Abstract

This study explores the relationship between board diversity and firm performance, with a focus on the moderating role of CEO duality in Chinese manufacturing firms. This study applies panel fixed-effect regression models for the period 2008–2022, and findings show that board diversity is positively associated with firm performance, and CEO duality negatively moderates the relationship. However, the findings also show that a highly diversified board can minimize the negative effect of CEO duality and increase the firm’s performance. Furthermore, the findings broaden the understanding of board attributes, showing that the education index is more evident among other board attributes for firm performance. This study verifies its results using the two-step system generalized method of moments approach and different board attributes in robust tests. The findings suggest that strategic efforts to promote board diversity may increase the board’s monitoring function and control managerial opportunism, ultimately improving firm performance in the Chinese business landscape.

Introduction

The board of directors has gained a significant role in corporate governance owing to its different attributes (Sierra-Morán et al., 2024). In recent years, corporate boards have increasingly changed regarding director attributes such as age, gender, education, expertise, and so on. For example, the representation of females in the top 100 fortune firms’ corporate boards has increased from 16.8% in 2004 to 26% in 2018 (Chen et al., 2023; Deloitte, 2019; Ting et al., 2021). However, the tendency for a more diversified corporate board has raised the following questions over time: Why would firms aim to diversify boardroom representation? And what’s the driving force behind this tendency? Although there are numerous possible answers to these questions, one of the reasons for promoting board diversity (BD) has been suggested to be the performance implications of diversity. Furthermore, it can also improve decision-making by bringing individuals together with different backgrounds, perspectives, and expertise, fostering creativity (Dong et al., 2023; Siciliano, 1996; Van der Walt & Ingley, 2003). Despite the increased interest and effort in mainstream business studies to address these questions, researchers in the manufacturing industry have shown little interest in this specific research area. However, the outcomes from earlier studies may relate to manufacturing firms to some extent. Still, several reasons push the manufacturing sector to examine the impact of board diversification on a firm’s outcomes, such as the corporate governance mechanism, which is a momentous managerial characteristic for manufacturing firms (Upton, 1994). This is because it is closely related to controlling and monitoring managerial activities (F. Ali et al., 2023; T. H. Nguyen et al., 2021), and these activities can influence the firm value.

Moreover, a diversified board carries distinctive insights and experiences, which can increase the ability to adjust in a rapidly changing business environment, such as implementing innovative ideas and lowering agency costs (Fayyaz et al., 2023; Xu & Li, 2022). According to Gill and Biger (2013), manufacturing firms with effective governance mechanisms can gain greater benefits from internal monitoring and boost their revenue. Therefore, it is economically crucial to understand how China’s manufacturing firms are governed because their governance may differ from the other sectors, particularly due to the industry’s features (Goh et al., 2014; Gu, 2024). For instance, the manufacturing industry is characterized by capital intensity, 1 large-scale operations, 2 complex global supply chains, 3 technological innovation, 4 stringent regulatory requirements, 5 and so on (F. Ali et al., 2024; Anazonwu et al., 2018; Asad et al., 2023; Y. x. Li & He, 2023; Miller & Triana, 2009; Reguera-Alvarado & Bravo-Urquiza, 2020). A recent study by Björkdahl (2020) underscores the importance of BD in enhancing the governance of Chinese manufacturing firms, indicating that firms with diverse boards perform better in terms of strategic decision-making. The diversity enables firms to effectively address the unique challenges and leverage the opportunities inherent in the manufacturing sector (Juniarti & Jie, 2024). This is because a diverse board that includes members with varied backgrounds can enhance decision-making processes and improve overall corporate performance (F. Ali et al., 2023). Therefore, diverse boards contribute to more comprehensive strategic decisions by bringing multiple perspectives and expertise.

Furthermore, on a corporate board, the dual role of the chief executive officer (CEO duality) is crucial in firm strategic planning and decision-making. It can enhance the accountability and responsibility of the executive, as they have a more direct stake in the board’s decisions (Ogoe & Suzuki, 2023; Riaz et al., 2023). Conversely, it may reduce the board’s independence and oversight, leading to potential conflicts of interest, less-effective checks and balances, and a risk of managerial entrenchment (M. Yu, 2023), which can negatively influence firm value. However, the link between BD and CEO duality lies in the potential influence of diverse boards on the decision to separate the roles of CEO and chairman. A diverse board may more likely recognize the importance of separating these roles to ensure effective corporate governance (Bukari et al., 2024; Giang & Hien, 2024; Pache et al., 2024). Therefore, it is anticipated as a feature that can influence the relationship between BD and firm value (Ogoe & Suzuki, 2023). Earlier studies showed that CEO duality had mixed results with firm performance; for instance, Chang et al. (2019) and Hassan et al. (2023) found a positive effect; H. Liu et al. (2021), T. Ali et al. (2021), Tang (2017), and Duru et al. (2016) found a negative effect; and Dahya et al. (2009) and Elsayed (2007) found no effect. Given these inconsistent results of CEO duality on firm performance, and up to the authors’ best knowledge, no study has examined the association among BD, CEO duality, and firm performance. Therefore, this study delivers new insight into the association between BD and firm performance by analyzing whether CEO duality modifies the impact of BD on firm performance.

Using a sample of Chinese manufacturing firms and panel fixed-effect regression models for the period 2008–2022, the study findings show that BD 6 is positively associated with firm performance, 7 and CEO duality negatively moderates the relationship. Furthermore, the findings show that both high- and low-diverse board groups positively relate to firm performance; however, their relationship strength differs. A highly diversified board is more likely to enhance the firm’s performance than a less-diversified board. Moreover, the results show that the CEO duality moderating role differs for high- and low-diverse board groups. The findings show that a highly diverse board is significantly positively associated with firm performance, and CEO duality positively moderates the relationship. However, in the case of a lower diversified board, the moderation results of CEO duality are the opposite. Furthermore, the findings broaden the understanding of board attributes, showing that the education index is more evident among other board attributes for firm performance. This study’s results are robust as we employ the two-step system generalized method of moments approach and different attributes of BD. Our results are consistent with the agency and resource dependency theories. The findings suggest that strategic efforts to promote BD may increase the board’s monitoring function and control managerial opportunism, ultimately improving firm performance in the Chinese business landscape. This study’s results could be generalized to other sectors with similar characteristics, such as technology, finance, and energy, which also benefit from diverse boards regarding strategic decision-making, risk management, and performance enhancement.

This study contributes to the existing literature in three different ways. First, this study stretches the literature on a comprehensive measure of BD by imputing the unique perspective of social psychology. It establishes a novel approach by studying the composition of the corporate board through two key dimensions: demographic and cognitive diversities. By integrating these diversity components, this study provides a better understanding of the perception of how diverse boards influence firm performance. This new perspective promises to shed light on the complex interplay between BD and firm success, offering valuable insights for businesses aiming to optimize their board composition for better firm performance. Earlier studies considered only a single aspect of the board of directors’ attributes, such as age or gender (Brahma et al., 2021; Y. Liu et al., 2020; Yarram & Adapa, 2021), their outcomes are difficult to generalize without considering the different composition of board attributes. Furthermore, this study broadens the understanding of board attributes, showing that the education index is more pronounced among other board attributes for firm performance.

Second, this study presents CEO duality as contingent on the relationship between the board members’ diversification and firm output. This study’s findings contribute to the literature by showing that BD is positively associated with firm performance, and CEO duality negatively moderates the relationship. Furthermore, the findings reveal that both highly diverse and less-diverse boards positively impact firm performance, although the extent of this impact varies. Highly diversified boards are more significant in boosting firm performance than less-diverse boards. In addition, the role of CEO duality as a moderating factor differs between these groups. For highly diverse boards, CEO duality strengthens the positive relationship with firm performance. Conversely, in less-diverse boards, CEO duality has the opposite effect, weakening the performance relationship. These insights underscore the importance of BD and the nuanced role of leadership structures in driving business success. Therefore, this study’s significant contribution comes from its use of a specific contingency, namely CEO duality.

Third, this study explores the association between BD and firm performance, with a particular focus on the moderating effect of CEO duality within manufacturing firms. 8 The rationales for including manufacturing are as follows: First, manufacturing is the fastest-growing sector, and it is one of the critical components of the driving force of economic development (Smriti & Das, 2018). Furthermore, 2022 reports state that China’s manufacturing output in 2021 was $4,865.83 billion, reflecting a 26.04% increase from 2020. 9 In 2022, the manufacturing industry accounted for nearly 27.44% of China’s gross domestic product (GDP), making it the largest contributor to the global manufacturing sector (Lin & Guan, 2023; X. Sun et al., 2023), producing 40% of the top 500 global industrial products, 10 and it has become the main operating force in developing China’s economy (Zhang & Yao, 2018). “Made in China 2025” is a national strategic plan and industrial policy implemented by the China Communist Party to advance China’s manufacturing sector (Commerce, 2017; Y. Wang, 2015; Xu & Sim, 2017), upgrading manufacturing capabilities 11 and transitioning from labor-intensive to technology-intensive powerhouses. By 2025, it is anticipated that China’s manufacturing industry will generate revenues of approximately 885.68 billion U.S. dollars. 12 Therefore, an effective board is crucial for managing market demand and supply, shaping strategies, and improving the decision-making process to improve the manufacturing sector’s performance. Second, manufacturing firms operate in competitive sectors, necessitating a focus on customers and suppliers. This highlights the importance of effective stakeholder management within the sector, which places additional responsibilities on the boards of directors. These include ensuring rigorous oversight of decisions regarding stakeholders, customer demand and supply, business partnerships, and fair competition. Resultantly, a diverse board gains additional importance in the manufacturing sector because its diversified characteristics can bring different skills, knowledge, industrial experience, and perspectives to the boardrooms following the agency and resource dependency theories (Fama & Jensen, 1983; Hillman & Dalziel, 2003; Hillman et al., 2007; Reitz, 1979). Therefore, this study’s findings are important for shareholders, investors, and policymakers in understanding how a diversified board enhances the performance of manufacturing sectors.

The rest of this article is organized as follows. The Theory Building and Hypotheses Development section describes the theoretical foundation and introduces the development of the research hypotheses, and the Methodology section presents the data collection process and research design. The Empirical Results section defines the key findings, and the Robustness Tests section provides additional tests to ensure the stability of the results. The Conclusion section shows the main insights of the study, limitations, and future direction.

Theory building and hypotheses development

Underpinning theory

Agency theory posits that BD can mitigate agency problems by enhancing organizational monitoring and accountability mechanisms. Therefore, it argues that the board is the key component of the corporate governance mechanism intended to oversee managerial decisions (F. Ali et al., 2023; Fama & Jensen, 1983). In light of the agency theory perspective, a diverse board can increase oversight function by bringing varied perspectives and expertise, leading to better governance and improved organizational performance. In this regard, a diversified board can reduce the shareholders’ and managers’ problems (Mehedi et al., 2024). Furthermore, board members spanning various ages, races, ethnicities, and cultural backgrounds bring a wealth of knowledge, education, skills, and unique perspectives to the boardroom. Resultantly, diversity fosters a challenging environment for the management teams, stimulating healthy debates on decisions, and ultimately improving firm value (W. Yu & Zheng, 2014). However, many traditional independent directors are speculative about a diverse boardroom (Carter et al., 2003; W. Yu & Zheng, 2014).

In addition, the resource-dependency theory also argues that the board of directors plays an important role in serving its legal obligations to the shareholders’ interests (Hillman et al., 2000). It emphasizes the significance of external resources for a firm’s survival and success, positing that firms depend on external resources such as capital, knowledge, and relationships to function effectively. In the context of resource dependency theory, the board of directors plays a vital role in supplying essential resources to the firm (Pearce & Zahra, 1992; Zalata et al., 2019) by leveraging their broader social networks to foster external relationships (T. Nguyen et al., 2015; Reguera-Alvarado et al., 2017). In addition, they offer strategic guidance to significant corporate decision-making processes, aiming to ensure firm survival and increase its competitive advantage and performance (Hendry & Kiel, 2004; Hillman & Dalziel, 2003; Macus, 2008).

Diverse boards deliver strategic direction to management, positioning corporate strategies with shareholder interests and leveraging external relationships to approach critical resources and opportunities. Therefore, both theories complement each other in offering a comprehensive understanding of the board’s significance in corporate governance and strategic management. In line with the agency and resource dependency theories assumptions, earlier studies found that boardroom can offer a significant positive role in firm performance (Ahmadi et al., 2018; Brahma et al., 2021; Dong et al., 2023; Duppati et al., 2020; Fernández-Temprano & Tejerina-Gaite, 2020; Kelemen et al., 2020; H. Li & Chen, 2018; Y. Liu et al., 2014; Ozdemir, 2020; Song et al., 2020).

BD and firm performance

The extant literature has explored the impact of BD in recent years, making it a prominent subject in academic research. The BD effect is often nuanced, offering both advantages and disadvantages. A diverse board offers several advantages regarding information analysis and processing; it is expected to possess a broader range and depth of knowledge and expertise (F. Ali et al., 2023). Ultimately, this leads to a board that is expected to make sound judgments compared to the one that is less diverse. A diverse board embraces diverse viewpoints within the organization and encourages open debate directly relating to firm performance. Miller and Triana (2009) explore that BD positively relates to performance, indicating that an increase in the social and human capital diversity on the board of directors, as assessed by race and ethnic diversity, enhances the firm’s decision-making mechanism, which boosts the firm’s financial performance. Furthermore, Erhardt et al. (2003) found that the proportion of females on board and minority board members positively relates to firm return on asset (ROA) and return on investment. Y. Liu et al. (2014) found that increasing women directors on corporate boards improves the financial performance (return of assets, return on sales, and Tobin Q) of Chinese non-financial firms (Brahma et al., 2021; Chen et al., 2023). Ozdemir (2020) measured BD by using different characteristics of board members, such as age, gender, and financial expertise, and found that BD positively affects the financial performance of the U.S. tourism sector.

Nevertheless, BD can harm group performance owing to conflicts of interest, differences of opinion, and significant delays in decision-making, ultimately causing a decline in firm performance (Amason, 1996; Kabir et al., 2023; Knight et al., 1999; Salancik & Pfeffer, 1978; Hatane et al., 2023). According to Hambrick et al. (1996), the heterogeneous top management team is less effective than homogeneous top management, and their actions and behaviors are slower than their counterparts. Knight et al. (1999) also claim that ethnic diversity is inversely associated with group consensus, implying that harmonizing various workforce opinions needs extensive coordination. In this regard, BD is negatively related to firm outcomes; this is because board members with diverse backgrounds make it difficult to integrate the firm’s decision-making processes and harmonize the workforce for productive outcomes (Adams & Ferreira, 2009; Shemla et al., 2016; Smith et al., 2006). It means that a board with greater gender diversity can effectively monitor and evaluate managers’ roles; however, this does not always result in improved firm performance (Adams & Ferreira, 2009; Pletzer et al., 2015). Evidence suggests that diverse boards may become inactive as a result of their directors’ divergent perspectives (Hambrick et al., 1996; Jackson et al., 2003).

Moreover, earlier literature related to the manufacturing sector focuses on corporate board structure and firm performance, specifically in terms of board size, independent directors, and ownership concentration (Mukherjee et al., 2019; Panda & Leepsa, 2019; Pucheta-Martínez & Gallego-Álvarez, 2020; Shan, 2019). He et al. (2022) examined the link between organizational management and dynamic efficiency in Chinese manufacturing firms. They find a positive relationship between ownership concentration and firm efficiency; however, the board size is negatively associated with firm efficiency. Ciftci et al. (2019) found that increasing ownership concentration improves firm performance, whereas increasing cross-ownership has the opposite effect. In addition, the findings show that firms perform better under female leadership. Prior management and corporate governance literature postulates the impact of board gender diversity on firm performance. Still, it does not align with the trespassing perceived view of BD on firm performance relationships. Contextually, manufacturing literature draws few inferences on the BD and firm performance link; despite that, a short stream of literature explored this dimension using the impact of board characteristics, including board composition, ownership concentration, board independence, board size, and director expertise performance.

Earlier literature has shown mixed empirical outcomes on the relationship between BD and firm performance. We assume that BD demonstrates several positive effects on firm performance through enhanced decision-making and broader perspectives. A diverse board extends several benefits regarding information analysis and processing; it is expected to possess a broader range and depth of knowledge and expertise. It embraces diverse viewpoints within the organization and promotes open debate, which directly relates to a firm’s performance. Therefore, understanding the nuanced interplay between BD and firm performance remains crucial for crafting effective governance strategies in modern organizations. This study contributes to revealing the uncharted status of BD and the firm performance relationship in the manufacturing sector. Based on the above literature and arguments, this study develops the following hypothesis.

Hypothesis 1 (H1). BD has a significant positive relationship with Chinese manufacturing firms’ performance.

BD, CEO duality, and firm performance

Exploring the influence of BD on firm performance is valuable and thoughtful for practitioners. Yet, the knowledge about when and under what conditions the impact of BD on performance changes is limited. The theoretical ambiguity and inconsistent results reveal that the alleged relationship is confusing and lends itself to deeper examination in which certain possibilities should be discovered to understand better this complex relationship (Miller & Triana, 2009). One possibility is a dual role of the CEO hired by firms in modern economies (Tang, 2017), indicating the combined power of the CEO and the board’s chairman of a firm (Elsayed, 2007). They have considerable influence and power over the board’s decisions, leading the management team and chairing the board meetings (Oussii & Klibi, 2024). This can raise concerns about a lack of checks and balances, potentially leading to conflicts of interest and a lack of independent oversight. It is anticipated as a feature that can influence the relationship between BD and firm performance (Ogoe & Suzuki, 2023). However, the link between BD and CEO duality lies in the potential influence of a diverse board on the decision to separate the roles of CEO and chairman. A diverse board may more likely recognize the importance of separating the roles to ensure effective corporate governance, such as broader perspective, independent oversight, stakeholder representation, and risk management (Arora, 2024; La Rocca et al., 2024).

Earlier studies on CEO duality have been conducted in response to the predominance of CEO duality in corporate governance. Duru et al. (2016) found that CEO duality negatively affects the firm’s operating performance. Furthermore, the findings show that corporate governance enhancement reduces the negative effect of CEO duality, implying that more independent directors decrease the negative impact of CEO duality on firm operational performance. Palaniappan (2017) examines the influence of board characteristics (CEO duality, independence, and board activity) on firm performance for Indian manufacturing firms and finds mixed outcomes. On the other hand, Walls and Berrone (2017) found that CEO duality has no impact on the association between the board of directors and the firm sustainable performance. Moreover, the CEO duality effect on performance is significant in two different views: the agency and stewardship theories explain the positive and negative aspects of CEO duality on firm corporate performance (Boyd, 1995; Kim et al., 2009; M. Yu, 2023). The agency theory suggests that CEO duality has negative consequences because it enables control over management power, which may influence the monitoring and decision-making process on a board (D. Wang et al., 2014). Specifically, the increase in the CEO’s power and reduction of the corporate board role brings more focus on self-interest over shareholders’ interests, incurring significant agency problems. On the other hand, the steward theory emphasizes the positive aspects of CEO duality, suggesting that combining two different top management positions increases corporate leadership performance and thus establishes centralized authority.

Moreover, prior literature shows duality’s influence on firm performance in many different contexts. For example, Velte’s (2020) findings reveal that CEO duality strengthens the association between the board of directors and financial performance. Moscu (2015) shows a positive association between CEO duality and financial performance using the earnings-per-share performance measure. However, Shrivastav and Kalsie (2016) include financial and accounting indicators to examine the association between CEO duality and performance. They find that CEO duality is negatively associated with ROE, while it has no impact on Tobin’s Q. Several studies find that CEOs’ duality limits the firm’s financial performance (Rechner & Dalton, 1991) owing to the concentration power of the CEO’s restricted control of directors and stockholders’ interests following agency theory (Fama & Jensen, 1983). They can effectively manage the inside information flow for their benefit rather than shareholders’ interests, increasing agency costs and negatively impacting firms’ value (Naciti, 2019; Shahbaz et al., 2020; M. Yu, 2023). On contrary, Iyengar and Zampelli (2009) and Linck et al. (2008) found that CEO duality does not impact firm performance.

Therefore, we assume that BD and CEO duality are distinct concepts connected through their impact on corporate governance practices and firm performance. CEO duality is an internal control instrument that complements management’s internal control and acts as a contingency factor in the BD–firm performance relationship. A diverse board is more likely to promote governance structures that increase transparency, accountability, and stakeholder value, potentially leading to a change in the dual role to improve performance. The dominant nature of CEO duality in persuading firm performance is ambiguous. Therefore, this study examines the role of the CEO duality in the relationship between BD and firm performance. Based on the above literature and arguments, this study develops the following hypothesis.

Hypothesis 2 (H2). CEO duality influences the relationship between BD and the Chinese manufacturing firm’s performance.

Methodology

Data sample

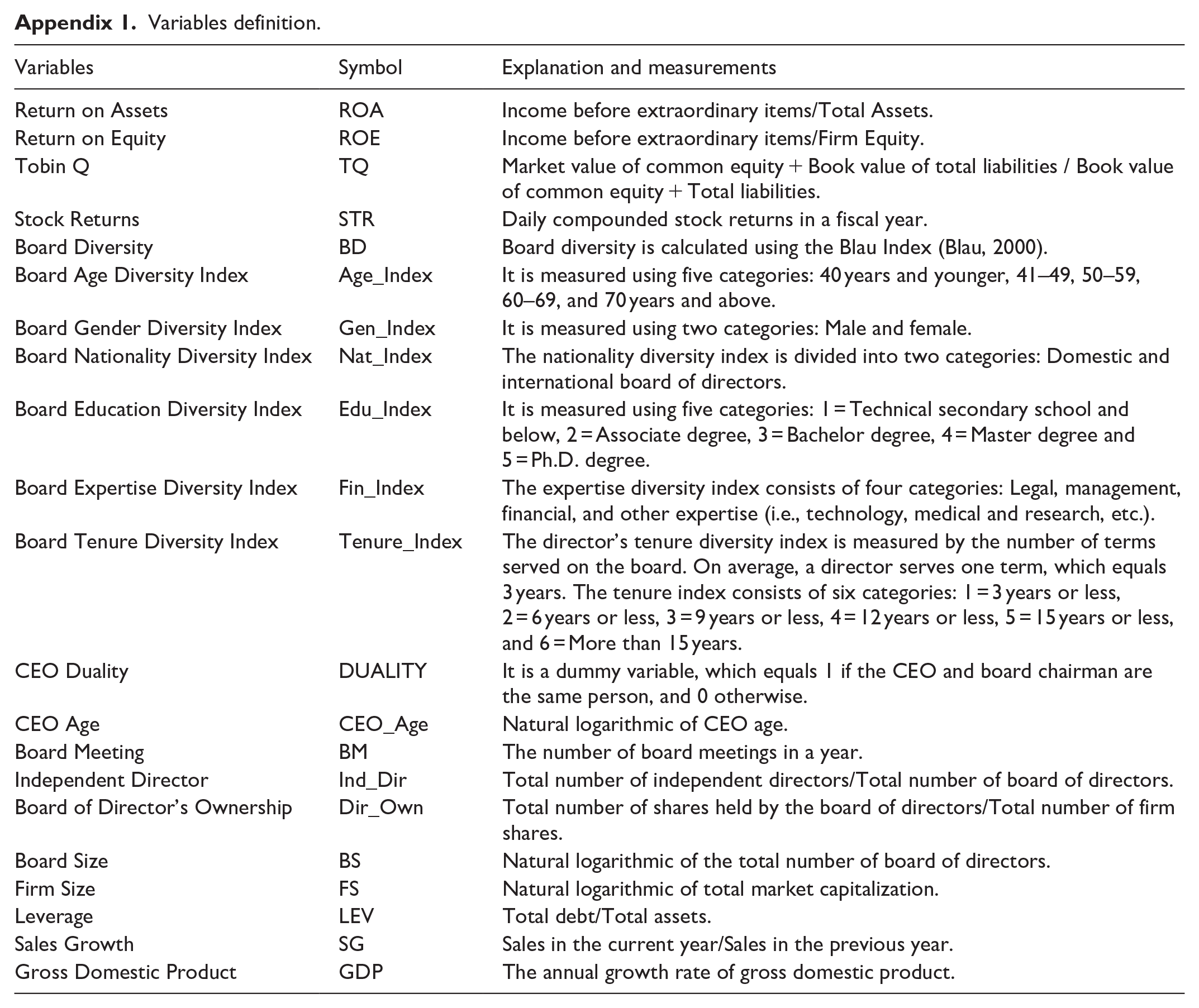

This study includes Chinese manufacturing firms listed on the Shanghai and Shenzhen stock exchanges throughout 2008–2022. We obtained firm data from RESSET and CSRMAR databases. We finalized the incorporated sample using the criteria of H. Li and Chen (2018) and Kim et al. (2009). First, we restrict the sample by dropping those firms that faced losses in the last two consecutive years because it creates financial anomalies. Second, we remove firms whose total assets and liabilities ratios are higher than 100% and are treated as bankrupt. Third, we excluded the firms with missing observations. Our final sample includes 11,117 firms’ observations.

BD formulation

Prior studies have measured BD using one or two demographic indicators of board members, such as age or gender (Song et al., 2020; Ye et al., 2021). However, this study incorporates the Blau (2000) diversity index (1 −

Moderating variable

The earlier literature shows that intervening variables exist in the association between BD and firm performance (Cheng et al., 2008; H. Li & Chen, 2018; Orazalin & Baydauletov, 2020; Tang, 2017). Based on the above literature and arguments in the Theory Building and Hypotheses Development section, we assume that the different levels of BD and firm performance relationships are influenced by CEO duality. Therefore, this study adds the interaction term of BD and CEO duality, which is being investigated in the model as a moderating variable. This study generates a dummy variable, denoted as DUALITY, which equals 1 if the CEO and board chairman are the same person, and 0 otherwise. The definition of the variable is also shown in Appendix 1.

Model

This study incorporates panel year-fixed-effect regression models to examine the effect of BD and CEO duality (moderating variable) on firm performance.

Empirical results

Descriptive statistics

Table 1 summarizes the descriptive statistics for BD, firm performance (accounting-and-market-based performance), and control variables. Panel A reports the mean and standard deviation values of accounting and market-based firm performance, consistent with the reported values of Y. Liu et al. (2014) and Hasan and Taylor (2020). Panel B shows the BD mean of 1.972 with a standard deviation 0.407. Furthermore, the director’s education, with 64.5%, is the most diverse board index, indicating the highest level of possible education in the sample. It shows that education is relatively more diverse among the directors, with a majority having a significant level of education. The least diverse board index is nationality, indicating that 2.9% of directors are from different nationalities in the sample. It shows that nationality diversity is very low relative to the other indices. The age index indicates that, on average, the directors’ ages represent 59.1% of the maximum possible age span observed among all directors in the sample. The tenure index shows that directors, on average, have 36.2% of the maximum possible tenure. The gender index indicates that, on average, gender diversity in the board is at 22.0% in the selected sample. It suggests that gender diversity is relatively moderate compared to other indices. The financial index indicates that, on average, directors with financial backgrounds contribute to 13.1% of the board composition in the sample. Duality has a mean value of 0.202, indicating that 20.2% of board members have dual roles in our selected sample. Panel C shows the mean and standard deviation values of the control variables. The control variables’ statistical values align with the existing literature (Pathan, 2009; J. Sun & Liu, 2014).

Descriptive statistic.

Note: This table presents the summary of descriptive statistics. Panel A represents firm performance variables based on accounting-and-market performance. The accounting-based performance measures are the return on assets (ROA) and returns on equity (ROE), and the market-based performance measures are Tobin Q (TQ) and stock return (STR). Panel B reports the board diversity (BD) and its components. BD is calculated using the Blau Index (Blau, 2000). We construct the BD index by using six different attributes of the board of directors, i.e., board age diversity index (Age_Index), board gender diversity index (Gen_Index), board nationality diversity index (Nat_Index), board education diversity index (Edu_Index), board financial expertise diversity index (Fin_Index), board tenure diversity index (Tenure_Index). The moderator variable is CEO duality (DUALITY). Panel C shows the list of control variables, i.e., CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). All variables’ measures are shown in Appendix 1.

Correlation Analysis

Table 2 indicates the relationship among the variables. This study finds that the highest correlation exists between FS and CEO_Age with a coefficient value of 0.184. Y. Liu et al. (2014) and J. Sun and Liu (2014) argue that multicollinearity issue arises when the correlation coefficient surpasses 0.700 or higher in absolute value. However, the correlation coefficients among the independent variables are less than 0.200 in our sample, showing that all correlation coefficients are within an acceptable range without multicollinearity problems.

Correlation matrix.

Note: This table presents the correlation between dependent and independent variables. The accounting-based performance measures are the return on assets (ROA) and returns on equity (ROE), and the market-based performance measures are Tobin Q (TQ) and stock return (STR). The board diversity (BD) is calculated using the Blau Index (Blau, 2000). The moderator variable is CEO duality (DUALITY). The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP).

Indicates the statistically significant level is at 5%. All variables’ measures are shown in Appendix 1.

Effect of BD on firm performance

This study incorporates a panel year-fixed-effect regression model to determine the association between BD and firm performance. Table 3 shows that BD is positively associated with firm accounting performance, with coefficient values of 0.027 (t-statistic = 2.077) and 0.098 (t-statistic = 2.333) for ROA and ROE, respectively. The findings show that a one-unit 13 increase of BD leads to 0.027 and 0.098 unit increases to average values of ROA and ROE, respectively. In economic terms, one standard deviation 14 increase in BD would result in a 0.380 (0.027/0.071) and 0.037 (0.098/2.668) standard deviation increase in ROA and ROE, respectively. It indicates that BD significantly improves a firm’s efficiency in utilizing its assets and profitability. It also suggests that diverse perspectives and experiences from a diverse board can lead to better decision-making processes within the firm. Furthermore, boardroom diversity can lead to more thorough discussions, a broader range of viewpoints, and ultimately, more effective strategies for maximizing firm performance.

Effect of board diversity on firm performance.

Note: This table presents year-fixed-effect panel regression results on the effect of board diversity (BD) on firm performance. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. The independent variable is BD, which is calculated using the Blau Index (Blau, 2000). DUALITY indicates the CEO duality. The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). The parentheses reported the variables’ standard errors.

** and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Moreover, BD significantly positively impacts firm market performance, with coefficient values of 0.019 (t-statistic = 2.111) and 0.020 (t-statistic = 1.818) for TQ and STR, respectively. The results show that a one-unit increase of BD leads to a 0.019- and 0.020-unit increase to average values of TQ and STR, respectively. In terms of economic impact, a one standard deviation increase in BD would lead to a 0.109 (0.019/0.174) and 0.033 (0.020/0.607) standard deviation increase in TQ and STR, respectively. It highlights that BD positively influences the firm’s market value and enhanced stock market performance, as a diverse board may be perceived as more adept at navigating market changes, fostering innovation, and seizing opportunities. Economically, the results indicate that market participants, such as investors, analysts, and so on, recognize the value of diversity within the boardroom and reward diverse board firms, with higher stock prices and better market performance. This is because a diverse board may signal to investors that the firm is well-equipped to adapt to changing market dynamics, innovate, and capture new opportunities. Our results are consistent with H1. Furthermore, our findings are consistent with earlier literature (Aggarwal et al., 2019; Carter et al., 2003; Song et al., 2020), which supports that the board of directors’ diverse characteristics positively impact the firm performance. Our findings are consistent with the agency and resource-dependency theories, indicating that BD brings several benefits, such as skills, education, knowledge, and perspective, which improve the board decision-making process and control managerial behavior to boost firm performance.

High- and low-diverse board difference

In the Effect of Board Diversity on Firm Performance section, this study finds that an overall diverse board increases the firm performance. However, it is interesting to examine further how different levels of a diverse board influence firm performance because this allows a clearer understanding of whether and how varying degrees of diversity impact firm outcomes differently. Therefore, we divide the whole sample into two groups, which are the higher board diversity (HBD) group and the lower board diversity (LBD) group, following the work of H. Li and Chen (2018). Dividing the sample into HBD and LBD groups allows for a more nuanced analysis of both individual groups’ influence on firm performance. This stratification can reveal whether the degree of diversity intensifies the observed positive effects, providing deeper insights into how varying levels of diversity contribute to firm performance and potentially uncovering thresholds that might be obscured in an aggregated analysis. This study develops the HBD and LBD groups by splitting the whole sample into two sub-groups. We measure the median value of firms’ BD; if the BD value is higher than the median value of BD, then it denotes the HBD group, and if the BD value is lower than the median value of BD, then it denotes the LBD group. To examine the impact of HBD and LBD groups on firm performance, we first run the mean difference test between HBD and LBD. Table 4 findings show that the HBD group performs significantly differently from the LBD group. HBD firms indicate significantly better performance than the LBD ones. In addition, HBD is associated with specific firm characteristics such as a higher proportion of independent directors, larger board size, older CEOs, and higher sales growth. Furthermore, it may be possible for a more diverse board to have frequent board meetings to make new strategies and evaluate performance. It means that greater BD has diverse resources and superior monitoring functions to improve firm performance.

Higher and lower diverse board difference.

Note: This table presents the results of the mean difference test for higher board diversity (HBD) and lower board diversity (LBD). This study develops the HBD and LBD groups by splitting the whole sample into two sub-groups. We measure the median value of firms’ BD; if the BD value is higher than the median value of BD, then it denotes the HBD group, and if the BD value is lower than the median value of BD, then it denotes the LBD group. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. The moderator variable is CEO duality (DUALITY). The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), Board of Director’s Ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP).

**, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Furthermore, we examine how different levels of a diverse board influence the firm performance using panel year-fixed-effect regression models. In Table 5, columns 1–2 and 5–6 and columns 3–4 and 7–8 indicate the HBD and LBD sample groups, respectively. This table shows that both high- and low-diverse board groups are significantly positively associated with accounting- and market-based firm performance; however, their relationship strength differs. HBD is positively related to firm accounting performance, with coefficient values of 0.060 (t-statistic = 20.000) and 0.029 (t-statistic = 14.500) for ROA and ROE, respectively. The findings show that a one-unit increase of HBD leads to a 0.060- and 0.029-unit increase to average values of ROA and ROE, respectively. In economic terms, one standard deviation increase in HBD results in approximately a 0.845 (0.060/0.071) and 0.011 (0.029/2.668) standard deviation increase in ROA and ROE, respectively. Similarly, HBD significantly positively impacts firm market performance, with coefficient values of 0.037 (t-statistic = 9.250) and 0.046 (t-statistic = 4.181) for TQ and STR, respectively. The findings show that a one-unit increase of HBD leads to a 0.037- and 0.046-unit increase to average values of TQ and STR, respectively. In economic terms, one standard deviation increase in HBD leads to a 0.212 (0.037/0.174) and 0.076 (0.046/0.607) standard deviation increase in TQ and STR, respectively. In addition, LBD also positively correlated with firm accounting performance, with coefficient values of 0.011 (t-statistic = 1.833) and 0.013 (t-statistic = 1.857) for ROA and ROE, respectively. The findings show that a one-unit increase of LBD leads to a 0.011- and 0.013-unit increase to average values of ROA and ROE, respectively. In economic terms, one standard deviation increase in LBD results in a 0.155 (0.011/0.071) and 0.005 (0.013/2.668) standard deviation increase in ROA and ROE, respectively. Similarly, LBD significantly positively influences firm market performance, with coefficient values of 0.017 (t-statistic = 2.125) and 0.018 (t-statistic = 1.800) for TQ and STR, respectively. The findings show that a one-unit increase of LBD leads to a 0.017- and 0.018-unit increase to average values of TQ and STR, respectively. In economic terms, one standard deviation increase in LBD leads to a 0.097 (0.017/0.174) and 0.030 (0.018/0.607) standard deviation increase in TQ and STR, respectively.

Effect of higher and lower board diversity on firm performance.

Note: This table presents the year-fixed-effect panel regression results on the effect of the higher board diversity (HBD) and lower board diversity (LBD) groups on firm performance. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. This study develops the HBD and LBD groups by splitting the whole sample into two sub-groups. We measure the median value of firms’ BD; if the BD value is higher than the median value of BD, then it denotes the HBD group, and if the BD value is lower than the median value of BD, then it denotes the LBD group. DUALITY indicates the CEO duality. The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). The parentheses reported the variables’ standard errors.

**, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Furthermore, the outcomes indicate that both groups increase firm performance; however, the magnitude of their effects varies. HBD is more considerable in improving firm performance than LBD, suggesting that firms with higher diversity experience greater benefits with notable profitability and market valuation improvements. This is because a highly diverse board may be better equipped to understand and cater to a broader range of customer needs and preferences, leading to improved firm performance. Furthermore, firms with more diverse boards may be perceived as more socially responsible and better positioned to navigate potential risks related to diversity and inclusion issues to improve firm performance. This study’s results are also consistent with those of Bernile et al. (2018) and Erhardt et al. (2003), indicating that a firm with a highly diverse board is more likely to focus on group discussion and better management, which improves board decision-making and leads to an increase in firm performance. Our control variables’ results are also aligned with the existing literature.

CEO duality as a moderator

In the Board Diversity, CEO Duality and Firm Performance section, the literature indicates that CEO duality influences the relationship between BD and firm performance. This section examines the moderating role of CEO duality; therefore, we use the interaction variable of BD and DUALITY on firm performance using a panel year-fixed-effect regression. In Table 6, Columns (1), (4), (7), and (10) indicate that BD is positively associated with firm performance; however, the interaction between BD and CEO duality (BD*DUALITY) negatively moderates the relationship, with coefficient values of −0.026 (t-statistic = −1.857) for ROA, −0.015 (t-statistic = −1.875) for ROE, −0.006 (t-statistic = −2.000) for TQ, and −0.024 (t-statistic = −1.846) for STR. The findings show that a one-unit increase in the BD*DUALITY interaction term would result in a 0.366 (−0.026/0.071) standard deviation decrease in ROA, a 0.006 (−0.015/2.668) standard deviation decrease in ROE, a 0.034 (−0.006/0.174) standard deviation decrease in TQ, and a 0.039 (−0.024/0.607) standard deviation decrease in STR. In economic terms, the negative impact of the BD*DUALITY interaction suggests that when a CEO holds the position of board chair, the benefits of BD on firm performance may diminish. The decrease in performance, as measured by standard deviations, highlights the significance of governance structures in moderating the positive effects of BD. For instance, the 0.366 standard deviation reduction in ROA suggests that duality might significantly impair the firm’s ability to effectively utilize its assets, even in the presence of a diverse board. Furthermore, BD*DUALITY may limit independent oversight, stifle diverse perspectives in decision-making, and impede open communication within the boardroom. It could be possible because their attention may be diverted from leveraging the benefits of diverse viewpoints. This dynamic may lead to risk-averse decision-making and reduced accountability, ultimately dampening the performance-enhancing effects typically attributed to BD. The dual role may divide their attention between executive reasonability and board oversight, resulting in less focus on leveraging the benefit for BD for firm performance. Our findings are consistent with H2, indicating that DUALITY impacts the relationship between BD and firm performance.

Effect of board diversity and CEO duality on firm performance.

Note: This table presents the year-fixed-effect panel regression results on the effect of board diversity (BD) groups (BD, HBD, and LBD) and CEO duality on firm performance. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. The BD is calculated using the Blau Index (Blau, 2000). This study develops the HBD and LBD groups by splitting the whole sample into two sub-groups. We measure the median value of firms’ BD; if the BD value is higher than the median value of BD, then it denotes the HBD group, and if the BD value is lower than the median value of BD, then it denotes the LBD group. The moderator variable is CEO duality (DUALITY). BD*DUALITY, HBD*DUALITY, and LBD*DUALITY are interaction terms. The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). The parentheses reported the variables’ standard errors.

**, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Moreover, the moderating role of CEO duality is significantly different for HBD and LBD groups. In Table 6, Columns (2), (5), (8), and (11) findings indicate that the effect of HBD is significantly positive on firm performance and CEO duality positively moderates the relationship, with coefficient values of 0.078 (t-statistic = 3.714) for ROA, 0.033 (t-statistic = 6.600) for ROE, 0.020 (t-statistic = 5.000) for TQ, and 0.022 (t-statistic = 2.200) for STR. The findings show that a one-unit increase in the HBD*DUALITY interaction term would lead to a 1.099 (0.078/0.071) standard deviation increase in ROA, a 0.012 (0.033/2.668) standard deviation increase in ROE, a 0.115 (0.020/0.174) standard deviation increase in TQ, and a 0.036 (0.022/0.607) standard deviation increase in STR. In economic terms, the findings reveal that CEO duality improves the positive effects of HBD on firm performance, as seen through significant upsurges in standard deviations across performance metrics. For instance, a one-unit increase in the HBD*DUALITY interaction results in a notable 1.099 standard deviation increase in ROA, indicating a strong positive effect on the firm’s ability to utilize its assets effectively. Furthermore, the results suggest that HBD*DUALITY can improve the monitoring and decision-making process by utilizing diverse talents and experience within the boardroom, which can enhance firm performance. Combining the two positions, HBD and CEO duality, can provide consistent leadership in a business, allowing for better alignment of corporate strategy proposition and execution and more efficient decision-making, which enhances firm efficiency (Donaldson & Davis, 1991).

Alternatively, in Table 6, findings in Columns (3), (6), (9), and (12) show that the LBD has a significant positive effect on firm performance; however, LBD*DUALITY negatively moderates the relationship, with coefficient values of −0.011 (t-statistic = −3.667) for ROA, −0.017 (t-statistic = −1.889) for ROE, −0.012 (t-statistic = −2.400) for TQ, and −0.064 (t-statistic = −1.939) for STR. The findings show that a one-unit increase in the LBD*DUALITY interaction term would result in a 0.155 (−0.011/0.071) standard deviation decrease in ROA, a 0.006 (−0.017/2.668) standard deviation decrease in ROE, a 0.069 (−0.012/0.174) standard deviation decrease in TQ, and a 0.105 (−0.064/0.607) standard deviation decrease in STR. In economic terms, LBD interaction with CEO duality negatively moderates firm performance, leading to decreases in standard deviations. For example, a one-unit increase in the LBD*DUALITY interaction results in a 0.155 standard deviation decrease in ROA, suggesting that CEO duality can undermine the positive effects of LBD on firm efficiency and profitability. Furthermore, the findings suggest that LBD*DUALITY may impact the board perspectives necessary for effective decision-making and strategic planning. LBD*DUALITY exacerbates this by consolidating power and limiting independent oversight, reducing the likelihood of considering diverse viewpoints and impacting firm performance (Fama & Jensen, 1983). In addition, with low-diverse representation, the board may struggle to adapt to changing market dynamics and innovate effectively, leading to lower firm performance. The CEO duality’s negative moderation could thus indicate a failure to leverage the potential benefits of diversity in driving organizational success. These outcomes are consistent with Haynes and Hillman (2010), suggesting that dual roles influence the board members, resulting in the CEO’s interests dominating executives, which may negatively impact the firms’ value.

Overall, these results highlight the importance of BD and its interaction with leadership structures in shaping firm performance. While higher diversity combined with CEO duality can amplify positive outcomes, the same combination with lower diversity can detract from performance, emphasizing the nuanced role of governance in organizational success. Furthermore, this study’s findings suggest that greater BD may enhance management oversight and encourage executives, which can enhance firm performance. In addition, diverse boards may expect to question management and voice their concerns about controversial management decisions, which may reduce idiosyncratic decision-making. This is because directors of highly diverse boards may bring a broader range of perspectives to a corporate board, which may positively impact firm value.

Robustness tests

Effect of BD and duality on firm performance using a two-step system generalized method of moments model

Earlier studies indicate that endogeneity concerns might exist between board structure, CEO duality, and firm value (Brahma et al., 2021; Chang et al., 2019; Dong et al., 2023; Duru et al., 2016; Elsayed, 2007; Ozdemir, 2020; Song et al., 2020). It can arise from omitted proxies bias, measurement errors, or reverse causality, where firm performance might impact BD and CEO duality. Therefore, to control the endogeneity issue, we incorporate the two-step system generalized method of moments (GMM), one of the most effective and versatile approaches to resolve the possibility of endogeneity in our estimations (Baum et al., 2003). It assists in solving these issues by including lagged values of the endogenous variables, allowing control for dynamic panel bias (Elmagrhi et al., 2019; Wintoki et al., 2012). The relationship between BD, CEO duality, and firm performance is inherently dynamic, meaning past performance can impact current BD decisions and CEO duality and vice versa. Therefore, two-step system GMM is suitable for dynamic panel data models because it can account for the persistence and evolution of firm performance over time, providing more accurate and reliable estimates. Furthermore, it helps to control unobserved heterogeneity, which refers to firm-specific characteristics that are not directly measured but could affect BD, CEO duality, and firm performance. Following the studies by Wintoki et al. (2012), Nadeem et al. (2017), and Dong et al. (2023), this study includes 1-year-lagged value of dependent variables, BD and DUALITY as endogenous variables, and the rest of the proxies treated as instrument control variables. Table 7 shows the two-step system GMM firm-year effect results on the effect of BD and DUALITY on firm performance. The findings are consistent with our primary outcomes, suggesting that empirical results are free from potential endogeneity problems.

Robustness test: Two-step system GMM model.

Note: This table presents the results of the two-step-system GMM model. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. L.ROA, L.ROE, L.TQ, and L.STR are 1-year-lagged values of dependent variables. The BD and DUALITY are endogenous variables. The instrumental control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG) and gross domestic product (GDP). The parentheses reported the variables’ standard errors.

**, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Effect of board attributes and duality on firm performance

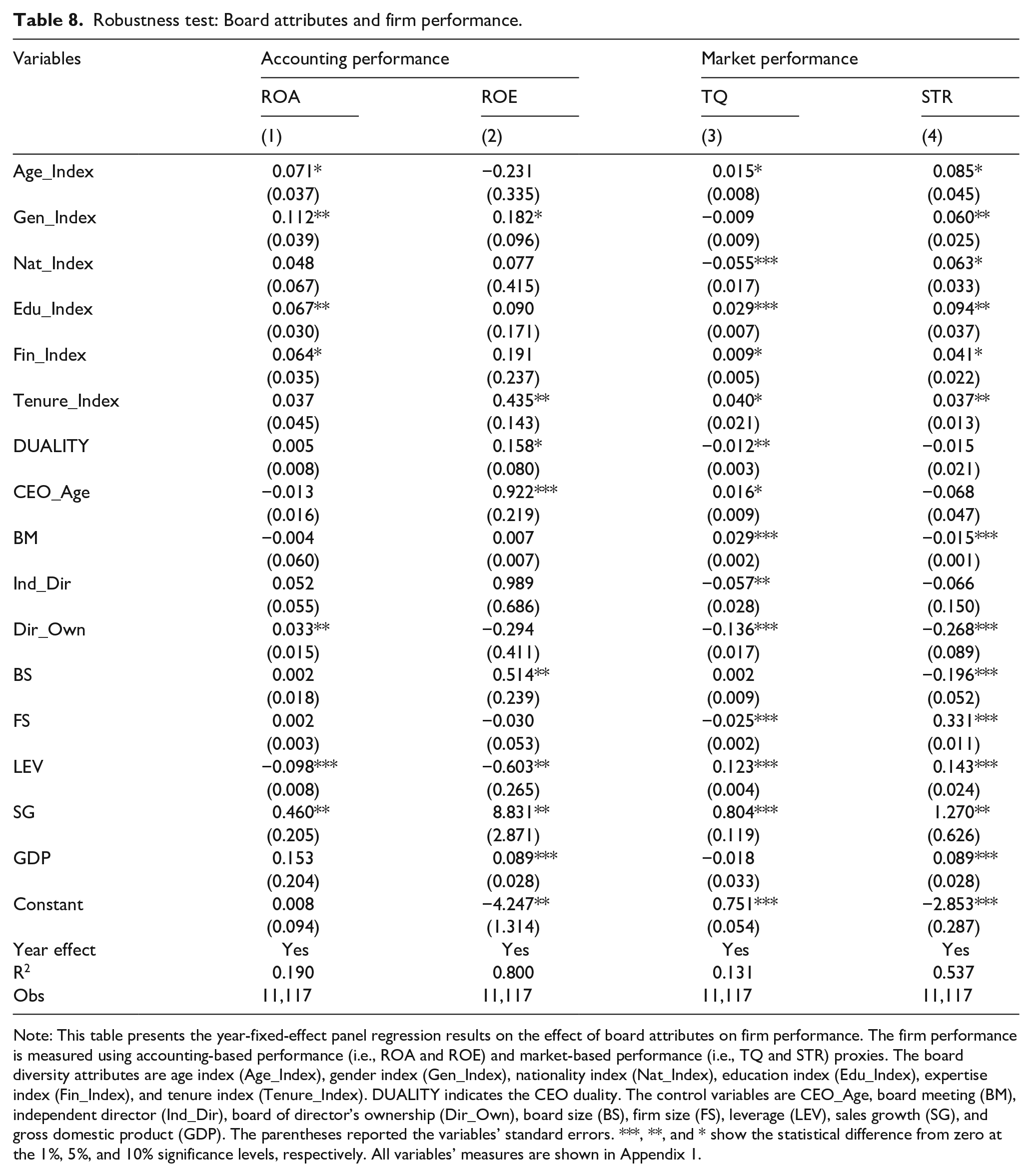

To further support our primary outcomes, this study incorporates six BD attributes (individual BD indexes) to examine their effect on firm performance using panel year-fixed-effect regression. Table 8 reports the results of each BD index with firm performance. The findings indicate that each BD index significantly positively impacts firm performance. It shows that all BD indexes equally contribute to improve the firm performance.

Robustness test: Board attributes and firm performance.

Note: This table presents the year-fixed-effect panel regression results on the effect of board attributes on firm performance. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. The board diversity attributes are age index (Age_Index), gender index (Gen_Index), nationality index (Nat_Index), education index (Edu_Index), expertise index (Fin_Index), and tenure index (Tenure_Index). DUALITY indicates the CEO duality. The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). The parentheses reported the variables’ standard errors. ***, **, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Moreover, this study also incorporates the interaction terms of six BD attributes and CEO duality to examine the influence of these interaction variables on firm performance using panel year-fixed-effect regression models. Table 9 reports the findings of each BD index with firm performance by including the moderating role of CEO duality. The results are consistent with primary outcomes. Furthermore, the findings indicate that the interaction term of education index and CEO duality, Edu_Index*DUALITY, plays a significant role in improving the firm performance.

Robustness test: Board attributes and CEO duality influence on firm performance.

Note: This table presents the year-fixed-effect panel regression results on the effect of board attributes and DUALITY on firm performance. The firm performance is measured using accounting-based performance (i.e., ROA and ROE) and market-based performance (i.e., TQ and STR) proxies. The board diversity attributes are age index (Age_Index), gender index (Gen_Index), nationality index (Nat_Index), education index (Edu_Index), expertise index (Fin_Index), and tenure index (Tenure_Index), and their interaction terms with DUALITY. The control variables are CEO_Age, board meeting (BM), independent director (Ind_Dir), board of director’s ownership (Dir_Own), board size (BS), firm size (FS), leverage (LEV), sales growth (SG), and gross domestic product (GDP). The parentheses reported the variables’ standard errors.

**, and * show the statistical difference from zero at the 1%, 5%, and 10% significance levels, respectively. All variables’ measures are shown in Appendix 1.

Conclusion

This study provides new insight into the impact of BD on firm performance by incorporating the moderating role of CEO duality. We incorporate Chinese manufacturing firms throughout 2008–2022 to achieve our objective. This study includes firm performance measures based on accounting-and-market proxies and a comprehensive measure of BD and its attributes. The findings show that BD is significantly positively associated with firm performance, and CEO duality negatively moderates the relationship. Furthermore, the findings show that both high- and low-diverse board groups positively relate to firm performance; however, their relationship strength differs. A highly diversified board is more effective in enhancing the firm performance than a less-diversified board. Moreover, the results show that the CEO duality moderating role differs for high- and low-diverse board groups. The findings show that a highly diverse board is significantly positively associated with firm performance, and CEO duality positively moderates the relationship. It indicates that a highly diverse board can mitigate the negative behavior of CEO duality, which ultimately enhances the firm performance. In other words, the results suggest that combining the two positions, HBD and CEO duality, can provide consistent leadership in a business, allowing for better alignment of corporate strategy proposition and execution and more efficient decision-making, which enhances firm efficiency (Donaldson & Davis, 1991). However, in the case of a lower diversified board, the moderation results of CEO duality are the opposite, reducing the likelihood of considering diverse viewpoints and controlling functions, which may impact firm performance (Fama & Jensen, 1983). Furthermore, the findings indicate that the interaction term of the education index and CEO duality can significantly improve the firm performance. This study’s results are robust as we employ the two-step system generalized method of moments approach and different attributes of BD. Our results are consistent with the agency and resource dependency theories.

Moreover, this study’s findings suggest that diversified boards can improve monitoring functions and encourage management to pursue value performance-enhancing strategies. This is because diverse boards are more likely to question management and voice their interests in controversial management decisions, decreasing idiosyncratic decision-making. Similarly, a highly diverse board can bring diverse knowledge, education, skills, and perspectives to a boardroom to improve monitoring. As a result, managers undergo such opponents from the diversified board, bringing a diverse perspective that can make more effective corporate board decisions to enhance firm performance. This study also shows the importance of highly diverse board and CEO duality, which is crucial in corporate board monitoring and decision-making. The findings suggest that combining the two positions, highly diverse board and CEO duality, can provide consistent leadership in a business, allowing for better alignment of corporate strategy proposition and execution and more efficient decision-making, which enhances firm efficiency. Given the study’s findings, one of the main recommendations is that manufacturing firms should consider BD’s importance in improving their internal and external monitoring functions.

This study enriches the understanding of how BD and CEO duality are associated with firms’ performance from the perspective of a contingency approach. However, CEO duality is just one potential moderating factor. There could be other variables, such as the firm’s corporate culture, leadership style, or industry-specific factors, that may play an important role in moderating the relationship between BD and firm performance. Future studies can build upon these findings and address these limitations to provide a more comprehensive understanding.

Footnotes

Appendix

Variables definition.

| Variables | Symbol | Explanation and measurements |

|---|---|---|

| Return on Assets | ROA | Income before extraordinary items/Total Assets. |

| Return on Equity | ROE | Income before extraordinary items/Firm Equity. |

| Tobin Q | TQ | Market value of common equity + Book value of total liabilities / Book value of common equity + Total liabilities. |

| Stock Returns | STR | Daily compounded stock returns in a fiscal year. |

| Board Diversity | BD | Board diversity is calculated using the Blau Index (Blau, 2000). |

| Board Age Diversity Index | Age_Index | It is measured using five categories: 40 years and younger, 41–49, 50–59, 60–69, and 70 years and above. |

| Board Gender Diversity Index | Gen_Index | It is measured using two categories: Male and female. |

| Board Nationality Diversity Index | Nat_Index | The nationality diversity index is divided into two categories: Domestic and international board of directors. |

| Board Education Diversity Index | Edu_Index | It is measured using five categories: 1 = Technical secondary school and below, 2 = Associate degree, 3 = Bachelor degree, 4 = Master degree and 5 = Ph.D. degree. |

| Board Expertise Diversity Index | Fin_Index | The expertise diversity index consists of four categories: Legal, management, financial, and other expertise (i.e., technology, medical and research, etc.). |

| Board Tenure Diversity Index | Tenure_Index | The director’s tenure diversity index is measured by the number of terms served on the board. On average, a director serves one term, which equals 3 years. The tenure index consists of six categories: 1 = 3 years or less, 2 = 6 years or less, 3 = 9 years or less, 4 = 12 years or less, 5 = 15 years or less, and 6 = More than 15 years. |

| CEO Duality | DUALITY | It is a dummy variable, which equals 1 if the CEO and board chairman are the same person, and 0 otherwise. |

| CEO Age | CEO_Age | Natural logarithmic of CEO age. |

| Board Meeting | BM | The number of board meetings in a year. |

| Independent Director | Ind_Dir | Total number of independent directors/Total number of board of directors. |

| Board of Director’s Ownership | Dir_Own | Total number of shares held by the board of directors/Total number of firm shares. |

| Board Size | BS | Natural logarithmic of the total number of board of directors. |

| Firm Size | FS | Natural logarithmic of total market capitalization. |

| Leverage | LEV | Total debt/Total assets. |

| Sales Growth | SG | Sales in the current year/Sales in the previous year. |

| Gross Domestic Product | GDP | The annual growth rate of gross domestic product. |

Data Availability

The data supporting this study’s findings are available from the corresponding author upon reasonable request.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

The researcher ensured complete compliance with ethical considerations in accordance with recommendations of the ethical principles of the psychologists and the code of conduct of the American Psychological Association.

Consent to Publish

All the authors agree to publish this manuscript.