Abstract

This study offers insight into the role of board politicization on the Spanish cajas’ performance from a dual perspective. First, we analyze the effect of a new kind of political directors who occupy board seats as representatives of stakeholders outside the public administrations while maintaining a political affiliation. We call these “hidden” political directors as politicians in disguise. Second, we analyze how political interests can prevent directors with financial expertise from applying their knowledge to improve cajas’ performance. Using a sample of hand-collected data from 45 Spanish cajas, we find that politicians in disguise destroy value in the caja and that politically motivated financial experts on the board do not benefit cajas’ performance.

Introduction

The financial crisis of 2007 led to a near-collapse of a critical part of the Spanish financial system that functioned for almost 200 years: savings banks (hereinafter, cajas). With a market share in loans and deposits of around 50% of the Spanish financial system (Bank of Spain, 2008), the goodbye of cajas was hard. Over a decade on from the beginning of the crisis, only two entities (Caja de Ahorros y Monte de Piedad de Ontinyent and Colonia-Caixa d’Estalvis de Pollença) maintained the legal status of caja, while the remainder disappeared, merged, or became foundations (Bank of Spain, 2017). The consequences of this process are highly relevant for Spanish society: the increase in financial exclusion (Alamá & Tortosa-Ausina, 2012), the hard-to-recover bailout of €65 billion requested by the Spanish government as part of its strategy to aid banks and cajas financially (about 5.5% of Spain’s GDP in 2018 (Bank of Spain, 2018)), and the numerous legal proceedings against cajas’ directors (24 unresolved at the time of writing (FROB, 2018)) that had concluded with many politicians convicted of corruption and fraud. 1

All these social and economic consequences of the cajas’ debacle generated an intense public debate about the role of politicians in their governance. This debate had two opposing positions: while public opinion (expressed through the media) complained about the harmful impact of the high volume of politicians on cajas’ boards, 2 the official reports from different Spanish authorities 3 play down the role of politicians as cajas’ directors. In this uncertain context, the academics have a fundamental responsibility to offer sound answers to society about the real role of the political directors of cajas. However, there are no conclusive empirical results so far. Previous evidence on this industry show a consensus on the negative influence of politicization on cajas’ performance (Azofra & Santamaría, 2004; Crespí et al., 2004; Fonseca Díaz, 2005; Melle Hernández & Maroto Acín, 1999), but the most recent evidence seems to indicate no influence (Cuñat & Garicano, 2010; García-Meca & Sánchez-Ballesta, 2014; Sagarra et al., 2015). How, then, do we solve this puzzle of outcomes? What is the real effect of political directors on cajas’ performance?

We argue here that politicians did expropriate rents in cajas, however, recent studies have not considered the phenomenon of governance politicization in all its complexity. In this study, we get closer to the particular reality of these entities to offer an answer about the effect of board politicization on cajas’ performance. Specifically, our study contributes to the existing literature in at least the two ways described below.

On the one hand, we present the problem of cajas’ governance in the form of a new model of board politicization. We argue that we cannot evaluate the real board politicization by considering only the number of nominated politicians on the board as previous studies do, but also those directors who, despite not representing any public administration nominally (being appointed by other stakeholders), maintain a direct link with politics (that is, they either hold/held political positions, or stood in political elections in the lists of a political party). This latter type of directors, which we call politicians in disguise, were not a trivial matter in some of the Spanish cajas (e.g., they reached 20% in Caja de Ahorros y Monte de Piedad de Segovia, which merged with Caja Madrid and had a dramatic end). As we see it, these “hidden” politicians were increasing the real degree of board politicization by improperly occupying seats of other cajas’ stakeholders. Thus, we expect that their influence on performance will be highly destructive.

On the other hand, our study on the dangers of the board politicization also addresses the indirect effect of this characteristic when it interacts with financial expertise. There are many cases of politicians with previous financial expertise on the boards of Spanish cajas (one of the best known is Rodrigo Rato, Managing Director of the IMF, Chairman of Bankia, and currently in prison 4 ). As financial experts, we might expect these directors to develop their roles as advisors and supervisors effectively, and so to have a positive effect on cajas’ performance. But since they may also be keeping an eye on other non-financial aims (i.e., political goals), the expected effect on cajas’ performance is not so clear. Here, we examine the resulting effect of these political directors with financial expertise on cajas’ performance.

Our research is based on an original database built from the biographies of 1,525 directors from the 45 cajas that operated in Spain from 2004 to 2010. As expected, we find a negative impact of board politicization on Spanish cajas’ performance, though not in the traditional sense. Specifically, we confirm a pernicious effect of the politicians in disguise on cajas’ performance. In other words, individuals who improperly occupy positions on the board corresponding to other interest groups (especially from the depositors’ quotas) act in a self-interested way and against the economic interests of other stakeholders (like those who they are meant to represent). In addition, we observe that political directors with financial expertise do not use their knowledge for the benefit of the caja, but their homologues without political connections do.

The remainder of the article proceeds as follows. In section “Theoretical background and hypotheses,” we review the literature on the role of politicization with a stakeholder approach and analyze the governance problems due to this issue in the Spanish cajas. In section “Empirical analysis,” we present the sample and the empirical results of the study, first describing the methodology of our analysis, (sample data, sources of information, model, variables, and methodology), and then presenting the results of both the descriptive and explanatory analyses. Finally, in section “Conclusion,” we provide a brief discussion of our results and the most relevant conclusions of this research.

Theoretical background and hypotheses

The board has been traditionally understood as the most important mechanism of the internal control system (Jensen, 1993). Thus, academic research has been focused on the search for an optimal board composition to minimize managerial discretionary behavior, reduce conflicts of interests among the different stakeholders, and finally, create value. However, there are some reasons why the pursuit of this ideal board is more complex in banks than in non-financial companies (John et al., 2016; Macey & O’Hara, 2003; Mehran et al., 2011). First, the complexity of the financial products and services provided by financial institutions and the opacity of the banking business (Andres & Vallelado, 2008; Levine, 2004) make it difficult for external agents to monitor their activities. This increases the relevance of the board of directors as a key mechanism for monitoring banking activities. Second, the high leverage of banking entities and the special (and weak) situation of depositors (as they have a double role as customers and contributors of financial resources) lead to high regulation of financial entities, including some mandatory guidelines about the composition of their boards (Freixas & Rochet, 1997; Heremans, 2000). Finally, the significant positive (their role in monetary policy that facilitates access to credit) and negative (the high risk of bank runs) externalities contributed by the banking business to all its economic agents require the study of the decision-making process of financial entities (including their board) from a broader perspective.

As such, banking entities are complex organizations that affect and/or involve many stakeholders and consequently, their governance is particularly challenging. From a theoretical approach, this large number of agents with a stake, or groups of interest, induces the study of banking entities under theories that take into account all such interests (García-Cestona & Sagarra, 2014). In this sense, while the agency theory considers that the governance mechanisms should be designed to ensure the maximization of shareholder value, the stakeholder theory (Clarkson, 1995; Freeman, 1984) maintains that the organization should be guided by the interests of all its stakeholders and thus, its governance mechanisms should be aimed at the welfare maximization of all the stakeholders. Therefore, the stakeholder theory leads to a broad vision of the role (and configuration) of the board of directors that is more in line with our conception of the banking business.

Spanish cajas from a stakeholder approach

Cajas were credit institutions subject to the same regulation in Spain as commercial banks in terms of the fulfillment of their financial activities, but their goals were broader (inherited from their origin as charitable financial institutions 5 ). Among these goals we can highlight: (1) the provision of universal access to financial services with a preferential attention to small and medium enterprises and domestic economies, (2) the promotion of competition and prevention of monopoly abuse, (3) the contribution to social welfare by allocating part of their earnings to social projects (Obra Social), and (4) their involvement in wealth distribution and sustainable development in the region where they operate (Azofra & Santamaría, 2004; García-Cestona & Surroca, 2008). Therefore, contrary to other financial entities, cajas not only pursue profit maximization but are also conceived as entities serving corporate and social interests, looking for the value maximization of many stakeholders (Argandoña et al., 2009; García-Cestona & Sagarra, 2014).

This concept of cajas led regulators to a broader design of their governing bodies, looking to guarantee the presence of their stakeholders. The nature of their design is based on the non-existence of ownership rights (Azofra & Santamaría, 2004) and the allocation of their control rights by law to different groups of stakeholders (public administrations, institutional founders, employees, and depositors).

The distribution of these control rights was performed for the general assembly (a governing body with functions similar to the general shareholders’ meeting in limited liability companies), the board of directors, and the control committee (charged with overseeing the board’s actions). Regional and state laws defined the voting power of each group of stakeholders through a quota system. The entity’s statues describe the composition of cajas’ boards, specifying the exact weight in the board of each group (within the limits defined by the regional and state laws in force), the procedure to elect the representatives of each group, and the members’ terms (usually 4–6 years). The renewal of the board was always partial, and in any case, the quota assigned to the different stakeholders was strictly applied.

On cajas’ boards, the public administrations, whose aim was to defend the interests of society, were represented by local and regional politicians; the institutional founders (local associations, city halls, and even the Catholic church) designated their own representatives; the employees’ representatives were elected by the trade unions of the entity; and finally, depositors’ representatives were voted by a group of depositors previously elected by a public draw process (called delegates). Therefore, we can say that the design of the cajas’ governing bodies constitutes a paradigmatic example of the practical application of the stakeholder theory because it includes “any individual or group who can affect or is affected by the achievement of the organization’s objectives” (Freeman, 1984, p. 46).

Under this theory all stakeholders defend their own interests and avoid being expropriated. However, the division of control derived from the multiple interests of the different stakeholders and the conflicts that may arise among them can create mistrust that leads to deadlocks in decision-making (Tirole, 2001). Moreover, though all stakeholders are represented on cajas’ governing bodies, not all of them have the same ability to influence its decisions (García-Cestona & Sagarra, 2014). State and regional regulations promoted the allocation of quasi-majority control rights on cajas’ boards to the public administrations’ representatives (see Table 8 of Appendix 1).

Several studies describe the benefits of inviting politicians to join their boards (e.g., Galaskiewicz & Wasserman, 1989; Hillman et al., 1999; Pfeffer, 1972), especially within more heavily regulated industries (Hillman, 2005), such as the banking industry. However, recent studies (Chaney et al., 2011; Sun et al., 2016) examine some other “dark sides” of politically connected boards. As Sun et al. (2016) show for a sample of Chinese firms, a board with political directors can also serve to buffer the legal and regulatory disciplinary pressures against blockholders’ appropriation, thereby making it easier for blockholders to extract rents. From this perspective, when control rights are accumulated in the hands of a group of stakeholders whose members do not bear the residual risk of their decisions, there may be potential problems of expropriation for other stakeholders, especially when there are politicians on the board. These problems, analogous to the traditional governance problem between majority and minority shareholders in stock companies (often termed “principal–principal” conflict), are more relevant in cajas because of their weaker governance mechanisms (Crespí et al., 2004). All this helps to explain why academic studies about cajas’ governance have been focused on the study of politicization.

The politicization of the Spanish cajas

The politicians assume a key role because the legislation gives them high voting quotas as representatives of the public administrations in the government of the cajas. Specifically, the State Law 31/1985 (known as Law on Governing Bodies of Savings Bank [LORCA]) established the voting distribution as follows: public administration, 40%; depositors, 44%; employees, 5%; and finally, founding entities, 11% (if there are no founders, their votes are divided equally among the rest of the stakeholders). However, this State Law had limited application since the Constitutional Court allowed in 1989 regional governments to modify these voting quotas. These new regional quotas introduced greater heterogeneity in the composition of cajas’ boards (Carbó et al., 2004), but in general public administrations reached a clear voting majority in many of them, which leads some authors (Fonseca Díaz, 2005; García-Cestona & Surroca, 2008) to define them as public entities. Thus, regional governments exercised decisive control in the renewal of the Spanish cajas’ governing bodies (García-Meca & Sánchez-Ballesta, 2014) and their voting distribution revealed their preferences about the cajas’ goals. Therefore, when regional governments allocated the majority of the votes to public administrations, they were showing their predilection toward universal access to financing, competition enhancement, or regional development, instead of profit maximization (García-Cestona & Surroca, 2008). In addition, as public administrations are represented on cajas’ boards by politicians, there also exists a high risk that they may use their privileged positions in the entity to obtain personal benefits (e.g., prestige, political influence, low interest loans, and others) as several studies have tested (Dinç, 2005; La Porta et al., 2002; Sapienza, 2004; Shleifer, 1998; Shleifer & Vishny, 1994).

In any case, when public administrations are the dominant stakeholder in cajas, such cajas are especially vulnerable to government control and political rent-seeking (García-Cestona & Sagarra, 2014), and the maximization of their economic benefit is considered as secondary. In this sense, empirical evidence indicates lower efficiency and higher operational risk of banks controlled by politicians (Altunbas et al., 2001; Berger et al., 2005, 2009; Iannotta et al., 2007; Micco et al., 2007). In the case of the Spanish cajas, early studies (Azofra & Santamaría, 2004; Fonseca Díaz, 2005; Melle Hernández & Maroto Acín, 1999) found that board politicization had a negative effect on cajas’ results, coinciding with the time when laws allocated higher control rights to public administrations.

Almost two decades after the approval of the LORCA, Spanish authorities passed the Law 44/2002 on measures to reform the financial system (see Table 8 in Appendix 1). Following European directives, this law was promulgated in the guise of increasing the efficiency of the financial system and also preventing the cajas from being considered “public,” limiting the political presence in their governing bodies to a maximum of 50%. Cajas had some years to adapt their boards and assemblies to this regulation.

This re-balancing of powers (which continued with subsequent laws enacted in 2010 and 2013) sought for the aims of the cajas to no longer be conceived only in social terms but be reconsidered keeping in mind other stakeholders’ interests, such as depositors or employees (whose concerns were more aligned with issues such as economic performance). In fact, the most recent literature finds a positive relationship between the number of political directors on the board and the performance of cajas (García-Cestona & Sagarra, 2014) or a lack of significant relationship between both of them (Cuñat & Garicano, 2010; García-Meca & Sánchez-Ballesta, 2014).

However, we argue that all these studies have not considered the problem of politicization in all its dimensions and complexity. First, from a quantitative viewpoint, they have understood politicization in a formal sense, that is, they have measured it by using the nominal percentage of votes allocated to politicians (i.e., considering only the percentage of seats assigned to public administrations). Second, from a qualitative perspective, the political interests of directors can be interfering with the positive influence that their other characteristics (such as financial expertise) may have on cajas’ performance. As such, we analyze the problem of governance politicization by considering these new quantitative and qualitative dimensions that lead us to propose the main thesis of this study: “Board politicization negatively affects cajas’ performance.”

A new quantitative dimension of politicization: the role of politicians in disguise

The quantitative dimension is related to the way in which researchers measure politicization. As Cuñat and Garicano (2010) point out, Spanish cajas have a level of formal or nominal politicization (calculated according to the number of nominal politicians elected by the group of public administrations) and a real level (related to the politicians elected on behalf of other groups of stakeholders). Thus, measuring the level of politicization based only on the number of nominal politicians does not quantify the actual level of politicization.

The process of selecting directors on cajas’ boards does not prevent the appointment of politicians as representatives of other groups of participants, such as employees or depositors. 6 This distortion in the governance system led some cajas to de facto increase their degree of politicization by appointing directors who, while being politicians, formally represented other groups of stakeholders. The role of these directors—which we refer to as politicians in disguise because their status as politicians is hidden by their representation of a group of participants besides public administrations—is a question that has not been studied before in isolation.

Here, we defend the idea that the presence of these politicians in disguise is detrimental to cajas’ performance in two ways. First, because the mere existence of these politicians implies the expropriation of decision rights of other stakeholders (those whose seats have been occupied) and therefore suggests that the power equilibrium called for by law is broken. When a politician fills the position of another stakeholder on cajas’ boards, the interests of the “replaced” stakeholder become underrepresented in the decision-making. Thus, although the governance model of the cajas were well defined in accordance with the principles of the stakeholder theory, the opportunistic behavior of some groups of stakeholders (traditionally the dominant ones) who circumvent the law supposes a breach of the balance of power determined by legislation that lead them to the control of the cajas’ decision-making. Second, politicians in disguise play an essential role on the board of directors of many cajas because their votes allow the group of public administrations to increase their power and/or achieve absolute majority in the decision-making process. Hence, in line with these two arguments, we propose:

A qualitative dimension of politicization: financial expertise

For the qualitative dimension of politicization, we refer to the consideration of political interest in combination with the rest of the director’s characteristics. Specifically, we focus on the potential differences in the influence of politicians on cajas’ performance depending on their financial experience.

The most recent literature on boards has emphasized the importance of incorporating qualified directors with proven experience in the sector to improve the board’s effectiveness (Dass et al., 2013; Drobetz et al., 2015; Faleye et al., 2013; Papakonstantinou, 2008; von Meyerinck et al., 2016). This experience is especially relevant in complex industries, such as the new technology or financial sectors.

We find empirical evidence to support this positive effect on the entity’s results in the banking industry (Aebi et al., 2012; Hau & Thum, 2009). In the Spanish cajas, the system of allocating representation by quotas made it difficult to improve board professionalism, but empirical literature on these entities also supports the positive effect of this professionalization on the economic results (Andrés et al., 2018; Cuñat & Garicano, 2010; García-Cestona & Sagarra, 2014; García-Meca & Sánchez-Ballesta, 2014).

However, none of these studies have investigated the concurrence of both politicization and financial experience in a director. As Adams (2017, p. 67) notes, “directors are not one-dimensional; directors have multiple attributes, each of which may or may not add value to the firm.” If we consider only the effect of a director with previous financial experience, we would expect an improvement of his or her effectiveness on the board, both as a monitor and an advisor. As several studies show, this feature can even improve when combined with other complementary factors (i.e., independence) related to the increase in the director’s effectiveness, either as a monitor or an advisor (Gul & Leung, 2004; Kroll et al., 2008). However, we wonder here what happens when the two features that interact have an opposing effect on the entity’s performance. Specifically, we examine which is the prevalent influence of a director with previous financial expertise, also on the condition of being a “politician.”

Following Hillman and Dalziel (2003), an increase in board capital (that is, knowledge, experience, etc.) only improves its capacity to monitor and/or advise when the directors who own the capital are motivated to use it. In the case of political directors with financial expertise, we consider that although they do have the knowledge/experience to improve the board’s effectiveness (and thus the entity’s performance), they do not have the motivation to do so because, as we explained previously, they do not usually pursue higher profitability but rather use the entity’s resources to support their social or political interests.

We expect that political directors use their financial skills to justify self-serving decisions instead of those that benefit the organization because previous research finds that political beliefs (often the basis of political status) endure throughout an individual’s lifetime and provide structure to his or her thinking and actions (Ashton et al., 2005; Park et al., 2019). Moreover, when a director maintains political connections, he or she develops a sense of group belonging that becomes a part of his or her identity (Smith & Mackie, 2008). This group feeling motivates the “individual toward attitudes, behaviors, and decisions that promote the in-group . . ., and maintain in-group membership through compliance with in-group norms” (Devine, 2015, p. 512). The psychological attachment to an ideological group, also known as social identity, can represent a process of depersonalization “whereby people come to perceive themselves more as the interchangeable exemplars of a social category than as unique personalities” (Roccas & Brewer, 2002, p. 50). In this sense, the motivation of a political director when making decisions on cajas’ boards will be in line with the interests of the political group which he or she is connected to. As a consequence, though a political director with financial expertise has the capacity to efficiently monitor or advise the caja, we expect that he or she will use it to search for the in-group interests (i.e., social and/or political interests), and when necessary, at the expense of the out-group interests (i.e., increasing the entity’s performance). Thus, we hypothesize:

Empirical analysis

Sample, model definition, variables, and methodology

In this study, we focus on the analysis of the boards of 45 cajas and their performance during the period from 2004 (when cajas were first obliged to publish corporate governance reports) to 2010 (see Table 8 in Appendix 1). 7 We do not include data from 2011 onward because most of the entities disappeared or merged and became commercial banks (there were 45 cajas in 2007 and only 11 at the end of the restructuring process). We manually built a database with the biographies of the 1,525 cajas directors. Relevant data about directors’ appointments, professional backgrounds, and political affiliations of every director were collected from publicly available sources—mostly from the annual corporate governance reports and cajas’ websites, 8 but also from the websites of political parties and regional/local governments, financial press (e.g., Expansion, CincoDias, and others), and social media websites (e.g., LinkedIn, Facebook, and others). In addition, we used the BoardEx database to complete our sample. We obtained financial data from the annual reports published by the Spanish Confederation of Savings Banks (Confederación Española de Cajas de Ahorro).

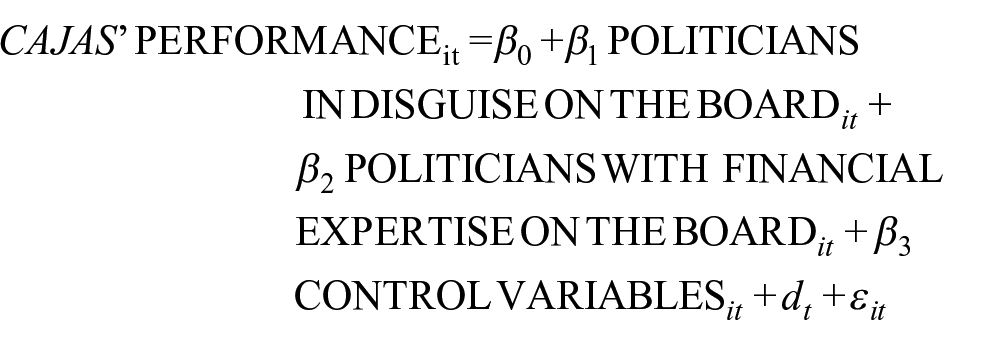

We have the following model to test our hypotheses

where subindex i identifies the caja, t indicates the year, dt represents the time effect, and εit represents the term for the random disturbance. We cannot use market values for the dependent variable because cajas are not publicly traded. Therefore, we use two variables as proxies for performance: return on assets (ROA) and cost efficiency (EFFICIENCY). Models of financial and nonfinancial entities commonly include ROA, where the higher its value is, the greater is the entity’s profitability. EFFICIENCY is a costs-to-assets ratio; that is, the general costs divided by total income. We introduce this variable due to the high fixed costs (e.g., human resources and branches) of cajas. It is important to note that this variable evaluates performance contrary to ROA (the higher the value of EFFICIENCY is, the less efficient the entity is).

Our hand-collected data allow us to identify the number of POLITICIANS IN DISGUISE ON THE BOARD; that is, directors who formally represent other groups of stakeholders, but maintain political connections (i.e., affiliated with a political party or appeared on their electoral lists; POLITICIAN_IN_DISGUISE). We can also combine both politicization and previous financial experience to create the POLITICIANS WITH FINANCIAL EXPERTISE ON THE BOARD (POLITICIAN_EXPERT) variable.

As CONTROL VARIABLES, we include those related to the board, cajas, and regions in which they were established. First, we introduce the number of directors on the board (BOARD_SIZE), the percentage of directors who officially represent the public administrations, and the founding entities that are also public administrations (NOMINATED_POLITICIANS), and the percentage of directors that previously worked in the financial industry (BOARD_EXPERTISE). Second, we include five variables to capture the characteristics of each entity: size (SIZE_CAJA), measured as the logarithm of total assets; solvency (SOLVENCY), measured by dividing total assets by the equity ratio; credit risk (CREDIT_RISK), measured as nonperforming loans divided by total loans; orientation toward lending (LOAN_ACTIVITY), measured by dividing the total amount of loans by total assets; and, finally, we introduce a variable to evaluate the policy of territorial expansion (OFFICES_REGION) through a Herfindahl index that reflects the distribution of the offices of the caja in the different regions. Third, to control for region, we include the maximum percentage of directors that can represent public administrations according to the applicable regional law (LAW_REGION; see a summary of regulations in Table 8 of Appendix 1) and the growth of the GDP of the region in which the caja was constituted (GDP_REGION).

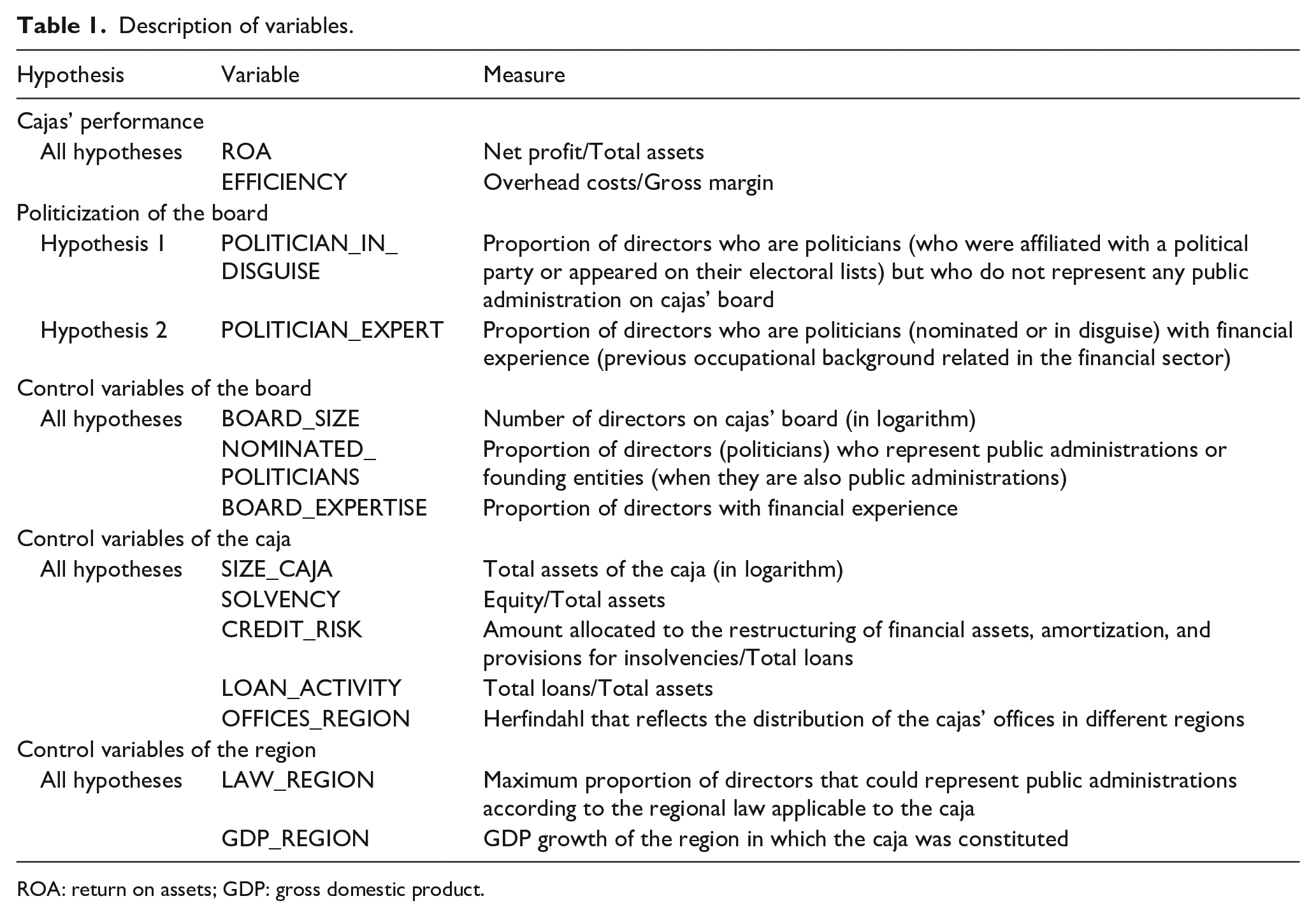

Table 1 summarizes the measures of all variables, and the hypothesis to which they are connected.

Description of variables.

ROA: return on assets; GDP: gross domestic product.

As our sample includes 7 years of data, we use a panel data analysis to test the hypotheses. This panel structure allows us to consider the unobservable and constant heterogeneity of each firm and examine the response processes over time (Arellano, 2003), which reduces the omitted variables problem (Hsiao, 2003). Specifically, we use fixed- and random-effects methodology to address the problems of unobserved heterogeneity by introducing additional firm-specific error terms that can be either fixed over time for each firm (fixed-effects models) or may vary randomly over time for each firm (random-effects models). To evaluate what type of effect best describes the model, we use the Hausman test.

The problem of endogeneity in cajas’ boards of directors is limited because changes in board composition do not follow economic efficiency, but rather legal criteria (the statutes governing the caja define the board member election procedure within the legal framework and outline the board members’ terms). However, we lag one-period all independent variables to control for potential endogeneity problems caused by reverse causality. We estimate all models using the statistical software STATA 14.0.

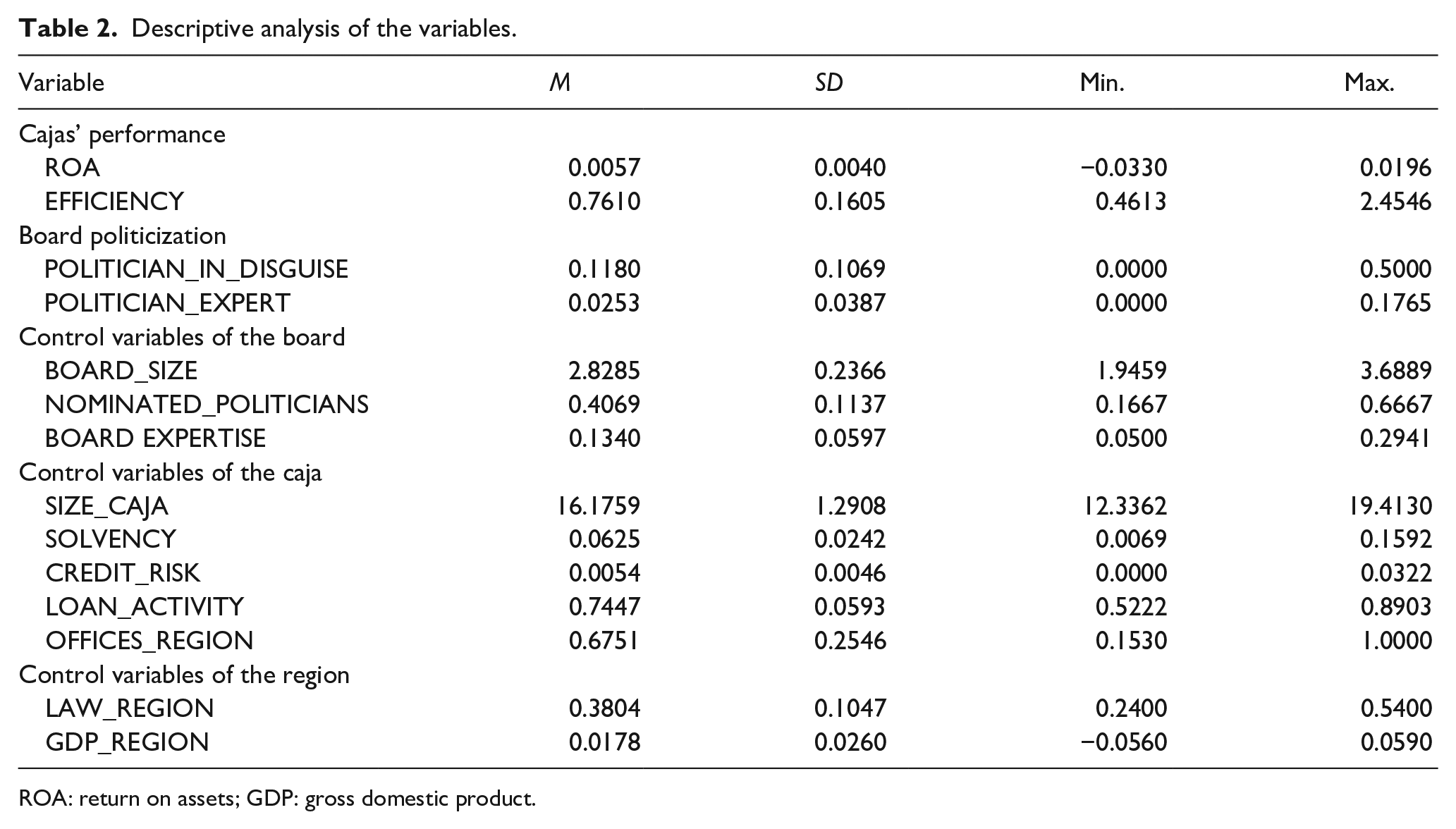

Descriptive statistics

Table 2 provides a summary of the descriptive statistics of our sample (Table 9 of Appendix 1 describes the cajas and regions). While the average ROA was close to 0.6%, cost efficiency (EFFICIENCY) was around 0.76.

Descriptive analysis of the variables.

ROA: return on assets; GDP: gross domestic product.

As in previous studies (i.e., Azofra & Santamaría, 2004; Crespí et al., 2004; Fonseca Díaz, 2005; García-Cestona & Sagarra, 2014; García-Meca & Sánchez-Ballesta, 2014; Melle Hernández & Maroto Acín, 1999), we find high levels of board politicization. More than half of the directors maintain some type of political link, either representing public administrations (NOMINATED_POLITICIANS) or other groups of stakeholders (POLITICIAN_IN_DISGUISE). According to the descriptive statistics, nearly 41% of the seats are allocated to public administrations by cajas’ statutes (NOMINATED_POLITICIANS), and an additional 12% of directors represent other groups of stakeholders while maintaining a recognized political affiliation (POLITICIAN_IN_DISGUISE). These figures show that although cajas were obliged by Law 44/2002 to limit the representatives of public administrations to 50%, this limit was only a de jure imposition that did not work de facto. This majority of politicians on the board is also a general phenomenon in our sample of cajas. In fact, only 16 of the 45 cajas maintain an average representation of politicians below 50% during the sample period, and of these, only eight maintain a proportion below 40%. Even so, we found high dispersion among entities, finding some cajas with a proportion of political directors above 70% (i.e., Caja España de Inversiones, Caja General de Ahorros de Badajoz, Caja de Ahorros de Segovia, and the three cajas from the Basque Country) while others have a percentage lower than 20% (i.e., Caixa d’Estalvis de Terrassa, Caixa d’Estalvis Laietana, and Caixa d’Estalvis de Sabadell).

Our results also show that most of the financial experts lack any kind of political connection. As we can see, 13% of the cajas’ directors work or previously worked in this sector (BOARD_EXPERTISE). This percentage of board financial expertise, although similar to that reported by other studies of public banks (11.1% in Germany according to Hau & Thum (2009) for a sample of public banks), is far from that found in their private counterparts (31.6% in Germany according to Hau & Thum (2009) for a sample of private banks and 20% in the United States according to Minton et al., 2014). However, according to our data, only 2.5% of the cajas’ directors are financial experts who either represent public administrations (nominated politicians) or represent other groups of stakeholders but maintain political links (politicians in disguise).

Explanatory analysis

After describing the variables, we proceed to the empirical testing of the theoretical model using the panel data methodology. For all estimations, we test for multicollinearity with the variation inflation factors (VIF). For greater transparency and rigor, we first test the model by incorporating each variable separately (POLITICIAN_IN_DISGUISE and POLITICIAN_EXPERT), and then include both together (see Table 3).

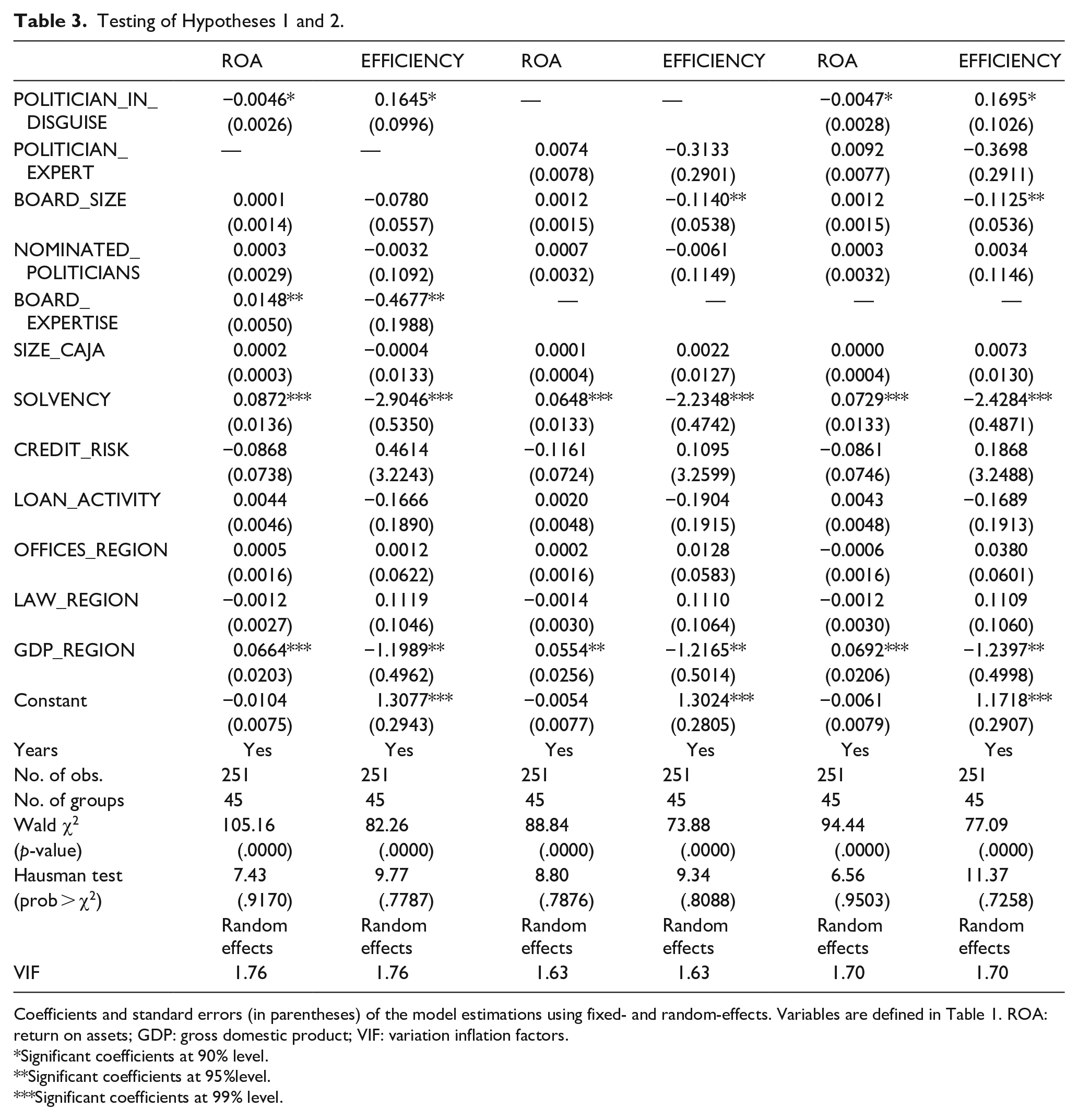

Testing of Hypotheses 1 and 2.

Coefficients and standard errors (in parentheses) of the model estimations using fixed- and random-effects. Variables are defined in Table 1. ROA: return on assets; GDP: gross domestic product; VIF: variation inflation factors.

Significant coefficients at 90% level.

Significant coefficients at 95%level.

Significant coefficients at 99% level.

Our analysis results show what we hypothesize—board politicization has a negative effect on cajas’ performance. Specifically, we find that the presence of politicians in disguise on the board (POLITICIAN_IN_DISGUISE) is especially harmful to the economic performance of Spanish cajas, which confirms our first hypothesis (H1). This result supports the idea that their presence on the boards means not only that most cajas breached the spirit of the law with respect to the reduction of politicization levels, but also that these directors were effectively using the decision rights of some groups of interest outside public administrations (such as depositors) to pursue their own interests. Thus, they were breaking the balance of power defined by the legislation, and ultimately destroyed corporate value.

We also include the traditional measurement of board politicization in the model (Azofra & Santamaría, 2004; Crespí et al., 2004; Fonseca Díaz, 2005; García-Meca & Sánchez-Ballesta, 2014; Melle Hernández & Maroto Acín, 1999), namely, the percentage of directors who officially represent the public administrations (NOMINATED_POLITICIANS). But, in line with the latest empirical findings (Cuñat & Garicano, 2010; García-Meca & Sánchez-Ballesta, 2014), our results show a lack of influence of this variable on cajas’ performance.

Moreover, the results in our tables show that the percentage of directors with financial experience on cajas’ boards (BOARD_EXPERTISE) is positively related to both the profitability and efficiency of the entities, which is consistent with previous research on this type of entity (Cuñat & Garicano, 2010; García-Cestona & Sagarra, 2014; Hau & Thum, 2009). However, when we introduce the individualized effect of directors who, in addition to being financial experts, maintain political links, this positive effect disappears (see the non-significant coefficients of POLITICIAN_EXPERT). That is, although these directors, as financial experts, have training to effectively carry out advisory and monitoring functions in theory, their status as political advisers seems to inhibit the behavior that would result in greater value creation. This result does not allow us to support our second hypothesis (H2) because we do not evidence any significant negative effect, as we expected. However, the positive effect of the financial expertise is lost when the director simultaneously has political motivations and a financial background.

Sensitivity analysis

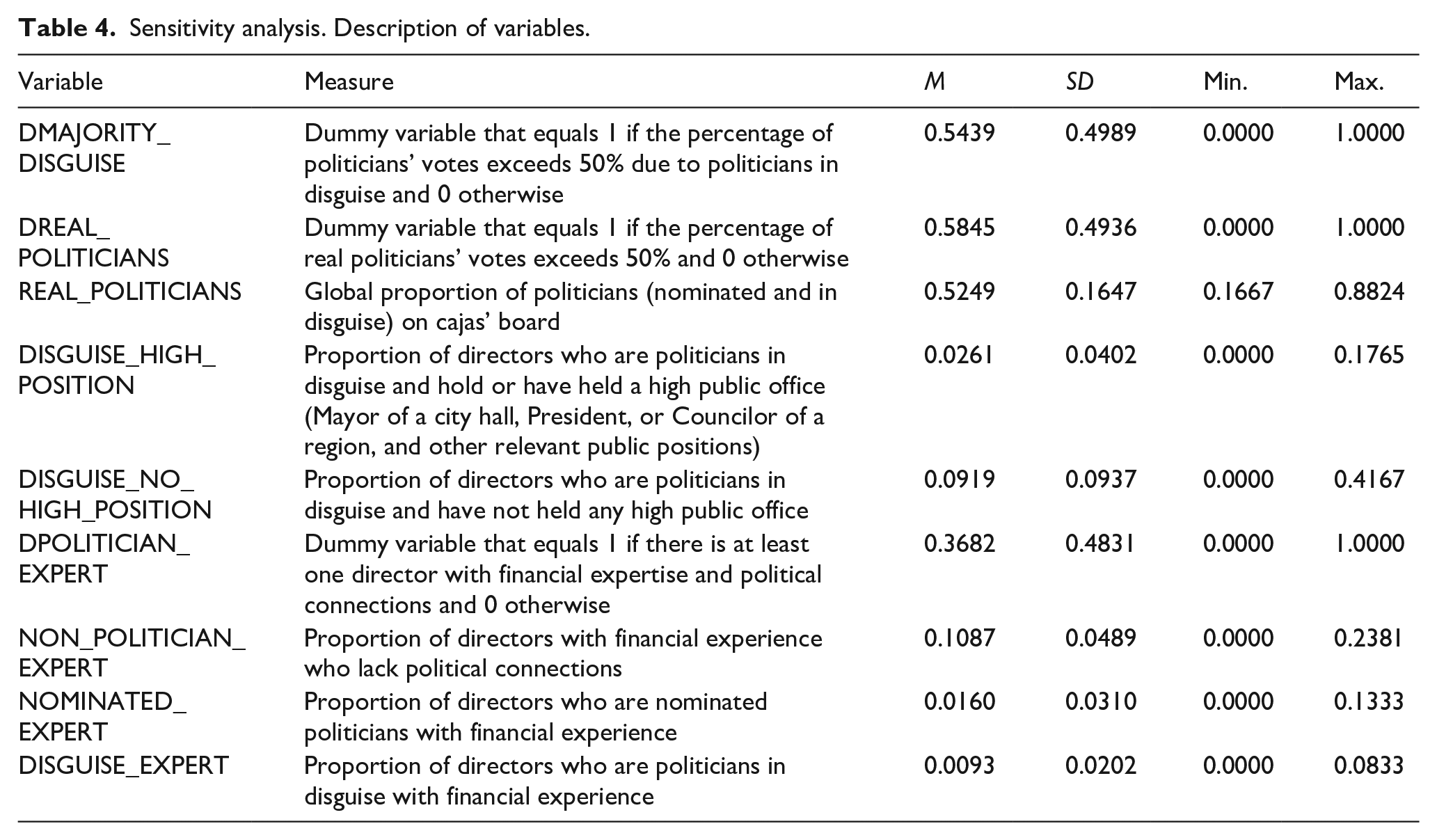

Here, we present some assessments on how politicians influence cajas’ performance. Table 4 summarizes all the variables we use in this sensitivity analysis.

Sensitivity analysis. Description of variables.

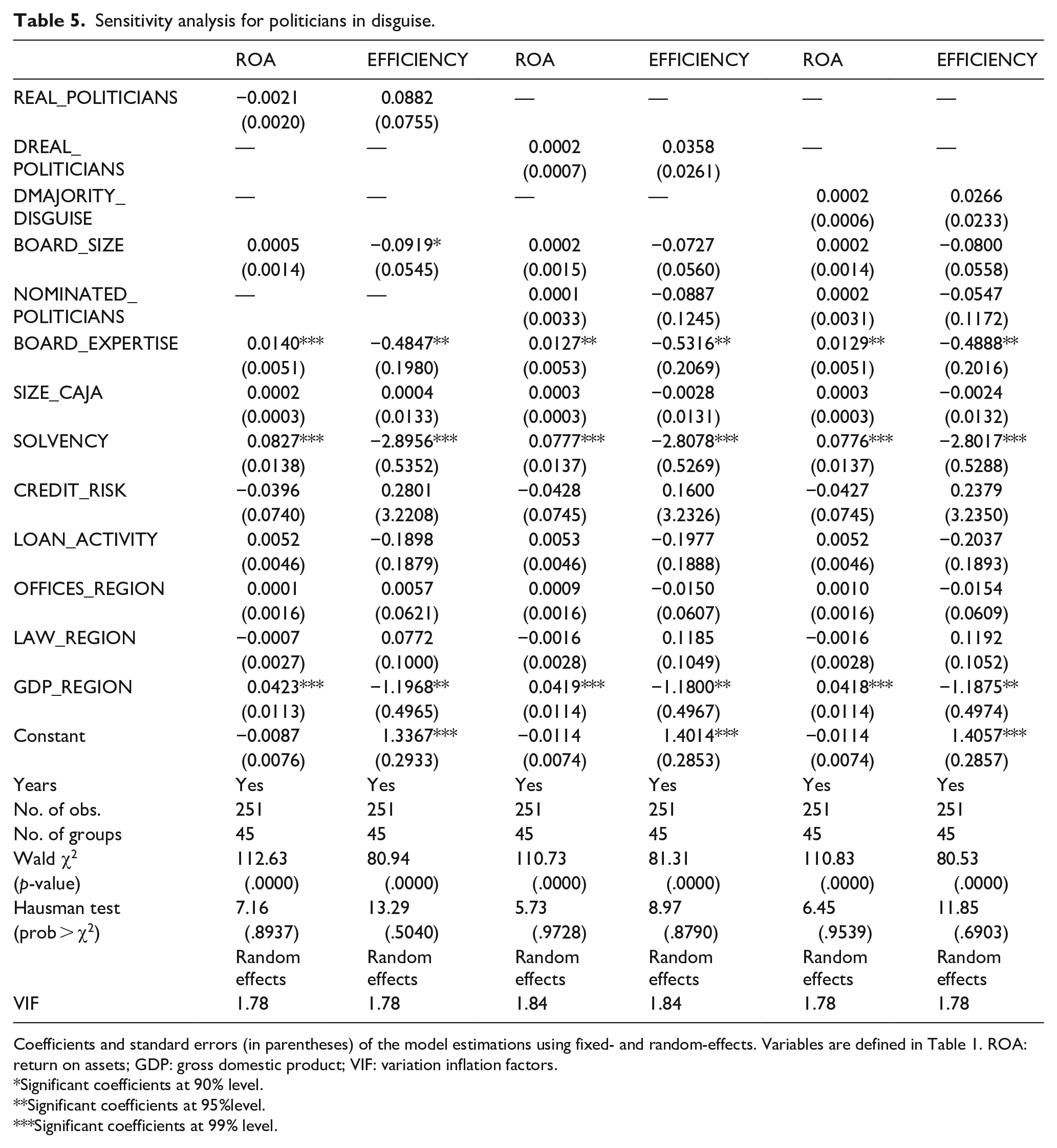

First, to further analyze why politicians in disguise destroy value in Spanish cajas, we go back to the theoretical arguments we offered when we proposed the first hypothesis. On the one hand, we explained how politicians in disguise were improperly using the decision rights of other stakeholders, breaking the balance of powers imposed by the legislation, and preventing groups such as depositors from pursuing the increase in cajas’ performance. We consider this argument as a direct effect of the variable POLITICIAN_IN_DISGUISE on cajas’ performance, which we tested in Table 3. On the other hand, these politicians in disguise could have an indirect effect on cajas’ performance, as they could suppose a way to circumvent the laws that limit the power of politicians on cajas’ boards by allowing them to achieve majority control of the board and fulfill their own interests. We evaluate the validity of this second argument by using three different variables: (1) REAL_POLITICIANS to measure the global effect of the political directors (both nominated and in disguise), (2) DREAL_POLITICIANS to measure whether there is a majority of directors on the board with political connections, and (3) DMAJORITY_DISGUISE to identify the entities in which the politicians in disguise allow the group of nominal politicians to attain the absolute majority of control rights on the board. However, as we can see in Table 5, none of these variables has a significant effect on the entity’s performance. Thus, we maintain the idea that the problem of cajas during these years was not an accumulation of politicians on the board, but the inappropriate behavior of some directors nominally representing a specific group of stakeholders though they defend the interests of others (politicians in disguise).

Sensitivity analysis for politicians in disguise.

Coefficients and standard errors (in parentheses) of the model estimations using fixed- and random-effects. Variables are defined in Table 1. ROA: return on assets; GDP: gross domestic product; VIF: variation inflation factors.

Significant coefficients at 90% level.

Significant coefficients at 95%level.

Significant coefficients at 99% level.

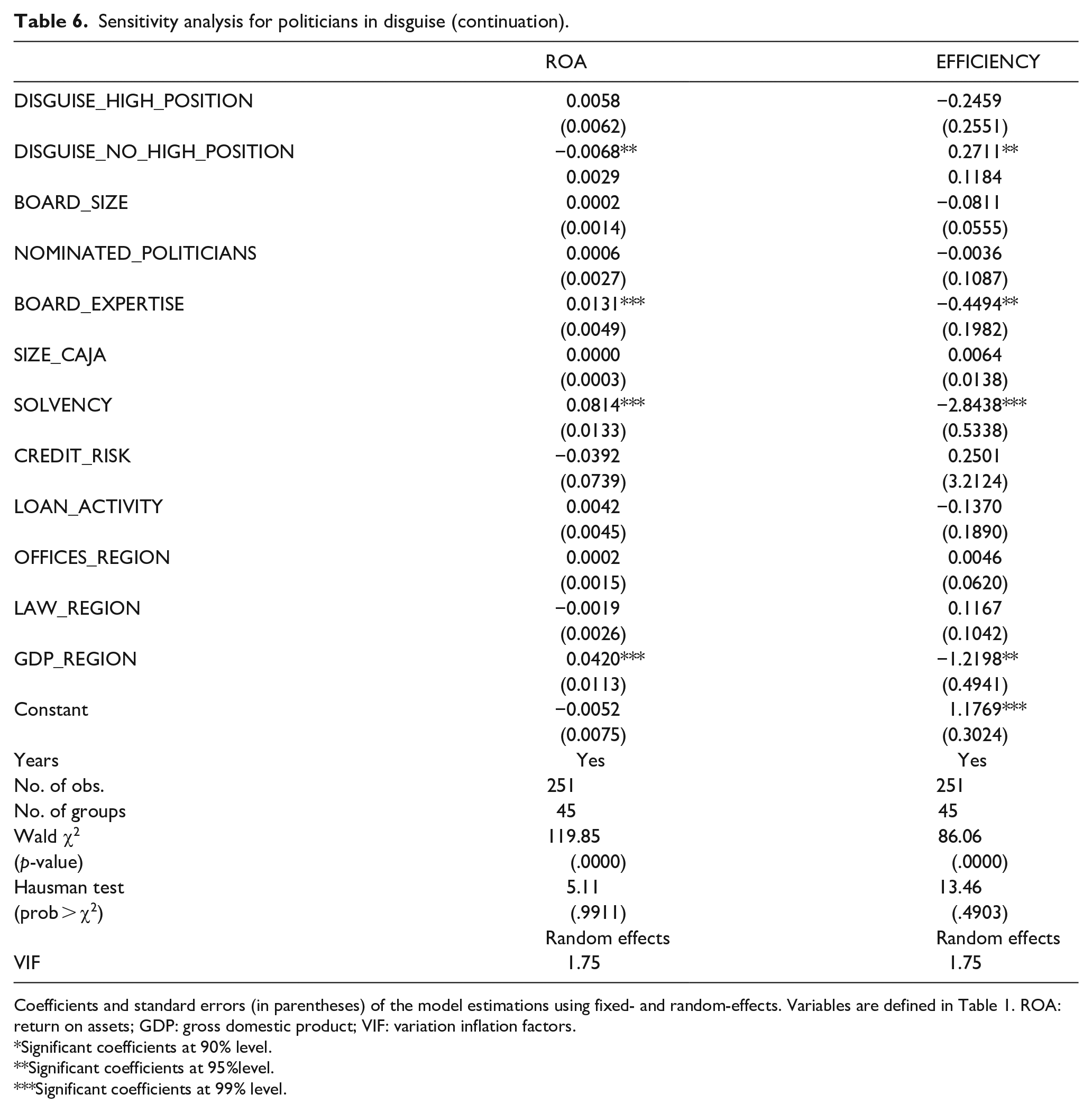

Second, after finding that the influence of politicians in disguise was not because they gave more power to the rest of the politicians, we try to shed more light on which kind of politicians in disguise are more harmful for cajas’ performance. In our opinion, their negative effect can be related to their lower public visibility. As they do not act on behalf of any public administration, they are in a more comfortable position to behave opportunistically. Their position “in the shadows” allows them to make decisions without affecting their public image and political reputation. The decisions of political directors on the board as representatives of some public administration (nominated or formal politicians) have both a high public (with regard to their voters) and political (with regard to their political party) visibility. This visibility provides these directors with greater reputational value, which increases their incentive to be seen as competent supervisors (Fama & Jensen, 1983; Masulis & Mobbs, 2014). On the contrary, directors who are “hidden” (i.e., their actions in the caja do not affect their public image) can make decisions for their own interest and enhance their reputation in their political party. In this sense, we think that politicians in disguise that hold or held a relevant public office (DISGUISE_HIGH_POSITION) are more exposed to public opinion than those who have political ties but who do not occupy high public positions (party-affiliated, but without holding a relevant public office) are (DISGUISE_NO_HIGH_POSITION). We therefore differentiate between these two types of directors to test this argument. According to our results (see Table 6), politicians who occupy high positions (DISGUISE_HIGH_POSITION) do not affect the results of the entity, while those with no relevant public positions (DISGUISE_NO_HIGH_POSITION) have a significant and negative influence on cajas’ performance. We could therefore conclude that as the actions of these anonymous politicians in disguise are less visible, they have more chances to behave opportunistically without directly bearing the consequences of their decisions.

Sensitivity analysis for politicians in disguise (continuation).

Coefficients and standard errors (in parentheses) of the model estimations using fixed- and random-effects. Variables are defined in Table 1. ROA: return on assets; GDP: gross domestic product; VIF: variation inflation factors.

Significant coefficients at 90% level.

Significant coefficients at 95%level.

Significant coefficients at 99% level.

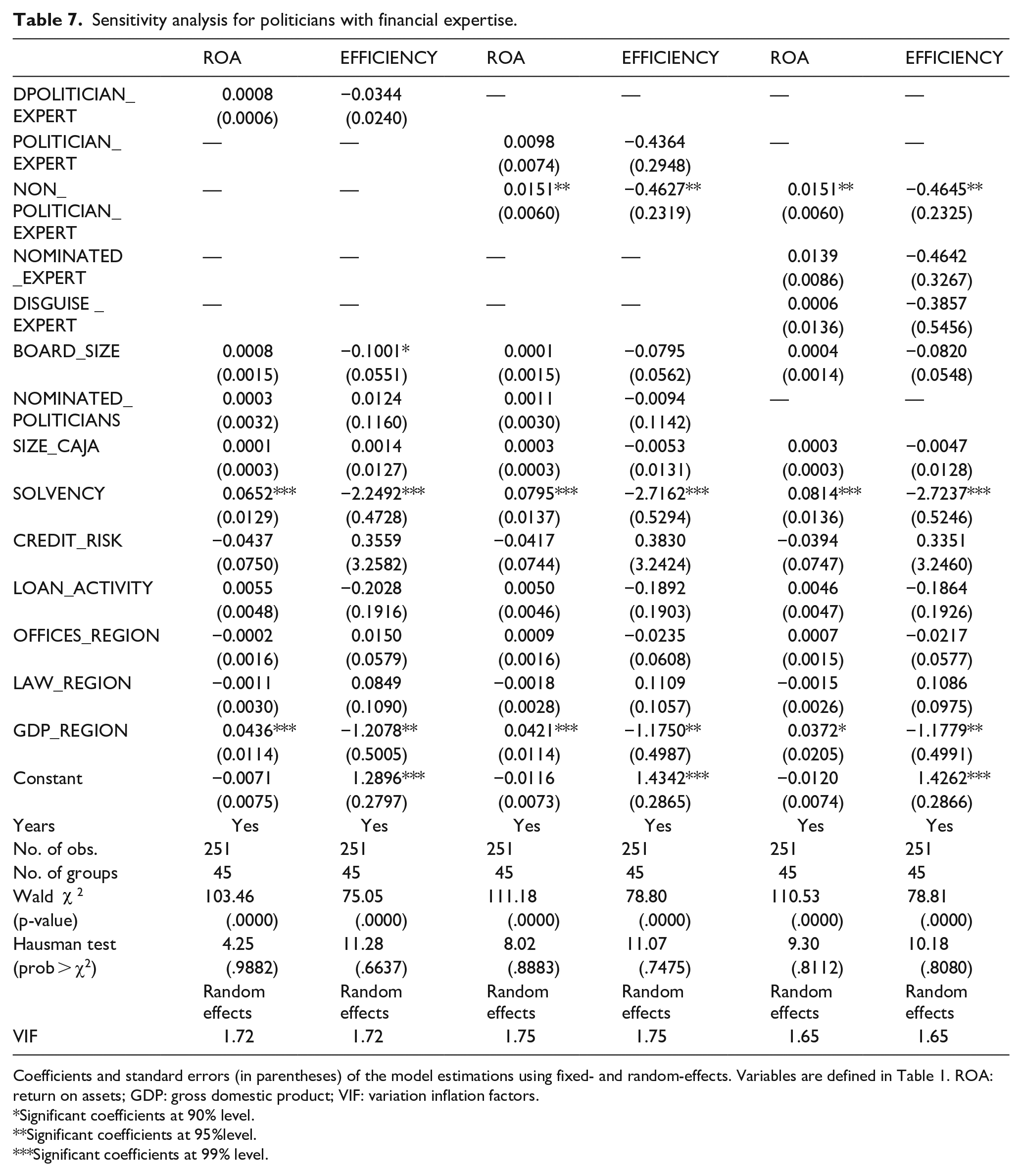

Finally, we explore the influence of political directors who also have financial experience in depth. To do so, we first calculate a dummy variable to measure whether there is at least one politician with financial experience on the board (DPOLITICIAN_EXPERT), and build an additional variable that measures the effect of financial experts who have no political connections (NON_POLITICIAN_EXPERT). As we can see in the first two columns of Table 7, the presence of at least one director on the board with combined previous financial experience and political interests (DPOLITICIAN_EXPERT) has no effect on cajas’ economic results, which is in line with our previous results when using the continuous variable. In addition, based on the results in the third and fourth columns of Table 7, the effect of the proportion of financial experts with political connections (POLITICIAN_EXPERT) remains insignificant, while the percentage of financial experts without political motivations (NON_POLITICIAN_EXPERT) is positive and statistically significant. This result suggests that the only directors who add value to cajas are those who have previous financial experience but lack any political interest. This positive effect is maintained throughout the fifth and sixth columns of Table 7, where we include the same variable, but we have divided the percentage of politicians with financial expertise (POLITICIAN_EXPERT) into two groups: nominated directors with financial experience (NOMINATED_EXPERT) and financial experts with political connections who do not represent any public administration on cajas’ board (DISGUISE_EXPERT). In line with the previous results, both types of politicians with financial experience have no significant effects on cajas’ economic results.

Sensitivity analysis for politicians with financial expertise.

Coefficients and standard errors (in parentheses) of the model estimations using fixed- and random-effects. Variables are defined in Table 1. ROA: return on assets; GDP: gross domestic product; VIF: variation inflation factors.

Significant coefficients at 90% level.

Significant coefficients at 95%level.

Significant coefficients at 99% level.

Conclusion

For years, academics and the public discussed the politicization of the governing bodies and their influence on cajas’ performance. This discussion intensified during the last financial crisis due to the scandals of opportunistic behavior of some caja directors, along with their disappearance as financial entities. Our study brings light on this topic by considering two novel aspects. First, we show a new way of politicization by detecting political directors that were “hidden” within cajas’ boards by occupying the seats of other stakeholders. Second, we examine the predominant effect when directors have the two attributes of politicization and experience.

Our study shows that the level of politicization in cajas was much higher than what nominally appeared in corporate governance reports because of the existence of politicians in disguise. However, we do not find that this higher level of real politicization leads to lower performance in cajas. Instead, we test that these hidden politicians destroyed corporate value by negatively affecting the entity’s performance, both in terms of efficiency and profitability. The existence of politicians in disguise on the boards and their negative effect supports the idea that the governance problems of cajas did not arise from the design of their governing bodies, but from the inappropriate behavior of some of their directors. This occurred because although the regulators’ design limited the participation of each group of stakeholders on cajas’ boards of directors, some politicians misappropriated some of the seats reserved for other stakeholders. When politicians in disguise championed their own interests instead of those of the groups they nominally represent, they violated the balance of power set by legislation, and ultimately destroyed value.

Analyzing the detrimental effect of politicians in disguise more deeply, we find that it is also related to the public visibility of their decision-making and the consequent ability to behave opportunistically. This assertion stems from the fact that according to our results, they have a negative influence only when they do not occupy a high political position; that is, when they are effectively less visible to the public. This lack of visibility prevents their actions in the caja from affecting their image, while allowing them to improve their political party position by making decisions that favor the party’s interests.

The existence of politicians in disguise highlights the need to go beyond standardized databases or corporate governance reports if we wish a more realistic analysis of the board composition. As McNulty and Pettigrew (1999, p. 52) point out, this kind of research addresses “a need to get closer to boards and directors to collect primary data about processes of contribution, power and influence.” In addition, our results, though specific to cajas, may also be relevant for other entities that might include individuals with political motivations, but no relevant public position, who also put their interests (or those of their political party) above those of the company.

We also find that when the director is politically motivated, the positive value of the directors’ experience is lost. Our results show that political interests interfere with a financial expert’s effective decision-making ability. Here, we deal exclusively with the effect of the conflict between professional experience and political interests, but the analysis could be extended to other types of conflicts due to professional interests (such as participation on the board or ownership in other companies), or personal connections (like alignment of votes between directors linked through their university, membership in exclusive clubs, or nationality), among others.

Therefore, both for future academic research and in hiring directors in practice, we highlight the need to think of directors in a more holistic way; that is, we cannot evaluate their independence, political motivations, or professional experience in isolation because all of these factors influence the directors’ actions, and thus their decision-making. In this line, the European Regulation 9 and consequent adaptation of Spanish legal framework (Bank of Spain, 2016) emphasize this holistic nature of directors, when they are required not only the necessary knowledge and experience to effectively accomplish their role, but also they ought to act with honesty, integrity and independence of mind. This independence of mind assessed in the guidelines of the European Banking Authority (EBA) refers to the potential conflicts of interests that would impede the directors’ ability to perform their duties independently and objectively, and it explicitly alludes to the political influence or political relationships as a situation that could create this kind of conflicts, see Guideline 109 (f) on EBA/GL/2017/12 and Guideline 84 (g) on EBA/GL/2017/12. In Spanish cajas, the Law 26/2013 (see Art. 3 and 4) avoids these political conflicts of interests by making explicit the incompatibility of being appointed director and having an executive or elected political position. All this tries to ensure directors keep an eye on the interests of the entity they govern above their own ones.

Footnotes

Appendix 1

Spanish cajas in 2004.

| Name | Region |

|---|---|

| Caja de Ahorros San Fernando de Sevilla y Jerez (Cajasol from 2007) | Andalusia |

| Caja de Ahorros y Monte de Piedad de Córdoba (CajaSur) | |

| Caja General de Ahorros de Granada | |

| Caja Provincial de Ahorros de Jaén | |

| Monte de Piedad y Caja de Ahorros de Huelva y Sevilla (Cajasol from 2007) | |

| Montes de Piedad y Caja de Ahorros de Ronda, Cádiz, Almería, Málaga y Antequera (Unicaja) | |

| Caja de Ahorros de la Inmaculada de Aragón | Aragon |

| Caja de Ahorros y Monte de Piedad de Zaragoza, Aragón y Rioja (IberCaja) | |

| Caja de Ahorros de Asturias | Asturias |

| Caja de Ahorros de Pollença “Colonya” | Balearic Islands |

| Caja de Ahorros y Monte de Piedad de Las Baleares (Sa Nostra) | |

| Bilbao Bizkaia Kutxa | Basque Country |

| Caja de Ahorros de Vitoria y Álava | |

| Caja de Ahorros y Monte de Piedad de Gipúzkoa y San Sebastián | |

| Caja General de Ahorros de Canarias | Canary Islands |

| Caja Insular de Ahorros de Canarias | |

| Caja de Ahorros de Santander y Cantabria | Cantabria |

| Caja de Ahorros de Salamanca y Soria (Caja Duero) | Castile and Leon |

| Caja de Ahorros Municipal de Burgos | |

| Caja de Ahorros y Monte de Piedad de Ávila | |

| Caja de Ahorros y Monte de Piedad de Segovia | |

| Caja de Ahorros y Monte de Piedad del Círculo Católico de Obreros de Burgos | |

| Caja España de Inversiones, Caja de Ahorros y Monte de Piedad | |

| Caja de Ahorro Provincial de Guadalajara | Castilla-La Mancha |

| Caja de Ahorros de Castilla La Mancha | |

| Caixa d’Estalvis Comarcal De Manlleu | Catalonia |

| Caixa d’Estalvis de Catalunya | |

| Caixa d’Estalvis de Girona | |

| Caixa d’Estalvis de Manresa | |

| Caixa d’Estalvis de Sabadell | |

| Caixa d’Estalvis de Tarragona | |

| Caixa d’Estalvis de Terrassa | |

| Caixa d’Estalvis del Penedes | |

| Caixa d’Estalvis i Pensions de Barcelona (La Caixa) | |

| Caixa d’Estalvis Laietana | |

| Caja de Ahorros y Monte de Piedad de Madrid | Community of Madrid |

| Monte de Piedad y Caja General de Ahorros de Badajoz | Extremadura |

| Caja de Ahorros y Monte de Piedad de Extremadura | |

| Caixa de Aforros de Vigo, Ourense e Pontevedra (Caixanova) | Galicia |

| Caja de Ahorros de Galicia | |

| Caja de Ahorros de La Rioja | La Rioja |

| Caja de Ahorros y Monte de Piedad de Navarra | Navarre |

| Caja de Ahorros de Murcia | Region of Murcia |

| Caja de Ahorros de Valencia, Castellón y Alicante (Bancaja) | Valencian Community |

| Caja de Ahorros del Mediterráneo (CAM) | |

| Caja de Ahorros y Monte de Piedad de Ontinyent |

Acknowledgements

The authors gratefully acknowledge the helpful suggestions received from the two anonymous reviewers and the Associate Editor, Mircea Epure. The authors also thank the comments received from B. Arruñada, G. Natividad, A. Martín, V. Salas and N. Suárez, and the participants at the ACEDE Conferences held in Vigo and Valladolid.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Spanish Ministry of Economy and Competitiveness (Grant ECO2017-85356).