Abstract

The aim of this article is to look at how two psychological factors affect financial risk tolerance (FRT) and financial risk-taking behaviour (FRB) of individual investors. The study also investigates the role of FRT in mediating the relationship between psychological factors and FRB. A standardized questionnaire was used to collect the information. For the study, a total of 303 completed questionnaires were used. The proposed research model was validated and assessed using partial least squares structural equation modelling. The findings revealed some important experiences. Emotional intelligence and impulsiveness have a significant relationship with both FRT and FRB, according to the results. The findings also support FRT’s position as a mediating factor in the proposed research model. The results emphasize the importance of psychological factors in determining an individual’s FRT and FRB. FRT is a complex mechanism that entails more than just psychological considerations. As a result, further research is needed to decide which additional factors financial advisors can use to increase the explained variance in FRT inequalities.

Introduction

The conceptual link between risk tolerance and investment decisions has been largely upheld by traditional financial models which for the most part expect that investors are rational. Expected Utility Theory

Researchers have been striving hard to identify the reason behind the inconsistency in the behaviour of individual as such, what they do is far different from they are expected to do. For instance, it was observed that individuals, who bought insurance, also gamble. Further, it was noticed that few individuals’ constantly averse risk all through their life thus challenging the assumption of standard utility function (Friedman & Savage, 1948). In consensus, various other researchers (Allais, 1953; Bell, 1982; Ellsberg, 1961; Kahneman & Tversky, 1979; Loomes & Sugden, 1982; Payne et al., 1984; Shefrin & Statman, 1985, 1993; Tversky, 1969; Tversky & Kahneman, 1981) also expressed the contention between normative theory and actual behaviour. This laid the foundation of ‘Prospect Theory’ (Statman, 1995; Tversky & Kahneman, 1981) which states that individuals are sure to take risks when they foresee certain losses while settle for gains when they expect certain rewards. The point-to-be noted is that all the three frameworks were built on assumptions that individual make decisions based on an assessment of the consequences of possible choice alternatives, though subjectively and perhaps with bias or error, and assimilate this information through some sort of desire-based analytics to reach a decision (Loewenstein et al., 2001). However, the assumption was not entirely correct in the field of risk management because emotional reactions (such as worry, fear, dread, and anxiety) towards risks often deviate from rational assessments and directly influence behaviour (Olson, 2006). Changes in risk toler-ance are therefore the result of changes in the psychological influences among investors. It is thus stated, difference in risk tolerance is not only a function of socio-economic and biological differences but also a function of psychological differences.

Thus, the current research seeks to contribute to the literature in a variety of ways. To begin, while most of the previous research has examined risk tolerance among young adults from a developing country perspective, there are relatively few studies from an emerging country perspective. The research fills a void in the literature by including respondents from India. Second, it is noted that previous research has examined financial risk tolerance using demographic, socioeconomic, and attitude variables as independent variables (Grable & Joo, 2000), with conflicting outcomes and it is well-documented in the literature that relying only on these factors fails to achieve the objectives of investment due to its limited efficacy (Grable & Lytton, 1999a, 1999b). Further, Financial Risk Tolerance does not remain static and changes over time. A periodic assessment of Financial Risk Tolerance helps individuals in choosing or changing the investment options according to the prevailing market conditions thus emphasizing the need to continuously assess and accurately measure Financial Risk Tolerance to achieve the desired gains (Yao et al., 2011).

It is thus expected that the study provides valuable insights to investment practitioners in three specific ways: (a) provides an objective assessment to gauge risk tolerance of investor that was largely built upon the mix of art, intuition and experiences; (b) contributes to the knowledge in the field of financial management by providing a multivariate analysis of the risk-tolerance and risk-taking behaviour using a sample which reflects investing public from large population database; and (c) adds to the ongoing discussion in regard to the efficacy of using psychological influences in determining financial risk tolerance and risk-taking behaviour of individual investors.

The study’s objectives are as follows:

To examine the role of psychological factors (namely emotional intelligence and impulsiveness) on individual investors’ financial risk tolerance and financial risk-taking behaviour. To explore the mediating role of financial risk tolerance on the relationship between psychological factors (namely emotional intelligence and impulsiveness) and financial risk-taking behaviour.

The next section covers review of literature followed by conceptual framework and hypotheses development. Afterwards methodology, results, discussion, limitations, conclusions, and implications are discussed.

Literature Review

Comprehensive literature review is very important as it provides research directions in the subject domain (Dhiman, 2018; Dhiman & Sharma, 2020; Paul & Dhiman, 2021; Rana & Sharma, 2015). We have made use of various databases such google scholar and EBSCO to extract quality papers. In the following sub-sections theme wise review has been carried out.

Financial Risk Tolerance

Financial risk tolerance and the various factors influence it have been extensively researched in the past, especially in the financial domain. Overall, a wide range of demographic, socioeconomic, and other factors have been linked to financial risk tolerance, with various levels of support (low, moderate, and high) (Grable, 2008).

Past research has focused on the impact of conventional demographic factors (age and gender) and socioeconomic factors (education, income) on financial risk tolerance of investors (Wang & Hanna, 1997) and the findings lack consensus. Notably, Grable and Lytton (1999a) suggested that relying solely on demographic factors would be ineffective because they only provide a ‘starting point’, and that other factors should be considered to help understand risk tolerance. Later, considering a sample of 220 white-collar university employees in the United States, Grable and Joo (1999) investigated the role of demographic and socioeconomic factors (such as gender, age, marital status, income, education, ethnicity, home ownership, financial knowledge, number of dependants, and financial solvency) in forecasting financial risk tolerance and observed that high financial risk tolerance was related to non-whites, people who did not own a home but had a high income, schooling, financial knowledge, financial solvency, and a smaller number of dependants, according to the findings. Sex, age and marital status had negligible influence. The study explicitly highlighted the importance of financial expertise in forecasting risk tolerance. They agreed with Grable and Lytton (1999a) that conventional demographic and socioeconomic factors explained only 24% of the variance in risk tolerance, and that including factors like financial knowledge, financial solvency, and the number of dependants made some demographic factors less important.

Furthermore, as research advanced, the relationship between socio-demographic factors and risk tolerance were explored in various contexts (Grable & Joo, 2000; Hallahan et al., 2003; Ostrovsky-Berman & Litwin, 2019; Ryack, 2011; Szatko et al., 2018; Yao & Hanna, 2005). The aim was to recognize numerous other possible contributing factors that might help describe risk tolerance better.

Grable and Joo (2004) grouped demographic, socioeconomic, and psychological factors into biopsychosocial and environmental factors in a research study that was influenced by Irwin’s (1993) research work. Unlike their previous study, this one focused on the effect of psychological or attitudinal factors, such as self-esteem, Type A personality, and sensation-seeking, on financial risk tolerance among faculty and staff members (N = 406) at American universities. Self-esteem (a biopsychosocial factor) was found to be a major determining factor of risk tolerance. Education, marital status, annual income, family income, and financial literacy were all major environmental influences. The results had similarity with the study conducted by Rai et al. (2019) amongst 394 working women from various public and private organizations of Delhi, India which concluded that financial attitude and financial behaviour had string association with financial literacy in comparison to the financial knowledge. These external factors played a major role in understanding risk tolerance. Age, gender, racial background, birth order, and home ownership were all found to have negligible influence.

Grable and Roszkowski (2008) continued the current trend of looking at new variables to truly predict the risk tolerance. Using a convenience sample of 460 people from the United States, they studied the impact of moods and emotions on financial risk tolerance while adjusting for environmental and biopsychosocial factors. The findings revealed that people in a good mood had higher risk tolerance. The findings were in consensus with the research study carried by Grable et al. (2020), which declared that mood was positively associated with investors’ willingness to take financial risk.

Also, Gibson et al. (2013) investigated the impact of market risk perception and use of financial advisers on individuals’ financial risk tolerance. The study used a survey of 2,000 people from the United States, and the findings showed that people who were financial advisor clients and considered more stock market risk had a lower risk tolerance and vice-versa. Moreover, according to an experimental study it was determined that gender identity helps clarify gender gaps in risk perceptions and values (D’Acunto, 2015; Lemaster & Strough, 2014; Sultana & Pardhasaradhi, 2015)

Further, the researchers looked at the determinants of financial risk tolerance outside of the financial services domain, namely from psychology, economics, and bio-sociology (self-esteem, personality type, and sensation seeking) in evaluating financial risk tolerance of retail investors and actual financial behaviour (Kannadhasan, 2015; Kannadhasan et al., 2016; Rahman, 2019; Rai et al., 2019; Wahl & Kirchler, 2020). The findings confirmed the utility of these factors in distinguishing between levels of financial risk tolerance and financial risk-taking behaviour, as well as categorising them into various groups.

In the most recent, the role of financial risk tolerance as a mediating factor was also predicted for the relationship between psychological factors and investment performance (Akhtar & Das, 2020; Grable & Lyons, 2018; Heo et al., 2016; Pinjisakikool, 2017).

However, it should be remembered that the conclusions are contradictory. The cause may be various study backgrounds, researchers, and risk tolerance levels. Another possible explanation for such conflicting results: (a) Basic financial services background research used demographic and socioeconomic indicators while clinical studies concentrated on psychological factors; (b) However, it has been suggested that understanding the financial risk tolerance of a person is a complicated mechanism that goes beyond the exclusive use of conventional demographic and socio-economic factors; therefore, further study must be done in various other fields.

Conceptual Framework and Hypotheses Development

The present study has taken a behavioural approach to explore the association between psychological factors and financial risk tolerance. A significant portion of investors would most likely be influenced by such a viewpoint so that they can opt for better financial decisions and can get out of dissatisfaction and build confidence in making decisions related to finance. Individuals interpret risk subjectively, according to the literature, and can be affected by psychological, socioeconomic, structural, and cultural factors (Slovic, 2000). Therefore, it is deemed necessary to understand these factors and assess the degree to which they affect a person’s financial risk tolerance. Emotional Intelligence and Impulsiveness are investigated as potential significant predictors of financial risk tolerance.

Emotional Intelligence

While there are numerous definitions for Emotional Intelligence (Bar-On, 1997; Goleman 1995; Matthews et al., 2004; Zeidner et al., 2004), the most logical meaning of the idea was proposed by Salovey and Mayer (1990) who defined emotional intelligence as, ‘the ability to screen one’s own sentiments and feelings, to segregate among them, and to utilize this data to control one’s reasoning and activity’. An overhauled definition by Mayer & Salovey (1997) outlined that ‘emotional intelligence involves the ability to perceive accurately, appraise, and express emotions; the ability to access and/or generate feelings when they facilitate thought; the ability to understand emotion and emotional knowledge; and the ability to regulate emotions to promote emotional and intellectual growth’.

Emotional abilities were thought to have significance in the context of decision-making related to risk (Hermalin & Isen, 2000; Elster, 1998). The research reported that emotions enhance the ability of an individual to make rational choices and drive behaviour consistent with economic predictions (Frank, 1988; Isen, 1999; LeDoux, 1996; Elster, 1998), that is, emotions allow one to work diligently on the details, prioritize, and focus on the decision to be made.

It is observed that numerous studies in the domain of economics and finance have incorporated this vital variable into their research models (Ameriks et al., 2009; Bell, 2011; Dohmen et al., 2010; Hess & Bacigalupo, 2011; Kidwell et al., 2008; Sjöberg & Engelberg, 2009; Trinidad et al., 2004; Yip & Côté, 2013). For instance, Lerner et al. (2004) revealed that investors who had the capacity to use his emotions insightfully settle on an investment choice when he is in a positive temper. That is, investors who can comprehend and deal with their emotions insightfully should be less influenced by the tone of external sources of information from other investors while picking investment choices. Olson (2006) expressed that emotions principally disregarded by the classical finance paradigm could influence financial behaviour. Furthermore, Demaree et al. (2009) have underlined that emotional reactions have a bearing on financial risk taking. More significantly, Ameriks et al. (2009) have showed that higher financial performance is related to higher emotional intelligence. An individual may undertake risky investments if he possesses the ability to perceive, use and regulate emotions skilfully, thereby fetching more confidence and optimism. As stated by Foo (2011) the individuals who are confident and optimistic tend to invest in risky choices since their emotions influence their perception towards risk about risky investment choices. EI has been massively accentuated in numerous domains (Aren & Aydemir, 2015). On the basis of arguments presented above, it can be proposed be that,

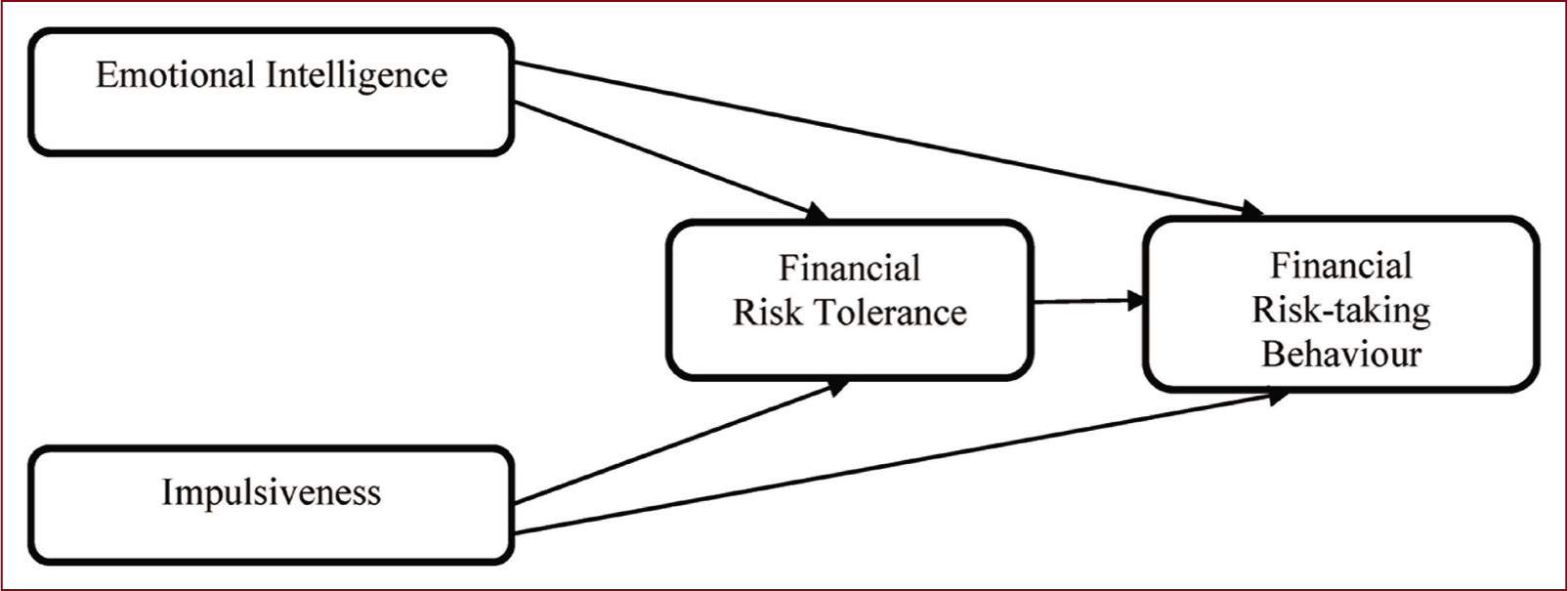

H1: Emotional Intelligence and the financial risk tolerance of an individual investor are significantly related. H2: Emotional Intelligence has a significant relationship with financial risk-taking behaviour of an individual investor.

Impulsiveness

Impulsivity is predisposition to act without thinking, that is, failing to analyse the consequences of a specific conduct before an act is performed. It is defined as an inability to insert between impulse and action, a phase of reflection, a cognitive analysis of a circumstance (Ross & Fabiano, 1985). The past writing has discovered relationship of impulsiveness with more serious dangers of smoking, drinking, drug abuse and hostility, impulsive gambling, extreme identity issue, and attention deficit problems. Impulsive behaviour strongly influences person’s social life; its adverse outcomes are crime, anti-social behaviour, addiction, suicide attempts, aggression, and pathological gambling (Flory et al., 2006; John et al., 1994; Luengo et al., 1994; Tremblay et al., 1994; Wong et al., 2013). Furthermore, various conceptualizations and estimations of impulsivity (Evenden, 1999; Moeller et al., 2001) have brought about the conflicting utilization of the term impulsivity and have reported varying outcomes with respect to the association between impulsivity and risky behaviour (Cyders & Coskunpinar, 2011; Smith et al., 2007; Whiteside & Lynam, 2001). Horvath and Zuckerman (1993) reported that impulsivity scores were positively correlated with other high-risk behaviours in the ―minor violation (e.g., motor vehicle accidents, expulsions from parties, clubs, etc.), financial, sport, and sexual (Human Immunodeficiency Virus risky behaviour) domain. Impulsiveness as a personality trait have been investigated to have strong association with either stimulating risk taking or instrumental Risk taking (Zaleskiewicz, 2001). While the stimulating form of risk taking is associated with pleasure and high excitement. It tends to be quick, easy, and even involuntary. This type of risk-taking is greatly critical in domains such as impulse buying, gambling, and outrageous games and is generally linked to an impulsive trait called sensation seeking. On the other hand, an individual who is engaged in instrumental risk-taking, strives for a long-term future benefit. This type of risk-taking is more towards goal-oriented and less towards the search for excitement. Ameriks et al. (2009) who were interested in examining instrumental risk, investigated the role of impulsiveness in investment decision-making and concluded that higher level of impulsiveness was associated with higher level of investment returns and vice-versa. An impulsive investor tends to engage in more frequent trading and may not likely analyse the situation or event fully, thus make quick decisions. The results were in consensus with Zuckerman and Kuhlman (2000) who reported that impulsiveness causes an individual to make quick decisions and often take more risks. However, it is often presumed that impulsiveness is a double-edged sword since it may have both positive as well as negative effects. If an investor is not impulsive, it can likewise prove to be dangerous for him, in the light of the fact that wavering or not making any move can turn into an obligation over quite a while. Agnew and Harrison (2017) propose that men having higher levels of impulsiveness and extraversion and lower levels of neuroticism exhibit a greater readiness to take risks in general. Hence, it is expected that:

H3: Impulsiveness and financial risk tolerance of an individual investor are significantly related. H4: Impulsiveness and financial risk-taking behaviour of an individual investor are significantly related.

Financial Risk-taking Behaviour

It is often seen that many individuals as well as the financial experts erroneously equate financial risk tolerance of an individual with that of his financial risk-taking behaviour (Kannadhasan, 2015). Any denotable overt action that an individual, a group of individuals, or some living system performs is defined as behaviour. Every action performed in an environmental context, has a denotable beginning and ending. Since, no two individuals are alike, so do their behaviour. It is the diversity in their actions that sometimes leads to positive while at other times to negative outcomes (Jaccard et al., 2005). Later, within the domain of personal finance, Grable (2008) defined behaviour as either, goal-oriented, or volitional. Behaviour can be called ‘goal oriented’ in a situation when an individual handle his finances in such a manner, that it provides a mechanism to achieve the desired goal, that is, goal influences the action. Whereas it is called volitional when the behavioural intention of an individual determines his money management behaviour. Further, it is presumed that an individual’s behaviour is influenced by uncontrollable external factors. Examples include, monetary crises, loss of occupation, and so on. These situations could lead to a behaviour resulting in outcome that is negative. There lie two perspectives from which behaviour could be approached: (a) determinant; or (b) consequence. An individual’s weight loss is not an overt behaviour but result of his previous actions such as diet or exercise (Jaccard et al., 2005). In this manner, it is essential to comprehend the outcomes of money management not its overt behaviour, for an overt behaviour is rational, thoughtful, and conscious or unconscious, inadvertent, and imprudent (Fazio & Towles-Schwen, 1999).

Money (mis)management, an issue to consider, is of utmost concern for individual as well as financial practitioners, because the way in which an individual handle his financial situation influences his social, personal and societal standing (Jaccard et al., 2005). Droms (1987) commented that selecting a portfolio that is found to be not consistent with one’s financial risk may lead to the frustration and anxiety of an investor and thus affect financial risk behaviour. In the similar line, Hatch et al. (2018) discovered that changes in risk tolerance flows through to investor decision making and choice of investment portfolio.

Later, Shim et al. (2010) declared the significance of relationship between attitude towards risk and financial management behaviour. The findings were in concordance with study conducted by Worthy et al. (2010) which confirmed that financial risk tolerance shares a significant relationship with financial management behaviour in credit card matters, where financial debt is a major concern.

Considering the arguments stated above, it is worth proposing:

H5: The financial risk tolerance of an individual investor and financial risk-taking behaviour are significantly related.

Based on the prior studies, FRT is conceptualized as the degree to which it can strength or weaken the relationship between psychological propensities and FRB. For instance, Akhtar and Das (2020) confirmed that FRT and financial overconfidence fully mediated on the relationship between personality traits of individual investors and their investment performance. As a result, the study continued to explore this relationship. Thus, it is hypothesized:

H6: Financial Risk Tolerance mediated the relationship between—(a) Emotional Intelligence and Financial Risk-taking Behaviour; (b) Impulsiveness and Financial Risk-taking Behaviour.

On the basis of this clarification, Figure 1 proposes a conceptual framework that encompasses how psychological factors affect FRT and FRB. The model identifies two factors incorporating Emotional Intelligence and Impulsiveness to determine the individual’s FRT and FRB.

Methodology

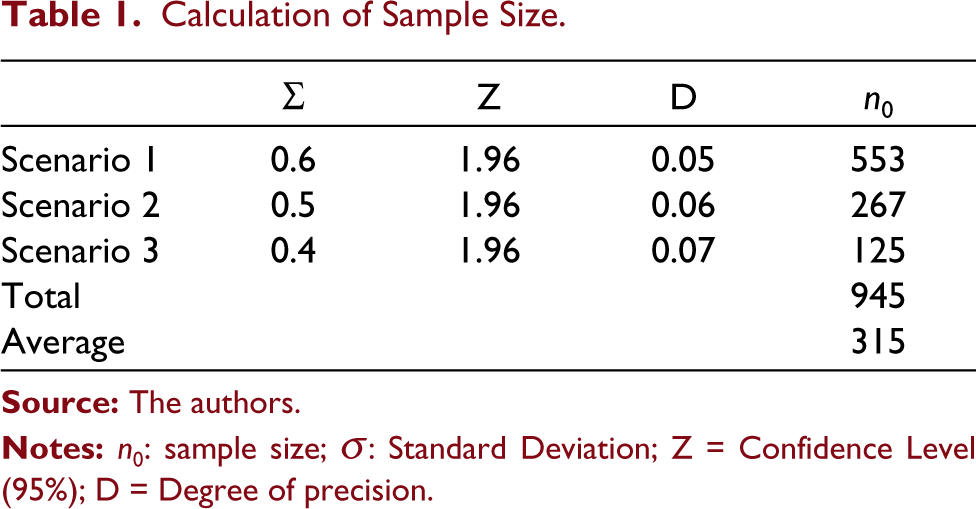

The research used a descriptive survey method. A standard questionnaire was used to collect data from retail (individual) investors in India. The survey instrument was in English; thus, the investigator sought clarification from the respondents as to whether the questions were difficult to understand. Taking a statistical approach for calculation of sample size, the following formula (Malhotra, 2011) was used;

Calculation of Sample Size

Scenario 1: Estimating 60% of standard deviation for 5% degree of precision.

Scenario 2: Estimating 50% of standard deviation for 6% degree of precision.

Scenario 3: Estimating 40% of standard deviation for 7% degree of precision.

Taking an average of the all the three scenarios, the estimated sample size for the study was 315. However, the actual number of responses (via offline forms and online google forms) as received after data cleaning process was 303 on which data analysis was performed.

Selecting a sample that reflects the structure of the population is imperative. Hence, this study adopted purposive sampling technique to approach target population of interest. The initial group of respondents selected, were then asked to help identify others who belong to the same group of interest using snowball technique

The study’s measurement items were adapted from previously validated instruments, as is recommended when using survey methods (Straub, 1989). Since the reliability and validity of constructs have already been developed, the previously validated instrument alerts the researcher to the measurement qualities of existing measures (Bryman & Bell, 2007). Measures for Emotional Intelligence have been adapted and developed from Wong and Law’s (2002) Emotional Intelligence Scale, Impulsive measures have been adapted and developed from Lynam (2013) UPPS-P Impulsive Scale, Financial Risk Tolerance measures have been adapted and developed from Grable and Joo’s (2004) Financial Risk Tolerance Scale, while Financial Risk Behaviour has been adapted and developed from Grable (2008) scale.

A pilot survey of 30 stock market participants was conducted. The measurement model was tested to determine the instrument’s reliability and validity, which were both within the appropriate threshold value, confirming the instrument’s reliability and validity. The questionnaire’s final draft was then prepared accordingly.

Data Collection

Both offline and online methods were used to collect primary data. Leading stock broking firms were approached for offline selection and asked for their help in disseminating the questionnaire among their clients. The same questionnaire, along with a cover letter, was generated using Google Forms for online data collection from the targeted respondents (refer to Appendix).

The aim of the cover letter was to convince respondents to complete the questionnaire by explaining the study’s purpose and significance. The survey was divided into four sections: Part A included items to determine individual investors’ Emotional Intelligence (EI). Appraisal of Emotions of the Self, Appraisal of Emotions of Others, Use of Emotions, and Control of Emotions were the four dimensions of Emotional Intelligence assessed by the scale, each with five items. Part B, meanwhile, included items to assess Impulsiveness (IMP). The four dimensions each having five items was used: Negative Urgency, Lack of Perseverance, Lack of Premeditation, and Positive Urgency. Part C gathered data on respondents’ financial risk tolerance. Part D included four elements that assessed respondents’ financial risk-taking behaviour. All of the items were graded on a five-point Likert scale, ranging from ‘strongly disagree’ to ‘strongly agree’ (Malhotra, 2011), with 1 being the least extreme and 5 being the most extreme.

Just 70 of the 200 questionnaires distributed to stock broking firms were returned, while over 1000 questionnaires distributed online received 233 responses. A total of 1200 questionnaires were distributed, yielding 303 useable responses with a total response rate of 25%. Secondary data informs the researcher about the direction in which he or she can pursue the relevant study. It included looking for books, journal articles, newspaper articles, websites, and blogs on the internet.

The study adopted Partial Least Square-Structural Equation Modelling using SMARTPLS 3.0 as the statistical technique to evaluate the proposed research framework, the reason being:

The study’s main aim was to predict factors related to financial risk tolerance and financial risk-taking behaviour. Therefore, the use of latent variable scores is meaningful in examining the underlying relationship between the latent variables. The study involved use of many latent variables in a combination of LOC’s (lower order constructs) and HOC’s (higher order constructs), leading to a complex modelling (Higher Component Model) of a research model. Therefore, PLS-SEM was considered appropriate for such a complex model containing many latent variables (Henseler et al., 2009).

The purpose of this study was to assess the relations based on prior theoretical evidence. Since, PLS-SEM measures the correlations between the residuals and assesses their impact on the model; hence it is considered a more suitable approach.

Results and Discussion

The inner (or structural) and outer (measurement) models were set up to specify the entire model. The relationships between the constructs (also known as latent variables) are depicted in the inner model. While the relationships between the indicator variables and their corresponding construct are described in the outer model.

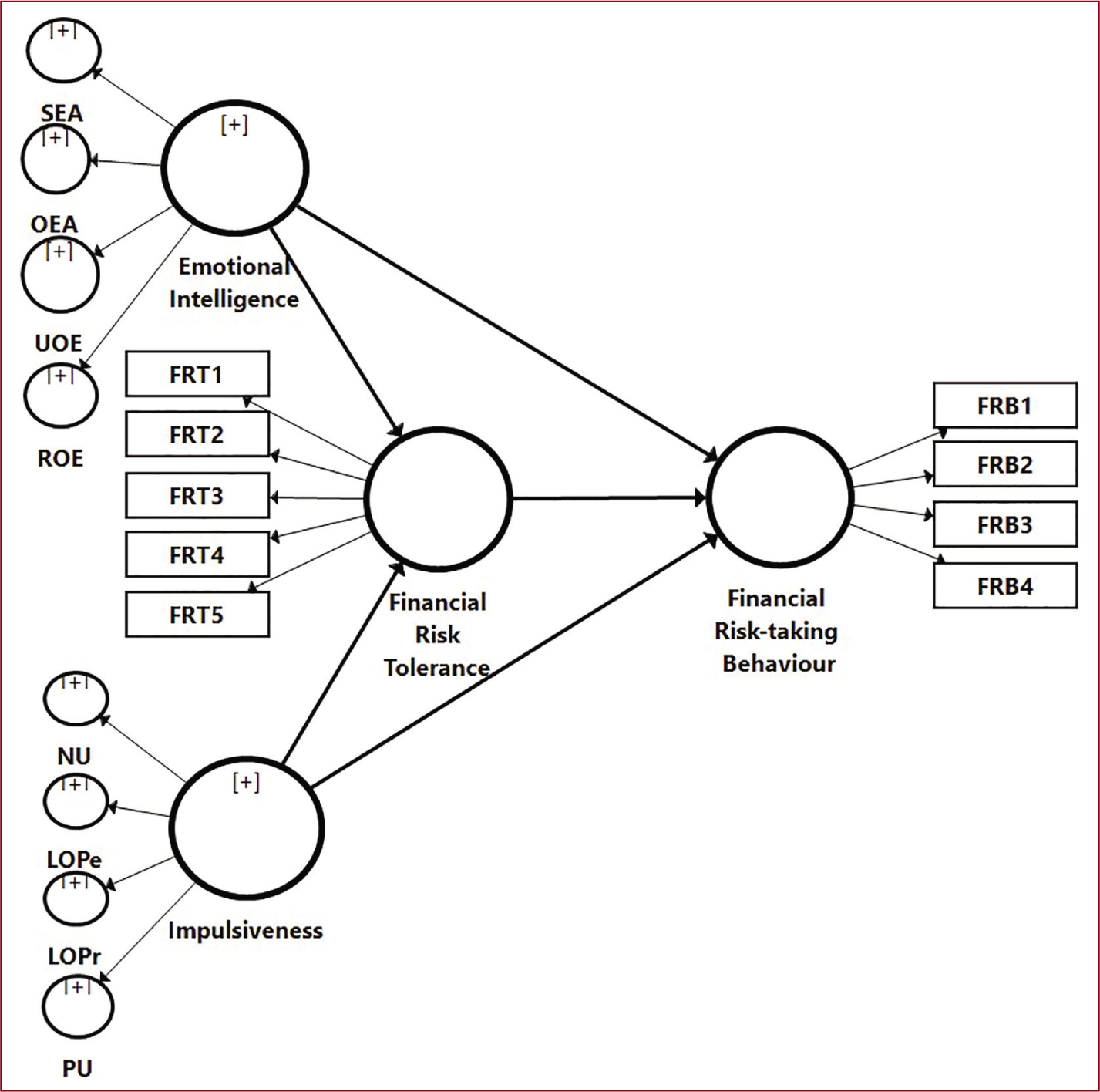

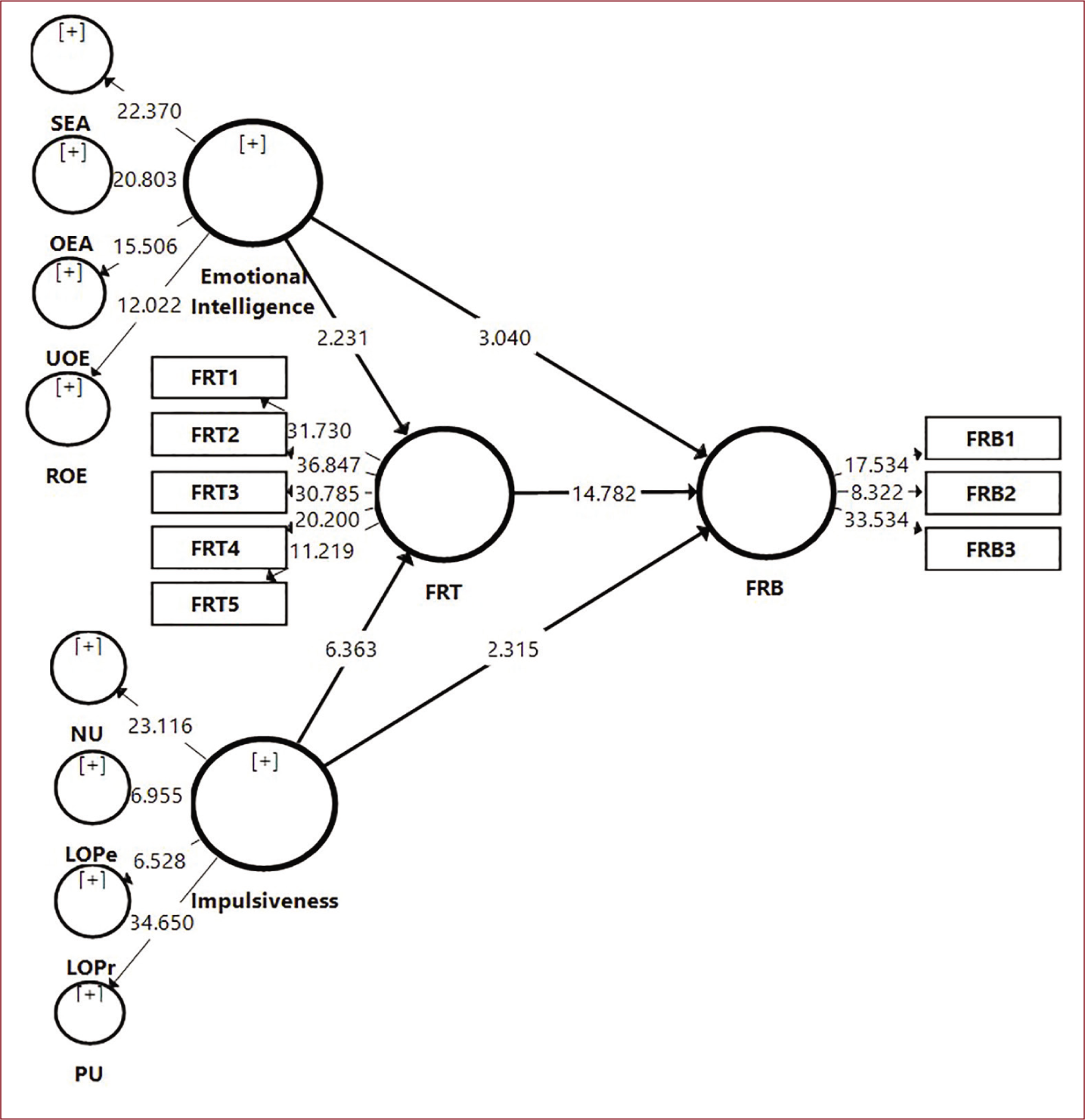

The first step in using PLS-SEM is to create a path model that links variables and constructs based on logic and theory (Hair et al., 2014). According to the concepts, the model incorporates simultaneous mapping of first order constructs, also known as LOC and second-order constructs also known as HOC (Lohmöller, 1989) to altogether form hierarchical component model (HCM). As a result, all indicators of reflectively assessed LOCs were simultaneously assigned to the reflective measurement model of HOC using a repeated-indicators approach.

Figure 2 represents the constructs SEA, OEA, UOE, ROE denoting the LOCs of more general construct Emotional Intelligence (EI) which is measured with twenty indicators SEA1, SEA2, SEA3, SEA4, SEA5, OEA1, OEA2, OEA3, OEA4, OEA5, UOE1, UOE2, UOE3, UOE4, UOE5, ROE1, ROE2, ROE3, ROE4, ROE5. Similarly, the constructs NU, LOPe, LOPr, PU represents the LOCs of construct Impulsiveness (IMP) measured using twenty indicators NU1, NU2, NU3, NU4, NU5, LOPe1, LOPe2, LOPe3, LOPe4, LOPe5, LOPr1, LOPr2, LOPr3, LOPr4, LOPr5, PU1, PU2, PU3, PU4, PU5.

Assessment of Measurement Model

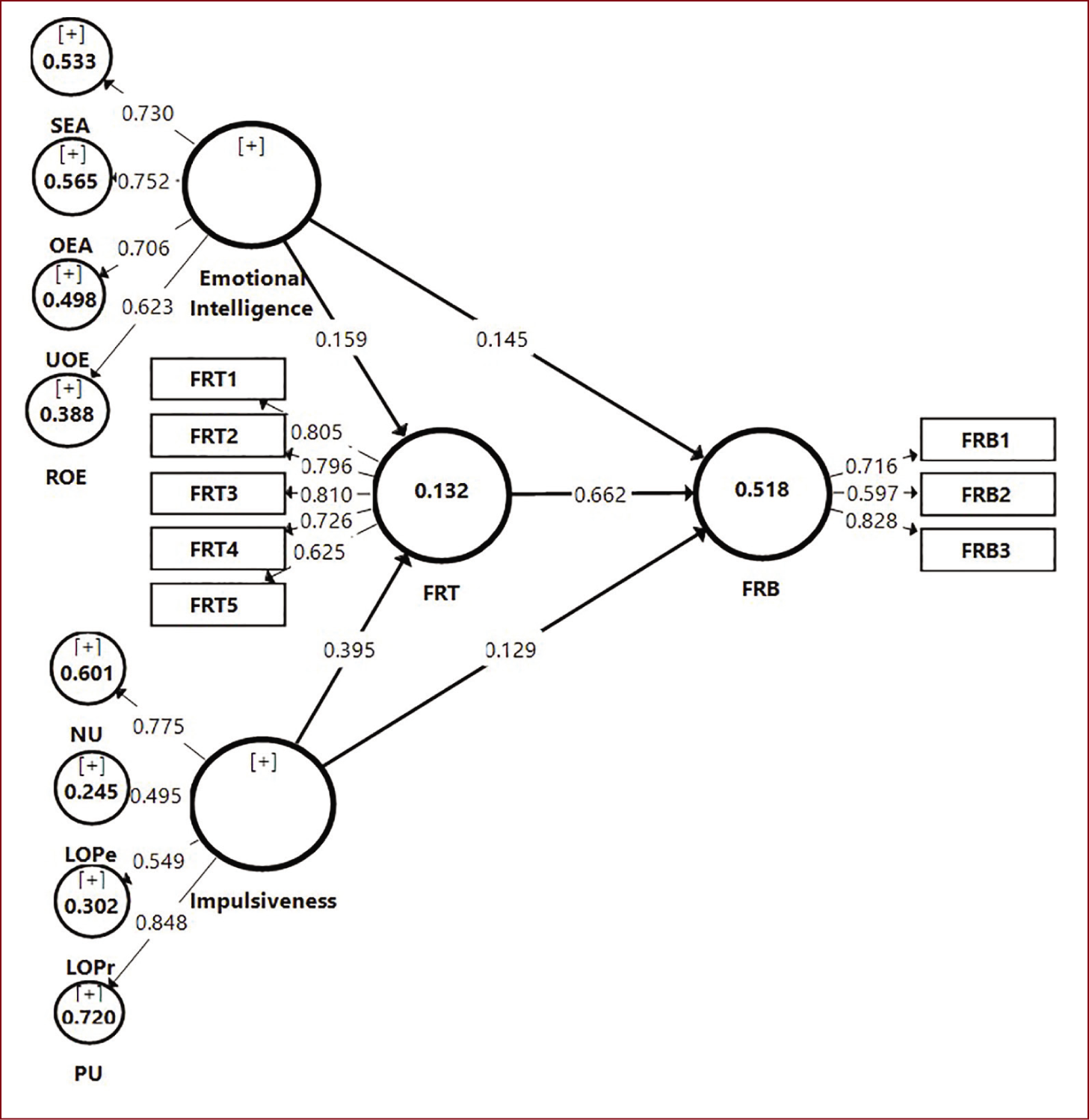

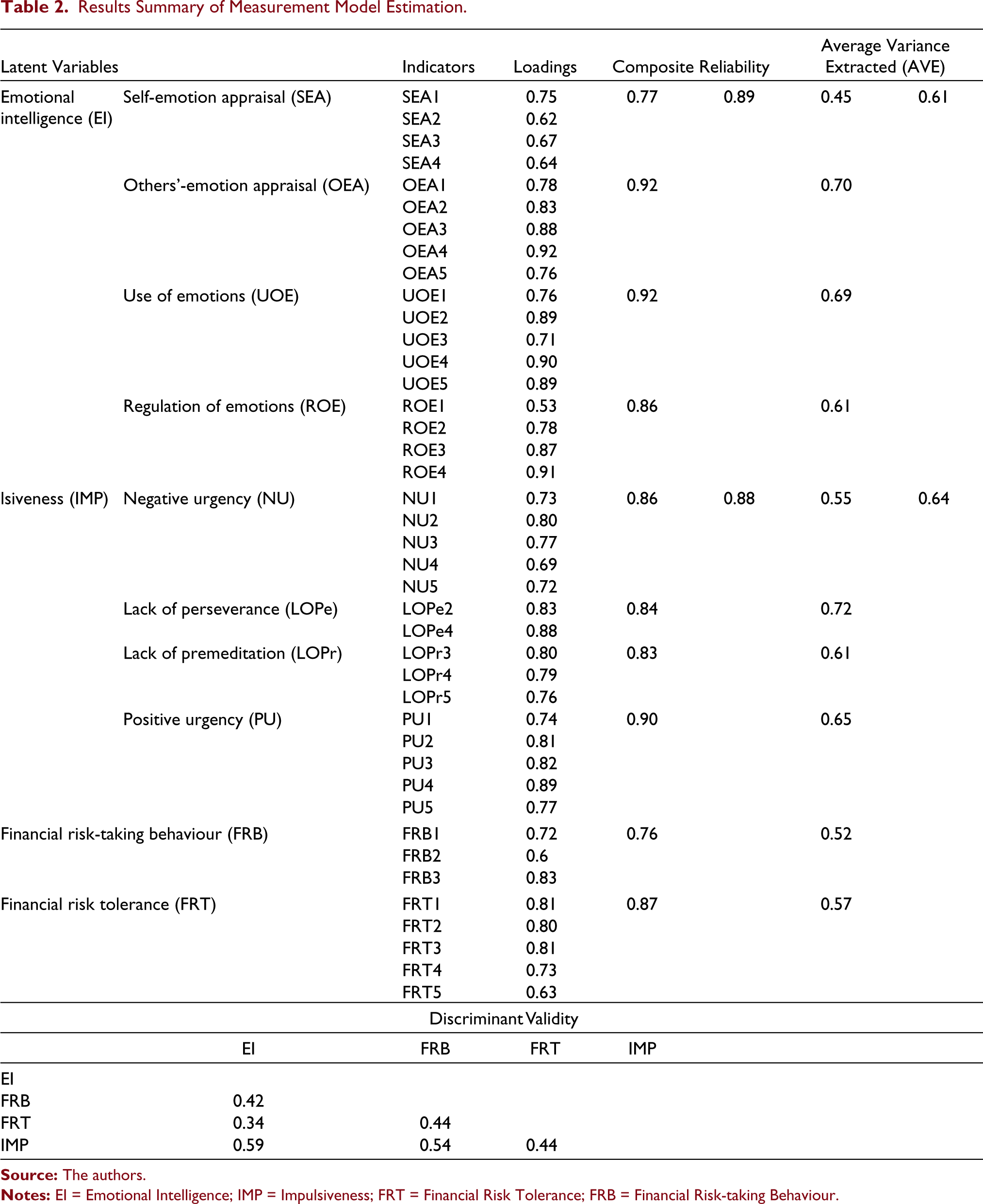

The assessment of the measurement model (refer to Figure 3) was performed by examining indicator reliability, internal consistency reliability (also called composite reliability), convergent validity, and discriminant validity. The outer loadings of greater than 0.5 for all the items of the constructs are considered statistically significant; hence the items having values of less than 0.5 were dropped (Hair et al., 2013). Similarly, the recommended composite reliability (CR) values must lie within the range of 0.6–0.9 (Nunnally & Bernstein, 1994), all the constructs had values greater than 0.7 (Table 2). The AVE (Average Variance Extracted) values were greater than the recommended value of 0.5, thus confirming the convergent validity (Hair et al., 2019). The discriminant validity was checked by calculating HTMT ratios (Heterotrait-Monotrait ratios). All the values were within the threshold limit of 0.85–0.90 (Henseler et al., 2009).

Results Summary of Measurement Model Estimation

Assessment of Structural Model

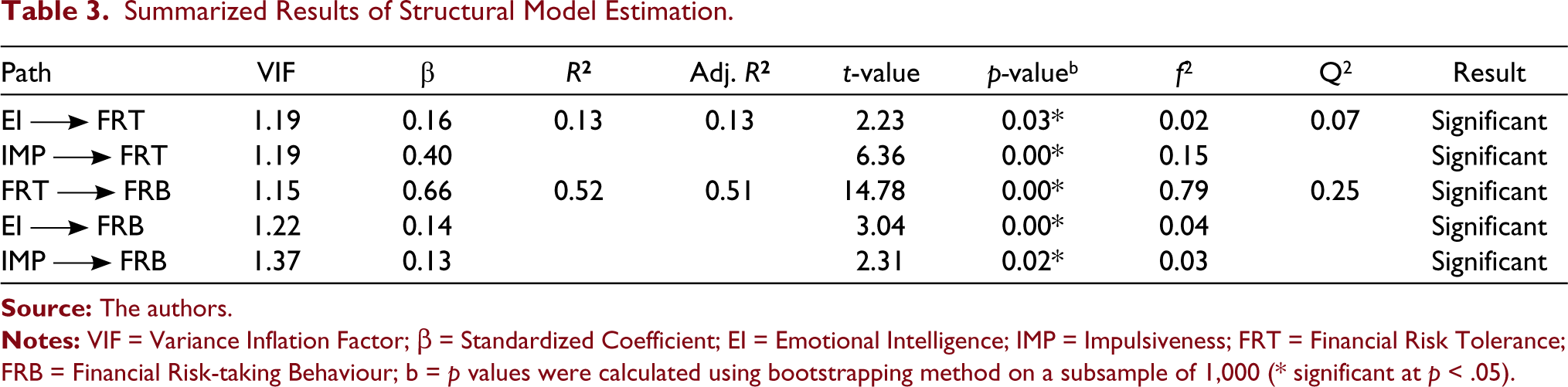

The structural model (refer to Figure 4) was evaluated using the complete bootstrapping method with 1000 sub-samples. Multicollinearity issues were checked for each construct using VIF (Variance Inflation Factor) values, that came out to be within the ideal values of 3–5 (Chand et al., 2020; Hair et al., 2010). Also, the value of R2 (refer to Table 3) suggests that the model has moderate explanatory power, as the rule states that the closer the value to 1, the greater the model’s explanatory power (Dhiman et al., 2018; Hair et al., 2011; Henseler et al., 2009). Moreover, to get a cross-validated redundancy measure of each dependent construct, the blindfolding method (Chin, 1998; Henseler et al., 2009; Tenenhaus et al., 2005) was employed with an omission distance of 7. The positive value of Q2 (greater than 0) signifies the predictive relevance of the model.

Summarized Results of Structural Model Estimation

According to Thaler (2016), there are numerous ostensibly irrelevant factors that influence how humans make decisions. The findings revealed that risk management is not a monolithic notion and that various psychological influences must be taken into consideration. The study’s primary contribution is to investigate all of those ostensibly irrelevant variables simultaneously in a multivariate model. The novelty of this technique rendered a broad investigation of factors to help us better comprehend economic and financial decision-making.

It is clear that emotional intelligence is positively related with financial risk tolerance (path coefficient = 0.16, p = 0.03; is supported) and financial risk-taking behaviour (path coefficient = 0.15, p = 0.00; is supported). The results are similar to those of a related study (Ameriks et al., 2009; Hemrajani & Sharma, 2017, 2018, 2020), which concluded that a person with the ability to perceive, use, and control his emotions is more likely to make risky investments. Furthermore, Krueger and Dickson (1994) found that people who think of themselves as successful decision makers (high EI) are far more likely to take chances than people who are doubt (low EI) on their own self. Also, Byrnes (2003) reported a positive correlation between risk-taking behaviour and cognitive, emotional, and social factors. Moreover, a positive relationship was determined between positive self-concept (i.e., a component of Emotional Intelligence) and risk taking (Judge et al., 1999).

The findings also revealed a positive relationship between Impulsiveness and Financial Risk Tolerance (path coefficient = 0.40, p = 0.00; is supported). These were consistent with the findings of prior research (Zuckerman & Kuhlman, 2000) which revealed that impulsive individuals have the tendency to invest and make decisions faster than non-impulsive individuals and take higher risk. The study presents the evidence for the positive association between Impulsiveness and Financial Risk-taking Behaviour (path coefficient = 0.13, p = 0.02; is supported). The results reported were consistent with that of Zaleskiewicz (2001), who concluded that individuals high in impulsiveness reflect high risk-taking tendencies. The findings suggest that individuals who are impulsive do not get affected by experience associated with risky behaviour and tend to exhibit risk-taking behaviour.

The study also found a positive relationship between Financial Risk Tolerance and Financial Risk-taking Behaviour (path coefficient = 0.66, p = 0.00; is supported). The findings were congruent with previous research (Grable, 2008) which reported that financial risk tolerance is directly related to financial risk-taking behaviour.

It was observed that empirical analysis revealed the significance of a direct relationship between the two variables. However, it is still unclear the cause of these relationships. Thus, to explain this, the role of mediating variable comes into importance. Further, Preacher and Hayes (2008) observed that the significance of indirect effects confirms the presence of mediation. Furthermore, the significance of indirect effect forms the basis for determining the strength of the mediating variable which is obtained with Variance Accounted Factor (VAF). The value below 0.20 (or less than 20%) represents ‘no mediation’; the value between 0.20–0.80 (or between 20% to 80%) represents ‘partial mediation’; while the values above 0.80 (or, 80%) represents ‘complete mediation’ (Hair et al., 2016).

The results revealed that emotional intelligence has a positive indirect impact on financial risk-taking behaviour through financial risk tolerance, which is of same sign as displayed when direct effect was determined, confirming the complementary nature of mediation. FRT also partially mediates the relationship between emotional intelligence and financial risk-taking behaviour, as indicated by the VAF value of 0.42 (refer to Table 4). Similarly, the indirect impact of impulsivity on financial risk-taking behaviour through financial risk tolerance is positive, meaning that the two are complementary, and the VAF value of 0.67 (refer to Table 4) confirms that FRT partially mediates the relationship between impulsivity and financial risk-taking behaviour. This contribution may be a valuable information source for consultants to advise their clients. Overall, the research results seem to contribute to the behavioural finance literature. The psychological factors discussed in this study are expected to affect investment decisions. They are both referring to the emotional aspects of financial behaviour. Most notably, in this analysis, EI and IMP were found to be significant in predicting FRT and FRB. At the same time, FRT can be identified as a cognitive aspect of risky financial behaviour. As a result, this research was structured in such a way that it could include both emotional and cognitive aspects of financial behaviour.

Mediation Analysis

Our findings revealed that the emotional component had a direct impact on financial behaviour. For example, those respondents with higher EI or IMP had a higher degree of risk tolerance and displays risk-taking behaviour in their investment portfolio. These results clearly reject the null hypothesis and support the analysis findings that the two psychological factors can be used to measure risk tolerance and risk-taking behaviour.

Conclusion and Recommendations

Researchers have agreed for decades that demographic variables are the measures of financial risk tolerance. Financial risk tolerance was found to be associated with younger individuals with higher income, being male, and being single (Grable & Joo, 2000; Sulaiman, 2012). However, the question remains: Are there any significant determinant(s) of financial risk tolerance that have been overlooked? Emotional Intelligence and Impulsiveness have been established as significant factors for preferences in several domains, including risk, but they have received little attention in the financial risk domain. As a result of this research, a conceptual model of the relationship between psychological structures, financial risk tolerance, and financial risk-taking behaviour was proposed and evaluated.

The researchers suggested that two psychological constructs, Emotional Intelligence and Impulsiveness, have a direct relationship with financial risk tolerance. Furthermore, previous research has found that nearly all of the factors linked to financial risk tolerance are also linked to financial risk-taking behaviour (Grable, 2008). As a result, in order to dig deeper into the topic, the study looked into the relationship between psychological constructs and financial risk-taking behaviour. In addition, in accordance with Grable and Lyons (2018), the study looked into evidence on the causal relationships between even amongst the variables, as well as the mediating function of financial risk tolerance.

The study found that the proposed psychological constructs of emotional intelligence and impulsiveness were significantly linked to financial risk tolerance and financial risk-taking behaviour, using data from 303 participants. Risk-taking behaviour was more likely among those who had a higher risk tolerance, as calculated by a valid and accurate scale. The fact that the behaviour being reviewed was negative had no impact on the hypothesis’ findings.

Furthermore, people with a high EI score had a higher financial risk tolerance than those with a low EI score. While all EI’s competencies added to the overall profile of investors, it is worth noting that the assessment of one’s own and others’ emotions had the greatest influence of all. Usage of Emotions did, in fact, play a middle ground role, with Regulations of Emotions playing a minor role. If he has insights of himself and others, that is, if he has strong emotional intelligence skills, a person may identify the emotions capable of guiding his thought and actions. Such an individual can channel his feelings into positive results, transforming his fears and worries into opportunities and effectively tackling challenges. The minor role played by Regulation of Emotions may reflect the fact that the trait is particularly important for the quality of social relationships, but it appears to have had little impact on the financial decision-making behaviour that the study was designed to assess.

Individuals with high emotional intelligence abilities were also found to be better at correctly assessing circumstances, determining appropriate responses, and keeping things in perspective. The explanation for this is that people with high emotional intelligence will focus only on emotions that are directly related to decision-making (financial risk-taking), while people with low emotional intelligence are affected by emotions that are irrelevant to those decisions.

Furthermore, people who are impulsive are more likely to invest in riskier stocks, indicating that they are more risk prone, and they seldom seek advice. Furthermore, Positive Urgency, an impulsiveness factor, was discovered to have the greatest impact. Although Negative Urgency had a major impact, the other two factors, Lack of Premeditation and Lack of Perseverance, had only a small impact.

On the basis of above findings, following suggestions are proposed.

Individuals who behave rashly, a financial advisor’s first task is to communicate his client to participate in cognitive enterprises before behaving so that any rash acts can be prevented, that is, teaching cognitive mediation to clients so that they can foresee both positive and negative effects of potential behaviour.

Financial advisors should assist their clients in identifying warning signs that they might be susceptible to impulsive behaviour and creating alert signals to help them stay focused on their long-term goals and interests.

A person should avoid investments that could cause anxiety if he or she has a stronger understanding of risk tolerance, since anxiety may cause fear to be stimulated, causing emotional (rather than logical) responses to the stressor. In the face of financial uncertainty, an investor who maintains a calm demeanour and practises a disciplined decision-making process consistently outperforms the competition.

Implications of the Study

The current study makes significant theoretical and practical contributions in the following areas:

Theoretical Implications

First, it validated the research model, revealing the importance of psychological factors in predicting individual investors’ financial risk tolerance. This study’s results are ground-breaking, and they contribute to the existing literature on Financial Risk Tolerance. Second, the results of the study lend support to a recent risk-taking paradigm known as the risk-as-feelings hypothesis, as it appears that personal characteristics such as emotional intelligence and impulsiveness affect individual financial risk tolerance, thereby offering insights into financial contexts involving risk that are not currently addressed using conventional economic models. Third, the research adds to the body of evidence on causal relationships, specifically the mediating impact of financial risk tolerance on the relationship between psychological constructs and individual investors’ financial risk-taking behaviour.

Practical Implications

The results can be used by professionals, financial engineers, policymakers, and individuals as a solid foundation for understanding various aspects of psychological effects on risk tolerance and how they affect risk-taking behaviour. With the increasing importance of financial management, such awareness would serve as a base for them to enhance their financial well-being.

The most critical role for financial advisors is to control investors’ emotions through market ups and lows. The foundation should be laid during quiet times when investments are performing admirably. Counsellors must then prepare their clients for the anticipated outcomes as well as the emotional responses that can arise. These quiet moments provide an opportunity to discuss and develop an investment plan that can be advised amid emotional turmoil.

The easiest way to replace one emotion with another is to replace it with another emotion (Leslie Greenberg). The explanation for this is that certain feelings are beneficial, and others are detrimental. Assisting clients in shifting toward positive feelings can have a significant effect on how unambiguously people feel in pursuit of their goals. The ability of a financial professional to sense and understand his client’s emotions, as well as control them, can be a pleasurable experience for a person (client).

Limitations and Scope for Future Research

Although the results of the current study are significant, they must be viewed in light of the following limitations:

The results were based on responses from a non-randomly selected sample. This might lead to biased answers from those who are more technically inclined. Furthermore, since the analysis is based on a one-time data collection, it is difficult to determine the causality of the relationship. Since complex shifts in an individual’s preferences are likely, a longitudinal study may be used to perform additional research. The present study did not identify the influence of demographic and other socio-economic variables such as gender, income, experience while measuring FRT and FRB. Future studies could include these factors in the research model. The psychological determinants of FRT and FRB are confined to Emotional Intelligence and Impulsiveness. There might be present other psychological factors which were not included due to time and cost constraints. Besides adding construct will require more samples since there will be an increase in the total numbers of items. Other variables may be included in future studies to predict FRT and FRB.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Dear Respondent,

You are requested to fill up the questionnaire, meant for research purpose. The information as obtained will be used for academic purpose only and the responses will be kept strictly confidential. Thank You for your time and patience.

Mark (√ ) yourself 1 to 5 on the basis of following guide.

1 = Strongly Disagree, 2 = Disagree, 3 = Neither Agree nor Disagree, 4 = Agree and 5 = Strongly Agree

Mark (√ ) yourself 1 to 5 on the basis of following guide.

1= Strongly Disagree, 2= Disagree, 3= Neither Agree nor Disagree, 4= Agree and 5=Strongly Agree

Mark (√ ) yourself 1 to 5 on the basis of following guide.

1= Strongly Disagree, 2= Disagree, 3= Neither Agree nor Disagree, 4= Agree and 5=Strongly Agree