Abstract

Generally, corporate governance research has been considered the preserve of economics, accounting, and finance scholars. However, attempts are being made to apply behavioral science knowledge in this domain that has traditionally been considered economics and finance. The purpose of this article is to further the efforts in establishing a tradition of behavioral science research in corporate governance. To accomplish this objective, the article establishes the gaps in the extant literature on corporate governance. The article argues from theoretical insights emanating from organizational psychology in particular and behavioral sciences in general. As a result, this article attempts to apply some of the existing theories in social and organizational psychology to explain factors influencing the performance of non-executive directors on boards as well as executive performance and remuneration. Principally, we utilized theories of motivation (expectancy and equity theories) and social influence theory (conformity) to highlight the potential contributions that the psychology of corporate governance can make to advance knowledge and practice. Further, applications and practical ways of testing derived assumptions are also discussed.

Introduction

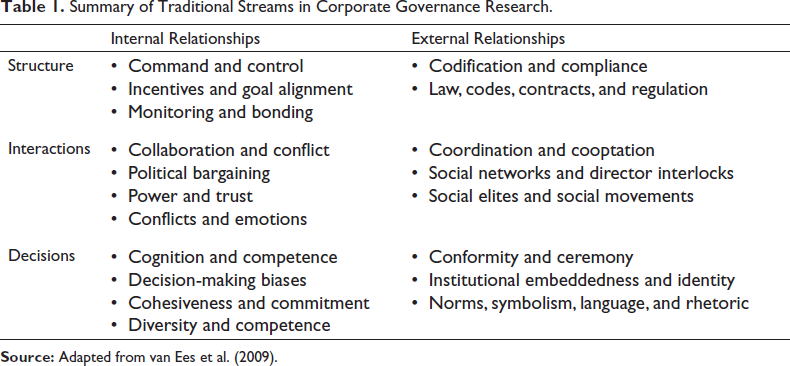

Corporate governance research has traditionally been dominated by scholars in law, economics, and finance (see Ferraro, 2019; Khan et al., 2013; Solomon & Solomon, 2010; van Ees et al., 2009). Despite this, Yusoff and Alhaji (2012) as well as Abdullah and Valentine (2009) have suggested that one of the key theories about corporate governance originates from social psychology, namely: stewardship theory. However, discussions and debates on corporate governance have been argued from economics, legal, and finance perspectives with theoretical positions heavily grounded on agency theory, stakeholder theory, resource dependence theory, social contract theory, legitimacy theory, and political theory (see Yusoff & Alhaji, 2012). Other researchers have also argued from the transaction cost theory as one of the fundamental theories of corporate governance as well as ethics theories (see Abdullah & Valentine, 2009). In the words of van Ees et al. (2009), there exist six (6) main recurring themes or domains when discussing corporate governance. These domains include (a) command and control, (b) collaboration and conflict, (c) cognition and competence, (d) codification, (e) coordination and cooptation, and (f) conformity and ceremony. Table 1 summarizes the topical issues considered under each of these research streams.

Summary of Traditional Streams in Corporate Governance Research.

Further, van Ees et al. (2009) proposed four main concepts for behavioral research in corporate governance. These include (a) bounded rationality of board decision-making, (b) satisficing nature of board decision-making outcomes, (c) problem solving inside and outside boardrooms, and (d) objective or goal setting. Though relevant for providing guidelines for future research in corporate governance, van Ees et al.’s (2009) propositions are not exhaustive. It also assumes that behavioral scientists in general and organizational psychologists, in particular, cannot make any contributions beyond board team dynamics which is essentially applications of group dynamics to board dynamics. However, one cannot undermine the role of non-executives as well as executives when discussing the issues of corporate as they play an integral part (El-Mahdy, 2016; El-Mahdy & Makkawi, 2015). Nevertheless, organizational psychologists have shown little or no interest in corporate governance research and where they do, the focus has been on the empirical link between corporate governance and human resource outcomes and within the stakeholder perspective in the form of corporate social responsibility (see Morgenson et al., 2013; Nmai & Delle, 2014).

The relevance of psychological explanations to corporate governance was re-echoed by El-Mahdy and Makkawi (2015) after a review of corporate governance in the context of the global financial crisis in an attempt to restore investor trust. These researchers pointed to the utilization of psychological theories as part of the effort to further theoretical and empirical arguments that would expand the aim of corporate governance codes. Again, McConvill (2005) also borrowed generously from positive psychology in order to establish the scope and promotion of positive corporate governance. McConvill (2005, p.55) defines positive corporate governance as:

A movement that views the behaviour and motivations of corporate participants (particularly executives) in a positive light…to recognize their personal strengths and virtues, and to promote tangible implications that this positive perspective has for corporate governance (in particular the regulation of internal governance arrangements and the performance of companies).

It is against this background that we argue that even the traditional research domains in corporate governance can equally benefit from theoretical insights from organizational psychology. Oppong and colleagues have already applied organizational psychological insights to the research concerns on codification and compliance (Oppong et al., 2016). Especially, they assessed the extent to which the codes being observed in a lower middle-income country (Ghana) has been informed by empirical evidence and thereby made recommendations for the improvement of these codes. Thus, unlike economics and finance scholars who may only be interested in the existence and compliance with the codes, the interest of organizational psychologists is twofold: (a) they are interested in ascertaining whether or not the codes are supported by the existing empirical studies and (b) the degree of compliance with these codes. The focus of the organizational psychologist may be due to the traditional scientist-practitioner training model used in educating the organizational psychologist (Aamodt, 2007). To further showcase the contributions that organizational psychologists can make in the traditional areas of corporate governance, attention is focused on providing theoretical insights on command and control. Thus, this article attempts to apply some of the existing theories of behavioral science in general and psychology in particular, to explain the performance of non-executive directors on boards and executive performance and remuneration.

Generally, corporate governance may be considered a set of mechanisms that are initiated to help to hold the management in check in order to inject accountability into the management of the corporation (Busru et al., 2019; Oppong et al., 2016; Saha & Kabra, 2020). In line with the agency theory about corporate governance (Solomon & Solomon, 2010, Oppong et al., 2016), it is the separation of management from ownership of companies that makes corporate governance so important, and this same separation creates the agency problem and its associated cost (Solomon & Solomon, 2010). To deal with the agency problem, a number of mechanisms have been developed to act as checks and balances on company management so that they act in accordance with the interests of the various stakeholders. These include shareholder activism or voting, shareholder resolutions, the threat of divestment, institutional investors’ engagement with company management, takeover constraints or risks, voluntary corporate governance codes, separation of positions of chief executive officer (CEO) and board chairman, presence of non-executive directors on board, and a host of new mechanisms.

Though finance and economics theories assume that human beings act rationally, Solomon and Solomon (2010, p.32) argue that “investors do not always behave rationally and human behavior and psychology are factors that are difficult to incorporate in a finance model or an economic theory.” Again, it is generally accepted among finance theorists that overregulation is not the way forward to create trusting and sound corporate governance and that rules can only lead to minimum requirements that organizational leadership will have to comply with (Solomon & Solomon, 2010). Indeed, no law can make someone trustworthy, and this is where psychologists have the potential to contribute a great deal. This, therefore, offers a window of opportunity for organizational psychologists interested in organization theory to consider the application of the existing theories and/or the development of new theories to help deal with the difficulty that finance and economic theorists face in mathematically modeling the behavior of directors and executives. If corporate governance is about regulating the behavior of individuals running organizations to act in the best interest of stakeholders and organizational psychology is about applying psychological theories to address human problems at work, then organizational psychologists can make an important contribution to corporate governance.

There exists an array of psychological theories that present to be useful in explaining corporate governance-related issues. Among such theories include, but are not limited to, theories of motivation, social influence theories, leadership theories, and personality theories. Even though these diverse psychological theories present different viewpoints of behavior at the workplace, it must be acknowledged that a few of these theories are well-rooted in explaining performance and therefore, corporate governance. For instance, whereas leadership and personality theories are much grounded in how personality affects how people lead and how that affects employee behaviors and ultimately organizational outcomes, they neglect how corporate governance can be assured; expectancy, equity, and conformity theories provide us an insight into the extent to which shareholders can control the actions of CEOs and board members as well as their performance. Thus, a social influence theory relating to conformity and a theory that links performance to corporate governance are needed. This formed the crux upon which the choice of specific and selected theories of motivation and social influence including the expectancy and equity theories of motivation and the conformity theory of social influence in providing explanations to corporate governance. That is to say, in order to demonstrate the contributions that organizational psychology can make to corporate governance, we will examine three theories in social and organizational psychology and apply these theories to account for non-executive directors’ behavior as well as executive performance and remuneration. These theories are expectancy, equity, and social influence (conformity) theories and where necessary any relevant psychological concept may be drawn upon.

Expectancy and Equity Theories of Motivation

Motivation theories help explain why people do what they do (Aamodt, 2007; Latham, 2007; Petri & Govern, 2012). We shall begin the discussion of the motivation theories by considering the expectancy theory first. The expectancy states that people will be motivated to take a certain action to the extent that they believe that taking that action will lead to something they value (Aamodt, 2007; Latham, 2007). It is proposed that motivation depends on how much an individual wants something and how likely he or she believes that taking a particular action will lead to that valued outcome (Latham, 2007; Oppong, 2011; Parijat & Bagga, 2014; Pinder, 1998). Victor Vroom argues that individuals will be motivated to exhibit a certain level of effort to the extent that the individual believes that doing so will lead to a certain acceptable level of performance and that the level of performance reached will lead to a valued outcome (Latham, 2007; Oppong, 2011; Parijat & Bagga, 2014).

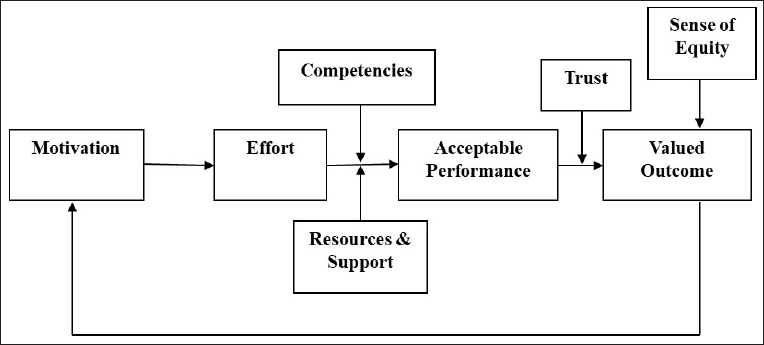

In the same vein, the equity theory argues that individuals must believe that the treatment they receive is fair relative to the treatment received by others (Adams, 1965; Armstrong, 2014). Thus, individuals will be motivated to perform if they perceive equitable treatment and will be demotivated if they perceive unfair treatment. The synthesis of the arguments by the expectancy and equity theories is illustrated in Figure 1.

Figure 1 identifies two important perceptions that can influence the level of motivation of the individual. These are the effort-to-performance (E–P) expectancy and performance-to-outcome (P–O) expectancy. The E–P expectancy is the individual’s expectation about whether his or her efforts will result in the desired level of performance. From Figure 1, we can deduce that E–P expectancy depends on possessing the required competencies and having the necessary resources and support. In other words, the individual must possess the requisite skills and must have the needed equipment and raw materials to perform. On the other hand, P–O expectancy constitutes the expectation about whether reaching the desired level of performance will lead to an outcome the individual longs for. Like the E–P expectancy, P–O expectancy is also moderated by another factor. In the case of P–O expectancy, its strength depends on the level of trust between the individual and the one who gives the rewards (in the workplace, it is the management). It is important to note that the level of trust is a function of the timing of the provision of the reward and the frequency with which management honors its promise to individuals. Now let us turn our attention to the social influence theory.

Social Influence Theory: Conformity

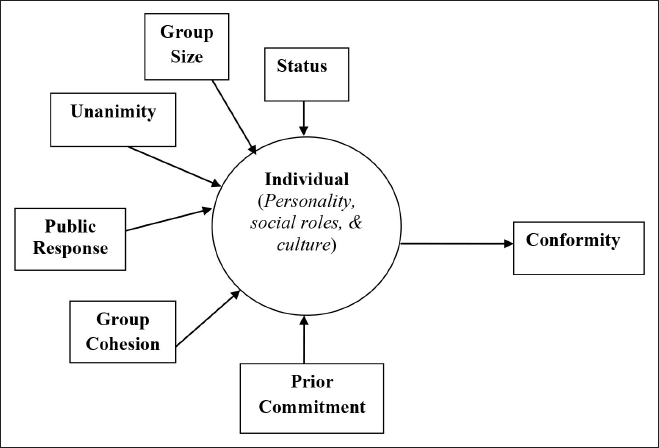

Social influence as an area of research is dominated by social psychologists. Indeed, social influence theory covers more than just conformity; other areas include compliance, persuasion, and group influence as well as a cultural influence on human behavior (Myers, 2008). However, our focus in this article shall be on conformity. Conformity is defined as a change in behavior or belief as a result of real or imagined group pressure (Myers, 2008; Oppong, 2011; Violato et al., 2022). Conformity experiments carried out over the years in social psychology show that people in a group setting are more likely to yield to group pressure, if the group is large, the group behavior is unanimous, and the group is cohesive. It has also been found that when people of high-status model the behavior or belief, there is a greater likelihood that conformity will be high (Asch, 2004; Milgram, 2004; Myers, 2008). Again, people also conform most when their responses are public or in the presence of others while a prior commitment to certain behavior or belief increases the possibility that a person will stick to that commitment rather than conform (Asch, 2004; Milgram, 2004; Myers, 2008).

Put another way, group size, status, public response, prior commitment, cohesion, and unanimity all influence the likelihood that people will conform. Studies in social psychology also indicate that personality, social roles, and culture all influence the degree to which individual yields to group pressure (Asch, 2004; Milgram, 2004; Myers, 2008). The group factors and personal factors that act on the individual to determine the degree of conformity are illustrated in Figure 2. At this juncture, attention will be turned to the applications of these theories (integrated expectancy-equity theory and conformity theory) to explain the behavior of non-director and executive remuneration and performance.

Behavior and Performance of Non-executive Directors

There is substantial evidence indicating that non-executive directors act as necessary monitors of management; however, there is also evidence suggesting that non-executive directors have a negative impact on corporate governance (Solomon & Solomon, 2010). Again, the independence of the non-executive directors has been questioned given their inability to help avert corporate governance disasters. Agrawal and Knoeber (1996, p. 394) explained the negative impact of non-executive directors in the following words:

One possible rationale is that boards are expanded for political reasons, perhaps to include politicians, environmental activist, or consumer representatives, and that these additional outside directors either reduce firm performance or proxy of the underlying political constraints that led to their receiving board seats.

Drawing on the expanded expectancy-equity theory presented in Figure 1, we can say that non-executive directors are more likely to take steps to be independent to the extent that they expect that their efforts will result in the desired level of performance (independence) and that their independence will result in some reward they value. The expanded expectancy-equity theory shows that the effort-to-performance (E–P) expectancy of the non-executive directors will depend on their knowledge and skills as well as the support of the top management team and shareholders; the support can take the form of job security and protection against arbitrary actions of the CEO. After all, Priem et al. (1999, cited in Oppong, 2014, p.173) argued that

The role and importance of the entire TMT [top management team] in strategy development would likely be reduced, thereby curtailing their contribution to firm performance. This diminished role can occur independently of the collective skills and capabilities resident in the TMT; as the power and assertiveness of the CEO increases, the other TMT members simply become less relevant.

Again, the performance-to-outcome (P–O) expectancy of the non-executive directors will depend on the level of trust they hold about the likelihood that the CEO and the other executive directors will not act arbitrarily or renege on their promise. Additionally, non-executive directors will determine whether they are being equitably rewarded by the companies on whose boards they serve compared to their counterparts playing similar roles elsewhere or on other boards. This means that non-executive directors are more likely to be independent if they have the requisite expertise and the support of the top management team to act independently and being independent will be rewarding for them. The practical implications of this theory are consistent with some of the recommendations by the various review commissions set up in the UK on corporate governance.

However, this recommendation did not go down well with some non-executive directors as there was a feeling among board directors that the non-executive directors have no need for training (Solomon & Solomon, 2010). Certainly, such an attitude displays a certain level of arrogance. Solomon and Solomon (2010, p.73) asked “To what extent can anyone ever claim to know everything about what they do?” and answered it by saying that “There is always more to learn.”

However, it is reasonable to expect that telling non-executive directors, who often are people of a certain stature in their respective societies, to attend training is to label them as incompetent and that is something that might not be taken lightly by persons of such stature. Such remarks have the potential to affect the individual’s self-esteem and self-efficacy negatively. But why can we not call a spade a spade? It is because non-executive directors may consider such a move insulting and a dent in their competence and image. It will have been a different thing if the non-executive directors were the ones who suggested that they had a training need; to impose on them a training need is to undermine their sense of autonomy given how highly persons of such stature might think of themselves. Based on psychological literature on self-concept and personnel psychology, two recommendations are provided here. First, existing non-executive directors should be encouraged to identify for themselves, with or without the support of an executive coach, their own training needs in the area of corporate governance. Once the training needs have been identified, the relevant bodies should develop training content to assist the non-executive directors to learn the necessary concepts, principles, practices, and possible applications to the organizations on whose boards they serve. For instance, in Ghana, after the training needs assessment, the Institute of Directors-Ghana together with the Institute of Chartered Accountants-Ghana, and other relevant professional bodies could develop executive development modules to facilitate the learning of the relevant concepts, principles, and practices by the non-executive directors.

The second recommendation focuses on the selection and appointment of non-executive directors. As Agrawal and Knoeber (1996) explained, the appointment of non-executive directors is often based on factors other than their competence. Put another way, in order to appeal to a wider stakeholder community, organizations appoint non-executive directors who may not be well-equipped to perform the monitoring role required of them. The personnel psychology literature suggests that personnel selection and training are two effective ways of matching individuals to the job of jobs to individuals (Searle, 2003). As a result, if the training option is not a welcome idea among non-executive directors, then the selected option should be considered seriously. This is to say that the appointment of non-executive directors should not be solely based on the stature of the individual and the effort to appeal to key stakeholders, but also equal attention should be paid to their competencies in corporate governance and the area of business the organization is in. Ultimately, the training and selection options should go hand in hand; while carrying out the competence-based appointment of new non-executive directors, the existing and even the new ones should be encouraged to identify their own training needs in the area of corporate governance so that they can be assisted to address their learning needs.

Again, the remuneration of non-executive directors has been similarly questioned as it is not enough to motivate them to effectively perform their monitoring role (Solomon & Solomon, 2010). Due to low levels of remuneration compared to the executive directors, non-executive directors may feel they are being treated inequitably and when people feel under-compensated, they react by reducing efforts or by showing less enthusiasm. In his study of Australian firms, Searle (2002) found that compensation represents a powerful way of matching jobs to individuals.

In addition, social influence theory can also be applied to explain the degree to which non-executive directors can be independent. As indicated earlier, group pressure on an individual can “force” him or her to conform to the decision or beliefs of a group. In the case of the non-executive directors, the size of the board, the status of board members making certain suggestions, the degree of “we feeling” among board members, prior commitments, public responses (lack of secret voting), and the need to reach unanimous decisions all determine the degree to which non-executive directors will act independently. Again, their personality can also influence the degree to which they can be independent in their decisions and monitoring tasks. This means that non-executive directors will only act independently if …

They possess the expertise needed to understand what is being discussed and do not allow their admiration for some board members to influence their assessment of issues. For instance, if finance experts on the board say that a glaringly “high risk” investment is not risky, who are you to think otherwise if you hold a PhD in African Culture and History? They are not part of a cohesive board that seeks a unanimous decision, or the board puts in place measures to deal with groupthink or group polarization. Thus, if there is no direct or indirect punishment for dissenting views, then non-executive directors will consider issues on their merit. For more information on how to avoid groupthink consult Manning and Curtis (2007, p. 203). They have not made a prior commitment to support any specific idea. This is to say that if non-executive directors publicly declare their support for or against a certain course of action, it is more likely that they will stick to the course of action even if it turns out to be wrong. Shareholders and business reporters or journalists can use their media to get non-executive directors to commit themselves to the courses of action in favor of the shareholders and other stakeholders. However, non-executive directors uncertain about their own decisions should not make public pronouncements about issues related to the companies on whose boards they serve. The non-executive directors do not make their decisions in the presence of others. That is, if there is secret voting, non-executive directors are more likely to act independently rather than conform. Their personality characteristics do not predispose them to conform. Even though extant literature linking personality factors to the degree of conformity is inconclusive (see DeYoung et al., 2002; Roccas et al., 2002), we can deduce that conscientious non-executive directors will examine issues thoroughly and carefully before deciding while non-executive directors “high on agreeableness” will generally seek a harmonious relationship with the other board members and as a result, conscientious non-executive directors are more likely to act independently while those with high agreeableness are more likely to act in accordance with the group in order to avert group displeasure.

Executive Performance and Remuneration

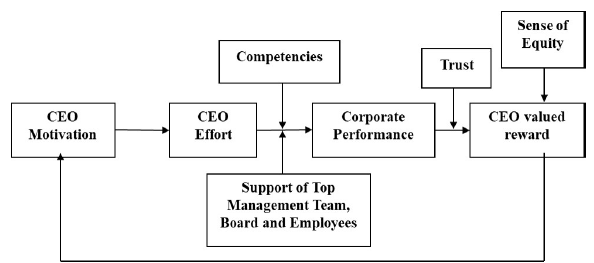

Drawing on the expanded expectancy-equity theory presented earlier (see Figure 3), it can be argued that CEOs are more likely to enhance company performance to the extent that they believe doing so will lead to some valued outcomes. This theory says that we can resolve the agency problem by ensuring that when CEOs formulate and implement strategies that lead to high corporate performance, they are provided with a reward of value to them. We can also deduce that the level of motivation of the CEO will also depend on the effort-performance (E-P) and performance-outcome (P-O) expectancies.

This is to say that if the CEO believes that his or her effort will result in the desired performance level and that achieving such performance level will lead to rewarding that he or she values, then the CEO will be motivated to put in the required efforts to maximize the shareholders’ value. In terms of the E–P expectancy, if the CEO possesses the knowledge and skills required to formulate and implement the necessary strategies and has the support of the top management and the employees, then he or she can convince himself or herself that such efforts will not be in vain. On the other hand, the P–O expectancy predicts that if the CEO trusts the top management including the board that in achieving the desired level of corporate performance his or her bonuses and other incentives will pay as promised, then the CEO will be motivated to engage in the effort necessary to get the organization to the level that the stakeholders expect. In fact, this has been the only way that the agency problem inherent in corporate governance has been addressed. However, there are several accounts that the CEO remunerations are not related to their performance and/or the performance of their companies (Brick et al., 2002; Solomon & Solomon, 2010). Some have also argued that executive remunerations are unreasonably excessive (Conyon et al., 2011; Griffin, 2006; Murphy, 2013; Solomon & Solomon, 2010).

In addition, there is also the problem of short-termism (the concentration of the CEOs on short-term financial performance indicators such as earnings per share [EPS]), though they are well aware of the impact on the long-term health of the organization. Hayes (2002, p. 205) argues that “many control systems are designed to reward current practice and offer little incentives for people to invest effort in changing organizations to promote long-term effectiveness.” How do we explain this? The finance literature explains this simply as the reaction of CEOs to the pressure mounted on them by institutional investors and the rest of the board to pursue corporate performance reflected in such indicators (Solomon, 2020; Solomon & Solomon, 2010). But how will the psychological literature explain this? One possible explanation for this short-termism is the law of effect, that actions followed by preferable consequences are more likely to recur as opposed to those that are followed by non-preferable consequences. But if that is the case, then the downfall of such entities as Enron (USA), WorldCom (USA), Coloroll (UK), and Barings Bank (UK) as well as takeover constraints should “compel” the CEO and the board to concentrate on the long-term effectiveness instead of the short-term financial performance such as EPS. However, it is known in psychology that the immediate rewarding or positive consequences of behavior have a greater impact on its likelihood of repetition than a delayed negative consequence of the same behavior. This is referred to as contingency or social trap in the psychology of learning literature (Chance, 1994; van Lange Paul et al., 2015). This concept of contingency trap helps explain why people continue to smoke knowing the negative consequences such as cancer; it is because smoking is immediately rewarding (e.g., nicotine triggers the release of endorphins—the body’s natural painkillers—and that may reduce stress) while the long-term effect, cancer, is delayed or may never occur (Brannon & Feist, 2007; Chance, 1994).

Drawing on the concept of the contingency trap, we can argue that focusing on long-term effectiveness is good in the long run as it will facilitate the avoidance of doom; however, concentrating on short-term financial performance is immediately rewarding and the doom talked about may never even occur. Until the shareholders through the board compel company management to focus on the long-term “drivers” of future performance, such as customer service, improved internal processes, and employee learning and development, the law of effect and contingency trap will act on CEOs to focus on the short-term financial measures of past performance. After all, “the universal experience of human nature is: what is inspected is to be expected—and what is ignored will be neglected” (MacLennan, 2006, p.384).

As hedonistic as many of us are and CEOs not being the exception, they are more likely to seek pleasure and avoid pain by focusing on what is paying (short-term financial performance). This means CEO performance contract negotiation should take place within the framework of a balanced scorecard approach to performance management in order to integrate “financial measures of past performance with the measures of the ‘drivers’ of future performance” (Hayes, 2002, p.205).

Based on the expanded expectancy-equity theory and the concept of the contingency trap presented thus far, we can conclude that CEOs will be motivated to maximize the values of shareholders if the following conditions exist:

The CEO has the requisite skills and knowledge needed by the company at that particular point in time in order to formulate and implement winning strategies. The CEO has the support of the internal management and the employees. The CEO believes that when he or she achieves that desired level of corporate performance, he or she will receive the reward as agreed. The desired level of corporate performance is cast within the balanced scorecard or similar framework to minimize short-termism. The CEO perceives his or her rewards and treatment as equitable or fair compared to other CEOs in their particular industry.

Managerial Implications

This section presents applications of the theoretical insights developed above to both enhance the independence of non-executive members of boards and improve executive performance. In the next section, some propositions that can be tested in empirical studies are examined. Based on the foregoing theoretical discussions, the following should be considered if firms and regulatory bodies wish to create conditions for non-executive members to become more independent and serve their purpose on boards:

Regulatory bodies should require non-executive directors to attend at least one mandatory corporate governance training course annually. This can be mandated by national corporate governance codes. Firms appointing non-executive directors should organize orientation programs focused on exposing them to new issues in corporate governance. This can take the form of a one- or two-day management retreat with invited speakers on corporate governance. Appointment of non-executive directors should not be only guided by the need to appeal to different stakeholders but must also take into account person-job fit and person-organization fit considerations. In other words, the candidates must have the competence to carry out the monitoring responsibility effectively and should be able to fit into the board of directors’ team. Similarly, personality profiling should be conducted to ensure that non-executive directors are not extremely high on agreeableness; this will affect their ability to remain independent. In reaching decisions in the boardrooms, secret balloting rather than open balloting should be used to minimize the influence of perceived experts among the directors on others. Where it is possible, non-executive directors as well as executive directors should be discouraged from making public pronouncements on certain decisions being taken by their firms through the media. This can be achieved through developing protocols for media interactions and providing training to the directors. In addition, the directors could be required to sign honor codes, violation of which should result in termination of appointment. This will not affect transparency and the right to information. The honor code will allow only appointed persons to speak on behalf of the board when the need arises.

In the case of executive performance, a lot of applied implications may hold based on the theoretical discussions on the integrated expectancy-equity theory about CEO performance and remuneration. One area of key application is CEO selection and appointment. CEO search committees of boards should focus on fitting the prospective candidates to the jobs, the organization, and its current challenges. This fit is needed to ensure that CEOs hired have the requisite skills and experience to deal with the challenges being faced by the company. Notwithstanding, CEOs, like other types of employees, are active crafters of their jobs. Wrzesniewski and Dutton (2001) have argued that employees do not passively take on and do the jobs designed and assigned to them by their employers. They also outlined key factors that motivate such job crafting; these include (a) the need for control over the job and meaning of work, (b) the need for a positive self-image, and (c) the need for human connections with others (Wrzesniewski & Dutton, 2001). They further suggested that employees craft their jobs by means of changing task boundaries (altering types and/or number of tasks), changing cognitive task boundaries (altering the view of the work), and changing relational boundaries (altering with whom one interacts and the nature of interactions at work). However, CEOs have more discretion to craft their jobs but must be within the defined performance contract signed. This will require a good set of SMART performance indicators and key results areas and principles.

Successful global CEOs admit that attracting and honing very powerful, tight teams that provide reliable support is critical to their success (Tappin & Cave, 2010). Tappin and Cave (2010) interviewed 200 successful global CEOs in both the West and the East. Developing these tight teams requires that the CEOs themselves find trustworthy managers to support and execute their agenda in the organization (see Tappin & Cave, 2010). It is already understood that the upper echelons of the organization influence policies, organizational actions, and success (see Oppong, 2014).

Testing the Assumptions

The assumptions derived from this theoretical analysis can be tested through randomized control group designs in group decision studies, quasi-experimental designs, and surveys. For instance, some of the assumptions on the independence of non-executive directors can be studied empirically through randomized control group designs. In the test of the influence of secret voting on the independence of non-executive directors, participants who are likely to be psychology students can be randomly assigned to an experimental group with secret voting and a control group without secret voting. In such a situational decision-making experiment, the decision to be made should be a business-related case, and 40%–50% of the participants should be “knowns.” By “knowns,” I mean 40%–50% of the participants should be individuals who know one another and interact regularly (daily or weekly); this will pass off as the internal managers. The other 50%–60% of the participants would become the “outsiders” and pass off as the non-executive directors as they should be drawn from outside the “knowns.” The recommended 50%–60% non-executive composition of the groups is supported by empirical evidence (see Oppong et al., 2016). The group size is recommended to be between 6 and 8 (see Oppong, et al., 2016). Based on power analysis, the required number of groups should be formed for such an experiment. The outcome variable measure could be the percentage of “outsiders” who vote the same way as the majority decision of the “knowns.” Alternatively, the “knowns” can be asked to argue and vote in the same.

On the issue of the relationship between prior commitment and the degree of independence of non-executive directors, randomized control experiments can equally be set up as well (see Figure 2). Using the same group size and composition discussed earlier, at least two conditions can be set up in which the “outsiders” are required to read public statements to an audience about their views on a decision to be made (experimental condition) and another where no such public statements are made (control group). However, the participants should be randomly assigned to either of the conditions. The approach discussed above or its variants can be used to measure the outcome variable. Similarly, the expertise of the “outsiders” can also be manipulated. This can be achieved by setting up three groups in which Group 1 is made up of “outsiders” who have expertise relating to the decision to be made, Group 2 is made up of “outsiders” with mixed expertise, and Group 3 is made of those without expertise in relations to the decision to be made. In all these experiments, the means of decision (open or secret voting) can also be manipulated, and this will produce factorial designs.

On the question of personality (see Figure 2), a survey can be conducted in which several non-executive directors are asked to complete an assessment of their personality using any standard measure of the Big Five traits and their self-assessment of the degree of independence. At the same, an executive director can also provide a measure of the independence of the non-executive director. In this case, multiple regression analysis can be run to determine which of the personality traits influence non-executive directors’ degree of independence. However, other personality traits like self-esteem and generalized self-efficacy can also be assessed alongside the Big Five traits. In a study like this, it will be expected that the following will hold (this is not exhaustive in any way):

Proposition 1: There will be a negative relationship between agreeableness (of the Big Five) and degree of independence. Proposition 2: Conscientiousness and openness will relate positively to the degree of independence. Proposition 3: There will be a positive relationship between self-esteem and degree of independence. Proposition 4: There will be a positive relationship between generalized self-efficacy and degree of independence.

Randomized control experiments or even their quasi-equivalent may not be appropriate for the CEO research on the assumptions derived in this article. Surveys are more appropriate in this case. However, it is important to note that CEO studies are often affected by the low response with a return rate often less than 20% (see Cycycota & Harrison, 2002). As a result, researchers interested in behavioral dimensions of corporate governance ought to implement some of the recommendations by Cycycota and Harrison (2002) on how to enhance response rate in executive-level studies. Cycycota and Harrison (2002) found that conventional ways for enhancing response rates among employees and consumers did not work for executives. They rather recommended alternative techniques including personal interviews, professional associations, industry or trade groups, executive round tables, and trade conventions where the executives are more relaxed and less likely to have “the traditional buffering mechanisms screening and discarding the survey and might feel more inclined to provide responses in a peer context” (Cycycota & Harrison, 2002, p. 171).

Alternatively, researchers can deal with the low response rate and the resulting low sample sizes through the recommendations by Hollenbeck et al. (2006). Hollenbeck et al. (2006) recommend using Bonferroni correction in such situations such that the chosen decision criterion or alpha level (say p < 0.05) is divided by the number of hypotheses to be tested in the same way the fishing error is dealt with (Shadish et al., 2002). Similarly, bootstrapping can equally be used to address the sample size problem (see Hesterberg, 2015). The issue of small sample size relates to statistical conclusion validity. Statistical conclusion validity has been defined as “the degree to which results of statistical analysis on a sample dataset will remain stable in the population from which the sample was drawn” (Oppong, 2018, p. 10).

Alternatively, another or perhaps more suitable way to analyze that data will be the use of structural equation modeling given the model specification as presented in Figure 3. Though not exhaustive, the following propositions can be tested in these CEO surveys:

Proposition 5: The relationship between CEO efforts and corporate performance will be moderated by CEO competence and perceived support from direct reports and the board. Proposition 6: The relationship between CEO motivation and corporate performance will be mediated by CEO efforts. Proposition 7: CEO motivation will be related to the attractiveness of the contingent reward.

To facilitate carrying out these studies, all the variables presented in Figure 3 have to be operationally defined. For instance, corporate performance can be defined in terms of financial performance, customer satisfaction, employee satisfaction or morale, or efficiency of internal business processes. Kanungo and Mendonca (1997) define effort as the expenditure of time and energy incurred in preparation for performance. Put another way, effort refers to the set of behaviors that are not organizationally required but that an employee must engage in, in order to perform the required job behaviors well. Thus, CEO efforts can be operationalized as the amount of time spent planning, organizing resources, leading (executing), and controlling (monitoring) his or her corporate goals.

Conclusion

From the ongoing discussion, we can conclude that the psychology of corporate governance has a role to play if we are to unravel the existing difficulties in addressing the human factor in corporate governance. Given that psychologists have no or fewer competitors in the understanding of human behavior, it is only appropriate that we accept the challenge and make our contributions to deepen the current insights about corporate governance.

It is important to note that the theories and issues addressed here are only illustrative of what organizational psychologists can contribute to the understanding of corporate governance. It is appropriate at this point to indicate other equally useful theories and evidence in areas, such as group dynamics, the psychology of decision-making, and self-beliefs and attitudes. Others include the regulatory focus theory, leadership, organizational commitment, psychology of strategic management, and a host of other theories from both organizational and social psychology which may be applicable to corporate governance. These and many others can be subsumed under the psychology of corporate governance. The psychology of corporate governance is being utilized to refer to a research and practice niche within organizational and social psychology that draws practical implications from theories of psychology and psychological technologies of regulation and carries out research in corporate governance with the ultimate goal of enhancing stakeholder value as well as the welfare of directors and management.

Again, theory and evidence from economic psychology (or behavioral finance) may also be useful here as well. However, further research will be required to test the hypotheses that will be derived from these theories; specifically, there is a need to develop motivation theories that address executive motivation.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.