Abstract

The goal of this study is to analyze the incidence of dominant owners in the probability of the presence of political directors and the effect of said presence on firm value. The study uses a sample of non-financial Spanish companies listed on the Spanish Stock Exchange over the period 2003–2012. The results show that around half of the firms have at least one ex-politician on their board of directors. Furthermore, the results indicate that dominant shareholders’ voting rights and family nature have a negative effect on the likelihood of having ex-politicians on the board of directors. Moreover, the results show that the presence of political connections positively affects firm value. Further analyses show that this relationship is dependent upon the nature of the dominant owner, the use of pyramidal structures, the tenure of board members and the political directors’ ownership stake.

Introduction

Spain, like most countries in Continental Europe, is in the process of changing its corporate governance system. In this context, institutions, academics, politicians and firms highlight the need to improve corporate governance in order to limit potential conflicts between internal agents as dominant owners and managers and minority shareholders. At the same time, the economic, financial and institutional crises affecting Europe since mid-2007, particularly in countries such as Greece, Italy, Ireland, Portugal and Spain, has led to an increased interest in the study of political and business ties and their effect on firm behaviour. The Spanish business environment is characterized by a high level of corruption. According to the

The low transparency associated with the links between corporate and political elites, as well as the absence of previous empirical evidence on the presence of political connections in the Spanish context, shows that the level of knowledge about this phenomenon does not exceed the level of anecdotal evidence and the number of cases with significant media coverage, such as the appointment of ex-Spanish president Don Felipe González Márquez as director of Gas natural, S.A. in 2010 or the hiring of the ex-Spanish president Don José María Aznar López as an external consultant for Endesa in 2011.

The studies focusing on political connections face two important challenges. First, the links between corporate and political elites are often characterized by their opacity to facilitate political rent-seeking, especially those rents of dubious legality (Leuz and Oberholzer-Gee, 2006). Thus, the connections between politicians and entrepreneurs can be made using private channels that remove the company from the scrutiny faced by politically connected firms (

Previous studies have found several motivations for the existence of politically connected firms. Thus, Khwaja and Mian (2005) argue that politically connected firms enjoy increased access to capital from financial institutions, and Boubakri et al. (2012) show that these firms have less budget constraints and are less sensitive to competitor pressure than firms without political connections. Moreover, Qian et al. (2011) find that dominant shareholders’ tunnelling and self-dealing activities are more pronounced in politically connected firms when the goal of the connection is to ensure access to bank financing. Chen et al. (2011) find that politically connected firms increase information asymmetries, and Chaney et al. (2011) and Bona et al. (2014) show a lower quality of accounting information in politically connected firms. Additionally, political directors could be an important source of benefits for the company because they provide knowledge on bureaucratic and regulatory procedures (

In Continental Europe, the presence of dominant shareholders in large public companies is extensive (

As such, the aim of this paper is to analyze the relationship between the presence of political directors on the board and dominant owners’ effective control, as well as to study the effect of political connections on firm value. For this purpose, we used a sample of non-financial Spanish firms listed on the Spanish Stock Exchange over the period 2003–2012. Moreover, we used the control chain methodology to identify the dominant owner for each firm and determine if said owner exercises effective control through a pyramidal structure (

The results of this study reveal that around half of listed Spanish companies have at least one ex-politician on its board of directors. Furthermore, the results indicate that both the dominant owner's voting rights and his/her family nature affect the likelihood that an ex-politician might be appointed as director. Moreover, the results show that the presence of a politically connected board positively affects firm value. Further analysis shows that this incidence is dependent upon the nature of the dominant owner, the use of pyramidal structures, the political director's tenure and his/her ownership stake.

Our study contributes to the literature on the effect of political ties and board composition in three ways. First, to the best of our knowledge, this is the first study that focuses on the presence of political directors over a large time period (ten years) in a country in Continental Europe. Second, it is the first work that analyses the relationship between the power of dominant owners and the presence of politicians on the board of directors in a country without a planned economy. In this sense, the study shows the power of the dominant owners in determining the composition of the board of directors and defining the different roles played by the appointed directors. The results are particularly relevant for increasing the knowledge of factors that determine the composition of the board in environments with concentrated ownership. In this line, Hermalin and Weisbach (1988) argue that to understand how board members are elected it is crucial to understand the role that the board plays in the whole system of corporate governance. Third, most studies on the impact of political connections on firm value have focused on the Anglo-Saxon countries or on the Asian environment using an event methodology and small samples; therefore, their results are hardly generalizable (Cooper et al., 2010).

The remainder of this paper is structured as follows. In section “Theoretical arguments”, we develop our hypotheses on the relationship between firms’ political connections and dominant owners. In section “Research design”, we describe our research design, and in section “Results” we present our empirical results. Finally, in the last section, we provide a summary and conclusion.

Theoretical arguments

Political connections and dominant owners

The previous literature does not provide conclusive results regarding the characteristics of a country that favours links between politicians and businesses. Thus, authors such as Faccio (2006) and Chen et al. (2011) argue that political connections are stronger and more common in countries with weak legal systems and high levels of corruption. However, political connectivity is also relevant in democratic governments because the greater transparency of political connections facilitates the detection of undesirable acts and the implementation of sanctions. Morck et al. (2000) show a large number of political connections in Canadian companies, and Goldman et al. (2009) and Cooper et al. (2010) demonstrate the high political connectivity of U.S. companies. Thereby, business elites have incentives to interact with the political arena in order to affect the development of the legal framework and economic development conditioning the distribution of capital and investment in an economy (La Porta et al., 1998).

The presence of dominant owners facilitates the exchange of favours with political elites, as the concentration of ownership offers the necessary stability to negotiate favours with politicians. On the contrary, this continuity is not guaranteed if control is held by managers or shareholders with a low ownership stake. Thus, Morck et al. (2004) argue that the stability provided by ownership concentration facilitates the collusion between business and political elites. For these authors, the existence of dominant owners allows the presence of an oligarchic capitalism that encourages the development of political lobbying to preserve their

Additionally, previous literature indicates that, outside the Anglo-Saxon environment, dominant owners use pyramid structures to acquire power (

However, the stability in a company's power is not solely determined by the ownership stake or control through a pyramidal group. In this sense, the nature of the dominant owner may influence the relevance attached to stability in control. Anderson and Reeb (2003) argue that family owners tend to maintain long-term control of a company as a large part of their family wealth is linked to company wealth. Consequently, as a result of their position, family elites may obtain non-pecuniary benefits from political ties. In addition to political rents, family elites can also obtain political influence, social

Nevertheless, in Continental Europe and particularly in Spain, family owners are not the only dominant owners that have traditionally been part of the “oligarchy” of controlling shareholders. Families have shared this role with banks, which have participated significantly in the ownership of listed Spanish firms and have played an active role in corporate governance (Ruiz and Santana, 2011). In this environment, banks have had a significant influence on Spanish economic development and the way of doing business (

In this context, the dominant owners have the ability and the incentives to influence the design of the corporate governance system, particularly regarding the composition of the board and the different roles of board members (

Hypothesis 1

Control in the hands of the dominant shareholder has a negative influence on the probability of having a politically connected board.

Political connections and firm value

Previous literature suggests several motivations for the existence of political connections, including access to privileged financing sources, subsidies or the use of contacts and knowledge to obtain favours when developing new regulations or participating in contracts with government authorities (

Therefore, maintaining a relationship with the political elite over time is a strategy that can generate value for a company. Fisman (2001) shows that the market value of Indonesian firms closely related to President Suharto's family experienced a significant decrease upon the release of negative news about the president's health. Similarly, Faccio and Parsley (2009) find a significant decrease in firm value after the death of politicians residing or born in the same geographic area as the head company. In addition, Goldman et al. (2009) show that corporate donations are a less reliable indicator of future performance that the presence of political directors on the board.

Moreover, an environment of ownership concentration and a weak legal system increases the importance of personal networks and reputation as valuable instruments for attenuating expropriation of minority shareholders’ wealth by the dominant shareholders (

However, political connections can be established to achieve goals other than value generation, especially in environments where shareholders are not sufficiently protected by the legal system and dominant owners can benefit from political rent-seeking. Therefore, Morck et al. (2004) consider the presence of an “oligarchic capitalism” in concentrated ownership environments as an incentive for political and business elites to preserve the

Qian et al. (2011) suggest that political connections can shape dominant owners’ incentive to expropriate minority shareholders because these connections limit capital market discipline. Consequently, as these authors indicate, the possibility of obtaining funds outside the financial market can provide greater incentives to carry out expropriation activities. Therefore, Qian et al. (2011) found that dominant owners’ tunnelling and self-dealing activities are more pronounced in firms where political connection aims to secure bank loan access. For these authors, dominant owners’ expropriation activities face a possible trade-off between short-term benefits and long-term costs arising from the loss of corporate reputation. In this context, this cost depends on future investment opportunities and the financial resources available to fund them. Accordingly, when political connections are established to ensure access to financing sources outside of the capital markets, dominant owners are less concerned about the loss of reputation and will have a greater incentive to obtain private benefits.

Therefore, the above arguments highlight the importance of considering the environment in which political connections are established because the environment could affect not only the purpose of such connections but also their costs and benefits. Faccio (2010) shows that the differences between connected and unconnected firms are greater in institutional environments characterized by weak protection of external shareholders and that the costs and benefits of political connections depend on the particular characteristics of the institutional environment. Consequently, the above arguments predict opposite effects regarding the relationship between political connections and firm value. Therefore, our second hypothesis is

Hypothesis 2

Political connections will affect the firm value.

Hypothesis 2a

Political connections have a positive effect on the firm value.

Hypothesis 2b

Political connections have a negative effect on the firm value.

Research design

Sample

The initial sample comprises 115 non-financial firms listed on the Spanish Stock Exchange between 2003 and 2012. In our regression analysis, we apply the method developed by Hadi (1994) to eliminate outliers. As a result, we obtain an unbalanced panel of 999 firm-year observations, with 95% of the firms having six or more observations over the 2003 to 2012 period.

Data

We hand-collect data on board composition and ownership structure, as well as additional information on the economic characteristics of the companies analyzed, for each year of the analyzed period. Thus, we have obtained the financial data from the financial information of listed companies published by the Spanish Securities Exchange Commission (CNMV). We examine the

Finally, consistent with previous research focused on the Spanish business environment (

Variables

To analyze the likelihood that a firm is politically connected, we define

The study of the effect of political connections on firm value has been accomplished by using a measure that reflects investor expectations about the ability of the company to produce future earnings. Thus, we define

Therefore, in relationship to the effect of

Moreover, to further explore this relationship, we define the variables

The remaining corporate governance variables used in the analysis of the likelihood that a company decides to establish political connections are detailed below. The variable

To control for the effect of other variables that could potentially affect the investigated relationship, we include

Results

Descriptive statistics

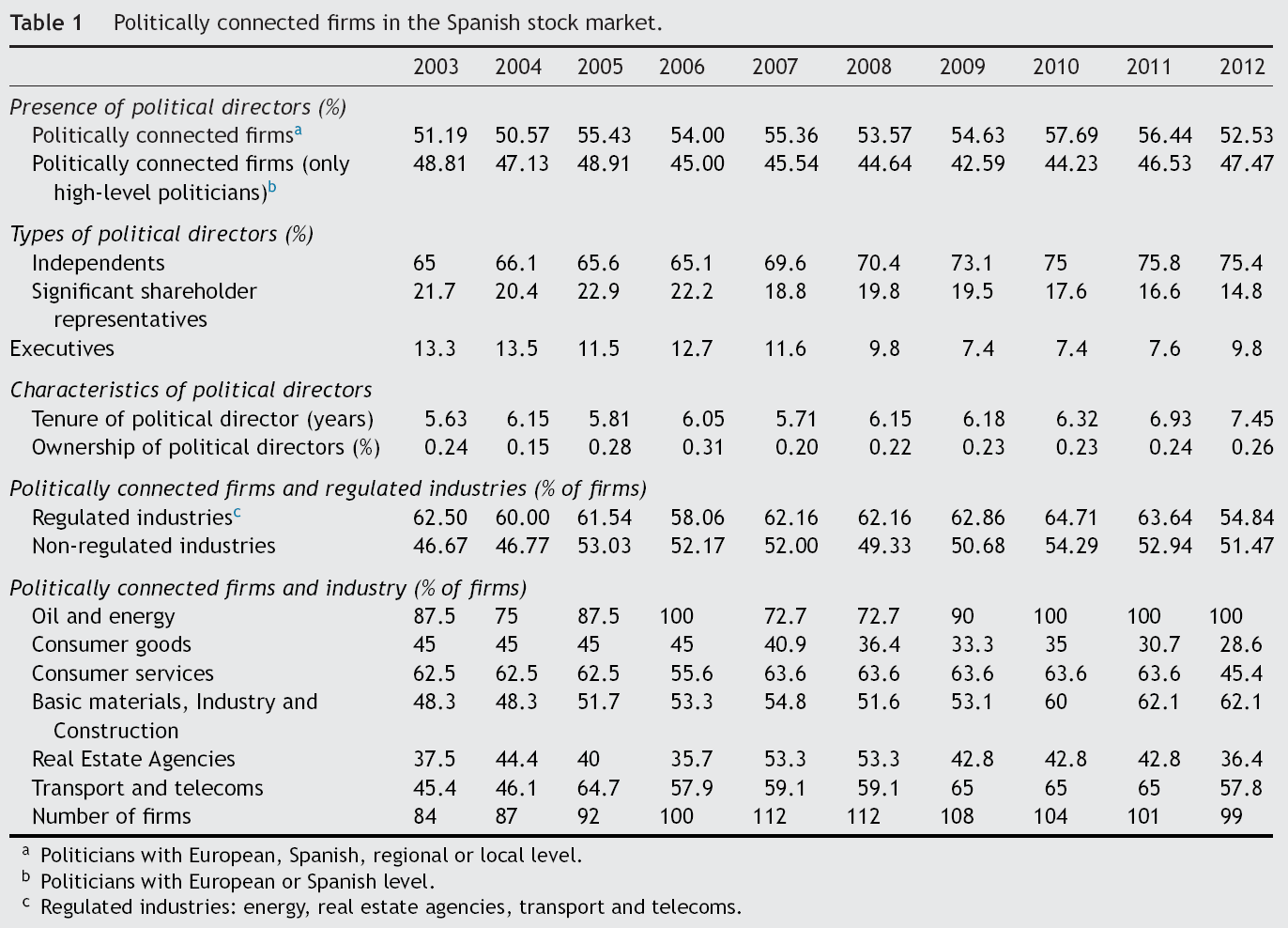

Table 1 shows the evolution of political connections in Spanish listed companies for the period 2003–2012. Thus, the table details the percentage of politically connected firms, both when considering ex-politicians at local, regional, national and European levels and when analysing only high-level politicians,

Politically connected firms in the Spanish stock market.

Politicians with European, Spanish, regional or local level.

Politicians with European or Spanish level.

Regulated industries: energy, real estate agencies, transport and telecoms.

Regarding the typology of political directors, the results show that 70% are independent directors, 20% represent significant shareholders and only 10% have an executive role in the company. Moreover, Table 1 shows that political directors have, on average, six years tenure, showing a growing trend for this variable. Therefore, the average tenure increases from 5.63 years in 2003 to 7.45 years in 2012. These results reflect the stability of political directors in the companies in which they have been appointed. Moreover, these directors hold, on average, 0.2% of the voting rights, keeping this ownership stake stable over the period analyzed.

Concerning the distribution of politically connected firms according to industry, the results show a greater presence of political connections in companies belonging to regulated industries. However, we can observe that the differences between regulated firms and unregulated sectors are decreasing. Thus, if we analyze the sectorial distribution of connected firms according to the classification used by the Madrid Stock Exchange, we note that 100% of boards in the Oil and Energy Industry are politically connected in the last three years analyzed, the increase in politically connected boards in the “Basic Materials, Industry and Construction” industries being relevant. In contrast, Real Estate Agencies and Consumer Goods sectors are less politically connected.

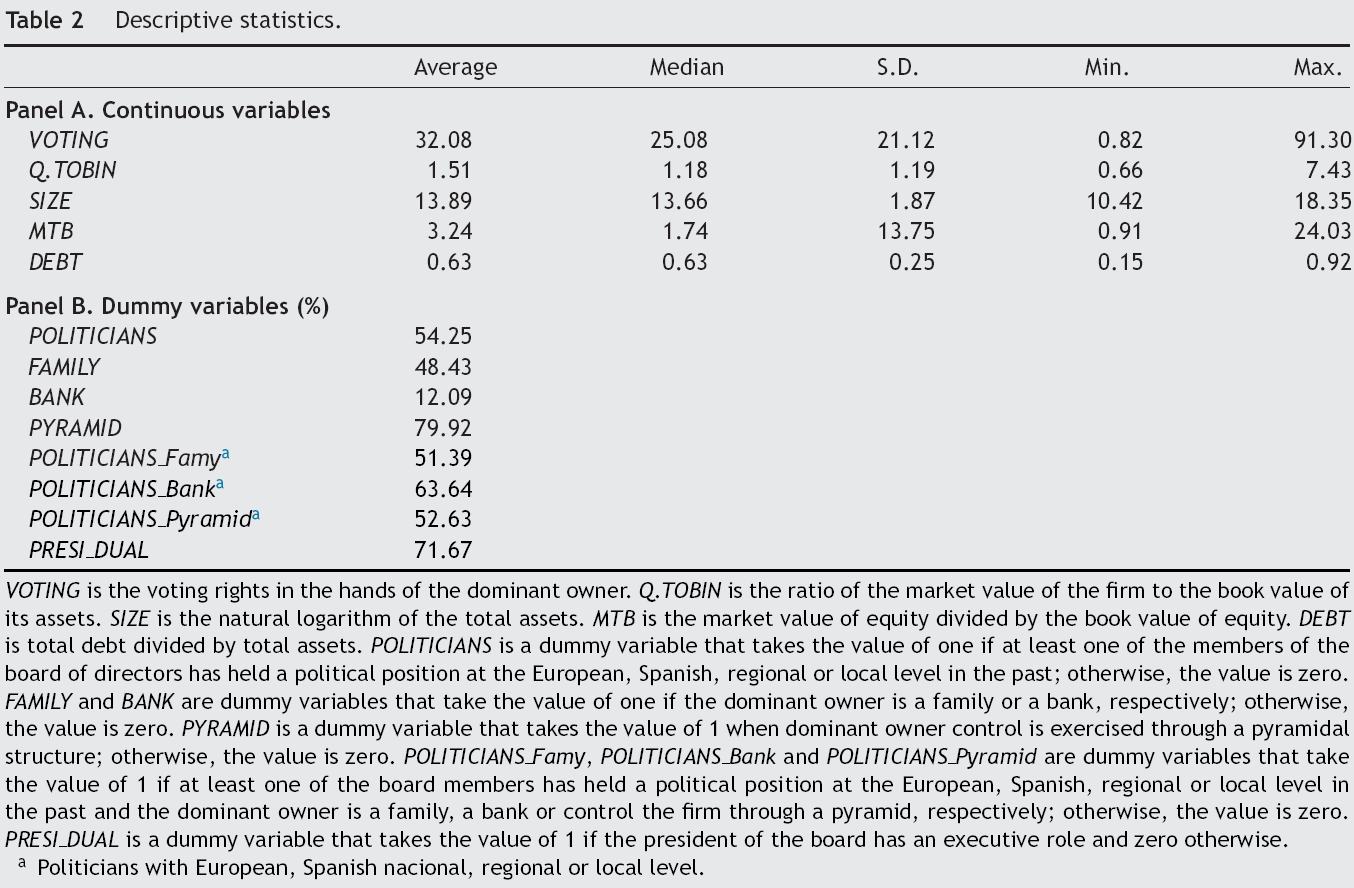

Table 2 shows the descriptive statistics of the variables used in the empirical study. Hence, regarding the ownership variables, the results reflect a 32.08% average ownership stake in the hands of the dominant owner. Moreover, 48.43% of the listed companies are family-controlled, while the domain of a bank is present in around the 12.09%. These percentages are consistent with previous studies focused on the Spanish context (

Descriptive statistics.

Politicians with European, Spanish nacional, regional or local level.

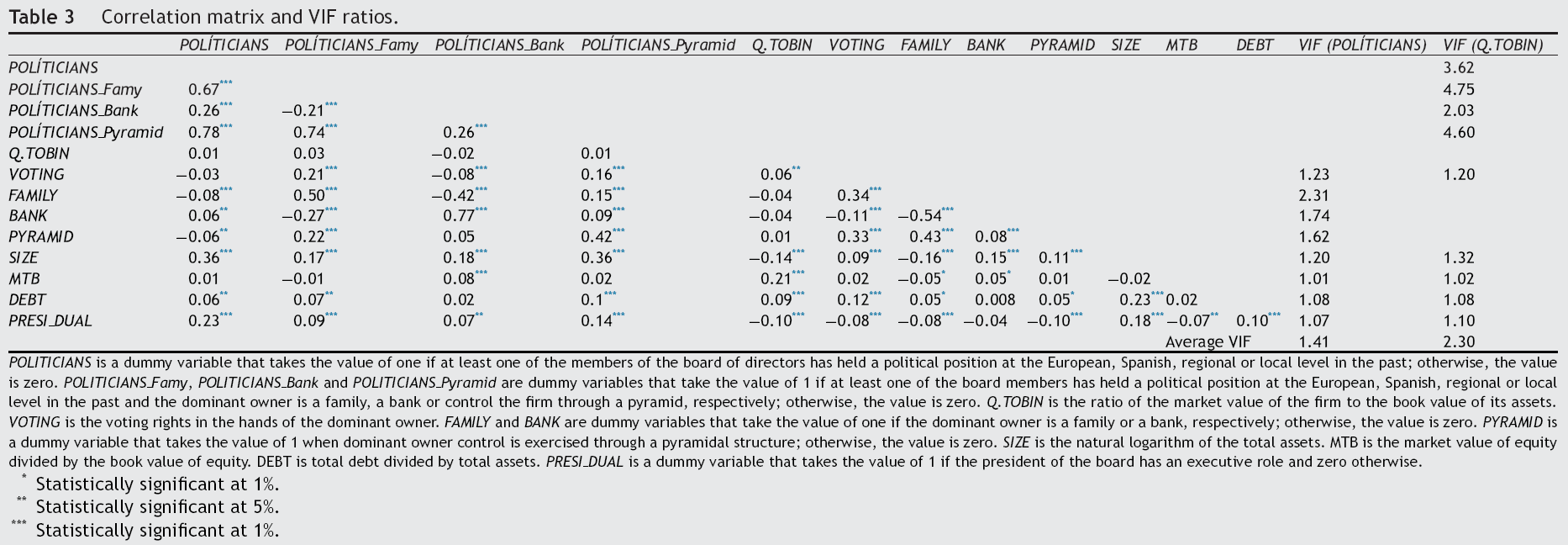

The descriptive analysis completed in Table 3 reports the correlations among the variables and suggests that multicollinearity does not affect subsequent estimations. Nevertheless, we conduct a formal test to ensure that multicollinearity is not a problem. In particular, we calculate the Variance Inflation Factor (VIF) for each independent variable included in the estimated model. The results show that the highest VIF value is 4.75, and the average is 1.41 and 2.30 for the study of the variables

Correlation matrix and VIF ratios.

Statistically significant at 1%.

Statistically significant at 5%.

Statistically significant at 1%.

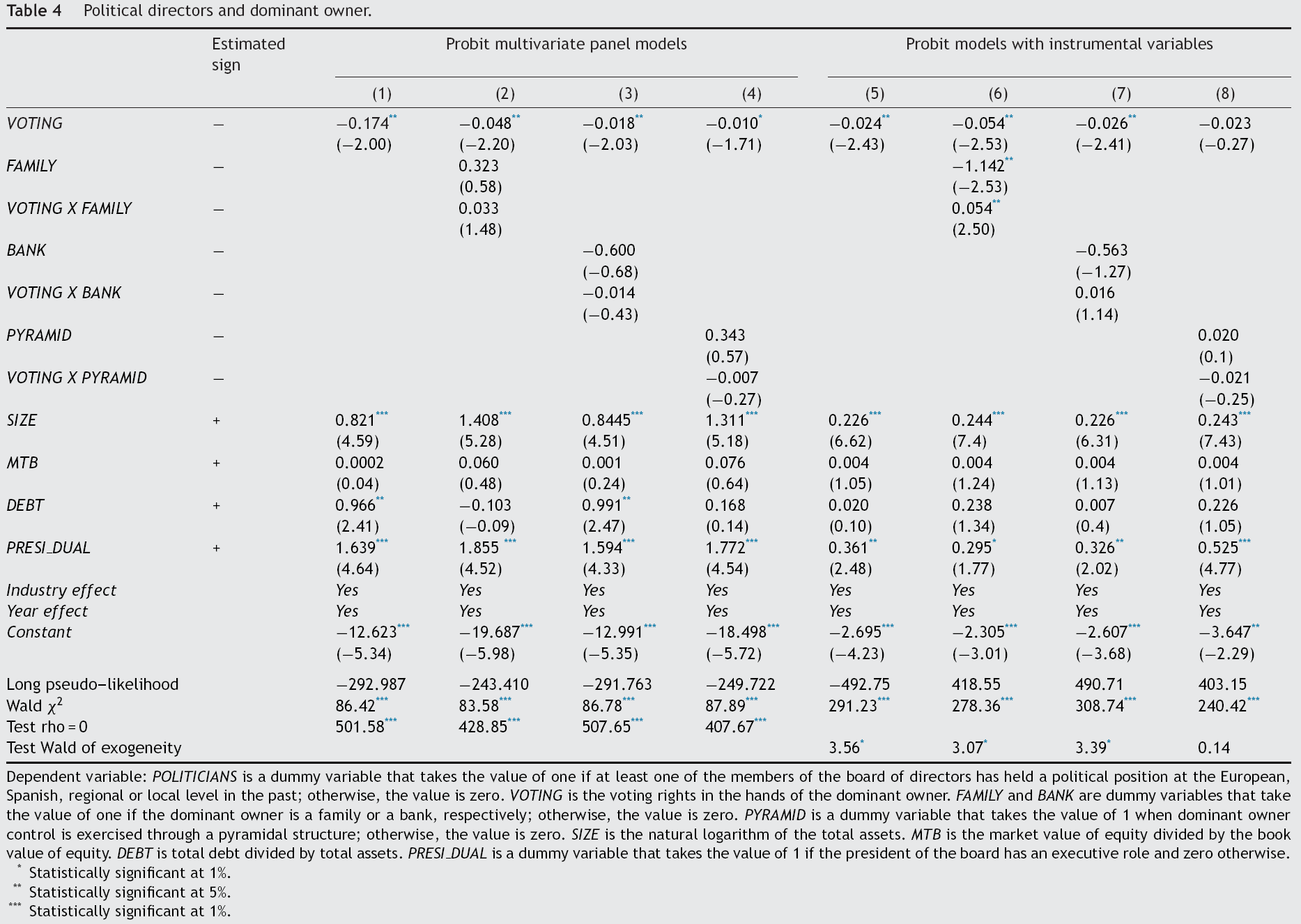

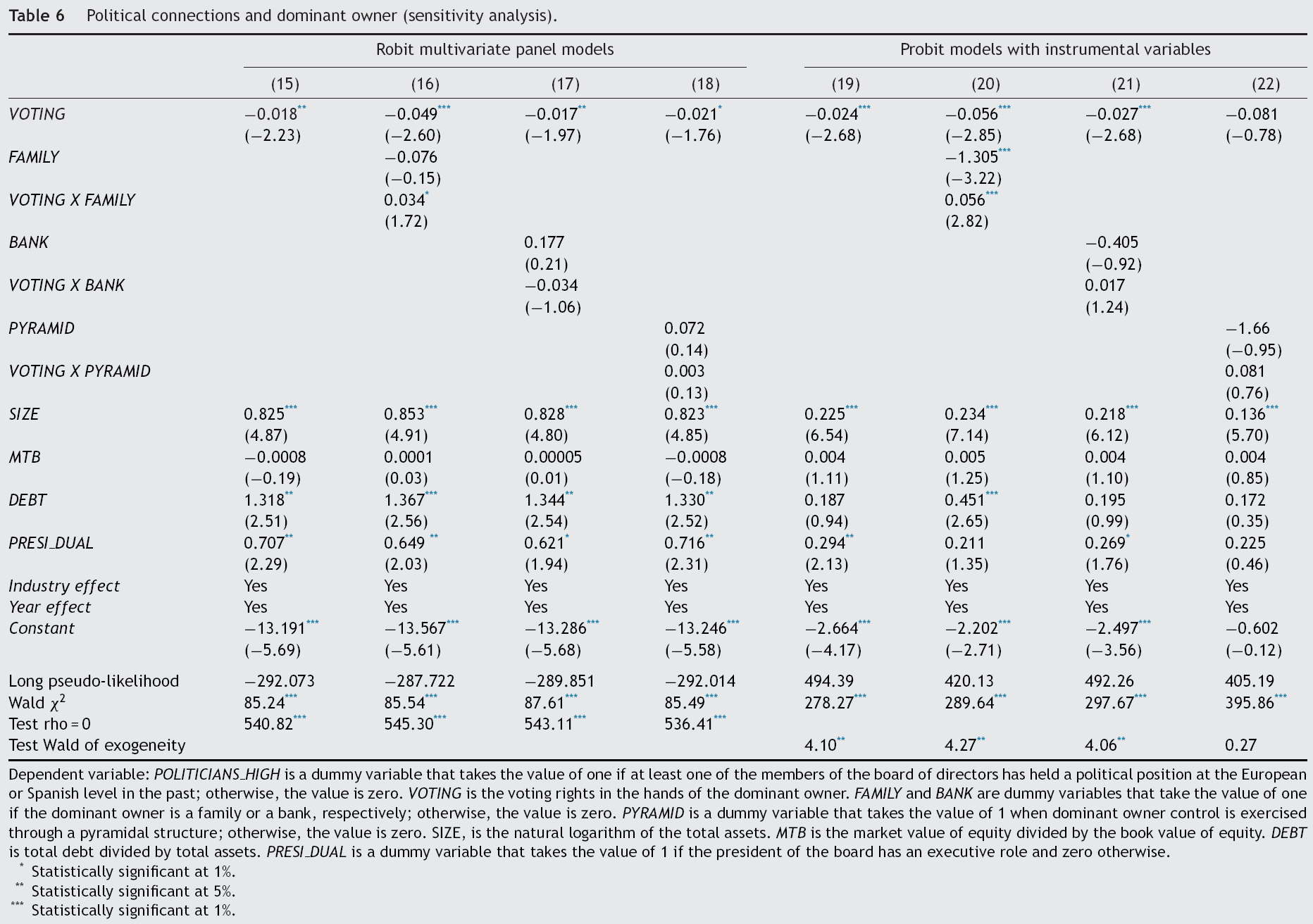

Political directors and the dominant owner

To test Hypothesis 1, we have performed two specifications. First, we have estimated a Probit multivariate panel model whose dependent variable is

In this case we used the inclusion of the company in the Ibex-35 and the 12-month Euribor rate as instrumental variables, with both variables measured at the end of each of the years analyzed.

Table 4 shows the results of estimating the Probit models and the consideration of the endogeneity of the variables by estimating a Probit model with instrumental variables. In this sense, exogeneity tests show a more adequate estimation in Probit models with instrumental variables, with the exception of the analysis of pyramidal structures (models 4 and 8). Accordingly, consistent with Hypothesis 1, the results suggest that voting rights and the family nature of the dominant owner have a significant negative influence on the probability that the board has at least one political director. In addition, the estimated coefficients in Model 6 indicate that participation in the voting rights of the dominant family does not affect the likelihood of establishing political connections on the board of directors;

Political directors and dominant owner.

Dependent variable:

Statistically significant at 1%.

Statistically significant at 5%.

Statistically significant at 1%.

This is because although the coefficients are statistically significant, the value of these coefficients implies that the effect of the voting rights in the hands of the dominant family is zero. Therefore, the influence of family control on the likelihood of the presence of political connection on the board would be (if

Thus, the results indicate that the dominant owner's level of voting rights and some qualitative aspects linked to family control influence board composition and, in particular, the presence of political directors. Thus, our results are consistent with previous studies that show dominant owners having an active role in the design of the governance system and, in particular, board composition (

Regarding the control variables, the results are as expected when we consider the size of the company and the dual role of president of the board and chief executive, in that both variables positively and significantly affect the likelihood of having a politically connected board. However, the results do not show a statistically significant effect of either debt or investment opportunities on propensity to have a politically connected board.

Political directors and firm value

The test of the hypothesis related to the effect of political connections on firm value has been performed by estimating regressions using the Generalized Method of Moments (GMM). The GMM procedure allows us to address potential endogeneity problems by using the right-hand-side variables in the model lagged as instruments; the only exceptions are the year and industry effects variables, which are considered exogenous. The original Arellano and Bond (1991) approach can perform poorly, however, if the autoregressive parameters or the ratio of the variance of the panel-level effect to the variance of the idiosyncratic error are too large. Drawing on Arellano and Bover (1995), Blundell and Bond (1998) develop a system GMM estimator that addresses these problems by expanding the instrument list to include instruments for the level equation. The consistency of GMM estimates depends on both an absence of second-order serial autocorrelation in the residuals and on the validity of the instruments. To check for potential model misspecification, we use the Hansen statistic of over-identifying restrictions. We next examine the

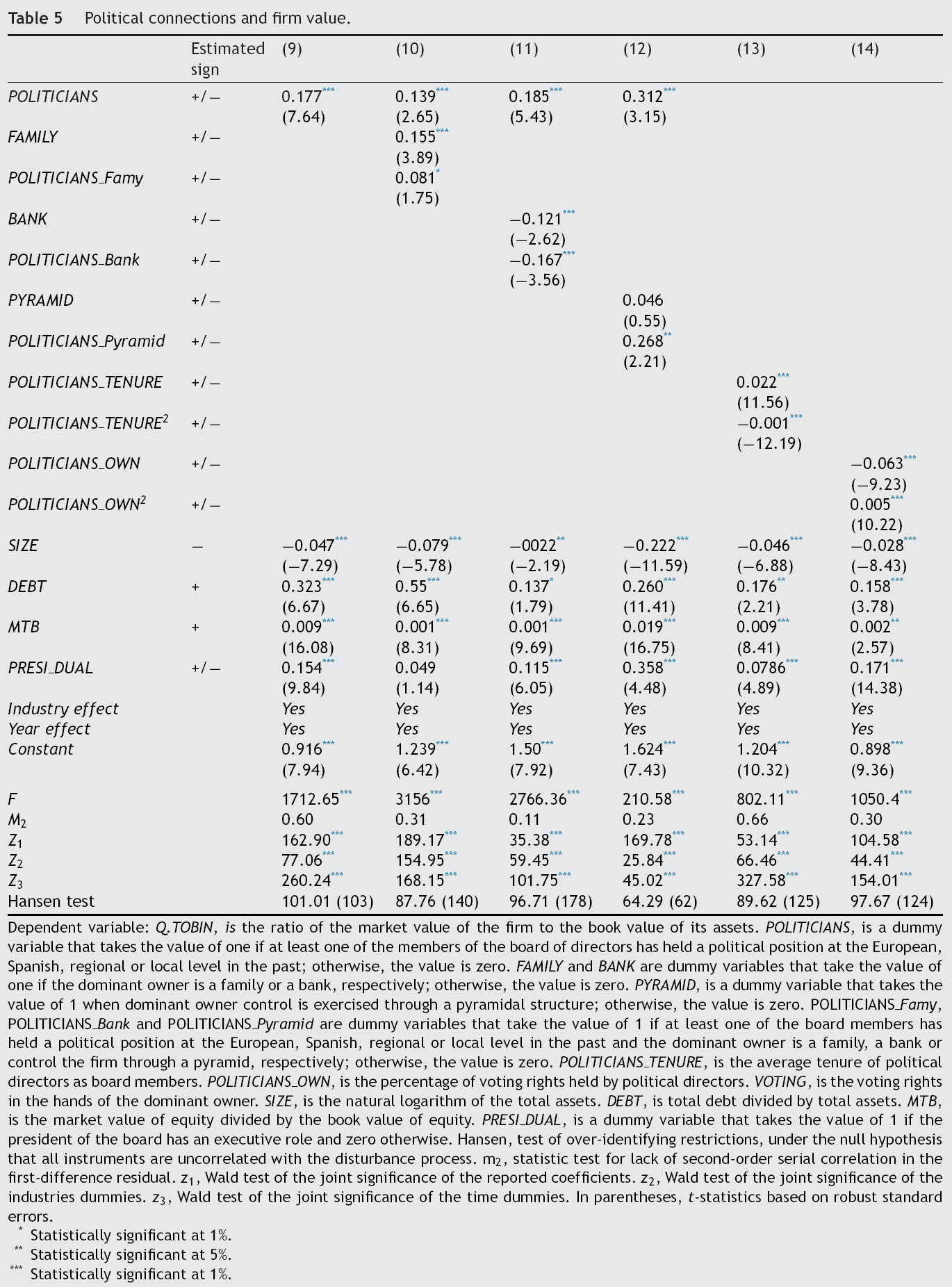

Thus, model 9 (Table 5) shows the presence of political directors to have a positive and significant effect on firm value, which is consistent with Hypothesis 2a. Furthermore, to extend the analysis of the effect of political connections on firm value in Models 10, 11 and 12, we analyze the effect of political connections on firm value when the dominant owner is a family, bank or control is exercised through a pyramid structure, respectively. Thus, the results are consistent with Hypothesis 2a in the case of family firms and when control is exercised through a pyramid, while when a bank is the dominant owner, the political connection negatively affects firm value as Hypothesis 2b predicts. In this line, we estimate the effect of directors’ tenure on firm value. The results show a nonlinear relationship (+/-) between directors’ tenure and firm value (model 13). Finally, we completed the analysis with model 14, which estimates the effect of ownership in the hands of political directors on firm value. The results show a nonlinear relationship (-/+) between both variables.

Political connections and firm value.

Dependent variable:

Statistically significant at 1%.

Statistically significant at 5%.

Statistically significant at 1%.

Regarding the control variables, the results indicate that firm size has a negative impact on value, which is consistent with the higher agency problems associated with larger companies. However, debt level, investment opportunities and the dual role of president of the board positively affect firm value.

Sensitivity analysis

To determine the robustness of our results, we first analyze the likelihood of having a politically connected board through the use of high-level politicians. Therefore, we define the variable

Political connections and dominant owner (sensitivity analysis).

Dependent variable:

Statistically significant at 1%.

Statistically significant at 5%.

Statistically significant at 1%.

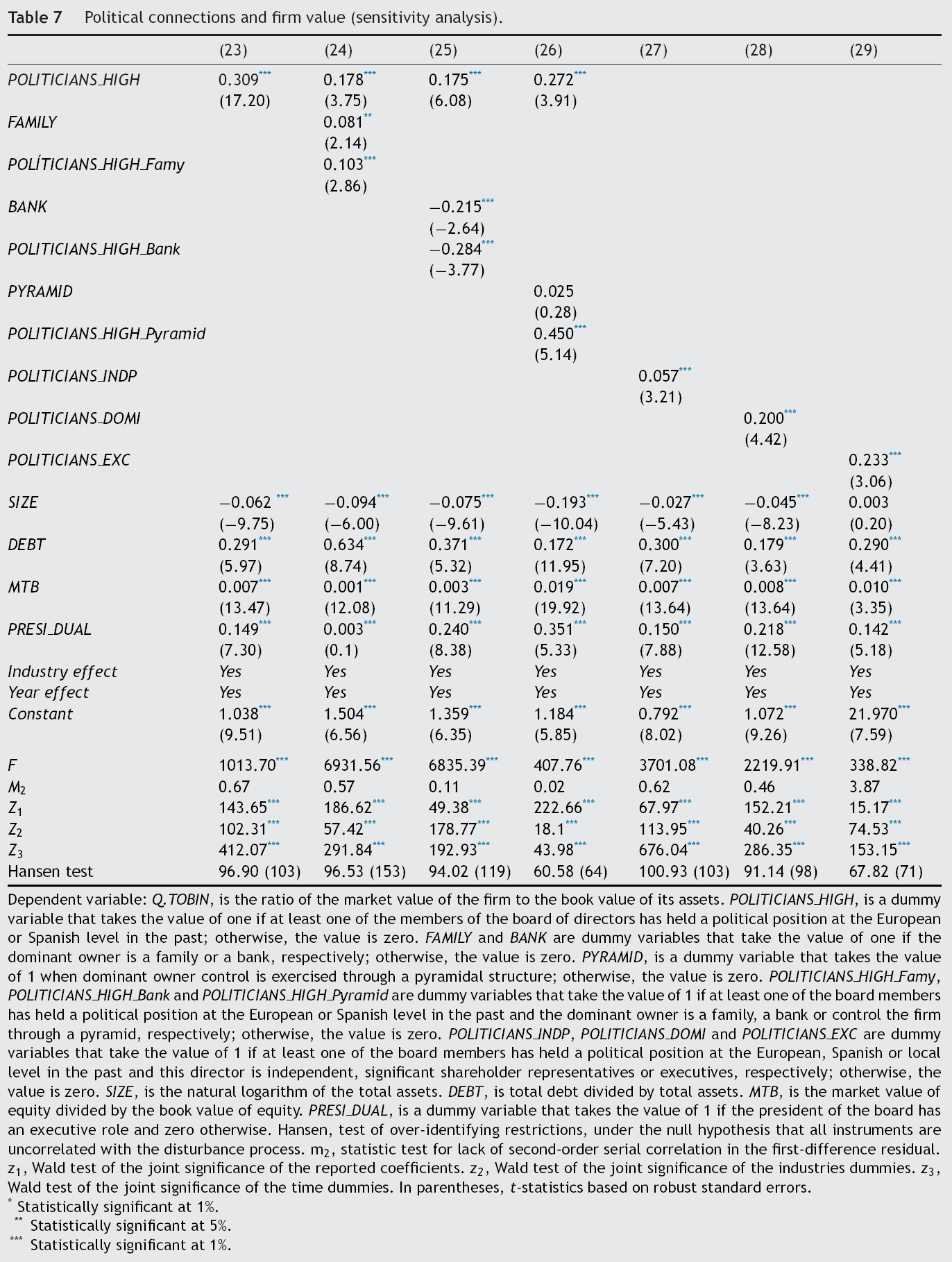

Moreover, regarding the study of the effect of political connections on firm value, Table 7 shows the estimation results when the analysis focuses on high-level politicians (model 23) and the impact of political directors is analyzed in terms of their classification as independent, significant shareholder representatives or executives (models 24, 25 and 26). With the exception of banks as dominant owners, in the remaining situations the results show that political connections have a positive and significant effect on firm value.

Political connections and firm value (sensitivity analysis).

Dependent variable:

Statistically significant at 1%.

Statistically significant at 5%.

Statistically significant at 1%.

Summary and conclusion

In this paper, we have analyzed the relationship between dominant owners’ control and the presence of a politically connected board, as well as the impact of a politically connected board on firm value, in a sample of Spanish listed companies over the period 2003–2012. The results show that about half of the listed companies have a politically connected board. Furthermore, the results show that most of the political directors are independent, have an average tenure of six years and have an approximately 0.2% share in the company's voting rights. These results place Spain in between US and Asian companies. The studies of Agrawal and Knoeber (2001) and Goldman et al. (2009) show that 30% of US firms have politically connected boards, and Qian et al. (2011) and Firth et al. (2012) show that in China and Shangai, respectively, the percentage of politically connected firms is 80%.

Furthermore, the results show that voting rights and the family nature of the dominant owner have a negative impact on the probability of having a politician on the board. Thus, the results obtained reveal that political connections may determine the structure of corporate governance and, in particular, the composition of the board of directors. In this sense, the results are in line with those obtained by Yeh and Woidtke (2005), Durnev and Kim (2005), Kim et al. (2007) and Dahya et al. (2008) and show the importance of the dominant shareholder's ability to influence the composition of the board. Our study suggests that concentration of ownership and control stability facilitate the establishment of relationships and private channels between the dominant owner and political elites (Chen et al., 2011), which may reduce the need for a director with a “political role” because this role can be assumed by the dominant owner.

Additionally, the results show that family control's negative effect on the likelihood of having a politically connected board is independent of the voting rights of the dominant family. This result may reflect the importance of the qualitative aspects related to family control. Therefore, the family long-term commitment, the stability in control or the importance of the family reputation (Anderson and Reeb, 2003) seem to have a greater influence on board composition than the concentration of ownership in the hands of the controlling family. Thus, in line with the arguments of Morck (2009), the results seem to indicate that family control, regardless of ownership stake, has the social status and political influence necessary to obtain political rents without establishing explicit political connections on the board, thereby avoiding greater scrutiny (

Regarding the impact of political connections on firm value, the results obtained show the presence of political directors to have a positive effect on firm value, irrespective of the political level of the director and the type of director (independent, significant shareholder representative or executive). Moreover, this positive effect is shown when we analyze the presence of political connections in family controlled firms and when the control is exercised through a pyramid structure. In this sense, the positive impact of political connections on firm value can reflect that political directors create value through their knowledge and influence on the development of laws that affect company performance or through the achievement of favours that benefit the company, and these advantages are expanded through pyramidal structures (

Our study reveals a U-shaped reverse relationship (+/-) between tenure and firm value. That is, the firm value-tenure relationship has a tendency to grow until a certain point, at which the relationship becomes negative. This result may reflect that the advantages linked to the role of political directors that positively impact firm value will deteriorate over time, possibly resulting in the director losing power or influence in the political arena. In this sense, the estimation obtained indicates that the positive relationship holds during a 11-year tenure. Considering the average political director tenure in our sample (six years), we can conclude that most of the Spanish listed companies are on the positive end of the tenure-firm value relationship. Furthermore, the results indicate a nonlinear U-shaped effect (-/+) of ownership in the hands of political directors on firm value. This result shows that the effect of ownership in the hands of the political directors is negative up to a certain point, from which the relationship is positive. This result may reveal that the market expects that when a politician assumes lower costs of expropriation activities, he/she is more likely to perform these expropriation practices until his/her ownership stake reaches a certain threshold, at which point the market expects political directors to have greater incentives for adopting value-maximizing behaviour. Thus, the results obtained indicate a negative relationship until ownership stake reaches 6.3%, from which point the relationship begins to be positive. The average ownership stake for this type of board member is 0.2%, so we can conclude that the majority of Spanish listed companies are on the decreasing side of the relationship between voting in the hands of the political directors and firm value.

Our research provides evidence for regulators and economic agents of the need for greater transparency in the relationship between business “oligarchs” and political elites. In a context where the main role of the board of directors would be the protection of minority shareholders’ interests, the results obtained in this study point to the need for greater transparency about the role and professional profile of all directors, beyond the role of executives, significant shareholders’ representatives or independent directors.

This study does have some limitations, mainly related to the difficulty of measuring the existence of political connections. We focused on one type of political connection, but there may be other nexuses between political and business elites not captured in the current study; for example, those derived from family or corporate links.

Finally, this work opens up opportunities for future research on the analysis of the relationship between political connections and firm behaviour. Thus, the results indicate the need to further explore the relationship between political connections and family control or the incidence of political ties in corporate decisions.

Footnotes

Acknowledgements

The authors gratefully acknowledge the helpful comments and suggestions received from the referees and from the Associate Editor, Susana Menéndez. We also thank the Research Agency of the Spanish Government for financial support (Project ECO2011-29144-CO3-02).