Abstract

In the process of operation, firms will face different types of performance pressure. The inconsistency among multiple performance pressure signals has an important impact on resource allocation and R&D investment. However, at present, studies on the impact of multiple performance pressures on the firm’s resource allocation and R&D investment are very limited, and few studies have analyzed the impact of inconsistencies among multiple performance pressure signals on the firm’s R&D investment. Given this research gap, this article empirically tested a model from the perspective of behavioral agency theory, in which inconsistency in long- and short-term performance pressure facilitates the accumulation of organizational slack. We further test the impact of an increase in organizational slack on the firms’ R&D investment intensity and find that this effect is stronger when the level of managerial ownership is comparatively low. These results together indicate that high inconsistency in performance pressure and low managerial ownership jointly facilitate the accumulation of organizational slack, enabling firms to go beyond local search and have more slack searches in the face of multiple performance pressure, which is conducive to an increase in R&D investment.

Keywords

Introduction

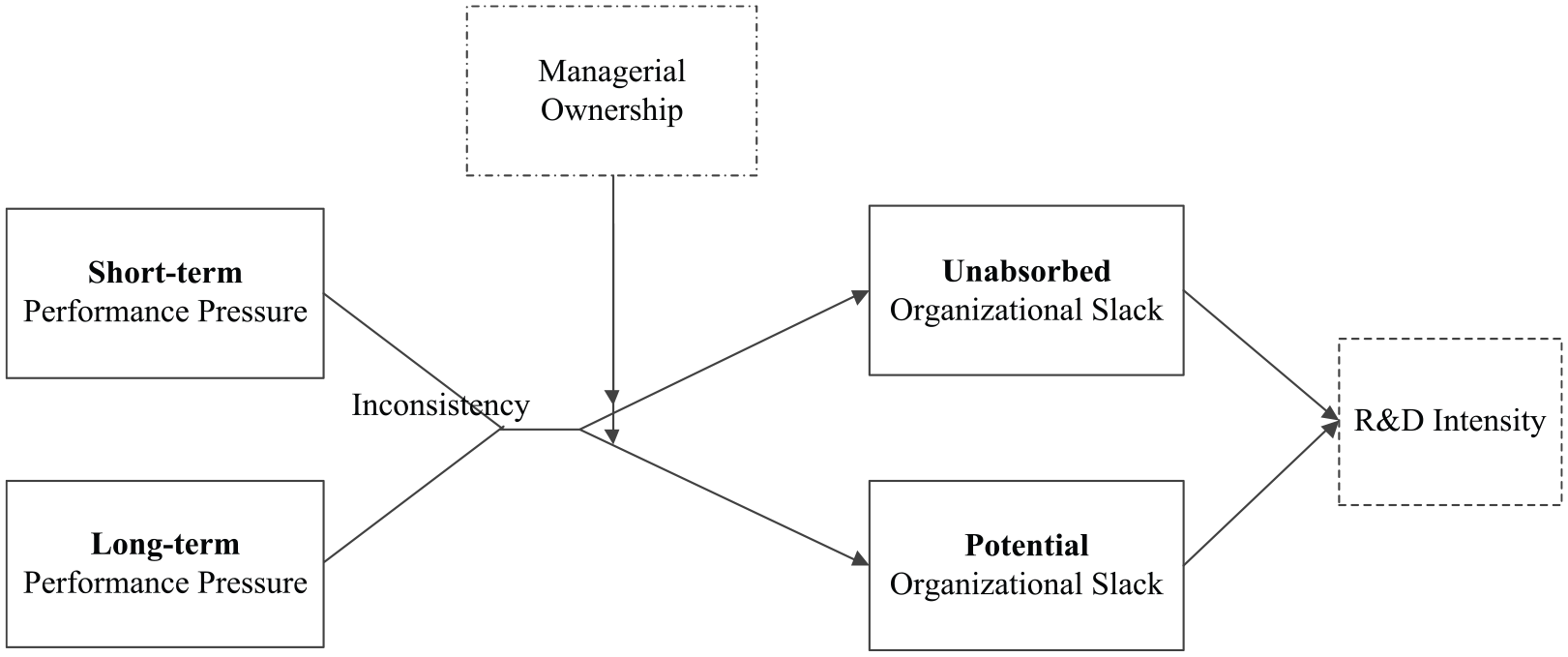

The aspiration of a firm is the minimum expectation level that a firm can accept for its own performance (Greve, 2003). Any performance above this level (i.e., positive performance feedback) is acceptable and satisfactory, while performance below this level (i.e., negative performance feedback) is unacceptable and unsatisfactory, and should be addressed by initiating a problemistic search (Cyert et al., 1963). From this definition, negative performance feedback is a source of performance pressure of the firm (Schneider, 1992). When the firm is faced with performance pressure, it is the most challenging time in the firm management to find the problem and start the problemistic search. To solve the performance problem, a problemistic search often requires managers to challenge existing practices, opinions, and culture (Li et al., 2018). The traditional view is that the key to solving a performance problem lies in identifying the performance pressure (Greve, 2003; Katila & Ahuja, 2002; Laursen, 2012). However, in reality, firms often face multiple and inconsistent performance pressure. Performance pressure inconsistency refers to the extent to which a firm experiences performance pressure presented different levels of severity in different reference systems. Inconsistency in performance pressure makes it more difficult for firms to quickly launch an efficient problemistic search. Firms need to reserve more time and resources (i.e., organizational slack) to deal with inconsistent performance pressure. Based on this, this study investigates the effect of inconsistency among multiple types of performance pressure. A specific focus is considered on the organizational slack, due to multiple performance pressure and inconsistencies, in order to evaluate how firms’ R&D investment decisions are affected.

On the relationship between multiple performance feedback and corporate decision making, recent studies have mainly reached the following consensus. (1) Firms prefer to make decisions based on consistent performance feedback. When there is inconsistency in performance feedback, firms willingly wait for more consistency, as there is no consistent conclusion to be made. They wait for more consistent signals before making decisions (Joseph & Gaba, 2015; Lucas et al., 2018). (2) Inconsistency in performance feedback provides more leeway for managers to interpret the performance feedback subjectively (Tarakci et al., 2018). When managers take a performance feedback that is relatively worse as a reference point, the less poor performance signal is interpreted as “a signal better than another performance feedback signal,” creating an impression that “the firm is not bad.” On the contrary, when managers take a relatively good performance feedback as the reference point, the relatively poor performance signal is interpreted as “a signal worse than another performance feedback signal,” thereby creating an impression that “the firm is very bad” (Blagoeva et al., 2019; Lv et al., 2019). We believe that for the former, the action logic of the firm is consistent with that of a firm with “poor performance near aspirations” (Ref & Shapira, 2017). In other words, the firm will take the initiative to respond to the performance pressure, actively carry out a problemistic search, and adjust its strategy to solve the problem. For the latter, the action logic of firms is consistent with that of a firm with performance well below aspirations. They do not respond to performance pressure immediately but adopt a defensive strategy dominated by a wait-and-see attitude, do not make decisions or judgments in a hurry, and tend to experiment with different solutions (Staw et al., 1981).

These aforementioned pioneering studies provide the basis for our research. Their findings suggest a new source of organizational slack that has yet to be identified: inconsistent performance pressures. When there is inconsistent performance pressure, cautious managers do not rush into decisions but wait for more consistent signals before making decisions. Such waiting time and shelved resources constitute new organizational slack. The finding is significant. First, in previous studies, the positive effect of organizational slack on the firm’s search has been widely concerned and proved. Research shows that when firms have more organizational slack, they have higher risk tolerance and are more active in innovation. For example, high-performing organizations have idle resources that employees can use for interesting projects: activities that are not directly monitored, measured, or selected by the organization (Alexy et al., 2016). In this regard, slack is particularly relevant to the firm’s innovation practices. They provide opportunities for organization members to engage in cooperation and R&D in unknown new areas (Argote & Greve, 2007). Second, in previous studies, organizational slack mainly comes from three aspects: (1) idle or waste of resources caused by low operating efficiency (Nohria & Gulati, 1996); (2) reserves of additional resources set aside as a result of conservative business strategies, which are retained to cope with unexpected risks (Gao et al., 2013); and (3) new resources, which mainly come from the positive performance feedback, that is, when the firm performance is higher than an aspiration, the higher part will be converted into the added resources of the organization and become the organizational slack available to the organization (Alexy et al., 2016). No literature has explored the relationship between inconsistent performance pressure and organizational slack. Previous literature mainly focuses on the direct relationship between the inconsistency of different performance feedback and the R&D investment decision of firms (Blagoeva et al., 2019; Joseph & Gaba, 2015; Lucas et al., 2018; Lv et al., 2019). Slack, though, is another very important way to influence firm R&D investment (Chen & Miller, 2007). Considering the important impact of slack on corporate R&D, in order to fill this gap, we will focus on the impact of such organizational slack on the firm’s R&D investment. Such organizational slack emerges when the multiple performance pressures are inconsistent. Specifically, we present and test a multi-stage model in which the organizational slack of firms mediates the relationship between the performance pressure inconsistency and the R&D investment intensity of firms. By changing the allocation of organizational slack, performance pressure inconsistency can produce an indirect impact on firms’ R&D investment decisions. On this basis, drawing on the behavioral agency theory (Patel & Chrisman, 2014; Wiseman & Gomez-Mejia, 1998), we study how managerial ownership, a commonly used incentive mechanism (Abrahamson & Park, 1994), moderates this relationship.

By examining the relationships between performance pressure inconsistency, organizational slack, managerial ownership, and the firm’s R&D investment, our study contributes to the literature in the following aspects. First, as mentioned earlier, previous studies have not yet examined the impact of organizational slack generated by inconsistencies in multiple performance feedback on problemistic search, although inconsistencies in multiple performance feedback in the same direction (i.e., all negative) have a direct impact on organizational search (Blagoeva et al., 2019; Joseph & Gaba, 2015; Lucas et al., 2018; Lv et al., 2019). Exploring these indirect effects yields interesting findings and provides inspiration to study the interaction between problemistic search and slack search. Second, we expand the theoretical framework with a behavioral agency perspective on multiple performance pressure and the firm’s R&D investment decisions. Various theoretical explanations have been proposed to understand the relationship between performance pressure and R&D investment decisions, but little attention has been paid to the influence of equity incentive arrangements made by firms to reduce agency problems on their R&D investment decisions (Blagoeva et al., 2019; Joseph & Gaba, 2015; Lucas et al., 2018). Therefore, we supplement existing theories by examining managerial ownership as another theoretical explanation of the relationship between multiple performance pressure and firms’ R&D investment decisions. Finally, our response surface analysis method proves helpful to the empirical study of performance feedback (Edwards & Cable, 2009; Mindruta et al., 2016). A key reason why it is not common to study the effect of inconsistent performance feedback on problemistic search in a multi-reference point structure is that analytical techniques that simultaneously consider multiple performance feedback signals are generally not available. By using response surface analysis technology (Edwards & Parry, 1993; Shanock et al., 2010), we establish a polynomial regression model to capture the effect of managerial ownership on the R&D investment of firms in the context of inconsistent performance pressure. In this process, we improve the research design and provide empirical evidence supporting the inconsistency effect between short- and long-term performance pressure in the context of firms’ R&D investment decisions, thus contributing to the literature on performance pressure from different time horizons (Ben-Oz & Greve, 2015).

Theory and hypotheses

Inconsistency in long-term and short-term performance pressure

Performance pressure inconsistency is essentially a kind of performance feedback inconsistency. Most studies on the inconsistency of performance feedback focus on the influence of two opposite combinations of performance feedback signals obtained by firms based on two different reference frames on firms. In different reference frames, the firm may get a positive performance feedback signal in one reference frame and a negative performance feedback signal in another. For example, in Joseph and Gaba’s (2015) research, they analyzed the influence of the negative and positive performance feedback combination on the firm’s decision making and called this combination as the ambiguity of performance feedback. In such cases, firms are in a fog, unable to make decisions because they do not know whether they are doing well or badly. Following their research, most subsequent studies focused on the joint impact of multiple performance feedback with opposite directions on the firm’s decision making. For example, Lucas et al.’s (2018) research analyzes the decision-making rules of firms in the face of negative–positive social–historical ambiguous performance feedback and believes that firms may adopt self-enhancing rules to make decisions, focusing on positive signals and ignoring negative ones. It is also possible to adopt the alarming rule to make decisions, focusing on negative signals and ignoring positive ones (Hu et al., 2017). In the end, they concluded that what kind of rules firms adopt depends on specific situational factors.

Here, we propose another special form of performance feedback combination, namely, inconsistent performance pressure. Unlike ambiguous performance feedback signals, inconsistent performance pressure signals are clear in direction. Both signals are negative performance feedback signals. The difference is that they differ in severity: firms may do rather badly in one frame of reference and “slightly less well” in another. This difference is significant. In the case of ambiguous performance feedback, there is at least one positive signal that can provide support for the firm to stick to the current strategy. However, under the circumstance of inconsistent performance pressure, the signals received by the firm are all negative, indicating that the firm has problems that need to be solved. In this case, firms need to spend extra time determining which performance issues need to be addressed first, or they need to set aside resources to wait for consistent performance feedback signals before making a decision.

Performance pressure inconsistency can occur for different reasons. First, firms need to meet different goals. Under these goals, the aspiration of the firm may be different. Consequently, inconsistent performance pressure may occur when a firm compares these performances to different aspirations. Second, firm management meets the assumption of sustainable operation. With the extension of the investment horizon, what seems small in the short term may have severe negative reactions in the long term (Ben-Oz & Greve, 2015). The change in long-term and short-term investment perspective may cause firms to experience inconsistent performance pressure.

Regardless of the origin of performance pressure inconsistency, performance pressure inconsistency poses a potential threat to the firm’s problemistic search. Since the resources of firms are scarce, firms need to spend more time and energy to determine which problems to allocate resources to solve in priority (Turner & Rindova, 2012). Second, there may also be correlations between different performance pressures (Joseph & Gaba, 2015). Studies show that when some problems are solved, others may be solved or alleviated (Colbert et al., 2008). Proper prioritization can help reduce the cost of problem-solving and improve efficiency (Meglino et al., 1991). Next, we draw on the behavioral agency theory to study the relationship between negative feedback inconsistency, organizational slack, and R&D intensity, as well as the moderating role of managerial ownership.

The behavioral agency theory

Behavioral agency theory is the research perspective adopted by this study; it combines the behavioral theory of a firm and agency theory (Wiseman & Gomez-Mejia, 1998). It is widely used for analyzing the behavior of managers and firms (Schulze et al., 2003). Its core point is that as an agent of a firm, the manager plays an extremely important role in the firm’s operation, the execution of its corporate strategy, and the allocation of its organizational resources. However, since the management’s interests are not always consistent with the interests of the firm’s shareholders, it is necessary to design an incentive mechanism for agents to manage the firm in ways that maximize the firm’s interests (X. Zhang et al., 2008). In terms of the design of the incentive mechanism, behavioral agency theory states that when corporate governance lacks an incentive mechanism, moral hazard and adverse selection of management likely occur (Schulze et al., 2001). Moral hazard refers to situations of information asymmetry in which the managers, who are responsible for corporate management, maximize their utility and may act against shareholders (Huyghebaert & Van de Gucht, 2004). The so-called adverse selection is another problem caused by information asymmetry, which means that managers have more information than a firm’s shareholders, thus benefiting themselves and damaging the interests of the firm or shareholders (Durand & Vargas, 2003). For example, when managers predict that a firm’s future performance may deteriorate and thus make decisions in advance that are not beneficial to the interests of the firm so as to protect their interest, the firm has the problem of adverse selection by the management.

In addition, behavioral agency theory has several new assumptions. Unlike the standard agency theory, which focuses on the alignment of monitoring cost and incentive, behavioral agency theory puts agent performance and motivation at the center of the agency model. Behavioral agency theory holds that, given the opportunities available, the interests of shareholders and their agents are most likely to align if agents are motivated to do their best. To some extent, it introduces the motivation crowding theory (Frey & Jegen, 2001) and goal-setting theory (Locke & Latham, 1990) to the traditional agency model, and represents a pragmatic way of contracting between principal and agent (Pepper & Gore, 2015). Specifically, this pragmatism is reflected in three new assumptions:

Time discounting

The behavioral agency theory assumes that agents discount time according to a double occurrence function, instead of discounting time in exponential form like financial discounting (Ainslie, 1991). Under the time discounting assumption, the future benefits of any delayed decision are discounted. This is particularly useful in explaining behavior that classical behavioral theories cannot. For example, taking action is enjoyable in the short run, but the actor knows that it is harmful to their well-being in the long run (Pepper & Gore, 2015). Behavioral agency theorists explain these anomalies by introducing the assumptions of time discounting. They argue that the manager’s discount to future events is hyperbolic, so the implied discount rate changes over time rather than exponentially (Ainslie, 1991). Managers usually discount time in an exaggerated way (Frederick et al., 2002; Graves & Ringuest, 2012). In the face of inconsistent performance pressure, waiting for more consistent performance feedback signals will make managers make more objective and rational decisions. However, under the influence of the exaggerated time discounting bias of “time waits for no one,” managers with managerial ownership cannot tolerate the performance gap to continue like this. Instead of waiting for more consistent signals, managers would take action to address the performance problem.

Inequity aversion

Agent theory assumes that agents are averse to inequity. If agents feel that their input is fairly and adequately rewarded, then agents will be satisfied with their work and motivated to continue to contribute at the same or higher level (Adams, 1965). Conversely, if the relationship between input and output is not proportional, then the agent becomes dissatisfied and loses momentum. Compared with managers without managerial ownership, managerial ownership will reduce managers’ perception of inequity and make managers make more active contributions. In the context of performance pressure, such proactivity can be manifested as high sensitivity to performance pressure: even if performance pressure is presented in inconsistent ways, proactive managers will still try to use slack resources to carry out problemistic search immediately.

The trade-off between intrinsic motivation and extrinsic motivation

Behavioral agency theory assumes that agents’ behavior is driven by intrinsic and extrinsic motives. According to Deci and Ryan (2010), intrinsic motivation refers to that managers perform an activity for its intrinsic satisfaction, rather than for some separable result. Extrinsic motivation, on the contrary, means that managers perform an activity for its instrumental value. Behavioral agency theory holds that external motivation can extrude internal motivation. Especially in the case of improper monetary incentive design, the increase of external rewards will lead to a decrease in overall motivation (Pepper & Gore, 2015).

It is in the best interests of shareholders to make decisions based on consistent performance feedback signals. However, as we will discuss later, due to the existence of external incentives, the internal motivation of managers to make decisions based on consistent signals will be reduced. In our case, if managers have a higher level of managerial ownership, they are more likely to make decisions before waiting for consistent signals so as to protect their own interests. Next, based on behavioral agency theory, we analyze and propose hypotheses on performance pressure inconsistency, organizational slack, managerial ownership, R&D investment, and other issues.

Performance pressure, inconsistent performance pressure, and organizational slack

Based on the behavioral agency theory, we believe that a firm is more prone to organizational slack when encountering inconsistent negative feedback than when encountering consistent negative feedback. This can be analyzed from the dimensions of moral hazard and adverse selection mentioned above.

From the dimension of moral hazard, when performance pressure is inconsistent, firms face greater moral hazard from the management. When negative performance feedback is presented in a highly consistent manner, the managers’ freedom to construct attributions unrelated to their competence becomes greatly constrained (Tarakci et al., 2018). After all, the combination of short-term and long-term performance aspirations is a credible reflection, considering many factors. As a result, consistent and severe underperformance can be a reliable indicator of managers’ incompetence, and these managers need to be held accountable for such problems. Moreover, self-enhancing attribution strategies that rationalize negative performance feedback become less feasible. In this case, the decision maker has to respond to negative performance feedback. Organizational slack represents resources that are available but not yet used by the firm. Under the accountability system, such resources are labeled as evidence of the low efficiency of resource allocation by managers. In response to performance pressure, managers have to scale back the organizational slack to show that they are “taking action” to solve problems (King, 1983). On the contrary, when multiple types of performance pressure are highly inconsistent (e.g., high short-term performance pressure vs. low long-term performance pressure), managers can use this inconsistency in performance pressure to guide outsiders to focus on long-term performance rather than short-term performance. Specifically, managers can interpret the long-term performance feedback as a relatively good performance signal compared with the short-term one and attribute poor performance to factors beyond managerial control (such as seasonal changes; Tarakci et al., 2018). In other words, inconsistent performance pressure gives management the opportunity to avoid responsibility and delay responding to performance problems. Managers who experience inconsistent performance pressure have more leeway to attribute poor performance to factors unrelated to their ability, compared with those who experience consistent performance pressure (Tarakci et al., 2018). A subjective interpretation reduces the positive impact of performance pressure and allows managers to continue to adopt a wait-and-see strategy in response to performance pressure. When the two negative signals reach a point of convergence, the manager uses organizational slack in response to performance pressure (Reuer & Leiblein, 2000). Under the wait-and-see strategy, firms preserve more free resources, time, and labor, which increase the organizational slack of firms.

From the dimension of adverse selection, managers have more information about their true competencies and the firm’s operations than the shareholders (French & Rosenstein, 1984; Y. Zhang, 2008). There is a gradual process of performance deterioration, which can be reflected in the inconsistency of multiple performance feedback signals (Lamont et al., 1994). In the initial stage of performance deterioration, firms may only see negative feedback signals of inconsistent severity. However, as the business operation problem is not properly solved, this performance deterioration becomes serious, and the negative feedback signals of different types of performance tend to become consistent. In this gradual process, as the managers have more information, they can make adjustments in advance to maximize their interests. In case of inconsistency, managers turn most resources into organizational slack to resist greater risks and prevent the deterioration of the firm’s performance from affecting their interests (Palich et al., 2000). In accordance with this analysis, we make the following hypothesis:

The moderating role of managerial ownership

From the perspective of behavioral agency theory, managers, as firms’ agents, play an important role in the firm’s decision making and resource allocation (M. Kim, 2016). Our analysis for Hypothesis 1 can be regarded as a typical case of the absence of incentives in behavioral agency theory. According to behavioral agency theory, the lack of incentives for managers leads to moral hazard and adverse selection problems (such as the retention of more organizational slack when the performance pressure does not reach a consistent level as analyzed in Hypothesis 1). As a possible solution, managerial ownership is a popular practice in behavioral agency theory, known to help alleviate the agency problem (R. Kang & Zaheer, 2018). However, in the context of multiple performance pressure, we believe that although this approach creates incentives for managers, it also has some negative effects, which have not been discussed in detail in previous studies.

Specifically, decision makers play an important role in decision making and analysis, as well as in controlling important resources and opportunities. Performance feedback results are subjective evaluations of the current performance of a firm based on a specific selected reference point that is susceptible to decision-maker bias and system bias (Ghosh & Olsen, 2009; Greve, 2002). Drawing on the behavioral agency theory, we believe that the firm’s R&D decision-making process under the context of inconsistent performance pressure signals is affected by managerial ownership.

First, compared with other firms, managerial ownership links the personal interest of managers with the performance of firms (Chang, 2003). Managers who have high managerial ownership not only directly participate in the management of firms but also control the firms and enjoy the right to distribute the earnings (Sison, 2011). In this case, the incentive of high managerial ownership motivates managers to actively respond to any signal that reflects poor performance. As the unsolved performance problems will hurt the firm’s benefit and have a negative impact on managers’ earnings, managers with high managerial ownership prefer to take relatively good performance as a reference point for upward comparison and solve the performance problem in time. They are also less likely to take inconsistency as an excuse to delay solving performance problems (Shi et al., 2017).

Second, managerial ownership increases the risk and opportunity cost of managers’ delay (in contrast to firms without managerial ownership). Moreover, with managerial ownership, as long as managers can mobilize organizational slack or organizational slack exists, these managers respond to performance pressure as soon as possible to reduce the risk and cost caused by delay. As for the reasons why managerial ownership increases the risk of delay and opportunity cost, previous studies mainly analyzed this from the perspective of personal career risk management. As far as career risk is concerned, the behavioral agency theory believes that holding shares by managers increases the concern of outsiders (especially investors in the capital market) about the problem of corporate governance (Boeker & Karichalil, 2002). With the increase of managerial ownership, outsiders think that he or she is less likely to be replaced, and the executive’s explanation of performance pressure is more distrusted (Fredrickson et al., 1988). In this case, compared with other firms, it is more difficult for managers of the firms in which the managers hold shares to dispel the doubts of the capital market with the excuse of inconsistent performance pressure. Managers not only operate firms but also own them, and a more lenient board supervision makes it difficult for managers to convince investors of their explanations for the occurrence of negative performance and to guide investors toward a downward comparison (Man Zhang & Greve, 2019). Multiple performance pressure is often accompanied by doubts in capital markets and mistrust of managers’ competence, even with consistency in performance pressure. When doubts in the capital market cannot be removed, managers eventually face a variety of adverse personal consequences, such as career crisis, re-employment risk, and reputation loss (Bogenrieder & Nooteboom, 2004). From this perspective, managers who are also shareholders of a firm have more difficulty in avoiding their management responsibilities and taking more risks than those who are not.

Third, the time discounting effect is strengthened by the managerial ownership. In this case, the manager with managerial ownership will give priority to the more severe performance pressure in the face of inconsistent short-term and long-term performance pressure. This priority focus on signals of severe performance pressure led managers making the hasty response to inconsistent performance. As mentioned earlier, under the assumption of time discounting, managers usually exaggeratedly discount time (Frederick et al., 2002; Graves & Ringuest, 2012). When there is an inconsistent performance gap, waiting for more consistent performance feedback signals will make managers make more objective and rational decisions. However, under the influence of the exaggerated time discounting bias of “time waits for no one,” managers with managerial ownership cannot tolerate the performance gap to continue like this. Instead of waiting for more consistent signals, he would take action to address the performance gap. In this case, prioritizing more severe performance pressures allows managers to respond more quickly to earlier signals of performance pressure that are not yet consistent. While this may lead to bad decisions and harm the interests of shareholders, it protects the interests of managers (e.g., the manager’s stock option awards). Specifically, the interests of managers are affected by both short-term and long-term performance. On one hand, managers with managerial ownership need to achieve certain performance (e.g., return on assets [ROA] to meet aspiration level) to exercise the right. On the other hand, when exercising the option, the stock market performance of the firm will affect the ultimate benefit of the manager after exercising. Managers gain more from exercising their rights when the firm’s market value is higher than the aspiration level. Conversely, to be below aspiration level hurts managers when they exercise power. Therefore, from the perspective of managers who have the ownership of managers, no matter whether the firm is facing long-term or short-term performance pressure, as long as the firm receives negative performance feedback signals, managers should respond immediately to avoid damage to their own interests. On the contrary, we believe that managers without managerial ownership or with a low percentage of managerial ownership will give priority to the relatively minor performance pressure signal when faced with inconsistent long-term and short-term performance pressure. Managers can use inconsistencies in performance pressures to direct outsiders to this slight performance signal. At this point, managers can interpret it as a better performance signal than another performance pressure signal, and attribute the poor performance to factors outside management control (such as seasonal changes; Tarakci et al., 2018). In other words, inconsistent performance pressures give management without external incentives an opportunity to escape responsibility and delay response to performance problems. Based on the above discussion, we believe that compared with managers without managerial ownership, those who are shareholders prefer to make an upward comparison and respond to inconsistent performance pressure more quickly and actively. According to this analysis, we propose the following hypothesis:

The mediating role of slack

The accumulation of organizational slack may be a short-term organizational phenomenon under multiple performance pressure, but it can still have a significant and lasting impact on organizational investment and decision making. We believe that it is practical and important to assess when and why firms accumulate more organizational slack and how organizational slack affects their investment decisions (H. Kim et al., 2008). A successful problemistic search requires abundant resources (Chen & Miller, 2007; Iyer & Miller, 2008). In such an environment, instead of focusing on solving local problems and performance pressure, firms can adopt a broader vision of solving general problems and multiple performance pressure, and take a more positive attitude toward R&D investment (Iyer & Miller, 2008; Vanacker et al., 2017).

When there is a great inconsistency in performance pressure, firms tend to make prudent decisions and put aside resources to wait for clearer performance feedback signals to determine the next decision (Joseph & Gaba, 2015). As a result, businesses are likely to generate more organizational slack. Consistent with previous studies, we regard the R&D investment of firms as the main behavioral response of firms to the performance pressure to conduct problemistic search (Chen & Miller, 2007; Greve, 2003). R&D investment is particularly important for innovation. A successful problemistic search requires a firm to change its decision on existing R&D investment in response to performance pressure. Firms should not be passively satisfied with solving local problems reflected by multiple types of performance pressure. Instead, firms should conduct more intensive searches, such as slack searches, in the problemistic search process and find innovative solutions to sluggish performance growth by increasing R&D investment.

When firms have more organizational slack, they have higher risk tolerance and generate more slack searches. Therefore, having organizational slack should encourage managers to put aside temporary performance pressure and make more tolerant responses (Martin et al., 2016). In the process of R&D investment decision, organizational slack enables managers to view multiple performance pressure more carefully and holistically, and be more willing to launch an extensive search and find new avenues for performance growth by increasing R&D investment. Therefore, we predict the existence of a mediating effect as follows:

Research design

Data and sample

Due to the implementation of new corporate accounting standards in 2007 concerning accounting recognition, certain aspects such as measurement, reporting behavior, and others have undergone great changes, and significant differences in the level of R&D between different industries arose. To ensure data consistency and exclude the potential influence of industry heterogeneity, this study selected Chinese A-share manufacturing listed firms from 2007 to 2017 as the research sample. To reduce the potential impact of endogeneity, the explanatory variables were processed with lag in this study. The sample base period of explanatory variables was from 2007 to 2015. Three major data sources were used: the China Stock Market and Accounting Research (CSMAR) database, China Center for Economic Research (CCER) database, and firms’ annual reports. The CSMAR is one of the largest databases on publicly listed Chinese firms and a primary source of information on Chinese stock markets and the financial statements of China’s listed firms. The CCER provides information on the institutional development of different regions in China. The firms’ annual reports are the primary source of information about firms’ R&D investments. Indeed, since 2007, China’s Accounting Standard for Business Firms (No. 6—Intangible assets) has required firms to disclose R&D spending in annual reports following international standards. We cross-checked the data by searching for information in annual reports, firm websites, and press releases. To ensure the quality and accuracy of the data, this study verified the data based on professional websites such as CAIXIN.com. Referring to previous research and considering this study’s theme, the sample was screened by (1) excluding firms with asset-liability ratio greater than 1 and (2) eliminating those with missing variable data. Through the above screening steps, this study finally obtained 5,397 unbalanced panel data involving 1,262 listed firms during the sample period.

Dependent variables

R&D intensity (RDi,t+2)

Following similar prior studies (Chen & Miller, 2007; Greve, 2003; Lim, 2015), we measured R&D intensity as the ratio of R&D expenditure to total sales revenues in year t + 2, and sales revenue in year t + 2 was used to measure the intensity of R&D investment (Miller, 2006; Wang et al., 2017).

Explanatory variables

Performance measure and aspirations

We calculated a firm’s performance pressure based on both its short-term aspiration and long-term aspiration. Short-term performance pressure (PAG_NSi,

t

) is the gap between actual short-term performance (P) and aspiration level (A) when the firm does not achieve the aspiration level. In this study, ROA was used to measure actual short-term performance (P) (Chen & Miller, 2007; Kuusela et al., 2017). Aspiration level includes the historical aspiration level based on the firm’s past performance and the social aspiration level based on the firm’s specific industry. In most previous studies, the aspiration level was measured as a mixture of both the historical and social aspiration levels (Greve, 2003). Consistent with the practice of previous studies, the aspiration level (A) in this study was obtained by weighting the historical aspiration level (HA) and social aspiration level (SA), setting the weight of

Long-term performance pressure (PAG_NLi, t , hereinafter referred to as “L”) is the gap between actual long-term performance (P) and aspiration level (A) when the firm does not achieve the aspiration level. In this study, firm market value (MV) was used to measure actual long-term performance (P) (Ben-Oz & Greve, 2015). The calculation method of long-term aspiration level is similar to that of the short-term performance pressure, obtained by weighting historical aspiration level (HA) and social aspiration level (SA). Finally, the long-term performance pressure was similarly treated with scale normalization to keep it comparable with the short-term performance pressure.

Organizational slack

Organizational slack is defined as the difference between the resources owned by a firm and the resources it requires to carry out normal activities in a given planning cycle. Since organizational slack can be deployed in various ways at any time, it is usually difficult to directly measure (Tyler & Caner, 2016). Therefore, previous studies used financial indicators to measure a firm’s organizational slack. Based on a previous study (Tan & Peng, 2003), organizational slack can be divided into absorbed, unabsorbed, and potential organizational slack. Considering that absorbed organizational slack is internalized in firm organizations and activities, which are difficult to transform and utilize and have poor fluidity (Geoffrey Love & Nohria, 2005), this study only considered unabsorbed and potential organizational slack. Specifically, unabsorbed organizational slack (NPR) in this study was measured by the ratio of current assets to current liabilities. Potential organizational slack (LRR) was measured by the ratio of total equity to total liabilities (Bourgeois, 1981). The theoretical fit and the ease of replication between different samples make such measurement the dominant measure in slack research (Nohria & Gulati, 1996; Wiseman & Bromiley, 1991). In addition, because innovation projects need time to develop, we measured the impact of organizational slack by using the average of a 4-year moving window period [t – 1, t + 2].

Managerial ownership

We measured management ownership by the percentage of equity owned by the top management team (MO). From the annual reports, we derived the percentage of shares owned by each member of the top management team each year. We then aggregated these data by year to form an overall measure of managerial ownership (Alessandri & Seth, 2014).

Control variables

Following previous studies on performance feedback, we included a comprehensive set of control variables. First, we included some control variables for the sample firms that vary in terms of size, age, and firm ownership (Ozer & Zhang, 2015; Park & Luo, 2001). Firm Size is the (logged) number of the employees of a firm, while Firm Age is the log of the number of years since establishment. Firm ownership is a dummy variable, coded as 1 if the target firm is state-owned and 0 otherwise. To control for the influence of firm-level product diversification (PDIV) (Palich et al., 2000), we adopted an entropy measure of product diversification (M. Kim, 2016). We controlled for the firm-level product diversification using an entropy measure, formally: PDIV = Σ Pia ln(1/Pia), where Pia is the proportion of a firm a’s sales in business segment i, to capture the degree to which a firm is diversified. The four-digit SIC code was used as the segment. Year dummies were included to control for possible annual effects. Following previous research (Ref & Shapira, 2017), the Herfindahl–Hirschman index (HHIt–1) in each industry was also included to control for industry competition (J. Kang et al., 2017). We normalized the data to range between 0 and 1, where 0 represents perfect competition and 1 represents a monopoly. Moreover, because managers can attribute poor performance to rapid changes in environmental factors (Giachetti et al., 2017; Greve, 2002), we also included Environmental uncertainty (EU) as a control variable, which was measured by the coefficient of variation in a firm’s sales revenue over the past 5 years, adjusted for the industry median (Ghosh & Olsen, 2009). Moreover, following previous studies, we used CEO Duality, Director Board Size, and Director Board Independence (measured as a percentage of the independent directors) to control for the effect of top management team heterogeneity. Finally, there are external factors that make R&D investment more/less attractive, such as market conditions and the overall economic environment. These factors change over time and vary across industries. Thus, the year effect and the industry effect were controlled by adding respective dummies.

Statistical analysis

In this study, we explain the inconsistency effect of multiple performance pressure from the theoretical perspective of multiple performance pressure interactions. With regard to the effect of inconsistency, how to measure “inconsistency” is an important issue worth discussing. One idea is to incorporate the concept of inconsistency into a comprehensive psychological perception of firm managers, using a psychological scale for its measurement. Another idea is to operationalize the concept into a two-factor relationship and measure the “inconsistency” indirectly by comparing the results of the corresponding factors. In general, compared with a self-reported direct measurement, an indirect measurement method can avoid social desirability bias to some extent (Edwards, 2001; Huang et al., 1998).

There are two main methods for indirect measurement of inconsistencies: by calculating an inconsistency index and by using response surface analysis. The inconsistency index measures consistency by constructing a single index, such as difference scores and interaction items. However, this method of measuring and matching with a single index has the following drawbacks in our study.

(1) When two types of performance pressure are significantly positively correlated, the reliability of their difference is usually less than the reliability of either component measure. (2) There is also the problem of vague theoretical concepts in single indices. Under the condition of dichotomous variables, two variables that build up interactive items can reflect the consistency between them. However, when the two variables are continuous variables, such as the two types of performance pressure in our study, a product term does not represent the effects of consistency (Edwards, 2001). (3) The construction of a single index may confuse the effect of two types of performance pressure on organizational slack, leading to some results that are not easy to explain or even wrong. (4) The use of a single index effectively converts an essentially multivariable model into a univariate model.

The response surface analysis based on a quadratic polynomial regression can overcome the above limitations to some extent, and the three-dimensional (3D) surface presented by it vividly depicts the effect of two variables and their inconsistency on the dependent variable, which is helpful for us to better explain the inconsistency effect (Ilmarinen et al., 2016).

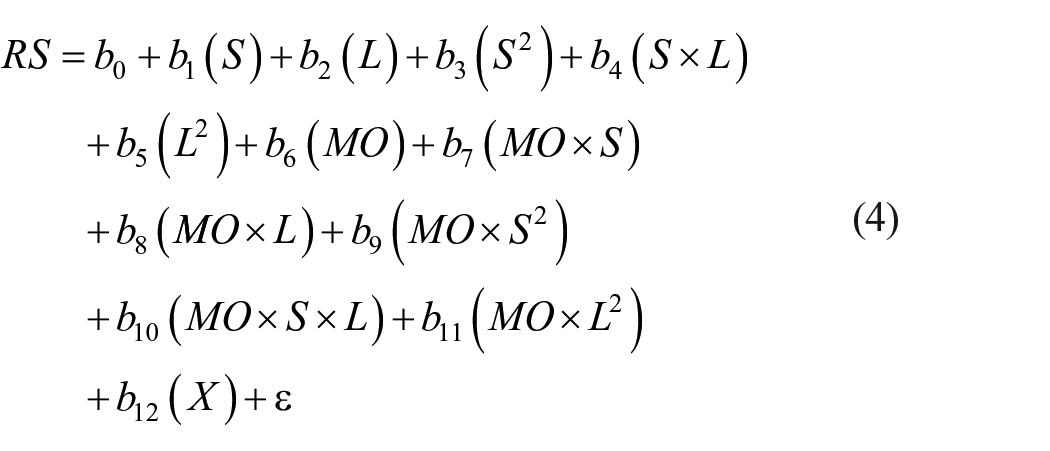

Based on the considerations mentioned above, we used polynomial regression and response surface modeling analyses (Edwards & Parry, 1993; Herhausen, 2016) to test our inconsistency hypotheses (see Figure 1). In this study, we chose quadratic polynomials (degree = 2) because our hypothesis assumes that a firm’s organizational slack is higher in the case of inconsistent performance pressure than in the case of consistent performance pressure. This is reflected in a U-shaped structure on the section of the response surface along the inconsistency line, which can be detected only including quadratic terms. More specifically, we estimated quadratic regression equations using a measure of two types of organizational slack (RS), the unabsorbed slack (NPR) and the potential slack (LRR), as the dependent variables; the performance below short-term aspiration (S) and the performance below long-term aspiration (L) as the independent variables; managerial ownership (MO) as the moderator; and quadratic terms constructed from these measures. To test the effect of performance feedback inconsistency on slack search behavior, we used polynomial regression and response surface methodology to test Hypotheses 1 to 3 (Edwards, 2002; Edwards & Parry, 1993). Specifically, the mediator variable, resource slack (RS), was regressed on the control variables, as well as the five polynomial terms

where RS represents resource slack, S represents short-term performance pressure, and L represents long-term performance pressure. X represents a set of control variables, and ε represents the error term. We mean-centered the short-term performance pressure (S) and long-term performance pressure (L) before calculating the three second-order polynomial terms to eliminate non-essential multicollinearity and facilitate the interpretation of results (Aiken & West, 1991). Consistent with past research that used polynomial regression (e.g., see Edwards & Cable, 2009; Lambert et al., 2012; Matta et al., 2015; Z. Zhang et al., 2012), we used the coefficients from the above equation to plot a 3D response surface with the perpendicular axes corresponding to values for short-term performance pressure (S) and long-term performance pressure (L), and the vertical axis corresponding to values for resource slack (Edwards & Parry, 1993).

Research model.

To estimate the coefficients and standard errors for the slope and curvature of the consistency (S = L) and inconsistency line (S = –L) of the response surface, we used procedures for testing the linear combinations of regression coefficients (Cohen et al., 2014; Edwards & Parry, 1993).

In response surface analysis, the consistency line is the set of points (S = L) on the S – L plane, where the intensity of the performance pressure is the same. S = L is substituted into equation (1) to obtain the calculation formula of the consistency line (equation (2))

In equation (2), the coefficient

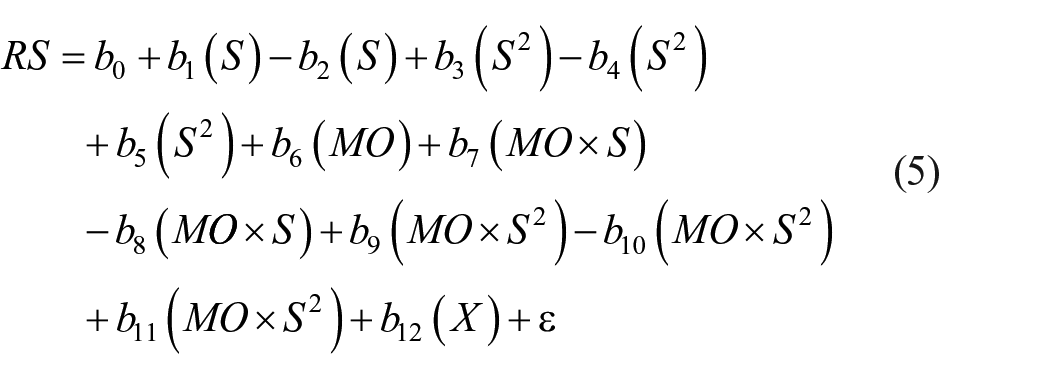

In response surface analysis, the inconsistent line is the set of points, where the sum of the two performance pressures on the S – L plane is equal to some constant (S + L = c). In our study, we specify that equations (3) and (5) refer to the case c = 0. By substituting L = −S + c into equation (1), the calculation formula of the inconsistency line can be obtained

In equation (3), the coefficient

According to Edwards and Parry (1993), to test Hypothesis 1, that is, the effect of performance feedback inconsistency of interest on organizational slack, we focus on the curvature of the inconsistency line of the response surface

To test Hypothesis 2, different from linear regressions where the statistical significance of the coefficient for a three-way interaction should be assessed to establish a three-way moderating effect, in polynomial regressions, the increment in R2 after adding a moderator and products of the moderator with each of the original terms should be assessed to establish the moderating effect (Edwards & Rothbard, 1999; Shao et al., 2017). Specifically, moderation can be tested by supplementing polynomial regression equations with moderator variables and building on principles of moderated regression. As a starting point, let us recall equation (1)

We then add the moderator variable MO to equation (1). Following the principles of moderated regression (e.g., Aiken & West, 1991), we add MO and the product of MO with each term in equation (1). This results in the following expression

Moderation is tested by assessing the increment in R2 yielded by the terms

If the increment in R2 yielded by the five terms

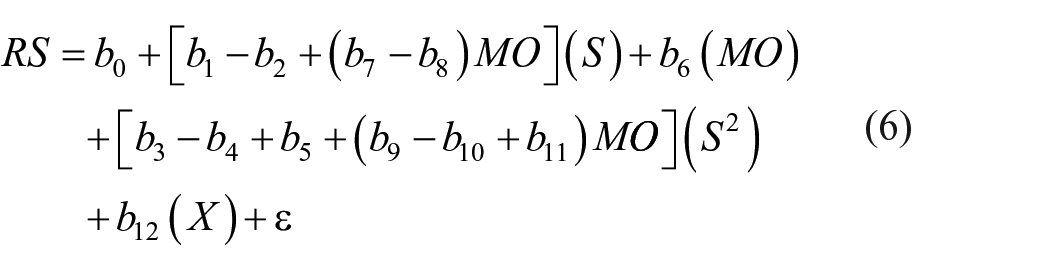

After re-arranging, the equation becomes

In equation (6), the slope of the surface along the inconsistency line is

To test Hypothesis 3, following previous research, we adopted the block variable approach (Matta et al., 2015). A block variable is a weighted linear composite of regression coefficients multiplied with the respective predictor, in which the weights are the estimated regression coefficients for the variables in the block (Edwards & Cable, 2009; Schuh et al., 2018). For instance, the block variable associated with equation (1) equals b1(S) + b2(L) + b3(S2) + b4(S × L) + b5(L2). The five quadratic terms are then replaced with the block variable, and the regression equation is re-estimated. The paths reported are standardized coefficients estimated from block variables constructed from the five quadratic terms for performance pressure inconsistency. The coefficients on the other predictors in the equation are unaffected, and the variance explained by the equation using the block variable is identical to that explained by the equation using the original quadratic terms, given that the block variable is computed from the coefficient estimates for the quadratic terms themselves. The path coefficients obtained from these procedures were used to assess the effects associated with our model, allowing us to determine the extent to which each of the mediators in our model carried the effects of short-term performance pressure and long-term performance pressure on the organizational slack. Specifically, we constructed a block variable to represent the joint effect of short-term performance pressure and long-term performance pressure on organizational slack, and the mediating effect and moderated mediating effect were tested using the bootstrap method (Colbert et al., 2008; Edwards & Cable, 2009; Edwards & Parry, 1993).

Results

Descriptive statistics

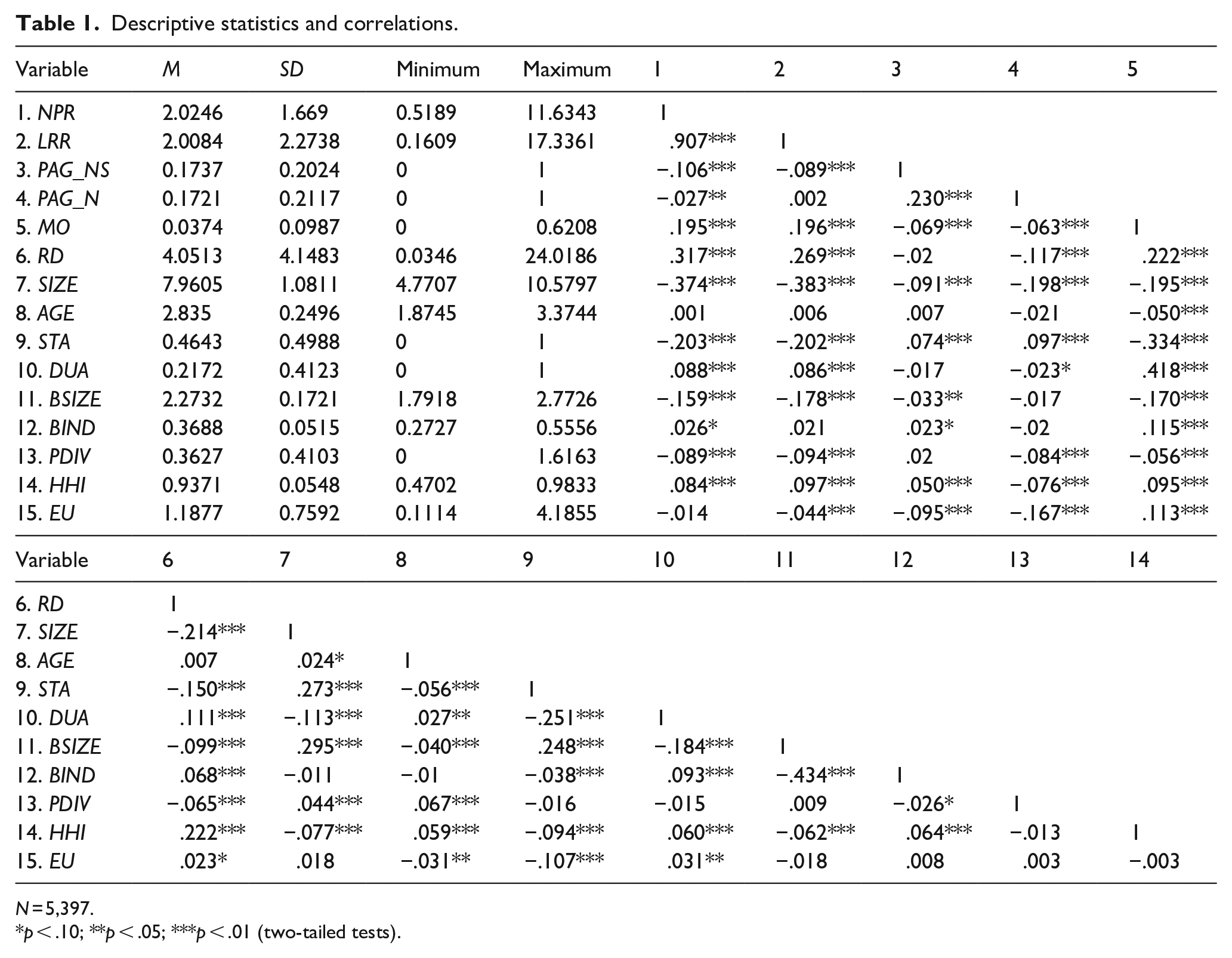

Table 1 lists the descriptive statistics and correlations of the main variables. The maximum correlation coefficient between the major variables was only .434, lower than the threshold of multicollinearity .5, indicating that there was no multicollinearity problem. Further statistical analysis of the relationship between these variables was carried out as discussed below.

Descriptive statistics and correlations.

N = 5,397.

p < .10; **p < .05; ***p < .01 (two-tailed tests).

Regression analysis

Before the empirical analysis, the following measures were taken to ensure the validity and consistency of the model estimation (Van de Vrande, 2013; Yang et al., 2014): (1) all the variables were mean-centered prior to calculating the interaction term, and (2) variance inflation factor (VIF) diagnosis was carried out on all the variables of the regression model. From the results, the average VIF of each model was about 2 and the VIF value of each variable was far less than 10, indicating that there was no multicollinearity problem, confirming suitability for further regression analysis. In this study, STATA 13.1 software was used for the calculation.

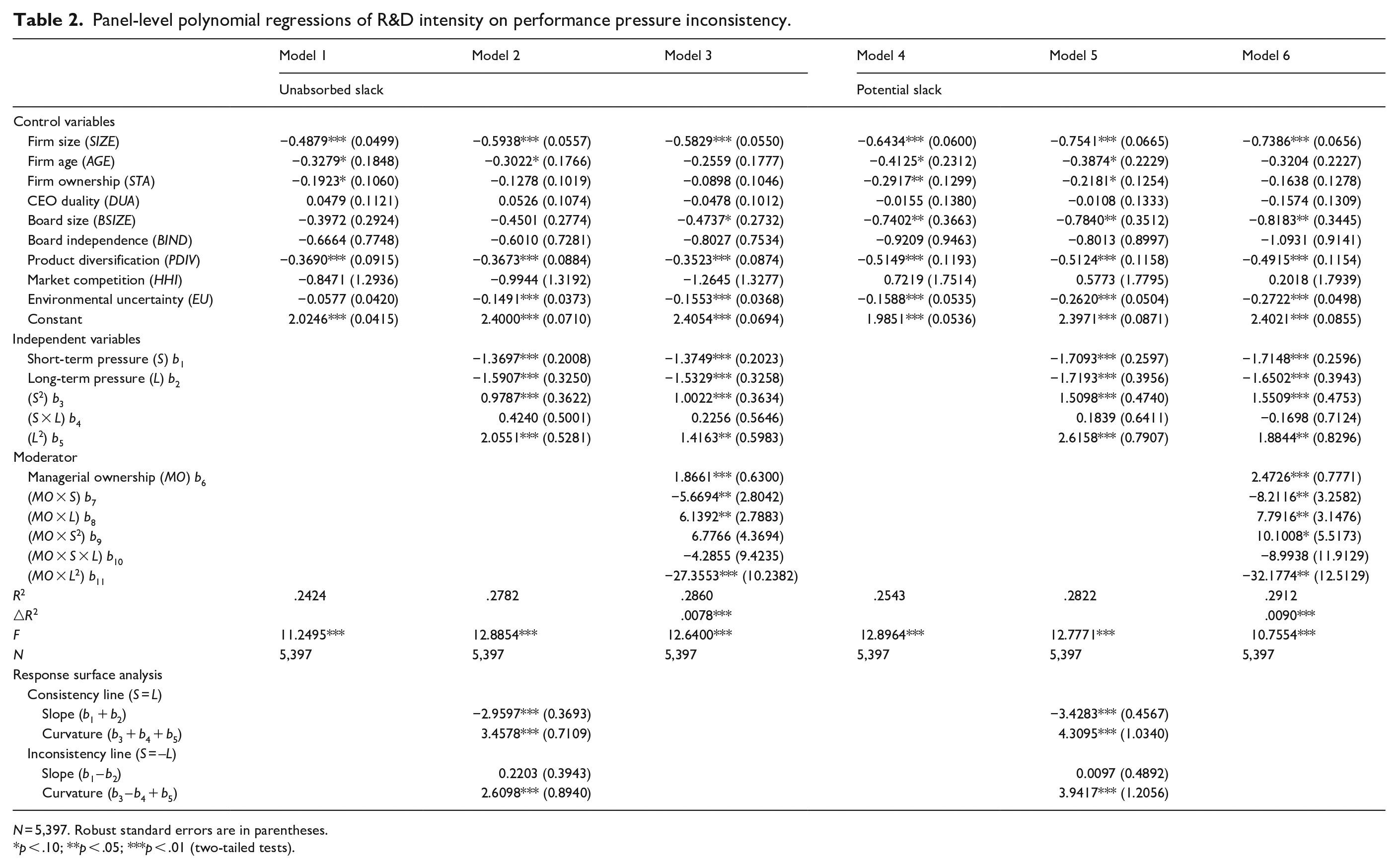

Table 2 lists the results of the polynomial regression and response surface analysis, and examines the impact of the inconsistency between short-term performance pressure and long-term performance pressure on organizational slack. Specifically, Model 1 to Model 3 list the impact of the inconsistency between short-term performance pressure and long-term performance pressure on unabsorbed organizational slack while Model 4 to Model 6 list the impact of the inconsistency between short-term performance pressure and long-term performance pressure on potential organizational slack. Among them, Models 1 and 4 are the benchmark models, where only control variables were added. In Models 2 and 5, five polynomials, S, L, S2, S × L, and L2, were added based on Models 1 and 4, respectively, and the corresponding regression coefficient, covariance, and standard error were obtained. Thereafter, the slope and curvature coefficient and the significance of the section corresponding to the consistency line and inconsistency line were calculated. On the section corresponding to the inconsistency line, the curvature

Panel-level polynomial regressions of R&D intensity on performance pressure inconsistency.

N = 5,397. Robust standard errors are in parentheses.

p < .10; **p < .05; ***p < .01 (two-tailed tests).

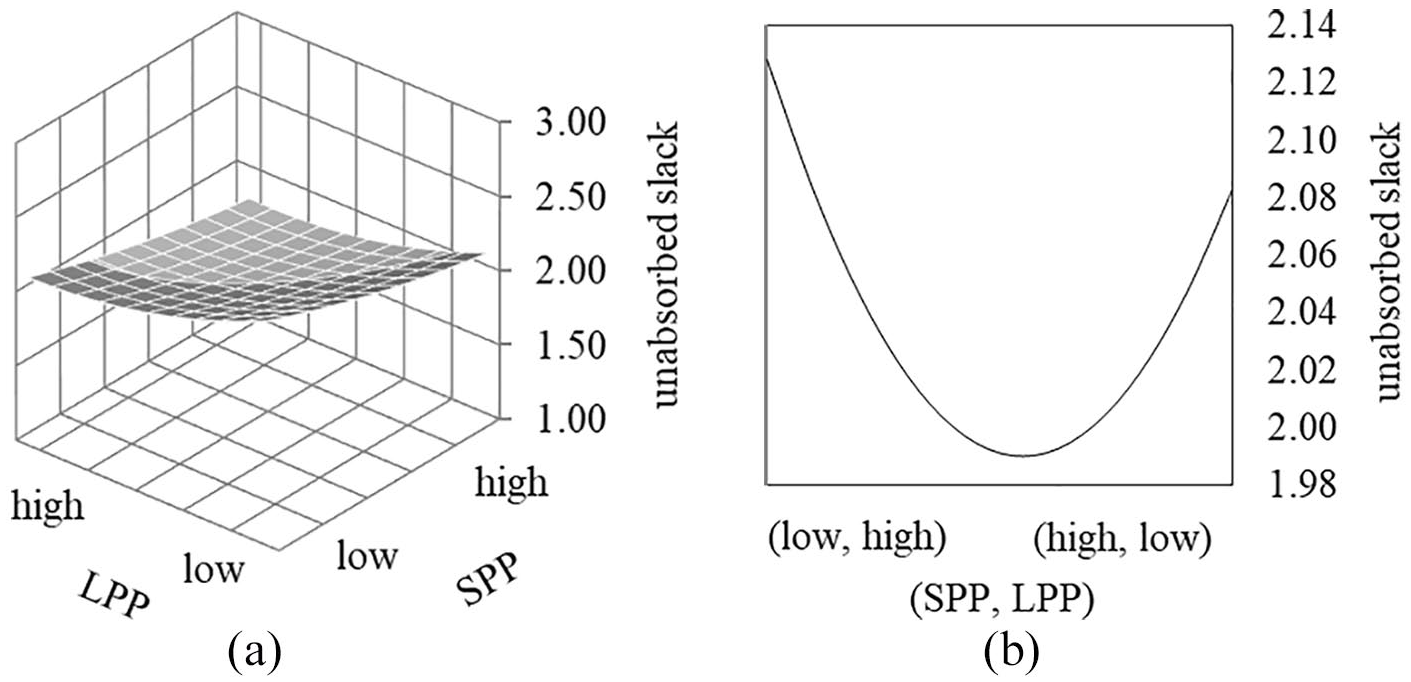

Hypothesis 1 suggests that the more inconsistent the performance feedback, the higher the organizational slack of a firm. According to the results of the response surface analysis of Model 2 in Table 2, the curvature of the response surface along the inconsistency line

Surface graphs of performance pressure inconsistencies (unabsorbed slack): (a) surface graphs of the inconsistency between SPP and LPP, predicting unabsorbed slack of a firm, and (b) a side view of the response surface in the inconsistency line (L = –S).

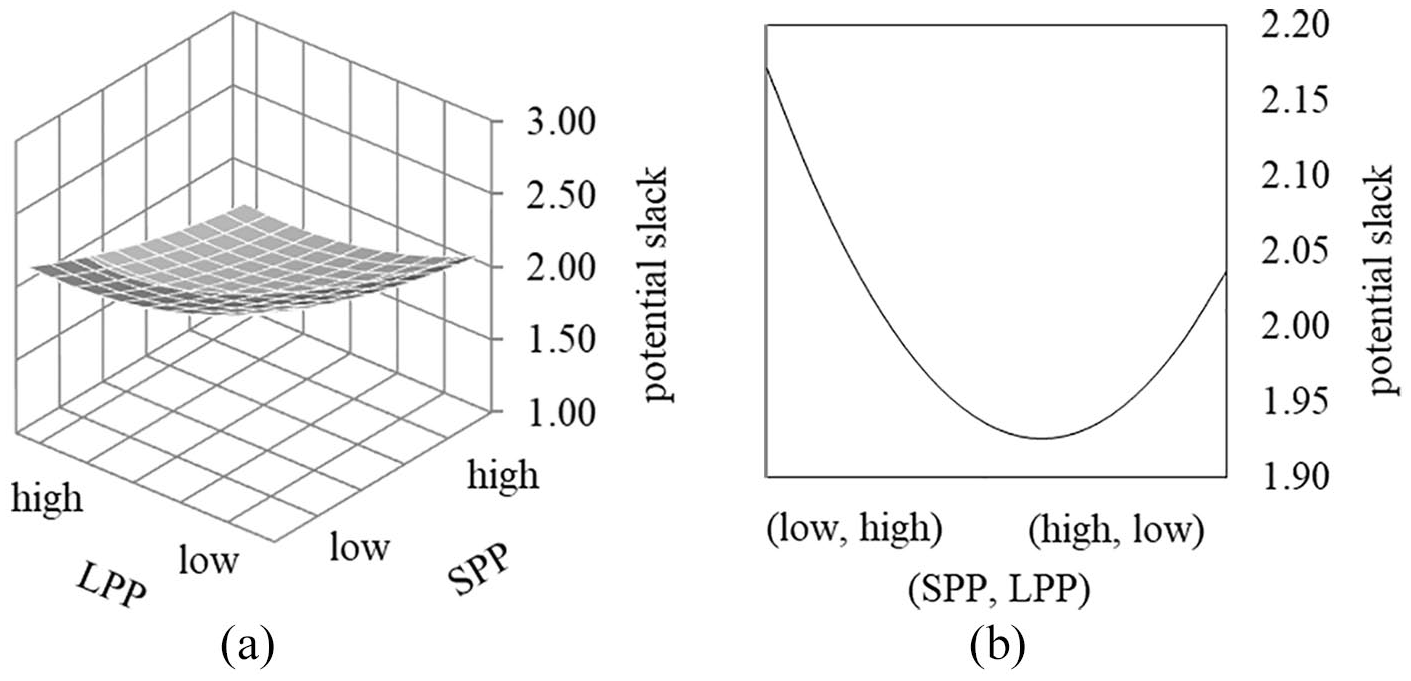

According to the response surface analysis results of Model 5 in Table 2, the curvature of the response surface along the inconsistency line

Surface graphs of performance pressure inconsistencies (potential slack): (a) surface graphs of the inconsistency between SPP and LPP, predicting potential slack of a firm, and (b) a side view of the response surface in the inconsistency line (L = –S).

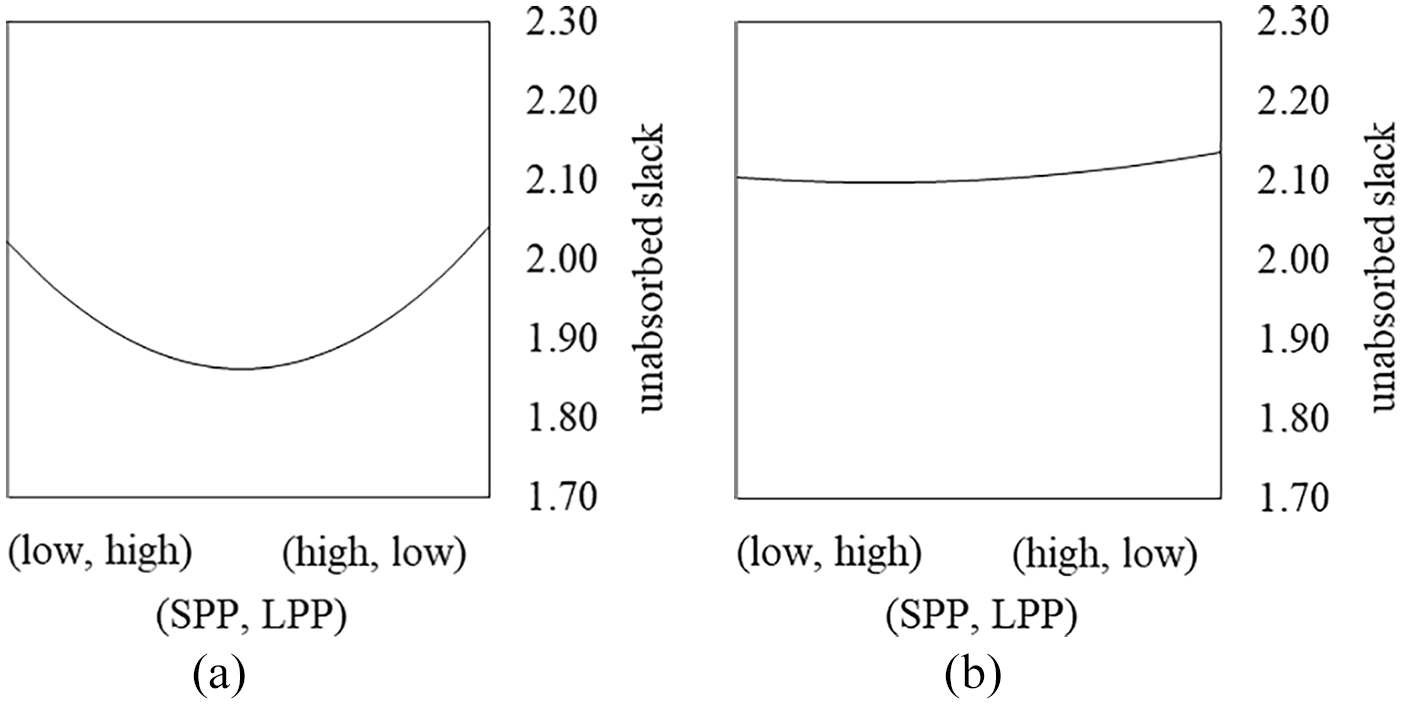

In this study, Hypothesis 2 proposes that managerial ownership weakens the positive correlation between performance pressure inconsistency and organizational slack. As can be seen from the results of Model 3 in Table 2, the explanatory power of the model was significantly improved after the introduction of managerial ownership (MO) and its interaction terms with S, L, S2, S × L, and L2 (ΔR2 = .0078, p < .01). This result indicates that managerial ownership moderates the relationship between multiple performance pressure inconsistency and unabsorbed slack. To more clearly identify the moderating effect of managerial ownership on the relationship between multiple performance pressure inconsistency and the potential slack of a firm, we provide the side views of response surfaces along the inconsistency line (M ± 1 SD) in Figure 4(a) and (b), respectively. The above results show that with the increase of the managerial ownership, the unabsorbed organizational slack of firms caused by the inconsistency of multi-operation performance pressure decreases.

Side view of response surface along inconsistency line (unabsorbed slack): (a) surface graphs when the level of managerial ownership is low, and (b) surface graphs when the level of managerial ownership is high.

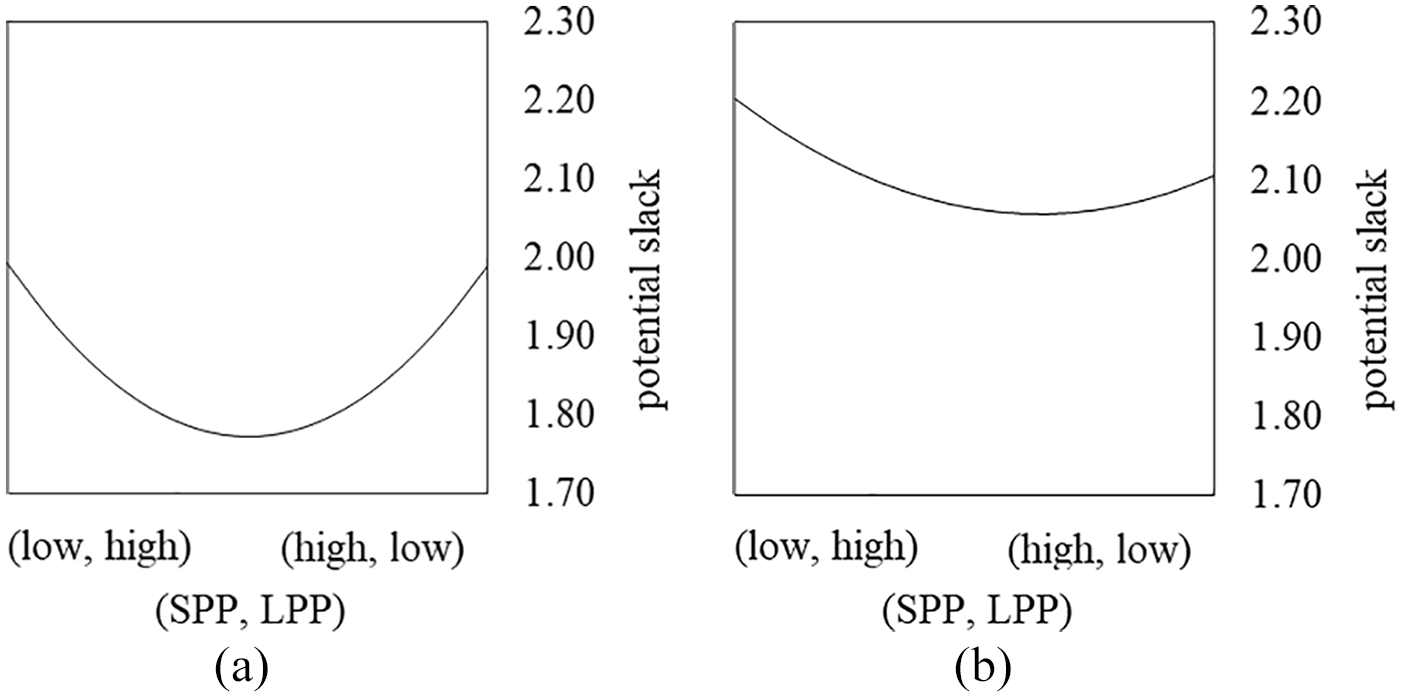

As can be seen from the results of Model 6 in Table 2, the explanatory power of the model was significantly improved after the introduction of managerial ownership (MO) and its interaction terms with S, L, S2, S × L, and L2 (ΔR2 = .0090, p < .01). This result indicates that managerial ownership moderates the relationship between multiple performance pressure inconsistency and potential slack. To more clearly identify the moderating effect of managerial ownership on the relationship between multiple performance pressure inconsistency and the potential slack of a firm, we provide the side views of response surfaces along inconsistency line (M ± 1 SD) in Figure 5(a) and (b), respectively. The above results show that with the increase of managerial ownership, the potential organizational slack of firms caused by the inconsistency of multi-operation performance pressure decreases. Therefore, Hypothesis 2 is supported.

Side view of response surface along inconsistency line (potential slack): (a) surface graphs when the level of managerial ownership is low, and (b) surface graphs when the level of managerial ownership is high.

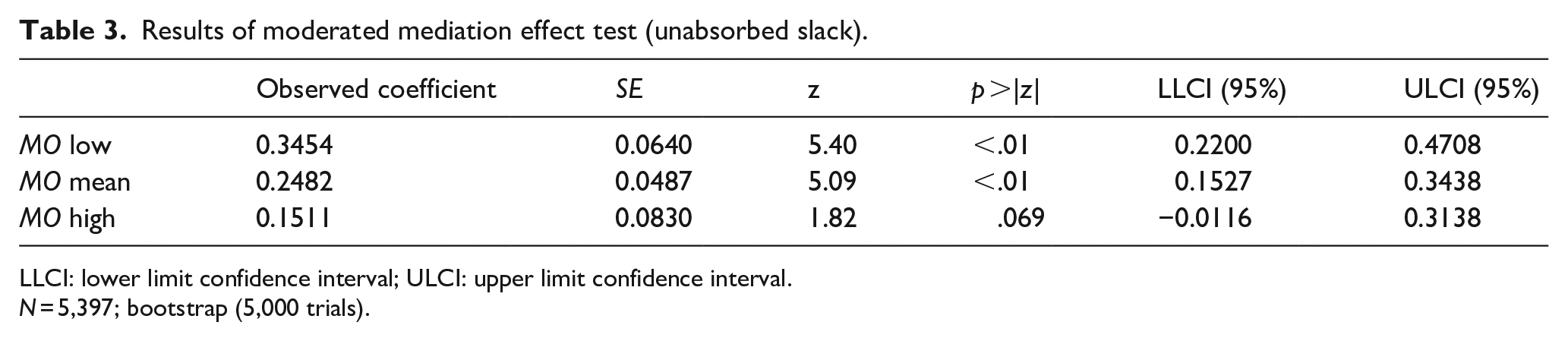

Hypothesis 3 stated that the conditional indirect effect of performance pressure inconsistency on R&D investment is mediated by organizational slack and moderated by managerial ownership such that the effect is weaker under conditions of high managerial ownership. Traditional methods for analyzing this mediating effect, such as the stepwise test and Sobel test, assume the normal distribution of variables and only involve one independent variable. Meanwhile, in the mediating effect test of curve relationship, the composition of an indirect effect violates the assumption of normal distribution and involves two independent variables; as such, the traditional method is no longer applicable. Therefore, the block variable approach was adopted for analyzing with reference to the previous research (Matta et al., 2015). Specifically, a block variable is constructed based on a polynomial regression coefficient to represent the joint effect of short-term performance pressure and long-term performance pressure on unabsorbed organizational slack. On this basis, the results were analyzed using bootstrap (5,000 trials).

Table 3 lists the mediating effect of unabsorbed organizational slack on the relationship between performance pressure inconsistency and R&D intensity, as well as the test results of the mediating effect under the moderation of managerial ownership. Table 3 shows that when the managerial ownership is 1 SD lower than the mean, the indirect effect of block variables on a firm’s R&D intensity through unabsorbed organizational slack is significantly positive (r = .3454, 95% confidence interval [CI] = [0.2200, 0.4708]). When the managerial ownership is the mean, the indirect effect of block variables on a firm’s R&D intensity through unabsorbed organizational slack is also significantly positive (r = .2482, 95% CI = [0.1527, 0.3438]). However, when the managerial ownership is the mean plus 1 SD, the indirect effect of block variables on a firm’s R&D intensity through unabsorbed organizational slack is not significant (r = .1511, 95% CI = [–0.0116, 0.3138]). Our findings show support for the conditional indirect effect such that the indirect effect is significant (CIs do not contain zero) at low levels of managerial ownership. This demonstrates that the indirect effect of performance pressure inconsistency on R&D investment through unabsorbed slack is weaker (less positive) when the managerial ownership is high. These results support Hypothesis 3.

Results of moderated mediation effect test (unabsorbed slack).

LLCI: lower limit confidence interval; ULCI: upper limit confidence interval.

N = 5,397; bootstrap (5,000 trials).

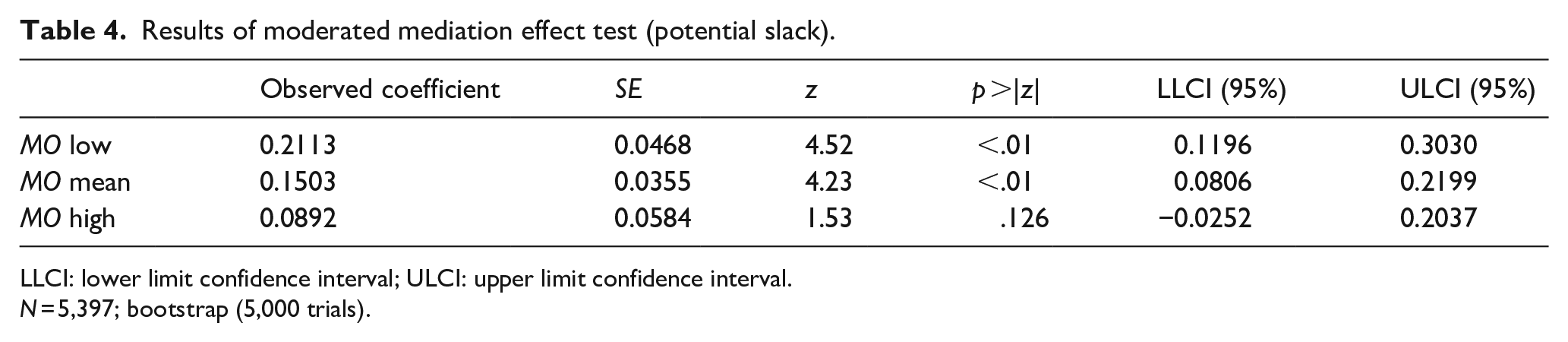

Table 4 lists the mediating effect of potential organizational slack on the relationship between performance pressure inconsistency and R&D intensity, as well as the results of the moderating effect of managerial ownership. Table 4 reveals that when the managerial ownership is 1 SD lower than the mean, the indirect effect of block variables on a firm’s R&D intensity through potential organizational slack is significantly positive (r = .2113, 95% CI = [0.1196, 0.3030]). When the managerial ownership is the mean, the indirect effect of block variables on a firm’s R&D intensity through potential organizational slack is also significantly positive (r = .1503, 95% CI = [0.0806, 0.2199]). However, when the managerial ownership is the mean plus 1 SD, the indirect effect of block variables on a firm’s R&D intensity through potential organizational slack is not significant (r = .0892, 95% CI = [–0.0252, 0.2037]). Similarly, our findings show support for the conditional indirect effect such that the indirect effect is significant (CIs do not contain zero) at low levels of managerial ownership. This demonstrates that the indirect effect of performance pressure inconsistency on R&D investment through potential slack is weaker (less positive) when the managerial ownership is high. These results support Hypothesis 3.

Results of moderated mediation effect test (potential slack).

LLCI: lower limit confidence interval; ULCI: upper limit confidence interval.

N = 5,397; bootstrap (5,000 trials).

Discussion

For many firms, starting a problemistic search becomes an uphill battle when they do not get consistent feedback in the event of poor performance. Therefore, it is of great interest to scholars and practitioners to understand the effects of inconsistency in multiple performance pressure. We propose a study that investigates the inconsistency effect between short-term and long-term performance difference. A specific focus is considered on the organizational slack, due to multiple performance pressure and inconsistencies, in order to evaluate how firms’ R&D investment decisions are affected. The results show that firms have more organizational slack when they encounter inconsistent negative feedback. Managerial ownership weakens the negative impact of inconsistency in performance pressure on the firm’s organizational slack, such that this effect is weaker in firms where managers are also shareholders. Furthermore, organizational slack mediates the positive relationship between inconsistency in performance pressure and R&D intensity, and the mediating effect weakens in the context of high managerial ownership.

Meanwhile, in the Theory and hypotheses’ section, we suggest that inconsistencies in performance pressure increase the burden on firms to analyze problems, and firms need to reserve more organizational slack (time and resources) to deal with such inconsistencies. An increase in organizational slack further promotes a search for firm slack, which is conducive to the increase of a firm’s R&D investment. The empirical results validate our hypothesis. We further discuss this finding in relation to current research and management practices. We think this finding is highly relevant, both in the context of current research and management practices, because inconsistencies are disruptive to organizations and should be avoided. Few studies have tried to analyze how inconsistencies can be used to benefit firms. What this finding actually tells researchers and managers is that inconsistencies may actually reduce the ability of firms to seek partial solutions, but they also create more organizational slack for firms, thus providing a basis for firms to find an overall innovative solution.

Moreover, we also make assumptions about the conditions surrounding the inconsistency effect. We assume that managers’ tolerance for inconsistencies is reduced by the incentives brought about by managers’ ownership. When managers have high ownership, they do not waste time or resources waiting for inconsistencies to disappear, nor they let inconsistencies in performance feedback prevent them from making adjustments. This weakens the effect of the inconsistency-organizational slack-R&D investment mechanism. The empirical results validate our hypothesis. The positive mediating effect of inconsistencies on R&D investment is weaker in cases where managers have high shareholding ratio. From the perspective of agency theory, this discovery is quite novel. According to the literature on agency theory, managerial ownership provides an incentive mechanism for reducing agency problems, which is beneficial to a firm. However, in the case of inconsistent performance pressure, we find that the incentive of equity hinders the firm’s search for an overall solution, which is not conducive to the increase of R&D investment.

Theoretical contribution

There is little consensus on why inconsistent performance feedback is now more frequent than in the past, but there is plenty of evidence that it is destructive to the organization. This study challenged this view and, using the theory of behavioral agency, provided some new insights into why and how performance pressure inconsistencies benefit organizations. Inconsistencies may reduce a firm’s ability to find partial solutions and also bring more organizational slack to the firm, thus providing a foundation for the firm to come up with more holistic, innovative solutions to solve performance problems.

Specifically, the behavioral agency theory is an important attempt to correct the defects of the standard agency theory. By adding a series of assumptions, the behavioral agency theory explains those behaviors that past cannot be explained by standard agency theory. In this article, on the basis of summarizing the frontier research achievements of behavioral agency theory, we put forward the concept of performance pressure inconsistency and the relationship model between this concept, organizational slack, and firm R&D investment behavior. This is an important framework, and one of its major contributions is that it communicates the hidden links between previous studies that have been scattered across different literature, such as problemistic search, organizational slack, and agency theory, by introducing the concept of inconsistent performance pressures. The empirical results confirm the hypotheses proposed by the behavioral agency theory and provide a reference for using the behavioral agency theory to explain the behavior that is difficult to be explained by the previous theories. Specifically, we demonstrate the superiority of the behavioral agency theory by placing this construct of managerial ownership in the multiple performance pressure decision model we set up. In behavioral agency theory, time discounting, inequity aversion, and trade-offs between internal and external motivations are the key assumptions that distinguish this theory from the standard agency theory. However, no relevant studies have provided empirical evidence on the impact of this assumption difference in the firm’s decision making, especially on the R&D investment of firms facing multiple performance pressures. Here, we derive Hypothesis 2 by using the new assumptions of behavioral agency theory about time discounting, inequity aversion, and trade-offs between internal and external motivations. The empirical results show that managers with higher managerial ownership and managers with lower managerial ownership will consume more organizational slack in the face of inconsistent performance pressure to deal with the inconsistency of performance pressure. This attempt reveals the concrete impact of the new hypothesis of behavioral agency theory on the firm’s decision making. In particular, it provides empirical evidence for the analysis of decision making under the pressure of inconsistent performance.

Second, inconsistent performance pressure is an important concept in this article. This gap not only brings new decision-making situations to managers but also brings new problems to firm decision making. Under the pressure of inconsistent performance, managers need to spend extra time or even lay aside part of the resources and investment to determine which kind of performance pressure the resources should deal with first. This setting is important. Specifically, as we reviewed in the “Introduction” section, previous studies have not linked performance feedback inconsistencies as a source of organizational slack to examine the impact of slack performance resulting from organizational inconsistencies on the firm’s search. Among them, most consider the direct impact of inconsistent performance feedback on organizational search (Blagoeva et al., 2019; Joseph & Gaba, 2015; Lucas et al., 2018; Lv et al., 2019). In our study, we identify a new source of a firm’s organization slack originating from extra time and pending resources needed in deciding which performance pressure should be resolved prior to others. We found that inconsistent performance pressure will not only directly affect the firm’s R&D but also indirectly affect the firm’s R&D through the increasing organizational slack. This attempt provides a new perspective for the in-depth study of this issue and inspires the study of the interaction between problemistic search and organizational slack.

Third, various theoretical explanations have been proposed to understand the relationship between performance pressure and R&D investment decisions, but little attention has been paid to the influence of equity incentive arrangements made by firms to reduce agency problems on R&D investment decisions (Blagoeva et al., 2019; Joseph & Gaba, 2015; Lucas et al., 2018). In this study, we supplemented existing theories by examining managerial ownership as another theoretical explanation of the relationship between multiple performance pressure and the firm’s R&D investment decisions. Our research shows that the positive indirect effect of inconsistency is inhibited by managers’ ownership. This novel finding extends existing research that aims to explain successful problemistic searches from a semiautomatic perspective and focuses only on organizational slack or the moderating effects of corporate governance (Arrfelt et al., 2013; Bansal, 2003; Barreto, 2012; Lungeanu et al., 2016; Steensma & Corley, 2001; Tan & Peng, 2003). By investigating inconsistencies in performance pressure and differentiating managers’ responses to problemistic searches, we reveal mechanisms that help determine how and why inconsistencies in performance pressure lead to negative or positive outcomes, thus providing recommendations for designing more effective governance mechanisms.

Finally, our response surface analysis method is helpful to the empirical study of performance feedback (Edwards & Cable, 2009; Mindruta et al., 2016). In this process, we improved the research design and provided empirical evidence to prove the inconsistency effect between short-term and long-term performance pressure in the context of R&D investment decisions of firms, thus contributing to the literature on performance pressure from different time horizons (Ben-Oz & Greve, 2015).

Managerial implications

The results also have implications for practitioners. It is not just the inconsistency between multiple performance feedbacks that matters. Conversely, in the context of problemistic search, management ownership must also be considered. Organizations should be cautious in using shared ownership as an incentive, which may induce managers to adopt a positive attitude toward the poor performance of the firm and to some extent hinder the firm from accumulating the organizational slack needed for slack search (De Cremer & Tao, 2015). This lack of resources can cause firms to become occupied looking for local solutions when faced with multiple types of performance pressure, rather than pursuing more distant holistic solutions. This has a negative impact on firms’ increased investment in R&D. By contrast, if managers do not have shared ownership, or only have low levels of shared ownership, then managers will be more tolerant of ambiguity and inconsistency, and will not let immature consensus or solutions prevent them from thoroughly looking for holistic solutions to improve performance. In this regard, we suggest that organizations establish a collective accountability mechanism to increase managers’ tolerance for inconsistency and ambiguity. This tolerance can help firms remain innovative and long-term oriented in the challenge of multiple performance pressure.

Limitations and future directions

The results of this study should be considered in light of several limitations, each of which could be addressed by further study. The first limitation relates to the extent to which our theory and results are generalized to other samples: our data are only collected from listed firms in China. Inconsistent levels of performance feedback may vary by region (Claes et al., 2005). Previous research classified China as an economy in transition, in which trade liberalization increases the risk of volatility in terms of trade (Smallbone & Welter, 2001). Firms tend to pay close attention to gaining internal and external legitimacy and hesitate to act in the face of inconsistent performance feedback. Therefore, there may be strong inconsistencies in economies under transition or institutional reforms (Elango et al., 2019; Xia et al., 2009). Other studies can address this limitation by using data from both economies in transition and developed economies.

Moreover, since we focused on negative performance feedback in an ambiguous context, this study only measured performance relative to short-term and long-term aspirations. Therefore, we cannot rule out other explanations for our results that may come from other aspirations, such as historical and social aspirations or financial and non-financial aspirations. For future research, it is meaningful to study how inconsistent feedback, relative to other types of aspirations, affects the problemistic search.In further research, we will be interested to see how inconsistent feedback, relative to other types of aspirations, affects the search for problems.

Conclusion

This study is a preliminary exploration of the effect of inconsistency between short- and long-term performance differences. We examined how the accumulation of organizational slack owing to multiple performance pressure and inconsistencies affects a firm’s R&D investment decisions, when this positive effect is triggered, and when it is weakened or is ineffective. There are many factors that lead to the failure of problemistic search; thus, scholars and practitioners are increasingly looking for the factors that account for an effective problemistic search. At the same time, multiple types of performance pressure are becoming increasingly common. In summary, this study provided some new insights and ways to help guide firms to go beyond the continuous effort of finding solutions to local problems and try to add more organizational slack to find innovative, holistic solutions in response to multiple performance pressure.

Footnotes

Acknowledgements

The authors are grateful to Editors and anonymous reviewers for their helpful comments and suggestions. Any errors remain our sole responsibility.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the National Natural Science Foundation of China (71902192; 71372155), the Fundamental Research Funds for the Central Universities (19wkpy16), and the China PostDoc Scientific Fund (2019M653264).