Abstract

Executive Summary

Financial risk tolerance (FRT) refers to the retail investors’ willingness to accept the negative changes in the value of investment or an outcome that is adversely different from the expected one. Understanding and assessing FRT plays a crucial role in individual choices about wealth accumulation, portfolio allocation, and all other investment and finance-related decisions, and in achieving financial goals. An advisor has to accurately assess FRT for achieving his/her goal or investor’s goal. Failure to do so leads to the choice of an investment option/portfolio which is inconsistent with one’s FRT, resulting in investor disappointment, that is, unbearable loss to the client. Such a situation may adversely affect the client–advisor relationship.

Measuring FRT is challenging as it is a multidimensional attitude. Besides, it is an elusive concept that appears to be influenced by a number of predisposing factors such as demographic, environmental, and psychosocial factors. This study aims to identify the factors that are related to risk tolerance from outside the financial services domain such as psychology, economics, and bio-sociology. It deals most specifically with the relationship between biopsychosocial factors and FRT. Those who are interested in assessing and predicting FRT can move closer to a theoretical account that blends psychological and economic insights and supplements the understanding of risk-taking attitudes and behaviour of retail investors. Such an understanding will help financial advisors, policy makers, and researchers in identifying the determinants of an individual’s FRT to suggest the suitable investment alternatives to their clients.

A single cross-sectional survey was conducted among 951 retail investors with various levels of investment experience through a structured questionnaire covering a variety of demographic factors. An analysis of the data collected through the questionnaire indicates that all the three factors—self-esteem, personality type, and sensation seeking—are positively related to FRT. This study adds to the extant literature on psychological determinants of FRT.

Any financial and investment decision-making process requires four fundamental inputs, namely goals, time horizon, financial stability, and financial risk tolerance (Garman & Forgue, 2011). While the first three inputs are relatively more objective in nature, financial risk tolerance (FRT) is highly subjective (Larkin, Lucey, & Mulholland, 2013). FRT refers to the retail investors’ willingness to accept the negative changes in the value of investment or an outcome that is adversely different from the expected one (Grable & Lytton, 1999).

Understanding and assessing FRT plays a crucial role in individual choices about wealth accumulation, portfolio allocation, and all other investment and finance-related decisions (Hanna, Gutter, & Fan, 2001) and in achieving financial goals. An advisor has to accurately assess FRT for achieving his/her goal or the investor’s goal. This is possible only if the advisor personally knows the client, for example, high-net-worth individual (HNWI) investors, but it is challenging for them while considering mass markets of small investors (Ardehali, Paradi, & Asmild, 2005). Nevertheless, it is important to measure FRT at best. Failure to do so leads to the choice of an investment option/portfolio which is inconsistent with one’s FRT resulting in investor disappointment, that is, unbearable loss to the client (Droms, 1987). Such a situation may adversely affect the client–advisor relationship (Larkin et al., 2013). In addition, it leads to an unfavourable impact on the advisor’s career and exposes him to litigation, arbitration, and legal jeopardy (Grable, Roszkowski, Joo, O’Neill, & Lytton, 2009). This problem could be minimized by an investor himself/herself measuring his/her FRT instead of FRT being measured by others (i.e., advisors) as there is a strong relationship between investment behaviour of an individual and his/her FRT (Bailey & Kinerson, 2005; Schooley & Worden, 1996).

Understanding the significance of measuring FRT correctly, financial advisors have been giving importance to the behavioural aspects of an investor while measuring FRT. Measuring FRT is challenging as it is a multidimensional attitude. Besides, it is an elusive concept that appears to be influenced by a number of predisposing factors (Trone, Allbright, & Taylor, 1996) such as demographic, environmental, and psychosocial factors. The extant literature shows that among all the factors, demographic characteristics are the most widely investigated determinants of FRT (e.g., Grable & Lytton, 1999; Grable, 1997; Moreschi, 2011; Wang & Hanna, 1998). In addition, demographic characteristics could be used to differentiate retail investors in terms of FRT and classify them into different FRT categories (Grable & Lytton, 1999). Nevertheless, there are several other variables that may also be important determinants of FRT, for example, personality (a psychological factor) and genetics (a biological factor) of an individual.

Despite the importance of FRT in financial and investment decision-making, specific theory related to the assessment and prediction of FRT is very limited (Hanna, Gutter, & Fan, 1998), but theories related to non-financial decisions (i.e., use of drug and alcohol) widely exist. For example, risk attitudes and behaviours of an adolescent on the basis of predisposing factors were investigated by Irwin Jr (1993). He classified these factors into two categories, namely environmental factors and biopsychosocial factors. Environmental factors included family situation, socioeconomic status, and social transitions. Biopsychosocial factors included birth order, gender, personality traits, age, and ethnicity. As stated above, the relationship between biopsychosocial factors and FRT is a relatively unexplored area as compared to demographic factors. One such important study was conducted by Grable and Joo (2004). They adapted and expanded Irwin’s framework and tested it using predisposing factors as determinants of FRT of faculty and staff of two universities. They found a significant association between biopsychosocial factors and FRT. With respect to psychological factors, extant literature shows that personality (Carducci & Wong, 1998; Grable & Joo, 2004; Mayfield, Perdue, & Wooten, 2008), sensation seeking (Zuckerman, 1994; Carducci & Wong, 1998; Grable & Joo, 2004), and self-esteem (Cohen, 2001; Grable & Joo, 2004) have a consistent positive relationship with FRT.

As FRT is dynamic in nature, it changes over time. In addition, FRT is influenced by life experiences (Van de Venter, 2006). In the recent past, experiences of retail investors were severely affected by various financial crises. For instance, the recent Greek crisis followed by global meltdown has increased the financial vulnerability of institutions as well as individuals. Individuals rather than institutions have mostly experienced the adverse impact of financial vulnerability by losing their investments and jobs and facing salary cuts (Bricker, Bucks, Kennickell, Mach, & Moore, 2011). Such scenario changes may or may not pull down the risk appetite of the financial advisors and investors. This emphasizes the need for continuous assessment and accurate measurement of FRT to achieve the desired results (Yao, Sharpe, & Wang, 2011).

CONTRIBUTION OF THE STUDY

There is no specific theory on the role of biopsychosocial factors in the financial services domain. This study aims to identify the factors that are related to risk tolerance from outside the financial services domain such as psychology, economics, and bio-sociology. It deals most specifically with the relationship between biopsychosocial factors and FRT. This study is expected to add value to the existing literature in a meaningful way. Moreover, those who are interested in assessing and predicting FRT can move closer to a theoretical account that blends psychological and economic insights and supplements the understanding of risk-taking attitudes and behaviour of retail investors. Such an understanding will help financial advisors, policy makers, and researchers in identifying the determinants of an individual’s FRT to suggest the suitable investment alternatives to their clients.

LITERATURE REVIEW

Over the past three decades, capital market in India has undergone various structural changes. A wide variety of investment options has been thrown open to the investors’ community. With the proliferation of investment options, the retail investors’ community has grown significantly in the recent years. The retail investors may choose from a number of investment options according to the level of FRT. Since then, financial advisors, policy makers, and researchers have shown their keen interest in identifying the determinants of an individual’s FRT to suggest the suitable investment alternatives to their clients. A number of studies have investigated the role of demographic factors as a determinant of FRT (Grable & Joo, 1999; Grable & Lytton, 1999; Grable, 1997; Grable, McGill, & Britt, 2011; Kannadhasan, 2006, 2015; Larkin et al., 2013; Moreschi, 2011; Ryack, 2011; Sung & Hanna, 1996; Wang & Hanna, 1998; Yao & Hanna, 2005). However, there are other determinants such as financial considerations, that is, the need for financial liquidity and income security and personal considerations (Boone & Kurtz, 1989; Widicus & Stitzel, 1989). There is no specific theory on the role of biopsychosocial factors in the financial services domain. Therefore, this section discusses some of the most important factors that are related to risk tolerance from outside the financial services domain such as psychology, economics, and bio-sociology.

Relationship between Self-Esteem and FRT

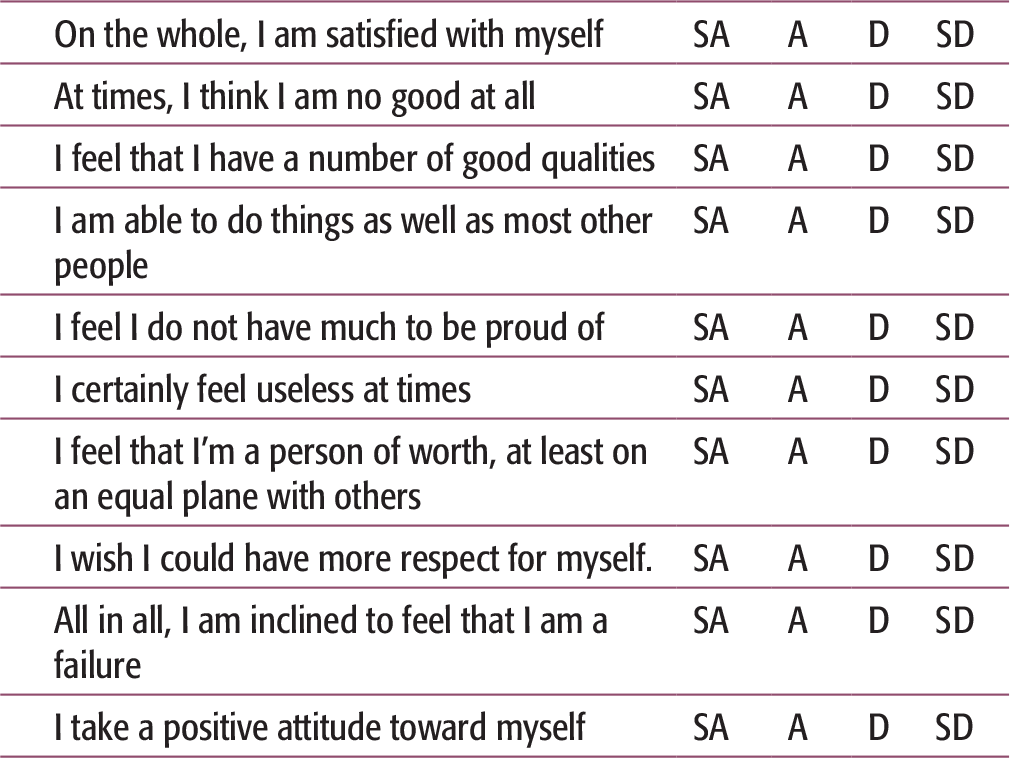

Self-esteem is an important personality trait and acknowledged as a multidimensional trait as it encompasses several characteristics such as goodness, skill and social competence, health, and worth (Baumeister, Campbell, Krueger, & Vohs, 2003; Liao, Hunter, & Weinman, 1995). It can be defined as ‘the perception of self-worth, or the extent to which a person values, prizes, or appreciates the self’ (Blascovich & Tomaka, 1991). Self-esteem could be either positive or negative and represents a favourable or unfavourable attitude towards self (Rosenberg, 1965). An individual, who possesses positive self-esteem, tends to take a higher risk than those who have negative self-esteem (Arch, 1993; Krueger, & Dickson, 1994). As the outcome of any investment decision will be known only in the future, investors have necessarily to deal with the uncertainty associated with their investment choice, which leads to some level of anxiety, thereby, affecting their level of self-esteem (Taylor, 1974). For instance, individuals who have higher self-esteem are likely to be higher achievers in all endeavours than those who have lower self-esteem, because their performance should be consistent with their perceived self-image (Korman, 1976). Similarly, the driving force behind individuals’ pursuit of wealth creation by choosing risky instruments is to maintain their economic status, which is consistent with their perceived self-worth (Bragues, 2005).

Self-esteem affects one’s portfolio allocation, wealth creation, and trading behaviour (Chatterjee, Finke, & Harness, 2009). Retail investors, who have a higher level of self-esteem, are able to cope with anxiety of experiencing losses, willing to invest in risky financial instruments as well as instruments with which they do have little knowledge, willingness to trade the instruments that have poor performance, and so on (Chatterjee et al., 2009). Individuals who have higher self-esteem never regret even when they make bad investments, that is, investing in under-performing investments as it lowers their self-esteem (Arkes & Blumer, 1985). Similarly, they are unwilling to admit their investment failure, that is, ‘sell the stock/portfolio that had generated a small loss than a stock/portfolio that had experienced a more serious loss’ (Tykocinski, Israel, & Pittman, 2004). When considering demographic factors, it is observed that men with a positive self-esteem would trade more excessively than women with a higher self-esteem and under-perform in investments (Barber & Odean, 2001). Women are more pessimistic than men and attempt to mitigate the drop in their own self-esteem in the event of investment failure (Mansour, Jouini, & Napp, 2006). Individuals with positive self-esteem exhibit their willingness to seek financial knowledge and financial advice (Joo & Grable, 2001). Having financial education/knowledge would help individuals to know their financial situation and control their financial situation as desired by themselves (Hogarth, Swenson, Gutenson, & Nichols, 1995). Controlling these demographic factors such as gender, education, age, income, net worth, and financial knowledge, several studies have found that self-esteem is a significant as well as a positive predictor of FRT (Cohen, 2001; Grable, Britt, & Webb, 2008; Grable & Joo, 2004;). Therefore, it is expected that:

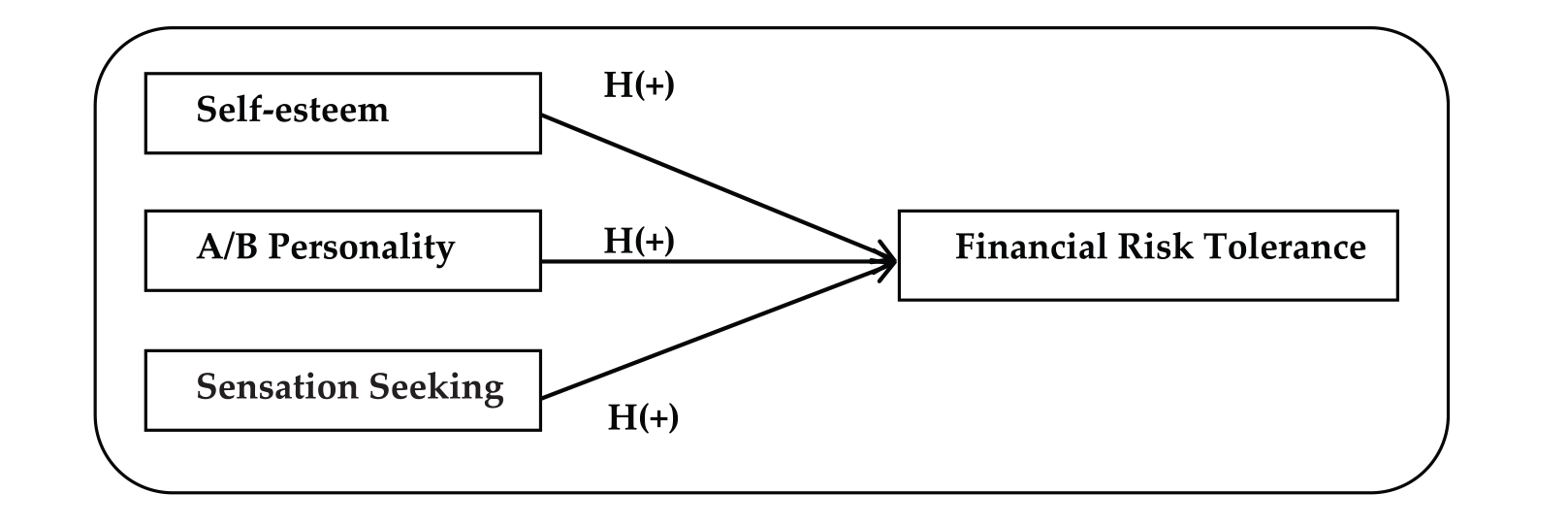

H1: Self-esteem is positively related to FRT.

Relationship between Personality and FRT

The internal (psychological) and external environment affects an individual’s human behaviour (Endler & Edwards, 1986) and thereby his decisions. Personality type plays a significant role in determining investor behaviour (Maital, Filer, & Simon, 1986; Sadi, Asl, Rostami, Gholipour, & Gholipour, 2011). According to Myers–Briggs Type Indicator (MBTI) personality theory, every person has inborn preferences that define how he or she will behave in a certain situation (Pittenger, 1993). Pompian and Longo (2004) suggested that investment advisors must consider an investor’s personality type in client profiling. Further, they can use it for suggesting suitable investment options (Pompian & Longo, 2004). For instance, retail investors can be grouped into two groups, viz., passive or active to help investment advisers to understand the nature of their clients and suggest suitable options (Barnewall, 1987). Typically, passive investors are those who earn money without putting a great effort and earn wealth by risking the capital of others. Conversely, active investors like to earn wealth by risking their own capital. In simple words, active investors have more tolerance for risk than passive investors (Barnewall, 1987). Previous studies have investigated the relationship between personality traits and investment decisions and found a relationship between personality and FRT (Barnewall, 1987; Bashir, Azam, Butt, Javed, & Tanvir, 2013; Carducci & Wong, 1998; Droms, 1987; Eaker & Castelli, 1988; Grable & Joo, 2004; Grable et al., 2008; Mayfield et al., 2008; Pittenger, 1993; Pompian & Longo, 2004; Price, 1982; Thoresen & Low, 1990; Zuckerman & Kuhlman, 2000).

There are many ways of classifying people’s personalities such as the five-way model, MBTI, and Type A/B traits method. In this study, Type A/B traits method is used to measure the retail investor’s personality. Type A personality generally refers to the individuals, who are competitive, with an underlying tendency for hostility and aggressiveness, a sense of time urgency and impatience (Grable, 2000; Strube, 1991; Thoresen & Low, 1990). Conversely, Type B refers to the individuals who are a contrast to those with Type A personality. Individuals with Type A personality trait tend to take greater risks than those more closely aligned with the Type B personality profile (Carducci & Wong, 1998). In addition, Type A individuals tend to pursue tangible accomplishments as a measure of one’s well-being/worth because the society values only material success. In this pursuit, they try to achieve more material success than others (Type B individuals) with less concern for one’s perceived personal limits (Price, 1982). Type A individuals are more financial risk tolerant than Type B individuals as they are associated with higher levels of income (Thoresen & Low, 1990) and higher level of education, financial knowledge, and occupational status (Carducci & Wong, 1998; Grable, 2000). For instance, a higher level of income gives a kind of financial security and makes it possible for Type A individuals to take greater financial risks than Type B individuals (Carducci & Wong, 1998). Very few studies have examined the relationship between personality and FRT by classifying investors into Type A/B category. A few studies have found that Type A individuals tend to be more risk tolerant than Type B individuals (Carducci & Wong, 1998; Grable & Joo, 2004). It is expected that:

H2: Type A investors have more Financial Risk Tolerance than Type B investors.

Relationship between Sensation Seeking (SS) and FRT

Sensation seeking is yet another important trait which is consistently related with FRT (Wong & Carducci, 1991). Sensation seeking is defined as ‘the seeking of varied, novel, complex, and intense sensations and experiences, and the willingness to take physical risks for the sake of such experiences’ (Zuckerman, 1994). In simple words, this type of behaviour is ‘due to the biochemical reactions in the brain’ (Larsen & Buss, 2008). Typically, an individual who has higher sensation seeking accepts risk as a possible outcome for attaining the desired level of excitement and stimulation (Zuckerman & Kuhlman, 1978). Such an individual tends to bet high and at higher odds in gambling for increasing the level of arousal (Anderson & Brown, 1984). This trait relates to the behavioural expressions that are generally described as risky such as high-risk sports, gambling, substance usage, risky sexual experiences, alcohol use, holiday preferences (Roberti, 2004; Zuckerman, 1979; Zumdick, 2007). Individuals with such a trait also exhibit a propensity to make risky financial investments (Harlow & Brown, 1990). A few studies have investigated the relationship of sensation seeking with financial management behaviour, especially the use of credit card in particular (e.g., Henry, Weber, & Yarbrough, 2001; Miller, 2001; Popham, Kennison, & Bradley, 2011; Worthy, Jonkman, & Blinn-Pike, 2010). They found that students exhibited risky financial behaviour such as accumulating more debt, overdrawing their accounts, borrowing money from their friends to pay their bills and so on. Nevertheless, a very limited number of studies explored the relationship between sensation seeking and FRT. Carducci and Wong (1991) concluded that higher sensation seekers would exhibit greater financial risk-taking tendencies. Further, they stated that men engaged in financial risk-taking more than women. In the similar line, the general trait of sensation seeking has some predictive value for financial risk behaviour (Grable & Joo, 2004; Horvath & Zuckerman, 1993). Therefore, it is expected that:

H3: Sensation Seeking is positively related to FRT.

RESEARCH MODEL

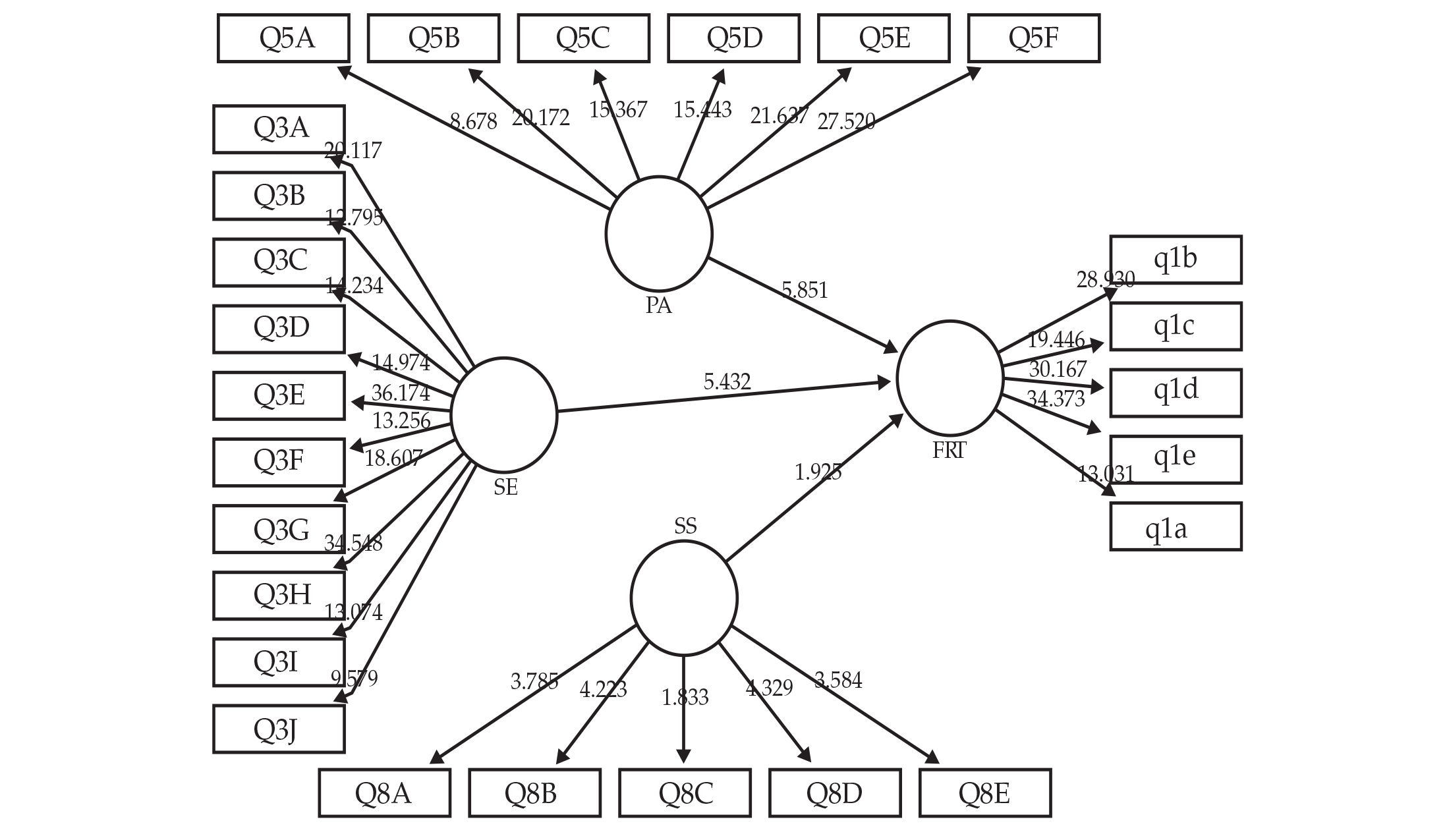

This article has conceptualized the research model with the help of extant literature (Figure 1). The proposed relationships were examined using Partial Least Square-Path Modelling (PLS-PM).

Methodology

Procedure and Sample

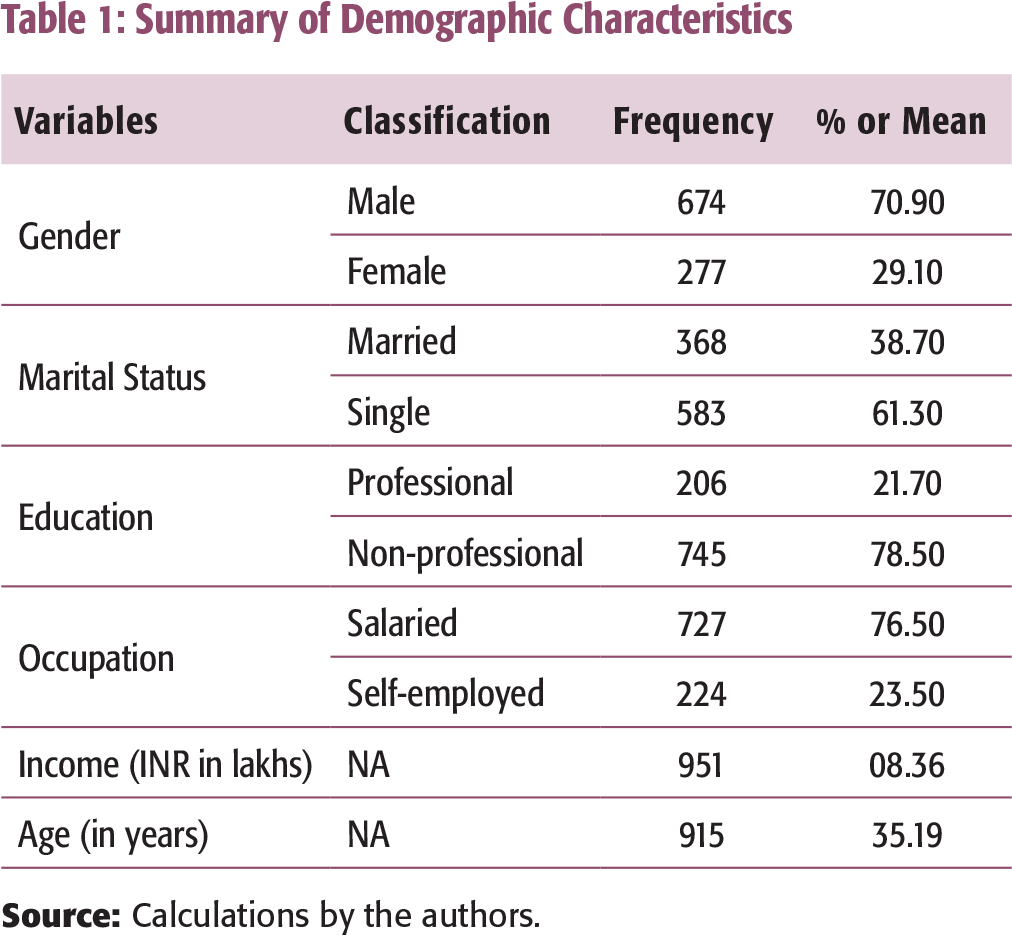

Summary of Demographic Characteristics

Measurement

Dependent Variable

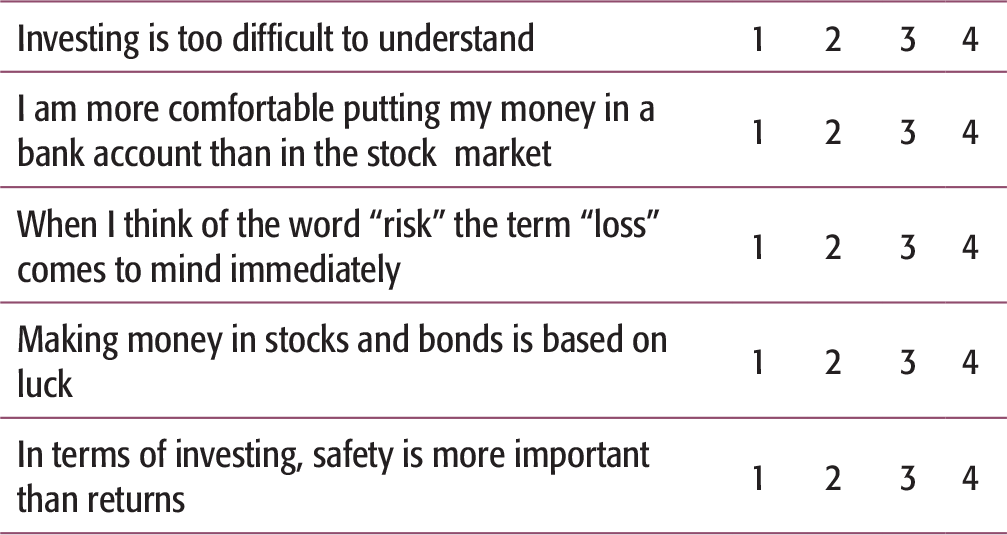

Assessment of the client’s risk preferences has now become an essential step in developing investment policy statement (IPS). It has also become essential to document the same prior to making an investment and subsequent financial planning recommendations to the clients. Despite the importance of FRT in making optimal financial decisions (Moreschi, 2004), the regulators of the financial market have not yet defined the term explicitly (Roszkowski, Davey, & Grable, 2005), and hence, FRT has been measured in diverse ways in practice (Van de Venter, 2006). For instance, some financial advisors measure FRT using proxies—either demographic characteristics or qualitative heuristics or combination of the both. Others use psychometrically designed FRT scales (Grable et al., 2009). Anecdotal evidence suggests that using the psychometric scale would exhibit FRT relatively better than the demographic factors. In addition, financial advisers are warned about the potential dangers of using single items of any sort (Callan & Johnson, 2002). Therefore, it was suggested that assessing FRT using multi-items as well as psychometrically designed scale with an appropriate level of reliability and validity would be better (Callan & Johnson, 2002; Corter & Chen, 2006; Roszkowski et al., 2005;). This study preferred to use such a scale for measuring FRT. Measuring one’s FRT could be done by advisors or oneself. However, it was suggested that individuals could best measure their FRT more accurately than the advisors (Hallahan, Faff, & McKenzie, 2004). In addition, investment behaviour of an individual reflects the level of one’s FRT which is measured by him/her, that is, self-assessment (Bailey & Kinerson, 2005; Schooley & Worden, 1996). Therefore, this study used a self-type measurement of FRT using five items on a 4-point scale that was developed by the researchers based on four risk assessment concepts as suggested by Maccrimmon and Wehrung (1986) and tested by Grable and Joo (2004). Responses are coded as 1, 2, 3, and 4 for strongly agree, tend to agree, tend to disagree, and strongly disagree respectively. Higher scores indicate higher FRT and vice versa.

Independent Variables

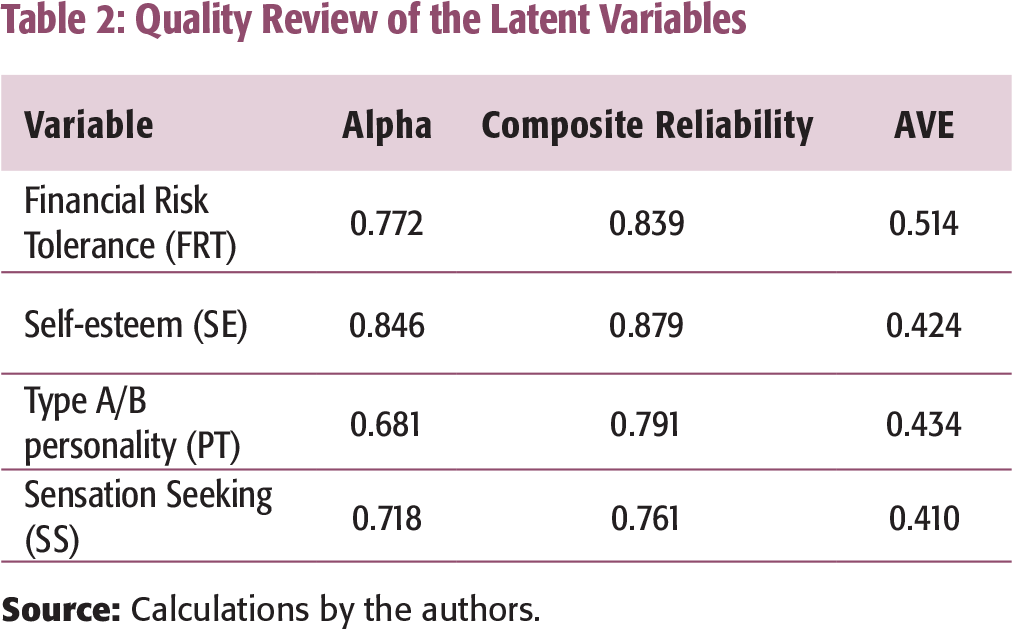

Quality Review of the Latent Variables

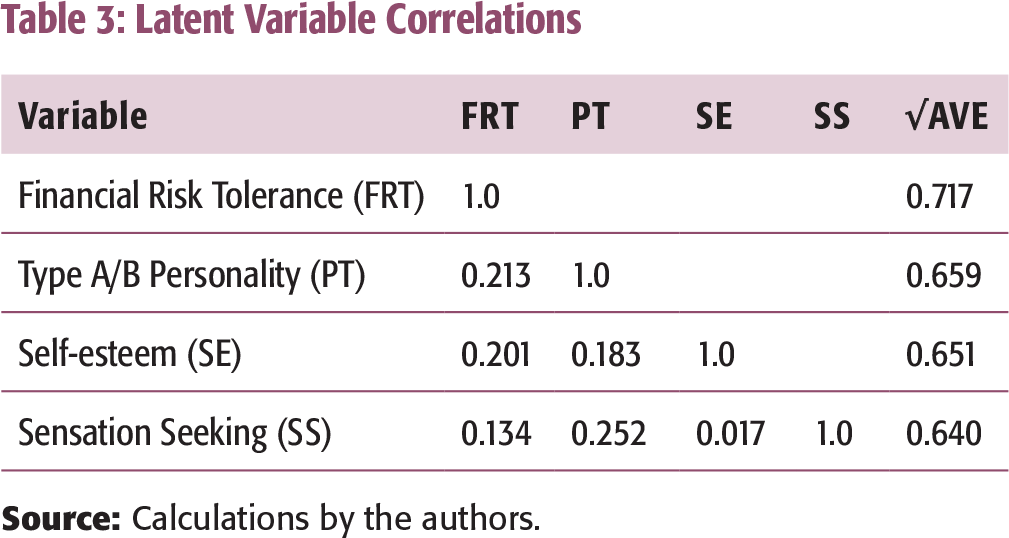

Latent Variable Correlations

Tools

The study used Partial Least Squares (PLS) approach to structural equation modelling (PLS-SEM) to examine the relationship of biopsychosocial factors with FRT using Smart PLS Software. In addition, the study estimated the Global Fit measures for path modelling to validate the model globally.

RESULTS

Descriptive Statistics

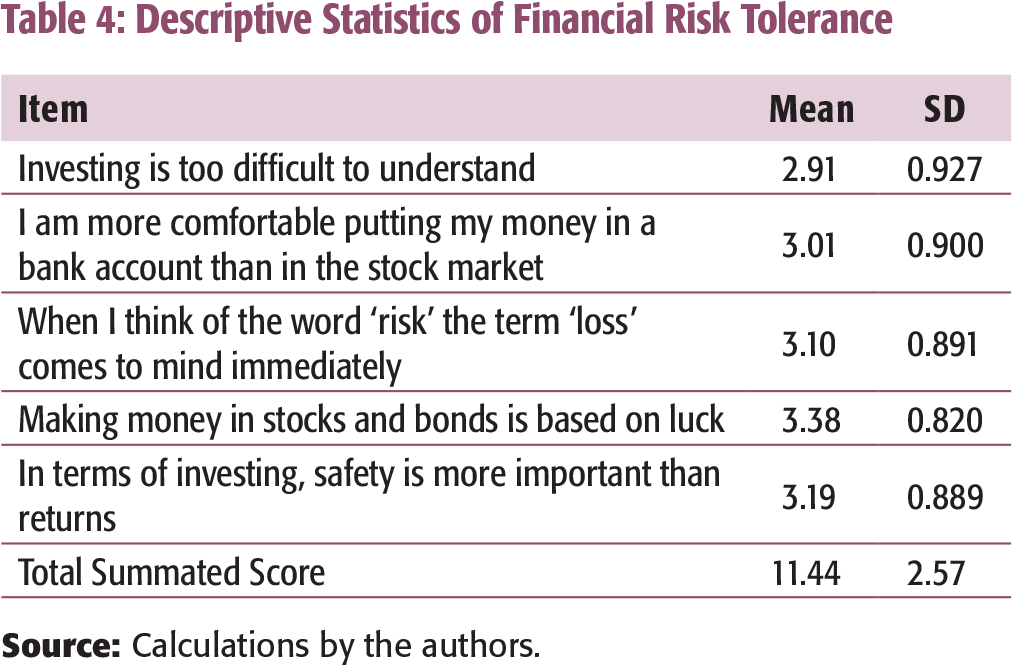

Descriptive Statistics of Financial Risk Tolerance

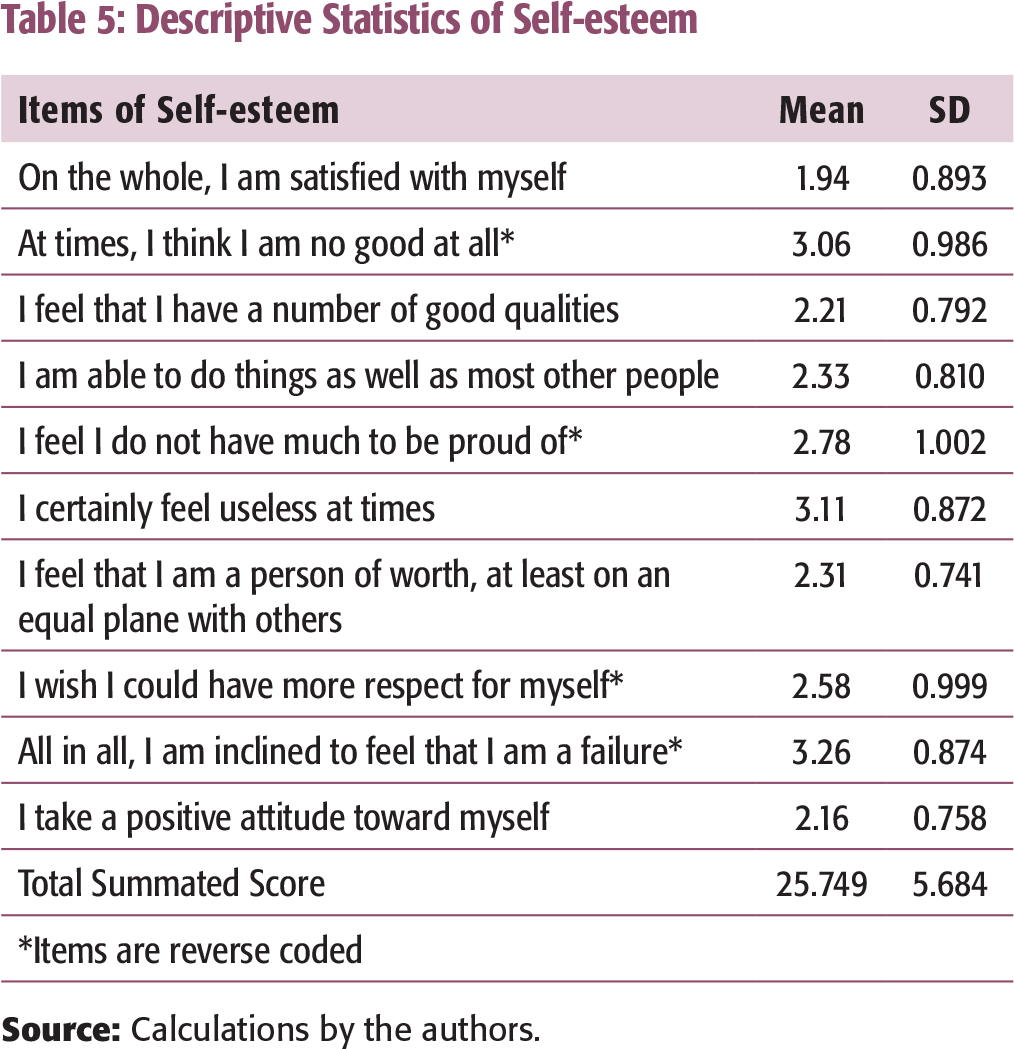

Descriptive Statistics of Self-esteem

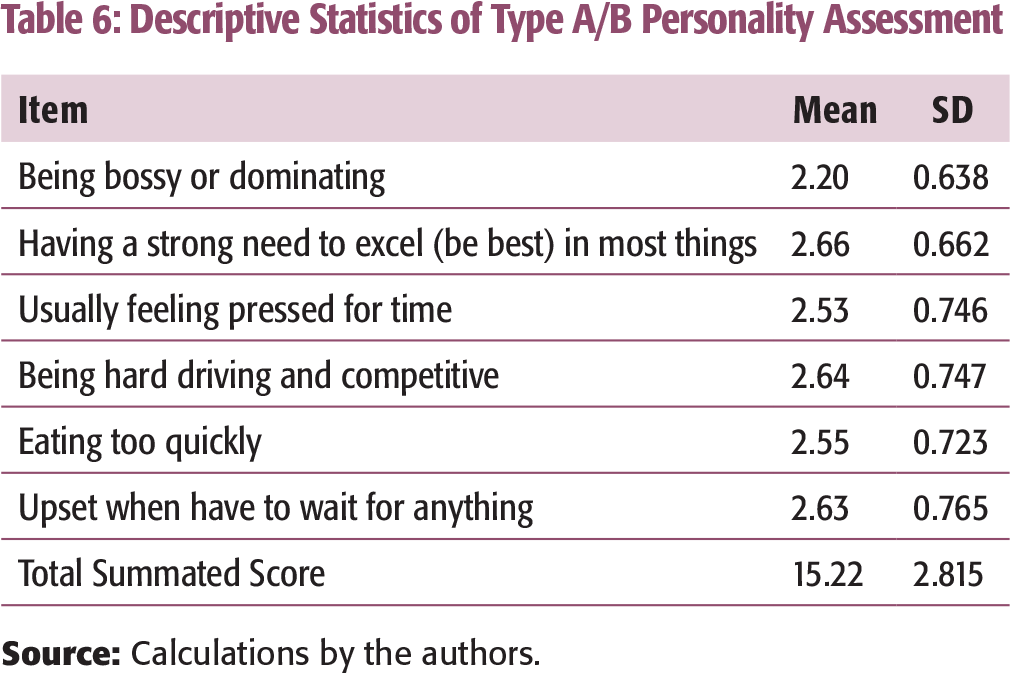

Descriptive Statistics of Type A/B Personality Assessment

Table 6 shows the summated score of each item as well as the total summated score of Personality type. The average summated score of personality type is 15.22, with an SD of 2.82 (refer to Table 6). A higher score indicates a greater likelihood of exhibiting Type A personality traits.

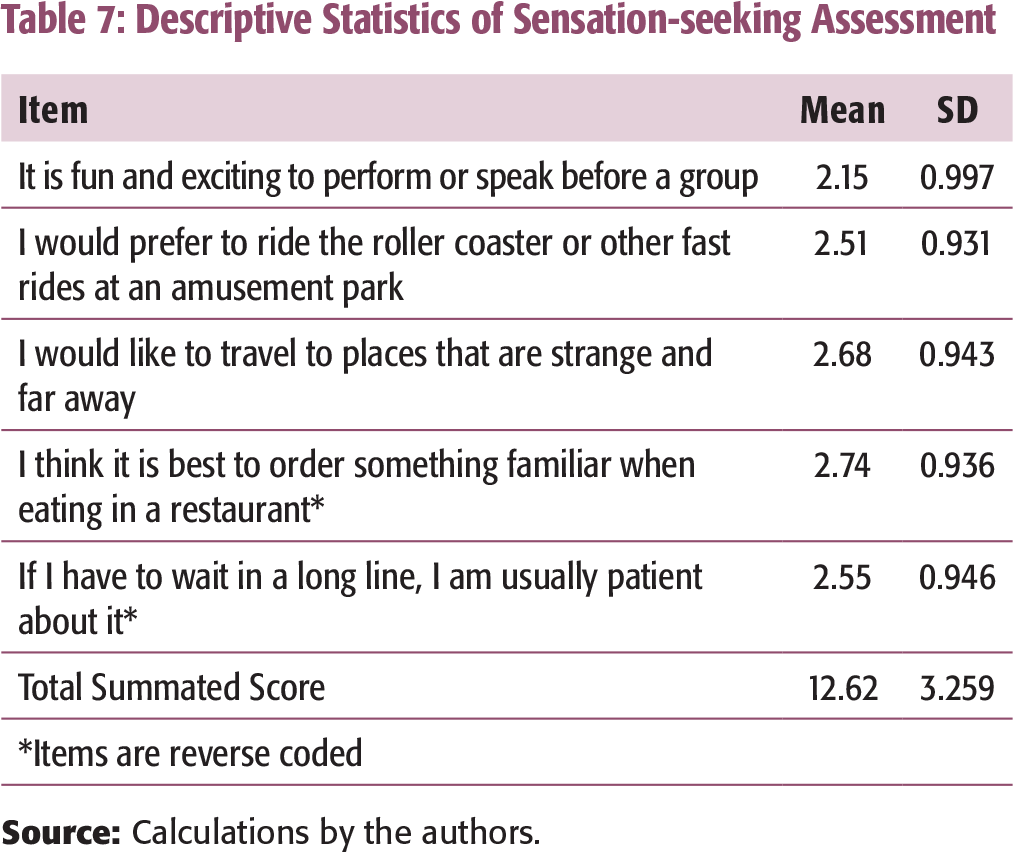

Descriptive Statistics of Sensation Seeking Assessment

Structural Model Results

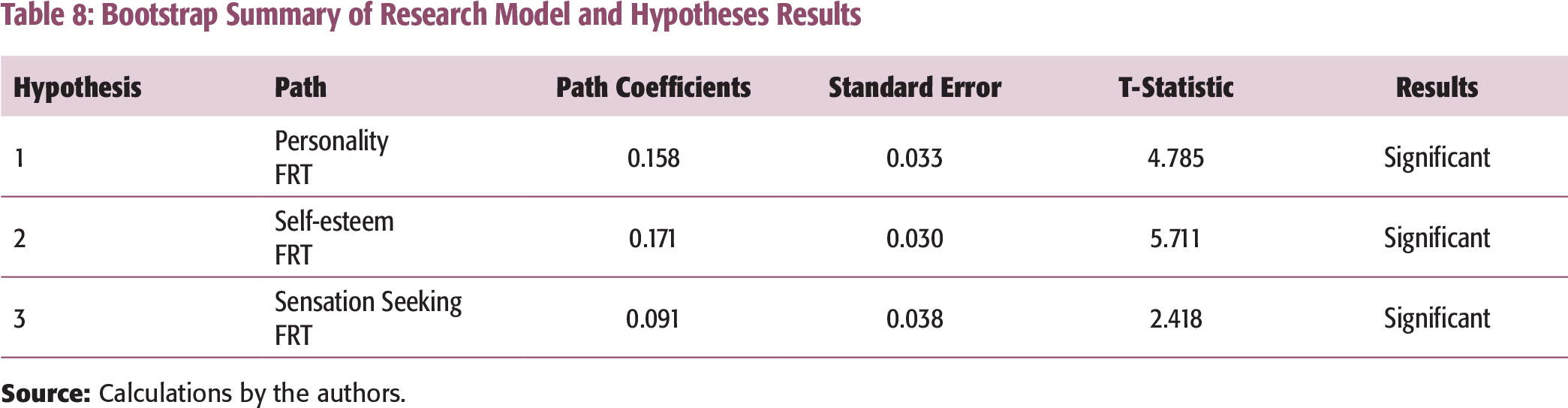

The study used PLS-SEM to examine the relationship between biopsychosocial factors and FRT. PLS-PM is a variance-based approach for assessing the interrelations of all the constructs simultaneously (Chin, 1998). In addition, PLS makes no assumptions on distributional requirements. The structural model was evaluated using the R-square for the dependent constructs and the size, t-statistics, and significance for the path coefficients. Path coefficients in PLS are standardized regression coefficients (Staples, Hulland, & Higgins, 1998). In order to assess whether path coefficients are statistically significant or not, bootstrap procedures are used to estimate standard errors for calculating t-values (Fornell & Barclay, 1983). The results are examined at 5 per cent significance level and the t-statistic value at the 0.05 level is 1.96. If the t-statistic value is greater than 1.96, the path is significant (Efron, 1979; Efron & Gong, 1983). Results from PLS-PM are given in Table 8 and Figure 2. Three variables namely self-esteem, personality type, and sensation seeking are positively related with FRT. In addition, these relationships are statistically significant at 5 per cent level.

Analysis of Global Fit Measures

The study also conducted Global Fit (GoF) measure for path modelling (Tenenhaus, Vinzi, Chatelin, & Lauro, 2005) as it may serve as a cut-off value for global validation (Wetzels, Odekerken-Schroder, & Van Oppen, 2009). GoF is defined as the geometric mean of the AVE and average R2. The GoF value of this study is 0.1983, that is, 19.83 per cent for the complete model that exceeds the small effect size of R2. This model has reasonable explaining power in comparison with the baseline values of explaining power (GoFsmall = 0.1, GoFmedium = 0.25, and GoFlarge = 0.36). Therefore, this study concludes that the model has adequate support to validate the PLS model globally (Wetzels et al., 2009).

DISCUSSION

Bootstrap Summary of Research Model and Hypotheses Results

Personality type is another significant predictor of FRT. The results are similar to those of Carducci and Wong (1998) and in contrast to those of Grable and Joo (2004). Individuals who belong to Personality Type A category are usually competitive in nature and are always concerned about their personal achievement (Ray & Bozek, 1980). Such individualities not only bring recognition for the community (Houston & Snyder, 1988), but also mediate willingness of the individuals to take risk (Carducci & Wong, 1998). ‘As financial success is proportional, to some degree, to financial risk taken, Type A individuals would be more willing to take greater financial risks to achieve financial success and the recognition such success would bring’ (Carducci & Wong, 1998). In addition, Type A individuals usually have higher income level than Type B individuals (Thoresen & Low, 1990), which is another reason for having more FRT. However, individuals/advisors need to evaluate their financial security status carefully because overstating one’s position motivates one to choose risky financial investment options, thereby destroying one’s wealth. Advisors need to recognize the consciousness of personality in terms of their managing ability in relation to financial and investment decisions because it is related to the way individuals think and act in the environment. Mismatching the personality and investment options would destroy the wealth of one’s clients. Another trait dealt in this study is sensation seeking. This study finds that individuals with a higher level of sensation seeking tend to take more financial risk. This finding is similar to that of Carducci and Wong (1991) and in contrast to Grable and Joo (2004). Individuals who have a higher sensation seeking exhibit a propensity to make risky financial investments.

Thus, the results of the study confirm the proposition made by Irwin (1993) with regard to determinants of FRT, biopsychosocial factors in particular. As hypothesized, this study finds that the biopsychosocial factors are positively associated with FRT. It indicates that an investor who has a higher level of sensation seeking and self-esteem and has Type A personality tends to be more risk-tolerant.

SUMMARY

The most prudent approach to asset allocation is to assess and integrate two types of information, namely, the capital market-related factors and the investors’ FRT. In real life, the self-perceived FRT might be different from the objective measurement of FRT as the objective measurement of FRT varies with age. It is plausible that an individual’s subjective (psychometric measurement) FRT does not change with age (Hanna & Chen, 1997). In recent years, financial planners have often preferred to use psychometric assessment of FRT to provide better services to the clients. This motivates the researchers to explore the relationship between biopsychosocial factors and FRT to identify the factors that determine FRT. To achieve this objective, this study used three biopsychosocial factors namely self-esteem, personality type, and sensation seeking. Findings of the study suggest that biopsychosocial factors are related to FRT. This study suggests to the practitioners, financial planners, and policy makers that consideration of these three factors would enhance the understanding of the client in a better manner rather than relying on only demographic factors. However, use of demographic variables and contextual variables along with biopsychosocial variables is suggested. It is because a small variation in any factor would be useful in preventing the wrong asset allocation decisions.

IMPLICATIONS

Incorrect measurement of FRT may lead to the choice of incorrect investment options, which in turn may lead to the diminution in the wealth and welfare of investors As a result one may sell a good investment or invest in an incorrect portfolio, which are not good for financial service providers. It will affect their credibility and reputation and result in loss of customers, and so on.

SCOPE FOR FURTHER RESEARCH

A further research could consider other variables such as racial background, financial satisfaction, net-worth, home ownership, birth order, age, gender, education, marital status, family relationship, the number of dependents, and income along with the biopsychosocial factors. Future research could also consider financial knowledge, financial satisfaction, and income level because knowledgeable individuals who possess a higher level of income and education have a greater FRT as pointed out by Grable & and Joo (2004).

APPENDIX

Research Questionnaire

1. Indicate your agreeableness on the following on a five-point scale (where 1 - Strongly agree, 2 - Tend to agree, 3 - Tend to disagree, 4 - Strongly disagree)

2. Below is a list of statements dealing with your general feelings about yourself on a five-point scale. (where

3. Indicate your agreeableness on the following on a five-point scale (where 5 - Strongly agree, 4 - Agree, 3 - Neutral, 2 - Disagree, 1 - Strongly disagree)

5. Indicate your response on the following on a four point scale that best describes your willingness to engage in sensation seeking behaviours (where 1 - not at all, 2 - Somewhat, 3 - Fairly well, 1 - Very well)

Personal Profile

1. Gender ☐ Male ☐ Female

2. Marital Status ☐ Married ☐ Single ☐ Divorced

3. Educational Qualification ☐ School Level ☐ Under Graduate

☐ Post Graduate ☐ Professional

☐Others (Please Specify) _____________________

4. Age (in Years) _______________________________

5. Occupation ☐ Private sector ☐ Public sector

☐ Self Employed ☐ Professional

☐ Retired

☐Others (Please Specify) _____________________

6. No. of Family Members ☐ Two ☐ Three

☐ Four ☐ Five

☐ More than 5

7. State your domicile ☐ Rural ☐ Urban ☐ Semi urban

8. Annual household Income (rupees in lakhs) ______________________________

9. Annual Savings ☐ Below 100,000

☐ Between 1, 00,001 and 1, 50,000

☐ Between 1, 50,001 and 200,000

☐ Between 2, 00,001 and 2, 51,000

☐ Above 2, 51,001