laws protecting intellectual property (IP). Because R&D usually requires significant investment of financial and human capital, IJVs might suffer huge losses if local partners fail to fully comply with agreements on technology protection and use R&D dividends for their own interest. This type of behavior uncertainty is even more salient in emerging economies (Richards & Yang, 2007). Second, foreign and local partners typically have asymmetric technological capabilities (Shu et al., 2017). IJVs in emerging economies may face a steep learning curve and be unable to adapt existing technology or products to the local context, which would reduce their ability to capture rents and generate profit from R&D investment. Although both perspectives provide valuable insights on the trade-offs between the operational risks and benefits, their competing logics and inconsistent results highlight the somewhat embryonic state of research in IJVs’ R&D strategy.

A related line of inquiry has focused on the importance of IJVs’ political ties in emerging markets. Political ties are a firm’s informal social connections with government officials in various levels of administration, including central and local governments, and officials in regulatory agencies (Sheng et al., 2011). For firms competing in emerging markets and transition economies, such as China, the value of political ties may be more compelling because the governments still control a wide range of financial and regulatory resources and maintain a tendency to expropriation (Sun et al., 2010). Previous literature showed that political ties could help firms access scarce resources and internal information from the government. In addition, firms with political ties are more likely to enjoy various favorable government policies and financial support (Yang et al., 2020). Therefore, political ties in those emerging markets could provide a mechanism that affects the decisions associated with the large capital requirements of many R&D projects.

However, the existing literature examining the importance of political ties in emerging economies is characterized by conflicting rationales and mixed findings. To illustrate, some scholars believe that firms with political ties tend to invest more on R&D projects because political ties could facilitate firm access to external financial resources and favorable governmental policies, which in turn result in greater confidence when firms make high-risk decision such as investment in R&D projects (Zhou & Poppo, 2010). Other scholars suggest that firms with political ties might invest less on R&D projects because their limited resources and attentions might be largely distracted by building and maintaining connections with governmental officials (Lin et al., 2011).

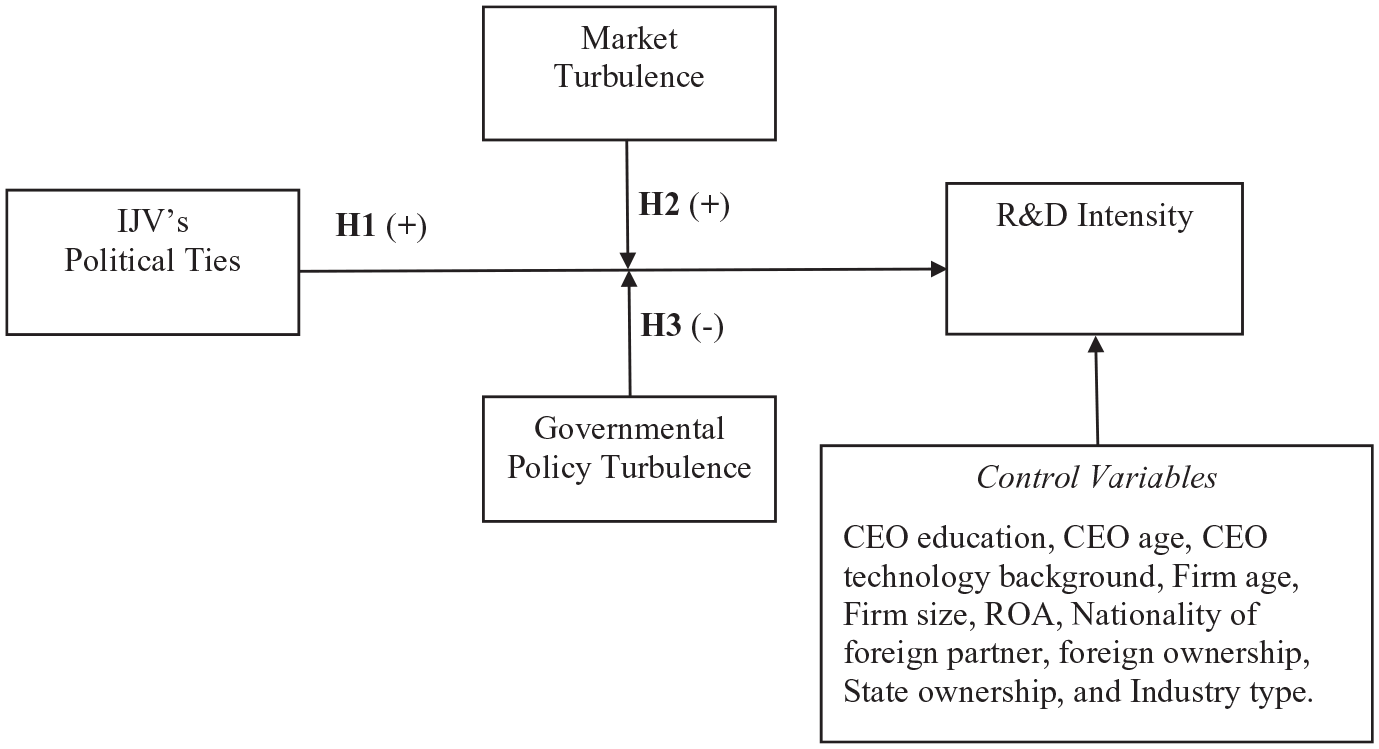

One avenue for resolving some of these conflicting theoretical positions and empirical results reported above is to move away from the universal logic embedded in many studies toward a contingency logic that can predict positive relationships under some conditions and negative relationships in other conditions (Delery & Doty, 1996). We introduce such contingency logic to clarify the relationship between political ties and R&D investment in China. We explore the factors in emerging economies posited to result in a positive relationship between political ties and R&D investment. Then, drawing on the logic of environmental determinism (Hrebiniak & Joyce, 1985), we argue that the conflicting results occur because the relationship between political ties and R&D investment is contingent on the environmental turbulence (i.e., market turbulence and governmental policy turbulence) the IJV encounters.

We focus on IJVs in China as the context to develop and verify our propositions for four major reasons. First, China already has the world’s second-largest gross domestic product (GDP) and is generally considered to be one of the most influential emerging economies due to its ongoing rapid growth. This growth has coincided with the massive restructuring of its innovation system (Zeng, 2017). Second, IJVs’ innovation strategy could be largely influenced by China’s unique institutional context. To illustrate, the weak protection of Intellectual Property Rights (IPRs) is widely considered as one of the biggest hurdles for IJVs to invest in R&D projects in China (Brander et al., 2017). However, IJVs with political connections could enjoy various forms of favorable governmental support. Thus, the intricacy of China’s institutional context provides an interesting field to explore IJV’s innovation strategy. Third, like other major emerging economies, China is experiencing a rapid economic and political transition (Tang et al., 2019; Yang, Ma, Zhang, & Hong, 2018). Much of this change is the result of direct government intervention designed to modernize the Chinese economy and rapidly advance the nation to developed nation status. As a result, IJVs in China face fluid governmental policies and ongoing changes in operating environments. Thus, the Chinese political climate and market environment are significantly different from the contexts of IJVs competing in developed countries with well-established markets and relatively consistent regulations. Finally, as the private sector expanded during economic transition, China has witnessed a proliferation of IJVs. They have become one of the most important engines for China’s economic growth since the 1990s. Because innovation capability is the fundamental determinant of the firm’s economic performance (Kandemir & Hult, 2005), an increasing number of Chinese companies choose to cooperate with foreign partners to conduct R&D projects and strengthen their innovation capabilities.

Based on the R&D activities of 224 IJVs listed on the Shenzhen stock exchange in China, we find that that IJVs with political ties tend to invest more in R&D projects than their counterparts without political ties. In addition, this positive relationship grows stronger when market turbulence is higher, but becomes weaker when governmental policy turbulence is higher. The results allow us to explore several areas of contribution, including how R&D investment of IJVs is influenced by internal capability, by the external operating environment, and how political ties and environmental turbulences affect IJVs’ R&D strategies.

The contribution of our study is threefold. First, IJVs’ decisions regarding R&D investment are unavoidably influenced to some extent by host countries’ market and political environment. This influence is even more prevalent and substantial for IJVs competing in developing economies that typically lack well-established economic and political regulations. By drawing on the environmental contingency perspective, our study provides a unique lens through which we may better understand how these factors are linked. Second, our study extends current research by exploring the relationship between political ties and IJVs’ R&D strategy in China as one of the largest and most influential developing economies in the world. Thereby, we provide additional empirical evidence and new insights to this growing research domain. Third, in addition to the theoretical contribution, our study offers some practical suggestions for IJVs’ managers. When IJVs implement their innovation strategy in emerging markets, they should realize the importance of political ties. In addition, they should be aware of the rapidly changing market and political environments and must be ready to adapt to new situations and circumstances.

The structure of this study is organized as follows: First, we briefly review the literature discussing how political ties affect IJVs’ innovation strategy. Then, we develop three research hypotheses to illustrate how and when political ties affect IJV’s R&D investment in China. Next, we describe the data collection process and the methodology applied to examine the hypotheses. Finally, we present our test results and conclude with a discussion of contributions and limitations.

Theory and hypotheses development

The influence of political ties on business practices has been embedded in Chinese history since ancient times and continues to play a crucial role in China’s unique institutional context (Ma et al., 2019; Yang, Ma, Zhang, & Hong, 2018). Previous literature documents that political ties can help firms gain legitimacy and access scarce resources (Ge et al., 2017). In addition, firms with political ties enjoy various favorable government policies and financial support. We argue that these political ties support higher levels of R&D investment, but that the relationship between political ties and R&D investment varies based on the level of market turbulence and governmental policy turbulence the IJV encounters.

Political ties and R&D investment

Political ties are defined as a firm’s formal and informal social connections with government officials in various levels of administration (Sheng et al., 2011). It is widely considered one of the most important sources of social capital for IJVs entering and competing in a foreign country (Frynas et al., 2006; Sun et al., 2010). However, evidence supporting the critical role of political ties to firms’ R&D investment is mixed. Many scholars argue that firms with political ties tend to invest more on R&D projects (Zhou & Poppo, 2010). The central argument is that R&D projects normally require consistent commitment and can incur large sunk costs. Political ties can facilitate firms’ access to external financial resources. Furthermore, favorable governmental policies, and the interpretation of those policies, are considered to be a critical prerequisite for the success of R&D projects in China (Guo et al., 2014). In addition, with strong government endorsement, firms with political ties are able to better protect their IPRs, thereby reducing the risk of IPRs infringement by their competitors (Sinkovics & Zagelmeyer, 2018). As a consequence of these factors, political ties could encourage firms to increase their investment in R&D projects.

Other scholars, however, argue that political ties might reduce firm’s incentives to spend on R&D investments. A central theme in these arguments is that gaining political ties at the various bureaucratic levels in China is time-consuming and costly due to the intricate nature of political ties (Lin et al., 2011; Yang, Ma, Zhang, & Hong, 2018). Therefore, managers of firms relying on political ties might get distracted by putting too much emphasis on political capital investments at the expense of the necessary attention and resource investments required by R&D projects. Furthermore, some managers have become accustomed to enjoying the “shortcut” gained from political ties and overlook the importance of R&D to firms’ long-term performance (Sinkovics & Zagelmeyer, 2018).

There is another group of scholars who found that the impact of political ties on IJVs’ R&D strategy and performance is more dynamic rather than static. For example, Sun et al. (2010) found that political ties could initially reduce pressure on first movers to invest more on R&D before other foreign competitors enter the market. However, that benefit could decline or even turn negative over time. Similarly, Frynas et al. (2006) argued that the causal relationship between political resources and first-mover advantage is a complex one. While nonmarket strategies, such as R&D investment, can be used successfully by first movers, they can also be used by late movers to neutralize first-mover advantages. Thus, they suggested that IJVs should adjust their R&D investment base on the timing or entry.

The inconsistent findings in the existing literature suggest that research on the impact of political ties on IJV’s innovation strategy remains somewhat embryonic. To better understand this issue, we explore how political ties and the host country’s unique institutional and industrial context influence IJV’s R&D investment in China, which is one of the largest emerging economies in the world.

Political ties are vital for IJVs competing in China because such political ties provide many benefits in the Chinese business environment (Bai et al., 2019; Yang, Ma, Zhang, & Hong, 2018) . For example, political ties can help firms secure scarce financial and regulatory resources to deal with uncertain environmental changes. Political ties can also enable firms to obtain useful internal information, gain exclusive institutional endorsements, and overcome administrative interventions by enforcing contracts and settling negotiations. While the issues regarding the importance of political ties to IJVs competing in China have been discussed, the issues related to how political ties influence IJV’s decisions on R&D investment have received considerably less attention. We offer four explanations explicitly addressing why political ties will help IJVs use R&D investments to overcome their competitors. First, political ties could empower IJVs to expand business networks and cooperate with local business partners. The increasing cost and complexity of R&D projects has made it more difficult for companies to finish R&D projects independently (Un & Rodríguez, 2018). In response to this, more IJVs have begun using cooperative innovation strategies to implement R&D projects. Political ties enable those IJVs to better navigate potential partners.

Second, political ties could help IJVs gain administrative support from local governments. Strong political connections can allow IJVs to gain favorable treatment from the Chinese government, which still controls a vast majority of scarce resources such as land and low-interest loans (Sheng et al., 2011). Preferential access to these resources could provide IJVs more financial and human capital and encourage them to increase R&D investment. The effects of political ties with government on competitive position of IJVs are a critical determinant for their R&D investment because governmental regulation frequently has asymmetric effects on IJVs’ commitment on their investment on innovation (Frynas et al., 2006).

Third, political ties can be developed through IJV managers’ “networking and boundary-spanning activities,” and these can be positively related to R&D investment, thus enhancing innovation commitment (Sheng et al., 2011). Political ties can thus augment an IJV’s network and political legitimacy, which can, in turn, increase institutional support that helps the IJV obtain both governmental resources for their R&D investment and new technological market opportunities (Hemmert et al., 2016). This is critical because governments control substantial “scarce and valuable resources” and thus have significant influence on industry development plans and regulatory policies that are directly associated with individual IJV’s R&D investment (Li & Zhou, 2010).

Fourth, it is easier for IJVs with political ties to seek legal protection from the government if their technologies or IPRs are stolen or breached by competitors (Sinkovics & Zagelmeyer, 2018). Due to China’s feeble IP laws, IJVs can find their R&D investments partially or even fully negated by leaks to competitors. With administrative protection from the Chinese government, IJVs are less hesitant to invest in R&D projects. Based on the aforementioned arguments, we hypothesize the following:

Environmental contingencies and R&D investment

A basic premise of the environmental determinism perspective (Hrebiniak & Joyce, 1985) is that corporations can improve organizational efficiency by maintaining a fit between the contingencies of the environment and the organization (Johns, 2006; Yang, Ma, Zhao, et al., 2018). Accordingly, firms should modify their strategy toward R&D investment to accommodate their internal operating capabilities and to be consistent with external environmental constraints.

We believe that the environmental contingency view could better explain IJVs’ R&D investment strategy and the importance of the firm’s political ties in emerging economies for two reasons. First, due to the liabilities of foreignness, IJVs suffer many competitive disadvantages, such as less access to local resources and weak negotiating power relative to their local competitors. These disadvantages could significantly limit their capability and willingness to invest in R&D projects. Second, unlike developed economies that normally feature well-established business rules and relatively predictable and consistent institutional environments, companies in emerging economies generally face much more turbulent environments due to ongoing market reforms and frequently changing governmental policies (Khan et al., 2015; Zhang et al., 2007). Thus, IJVs might face dramatically different levels of market turbulence and governmental policy turbulence when they compete in those emerging economies. For example, because of the rapid wealth growth at both the national and individual levels, consumers’ preference and taste are upgraded more frequently and changed more dynamically in those emerging economies than in developed countries. Thus, IJVs in different industries might face various levels of pressure to innovate new products to meet consumers’ rapidly changing needs. In addition, the government support varies significantly across different regions in China as a result of uneven economic and institutional reforms (Sheng et al., 2011). IJVs could also face varied policies and regulations toward innovations as a result of these regional imbalances. Because R&D investment normally requires consistent and long-term commitment, turbulent governmental policies might challenge IJVs’ determination to invest in R&D projects due to the high uncertainty. As suggested by the environmental determinism perspective, firms should innovate by maintaining a fit between the environmental contingencies and internal conditions (Johns, 2006). Therefore, if they ignore the market turbulence and governmental policy turbulence, IJVs might suffer huge losses on R&D investment in the long run.

Market turbulence

Market turbulence represents the instability of consumer preferences and expectations (Kohli & Jaworski, 1990). Companies in different industries face dramatically different levels of market turbulence. In general, market turbulence tends to be high in the electronics and entertainment industries because firms in those industries continuously modify their products to meet consumers’ rapidly changing needs (Kumar et al., 2011; Yang, Ma, Zhao, et al., 2018). The environmental contingency view suggests that market turbulence could enhance the positive influence of political ties on IJVs’ R&D investment for two key reasons. First, IJVs from developed countries normally have more international experience and advanced technology than their local competitors. When market turbulence is high, consumers tend to have stronger desires for new products and technologies that create corresponding demand for R&D. IJVs typically consider these new needs as a great opportunity to attract new customers and make their businesses grow. With greater government endorsement and administrative support, IJVs with political ties could have more financial resources and less concern about the operating risks associated with R&D projects. They are therefore more likely to invest in R&D.

Second, previous research has shown that when firms face high market turbulence, the closeness of their bonds with customers and suppliers becomes more apparent (Kumar et al., 2011; Xiong & Bharadwaj, 2011). The ability to tap customers and suppliers for R&D insight is critical in turbulent market environments. IJVs normally lack the strong customer and supplier support their local competitors enjoy. Political ties, however, can help IJVs overcome this issue and gain endorsement with their business partners. Existing literature reports that consumers can provide highly novel ideas for their suppliers because the customers are not constrained by a firm’s corporate culture or operating routines (Mahr et al., 2014). Since client success can lead to more business, suppliers also have strong motivation to work with trusted customers on new product development, process improvement, and the exchange of personnel to facilitate knowledge transfers (Un & Rodríguez, 2018). Accordingly, IJVs with political ties can benefit from R&D collaboration with both customers and suppliers through various ways such as favorable payment terms or technology transfers. Thus, when market turbulence is high, more robust support from governments tends to give IJVs greater motivation to fulfill consumers’ new demands via R&D investment. Based on these arguments, we hypothesize the following:

Governmental policy turbulence

Emerging economies like China are characterized by industries in transition, inefficient markets, and active government involvement (Baglieri et al., 2014; Xu & Meyer, 2013). Rapid institutional reforms heighten uncertainty in the business environment and challenge IJVs to adapt to a swiftly changing rulebook (Xu & Meyer, 2013). Although China’s central government attempts to build a unified system to attract foreign direct investment and facilitate IJVs’ operations, uneven economic and political reforms mean that government support can vary wildly across regional or bureaucratic lines (Sheng et al., 2011). While some provinces in China are keeping their governmental policies relatively consistent to lure foreign companies and make local economies grow, many other provinces have frequently changed their local policies toward IJVs as their economic reforms are stymied or even rolled back (Banalieva et al., 2015). As such, IJVs might experience dramatically different levels of governmental policy turbulence across different regions in China. By definition, governmental policy turbulence refers the transparency and stability of local governmental policy (Yang, Ma, Zhao, et al. 2018). It represents the development level of regional economic and political environments. If a province provides relatively consistent policies and regulations for IJVs, then we consider it to have low governmental policy turbulence. In contrast, if a province frequently changes their policies and regulations, it will be very difficult for IJVs to implement their long-term strategies and operations. Thus, IJVs in that region might face high governmental policy turbulence.

We suggest IJVs with political ties might invest less in R&D projects when they experience high governmental policy turbulence for two reasons. First, turbulent governmental policy entails substantial risk for business operations, which is difficult for IJVs to absorb (Slangen & Beugelsdijk, 2010). As we discussed above, the R&D projects normally require long-term commitment and substantial monetary and human resource investments. When governmental policy turbulence is high, IJVs will face rapid changes in investing, financing, and operating policies. IJVs with political ties understand that they might lose the support they initially gained from the administration. Under these circumstances, their liability of foreignness will make them more cautious about investing in R&D projects. In addition, a high level of governmental policy turbulence might create divergent expectations between IJVs’ foreign partners that make coordination among partners more difficult (Gulati et al., 2012). Friction and doubt among partners are antithetical to R&D investments as they typically require close cooperation and mutual trust (Zhao et al., 2005). When IJVs’ foreign partners realize that their local partner might not able to provide the same level of protection from local government as before, they are more likely to engage in opportunistic behaviors such as withholding full efforts or exhibiting a “wait-and-see” attitude toward R&D projects (Luo, 2007).

Second, as the result of the intricate nature of political ties in China, it is time-consuming and costly to build connections with government officials. When governmental policy turbulence is high, it is often accompanied by higher turnover among government officials. IJVs that witness the turnover of governmental officials might suffer the depreciation of the relational capital with certain politicians and regulators (Siegel, 2007). For example, China’s acceptance of capitalism as a way of market liberalization may reduce the influence of business–government political ties as some studies argue (Guthrie, 1998), whereas the value of the political ties can still remain even after the market liberalization as other studies argue (Kroszner & Stratmann, 1998; Park & Luo, 2001; Peng, 1994). Thus, there might be a possibility that “such [business-government] ties can be either assets or liabilities and . . . the value of business-government ties varies in the face of multiple regime changes and the onset of liberalization” (Siegel, 2007, p. 623). Also, the support from the social and human capital, which is provided by former domestic politicians, can help the IJVs better understand and anticipate the actions of the domestic government by improving the business–government relationship (Fernández-Méndez et al., 2018; González-Bailon et al., 2013). Thus, using the leverage of political ties can facilitate IJVs’ opportunities to undertake R&D investment in the home country rather than to grow abroad. In this vein, to maintain political ties and secure governmental support, they are more likely to spend more time and resources on weaving connections with different governmental officials than investing on R&D projects. Based on the aforementioned arguments, we hypothesize the following:

Method

Data

Our sample was composed of all manufacturing IJVs listed on the Shenzhen Stock Exchange in China. Since the major function of the Shenzhen stock exchange is to offer a platform for private firms rather than state-owned firms to resolve financing problems in the entrepreneurial process, firms listed on the Shenzhen exchange serve as a viable representative research sample of IJVs operating in China. The Shenzhen exchange, which was launched on May 27, 2004, included 903 firms by the end of December 2017. In the current study, we first excluded firms in the utility and service industries because of substantial comparative differences with manufacturing firms in both operational models and underlying managerial processes (Patel & Chrisman, 2014). Next, we excluded firms without any type of foreign partnership. Finally, we manually collected data from each firm’s prospectus and 6-year financial reports (2012–2017). Our data collection process yielded a unique panel data set with a sample of 224 IJV manufacturing firms and 1,344 observations. Among those 224 IJVs, 116 companies were identified with political ties. In addition, 200 IJVs have partner(s) from developed countries. The average foreign ownership is 30.59%.

Measures

Dependent variable

The dependent variable in this study is firms’ R&D expenditures over sales. This reflects firm-specific R&D expenditures adjusted by firm size. Consistent with prior studies (Chen & Miller, 2007; Gentry & Shen, 2013), we measured R&D intensity as the average percentage of firm R&D expenses over sales during six consecutive fiscal years with t + 1.

Independent variable

Informed by previous literature (Ge et al., 2017; Wang & Qian, 2011), we used the IJV top management team’s affiliation with the state’s political councils as an important indicator of political ties. We manually collected this information from each firm’s initial public offering (IPO) prospectus, annual financial reports, and China’s stock exchange website. We checked whether the firm’s top management team served as a representative in the Chinese People’s Political Consultative Conference (CPPCC) or National People’s Congress (NPC) at the national, provincial, city, or county level. These councils are the most critical political institutions in which entrepreneurs can participate and both can provide political connections to their members (Jia, 2014). We coded political ties as a dummy variable (yes = 1; no = 0).

Moderating variables

The first moderating variable is market turbulence. Following existing approaches from leading marketing journals (Chung & Low, 2017; Saboo & Grewal, 2013), we measured market turbulence as the average ratio of sales and marketing expenses to the sales of the firms within the same standard industrial classification (SIC) code. The logic behind this is that industries with stable consumer preferences normally do not require big investments in marketing activities such as market branding and promotion. Thus, marketing expenses should increase as market turbulence increases (Saboo & Grewal, 2013).

The second moderating variable in our model, governmental policy turbulence, refers to the transparency and stability of local governmental policy. It integrates both the development of a market economy and the level of financial policy transparency at the provincial level. The logic behind this is that if a province has a higher level of financial policy transparency and a higher level of market economy, then it typically has a relatively stable business environment and predictable governmental regulations for IJVs competing in China. It was measured by archival data reported by the Chinese Academy of Social Sciences. Their reporting grades the transparency and stability. We use a 6-year average (2012–2017) value to represent a firm’s regional governmental policy turbulence.

Control variables

To account for potential confounding factors, three individual-specific (CEO age, CEO education, CEO technological background), six firm-specific (firm size, firm age, return on assets [ROA], nationality of foreign partner, percentage of state ownership, and percentage of foreign ownership), and one industry-specific (manufacturing industry type) variables were controlled in this study. Following Conyon et al. (2015), we defined the CEO’s technology background based on whether the IJV’s CEO had either an advanced degree in engineering area or had served in the firm’s R&D department for more than 1 year. Technology background is treated as a dummy variable by assigning a value of 1 to CEO with a technological background and 0 to CEO without.

Following existing literature (Arthurs et al., 2008), firm size was measured by the natural logarithm of the firm’s total assets. ROA was measured by firm average net income divided by total assets. We coded the nationality of a foreign partner as a dummy variable. We assigned 1 if the foreign partner was from a developed country and 0 if the foreign partner was from other emerging economies. Foreign ownership represents the percentage of foreign ownership within the IJV. Similarly, state ownership represents the percentage of state-controlled ownership within the IJV. To control for the influence of manufacturing industry type, we followed previous literature (Garcia & Calantone, 2002; Tsai & Yang, 2014) and coded manufacturing industry type as a dummy variable, which was coded 1 if the firm operated in high-technology industries or 0 if the firm operated in low- or medium-technology industries. Some examples of products from high-technology industries are communication equipment, aerospace product and parts, precision instruments, and medical equipment.

Results

Descriptive statistics and correlation analysis

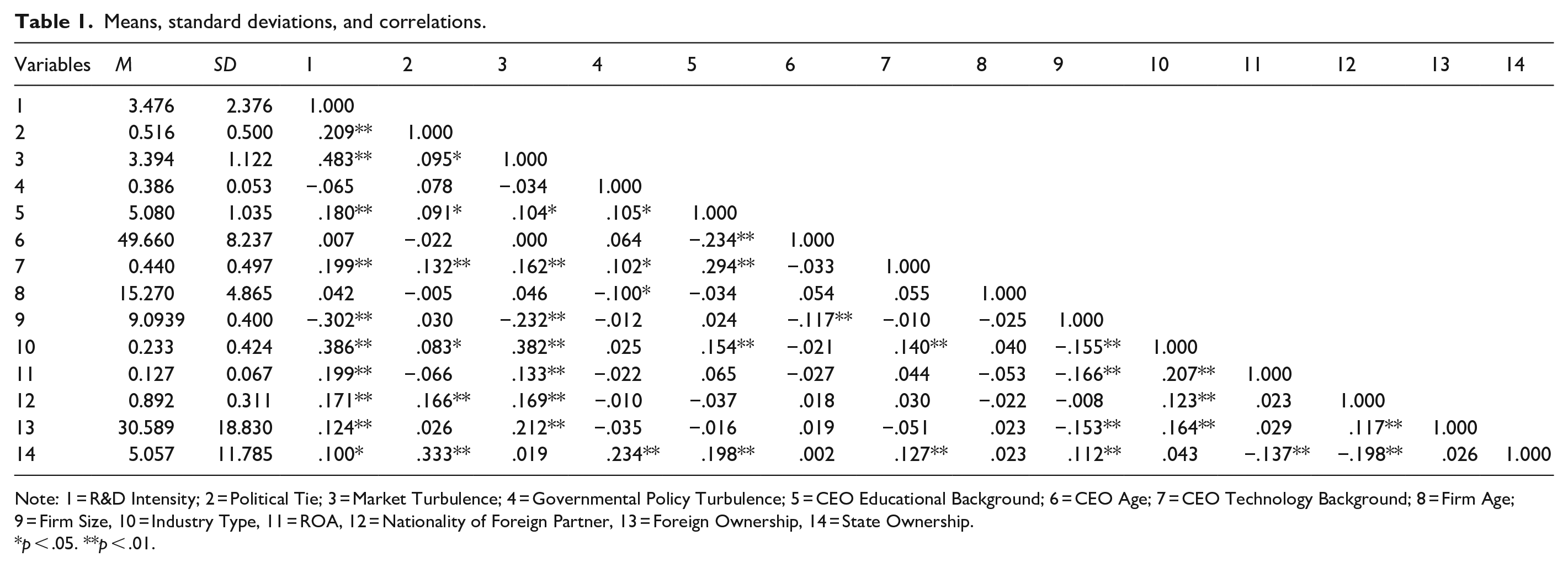

In Table 1, we report the means, standard deviations, and correlation coefficients for the study. As Table 1 shows, IJV’s R&D intensity is positively and significantly correlated to firm’s political ties (r = .209, p < .01), CEO educational background (r = .180, p < .01), CEO technological background (r = .199, p < .01), industry type (r = .386, p < .01), ROA (r = .199, p < .01), nationality of foreign partner (r = .171, p < .01), state ownership (r = .100, p < .05), and foreign ownership (r = .124, p < .01). In addition, R&D intensity is negatively correlated with firm size (r = −.302, p < .01). Overall, these correlations suggest that multicollinearity among the predictor variables is not problematic because the correlations are all below the threshold of .65 (Cao et al., 2009).

Means, standard deviations, and correlations.

Note: 1 = R&D Intensity; 2 = Political Tie; 3 = Market Turbulence; 4 = Governmental Policy Turbulence; 5 = CEO Educational Background; 6 = CEO Age; 7 = CEO Technology Background; 8 = Firm Age; 9 = Firm Size, 10 = Industry Type, 11 = ROA, 12 = Nationality of Foreign Partner, 13 = Foreign Ownership, 14 = State Ownership.

p < .05. **p < .01.

Before testing the hypothesized interactions, we mean-centered the predictors and then created the two-way interaction terms by multiplying the two mean-centered predictors together. This allowed us to avoid multicollinearity between the predictors and the interaction terms (Aiken et al., 1991). We used the variance inflation factor (VIF) to examine the effect of multicollinearity. The VIF values associated with the mean-centered predictors and interaction terms ranged from 1.028 to 1.682, all of which are well below the acceptable upper limit of 10 (Hair et al., 1998). Again, these results suggest that multicollinearity is not a problem in the present study.

Hypothesis testing

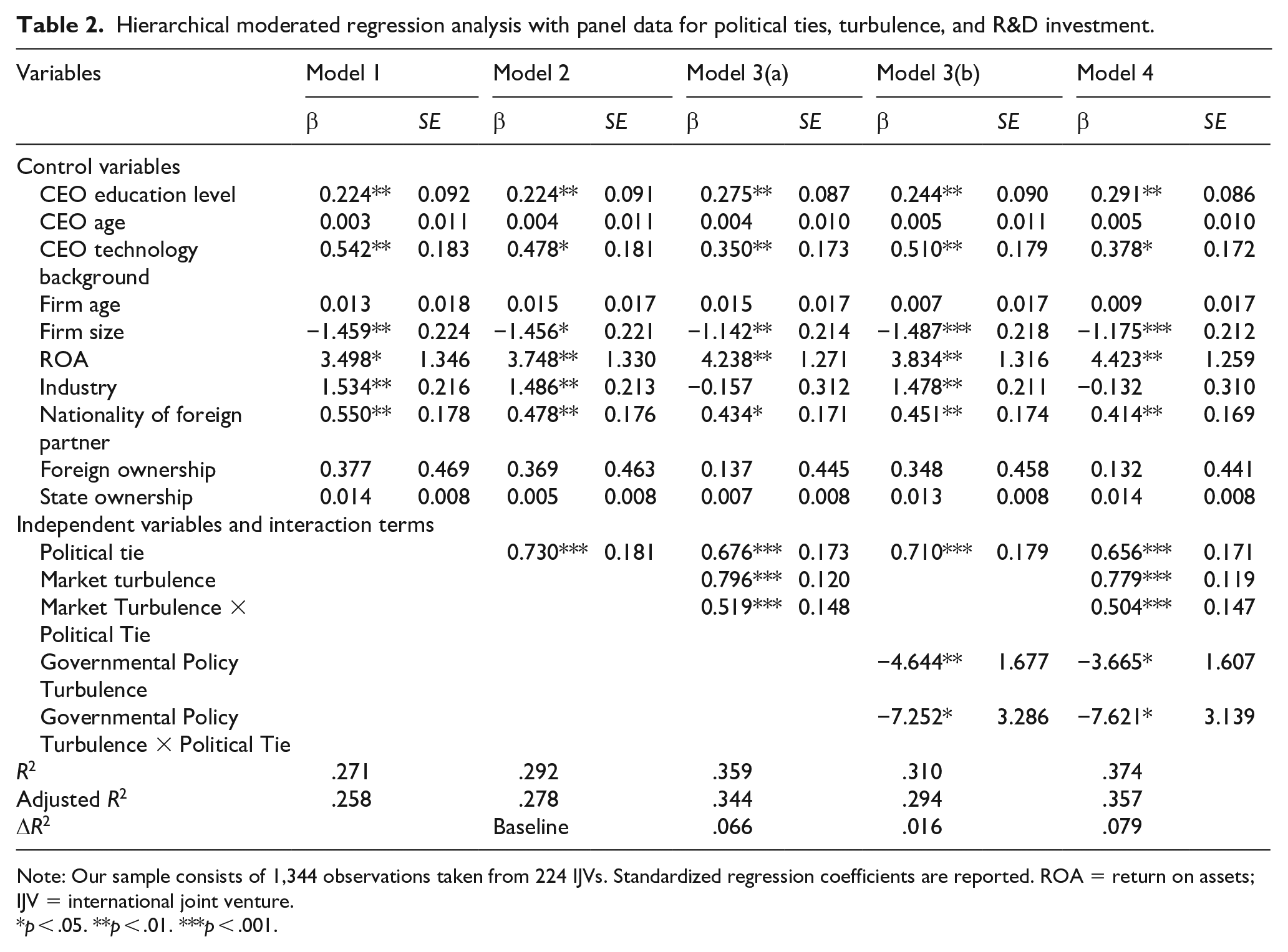

This study used hierarchical moderated regression analysis (HMRA) with panel data and followed Aiken et al. (1991) to test the hypotheses. In HMRA, there are two statistical requirements for determining the existence of an interaction term (Bedeian & Mossholder, 1994; Bing et al., 2007). We used five models in Table 2 to show the overall model fit improvement as the variables of interest were added to the analysis. A set of control variables were first included in Model 1. The independent variable, IJV’s political ties, was then added to the control variables in Model 2. As shown in Model 2, IJV’s political ties have a positive and significant effect on firm’s R&D intensity (b = 0.730, p < .001), which provides support for Hypothesis 1. The R2 change from Model 1 to Model 2 is also significant (ΔR2 = .020, p < .001). Two moderators were separately tested in Model 3(a) and Model 3(b). Because Model 2 includes the main effect, we used it as the baseline model to evaluate the improvement in Models 3(a) and 3(b). The R2 change from Model 2 to Model 3(a) is significant (ΔR2 = .066, p < .001), and the interaction term between market turbulence and IJV’s political ties is also positive and significant (b = 0.519, p < .001). Thus, Hypothesis 2 is supported. In addition, the R2 change from Model 2 to Model 3(b) is significant (ΔR2 = .016, p < .01). As predicted, the interaction term between governmental policy turbulence and IJV’s political ties is negative and significant (b = −7.252, p < .05), providing support for Hypothesis 3. Our hypotheses are illustrated by Figure 1. Finally, we examined all variables in Model 4. The R2 change from Model 2 to Model 4 is significant (ΔR2 = .079, p < .001). Market turbulence (b = 0.504, p < .001) and governmental policy turbulence (b = −7.621, p < .05) are significant moderators of the relationship between IJV’s political ties and R&D investment.

Hierarchical moderated regression analysis with panel data for political ties, turbulence, and R&D investment.

Note: Our sample consists of 1,344 observations taken from 224 IJVs. Standardized regression coefficients are reported. ROA = return on assets; IJV = international joint venture.

p < .05. **p < .01. ***p < .001.

Conceptual model of IJV’s political tie and R&D intensity.

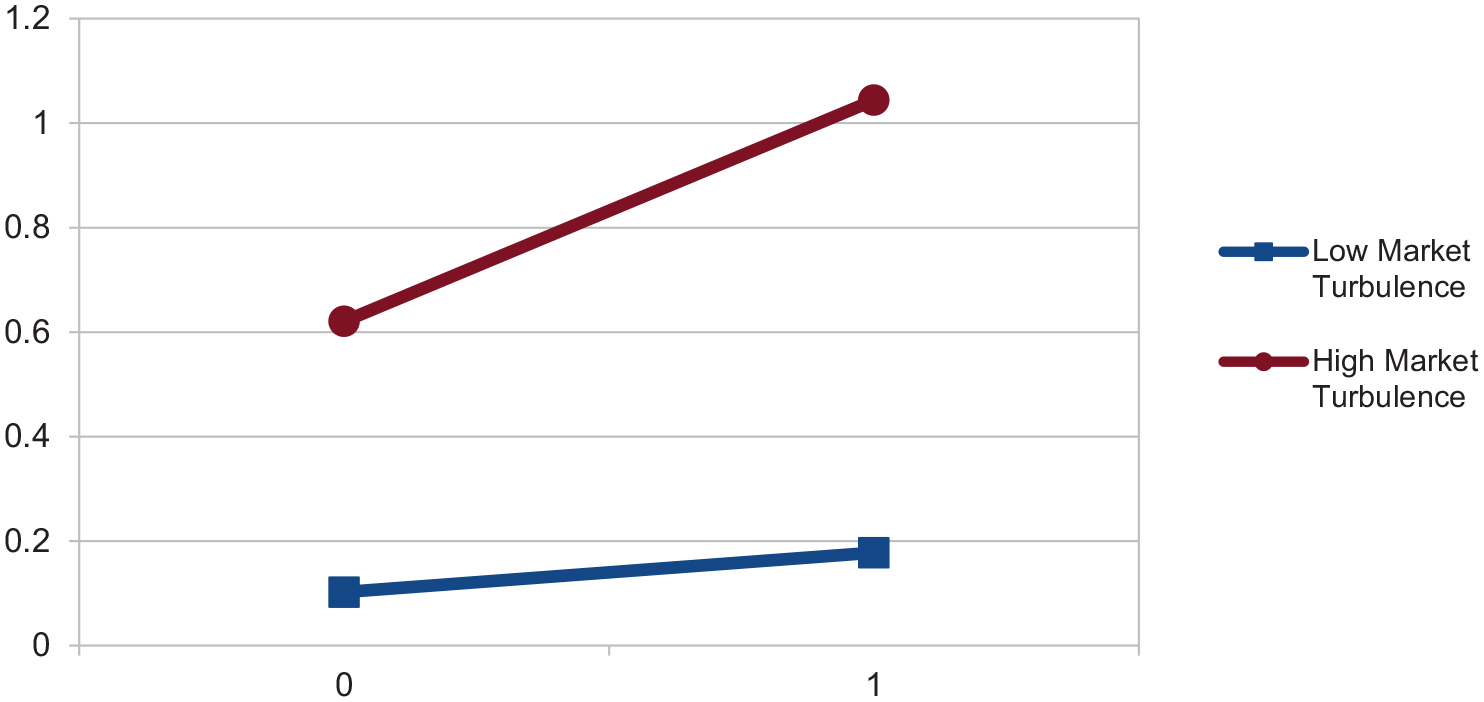

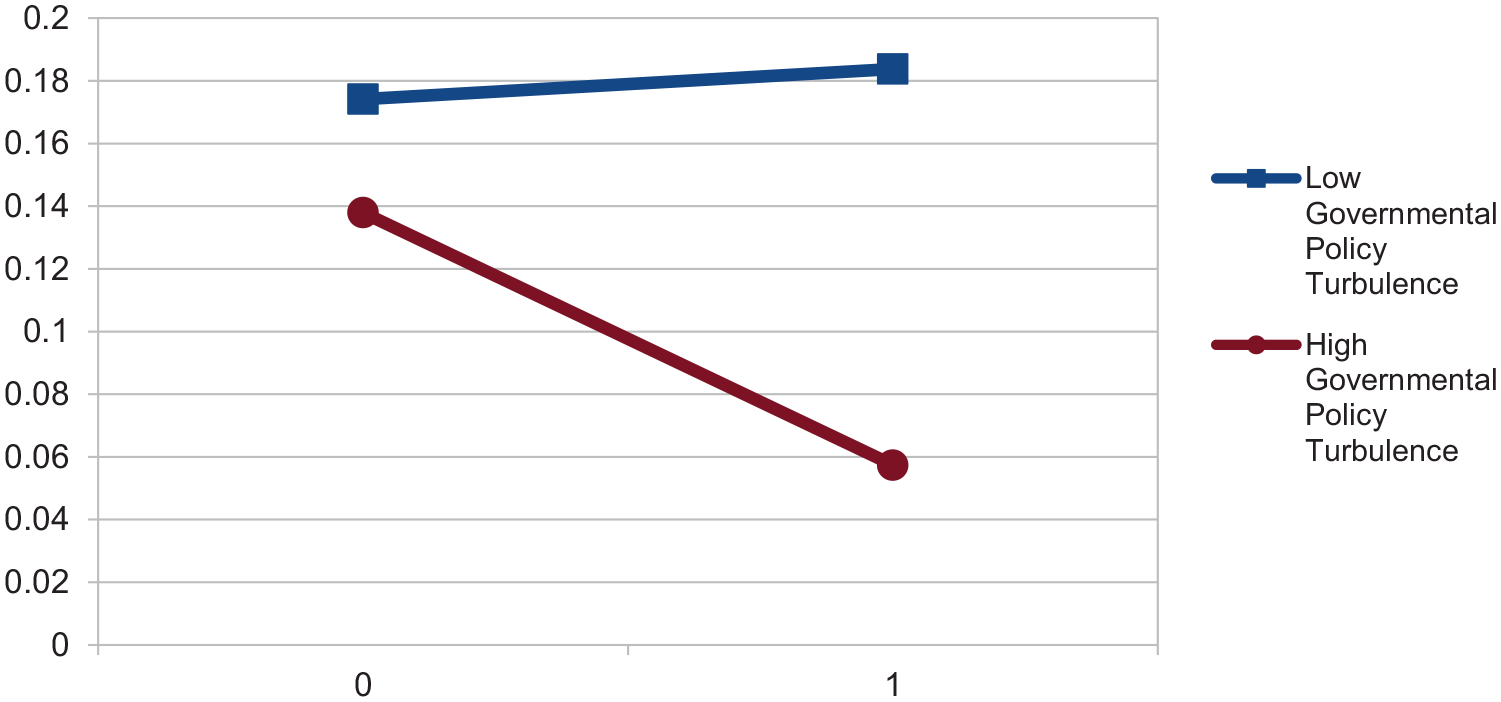

We further plotted the interaction effects in Figures 2 and 3. Specifically, we used three standard deviations above and below the mean as the values for comparison. As shown in Figure 2, the positive effect of political ties on R&D intensity is stronger under high market turbulence and weaker in low market turbulence. Similarly, in Figure 3, the original positive effect of political ties on R&D intensity is reversed under high governmental policy turbulence, confirming the negative moderation effect of governmental policy turbulence.

Moderating effects of market turbulence on the relationship between IJV’s political ties and R&D intensity.

Moderating effects of governmental policy turbulence on the relationship between IJV’s political ties and R&D intensity.

Robustness test

To validate the robustness of our results, we consider IJVs’ political ties as a continuous variable coded as 1 at the county level, 2 at the city level, 3 at the provincial level, and 4 at the national level. The regression test shows that IJV political ties has a positive and significant effect on firm’s R&D investment (b = 0.447, p < .001), which provides support for Hypothesis 1. In addition, the interaction term between market turbulence and R&D investment is positive and significant (b = 0.323, p < .001), suggesting that Hypothesis 2 is supported. Finally, the interaction term between governmental policy turbulence and R&D investment is negative and significant (b = −4.473, p < .05), providing support for Hypothesis 3. In summary, all three hypotheses supported in the initial analyses are supported in the robustness tests, which provide increased confidence in the stability of the support for each of the hypotheses.

Discussion

Previous studies on IJVs’ R&D activities draw on different logics and show mixed findings because they do not consider the fit between firms’ internal capabilities and external operating environments, which is particularly critical in an emerging market or transition economy context like China. IJVs tend to be more sensitive to environmental change and risk-taking activities because they lack their local counterparts’ relatively strong governmental support and local resources. In addition, unlike developed countries which enjoy comparatively stable economies and established business regulations, emerging markets such as China experience rapid market transformations and fundamental industrial shifts. To optimize performance, IJVs’ top management must modify their innovation strategy to fit the local business environment.

To resolve the disagreement in the literature, we applied the environmental determinism perspective to articulate a contingency view of IJVs’ dynamic decision-making procedures with respect to R&D investments in emerging economies. The empirical results indicate that due to the critical role of political ties in China, strong governmental support tends to give IJVs with political ties confidence to invest more on R&D activities than competitors. In addition, IJVs with political ties tend to asymmetrically modify their intensity of R&D investment under turbulent business environments. They tend to invest more under high market turbulence and less when governmental policy turbulence is high.

Theoretical contributions

The results of the current work allow us to offer two major theoretical contributions to the existing literature. First, because political ties are widely considered as one of the most critical social capitals for IJVs competing in emerging economies, and firm’s R&D project normally requires large sunk cost and long-term commitment, there is an urgent need to understand how political ties could affect IJVs’ R&D strategy in those emerging economies. In addition, the competing logics and mixed findings from the existing IJV literature reflect the somewhat embryonic state of research in IJVs’ R&D strategy. Our study extends current research by exploring the relationship between political ties and IJVs’ R&D strategy in China as one of the largest and most influential developing economies in the world. Thereby, we provide additional empirical evidence and new insights to this growing research domain.

Second, our study applies the environmental contingency view to explore the impact of political ties on IJVs’ R&D strategy in China. Because IJVs are not isolated islands, but rather are deeply embedded in a nexus of socioeconomic relationships which make the local business environment influential on strategic decisions (Khan et al., 2015), they should constantly modify their innovation strategies to fit the dynamically changing external environment. This is especially critical for IJVs competing in emerging economies experiencing rapid market transformation and institutional reform. By drawing on the environmental contingency perspective, our study provides a contingent view to better understand how market and governmental policy turbulences affect IJVs’ R&D decisions in emerging economies.

Managerial implications

In addition to the aforementioned theoretical contributions, our study has important managerial implications for IJV managers and government policy makers in emerging economies. Although it is generally beneficial for IJV managers in emerging economies to build connections with various levels of government, they should remain cautious during periods of high governmental policy turbulence. This is especially necessary when competing in China, where the general lack of IP protection makes costly R&D investment perilous without government support. Absent political influence, IJVs have little recourse if IP is stolen by local partners or competitors. In addition, business managers should understand the importance of environmental turbulence to IJVs’ strategic decision-making process. When IJVs experience high market and governmental policy turbulence, their strategic decisions might change due to different levels of perceived risk, uncertainty, and transaction costs.

On the other side, government policy makers in emerging economies should work to provide a stable institutional environment with transparent and consistent policy to inspire R&D investment from IJVs. Since firms’ competitive advantages and long-term success are largely determined by their technological capability, fostering innovation is a key component to sustainable growth. Furthermore, our study also provides practical implications for outside investors. Existing research has suggested that firms with greater incentives to invest in R&D tend to have a better chance capturing emerging business opportunities (Rodríguez & Nieto, 2016; Spieth et al., 2014). Therefore, they are more likely to obtain the first-mover advantage and achieve success in the global market (Cleff & Rennings, 2012). Viewed from this perspective, we recommend that investors pay close attention to IJVs’ political connections and market and governmental policy contingencies.

Limitations and future research

Like all research, the present study is not without limitations. However, these limitations present opportunities for future research. First, since R&D investments normally require long-term commitment, IJVs might not able to capture its benefits in the short run. Another point of interest is the reinforcement of innovation through the coevolution of IJVs and their local environments (Cantwell et al., 2010; Un & Rodríguez, 2018). In this study, the short timeframe of our panel data might prevent us from analyzing this coevolution.

Second, as a result of our data constraints, we measure firms’ R&D investment by their total input on innovation without differentiating various types of innovation activities. However, different firms might focus on different types of innovations. For example, some start-ups might invest more on revolutionary new technologies, whereas established firms might put more emphasis on incremental improvements for their existing technologies. Future studies might dig deeper into this topic and generate a more detailed understanding about IJVs’ R&D activities.

Third, Martínez-Noya and Narula (2018) argued that “alliances have become dispersed worldwide, formed with partners in both developed countries as well as in developing ones,” and alliances “also involve more complex activities that require a higher intensity of cooperation” (p. 206). Hence, this complexity of managing IJVs’ R&D investment may lead to the failures of IJVs. However, the present study does not address this issue, so future research in this area is needed.

Fourth, Diéguez-Soto et al. (2019) argued that “R&D investment is a fundamental influence on competitiveness and national development and may result in superior performance and growth” (p. 107). However, in this study, we do not include the link between R&D investment and firm performance or growth. Future research should investigate this link between IJVs’ R&D investment and its performance or growth.

Finally, because the scope of our study is also limited, we were not able to fully address several issues such as the impact of IJVs’ industry structure and market orientation on their R&D strategy. Future studies using more comprehensive data sets across a longer period could better examine IJV’s R&D phenomenon.

Conclusion

In conclusion, our study extends the findings of current empirical research by exploring IJVs’ R&D activities in the world’s largest emerging economy, China. IJVs’ approach to R&D investment is unavoidably influenced by their respective institutional and industrial environments. Due to the unique nature of the Chinese market, this influence is even more prevalent and substantial. Our results show that IJVs with political ties tend to invest more in R&D. More interestingly, we found market turbulence intensifies the positive relationship. In contrast, governmental policy turbulence mitigates this relationship. These asymmetric contingency effects can give the academy, managers, and policy makers critical insights to pave the way of future research.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.