Abstract

Financial well-being (FWB) is critical to subjective well-being—a crucial component in measuring social progress. This study explores the simultaneous influence of five psychological traits of financial self-efficacy, risk tolerance, a propensity to plan, materialism and the tendency for social comparison on FWB. The study is a cross-sectional causal investigation using a web-based survey. The survey was administered to individuals who were active in financial decision-making activities and selected using a combination of judgmental and snowball sampling. Structural equation modelling revealed a positive influence on financial self-efficacy and propensity to plan and the negative impact of risk-tolerance, materialism and a tendency for social comparison on subjective FWB. Financial institutions and educators may utilize the study results for improving characteristics that help their clients make better financial decisions and enjoy higher levels of financial and subjective well-being. The study makes two contributions to the existing literature on the subject. First, the study simultaneously investigates the effect of the five psychological traits on subjective FWB—not attempted hitherto. Additionally, the study provides an Indian perspective on the subject, an emerging country covering one-sixth of the world population.

Introduction

Monetary and financial stress have a significant bearing on modern human lives. Nearly 72% of Americans and 82% of Indian adults face financial stress (ET Bureau, 2019; United Healthcare, 2021). The magnitude of the problem is so immense that the American Psychological Association—a premier global association of psychologists, considers financial stress as a leading cause of unhealthy behaviours like substance abuse and poor dietary habits (American Psychological Association, 2015). A person’s financial well-being (FWB) is directly related to the quality of their overall well-being, which includes productivity at work, relationships, health and quality of life in general (Netemeyer et al., 2017; Ngamaba et al., 2020). Thus, lack of FWB has been associated with behaviours that negatively affect the quality of life. Recent reports have shown that financial concerns are the top stressor for most Indians—a stress factor that has been exacerbated by the pandemic (PwC, 2022). FWB is a significant issue in India as 40% of Indian adults consider financial issues the primary cause of stress compared to other aspects of life, such as job, health and relationships (Koppr, 2021).

India is the world’s largest democracy and accounts for about 16% of the global population. It is an emerging economy with a targeted GDP of 5 trillion dollars by 2025; and enjoys the demographic dividend of a large and young workforce (UNFPA, 2017). While India has a nearly 80% literacy rate, only 27% of its people are financially literate. Having roughly three-fourths of its population ignorant of the pressing need for handling finances is alarming for a country that relies on its economy for its development (NCFE, 2019). As of March 2021, the household debt in India amounted to 14.5% of the country’s nominal gross domestic product, while the gross savings rate stood at 28.2%.

Indian households have a much lower participation rate in financial assets than developed countries. Compared to other countries, the Indian household balance sheet possesses unusual characteristics, like having a high proportion of wealth allocated to physical assets such as gold and real estate and underinvestment in long-term insurance and pension products (Household Finance Committee, 2017). The Government of India and the Financial Sector Regulators have emphasized strengthening financial inclusion and imparting financial education to its citizens to address these conditions. Through these interventions, the citizens will be empowered with access to financial services and information that will allow them to make informed financial choices that can enhance their FWB.

In light of recognizing the importance of an individual’s finances on well-being, there have been numerous studies on FWB across disciplines over the past few decades. A significant amount of work has been done on conceptualizing and measuring FWB (Consumer Financial Protection Bureau, 2015; Kempson et al., 2017; Prawitz et al., 2006) and exploring the different determinants of FWB (Hira & Mugenda, 1998; Netemeyer et al., 2017; Shim et al., 2009). The impact of socioeconomic and demographic characteristics, such as gender, age, education, marital status, family structure and income in determining one’s levels of financial satisfaction and well-being has been widely investigated (Cheng, 2010; Hira & Mugenda, 1998; Joo & Grable, 2004; Mahendru et al., 2020). Financial capability related factors, such as financial knowledge, financial attitude and financial practices also significantly influenced FWB (O’Neill et al., 2005; Parrotta & Johnson, 1998; Shim et al., 2009; Xiao et al., 2014). However, people with similar socioeconomic and demographic characteristics and comparable financial capability levels may experience different levels of FWB (Kahneman & Deaton, 2010). This difference in perception of FWB can be attributed to differences in psychological traits in people (Brüggen et al., 2017; Consumer Financial Protection Bureau, 2015; Davis & Runyan, 2016; Netemeyer et al., 2017). Though the role of psychological factors on financial decisions and outcomes has been recognized and considered for research, there is still a lack of clarity on how the various psychological factors influence the FWB of individuals. The present study aims to give additional insights into the underlying psychological sources that influence financial decision-making and outcomes. Studying FWB and its psychological determinants in India can provide a perspective that may be useful across similar markets worldwide. With better knowledge of the psychological determinants of FWB, policymakers can design efficient ways to improve desired financial behaviour, promoting financial and subjective well-being (SWB) among subjects.

The article’s organization is as follows: The second Section begins by reviewing the existing academic literature on psychological determinants of FWB. Hypotheses involving the key constructs are formulated in the light of reviewed literature. The third Section outlines the sampling, instrument, data collection and statistical analysis, followed by the study results and discussion. The concluding section deals with the current research’s contribution, implications and limitations.

Literature Review

Subjective Well-being (SWB)

Well-being is a topic that has attracted researchers’ attention from several domains in the past few decades. SWB refers to one’s assessment of their quality of life and describes how people think, feel and experience their state of living (Diener, 1984). It is the product of a cognitive, judgmental process reflecting the gap or discrepancy between what one experiences and the personal reference point that one sets for oneself (Cummins & Nistico, 2002). Overall well-being or satisfaction with life depends on satisfaction with different domains of life—such as health, financial situation, job, leisure, housing and environment (Van Praag et al., 2003). Among these domains, FWB is a significant component of the overall well-being of a person (Netemeyer et al., 2017) and is an important contributor to one’s overall life satisfaction (Ngamaba et al., 2020; Weiting & Diener, 2014).

FWB—Definitions and Conceptualizations

FWB-related concepts are investigated across disciplines ranging from economics, psychology and consumer decision-making to services marketing. Such multi-faceted treatment has resulted in various definitions and conceptualizations covering different aspects of one’s financial situation. Terms such as economic satisfaction, financial satisfaction and FWB are interchangeably used without a clear distinction between the terms or their measures (O’Neill et al., 2005; Shim et al., 2009). In one of the earliest and most comprehensive works on FWB, financial satisfaction was defined as the ‘objective and subjective aspects of the financial situation evaluated against standards of comparison to form a person’s opinion of his/her financial situation’ (Porter & Garman, 1993). Most of the work on FWB has defined it in terms of one’s ‘subjective perception or evaluation of their financial condition’ (Weiting & Diener, 2014; Xiao et al., 2014) or perception of ‘adequacy of financial resources’ (Hira & Mugenda, 1998) or the feeling of ‘contentment’ with various aspects of ones’ financial position (Joo & Grable, 2004; Sahi, 2017). Xiao et al. (2006) proposed a broader definition for financial satisfaction, which encompasses the degree to which one has financial adequacy, financial security and the feeling of being able to ‘accomplish certain financial goals’ or meet their specific financial needs. A contrasting approach was suggested by Prawitz et al. (2006). They consider FWB ‘a continuum of negative to positive feelings/reactions to the financial condition’. From the consumer’s perspective, Consumer Financial Protection Bureau (CFPB) defines FWB as ‘the state of being whereby a person can fully meet current ongoing financial obligations, can feel secure in their financial future and is able to make choices that allow enjoyment of life’ (Consumer Financial Protection Bureau, 2015). CFPB considers four critical components to FWB: control over one’s finances, capacity to absorb a financial shock, ability to meet financial goals and financial freedom of choice. In a recent review paper, Brüggen et al. (2017) proposed that FWB was ‘the perception of being able to sustain current and anticipated desired living standards and financial freedom’. Thus, more recent studies have incorporated the dynamic nature of the construct (Brüggen et al., 2017; Netemeyer et al., 2017).

Psychological Determinants of Financial Well-Being

Behavioural finance literature emphasizes the irrationality in human behaviour. The observed departures in utility theory and other traditional theories on economic behaviour can be understood by studying the influence of psychological traits on human preferences and behaviour. These traits can offer valuable insight into why people behave the way they do and how they feel and perceive their outcomes. The role of psychological and attitudinal traits like motivation to gather relevant financial information, the ability to control emotions, confidence in decision-making and financial management capabilities are crucial for successfully managing one’s finances (Mahendru et al., 2020). Psychological traits, such as locus of control, a propensity to plan, susceptibility to interpersonal influence and life values related to money, consumption, spending and saving are also significant predictors of FWB (Brüggen et al., 2017; Consumer Financial Protection Bureau, 2015; Netemeyer et al., 2017; Rehman, 2021; Strömbäck et al., 2017). These non-cognitive traits and skills are highly influential in causing differences in financial behaviour and may predispose individuals to experience different levels of FWB.

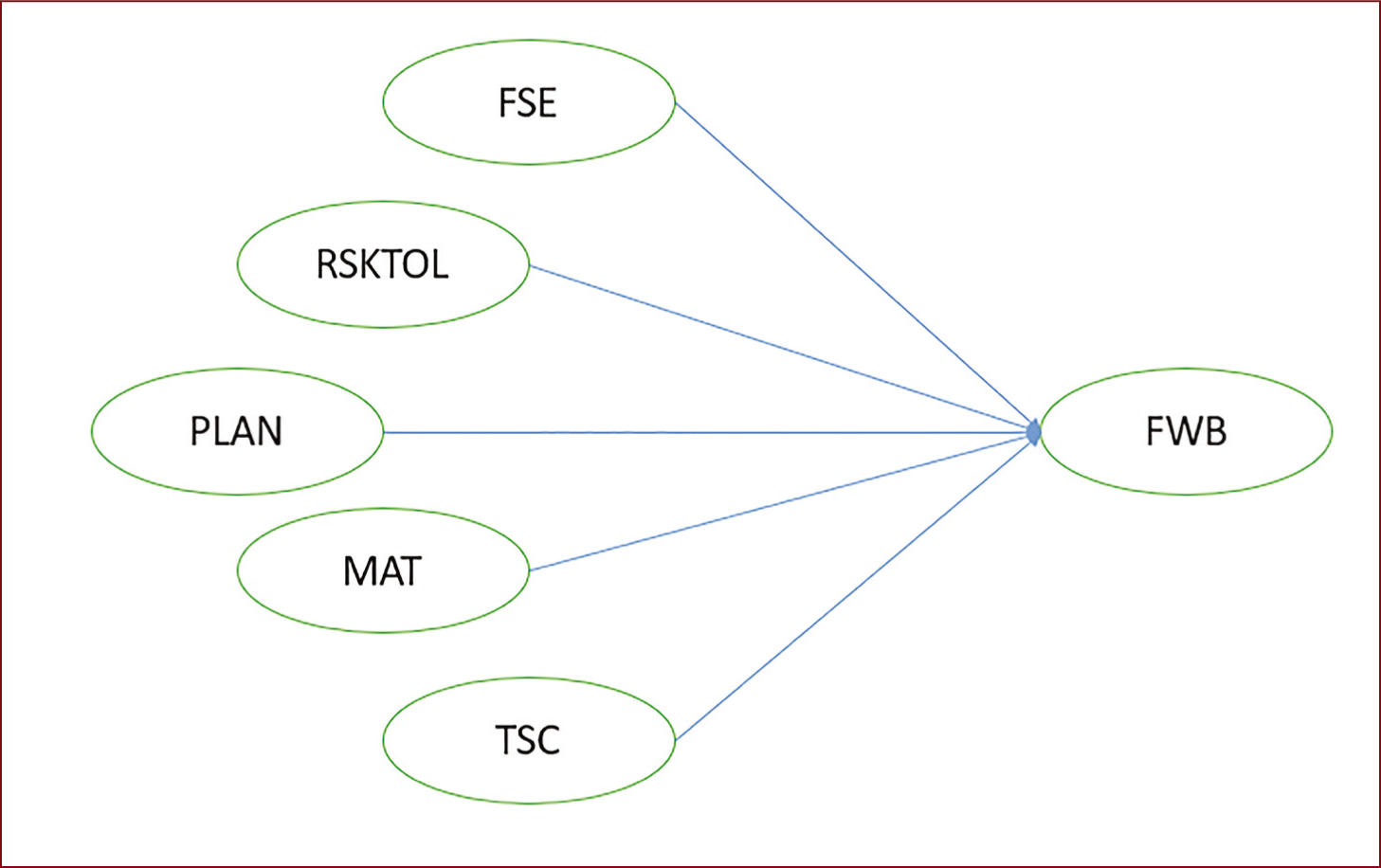

Though studies have suggested that psychological traits play a crucial role in successfully managing one’s finances and their resulting outcomes, the actual mechanism through which these factors affect FWB is unestablished. Based on previous literature exploring the relationship between personality traits and attitudes on FWB (Brüggen et al., 2017; Consumer Financial Protection Bureau, 2015; Kempson et al., 2017), we focus on five traits—financial self-efficacy, risk tolerance, the propensity to plan, materialism and tendency for social comparison. A search of three of the largest research databases—Google-Scholar, Scopus and Proquest, for the Boolean string ‘financial well-being AND financial self-efficacy AND risk tolerance AND propensity to plan AND materialism AND social comparison’ yielded no matching results. Such a search result indicates that there have been no prior studies simultaneously investigating the impact of the five psychological traits on FWB. Another shortcoming in the FWB literature is that most research emanates from the western developed economies (Ponchio et al., 2019; Santos et al., 2016). Hence the various aspects of FWB are drawn only in the cultural context of these countries. It is essential to consider cultural context as it influences beliefs, attitudes, perceptions, norms, preferences and behaviours to a great extent. Emerging market contexts differ significantly in socioeconomic, cultural and political realities; therefore, the developed countries’ constructs, theories and findings may not apply here (Burgess & Steenkamp, 2006). With a population of around 1.3 billion and being the fastest growing economy globally, studying FWB and its psychological determinants in India can provide a perspective that may be useful across similar markets worldwide. The present study addresses these gaps in the literature. It tests the simultaneous effect of select psychological traits on the FWB, as shown in the conceptual model in Figure 1.

Conceptual model

Based on existing academic literature, this section constructs a theoretical framework in the form of a nomological network and hypothesizes the relationships among the constructs. We employ a building-block approach (Meneau & Moorthy, 2021) to explain how each construct relates to the other constructs in the model. The endogenous construct, FWB, is hypothesized to be influenced by the exogenous constructs—the five psychological traits: financial self-efficacy, risk tolerance, a propensity to plan, materialism and the tendency for social comparison.

The model can be represented as follows:

Financial self-efficacy

Financial self-efficacy is the level of confidence of an individual to deal with financial matters. It represents a belief in one’s ability to make complex financial decisions and financial management skills (Netemeyer, Warmath, Fernandes, & Lynch Jr, 2017). The social cognitive theory states that an individual is more likely to attempt, persist and succeed at activities if he possesses a strong sense of self-efficacy (Bandura, 1977). A positive self-concept is one of the best predictors of future performance since it builds one’s self-esteem and boosts one’s self-confidence (Chandra et al., 2019; Limbu & Sato, 2019; Sachitra et al., 2019). Individuals with high levels of financial self-efficacy are confident in their financial management capacities and thereby exhibit desirable financial behaviour and enjoy positive financial outcomes (Asandimitra & Kautsar, 2019; Asebedo & Payne, 2019; Gamst-Klaussen et al., 2019; Vosloo, 2014). Perceived behavioural control, a similar construct to financial self-efficacy, was one of the critical factors influencing financial behaviour and satisfaction (Shim et al., 2009). Based on the above premise, the following hypothesis is proposed.

Propensity to plan

Propensity to plan refers to a person’s tendency to predetermine a course of action to achieve long-term goals (Hayes-Roth & Hayes-Roth, 1979). Those with this trait are patient and good at budgeting and saving regularly, thereby fulfilling their wealth accumulation goal in the long run (Ameriks et al., 2003; Tam & Dholakia, 2014). They make conscious efforts to monitor their financial decisions and ensure their consistency with financial goals, wealth accumulation for retirement and improved FWB (Lee & Kim, 2016; Lee et al., 2019; Hastings & Mitchell, 2020). Propensity to plan has demonstrated a positive effect on financial satisfaction in previous research (O’Neill et al., 2016; Xiao & O’Neill, 2018). Based on the above premise, the following hypothesis is proposed.

Risk tolerance

Financial risk tolerance is the maximum finance-related uncertainty acceptable to an individual and can lead to differences in financial decisions and outcomes. Willingness to take up risks determines the type of instruments a person invests in and is, therefore, a critical antecedent of financial behaviour and, ultimately, FWB (Fernandes et al., 2014; Hemrajani et al., 2021; Woodyard & Robb, 2016). A person whose risk tolerance is higher may prefer to invest in high-risk options like equities instead of a risk-averse person who is likely to park his investments in conservative investment vehicles like bank deposits or bonds (Akhtar & Das, 2019; Sivaramakrishnan & Srivastava, 2019). Thus, risk-tolerant individuals invest in higher-risk instruments and reap higher returns in the long run, and thereby experience higher financial satisfaction (Woon-Yong & Hanna, 2004). Based on the above premise, the following hypothesis is proposed.

Materialism

Richins and Dawson (1992) define materialism as the ‘importance one attaches to the ownership and acquisition of material things in achieving his major life goals’. They use material goods owned as a measure to judge one’s success in life. Studies have shown that materialism is associated with undesirable practices, such as compulsive and impulsive shopping, over-borrowing and excessive credit card debt, resulting in lower wealth and ultimately heightened levels of financial worry and lower FWB and life satisfaction (Garðarsdóttir & Dittmar, 2012; Potrich & Vieira, 2018). Research indicates that materialistic outlooks are associated with lower levels of FWB (Chatterjee et al., 2019; Ponchio et al., 2019; Sinha et al., 2021). A meta-analysis of studies on materialism (Dittmar et al., 2014) found a significantly negative association between materialistic values and well-being. Such negative relation is in line with the classic observation by Sirgy (1998) that people who endorse materialistic values experience higher levels of dissatisfaction in their life.

Tendency for social comparison

People in similar financial conditions experience different levels of well-being depending on their comparison (Brüggen et al., 2017). Such difference follows the social comparison theory (Festinger, 1954), which states that humans have an intrinsic need to evaluate themselves against their reference groups. Therefore, perceived FWB depends on how individuals perceive their financial situation compared to their peers or other family members (Porter & Garman, 1993; Hira & Mugenda, 1998). Individuals in collectivistic societies like India are more likely to compare themselves with others, affecting their self-evaluation and social standing (Chatterjee et al., 2019). Ferrer-i-Carbonell (2005) found that people are happier when their income or financial status is better off when compared to comparable others in society. However, such comparative tendencies negatively affect SWB when comparing those who are better off than oneself (Brown & Gray, 2016; Hagerty, 2000; White et al., 2006). Based on the above premise, the following hypothesis is proposed.

Thus, the current study proposes to test the conceptual model as shown in Figure 1. This model is built primarily on the foundations of the social cognitive theory (Bandura, 1977) and the social comparison theory (Festinger, 1954). The social cognitive theory accounts for financial self-efficacy and propensity to plan, and the social comparison theory for social comparison, materialism, and risk tolerance.

Methodology

Measures

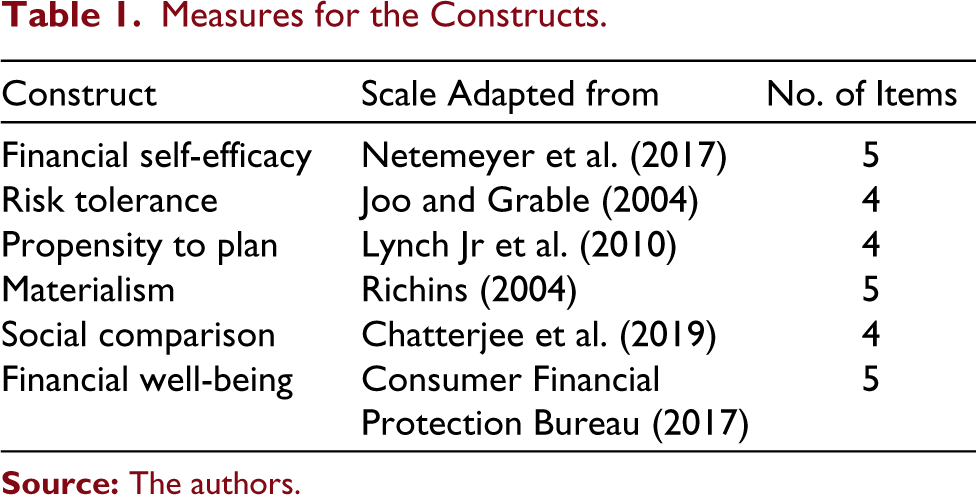

The study used pre-validated scales to measure the research variables. The list of constructs used in the research and the scales used to measure them are in Table 1. All items were measured using a 5-point Likert scale. The critical variable of the study, FWB, was measured by adopting the shortened scale developed by CFPB (2017) based on its earlier application and validation in the Indian context (Ali & Talha, 2021; Sehrawat et al., 2021). As the scales were designed for a different research context, a questionnaire pre-test was done on 15 respondents matching the survey respondent characteristics. Minor changes were effected in the wordings to improve comprehension, based on the pre-test survey feedback. As the study subjects were English educated at the graduation level, translation was not considered necessary. Apart from the study variables, demographic variables including age, gender, employment sector, education, experience, marital status and income levels were collected. The reliability and validity of the scales were re-assessed during data analysis. The data analysis used partial least square based structural equation modelling (PLS based SEM) with WARP PLS v 8.0 software (©ScriptWarp Systems).

Measures for the Constructs

Participants

Considering the research objectives, the study recruited respondents from all over India who were actively involved in financial decision-making activities. The respondent characteristics included employment in the organized sector, with a minimum of 2 years’ experience and currently in work. They had to be making independent financial decisions regarding the use of their incomes. Respondents from unorganized sectors were excluded from the study as their sources of income were not regular, especially during the pandemic, temporarily altering their financial behaviour.

Procedure

The study used a combination of judgmental and snowball sampling to recruit the survey respondents. As the purpose of the study is to examine the relationship among variables and not to achieve statistical generalizations, non-probability sampling techniques are justified. The initial respondents were recruited from the contacts of the researchers, and further respondent recruitments snowballed from the initial ones. However, no more than three referrals were considered for snowballing to prevent recruitment biases commonly seen with snowballing technique. The survey instrument was hosted online (Google forms), and no physical data collection was done due to the prevailing pandemic. The recruits were mailed the survey link to introduce the survey, its objectives, referral and the request for participation. The survey respondents were appraised of their right to refusal and anonymity. No personal information (identifying the respondent) was collected from the recruits. A total of 800 recruits were mailed a request to participate in the survey. The survey was conducted/hosted for 8 weeks online and three reminders were sent—one each at the end of the second, fourth and sixth week from the first mail.

Results

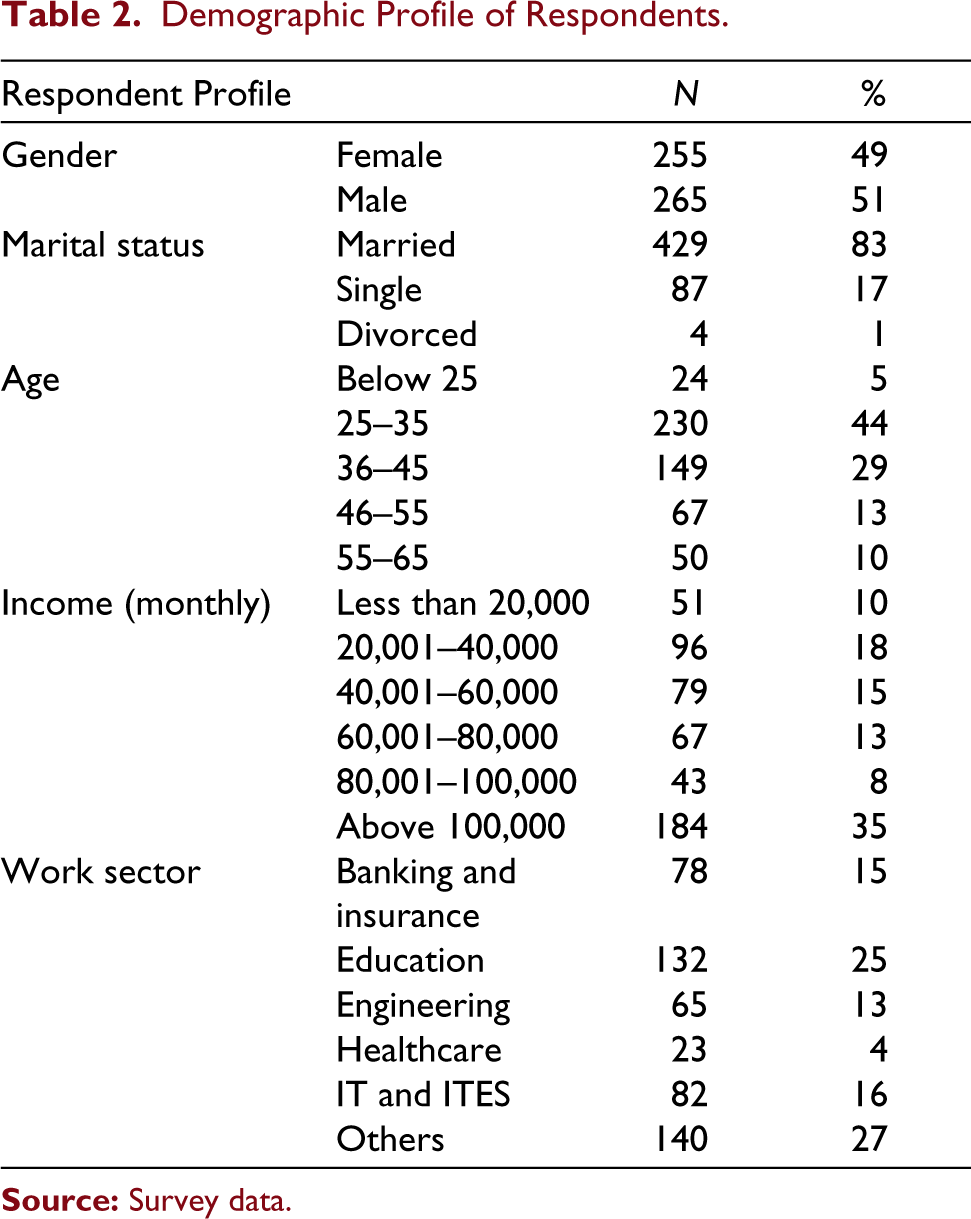

The response rate was 68%, with 544 returned responses. After initial data validation checks, 520 responses were selected for inclusion in the final analysis. The gender distribution of responses was near equal (49% females and 51% males). Eighty-three percent of respondents were married and most of the respondents (73%) were between 25 and 45 years. All the respondents had a minimum of 15 years of education. A detailed description of the demographic profile is provided in Table 2.

Demographic Profile of Respondents

Since this study is cross-sectional and relies on self-report responses, it is prone to measurement errors resulting from common method bias (CMB). The authors of the study tried to control for CMB at the procedural level by informing the respondents about the purpose of the study and assuring anonymity and confidentiality of the information collected (Podsakoff et al., 2003). Harman’s single factor test was performed at the statistical level to check for method biases. Variance explained by the single factor was 21.56%, which is less than 50%, implying that the study is free from CMB (Podsakoff et al., 2003).

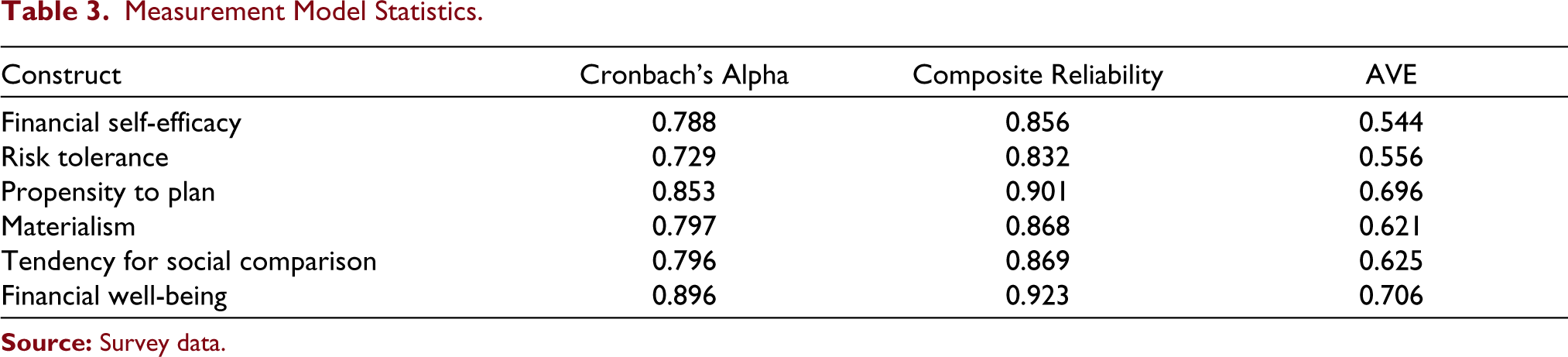

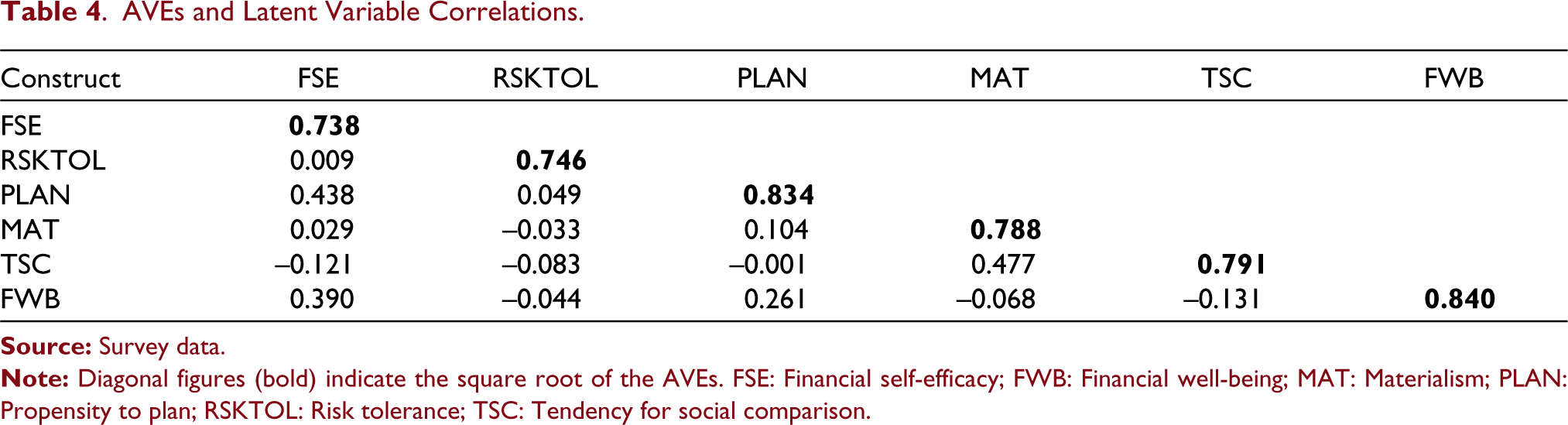

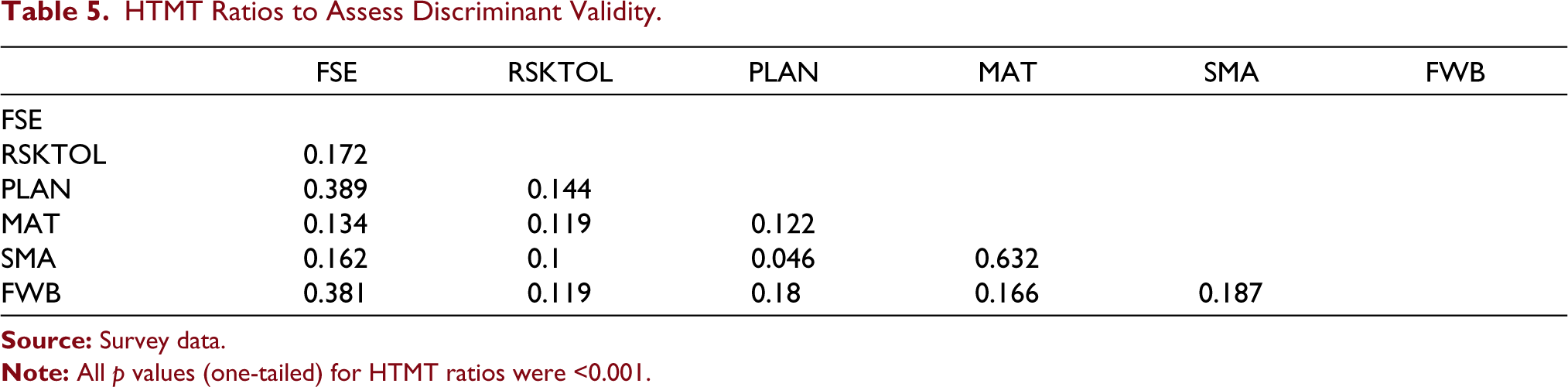

No items were deleted as all item loadings were more than 0.6 and there was no significant cross-loading of items on the constructs (Hair et al., 2012). Table 3 summarizes the measurement model, which indicated good reliability and validity. The Cronbach’s alpha and composite reliability values of all the scales (measuring the different study constructs) are higher than 0.7, signifying their reliability (Hair et al., 2006). As indicated in Tables 2 and 3, the average variance extracted (AVE) for all the constructs is greater than 0.5. Also, Table 4 indicates that the square root of AVEs is greater than latent variable correlations, indicating convergent and discriminant validity, respectively (Fornell & Larcker, 1981). Additionally, the heterotrait-monotrait Ratio (HTMT) ratios for all constructs, as shown in Table 5, were lower than the suggested threshold of 0.85, indicating good discriminant validity (Henseler et al., 2015).

Measurement Model Statistics

AVEs and Latent Variable Correlations

HTMT Ratios to Assess Discriminant Validity

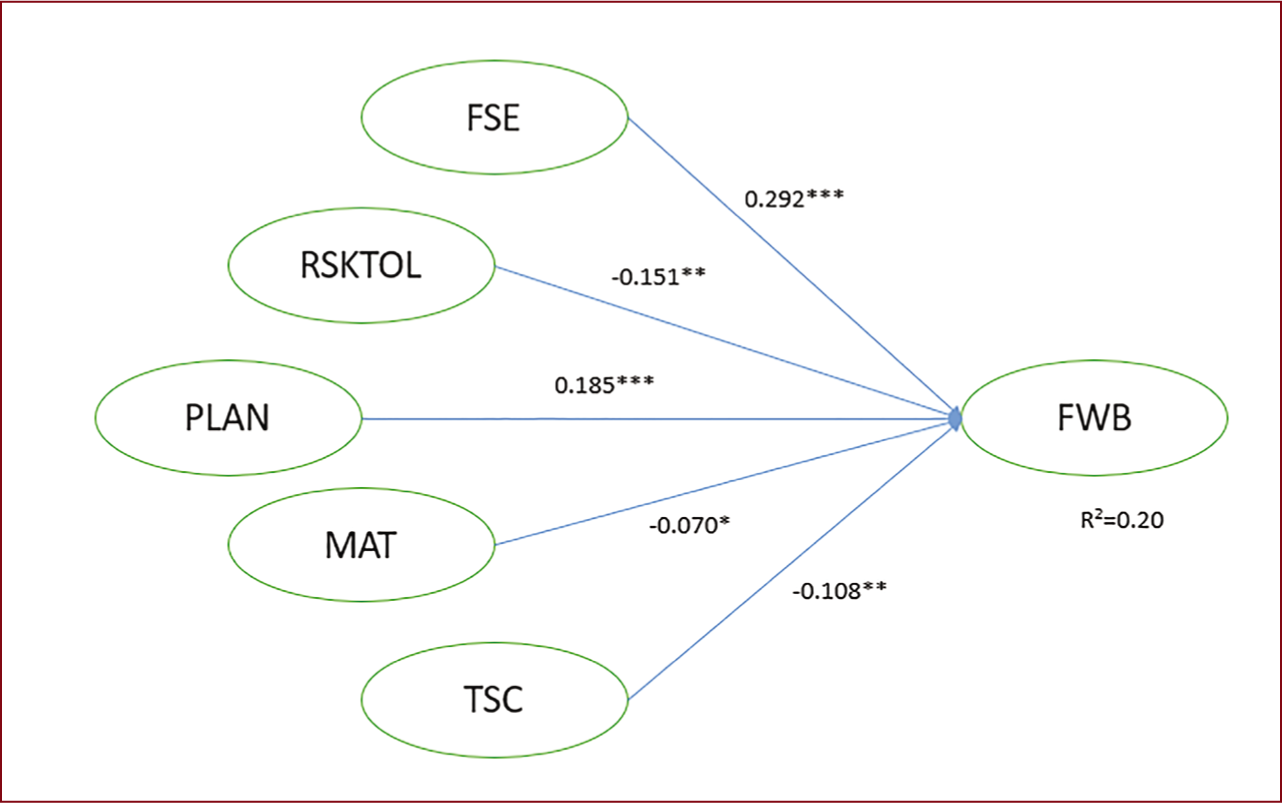

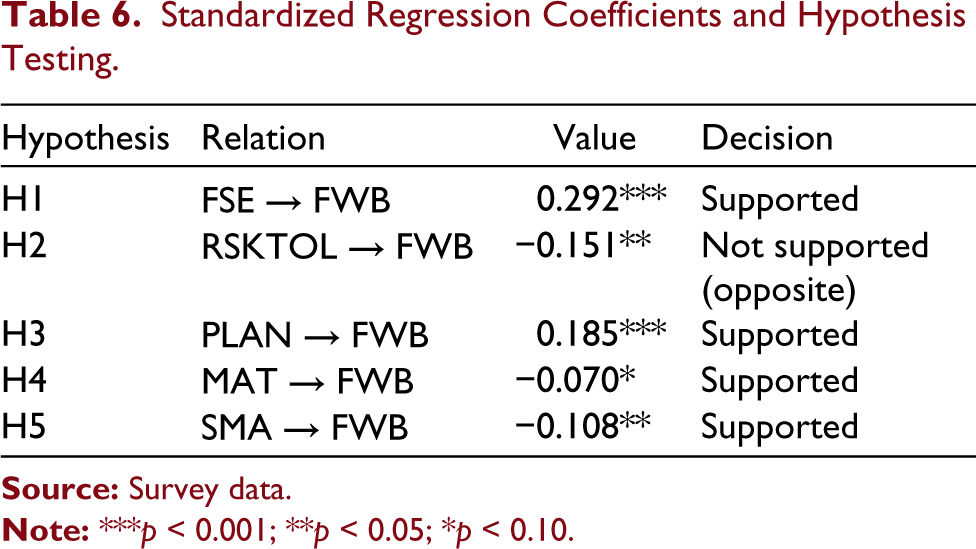

Structural model analysis revealed a simultaneous relationship between the latent constructs (Figure 2). The model explains 20% of the variance of FWB as indicated by R-squared coefficient = 0.200 and Adjusted R-squared coefficient = 0.188. All the standardized path coefficients (β-value) were significant (Table 6). Path coefficients support the hypotheses that financial self-efficacy (β = 0.292, p <0.001) and propensity to plan (β = 0.185, p < 0.001) positively affect FWB; whereas materialism (β = −0.070, p < 0.10) and tendency for social comparison (β = −0.108, p < 0.05) negatively affects FWB. The path coefficient for risk tolerance with FWB (β = −0.151, p < 0.01) shows a negative relationship and is contradictory to the hypothesized relation.

Standardized Regression Coefficients and Hypothesis Testing

The final empirical model can be represented as

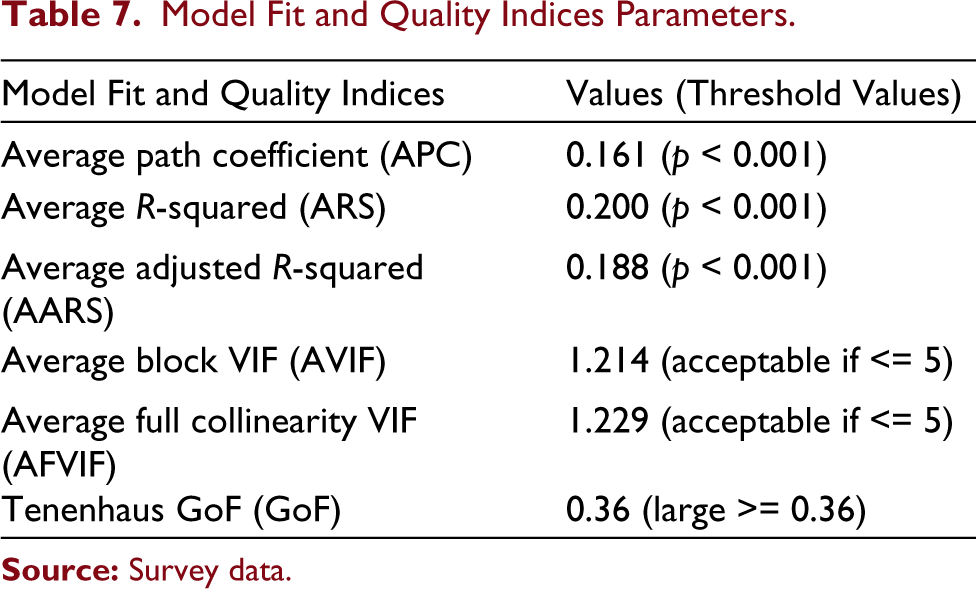

The measurement model fit and quality indices, shown in Table 7, were all within the suggested thresholds indicating a good fit for the proposed research model (Rosenthal & Rosnow, 1991; Tenenhaus et al., 2005). Collinearity issues were also ruled out as average block variance inflation factor (1.214) and Average full collinearity variance inflation factor (1.229) was less than 10 (Kock, 2015).

Model Fit and Quality Indices Parameters

Discussion

The current study is a unique attempt to investigate the simultaneous impact of five psychological traits on FWB. The predictor variables included financial self-efficacy, risk tolerance, the propensity to plan, materialism and a tendency for social comparison—and have their origins in the social cognitive theory and social comparison theory. Previous studies have taken such personal traits into account while analysing financial outcomes. However, no prior research has used empirical investigations to examine associations between the five psychological factors and FWB simultaneously. Analysis of the relative and combined effect of the select psychological factors on FWB revealed the positive influence of financial self-efficacy and propensity to plan on FWB and the negative impact of risk tolerance, materialism and a tendency for social comparison; on FWB. The study’s findings corroborate with similar studies on financial outcomes (Chatterjee et al., 2019; Vosloo, 2014; Xiao & O’Neill, 2018) except in the case of risk tolerance.

The results from this study and previous studies (Hagerty, 2000; Sirgy, 1998) highlight the negative influence of materialism and a tendency for social comparison on FWB. Previous study results have indicated a negative relationship between materialism and FWB (Dittmar et al., 2014; Potrich et al., 2018). The study results also repeat the earlier trend in research on the relationship between the tendency for social comparison and FWB (Brown & Gray, 2016; White et al., 2006). The negative association of materialism is not restricted to FWB; it extends to satisfaction with life and its various other domains. A highly materialistic society may not consistently achieve high levels of FWB and life satisfaction, and their relationship is curvilinear (Proto & Rustichini, 2013). Increased tendency for social comparison results in a need for accumulating worldly possessions and negatively affects FWB. Hence, it is high time to contemplate the importance attached to material possessions and our inherent need to compare ourselves with others. Such findings also need to be incorporated into formal and social financial education programs designed for improving FWB.

Financial risk tolerance is critical for individual planning and investment (Garman & Forgue, 1997). Earlier studies had explained the positive association between risk tolerance and FWB in terms of higher returns realized from risky assets in the long run, resulting in increased net worth (Woon-Yong & Hanna, 2004). However, the current study indicates a negative relationship between risk tolerance and FWB and is contrary to the previous findings that risk tolerance positively influences FWB (Fernandes et al., 2014; Jeong & Hanna, 2004). The results may be different due to two main differences—the difference in the cultural context and the second due to the subjective nature of the measure employed in the study. Culturally Indians are highly restrained, making them less materialistic. The lower levels of materialism, in turn, result in lower levels of risk tolerance (Hofstede-Insights, 2021; Mishra & Mishra, 2016; Richins, 2011; Thanki et al., 2020). Therefore, people are financially happy with lower but safer returns while investing as they have limited materialistic possessions to accumulate. The appetite for riskier investments like stocks has always been lower in India. Only about 3.7% of Indians have exposure to equity markets, whereas 55% of the American households own stocks. However, the Indian trend may be showing a generational shift as more young Indians opt for riskier investments like stock (Balwani et al., 2021; Ghilarducci, 2020). Another reason for the contradicting nature of the study results on the risk tolerance and FWB may be the subjective nature of the measure. The use of objective measures between risk tolerance and FWB may yield different results.

The current study results also support the positive relationship between financial self-efficacy and FWB found in earlier research (Asandimitra & Kautsar, 2019; Asebedo & Payne, 2019; Gamst-Klaussen et al., 2019; Sehrawat et al., 2021). Previous studies have emphasized the importance of financial literacy/awareness as the pathway to enhanced FWB through improving financial self-efficacy (Mishra, 2022; Sehrawat et al., 2021; Shim et al., 2009; Xiao et al., 2014). However, a few studies have also demonstrated that financial education interventions to impart knowledge are not successful in inducing a behavioural change (Fernandes et al., 2014; Mandell, 2008; Willis, 2011). Such results indicate that even though financial knowledge is associated with financial behaviour, intrinsic psychological attributes, like financial self-efficacy, determine whether they bring this knowledge into practice (De Meza et al., 2008). This has been a classical behavioural change problem where improved knowledge does not always result in enhanced attitude or behaviour, for which a nudging is required. However, the current study results imply that managers cannot just rely on the financial education of their customers but need to ensure the improvement of psychological traits (like financial self-efficacy) to promote prudent financial behaviour.

A propensity for financial planning is also critical for FWB. The current study results corroborate the positive relationship between a propensity to plan and FWB (Asebedo & Payne, 2019; Lee et al., 2019; Netemeyer et al., 2017; Xiao & O’Neill, 2018). Recent investigations have corroborated the joint role of propensity to plan and financial self-efficacy in promoting long-term financial sustainability FWB in the Indian context (Sehrawat et al., 2021). Individuals who are more confident in their financial skills are more likely to engage in responsible financial practices, including higher investments, savings, retirement planning and better credit behaviour, thus paving the way to improved FWB. Under such circumstances, financial literacy efforts must improve financial self-efficacy and financial planning if they have to strengthen FWB. However, the different roles of formal financial education (school-based financial education) and family financial socialization (financial education through family and friends) in financial education need to be fully well understood (Jin & Chen, 2020). Many studies have confirmed the effectiveness of family financial socialization in improving financial outcomes. They have encouraged parents to discuss financial matters with their children at home early in life (Pandey et al., 2020; Rea et al., 2019; Zhao & Zhang, 2020). Such blending of formal and informal financial education can promote desirable psychological traits like financial self-efficacy and propensity to plan, resulting in improved FWB. Such efforts are more critical to a developing country like India, where most workers belong to the informal sector with no access to any social security measures.

Conclusion

Due to their socio-cultural differences, psychological traits and their effect on FWB in emerging countries may differ from developed countries. Although the impact of psychological characteristics on financial outcomes had been previously examined in combination or isolation, this is a maiden attempt to simultaneously explore the influence of five psychological factors on FWB from an Indian perspective, which represents a significant portion of the emerging world. Based on structural equation modelling analyses of the influence of selected psychological factors on FWB, financial self-efficacy and propensity to plan positively influenced FWB, while risk tolerance, materialism and a tendency for social comparison negatively impacted FWB. Study findings are in line with similar studies on financial outcomes, except where risk tolerance is concerned. The contrarian relationship between risk tolerance and FWB revealed in the current study is a testimony to the contextual differences. Prima facie, a higher risk appetite may provide higher returns resulting in improvement of FWB and life satisfaction. However, the relationship might be more complex and the relationship between materialism-risk tolerance-financial satisfaction might not be linear and may be highly contextual. Future research should consider longitudinal data to uncover the dynamic nature of FWB–risk tolerance–materialism relations.

Research findings from this study contribute to the existing academic discourse on FWB, a major national and global concern. This study extends the research work on predictors of FWB. It establishes psychological traits, such as financial self-efficacy, the propensity to plan, risk tolerance, materialism and tendency for social comparison as crucial antecedents of FWB. The findings of this study provide several practical implications for financial educators, financial institutes and policymakers in enhancing financial behaviour and FWB by influencing the five psychological traits. The study emphasizes the need to develop financial literacy strategies that directly impact one’s innate psychological factors to improve their financial future. The study results indicate that improving financial self-efficacy and planning through appropriate financial education can promote FWB. Financial education should also aim to reduce risk tolerance, materialistic tendencies and the tendency for social comparison, if it needs to improve FWB. These three psychological variables negatively correlate to FWB and thus need to be reduced through appropriate education and moral suasion to promote well-being. Financial institutes and advisory firms can develop customized products and strategies based on the insights from this study to help their clients make better financial decisions and choices.

Yet another implication of the current study results may be its usefulness in developing financial education solutions for customers, primarily gamification. Gamified apps for personal financial management can provide the opportunity to learn and experience similar financial situations through ‘learning by doing’ and enhancing one’s confidence through that experience. This is in line with several recent research findings (Bitrián et al., 2021; Meneau & Moorthy, 2021). The study results also find applications in promoting financial and social well-being among Indians. Though a welfare state according to the constitution, India is far from achieving universal social security, unlike the developed nations. Thus, promoting prudent financial behaviour among the public helps promote financial safety and well-being. Such behaviour can become an adjunct to the government’s efforts to provide universal public welfare.

The main limitation of this study is that it investigates only subjective FWB. To develop a holistic understanding of the subject, objective indicators of FWB like the actual amount of savings, wealth, debt and so forth, should also be considered. Combining objective and subjective measures helps achieve different objectives in understanding happiness and well-being in societies (Brulé & Maggino, 2017; Maggino, 2009). The current study is also limited by the method biases inherent in single method research. Though the researchers have taken steps to minimize such biases, they cannot be completely ruled out. Thus, there is an opportunity for future researchers to use mixed-method approach to improve the reliability and validity of such research findings. Mixed-method approach combines theories, methods or observers in research. For example, future research can triangulate the findings by combining the survey methods with the survey participant’s investment portfolio analysis. Future researchers can also consider exploring the differences in psychological traits among different age cohorts, life stages and genders. These demographic factors are essential in shaping one’s personality and should be considered in conjunction with personal traits while assessing FWB. The generational shift in financial behaviour and its effects on FWB can also be investigated. The role of values, attitudes and expectations on financial behaviour and its impact on FWB is also plausible for future investigation.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Ethical Approval

All procedures performed in studies involving human participants were in accordance with the ethical standards of the institutional and/or national research committee.

Informed Consent

Informed consent was obtained from all individual participants included in the study.